Embed Size (px)

Citation preview

FX Forecast UpdateTaking a breather before next leg of ‘central-bank exit pricing’

16 August 2017

Follow us on Twitter @Danske_Research

Important disclosures and certifications are contained from page 30 of this report

Thomas Harr

Global Head of FICC Research

Christin Tuxen

Chief Analyst

Jakob Ekholdt Christensen

Chief Analyst

Allan von Mehren

Chief Analyst

Nicolai Pertou Ringkøbing

Assistant Analyst

Kristoffer Kjær Lomholt

Senior Analyst

Morten Helt

Senior Analyst

Stefan Mellin

Senior Analyst

Jens Nærvig Pedersen

Senior Analyst

Vladimir Miklashevsky

Senior Analyst

Aila Mihr

First Year Analyst

Investment Research

www.danskebank.com/CI

22

• EUR/NOK. We have reached our 1M forecast of 9.30. As written in the last update, we think the near-term downside potential fromhere is more limited for two reasons. First, given below target inf lation, the level of the NOK and the cooling housing market we do notthink Norges Bank is likely to hike rates before mid-2018. Secondly, the upside potential for the oil price seems more limited on theback of US producers re-entering the market for an oil price rise of USD3-5 from here. Also, long NOK positions have becomeincreasingly crowded, albeit not historically stretched so. The Norwegian normalisation story, valuation and real rates remain clearNOK positives but we think we will first have to see the cross range trade in the 9.25-9.45 range in the coming months. We leave ourforecasts unchanged.

• EUR/SEK. The SEK’s advance vs the EUR over the summer has been fundamentally justified on the back of a very strong GDP and much-higher-than-expected inflation data in our view. The recent (inflation) numbers must be followed by a clear hawkish shift by the Riksbank ifEUR/SEK is to fall substantially lower in our view. While we do expect an adjustment to the Riksbank’s language, we think it will make onlymarginal policy adjustments which may clash with current pricing (rate hikes and sharp drop in KIX) at the September meeting. We thinkthat the Riksbank will put an end to QE in December, which could prompt a steeper yield curve and lend support to the SEK. On balance, welower our EUR/SEK profile to 9.50 (9.60) in 1M, 9.40 (9.50) in 3M, 9.30 (9.40) in 6M and 9.20 (9.30) in 12M.

• EUR/DKK. Danmarks Nationalbank (DN) has not needed to intervene in the FX market for the past four months as EUR/DKK hastraded close to 7.4400. In particular, it is noteworthy that EUR/DKK has not responded to the recent strong rally in EUR partly on theback of repricing of ECB monetary policy. We forecast EUR/DKK will trade at 7.4400 in 1-12M.

• EUR/USD. We have left our forecasts unchanged and maintain the view we laid out in FX Strategy: More upside for EUR/USD in store, 25July, where we pencilled in EUR/USD at 1.17 in 1-3M, as we see the summer level shift as permanent even if upside should be cappednear term by stretched positioning and a cyclical turn in the US. Longer term, support from the ECB and valuation is set to take us to 1.18in 6M and 1.22 in 12M. Fundamentally, we view EUR/USD as still undervalued and the big move that investors should focus on is a higherEUR/USD. We maintain that any dips in EUR/USD are likely to prove short-lived and maintain that we are headed towards the mid-1.20swhen the pricing of an ECB exit gains further traction.

Forecast review part I

33

• EUR/GBP. Over the coming 1-3 months, we expect EUR/GBP to test higher on the back of a strong EUR and BoE repricing. We targetEUR/GBP at 0.91 in 1-3M, expecting the cross to trade within a narrow range of 0.90-0.92. Longer term, we continue to see somestabilisation in GBP on the back of potential for clarification regarding the Brexit negotiations and valuations. However, as relative growthand relative monetary policy are set to remain EUR/GBP supportive in the medium term, we see only modest downside potential in the yearahead. We target 0.90 in 6M and 0.88 in 12M. We leave our forecasts for EUR/GBP unchanged.

• USD/JPY. We still expect the broader trading range for USD/JPY of 108-115 to hold over the next 3-6 months, and while both US andJapanese domestic politics and not least North Korea remain key downside risk factors for USD/JPY, a dovishly priced Fed and shortUSD positioning look set to support the cross in the coming months. We target USD/JPY at 111 in 1M (prev. 114) and 114 in 3M.Longer term, we still expect the JPY to underperform vis-à-vis USD and EUR driven by real interest rates and portfolio outf lows fromJapan. We target USD/JPY at 116 in 6-12M.

• USD/CNY. We lower our forecast for USD/CNY yet again as the cross continues to surprise on the downside, pulled lower by USDweakness. Our forecast is now 6.75 (6.9) on 3M, 6.80 (6.95) on 6M and 6.95 (7.1) on 12M. Further USD depreciation is set to putdownside pressure on USD/CNY, while slowing growth in China, Fed hikes and Chinese financial risks will create upward pressure onthe cross. EUR/CNY has moved in line with our expectations and we keep the forecast broadly unchanged looking for 8.48 (8.38) on12M – hence continued weakening of the CNY versus the EUR. This is weaker than the forward market and we continue to recommendhedging of CNY receivables.

• EUR/CHF. As we noted in FX Research: EUR/CHF: Patient SNB to let 'reverse gravity' gain traction, 9 August, the SNB will make sure tokeep a distance to an eventual ECB exit as Switzerland still needs a helping hand from CHF depreciation to effectively escape deflationaryterritory. Near term, the euro uptick may take a breather but we still see SNB being more than happy to let EUR/CHF edge towards 1.20before considering its own exit from negative rates. We keep our forecast profile unchanged and thus still look for the cross to trade at1.14 in 1-3M, 1.16 in 6M, and 1.20 in 12M as the pricing of an ECB exit gains traction.

Forecast review part II

44

• USD/RUB. Given persisting external risks for the RUB and possible downside risks from the oil price, we roll the current RUB levels. Weexpect RUB and oil price divergence to shrink on worsened sentiment. Expecting USD/RUB at 60.00 in 1M, 59.40 in 3M, 54.70 in 6Mand 53.50 in 12M.

• USD/TRY. We see good prospects for the TRY in the short term supported by encouraging macro fundamentals and attractive carry,while staying more cautious in the medium to long term. Surprise easing by the Turkish central bank on political pressure andimproving macro is further downside risk to our TRY forecasts. We roll our USD/TRY forecasts as follows: 3.60 in 1M, 3.65 in 3M,3.80 in 6M, and12M view at 4.00.

• EMEA. Developments in the HUF and PLN have been strikingly different over the past month. While the PLN has been hit by a renewedstandoff with the EU, the HUF has been aided by the strength of the Hungarian economy sending EUR/HUF down to levels not seensince early 2015. We think that the uncertain relations with the EU (possible suspension of Poland’s EU voting rights) will weigh on theoutlook for the PLN despite the underlying economic strength. We have therefore raised the forecast path for EUR/PLN to 4.26 in 1M(4.18 previously), 4.24 in 3M (4.16 previously), falling to 4.18 in 6M (4.14 previously) and 4.16 in 12M. In the case of the HUF, we thinkthat the NBH liquidity measures will cap further upside near term but we expect the strong external balance and an undervaluedexchange rate to aid the currency in the longer term. In light of the recent move, we lower our short-term EUR/HUF forecast to 305 in1M (308 previously), 306 in 3M, 304 in 6M and 300 in 12M.

• EUR/CZK. Following the first CNB interest rate hike in August, we look for further EUR/CZK depreciation ahead, based on relative monetarypolicy divergence as well as strong Czech economic fundamentals. Profit-taking on sizeable short EUR/CZK positions accumulated in themarket will, however, prevent any rapid CZK appreciation. As a reaction to the CNB move, we have slightly lowered our short-termEUR/CZK forecast profile to 26.00 in 1M, 25.90 in 3M, 25.70 in 6M and 25.50 in 12M.

Forecast review part III

55

• AUD, NZD, CAD. The global business cycle environment has turned increasingly positive for the traditional G10 and commoditycurrencies over the last months. Meanwhile, we still think the upturn in China will prove temporary post the Chinese CommunistCongress in autumn which limits the medium- to longer- term upside potential (see China leading indicators – summer rebound – butstill slowdown ahead, 3 August). Also, with the US tightening cycle likely to continue amid indications of a forthcoming re-accelerationin the US economy it should add some downside pressure on the three currencies vis-à-vis- the USD. In terms of central bank pricingwe pencil in one Bank of Canada hike over the coming year (markets price almost two). We do not expect Reserve Bank of Australia orReserve Bank of New Zealand to hike rates in the coming year (markets price a little more than 50% probability for both). As such weregard relative rates as negative for the three. Fundamentally, CAD seems undervalued while AUD and NZD seem overvalued (versusUSD). We now forecast AUD/USD at 0.78 in 1M (previously 0.77), 0.76 in 3M (0.75), 0.75 in 6M (0.74) and 0.75 in 12M (0.74),NZD/USD at 0.72 in 1M (unchanged), 0.71 in 3M (unchanged), 0.70 in 6M (unchanged) and 0.70 in 12M (unchanged) and finallyUSD/CAD at 1.28 in 1M (unchanged), 1.30 in 3M (unchanged), 1.33 in 6M (unchanged) and 1.34 in 12M (unchanged).

Forecast review part IV

66

Forecast: 9.30 (1M), 9.30 (3M), 9.10 (6M), 9.00 (12M)• Growth. The data releases received during summer continue to

show a recovering economy. The labour market reports still suggestabove-trend-growth, the manufacturing sector is stabilising andprivate consumption is picking up driven by improved confidenceand higher real wages. The housing market continues to cool –especially in Oslo – but we do not pencil in any dramatic real effectson the economy. The yearly core inflation rate has as expected fallenbut the decline has been less than expected (see overleaf).

• Monetary policy. As expected, Norges Bank (NB) left the sightdeposit rate unchanged at 0.50% at the June meeting. The Boardmaintained the ‘neutral bias’ introduced back in September 2016,and stated that ‘the Executive Board’s current assessment of the

outlook and the balance of risks suggests that the key policy rate will

remain at today’s level in the period ahead’. NB also announced thatthe decision was ‘unanimous’. Importantly, the 40% cut probabilityembedded into the rate path was removed, thereby mirroring thesignals from the ECB. We think NB will leave rates unchanged forthe rest of this year and pencil in the first hike in mid-2018.

• Flows. Foreign banks (proxy for speculative flows) have over the pastmonths increased their long positions considerably. However, overallwe still estimate that NOK positioning is ‘neutral’.

• Valuation. From a long-term perspective, the NOK seemsfundamentally undervalued. Our PPP model has 8.43 as a long-termfair-value anchor.

• Risks. The biggest risk factor to our forecast is a global risk-off eventthat would weigh on oil prices and send the cross higher.

EUR/NOK – in for range trading over the next few months

Conclusion. We have reached our 1M forecast of 9.30. Aswritten in the last update, we think the near-term downsidepotential from here is more limited for two reasons. First,given below target inflation, the I44 (see overleaf) and thecooling housing market we do not think NB is likely to hikerates before mid-2018. Secondly, the upside potential forthe oil price seems more limited on the back of USproducers re-entering the market for an oil price rise ofUSD3-5 from here. Also, long NOK positions have becomeincreasingly crowded, albeit not historically stretched so.

The Norwegian normalisation story, valuation and realrates remain clear NOK positives but we think we will firsthave to see the cross range trade in the 9.25-9.45 range inthe coming months. We leave our forecasts unchanged.

Kristoffer Kjær Lomholt, Senior Analyst, [email protected], +45 45 12 85 29

Source: Danske Bank

EUR/NOK 1M 3M 6M 12M

Forecast (pct'ile) 9.30 (41%) 9.30 (42%) 9.10 (25%) 9.00 (23%)

Fwd. / Consensus 9.35 / 9.32 9.38 / 9.25 9.41 / 9.16 9.47 / 8.99

50% confidence int. 9.22 / 9.47 9.16 / 9.57 9.10 / 9.67 9.01 / 9.82

75% confidence int. 9.13 / 9.57 9.01 / 9.74 8.88 / 9.93 8.72 / 10.18

k

8.50

8.75

9.00

9.25

9.50

9.75

10.00

10.25

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

EUR/NOK

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

77

• Yearly core inflation has fallen …

− As expected the yearly core inflation rate fell significantly lastmonth: from 1.6% in June to 1.2% in July. The drop was notleast driven by base effects from the strong rise in July foodprices last year but also a record drop in clothes prices thisyear acted as a drag. Meanwhile, airfares did not correct afterthe surprisingly strong June, adding a positive contribution tothe monthly print. As expected food prices was the largestpositive contributor to the print.

• … but by less than pencilled in by Norges Bank

− With the June and July inflation prints behind us, we now onlyhave one print left ahead of the 21 September Norges Bankmeeting. Meanwhile, already at this stage it seems likely thatinflation will be a significant positive factor for the revised ratepath. Historically, the current inflation gap would raise thefront-end of the rate path by more than half a full 25bp interestrate hike.

The stronger NOK will counter inflation rate path effect

− On the back of the July NOK rally, the import-weighted NOK(I44) is now 2% stronger than pencilled in by Norges Bank.Historically, that is a substantial gap, which would have anegative effect on the rate path of almost the same size as thepositive inflation effect above. In other words, the currencyeffect will counter the inflation effect and since inflation is stillbelow target and with the housing market cooling we do notexpect any interest rate hikes before mid-2018.

EUR/NOK – important issues to watch

… but the stronger NOK will counter the rate path

effect at this stage

Source: Macrobond Financial, Norges Bank, Danske Bank

The yearly core inflation rate has fallen less than

expected by Norges Bank

Source : Macrobond Financial, Norges Bank, Danske BankKristoffer Kjær Lomholt, Senior Analyst, [email protected], +45 45 12 85 29

88

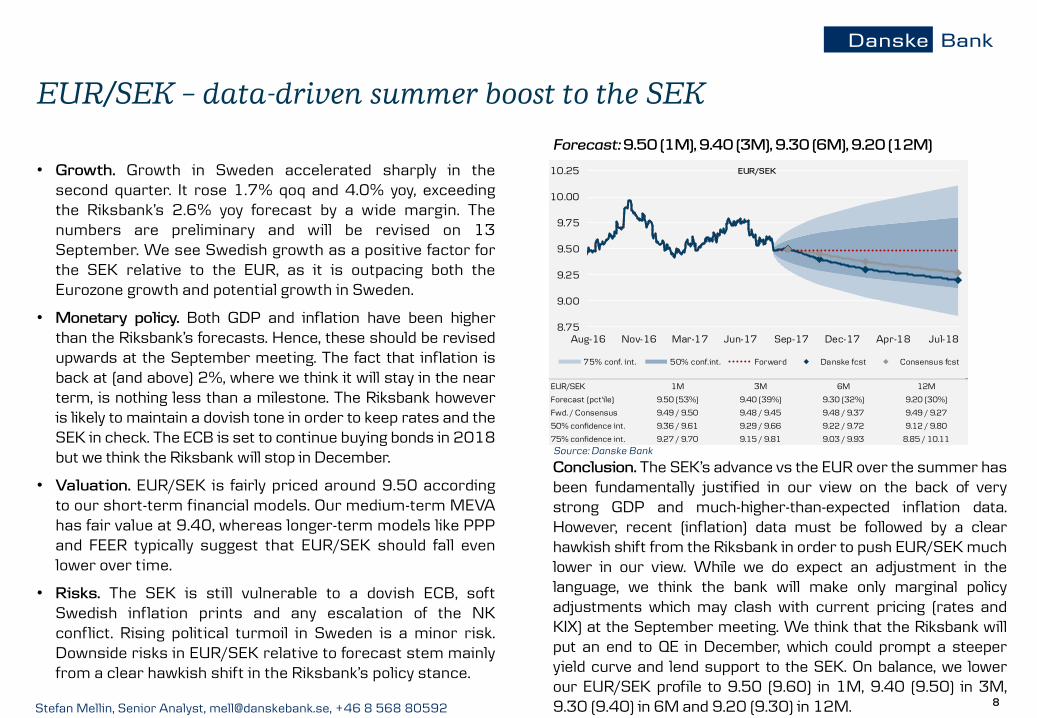

Forecast: 9.50 (1M), 9.40 (3M), 9.30 (6M), 9.20 (12M)

• Growth. Growth in Sweden accelerated sharply in thesecond quarter. It rose 1.7% qoq and 4.0% yoy, exceedingthe Riksbank’s 2.6% yoy forecast by a wide margin. Thenumbers are preliminary and will be revised on 13September. We see Swedish growth as a positive factor forthe SEK relative to the EUR, as it is outpacing both theEurozone growth and potential growth in Sweden.

• Monetary policy. Both GDP and inflation have been higherthan the Riksbank’s forecasts. Hence, these should be revisedupwards at the September meeting. The fact that inflation isback at (and above) 2%, where we think it will stay in the nearterm, is nothing less than a milestone. The Riksbank howeveris likely to maintain a dovish tone in order to keep rates and theSEK in check. The ECB is set to continue buying bonds in 2018but we think the Riksbank will stop in December.

• Valuation. EUR/SEK is fairly priced around 9.50 accordingto our short-term financial models. Our medium-term MEVAhas fair value at 9.40, whereas longer-term models like PPPand FEER typically suggest that EUR/SEK should fall evenlower over time.

• Risks. The SEK is still vulnerable to a dovish ECB, softSwedish inflation prints and any escalation of the NKconflict. Rising political turmoil in Sweden is a minor risk.Downside risks in EUR/SEK relative to forecast stem mainlyfrom a clear hawkish shift in the Riksbank’s policy stance.

EUR/SEK – data-driven summer boost to the SEK

Conclusion. The SEK’s advance vs the EUR over the summer hasbeen fundamentally justified in our view on the back of verystrong GDP and much-higher-than-expected inflation data.However, recent (inflation) data must be followed by a clearhawkish shift from the Riksbank in order to push EUR/SEK muchlower in our view. While we do expect an adjustment in thelanguage, we think the bank will make only marginal policyadjustments which may clash with current pricing (rates andKIX) at the September meeting. We think that the Riksbank willput an end to QE in December, which could prompt a steeperyield curve and lend support to the SEK. On balance, we lowerour EUR/SEK profile to 9.50 (9.60) in 1M, 9.40 (9.50) in 3M,9.30 (9.40) in 6M and 9.20 (9.30) in 12M.

Source: Danske Bank

Stefan Mellin, Senior Analyst, [email protected], +46 8 568 80592

EUR/SEK 1M 3M 6M 12M

Forecast (pct'ile) 9.50 (53%) 9.40 (39%) 9.30 (32%) 9.20 (30%)

Fwd. / Consensus 9.49 / 9.50 9.48 / 9.45 9.48 / 9.37 9.49 / 9.27

50% confidence int. 9.36 / 9.61 9.29 / 9.66 9.22 / 9.72 9.12 / 9.80

75% confidence int. 9.27 / 9.70 9.15 / 9.81 9.03 / 9.93 8.85 / 10.11

k

8.75

9.00

9.25

9.50

9.75

10.00

10.25

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

EUR/SEK

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

99

Growth, inflation and the Riksbank

• Growth in Q2 came in much stronger than forecast andlifted the SEK temporarily. The revised numbers are duefor release on 13 September and will be closely watched.The growth backdrop is fundamentally SEK positive. Notehowever, that the threshold for beating expectations hasrisen (surprise index at historically high levels) whichraises the risk of a period of macro disappointments.

• Inflation is back at (and above) 2%. Great news for theRiksbank, which has not seen inflation above target formore than six years! Inflation expectations (Prospera) havebeen re-anchored. Although some of the inflation driverslook temporary – the Riksbank seems to share this view -we see CPIF running above 2.0% for the next few months.

• Domestic macro developments including inflation suggestthat the Riksbank will take another step towards lessaccommodative monetary policy in September. We think itwill err on the side of caution though, in order to mitigateany premature tightening of financial conditions, includingtoo fast an appreciation of the krona. Note that the SEK isalready trading nearly 3% stronger than the Riksbankforecast. We think the Riksbank will end QE in December(while the ECB will continue), which may prompt asteepening of the Swedish yield curve and a stronger SEK.

EUR/SEK – important issues to watch

Inflation has surprised substantially on the upside

Source: Macrobond Financial, Danske Bank

Source: Macrobond Financial, Danske Bank, Riksbank

Stefan Mellin, Senior Analyst, [email protected], +46 8 568 80592

EUR/SEK vs 10y swap spread

1010

• FX. Danmarks Nationalbank (DN) has not needed to intervene inthe FX market for the past four months as EUR/DKK has tradedclose to 7.4400. In particular, it is noteworthy that EUR/DKKhas not responded to the recent strong rally in EUR partly onthe back of repricing of ECB monetary policy. We forecastEUR/DKK will trade at 7.4400 in 1-12M.

• Rates. We expect DN to keep the rate of interest on certificatesof deposit (CD rate) unchanged at -0.65% in 12M. Should theECB lift its deposit rate over the next year (not our mainscenario), we would expect DN to increase the CD ratecorrespondingly as we expect DN to value a less negative policyrate more highly than a higher EUR/DKK spot.

• Flows. The Danish current account surplus is growing againand is on track to exceed 9% of GDP this year, adding strongfundamental support to DKK. More than one-third of the surplusis earned in the US, so we expect the DKK market to monitorclosely what policies President Donald Trump implements. Inour view, a ‘Homeland Investment Act 2’ would probably notlead to significant flows out of DKK, as US companies have lowforeign direct investment in Denmark.

• Regulation. On 1 October 2017, the so-called liquidity coverageratio (LCR) in significant currencies will be raised to 100% forDanish banks. On 1 January 2018, the general LCR will beraised to 100% for European and smaller Danish banks.

EUR/DKK – not biting on EUR rally

• Liquidity. Conditions in the DKK money market havenormalised on the back of DN selling DKK via FXintervention and buybacks of government bonds. TheDMO has ample government deposits to continuegradual DGB buybacks for the rest of the year to supportDKK liquidity and the secondary DGB market. In the pastcouple of months the DMO looks to have stepped upbuybacks slightly.

• Conclusion. We expect EUR/DKK to continue to tradearound 7.4400 on 12M. We could see some temporarysupport in H2 before the implementation dates of furthertightening of the LCR requirements.

Source: Macrobond Financial, Danske Bank

Jens Nærvig Pedersen, Senior Analyst, [email protected], +45 45 12 80 61

Forecast: 7.4400 (1M), 7.4400 (3M), 7.4400 (6M) and 7.4400 (12M)

1111

Forecast: 1.17 (1M), 1.17 (3M), 1.18 (6M), 1.22 (12M)• Growth. US data have made a marked turn for the better inrecent months and our quantitative business-cycle modelssuggest that the US economy is set to recover in H2. Incontrast, the eurozone has seemingly lost some growthmomentum lately and our models suggest this will continuenear term. There is renewed optimism regarding the outlookfor the eurozone following populist parties losing support.

• Monetary policy. ECB’s Draghi in our view let the euro out ofthe bottle when he spoke at the late-June Sintra conference,revealing that the ECB is starting to flirt with exit discussions.While a first 10bp hike from the ECB is priced a bit early atpresent (around New Year 2018/19) we stress that key forthe FX market is the direction in which the ECB is now headed.Albeit challenged by the lack of sustained inflationarypressure, the Fed looks eager to move on with both rate hikes(next in December in our view which is priced with only 40%probability) and balance-sheet reduction (QT) near term, butmay, as a result, be forced to pause further out.

• Flows. Eurozone equity inflows have been a key driver ofEUR/USD upside recently but may be fading. The euro-areacurrent-account surplus versus a US deficit implies that the’natural’ f low remains EUR/USD positive. Speculators arenow stretched on EUR/USD longs (IMM data).

• Valuation. The Danske Bank G10 MEVA model suggeststhat fair value for the cross is around 1.27; PPP at 1.30.

• Risks. The risk of a political and/or banking crisis in Italycannot be dismissed and could weigh on the EUR if flares up.

EUR/USD – heading for the 1.20s once pricing of ECB exit resumes

Conclusion. EUR/USD has staged a significant upturn in recentmonths driven first by political risks abating following the Frenchelection, and thereafter by ECB letting the exit discussion out. Whilethe latest uptick has not been shadowed by the usual short-termfactors such as relative interest rates, unhedged equity flows appearto have played a key role in supporting the single currency. We thinkthe cross is currently in a consolidation phase and will stay range-bound around the 1.17 level near term. We have left our forecastsunchanged and thus we maintain the view we laid out in FX Strategy:More upside for EUR/USD in store, where we pencilled in EUR/USDat 1.17 in 1-3M as we see the summer level shift as permanenteven if upside should be capped near term by stretched positioningand a cyclical turn in the US. Longer term, support from the ECB andvaluation is set to take us to 1.18 in 6M and 1.22 in 12M.

Source: Danske Bank

Christin Tuxen, Chief Analyst, [email protected], +45 45 13 78 67

EUR/USD 1M 3M 6M 12M

Forecast (pct'ile) 1.17 (48%) 1.17 (44%) 1.18 (48%) 1.22 (63%)

Fwd. / Consensus 1.17 / 1.16 1.18 / 1.16 1.18 / 1.16 1.20 / 1.18

50% confidence int. 1.15 / 1.19 1.15 / 1.20 1.14 / 1.22 1.14 / 1.25

75% confidence int. 1.14 / 1.20 1.13 / 1.23 1.11 / 1.25 1.08 / 1.29

k

1.00

1.10

1.20

1.30

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

EUR/USD

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

1212

EUR/USD – important issues to watch

Source: Macrobond Financial, Danske Bank

Source: Macrobond Financial, Danske Bank

Peripheral spreads fading as a key EUR driver (for now)

Danske Bank ETF equity flow data suggesting EUR

inflows picked up early 2017

Christin Tuxen, Chief Analyst, [email protected], +45 45 13 78 67

Eurozone equity inflows may provide less support

• Unhedged equity f lows into the eurozone have seemingly been a key factor behind the euro uptrend in H1. First, Danske Bank ETF flow data on assets under management in eurozone equity ETFs suggest EUR inflows outpaced those into USD in the first half of the year. Second, IMM positioning data suggest commercial positioning in EUR has reversed, a hint that real-money funds and corporates are hedging less of their EUR exposure.

• On a 1-3M horizon the recent turn in f lows into the top-3 eurozone equity ETFs (Vanguard, iShares, SPDR – see chart) hints at support to the euro from positive equity sentiment may be fading. Also, the EUR/USD forward premium makes hedging EUR assets attractive from a US point of view, which implies that some US investors may start to hedge EUR equity exposure to a greater extent again, thus taking away some of the support to EUR/USD from equity f lows.

Italy – a key euro risk factor not to be forgotten

• In Significant challenges for Italy: All you need to know about key issues, 14 August, we take a look at a potential upcoming risk factor for the Eurozone: the forthcoming Italian general election, likely to take place in Q1 next year.

• In our base case of limited Italian tensions, we see this playing only a minor role for EUR crosses throughout our forecast horizon: it would merely have the potential to limit the appreciation pace for EUR crosses heading into 2018.

• However, in our risk scenario of a debt/political crisis unfolding in Italy, we would expect some sell-off in the single currency as this would (again) put the future of the eurozone back on the table, in the form of either the issue of an Italian bailout and/or a referendum on euro membership. Short EUR/CHF and EUR/Scandies look attractive in such an environment.

1313

Forecast: 0.91 (1M), 0.91 (3M), 0.90 (6M) and 0.88 (12M)• Growth. The UK economy has slowed substantially and while GBP

growth in Q2 accelerated to 0.3% q/q from 0.2% q/q in Q1, GDPgrowth in H1 17 was the weakest since the European debt crisis.The near-term growth outlook remains subdued as real wagegrowth has turned negative, implying less scope for privateconsumption growth. CPI inflation is running at relatively high levelsand could peak at around 3% later this year. Additional uncertaintyfollowing the UK general election adds to the risk of slowing activity.

• Monetary policy. The Bank of England (BoE) maintained the BankRate at 0.25% in August and kept the targets for the governmentbond purchases and corporate bond purchases at GBP435bn andGBP10bn, respectively. The vote count for the Bank Rate was 6-2against 5-3 last time, which was interpreted dovishly. In our view,it underscores that a rate hike is not imminent, and we still expectthe BoE to remain on hold until the Brexit negotiations areconcluded in spring 2019. The main reasons are that we think thebank is still too optimistic on both wage growth and GDP growthand political uncertainty remains high due to Brexit.

• Flows. Speculators are positioned neutrally in GBP but stretchedlong EUR (IMM). The UK runs a current-account deficit – notablyagainst EU countries – whereas the euro area has a surplus.

• Valuation. Our G10 MEVA model puts EUR/GBP at 0.77, while ourPPP estimate is 0.76.

• Risks. Uncertainty regarding the new government adds risks to theBrexit negotiations and this prolonged uncertainty will likely keepGBP undervalued and volatile for longer.

EUR/GBP – strong EUR and BoE on hold to underpin the cross near term

Conclusion. Over the coming 1-3 months, we expect EUR/GBP totest higher on the back of a strong EUR and BoE repricing. Wetarget EUR/GBP at 0.91 in 1-3M expecting the cross to tradewithin a narrow range of 0.90-0.92.

Over 3-12M, we continue to see some stabilisation in GBP,expecting EUR/GBP to drift back below 0.90 on the back ofpotential for clarifications regarding the Brexit negotiations andvaluations. However, as relative growth and relative monetarypolicy are set to remain EUR/GBP supportive in the mediumterm, we see only modest downside potential in the year ahead.We target 0.90 in 6M and 0.88 in 12M.

Source: Danske Bank

Morten Helt, Senior Analyst, [email protected], +45 45 12 85 18

EUR/GBP 1M 3M 6M 12M

Forecast (pct'ile) 0.91 (50%) 0.91 (49%) 0.90 (40%) 0.88 (30%)

Fwd. / Consensus 0.91 / 0.90 0.91 / 0.90 0.91 / 0.90 0.92 / 0.90

50% confidence int. 0.90 / 0.92 0.89 / 0.93 0.88 / 0.94 0.87 / 0.96

75% confidence int. 0.89 / 0.94 0.87 / 0.95 0.86 / 0.97 0.83 / 1.00

k

0.80

0.85

0.90

0.95

1.00

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

EUR/GBP

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

1414

Divided cabinet complicates Brexit negotiations

− The third round of Brexit negotiations is set to take place in Brusselsbetween 28 August and 4 September. Previously, the EU’s chiefnegotiator Michel Barnier, had said the negotiations were proceedingtoo slowly, meaning that negotiations in phase 1 (divorce bill, citizens’rights and Irish border) may not be concluded in October as hoped for.If not, the next possibility is in December, when the next EU summitafter the one in October takes place.

− The UK government is expected to publish a series of position paperson the divorce bill and the Irish border issue over the coming months– one tranche before the third round of the negotiations and thesecond before the fourth round Markets will focus on whether the UKis willing to compromise in order to reach an agreement. In our view,the divorce bill remains the biggest obstacle to the negotiations. TheDaily Telegraph reported that the UK is ready to pay a divorce bill ofEUR40bn (against the EU’s estimates in the range of EUR60-100bn)but only if the EU starts negotiations about the future relationship.

What Brexit means for fundamental GBP estimates

− What matters for sterling longer term are the Brexit terms – and theprospects for these have not become more favourable following theelection result as negotiating power has essentially shifted from theUK to the EU.

− A possible scenario could be a 10% deterioration in UK terms oftrade vis-à-vis the eurozone. Incorporating this into our Brexit-corrected medium-term valuation (MEVA) model, our estimate forEUR/GBP is around 0.83, which suggests that even when Brexituncertainty is out of the way, GBP is not necessarily set for large-scale appreciation.

EUR/GBP – important issues to watch

Source: Danske Bank

Brexit timeline

‘Brexit’-corrected MEVA estimate for EUR/GBP: 0.83

Source: Danske Bank

Morten Helt, Senior Analyst, [email protected], +45 45 12 85 18

1515

Forecasts: 111 (1M), 114 (3M), 116 (6M) and 116 (12M)• Macro outlook. Exports have shown signs of weakness in Q2 after afew impressive quarters. However, the Q2 Tankan report and thePMIs continue to paint a positive economic outlook and domesticdemand has also shown signs of improvement recently with bothretail sales and consumer confidence looking fairly good. We expectthe economy to continue to expand in the coming year and expect afurther increase in the already positive output gap. Consumer priceinf lation (CPI) remains low, standing at 0.4 % y/y in June and wageinflation also remains low.

• Monetary policy. The Bank of Japan (BoJ) has explicitly promised tocontinue easing until inflation expectations are above the 2% targeton a sustainable basis. In our main scenario, we expect the BoJ tokeep its policy unchanged: maintaining the short-term policy interestrate at -0.1% and the 10Y Japanese government bond (JGB) yield at0% throughout our 12M forecast horizon assuming that BoJgovernor Koruda will be reappointed when his term as governor endsin April 2018.

• Flows. Japan runs a sizable current-account surplus while theopposite is the case for the US. Speculators are short JPY,suggesting risks are tilted to the downside for USD/JPY from apositioning point of view.

• Valuation. PPP is around 83, while our MEVA model suggests that105 is ‘fundamentally’ justified.

• Risk. USD/JPY remains highly correlated with yields on 10-year USgovernment bonds and risk appetite. Further escalation in the tensionsbetween the US and North Korea, could initially lead to JPYappreciation via the risk channel. However, if it develops into an outrightwar, it is less clear that this would be JPY positive.

USD/JPY – rising downside risks but steady soft BoJ supports USD/JPY

Conclusion. Broad-based USD weakness and more recently risingtensions between the US and North Korea have weighed on thecross over the past month and countered the steady soft stancefrom the BoJ. As such, we still expect the broader trading range forUSD/JPY of 108-115 to hold over the next 3-6 months, and whileboth US and Japanese domestic politics and not least North Korearemain key downside risk factors for USD/JPY, a dovishly pricedFed and short USD positioning look set to support the cross in thecoming months. We target USD/JPY at 111 in 1M (previously114) and 114 in 3M. Longer term, we still expect the JPY tounderperform vis-à-vis USD and EUR driven by real interest ratesand portfolio outflows from Japan. We target USD/JPY at 116 in6-12M.

Source: Danske Bank

Morten Helt, Senior Analyst, [email protected], +45 45 12 85 18

USD/JPY 1M 3M 6M 12M

Forecast (pct'ile) 111.00 (52%) 114.00 (77%) 116.00 (79%) 116.00 (73%)

Fwd. / Consensus 110.58 / 111.53 110.57 / 113.00 110.56 / 114.51 110.55 / 114.75

50% confidence int. 108.88 / 112.52 107.77 / 113.62 106.60 / 114.97 104.96 / 116.48

75% confidence int. 107.29 / 113.73 105.13 / 115.72 102.65 / 118.03 99.55 / 120.96

k

95

100

105

110

115

120

125

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

USD/JPY

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

1616

USD/JPY – important issues to watchRising political uncertainty the main risk to BoJ’s policy

− The main risk to the BoJ’s extremely accommodative policy stance is PMAbe’s plummeting approval ratings. Recently they have tumbled to around35% in the wake of a series of scandals involving him and his close politicalallies and accusations that Abe used his influence to secure the approval ofa new department at a university run by a close friend.

− While a possible change of political leadership is not likely to affectmonetary policy in the short term, the further increase in politicaluncertainty could lead to a repricing of the BoJ further out the curve, ifmarkets start to speculate that Abenomics is coming to an end. The nextimportant election is not until the general Lower House election inDecember 2018 and Abe thus still has time to regain voters’ trust.However, this theme could develop during the autumn, and represents adownside risk to EUR/JPY and USD/JPY, if further scandals emerge orOctober’s by-election in the Shikoku area turns into defeat.

We expect BoJ to keep YCC unchanged despite rising global yields

− BoJ has explicitly promised to continue easing until inflation expectations areabove the 2% target on a sustainable basis. Even the BoJ believes that it willtake some time before this is achieved, and in our main scenario, we expectthe BoJ to keep its policy unchanged throughout our 12M forecast horizon.In July, the BoJ demonstrated its strong commitment to the yield curvecontrol by announcing an unlimited fixed-rate purchase of 10Y JGBs. TheBoJ’s strong easing bias stands in contrast to other major central banks(ECB, BoC and BoE,) which have all recently shifted their communications ina more hawkish direction.

− An increase in global yields could indeed put renewed pressure on the BoJand test its willingness to maintain its current yield curve control policy.However, in order to avoid tightening signals, we think the bar for policychanges is very high.

Source: Bloomberg, Danske Bank

Source: Bloomberg, Danske Bank

Abe’s approval rating is plummeting

Morten Helt, Senior Analyst, [email protected], +45 45 12 85 18

BoJ likely to maintain 0% ceiling on 10Y JGB

1717

Forecast: 1.14 (1M), 1.14 (3M), 1.16 (6M), 1.20 (12M)• Growth. Swiss economic indicators have continued to surpriseon the upside lately with notably the KOF indicator hovering atstrong levels. Unemployment remains low, both relative topeers and by historical standards, steady at 3.0% and theSwiss economy has finally escaped deflationary territory withCPI inf lation running at 0.3% y/y in July, albeit this is still farbelow the inflation target.

• Monetary policy. The SNB has been awaiting an ECB exit for longand the recent shift in rhetoric from Draghi and co and theassociated uptick in EUR/CHF will be much welcomed by theSNB. According to the weekly sight deposit figures the SNB hasceased its long-standing CHF selling lately, in a sign that CHFinflows are starting to evaporate. That said, the SNB has beenremarkably silent during the recent move among central banksto flirt with exit talk and we think the central bank will stick to itsnegative deposit rate for the foreseeable future, awaiting amove in EUR/CHF to around 1.20 before starting to signal anyexit thoughts. With ECB set to stay in QE mode into 2018, wesee the SNB keeping the Libor target and the sight deposit rateunchanged at -0.75% in 12M.

• Flows. Positioning in CHF is close to neutral but stretched onEUR longs. Both Switzerland and the euro area have largecurrent-account surpluses and thus there is no clear ‘naturalf low’ in the cross.

• Valuation. Both our G10 MEVA and PPP model put ‘fair’ value forthe cross around 1.25.

• Risks. Both renewed North Korean tensions and a politicaland/or banking crisis in Italy pose upside CHF risks.

EUR/CHF – SNB set to keep a distance to an ECB exit

Source: Danske Bank

Conclusion. As we noted in FX Research: EUR/CHF: Patient SNB tolet 'reverse gravity' gain traction, while a range of central banksincluding notably the ECB has had a hard time concealing theireagerness to start ‘normalising’ monetary policy in a move that wehave dubbed ‘the Sintra accord’, 14 July, the SNB has used everyopportunity to stress that it is in no hurry to exit from negativerates. Indeed, we think the SNB is for now keen to embrace thepricing of eventual ECB rate hikes, as these are viewed as the onlyeffective way to help correct the overvaluation of the CHF. Nearterm the euro uptick may take a breather but we still see SNBbeing more than happy to let EUR/CHF edge towards 1.20 ascurrency help on inflation remains much needed. We keep ourforecast profile unchanged and thus still look for the cross to tradeat 1.14 in 1-3M, 1.16 in 6M, and 1.20 in 12M as the pricing of anECB exit gains traction.Christin Tuxen, Chief Analyst, [email protected], +45 45 13 78 67

EUR/CHF 1M 3M 6M 12M

Forecast (pct'ile) 1.14 (49%) 1.14 (49%) 1.16 (66%) 1.20 (83%)

Fwd. / Consensus 1.14 / 1.13 1.14 / 1.12 1.14 / 1.12 1.14 / 1.13

50% confidence int. 1.12 / 1.16 1.11 / 1.16 1.11 / 1.17 1.10 / 1.18

75% confidence int. 1.11 / 1.17 1.09 / 1.18 1.08 / 1.20 1.06 / 1.21

k

1.05

1.10

1.15

1.20

1.25

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

EUR/CHF

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

1818

Forecast: 6.70 (1M) 6.75 (3M), 6.80 (6M) and 6.95 (12M)• Monetary policy. Official monetary policy rates have been keptunchanged but de facto China has tightened policy a lot this year.Money market rates and bond yields have shot higher and creditgrowth has slowed quite a lot. Financial stress after a crackdownon shadow financing has added to the squeeze on credit. However,lately some of the tightening has been scaled back a bit and moneymarket rates and bond yields are lower. Official production datasuggest that China is losing some pace going into H2 in line withour expectations. Our China leading indicators point to furthermoderation in growth over the next year but not a hard landing.While the housing market is expected to slow further, the inventoryof houses for sale is quite low and should keep a floor underconstruction activity.

• FX policy. China continues to manage the currency against abasket. China uses occasional intervention in the offshore marketto send a signal to the market. This has happened several timesthrough squeezing offshore liquidity to push up offshore rates andthus deter short positions in the CNY. The CNY basket has beenbroadly stable since mid-2016 despite big swings in the rateversus for example the USD. We expect the CNY basket to staybroadly stable over the forecast horizon.

• Valuation. China’s currency is seen broadly as close to equilibrium.

• Risks. The uncertainty over the CNY outlook has increased andrisks are more two-sided. On the one hand, weaker economicdevelopment in China still poses upside risks to USD/CNY. On theother hand, more general USD weakness than expected could leadto a decline in USD/CNY.

USD/CNY – too far too fast

Conclusion. We revise down our USD/CNY forecast again to6.95 in 12M to reflect the weaker USD. While a weaker USDwill weigh on USD/CNY, softer growth and Fed tightening areexpected to weaken the CNY versus the USD. EUR/CNY isstill expected to move higher in tandem with a higherEUR/USD.

The CNH-CNY spread has seen periods of widening (CNHstronger than CNY) when China has engineered a squeeze ofoffshore liquidity to deter short positions in CNH (and CNY). Itnormalises fairly quickly, though, to around zero after a while.We expect the spread to continue to hover around zero.

Source: Macrobond Financial, Danske Bank

Allan von Mehren, Chief Analyst, [email protected], +45 45 12 80 55

1919

Forecast: 60.00 (1M), 59.40 (3M), 54.70 (6M) and 53.50 (12M)• Growth. Russia’s economy continues to grow, surprisingpositively in Q2 17 with growth climbing to 2.5% y/y accordingto preliminary estimates, versus a 0.5% expansion in Q1 17. TheBrent average rose 8% in Q2 17 versus the average in Q2 16,while the RUB/USD Q1 17 average rose 15%. In Q2 17 retailsales started to expand for the first time since late 2014, whileindustrial production continued to increase. We see substantialupside risks to our 2017 GDP growth forecast of 1.2% y/y whichwe have had since spring 2016.

• Monetary policy. Russia’s central bank (CBR) held its key rateunchanged at 9.00% on 28 July after a series of cuts. Webelieve that the CBR’s main concern was the worseninggeopolitical environment, which hit sentiment, on new anti-Russia sanctions by the US. We expect the CBR to cut to 8.25%by the end of 2017 (8.00% previously), while a more hawkishstance shouldn’t be excluded if the Brent price drops or moregeopolitical woes arise.

• Flows. As we write above, geopolitical risk did arise and the RUBsaw some outf lows on the US’s new anti-Russia sanctions.While the crude price has remained stable, hovering overUSD50/bbl, the RUB’s earlier divergence with oil has vanished.

• Valuation. Crude and the RUB’s correlation has strengthened.The RUB has seen periods of outf lows on geopolitical woes. Yet,high carry is supporting the RUB buyers. In our view, theUSD/RUB pair is hovering slightly below its ‘fair value’, given thepressure arising from decreased Brent.

USD/RUB – erasing divergence with oil

Risks. While the internal environment continues to befavourable for the RUB outlook, external risks are currentlymost significant for the RUB: downside pressure on the crudeoil price and worsening anti-Russia sanctions by the UScombined with China’s slowdown risk are RUB negative in theshort and medium term. Long-term downside risk for the RUBis a deteriorating current account surplus.

Conclusion. Given persisting external risks for the RUB andpossible downside risks from the oil price, we roll the currentRUB levels. We expect RUB and oil price divergence to shrinkon worsened sentiment.

Vladimir Miklashevsky, Senior Economist/Trading Desk Strategist, [email protected], +358 10 546 7522

Source: Danske Bank

1M 3M 6M 12M

Forecast 60.00 59.40 54.70 53.50

Fwd. / Consensus 60.27 / 59.96 60.96 / 59.98 61.95 / 59.60 63.84 / 58.32

30

40

50

60

70

80

90

Aug-15 Feb-16 Aug-16 Feb-17 Aug-17 Feb-18

USD/RUB Forward Forecast

2020

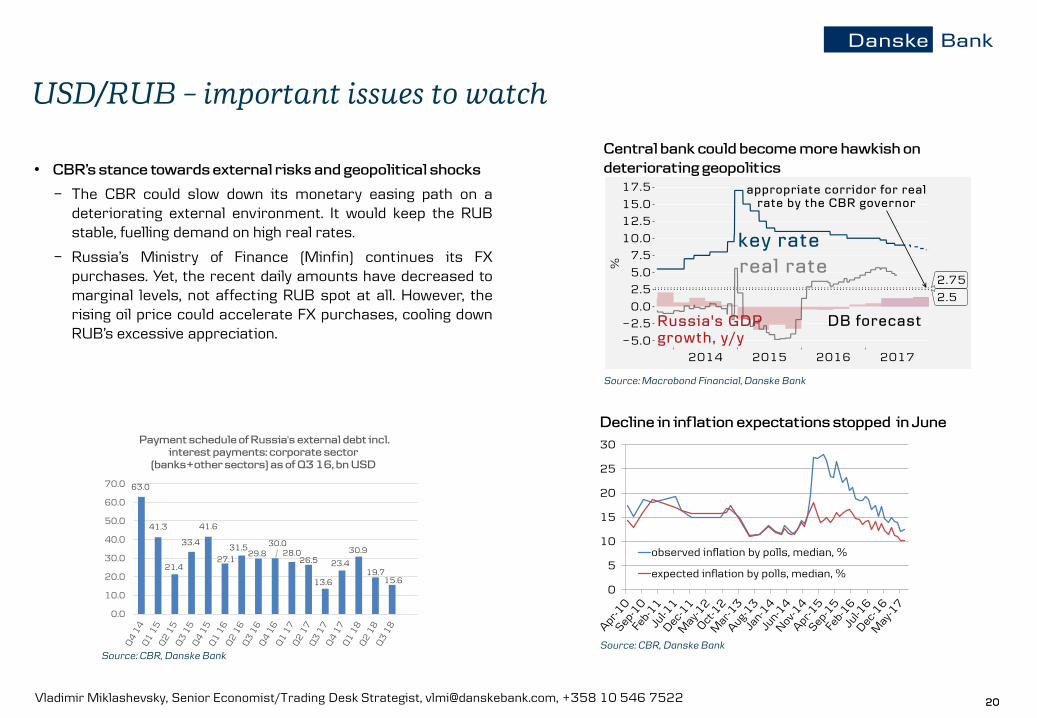

• CBR’s stance towards external risks and geopolitical shocks

− The CBR could slow down its monetary easing path on adeteriorating external environment. It would keep the RUBstable, fuelling demand on high real rates.

− Russia’s Ministry of Finance (Minfin) continues its FXpurchases. Yet, the recent daily amounts have decreased tomarginal levels, not affecting RUB spot at all. However, therising oil price could accelerate FX purchases, cooling downRUB’s excessive appreciation.

USD/RUB – important issues to watch

Vladimir Miklashevsky, Senior Economist/Trading Desk Strategist, [email protected], +358 10 546 7522

Source: Macrobond Financial, Danske Bank

Source: CBR, Danske Bank

Source: CBR, Danske Bank

Decline in inflation expectations stopped in June

63.0

41.3

21.4

33.4

41.6

27.1

31.529.8

30.028.0

26.5

13.6

23.4

30.9

19.715.6

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Payment schedule of Russia's external debt incl.

interest payments: corporate sector

(banks+other sectors) as of Q3 16, bn USD

Central bank could become more hawkish on

deteriorating geopolitics

0

5

10

15

20

25

30

observed inflation by polls, median, %

expected inflation by polls, median, %

2121

Forecast: 4.26 (1M), 4.24 (3M), 4.18 (6M) and 4.16 (12M)• Economic and political developments. Polish economic growthremains solid. Private consumption is being boosted by thechild benefit cheque and record low unemployment (which fellto an all-time low of 7.1% in June) and higher real wage growth.Industrial production is holding up despite moderation in themanufacturing PMIs. We raised our real GDP growth forecastfor 2017 to 3.7% (previously 3.4%) at end-June. Politically,relations between Poland and the EU deteriorated again in lateJuly over new legislation proposals by the government in thejudicial sector, with the EU launching an infringementprocedure against Poland. The Polish authorities have untilend-August to respond to the formal notice by the EU andinvestor sentiment towards Poland may be affected in the fall.

• Monetary policy. The monetary policy committee of theNational Bank of Poland (NBP) kept its policy rate unchanged at1.5% at its 5 July meeting. While governor Glapiński continuesto expect only benign inflationary pressure over the next twoyears, other governors sounded more concerned over themonetary policy stance. Since the meeting, while headlineinflation has surprised on the upside at 1.7%, core inflationremained stable at 0.8% in July. Market expectations of a hikehave increased slightly and now assigns about 60% chance of arate hike over the next year, slightly too dovish in our view.

• Risks. The balance of risk to our EUR/PLN forecast appearsclearly on the upside. The biggest risk is the EU suspendingPoland’s EU voting rights. However, it is not clear how long theprocess would drag on for and whether the EU would dare totake action. Also, a deterioration in global risk sentiment couldtrigger an upward move in EUR/PLN.

EUR/PLN – PLN hit by renewed political risk and global risk-off

Conclusion. After a strong run this year, the Zloty has weakenedalmost 2% over the past month. The main driver has been the newstrain in relations with the EU over judicial reforms, as well asdeterioration in global risk sentiment and still-benign Polishinflation developments. Looking ahead, we still see the potential forthe PLN to strengthen versus the EUR due to expansion in thePolish economy. Our forecasts for EUR/PLN are 4.26 in 1M (4.18previously), 4.24 in 3M (4.16 previously), falling to 4.18 in 6M(4.14 previously) and 4.16 in 12M. But as noted in the riskssection, there appear to be clear upside risks to our forecasts givenpossible EU action in relation to the latest infringement procedureand global risk sentiment.

Source: Danske Bank

Jakob Christensen, Chief Analyst, [email protected], +45 45 12 85 30

EUR/PLN 1M 3M 6M 12M

Forecast (pct'ile) 4.26 (35%) 4.24 (29%) 4.18 (18%) 4.16 (20%)

Fwd. / Consensus 4.29 / 4.26 4.31 / 4.23 4.34 / 4.20 4.38 / 4.20

50% confidence int. 4.24 / 4.33 4.23 / 4.37 4.21 / 4.42 4.19 / 4.49

75% confidence int. 4.21 / 4.37 4.18 / 4.45 4.13 / 4.53 4.07 / 4.66

k

4.00

4.20

4.40

4.60

4.80

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

EUR/PLN

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

2222

Forecast: 3.60 (1M), 3.65 (3M), 3.80 (6M) and 4.00 (12M)• Growth. Turkey’s economic growth surprised positively asGDP expanded 5.0% y/y in Q1 17 while the Bloombergconsensus expected 3.5% y/y growth. Expansive fiscal policyhas been the strongest growth driver supporting fixedinvestments and private consumers through wage increases.The external environment remains positive for Turkey’sexports as Russia has removed anti-Turkey sanctions andexports to the EU are growing. We raise our cautious 2017GDP forecast to 2.9% y/y from 1.9% y/y previously asimproving macro is gaining momentum in private consumptionand exports.

• Monetary policy. Disinflation continues, giving more room forthe central bank to ease its monetary policy in H2 17, weexpect. During its last monetary policy meeting, Turkey’scentral bank (the TCMB) kept all its rates unchanged, which weinterpret as preparation for monetary easing, if currentconditions remain favourable. We expect more signs ofmonetary easing inception to arise, which should restrainTRY’s appreciation on improving macro conditions.

• Valuation. Given the improving macro indicators which arehelping the current account balance, we see that the TRY ishovering around its ‘fair value’.

USD/TRY – improving macro brings stability, carry supports appetite

Risks. Major downside risks to our TRY forecasts aregeopolitical – both external and internal – such as Turkey’smilitary operations in Syria and its shaky relationships with theEU and the US. Surprise easing by the TCMB on politicalpressure and improving macro are further downside risks.

Conclusion. We see good prospects for the TRY in the shortterm supported by encouraging macro fundamentals andattractive carry, while staying more cautious in the medium tolong term.

Source: Danske Bank

Vladimir Miklashevsky, Senior Economist/Trading Desk Strategist, [email protected], +358 10 546 7522

USD/TRY 1M 3M 6M 12M

Forecast (pct'ile) 3.60 (78%) 3.65 (63%) 3.80 (70%) 4.00 (71%)

Fwd. / Consensus 3.54 / 3.58 3.64 / 3.63 3.73 / 3.70 3.91 / 3.83

50% confidence int. 3.48 / 3.59 3.49 / 3.72 3.48 / 3.85 3.43 / 4.06

75% confidence int. 3.44 / 3.64 3.41 / 3.84 3.34 / 4.04 2.92 / 4.38

k

2.50

3.00

3.50

4.00

4.50

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

USD/TRY

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

2323

Forecast: 305 (1M), 306 (3M), 304 (6M) and 300 (12M)• Growth. The Hungarian economy is supported by strong

momentum in private consumption, and leading indicators stillpoint to robust growth in Q2: retail sales accelerated to 6.0%y/y and, supported by a rise in the minimum wage and a tightlabour market (unemployment at 4.3%), gross wages grewstrongly by 12.9% y/y in May. Despite a recent moderation inthe PMI, industrial production expanded by a healthy 4.0% y/yin June. We still project real GDP growth of 3.6% in 2017,supported by a recovery in investments due to improved EUfunds absorption.

• Monetary policy. Core inf lation has accelerated markedly inrecent months to 2.6% y/y in July. But although underlyingprice pressures are rising, headline inf lation at 2.1% y/yremains still below the central bank’s 3% target due to thedrag from energy prices, imported disinf lation and VAT cuts. Atthe latest meeting in July, NBH kept its policy rate unchangedat 0.9% and also maintained its dovish stance, expectinginf lation to reach the target only in early 2019. However,through a combination of pro-cyclical fiscal and monetarypolicies as well as rising wage pressures, we project thatinf lation will hit the central bank’s 3% target in 2018. Theresulting shift in market expectations about a pull-back incentral bank stimulus, would be supportive for the HUF.

• Risks. A clear upside risk to our EUR/HUF forecast is adeterioration in global risk sentiment. The recent strength ofthe HUF could also induce the NBH to react with additionalstimulus. However, there are also downside risks fromstronger-than-expected economic and inf lation developmentsin Hungary.

EUR/HUF – range trading set to continue

Conclusion. Aided by strong domestic economic data as wellas favourable global risk sentiment towards EMs, EUR/HUFhas depreciated more than we expected over the past month,breaking below important resistance levels around 305 and303. However, in light of the ongoing NBH liquidity measures,we think EUR/HUF downside will be capped in the short-term.Longer term, we see a positive external balance and anundervalued exchange rate as further supporting factors forthe HUF. Given the recent move, we lower our short-termEUR/HUF forecast to 305 in 1M (308 previously), 306 in 3M,304 in 6M and 300 in 12M.

Source: Danske Bank

Aila Mihr, First Year Analyst, [email protected], +45 45 12 85 35

EUR/HUF 1M 3M 6M 12M

Forecast (pct'ile) 305.00 (62%) 306.00 (67%) 304.00 (55%) 300.00 (42%)

Fwd. / Consensus 304.42 / 308.17 304.42 / 310.00 304.42 / 309.49 304.42 / 308.50

50% confidence int. 301.87 / 306.37 300.04 / 307.50 297.83 / 308.58 294.49 / 310.68

75% confidence int. 300.09 / 308.69 297.23 / 311.36 293.78 / 314.54 287.78 / 319.65

k

280

290

300

310

320

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

EUR/HUF

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

2424

Forecast: 26.00 (1M), 25.90 (3M), 25.70 (6M) and 25.50 (12M)• Growth. With retail sales growing by 6.6% y/y in June andconsumer confidence still high, private consumption remainedstrong in Q2. Although the PMI recently moderated to 55.3from the highs reached in April, it is still pointing to continuingstrong economic activity and GDP growth in Q2 (4.5% y/y)surprised strongly on the upside. Domestic and foreign demandwill remain the main growth drivers in our view, as consumersprofit from rising wages due to a tight labour market and theeconomic recovery in the eurozone is supporting exports. TheCNB also significantly revised up its GDP forecast for 2017(3.6%) and 2018 (3.2%) at its latest meeting in August.

• Monetary policy. At the policy meeting on 3 August, the CNBdelivered its first 20bp interest rate hike since February 2008,citing the pro-inflationary risks from a weaker-than-forecastcurrency and strong wage and housing price growth (see alsoour CNB Review, 3 August). Monetary policy relevant inflationrose to 2.6% y/y in July, lending further support to the CNB’sdecision, although volatile food prices are mainly behind the fastrise in inflation this year. We expect the CNB to stay on hold forthe remainder of this year and watch inflation and exchangerate developments closely. We currently do not expect the nextCNB hike before Q2 18, as we project inflation will deceleratesomewhat in the coming months and drop back towards 2.0%at the end of this year.

• Risks. Given the sizable amount of long CZK positionsaccumulated in the market prior to the exit, EUR/CZK is stillvulnerable to spikes higher. The greatest risks to the growthoutlook stem from external shocks, especially in the euro area,due to the high degree of openness of the Czech economy.

EUR/CZK – CNB hike opens door for more CZK strengthening ahead

Conclusion. Following the CNB rate announcement, EUR/CZKinitially broke below the 26.00 level, but CZK struggled to hold on toits gains. This was probably due to some profit-taking on long CZKpositions after the CNB move, illustrating that any rapid EUR/CZKdepreciation will be prevented by the still large speculativepositions in the market. We project that the cross will hover aroundcurrent levels in the short term and look for more gradual CZKstrengthening over the medium term based on robust Czecheconomic fundamentals and relative monetary policy divergenceas the CNB moves towards tighter monetary conditions while wedo not expect the first ECB hike before 2019. Overall, we forecastEUR/CZK at 26.00 in 1M, 25.90 in 3M, 25.70 in 6M and 25.50 in12M.

Source: Danske Bank

Aila Mihr, First Year Analyst, [email protected], +45 45 12 85 35

EUR/CZK 1M 3M 6M 12M

Forecast (pct'ile) 26.00 (27%) 25.90 (28%) 25.70 (24%) 25.50 (24%)

Fwd. / Consensus 26.18 / 26.12 26.18 / 26.05 26.18 / 25.90 26.18 / 25.68

50% confidence int. 25.98 / 26.33 25.85 / 26.40 25.71 / 26.48 25.52 / 26.57

75% confidence int. 25.84 / 26.51 25.63 / 26.72 25.41 / 26.94 25.07 / 27.20

k

25.0

25.5

26.0

26.5

27.0

27.5

Aug-16 Nov-16 Mar-17 Jun-17 Sep-17 Dec-17 Apr-18 Jul-18

EUR/CZK

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

2525

Danske Bank FX forecasts vs EUR and USD

Source: Danske Bank

Spot +1m +3m +6m +12m +1m +3m +6m +12m

Exchange rates vs EUR

USD 1.171 1.17 1.17 1.18 1.22 -0.2 -0.5 -0.2 2.1JPY 129.5 130 133 137 142 0.2 2.9 5.6 9.1GBP 0.910 0.91 0.91 0.90 0.88 -0.1 -0.2 -1.5 -4.1CHF 1.140 1.14 1.14 1.16 1.20 0.0 0.1 2.0 5.7

DKK 7.4363 7.4400 7.4400 7.4400 7.4400 0.1 0.1 0.1 0.2NOK 9.36 9.30 9.30 9.10 9.00 -0.7 -0.9 -3.4 -5.1SEK 9.49 9.50 9.40 9.30 9.20 0.1 -0.9 -2.0 -3.1

Exchange rates vs USD

JPY 110.7 111 114 116 116 0.5 3.5 5.8 6.9GBP 1.29 1.29 1.29 1.31 1.39 -0.1 -0.3 1.3 6.5CHF 0.97 0.97 0.97 0.98 0.98 0.2 0.6 2.2 3.5

DKK 6.35 6.36 6.36 6.31 6.10 0.3 0.6 0.4 -1.8NOK 7.99 7.95 7.95 7.71 7.38 -0.5 -0.4 -3.2 -7.0SEK 8.11 8.12 8.03 7.88 7.54 0.3 -0.4 -1.7 -5.0

CAD 1.28 1.28 1.30 1.33 1.34 0.4 2.0 4.4 5.3AUD 0.78 0.78 0.76 0.75 0.75 -0.1 -2.6 -3.8 -3.6NZD 0.72 0.72 0.71 0.70 0.70 -0.5 -1.7 -3.0 -2.7

RUB 59.93 60.00 59.40 54.70 53.50 -0.5 -2.7 -11.8 -16.3CNY 6.69 6.70 6.75 6.80 6.95 0.0 0.5 0.7 2.2

Note: GBP, AUD and NZD are denominated in local currency rather than USD

Forecast Forecast vs forward outright, %

2626

Danske Bank FX forecasts vs DKK

Source: Danske Bank

Spot +1m +3m +6m +12m +1m +3m +6m +12m

Exchange rates vs DKK

EUR 7.4363 7.4400 7.4400 7.4400 7.4400 0.1 0.1 0.1 0.2USD 6.35 6.36 6.36 6.31 6.10 0.3 0.6 0.4 -1.8JPY 5.74 5.73 5.58 5.44 5.26 -0.2 -2.8 -5.2 -8.2GBP 8.17 8.18 8.18 8.27 8.45 0.2 0.3 1.7 4.5CHF 6.52 6.53 6.53 6.41 6.20 0.0 0.0 -1.8 -5.2

NOK 0.79 0.80 0.80 0.82 0.83 0.8 1.0 3.6 5.5SEK 0.78 0.78 0.79 0.80 0.81 0.0 1.0 2.1 3.4

CAD 4.98 4.97 4.89 4.74 4.55 -0.1 -1.4 -3.9 -6.8AUD 4.96 4.96 4.83 4.73 4.57 0.2 -2.0 -3.4 -5.4NZD 4.60 4.58 4.51 4.41 4.27 -0.2 -1.1 -2.6 -4.5

PLN 1.73 1.75 1.75 1.78 1.79 1.0 1.8 3.8 5.5CZK 0.284 0.286 0.287 0.289 0.292 0.7 1.0 1.6 2.4HUF 2.44 2.44 2.43 2.45 2.48 -0.1 -0.3 0.4 2.2RUB 0.106 0.106 0.107 0.115 0.114 0.8 3.4 13.8 17.2TRY 1.79 1.77 1.74 1.66 1.52 -0.4 0.3 -1.3 -3.9

CNY 0.95 0.95 0.94 0.93 0.88 0.2 0.2 -0.4 -4.0

Forecast Forecast vs forward outright, %

2727

Danske Bank FX forecasts vs SEK

Source: Danske Bank

Spot +1m +3m +6m +12m +1m +3m +6m +12m

Exchange rates vs SEK

EUR 9.49 9.50 9.40 9.30 9.20 0.1 -0.9 -2.0 -3.1USD 8.11 8.12 8.03 7.88 7.54 0.3 -0.4 -1.7 -5.0JPY 7.33 7.32 7.05 6.79 6.50 -0.1 -3.7 -7.2 -11.2GBP 10.43 10.44 10.33 10.33 10.45 0.2 -0.7 -0.5 1.1CHF 8.32 8.33 8.25 8.02 7.67 0.1 -1.0 -3.9 -8.3

NOK 1.01 1.02 1.01 1.02 1.02 0.8 0.0 1.5 2.1DKK 1.28 1.28 1.26 1.25 1.24 0.0 -1.0 -2.1 -3.2

CAD 6.36 6.34 6.18 5.93 5.63 -0.1 -2.4 -5.9 -9.8AUD 6.33 6.33 6.11 5.91 5.66 0.2 -3.0 -5.5 -8.4NZD 5.87 5.85 5.70 5.52 5.28 -0.1 -2.1 -4.7 -7.6

PLN 2.21 2.23 2.22 2.22 2.21 1.0 0.7 1.7 2.1CZK 0.363 0.365 0.363 0.362 0.361 0.7 0.0 -0.5 -0.9HUF 3.12 3.11 3.07 3.06 3.07 -0.1 -1.4 -1.7 -1.1RUB 0.135 0.135 0.135 0.144 0.141 0.9 2.3 11.4 13.4TRY 2.29 2.26 2.20 2.07 1.89 -0.3 -0.7 -3.4 -7.0

CNY 1.21 1.21 1.19 1.16 1.09 0.3 -0.9 -2.5 -7.1

Forecast Forecast vs forward outright, %

2828

Danske Bank FX forecasts vs NOK

Source: Danske Bank

Spot +1m +3m +6m +12m +1m +3m +6m +12m

Exchange rates vs NOK

EUR 9.36 9.30 9.30 9.10 9.00 -0.7 -0.9 -3.4 -5.1USD 7.99 7.95 7.95 7.71 7.38 -0.5 -0.4 -3.2 -7.0JPY 7.22 7.16 6.97 6.65 6.36 -1.0 -3.7 -8.5 -13.0GBP 10.28 10.22 10.22 10.11 10.23 -0.6 -0.7 -1.9 -1.0CHF 8.21 8.16 8.16 7.84 7.50 -0.7 -1.0 -5.3 -10.2

SEK 0.99 0.98 0.99 0.98 0.98 -0.8 0.0 -1.4 -2.1DKK 1.26 1.25 1.25 1.22 1.21 -0.8 -1.0 -3.5 -5.2

CAD 6.27 6.21 6.11 5.80 5.51 -0.9 -2.3 -7.3 -11.7AUD 6.24 6.20 6.04 5.78 5.53 -0.6 -3.0 -6.8 -10.3NZD 5.79 5.72 5.64 5.40 5.16 -1.0 -2.1 -6.0 -9.5

PLN 2.18 2.18 2.19 2.18 2.16 0.2 0.8 0.2 0.0CZK 0.357 0.358 0.359 0.354 0.353 -0.1 0.0 -2.0 -2.9HUF 3.07 3.05 3.04 2.99 3.00 -0.9 -1.3 -3.1 -3.2RUB 0.133 0.132 0.134 0.141 0.138 0.0 2.3 9.8 11.1TRY 2.26 2.21 2.18 2.03 1.84 -1.1 -0.7 -4.8 -8.9

CNY 1.20 1.19 1.18 1.13 1.06 -0.5 -0.8 -3.9 -9.0

Forecast Forecast vs forward outright, %

2929

Danske Bank EMEA FX forecasts

Source: Danske Bank

Danske Forward Danske Forward Danske Forward Danske Forward Danske Forward

PLN 15-Aug-17 4.29 3.67 173 221 218

+1M 4.26 4.30 3.64 3.67 175 173 223 221 218 218

+3M 4.24 4.31 3.62 3.67 175 172 222 220 219 218

+6M 4.18 4.34 3.54 3.67 178 171 222 219 218 217

+12M 4.16 4.38 3.41 3.66 179 170 221 217 216 216

HUF 15-Aug-17 304 260 2.44 3.12 3.07

+1M 305 305 261 260 2.44 2.44 3.11 3.12 3.05 3.08

+3M 306 305 262 259 2.43 2.44 3.07 3.11 3.04 3.08

+6M 304 305 258 258 2.45 2.44 3.06 3.11 2.99 3.09

+12M 300 306 246 256 2.48 2.43 3.07 3.10 3.00 3.10

CZK 15-Aug-17 26.2 22.4 28.4 36.3 35.7

+1M 26.0 26.2 22.2 22.3 28.6 28.4 36.5 36.3 35.8 35.8

+3M 25.9 26.1 22.1 22.2 28.7 28.4 36.3 36.3 35.9 35.9

+6M 25.7 26.1 21.8 22.0 28.9 28.5 36.2 36.4 35.4 36.1

+12M 25.5 26.1 20.9 21.8 29.2 28.5 36.1 36.4 35.3 36.4

RUB 15-Aug-17 70.1 59.9 10.6 13.5 13.3

+1M 70.2 70.7 60.0 60.3 10.6 10.5 13.5 13.4 13.2 13.2

+3M 69.5 71.8 59.4 61.0 10.7 10.4 13.5 13.2 13.4 13.1

+6M 64.5 73.4 54.7 62.0 11.5 10.1 14.4 12.9 14.1 12.8

+12M 65.3 76.4 53.5 63.9 11.4 9.7 14.1 12.4 13.8 12.4

TRY 15-Aug-17 4.15 3.54 179 229 226

+1M 4.21 4.19 3.60 3.58 177 177 226 226 221 223

+3M 4.27 4.28 3.65 3.64 174 174 220 222 218 219

+6M 4.48 4.42 3.80 3.73 166 168 207 215 203 213

+12M 4.88 4.68 4.00 3.91 152 159 189 203 184 203

CNY 15-Aug-17 7.83 6.69 95 121 120

+1M 7.84 7.85 6.70 6.70 95 95 121 121 119 119

+3M 7.90 7.90 6.75 6.72 94 94 119 120 118 119

+6M 8.02 7.98 6.80 6.75 93 93 116 119 113 118

+12M 8.48 8.13 6.95 6.80 88 91 109 117 106 117

EUR USD DKK SEK NOK

3030

Disclosures

This research report has been prepared by Danske Bank A/S (‘Danske Bank’). The authors of this research report are Thomas Harr (Global Head of FICC Research), Christin Tuxen (Chief Analyst), Morten Helt (Senior Analyst), Jens Naervig Pedersen (Senior Analyst), Kristoffer Kjær Lomholt (Senior Analyst), Jakob Ekholdt Christensen (Chief Analyst), Stefan Mellin (Senior Analyst), Vladimir Miklashevsky (Senior Analyst), Allan von Mehren (Chief Analyst), Aila Mihr (First-year Analyst) and Nicolai Pertou Ringkøbing (Assistant Analyst).

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

Danske Bank’s research reports are prepared in accordance with the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including as sensitivity analysis of relevant assumptions, are stated throughout the text.

Expected updates

Monthly.

Date of first publication

See the front page of this research report for the date of first publication.

3131

General disclaimer

This research has been prepared by Danske Bank A/S. It is provided for informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date hereof. These opinions are subject to change and Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is not intended for, and may not be redistributed to, retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior written consent.

Disclaimer related to distribution in the United States

This research report was created by Danske Bank A/S and is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank A/S, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The research report is intended for distribution in the United States solely to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S. Securities and Exchange Commission.

Report completed: 16 August 2017, 10:37 GMTReport first disseminated: 16 August 2017, 11:25 GMT