Embed Size (px)

Citation preview

Funding an Indian business

Coinmen Consultants LLP www.coinmen.com Coinmen Consultants LLP www.coinmen.com

01 April 2021

Disclaimer

Coinmen Consultants LLP www.coinmen.com

The information contained in this document is of a general nature only. It is not meant to be comprehensive and does not constitute financial, legal, tax, or other professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. This document is not intended as an offer or solicitation for business to anyone in any jurisdiction; and is also is not intended for distribution to anyone located in or resident in jurisdictions which restrict the distribution of this document. It shall not be copied, reproduced, transmitted or further distributed by any recipient. Whilst every care has been taken in preparing this document, Coinmen Consultants LLP does not guarantee, represent, or warrant (express or implied) as to its accuracy or completeness, and under no circumstances will be liable for any loss caused by reliance on any opinion or statement made in this document. Except as specifically indicated, the expressions of opinion are those of the Coinmen Consultants LLP only and are subject to change without notice. This document is not a ‘Financial Promotion’. The materials contained in this publication were assembled in April 2021 and were based on the law enforceable and information available at that time.

This document has been developed to simply�provide a quick overview in simple terms of the manners or models under which a company could setup an establishment in India; and the tax and regulatory frameworks that could preside over such an entity.

Abbreviations AD Bank-1 Authorized Dealer Bank -1 AE Associated Enterprises ALP Arm’s Length Price AMT Alternate Minimum tax APA Advance Pricing Agreements BEPS Base Erosion Profit Shifting BO Branch Office BOD Board of Directors CBDT Central Board of Direct Taxes CFS Consolidated Financial statements DDT Dividend Distribution Tax DTAA Double Taxation Avoidance Agreement ECB External Commercial Borrowings ED Executive Director FCCB Foreign Currency Convertible Bond FDI Foreign Direct Investment FTS Fee for Technical Services FY Financial Year GAAR General Anti Avoidance Rules GDR Gross Depository Receipt GOI Government of India

HO Head Office JV Joint Venture LLP Limited Liability Partnership LO Liaison Office MAT Minimum Alternate Tax MCAA Multilateral Competent Authority Agreement MNC Multi-National Company OECD Organization for Economic Co-operation and Development PE Permanent Establishment PO Project Office POEM Place of Effective Management RBI Reserve Bank of India ROC Registrar of Companies ROI Return of Income R&D Research & Development SHR Safe Harbor Rules The Act Income Tax Act 1961 TP Transfer Pricing TRC Tax Residency Certificate WOS Wholly-Owned Subsidiary

Coinmen Consultants LLP www.coinmen.com

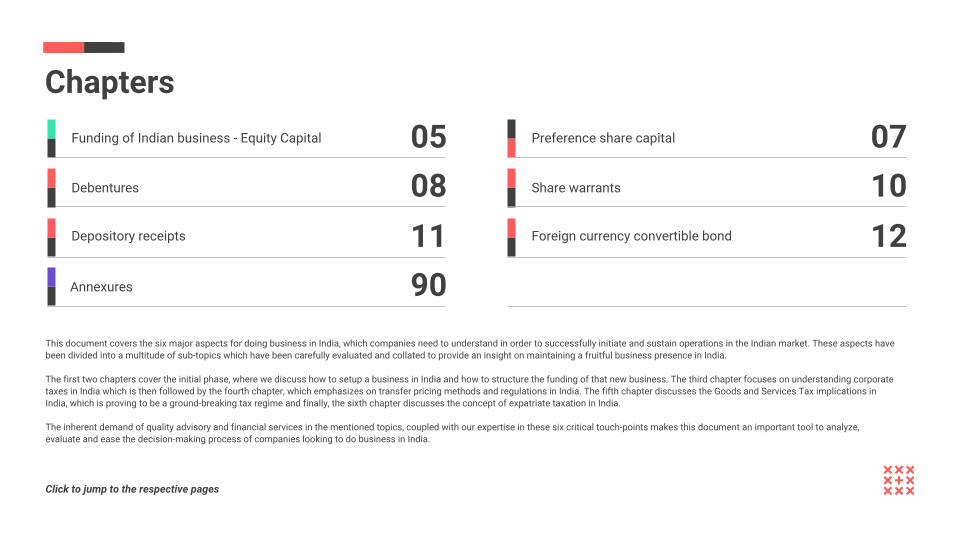

Chapters

Click to jump to the respective pages

05 08 11 90

Funding of Indian business - Equity Capital

Debentures

Depository receipts

Annexures

07 10 12

Preference share capital

Share warrants

Foreign currency convertible bond

This document covers the six major aspects for doing business in India, which companies need to understand in order to successfully initiate and sustain operations in the Indian market. These aspects have been divided into a multitude of sub-topics which have been carefully evaluated and collated to provide an insight on maintaining a fruitful business presence in India. The first two chapters cover the initial phase, where we discuss how to setup a business in India and how to structure the funding of that new business. The third chapter focuses on understanding corporate taxes in India which is then followed by the fourth chapter, which emphasizes on transfer pricing methods and regulations in India. The fifth chapter discusses the Goods and Services Tax implications in India, which is proving to be a ground-breaking tax regime and finally, the sixth chapter discusses the concept of expatriate taxation in India. The inherent demand of quality advisory and financial services in the mentioned topics, coupled with our expertise in these six critical touch-points makes this document an important tool to analyze, evaluate and ease the decision-making process of companies looking to do business in India.

Funding of Indian business

05 Funding an Indian business

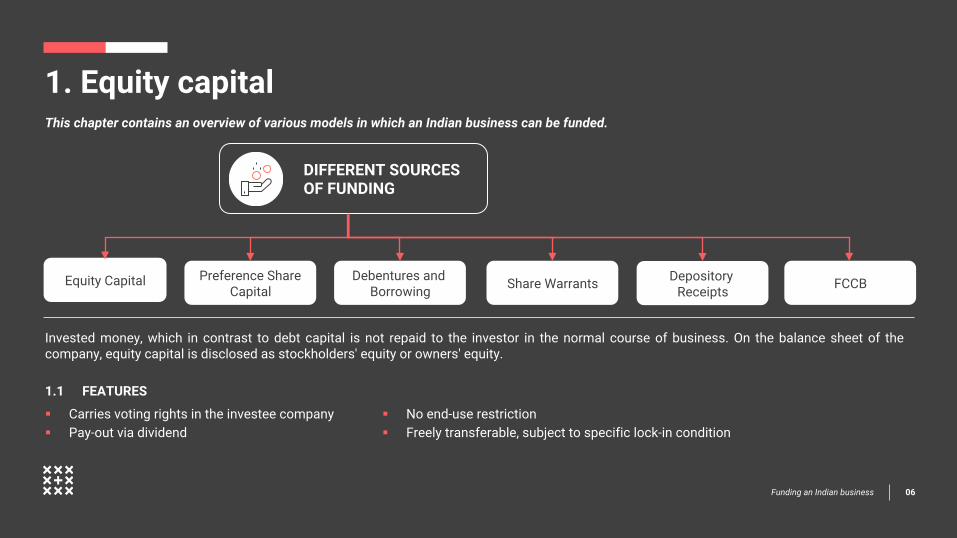

This chapter contains an overview of various models in which an Indian business can be funded.

06 Funding an Indian business

Equity Capital Preference Share Capital

Debentures and Borrowing Share Warrants Depository

Receipts FCCB

Invested money, which in contrast to debt capital is not repaid to the investor in the normal course of business. On the balance sheet of the company, equity capital is disclosed as stockholders' equity or owners' equity. 1.1 FEATURES

DIFFERENT SOURCES�OF FUNDING

§ Carries voting rights in the investee company § Pay-out via dividend

§ No end-use restriction § Freely transferable, subject to specific lock-in condition

1. Equity capital

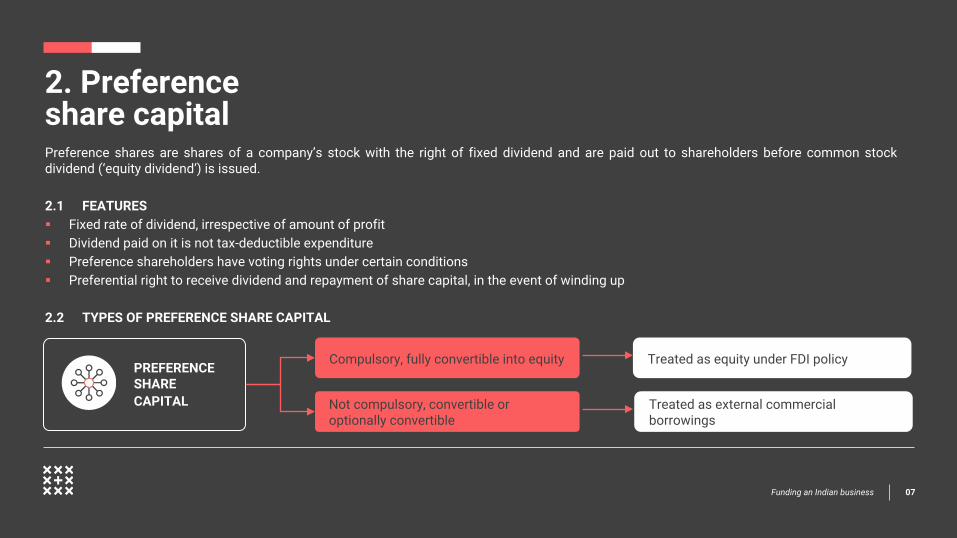

Preference shares are shares of a company’s stock with the right of fixed dividend and are paid out to shareholders before common stock dividend (‘equity dividend’) is issued. 2.1 FEATURES § Fixed rate of dividend, irrespective of amount of profit § Dividend paid on it is not tax-deductible expenditure § Preference shareholders have voting rights under certain conditions § Preferential right to receive dividend and repayment of share capital, in the event of winding up

2.2 TYPES OF PREFERENCE SHARE CAPITAL

07 Funding an Indian business

Compulsory, fully convertible into equity

Not compulsory, convertible or optionally convertible

Treated as equity under FDI policy

Treated as external commercial borrowings

PREFERENCE SHARE CAPITAL

2. Preference share capital

3. Debentures

08 Funding an Indian business

Companies can raise funds by issuing debentures, bonds and other debt securities or by accepting deposits from the public. Debentures can be redeemable, perpetual, bearer or registered, and convertible or non-convertible. Compulsory, fully convertible debentures are treated as equity under the FDI policy. Non-convertible/optionally convertible debentures are treated as ECB and should conform to ECB guidelines. Conversion ratio on compulsory, convertible debentures should be determined upfront. The rate of interest is subject to Indian TP regulations and corporate laws. 3.1 EXTERNAL COMMERCIAL BORROWINGS (ECB) Commercial loans availed in foreign currency are termed as ECB. The RBI, with a view to further improve the ease of doing business in India has rationalized the extant framework for ECB and Rupee Dominated Bonds. Under the revised framework, the loans can be raised under the following 2 options: - Foreign Currency (‘FCY’) denominated ECB; - INR denominated ECB� ECB under the above mentioned 2 options have certain conditions with respect to eligible borrowers, lenders, all-in-cost ceiling, end use restriction, exchange rate, etc. which has been duly explained in the ECB Master Directions as issued by RBI..

09 Funding an Indian business

Further, the list of eligible borrowers has now been extended to include “all entities eligible to raise Foreign Direct Investment (‘FDI’)”. As a result of the same, LLPs and trading entities are now eligible to raise ECB. Indian entities who have borrowed monies from outside lender by way of issuance of Rupee Denominated Bonds are allowed concessional tax rates on the interest income earned, subject to satisfaction of certain conditions. 3.2 LISTED DEBENTURES/BONDS SEBI-registered FIIs/FPIs/FPIs are allowed to invest in listed debt securities, subject to regulatory conditions. 3.3 BANK LOANS A bank loan is the most common form of loan capital for a business. A bank loan provides medium or long-term finance. 3.4 CONVERTIBLE NOTES Convertible Note is an instrument issued by an Indian startup company for an amount of INR 2.5 million or more initially as debt, which is repayable at the option of the holder, or convertible into equity shares of such startup company, within a period not exceeding five years from the date of issue of the convertible note.

3. Debentures

10 Funding an Indian business

Share Warrants can be issued by an Indian Company in accordance with the provisions of the Companies Act, 2013 and Regulations issued by the Securities and Exchange Board of India (in case of listed companies). Further, as per the FEMA guidelines, at least 25% of the consideration shall be received upfront and the balance amount within 18 months of issuance of share warrants. In case of non-payment of balance consideration, the forfeiture of the amount paid upfront will be in accordance with the provisions of the Companies Act, 2013 and the Income Tax provisions, as applicable.

4. Share warrants

11 Funding an Indian business

Depository Receipt means a foreign currency denominated instrument whether listed on an international exchange or not, issued by a foreign depository in a permissible jurisdiction on the back of eligible securities issued or transferred to that foreign depository and deposited with a domestic custodian and includes ‘global depository receipt’ as defined in the Companies Act, 2013. A company can issue depository receipts after complying with the provisions as prescribed under the Companies Act, Depository Receipts Scheme, 2014, FEMA guidelines and other prescribed regulations issued by RBI. The depository receipts shall be issued by an overseas depository bank appointed by the company and the underlying shares shall be kept in the custody of a domestic custodian bank.

5. Depository receipts

12 Funding an Indian business

FCCB is a bond issued in accordance with the Issue of Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository Receipt Mechanism) Scheme, 1993 and as amended from time to time. It is subscribed by a non-resident in foreign currency and convertible into ordinary shares of the issuing company in any manner, either in whole or in part. FCCBs having underlying of instruments in the nature of debt will not be reckoned for total foreign investment.

6. Foreign currency convertible bond (“FCCB”)

Annexures for compliance matters

13 Funding an Indian business

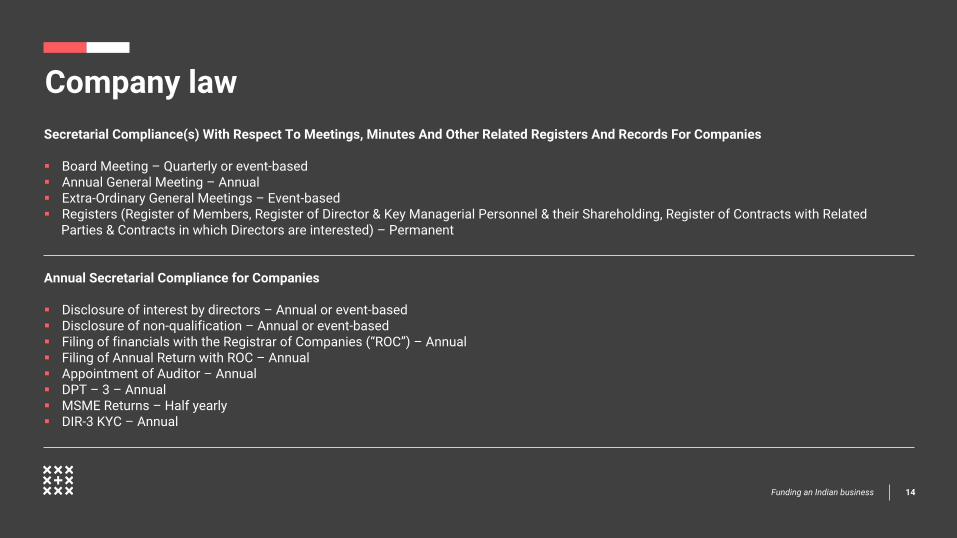

14 Funding an Indian business

Secretarial Compliance(s) With Respect To Meetings, Minutes And Other Related Registers And Records For Companies § Board Meeting – Quarterly or event-based § Annual General Meeting – Annual § Extra-Ordinary General Meetings – Event-based § Registers (Register of Members, Register of Director & Key Managerial Personnel & their Shareholding, Register of Contracts with Related

Parties & Contracts in which Directors are interested) – Permanent Annual Secretarial Compliance for Companies § Disclosure of interest by directors – Annual or event-based § Disclosure of non-qualification – Annual or event-based § Filing of financials with the Registrar of Companies (“ROC”) – Annual § Filing of Annual Return with ROC – Annual § Appointment of Auditor – Annual § DPT – 3 – Annual § MSME Returns – Half yearly § DIR-3 KYC – Annual

Company law

15 Funding an Indian business

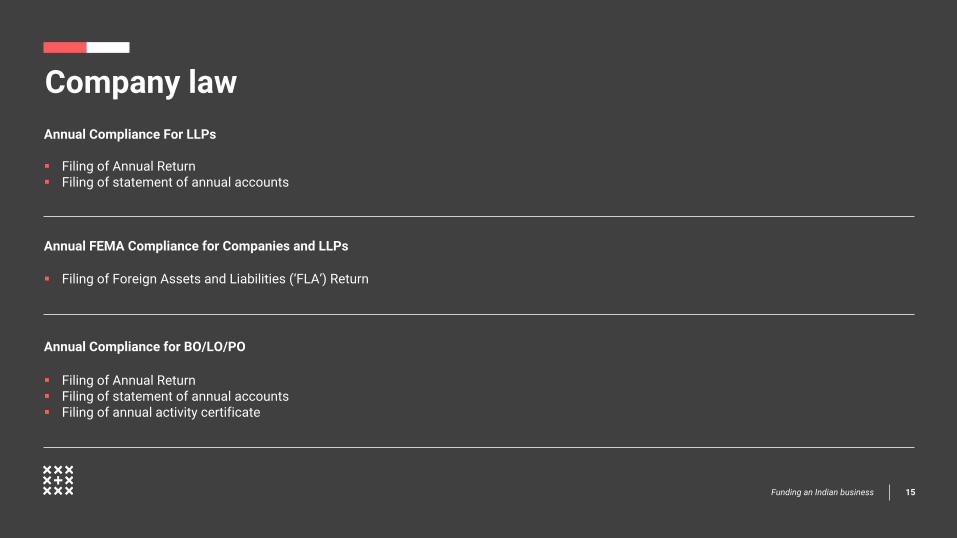

Annual Compliance For LLPs § Filing of Annual Return § Filing of statement of annual accounts

Annual FEMA Compliance for Companies and LLPs § Filing of Foreign Assets and Liabilities (‘FLA’) Return

Annual Compliance for BO/LO/PO § Filing of Annual Return § Filing of statement of annual accounts § Filing of annual activity certificate

Company law

16 Funding an Indian business

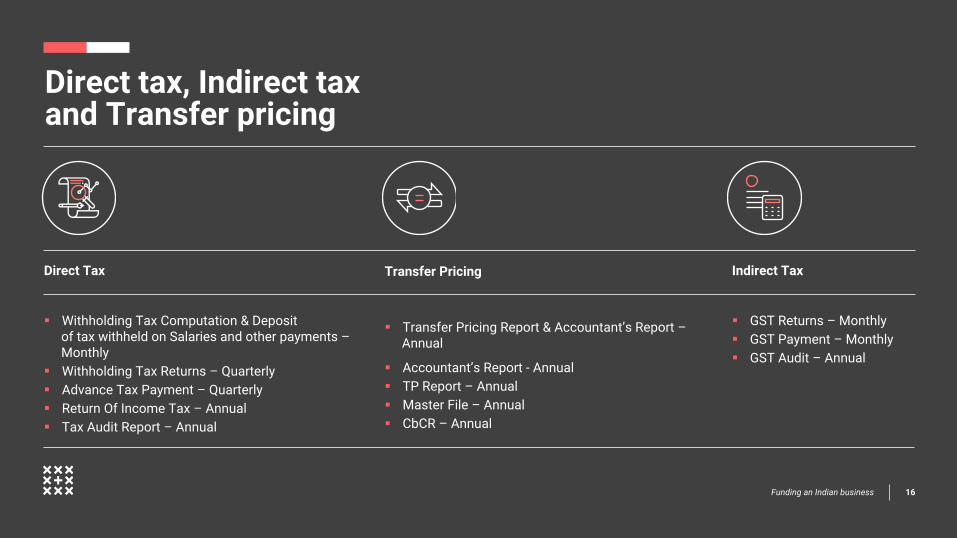

Direct Tax § Withholding Tax Computation & Deposit �

of tax withheld on Salaries and other payments – Monthly

§ Withholding Tax Returns – Quarterly § Advance Tax Payment – Quarterly § Return Of Income Tax – Annual § Tax Audit Report – Annual

Direct tax, Indirect tax and Transfer pricing

Indirect Tax

§ GST Returns – Monthly § GST Payment – Monthly § GST Audit – Annual

Transfer Pricing § Transfer Pricing Report & Accountant’s Report –

Annual

§ Accountant’s Report - Annual § TP Report – Annual § Master File – Annual § CbCR – Annual

Coinmen Consultants LLP NEW DELHI | MUMBAI | GURGAON | HYDERABAD

+91 11 4016 0160 | [email protected]�www.coinmen.com