Embed Size (px)

Citation preview

From Startup to Expansion;

Preparing Your Brewery or Distillery

to Raise Capital

2 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Introduction

• Matthew McLaughlin, Baker Donelson

• Alan Lange, Grits Capital

• Keith Merklin, Live Oak Bank

3 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Introduction

• Matthew McLaughlin: Discuss five areas of focus in getting your

brewery or distillery ready to raise capital from an organizational and

legal readiness perspective

• Alan Lange: Provide insight as to what his organization looks for

from an investment perspective and issues to consider when

bringing in an equity investor

• Keith Merklin: Discuss the different types of bank and non-bank

financing that are available for breweries and distilleries

4 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Introduction

• Before we get into the substance of the content, everyone should

recognize that regardless of whether you are raising startup capital

or raising capital for an expansion project…

− Raising capital takes time

− Raising capital is a process

− Raising capital is relationship driven

“It’s almost always harder to raise capital than you thought it would

be, and it always takes longer. So plan for that.” – Richard Harroch,

Venture Capitalist and Author

5 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Team

• Going at it alone is never a good idea

• You must always start with a good team; a team is made up of many

different individuals

• At the core of the team are the brewery or distillery founders

− The hipster, the hacker, and the hustler

− Experienced management with industry success

− Contractual agreements in place that set forth the roles and

responsibilities of the founders

6 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Team

• Key Employees

− Head brewer or head distiller

− Sales team

− Contractual agreements in place that set forth the roles and

responsibilities of the key employees

• Mentors

− Other brewery or distillery founders

− Industry experts

− Demonstrate an ability to leverage the knowledge of others and

an ability to collaborate

7 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Team

• Advisors that know the industry

− Financial advisor

− CPA

− Attorney

− Demonstrate an openness to coachability

Your mentors and advisors not only add value, but also provide your

brewery or distillery credibility with investors and lenders

8 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Team

• Ultimately, your team needs to be reflective of skills and experience

in the brewing and distilling industry.

• Investors are investing in a business and lenders are lending to a

business, but both are making bets based on the teams.

9 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Capital Strategy

• Formulate a strategy around raising capital

• Understand the differences between equity and debt and know

where and when to look for both

• Be able to provide a clean, projected capital stack and a clean,

existing capital stack

− Founder equity

− Friends and family

− Outside investors

− Debt

10 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Capital Strategy

• As a startup, develop a sound business plan or as an existing

production brewery or distillery, develop a sound expansion plan

− Competitive advantage

− Value proposition

− Defensible business model

Brewpub, production brewery or distillery, plan of distribution,

sales and managing retail accounts

• But most importantly, make sure you have…

− Sound and vetted financial projections

− Reasonable and realistic valuation

11 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Capital Strategy

• Ensure that the capital you are seeking fits together with all of the

other sources of funding

− Pre-emptive rights

− Loan covenants

• You are adding another piece to a puzzle, not cramming a square

peg in a round hole

12 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

“Clean” Business Looking Back

• Investors and lenders are underwriting deals based on going

forward risk and do not want legacy risk

• Look back from the current point in time to inception and try to

identify potential risk

− Was stock issued pursuant to securities laws?

− Have you protected existing intellectual property?

− How have you handled problem employees?

− Are you complying with all federal, state, and local permits?

− Can you demonstrate TTB and state regulatory compliance,

excise tax payments, reporting, and recordkeeping?

13 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

“Clean” Business Looking Back

• Have your advisors “audit” the business to determine whether

remedial action is necessary if anything appears to create any

legacy risk

• You unequivocally do not want…

− An investor or a lender to find a problem during the diligence

period

− Or even worse, discover a problem after closing that was not

discovered or disclosed during the due diligence process

14 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

“Clean” Operating Business

• An investor or lender is going to perform a significant amount of due

diligence on your existing operations

• The starting point is almost always your company’s organizational

documents, which need to be…

− Thoughtful

− Deliberate

− Artfully drafted

− Industry specific

15 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

“Clean” Operating Business

• Do the company organizational documents address key issues?

− Management, corporate governance and voting

− Capital and subsequent contributions

− Distributions and dividends

− Tax and accounting matters

− Transfers and pledges of equity

− Intellectual property matters

− Investor representations and warranties

Tied house issues

Ownership in other breweries or distilleries

Felony convictions and other bad boy acts

16 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

“Clean” Operating Business

• Permits:

− Compliance with all federal, state and local permits

− TTB, state license(s), FDA, EPA, DEQ, local zoning and land use

• Policies:

− Industry specific employee handbook

− Effective training programs, i.e. manufacturing, handling and

serving alcoholic beverage products

17 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

“Clean” Operating Business

• Processes:

− Brand development and ideation

− Protection of intellectual property and trade secrets

− Managing distributors

− Managing retail accounts

− Dealing with troubled employees

18 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Process

• So, once you have effectively addressed all of the previous issues,

you must be prepared to manage the process:

− Confidentiality agreements and non-disclosure agreements

− Transmission of meaningful and confidential data through email

or data rooms

− Due diligence

− Term sheet

− Closing document negotiation

− Closing

− Post-closing compliance

19 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Final Thoughts

• You must be unbelievably organized

• All money is green, but it is not all the same

• If you have nothing at risk, do not expect anyone else to put

anything at risk

20 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Startup Phase: $0 to $1,000,000 in Revenue

• What investors are looking for:

− Skin in the game

− Market validation

− Can you execute?

− Is it scalable?

− Solid management team

− Sound legal and accounting foundation

− Profitability

21 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Startup Phase: $0 to $1,000,000 in Revenue

• What is the payoff?

− Be realistic

− No “dreamy” valuations

− Accurate projections

− Your key advantages

− Assigning risk

− Mature multiples 5-8x

22 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

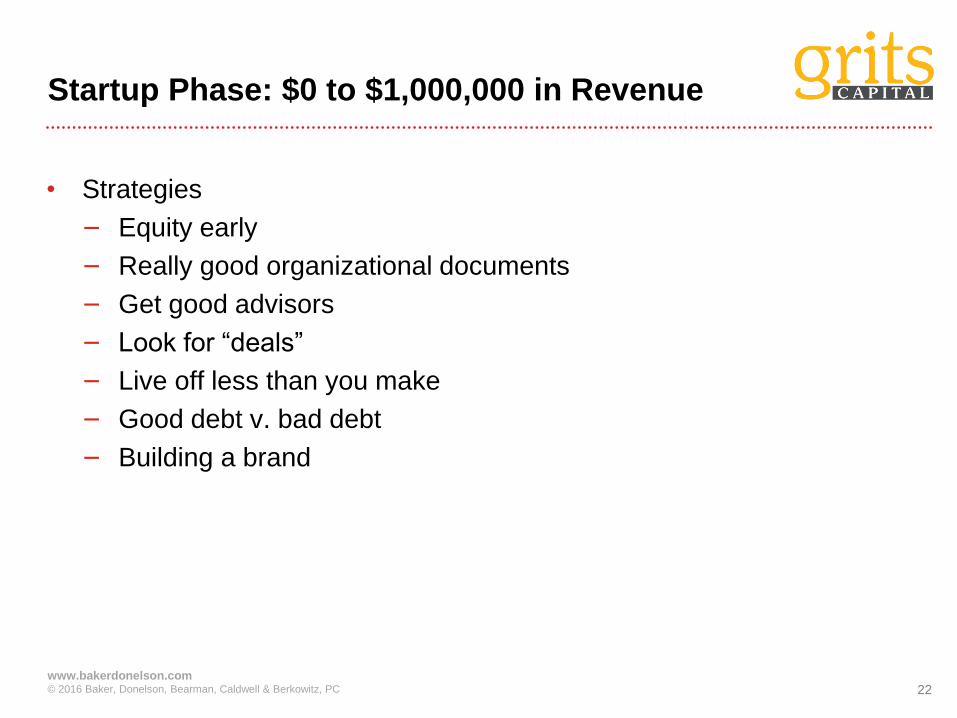

Startup Phase: $0 to $1,000,000 in Revenue

• Strategies

− Equity early

− Really good organizational documents

− Get good advisors

− Look for “deals”

− Live off less than you make

− Good debt v. bad debt

− Building a brand

23 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Ramp Phase: $1,000,000 to $5,000,000

in Revenue

• What you do well

− Track record

− Market validates you

− Organic growth

− Less revenue volatility

− Is it scalable?

− Profitability

24 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Ramp Phase: $1,000,000 to $5,000,000

in Revenue

• How do you finance it?

− Asset based debt

− Incentive financing

Local (city/county)

▫ TIF and abatements

State

▫ Grants and guarantees

Federal

▫ SBA loan and NMTCs/HTCs

− Equity

25 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Ramp Phase: $1,000,000 to $5,000,000

in Revenue

• Strategies

− Lock down key people

− Be super efficient

− Build capacity

− Stay liquid

− Solidify brand

26 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

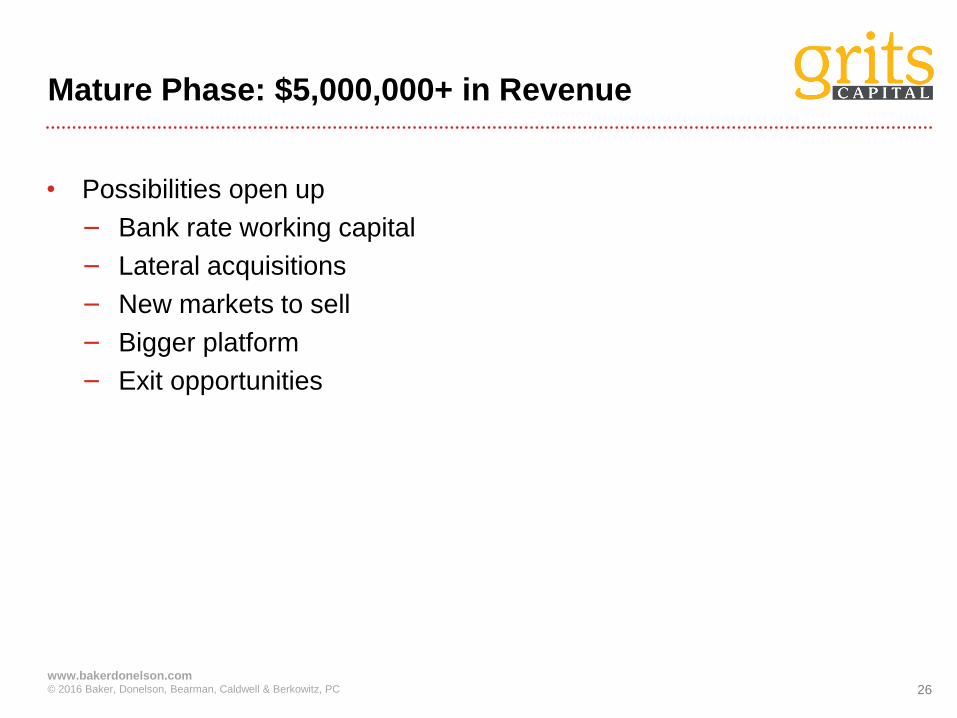

Mature Phase: $5,000,000+ in Revenue

• Possibilities open up

− Bank rate working capital

− Lateral acquisitions

− New markets to sell

− Bigger platform

− Exit opportunities

27 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Lender’s Perspective

− Bank Loans

Conventional – Traditional Bank Loan

SBA – Small Business Administration

− Non-bank loans

− Qualifying for a loan

− Business Plan

− Case Study

Expansion

Start-Up

28 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Bank Loans - Conventional Loans

• Risk to Lender – Low

−Mitigated by historic cash flow

−Mitigated by collateral

• Structure

−Down payment 20-25%

−Longer Amortizations

• Advantages

−Usually lower rates and fees

−Quick closings

• Disadvantages

−Balloons

−Down payments

−Require banking relationship

−Covenants

29 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Bank Loans – SBA Loans

• Risk to Lender – Very Low

− Mitigated by historic and projected cash flow

− Mitigated by U.S. government guarantee

• Structure

− Low to no down payments

− Longer repayment terms

• Advantages

− Up to 100% financing

− Longest terms with no calls

− No covenants

• Disadvantages

− Higher fees and closing costs

− Longer closing process

30 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Non Bank Loans

• Risk to Lender – High

− Mitigated by shorter terms

− Mitigated high rates

• Structure

− Low to no down payments

− 1 3 Year terms

• Advantages

− Up to 100% financing

− Easy Qualifications

− Quick closing

• Disadvantages

− Unregulated

− Very high rates

− Short terms

31 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Banks Credit Decisions are Governed by

the “5 C’s”

• Character − Can you run the business? Are you a borrower the bank wants to be in business

with? Banks consider the long-term relationship.

• Capacity (Cash Flow) − Expansion – Will historical cash flows support the business, the debt and pay you

a reasonable salary? − Startup – Are the projections reasonable? Do they cover the business operations

and debt and pay you a salary?

• Condition − Understand the condition of the business, the industry and the economy; why it is

important to work with a lender who understands the beverage industry.

• Capital − What personal investment do you plan to make in the business? − Injecting capital - decrease the chance of default - ‘skin in the game.’

• Collateral − Generally very important in a conventional loan; not as important with an SBA

lender.

32 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Business Plan

• Executive Summary

• Market Analysis

• Organization and Management

• Marketing and Sales Strategies

• Funding Requirements

• Financials

33 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

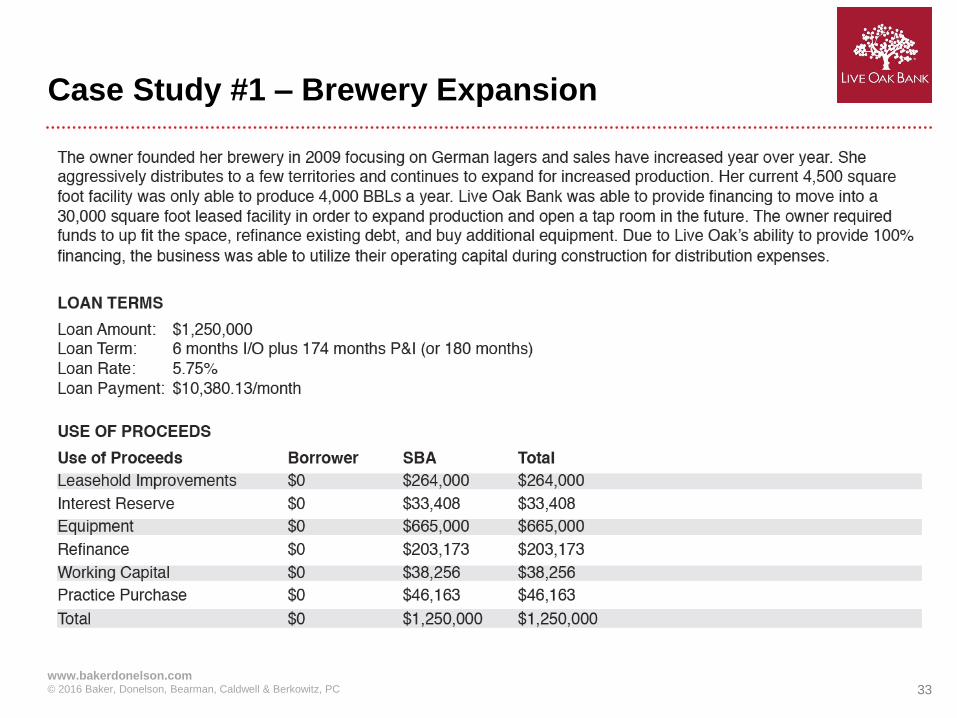

Case Study #1 – Brewery Expansion

34 www.bakerdonelson.com © 2016 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

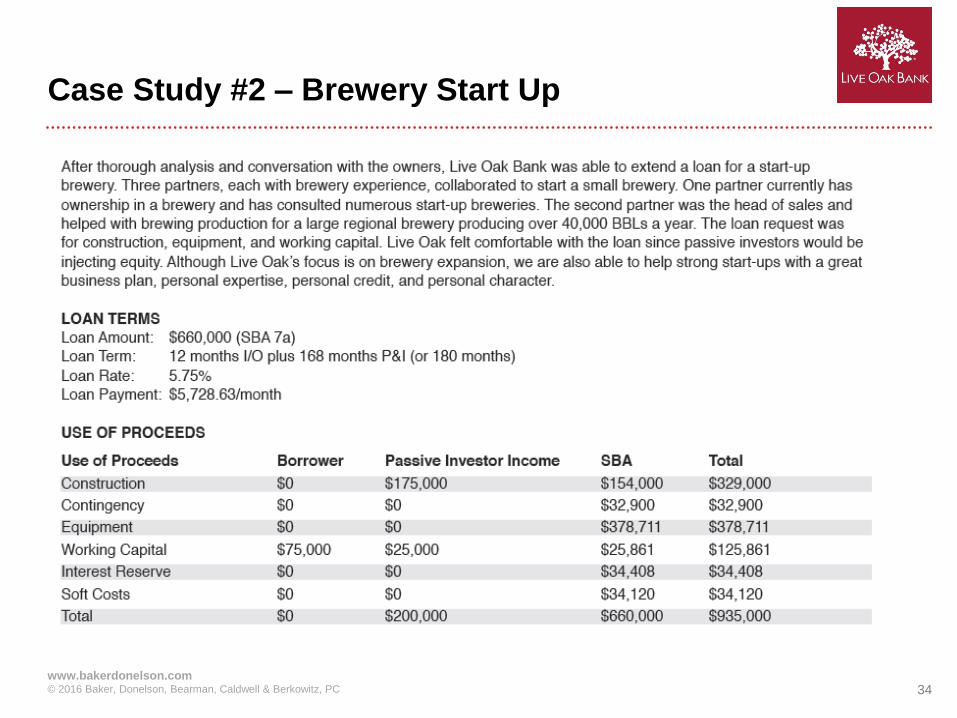

Case Study #2 – Brewery Start Up