Embed Size (px)

Citation preview

From Listing to Delisting: Foreign Firms’ Entry and Exit from the U.S. *

Susan Chaplinskya and Latha Ramchandb

aDarden Graduate School of Business, University of Virginia, Charlottesville, VA bCollege of Business Administration, Dept. of Finance, University of Houston, Houston, TX

Abstract

We examine the listings and delistings of foreign firms from major U.S. exchanges over the period 1961 – 2004. Over this period a total of 1,330 firms listed and 728 firms delisted due to merger and acquisitions, involuntary, or voluntary reasons. The large number of listings and delistings spanning over 40 years suggests that there is a long standing dynamic to foreign firms’ entry and exit from the United States. Over this period, we find a steady decline in the length of time foreign firms stay listed in the U.S. A major reason for this decline is that, not unlike the pattern for U.S. new lists, the quality of foreign firms listing in the U.S. has deteriorated over time. Probit analysis suggests that large, profitable firms able to attract U.S. trading volume survive, whereas weak firms exit. We also examine the circumstances surrounding the voluntary delistings as their exit has raised the greatest concern about the overall competitiveness of the U.S. market. After controlling for firms close to distress, we find only 48 “true” voluntary delistings. The firms voluntarily delisting following passage of Sarbanes-Oxley have low average profitability, median assets and market capitalization less than $230 million, stock prices that decline by over 50% from listing to delisting, and 60% have no analyst coverage. The evidence suggests these firms are driven from the U.S. as much by a lack of quality and investor interest as regulatory costs. Our results suggest that foreign firms’ decision to delist from U.S. exchanges must be examined within the broader context of what makes foreign firms viable candidates for listing. JEL codes: F36, G15, G28 Key words: international finance, ADRs, delistings, Sarbanes Oxley First Draft: November 2006; Revised Draft: February 2007 Not for Quotation, Comments Welcome *We thank Michael Schill and the participants of the University of Virginia Darden Research Seminar for helpful comments. Kulwant Rai provided excellent research assistance. Author contact information: a. Susan Chaplinsky (corresponding), Darden Graduate School of Business, University of Virginia, Charlottesville, VA 22906-6550, email: [email protected], phone: 434-924-4810. b. Latha Ramchand, University of Houston, College of Business Administration, Department of Finance, Houston, TX 77204-6282, email: [email protected], phone: 713-743-4769.

From Listing to Delisting: Foreign Firms’ Entry and Exit from the U.S.

Abstract

We examine the listings and delistings of foreign firms from major U.S. exchanges over the period 1961 – 2004. Over this period a total of 1,330 firms listed and 728 firms delisted due to merger and acquisitions, involuntary, or voluntary reasons. The large number of listings and delistings spanning over 40 years suggests that there is a long standing dynamic to foreign firms’ entry and exit from the United States. Over this period, we find a steady decline in the length of time foreign firms stay listed in the U.S. A major reason for this decline is that, not unlike the pattern for U.S. new lists, the quality of foreign firms listing in the U.S. has deteriorated over time. Probit analysis suggests that large, profitable firms able to attract U.S. trading volume survive, whereas weak firms exit. We also examine the circumstances surrounding the voluntary delistings as their exit has raised the greatest concern about the overall competitiveness of the U.S. market. After controlling for firms close to distress, we find only 48 “true” voluntary delistings. The firms voluntarily delisting following passage of Sarbanes-Oxley have low average profitability, median assets and market capitalization less than $230 million, stock prices that decline by over 50% from listing to delisting, and 60% have no analyst coverage. The evidence suggests these firms are driven from the U.S. as much by a lack of quality and investor interest as regulatory costs. Our results suggest that foreign firms’ decision to delist from U.S. exchanges must be examined within the broader context of what makes foreign firms viable candidates for listing.

1

From Listing to Delisting: Foreign Firms’ Entry and Exit from the U.S.

Visits give pleasure ― if not the coming, then the going.

Portuguese saying 1. Introduction

Over the past 30 years the U.S. capital markets have been the primary destination of

foreign firms seeking into increase their global footprint and opportunities. Recently a number of

international firms have announced their intentions to delist from major U.S. stock exchanges.

Among other reasons, these firms often cite the low U.S. trading volume in foreign owned shares,

the increased complexity of U.S. capital market regulation, spurred by passage of the Sarbanes-

Oxley Act in 2002, and the belief that non-U.S. markets can meet U.S. shareholders’ and capital

raising needs. These actions have raised concerns that the U.S. capital markets could be losing

competitiveness and that increased regulation may be driving foreign firms away. At the same

time, foreign firms continue to list in the U.S. In this paper we examine the entry and exit of

foreign firms into the U.S. over the period 1961 – 2004. In total, there have been 1,330 listings

and 728 delistings of foreign firms from major U.S. exchanges over this period.1 The large

number of listings and delistings spanning some 43 years suggests there is a long standing

dynamic to foreign firm’s entry and exit from the United States. This pattern – as revealed in the

characteristics of the entering and exiting firms – provides insight into two important and timely

questions. First, by examining the characteristics of foreign firms listing in the U.S. over time we

observe the profile of foreign firms that are viable candidates for public listing. Earlier studies

examining the motivation of firms to list in the U.S have been conducted at different points in a

1 While there is a large literature on foreign listings (Karolyi 1998, 2004 provides a survey), we are aware of only three studies examining foreign delistings. Liu (2004) examines the announcement date effects to 103 involuntary foreign delistings from 1990-May 2003, Smith (2005) examines abnormal returns for a sample of 179 foreign delistings from 2000-September 2004, and Witmer (2006) examines announcement date effects and other aspects of delisting for 140 cross delistings from 1990-2003. All three studies find significantly negative announcement date returns to delisting announcements.

2

period of secular advances in global market integration. We take a systematic longitudinal

approach and examine all foreign entrants – listing via ADRs and ordinary shares – over the

entire period of time in which these advances have occurred. We wish to know whether the

profile of entrants has changed over time and to identify the enduring characteristics of successful

foreign entrants. Identifying the most viable listing candidates enhances the overall

competitiveness of the U.S. market because these firms drive investor interest and its attendant

benefits, which in turn, attract new foreign firms to the U.S.

A number of studies have advanced motivations for firms to list in the U.S. While not

mutually exclusive, observers have noted the foreign firms may seek a lower cost of capital

(Merton, 1987; Karolyi, 1998), greater access to capital (Lins, Strickland, and Zenner, 2004),

greater liquidity (Amihud and Mendelson, 1986; Brennan and Subrahmanyam, 1996), improved

product market visibility (Roell, 1996), the bonding provided by the stricter regulation of U.S.

security markets (Coffee, 1999), and higher market valuation (Doidge, Karolyi, and Stulz, 2004).

The common theme behind these motivations is that firms expected benefits in excess of the costs

of listing from the U.S. market’s improved liquidity, visibility, transparency, and capital raising

opportunities relative to their home markets. Over time changes have occurred with respect to

both the benefits and costs of listing that may have altered the advantages of a U.S. listing. The

benefits of listing could be reduced if, all else equal, liquidity is less than anticipated, if a firm’s

desire for product market visibility declines, or if a firm’s access to capital is anticipated to be

less in the future. Similarly, low liquidity and trading volume often result in reduced analyst

following which hinders a foreign firm’s ability to gain investor recognition and contributes to

higher costs of capital through a less diversified shareholder base (Merton, 1997). Further, as the

number of foreign entrants has grown it may have become more difficult for firms to gain

investor recognition. In addition, non-U.S. markets have grown and liberalized over the past

decades narrowing the advantages of the U.S. market in terms of liquidity, transparency, and

capital raising over competing markets (Bekaert and Harvey, 1995; Henry, 2000a and 2000b).

3

Finally, markets have seen technology and different trading platforms emerge that have reduced

the localized benefits of trading in a particular market (Karolyi, 2003). Thus, firms could delist in

response to a changing set of circumstances which reflect reduced benefits from of a U.S. listing.

With respect to costs, although the exchange listing requirements have changed only modestly

over time there have been larger changes in regulatory costs. Some initiatives such as Rule 144A,

enacted in 1991, allowed (non-listing) foreign firms access to the U.S. capital markets with fewer

disclosure requirements, while others such as the Sarbanes-Oxley Act (hereafter SOX), enacted in

July 2002, have been perceived to increase the compliance costs of a U.S. listing.

To assess the impact of these and other changes on the motivation of foreign firms to list

or delist, we track foreign firms on a number of firm-specific, U.S. and home market

characteristics from the time of listing to delisting (or 2004 if they remain listed). Our analysis of

entry and exit is focused on the conditions of “survivorship” for foreign firms over time. At the

time of listing, firms list in the U.S. if the expected net benefits (benefits minus costs) of listing

are positive compared to non-U.S. markets. Thereafter several possible outcomes can result.

Firms can continue to remain listed if certain regulatory and implicit quality conditions are met

and the net benefits remain positive. Firms can fail to meet regulatory requirements and be

forced to involuntarily delist. Or firms can voluntarily choose to delist if the net benefits to U.S.

listing decline sufficiently. A final category includes firms that meet regulatory requirements but

delist due to mergers or acquisitions (M&A).

Each of the delisted groups tells something in relation to the firms that remain listed.

Involuntary delistings occur because firms are unable to meet regulatory standards – most often

due to poor performance. Important here is how the quality of foreign new lists has changed over

time. Decreasing quality is associated with a greater number of exits and reduced survivorship

but foreign firms can fail for the same reasons as U.S. firms. The number of firms “delisted for

cause” reveals how the quality of foreign new lists has changed over time but it says little about

the potential benefits of a U.S. listing. Some modicum of performance is necessary for a firm to

4

benefit from listing, in the absence of which there is little chance of achieving the hoped for

benefits. M&A delistings can result from a strategic decision to list in the U.S. until such time as

the firm is able to attract a takeover offer. While we cannot identify the firms with an ex ante

intention to be acquired, we can examine the type of foreign firms that attract M&A activity and

their gains in valuation in determining whether the U.S. market has served them well. Voluntary

delistings raise the question why these firms exit the U.S. market and what criteria distinguish

them from the firms that remain listed. Do the anticipated benefits of a U.S. listing fail to

materialize resulting in, for example, low investor recognition, low liquidity, or little need for

capital raising? Do they exit because the costs associated with a U.S. listing exceed the benefits

and drive them from the market, and more so in cases where non-U.S. markets offer viable

substitutes?

The 728 delistings of foreign firms from major U.S. exchanges over 1961-2004 break

down into, 371 involuntary delistings, 309 M&A delistings, and 48 voluntary delistings. The

pattern of foreign firms listing in the U.S. over this period shows a steady and persistent decline

in the length of time a foreign firm stays listed in the U.S. For firms listing in the U.S. prior to

1970, the average duration of listing is 33 years and this decreases to five years for the firms

listing during the period 1996-2000. Likewise the proportion of foreign firms that stay listed ten

or more years declines from 100% for firms listed before 1970 to 34% for firms listed between

1991-1995. Irrespective of the reason firms delist, all three delisted groups experience similar

drop offs in their duration of listing time.

Consistent with the findings reported for U.S. “new lists” by Fama and French (1997),

foreign new lists exhibit similar deterioration in quality, particularly profitability, over time. This

deterioration in quality would not necessarily have been predicted for foreign new lists because

many are large and seasoned firms in their home markets and foreign firms conducting IPOs in

the U.S. are higher quality firms than domestic U.S. new lists (Bruner, Chaplinsky, Ramchand,

2004). Moreover, seasoned firms in Fama and French’s (1997) study reveal little evidence of

5

declining quality. Nonetheless, a major reason for the decrease in foreign firms’ listing time is a

large and increasing number of involuntarily delists. The exit of low quality firms poses less

concern for U.S. market regulators. In fact, the large number of firms “delisted for cause” is

more likely to raise questions about whether U.S. listing standards are too low rather than the

current concern that standards may be too high.

Our results suggest that size, profitability, and U.S. market conditions are important

determinants for firms’ survival in the U.S. market. All else equal, larger, more profitable firms

able to generate a larger proportion of their trading volume in the U.S. are less likely to delist.

Firms originating from emerging markets, firms that compete for investors’ attention with fewer

firms from the same country, and firms that have raised capital in the U.S. also are less likely to

delist. While stronger U.S. market performance significantly reduces the probability of delisting,

home market stock performance, GDP growth, and exchange rate movements appear to have little

influence on delisting. Simply put, stronger foreign firms that are able to gain U.S. investor

interest are more likely to survive.

Out of 728 delistings, only 48 firms appear to be “truly” voluntary delistings. Focusing

on the post 2000 period following passage of Sarbanes-Oxley, where the majority of these

delistings occur, we find that voluntary delistings have low average profitability, median assets

and market capitalization less than $230 million, the average share price declines by 54% from

listing to delisting, and 60% have no analyst coverage within a year following listing. While a

few voluntary delists appear to have the size and strength to be viable candidates for listing, the

majority struggle from a lack of quality and investor recognition. Absent these traits, it is

difficult to achieve the benefits expected from listing. As few strong foreign firms choose to exit,

regulatory costs alone cannot be the predominate explanation for why these firms voluntarily

delist. Rather their exit appears more related to issues of whether these firms are viable

candidates for listing. Therefore the issue of foreign firms’ ability to attract U.S. investor interest

6

merits greater attention in determining the role of SOX and the competitiveness of the U.S.

markets.

The paper is organized as follows. Section 2 describes the sample of foreign listed and

delisted firms and examines the characteristics of listed firms over time. Section 3 explores the

delisted firms in more detail and the factors associated with various types of delistings. Section 4

examines in more detail the characteristics of M&A and voluntary delists, or foreign firms that

have more choice about their decision to delist. Section 5 contains our conclusions.

2. Exit and Entry into the U.S.

2.1 Sample of Lists and Delists

Using the shares codes 12 and 30 and 31 from CRSP, we identify all foreign firms that

listed on a major U.S. stock exchange from 1961 – 2004.2 Because of the use of exchange

listings, our sample includes Level II and III ADRs and ordinary share listings but does not

include Level I and Rule 144A ADRs. We focus on listings on major stock exchanges to ensure

better data availability and more uniform listing requirements.3 Although CRSP indicates that a

share is foreign owned, it does not give the country of origin and therefore to be included in our

sample we must be able to independently verify the country of origin.4 From this sample of

exchange listed firms, we eliminate all duplicate entries with the same company name and

identify all firms that delisted through 2004.5 A total of 1,579 foreign firms meet these two

requirements. To ensure a more uniform set of firms are used in the ensuing analysis we also

require these firms to have Compustat data available on total assets (item #6) in either their first 2 Share code 12 refers to an ordinary share listed by a firm incorporated outside the U.S. and share codes of 30 and 31 denote American Depositary Receipts (ADRs). 3 Our sample also does not include ADRs which originally began as Rule 144A and Level I ADRs and later become Level II or Level III ADRs. Since we are interested in the profile of entrants at the point of listing these firms have already had some exposure to the U.S. market prior to their exchange listing. 4 Compustat provides country information for a subset of firms but we find errors in the data as many firms listed as foreign firms turn out to be U.S. firms. Therefore we hand check each firm to verify its country of origin using the Mergent and Hoover’s databases, or consulting the firm’s own website. 5 Duplicate entries can result for example if a foreign firm has dual class shares or common and preferred shares. In our sample, each observation represents one firm.

7

or second year post-listing, which reduces the number of listed firms to 1,330.6 From this sample

we compile the sample of delisted firms also using the CRSP share codes. We verify that the

delisted firms do not trade under a new name and that the firm did not move from one major

exchange to another. Firms that move from one major exchange to another are not treated as

delists whereas firms that delist to the Over the Counter (OTC) market or to the “Pink Sheets” are

treated as delists. A total of 728 foreign firms delist from a major exchange over the period 1961-

2004. Therefore our final sample of 1,330 firms is made up of 728 firms that subsequently delist

and 602 firms that continue to be listed on the NYSE/AMEX or NASDAQ as of December 31,

2004. The 602 foreign firms that continue to be listed in the U.S. are referred to in the remainder

of the paper as the “stay listed” sample. Our final sample is the most complete sample of foreign

listings and delistings to date.

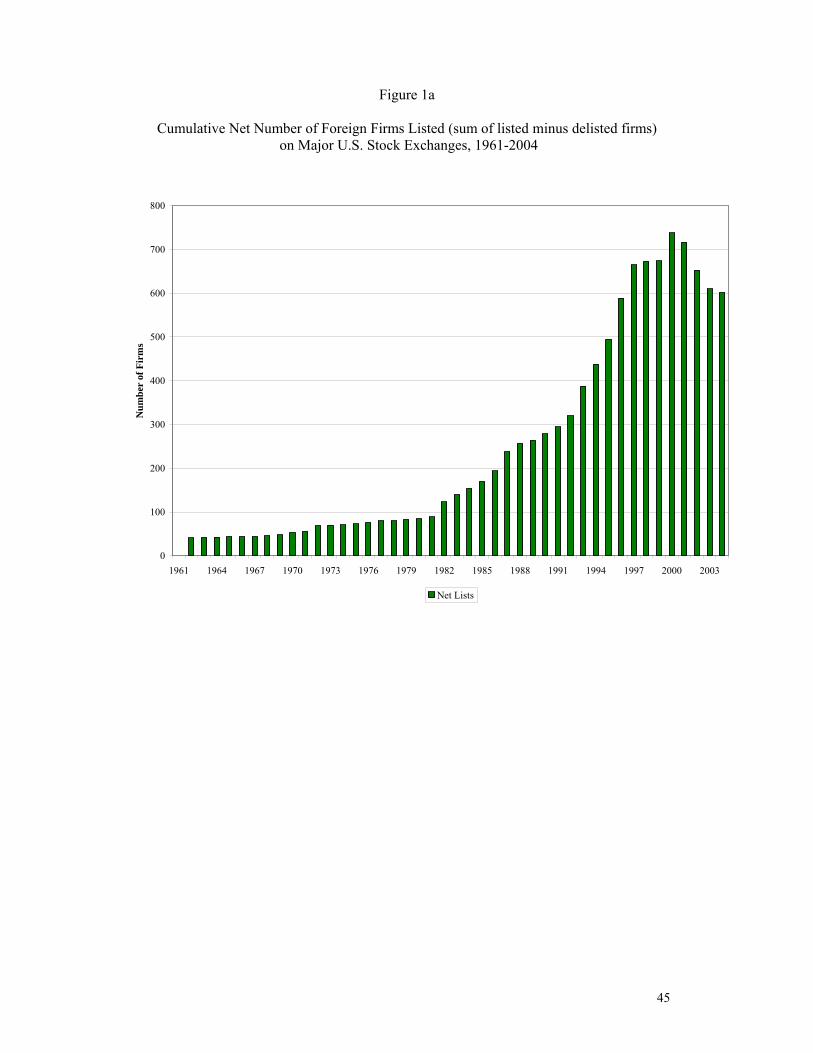

Figure 1a illustrates the total number of foreign firms listed (cumulative sum of listings

minus delistings) on major U.S. exchanges over the sample period. From a beginning of no

listings in 1961, total listings increase to 85 in 1980, to 279 in 1990, peak at 738 in 2000, and

then decrease to 602 in 2004. The figure reveals that the stretch of time from 1994-2000 has the

largest increase in the number of foreign listings, which is followed by a period from 2001-2004

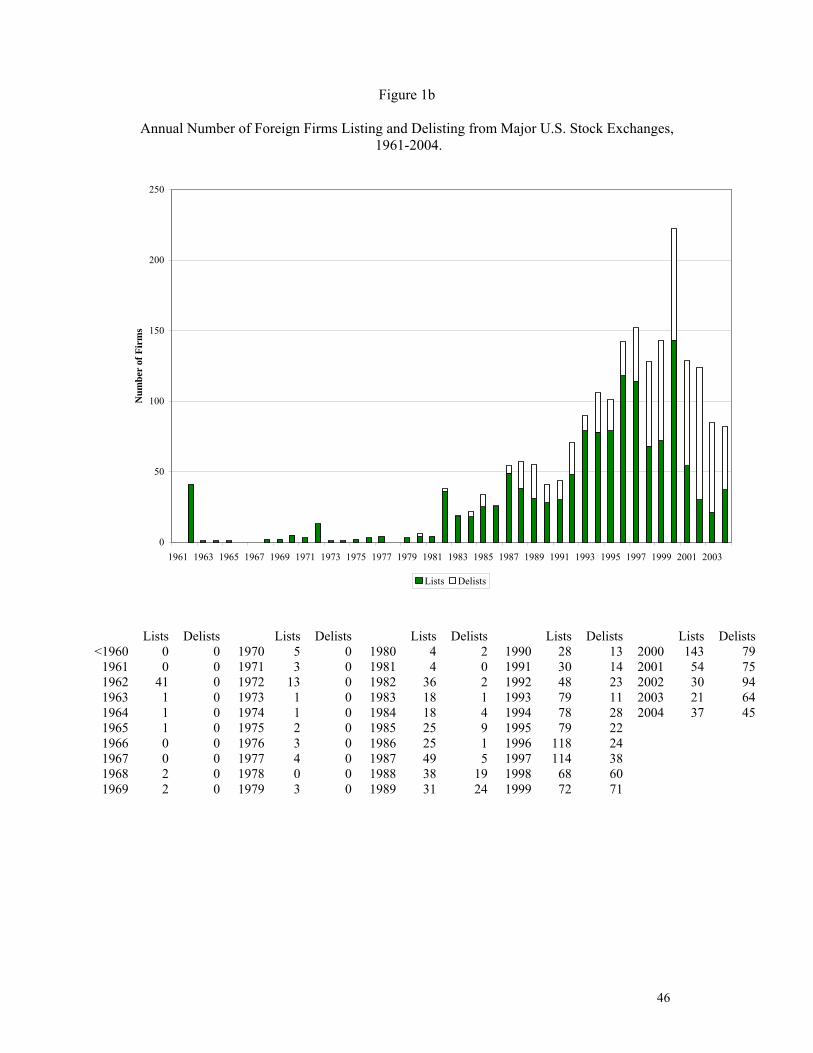

where delistings outnumber listings. Figure 1b shows the annual number of foreign firms listing

and delisting from major U.S. stock exchanges over 1961-2004. Before 1980, there are two years

with a sizeable number of listings but otherwise listings are sparse. Thereafter there is a steady

increase in the number of foreign listings – no year has fewer than 15 listings and listings peak at

143 in 2000. The first delistings occur in 1980 and grow more pronounced after 1997. The ratio

of the number of delists to lists over five year intervals shows a rise in the proportion of delists

over time. For example, the ratio of delists to lists is 0.16 from 1981-1985, 0.36 from 1986-1990,

6 There are a total of 1,579 foreign firms that list on a major exchange for which we can verify the country of origin and confirm they are not dual or cross exchange listings. The imposition of the data requirement that sample firms have data on total assets available from Compustat in either their first or second year post-listing results in a loss of 249 firms. Seventy percent or 171 firms of the 249 firms omitted for this reason were listed before 1986. The results of the paper are not sensitive to the exclusion of the 249 firms.

8

0.31 from 1991-1995, 0.53 from 1996-2000, and 1.96 from 2001-2004. It is the spike in this ratio

over 2001-04 – a rise in delists coupled with a decline in lists – that has raised concerns about the

competitiveness of the U.S. market.

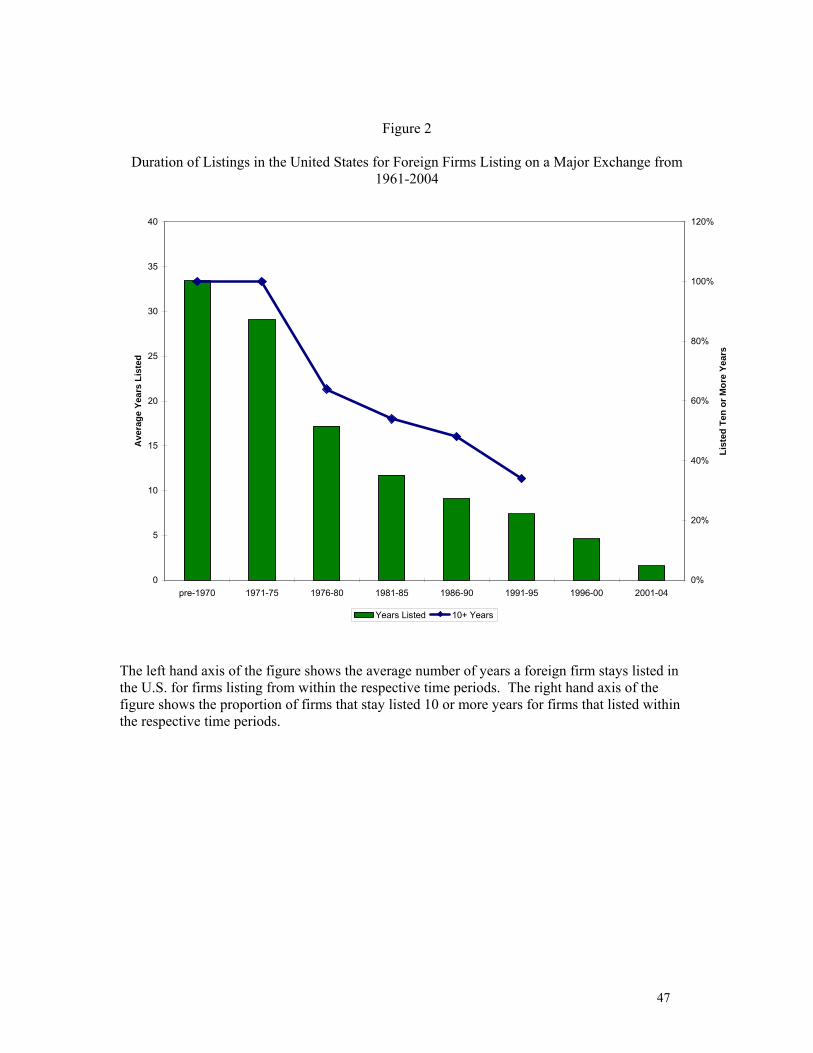

Figure 2 shows the length of time foreign firms stay listed in the U.S. Firms listed before

1970 stay listed an average of 33 years and this declines steadily over the next three decades to

five years for firms listed after 1995. We also compute the proportion of firms that stay listed at

least ten years following their listing date. The proportion of firms staying listed at least ten years

declines from 100% for firms listed prior to 1970 to 34% for firms listed from 1991-1995. A

similar trend emerges if we examine the proportion of firms that stay listed five or more years.

Hence, there has been a gradual reduction in the time foreign firms maintain a U.S. listing and

this pattern is apparent well before the passage of SOX.

2.2 Characteristics of Listing Firms over Time

A reduction in listing time has also been observed for U.S. “new lists.” Fama and French

(1997) attribute the reduction in listing time to greater acceptance of risks by U.S. investors as

evidenced by an increase in the number of poor quality firms that go public after 1980. Among

domestic IPOs, they attribute the drop in survivorship primarily to the large increase in new lists

“delisted for cause” after 1980. However, foreign new lists differ from U.S. new lists in several

respects that could impact their survivorship. First, a large number of foreign new lists are listed

in their home markets prior to their U.S. listing and thus are seasoned firms. Seasoned firms in

Fama and French’s (1997) study reveal little evidence based on profitability and asset growth of

declining quality. Second, the characteristics of “first time” U.S. IPOs by foreign firms (i.e.,

those without a prior trading history in their home market) indicate they are higher quality firms

at the point of listing compared to a matched sample of domestic U.S. IPOs (Bruner, Chaplinsky,

and Ramchand, 2004). All else equal, these factors might point to a higher survivorship rate for

foreign firms. Third, a foreign firm can voluntarily delist if a U.S. listing fails to provide positive

net benefits on an on-going basis and this is more likely to happen if the firm has a viable listing

9

in a non-U.S. market, typically its home market. These firms exit the U.S. market but since they

are able to meet regulatory requirements their choice to leave is presumably not related to poor

quality. All of this suggests that the factors affecting “survivorship” could differ between foreign

and U.S. new lists. On the other hand, foreign firms are not immune from poor performance and

the reduction in survivorship that is attributable to poor performance is also important to

ascertain. The U.S. market is regarded as having the highest listing standards in the world and one

role of standards is to ensure that high quality firms list in the U.S. Regulators are likely to be

less concerned about the loss of foreign firms that delist due to poor performance.

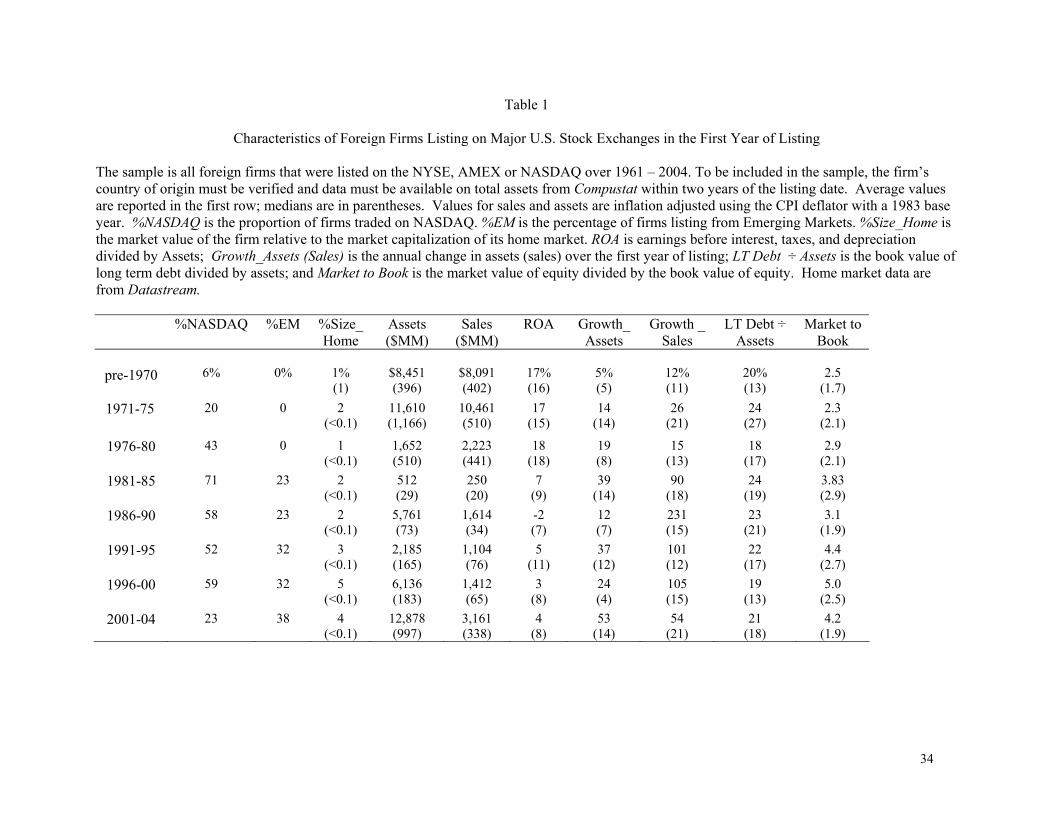

In Table 1 we examine characteristics related to the quality of foreign new lists over time.

The average and median values of the characteristics are reported for the first year of listing for

the full sample of listings over five year time periods from 1961-2004. To adjust for the effects

of nominal price increases over time, the reported levels of assets and sales are deflated by the

Consumer Price Index. Generally speaking, prior to 1980, the foreign firms listing in the U.S. are

large based on asset size, have high levels of sales and profitability, and originate exclusively

from developed market countries.7 The return on assets (ROA) is consistently above 17% on

average (median=15%) prior to 1980 and thereafter exhibits a distinct downtrend trend resulting

in an average ROA of 4% or less (median= 8%) in the final two five year periods. Hence, the

average and median firm’s operating profitability is cut by half or more over the course of the

sample period. At the same time, the growth rates in assets and sales generally increase over time

as does the market-to-book ratio. In the final time period, there is also some evidence of a

reversal in these general trends. During 2001-2004, firms have the largest asset size, positive

average and median ROA, higher levels of sales than in all but the pre-1980 periods, and are

more frequently listed on the NYSE, an indicator of quality (Baker, Powell, and Weaver, 1999).

7 Emerging and developed country status are based on country risk (CR) ratings from EuroMoney. EuroMoney ratings are not available at the beginning of our sample. The first rating that becomes available for the country is used to fill in the ratings in the early sample years. Rating levels below 85 are used as the cut-off for emerging markets, because this cut-off results in all G-8 countries being included in the developed market sample.

10

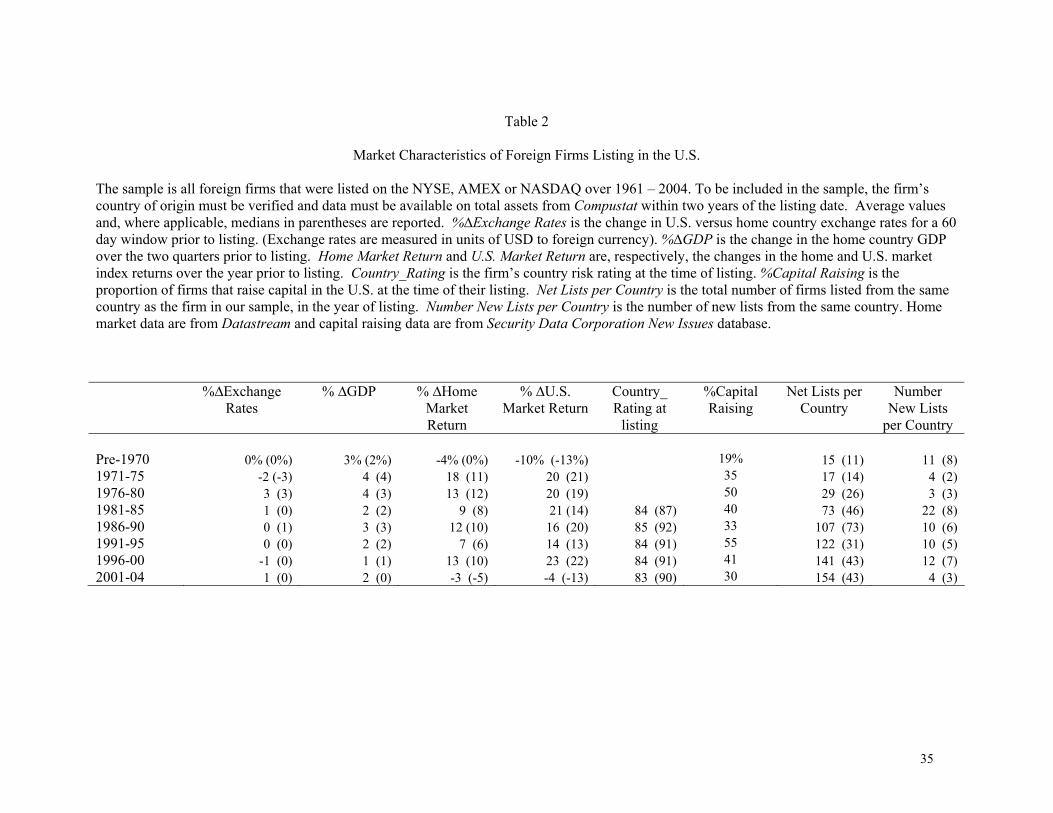

In Table 2 we report home and U.S. market characteristics related to growth, risk, and

visibility. First, the decline in the quality of firms noted in Table 1 could mirror deterioration in

the underlying home market conditions over time. Second, investor interest in foreign shares can

stem from the diversification benefits they provide. Diversification can relate to the differing

prospects for growth and market performance between the home market and U.S. market. The

aggregate characteristics we report shed light on the opportunities brought by the cohort of

foreign firms entering the U.S. over time. There is little evidence in Table 2 to suggest that the

declining quality of foreign entrants observed in Table 1 is explained by deteriorating home

market conditions. Foreign entrants are consistently associated with positive home country GDP

growth that has ranged from 1% to 4% over the two quarters prior to listing. With the exception

of two periods, foreign firms enter the U.S. under favorable home and U.S. stock market

conditions, and in all periods, the U.S. and home stock market performance move in parallel

fashion. The mean and median country risk measures also show a high degree of stability over

time which suggests that the cohorts of foreign entrants have not come from increasingly riskier

countries.

In the right hand columns of Table 2, we report several indicators of investor awareness

of foreign firms. Early on, one can imagine that the first firm entering the U.S. from a particular

country (e.g., China or Argentina) would be in high demand for its diversification value.

However as more foreign firms enter the U.S., the ability of a new entrant to be valued for

diversification purposes or to attract the attention of U.S. investors declines because investors

have more choices from the same country. For each firm in the sample we track at the point of

listing and delisting, the net number of listed firms from the same country. Net Lists per Country

reports the total number of firms listed in the U.S. from the same country. Foreign firms entering

the U.S. prior to 1970 for instance competed with 15 previously listed firms in the U.S. from the

same country on average (median=11). In this period the entrants came from predominantly two

countries, U.K and Canada. Over time more firms have entered the U.S. from an increasingly

11

diverse set of countries. By 2001-2004, there are 154 firms on average from each country

(median = 43) with listings in the U.S. Therefore, a challenge for any foreign entrant to the U.S.

today is how to “become known” and attract the attention of U.S. investors who have many more

firms to choose among from any given country. Merton (1987) argues that capital raising is

another activity that can enhance U.S. investors’ awareness of a firm. The capital raising variable

measures the proportion of firms that raise capital at the time of their listing. Since these listings

involve a “road-show” and efforts at investor outreach, firms raising capital may achieve greater

visibility. In Table 2, no trend is apparent in the proportion of firms raising capital over time.

With the exception of two periods, the majority of foreign firms list but do not raise capital.

The above results bear on the ability of foreign firms to generate some important benefits

associated with listing, namely greater investor recognition and liquidity. All else equal, lower

profitability and less distinctiveness among foreign firms might imply less ability to generate an

analyst following or trading volume over time. On the other hand, if over time investors become

more accepting of the risks associated with foreign shares then greater analyst coverage and

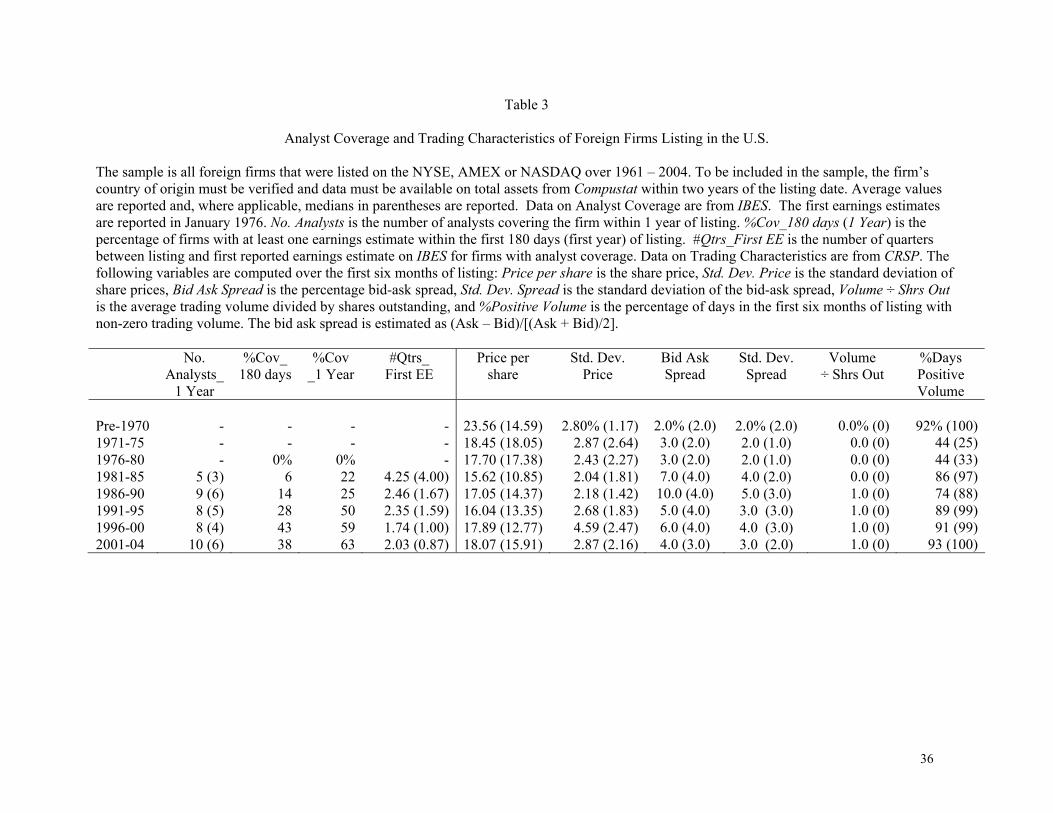

trading volume could increase over time despite the decline in profitability. In Table 3 we

examine the trends in analyst coverage, as an indicator of investor recognition, and the trading

characteristics in the U.S. market, as an indicator of liquidity. Information on analyst coverage is

gathered from the Institutional Broker Estimates System (IBES) database. As earnings estimates

only become available on IBES beginning in January 1976, our analysis of analyst coverage

begins with the 1976-1980 period. Of note in Table 3 is the large gain in the proportion of firms

able to generate analyst coverage over time. In 1976-1980, no firms have analyst coverage within

180 days of listing but the proportion with coverage increases to 38% by 2001-2004. If the post-

listing time period is extended from 180 days to one year, the same pattern of increased coverage

is observed – although the incremental gain in coverage over the expanded time frame is

relatively modest. Since 1996, the proportion of firms with analyst coverage has remained

relatively flat at roughly 40% after 180 days and 60% after one year. While over time there has

12

been a marked increase in the proportion of foreign firms with analyst following, a large fraction

of foreign firms – some 40% – remain without coverage at intervals up to one year post-listing.

By comparison, Bradley, Jordan, and Ritter (2003) reports that 75% of IPOs made during 1996-

2000 have coverage initiated immediately following the end of the quiet period or the 25th

calendar day post-offering. Cliff and Denis (2004) reports for a sample of 1,085 IPOs between

1993 and 2000 that 77.4% have at least one analyst recommendation within one year after the

IPO.8 Hence, relative to domestic firms the results suggest that foreign firms do not gain

comparable levels of analyst coverage.

In Table 3 we also report information on the share price, volatility, and other

characteristics associated with the volume and costs of trading. Since trading volume tends to be

positively related to good performance, one might expect that a decline in quality overtime would

be met by increased trading costs, but this is not the case in Table 3. While there is some evidence

that the average bid ask spreads increase and trading volume decreases (based on %Days Positive

Volume) in the middle portion of the sample, there is no discernable trend in the data.9 The

median bid ask spreads are approximately the same at the beginning and end of the sample, and

with the exception of adjusted volume (volume ÷ shares outstanding) which increases from zero

to 1% over time, the same finding holds for other characteristics. These results, when combined

with the conclusion that the quality of foreign entrants has declined over time, suggest that the

market has become more accepting of foreign firms over time.

8 Typical of many studies of U.S. IPOs, Bradley, Jordan, and Ritter (2003) and Cliff and Denis (2004) exclude ADRs from their samples. 9 By comparison, Cowan, Carter, Dark, and Singh (1992) reports that the average bid-ask spread for firms moving from the NASDAQ to the NYSE is 2.7% in the year prior to the move and 2.5% in the first year of trading on the NYSE. Macey, et. al (2004) reports an average bid-ask spread of 5.91% over a 60 day period prior to delisting for 54 NYSE firms delisting to the Pink Sheets.

13

3. Characteristics of Foreign Delistings

3.1 Classifications of Delistings

The pattern of survivorship is directly traceable to the firms that delist and in this section

we explore the characteristics of the delistings over time. We classify delistings into three broad

categories based on the CRSP share codes and our independent verification of the CRSP code.

Firms that are removed from major exchanges are classified into mergers and acquisition (CRSP

codes 200 - 400), involuntary (CRSP codes ≥ 400 excluding 570 and 573), or voluntarily

delistings (CRSP code 570). We verify that none of the delisted firms trades under a new name

or ticker on the NYSE or NASDAQ through December 31, 2004. Because code 570 delistings are

“delisted at the request of the company” and not at the behest of the exchange or market

regulators, they are classified as “voluntary” delistings. We check the accuracy of the voluntary

delists and the other categories of delists through text and web searches. For example, a firm

with CRSP code 570 is initially classified as a voluntary delisting. If, however, our search

uncovers information that the firm is in financial difficulty (i.e., missed interest payments,

rumored to be near Chapter 11, previously served a delisting notice by the exchange), its delisting

status is changed to involuntary. In these instances, we view the company’s request to be delisted

as akin to “resigning in advance of being fired.” Other code 570 delistings which prove to be the

result of a previously agreed to merger or tender offer are reclassified as M&A delistings. CRSP

code 551 (“too few shareholders”) is almost always associated with the successful completion of

a tender offer and these delistings are classified as M&A delists rather than involuntary delists.

An important caveat is that the amount and quality of information about the delisted firms has

improved over time. In those instances, where we are unable to find information about the firm,

typically for delists occurring before 1990, we rely on the CRSP code for the classification.10 As

a result, the distinctions between voluntary and other categories of delists are likely to be noisier 10 The large number of reclassifications suggests that the CRSP codes are noisy indicators of the reasons for delisting. For example, of the 96 firms with initial delist codes of 570 we end up with 48 as “voluntary” delists after the verification process.

14

in the early part of the sample. Nonetheless, to the greatest degree possible the code verification

process ensures that our final coding reflects the firm’s actual reason for delisting.

When foreign firms list on a U.S. exchange, they must meet both the listing requirements

of the exchange and the registration requirements of the SEC. By contrast, delisting removes the

obligation to meet exchange requirements but it does not eliminate SEC registration

requirements. To eliminate all costs of compliance of U.S. regulation, foreign firms must also

deregister which requires them to establish and maintain fewer than 300 U.S. shareholders over

time. Because deregistration has implications for the potential costs savings firms can realize

from ending SEC reporting obligations and compliance with Sarbanes-Oxley, we defer our

discussion of this topic to section 4.2 on voluntary delistings. To voluntarily terminate a listing,

the NYSE requires that a firm gain the approval of its audit committee and Board of Directors

before delisting, while NASDAQ simply requires a letter stating the reasons for delisting. In

neither case is shareholder approval required.11

If a foreign firm has ADRs trading and delists, there is also no reason to maintain its

ADR program. An ADR program generally may be terminated by giving the depositary bank at

least 30 days written notice of termination. Until the stated termination date, ADR holders

typically receive the underlying ordinary shares in exchange for their ADRs. At the stated

termination date a depositary bank ceases to make new ADRs and active trading in the ADRs is

suspended. The depositary agreement generally allows ADR holders up to a year following the

stated termination date to remit their ADRs for cash. However, because “cashed-out” holders are

no longer counted as U.S. shareholders, which helps in meeting the 300 limit for deregistration,

issuers frequently amend the depository agreement to accelerate the termination date of an ADR.

11 See Macey, et. al (2004) for a discussion of NYSE and NASDAQ delisting procedures.

15

As a result, it typically takes four to five months from the notification of the intent to delist until

the actual cessation of trading.12

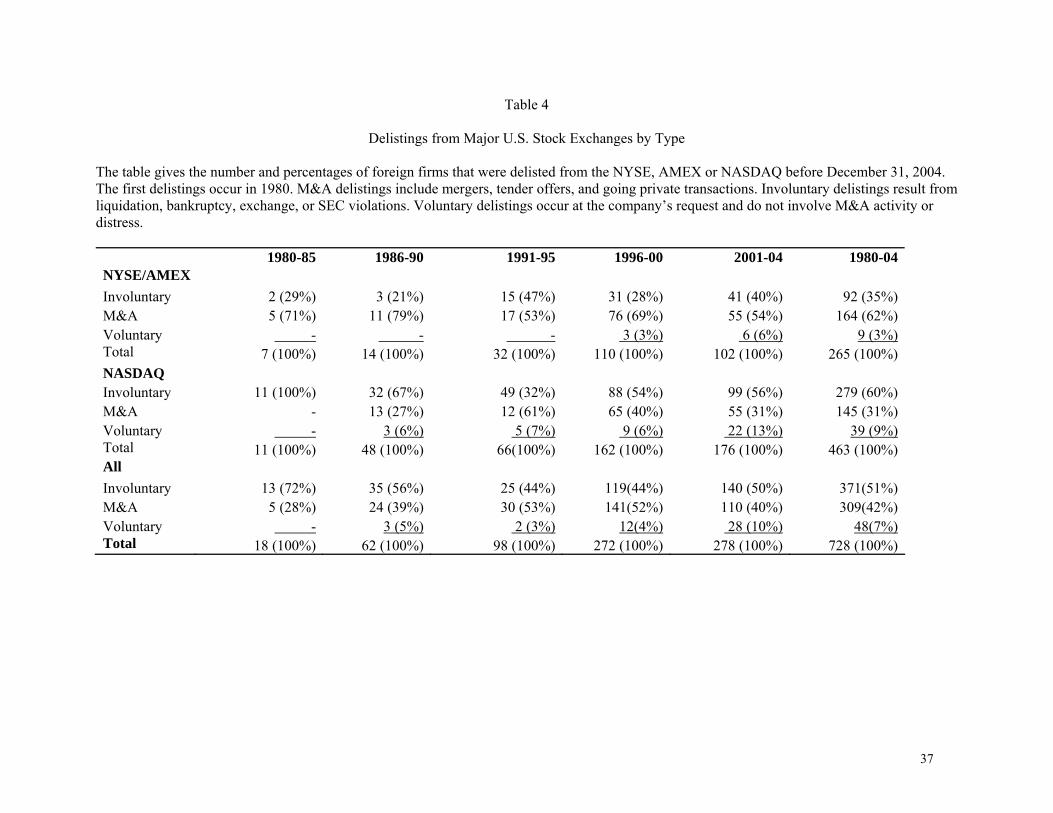

Table 4 presents the number and type of delists over time. Although our sample period

covers 1961-2004, the first delists do not occur until 1980. Of the 728 delistings, 463 firms

(63.6%) of the sample delist from NASDAQ and 265 (36.4%) delist from the NYSE/AMEX over

the period 1980-2004. For the overall sample of delistings, M&As make up the largest category

of NYSE delistings (62%) and involuntary delistings make up the largest category of the

NASDAQ sample (61%). For all exchanges, 51% of delistings are M&A, 42% are involuntary,

and 7% are voluntary. While all categories of delists trend upward over time, one observes a large

increase in the number of voluntary delistings in the final period. Over the twenty year period

from 1980-2000, there are a total of 17 voluntary delistings but this increases to 28 in 2001-2004

alone. Thus, the increase in voluntary delistings occurs in the period following passage of

Sarbanes-Oxley in July 31, 2002. The results for foreign firms parallel the findings of Leuz,

Triantis, and Wang (2004) and Marosi and Massoud (2005) which document an increase in the

number of U.S. firms delisting post Sarbanes-Oxley.

3.2 Reasons for Foreign Delistings

The results in Table 1 point to a deterioration in the quality of foreign entrants over time.

Yet some firms stay listed while others do not. In this section, we explore several potential

explanations for this finding. At the time of entry, delisted firms may have hoped to achieve a

level of benefits that ultimately failed to materialize and the question is why these listings prove

less successful. A useful analogy by which to consider foreign listings is the college admission

process. Foreign new lists are all “admitted” to the U.S. market but admission alone is not a

complete indicator of the success that a firm might ultimately achieve. At the point of entry stay

listed firms could be higher quality firms compared to delisted firms in a way that presages

12 Liu (2004) reports an average of 70 trading days between the announcement of an involuntary foreign delisting and actual delisting.

16

greater likelihood of success. That is, delisted firms could have lower admission criteria (e.g.,

lower grades and test scores) and be “weaker students” in the pool of admits than stay listed firms

and thus have a lower probability of success from the beginning. If these quality differences are

evident at entry, then it follows that there will also be differences between the firms entering and

the firms exiting in any given period. Alternatively, it could be that delisted firms deteriorate in

quality after listing. If this is the predominate explanation for their exit, then at the point of entry

all firms should be of similar quality. Likewise, one would expect to see deterioration in quality

on average between listing and delisting firms. In the ensuing analysis we look for evidence

consistent with these effects. First, we compare the entry characteristics of firms that stay listed

to firms that delist. This comparison occurs for the first year of listing. Second, we compare the

characteristics of entering firms to exiting firms at the same point in time. Finally we focus on

the delisted firms and compare their characteristics at various points in time between their entry

and exit. The change in the characteristics of the firms from listing to delisting amounts to a

“report card” on the firm’s stay in the U.S.

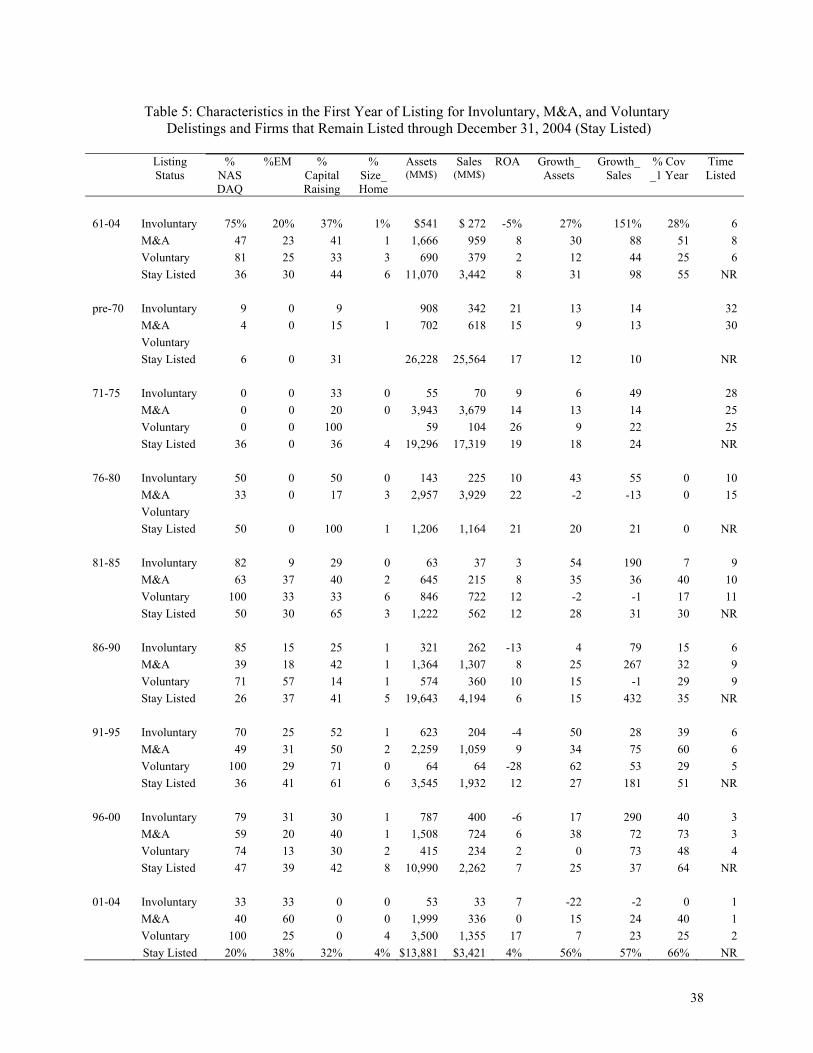

In Table 5, we compare entry characteristics related to quality for the stay listed firms and

the firms that delist. This analysis provides a first look at the “seeding” of the players upon their

arrival in the U.S. Looking first at the results over the entire sample period, 1961 – 2004, one

observes that at the time of listing the stay listed firms are larger in terms of size (%Size_Home,

Assets, and Sales) and have the highest profitability in comparison to the delisted firms.13

However the firms that eventually delist due to mergers and acquisitions are closer in size and

equal in profitability to the stay listed firms compared to the voluntary and involuntary delists. At

the time of listing, voluntary delistings are similar in size to the involuntary delistings but they are

distinguished by higher levels of profitability. Involuntary delistings are revealed to be inferior

13 With respect to time listed, as of year end 2004 the firms in the stay listed group have been listed in the U.S. for an average of nine years.

17

on many dimensions – small size and negative operating performance – in comparison to the

other groups.

When we break the full sample into five year time periods, with few exceptions the

findings for the overall sample continue to hold. M&A delistings remain closer in terms of size

and profitability to the stay listed firms. In all periods the stay listed and M&A delistings

experience positive ROA on average. Involuntary delistings are profitable firms on average

before 1986 but thereafter their profitability turns markedly negative until the final period. Since

the averages of the size variables exceed the medians by wide margins, involuntary delistings are

exceedingly small firms at the time of listing. Similar to the full sample, voluntary delistings tend

to be similar in size but more profitable than the involuntary delistings with the exception of

1991-1995 where voluntary delistings are the smallest and least profitable firms. Finally of note,

in the last period the voluntary delistings are closer in size to the stay listed firms than in the

previous periods and have the highest ROA of all groups. Thus, the evidence suggests that the

firms voluntarily delisting in 2000-2004 are of higher quality compared to the earlier sub-periods.

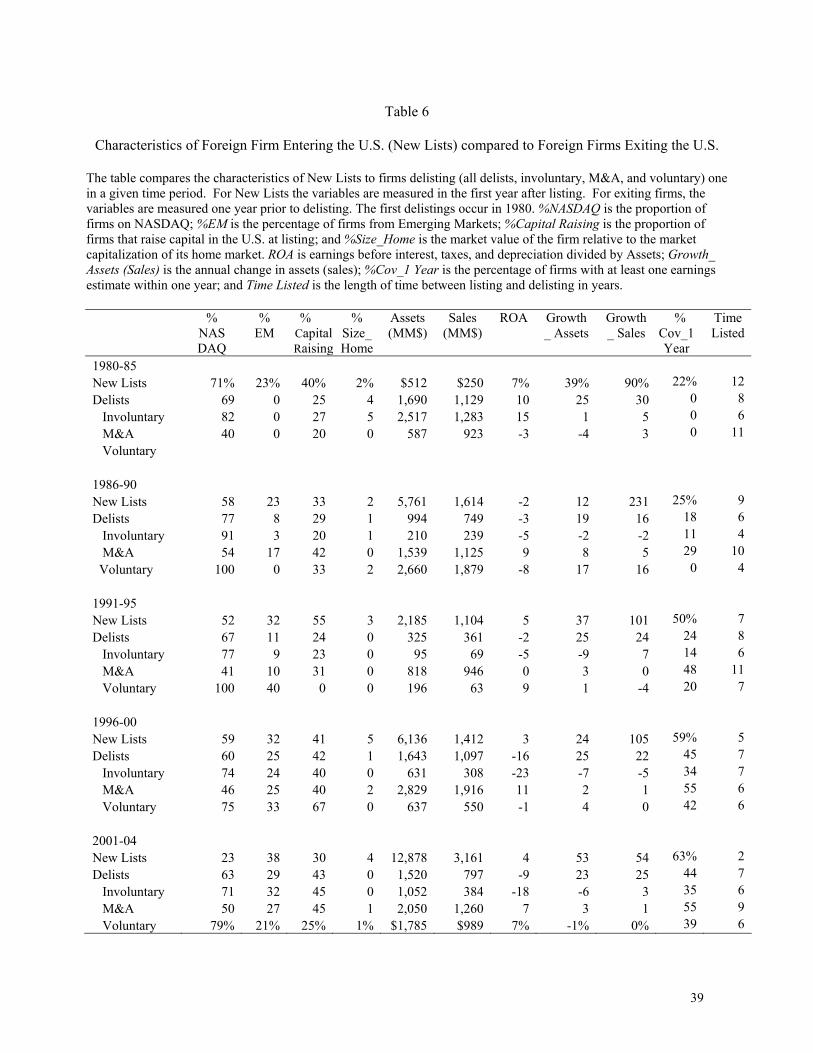

In Table 6, we compare the characteristics of the firms entering and exiting in a particular

time period. For example, the “New Lists” category shows characteristics of the firms entering

during 1980-1985, while the delist categories show characteristics of the firms delisting during

1980-1985. In any given time period, entering firms are presumed to be acceptable to U.S.

investors. Hence, holding the time period constant, comparing the characteristics of entering

firms with those exiting provides a framework to gauge acceptability. Without some minimal

level of acceptability, it is hard for firms to gain the investor recognition, liquidity and the other

benefits anticipated from listing. Focusing on the periods after 1986 where there are a larger

number of delists in each category, with the exception of 1991-1995, the profitability of M&A

delists at exit exceeds that of New Lists and they are closer in size to the New Lists than the other

18

categories of delists.14 Firms can merge because they are doing well or poorly. In section 4.1 we

separate the merged firms based on an assessment of their financial strength but even in the

“pooled sample” in Table 6 the evidence suggests M&A delists possess the necessary quality to

be acceptable to U.S. investors. The same cannot be said for the involuntary delists. They have

negative profitability at exit and are several time smaller in size than the New Lists in all time

periods. Voluntary delists again are mixed. In 1986-1990 and 1996-2000, they have negative

ROA on average and tend to be smaller firms than New Lists, while in 2001-2004, their quality,

especially profitability, improves compared to New Lists. Although the small number of earlier

voluntary delists makes definitive judgment difficult, the cumulative evidence points to higher

quality firms voluntarily exiting the U.S. compared to earlier periods. If true, the increased

number of voluntary delists in recent years is a concern in light of the evidence that the quality of

these firms has increased over time. We investigate the circumstances surrounding the voluntary

delists more fully in section 4.2

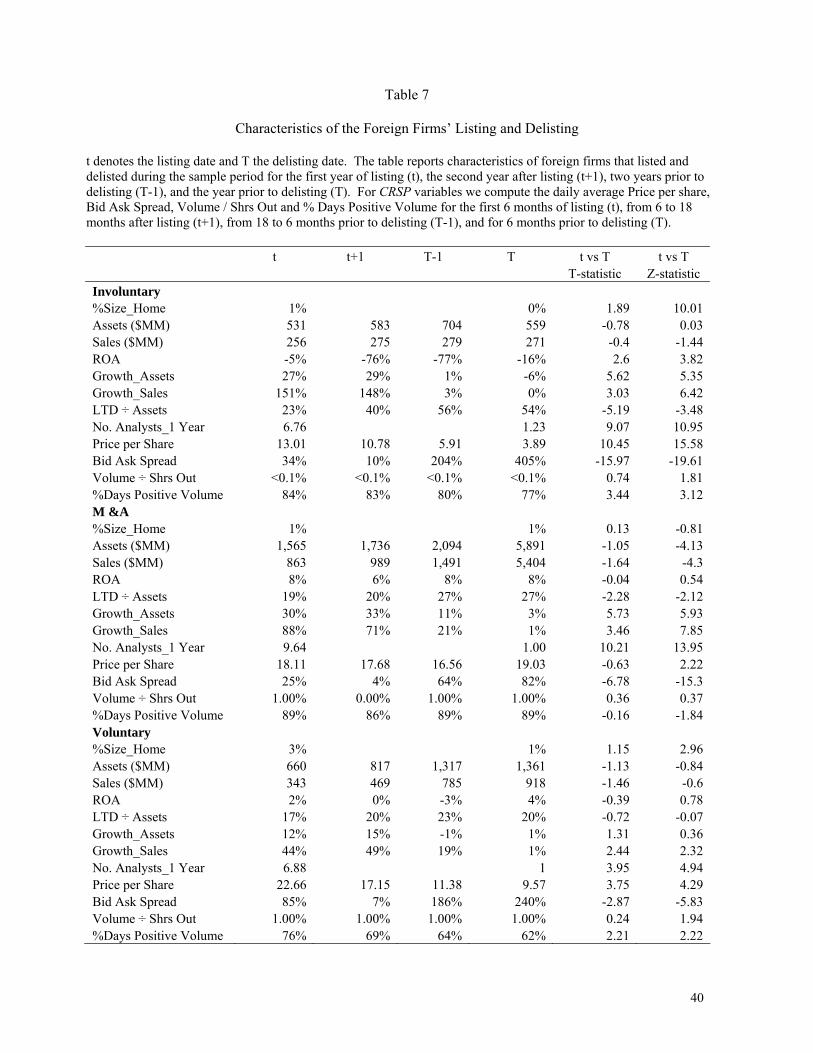

In Table 7 we compare the same firm at four points in time over the course of their listing

to delisting. In Table 7, t denotes the year of listing and T the year of delisting. Compustat

variables represent averages across firms for the year of listing (t), the year after listing (t+1), the

year before delisting (T-1), and the year of delisting (T).15 For the variables computed from

CRSP data (e.g., Price per Share, Bid Ask Spread), we take the average (and median) values for

each variable over four sub periods: t denotes the period from the listing date to 6 months post-

listing, t+1 denotes the period from 6 months to 18 months post-listing, T-18 denotes the period

18 months to 6 months prior to delisting, and T is the 6 month period prior to the delisting date.

14 In the period before 1990, the voluntary delists show more similarity to involuntary delists than in later time periods. This is likely due to the small number of voluntary delists (3) and the inability to find information on the nature of delists that occurred in this period. 15 For annual Compustat variables, the year of listing (t) corresponds to the first fiscal year end following the month of listing. For example, if a firm lists in November 1999 and data are available for 1999, the first year of listing is 1999. If data are not available then the first year corresponds to 2000.

19

The use of four periods isolates the periods closest to listing and delisting which might be colored

by the events of listing or delisting.

Some interesting findings emerge across the categories of delists in Table 7. For one,

constant dollar assets and sales increase for all categories of delists indicating that foreign firms

grow larger over the course of listing but the effect is muted for involuntary delists. M&A delists

have the highest and most consistent average ROA across the four periods and the median ROA

(not reported) is 10% in all periods. M&A delists are the only category of delists to experience

an increase in their average share price from $18.11 in the first 6 months of listing to $19.03

(median=$13.05) at delisting. By comparison the ROA of the involuntary delists rapidly

deteriorates over the first two periods declining from -5% in period t to -76% in period t+1.

Consistent with this, the average share price falls from $13.01 at listing to $3.89 (median=$0.90)

at delisting. Again the voluntary delists fall in between the two groups. Their average ROA

increases from 2% at listing to 4% at delisting, with some variation in between. However the

median ROA of the voluntary delists shows greater and more stable profitability, ranging from

7% to 9% across the periods, suggesting that average is brought down by a few firms with

extremely poor profitability. The average share price at listing ($22.66) is the highest among the

delist categories but falls to $9.57 (median=$4.92) at delisting. With respect to trading

characteristics, the bid-ask spreads are lowest for all three delist categories in period t+1, a period

reflecting some seasoning of the firm but before concerns for delisting begin to arise. Thereafter

the bid-ask spreads balloon for all delists, reflecting the difficultly of measuring the percentage

spreads for low priced shares. The %Days Positive Volume is less affected by these issues and it

shows that the voluntary delists have the highest number of days with zero trades of the delist

groups.

Taken together the above results suggest that the decline in quality of listing firms

documented in Table 1 is attributable in large part to the involuntary delists. Compared to others,

involuntary delists are smaller and less profitable firms at the time of entry, their quality

20

deteriorates between listing and delisting, and over the sample period. By contrast M&A delists

are larger firms at entry, increase in size over the course of listing, and have, almost without

exception, positive and stable profits. The voluntary delists fall in between the other groups but

their numbers are so few that their influence is small on the overall results. That poor quality

firms leave the U.S. is not an indictment of the U.S. market but rather a strength. Of greater

import is how firms with the requisite quality to be of interest to investors and that can potentially

benefit from listing fare in the U.S. market. From the univariate results, it appears that the U.S.

market is retaining the largest sized firms while facilitating mergers of better performing firms.

Some quality firms also appear to be voluntarily exiting the U.S. market. We examine whether

these findings hold in a multivariate setting in the next section.

3.3 Multivariate Analysis of Listing Status

To gauge the robustness of the previous univariate results, in this section we examine the

factors associated with survivorship in the U.S. market using a probit and multinomial logit

analysis in Table 8.16 In particular, we examine what characteristics at the time of delisting

distinguish between the firms that remain listed versus those that delist. A probit analysis is used

to uncover broad distinctions between all foreign firms delisting (dependent variable=1) and

those that remain listed (dependent variable=0). For the delisted firms the independent variables

are measured one year prior to delisting. For stay listed firms, the independent variables are

constructed relative to December 31, 2004, the end of our sample period.17 Consistent with the

univariate results, foreign firms are significantly more likely to delist if they are small firms with

16 To economize in reporting the results, we report the most parsimonious probit and multinomial logit specification. In unreported results, we estimate other specifications that examine a broader set of firm profitability measures, growth measures such as the market-to-book ratio or growth in assets, and the difference between home and U.S. market returns. The main findings with respect to size, profitability, and market conditions are not sensitive to the specification reported. 17 We also conduct the probit analysis using a matched sample approach. Each foreign delisted firm is matched to a stay listed firm from the same country that listed in the same year. To avoid duplicate matches, we pick a match without replacement. If we do not find a match for either the country or the listing year, the delisted firm is removed from the sample. The matched stay list firm is then assigned the same delisting date as its paired delisted firm and the independent variables are computed for a year prior to that date. The results are qualitatively similar to those reported.

21

poor profitability (ROA). Several variables assess the strength of home market conditions at the

time of delisting and how this influences survivorship. One hypothesis is that U.S. investors

could find foreign firms of greater interest when home market performance or GDP growth is

strong. Conversely, if weaker home market conditions are accompanied by a depreciation of the

home currency relative to the U.S. dollar, U.S. investor interest could increase as shares of

foreign firms become more attractively priced. However, there is little evidence that home

market conditions influence the delisting decision as the coefficients of %∆GDP, Home Market

Return, and %∆Exchange Rates are insignificant. More evidence points to issues of investor

awareness influencing the decision. For example, foreign firms with a higher portion of trading

volume in the U.S. relative to their home market (US_Home Volume) and firms that have raised

capital in the U.S. market are significantly less likely to delist. Since trading volume and security

purchases are the outright expressions of investor interest (or lack thereof) foreign firms less able

to generate trading volume or that do not raise capital in the U.S. are more likely to delist. The

coefficient of Net Lists per Country is positive and significant indicating that firms with more

substitutes vying for investor attention are more likely to delist. Firms from emerging markets

(Country_Rating) are also less likely to delist. One interpretation of this result, when coupled

with the finding for capital raising, is that the home markets of emerging market firms are less

able to support their liquidity and funding needs compared to firms from developed markets. An

alternative interpretation is that emerging market status and capital raising are synonymous with

greater growth prospects, which U.S. investors value, although the previous lack of significance

for home market conditions weighs against this.

In columns 2-4 of Table 8, we estimate the same specification using a multinomial

logistic regression. The multinomial logit model permits the dependent variable to take on a

wider range of outcomes for listing status than the probit model. Further, by simultaneously

estimating the probabilities associated with the outcomes, the model provides more consistent

estimates and ensures that the probabilities sum to unity across the outcomes. The multinomial

22

logit is modeled as Pj=exp(X βj )/ [1 + Σkexp(Xβk)] where β is a vector of coefficients, X, the

vector of independent variables, and k equals 1 to J. The probability that the foreign firm “stays

listed” equals P0 = 1/[1 + ΣkexpXβk)], which represents our base case. The categorical dependent

variable is equal to 1 if a foreign firm is delisted for cause (“involuntary”), 2 if a foreign firm is

delisted following a merger or acquisition (“M&A”), and 3 if a foreign firm voluntarily delists

from a major U.S. exchange (“voluntary.”) These categories of the dependent variable measure

the probability relative to the base case of “stay listed.” The multinomial results reveal that

greater size, stronger U.S. market conditions, and more firms listed per country significantly

reduce the probability of delisting for all categories of delists. Again there is little evidence that

home market conditions influence delisting. Lower profitability increases the probability of M&A

and involuntary delisting but does not significantly affect the probability of voluntarily delisting.

Voluntary delists are more likely to occur for ADRs and NASDAQ quoted firms.

For firms having more choice about delisting, the multivariate results suggest that M&A

delists are more likely to occur for smaller firms, less profitable firms originating from developed

markets compared to stay listed firms. M&A delists also have a greater likelihood of occurrence

if firms do not raise capital with their listing, have lower percentages of U.S. trading volume, and

when there are more listed firms from the same country. Voluntary delists are more likely to

occur for smaller, NASDAQ quoted firms, and in circumstances where there are more firms from

the same country. Firm specific and U.S. market characteristics rather than home market

characteristics appear to be more influential in delisting. Further, it should be noted, that many of

the above noted factors also reflect lower investor interest in the firms’ shares.

4. A Closer Look at M&A and Voluntary Delists

In this section we examine two groups of firms, the M&A and voluntary delists, that can

meet regulatory standards but choose to delist. Because firms that are of sufficient quality to

23

meet listing standards represent a larger potential opportunity loss to U.S. investors than the firms

delisted for cause, these delisting firms deserve further attention.

4.1 M&A Delists

As noted earlier, M&A delists provide a mixed signal with respect to quality. Some

firms are acquired because it is a better alternative than failing; others choose to be acquired

because they have some asset or potential value that other firms recognize and will pay for. In

this section, we identify the firms that merge “from strength” as opposed to those which appear to

have few alternatives. These firms have greater potential to be of interest to other firms and in

delisting choose to avail themselves of the opportunities that arise following listing in the U.S.

By eliminating the weaker M&A delists, we obtain a clearer picture of how these firms compare

to the stay listed firms than in the earlier analysis.

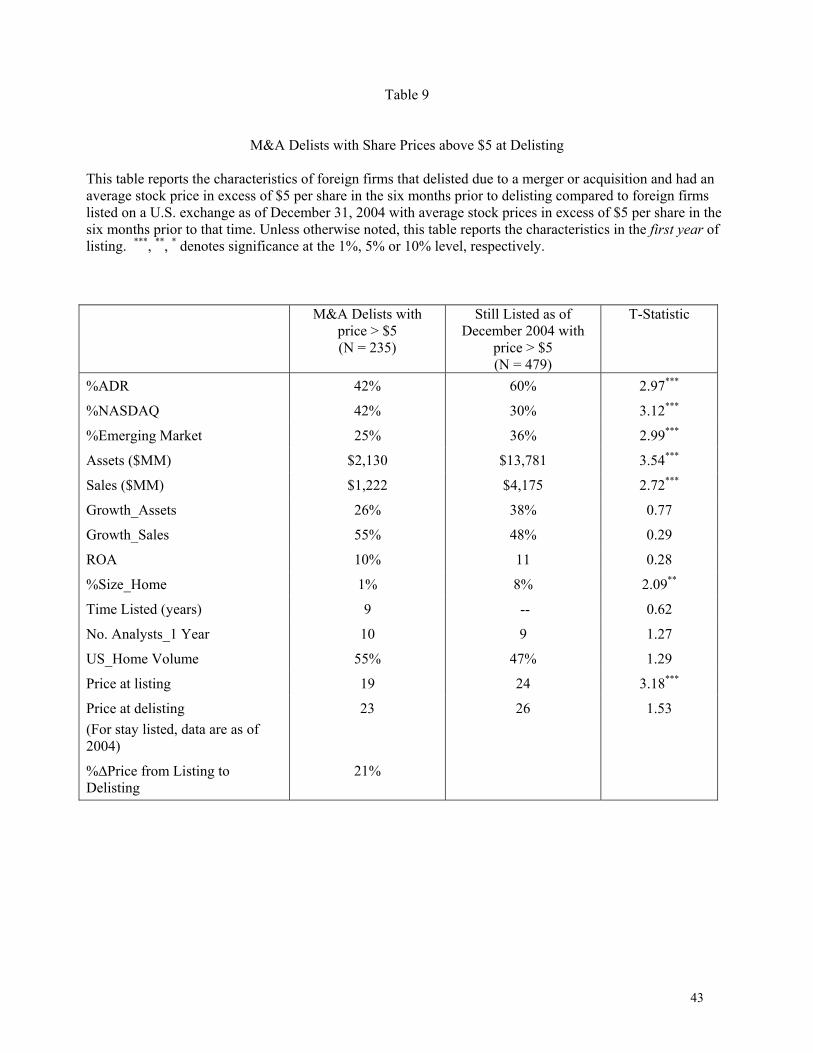

To focus on the M&A delists with stronger performance, we search Mergent for more

information on the firms. We previously eliminated firms that were classified by their CRSP

codes as M&A delists but showed evidence of financial distress, moved to the Pink Sheets, or to

the OTC market. For this analysis we further eliminate firms that have average share prices

below $5 in the six months prior to delisting. Since $5 is often used as a threshold below which

certain institutional investors cannot hold the shares, it is a reasonable first cut at quality,

although the results are not sensitive to cut-offs between $1.50 and $5.00. Relative to the 309

M&A delists in the original sample, this criterion eliminates 74 firms. The 235 M&A delists that

remain are compared to stay listed firms with average share prices above $5 in the six months

prior to December 31, 2004. The original stay listed sample is reduced by 123 firms by the

imposition of the $5 price cut-off.

The elimination of weaker M&A delists in Table 9 produces, as expected, a sample of

larger and more profitable firms relative to Table 5. For example, in Table 5 the original sample

of M&A delists had at listing average total assets of $1,666 million, sales of $959 million, and

8% ROA. By comparison “strong” M&A delists are larger in terms of total assets ($2,130

24

million) and sales ($1,222 million) and have higher ROA of 10%. The stay listed group remains

significantly larger firms in terms of assets and sales but have comparable profitability and

growth rates of assets and sales. Strong M&A delists and stay listed firms also have similar

analyst coverage and similar proportions of volume traded in the U.S. versus the home market.

This evidence indicates that the firms achieve equivalent levels of investor recognition as the stay

listed firms, which helps create the opportunity to be acquired. Relative to earlier results, one

also observes a larger change in share price from listing to delisting for this group as their average

share price increases by 21% over the course of listing.

We repeat the analysis in Table 9 using a matched sample of strong M&A delists and stay

listed firms (not reported). For this analysis we match each M&A delist to a stay listed firm from

the same country that listed in the same year (see footnote 17 for a discussion of the approach).

The matched sample results in 51 pairs of firms for comparison. In the year of listing strong

M&A delists have average assets of $2.1 billion and a share price at listing of $20.35 compared

$21.8 billion in assets and a $26.85 share price for the matched firms. The other variables, such as

ROA, growth rates in assets and sales, and analyst coverage, do not differ between the groups.

Thus, the results are qualitatively similar to those reported in Table 9.

In unreported results, we find that the majority of the strong M&A delists do not leave

the U.S. but become part of a larger entity that stays in the U.S. Although these foreign firms

delist, their entry and subsequent take over by firms operating in the U.S. redounds to the benefit

of the U.S. economy.

4.2 Voluntary Delists

Voluntary delistings raise the question why firms that can meet the necessary regulatory

thresholds exit the U.S. market. Because these firms possess the requisite quality, their exit raises

the greatest concern about the competitiveness of the U.S. markets. Since 2002 most this concern

has centered on whether the high regulatory costs accompanied by the passage of SOX are

driving foreign firms to leave the U.S. There are several reasons to believe that SOX may not be

25

the only driver of voluntary delistings. First, as discussed in the studies of U.S. delistings by

Leuz, Triantis and Wang, (2004) and Marosi and Massoud (2005) the extent of potential cost

savings from delisting is complicated by the fact that delisting from a U.S. exchange removes the

obligation to meet exchange requirements but it does not eliminate SEC registration

requirements. There is general agreement that the bulk of listing requirements and costs involve

SEC registration.18 By comparison to U.S. firms, the process of deregistration is more arduous

for foreign firms. SEC registration is triggered not only by listing, but also by the existence of a

significant shareholder base. Foreign firms with assets greater than $10 million that have over

500 shareholders world-wide of whom 300 or more are resident in the United States, are required

to register their shares under Section 12 of the Exchange Act, regardless of whether they are

exchange listed. Hence, before a foreign firm can terminate its registration and cease filing with

the SEC it must verify that it has fewer than 300 shareholders in the United States. If the firm has

fewer than 300 U.S. shareholders, it can terminate its registration under the Exchange Act by

filing Form 15 with the SEC. However, Form 15 is effective only for as long as the issuer

maintains fewer than 300 shareholders in the United States. For firms that have previously issued

securities in the U.S., if the number of shareholders in the United States increases above 300, the

issuer can again find itself subject to the reporting requirements of the Exchange Act.19 Moreover

for dual listed firms, it is difficult to police the nationality of individuals purchasing their shares –

18If the foreign firm conducts a public offering, the issuer will have filed a Form F-1 registration statement with the SEC under the Securities Act and Form 8-A to effect the registration under the Exchange Act. If the firm only lists securities, it will have filed a Form 20 – F registration statement under the Exchange Act. In either case, if the issuer enters the United States using an ADR, it will have also filed a Form F-6 registration statement. 19 This complication occurs for firms that conduct public offerings in the United States. They become subject to an independent SEC reporting requirement under Section 15(d). Section 15(d) provides that if an issuer has ever filed an effective registration under the Securities Act of 1933, the issuer has continuing reporting obligations under the Exchange Act. For issuers that are registered under Section 12 (b) and (g) of the Exchange Act, practically speaking this is a redundant reporting requirement. However, should the foreign firm later terminate its Exchange Act registration, Section 15(d) reporting obligations do not terminate and can only be temporarily suspended if U.S. shareholders number less than 300.

26

making it potentially more difficult for foreign firms to stay permanently below the 300

shareholder limit. 20

An additional challenge foreign firms’ face in meeting the 300 shareholder limit is the

manner in which they are required to count the number of U.S. shareholders who hold their ADRs

and the underlying ordinary shares. If securities are held in street name by financial institutions

(e.g., brokers, mutual finds, and banks), foreign firms are currently required to identify the

number of separate accounts containing shares of U.S. residents on a worldwide basis.21 In

meeting the 300 holder limit, a foreign firm must count each of the separate accounts as a holder

of record, whereas a U.S. firm is allowed treat all the shares held in street name by a single

institution as one holder of record. Also counting toward the 300 holder limit are the ordinary

shares held by U.S. investors in accounts at foreign banks and brokers. The law is silent with

respect to whether firms can rely on third parties to assist in counting their shares. Consequently,

foreign firms frequently complain that it is more difficult for them to accurately identify the

number of U.S. shareholders and to meet the 300 holder limit than for U.S. firms. Absent

deregistering, foreign firms do not escape SEC regulation and are unable to achieve the bulk of

the costs savings from exiting the U.S.22

While foreign firms voluntarily exiting the U.S. often point to the increased regulatory

burden of the U.S. markets post-SOX, they often cite other reasons for their delistings. The

20 The temporary nature of the suspension from registration has prompted some deregistered foreign issuers to amend their articles of incorporation to limit the number of U.S. shareholders below 300. 21For example, if 10 individuals hold shares at Fidelity, Inc. in individual accounts a U.S. firm can count that as one holder of record, whereas a foreign firm must count it as 10 holders of record. 22 Another distinction between U.S. and foreign firms’ delistings concerns access to alternative vehicles for liquidity and capital in the U.S. U.S. firms that “go dark” will often immediately become eligible to trade on the Pink Sheets which does not require that a firm be registered with the SEC (see Leuz, Triantis and Wang, 2004, and Marosi and Massoud, 2005). Foreign firms quoted on the Pink Sheets are required to have a Rule 12g3-2(b) exemption from registration, which allows a foreign firm, not otherwise listed in the U.S., to avoid registration if it furnishes an English translation of its local filings to the SEC. Before a delisted foreign firm can seek a Rule 12g3-2(b) exemption it must establish that it has fewer than 300 U.S. shareholders for a continuous period of at least eighteen months. Were this rule not in place, more foreign firms might upon delisting establish Level I ADRs that trade on the Pink Sheets and maintain a market for U.S. investors without being subject to SEC regulation. In addition, access to the Rule144A market and the potential capital raising opportunities provided through Qualified Institutional Buyers also requires a 12g3-2(b) exemption.

27

recent experience of Fisher and Paykel Industries illustrates the set of circumstances that

managers face in delisting their securities. Fisher and Paykel Industries, a New Zealand

conglomerate, had a low-growth appliance division and high-growth healthcare division. In

November 2001, the company decided to separate into two companies and conducted a U.S. IPO

on NASDAQ of the health care company issuing 4.4 million ADRs representing 17.6 million

ordinary shares or 18% of its outstanding shares. Tony Buckley the CFO of Fisher and Paykel

describes the motivation to voluntarily delist from NASDAQ just 15 months later.

“In February, 2003, the board made the decision that the ADR wasn’t cost effective. Only 1% of our shareholders held ADRs, we had Sarbanes-Oxley and heavy compliance costs and our shareholders in Australia and New Zealand kept asking us why were we still listed in the U.S. when it was costing as half a million bucks a year. Our New Zealand and Australian investors told us they would fund our capital raising so it wasn’t as if we couldn’t raise capital elsewhere. The decision was made to remove the compliance cost and return to being an Australasian listed company – where the volume was and at that stage too where the majority of the investors were. Of course if we had 20% of our shares in ADRs and there was reasonable trading in them then Sarbanes-Oxley would’ve been just another thing to manage.”

This example underscores what most firms say upon delisting – that the costs of SOX are not in

proportion to the extent of U.S. investor interest in their shares.23 This suggests that the role

regulatory costs play in affecting the firm’s decision to stay or exit the U.S. market is properly

placed within the larger context of understanding what factors contribute to viable foreign

listings.24 Also contributing to this view is an acknowledgement among some practitioners that

too many firms have ADRs. Patrick Colle, Global Business Head for the JP Morgan ADR group,

notes: “In slow times some banks do go out and pitch ADRs to three men and a shovel. There are

23 Consistent with this, a recent survey by the Bank of New York finds that only 8% of foreign firms view of the provisions of Sarbanes-Oxley as onerous enough to consider delisting (see Bank of New York, 2004). 24 A related study by Karolyi (2003) recounts the creation of global registered share (GRS) by DaimlerChrysler in November 1998. The DCX share, created following the merger of Daimler Benz and Chrysler, attempted to increase shareholder value by creating a fully fungible, seamlessly traded security that was expected to increase liquidity, and reduce volatility and cross-border trading and settlement costs. Ironically a security designed to facilitate trading across a number of markets resulted in a higher concentration of trading in one market–Frankfurt–and a drying up of liquidity in other markets.

28

too many ADR programs. There are companies that have them and don’t know why they have

one and clearly do not need one (Neville, 2004).” ADRs that result from pitches to “three men

and a shovel” are more likely to be the kind of firms that struggle to achieve benefits from listing

and in the face of increased regulatory costs these firms are more likely to delist. These firms

then are also less likely to have been viable candidates for listing.

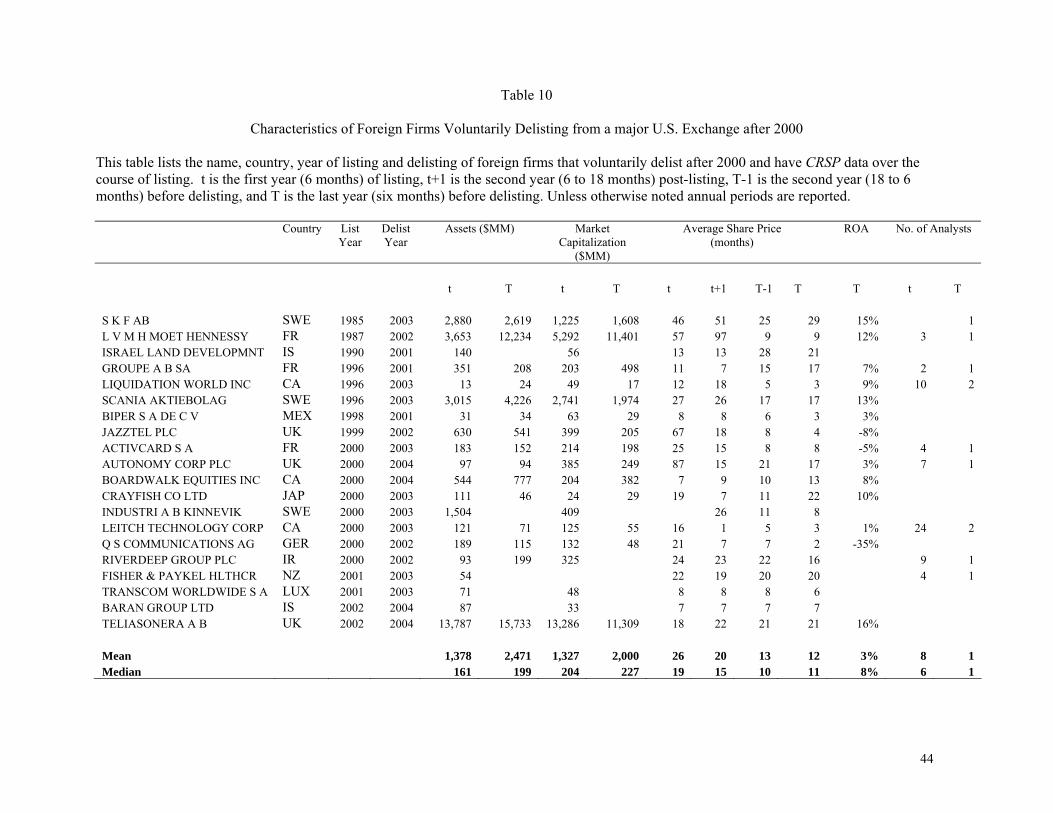

In Table 10 we examine characteristics of the 20 firms that voluntarily delisted from a

major U.S. exchange between 2001 and 2004. This sample is smaller than the 28 voluntarily

delists reported in Table 4 over the same period because we require the firms to have CRSP data

available over the course of listing. Our sample starts a year before the first reported notice of

SOX in February 2002, but in a year colored by concerns in the press about corporate excesses

and lax corporate governance (Smith, 2005). First note that the firms voluntarily delisting are

almost exclusively from developed countries. This is consistent with the view frequently

expressed by the firms that their home markets are of sufficient size to meet their needs. Twelve

of the 20 firms voluntarily delisting were also listed after 1999 (60%), indicating the rapid speed

of delisting. Firms listed after 1999 also reflect the deteriorating quality of new lists as they are

generally smaller and less profitable firms than those listed before 1999. In the year of listing

assets average $1,378 million but the average is driven by a few large firms so that the median

assets is $161 million. Likewise, the median market capitalization of the firms at listing and

delisting is less than $230 million. Eleven firms have share prices lower at delisting than at

listing (55%) and the average firm’s share price declines by 54% (median=42%) over the course

of listing. Despite our attempts to screen for evidence of distress, five firms have share prices

below $5 at delisting. Only eight of the 20 firms (40%) have analyst coverage within a year

following listing. Overall, the picture that emerges from Table 10 is that while a few voluntary

delists appear to have the size and strength to be viable candidates for listing, the majority

struggle to gain U.S. investor recognition. Absent investor recognition, it is difficult to achieve

the benefits expected from listing. Therefore, foreign firms’ decision to voluntarily delist appears

29

to involve issues of quality and investor recognition or the lack thereof. No doubt an increase in

regulatory costs can cause firms to revisit their decision to list.25 Since we do not observe large

numbers of strong firms voluntarily delisting, the evidence does not suggest that regulatory costs

alone are driving firms from the U.S. The dimension of foreign firms’ ability to attract U.S.

investor interest deserves to be a greater part of the discussion in determining the role of SOX.

5. Conclusions

Much (too much in our view) of the discussion about the overall competitiveness of the

U.S. capital markets has taken place without regard for the factors that contribute to viable

foreign listings. Firms choose to list in the U.S. if the benefits of listing exceed the costs – but to

focus only on the costs without examining the potential for firms to benefit from listing misses an

important part of the equation. Absent sufficient quality, it is difficult for firms to achieve the

benefits expected from listing. To address this issue, we examine the listings and delistings of

foreign firms from major U.S. exchanges over the period 1961 – 2004. Over this period a total of

1,330 foreign firms listed and 728 firms delisted due to merger and acquisitions, involuntary, or

voluntary reasons. The large number of listings and delistings spanning over 40 years suggests

that there is a long standing dynamic to foreign firm’s entry and exit from the U.S. The pattern of

foreign firms listing and delisting in the U.S. over this period shows a steady and persistent

decline in the length of time a foreign firm stays listed in the U.S. Firms listed before 1970 stay

listed an average of 33 years and this declines steadily over the next three decades to five years

for firms listed after 1995. A major reason for the decline is that over time, not unlike the pattern

for U.S. new lists, there has been deterioration in the quality of foreign firms listing in the U.S.

with respect to their size and profitability.