Embed Size (px)

Citation preview

Fugro investor presentation

May 2018

www.fugro.com2

Cautionary statement

This presentation may contain forward-looking statements. Forward-looking statements are statements that are not historical facts, including (but not limited to) statements expressing or implying Fugro’sbeliefs, expectations, intentions, forecasts, estimates or predictions (and the assumptions underlying them). Forward-looking statements necessarily involve risks and uncertainties. The actual future results and situations may therefore differ materially from those expressed or implied in any forward-looking statements. Such differences may be caused by various factors including, but not limited to, developments in the oil and gas industry and related markets, currency risks and unexpected operational setbacks. Any forward-looking statements are based on information currently available to Fugro’smanagement. Fugro assumes no obligation to make a public announcement in each case where there are changes in information related to, or if there are otherwise changes or developments in respect of, the forward-looking statements in this presentation.

Investor presentation May 2018

www.fugro.com3

1. Company overview and strategy

2. Markets summary

3. Project examples

4. FY 2017 results

5. Outlook

Contents

Investor presentation May 2018

www.fugro.com4

Company overview and strategy

Investor presentation May 2018

www.fugro.com5

Fugro company overview

The world’s leading, independent provider of geo-intelligence and asset integrity solutions: Fugro acquires and analyses data on topography and the subsurface, soil composition, meteorological & environmental conditions, and provides related advice

With its services, Fugro supports the safe, efficient and sustainable development & operation of buildings, industrial facilities & infrastructure and the exploration & development of natural resources

Fugro works offshore and onshore, with around 10,000 people in 65 countries

Investor presentation May 2018

AcquisitionSpecialist data acquisition technology and services to investigate the Earth and assets

AnalyticsData management, processing, analysis, interpretation, visualisation and data hosting

AdviceCustomised consulting covering wide spectrum of geo-engineering and asset integrity

Revenue by market segment Business model

www.fugro.com6

Global trends drive demand for Fugro services

Over the coming decades, population growth, urbanisation and climate change will increase demand for energy, water, natural resources, buildings and infrastructure.Our purpose is to provide geo-intelligence and asset integrity solutions to contribute to meeting this demand and to create a safe and liveable world.

Investor presentation May 2018

www.fugro.com7

Essential data for sustainable construction and operation

Geo- and asset integrity data are essential for sustainable development and management of large constructions, infrastructure and natural resources. Fugro is one of the world’s largest inspection & consulting engineering companies collecting site information and providing advice to support building and infrastructure development.

Investor presentation May 2018

From conceptionto decommissioningOur clients needs smart, practical information.

Every step of the way, we provide them with geo-intelligence, to help ensure their assets a lifetime of excellent service.

Relevant, reliable, insightful information

www.fugro.com9

Marine and Land divisions organised in uniform business lines…

Since launch of Building on Strength strategy, Fugro has been transformed from a group of locally managed operating companies into an integrated organisation

Fugro now managed through 2 main divisions, Marine and Land, both offering integrated services to clients from uniform site characterisation and asset integrity business lines

Site characterisationDetermine ground andenvironmental conditionsof project sites

Asset integrityDetermine conditions of

existing constructionsand infrastructure

Operate & ManageBuildPlan & Design Decom-mission

Investor presentation May 2018

www.fugro.com10 Investor presentation May 2018

Client centric organisation

Has strengthened Fugro’s ability to effectively provide integrated, standardised solutions across the globe

Cost efficient organisation

Allows Fugro to capture further synergies by having all marine assets under central management structure; other assets regionally or globally pooled

Shared service centres in operation in largest hubs in USA, EU, Middle East, Asia and Australia

50 additional legal entities closed in 2017

Rationalisation of legal entity structure and implementation of shared service centres largely finalised in 2018

… resulting in more client centric and efficient organisation

www.fugro.com11

Organisational structure as of 2017

Innovation & Technology

Fugro NV

MarineLand Geoscience

5 regions

Site Characterisation

AssetIntegrity

Shared service centers for HR, finance, QHSSE, IT, legal

Seabed Geosolutions5 regions

Site Characterisation

AssetIntegrity

Investor presentation May 2018

www.fugro.com12

Clear market leadership in several market segments

Capability to deliver complete suite of services from data acquisition, analysis (processing, interpretation, visualisation and hosting) through to advice

Independent position, which assures clients of impartial data and advice

Vast expertise and experience of staff Local presence throughout the world, with 178

offices located in 59 countries Technology leadership through continuous

investment in R&D and innovation Capability to take on large integrated projects

and multi-year framework contracts Consistently delivering quality services safely,

meeting standards, on time and meeting or exceeding requirements

Multi-market exposure, creating resilience against market volatility

Market leading positions

Investor presentation May 2018

to offer unified support for large scale projects

Global network of offices andfacilities

10,000 employees169 offices16 R&D centres65 countries5 regions

Global network

Investor presentation May 2018

www.fugro.com14

68143 159 108

100

318 373 369 360

20101757

1172855

0

500

1000

1500

2000

2500

3000

FY14 FY15 FY16 FY17

6 4

36 9 7

712 16

21

24

78 7466

57

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 FY16 FY17

Increasing importance of non-oil and gas markets

+ 9%

- 25%

Revenue - % of total Revenue – EUR (x million)

* until 2017, renewables included in power, and nautical in building & infrastructure

oil & gas building & infra renewables * power nautical * mining other

Y-o-Ycurrency

comparablerevenue

growth

Investor presentation May 2018

www.fugro.com15

Fugro’s activities across life cycle of offshore oil and gas field

Decom-missioning

Exploration & appraisal

Development planning

Field development

Production & maintenance

Inspection, repair and maintenance services

Drill support

Ocean bottom seismicsurveys

Geophysical survey

Construction support

Monitoring and forecasting

Geoconsulting

Geotechnical investigation

Ocean bottomseismic surveys

Final investment decision

Positioning

Drill support

Construction support

Investor presentation May 2018

www.fugro.com16

Fugro’ s activities across life cycle of offshore wind farm

Decom-missioningSite appraisal Design &

contracting Construction Operation & maintenance

Inspection, repair and maintenance services

Geophysical survey

Monitoring and forecasting

Geoconsulting

Geotechnical investigation

Final investment decision

Positioning

Construction support

Construction support

Investor presentation May 2018

www.fugro.com17

Fugro’s activities across life cycle of building and infrastructure project

Testing and monitoring

Asset integrity services

Geoconsulting

Construction support

Investor presentation May 2018

Decom-missioningSite appraisal Design &

contracting Construction Operation & maintenance

Final investment decision

Drilling servicesCone penetration testingGeophysical surveys

www.fugro.com18

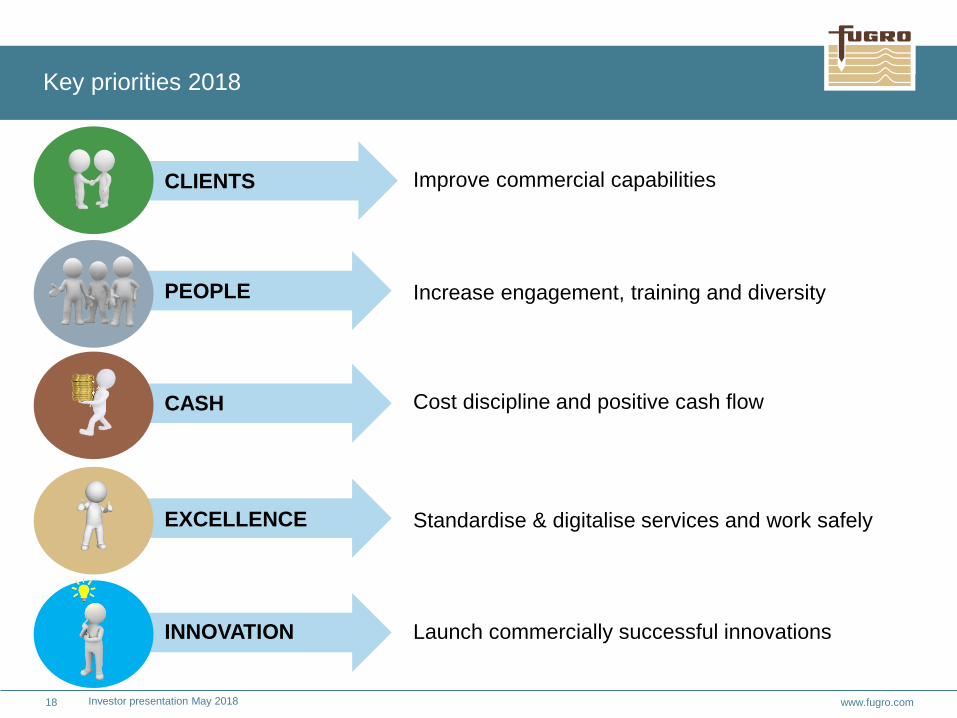

Improve commercial capabilities

Standardise & digitalise services and work safely

Launch commercially successful innovations

Increase engagement, training and diversity

Cost discipline and positive cash flow

CLIENTS

CASH

PEOPLE

EXCELLENCE

INNOVATION

Key priorities 2018

Investor presentation May 2018

We areFugroMarketsSummary

www.fugro.com20

+10% +1%

Key market developments 2018

World economy growth continues

Gradual but volatile increase in oil price expected

Offshore oilfield services market stabilising

Building & infrastructure investments growing

Offshore wind capital expenditure growing

Global growth Brent oil price

+15%

Offshore OFSexpenditure

Offshore wind capital expenditure

Metals & minerals price index

Buildings & Infrastructure expenditure

+4% -3%

+7%

Market forecast annual growth 2018

Investor presentation May 2018

www.fugro.com21

Global demand for energy growing

World economy continues to grow, impacting world energy demand

Demand for all energy sources expected to grow, except coal

Additional investments needed to meet energy demand growth

Source: IEA – World Energy Outlook 2017, 14 November 2017; IEA – World Energy Investment 2017, June 2017

2.3 3.0 3.7 3.8 3.8

3.74.0

4.1 4.3 4.52.1

2.42.7

2.9 3.2

0.7

0.7

0.70.7 0.8

1.3

1.4

1.61.9

2.2

10.0

11.5

12.913.6

14.3

0

20

40

60

80

100

0

3

6

9

12

15

2000 2005 2010 2015 2020e

GD

P: U

SD tr

illion

s

Ener

gy d

eman

d: th

ousa

nds

Mto

e

World energy demand and GDP

Coal OilGas NuclearRenewables World GDP output (RHS)

Investor presentation May 2018

www.fugro.com22

Offshore oil and gas competitive with shale

Large volumes of US shale oil available around US$ 55 / barrel

Shale is important factor for oil demand/supply balance as production can be developed in short time frame

Non-shale offers many lower cost opportunities but with higher upfront cost and longer lead times

Many oil companies continue to develop offshore opportunities

Source: Goldman Sachs – Top Projects 2017, 25 May 2017 Brent oil price as per 19 February 2018

Investor presentation May 2018

Cumulative peak oil production with range of breakeven for new developments

www.fugro.com23

317348 366

306244 218 206

0

100

200

300

400

500

600

2012 2013 2014 2015 2016 2017e 2018f

USD

billi

ons

Offshore OFS expenditures

Exploration Development Production Decommissioning

Onshore oilfield services growing, offshore stabilising

Onshore OFS expenditure growth driven by shale

Offshore OFS expenditure stabilising in 2018

Increase in sanctioned offshore FIDs in 2017 and 2018, expected to result in OFS growth from 2019 onwards

Source: Rystad Energy – UCube / DCube analysis, 19 February 2018

540577 598

452

351395 422

0

100

200

300

400

500

600

2012 2013 2014 2015 2016 2017e 2018f

USD

billi

ons

Onshore OFS expenditures

Conventional Shale Oil sands

18 306523 15

4370

68

40

115

176

0

50

100

150

200

2016 2017 2018e

USD

billi

ons

Sanctioned offshore FID capex

Subsea tie back Fixed Floater

Investor presentation May 2018

www.fugro.com24

1.7 1.8 1.8 1.8 1.9 2.0 2.1

2.7 2.7 2.7 2.3 2.3 2.4 2.6

3.23.6 3.9

3.8 3.94.1

4.4

0.60.7

0.70.7 0.7

0.70.7

8.48.9

9.38.8 8.9

9.410.1

0

2

4

6

8

10

12

2012 2013 2014 2015 2016 2017e 2018f

USD

trilli

ons

Buildings & Infrastructure construction expenditure by region

Americas Europe & Caspian Africa Asia-Pacific Middle East & India

Growth building & Infrastructure market

Source: Construction IC / Infrastructure IC – Custom data report, 15 February 2018

Investor presentation May 2018

www.fugro.com25

443573

159437

575375

592391

572 664

114

140

166

538

517

398

455

502417

527 575

299

608

1113

892990

852

11121195

0

200

400

600

800

1000

1200

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Annual offshore wind turbine foundations entering construction

Europe North America Asia

Growth in offshore wind farms

Main markets for offshore wind are North-West Europe and China, and are expected to grow

Fugro involved in first North American, Taiwanese and Indian offshore wind farms

Offshore wind farms getting larger in terms of generation capacity, turbines increasing in size

Source: 4C Offshore – Project Opportunity Pipeline, 2 February 2018

5 5 4 4 7 8 9 10 11 13

2

24

5 66

78

5 6 5 6

1014 15

1619

22

0

2

4

6

8

10

0

5

10

15

20

25

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

GW

EUR

billi

ons

Annual offshore wind capital expenditure vs. annual capacity entering construction

Europe North America Asia Capacity (Annual)

Investor presentation May 2018

www.fugro.com26

Increasing investment in power plants and infrastructure

Global power demand is growing strongly, resulting in increasing power plant and infrastructure investments

Nuclear dominates power generation projects pipeline

Growing investments in electricity networks, driven by need to integrate new renewables-based generation, improve system reliability and replace ageing assets

0

200

400

600

800

1000

1200

USD

billi

ons

Power generation projects pipeline up to 2025

154 151 162 147 143 153 159

101 112 114 110 106 112 121

311 348 365 360 396458

52397

98 103 103 106114

122677 726 764 738 768

856945

0

200

400

600

800

1000

2012 2013 2014 2015 2016 2017e 2018f

Electricity and power plants expenditure

Americas Europe & Caspian Africa Asia-Pacific Middle East & India

Source: Construction IC / Infrastructure IC – Custom data report, 15 February 2018

Investor presentation May 2018

Project examples

www.fugro.com28

Real time5,000 sensors

GeoRiskPortal so far been used in 70+ projects world wide

Safe realisation and operation of tunnel in urban area

Rotterdamsebaan tunnel, the Hague

Monitoring of buildings and surface during construction

One of the largest monitoring systems ever developed in the Netherlands

GeoRiskPortal® presents results inreal-time to client and contractors

Broad use of Fugro’s capabilities: acquisition, analytics and advice

Client benefits

During construction: real time assessment of risks, more rapid decision making

During operation: reduces maintenance costs, extends life time, detects failure risks

Investor presentation May 2018

www.fugro.com29

Optimisation of foundation design for one of world’s tallest buildings

OptimisationAnticipated height: 928 metres

36,300 tons: world record for deepfoundation testing load, applied on a single barrette

Dubai Creek Tower

Fugro performed one of the most comprehensive geotechnical site investigations ever in the region

Additional load testing of proposed foundations

Client benefits

During design & construction: optimised foundation design, reduced construction costs and risks

During operation: monitor behaviour of foundations through fibre optic sensing

Investor presentation May 2018

www.fugro.com30

3D solution for precise and safe installation of offshore wind farm

Efficient & Accurate

Successful installation of 344 piles on 86 locations

Using approximately 50 sensorson installation frame

Beatrice wind farm

Fugro supported installation by acquiring data with real time analysis in specialised decision support survey system

Allowing the client to install the piles precisely and efficiently, and to support smooth installation of the jackets

Client benefits

Cost and risk reduction of pile and jacket installation

Enhanced safety by remote monitoring of installation

Investor presentation May 2018

FY 2017 results

www.fugro.com32

FY 2017 results in line with expectations

Strong progress strategic agenda:

activities regrouped into Marine and Land division, with uniform business lines more client centric and efficient organisation divestment non-core marine construction and installation business growing in other markets

Measures to reduce costs and improve performance on track and mostly implemented

Oil and gas market stabilising after challenging 2017; growth in other markets

Results expected to improve in 2018

Key take-aways

Investor presentation May 2018

www.fugro.com33

Financial highlights FY 2017

FY 2017 resultsContinued revenue decline

Negative cash flow after investments

Q-o-Q backlog growth

Low single digit EBIT loss

EBIT margin (before exceptional items)

2017

-2.1%

2016

0.5%

1.9 x2.2 x

12-month backlog

2017

- 51

2016excl. proceedsasset disposals

75

1,776 1,497

Revenue growth corrected for currency effect; 2017 backlog corrected for currency effect and for portfolio changes related to marine construction and installation activities

2017

1,497

2016

1,776

Dec. 2016 Dec. 2017

1,170

Sept. 2017

867 928

*

-13.2%*-7.3% *

+9.1% *

Investor presentation May 2018

www.fugro.com34

Another difficult year due to double digit decline in offshore oil and gas

Investor presentation May 2018

Revenue (currency comparable) Declines of 11.3% in Marine, 3.0% in Land and 55.7% in Seabed GeosolutionsEBIT (margin) excluding exceptional items Low utilisation APAC, price pressure and incidental operational issues in Marine division Improved profitability in Land division Low activity level Seabed GeosolutionsCapital employed Reduced due to lower working capital, capex below D&A, impaired deferred tax assets and exchange rate differencesCash flow Cash generated from operating activities insufficient to support 2017 investment level

* Currency comparable * * NOPAT last 12 months (applying domestic weighted average tax rate); capital employed average of last three reporting periods

excl. proceedsasset disposals

Revenue EBIT (margin)excluding exceptional items

Capital employed ROCE **excluding exceptional items

Cash flow

1,184

2016

1,341

2017 2017

- 3.3%

2016

- 0.7%

1,497

2016

1,776

2017 2017

- 2.1%

2016

0.5%

2016

- 51

2017

75 X EUR million

- 32

9

- 13.2%*

www.fugro.com35

EBIT decline in Marine and Geoscience divisions, Land improved

Investor presentation May 2018

excl. exceptional itemsX EUR million

9

- 31

Geoscience

- 32

2017Land

15

Marine

- 25

2016

One

-off

oper

atio

nal

bene

fit 2

016

- 11

- 20

One

-off

oper

atio

nal

bene

fit 2

017

6

9

www.fugro.com36

Strong cost reductions, yet insufficient to offset revenue decline

Investor presentation May 2018

excl. exceptional itemsX EUR million

- 32

9

38

Depreciation + amorisation

EBITFY 2017

FX

2

Other income and expenses

45

Personnel expenses

50

Third party costs

59

Revenue

- 235EBIT

FY 2016

www.fugro.com37 Investor presentation May 2018

Finalisation active involvement in marine construction & installation business

cable laying and trenching business divested

early termination of long-term charters of the 2 remaining construction and installation vessels

Significant improvement in charter terms 2 IRM vessels

Retirement of 2 old vessels in Q4

Headcount reduction in 2017 by 486 employees to 10,044 at year-end

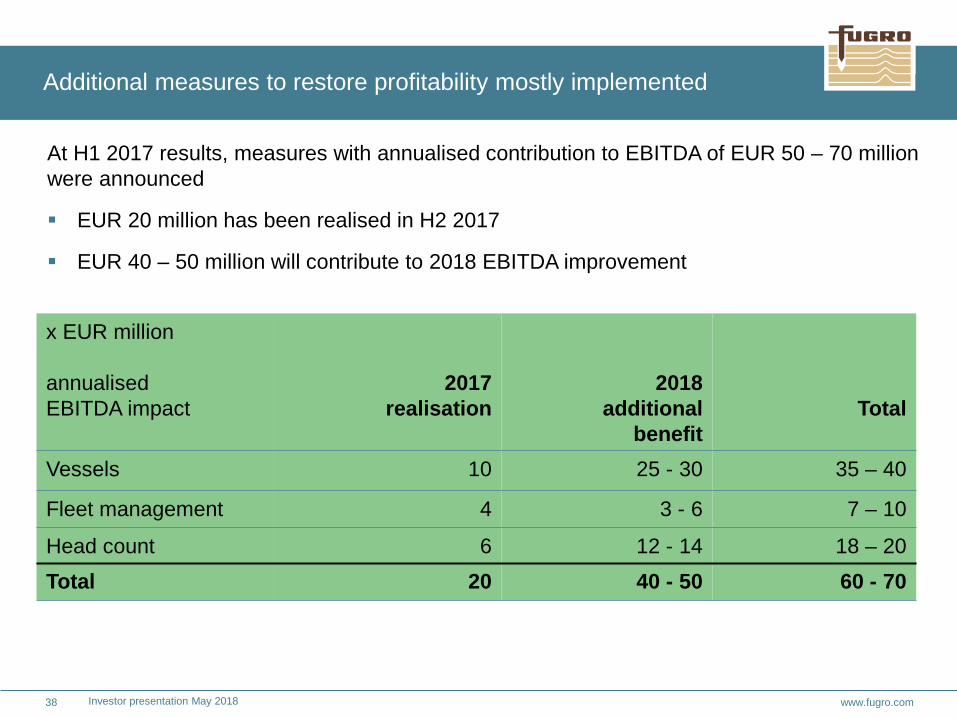

Measures to reduce costs mostly implemented

EUR 20 million of financial benefit realised in H2 2017, EUR 40 – 50 million will contribute to 2018 EBITDA improvement

www.fugro.com38

Additional measures to restore profitability mostly implemented

Investor presentation May 2018

x EUR million

annualisedEBITDA impact

2017 realisation

2018 additional

benefitTotal

Vessels 10 25 - 30 35 – 40

Fleet management 4 3 - 6 7 – 10

Head count 6 12 - 14 18 – 20Total 20 40 - 50 60 - 70

At H1 2017 results, measures with annualised contribution to EBITDA of EUR 50 – 70 million were announced

EUR 20 million has been realised in H2 2017

EUR 40 – 50 million will contribute to 2018 EBITDA improvement

www.fugro.com39

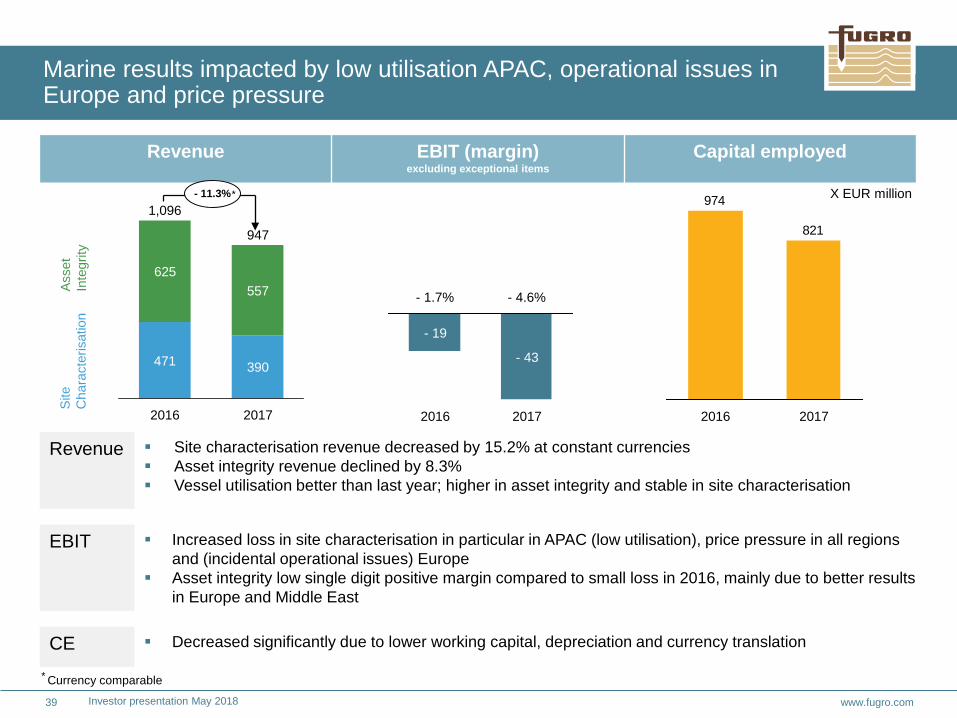

Marine results impacted by low utilisation APAC, operational issues in Europe and price pressure

Investor presentation May 2018

625557

390

2017

471

947

2016

1,096

- 19

2017

- 43

2016

821

974

20172016

- 1.7% - 4.6%

Revenue Site characterisation revenue decreased by 15.2% at constant currencies Asset integrity revenue declined by 8.3% Vessel utilisation better than last year; higher in asset integrity and stable in site characterisation

EBIT Increased loss in site characterisation in particular in APAC (low utilisation), price pressure in all regionsand (incidental operational issues) Europe

Asset integrity low single digit positive margin compared to small loss in 2016, mainly due to better results in Europe and Middle East

CE Decreased significantly due to lower working capital, depreciation and currency translation

Asse

t In

tegr

itySi

te

Cha

ract

eris

atio

n

Revenue EBIT (margin)excluding exceptional items

Capital employed

X EUR million - 11.3%*

* Currency comparable

www.fugro.com40

Improved profitability of Land division driven by growth in building & infrastructure and power

Investor presentation May 2018

7

15

2017

6

2016

219231

20172016

1.3%

4.5%

Revenue Strong decline oil and gas related revenue largely offset by growth other markets Site characterisation flat at constant currencies; higher revenue in Europe, Middle East and APAC offset

by finalisation large LNG projects in USA Asset integrity decreased by 12.5% as a consequence of reduced oil and gas infrastructure activity

EBIT Improvement reflects improved profitability in Middle East, Europe and APAC; reduced losses in Africa; and positive one-off operational effect of EUR 6.1 million

Site characterisation mid single digit EBIT margin, slightly better than prior year; asset integrity improved from high single digit loss to breakeven

CE Slight decrease due to improvement working capital

122 105

371385

2017

476

2016

507

One-off operationaleffect

*

* Currency comparable

Asse

t In

tegr

itySi

te

Cha

ract

eris

atio

n

Revenue EBIT (margin)excluding exceptional items

Capital employed

X EUR million - 3.0%*

www.fugro.com41

Seabed results impacted by low utilisation, despite good project performance

Investor presentation May 2018

173

74

740

1730

2017

-13.8%

1

2016

12.0%

11

4136

136

136

0

2017

145

9

2016

Revenue Seabed: Low utilisation, with only two crews active during 1HY and idleness from June to November

EBIT Seabed: despite exceptionally low utilisation, loss contained by robust operational project performance and further cost reductions

Seabed: Last years’ EBIT included positive one-off operational benefit of EUR 11.3 million, related to conversion of vessel charter into lease and purchase agreement

CE Seabed: higher working capital due to the later start of Lula project Other: includes EUR 22.5 million for indirect interests in Australian exploration projects, partly offset by

other provisions and payables* Currency comparable* * Indirect interests (via Finder Exploration) in Australian exploration projects

Seabed

Other * *

2016 2017

One-off operationaleffect

136

6

-11

*

Revenue EBIT (margin)excluding exceptional items

Capital employed

X EUR million - 55.7%*

www.fugro.com42

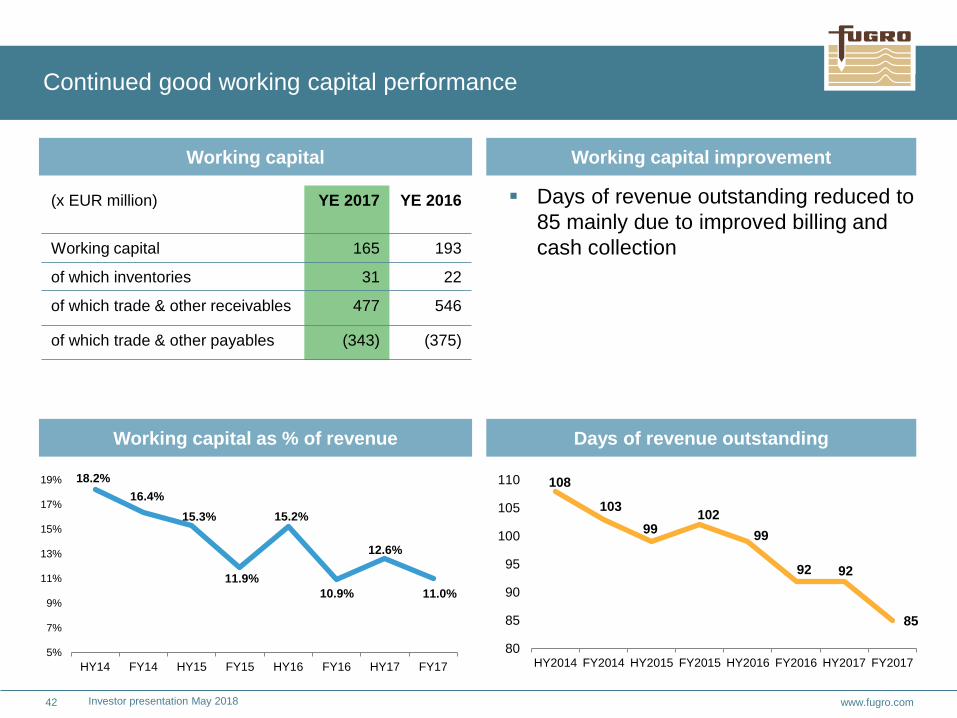

Continued good working capital performance

Investor presentation May 2018

18.2%16.4%

15.3%

11.9%

15.2%

10.9%

12.6%

11.0%

5%

7%

9%

11%

13%

15%

17%

19%

HY14 FY14 HY15 FY15 HY16 FY16 HY17 FY17

(x EUR million) YE 2017 YE 2016

Working capital 165 193

of which inventories 31 22

of which trade & other receivables 477 546

of which trade & other payables (343) (375)

Days of revenue outstanding reduced to 85 mainly due to improved billing and cash collection

Working capital improvement

Working capital as % of revenue Days of revenue outstanding

108

10399

10299

92 92

85

80

85

90

95

100

105

110

HY2014 FY2014 HY2015 FY2015 HY2016 FY2016 HY2017 FY2017

Working capital

www.fugro.com43

Well within covenants and good liquidity

Investor presentation May 2018

100

00

190

387

00

202320222021202020192018 2024

*

430427434351

467535734801

187

467

4q173Q17

267

2Q17

277

4Q16

198

2Q164Q152Q154Q14

Net debt (X EUR million)

Debt maturity per December 2017 (X millions, euro equivalents)

Net debtNet debt for covenant purposes*

* Will be lower than EUR 290 million when bond will be (partly) converted into equity

4Q16

2.4

3Q16

2.6

2Q16

2.5

4Q17

2.2

1Q16

2.8

4Q15

3.1

3Q15

2.9

2Q15

2.8

1Q15

3.1

4Q14

2.9

3Q17

1.9

2Q17

2.3

1Q17

2.3

1.6

3Q15

2.0

2Q15

2.0

1Q15

2.2

1Q17

1.3

4Q16

1.1

3Q16

1.8

2Q16

1.8

1Q16

1.7

4Q15 4Q17

1.9

3Q17

2.9

2Q17

2.2

4Q14

2.2

Net debt/EBITDA

Fixed charge cover

revolving credit facility

subordinated convertible

bond 2016

subordinated convertible

bond 2017

* Difference between net debt and net debt for covenant purposesrelates to debt component of convertible bonds

*≥ 1.8 covenant

≤ 3.0 covenant

Q1 2018 trading update & outlook

www.fugro.com45

First year-on-year revenue and backlog growth since 12 quarters

Offshore oil and gas market stabilising

Non-oil and gas markets, mostly building & infrastructure and offshore wind, continue to develop positively

Margin improvement still limited due to oversupply and consumption of down cycle backlog

Continued focus on price improvement, cost control and positive cash flow generation

Results 2018 expected to improve compared to 2017

Financial highlights Q1 2018

Investor presentation May 2018

www.fugro.com46

Backlog: first year-on-year increase after 12 quarters of decline

959 917 795 797 727 676 647 720 655 606 508 545

418 382334 371 368 335 343 357 341 299 280 274

588

272

213208233

1.05256

4Q16

1,17093

3Q16

1,05565

2Q16

1,06554

1Q16

1,17681

4Q15

1,323155

971

1,342

2Q15

1,507

1Q15

1,610

66 104

3Q17

867

2Q17

79

1Q17

964

1Q184Q17

109928

3Q15* Corrected for currency effect (of around – 9% year-on-year) and for portfolio changes related to divestment of marine construction & installation activities in 2017Marine Land Geoscience

7.7%*6.1%*

12 month backlog Comparable growth*

(x EUR million) 1Q17 4Q17 1Q18 Y-on-Y Q-on-Q

Site characterisation Marine 240 212 247 12.5% 18.5%

Asset integrity Marine 415 333 341 6.5% 4.4%

Marine 655 545 588 8.9% 9.9%

Site characterisation Land 270 203 204 (16.7%) 2.2%

Asset integrity Land 71 71 68 4.7% (0.9%)

Land 341 274 272 (12.2%) 1.4%

Geoscience (Seabed) 56 109 104 116.7% (0.9%)

Total 1,052 928 964 7.7% 6.1%

Investor presentation May 2018

www.fugro.com47

Outlook 2018

General market developments

stabilising oil and gas environment

continued growth in building & infrastructure and renewables markets

Fugro outlook 2018

revenue growth

improved EBIT margin

positive cash flow from operating activities after investments

capex of around EUR 80 million

Investor presentation May 2018

Questions?CONTACT CATRIEN VAN BUTTINGHA, DIRECTOR IR: [email protected]