Embed Size (px)

Citation preview

A Strategic Energy Resource

Future of COAL

YEAR September, 2014

COPYRIGHT

DISCLAIMER

CONTACTS

YES BANK Ltd.

Tushar PandeySenior President & Country Head - PSPM

Registered and Head Office

th9 Floor, Nehru Centre,Dr. Annie Besant Road,Worli, Mumbai - 400 018

Tel : +91 22 6669 9000Fax : +91 22 2497 4088

Northern Regional Office

48, Nyaya Marg, ChanakyapuriNew Delhi – 110 021

Tel : +91 11 6656 9000Email : [email protected] : www.yesbank.in

TITLE Future of Coal – A Strategic Energy Resource

AUTHORS

INDIAN CHAMBER OF COMMERCE

Dr. Rajeev Singh,Director General

ICC TOWERS4, India Exchange PlaceKolkata - 700 001. West Bengal.

Tel : 91-33 2230 3242 - 44Fax : 91-33 2231 3377/ 3380E mail : [email protected]

Public and Social Policies Management (PSPM) Group, YES BANK

No part of this publication may be reproduced in any form by photo, photoprint,

microfilm or any other means without the written permission of YES BANK Ltd. & ICC

This report is the publication of YES BANK Limited (“ICC”) & ICC and so YES BANK & ICC has editorial control over the content, including opinions, advice, statements, services, offers etc. that is represented in this report. However, YES BANK & ICC will not be liable for any loss or damage caused by the reader's reliance on information obtained through this report. This report may contain third party contents and third-party resources. YES BANK & ICC takes no responsibility for third party content, advertisements or third party applications that are printed on or through this report, nor does it take any responsibility for the goods or services provided by its advertisers or for any error, omission, deletion, defect, theft or destruction or unauthorized access to, or alteration of, any user communication. Further, YES BANK & ICC does not assume any responsibility or liability for any loss or damage, including personal injury or death, resulting from use of this report or from any content for communications or materials available on this report. The contents are provided for your reference only.

The reader/ buyer understands that except for the information, products and services clearly identified as being supplied by YES BANK & ICC it does not operate, control or endorse any information, products, or services appearing in the report in any way. All other information, products and services offered through the report are offered by third parties, which are not affiliated in any manner to YES BANK & ICC.

The reader/ buyer hereby disclaims and waives any right and/ or claim, they may have against YES BANK & ICC with respect to third party products and services.

All materials provided in the report is provided on “As is” basis and YES BANK & ICC makes no representation or warranty, express or implied, including, but not limited to, warranties of merchantability, fitness for a particular purpose, title or non – infringement. As to documents, content, graphics published in the report, YES BANK & ICC makes no representation or warranty that the contents of such documents, articles are free from error or suitable for any purpose; nor that the implementation of such contents will not infringe any third party patents, copyrights, trademarks or other rights.

In no event shall YES BANK & ICC or its content providers be liable for any damages whatsoever, whether direct, indirect, special, consequential and/or incidental, including without limitation, damages arising from loss of data or information, loss of profits, business interruption, or arising from the access and/or use or inability to access and/or use content and/or any service available in this report, even if YES BANK & ICC is advised of the possibility of such loss.

Maps depicted in the report are graphical representation for general representation only.

Coal is the most significant source of primary energy in India and caters to around 52% of

primary commercial energy needs. While India has the fifth largest coal reserves in the world,

estimated at over 250 billion tonnes, it imports nearly a third of the world's coal to fuel its power

plants. By 2030, this coal demand is estimated to reach 2 billion tones, creating significant

pressure on extraction costs, market prices and the cost of power.

Despite enormous potential, the sector is plagued with regulatory challenges, unresolved policy

issues, inadequate infrastructure facilities and environmental and capacity issues. These

significantly dampen the potential of the sector and in turn, overall growth and development of

the economy. The Government should augment its policy framework and encourage institutional

innovation for effective coal reserve management and address the challenges of capital and

operational costs, infrastructural requirement, as well as labour, land, mining and taxation

reforms.

The Government has demonstrated a strong focus on the sector in the Budget, which

emphasizes several comprehensive measures for enhancing domestic coal production along

with stringent mechanisms to ensure quality control and environmental impact. Additionally,

standardization of customs duty on coal, across grades and types, will eliminate assessment

disputes. The Government's commitment to provide adequate quantity of coal to power plants

by resolving the existing impasse in the sector will also boost investor confidence. The recent

Nuclear Cooperation agreement between India and Australia and availability of top-quality

Australian coal will significantly augment India's energy security.

YES BANK is committed to working closely with all key stakeholders to bring about a

transformational change in the energy sector and realize the Government's vision of providing

24x7 Power at Affordable Rates to All.

In this context, I am pleased to present the YES BANK - ICC Knowledge Report 'Future of Coal –

A Strategic Energy Resource' which highlights key opportunities and focus areas in the Coal

and Energy sector.

I am confident that the contents of the knowledge report will provide important insights on

addressing concerns of the coal and energy sector for realizing it's true growth potential and

energy security for the Nation.

FOREWORD

Thank you.

Sincerely,

Rana Kapoor

MD & CEO

Coal contributes over half of India's primary commercial energy. Though the share of renewable

energy is gradually expected to increase in the coming years, coal is likely to remain India's most

important source of energy for the coming decades. The sector has been beset with

controversies of late such as the controversy related to allocation of captive coal blocks, or

insufficient coal production leading to questions about who should bear the increased costs of

coal imports.

However, these controversies have not helped the coal sector at all, nor have they been able to

identify the fundamental challenges that need to be addressed if the sector has to function

healthily and promote the causes of energy access and energy security in India.

The gap between demand and availability of coal in India is expected to rise every year. Today

nearly most of the country's total installed power capacity is generated using coal. India ranks

fourth largest in coal reserves and the third largest coal producing country in the world.

Though the coal demand has risen considerably over the last couple of years, coal production has

not been able to keep up with the requirements. Organisations are acquiring mines abroad to

augment the capacity and meet the growing demand. Besides, there is also an urgent need to

adopt some possible measures like rationalization of coal linkage, dedicated freight corridors to

improve the situation, need to develop skill sets of mining professionals, promoting under ground

mining, cleaner coal technologies for sustainable development.

In this context, Indian Chamber of Commerce to further strengthen its support amongst thindustry representatives and policy-makers presents the 6 India Coal Summit during 23rd

September 2014 at New Delhi. Yes Bank Ltd is the Knowledge Partner of this initiative. This

platform will bring together various stakeholders to discuss, share and evolve suitable strategies

and development models. I am certain that this summit will be able to come up with some

answers to the many vexed questions of this sector.

MESSAGE FROM ICC PRESIDENT

Roopen Roy

President

Indian Chamber of Commerce

1. Overview: Global & Indian Coal Industry 1

2. Growth – India Perspective 7

3. Policy & Regulatory Environment 11

4. Inclusive Growth – Scope for 15

Greater Partnerships

5. 10 - Point Roadmap to Sustainable ..................29

Development in Coal Mining

..........

1.1 Global Trends of Coal ....................................2

1.2 Strategic Importance of Coal in India ............4

.................................

2.1 Future Demand & Supply Gaps .....................8

2.2 Dependency on Imported Coal......................8

2.3 Energy Security – Investment in....................9

Coal Mines Abroad

.....................

3.1 Coal Mining Legislations..............................12

3.2 Reforms in Coal Mining ...............................13

3.3 Land Acquisition ..........................................14

............................

4.1 Private Sector Participation ..........................16

4.2 Securing Finances for Development............20

4.3 Sustainable Development............................22

4.4 The Social Equity Model ..............................24

Contents

Overview:Global & Indian Coal Industry 01

1Coal is one of the most vital sources of energy fueling nearly 40%

of the global production of electricity and bolstering steel and

cement productions among other industrial activities. Coal has also

been the fastest growing energy source in the last decade while

exceeding the growth of gas, oil, nuclear, hydro and renewable.

Globally, proved coal reserves stood at 891 billion tons in 2013, of which 34.8% was

recorded in Europe and Eurasia, 32.3% in Asia Pacific, 27.5% in North America, 3.7% in 2

Middle East and Africa and 1.6% in South and Central America . World’s proven coal

reserves in 2013 were adequate to last 113 years at current world production level. US,

Russia and China together hold the largest reserves in the world, however, regionally,

Europe & Eurasia record the maximum reserves. Currently, India has the 5th largest reserve

of coal in the world accounting for nearly 6.8% of the accumulated global coal reserves.

1.1 Global Trends of Coal

NorthAmerica27.50%

South &Central America,

1.60%

AsiaPacific,32.30%

Europe andEurasia,34.80%

Middle East &Africa, 3.70%

Other, 5.30%

Figure 1: Proved Coal Reserves in the World (2013)

1 The Coal Resource - World Coal Association (www.worldcoal.org)2 BP Statistical Review of World Energy, June 2014

Source: BP Statistical Review of World Energy, June 2014

2 Future of Coal – A Strategic Energy Resource

01 | Overview: Global & Indian Coal Industry

Source: BP Statistical Review of World Energy, June 2014

rdDespite such abundance, India is the 3 largest importer of coal in the world. In 2012-13,

coal imports stood at 145 million tonnes. This figure rose by 17.9% to 171 million tonnes in 3

2013-14 amid the growing demand supply gap of coal .

In 2013, World coal production increased by 0.8% with the highest production increment

recorded in Indonesia at 9.4%. This was followed by Australia at 7.3% increment sufficient

to offset the decline in US of 3.1%. China recorded the weakest volumetric growth in

production since 2000 at 1.2%. Coal consumption on the other hand grew by 3%, well

below the 10-year average of 3.9%, yet the fastest-growing fossil fuel amongst others. 4India and China alone accounted for nearly 88% of global growth .

3 BP Statistical Review of World Energy, June 2014

4 BP Statistical Review of World Energy, June 20145 BP Statistical Review of World Energy, June 2014

The share of coal globally as a primary energy source has reached 30.1%, the highest since

1970. Consumption of coal outside OECD rose by a below average 3.7% while still

accounting for 89% of global growth. OECD consumption rose by 1.4% with the increases

in Japan and US countering the subsequent declines in EU. China experienced the weakest

absolute growth since 2008, however, still accounted for 67% of the global growth. India

accounted for 21% of the global growth while recording its second largest volumetric 5increase on record .

Future of Coal – A Strategic Energy Resource3

69%

14%1%

12%

0%

4%

North America

South & Central America

Europe & Eurasia

Middle East

Africa

Asia Pacific

Production of Coal (Million Tonnes Oil Equivalent)

Figure 2: Global Production of Coal 2013

Company 2012-13 2013-14 2013-14 Achievement Growth

Target Actual (%) (%)

CIL 452.21 482.00 462.53 95.96 2.3

SCCL 53.19 54.30 50.47 92.95 -5.1

Captive 34.23 50.00 38.88 77.76 13.6

Others 16.78 18.25 13.76 75.40 -18.0

Total 556.41 604.55 565.64 93.56 1.7

Source: Ministry of Coal, Annual Report 2013-14

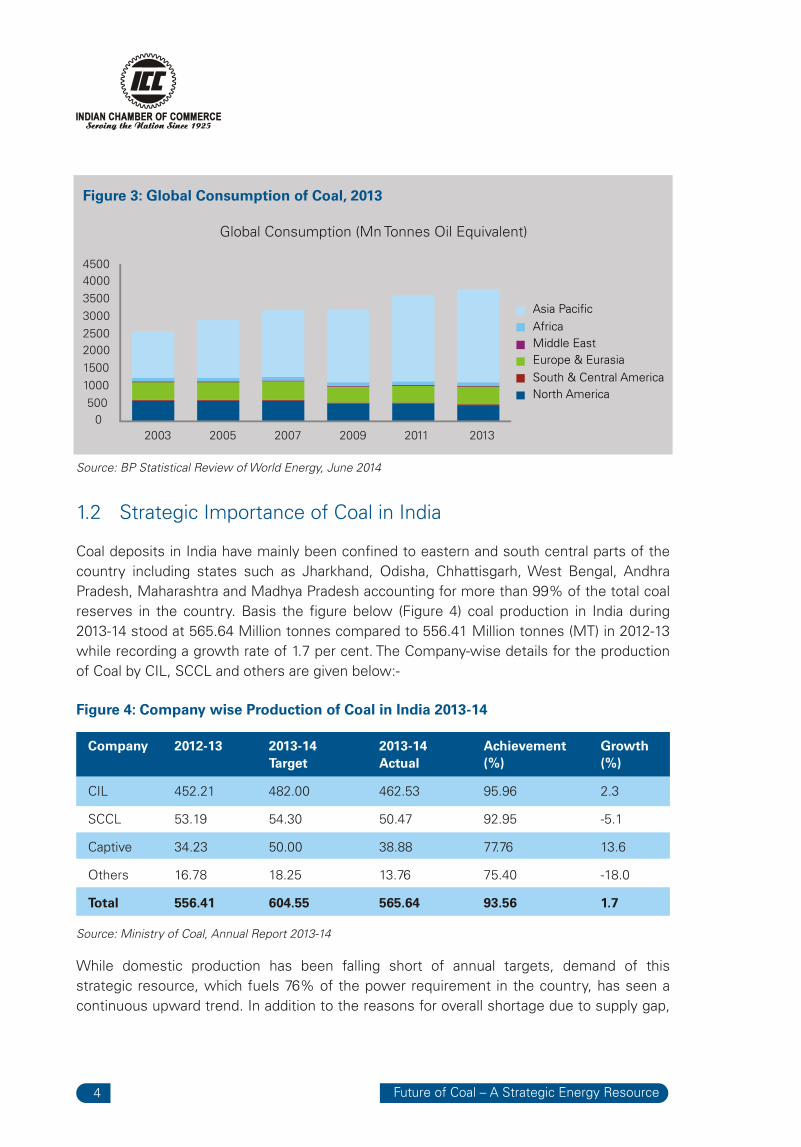

1.2 Strategic Importance of Coal in India

Coal deposits in India have mainly been confined to eastern and south central parts of the

country including states such as Jharkhand, Odisha, Chhattisgarh, West Bengal, Andhra

Pradesh, Maharashtra and Madhya Pradesh accounting for more than 99% of the total coal

reserves in the country. Basis the figure below (Figure 4) coal production in India during

2013-14 stood at 565.64 Million tonnes compared to 556.41 Million tonnes (MT) in 2012-13

while recording a growth rate of 1.7 per cent. The Company-wise details for the production

of Coal by CIL, SCCL and others are given below:-

4 Future of Coal – A Strategic Energy Resource

Figure 4: Company wise Production of Coal in India 2013-14

While domestic production has been falling short of annual targets, demand of this

strategic resource, which fuels 76% of the power requirement in the country, has seen a

continuous upward trend. In addition to the reasons for overall shortage due to supply gap,

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2003 2005 2007 2009 2011 2013

Asia Pacific

Africa

Middle East

Europe & Eurasia

South & Central America

North America

Figure 3: Global Consumption of Coal, 2013

Global Consumption (Mn Tonnes Oil Equivalent)

Source: BP Statistical Review of World Energy, June 2014

the country imports coal due to low caloric and high ash content nature of Indian coal

which necessitates import of high quality coal to meet specific requirements like in steel

plants.

Future of Coal – A Strategic Energy Resource5

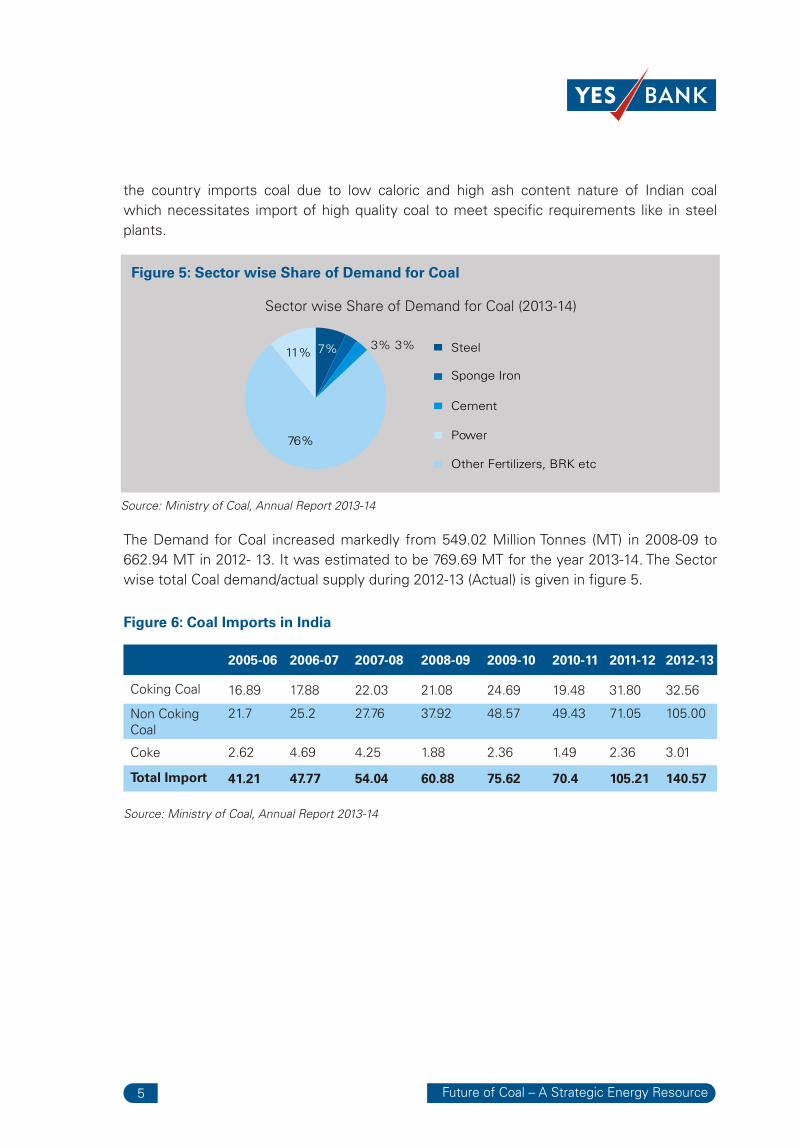

The Demand for Coal increased markedly from 549.02 Million Tonnes (MT) in 2008-09 to

662.94 MT in 2012- 13. It was estimated to be 769.69 MT for the year 2013-14. The Sector

wise total Coal demand/actual supply during 2012-13 (Actual) is given in figure 5.

Figure 6: Coal Imports in India

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Coking Coal 16.89 17.88 22.03 21.08 24.69 19.48 31.80 32.56

Non CokingCoal

21.7

25.2

27.76

37.92

48.57

49.43

71.05

105.00

Coke 2.62 4.69 4.25 1.88 2.36 1.49 2.36 3.01

Total Import 41.21 47.77 54.04 60.88 75.62 70.4 105.21 140.57

Source: Ministry of Coal, Annual Report 2013-14

Figure 5: Sector wise Share of Demand for Coal

7% 3%3%

76%

11% Steel

Sponge Iron

Cement

Power

Other Fertilizers, BRK etc

Sector wise Share of Demand for Coal (2013-14)

Source: Ministry of Coal, Annual Report 2013-14

Growth – India Perspective 02

2.1 Future Demand and Supply Gaps

The demand for Coal during 2013-14, was estimated to be 769.69 MT, whereas the

domestic availability was estimated at 614.55 MT. The gap of 155.14 MT was projected to be 6met through imports. However, during the year 2013-14 , the actual indigenous supply of

Coal stood at 571.00 MT. As per figures provided, about 168.5 Million Tonnes of Coal was

imported during 2013-14. The demand supply gap has evidently been increasing over the last

decades with growing pressure on imports.

thAs per forecasts, the demand for coal by the end of 12 Five Year Plan (2016-17) is expected

to increase to about 980 MT while domestic availability is expected to fall short at 795.0 MT,

subject to availability of requisite land for coal mining and all clearances in time. Therefore,

there is likely to be a gap of 185.50 MT, which is required to be met through imports. The

details of projected demand supply gaps are given below:-

Figure 7: Coal Supply and Demand in India

6 Ministry of Coal, Annual Report 2013-14

8 Future of Coal – A Strategic Energy Resource

02 | Growth – India Perspective

2012-13 (BE) 2013-14 (BE)

Total Indigenous Supply 795.00

Demand Projected 980.50

Projected Import Requirement 185.50

Total Import 140.57

Source: Ministry of Coal, Annual Report 2013-14

2014-15 (BE) XII PlanProj. 2016-17

580.3

772.84

192.54

140.57

614.55

769.69

155.14

140.57

643.75

787.03

143.28

140.57

2.2 Dependency on Imported Coal

India is the fourth largest consumer of energy in the World after USA, China and Russia.

Despite having some of the largest coal deposits in the world, India’s quest of securing

energy security has been marred by inadequate exploration budgets and planning, excessive

delays in project clearances, inadequate logistics and more recently, intervention of the

Supreme Court in captive block allocations.

Evidently, as energy intensity and needs have been

rising, India has been progressively becoming

dependent on the imports. High energy prices have

further impinged energy security.

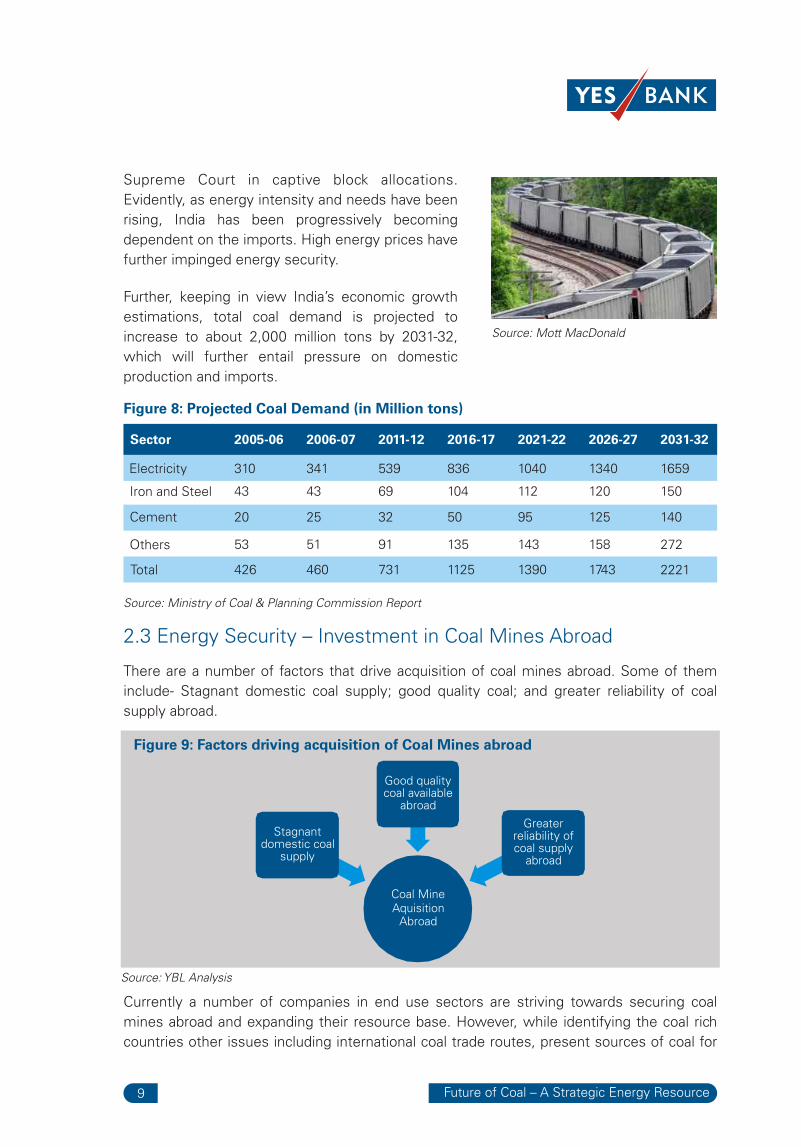

Further, keeping in view India’s economic growth

estimations, total coal demand is projected to

increase to about 2,000 million tons by 2031-32,

which will further entail pressure on domestic

production and imports.

Future of Coal – A Strategic Energy Resource9

Figure 8: Projected Coal Demand (in Million tons)

Sector 2005-06

Electricity

2006-07 2011-12 2016-17 2021-22 2026-27 2031-32

310 341 539 836 1040 1340 1659

Iron and Steel 43 43 69 104 112 120 150

Cement 20 25 32 50 95 125 140

Others 53 51 91 135 143 158 272

Total 426 460 731 1125 1390 1743 2221

Source: Ministry of Coal & Planning Commission Report

2.3 Energy Security – Investment in Coal Mines Abroad

There are a number of factors that drive acquisition of coal mines abroad. Some of them

include- Stagnant domestic coal supply; good quality coal; and greater reliability of coal

supply abroad.

Currently a number of companies in end use sectors are striving towards securing coal

mines abroad and expanding their resource base. However, while identifying the coal rich

countries other issues including international coal trade routes, present sources of coal for

Source: Mott MacDonald

Figure 9: Factors driving acquisition of Coal Mines abroad

Coal Mine Aquisition

Abroad

Stagnant domestic coal

supply

Good quality coal available

abroad

Greater reliability of coal supply

abroad

Source: YBL Analysis

India, port and logistics infrastructure facilities available in source countries and port

facilities available in India need to be taken into consideration.

Moreover, a number of constraints with respect to

the conservative attitude of the coal rich countries

in regards to permit entry to foreign players in

controlling a strategic asset like coal, absence of

any sovereign fund for developing infrastructure in

the host countries, the aggressive Chinese model

of Merger & Acquisition to control coal properties

in different parts of the world and limited

empowerment of Indian PSUs to take strategic

business decisions are identified as major

hindrances in acquiring coal assets worldwide.

In order to ensure effective coal block acquisitions worldwide, the government should

propose clear guidelines permitting PSUs to be strategically aggressive for maiden foreign

acquisitions, to omit the distinction between listed and unlisted companies with regards to

acquiring foreign assets, to encourage the appointment of Investment Bankers on

nomination basis to incentivize them for bringing exclusive deals which can be transacted

on one-to-one basis, to introduce tools and guidelines related to financial parameters to

facilitate speedy decision making that would fast track the entire Merger & Acquisition

(M&A) transaction, and to include a suitable clause that would mandate the process of

reviewing the proposed financial powers of the board linked to periodic foreign investment.

An initiative of Ministry of Steel, Government of India, has been the set up of the

International Coal Ventures Private Limited which is a Joint Venture Company with SAIL,

CIL, RINL, NMDC and NTPC as the promoter companies for securing metallurgical coal and 7

thermal coal assets in overseas territories. Its primary objectives include :

üTo ensure supply of imported met coal, of at least 10% of the 2019-20 requirements

of SAIL and RINL, i.e. say five million tonnes per annum, from assets overseas as

medium term target to be achieved by 2011-12, being a step towards security of

supply.

üown of about 500 million tonnes of met coal reserves by 2019-20.

üTo meet the requirements and to serve the organizational aspirations of other

participating companies like CIL, NTPC and NMDC by providing a facility for

enhancing and leveraging their domain knowledge and human capital for

international mining business development and also for procuring high quality

thermal coal for companies like NTPC.

10 Future of Coal – A Strategic Energy Resource

7 http://icvl.in/aboutus.php?tag=company-aboutus

Source: theblaze.com

Policy andRegulatory Environment 03

12 Future of Coal – A Strategic Energy Resource

03 | Regulatory Environment

Policy and

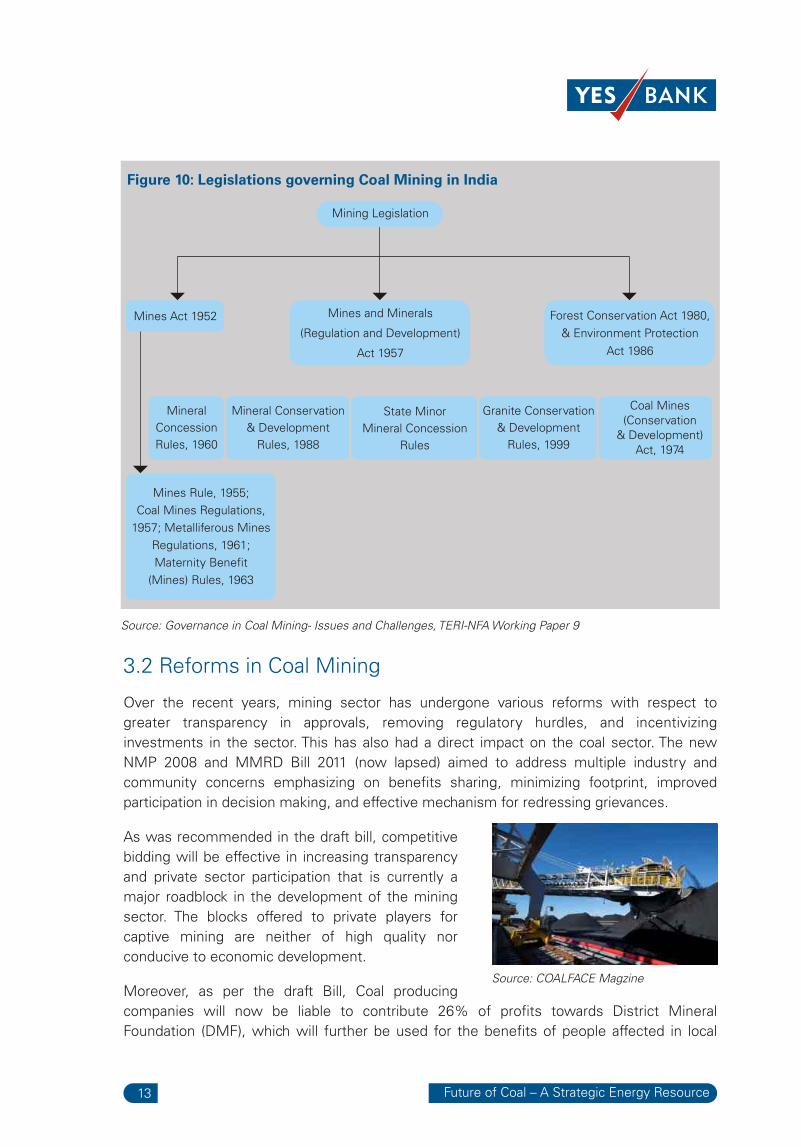

3.1 Coal Mining Legislation

Resources in India are primarily managed by the

central and state government. The proprietary title

vests in the federating states while the center has

jurisdiction over the development of mines and

minerals. As per the Mines and Minerals

(Regulation and Development) Act (MMRDA), 1957

coal was listed as a schedule one mineral. This

implied that although the ownership of coal

resources vests with state, prospecting and mining

are controlled by the central government There

exists several policies and legislations that govern various aspects of the coal sector. The

figure below gives the legislations governing coal mining in India. Basic laws constitute -

The MMRD Act, 1957; Mines Act 1952; Forest Conservation Act 1980; Environment

Protection Act 1986; and all the rules framed under them are applicable to coal mining.

The National Mineral Policy (NMP) which was first formulated in 1993 and subsequently

revised in 2002 and 2008, guides the implementation of MMRD Act and other legislations.

As per the Hoda Committee's recommendations and the subsequent revision of the NMP

in 2008, the MMDR Act is being amended to ensure that developments in mineral

resources are in harmony with the national policy goals. A draft bill for the same, MMDR

Act, 2011 was also tabled in the parliament, which could not be passed and has since

lapsed.

Source: ABC News

3.2 Reforms in Coal Mining

Over the recent years, mining sector has undergone various reforms with respect to

greater transparency in approvals, removing regulatory hurdles, and incentivizing

investments in the sector. This has also had a direct impact on the coal sector. The new

NMP 2008 and MMRD Bill 2011 (now lapsed) aimed to address multiple industry and

community concerns emphasizing on benefits sharing, minimizing footprint, improved

participation in decision making, and effective mechanism for redressing grievances.

As was recommended in the draft bill, competitive

bidding will be effective in increasing transparency

and private sector participation that is currently a

major roadblock in the development of the mining

sector. The blocks offered to private players for

captive mining are neither of high quality nor

conducive to economic development.

Moreover, as per the draft Bill, Coal producing

companies will now be liable to contribute 26% of profits towards District Mineral

Foundation (DMF), which will further be used for the benefits of people affected in local

Future of Coal – A Strategic Energy Resource13

Source: COALFACE Magzine

Figure 10: Legislations governing Coal Mining in India

Mines Act 1952 Mines and Minerals

(Regulation and Development)

Act 1957

Forest Conservation Act 1980,

& Environment Protection

Act 1986

State Minor

Mineral Concession

Rules

Mineral

Concession

Rules, 1960

Mineral Conservation

& Development

Rules, 1988

Granite Conservation

& Development

Rules, 1999

Coal Mines(Conservation

& Development)Act, 1974

Mines Rule, 1955;

Coal Mines Regulations,

1957; Metalliferous Mines

Regulations, 1961;

Maternity Benefit

(Mines) Rules, 1963

Mining Legislation

Source: Governance in Coal Mining- Issues and Challenges, TERI-NFA Working Paper 9

areas. The compensation to local people and rehabilitation measures as given in the

national Resettlement & Rehabilitation policy could holistically improve standards of living

of people displaced by mining activities. Effective utilization of this fund is of great

importance. In this respect, it is vital to have transparent and participatory mechanisms that

encourage effective utilization of funds collected through DMF for community

development.

In order to improve regulatory oversight, establishing a coal regulator would be timely for

inducing competition, transparency and creating a level playing field. However, a vital factor

determining its success in instilling faith in the governance system and acceptance of

mining is its independence from the government as well as the industry.

The Land Acquisition and Relief and Rehabilitation Bill introduced in 2011 attempts to

address the problems with Land Acquisition Act 1894, which have been the center of

debates and controversies for many years. Unclear definitions and clauses, absence of

requirements for compensation, participation and R&R in the Act are some of the issues.

The Bill has introduced a number of effective changes which mandate provisions with

regards to taking consent of atleast 80% of the affected people, broadening the definition

of affected people to include sharecroppers, agricultural labourers, tenants etc. and

conducting Social Impact Assessments (SIA) through independent bodies for better

evaluation of the ill effects of mining.

While these policy initiatives are effective in terms of addressing the shortcomings in

governance in the coal mining sector, much is dependent on the implementation of these

policies. As observed, much of the challenges in governance are not due to the lack of

policies, but due to their flawed implementation. Therefore, adoption of policies coupled

with effective implementation is vital for the future of this sector. Some critical

reformations include:

1. Increasing transparency and knowledge on various issues

2. Strengthening capacity of existing regulatory agencies and local institutions

3. Ensuring timely and regular co-ordination among centre, state and district level

agencies

4. Enhancing the responsiveness and accountability across all levels of government

5. Laying clear rules and guidelines on the power, functions, and responsibilities of

different institutions

3.3 Land Acquisition

14 Future of Coal – A Strategic Energy Resource

Inclusive Growth – Scope forGreater Partnerships 04

04 | Inclusive Growth – Scope for Greater Partnerships

Importance of Coal to India’s energy security

cannot be underestimated, and in spite of having

huge Coal reserves, the country still faces

shortages. Coal as a sector has always been slow

on policy reforms, and is still highly regulated.

Since the beginning government-owned companies

had spearheaded the growth in the industry,

however going forward the rising demand for coal

in the country substantiates the need for

promoting greater private sector participation.

The chain of activities starting from exploration of Coal resources to planning of mines and

extraction of Coal after shaft sinking or removal of overburden (OB) and Coal washing,

preparation and transport involves several separate disciplines and calls for different types

of skills. Modern management practice suggests that in such cases each individual activity

should be entrusted to a separate company who have specialized knowledge and skill in

that part of the production chain. Leasing and out sourcing of services has made significant

contribution to the high productivity in many industries and the same will be productive in

the Indian Coal Industry.

Exploration is the foremost activity crucial for identifying new and economically viable

mines. The process of exploration being a multistage pursuit and involving a plethora of

activities and technologies culminates into the modeling of the resource for projects. Today

the country has indicated and inferred reserves and having these reserves underground is

no assurance of its availability. Therefore exploration efforts should not just aim at enlarging

the resource base but to upgrade these known resources remaining under ‘Indicated and

‘Inferred’ categories through detailed exploration. Such exploration will provide the

information required to evaluate the potential profitability of developing or expanding

mineral operations at a particular site or area.

4.1 Private Sector Participation

1. Exploration Technologies

216 Future of Coal – A Strategic Energy ResourceFuture of Coal – A Strategic Energy Resource

Source: National Geographic.com

Such exploration activities are time consuming and require huge investments.

Consequently, world over rather than expending tax-payers' money, `junior exploration

companies' funded by private capital are encouraged to pursue these risky activities. The

role of the government is to continue performing the tasks assigned for exploration and

survey however going forward private sector should spearhead investments in

reconnaissance and exploration.

Coal mining was brought under the public sector

with the passing of Coal Mines (Nationalization)

Act, 1973; although the act has been amended in

June, 1993 to allow for captive mining by the

private sector, initially for generation of power and

coal washeries, and later extended to select few

industries. Commercialization of the sector and

entry of new players will result in improvements in

eff ic iency and product iv i t y, increase in

investments, delivery of better quality of services

and improved access, and lowering of prices for the consumers. However, despite the

realization, there has not been much progress in improving private sector participation in

the sector.

Still the role of private sector in the Coal mining and development has been very limited

with limitations both on the end use and restrictions on open commercial sale of coal.

Allowing private participation either directly or by partnering Government companies could

be the possible solution for ramping up Coal production in the country and taking the

country towards self-sufficiency. Public-Private Partnerships (PPP) and Joint-Venture models

should the possible routes for facilitating large private sector investments in Coal mining

sector. However it has to be implemented in its true spirit and must involve ownership, to

achieve the desired results of such a partnership.

Another key area for partnerships with private sector is underground mining, which has

made rapid strides in technology up gradation in the world and has been relatively stagnant

in India. In the area of underground mining, new technologies will have to be introduced in

mine development to reduce the gestation period of mines, introduce better mine support

through appropriate strata control investigations, development of suitable methods for

induced caving such as hydro-fracturing for hard roof management for shallow and medium

depth of cover and also in the other areas like drilling and blasting, transportation, etc.

Some of the challenges being faced by Captive Mine owners in development of their blocks

include remote location of allocated blocks, delays in land acquisition and environmental

clearances, lack of access infrastructure for evacuation of Coal, and frequent policy

impasse. Focus of the Government should be in facilitating the removal of such barriers in

Coal mining and opening of the sector to free market conditions.

2. Coal Mining & Development

Future of Coal – A Strategic Energy Resource17

Source: Galleryhip.com

3. Logistics Infrastructure:

Logistics is a key factor in the Coal supply chain, as transportation can account for up to 70

percent of the delivered cost of Coal. Efficient use of Coal requires enabling infrastructure

support to transport from mine head to consumption centers. Today, supply chain logistics

is one of the major challenges facing the sector, as the allied transport infrastructure in

India is underdeveloped. This effect is clearly visible as Coal from pit heads lying idle for

months cannot find its way to the railways sidings for further transportation. Effective

management of logistics will ensure increased availability of Coal, since the production

capacity of a mine is directly dependent on the pace of excavation to end users.

The usual modes for Coal movement in India are rail, rail-cum-sea (coastal movement),

road, merry-go-round, belt and ropeways.

18 Future of Coal – A Strategic Energy Resource

Figure 11: Coal Transportation Mix in India

Means Characteristics

Railways Economical, cheapest and fastest mode for bulk amount for long distance

Roadways Viable, beneficial for distance between 50 to 300 meters and for small quantity

MGR Best suitable for pithead power plant and for bulk amount

Others Inland Waterways etc.

Source: Planning Commission, 2011

Share

56%

19%

18%

7%

Although already diminishing, Coal transport by road will remain a reality in India for some

time to come. The increasing share of railway transportation is making Coal logistics in India

more sustainable over the long term. The construction of expensive new lines is, however,

proceeding slowly and the overburdened railway transport network is causing bottlenecks

in the transport of Coal.

Since import of Coal would be an important feature for bridging the demand-supply gap,

planning for creating port facilities and capacity building for hinterland movement of

imported Coal from ports to consuming centers would also be of immense importance.

Increased availability of rolling stock, improving turn round of rakes and harnessing the

potential of alternative modes of transportation for Coal evacuation, particularly the use of

inland waterways are some of the avenues identified as thrust areas. The critical issues in

respect of movement logistics are:

1. Railway capacity

2. Port Capacity: Mechanization of Ports, Available Stack Space, Draft Availability

3. Capacity for transportation of Coal at the railway sidings

4. In case of pithead consumption centers, synchronization of development of mining

project and captive mode of transportation

The importance of optimization of available logistics infrastructure through source

rationalization, investment in logistics infrastructure and development of end-to-end

logistics solution companies in PPP model, and harnessing the potential of alternate modes

of transport of Coal are important areas for building up the logistics strategy. Private sector

will have a critical role to play in building the necessary infrastructure, since they form the

majority of the Coal end users.

Clean Coal Technologies (CCTs) are the technologies

being employed and developed globally to meet

Coal’s environmental challenges. These technologies

include Coal Washing, Coal Gasification, Coal Bed

Methane, Underground Coal Gasification and Coal

Liquefaction. R&D in these technologies will allow for

continued use of India’s abundant domestic

resources and the affordable energy they provide to

business and consumers. CCTs are required to

continue improving energy efficiency and to meet increasingly stringent environmental

challenges and expectations.

Most of these CCTs which are emerging as in Coal sector in the world are still at a nascent

stage in the India and needs both policy impetus and R&D investments. Coal companies

could consider investing a certain percentage of their Post-tax Profits in R&D every year.

Private sector participation in R&D work should be encouraged by involving research

scholars, academicians and reputed overseas institutions in joint projects.

While industry will finance significant portions of each CCT project, it is critical that the

central government provide funding through the appropriations process. Sufficient funding

is needed to assure continued research, development and demonstration of a new

generation of advanced technol¬ogies that are promising but too high-risk to be financed

solely by private industry. A strong commitment to clean Coal technology from the Central

Government will allow the country to take full advantage of its vast Coal reserves and meet

growing demand for electricity while meeting critical environmental objectives.

Another possible option should be to create a R&D fund by pooling a certain percentage of

combined revenue of Coal industries in the public

and private sector. The companies paying the levy

should be encouraged to set out their perceived

research & development priorities and get such

projects included in the list and bid for taking up the

projects when the bids are invited. The selection of

project and management of the fund can be

performed by a regulator set up by the Ministry of

Coal.

4. Clean Energy Technologies

Future of Coal – A Strategic Energy Resource19

Source: Asia Energy Journal

Source: CSIRO

4.2 Securing Finances for Development

Coal supply chain is made up of very large, well-capitalized companies as well as medium

and small companies; public companies which operate for profit and state-owned

companies which are not always profitable. Regardless of the size and structure all

companies operating in the supply chain require vast amounts of capital.

Natural resources companies have been evolving their financing needs and are moving

from primarily equity-based financing (which obviously has a diluting effect for

shareholders) to debt-based financing, in particular, via project financing. Successful project

financing of mining and natural resources projects requires a number of specific issues to

be considered. The ability of a mining project to attract finance is often dependent on

where it lies in the development cycle. The closer it is to the exploration stage the more

likely it will have to be funded with equity. The likelihood of a project securing debt will

increase as it moves through the cycle towards development.

Equity is the most common type of capital for mining projects and no project is fully

funded by debt finance regardless of how economically robust the project might be. In

majority of cases the projects have a debt: equity ratio in the range of 50:50 to 80:20.

Equity is usually sourced from private investors or through stock exchange listings and

rights issues, or generated within the business.

Venture capital is an essentially equity that is provided in

the form of a speculative investment. It is not normally

intended to be permanent capital but injected into a

company for a definitive period during which the investor

would be looking for a substantial move in the share price

before exiting the investment.

Quasi-equity is debt that is structured in such a way that it

appears to be equity, and usually takes the form of

convertible debt that can be converted to ordinary equity should its value increase due to

movements in the share price. Quasi-equity is normally subordinated to senior debt (in

return for the option of converting it into equity), and has the effect of reducing the level of

gearing as it is reflected as equity. Generally the risk profile of a potential project is at its

peak in the early stages and decreases with progression through the development phases.

The risks at the early stages, usually up to the point where a pre-feasibility study ('PFS') has

been completed, are normally beyond what typical commercial banks would be willing to

expose themselves to. Selected banks however, have the appetite for this level of risk and

where the PFS indicates a very strong project, they are prepared to provide funding for

completion of the Bankable Feasibility Study ('BFS'). This is normally with the intention of

securing the right to arrange the finance for the development of the project.

Risks common to the mining industry can be characterized as:

Direct Risk - As countries tighten their environmental regulations and public concern about

the mining industry grows, pressures increase on companies to minimize their

environmental impacts and pay greater heed to local social issues. This may increase

20 Future of Coal – A Strategic Energy Resource

Source: Minerals Education Coalition

companies' capital and operating costs in order to comply with increased environmental

regulations and social expectations. This can have an impact on cash flow and profitability, a

borrower's ability to meet loan repayments and the value of the entire operation. It is

therefore, important to thoroughly assess environmental performance as part of the normal

credit appraisal process.

Indirect Risk - Legislation impasses from country to country but many adopt the 'polluter

pays' principle to pollution incidents. Financiers are increasingly concerned to avoid being

placed in positions where they might be considered directly responsible for the polluting

actions of their clients, in this case mining companies. Otherwise, in the case of a pollution

incident, financial entities may find that not only have they lost the value of their original

involvement in a particular project, but they may find themselves being forced to meet

what may prove to be substantial clean-up costs or even further liabilities.

Reputational Risk - Financial institutions are under increasing scrutiny concerning their

involvement in a number of sectors, from governments, regulators, NGOs, the public and

the media. Failure to give careful consideration to environmental impacts from projects

financed, invested in or insured can result in negative publicity for both the respective

company and the financial institution.

There are many other factors which influence an investor's decision to finance a mining

project which include an analysis of the current state of the industry (supply, demand and

price factors), the profile of the company (cost profile, operating efficiency, technology,

labor factors, access to raw materials, reserve replacement strategy, contingency and

emergency planning, safety and environmental record, management) and the state where

the project will be located (political risk). All these aspects are important as mining projects

can experience various difficulties throughout its development cycle.

Future of Coal – A Strategic Energy Resource21

Figure 12: Financing of Mining Projects

Development Phase Type of Funding

Prospecting Equity

Source: YES BANK Analysis

Funding Sources

Shareholders

Initial Exploration Equity Shareholders

Advanced Exploration Equity Shareholders

Venture Capital Specialized Resource Funds

Pre-Feasibility Report Equity Shareholders

Venture Capital Specialized Resource Funds

Quasi-Equity Select Financial Institutions

Bankable Feasibility Study

Mine Development

Post-Commission

Equity Shareholders

Venture Capital Specialized Resource Funds

Quasi-Equity Select Financial Institutions

Debt with Recourse Commercial Banks

Equity Shareholders

Debt with Limited Recourse Select Financial Institutions

Equity Shareholders

Debt with Recourse Select Financial Institutions

Expertise needed for underwriting a mining project in general is limited in India. Though

environmental, health & safety concerns are considered as major issues, they form only a

part of the problems for the lender. Finding the right means to safeguard lenders from

these risks is very important.

1. Allowing assignment of mining rights in favor of lenders in case of default

2. Removal of the bar on outside sale in case of financial stress or lower captive

consumption

3. Blocks being made available based on competitive bidding, without restriction of

captive use, so that experienced players can come in

4. Shielding lenders from environmental issues

5. Greater focus on the mining sector by advisory institutions

6. Better coordination amongst agencies for providing vital connection infrastructure

Mining in general while increasing employment and

economic activity in the country, can create

environmental damage and undermine other

socioeconomic development opportunities of local

communities. Various attempts to redress these

impacts have so far been piecemeal and ad hoc with

little research or consultation with the affected

groups, thus resulting in growing disaffection

amongst the community. There is an immediate need

for focusing on sustainable development of the

industry.

Increased and long term damages sustained as a result of this increase has already

resulted and severely compromised the lives of the local communities and is set to

manifest into long term damages. Unorganized mining is the characteristic of certain

mining areas. In the recent past, mining companies have emerged as significant defaulters

on issues such as provision of safe working environment, labor health and safety and

human rights.

Many states have demonstrated improved administrative practices through royalty sharing

arrangements to work towards local area improvement and improving the relationship

between area improvement and mining. This is done by allowing a certain percentage of

the royalties collected by the state to move back to the source district.

The sustainable development framework of the mining sector rests on the following eight

components:

1) Incorporating environmental and social sensitivities in decisions on leases: This

principle integrates sustainable development concepts at the earliest phase of the mining

life cycle. The underlying philosophy of the principle is to categorize mineral bearing areas

4.3 Sustainable Development

22 Future of Coal – A Strategic Energy Resource

Source: Womens Mining Coalition

based on an environmental and social analysis taking a risk based approach. At the bidding

stage the categorization of lease areas into High and Low risk will allow the investors to

take business decisions with the knowledge that the cost and uncertainties of getting

approvals as well as operations in high risk areas will be significantly higher than the low

risk areas. It will also allow regulators to put additional commitments at an early stage for

environmental and social performance.

2) Strategic assessment in key mining regions: Understanding that mining activities

occur in clusters which have impacts at a regional level, a strategic assessment of regional

and cumulative impacts and development of a Regional Mineral Development Plan based

on an assessment of the regional "capacity" needs to be carried out at periodic intervals is

important. Creating an institutional structure to own and implement such plans in key

mining regions is critical and taking critical decisions on mining, new leases, allocation of

resources, and even possible moratorium on mining need to be taken up to ensure more

sustainable planning and development in such regions.

3) Managing impacts at the mine level through sound management systems: The key

elements of this principle are impact assessment of key environmental, social, health and

safety issues, and development of management frameworks and systems at the mine level

and continual improvement of the same on the basis of international standards on a self

driven basis. An important component is disclosing performance on environmental and

social parameters to external stakeholders at every stage of the project lifecycle.

4) Addressing land resettlement and other social impacts: This principled and

comprehensive assessment of social impacts and displacement of mining projects at the

household, community and mining region level, and management commitment to address

those impacts through mitigation measures and management plans.

5) Community engagement, benefit sharing and contribution to socio-economic

development: This principle seeks commitment to regular engagement with the local

community as well as sharing of project benefits with the affected families. It is rooted in

the principle of sharing profits with the affected communities already provisioned for in the

draft MMDR Act awaiting approval. It dovetails the social impact management of project

operations with the initiatives being undertaken and looks at an integrated approach to

mitigate impacts and improve local livelihoods and living conditions in the neighborhood

areas and communities.

6) Mine closure and post closure mining operations must prepare, manage and

progressively work on a process for eventual mine closure. This process must cover all

relevant aspects and impacts of closure in an integrated and multidisciplinary way. This

must be an auditable document and include a fully scoped and accurate estimate of

planned cost of closure to the company. The cost estimates must be adequately

provisioned to cover national, regional and local legal and regulatory requirements for

closure; and must also include the cost of servicing all agreements/commitments made

with stakeholders towards post-closure use.

Future of Coal – A Strategic Energy Resource23

7) Ethical functioning and responsible business practices: This principle underlines the

need for ethical business practices and a strong sense of corporate responsibility among

mining companies. It recommends companies to go beyond legal compliance and do their

bit to ensure the sustainability of their business as well as the local communities.

8) Assurance and Reporting: This principle seeks mining sector stakeholders to assess

their performance against this SDF and demonstrate continual improvement on this

performance over the life of the project. It requires this performance to be reported in a

structured manner in a Sustainable Development Report to be disclosed in the public

domain as well as to regulatory agencies which is to be considered during approval

processes. Implementation of the above framework is expected to lower the conflicts

arising out of environmental and social concerns in mining areas. Moreover such a

framework is expected to reduce delays emerging in the long run, contribute towards

developing a regional mining development fund for selected mining areas and addressing

key regional and cumulative impacts of mining through coordinated and collective action.

Given the diverse and difficult nature of the challenges faced by the Indian Coal sector,

there cannot be a single ‘silver bullet’ solution to them and a comprehensive approach is

necessary to address them. Reforming the sector requires action on many fronts,

especially from the private sector and such reforms are unlikely to be easy given the

entrenched nature of the problems and the associated vested interests. However, India has

no choice but to initiate these steps as it would have to significantly depend on Coal for the

short and medium term energy needs.

For long term sustainability, a cohesive and synergetic structure focused on developing an

environmentally benign mineral industry is vital to achieve economies to scale and expand

mineral exploration and production in the economy. This structure should bring together

various stakeholders in the value chain and adopt measures that are conducive to attracting

investments.

The Social Equity Model follows an integrated approach to development involving the

private developer, community, NGO’s, Governmental organizations, Financier and

Knowledge Bank in formation of SPVs during exploration or mining processes. The model is

based on a cooperative approach to development. Such partnerships provide a platform for

fruitful collaborative partnerships, and also create a strong knowledge base that pushes

sustained development and ensures social equity in the growth strategies. Partnerships

involving Govt./Pvt Sector/ NGOs can assist in giving a larger/ global perspective to local

problems

4.4 The Social Equity Model

24 Future of Coal – A Strategic Energy Resource

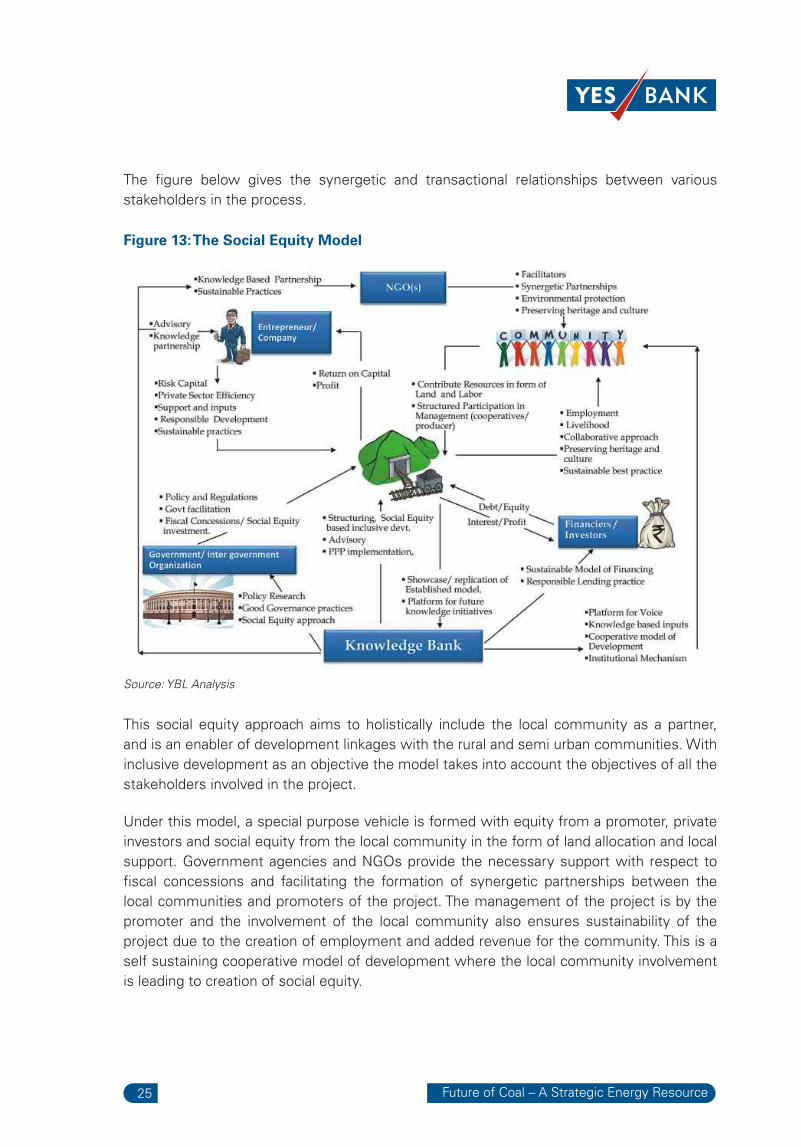

This social equity approach aims to holistically include the local community as a partner,

and is an enabler of development linkages with the rural and semi urban communities. With

inclusive development as an objective the model takes into account the objectives of all the

stakeholders involved in the project.

Under this model, a special purpose vehicle is formed with equity from a promoter, private

investors and social equity from the local community in the form of land allocation and local

support. Government agencies and NGOs provide the necessary support with respect to

fiscal concessions and facilitating the formation of synergetic partnerships between the

local communities and promoters of the project. The management of the project is by the

promoter and the involvement of the local community also ensures sustainability of the

project due to the creation of employment and added revenue for the community. This is a

self sustaining cooperative model of development where the local community involvement

is leading to creation of social equity.

Future of Coal – A Strategic Energy Resource25

Figure 13: The Social Equity Model

Source: YBL Analysis

The figure below gives the synergetic and transactional relationships between various

stakeholders in the process.

Eco System Approach

The model follows an eco system approach where sustainability of the entire eco system is

built upon smaller ecosystems which contributes to the synergetic alignment of the entire

chain. Various sub ecosystems and their inter linkages are explained below

The private player brings with him the much needed risk capital for developing resource

which along with efficiency in operation is expected to provide adequate return on

capital in terms of profitability and positive payback from investment. The Knowledge

Bank provides the private players, knowledge advisory in terms of various sustainable

development practice and good governance practice which promote and facilitate

responsible mining operations being carried out for the various stakeholders in the Eco

system.

The Government forms policies and regulations within which the mining company

operates. These policies form the broad framework of operation and adherence to the

same is required to carry out the mining activity by the SPV. The Knowledge Bank

through its policy focused research provides inputs with regards to various sustainable

best practice and good governance which can be adopted at the policy level to bring

about a change in the current mining activities enabling a comprehensive socio

economic development.

The Knowledge Bank using its Social equity approach to development brings

Community and NGO’s within the Value chain of development thereby ensuring the

sustenance of eco system. The knowledge bank through its cooperative model of

development provides inputs to NGOs and Communities too. Building on this

collaborative community model of development, the community provides inputs to the

Mining SPV in terms of land and labor in return for structured participation in

management and adoption of sustainable development practice for preservation of

heritage and culture.

Foreign investors play an instrumental role in bringing in capital and technical know- how

in the sector. This facilitates the adoption of worldwide best practices and technology

that are environmentally sustainable. The knowledge bank, through its policy focused

research can effectively advise the government on adopting policies that are globally

1. Knowledge Bank – Private Player – Mining SPV

2. Knowledge Bank – Government – Mining SPV

3. Knowledge Bank – NGO- Community – Mining SPV

4. Knowledge Bank – Foreign Investors – Government – Mining SPV

26 Future of Coal – A Strategic Energy Resource

competitive and attractive to foreign investors who bring along a gamut of benefits. The

knowledge bank could also act as a mediator by educating the foreign investors on the

country’s industry and directing efforts in the right direction.

Developmental Partnerships

• Multi Stakeholder response to local challenges as an effective tool for sustainability

• Capacity Building and cooperative structures 'enable' communities to manage and

solve their issues themselves

• Partnerships with Foreign Investors facilitate the inflow of environmentally and

socially sustainable technology

• Such partnerships provide a platform for fruitful collaborative partnerships, and also

create a strong knowledge base that pushes skill development and ensures social

equity in the growth strategies

• Partnerships with Govt./Pvt Sector/ NGOs assist in giving a larger/ global

perspective to local problems

• Policy Framework: Institutional innovation to consolidate structures that guide

communities and entrepreneurs

• An equal voice for all stakeholders

• ‘Real’ Ownership: Align aspirations and foster ownership/responsibility for common

purpose/goals

• Provide platforms, skills and opportunities for communication

Collaborative Community Models: Facilitating Inclusive Growth

Stakeholder alignment

Future of Coal – A Strategic Energy Resource27

10 - Point Roadmap toSustainable Development in Coal Mining 05

2 Future of Coal – A Strategic Energy Resource

05 | 10 - Sustainable Development in Coal Mining

Point Roadmap to

1. Enhance Policy and Regulatory Framework in Coal Mining

India has long been known for its richness of minerals. It currently stands to have the

5th largest reserve of coal in the world. Despite the abundance of coal, India has not

been able to tap its innate potential. Current policies have not been successful in

attracting foreign investors which has created a considerable lag in technological

upgradations. There is therefore a strong need to adopt policies that help revive the

industry by making its operations more resourceful and sustainable in the long run.

Moreover, policies need to focus on promoting investments through modes of Public

Private Partnerships. The establishment of a coal regulator would be timely for inducing

competition, transparency and creating a level playing field.

30 Future of Coal – A Strategic Energy Resource

Figure 14: Sustainable Development in Coal Mining

Source: Womens Mining Coalition

EconomicSustainability

2. Incorporating environmental and social sensitivities in decisions on leases

3. Benefits sharing and Community engagement

4. Logistics Infrastructure Development

5. Strategic assessment in key mining regions

This principle integrates sustainable development concepts at the earliest phase of the

mining life cycle. The underlying philosophy of the principle is to categorize mineral

bearing areas based on an environmental and social analysis taking a risk based

approach. At the bidding stage the categorization of lease areas into High and Low risk

will allow the investors to take business decisions with the knowledge that the cost

and uncertainties of getting approvals as well as operations in high risk areas will be

significantly higher than the low risk areas. It will also allow regulators to put additional

commitments at an early stage for environmental and social performance.

This principle seeks commitment to regular engagement with the local community as

well as sharing of project benefits with the affected families. It is rooted in the principle

of sharing profits with the affected communities. This entails the social impact

management of project operations with the initiatives being undertaken, looking at an

integrated approach to mitigate impacts, and improve local livelihoods and living

conditions in the affected communities.

Create an institutional mechanism for planning and development of common

infrastructural facilities for use by all the block owners. A local area development

authority could be created with participation of block allocates, coal mining companies

and the respective state governments to develop comprehensive plans for

infrastructural facilities and requirements in each identified coalfields areas. The

importance of optimization of available logistic infrastructure through source

rationalization, investment in logistics infrastructure and development of end-to-end

logistics solution companies in PPP model, and harnessing the potential of alternate

modes of transport should be the thrust areas for the Government.

Understanding that mining activities occur in clusters which have impacts at a regional

level, a strategic assessment of regional and cumulative impacts and development of a

Regional Mineral Development Plan based on an assessment of the regional "capacity"

needs to be carried out at periodic intervals is important. Creating an institutional

structure to own and implement such plans in key mining regions is critical and taking

critical decisions on mining, new leases, allocation of resources, and even possible

moratorium on mining need to be taken up to ensure more sustainable planning and

development in such regions.

Future of Coal – A Strategic Energy Resource31

6. Encourage Private Sector Participation

7. Encourage Technological Innovations and Skill Development

8. Promote Environmentally, Social and Economically Sustainable Practices

The role of private sector in the Coal mining and development has been very limited,

largely due to the restriction on end use and open commercial sale of coal. Allowing

private participation either directly or by partnering Government companies could be

the possible solution for ramping up Coal production in the country and taking the

country towards self-sufficiency. Public-Private Partnerships (PPP) and Joint-Venture

models should be the possible routes for facilitating large private sector investments in

Coal mining sector. However it has to be implemented in its true spirit and must involve

ownership, to achieve the desired results of such a partnership

Technology is the key to higher production, productivity and safety. The country is

lagging behind in terms of technology and availability and use of high technology

equipment is still below potential. International best practices and bench marks,

particularly in underground mining technologies and Clean Coal Technologies etc have

to be adopted at a faster pace to ensure cost-effective Coal mining and energy security.

There has to impetus from policy makers and management of Coal companies for

adopting these practices and also for creating cost effective cost beneficiation

technologies. The industry also has a shortage of trained workforce comprising of

engineers, diploma holders and skilled/semi-skilled workers; a major deterrent in

enhancing workforce strength and efficiency. There is therefore a pressing need to

divert investments towards expanding the human capital pool to bolster the expected

growth in future.

With the outlook of mining evolving over time, greater emphasis is now being laid on

the sustainability aspect. Sustainable Mining now encompasses practices that are

financially viable; socially responsible; environmentally, technically and scientifically

sound; with a long term view of development. To ensure overall development and

inclusive growth, it has become imperative to adopt sustainable mining practices that

encourage community participation and augment rural income and livelihood.

Moreover, there is an urging need for the government to propose an economic model

that aligns stakeholders’ expectations with sustainable profit sharing ratios that include

local communities. Mining companies should also be responsible for augmenting

infrastructure and basic amenities in these regions.

32 Future of Coal – A Strategic Energy Resource

9. Geological Explorations to Uncover Proven Reserves

10. Speedy Clearances through Single Window Systems

Coal exploration is to be speeded up exponentially to ensure availability of more

explored coal blocks for mining by the private and public sector. Majority of the

reserves in ‘Inferred’ and ‘Indicated’ categories have to be proven by detailed

exploration and ensure such information is available at least 10 years in advance to

allow projectisation and mine development. To accomplish this goal, the existing

capacities of the exploration agencies have to be enhanced and global companies have

to be invited to strengthen drilling capacities as well as technical support system both

in terms of drilling equipments and manpower.

To expedite clearances a co-ordination committee at the Centre and State level should

be set up (Single window concept) with senior representation from the concerned

departments. To ensure a leaner, transparent and efficient approval process, there is

also a need to ensure Forest and environmental clearances in a time bound manner, by

reducing the number of levels and stages. Clearances once given should be valid so

long as there is no expansion or major modifications in the mine/washery; it should not

be required afresh merely because lease is being renewed. Also to ensure there is no

wide disparity in environmental performance of coalmines in the country, a system of

third party audit or the adoption of a ‘Green Rating System’ may be established to bring

out the best practices and establish benchmarks for those not doing so well to

improve.

Future of Coal – A Strategic Energy Resource33

YES BANK, India’s fourth largest private sector Bank, is the outcome of the professional &

entrepreneurial commitment, vision & strategy of its Founder Rana Kapoor and his top

management team, to establish a high quality, customer centric, service driven, private

Indian Bank catering to the Future Businesses of India.

YES BANK has adopted international best practices, the highest standards of service quality

and operational excellence, and offers comprehensive banking and financial solutions to all

its valued customers. YES BANK has a knowledge driven approach to banking, and a superior

customer experience for its retail, corporate and emerging corporate banking clients.

YES BANK is steadily evolving its organizational character as the Professionals’ Bank of India

with the uncompromising Vision of “Building the Best Quality Bank of the World in India by

2020!

Founded in 1925, Indian Chamber of Commerce (ICC) is the leading and only National

Chamber of Commerce operating from Kolkata, and one of the most pro-active and forward-

looking Chambers in the country today. Its membership spans some of the most prominent

and major industrial groups in India. ICC is the founder member of FICCI, the apex body of

business and industry in India. ICC’s forte is its ability to anticipate the needs of the future,

respond to challenges, and prepare the stakeholders in the economy to benefit from these

changes and opportunities. Set up by a group of pioneering industrialists led by Mr G D Birla,

the Indian Chamber of Commerce was closely associated with the Indian Freedom

Movement, as the first organised voice of indigenous Indian Industry. Several of the

distinguished industry leaders in India, such as Mr B M Birla, Sir Ardeshir Dalal, Sir Badridas

Goenka, Mr S P Jain, Lala Karam Chand Thapar, Mr Russi Mody, Mr Ashok Jain, Mr.Sanjiv

Goenka, have led the ICC as its President. Currently, Mr. Roopen Roy is leading the Chamber

as it's President.

ICC is the only Chamber from India to win the first prize in World Chambers Competition in

Quebec, Canada.

ICC’s North-East Initiative has gained a new momentum and dynamism over the last few

years, and the Chamber has been hugely successful in spreading awareness about the great

economic potential of the North-East at national and international levels. Trade & Investment

shows on North-East in countries like Singapore, Thailand and Vietnam have created new

vistas of economic co-operation between the North-East of India and South-East Asia. ICC

has a special focus upon India’s trade & commerce relations with South & South-East Asian

nations, in sync with India’s ‘Look East’ Policy, and has played a key role in building synergies

between India and her Asian neighbours like Singapore, Indonesia, Bangladesh, and Bhutan

through Trade & Business Delegation Exchanges, and large Investment Summits.

ICC also has a very strong focus upon Economic Research & Policy issues - it regularly

undertakes Macro-economic Surveys/Studies, prepares State Investment Climate Reports

and Sector Reports, provides necessary Policy Inputs & Budget Recommendations to

Governments at State & Central levels.

The Indian Chamber of Commerce headquartered in Kolkata, over the last few years has truly

emerged as a national Chamber of repute, with full-fledged offices in New Delhi, Guwahati,

Patna and Bhubaneshwar functioning efficiently, and building meaningful synergies among

Industry and Government by addressing strategic issues of national significance.

DELHI OFFICE

TelFax

D – 118, 1st FloorAashirwad ComplexGreen Park MainNew Delhi - 110 016

: +91-11-4610 1431 to 1439: +91-11-4610 1440 & 1441

GUWAHATI OFFICE

Tel :Fax :

House No. - 209, R. G. Baruah Road(Near - AIDC) Opp. Overnite CourierGuwahati - 781024, Assam

+91-361-2460216/2464767+91-361-2461763

BIHAR STATE OFFICE

Tel :Fax :

11/B DUMRI HOUSEKavi Raman PathEast Boring RoadPatna - 800001, Bihar

+91-612- 6500357+91-612- 2533636

JHARKHAND STATE OFFICE

Tel :Fax :

181 - CROAD NO. - 4ASHOK NAGARRANCHI - 834002, Jharkhand

+91-651-2243236+91-651-2243236

ODISHA STATE OFFICE

Tel :Fax :

11, Kharavela Nagar1st Floor, Unit-III Bhubaneswar - 751001, Odisha

+91-674-2532744/2534744+91-674-2533744

State offices of ICC