Embed Size (px)

Citation preview

Reg

ulatio

n:all risk an

d n

o rew

ard?

fron

tiers in fin

ance

jun

e 2004

Regulation: all risk and no reward?

frontiers in financefor decision makers in financial services June 2004

Expanding regulatory horizonsRegulatory risks around the world are escalating andregulators are now interacting on many levels. So howcan you protect your organization everywhere fromrisks that can rise anywhere?

The art of compliance The role of the compliance function continues to evolve but what does a successful function look like?

Capital adequacy: insurers play catch-upPrudential regulation within the insurance sector ismoving towards a Basel II-type model. Can insurers step up to the challenge?

Beware: consumersHow can organizations successfully respond to an increasing consumer regulatory trend and what are the dangers they face?

A quiet revolutionChina’s accession to the WTO has profoundimplications for the country’s financial services markets, creating risks, challenges and opportunities in equal measure.

FINANCIAL SERVICES

For further information on issues raised,please contact:

Brendan Nelson

Global Chairman, KPMG’s Financial Services practiceKPMG LLP (UK)1 Canada Square Canary Wharf London E14 5AG United Kingdom

Tel: +44 (0) 20 7311 6157 Fax: +44 (0) 20 7311 5891e-Mail: [email protected]

Joseph Mauriello

Regional Coordinating Partner, KPMG’s Financial Services practice, AmericasKPMG LLP (US)757 Third Avenue New York, NY 10017 USA

Tel: +1 (212) 954 3727 Fax: +1 (212) 954 2394e-Mail: [email protected]

Steve Roder

Regional Coordinating Partner, KPMG’s Financial Services practice, Asia PacificKPMG in Hong Kong8th Floor, Prince’s Building 10 Chater Road Central Hong Kong

Tel: +852 (-) 2826 7135 Fax: +852 (-) 2845 2588e-Mail: [email protected]

Peter Nash

Head of KPMG’s Financial Services practice,Australia KPMG in Australia7th Floor, KPMG House 161 Collins Street Melbourne, Victoria 3001 Australia

Tel: +61 (3) 9288 5613 Fax: +61 (3) 9288 6986 e-Mail: [email protected]

Georg Rönnberg

Regional Coordinating Partner,KPMG’s Financial Services practice, Europe, Middle East and Africa (EMA),KPMG Deutsche Treuhand-Gesellschaft AG. Marie-Curie-Straße 30 D-60439 Frankfurt /MainGermany

Tel : +49 (69) 9587 2686 Fax. +49 (69) 9587 2688e-Mail: [email protected]

kpmg.com

Please visit www.kpmg.com/financial_services to learn more about KPMG’s Global FinancialServices practice

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

Regulation: all risk and no reward?

01 Introduction

For financial institutions, regulatoryrisk is on the increase but there arebenefits to be had, if it is managedproperly.Brendan Nelson

06 Expanding regulatory horizons

Regulatory risks around the worldare escalating and regulators arenow interacting on many levels. So how can you protect yourorganization everywhere from risksthat can rise anywhere?Hugh Kelly and John Somerville

10 The art of compliance

The role of the compliance functioncontinues to evolve but what does asuccessful function look like?Pamela Hauser and Marcus Sephton

14 Capital adequacy: insurers play

catch-up

Prudential regulation within theinsurance sector is moving towards a Basel II-type model. Can insurersstep up to the challenge?Tim Childs and Peter de Groot

18 Beware: consumers

How can organizations successfullyrespond to an increasing consumerregulatory trend and what are thedangers they face?Douglas Henderson and Sarah Willison

22 Fighting financial crime

Financial crime continues to pay, butfinancial institutions can fight back byimplementing a comprehensive, risk-based program.Bernard Factor and Giles Williams

26 No entry for money launderers

UBS, one of the largest Swiss globalbanks, shares its thorough approachto combating financial crime.Stuart Robertson

30 Avoiding the regulators’ red flag

on outsourcing

When implemented properly,outsourcing has proven its worth,but regulators are insisting financialinstitutions exercise more care.Michael Conover, Scott Harrison andJohn Machin

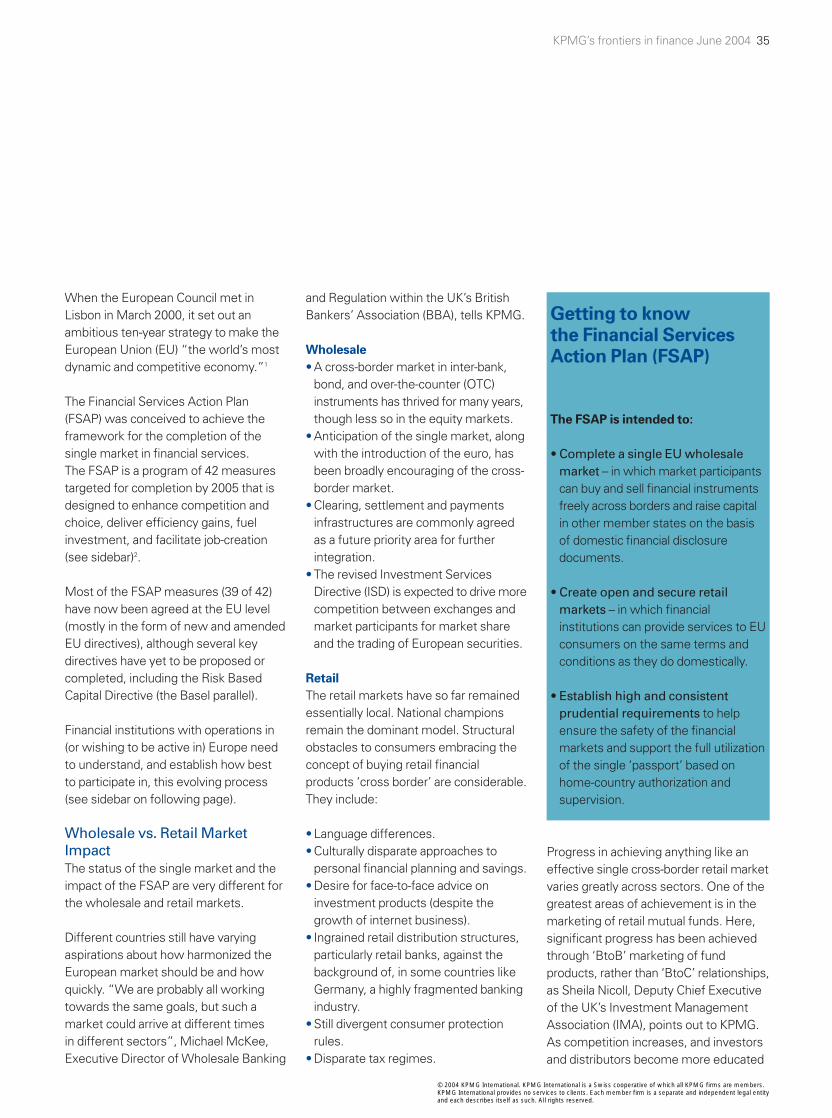

34 Tracking the European

single market

Financial institutions need tounderstand how evolving singlemarket legislation could affect themand how they could influence itsdevelopment.Dirk Auerbach, Richard Cysarz andJonathan Jesty

38 A quiet revolution

China’s accession to the WTO hasprofound implications for thecountry’s financial services markets,creating risks, challenges andopportunities in equal measure.Jack Chow, Paul Kennedy, Bonn Liuand Stephen Yiu

44 A common language for a

common goal

A computer language, XBRL, willhelp regulators worldwide improvetheir reporting processes, and itsvalue will extend to financialinstitutions.Michael Elysée, Geoff Shuetrim and John Turner

48 Basel II, OECD and tax: a complex

relationship?

Banks need to consider carefully how tax and regulation impact oneach other and what they should be doing to manage the effect.Jörg Hashagen and Jane McCormick

In this issue

The information contained herien is of a general nature and is not intended to address the circumstances of any particularindividual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that suchinformation is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on suchinformation without appropriate professional advice after a thorough examination of the particular situation.

KPMG International is a Swiss cooperative that serves as a coordinating entity for a network of independent firms. KPMGInternational provides no audit or other client services. Such services are provided solely by member firms in their respectivegeographic areas. KPMG International and its member firms are legally distinct and separate entities. They are not and nothingcontained herein shall be construed to place these entities in the relationship of parents, subsidiaries, agents, partners, or jointventurers. No member firm has any authority (actual, apparent, implied or otherwise) to obligate or bind KPMG International or any member firm in any manner whatsoever.

© 2004 KPMG International. KPMG International is a Swisscooperative of which all KPMG firms are members. KPMGInternational provides no services to clients. Each memberfirm is a separate and independent legal entity and eachdescribes itself as such. All rights reserved.

Editor: Melanie Hutchings e-Mail: [email protected] by Mytton WilliamsPrinted by Jevons Brown, UKProduced by KPMG’s Global Financial Services practice

208652

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 1

Much has happened in international financial services in thepast six months. Business confidence has improved as theeconomies of the world’s richest countries have recovered,most noticeably in Asia, North America and the UK. There are still weaknesses in the economies of continentalEurope, but the Organisation for Economic Co-operationand Development (OECD) is predicting real GDP growth inthe eurozone of 1.8 percent this year,and 2.5 percent in 2005.

Financial markets around the world got off to a good start in 2004, adding to the impressive gains of last year.“Improvements in global growth prospects and corporatefinances, coupled with a robust appetite for risk,underpinned increases in equity and credit prices,” says the Bank for International Settlements* (BIS) in its firstquarter review. “Not even further revelations of corporatemalfeasance seemed to unsettle investors.”

It would be hard to get more bullish than this, which is why merger and acquisition activity in the financial servicessector has started up in earnest after two years in thedoldrums. Much of this is confined to domestic markets,but we are seeing significant cross-border activity too, withbanks and insurers pursuing acquisitions in Europe and theUS. And there is intense activity in emerging markets,particularly in China which is drawing direct and indirectforeign investment into its banks and insurance companies.

Regulation:all risk and no reward?

*BIS Quarterly Review March 2004 © 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

Unfortunately, with all this renewed activity comes notjust the promise of reward, but the risk of failure. Marketrisk, credit risk, operational risk – you name them, allthese risks and many more loom larger on risk managers’radar screens when their companies are in expansionmode. And in an environment of change and heightenedrisk the regulators are monitoring the situation ever moreclosely to maintain the stability of the financial system,prevent financial crime and protect the interests ofcustomers.

Regulatory risk is on the increase…

So from a financial institution’s point of view, regulatoryrisk must be high on the risk agenda. Despite globalization,we still live in a very diverse world when it comes tofinancial services regulation. In some countries, intensiveregulation has been around a very long time, and althoughthe issues change and best practice evolves, the art ofcompliance is generally well developed. But in others,where regulations and regulators are much younger –especially in the area of dealing with customers asopposed to prudential and capital issues – even theconcept of a compliance function and what it should do is quite new.

This issue of frontiers in finance is designed to helpreaders in all regulatory environments – from the matureto the recently created – in understanding the issues thataffect them. Any firm that falls foul of the regulators facesnot only having to pay fines and compensation, it alsofaces major reputational damage.

2 KPMG’s frontiers in finance June 2004

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 3

In the US, we have seen very large fines and remedialactions imposed on major financial institutions for conflictsof interest between their research and investment bankingactivities, and on mutual fund companies for late trading andmarket timing abuses. In the UK, retail banks and insurerscontinue to be punished for mis-selling financial products toconsumers. And in various jurisdictions, institutions havebeen disciplined for failing to comply with anti-moneylaundering measures. There are countless other recentexamples of regulatory failure and regulator enforcementaction across the globe.

…but there are rewards

So regulatory risk has become, perhaps, the biggest risk of all. But it does not have to be a case of ‘all risk and noreward’. There are benefits to be had, if it is managedproperly.

If a bank achieves higher risk management standards under the new Basel Capital Accord, it will benefit fromlower capital requirements. If, as insurance regulationmoves to a more risk-based approach, an insurer handles its risk management issues effectively, it will become more capital efficient.

If firms consider their compliance arrangements asstrategically critical, there is great scope for benefits intechnology leverage, business and functional integration,resource optimization and cost reduction.

If, in dealing with consumers, retail financial servicesproviders take on the spirit and objectives of regulation, not just the letter of the law, there are great opportunities for reward from consumers with their continued custom and loyalty.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

And if groups set themselves, and demonstrably maintain,high standards of governance, customer treatment andcompliance, they are entitled to expect the ‘regulatorydividend’ of less onerous and intrusive supervision from theregulators. We believe that regulators should be seen to beproviding such an incentive more extensively.

Regulatory risk must be managed

That’s why we’re focusing on regulatory risk and reward inthis issue of frontiers in finance. We deal with a number ofthemes, but four in particular stand out.

The first is the increasing globalization of regulation. Thereis an increasing degree of coordination between nationalregulators on policy, supervision and enforcement matters.The ripple effect should not be underestimated. On theother hand, detailed rules still differ widely from country tocountry. Both phenomena create extra risk for global groups.

The second key theme is the regulators’ focus on effectivecorporate governance, the role of the board and especiallythe accountability of senior management, with regulatorsmaking it clear (in a variety of ways and with a variety ofpowers) that they will hold senior managers responsible forany significant regulatory failures in their organization.

The third theme is rising consumer protection. As Sir BrianPitman, Senior Adviser to Morgan Stanley, pointed out at a European retail banking conference recently, “caveatemptor, buyer beware, is steadily being eroded in most ofthe western world.” We are moving towards a principle of‘let the seller beware’, with the onus falling on personalfinancial services firms to ensure that customers buy theappropriate products.

4 KPMG’s frontiers in finance June 2004

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 5

The fourth is the convergence of regulation across differentfinancial sectors. There has been a trend, with notableexceptions, for countries to merge their various financialregulatory bodies into a single regulator. And although thereare still big differences in the way different sectors aresupervised, moves are being made in many countries toput all sectors on similar supervisory footings. Oneconsequence is that an issue or expectation arising in oneindustry sector is rapidly extended across all other sectors.

But, as with all types of risk, there is an upside as well as a downside. The essence of any type of business – andfinancial services is no exception – is that if regulatory risksare properly identified and managed, then the regulatoryenvironment can be turned to business advantage.

So regulation is definitely not ‘all risk and no reward’. The rewards are there to be taken. Financial servicesregulation is at different stages of development around theworld. Readers in countries where it is a relatively newconcept may want to learn more about what goodcompliance looks like. Readers operating in jurisdictionswhere regulation has long been a fact of life may want tobenchmark themselves against best practices operating inother companies to ensure their regulatory riskmanagement is up to scratch. Either way, we hope you findthis issue of frontiers in finance useful.

Brendan Nelson, KPMG LLP (UK)Global Chairman, KPMG’s Financial Services practice

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

For multinational financial services firms, regulations worldwide are everincreasing; regulators are becomingmore aggressive and compliance risksare growing. Regulatory standards aregetting tougher. But standards aregetting tougher in different ways indifferent jurisdictions. Regulatoryenvironments around the world remaindisparate and often contradictory, evenas they become more stringent. Thisposes a serious challenge for globalorganizations – particularly theircentral/head office risk and complianceoversight arrangements.

Of the largest international financial sectorregulatory and control failures of the last10 years, a very high proportion derivedfrom operations away from the group’shome-country and center of risk control. In many cases, these failures were injurisdictions where the group’s operationswere not particularly significant.

As businesses become decentralized intheir management structures, in manycases relying on a complex matrixmanagement configurationencompassing a mixture of line ofbusiness, geographical and legal entityreporting structures, the challenge of

obtaining sufficient assurance atgroup/head office level that globalregulatory risks are well understood andmanaged has greatly increased.

Successfully meeting this challengerequires unprecedented rigor in corporategovernance, group risk management,and regulatory compliance arrangements.

A shrinking worldRegulators are talking on many levels:

• Multilaterally through internationalsupervisory bodies, such as the BaselCommittee, the InternationalOrganization of Securities Commissions(IOSCO) and the InternationalAssociation of Insurance Supervisors(IAIS), as well as the cross-sectorcoordination efforts of the Joint Forum.

• On the regional level, e.g. in Europewhere the focus of the European Union(EU) and Committee of EuropeanSecurities Regulators (CESR) is nowexpected to move rapidly from policy to implementation/enforcement;

• And, most significantly for individualgroups, bilaterally: home-countryregulators are increasingly talking invery specific terms to the host countryregulators across the world of their

supervised groups. For example, theJapanese Financial Services Authority(FSA) holds regular bilateral meetingswith the UK’s FSA, the US FederalReserve (Fed) and Office of theComptroller of the Currency (OCC), and Germany’s Bundesanstalt fürFinanzdienstleistungsaufsicht (BaFin).So, for example, a compliance problemin a small Japanese subsidiary of aglobal organization can come to theattention of a home-country regulatorand rapidly become a big issue. Indeed,emerging issues such as the Basel IICapital Accord and increased financialsector reliance on cross-borderoutsourcing arrangements, will provideeven greater impetus to home-countryregulators to coordinate more closelywith their host country counterparts inthe future.

It has become critically important,therefore, for group senior managementand compliance and control functions tounderstand, for every jurisdiction wherethe group does business, both thecharacter of the current regulatory regimeand the trends in regulation that affectthat regime; and how their own operation’sbusiness, governance and risk profilemap against that external assessment.

6 KPMG’s frontiers in finance June 2004

Expanding regulatoryhorizons

Regulatory risks around the world are increasing and oftendifficult to track. Unless your regulatory risk managementoperations are effective, you may not understand, let alonemanage, your growing risks nor maximize your emergingopportunities. By Hugh Kelly and John Somerville

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 7

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

Global challengesBut how do you protect your organizationeverywhere from risks that can ariseanywhere?

“These are big challenges,” SeanHughes, Group Head of Compliance for Australia’s international bankingorganization ANZ, tells KPMG. As a firststep, he emphasizes the importance offostering an understanding of thefundamental business benefits ofcompliance. “As complianceprofessionals, we want our people toown their compliance obligations. If theydon’t see the sound business reasonsfor complying with regulations, it’s hardfor them to be willing to expend theresources necessary to do so.”

Sound business reasons for rigorouscompliance operations include, ofcourse, the avoidance of regulatoryviolations and enforcement actions. But the benefits do not stop there. A proactive attention to compliance can, in fact, help you educate regulatorsabout the nature of your business andinfluence the development of theregulatory environment. Listed beloware strategies that can help you achieveboth sets of benefits.

Strategies for successAssume the aggressive trend

among regulators will continue

Regulators everywhere must be seen as tough and effective to meet theexpectations of their stakeholders – and, fundamentally, to fulfill their raisond’être. The publicity of a successfulenforcement action can be helpful tothem, both in demonstrating theireffectiveness and in conveying adeterrent message. Groups which are‘tall poppies’ in local markets may beespecially at risk. Such awareness shouldbe built into your business risk profiles.

Know your regulators

Leading groups are proactive. Seniorhead office representatives meet oftenwith local regulators. They activelyparticipate in local industry policydevelopment and debate, inputting toregulators during development of

regulations, rather than reactingnegatively once new regulations areissued.

Global groups can also benefit fromhelping to inform local regulators –particularly in emerging regulatoryjurisdictions – about industrydevelopments in other financial centers.For example, a multinational insurancefirm recently helped Japanese regulators become more open to trendselsewhere by creating a joint effort tostudy how other insurance marketswere deregulated.

Let your regulators get to know you

This will help regulators understand your business. In some large banks inGermany, for example, regulators areinvited to sit in on meetings of thesupervisory board. In the US, the OCCand the Fed have resident examinerspermanently located in large banks inorder to facilitate real-timecommunication with bank managementand quicker follow-up on issues andrisks. And in Japan, dialogue betweenregulators and firms’ internal audit stafffrom head office has improved as theJapanese FSA shared its perceptions of the local operations’ risks and theirregulatory concerns.

Know your business thoroughly,

including your weak spots

Companies may know their own localregulatory environments well, but theycan sometimes overlook those ofoverseas countries where they are eithernew or only small players. Issues may notget onto their ‘radar screen’ due to therelative size of the local operations. Forexample, in Australia, some foreign bankswith large home-country operations hadnot considered the possible impact of

Australia’s new licensing regime. As aconsequence, some have been very latein turning their attention to the issue. It isnow too late to take action, and they arefacing a risk of either operating without a license with attendant threat of finesand reputational damage; or having towithdraw temporarily from the relevantbusiness.

Assess the effectiveness/sufficiency

of your global and regional

compliance oversight functions

Are you able to track standards ofcompliance and emerging risks in all the countries where you operate?Regulators are increasingly scrutinizinggroups’ oversight of overseas operationsand examining the adequacy of theircentral controls. What resources do youdevote to this? How well structured isthe process? How much is it based onon-site challenge to the overseasoperations and how much reliance isplaced on self-assessment stylereporting? What is the quality of groupreporting of global compliance risks (aswell as issues that have already arisen)to the group board/audit committee?

Challenge whether you have the right

balance between global standards and

local compliance procedures

For example, some organizations take theregulation providing the highest standard(from among all of the countries in whichthey operate) and apply this standardacross all jurisdictions. While this resultsin‘over-complying’, some groups considerit to be a more effective and manageablepractice than applying and trackingmultiple rules in multiple jurisdictions. But, they cannot apply this rule withoutflexibility. So, if in a particular jurisdiction itmakes good commercial sense to adopt a lesser standard or rule in line with localrequirements, then this should beconsidered.

Other groups adopt a limited number of high level group compliancestandards/principles with which all theirglobal operations must comply and thenoverlay the detailed local requirements in each jurisdiction.

8 KPMG’s frontiers in finance June 2004

A proactive attention tocompliance can, in fact,help you educate regulatorsabout the nature of yourbusiness and influence the development of theregulatory environment.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 9

Whichever approach is adopted, localoperations may complain that they cannotcompete effectively when they aresubject to more onerous requirementsthan their local competitors. That’s whenthe tough decisions have to be madearound the different pulls of risk,reputation and profitability.

Compliance awareness and

accountability must be integrated

in core business operations

In some countries with less developedlocal regulatory environments, this iseasier said than done. But, unless localbusiness management heads are boughtinto the need to adhere to high standardsof conduct and group complianceprinciples, and take ownership ofcompliance themselves, the effectivenessof local compliance functions will beseverely constrained. Group/head officemanagement have an important role toplay in setting the right expectations in thisarea of subsidiary/divisional management.

Good communication is essential

Ensure efficient compliance and issuesreporting, particularly withincommunication channels betweenheadquarters and all subsidiaries. Mostorganizations have found the need tocombine regular written status reportswith mechanisms to encourage lessformal and more immediate dialogue,e.g. regular and ad hoc telephonecontact. Information once thoughtincidental, such as a risk managementissue within a small subsidiary, must beable to reach the attention of seniormanagement quickly.

Again, Sean Hughes at ANZ emphasizesthe importance of communication aboutcompliance. “We operate on a ‘nosurprises’ basis,” he says, “whichmeans bad news within the organizationreaches senior management, who, along with me, present discoveries of compliance failures to regulators. We don’t wait for them to discover ourmistakes”. Most organizations aspire to the same, but achievement of thisrequires exceptionally strong andeffective lines of communication andmeasures to mitigate a ‘blame culture’.

Know your competitors

Monitor other firms’ issues withregulators and assess the extent towhich you share their exposedweaknesses. Don’t assume theirtroubles cannot become yours.

Benefits of a global complianceapproachAmong the benefits of fostering aneffective global compliance approach in these ways are:

Reputation protection: Top of the list –a ‘must have’ – for financial sector CEOs. The cost of poor regulatory riskmanagement can be very significant interms of reputational loss in localmarkets as well as globally.

Promotion of your global brand: Theeffective implementation of globalcompliance standards will make it easierfor you to create and meet commoncustomer expectations worldwide,particularly around the core values ofintegrity and fair dealing.

More efficient operations: As well assynergies in compliance processes,businesses that communicate wellacross national boundaries on risk andcompliance issues tend to learn morequickly and effectively about what workswell and can be shared (e.g. use oftechnology in compliance managementand surveillance).

The exponential growth of financialservices regulation, its disparate detailand the increasing aggressiveness ofmany country regulators all highlight anarea of increasing reputational risk toglobal financial services groups.Management of this risk requireseffective compliance structures,excellent communication, clear commonstandards and active regulatorrelationship management. Head officeregulators are increasingly challenginggroups’ governance in this area andefforts to ensure such challenges can beeffectively answered are likely to behandsomely repaid.

➜ CEO discussion points

➜ How good is our understanding ofthe regulatory environments andtrends in all the jurisdictions in whichwe operate?

➜ How well do we evaluate ourstandards of compliancearrangements in all of thosecountries?

➜ How well are our global and regionalcompliance oversight structuresdesigned and resourced?

➜ What is the quality and depth of ourdialogue with regulators in eachjurisdiction?

➜ How quickly are potentialcompliance concerns, wherever they arise in the world, notified andescalated to group compliance andgroup management, and is it quicklyenough to enable effective pre-emptive action to be taken?

Hugh C Kelly

Director, KPMG LLP (US)KPMG’s Regulatory Risk Advisory ServicespracticeTel: +1 (202) 533 5200Fax: +1 (202) 533 8528e-Mail: [email protected]

John Somerville

Partner, KPMG in AustraliaHead of KPMG’s Financial Risk Managementand Regulation and Compliance practicesTel: +61 (3) 9288 5074Fax: +61 (3) 9288 5977e-Mail: [email protected]

For more information please contact:

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

10 KPMG’s frontiers in finance June 2004

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 11

Some of the most celebrated recentscandals are cases of fraud or outrightmis-management. It is notable that theworst cases are not in the financialservices world, however, there areenough examples of regulatory andcompliance failures to make this aspecial area of focus. Just think ofmutual fund practices in the US, andpension and mortgage endowment mis-selling in the UK. And think also of the reputational impact on the firms involved in these scandals.

How are businesses responding?In all these cases the authorities areholding business leaders to account – in the most serious cases through thecriminal courts – for regulatory failures.How are successful business leadersresponding to this challenge? Through a focus on corporate governance with a combination of:

• Setting out a clear vision for theorganization, with clarity around valuesand desired culture.

• Recognition that primary responsibilityfor regulatory risk management restswith the board and seniormanagement.

• Clear accountabilities, delegatedauthorities, objectives and performancemanagement and reward.

• Unequivocal business standards andexpectations of behavior.

• Risk management and oversight.• Independent internal audit.• A function that advises on and monitors

regulatory risks and standards ofcompliance.

An increasingly vital element of theresponse of businesses is this lastdevelopment: a function whose purposeis to help businesses manage regulatoryrisks and compliance. This articleexplores how the function is developingand evolving in different parts of theworld, and some of the essentialingredients for success.

As a reader, your response to thechallenges set out in this article will varydepending on the jurisdictions in whichyou operate. Those sitting in Australia,the US and the UK, for example, whichare more mature markets in terms ofregulation, may welcome the opportunityto go back to basics, to stand back fromthe day-to-day challenges of heavilyregulated markets and ask: what is our

The art of compliance

Amid the constant ramping up of expectations by the public,by government, by consumers and by regulators, and thespate of corporate scandals over the last few years, those whorun financial services organizations are asking “Are we doingeverything we should be doing to prevent a problem blowingup in our face?”. By Pamela Hauser and Marcus Sephton

compliance function trying to achieve,and what progress have we madetowards that objective? Those in othercountries may be asking themselvesdifferent questions – where do we beginin developing a compliance function andwhy do we need one anyway? Surely ourlegal/internal audit/risk functions coverour regulatory responsibilities?

This very fact illustrates one of thegreatest challenges for multinationalgroups – how to establish compliancefunctions and a compliance frameworkwhich are capable of providing anexecutive and board with appropriateinformation to assess the level ofregulatory risk within a group, when‘compliance’ means different things indifferent jurisdictions and the skill basefor conducting the work varies so widelyaround the world.

The changing face of complianceand regulatory risk management‘Compliance’ is a term that has beenaround for some time in many countries,but it is often used without consistencyor consensus as to its meaning and oftenwithout too much thought. ‘Compliance’– and the associated scope of the

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

12 KPMG’s frontiers in finance June 2004

compliance function – can thereforemean many different things to differentorganizations. For some, that scopeembraces all or many of the laws andrules that the business faces, includingfinancial services regulations, dataprotection, disclosure requirements, etc.For others, the scope can be limited toelements of the rules of the financialservices regulator(s), including:

• How the business conducts its affairswith customers and other externalparties.

• How the business manages its owncapital.

• The effectiveness of internal systemsand controls.

• Corporate governance and seniormanagement responsibilities.

These variations in the scope of thecompliance function are largely due tothe fact that the need for such a functionhas emerged as regulatory regimes havedeveloped, and the scope and role of thefunction is often shaped by the regulatoryfocus in that regime.

In the US, for example, the in-housefunction has had a long history, initially in the areas of anti-trust laws, highlyregulated industries such as financialservices, and activities involving risk topersonal safety or the environment. Oftenthis function has been staffed by lawyersand has tended to focus on technicalaspects of interpretation of the rules.

Outside of the US, in the UK andAustralia, the breadth of regulation haschanged to cover not just prudentialrequirements but also the manner inwhich products are sold, theresponsibilities of senior managementand the effectiveness of controls.Compliance functions have thereforebecome business consultants, whoadvise the business across a whole rangeof activities which may be impacted byregulation. This requires a completelydifferent mind – and skill – set.

This more active role is also illustrated bythe way in which compliance functions inmore highly regulated jurisdictions

monitor the extent to which theircompanies are complying with the rules– a responsibility which is recognized inthe October 2003 Basel consultativedocument, “The compliance function inbanks.”

In summary , taking a broad view ofcompliance functions around the world,what we can say is that:

• Whatever the jurisdiction, there isincreasing acceptance among financialorganizations of the need for aspecialist function that assists thoseorganizations in understanding how tocomply with a defined set of rules andregulations. For each organization thatset of rules might be different; thecrucial thing is to be clear about thescope of the function.

• But this does not mean that thecompliance function is responsible for‘ensuring’compliance with the rules –there is widespread recognition amongregulators that the burden ofmaintaining adequate controls to meetregulatory requirements rests squarelywith management. At the same time,regulators themselves recognize thevalue of a separate and independentcompliance function that supportssenior management in relation to theirregulatory responsibilities, monitorsstandards of compliance within thebusiness and alerts seniormanagement to key regulatory risks. In the absence of such a function,regulators understand that there is avery real risk that those at the top oforganizations will be unaware of thestandards of compliance within theirorganizations.

So, the need for a compliance function is accepted. But in regulatory circles the talk now is not just of compliance – a simple ‘meeting the letter of theregulations’ approach – but also of‘regulatory risk management’, sinceregulators and financial services groupsin many countries are increasingly seeingcompliance with regulations as anotherarea of risk to be managed – indeed as asubset of operational risk.

Unlike other forms of risk management,there is less scope to live with or takesteps to mitigate regulatory risk; ascompliance with the law and regulationsis not optional. Where responsibility forregulatory risk management lies withinorganizations varies significantly. Insome countries the move is towardsdeveloping compliance functions thatcan take on this new and moredemanding role.

A clear sign of this change in thinking is evident in both the UK and Australia,where the function now commonlyreports through to the Head of Risk andis positioned internally to work closelywith the operational risk team. This isopposed to the strong trend in the USwhere the function typically reportsthrough to the Head of Legal.

So what is the role of a compliancefunction and what can and should itachieve?

Different places, differentchallengesWhen establishing compliance functionsthere is no ‘one size fits all’ solution. Theresponse will vary according to therelevant jurisdictions. Some things,however, are clear:

• The role of the function must be clearlydefined with measurable objectivesagainst which its progress can bemonitored and assessed. In simpleterms this means considering theextent to which the compliancefunction will take responsibility for:– educating and briefing the business

on the regulatory requirements whichimpact upon it;

When establishingcompliance functions there is no‘one size fits all’solution. The response will vary according to therelevant jurisdictions.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 13

– assisting the business to develop itsown controls and associatedprocedures;

– monitoring the effectiveness of thosecontrols, reporting on the results anddefining remedial action to addressweaknesses identified;

– tracking regulatory developments and maintaining good relationshipswith regulators.

• The compliance function must beindependent. Successful compliancefunctions within groups often have tworeporting lines – one to the CEO of therelevant business unit and one to theHead of Group Compliance whoreports in to the parent company.

• The compliance team must have theright skill set. In countries where theconcept of a compliance function isnew, these skills are often drawn fromlegal and internal audit departments.What is vital is that the compliancefunction understands not just theregulations but also the business –indeed the markets – in which anorganization operates and can providepractical solutions to regulatorychallenges that do not involveexcessive or disproportionate costs,where this is avoidable.

The forces that are shaping the functionDespite all we have said about thedifferences in compliance functionsaround the world, there are a number of forces at work that are pushing in the same direction:

• The convergence of regulators’thinking: Regulators increasingly agreeon the need for a compliance function.However, in many countries thisconcept is a new one, not just fororganizations but also for regulators, soexpectations for the function will vary.

• The impact of Basel: The Baselconsultative document was issued aspart of the ongoing efforts of the BaselCommittee to address banksupervisory issues and enhance soundpractices in banking organizationsaround the world. The documentprovides basic guidance for banks and

sets out banking supervisors’ views oncompliance in banking organizations,although it acknowledges the differingregulatory environments and approachesto compliance functions that exist fromjurisdiction to jurisdiction.

• Cost effectiveness and businessbenefit: All businesses, wherever theyare located, operate under costconstraints and these apply as much to compliance functions as to any otherpart of an organization’s operations. In fact, some might argue that the costpressures are greater on a functionwhich is often seen as an expensiveoverhead, rather than a vital part of therisk management framework.

The concern among senior executivesis that the compliance function thatthey establish will grow exponentially,as it addresses the need to monitor thebusiness. This is not necessarily so: incountries where compliance functionshave matured over time, experiencehas shown that the key to success isnot to employ armies of compliancemonitors but rather to ensure that thereis a partnership approach between thebusiness and compliance oversight,that key risk areas within the businessare identified and that resources aretargeted appropriately. Also, with theefficient use of technology, for exampleto assist in the collation of managementinformation, some financial servicesorganizations are finding that theircompliance function has grown smallerover time as they learn the art ofcompliance.

As regulators’ thinking on compliancefunctions converges, and as businessesbecome more complex in terms of thenature of their activities and thecountries in which they operate, theneed for an effective compliancefunction becomes ever greater. Thatfunction will evolve over time – as itdoes, it can develop its role and take onmore active oversight of the business.The end game must be that thecompliance function becomes anessential part of the risk managementuniverse.

➜ CEO discussion points

New compliance functions

➜ Have you established a compliancefunction for all of your operations?

➜ If not, what objectives do you havefor your compliance function?

➜ Where can you find the necessaryskills for this function?

➜ How will you maintain theindependence of the function?

For those where the function

is already set up

➜ How does your compliance functionmatch up to its original objectives?

➜ To what extent is that functionactively helping you to manageregulatory risks?

➜ How do you measure the cost ofcompliance and how is this beingmanaged for cost effectiveness over time?

Pamela Hauser

Director, KPMG in AustraliaKPMG’s Regulation and Compliance practiceTel: +61 (3) 9288 6074Fax: +61 (3) 9288 6666e-Mail: [email protected]

Marcus Sephton

Partner, KPMG LLP (UK)KPMG’s Regulatory Services practiceTel: +44 (0) 20 7311 5171Fax: +44 (0) 20 7311 5882e-Mail: [email protected]

For more information please contact:

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

14 KPMG’s frontiers in finance June 2004

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 15

Preparing for Basel II, and complyingwith Basel I‘s market risk requirements,has compelled many banks to investsubstantially in highly sophisticated riskmeasurement models and managementpractices to satisfy their regulators andhelp maintain their competitive positionin the marketplace.

Even those banks regarded assophisticated, however, have beendaunted by Basel II’s data and systems’requirements and their implementationcosts. At the same time, they have yet to see the effects of the enhancedtransparency expected to result fromincreased disclosures. As Basel IIcontinues to evolve, however, itsinfluence is extending beyond banking tochallenge the insurance sector with theprospect of a new approach to capitaladequacy that is risk-based and marketfocused.

Risky business The European Commission’s (EC)development of Solvency II is onesignificant indication that prudential

regulation within the insurance sector is moving inexorably towards a Basel II-type model – one in which internalmodels are used to establish capitalrequirements, and the risk managementframework adopted by the board andsenior management is scrutinized byboth regulatory authorities and themarket (see sidebar). However, theoutcome for Solvency II is by no meanscertain and there is still a lot ofnegotiating to be done.

Many international bodies are seeking to influence Solvency II: the InternationalAssociation of Insurance Supervisors(IAIS), for example, which represents150 jurisdictions and has a set of coreprinciples for insurance supervision, isexpected to be extensively involved inthe evolution of Solvency II. Moreover,countries including the Netherlands and the UK are anticipating its policies by developing their own risk-basedapproaches to insurance regulation. In the wake of these developments,insurance leaders worldwide havenumerous questions, including:

Capital adequacy:insurers play catch-upThe insurance sector has generally followed the lead of others with regard to risk management and capital adequacypractices. Change is coming, however, driven by regulators,the capital markets, and, increasingly, leading insurers thatrecognize the business benefits of a new regulatory model. By Tim Childs and Peter de Groot

• Why is a new approach appropriate forinsurance regulation?

• How are new risk-based approachesdeveloping, and what are their potentialimplications for insurers?

• What business benefits could offsetthe potential cost of compliance?

A Solvency I I snapshot

Like Basel II, Solvency II in theEuropean Union (EU) is expected totake a three-pillar approach to capitalrequirements, regulatory supervision,and market discipline. Its aims include:

• Enhanced policyholder protection.• Greater transparency, comparabilityand coherence.

• A methodology positioned to reflectrisks in individual companies and avoidunnecessary complexity.

• Avoidance of unnecessary capitalcosts.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

in this region for many years, butcountries including Singapore, Korea,and Hong Kong are beginning to focusmore on managing their capital, data, and shareholders’ expectations. They are looking to Australia, Europe, and the US for useful lessons.

A risk-based model offersinnumerable benefits…A fundamental business question forinsurers is: Are you charging enoughpremium to cover your risks and yourcapital costs? The argument is that if you can’t prove to shareholders that abusiness is profitable, you should not beunderwriting it. Being focused on risk,Solvency II can be expected to addressthose issues:

• A more transparent system will helpinsurers make decisions based oncapital needs; thus, business strategycan be aligned with the capital used in the business.

• Risk modeling can help you assesscapital needs more closely, identify andevaluate major risks, and determinecapital implications by risk category.

• Scenario analysis can enable a futurefocus, rather than past-period snapshotanalysis.

…but, the transition posesconsiderable practical difficulties The problem, of course, is that manyinsurance companies lack sufficient lossdata, and highly developed riskmanagement models, to make riskdecisions effectively. Taking risk isinsurers’ bread-and-butter, but,paradoxically, their own risk managementsystems have long been considered lessrobust than that of banks:

• Many insurers lack a sophisticatedmeans of evaluating exposures tolosses – the foundation of a capitalrequirements calculation. Or, they donot trust the data: if their modelsrecommend a GBP£600 premium, butthe market will bear only GBP£400,some may choose to maintain marketshare by charging the lower price – atactic that has resulted in some largebusiness losses.

Changing approaches to capital adequacy When the EC and its member statesinitiated the Solvency II project in 2000, a primary goal was to better align capitaladequacy requirements with the truerisks of insurance companies. The capitalmarkets will increasingly demandimproved transparency in the insurancecompanies in which they invest. To thatend, closer alignment between SolvencyII and the proposed InternationalFinancial Reporting Standards (IFRS) isexpected, which could pose significantthreats to Europe’s current fixed-ratiocapital adequacy model.

Moreover, in the wake of Basel II, the EUand other regulatory bodies also saw anincreasing need for a level playing fieldacross the financial sector globally aswell as an emerging trend towardconvergence of prudential rules fordifferent sectors.

Talking to KPMG, Paul Sharma, Head ofPrudential and Accounting Standards atthe UK’s Financial Services Authority(FSA), says “Basel is exerting indirectpressure on insurance regulators inEurope to move to a risk-basedapproach. Within single regulators, likethe FSA, there’s a lot of institutionalpressure that says, ‘we’ve got onereputation, one quality way of doingthings; it’s not acceptable to offer asecond-rate product when it comes toregulation in the insurance sector.’ Incountries with separate regulators, theinsurance regulators are recognizing theneed to ‘show that they’re able tomodernize without being merged’.”

Several market factors intrinsic to the insurance sector also play an important role in the drive forSolvency II: The presence of financialconglomerates (of banks and insurancecompanies), and regulators’ consolidatedsupervision of such entities, createsadditional pressure on regulators toimpose similar capital and accountingstandards across sectors.“If I were theleader of a conglomerate,” notesSharma, “why would I want strong riskmanagement in the banking (less risky)part of my business and less strong riskmanagement in the insurance (morerisky) part of my business?”

Cross-sectoral arbitrage – where risk is transferred from the banking sector to the insurance sector because lesscapital is required to support the risk,such as in the use of credit derivatives –is becoming increasingly prevalent andhas the potential to create increasinglylarge flows of capital from one sector to another.

High-profile failures of insurancecompanies in countries worldwideunderscore the need for regulators tocatch up with the market – and forinsurance companies to betterunderstand their risks.

Foreign investor expectations are alsoimportant factors in some Asiancountries. Growth has been the model

16 KPMG’s frontiers in finance June 2004

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 17

• Like banks, insurers struggle withdefining risk appetite (that is, what aremy major risks, how much risk am Iprepared to accept, am I taking enoughrisk?) and then building the answersinto a policy framework that drives therisk management of the business.Solvency II can be expected to focusminds on establishing a clearer linkbetween how much capital is used inunderwriting and how much is used to value that potential business.

• Banks have long relied on formalizedkey performance indicators andscorecards. Many insurers, on theother hand, have yet to differentiatetheir risks – insurance, market, credit,liquidity, operational – and to work outthe interactions between them.

• Many insurers are unable to quantifytheir exposures to individual re-insurerswithout significant manual interventionin systems that do not capture thatfundamental information.

These data inadequacies are formidable.Yet building the systems, and capturingthe necessary data, will demand sizableinvestments of time, energy, andfinancial resources. Many companieshave yet to be persuaded of the value ofthose investments.

Why are some insurersembracing a new model?Even among those US, Australian andAsian insurers that use risk-based capitaladequacy models, the goal of increasingmarket share has historically takenprecedence over improving profitability.But some senior leaders around theglobe are reconsidering their businesspriorities. What factors are driving thisshift?

Capital is expensive. Effective use ofcapital becomes increasingly importantin an environment in which insurers havelost money on their investments, and, as in Japan, face a negative spread. To secure lower-cost capital, and to meetshareholder expectations, insurers willface increasing pressure to demonstratehow they calculate both premiums andtheir risks.

Profitability is increasingly preferableto volume. Increased capital marketscrutiny means that competitors thatunder-price will find their ability to stay in the market severely limited.

Regulators worldwide are holdingsenior management to a higherstandard. A comprehensiveunderstanding of different risks and theirimpact is not common among insurers’senior management and boards.Information may be available internallybut may not be shared appropriately withthe most senior level of management – a situation that regulators will finduntenable in a post-Enron world.

What are the implications forinsurers?As Solvency II evolves, nationalregulators worldwide are moving towardrisk-based capital adequacy models in a variety of ways and at varying speeds.Insurers now need to consider theirstrategies for meeting the increasedregulatory burden to preserve, orenhance, their competitive position inthe market. They also need to considerhow to align systems and datamanagement strategies with parallelstandards such as IFRS. New resourceswill inevitably be needed.

Solvency II is more than a regulatoryissue. In fact, it is a business opportunityCEOs should use – not just respond to –as a means of improving their ownmanagement information systems andincreasing organizational awareness ofthe high costs of unknown risk.

➜ CEO discussion points

➜ Do I genuinely know my risk-adjusted return for variousbusinesses and products, or just my return?

➜ Do we have the data and systems to achieve internal models’ relianceand, if not, will we be at acompetitive disadvantage? What willit take to get the data and developthe needed risk managementsystems?

➜ Will our risk management frameworkwithstand scrutiny?

➜ Can we achieve capital savings andmore efficient capital allocationsthrough the adoption of more robustrisk measurement models?

Tim Childs

Senior Manager, KPMG LLP (UK)KPMG’s Financial Risk Management practiceTel: +44 (0) 20 7694 2040Fax: +44 (0) 20 7311 1489e-Mail: [email protected]

Peter de Groot

Partner, KPMG Business Advisory Services B.V. (The Netherlands)Head of KPMG’s Insurance Risk Managementpractice Tel: +31 (20) 656 7489Fax: +31 (20) 656 7966e-Mail: [email protected]

For more information please contact:

The problem, of course, is that many insurancecompanies lack sufficientloss data, and highlydeveloped risk managementmodels, to make riskdecisions effectively.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

In many countries, especially where the spirit of free enterprise is mostenthusiastically embraced andcompetition is fiercest, financial sectorregulators are asserting that prosperingorganizations are failing to meetcustomers’ needs. Indeed, regulatorsare intervening more deeply in howbusinesses go about marketing andselling to their customers. They may not have the same approach, or evenfocus on the same issues, but they are promoting an increasing level ofconsumer protection regulation.

How can global organizations takeaccount of this consumerist regulatorytrend in shaping their commercialstrategies and managing their regulatoryand reputational risks? And how shouldthis align with global branding and thedesire to achieve a consistent approachto the treatment of customers, whereverthey are located? To answer thesequestions, we need to reflect on thedynamics of the trend itself.

The trendRegulators’ growing assertiveness isdriven by:

• Information asymmetry: An increasinggap between the sophistication offinancial products and the financialliteracy of consumers, leading to a lackof confidence among regulators that

consumers understand the products orservices that they are buying; and

• Recent regulatory failures: A spate of high profile cases around the worldthat have led regulators to strengthenconsumer protection regulation.

While regulators around the world mayagree on the problem, their response toit is globally disparate. In some countriesthe focus is on product regulation, inothers on disclosure of financialinformation, and in still others on sellingpractices. In some countries, regulatorsare seeking to close the gap betweenproducts and consumers’ financialliteracy. In others, the view (and the law)is that it is not the regulator’s job toeducate consumers. And while regulatorshave introduced consumer protectionmeasures and pursued enforcementactions, many have also recognized aparadoxical effect. Well-publicizedregulatory action can create an unhelpfullevel of risk aversion in investors.

Indeed, critics of aggressive consumeristregulation argue that there is a large and developing risk: heavily regulatedjurisdictions will increasingly foster acompensation culture which will, in thelong run, hamper innovation andentrepreneurial behavior and increasecost. This risk is recognized by the UK’sFinancial Services Authority (FSA) where

18 KPMG’s frontiers in finance June 2004

Beware:consumersAs Adam Smith1 articulated over 200 years ago, a key justification for free enterprise capitalism is that organizations survive and prosper throughmeeting the needs of customers.By Douglas Hendersonand Sarah Willison

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 19

Anna Bradley, Head of Retail Themes,acknowledges to KPMG, “Competitionis fantastically important. In trulycompetitive markets, consumers do verywell. So, in addressing market failures,we have to be careful not to put shackleson firms and prevent them fromdeveloping innovations. It’s the first-stepfirms that will drive change in this arena.”

An overview of consumerprotection regulation in key jurisdictionsWhile the trend in prudential regulationhas clearly been one of internationalharmonization, there has been nocomparable unifying force in consumerregulation. This may well be becausevariations in product development andselling practices reflect the cultures of individual countries and the strengthof the consumer lobby. The challenge for multinational firms is to comply withthe accompanying regulatory variationswhile achieving consistency in customerexpectations.

Below are examples of key markets andtheir consumerist regulatory approach.

Europe

The European Commission’s FinancialServices Action Plan (FSAP) includesconsumer protection among thecornerstones of its design for a singlemarket in financial services by 2005, andmany directives address aspects of thesubject (e.g. the Investment Services,the Distance Marketing, and InsuranceMediation Directives). Nevertheless, theapproach and scope are very fragmented,and the philosophy of implementationbetween member states is very diverse.Some countries (e.g. the UK)unapologetically go far beyond theminimum directive requirements in theirconsumer regulation; others appear totake a very light-touch approach toimplementing or enforcing even theminimum requirements.

In the UK, the FSA’s current campaign of“Treating Customers Fairly” emphasizesthe responsibility of financial servicesfirms to incorporate a consumer-focusedapproach in the development ofbusiness strategy.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

In discussing the concept of “TreatingCustomers Fairly”, the FSA’s AnnaBradley says, “Financial institutions needto ask themselves whether or not theyhave properly integrated thinking about‘treating customers fairly’ into theircorporate strategy – not delegated it to a compliance department but takenresponsibility for it at a seniormanagement level.”

Bradley goes on to articulate the kind of measures which the FSA believesorganizations should have in place inorder to ensure that they treat theircustomers fairly, including:

• Processes to identify the long-termneeds (not just short-term appetite) of consumers for whom they aredesigning and distributing products.

• Approaches to advertising and saleswhich take account of the financialliteracy of customers.

• Stress-testing of product risks againstchanging economic scenarios.

Australia

Financial services reform has seen theintroduction of a new ‘single’ licensingregime, new rules at point of sale includingenhanced disclosure requirements andan attempt to raise the standard of advicegiven to retail customers generally withextensive new training requirements forthose providing ‘advice’.

Asia

Historically, very little consumeristregulation has existed in the region. So-called ‘know your client’ issues havebegun to emerge, and this has beenencouraged through the presence of the global players operating in the region.At the same time, Asian regulators arebecoming more protective of theconsumer and take the view thatvoluminous disclosures to the consumeraround, for example, illustrations ofinvestment return are not in practiceprotecting most consumers due tocomplexity.

Meeting the challengesRegulators and firms may agree with theprinciple of fair treatment of customers,but there is widespread debate abouthow best to put it into practice. The basictask for firms is to explore whether, andto what extent, their business operationsagree with regulators’ expectations ofcustomer treatment. We suggest thechallenge is at two levels.

The first is strategic, whereby firms mustensure that there is alignment ofcommercial and regulatory objectives.When deciding what products to offerthrough which distribution channels, i.e.in developing their commercial strategy,organizations must take into account thelong-term needs of their customers. Inother words, firms must considerwhether their strategy is designed tocontribute to meeting their customers’needs, rather than just their own short-term profitability. As Bradley says, “Thefirst thing I would ask CEOs is whether ornot they can put their hands on theirhearts and say that they, as a firm, aretreating their customers fairly.” Apreliminary step in this process is toengage with regulators, to convince

20 KPMG’s frontiers in finance June 2004

• Stress-testing of risks to the firm itselffrom its retail strategy, includingcustomer types/segments, producttypes,sales and distribution methodsetc.

United States

In the US, the focus is shifting frommandatory disclosure of financialinformation to measures to protect theconsumer against what regulators deemabusive practices. Historically in the US,caveat emptor has been the guidingprinciple, with regulations focusing onfull disclosure. Sales practice regulationin the securities, investments andinsurance sectors and fair lendingregulation in the banking sector havelong been in evidence. But the much-publicized prosecutions by New YorkAttorney General Elliot Spitzer havebrought a fresh regulatory prominence tothe fair treatment of customers andmeasures to combat abuses. Thischanging focus may encourage theadoption of more principles-basedstrategies among firms.

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

KPMG’s frontiers in finance June 2004 21

them that consumer needs are beingconsidered at the strategic level.

The second challenge is at the level ofbusiness control and execution. This istougher. Here the managementchallenge is to embed in the organizationa customer-led culture by incentivisingthe right behaviors in staff; and todevelop customer- and quality-orientatedmanagement information which can giveearly warning of customer neglect andnon-compliant behavior.

Here an essential step is to developsubstantive compliance controls, toenable compliance not just with theletter but also with the spirit ofregulation. In meeting disclosureregulations, for example, firms havebeen able to develop processes thatprovide customers with essentialinformation without antagonizing themwith an unnecessary cascade of paper.

Another step is the development ofsystems to monitor all the disparateconsumer regulations governing a firm’soperations in every location and all thecompliance processes embedded in the business to meet them. Becauseregulators almost everywhere aregetting more aggressive, thereputational risk is huge.

Among the dangers formultinationals attempting tomeet these challenges, two are key:

• Failure to comprehend the scope of regulatory requirements in everyjurisdiction where you operate.Overseas companies entering newmarkets frequently make the error oftransporting successful products orselling practices from another marketwithout properly assessing the impactof the new regulatory regime on thoseproducts or practices.

• Failure to understand who yourcustomers are, including their levelof financial literacy and their range of needs. At present, regulators assertthat an in-depth understanding of the

dynamics of consumer needs andbehaviors is lacking in the industry.There is developing agreement amongregulators and firms that consumersmust learn to be responsible for theirown financial decisions, but that theindustry must help them get there.

The really enlightened – and successful –business will be one that can integratecompliance in its operations and by doingso meet the rising challenges withoutcommitting the above mistakes.

Consistency of approachA complementary aim for multinationalsis to have their global brands associatedwith consistent customer expectationsaround the world. Customers flying fromSan Francisco to Singapore expect toreceive the same level of service in bothplaces, and when they do, their trust andloyalty are strengthened. Sharingexperience of good practice in differentjurisdictions can help multinationalsdefine global compliance standards,meet regulatory requirements in eachjurisdiction and achieve consistency incustomer expectation and satisfaction.

In summary, then, regulators arebecoming more assertive in theirprotection of consumers, although theyare approaching their objective in widelydifferent ways. Multinational firms mustmeet this challenge at two levels – thestrategic and the operational. Failure todo either can expose them to significantregulatory and reputational risk. Inaddition to the risks, however, there aresignificant business opportunities. Byadopting a consumer-driven approachmultinational firms can begin to establishglobal compliance standards and achieveconsistency of service for theircustomers around the world.

For more information please contact:

1 “An Inquiry into the Nature and Causes of the Wealth ofNations”, 1776.

➜ CEO discussion points

➜ Are we having a meaningful dialoguewith our regulators on the matchbetween our business strategies andtheir expectations?

➜ How do we gain assurance that wehave understood the panoply ofrelevant consumer regulations in allthe countries where we do businessand have adequate awareness andcompliance processes to satisfythem?

➜ Are we stress-testing our productsand business models for thoseproducts to see if they are meetingour standards of consumer service?

➜ Do we have adequate systems andcontrols in place to understand thelong-term impact of our products onour customers?

Douglas Henderson

Managing Director, KPMG LLP (US)Head of KPMG’s Securities Segment of the USRegulatory Advisory Services practiceTel: +1 (212) 872 6687Fax: +1 (212) 954 7251e-Mail: [email protected]

Sarah Willison

Senior Manager, KPMG LLP (UK)KPMG’s Regulatory Services practiceTel: +44 (0) 20 7694 2206Fax: +44 (0) 20 7311 5861e-Mail: [email protected]

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

22 KPMG’s frontiers in finance June 2004

© 2004 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

on financial institutions, as the criminalsneed to bank and invest their ill-gottengains. More specifically financial crimewill impact financial institutions in avariety of ways:

Money laundering

• The United Nations Office of DrugControl and Prevention estimates thatUS$500 billion to US$1 trillion in fundsis laundered worldwide annually bydrug dealers, arms traffickers, terroristsand other criminals4.

• US federal law enforcement agenciesseized more than US$300 million incriminal assets that were attributable tomoney laundering in fiscal year 20015.

The terrorist threat

• ATM and credit-card fraud by organizedcriminals and terrorist cells is on therise, as well as soaring levels of identityfraud, which compound the globalproblem.

Credit risk

Levels of corporate fraud have continuedto rise in recent years:

• KPMG’s LLP (US) 2003 Fraud Surveyindicated that 75 percent of the 459listed companies surveyed reportedthat they have experienced an instanceof fraud6.

Financial institutions face increasingthreats from a wide range of financialcriminals. Globalization, increasing politicalpressure, economic conditions, and thesophistication of information technologyare among the factors that are helping tocreate an environment in which fraudstersand money launderers can prosper.

The problemFraud increasingly poses a threat tosociety as a whole – and the scale of the problem is growing exponentially:• The UK’s Home Office estimates fraud

in 2003 to have cost approximatelyGBP£14 billion1.

• The Hong Kong Police measured a 59 percent increase in fraud in the firstnine months of 2003. With a significantmigration to e-based transactions(estimated to rise in Hong Kong by3,500 percent from US$2 billion in 2000to US$70 billion by 2004), the HongKong Police anticipate increasedpotential for fraudulent activity2.

• The US-based Association of CertifiedFraud Examiners estimated that sixpercent of revenues would be lost in2002 as a result of occupational fraudand abuse, equalling US$600 billion ofUS GDP3.