Embed Size (px)

Citation preview

FRONTIER EFFICIENCY METHODOLOGIES TO MEASURE PER-

FORMANCE IN THE INSURANCE INDUSTRY: OVERVIEW AND NEW

EMPIRICAL EVIDENCE

Martin Eling, Michael Luhnen∗

JEL Classification: D23, G22, L11

ABSTRACT

The purpose of this paper is to provide an overview and new empirical evidence on frontier effi-

ciency measurement in the insurance industry, a topic of great interest in the academic literature

during the last several years. In the first step, we review 83 studies and put them into a joint

evaluation of efficiency measurement in the field of insurance. In the second step, an efficiency

comparison of 3,710 insurers from 37 countries is conducted using a dataset that has not yet been

subject to efficiency analysis (the AM Best Non US database). We compare different methodolo-

gies, countries, organizational forms, distribution systems, lines of business, and company sizes.

We find a steady efficiency growth in international insurance markets from 2002 to 2006 with

large differences across countries. Furthermore, we find evidence that stock companies are more

efficient than mutuals as well as for economies of scale, but no evidence for economies of scope in

the insurance industry. Only minor variations are found when comparing different frontier effi-

ciency methodologies (data envelopment analysis, stochastic frontier analysis) and different distri-

bution types (agency-based vs. direct writers). Our results give valuable insight into the competi-

tiveness of insurers in various countries.

(At the end of the paper there is an outline of further research that we would like to integrate in a

revised version of the paper to be presented at the conference on “Performance Measurement in

the Financial Services Sector.”)

1. INTRODUCTION

In recent years, efficiency measurement has captured a great deal of attention. The in-

surance sector in particular has seen rapid growth in the number of studies applying

frontier efficiency methods. Berger/Humphrey (1997) and Cummins/Weiss (2000)

surveyed eight and 21 studies, respectively; now, less than ten years after the Cum-

mins/Weiss survey, there are 83 studies on efficiency measurement in the insurance

industry. Recent work in the field has refined methodologies, addressed new topics

(e.g., market structure and risk management), and extended geographic coverage from

a previously US-focused view to a broad set of countries around the world, including

emerging markets such as China and Taiwan.

∗ Martin Eling is with the University of Wisconsin, School of Business, 4279 Grainger Hall, 975 University

Avenue, Madison, WI 53706, USA. Michael Luhnen is with the University of St. Gallen, Institute of Insurance

Economics, Kirchlistrasse 2, 9010 St. Gallen, Switzerland. We are grateful to Mareike Bodderas, Thomas Par-

nitzke, Hato Schmeiser, and Denis Toplek for valuable suggestions and comments.

2

The first aim of this paper is to survey these 83 studies. We provide a comprehensive

categorization of this rapidly growing body of literature and point out new develop-

ments. Frontier efficiency methodologies have been used to analyze many important

economic questions, such as comparison of countries (see, e.g., Fenn et al., 2008), or-

ganizational forms (see, e.g., Cummins/Weiss/Zi, 1998), and scale economies (see,

e.g., Fecher/Perelman/Pestieau, 1991). Other research questions have involved the ef-

ficiency effects of mergers and acquisitions (see, e.g., Cummins/Tennyson/Weiss,

1999) and the comparison of different frontier efficiency methodologies (see, e.g.,

Cummins/Zi, 1998). In our overview, we will review these fields of application, sum-

marize the methodologies, and highlight recent developments in the field.

Existing cross-country comparisons of efficiency in the insurance industry provide

valuable insights into the competitiveness of insurers in different countries. However,

the geographic coverage of these studies is limited to certain countries or regions.

Weiss (1991b) compares the United States, Germany, France, Switzerland, and Japan;

Donni/ Fecher (1996) analyze 15 OECD countries. Both authors were restricted to us-

ing aggregated economic information instead of individual company data. Di-

acon/Starkey/ O’Brien (2002) and Fenn et al. (2008) do use individual company data,

but concentrate on European countries (15 and 14, respectively). Rai (1996) takes a

look at nine European countries, Japan, and the United States, but considers a rela-

tively small dataset of 106 companies. What is missing is a broad comparison of effi-

ciency at the international level that incorporates a large number of countries and

companies.

The second aim of this paper is thus to contribute to the growing body of literature on

frontier efficiency at the international level by answering key research questions based

on a large number of countries and companies. We therefore consider a broad interna-

tional dataset that has not yet been the subject of efficiency study—the AM Best Non

US database. Our cross-country analysis uses data on 3,710 insurance companies from

37 countries, which gives our study—to our knowledge—the largest sample ever ana-

lyzed for the insurance industry. We consider six main aspects: (1) methodologies, (2)

countries, (3) organizational forms, (4) distribution systems, (5) lines of business, and

(6) company size. These six aspects allow us to address many of the important eco-

nomic questions set out in the first survey part of the paper. Another important contri-

bution of this paper is that we determine and compare efficiency for a large number of

countries that have not been considered, at least to our knowledge, in the literature to

date: the Bahamas, Barbados, Bermuda, Brazil, the Czech Republic, Hong Kong,

Hungary, Indonesia, Lithuania, Mexico, Norway, Poland, Russia, Singapore, and

South Africa. Thus, the main contribution of this paper is to provide a broad evaluation

3

of efficiency measurement in the insurance industry with a special emphasis on an in-

ternational comparison of efficiency.

Our main empirical findings can be summarized as follows:

(1) We find a steady efficiency growth in international insurance markets during the

sample period (2002–2006), with large efficiency differences between the 37 coun-

tries. The highest efficiency is found for Japan; the lowest for the Phillipines.

(2) We find evidence for the expense preference hypothesis (i.e., stock companies are

more efficient than mutuals) and for economies of scale (i.e., larger companies are

more efficient than smaller companies).

(3) We find only minor difference between distribution types (agency-based vs. direct

writers) and very little evidence for economies of scope (i.e., multi-line insurers are

not necessarily more efficient than mono-line insurers).

(4) We find that there is not much difference between the two frontier efficiency meth-

odologies data envelopment analysis and stochastic frontier analysis.

The remainder of the paper is organized as follows. Section 2 contains an overview of

83 studies on efficiency measurement in the insurance industry. The empirical exami-

nation is performed in Section 3. The results of the study are summarized in Section 4.

2. OVERVIEW OF EFFICIENCY MEASUREMENT IN THE INSURANCE INDUSTRY

In this section we provide an overview of 83 studies on efficiency measurement in the

insurance industry. Our overview builds upon and significantly extends two earlier

surveys of efficiency measurement in the financial services industry: one by Ber-

ger/Humphrey (1997), which focuses on banks and provides a valuable criteria frame-

work that we use to analyze the studies in the field of insurance, the second by Cum-

mins/Weiss (2000), which focuses on the insurance industry and covers 21 studies that

had been published by the year 1998.

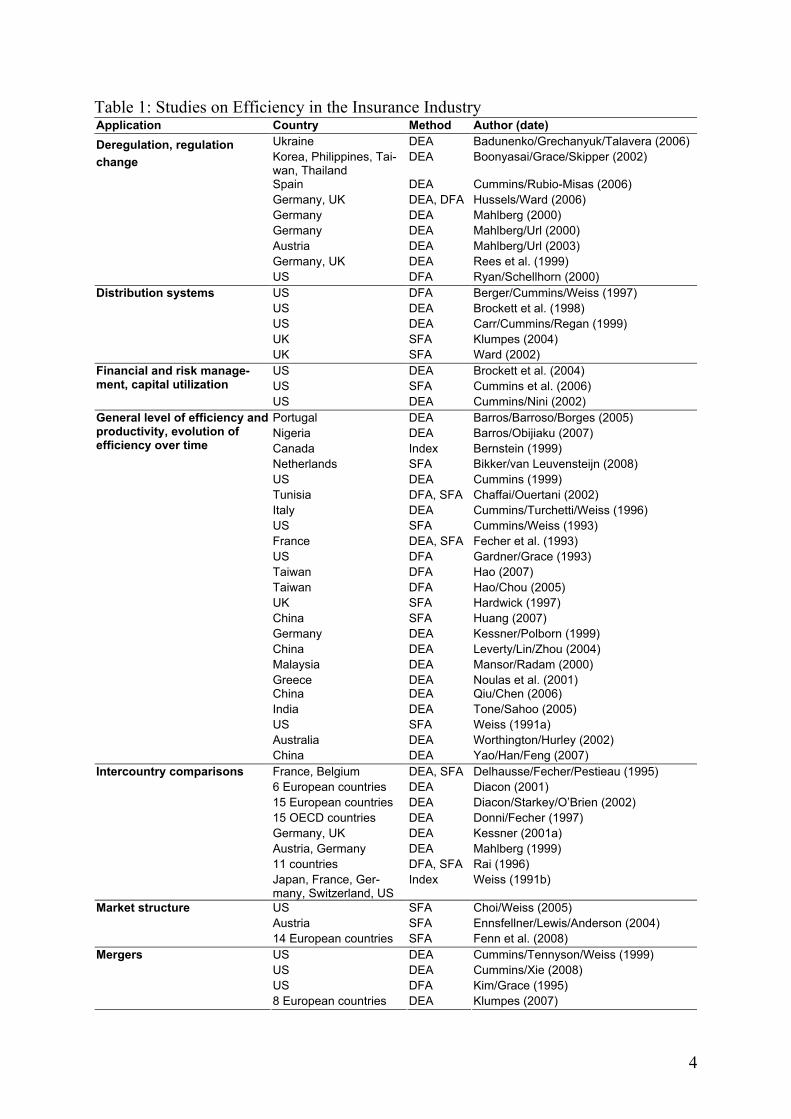

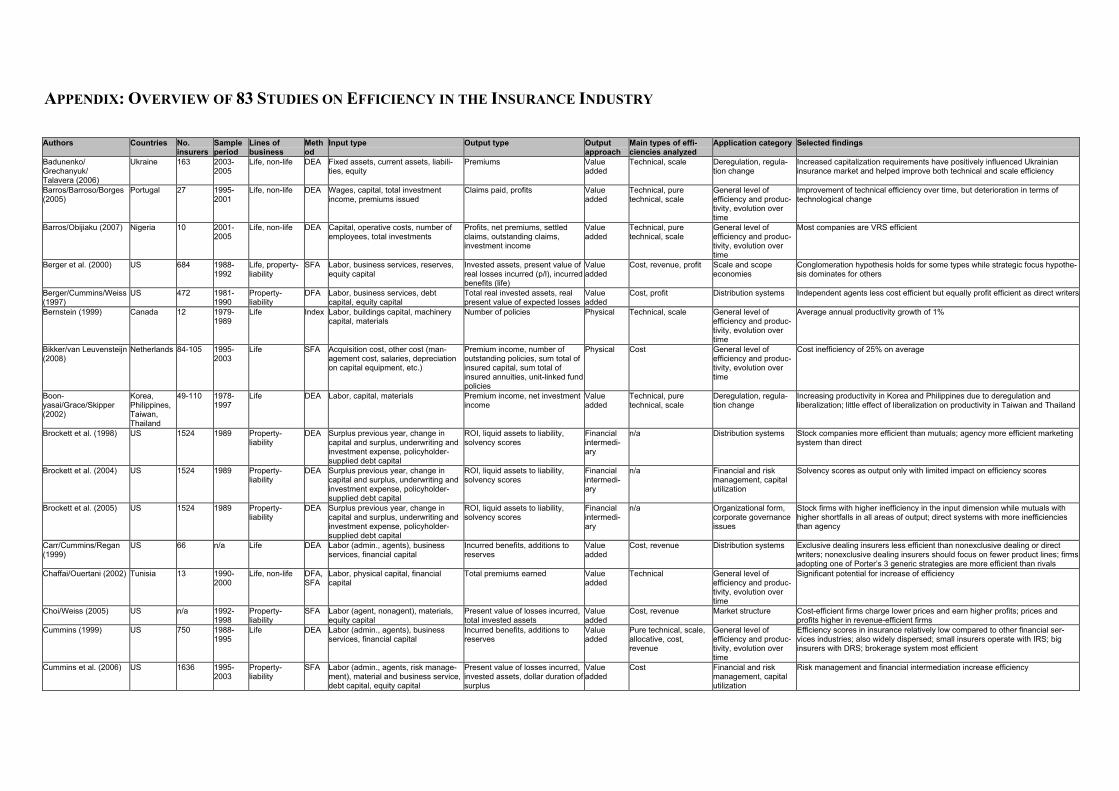

Table 1 summarizes the main features of the 83 studies. Although many of the studies

make contributions to more than one topic, in order to categorize them, we have ar-

ranged them according to their primary field of application (first column). The ten ap-

plication categories were chosen and refined based on the earlier overview by Ber-

ger/Humphrey (1997). Columns 2 and 3 show the country(ies) under investigation and

the efficient frontier method used; the fourth column lists the authors and year of pub-

lication of the study. More detailed information, such as input and output factors, types

of efficiency analyzed, sample periods, lines of business covered, and main findings,

can be found in the Appendix. In the following we discuss these studies, particularly

focusing on recent developments.

4

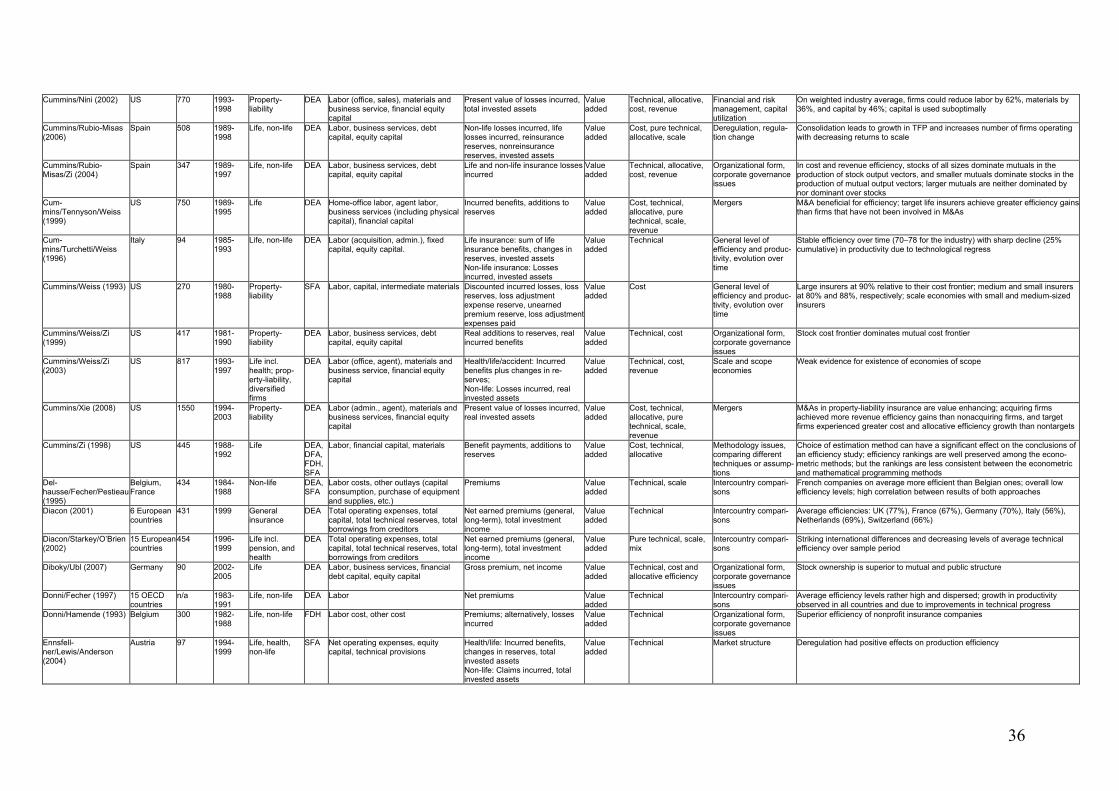

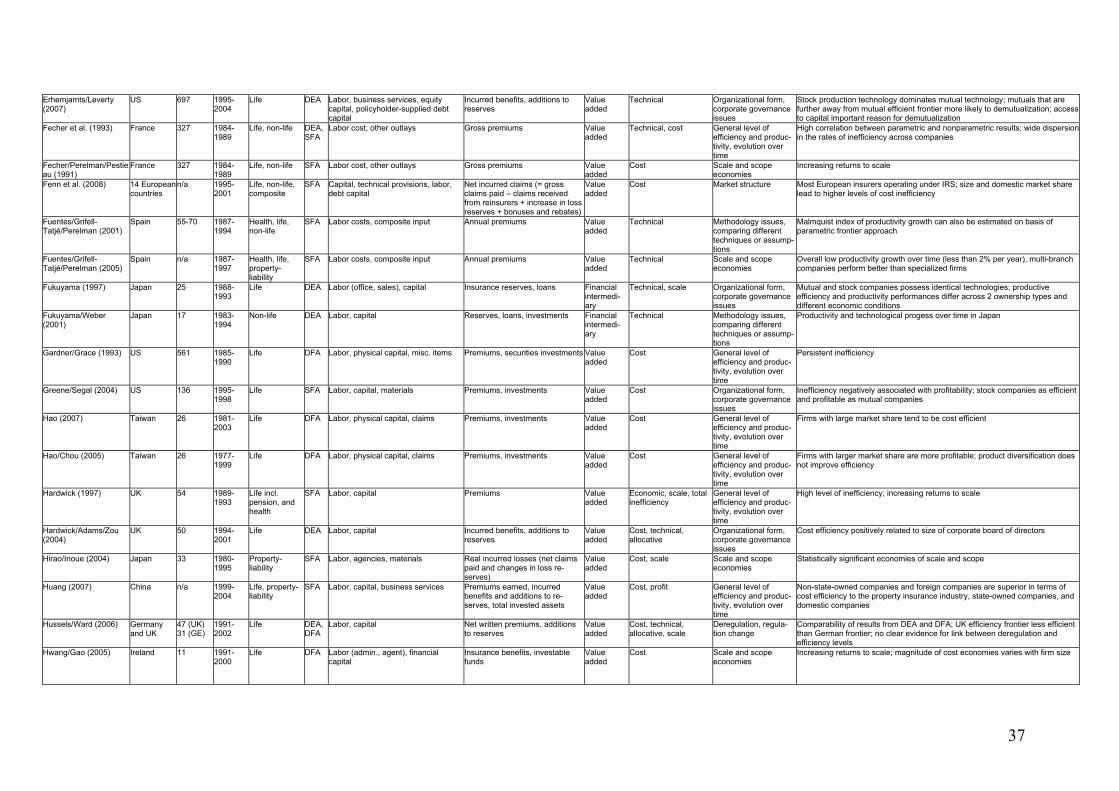

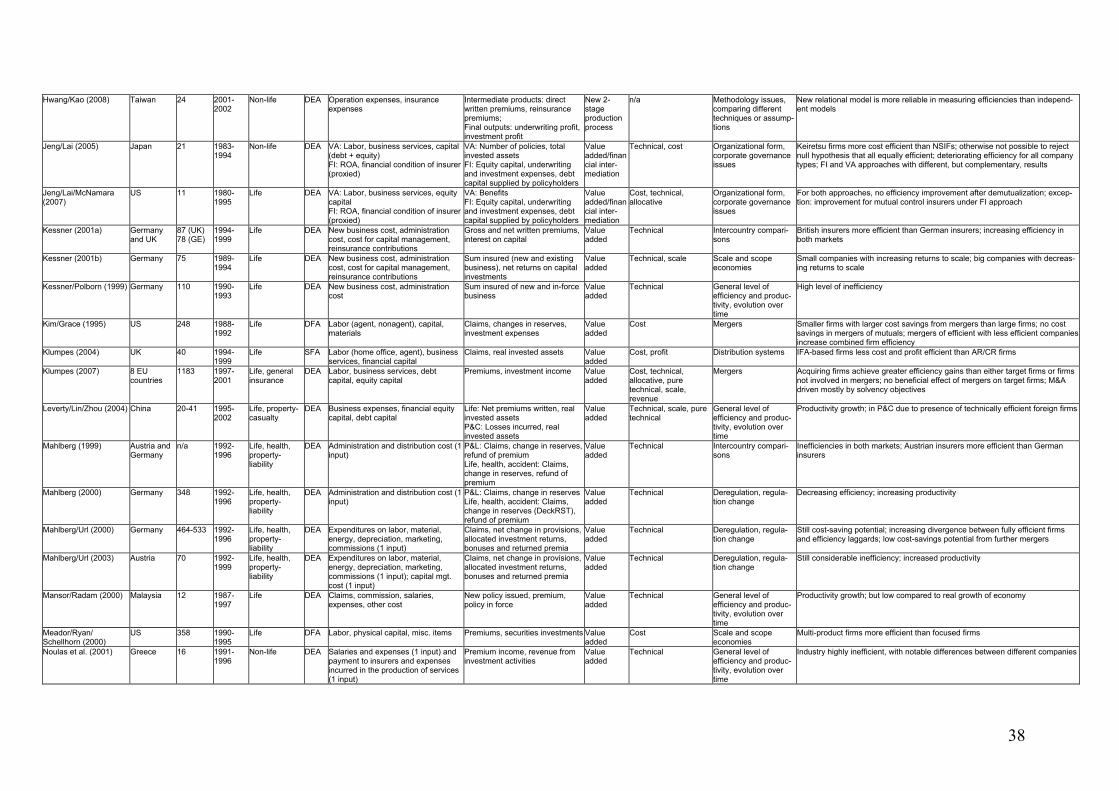

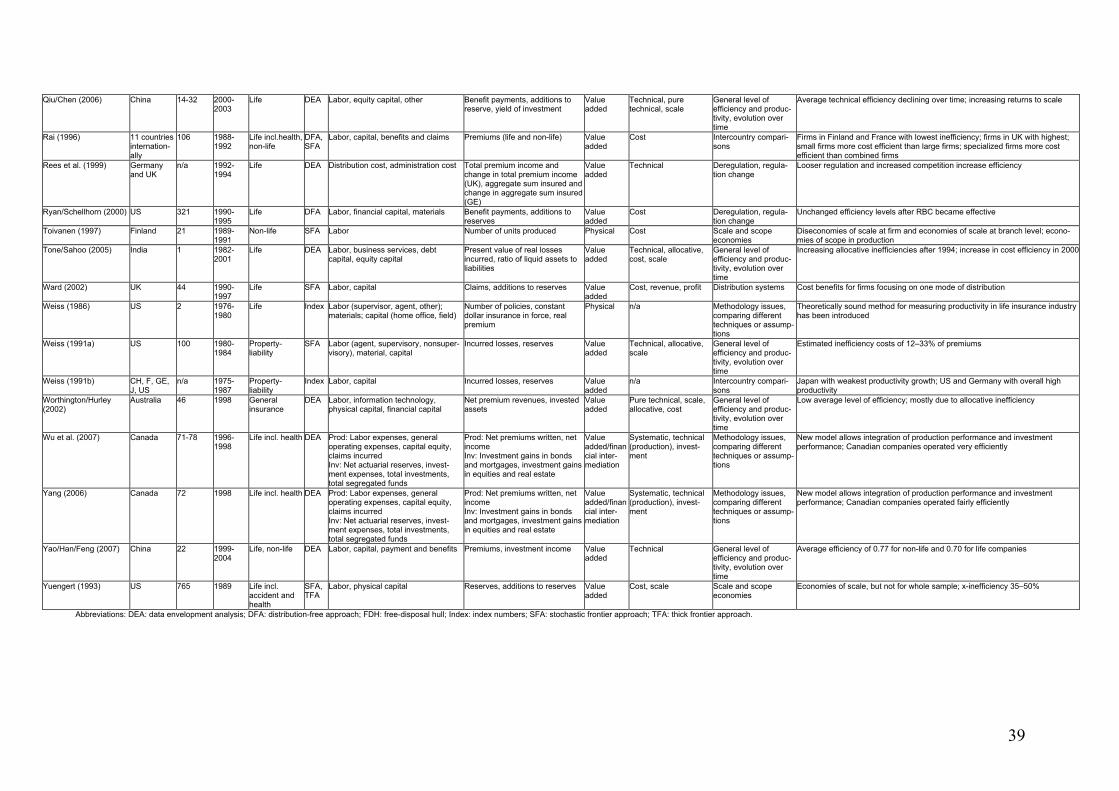

Table 1: Studies on Efficiency in the Insurance Industry Application Country Method Author (date)

Ukraine DEA Badunenko/Grechanyuk/Talavera (2006)

Korea, Philippines, Tai-wan, Thailand

DEA Boonyasai/Grace/Skipper (2002)

Spain DEA Cummins/Rubio-Misas (2006)

Germany, UK DEA, DFA Hussels/Ward (2006)

Germany DEA Mahlberg (2000)

Germany DEA Mahlberg/Url (2000)

Austria DEA Mahlberg/Url (2003)

Germany, UK DEA Rees et al. (1999)

Deregulation, regulation

change

US DFA Ryan/Schellhorn (2000)

US DFA Berger/Cummins/Weiss (1997)

US DEA Brockett et al. (1998)

US DEA Carr/Cummins/Regan (1999)

UK SFA Klumpes (2004)

Distribution systems

UK SFA Ward (2002)

US DEA Brockett et al. (2004)

US SFA Cummins et al. (2006)

Financial and risk manage-ment, capital utilization

US DEA Cummins/Nini (2002)

Portugal DEA Barros/Barroso/Borges (2005)

Nigeria DEA Barros/Obijiaku (2007)

Canada Index Bernstein (1999)

Netherlands SFA Bikker/van Leuvensteijn (2008)

US DEA Cummins (1999)

Tunisia DFA, SFA Chaffai/Ouertani (2002)

Italy DEA Cummins/Turchetti/Weiss (1996)

US SFA Cummins/Weiss (1993)

France DEA, SFA Fecher et al. (1993)

US DFA Gardner/Grace (1993)

Taiwan DFA Hao (2007)

Taiwan DFA Hao/Chou (2005)

UK SFA Hardwick (1997)

China SFA Huang (2007)

Germany DEA Kessner/Polborn (1999)

China DEA Leverty/Lin/Zhou (2004)

Malaysia DEA Mansor/Radam (2000)

Greece DEA Noulas et al. (2001) China DEA Qiu/Chen (2006)

India DEA Tone/Sahoo (2005)

US SFA Weiss (1991a)

Australia DEA Worthington/Hurley (2002)

General level of efficiency and productivity, evolution of efficiency over time

China DEA Yao/Han/Feng (2007)

France, Belgium DEA, SFA Delhausse/Fecher/Pestieau (1995)

6 European countries DEA Diacon (2001)

15 European countries DEA Diacon/Starkey/O’Brien (2002)

15 OECD countries DEA Donni/Fecher (1997)

Germany, UK DEA Kessner (2001a)

Austria, Germany DEA Mahlberg (1999)

11 countries DFA, SFA Rai (1996)

Intercountry comparisons

Japan, France, Ger-many, Switzerland, US

Index Weiss (1991b)

US SFA Choi/Weiss (2005)

Austria SFA Ennsfellner/Lewis/Anderson (2004)

Market structure

14 European countries SFA Fenn et al. (2008)

US DEA Cummins/Tennyson/Weiss (1999)

US DEA Cummins/Xie (2008)

US DFA Kim/Grace (1995)

Mergers

8 European countries DEA Klumpes (2007)

5

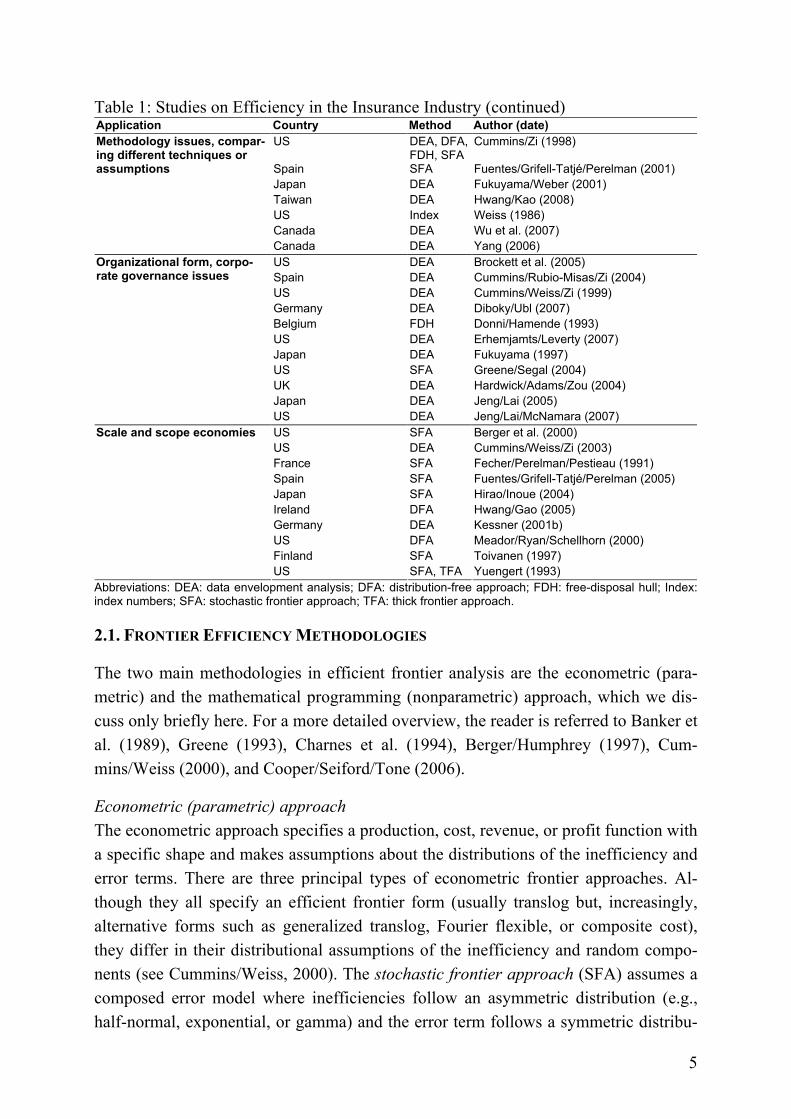

Table 1: Studies on Efficiency in the Insurance Industry (continued) Application Country Method Author (date)

US DEA, DFA, FDH, SFA

Cummins/Zi (1998)

Spain SFA Fuentes/Grifell-Tatjé/Perelman (2001)

Japan DEA Fukuyama/Weber (2001)

Taiwan DEA Hwang/Kao (2008)

US Index Weiss (1986)

Canada DEA Wu et al. (2007)

Methodology issues, compar-ing different techniques or assumptions

Canada DEA Yang (2006)

US DEA Brockett et al. (2005)

Spain DEA Cummins/Rubio-Misas/Zi (2004)

US DEA Cummins/Weiss/Zi (1999)

Germany DEA Diboky/Ubl (2007)

Belgium FDH Donni/Hamende (1993)

US DEA Erhemjamts/Leverty (2007)

Japan DEA Fukuyama (1997)

US SFA Greene/Segal (2004)

UK DEA Hardwick/Adams/Zou (2004)

Japan DEA Jeng/Lai (2005)

Organizational form, corpo-rate governance issues

US DEA Jeng/Lai/McNamara (2007)

US SFA Berger et al. (2000)

US DEA Cummins/Weiss/Zi (2003)

France SFA Fecher/Perelman/Pestieau (1991)

Spain SFA Fuentes/Grifell-Tatjé/Perelman (2005)

Japan SFA Hirao/Inoue (2004)

Ireland DFA Hwang/Gao (2005)

Germany DEA Kessner (2001b)

US DFA Meador/Ryan/Schellhorn (2000)

Finland SFA Toivanen (1997)

Scale and scope economies

US SFA, TFA Yuengert (1993)

Abbreviations: DEA: data envelopment analysis; DFA: distribution-free approach; FDH: free-disposal hull; Index: index numbers; SFA: stochastic frontier approach; TFA: thick frontier approach.

2.1. FRONTIER EFFICIENCY METHODOLOGIES

The two main methodologies in efficient frontier analysis are the econometric (para-

metric) and the mathematical programming (nonparametric) approach, which we dis-

cuss only briefly here. For a more detailed overview, the reader is referred to Banker et

al. (1989), Greene (1993), Charnes et al. (1994), Berger/Humphrey (1997), Cum-

mins/Weiss (2000), and Cooper/Seiford/Tone (2006).

Econometric (parametric) approach

The econometric approach specifies a production, cost, revenue, or profit function with

a specific shape and makes assumptions about the distributions of the inefficiency and

error terms. There are three principal types of econometric frontier approaches. Al-

though they all specify an efficient frontier form (usually translog but, increasingly,

alternative forms such as generalized translog, Fourier flexible, or composite cost),

they differ in their distributional assumptions of the inefficiency and random compo-

nents (see Cummins/Weiss, 2000). The stochastic frontier approach (SFA) assumes a

composed error model where inefficiencies follow an asymmetric distribution (e.g.,

half-normal, exponential, or gamma) and the error term follows a symmetric distribu-

6

tion, usually normal. The distribution-free approach (DFA) makes fewer specific as-

sumptions, but requires several years of data; efficiency of each company is assumed

to be stable over time, and the random noise averages out to zero. Finally, the thick

frontier approach (TFA) does not make any distributional assumptions for the random

error and inefficiency terms, but assumes that inefficiencies differ between the highest

and lowest quartile firms (see Berger/Humphrey, 1997).

Mathematical programming (nonparametric) approach

Compared with the econometric approach, the mathematical programming approach

puts significantly less structure on the specification of the efficient frontier and does

not decompose the inefficiency and error terms. The most widespread mathematical

programming approach is data envelopment analysis (DEA), which uses linear pro-

gramming to measure the relationship of produced goods and services (outputs) to as-

signed resources (inputs). As an optimization result, DEA determines an efficiency

score, which can be interpreted as a performance measure. DEA was introduced by

Charnes/Cooper/Rhodes (1978) and builds on the method suggested by Farell (1957)

for computation of technical efficiency. DEA models can be specified under the as-

sumption of constant (CRS) or variable returns to scale (VRS) and can be used to de-

compose cost efficiency into its single components—technical, pure technical, alloca-

tive, and scale efficiency (see Cummins/Weiss, 2000). The free-disposal hull (FDH)

approach is a special configuration of DEA. Under this approach, the points on the

lines connecting the DEA vertices are excluded from the frontier and the convexity

assumption on the efficient frontier is relaxed (see Berger/Humphrey, 1997).

Although it is not the focus of our overview, we will briefly mention total factor pro-

ductivity, since many of the reviewed studies calculate this measure. The Malmquist

productivity index is the most common measure of total factor productivity. It is effi-

cient-frontier based (mostly DEA) and able to split total factor productivity growth

into a technical efficiency and a technological change component (see Grosskopf,

1993). Another approach to total factor productivity measurement is the calculation of

index numbers (IN), which are, however, not frontier based, and have to do with the

difference between input and output growth (see Cummins/Weiss, 2000).

Both these approaches—econometric and mathematical programming—have their

supporters and there is no consensus in the field as to which method is superior (see,

e.g., Cummins/Zi, 1998; Hussels/Ward, 2006), most likely because both approaches

have their advantages and disadvantages. While the econometric approach uses strong

assumptions regarding the form of the efficient frontier, and therefore implies a certain

economic behavior, the mathematical programming approach has the advantage of

assuming less structure for the frontier; however, it does not take into account a ran-

7

dom error and therefore runs the risk of mistaking a true random error for inefficiency

(see Berger/Humphrey, 1997).

Looking at the overview of methods used in frontier efficiency studies as set out in

Table 1, it becomes obvious that the nonparametric DEA approach has been most fre-

quently used: out of the 83 surveyed studies, 46 use DEA, 18 SFA, eight DFA, one

FDH, and three use index numbers. Additionally, total factor productivity using the

Malmquist productivity index has been calculated by 22 studies. For DEA, the most

widely used specification has been under the assumption of VRS. Only seven studies

follow the advice given by Cummins/Zi (1998) to consider multiple approaches, ide-

ally from both the econometric and mathematical programming sides. However, most

of those seven studies find highly correlated results across different approaches (see,

e.g., Hussels/Ward, 2006; Fecher et al., 1993; Delhausse/Fecher/Pestieau, 1995). Of-

ten, the choice of methods is determined by the available data, e.g., if the available

data are known to be noisy, the econometric approach, featuring an error term, may

lead to more accurate results than the mathematical programming approach (see Cum-

mins/Weiss, 2000).

In recent years, there have been a number of proposals for the improvement of effi-

cient frontier methodology in the insurance field. For the econometric approach, a ma-

jor direction has been to find more flexible specifications of the functional form, such

as the Fourier flexible distribution. This form approximates the real underlying distri-

bution more closely than do other forms, such as the translog, and thus addresses the

main drawback of the econometric approach (see, e.g., Berger/Cummins/Weiss, 1997;

Fenn et al., 2008; Klumpes, 2004), which is the possible misspecification of the shape

of the efficient frontier due to strong distributional assumptions. A further proposal has

been made regarding the incorporation of firm-specific variables into the estimation

process. Instead of using a two-stage approach, which first estimates inefficiency of

sample firms and then examines the association of inefficiency with firm-specific vari-

ables (such as organizational form), a one-stage approach is suggested. The estimated

frontier directly takes into account firm-specific variables and allows a joint modeling

of inefficiency effects (see, e.g., Greene/Segal, 2004; Fenn et al., 2008). Another con-

tribution has been made with regard to the Malmquist index of total factor productiv-

ity. Although this index is usually applied to nonparametric DEA for insurance com-

panies, Fuentes/Grifell-Tatjé/Perelman (2001) develop a parametric distance function

approach for the Malmquist productivity index calculation.

The mathematical programming approach has traditionally been viewed as a strictly

nonparametric approach; however, it has been shown that DEA can be interpreted as a

maximum likelihood estimator, providing a statistical base to DEA (see, e.g., Banker,

8

1993). Nevertheless, efficiency estimates are biased upward in finite examples and

therefore need to be corrected. That is why the bootstrapping procedure proposed by

Simar/Wilson (1998) has been applied to and extended for the insurance industry to

account for various kinds of efficiency (cost, technical, revenue) as well as CRS and

VRS models (see, e.g., Cummins/Weiss/Zi, 2003; Erhemjamts/Leverty, 2007;

Diboky/Ubl, 2007). A further innovation is the introduction of cross-frontier efficiency

analysis, which estimates efficiency of one particular technology relative to a best

practice frontier of an alternative technology (see Cummins/Weiss/Zi, 1999, 2003;

Cummins/Rubio-Misas/Zi, 2004). Cross-frontier analysis has been mainly used to ex-

amine the efficiency of different organizational forms. Finally, Brocket et al. (2004,

2005) apply a RAM (range-adjusted measure) version of DEA to the insurance indus-

try, addressing theoretical problems regarding the comparison set of each firm for

which efficiency has been calculated.

2.2. INPUT AND OUTPUT FACTORS USED IN EFFICIENCY MEASUREMENT

An important decision when employing frontier efficiency models involves the choice

of inputs, outputs, and their prices, since the definition of these factors can signifi-

cantly impact the results of a study (see Cummins/Weiss, 2000).

Choice of input factors

There are three main insurance inputs: labor, business service and materials, and capi-

tal. Labor can be further divided into agent and home-office labor. The category of

business service and materials is usually not further subdivided, but includes items like

travel, communications, and advertising. At least three categories of capital can be dis-

tinguished: physical, debt, and equity (see Cummins/Tennyson/Weiss, 1999; Cum-

mins/Weiss, 2000). Since data on the number of employees or hours worked are not

publicly available for the insurance industry, to proxy labor and business service input,

input quantities are derived by dividing the expenditures for these inputs by publicly

available wage variables or price indices, e.g., the US Department of Labor data on

average weekly wages for SIC Class 6311 (home-office life insurance labor), in the

case of a US study (see Berger/Cummins/Weiss, 1997; Cummins/Zi, 1998). Physical

capital is often included in the business service and materials category, but debt and

equity capital are important inputs for which adequate cost measures have to be found

(see Cummins/Weiss, 2000). One example of how to derive equity cost is the three-tier

approach to measuring cost of equity capital based on AM Best ratings (see Cum-

mins/Tennyson/Weiss, 1999).

There appears to be widespread agreement among researchers with regard to the

choice of inputs (see Appendix): 55 out of 83 studies use at least labor and capital as

inputs and most of them also add a third category (miscellaneous, mostly business ser-

9

vices). Out of those 55 studies, 15 differentiate between agent and nonagent labor.

Also, the number of studies differentiating between equity and debt capital is quite

low; only ten papers do so. Looking at the remaining 28 contributions that do not fol-

low the standard input categories, it becomes obvious that 15 of them incorporate

broader expenditure categories as inputs (e.g., total operating expenses) without de-

composing them into quantities and prices (see, e.g., Rees et al., 1999; Mahlberg/Url,

2003). There are a further nine studies that do not cover capital explicitly, i.e., they

consider labor only or labor and an additional composite category. Finally, four studies

that focus on financial intermediation consider only capital-related inputs (see, e.g.,

Brocket et al., 1998). The choice of input prices is mainly determined by the data that

are publicly available in the countries under investigation.

Choice of output factors

There are three principal approaches to measuring outputs in the financial services in-

dustry: the asset or intermediation approach, the user-cost approach, and the value-

added approach (see Berger/Humphrey, 1992). The intermediation approach views the

insurance company as a financial intermediary that manages a reservoir of assets, bor-

rowing funds from policyholders, investing them on capital markets, and paying out

claims, taxes, and other costs (see Brocket et al., 1998). The user-cost method differen-

tiates between inputs and outputs based on the net contribution to revenues: if a finan-

cial product yields a return that exceeds the opportunity cost of funds or if the financial

costs of a liability are less than the opportunity costs, it is deemed a financial input;

otherwise, it is considered a financial output (see Hancock, 1985; Cummins/Weiss,

2000). The value-added approach counts outputs as important if they contribute a sig-

nificant added value based on operating cost allocations (see Berger et al., 2000). Usu-

ally, several types of outputs are defined, representing the single lines of business un-

der review. In line with the theoretical literature on insurance pricing, the price of in-

surance outputs is calculated as the sum of premiums and investment income minus

output divided by output (see Cummins/Weiss, 2000).

The value-added approach to output measurement is clearly dominant in the insurance

industry: 69 out of 83 studies apply this approach (see Appendix). However, there is

an intense debate among those using the value-added approach as to whether

claims/benefits or premiums are the most appropriate proxy for value added (see, e.g.,

Cummins/Weiss, 2000). Out of the 69 articles, 32 specify output as either

claims/present value of claims (property-liability) or benefits/net incurred benefits

(life), following the arguments of Cummins/Weiss (2000). However, 35 studies spec-

ify output as premiums/sum insured, most likely because these measures are more

readily available for most countries. Two of the 69 studies applying the value-added

approach use neither of the two main proxies (e.g., Yuengert (1993) uses re-

10

serves/additions to reserves to proxy value added). There is no recognizable trend over

time as to whether either of the two main proxies is gaining more of a following

among researchers. Regarding the other two approaches for output measurement, five

studies employ the intermediation approach, e.g., taking ROI, liquid assets to liability,

and solvency scores as outputs (see Brockett et al., 2004, 2005). As argued by Cum-

mins/Weiss (2000), this approach is not optimal because insurers provide many ser-

vices in addition to financial intermediation. None of the studies reviewed uses the

user-cost approach, because this approach requires precise data on product revenues

and opportunity costs, which are not available in the insurance industry (see Klumpes,

2007). Four studies use both the value-added and intermediation approaches (see, e.g.,

Jeng/Lai, 2005). One study proposes a new relational two-stage approach to output

measurement (see Hwang/Kao, 2008): the authors construct a series relationship be-

tween the first output process (premium acquisition), providing the inputs for the sec-

ond output process (profit generation). Four studies apply physical outputs, e.g., Weiss

(1986) and Bernstein (1999) use number of policies as insurance output.

2.3. FIELDS OF APPLICATION IN INSURANCE EFFICIENCY MEASUREMENT AND SE-

LECTED RESULTS

Frontier efficiency methods have been applied to a wide range of countries (33 coun-

tries according to our survey) as well as to all major lines of business. Furthermore,

frontier efficiency methods have been used to investigate various economic issues,

including risk management (see, e.g., Cummins et al., 2006), market structure (see,

e.g., Choi/Weiss, 2005), organizational forms (see, e.g., Jeng/Lai, 2005), and mergers

(see, e.g., Cummins/Xie, 2008). However, it should be noted that findings regarding

the same economic issues often vary depending on country, line of business, time ho-

rizon, and method considered in the different studies. In the following, we analyze the

83 studies of our survey according to their field of application and selected main re-

sults. For this purpose, we consider ten application categories (see Table 1).

Deregulation and regulation change

There has been significant market deregulation of financial services in many countries

(e.g., European Union Third Generation Insurance Directive, 1994). The aim of de-

regulation in the financial services sector is to improve market efficiency and enhance

consumer choice through more competition. Consolidation, in particular, has the po-

tential to improve efficiency by efficient firms taking over less efficient ones and real-

izing economies of scale (see Cummins/Rubio-Misas, 2006). However, the evidence

on efficiency gains due to deregulation have been mixed. Rees et al. (1999) find mod-

est efficiency gains from deregulation for the United Kingdom and Germany for the

period from 1992–1994; however, Hussels/Ward (2006) do not find clear evidence for

11

a link between deregulation and efficiency for the same countries during the period

1991–2002. Mahlberg (2000) finds decreasing efficiency for Germany for the period

of 1992–1996, but an increase in productivity. For Spain, Cummins/Rubio-Misas

(2006) find clear evidence for total factor productivity growth for the period of 1989–

1998, with consolidation reducing the number of firms in the market. Boonyasai/

Grace/Skipper (2002) find evidence for productivity increases in Korea and the Philip-

pines due to deregulation. On the issue of changing regulation in the United States,

Ryan/Schellhorn (2000) find unchanged efficiency levels from the start of the 1990s to

the middle of that decade, a period during which risk-based capital requirements

(RBC) became effective.

Distribution systems

The effect of different distribution systems on the efficiency of insurance companies

has been another field of investigation but in this case the results have been more con-

sistent. Brockett et al. (1998, 2004), studying the United States, and Klumpes (2004),

studying the United Kingdom, both find that independent agent distribution systems

are more efficient than direct systems involving company representatives or employed

agents. However, Berger/Cummins/Weiss (1997) find in their study of the United

States that agent systems are less cost efficient, but equally profit efficient, as direct

systems due to differences in service intensity that are offset by higher revenues. On a

more general level, Ward (2002), in his study of the United Kingdom, finds that insur-

ers focusing on one distribution system are more efficient than those employing more

than one mode of distribution.

Financial and risk management, capital utilization

A relatively new field of application for frontier efficiency methods is that of financial

and risk management. Cummins et al. (2006) were the first to explicitly investigate the

relationship between risk management, financial intermediation, and economic effi-

ciency of insurance companies. In their application to the US property-liability indus-

try, they find that both activities significantly increase efficiency. In a similar vein,

Brockett et al. (2004) find that solvency scores used as an output have only limited

impact on efficiency scores and Cummins/Nini (2002) state that capital is used subop-

timally in US property-liability insurance.

General level of efficiency and productivity, evolution of efficiency over time

This category is comprised of all those studies whose primary research objective is to

show a country’s levels of efficiency and productivity and, in most cases, also to in-

vestigate the evolution of those measures over time. Many of these studies also look at

other issues, such as scale or scope economies. Naturally, this category contains a

large number of studies that represent a first application of efficiency frontier methods

12

to countries such as Nigeria (see Barros/Obijiaku, 2007), Tunisia (see Chaffai/

Ouertani, 2002), Malaysia (see Mansor/Radam, 2000), or Australia (see Worthington/

Hurley, 2002). Given the broad range of countries and time horizons employed, find-

ings regarding efficiency and productivity are obviously mixed; however, nearly all

studies note that there are significant levels of inefficiency in most countries with cor-

responding room for improvement, e.g., the Netherlands with 75% cost efficiency on

average (see Bikker/van Leuvensteijn, 2008), average efficiency of 77% (non-life) and

70% (life) in China (see Yao/Han/Feng, 2007), and average efficiency of 65% for

Greece (see Noulas et al., 2001).

Intercountry comparisons

Cross-country comparisons in the insurance industry can provide valuable insight into

the competitiveness and efficiencies of insurers in different countries. This sort of

study is especially interesting for the European market, where implementation of the

single European Union (EU) insurance license in 1994 raised concerns about interna-

tional competitiveness among insurers (see Diacon/Starkey/O’Brien, 2002). Conse-

quently, there have been quite a few efficiency studies on this topic. For a sample of

450 companies from 15 European countries and for the period 1996–1999, Diacon/

Starkey/O’Brien (2002) find striking international differences in average efficiency.

According to their study, the United Kingdom, Spain, Sweden, and Denmark have the

highest levels of technical efficiency. Additionally, in a recent study involving 14

European countries for the period 1995–2001, Fenn et al. (2008) find increasing re-

turns to scale for the majority of EU insurance companies, indicating that mergers and

acquisitions, facilitated by the liberalized EU market, have led to efficiency gains.

There are also cross-country efficiency studies looking at international country sam-

ples, e.g., Weiss (1991b), covering the United States, Germany, Switzerland, France,

and Japan; Donni/Fecher (1997), comparing 15 OECD countries; and Rai (1996), ana-

lyzing 11 countries.

Market structure

Several contributions to the efficient frontier literature study the effects of deregulation

and consolidation in general (see above), but only very few explicitly analyze the rela-

tionship between market structure and performance. In a recent contribution looking at

the US property-liability market, Choi/Weiss (2005) introduce the efficiency measure

into market structure analysis. They formalize the efficient structure hypothesis, which

claims that more efficient firms charge lower prices than their competitors, allowing

them to capture larger market shares as well as economic rents, leading to increased

market concentration, and incorporate x-efficiency and scale-efficiency into their

analysis. Results suggest that regulators should be more concerned with efficiency

rather than market power arising from industry consolidation. Further contributions to

13

the topic of market structure, but with a focus on the EU, have been made by Fenn et

al. (2008) and Ennsfellner/Lewis/ Anderson (2004).

Mergers

Another relatively new field for the application of frontier efficiency methods is that of

mergers and acquisitions. The few studies that have been done aim at understanding

the motivations of merger activity from the angle of efficiency gains. An early study

by Kim/Grace (1995) simulating efficiency gains from hypothetical horizontal mergers

in the US life insurance industry indicates that most mergers would improve cost effi-

ciencies, with the exception of mergers between large firms. Two other studies looking

at the US market are Cummins/Tennyson/Weiss (1999) for life insurance and Cum-

mins/Xie (2008) for property-liability insurance. Both studies conclude that mergers

are beneficial for efficiency, for both the acquiring and the target firm. Also, finan-

cially vulnerable firms are found more likely to be acquired. In his application to the

European insurance market, Klumpes (2007) tests the same hypothesis as did Cum-

mins/Tennyson/Weiss (1999) and Cummins/Xie (2008) and finds that acquiring firms

are more likely to be efficient than nonacquiring firms. However, he finds no strong

evidence that target firms achieve greater efficiency gains than nontarget firms. He

also implies that merger activity in the major European insurance markets seems to be

mainly driven by solvency objectives (i.e., financially weak insurers are bought by

financially sound companies) and less by value maximization, as found in the US.

Methodology issues, comparing different techniques or assumptions

There are a few studies whose primary objective is to solve methodological issues or

compare different techniques or assumptions over time. Among the most important of

these are Cummins/Zi (1998), comparing different frontier efficiency methods (DEA,

DFA, FDH, SFA), and Fuentes/Grifell-Tatjé/Perelman (2001), introducing a paramet-

ric frontier approach for the application of the Malmquist index. For a discussion of

these and other studies having methodological issues as their primary or secondary

research objective, the reader is referred to Section 2.1 of this paper, covering different

efficiency frontier techniques, and Section 2.2, covering different ways of treating in-

puts and outputs.

Organizational form, corporate governance issues

A very important and well-developed field of frontier efficiency analysis deals with

the effect of organizational form on performance. The two principal hypotheses in this

area are the expense preference hypothesis (see Mester, 1991) and the managerial dis-

cretion hypotheses (see Mayers/Smith, 1988). While the expense preference hypothe-

sis states that mutual insurers are less efficient than stock companies due to higher

perquisite consumption of mutual managers, the managerial discretion hypotheses pos-

14

its that the two organizational forms use different technologies and that mutual com-

panies are more efficient in lines of business with relatively low managerial discretion

(see Cummins/Weiss, 2000). Frontier efficiency studies have confirmed these hy-

potheses with the general finding that stock companies are more efficient than mutual

companies in most cases (see, e.g., Cummins/Weiss/Zi (1999) and Erhem-

jamts/Leverty (2007) for the United States and Diboky/Ubl (2007) for Germany).

However, in some areas, mutuals have been found to be more efficient. For example,

in the study by Cummins/Rubio-Misas/Zi (2004) for Spain smaller mutuals dominate

stock companies in the production of mutual output vectors. In another study covering

Japan, Fukuyama (1997) rejects the managerial discretion hypothesis, finding that mu-

tual and stock companies possess identical technologies. Other studies investigate effi-

ciency improvements after demutualization (see, e.g., Jeng/Lai/McNamara, 2007) and,

looking at corporate governance issues, the relation between cost efficiency and the

size of the corporate board of directors (see Hardwick/Adams/Zou, 2004).

Scale and scope economies

Scale and scope economies are classic areas of research in frontier efficiency litera-

ture. So far, scale economies has been the more extensively researched of the two and

is particularly important in the context of consolidation and the justification of mergers

(see Cummins/Weiss, 2000). Although detailed results vary across studies, depending

on countries, methods, and time horizons employed, many contributions have found,

on average, evidence for increasing returns to scale, meaning that unit costs of produc-

tion decline as firm size increases (see, e.g., Hardwick (1997) for UK, Hwang/Gao

(2005) for Ireland, Qiu/Chen (2006) for China, and Fecher/Perelman/Pestieau (1991)

for France). However, the differentiation between size clusters must be considered to

achieve more specific results. For example, Yuengert (1993), in his application to the

US life insurance market, finds increasing returns to scale for firms with up to US$15

billion in assets and constant returns to scale for bigger firms. In contrast, Cummins/Zi

(1998), for the same market, find increasing returns to scale for firms having up to

US$1 billion in assets, and decreasing returns to scale for all others except for a few

firms with constant returns to scale. The topic of scope economies is also of impor-

tance, since there is an increasing number of cross-industry mergers involving insurers

from different lines of business (see Cummins/Weiss, 2000). In general, researchers

have found evidence for the existence of economies of scope, meaning that multi-

product/-branch firms are more efficient than specialized firms (see, e.g., Meador/

Ryan/Schellhorn, 2000; Cummins/Weiss/Zi, 2003; Fuentes/Grifell-Tatjé/Perelman,

2005). Again, however, looking at the study results in more detail is revealing. For

example, in Berger et al. (2000), a US application, it is shown that profit scope

economies are more likely to be realized by larger firms.

15

3. NEW EMPIRICAL EVIDENCE

As mentioned above, the geographic coverage of efficiency studies in the insurance

industry has to date been limited to certain countries or regions. The contribution of

this section is to give new insights into efficiency at the international level by analyz-

ing a large number of countries and insurance companies. We compare different (1)

methodologies, (2) countries, (3) organizational forms, (4) distribution systems, (5)

lines of business, and (6) company sizes, which allows us to address many of the re-

search questions surveyed in Section 2. In each case, the results are presented at differ-

ent levels of aggregation, which enables us to identify the pure effect of methodolo-

gies, countries, organization, distribution, lines of business, and size on efficiency.

Additional cross-sectional insights including a Tobit regression analysis are provided

at the end of this section. In our analysis, we determine and compare efficiency for 15

countries that have not been considered in the literature to date: the Bahamas, Barba-

dos, Bermuda, Brazil, the Czech Republic, Hong Kong, Hungary, Indonesia, Lithua-

nia, Mexico, Norway, Poland, Russia, Singapore, and South Africa.

3.1. DATA AND METHODOLOGY

Our main data source is the 2007 edition of the AM Best Non US database (Version

2007.3). It contains information on 5,031 life and non-life insurance companies from

98 countries. The database has five years of data, covering the period 2002–2006.

Companies were included in our analysis if they had positive values for all the inputs

and outputs described in Table 2. This reduces our sample to 4,103 companies from 90

countries. Furthermore, in order to appropriately compare the different countries we

require each country to have at least a total of 30 firm years and to have data for each

of the five years that we analyze. This reduces our sample to 3,710 companies from 37

countries. The remaining 393 companies from 53 countries were included in the analy-

sis as “other” countries.1/2

1 These countries are : Antigua and Barbuda (1 company/3 firm years), Argentina (4/15), Bahrain (4/18), Bo-

livia (14/37), British Virgin Islands (3/8), Bulgaria (5/14), Cayman Islands (14/57), Chile (50/144), China

(8/19), Croatia (4/12), Cyprus (5/17), the Dominican Republic (1/4), Ecuador (40/107), Egypt (6/27), El Sal-

vador (8/17), Estonia (12/47), Greece (3/6), Guernsey (2/6), Iceland (7/21), India (12/52), the Isle of Man

(3/9), Israel (10/28), Jamaica (3/12), Jordan (2/6), Kazakhstan (1/5), Kenya (4/14), Kuwait (4/17), Latvia

(8/29), Lebanon (1/5), Macau (4/19), Malta (2/8), Monaco (1/1), Montserrat (1/2), Nigeria (2/9), the Northern

Mariana Islands (1/4), Oman (3/8), Pakistan (4/14), Panama (3/13), Peru (9/27), Qatar (3/14), Romania (3/6),

Saudi Arabia (1/5), Slovakia (10/23), Slovenia (4/15), South Korea (9/45), Tanzania (5/16), Thailand (17/45),

Trinidad and Tobago (6/27), Tunisia (2/10), the Ukraine (3/9), the United Arab Emirates (3/7), Uruguay

(12/34), and Venezuela (46/192). Unfortunately, for many South American countries (e.g., Venezuela), there

are no data available for 2006, which is why we excluded these from the country-specific analysis even though

the number of companies is relatively large. However, detailed results for all these countries are available upon

request. 2 We did not include Canadian insurers, which are covered in the database, but presented in a separate section

with different data fields.

16

As discussed above, there is widespread agreement in literature with regard to the

choice of inputs. We thus use labor, business services and material, debt capital, and

equity capital as inputs. Due to data availability, it was necessary to simplify this

scheme by combining labor and business services; only operating expenses (including

commissions) are available in the AM Best data. This simplification is common in

many other international comparisons (see Diacon/Starkey/O’Brien, 2002; Fenn et al.,

2008) for much the same reason it is made here. Furthermore, Ennsfell-

ner/Lewis/Anderson (2004) argue that the operating expenses should be treated as a

single input in order to reduce the number of parameters that will need to be estimated.

We thus use operating expenses to proxy both labor and business services and handle

these as a single input in the following analysis.

Cummins/Weiss (2000) showed in their analysis of operating expenses in the US in-

surance market that these are mostly labor related, e.g., in both life and non-life insur-

ance, the largest expenses are employee salaries and commissions. We therefore con-

centrate on labor to determine the price of the operating-expenses-related input factor.

The price of labor is determined using the ILO October Inquiry, a worldwide survey

of wages and hours of work published by the International Labour Organization (ILO;

see http://laborsta.ilo.org/) and used in a variety of efficiency applications (see, e.g.,

Fenn et al., 2008). The price of debt capital is determined using country-specific one-

year treasury bill rates for each year of the sample period; the price of equity capital is

determined using the yearly rate of total return of the country-specific MSCI stock

market indices (all data were obtained from the Datastream database; see Cummins/

Rubio-Misas (2006) for a comparable selection and a discussion on selection depend-

ing on the insurer’s capital structure and portfolio risk). To ensure that all monetary

values are directly comparable, we deflate each year’s value by the consumer price

index to the base year 2002 (see Weiss, 1991b; Cummins/Zi, 1998). Country-specific

consumer price indices were obtained from the International Labour Organization.

As is usual in most studies on efficiency in the insurance industry, we use the value-

added approach to determine the outputs. We thus distinguish between the three main

services provided by insurance companies—risk-pooling/-bearing, financial services,

and intermediation. According to Yuengert (1993), a good proxy for the amount of

risk-pooling/-bearing and financial services is the value of real incurred losses, defined

as current losses paid plus additions to reserves. As different types of services are pro-

vided by life and non-life insurance firms, we need separate output measures for each

type of firm (see Choi/Weiss, 2005). We use the present value of claims plus additions

to reserves as a proxy for the output volume for non-life insurance and the present

value of net incurred benefits plus additions to reserves for life insurance. As done, for

example, in Berger/Cummins/Weiss (1997), the price of risk-pooling/-bearing and

17

financial services is calculated as net premiums minus the volume proxy, expressed as

a ratio to the volume proxy. The output variable, which proxies the intermediation

function, is the real value of invested assets. To obtain present values we again deflate

each year’s value using the consumer price index. The price of the intermediation out-

put is the expected rate of return on assets (see Berger/Cummins/Weiss, 1997); we

therefore again use the yearly rate of total return of the country-specific MSCI stock

market indices.

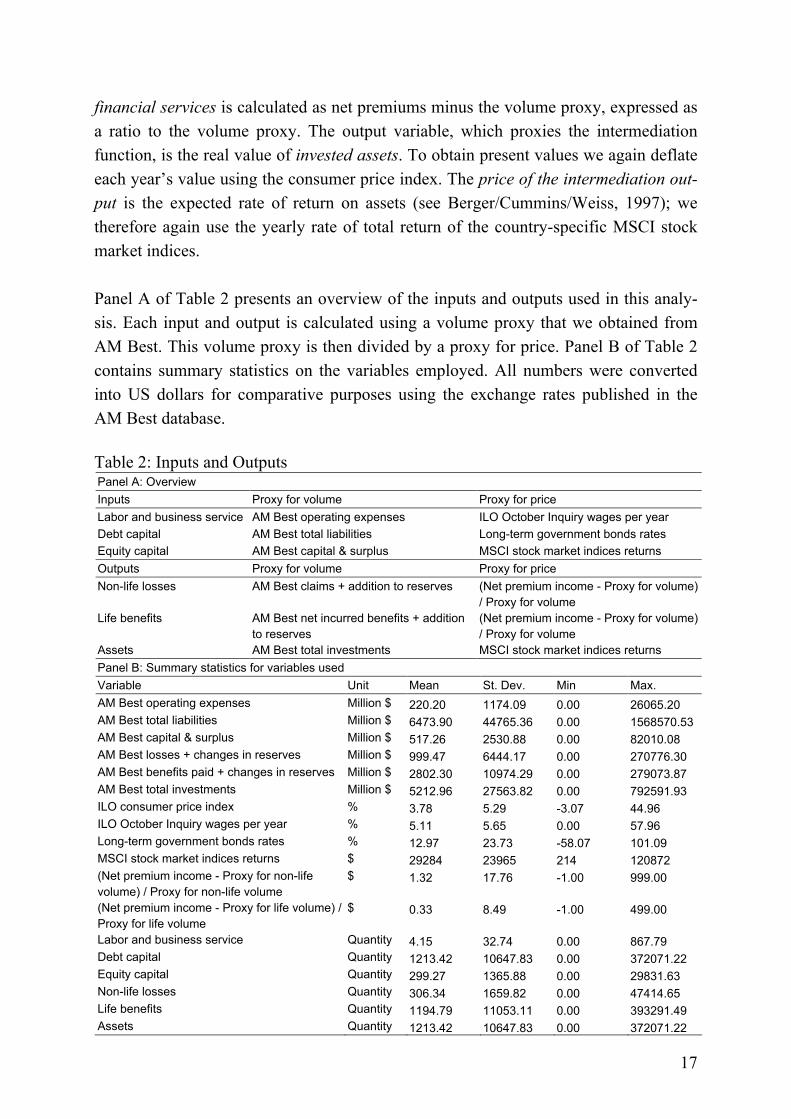

Panel A of Table 2 presents an overview of the inputs and outputs used in this analy-

sis. Each input and output is calculated using a volume proxy that we obtained from

AM Best. This volume proxy is then divided by a proxy for price. Panel B of Table 2

contains summary statistics on the variables employed. All numbers were converted

into US dollars for comparative purposes using the exchange rates published in the

AM Best database.

Table 2: Inputs and Outputs Panel A: Overview

Inputs Proxy for volume Proxy for price

Labor and business service AM Best operating expenses ILO October Inquiry wages per year

Debt capital AM Best total liabilities Long-term government bonds rates

Equity capital AM Best capital & surplus MSCI stock market indices returns

Outputs Proxy for volume Proxy for price

Non-life losses AM Best claims + addition to reserves (Net premium income - Proxy for volume)

/ Proxy for volume

Life benefits AM Best net incurred benefits + addition

to reserves

(Net premium income - Proxy for volume)

/ Proxy for volume

Assets AM Best total investments MSCI stock market indices returns

Panel B: Summary statistics for variables used

Variable Unit Mean St. Dev. Min Max.

AM Best operating expenses Million $ 220.20 1174.09 0.00 26065.20

AM Best total liabilities Million $ 6473.90 44765.36 0.00 1568570.53

AM Best capital & surplus Million $ 517.26 2530.88 0.00 82010.08

AM Best losses + changes in reserves Million $ 999.47 6444.17 0.00 270776.30

AM Best benefits paid + changes in reserves Million $ 2802.30 10974.29 0.00 279073.87

AM Best total investments Million $ 5212.96 27563.82 0.00 792591.93

ILO consumer price index % 3.78 5.29 -3.07 44.96

ILO October Inquiry wages per year % 5.11 5.65 0.00 57.96

Long-term government bonds rates % 12.97 23.73 -58.07 101.09

MSCI stock market indices returns $ 29284 23965 214 120872

(Net premium income - Proxy for non-life

volume) / Proxy for non-life volume

$ 1.32 17.76 -1.00 999.00

(Net premium income - Proxy for life volume) /

Proxy for life volume

$ 0.33 8.49 -1.00 499.00

Labor and business service Quantity 4.15 32.74 0.00 867.79

Debt capital Quantity 1213.42 10647.83 0.00 372071.22

Equity capital Quantity 299.27 1365.88 0.00 29831.63

Non-life losses Quantity 306.34 1659.82 0.00 47414.65

Life benefits Quantity 1194.79 11053.11 0.00 393291.49

Assets Quantity 1213.42 10647.83 0.00 372071.22

18

In the next section, we analyze two methodologies (data envelopment analysis, sto-

chastic frontier analysis), 37 countries (see Table 3 for listing), three organizational

forms (stocks, mutual, other), three distributional forms (agency based, direct writers,

both), three lines of business (life, non-life, groups), and three company sizes (large,

medium, small). For data envelopment analysis, we use Deap, Version 2.1 (see Coelli,

1996a) and calculate efficiency values assuming input orientation and variable returns

to scale. For stochastic frontier analysis, we calculate a translog production frontier

using Frontier, Version 4.1 (see Coelli, 1996b), assuming the inefficiencies to follow a

half-normal distribution. Company-specific information on domiciliary country, or-

ganization type, distribution type, and lines of business is extracted from the AM Best

database. Total assets is a widespread measure of insurer size (see, e.g., Cummins/Zi,

1998; Diacon/Starkey/O’Brien, 2002). For comparison of different company sizes, we

thus subdivide all companies by their total assets into large (total assets larger than

$816 million), medium, and small (total assets smaller than $64 million) insurers.

3.2. RESULTS

Data envelopment analysis

The results of the data envelopment analysis are set out in Table 3, presented at differ-

ent levels of aggregation so as to focus on different aspects of efficiency. The first fo-

cus is on countries (Panel A), the second on organization (Panel B), the third on distri-

bution (Panel C), the fourth on lines of business (Panel D), and the fifth on size (Panel

E). For comparison purposes, the average values are presented in the last line of the

table. Altogether our analysis covers 4,103 insurers, with a total of 15,306 firm years.

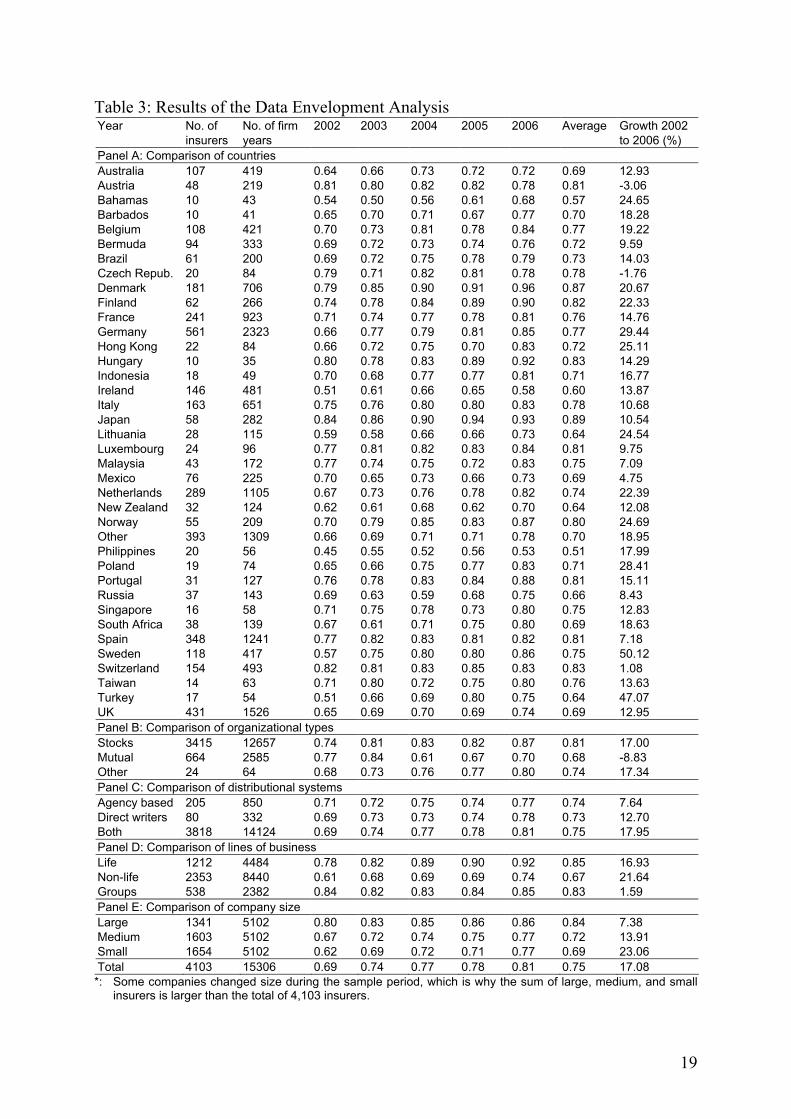

The last line of Table 3 shows that across all 4,103 companies efficiency increased by

17.08% from 2002 to 2006. There is a steady growth in efficiency from 0.69 in 2002

to 0.75 in 2006. However, large differences can be found between countries (see Panel

A). The country with the highest efficiency is Japan (average efficiency 0.89), fol-

lowed by Denmark (0.87) and Switzerland (0.83). The lowest efficiency values are

found for the Philippines (average efficiency 0.51), the Bahamas (0.57), and Ireland

(0.60). Overall, it appears that developed countries in Asia and Europe achieve higher

efficiency scores than do emerging market countries. The efficiency of the largest

economies under evaluation is in the upper-middle field: Germany is in 13th place

(average efficiency 0.77); France is in 15th place (0.76). Relatively low efficiency val-

ues were found for the United Kingdom, which is in 28th place (0.69). Considering the

development of efficiency over the sample period, the highest efficiency gains were

obtained in Sweden (+50.12%) and Turkey (+47.07%). Austria (–1.76%) and the

Czech Republic (–3.06%) are the only countries that did not increase efficiency from

2002 to 2006.

19

Table 3: Results of the Data Envelopment Analysis Year No. of

insurers No. of firm years

2002 2003 2004 2005 2006 Average Growth 2002 to 2006 (%)

Panel A: Comparison of countries

Australia 107 419 0.64 0.66 0.73 0.72 0.72 0.69 12.93 Austria 48 219 0.81 0.80 0.82 0.82 0.78 0.81 -3.06 Bahamas 10 43 0.54 0.50 0.56 0.61 0.68 0.57 24.65 Barbados 10 41 0.65 0.70 0.71 0.67 0.77 0.70 18.28 Belgium 108 421 0.70 0.73 0.81 0.78 0.84 0.77 19.22 Bermuda 94 333 0.69 0.72 0.73 0.74 0.76 0.72 9.59 Brazil 61 200 0.69 0.72 0.75 0.78 0.79 0.73 14.03 Czech Repub. 20 84 0.79 0.71 0.82 0.81 0.78 0.78 -1.76 Denmark 181 706 0.79 0.85 0.90 0.91 0.96 0.87 20.67 Finland 62 266 0.74 0.78 0.84 0.89 0.90 0.82 22.33 France 241 923 0.71 0.74 0.77 0.78 0.81 0.76 14.76 Germany 561 2323 0.66 0.77 0.79 0.81 0.85 0.77 29.44 Hong Kong 22 84 0.66 0.72 0.75 0.70 0.83 0.72 25.11 Hungary 10 35 0.80 0.78 0.83 0.89 0.92 0.83 14.29 Indonesia 18 49 0.70 0.68 0.77 0.77 0.81 0.71 16.77 Ireland 146 481 0.51 0.61 0.66 0.65 0.58 0.60 13.87 Italy 163 651 0.75 0.76 0.80 0.80 0.83 0.78 10.68 Japan 58 282 0.84 0.86 0.90 0.94 0.93 0.89 10.54 Lithuania 28 115 0.59 0.58 0.66 0.66 0.73 0.64 24.54 Luxembourg 24 96 0.77 0.81 0.82 0.83 0.84 0.81 9.75 Malaysia 43 172 0.77 0.74 0.75 0.72 0.83 0.75 7.09 Mexico 76 225 0.70 0.65 0.73 0.66 0.73 0.69 4.75 Netherlands 289 1105 0.67 0.73 0.76 0.78 0.82 0.74 22.39 New Zealand 32 124 0.62 0.61 0.68 0.62 0.70 0.64 12.08 Norway 55 209 0.70 0.79 0.85 0.83 0.87 0.80 24.69 Other 393 1309 0.66 0.69 0.71 0.71 0.78 0.70 18.95 Philippines 20 56 0.45 0.55 0.52 0.56 0.53 0.51 17.99 Poland 19 74 0.65 0.66 0.75 0.77 0.83 0.71 28.41 Portugal 31 127 0.76 0.78 0.83 0.84 0.88 0.81 15.11 Russia 37 143 0.69 0.63 0.59 0.68 0.75 0.66 8.43 Singapore 16 58 0.71 0.75 0.78 0.73 0.80 0.75 12.83 South Africa 38 139 0.67 0.61 0.71 0.75 0.80 0.69 18.63 Spain 348 1241 0.77 0.82 0.83 0.81 0.82 0.81 7.18 Sweden 118 417 0.57 0.75 0.80 0.80 0.86 0.75 50.12 Switzerland 154 493 0.82 0.81 0.83 0.85 0.83 0.83 1.08 Taiwan 14 63 0.71 0.80 0.72 0.75 0.80 0.76 13.63 Turkey 17 54 0.51 0.66 0.69 0.80 0.75 0.64 47.07 UK 431 1526 0.65 0.69 0.70 0.69 0.74 0.69 12.95

Panel B: Comparison of organizational types

Stocks 3415 12657 0.74 0.81 0.83 0.82 0.87 0.81 17.00 Mutual 664 2585 0.77 0.84 0.61 0.67 0.70 0.68 -8.83 Other 24 64 0.68 0.73 0.76 0.77 0.80 0.74 17.34

Panel C: Comparison of distributional systems

Agency based 205 850 0.71 0.72 0.75 0.74 0.77 0.74 7.64 Direct writers 80 332 0.69 0.73 0.73 0.74 0.78 0.73 12.70 Both 3818 14124 0.69 0.74 0.77 0.78 0.81 0.75 17.95

Panel D: Comparison of lines of business

Life 1212 4484 0.78 0.82 0.89 0.90 0.92 0.85 16.93 Non-life 2353 8440 0.61 0.68 0.69 0.69 0.74 0.67 21.64 Groups 538 2382 0.84 0.82 0.83 0.84 0.85 0.83 1.59

Panel E: Comparison of company size

Large 1341 5102 0.80 0.83 0.85 0.86 0.86 0.84 7.38 Medium 1603 5102 0.67 0.72 0.74 0.75 0.77 0.72 13.91 Small 1654 5102 0.62 0.69 0.72 0.71 0.77 0.69 23.06

Total 4103 15306 0.69 0.74 0.77 0.78 0.81 0.75 17.08 *: Some companies changed size during the sample period, which is why the sum of large, medium, and small

insurers is larger than the total of 4,103 insurers.

20

The second focus of our analysis concerns different organizational forms and their ef-

fects on efficiency (see Panel B of Table 3). We find evidence for the expense prefer-

ence hypothesis, as the average efficiency values of stock companies (0.81) are much

higher than those of mutual insurers (0.68). This finding is in line with most research

in the field, e.g., Cummins/Weiss/Zi (1999) and Erhemjamts/Leverty (2007). Other

legal forms (e.g., public companies) play only a very minor role in our sample. While

there is a steady growth in efficiency over time for stocks and other companies, we

find large variations and a decreasing efficiency for mutuals over time, an effect that

might be due to mergers, acquisitions, and demutualization occurring during the period

of investigation.

Panel C of Table 3 shows the results for different distribution systems. The DEA re-

sults do not confirm Ward’s (2002) finding that insurers focused on one distribution

system are more efficient than those using more than one system. Indeed, in our study,

the highest efficiency values are found for insurers using different distribution systems

(average efficiency 0.75), followed by agency based (0.74) and direct writers (0.73).

However, the differences are minor. Furthermore, note that the number of insurers that

identify as pure direct writer or agency based is relatively small in our sample (but still

large in absolute terms compared to other studies covering this aspect; e.g., Ward,

2002 covers 44 companies and Klumpes, 2004, 90 companies).

Interesting differences can be found when comparing different lines of business (see

Panel D of Table 3), a field that has not been in focus of literature to date. On a very

aggregate level (detailed results on less aggregated level are available upon request),

we compare life insurers, non-life insurers, and groups (i.e., companies offering both

life and non-life insurance). We find that average efficiency in life insurance is much

higher than in non-life insurance (0.85 vs. 0.67). This effect might be connected with

the size effects and economies of scale (see next paragraph) as, based on total assets,

the average life insurer is six times larger than the average non-life insurer. We find no

evidence for economies of scope; the multi-product/-branch firms are not more effi-

cient than specialized firms.

In Panel E of Table 3 the total sample is subdivided by total assets into three size

groups—large, medium, and small insurers. In agreement with most research on

economies of scale, we find that large companies have much higher efficiency than

small companies. Average efficiency for large companies is 0.84, while it is only 0.72

for medium companies, and 0.69 for small companies. However, smaller companies

have the most rapid gains in efficiency: from 2002 to 2006, efficiency increased for

21

large insurers by 7.38%, by 13.91% for medium insurers, and by 23.06% for small

insurers.

Stochastic frontier analysis

Table 4 is structured like Table 3 and shows the results of the stochastic frontier analy-

sis. Again, average efficiency is presented for different countries (Panel A), organiza-

tion types (Panel B), distribution systems (Panel C), lines of business (Panel D), and

company sizes (Panel E). The last line of the table shows the efficiency values of the

full sample. Below, we briefly highlight the main results and the main differences

compared to the DEA (Table 3).

One obvious difference between the results in Tables 3 and 4 is that the efficiency val-

ues are lower and more variable under the stochastic frontier analysis. The average

efficiency across all 4,103 companies is only 0.36 compared to 0.75 with the data en-

velopment analysis. Nevertheless, the results of the two types of analysis are very

similar, leading to identical economic insights. Under the SFA, efficiency increased by

30.20% from 2002 to 2006 and there is a growth in efficiency from 0.30 in 2002 to

0.38 in 2006. Large differences between countries are also found when employing sto-

chastic frontier analysis. The country with the highest efficiency is again Japan (aver-

age efficiency 0.62) and the country with the lowest efficiency is, again, the Philip-

pines (0.18). We again confirm the expense preference hypothesis: the average effi-

ciency value of stock companies (0.36) is higher than that of mutual insurers (0.33).

Again, efficiency in life insurance is on average much higher than in non-life insur-

ance (0.48 vs. 0.27). Efficiency for the multi-line groups (0.43) is lower than for the

mono-line life insurers; we thus, once more, find no evidence for economies of scope.

Finally, we find that efficiency for large companies (0.61 on average) is much higher

than for medium-sized (0.28) and small companies (0.19). All these observations con-

firm the results of the data envelopment analysis.

One difference between the results in Tables 4 and 3 has to do with distribution sys-

tems. The results of the SFA confirm Ward’s (2002) result that insurers focusing on

one distribution system have higher efficiency than those using more than one system.

Efficiency of agency-based insurers (0.51 on average) is again higher than that of di-

rect writers (0.45), but the individual efficiency of these two groups is now much

higher than the efficiency of those insurers using both (0.35). SFA thus provides more

clear results than DEA in this case. The finding that agency-based insurers are more

efficient than direct writers is in agreement with the findings of Brockett et al. (1998,

2004) for the United States and the findings of Klumpes (2004) for the United King-

dom.

22

Table 4: Results of the Stochastic Frontier Analysis Year No. of

insurers No. of firm years

2002 2003 2004 2005 2006 Average Growth 2002 to 2006 (%)

Panel A: Comparison of countries

Australia 107 419 0.34 0.52 0.35 0.44 0.34 0.40 0.15 Austria 48 219 0.29 0.42 0.33 0.50 0.29 0.37 -0.62 Bahamas 10 43 0.16 0.40 0.14 0.23 0.30 0.24 84.41 Barbados 10 41 0.27 0.26 0.29 0.33 0.22 0.27 -21.45 Belgium 108 421 0.28 0.40 0.28 0.38 0.32 0.33 12.78 Bermuda 94 333 0.32 0.35 0.37 0.45 0.30 0.36 -5.00 Brazil 61 200 0.19 0.37 0.17 0.32 0.31 0.26 64.50 Czech Repub. 20 84 0.18 0.29 0.19 0.37 0.21 0.25 18.48 Denmark 181 706 0.24 0.37 0.24 0.34 0.40 0.31 67.20 Finland 62 266 0.37 0.59 0.37 0.47 0.51 0.46 38.38 France 241 923 0.42 0.54 0.43 0.51 0.56 0.48 31.97 Germany 561 2323 0.35 0.52 0.32 0.42 0.45 0.41 28.39 Hong Kong 22 84 0.21 0.21 0.17 0.29 0.19 0.21 -7.85 Hungary 10 35 0.18 0.31 0.20 0.41 0.15 0.26 -19.89 Indonesia 18 49 0.23 0.19 0.20 0.39 0.14 0.22 -40.83 Ireland 146 481 0.27 0.40 0.25 0.35 0.28 0.31 4.83 Italy 163 651 0.39 0.55 0.42 0.51 0.49 0.47 25.84 Japan 58 282 0.56 0.73 0.54 0.66 0.60 0.62 6.01 Lithuania 28 115 0.15 0.20 0.14 0.27 0.18 0.19 17.46 Luxembourg 24 96 0.27 0.45 0.27 0.36 0.29 0.33 9.14 Malaysia 43 172 0.24 0.33 0.20 0.31 0.22 0.27 -7.18 Mexico 76 225 0.18 0.33 0.17 0.26 0.34 0.24 83.77 Netherlands 289 1105 0.32 0.41 0.30 0.38 0.34 0.35 6.48 New Zealand 32 124 0.20 0.29 0.18 0.26 0.22 0.23 12.29 Norway 55 209 0.32 0.34 0.33 0.38 0.40 0.35 26.99 Other 393 1309 0.20 0.32 0.20 0.38 0.27 0.26 35.72 Philippines 20 56 0.18 0.22 0.14 0.24 0.15 0.18 -14.53 Poland 19 74 0.29 0.43 0.27 0.33 0.29 0.33 -0.80 Portugal 31 127 0.27 0.45 0.28 0.38 0.28 0.34 4.33 Russia 37 143 0.18 0.25 0.18 0.33 0.15 0.22 -17.35 Singapore 16 58 0.24 0.20 0.20 0.32 0.24 0.24 -2.22 South Africa 38 139 0.26 0.44 0.30 0.40 0.50 0.36 89.25 Spain 348 1241 0.23 0.34 0.22 0.33 0.33 0.28 44.23 Sweden 118 417 0.31 0.39 0.31 0.41 0.41 0.36 35.28 Switzerland 154 493 0.37 0.41 0.32 0.41 0.54 0.38 47.40 Taiwan 14 63 0.36 0.40 0.33 0.43 0.32 0.37 -11.79 Turkey 17 54 0.19 0.25 0.22 0.33 0.22 0.23 12.14 UK 431 1526 0.27 0.49 0.34 0.45 0.39 0.39 44.40

Panel B: Comparison of organizational types

Stocks 3415 12657 0.30 0.43 0.30 0.42 0.39 0.36 30.58 Mutual 664 2585 0.29 0.40 0.27 0.36 0.38 0.33 29.79 Other 24 64 0.17 0.27 0.35 0.43 0.31 0.34 80.14

Panel C: Comparison of distributional systems

Agency based 205 850 0.48 0.54 0.48 0.56 0.49 0.51 0.82 Direct writers 80 332 0.44 0.50 0.41 0.50 0.39 0.45 -12.87 Both 3818 14124 0.28 0.42 0.28 0.39 0.38 0.35 33.41

Panel D: Comparison of lines of business

Life 1212 4484 0.31 0.73 0.30 0.49 0.61 0.48 96.20 Non-life 2353 8440 0.28 0.25 0.27 0.32 0.26 0.27 -5.69 Groups 538 2382 0.34 0.47 0.39 0.58 0.38 0.43 11.07

Panel E: Comparison of company size*

Large 1341 5102 0.52 0.73 0.53 0.65 0.60 0.61 14.38 Medium 1603 5102 0.24 0.37 0.22 0.31 0.23 0.28 -3.06 Small 1654 5102 0.17 0.23 0.14 0.23 0.18 0.19 4.92

Total 4103 15306 0.30 0.43 0.30 0.41 0.38 0.36 30.20 *: Some companies changed size during the sample period, which is why the sum of large, medium, and small

insurers is larger than the total of 4,103 insurers.

23

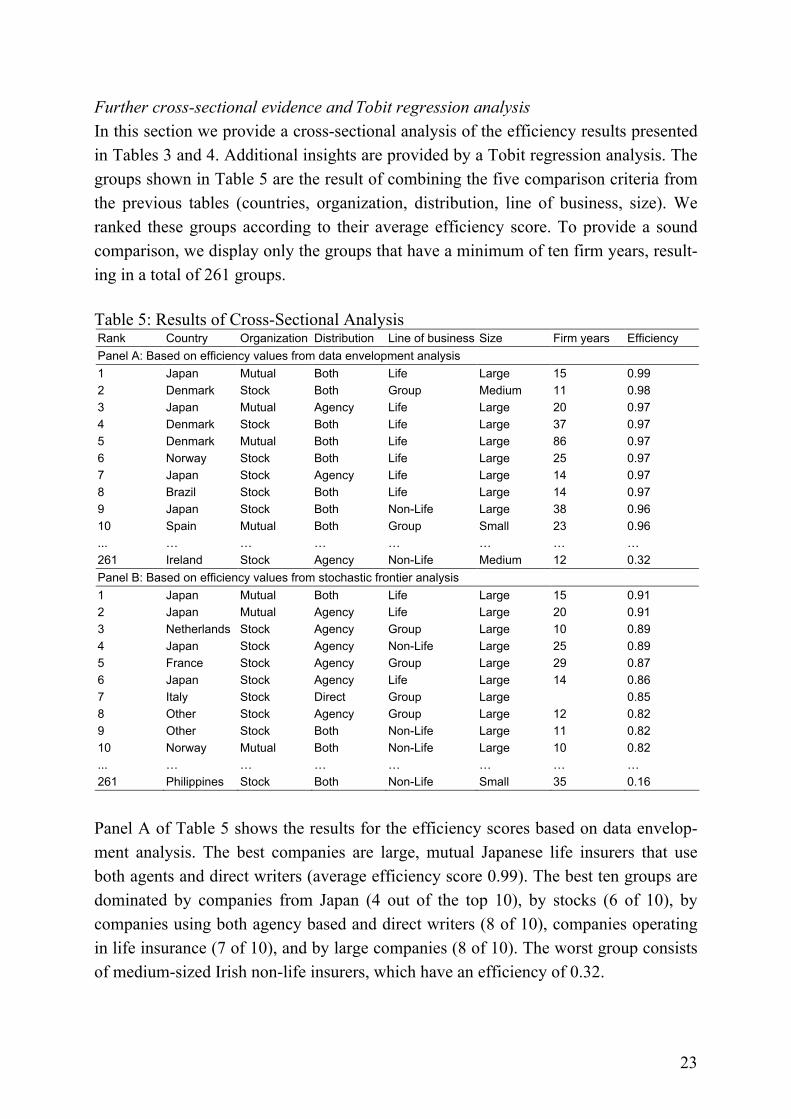

Further cross-sectional evidence and Tobit regression analysis

In this section we provide a cross-sectional analysis of the efficiency results presented

in Tables 3 and 4. Additional insights are provided by a Tobit regression analysis. The

groups shown in Table 5 are the result of combining the five comparison criteria from

the previous tables (countries, organization, distribution, line of business, size). We

ranked these groups according to their average efficiency score. To provide a sound

comparison, we display only the groups that have a minimum of ten firm years, result-

ing in a total of 261 groups.

Table 5: Results of Cross-Sectional Analysis Rank Country Organization Distribution Line of business Size Firm years Efficiency

Panel A: Based on efficiency values from data envelopment analysis

1 Japan Mutual Both Life Large 15 0.99

2 Denmark Stock Both Group Medium 11 0.98

3 Japan Mutual Agency Life Large 20 0.97

4 Denmark Stock Both Life Large 37 0.97

5 Denmark Mutual Both Life Large 86 0.97

6 Norway Stock Both Life Large 25 0.97

7 Japan Stock Agency Life Large 14 0.97

8 Brazil Stock Both Life Large 14 0.97

9 Japan Stock Both Non-Life Large 38 0.96

10 Spain Mutual Both Group Small 23 0.96

... … … … … … … …

261 Ireland Stock Agency Non-Life Medium 12 0.32

Panel B: Based on efficiency values from stochastic frontier analysis

1 Japan Mutual Both Life Large 15 0.91

2 Japan Mutual Agency Life Large 20 0.91

3 Netherlands Stock Agency Group Large 10 0.89

4 Japan Stock Agency Non-Life Large 25 0.89

5 France Stock Agency Group Large 29 0.87

6 Japan Stock Agency Life Large 14 0.86

7 Italy Stock Direct Group Large 0.85

8 Other Stock Agency Group Large 12 0.82

9 Other Stock Both Non-Life Large 11 0.82

10 Norway Mutual Both Non-Life Large 10 0.82

... … … … … … … …

261 Philippines Stock Both Non-Life Small 35 0.16

Panel A of Table 5 shows the results for the efficiency scores based on data envelop-

ment analysis. The best companies are large, mutual Japanese life insurers that use

both agents and direct writers (average efficiency score 0.99). The best ten groups are

dominated by companies from Japan (4 out of the top 10), by stocks (6 of 10), by

companies using both agency based and direct writers (8 of 10), companies operating

in life insurance (7 of 10), and by large companies (8 of 10). The worst group consists

of medium-sized Irish non-life insurers, which have an efficiency of 0.32.

24

In Panel B of Table 5, the results for the efficiency scores based on stochastic frontier

analysis are presented. The best group in Panel A (large, mutual Japanese life insurers

using both agents and direct writers) is also the best group in Panel B, the second best

group with the DEA (large, mutual Japanese life insurers using agents) is in third place

with SFA. We again find mostly Japanese companies among the best ten groups (4 of

10). In contrast to the DEA, there are no Danish companies among the best 10, but,

instead, insurers from the Netherlands, France, Italy, and Norway. The worst group

with SFA are small non-life insurers from the Philippines, which have an efficiency of

0.16. In summary, it appears that the most efficient companies are large life insurers

from Japan, operating as either stock or mutuals.

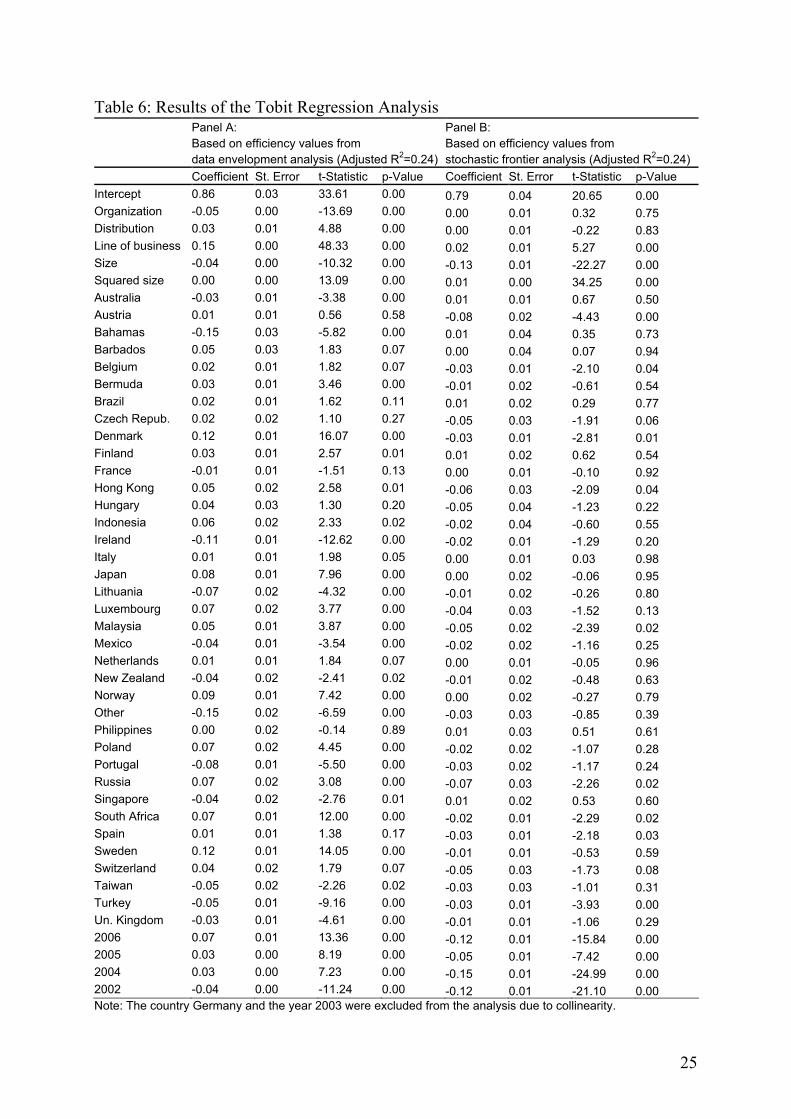

Finally, we conduct a Tobit regression analysis in order to identify the key drivers of

efficiency with respect to different independent variables. As the dependent variable

(i.e., the efficiency value) is limited between zero and one, standard regression coeffi-

cients will be underestimated and thus need to be corrected. This correction is pro-

vided by Tobin’s (1958) modified form of a standard regression analysis for the inves-

tigation of limited dependent variables. We determine Tobit regression parameters us-

ing the statistic software R. We use the following independent, explanatory variables

for our regression on the efficiency scores (see Diacon/Starkey/O’Brien (2002) for a

comparable selection): (1) organization (1 if company is stock; 0 otherwise), (2) distri-

bution (1 if both agency based and direct writers; 0 otherwise), (3) line of business (1

if life/group; 0 if non-life), (4) company size (natural logarithm of the total assets), and

(5) squared size (to capture nonlinearities between size and efficiency). Country and

year dummy variables are included to pick up country and time effects. The Tobit re-

gression results for the efficiency values based on data envelopment analysis are pre-

sented in Panel A of Table 6; the results based on stochastic frontier analysis in Panel

B of Table 6.

Considering Panel A, the results of the Tobit regression analysis confirm that organi-

zation and line of business are particularly and strongly associated with efficiency;

these have the (absolute) highest t-statistics and lowest p-values. Size and squared size

are also important for determining efficiency. The country dummies confirm the inter-

national differences previously identified. The results confirm the above findings that

the most efficient companies are insurers from Japan. Considering Panel B, the results

again show the importance of company size for efficiency. Surprisingly, though, and

in contrast to Panel A, organization and distribution do not significantly influence effi-

ciency. Line of business is again positively connected with efficiency.

25

Table 6: Results of the Tobit Regression Analysis Panel A:

Based on efficiency values from

data envelopment analysis (Adjusted R2=0.24)

Panel B:

Based on efficiency values from

stochastic frontier analysis (Adjusted R2=0.24)

Coefficient St. Error t-Statistic p-Value Coefficient St. Error t-Statistic p-Value

Intercept 0.86 0.03 33.61 0.00 0.79 0.04 20.65 0.00

Organization -0.05 0.00 -13.69 0.00 0.00 0.01 0.32 0.75

Distribution 0.03 0.01 4.88 0.00 0.00 0.01 -0.22 0.83

Line of business 0.15 0.00 48.33 0.00 0.02 0.01 5.27 0.00

Size -0.04 0.00 -10.32 0.00 -0.13 0.01 -22.27 0.00

Squared size 0.00 0.00 13.09 0.00 0.01 0.00 34.25 0.00

Australia -0.03 0.01 -3.38 0.00 0.01 0.01 0.67 0.50

Austria 0.01 0.01 0.56 0.58 -0.08 0.02 -4.43 0.00

Bahamas -0.15 0.03 -5.82 0.00 0.01 0.04 0.35 0.73

Barbados 0.05 0.03 1.83 0.07 0.00 0.04 0.07 0.94

Belgium 0.02 0.01 1.82 0.07 -0.03 0.01 -2.10 0.04

Bermuda 0.03 0.01 3.46 0.00 -0.01 0.02 -0.61 0.54

Brazil 0.02 0.01 1.62 0.11 0.01 0.02 0.29 0.77

Czech Repub. 0.02 0.02 1.10 0.27 -0.05 0.03 -1.91 0.06

Denmark 0.12 0.01 16.07 0.00 -0.03 0.01 -2.81 0.01

Finland 0.03 0.01 2.57 0.01 0.01 0.02 0.62 0.54

France -0.01 0.01 -1.51 0.13 0.00 0.01 -0.10 0.92

Hong Kong 0.05 0.02 2.58 0.01 -0.06 0.03 -2.09 0.04

Hungary 0.04 0.03 1.30 0.20 -0.05 0.04 -1.23 0.22

Indonesia 0.06 0.02 2.33 0.02 -0.02 0.04 -0.60 0.55

Ireland -0.11 0.01 -12.62 0.00 -0.02 0.01 -1.29 0.20

Italy 0.01 0.01 1.98 0.05 0.00 0.01 0.03 0.98

Japan 0.08 0.01 7.96 0.00 0.00 0.02 -0.06 0.95

Lithuania -0.07 0.02 -4.32 0.00 -0.01 0.02 -0.26 0.80

Luxembourg 0.07 0.02 3.77 0.00 -0.04 0.03 -1.52 0.13

Malaysia 0.05 0.01 3.87 0.00 -0.05 0.02 -2.39 0.02

Mexico -0.04 0.01 -3.54 0.00 -0.02 0.02 -1.16 0.25

Netherlands 0.01 0.01 1.84 0.07 0.00 0.01 -0.05 0.96

New Zealand -0.04 0.02 -2.41 0.02 -0.01 0.02 -0.48 0.63

Norway 0.09 0.01 7.42 0.00 0.00 0.02 -0.27 0.79

Other -0.15 0.02 -6.59 0.00 -0.03 0.03 -0.85 0.39

Philippines 0.00 0.02 -0.14 0.89 0.01 0.03 0.51 0.61

Poland 0.07 0.02 4.45 0.00 -0.02 0.02 -1.07 0.28

Portugal -0.08 0.01 -5.50 0.00 -0.03 0.02 -1.17 0.24

Russia 0.07 0.02 3.08 0.00 -0.07 0.03 -2.26 0.02

Singapore -0.04 0.02 -2.76 0.01 0.01 0.02 0.53 0.60

South Africa 0.07 0.01 12.00 0.00 -0.02 0.01 -2.29 0.02

Spain 0.01 0.01 1.38 0.17 -0.03 0.01 -2.18 0.03

Sweden 0.12 0.01 14.05 0.00 -0.01 0.01 -0.53 0.59

Switzerland 0.04 0.02 1.79 0.07 -0.05 0.03 -1.73 0.08

Taiwan -0.05 0.02 -2.26 0.02 -0.03 0.03 -1.01 0.31

Turkey -0.05 0.01 -9.16 0.00 -0.03 0.01 -3.93 0.00

Un. Kingdom -0.03 0.01 -4.61 0.00 -0.01 0.01 -1.06 0.29

2006 0.07 0.01 13.36 0.00 -0.12 0.01 -15.84 0.00

2005 0.03 0.00 8.19 0.00 -0.05 0.01 -7.42 0.00

2004 0.03 0.00 7.23 0.00 -0.15 0.01 -24.99 0.00

2002 -0.04 0.00 -11.24 0.00 -0.12 0.01 -21.10 0.00 Note: The country Germany and the year 2003 were excluded from the analysis due to collinearity.

26

4. CONCLUSION

The purpose of this paper was to review recent studies on efficiency in the insurance

industry and to provide new empirical evidence on this widely discussed topic. Our

overview extends two earlier surveys, one by Berger/Humphrey (1997) and the other

by Cummins/Weiss (2000), and analyzes 83 studies on efficiency measurement in the

insurance industry. Our results show that during the last several years, methodologies

have been refined, new topics have been addressed, and geographic coverage has been

extended beyond a US focused view to a broad set of countries. The large number of

studies illustrates the increasing interest in the international competitiveness and effi-

ciency of insurance companies.

In the second part of the paper, we extended existing cross-country comparisons of

efficiency in the insurance industry by analyzing a broad international dataset that has