Embed Size (px)

Citation preview

FY 2013

Pre-Award Fundamentals

FY 2013

Objectives• Upon completion of this class participants will be able to:

– Locate and apply knowledge of basic Federal sponsor rules and regulations

– Understand and apply fundamental compliance concepts to research/grant management

– Locate and apply Duke University grant management policies and procedures related to proposal development

– Have an understanding of a grant manager’s role in proposal development

– Locate and have a basic understanding of guidance cited in funding announcements

– Understand basic budget development concepts

– Understand federal costing guidelines and how to use these guidelines in budget development

– Locate and understand basic budgetary components

– Understand the proposal submission process

Slide 2

FY 2013

Learning Outcomes

• Upon completion of this class participants will be able to:– Understand and apply basic Federal regulations towards

charging costs to Federal awards– Able to understand basic compliance rules of allowability,

allocability, consistency, and reasonableness– Ability to distinguish and apply charges based on allowable

and unallowable costs– Ability to distinguish differences between direct charges and

F&A costs – Understand basic concept of charging Administrative and

Clerical costs to Federal awards– Locate and have a basic understanding of guidance cited in

funding announcements– Identify and advise the PI of administrative requirements

and proposal elements related to proposal preparation

Slide 3

FY 2013

Learning Outcomes

– Ability to understand and apply basic knowledge of who funds sponsored research and the basic funding mechanisms used by sponsors

– Ability to understand and apply guidance on funding opportunity announcements from different sponsors

– Awareness of various search engines and resources at Duke in order to find funding opportunities for PIs

– Ability to understand the basic concepts and terminology related to proposal development

– Understand and be able to advise PIs of required proposal elements (Biosketch, Other Support, Facilities & Resources) for proposal preparation

– Understand how to include collaborations and subcontractors in proposal budgets and submissions

– Ability to advise the PI of submission requirement (paper vs. electronic)

Slide 4

FY 2013

Compliance Basics: What is Compliance?

Slide 5

FY 2013

What is Compliance?

• Meeting all the obligations associated with accepting funds to conduct research or perform an activity proposed to the sponsor

• Establishing internal controls/checks and balances within the university and the department to manage funds effectively and appropriately (according to the rules)

• Meeting the stated management requirements of the sponsor and the university

• Communicating compliance expectations to all constituencies – including colleagues and faculty researchers (PIs)

In the most basic terms, compliance is following the rules.

Slide 6

FY 2013

Why is Compliance So Important to Duke University?

• Federal research investment comes from public funds – taxpayer dollars. It is important that Duke University honor that investment and spend/account for funds wisely

• Penalties, fines, and potential loss of federal funding could result if the university is not compliant:– Negative publicity– Large financial settlements– Greatly reduced flexibility in the management of

federally provided resources (The federal government could put restrictions and additional reporting burden on the university)

– Audit findings– Disallowance of costs (Duke University would have

to pay back federal funds)– Extrapolation to University grant portfolio

Key point: One small item may be “extrapolated” or used as evidence that other similar items were also non-compliant. This means that a $10.00 item found on an audit may possibly be “extrapolated” to $100,000 and Duke University held responsible for paying Federal funds in that amount. Slide 7

FY 2013

Summary

• Compliance is following the rules – federal laws, sponsor regulations, and Duke policies

• Compliance is important because non-compliance can cost Duke in fines, penalties, and reputation. It can also cause employees to lose their job, or in severe instances, go to jail.

• The RAA program is designed to provide you with the tools to monitor compliance

Slide 8

FY 2013

Rules and Regulations

Slide 9

Compliant grant management starts with knowing the rules you must follow…

FY 2013

Order of Precedence

Award

Specific Program Guidance

Agency Specific Terms & Conditions

OMB Circulars

Public Law Institutional Policy

10 Slide 10

FY 2013

OMB Circulars Are…

• Instructions issued by the Office of Management and Budget to the federal agencies

• Purpose:– To assure that grants are managed properly and that federal dollars are spent

in accordance with applicable laws and regulations

• Agencies then implement into their own requirements

• Regulations specifically governing Federally sponsored activities

• Codified in Title 2 of the Code of Federal Regulations

– 2 C.F.R. Pt. 215 (A-110)

– 2 CFR Pt. 220 (A-21)

• Not directly applicable to recipients; only applicable through agency implementation

All OMB Circulars can be found on this web site: www.whitehouse.gov/omb/grants_default Slide 11

FY 2013

OMB Circular A-21: 2CFR Part 220Cost Principles

Circular A-21 provides guidance on:• Allowability of costs• Consistency in cost treatment• Direct and F&A costs• Identification & assignment of F&A costs and calculating F&A cost

rates• Guidance for selected cost items• Examples of “major project” where direct charging of

administrative costs may be appropriate• Cost Accounting Standards for educational institutions

12

We will discuss Circular A-21 in more detail in the budget development section of this course

Slide 12

Appendix 1: Circular A-21

FY 2013

OMB Circular A-110 (2CFR Part 215): Administrative Requirements

• A-110 provides direction as to the systems and processes required to manage grants/contracts at Duke University

• The circular also provides agencies with guidance on– Award instruments– Forms – “Eligible” recipients – Special award conditions– Certifications and Representations

• Procurement standards • Reports and records

• University requirements include:– Payments– Matching or Cost sharing – Accounting for program income– Revision of budget and program

plans– Non-Federal audits– Allowable costs

• Financial management systems standards

• Property standards

13Slide 13

FY 2013

OMB Circular A-110 (Now 2CFR Part 215): Administrative Requirements

• Expanded Authorities granted to the recipient institution• Means that agencies can waive cost-related and

administrative prior approvals for:– Pre-award Costs (90 days prior to award)– One-time 12 month extension– Carry forward of balances

• This means that Duke University is

not required to seek Federal

permission for these actions, but

can authorize these actions on its

own.

14Slide 14

FY 2013

To Learn More About the Circulars

• AGM: Regulatory Environment: A-21, A-110, A-133, F&A– Check the course catalog in the LMS to see a list of available classes

• Appendix 2 provides a crosswalk to Circulars that apply to recipients other than universities

15Slide 15

Appendix 2: Crosswalk toCirculars

FY 2013

Rules and Regulations: Sponsor Guidance

Public LawInstitutional

Policy

Slide 16

FY 2013

Sponsor Rules and PoliciesFederal Demonstration Partnership (FDP)

• History– FDP began as an experiment in Florida to reduce the need for agency

permission for certain actions. Several years ago Federal agencies exerted a great deal more control over how research was managed at Universities. As a result of FDP most research-funding agencies have agreed to reduced management requirements

• Purpose– To demonstrate that accountability can be maintained while simplifying

research management

• The FDP matrix – Provides an overview of the specific actions Universities can take without

approval from the Federal agency

17Slide 17

Handout 1: FDP Matrix

FY 2013

FDP Matrix Exercise

Using the FDP Matrix:

Does NASA require prior-approval for initial no-cost extension? Prior approval waived

1. Does NIH require prior-approval for pre-award costs exceeding 90 days? Prior approval required

2. Does NSF require prior approval to purchase equipment that was not originally in the proposed budget? What about NIH? NSF: Prior approval waived NIH: Prior approval waived, unless change in scope

3. Does the EPA allow a grant recipient to trade in a piece of equipment purchased with project funds in order to buy a replacement? This is permitted

Slide 18

Handout 2: Answer Key

FY 2013

Sponsor Rules and Policies: Federal Sponsors

• Each federal agency has their own rules, policies, and guidelines that can be more restrictive than the OMB circulars

• Review specific agency guidance in policy statements and funding announcements prior to submitting a proposal

• NIH Policy Statement:http://grants.nih.gov/grants/policy/nihgps_2013/nihgps_ch2.htm#appl_forms

• NSF Policy Statement:http://www.nsf.gov/publications/pub_summ.jsp?ods_key=gpm

Slide 19

FY 2013

Sponsor Rules and Policies: Non-Federal Sponsors

• Non-federal sponsors such as associations, industry, foundations, etc. have different rules and requirements

• When managing a non-federal award, it is important to find and understand the rules and requirements of these sponsoring organizations– Sponsor policy manuals– Guidance on sponsor website– Proposal Central

• When in doubt, contact your pre-award office (ORA or ORS) for guidance

20Slide 20

FY 2013

Sponsor Rules and Policies Non-Federal Agency Policy Manuals

• Susan G. Komen For the Cure • Robert Wood Johnson Foundation

21Slide 21

FY 2013

Public LawInstitutional

Policy

Duke University Policies and Procedures: • General Accounting Procedures (GAPs) are tools

to assist in day-to-day tasks

• GAPs provide actual procedures for managing grants and contracts, handling consultants, understanding faculty effort, payroll, plant and equipment, and other accounting topics

• GAPs: http://www.finsvc.duke.edu/gap/topics.html

The Faculty Handbook:• Faculty Handbook contains policies and

procedures pertinent to faculty at Duke University.

• The Office of the Provost is responsible for the compilation of the faculty handbook.

• Chapter 5 of the faculty handbook specifically addresses Sponsored Research.

• Faculty Handbook: http://www.provost.duke.edu/policies/fhb.html

Institutional Implementation

22Slide 22

FY 2013

Entity Rule More Information

Federal Circular A-21: Costing Principles

www.whitehouse.gov/omb/grants_default

Federal Circular A-110: Administrative Requirements

www.whitehouse.gov/omb/grants_default

Federal Circular A-133: Audit Guidance

www.whitehouse.gov/omb/grants_default

Sponsor NIH Grants Policy Statement http://grants.nih.gov/grants/policy/nihgps_2013/

grants1.nih.gov/grants/funding/424/index.htm#inst

Sponsor NSF Grants Policy Statement http://www.nsf.gov/publications/pub_summ.jsp?ods_key=gpm

Sponsor Non-Federal Sponsor Guidance

See specific sponsor for information

Institutional Duke GAPS http://finance.duke.edu/accounting/gap/index.php

Institutional Duke Policies- selected policies that may impact research administration

http://finance.duke.edu/travel/policies/index.php

https://ors.duke.edu/export-controls

http://finance.duke.edu/procurement/

http://finance.duke.edu/research/policies/index.php

Slide 23

FY 2013

Order of Precedence: Which Rules Do I Follow?

Specific Program Guidance

Agency Specific Terms & Conditions

OMB Circulars

Public LawInstitutional

Policy

24 Slide 24http://www.youtube.com/watch?v=szF-_zmCYEs&feature=c4-overview-vl&list=PLFA91D9F37D585F00

FY 2013

Now that you are familiar with some of the rules that regulate research

administration, what is the grant manager’s role in research

administration?

Slide 25

FY 2013 Slide 26

FY 2013

What Do Research Administrators Do?

• Assist PIs with the creation and submission of proposals• Manage sponsored programs for our faculty• Review, sign and submit proposals on behalf of the Institution• Review and negotiate sponsor terms and conditions for grants,

contracts and subagreements• Assure compliance with federal, state and university regulations

Slide 27

FY 2013

Research Administrator: Roles and Responsibilities

• Financial Administrator (Research Administrator, Grant Manager)– Shares responsibility for financial compliance – Manages finances– Reconciles individual expenses to the award budget– Ensures proper documentation is maintained– Prepares non-financial reports– Serves as an advisor to the PI and Chair’s or Dean’s Office on

financial/administrative matters– Prepares and/or approves documents for sponsored projects

• Financial• Human Resources • Other documents

Slide 28

FY 2013

Research Administrator: Roles and Responsibilities

• Financial Administrator (Research Administrator, Grant Manager) Cont.– Serve PD/PI

• Provide assistance to support (funded) research• Keep PI out of trouble

– Serve Institution• Keep institution out of trouble • Reports/investigates instances of unresolved financial non-compliance• Seeks the advice and approval of higher authority resources for guidance on

proper procedures and resolution of compliance issues– Serve the Sponsor

• Ensure sponsor funds are spent according to the award• If a federal award, you are ensuring tax dollars are spent wisely

Research administrators wear many hats and have many roles in serving the PI, the Institution, and the Sponsors Slide 29

FY 2013

Research Administrator: Roles and Responsibilities

Elective Matrix• As part of RAA, you and your supervisor reviewed your role in

research administration in your unit and selected applicable electives based on your role

• Not every research administrator has the same responsibilities

• You can use the decision matrix to help with choosing classes for career development

Slide 30

FY 2013

The Life Cycle of a Funded Project

Slide 31

FY 2013

Life Cycle of a Funded Project

• Proposal Development• Institutional Clearances• Proposal Submission &

Sponsor Review• Award Negotiation &

Acceptance• Award & Project Set-Up• Spending Award Funds• Project Monitoring• Approaching Project End

Slide 32Slide 32

FY 2013

Pre-Award and Post-Award

Most universities define the various functions and activities that occur throughout the life cycle of a funded project as either pre-award or post-award.

33Slide 33

FY 2013

• Pre-award is the general term applied to the services, functions and responsibilities that involve:– Identification of funding sources

and guidelines– Preparation of a proposal

(statement of the work to be done, budgets, personnel roster and resumes/vitae, other proposal required forms)

– Submission of the proposal according to sponsor requirements

– Review of the award and negotiation of the award if necessary to adjust to changes

34Slide 34

FY 2013

• Post-award is the general term applied to the services, functions, and responsibilities that involve:– Setting up the awarded project in the Duke

University financial system– Charging costs to the project in accordance

with the approved budget and sponsor regulations

– Reconciling and adjusting the project budget as needed to accommodate changes in research, corrections to charges, and increases/decreases in the effort levels of individuals working on the project

– Reporting on the financial progress of the project, including projecting costs for future expenses and effort of individuals working on the project

– Closing the project, including ensuring that all charges are accounted for, incorrect or unallowable charges are removed, all reports are filed, and all revenues accounted for

Slide 35

FY 2013

Role of Grant Manager in Pre-Award

• Facilitate and assist PI with proposal preparation, which may include:– Finding funding opportunities– Updating Biographical Sketch or Other Support– Completing Budget and/or Budget Justification

• Communicate and ensure correct formatting and other requirements

• Ensure that all proposal elements are complete and meet all sponsor requirements

• Ensure the complete proposal is submitted on time to appropriate pre-award office (ORA or ORS)

Slide 36

FY 2013

Role of PI in Pre-Award

• Determine which opportunity to apply for• Develop and write the project description and other scientific-

based sections• Communicate budget and other project needs to grant manager• Upload documents into SPS

*Remember that every PI has different needs from their grant manager while preparing a proposal for submission

Slide 37

FY 2013

Role of Pre-Award Offices

• Ensures that submissions meet requirements of announcement, as well as regulations and university policies

• Check all proposals for correct formatting, submission requirements, appropriate internal approvals (DPAF), etc.

• Communicate with grant manager/dept. regarding the successful submission of proposals, including answering dept. questions

Slide 38

FY 2013

Working Together

PI

Grant Manager

ORA/ORS

PI, Grant Manager and ORA/ORS all work together for the success of the proposal submission.

Slide 39Slide 39

FY 2013

Finding Funding

Slide 40

FY 2013

Sources of Sponsored Program Support

• Who funds research?– United States Government– State Agencies– Private Industry– Associations, Professional Groups– Foundations

• Corporate• Private

– Other entities• Foreign Governments• Foreign Corporations• Foreign Organizations

Slide 41

FY 2013

587

6

226

66 123 1

FY 2012 Sources of Duke University R&D Funds (in millions)

Federal

State and local

Business

Nonprofits

Institutional funds

other sources

total Duke R&D funding in FY12 = $1,009,911,000

Slide 42

FY 2013

Information Sources: How to find Funding

• Other resources provided include:– Funding Alert Newsletter– Grant Deadlines Newsletter– Use Funding Search Subscription Databases: – Pivot (COS): http://pivot.cos.com/– Foundation Directory Online:

http://www.ors.duke.edu/funding-search-tools – FundSource:

http://www.decadeofbehavior.org/intro.html– GrantsNet:

http://sciencecareers.sciencemag.org/funding– Grants.gov: http://

www.grants.gov/web/grants/home.html

The Funding Opportunities Team at the Office of Research Support provides funding workshops and seminars available to both Campus and Medical Center

Slide 43

FY 2013

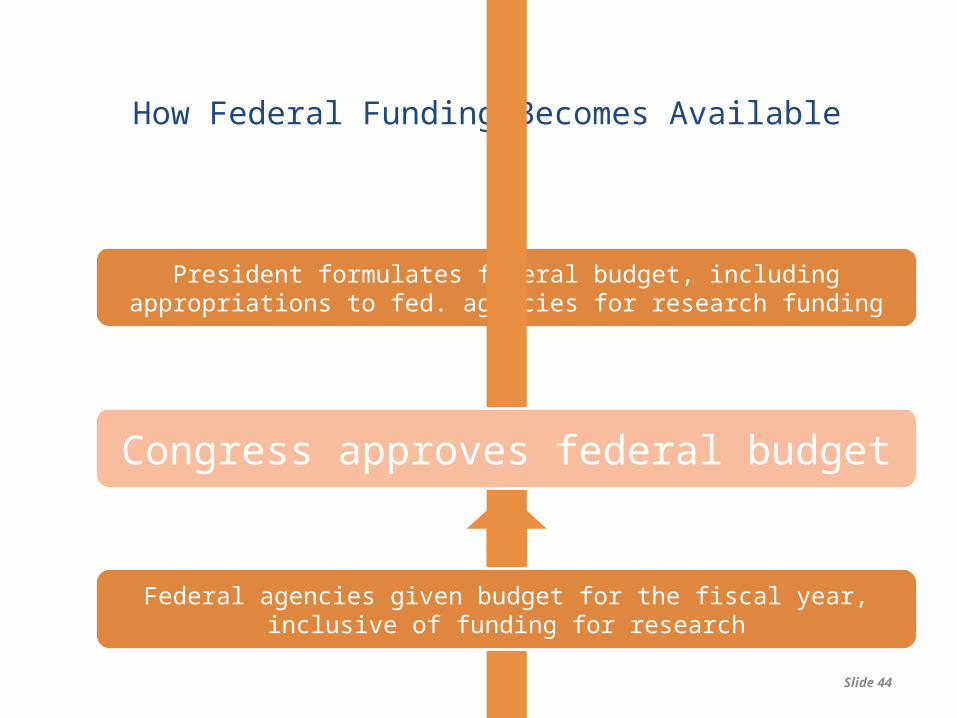

How Federal Funding Becomes Available

President formulates federal budget, including appropriations to fed. agencies for research funding

Congress approves federal budget

Federal agencies given budget for the fiscal year, inclusive of funding for research

Slide 44

FY 2013

PA: Program Announcement:

Describes existence of a research opportunity. It may describe new or expanded interest in a particular extramural program or be a reminder of a continuing interest in an extramural program.

NIH Specific PA: Parent Announcement: For common grant mechanisms that have transitioned to electronic submission, for use by applicants who wish to submit “unsolicited” or "investigator-initiated" applications.

Grants

Cooperative Agreements

RFA: Request for Applications:

Indicates the availability of funds for a research area of specific interest to a sponsor. Proposals submitted in response to RFAs generally result in a grant award. Specific grant announcements may be published in the Federal Register and/or specific sponsor publications. The RFA instructions include the information necessary to complete the application and mailing instructions

Grants

Cooperative Agreements

How Federal Sponsors Announce OpportunitiesWhat do the Letters Mean?

Slide 45

FY 2013

FOA: Funding Opportunity

Announcement:

A publicly available document by which a federal agency makes known its intentions to award discretionary grants or cooperative agreements, usually as a result of competition for funds.

Funding opportunity announcements may be known as program announcements, notices of funding availability, solicitations, or other names depending on the agency and type of program. Funding opportunity announcements can be found at Grants.gov and on the funding agency’s or program’s website.

Grants

Cooperative Agreements

Contracts

RFP: Request for Proposal:

Announcements that specify a topic of research, methods to be used, product to be delivered, and appropriate applicants sought. Proposals submitted in response to RFPs generally result in a contract award. Notices of Federal RFPs are published in the Commerce Business Daily.

Contracts

How Federal Sponsors Announce OpportunitiesWhat do the Letters Mean?

Slide 46

FY 2013

RFQ: Request for Quotation:

A type of bidding solicitation in which vendors provide a cost quote for the completion of a particular project or program. A Request For Quote is a variation of a Request For Proposal (RFP), and typically provides more information to the bidder about the project's requirements. It often requires the bidder to break down costs for each phase of the project so as to allow the soliciting agency to compare different bids.

A Request for Quote is typically used in situations where products and services are standardized, since this allows the soliciting agency to compare the different bids easily. It is also more likely to be used when the soliciting agency knows the volume of products that it wishes to purchase.

Contracts

How Federal Sponsors Announce OpportunitiesWhat do the Letters Mean?

Slide 47

FY 2013

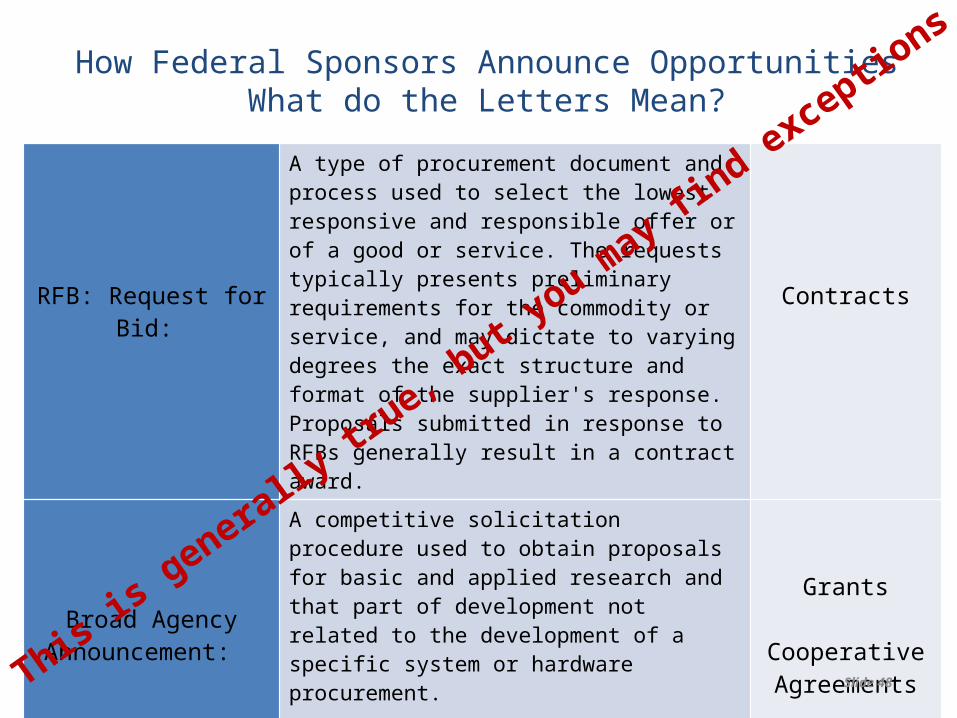

RFB: Request for Bid:

A type of procurement document and process used to select the lowest responsive and responsible offer or of a good or service. The requests typically presents preliminary requirements for the commodity or service, and may dictate to varying degrees the exact structure and format of the supplier's response. Proposals submitted in response to RFBs generally result in a contract award.

Contracts

Broad Agency Announcement:

A competitive solicitation procedure used to obtain proposals for basic and applied research and that part of development not related to the development of a specific system or hardware procurement.

The type of research solicited under a BAA attempts to increase knowledge in science and/or to advance the state of the art as compared to practical application of knowledge.

Grants

Cooperative Agreements

Contracts

How Federal Sponsors Announce OpportunitiesWhat do the Letters Mean?

Slide 48

This is generally

true, b

ut you m

ay find exceptio

ns

FY 2013

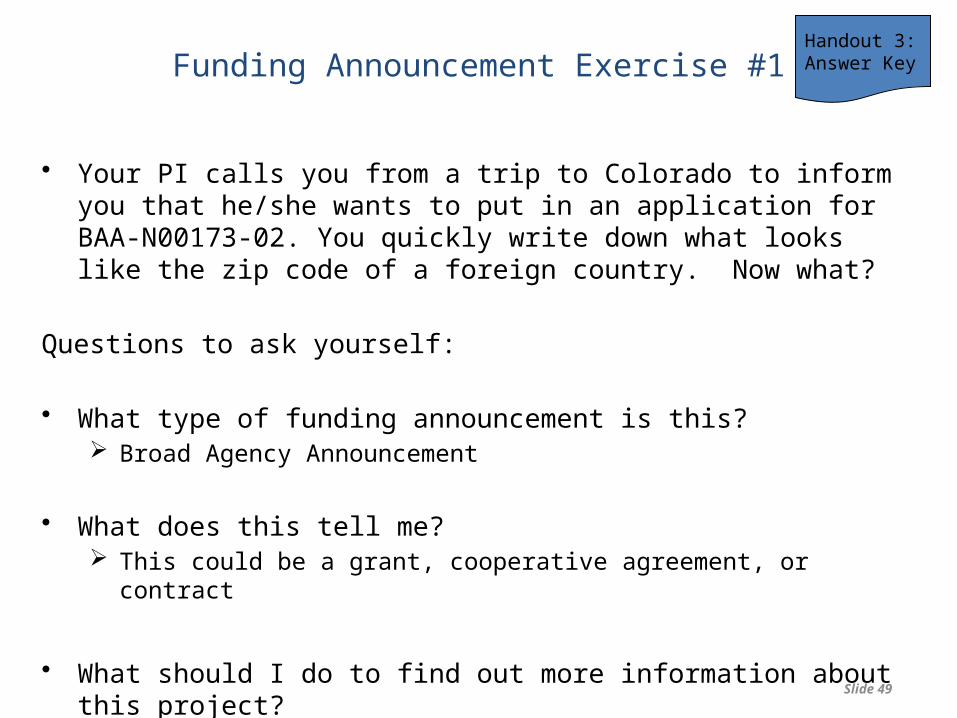

Funding Announcement Exercise #1

• Your PI calls you from a trip to Colorado to inform you that he/she wants to put in an application for BAA-N00173-02. You quickly write down what looks like the zip code of a foreign country. Now what?

Questions to ask yourself:

• What type of funding announcement is this? Broad Agency Announcement

• What does this tell me? This could be a grant, cooperative agreement, or contract

• What should I do to find out more information about this project? Google it! Look it up the announcement number on grants.gov

Handout 3: Answer Key

Slide 49

FY 2013

Funding Announcement Exercise #2

You had a pre-work assignment to find two funding announcements using grants.gov. PA-13-302 NSF 13-606

Using these announcements, identify the following key elements:• What is the sponsoring agency?• What is the application due date?• What is the maximum project period?• Is Duke University an eligible organization to apply to this

announcement?• Where can you go to find more specific application

instructions?Slide 50

FY 2013

Funding Announcements Exercise Answer Key

NIH PA-13-302• Funding Agency: NIH• Due dates: Standard dates

apply• Can Duke apply? Yes• More instructions: SF-424

Application Guide

NSF 13-606• Funding Agency: NSF• Due dates: January 13,

2014, January 12, 2015, January 11, 2016

• Can Duke apply? Yes• More instructions: NSF Grant

Proposal Guides

Slide 51

Takeaway: Funding announcements often provide general information. You will likely need to review specific sponsor guides to determine specifics such as formatting, page lengths, required forms, etc. We will discuss this more in a few minutes.

Handout 4: Answer Key

Slide 51

FY 2013

Find FOA’s to use in ORA/ORS class

Get text from pre-award

Slide 52

Homework #1: Find FOA’s for your next

class

Homework #2: Review the Komen

FOA, and answer the associated questions

FY 2013

Funding Mechanisms

• Contracts

• Cooperative Agreements

• Grants

• Fellowships

• Gifts

Leve

l of

Res

tric

tions

Less

M

ore

53 Slide 53

Basic Types of SupportType of Support

Mechanism Rules & Regulations

Management Budget

Grant Provides assistance: PA, RFA, FOA, BAA

A-21, A-110, A-133, FDP, Duke’s GAPs

Flexible, expanded authorities can usually be applied, movement between budget categories generally allowed, major changes require sponsor approval

Estimate, Flexible, sponsor expectation is new or advanced discovery, project completion, etc.

Cooperative Agreement

Provides assistance with substantial sponsor involvement: RFA, FOA, BAA

A-21, A-110, A-133, FDP, Duke’s GAPs

Expanded authorities can be usually applied, movement between budget categories generally requires sponsor involvement, major changes require sponsor approval

Estimate, Flexible, significant interaction between the recipient and the sponsor

Contract Acquisition of goods or services: RFP, RFQ, RFB

Federal Acquisition Regulations

Sponsor approval required for changes, deliverables and results expected as agreed upon

Detailed, category specific, very limited authority to change scope of work, expectation of the sponsor for a tangible deliverable (product, report, etc.)

Gift Informal/Formal letter or agreement

Donor terms and conditions, Duke’s GAPs

Flexible, Stewardship reports may be required

May be very informal, or may be extensive, dependent on sponsor

Slide 54

FY 2013

Do I Check the FOA or Proposal Guide?

FOA• General guidelines• Funding mechanism• Eligible institutions• Eligible applicants• References sponsor rules• Allowable budget requests• Due dates• Submission type

Proposal Guide• Required forms• Required formatting• Page limits• Additional help:

– NIH Writing Instructions to PIs• http://

grants.nih.gov/grants/writing_application.htm

– NSF Writing Instructions to PIs• http://www.nsf.gov/pubs/policydocs/pap

pguide/nsf13001/nsf13_1.pdf

Slide 55

FOAs usually provide high-level information. Each sponsor publishes more generic instructions for writing the proposal in their proposal guidelines/policy statements.• NIH Grants Policy Guide:grants1.nih.gov/grants/funding/424/index.htm#inst• NSF Guide:http://www.nsf.gov/publications/pub_summ.jsp?ods_key=gpm

FY 2013

A Reasonable TimelinePI Responsibilities:

Start Proposal Development

Outline Specific Aims

Notify Grant Manager of planned submission Study Section Review

Receive Summary Statement

Advisory Council Review

PI Responsibilities:

Develop Proposal

Submit Proposal

GM Responsibilities

Award Setup

Slide 56It almost never happens this way!

Proposal Due Date

Project Start Date

Min. 6 months 3 months

GM Responsibilities

Read the full announcement

Prepare Application Package

Route application for sign-off

FY 2013

Announcement Review Tips

• Always read the full announcement• Highlight details regarding deadlines, limitations, exceptions,

inclusions, exclusions, submission type• Refer to sponsor proposal guidelines• Communicate submission requirements and deadlines to PI• Ask clarifying questions to PI and ORA/ORS when needed• Plan timeline according to sponsor deadline• Check for additional limitations, exceptions, etc.• Review sponsor FAQ’s for common mistakes and warnings• Maintain organization of both electronic and paper documents• Attention to detail!• Every announcement is unique; handle each and every one with care

Slide 57

FY 2013

Announcement Review Tips, Continued

• Be proactive, rather than reactive (think ahead)• Give PIs deadlines for providing you with documents needed for

submission• Regularly update the PI on your status of the proposal preparation

and request the same in return• Always be a student! Continued education in research

administration will improve your PI communication

Slide 58Slide 58

FY 2013

Remember

• The PI may not always know the funding opportunity number • You may have to search by agency for the title of the opportunity• You may only know pieces of information such as the CFDA number, title

and agency• Use your information resources to assist you in tracking down the

appropriate announcement and verify the information with the PI.• Use search engines, like Google, to help locate the opportunity

*If the information provided is not enough to locate the opportunity, ask the PI for more information that may help you.

Slide 59

FY 2013

Now that you’ve located the funding opportunity announcement, make sure you and the PI are both ready to begin the proposal preparation process.

Slide 60Slide 60

FY 2013

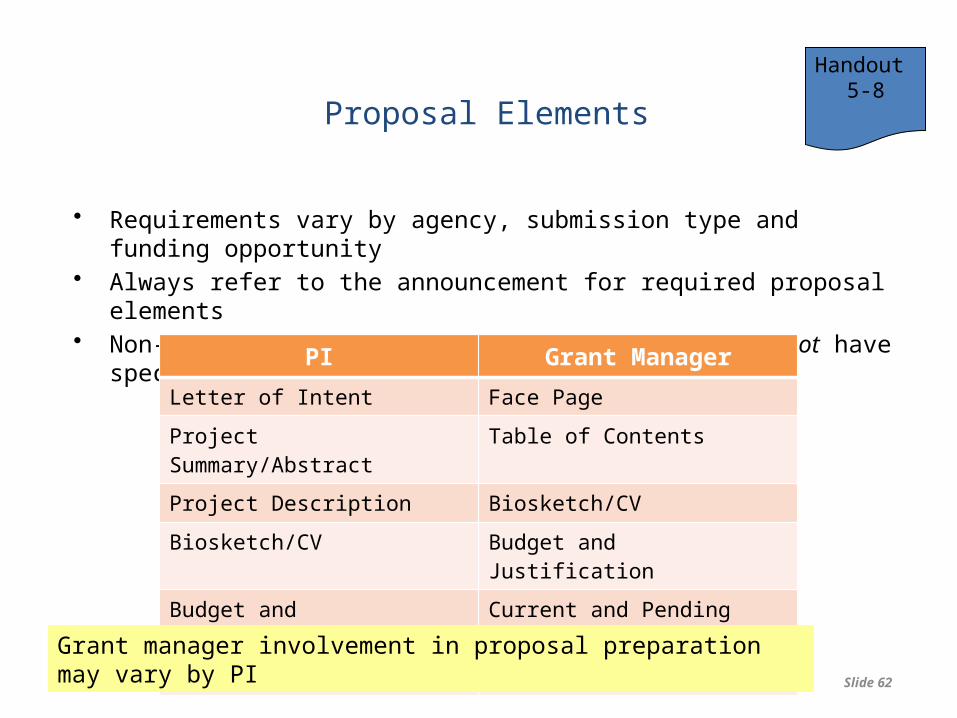

Proposal Elements

• Letter of Intent• Face Page/Cover Sheet• Project Summary/Abstract• Table of Contents• Project Description• Biographical Sketch/Vitae• Budget• Budget Justification• Current and Pending Support• Subcontract/Consortium• Appendices

*Many Federal sponsors use an application package called SF424 (R&R)

Slide 61Slide 61

Appendix 3

You had a pre-work exercise to review a list of common grant terms. That list is provided in Appendix 3.

FY 2013

Proposal Elements

• Requirements vary by agency, submission type and funding opportunity• Always refer to the announcement for required proposal elements• Non-federal sponsors, such as foundations, may not have specific forms

Slide 62Slide 62

Handout 5-8

PI Grant Manager

Letter of Intent Face Page

Project Summary/Abstract Table of Contents

Project Description Biosketch/CV

Biosketch/CV Budget and Justification

Budget and Justification Current and Pending Support

Appendices Subcontract

Grant manager involvement in proposal preparation may vary by PI

FY 2013

How Is a Proposal Reviewed and Approved for Submission?

Slide 63

FY 2013

SPS – Sponsored Project System• Used by grant managers to route proposals for approval• Use is mandatory for proposals

• Exceptions: Internal Duke proposals and gifts• Routes electronically for approvals• Transmits to Grants.Duke for NIH, DOE, and many DOD electronic

submissions• Record of project life-cycle• Reporting tool• Step-by-step budget entry• Provides budget templates• Allows automatic calculation:

– Salaries– Fringe Benefits– Inflation for out-years (exceptions: equipment and subcontracts)– Facilities & Administrative Costs (F&A)

• Has Duke business rules built in• Generates some Federal and generic forms

64 SPS Registration: http://research.som.duke.edu/resources/ora-training-session-registration Slide 64

Handout9

FY 2013

Institutional Considerations

• Who needs access to SPS?– Contact ORA or ORS to obtain access

• Is it an “institutionally limited opportunity”?– Contact ORS

• What are my internal deadlines for routing and approvals?– Due to ORA 7 business days prior to sponsor deadline (SOM/SON)– Due to ORS 5 business days prior to sponsor deadline (Campus)

Slide 65Slide 65

FY 2013

Institutional Considerations

• Does my PI have PI status according to Duke’s guidelines?– Automatic PI/co-PI status: Regular rank and tenure/tenure track

faculty, research professors, professor of practice– Must request PI/co-PI status: non-regular rank faculty

• Authorization from Chair and/or Dean (commit resources)• Forms available from Office of Research Administration (ORA)/

Office of Research Support (ORS)

Resources:– Forms available from Office of Research Administration (ORA) and

Office of Research Support (ORS)– See Faculty Handbook for policy:

http://www.provost.duke.edu/policies/fhb.html

Slide 66Slide 66

FY 2013

Proposal Budgeting

Slide 67

The grant manager has many responsibilities in proposal preparation. Often, the grant manager has the most

responsibility in budget development.

FY 2013

What is the Budget?

“The budget plan is the financial expression of the project” – Circular A-110

The budget is a reflection of how well the PI understands the cost associated with the project

68 Slide 68

FY 2013

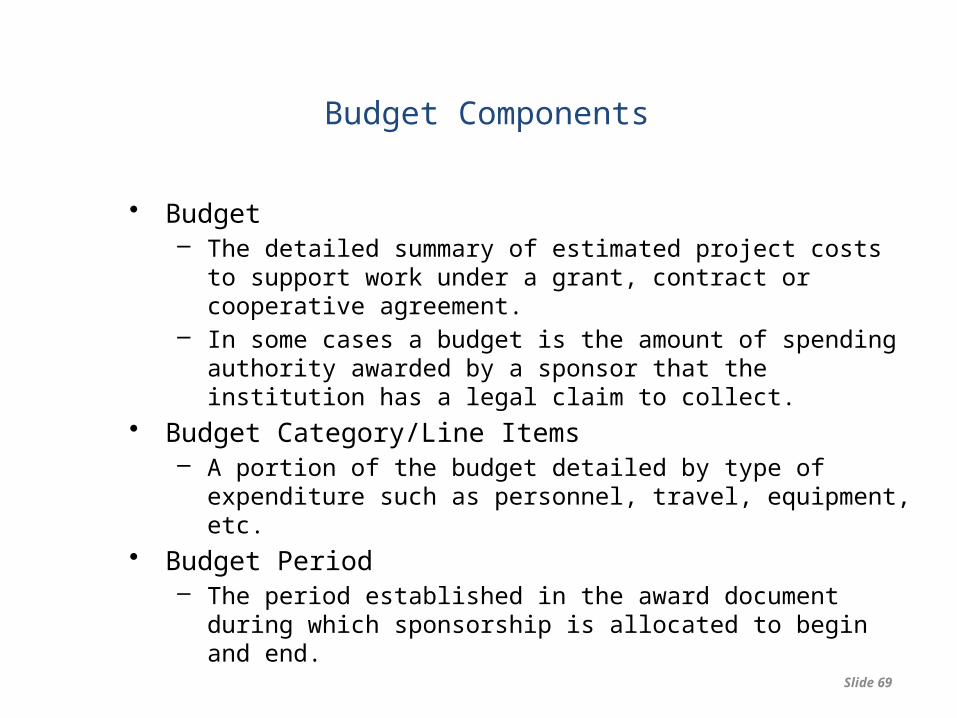

Budget Components

• Budget– The detailed summary of estimated project costs to support work

under a grant, contract or cooperative agreement. – In some cases a budget is the amount of spending authority

awarded by a sponsor that the institution has a legal claim to collect.

• Budget Category/Line Items– A portion of the budget detailed by type of expenditure such as

personnel, travel, equipment, etc.• Budget Period

– The period established in the award document during which sponsorship is allocated to begin and end.

69 Slide 69

FY 2013

Budget Components

• Budget Justification/Narrative– The section of a proposal that explains the budget– The itemization of totals, the purpose of purchased supplies and

services, and the justification of the size of salaries, fringe benefits, and indirect costs

70 Slide 70

FY 2013

Cost

• The outlay or expenditure made to achieve an objective on a sponsored project.

• Cost are either allowable or unallowable.

Slide 71

Duke has many GAPs that provide guidance on charging costs to sponsored projects that are referenced throughout this material.

FY 2013

Allowable Costs

• Generally, it is not the type of cost that determines allowability, it is the purpose and circumstance of the expenditure. Many categories of costs are allowable as a direct or indirect, e.g., salaries, travel, materials, etc.

• An allowable cost must be:– Reasonable

• A prudent business person would have purchased this item and paid this price. It also means that you should not purchase items with “add-on” features that are not essential to the project

• The item purchased must be necessary to the project; in other words, the project will not function effectively without this item or charge

– Allocable• It can be assigned to the activity on some reasonable basis.

– Consistently Treated• Like costs must be treated the same in like circumstances, as either direct or F&A costs.

(OMB A21 sections C.2 – C.4)

• If a cost cannot meet the above criteria, it is unallowable, no matter what.

Costs must be easily identified as specifically associated with the project’s activities. For this reason, it might be hard to justify sharing the cost of the office copier or charging a local phone line to the project unless there is very good documentation, record-keeping, and prior approval from the university.

Slide 72

FY 2013

“Unallowable”

• An “unallowable” cost is one that is not eligible for reimbursement by the Federal government, either as Direct or F&A.

• An unallowable cost cannot be used as cost share.

• alcoholic beverages

• entertainment

• fund raising

• Alumni events

Slide 73

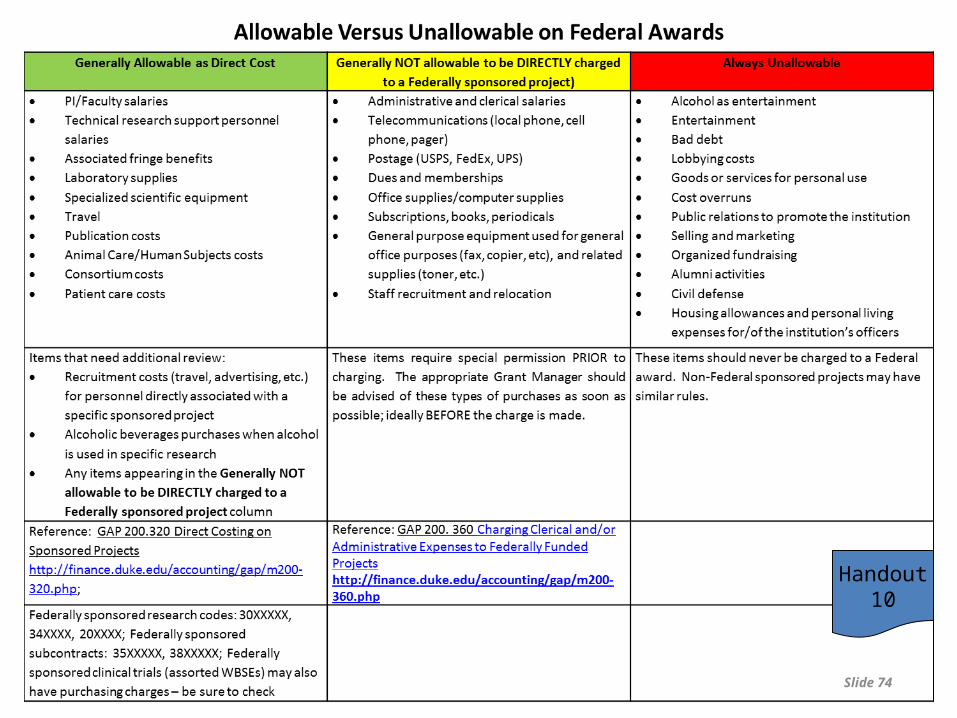

FY 2013 Slide 74

Handout10

FY 2013

Allowable or Unallowable?

AllowableSpeeding Ticket: PI received a ticket while driving to attend meeting as required by the project

Kindle reading devices:

Pantyhose:Used to collect ticks for Lyme Disease research

Pt. care charges: Alcoholic Drinks:PI travels to Germany, and submits receipts that include beer with dinner.

Unallowable

Fines and penalties areunallowable.

Allowable as an incentive To participants in a Literacy study

Pantyhose are a supply that directly benefits the award.

Study on language evolution of 15th century Incans. Un-likely that pt. care directly benefits this award.

Phase III cancer drug trial. Likely that pt. care directly benefits this award.

Alcohol is unallowable.See Public Relationsand Social expenses g/l definition 693200 for clarification.

For more information on allowable charges, consult section J of OMB circular A-21

Unallowable as a Piece of general-Purpose equipment

Slide 75

Homework Assignment #3- A-

21 and GAP Preview

FY 2013

Allocability

• A cost is allocable to a particular sponsored project if the goods or services involved are chargeable or assignable to the sponsored project.

• How is allocability determined?– A cost can be allocable as a direct or an indirect cost– A cost is allocable as a direct cost if the goods or services provided are

assignable in accordance with the relative benefits received:• It is incurred solely to advance the work under the sponsored agreement• It benefits both the work under the sponsored agreement and other work of

the institution in proportions that can be approximated

Slide 76

FY 2013

Allocability

• How is Allocability Determined, Continued:– Sometimes an item will be used for two or more projects or activities.

This means that you should split the cost among all the projects that will use the item.

• Such costs must be allocated to sponsored awards in proportion to the actual benefit received by the award

• If actual allocation cannot be accurately stated, then an allocation methodology must be developed, and costs distributed accordingly

• There are several good methods for documenting how a charge is assigned to multiple projects

FY 2013

Easily AllocableProject-specific items and services – Charged

to a single project

May Require Additional Allocation DocumentationItems and services used for multiple projects

Project-specific reagents (e.g., drugs, chemicals, specific antibodies)Specialized scientific equipment used to support a specific project

Animal Care/Human Subjects costs associated with a specific project

Oligonucleotides/siRNAs used for a single project

Project-specific cell lines Project-specific services (e.g., flow

cytometry, mass spec, peptide/antibody production)

Acetone Breeder colonies for future animal experiments Cell culture consumables Culture media General cell lines Radiation Routinely used reagents (e.g., secondary/common antibodies, BSA, transfection reagent) Office supplies used as laboratory support (binders, etc.) Gas Purchase/Tank rental Subscriptions, books, periodicals General office supplies/computer supplies General purpose equipment used for general purposes (fax, copier, etc), and related supplies

(toner, etc.) Gloves/PPE Glassware Lab Safety Equipment (e.g. lab coat, spill kit, etc.) Common reagents (e.g., salts, alcohols, gel reagents) Common services (e.g., equipment repair, water system maintenance, service contracts) Common consumables (e.g., pipet tips, filter paper, blotting membrane) Common equipment (e.g., centrifuge, oven, shaker)

Allocating Charges on Federal Awards

Slide 78

FY 2013

Direct Costs on Sponsored Awards

References: GAP 200.320 Direct Costing on Sponsored Projects:

http://finance.duke.edu/accounting/gap/m200-320.php

OMB Circular A21 section D.1.

• Identified specifically with a particular sponsored

agreement

• Incurred to advance the work under that sponsored agreement

• Assigned to that sponsored agreement with relative ease and a high degree of accuracy

Slide 79

FY 2013

Direct Cost Examples

Costs that can be directly

assignableto one

program

Equipment

Laboratory Technicians

Principal Investigator

Project related travelAssociated fringe benefits

Research Associatesand Assistants

Project relatedmaterials & supplies

Subcontract costs

Slide 80

FY 2013

Direct Costs Guidelines

Allocable?

Reasonable?

Consistent withDU Practices?

Sponsor FundsAvailable?

Direct Charge onSponsored project

Allowable?

Not an Appropriate Direct Charge on

Sponsored Project

Direct Cost to Institutional Funds

Cost Incurred?

Funded Project?

Yes

No

Yes

Yes

Yes

Yes

Yes

No

No

No

No

Slide 81

FY 2013

Now that you are familiar with the allowable direct charges on a budget, let’s

examine building a compliant budget

Slide 82

FY 2013

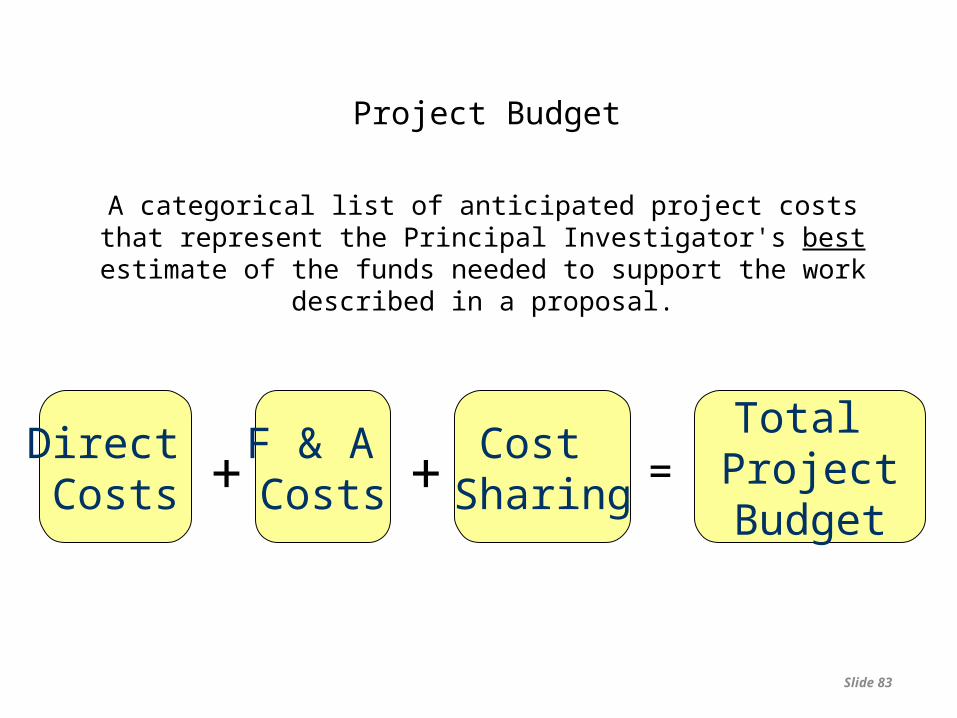

Project Budget

A categorical list of anticipated project costs that represent the Principal Investigator's best estimate of the funds needed to support

the work described in a proposal.

Direct Costs

F & A Costs

Cost Sharing

Total ProjectBudget

++ =

Slide 83

FY 2013

Building a Compliant Budget

• It is important to remember that the budget for a sponsored project must be in accordance with the applicable policies, rules and regulations of both the sponsor and Duke University.

• Duke University adheres to the federal cost principles as defined in OMB Circular A-21, Cost Principles for Educational Institutions. This guidance defines the rules applied to educational institutions when doing business with the federal government and forms the basis for Duke University’s costing practices.

The following will provide tools and resources to help you build a strong and compliant project budget:

• Allowable vs. Unallowable

• Direct Costs vs. Indirect Costs

• Rates and Institutional Information

• Cost Sharing

• Tuition RemissionSlide 84

FY 2013

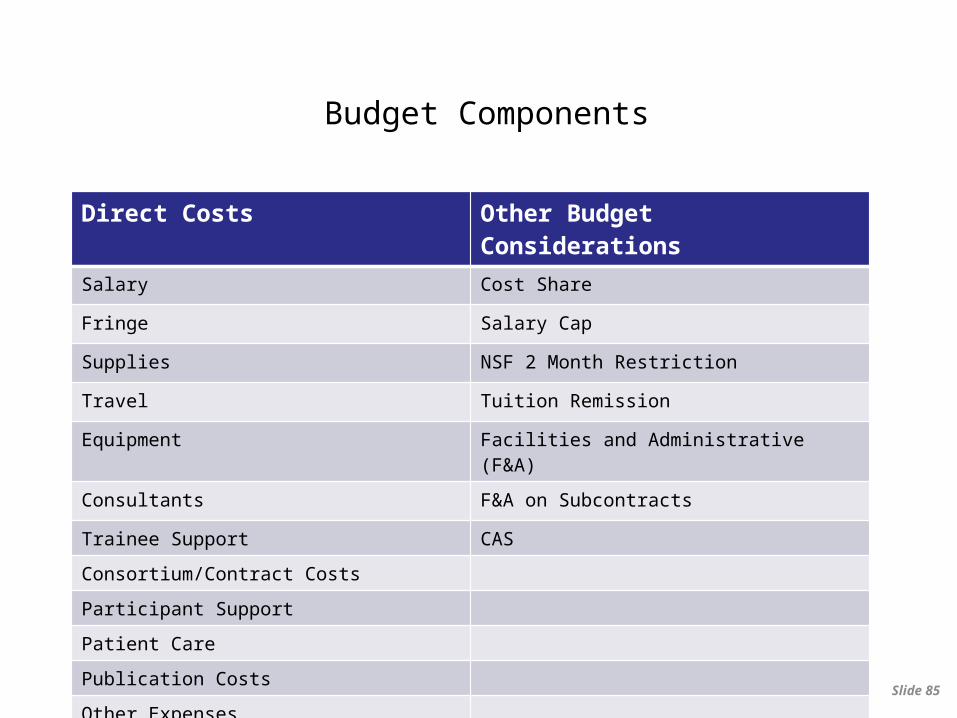

Budget Components

Direct Costs Other Budget Considerations

Salary Cost Share

Fringe Salary Cap

Supplies NSF 2 Month Restriction

Travel Tuition Remission

Equipment Facilities and Administrative (F&A)

Consultants F&A on Subcontracts

Trainee Support CAS

Consortium/Contract Costs

Participant Support

Patient Care

Publication Costs

Other Expenses

Slide 85

FY 2013

Let’s take a closer look at direct costs…

Slide 86

As we move through this section, keep the budget template handy so you can see how each component

fits into the budget proposal.

FY 2013

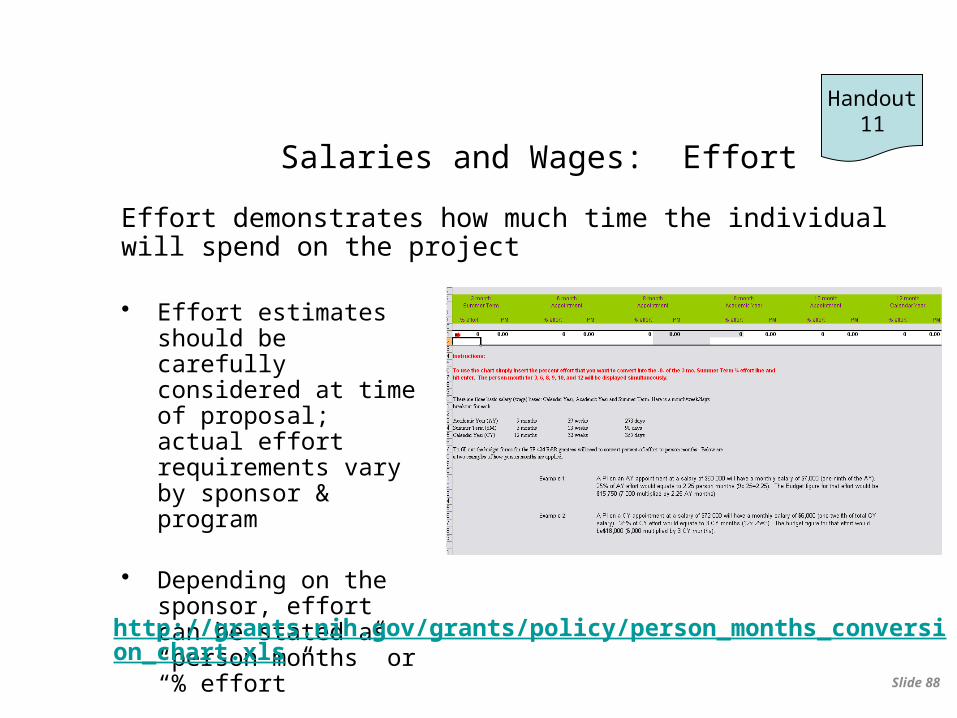

Salaries and Wages: Effort

• Salary and Wages: compensation for personal services which include fringe benefits

• Effort: the total work done to achieve a particular end

• Effort can be:– Total Professional Effort: The amount of time spent on ALL activities

– both University activities AND Non-University (examples: VA and Clinical Services) activities.

– University Effort: The amount of time spent ONLY on University (research, instruction, and administrative) activities.

• Also Institutional Base Salary (IBS): the annual compensation that the university pays for an individual's appointment, whether that individual's time is spent on research, teaching, patient care, or other activities

87 Slide 87

FY 2013

Salaries and Wages: Effort

• Effort estimates should be carefully considered at time of proposal; actual effort requirements vary by sponsor & program

• Depending on the sponsor, effort can be stated as “person months” or “% effort”

http://grants.nih.gov/grants/policy/person_months_conversion_chart.xls

Effort demonstrates how much time the individual will spend on the project

88

Handout11

Slide 88

FY 2013

Salaries and Wages: Effort

• The Duke Process– The owning department/center/institute of the SPS proposal must

complete the Employee Salary Request Form and forward it to the Salary Single Point of Contact (SSPOC) or delegate for the employee’s department/center/institute.

• School of Medicine SPOC list: http://research.som.duke.edu/research-administration/financial-administration/salary-requests/fringe-benefits

• School of Medicine Employee Salary Request Form: http://research.som.duke.edu/files/documents/Salary_Request_Form.pdf

• Campus SSPOC list: https://ors.duke.edu/op2/op2-requesting-employee-salary-information

• Campus Employee Salary Request Form: https://ors.duke.edu/forms/employee-salary-request-form

89

Handout12

Duke Effort Reporting GAP: http://finance.duke.edu/accounting/gap/m200-170.php Slide 89

FY 2013

Salaries and Wages

• Senior/Key Personnel

– OMB Circular A-21 Clarification: Must have measurable effort (1% or more)

– SOM Maximum Effort for PI:• Faculty members that have (or expect to have) Principal Investigator (PI)

status on an awarded sponsored research project(s) should not be externally funded for greater than 98% (11.76 calendar months) for their sponsored research effort

• Exceptions/Approvals: Exceptions must be documented and requested in writing through the office of the Vice Dean for Research of the School of Medicine

90Slide 90

FY 2013

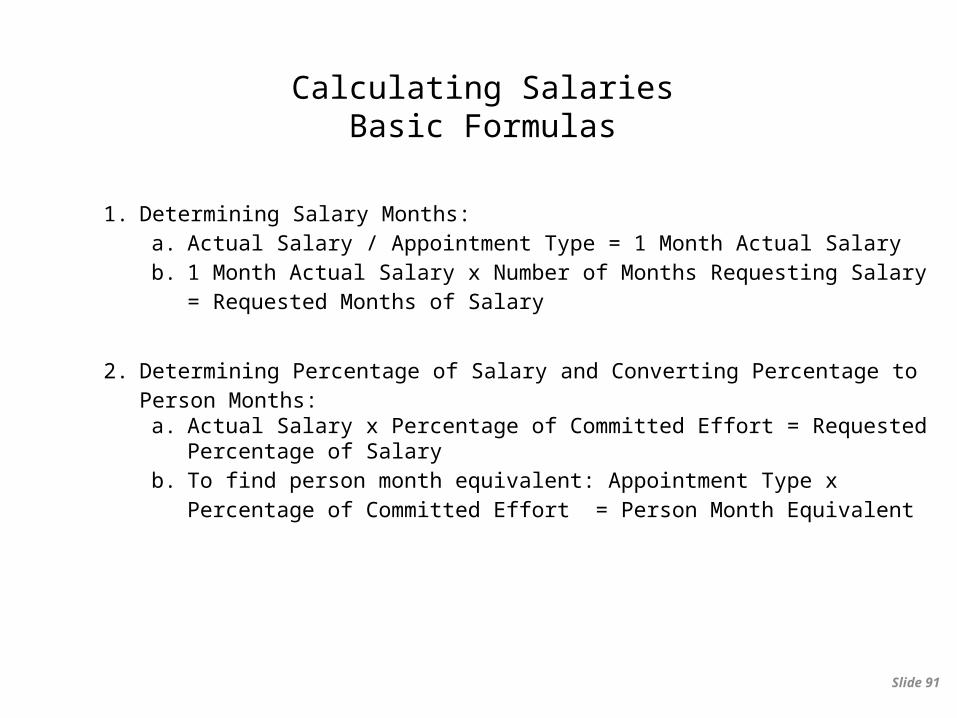

Calculating SalariesBasic Formulas

1. Determining Salary Months:a. Actual Salary / Appointment Type = 1 Month Actual Salaryb. 1 Month Actual Salary x Number of Months Requesting Salary = Requested

Months of Salary

2. Determining Percentage of Salary and Converting Percentage to Person Months:a. Actual Salary x Percentage of Committed Effort = Requested Percentage of

Salaryb. To find person month equivalent: Appointment Type x Percentage of

Committed Effort = Person Month Equivalent

91 Slide 91

FY 2013

Salaries and Wages: Fringe Benefits

• Fringe Benefits are a form of non-wage compensation for Duke employees

• Negotiated with the federal government annually• Actual and projected rates• Rates vary by sponsor and employee type

Handout13

Slide 92

FY 2013

• Consistent with research plan

• Group supplies into logical categories

• Provide detail justification in budget narrative

• Describe changes that occur from year to year

Note: Operational supplies, such as office supplies, may not be allowable as a direct cost without project specific / need based justification

Supplies

Slide 93

FY 2013

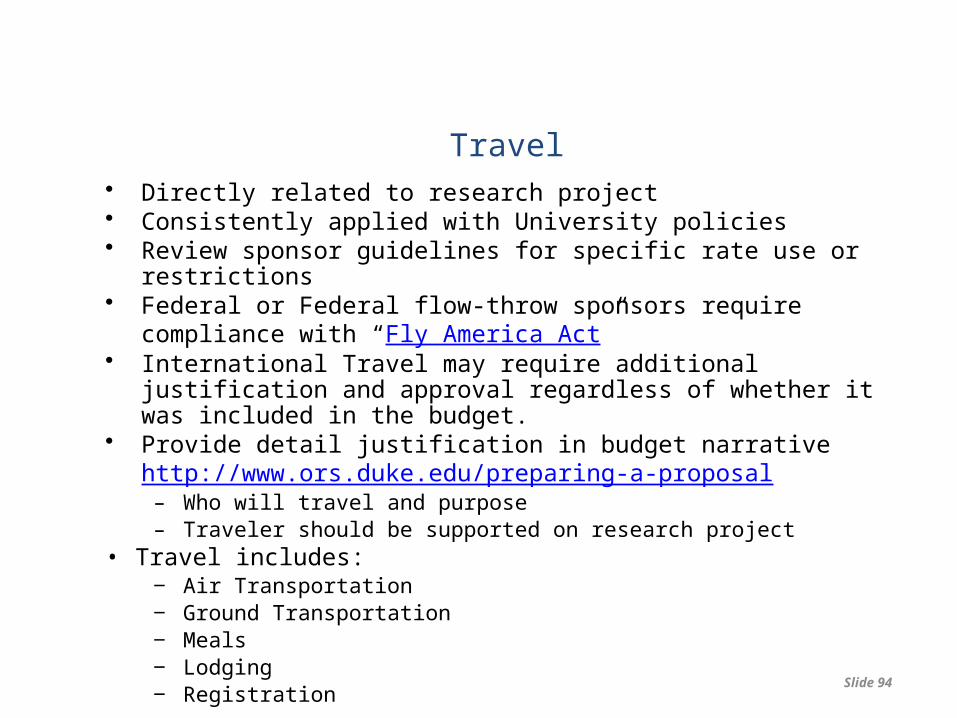

• Directly related to research project• Consistently applied with University policies• Review sponsor guidelines for specific rate use or restrictions• Federal or Federal flow-throw sponsors require compliance with “

Fly America Act”• International Travel may require additional justification and approval

regardless of whether it was included in the budget.• Provide detail justification in budget narrative

http://www.ors.duke.edu/preparing-a-proposal – Who will travel and purpose– Traveler should be supported on research project

• Travel includes:‒ Air Transportation‒ Ground Transportation‒ Meals‒ Lodging‒ Registration

Travel

Slide 94

FY 2013

• Capital equipment >$5,000 • Useful life >1 year• Excluded from F&A• Item required to perform work and not currently available

• Auditors will require documentation that the equipment is needed and not readily available

• Provide justification, including make and model, if known (Note that this does not allow the institution to by-pass fair bidding standards when purchasing the equipment)

• GAP 200.100 Capital Equipment Purchases On Sponsored Projects

Equipment

Slide 95

FY 2013

• Not salary• External Consultants can be:

– Key personnel if time is stated in the letter and budget justification (should be listed under Consultants)

– Individual should be expert in the field – Commercial entity should be in the business of conducting this type

of service– Meet IRS test for independent contractor – Ownership of service or product determines whether “consultant” or

“subcontractor”

• Remember: Duke employees should not be listed as consultants on a Duke budget unless approved by the sponsor.

Consultants

Slide 96

FY 2013

Stipends

• Subsistence allowance to help defray living expenses during the period of training

• Not a salary, not considered employees of either the government or the institution

• Grantees may supplement stipends– Amount determined according to formally established policies

applied to all in similar training status• Supplements should come from non-Federal funds• Without additional effort or obligation to the trainee

Slide 97

FY 2013

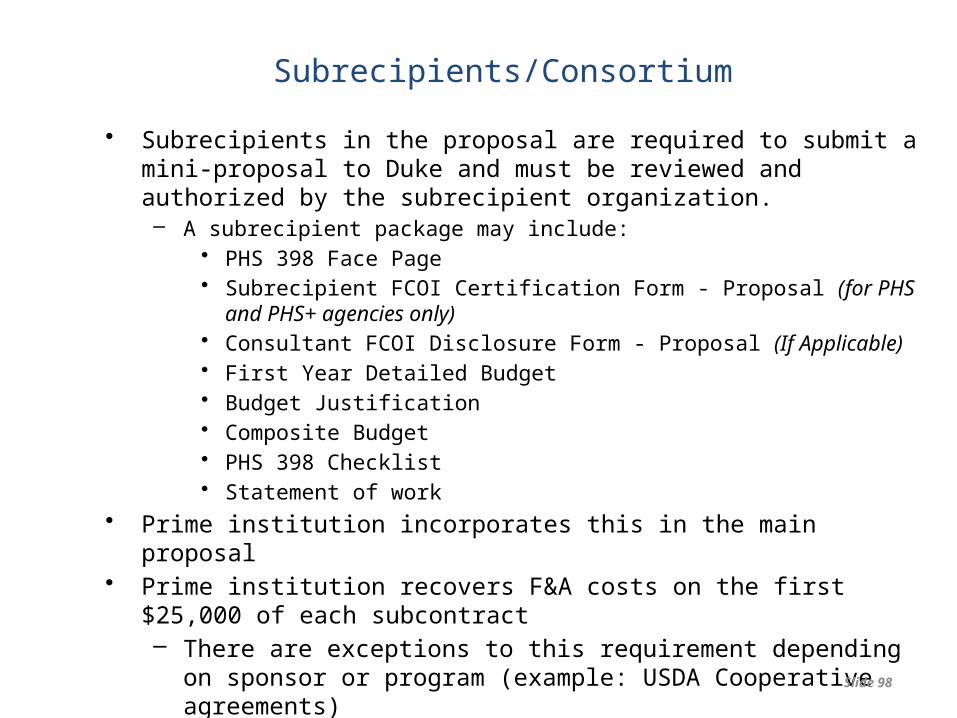

Subrecipients/Consortium

• Subrecipients in the proposal are required to submit a mini-proposal to Duke and must be reviewed and authorized by the subrecipient organization.– A subrecipient package may include:

• PHS 398 Face Page• Subrecipient FCOI Certification Form - Proposal (for PHS and PHS+

agencies only)• Consultant FCOI Disclosure Form - Proposal (If Applicable)• First Year Detailed Budget• Budget Justification• Composite Budget• PHS 398 Checklist• Statement of work

• Prime institution incorporates this in the main proposal• Prime institution recovers F&A costs on the first $25,000 of each

subcontract– There are exceptions to this requirement depending on sponsor or

program (example: USDA Cooperative agreements)Slide 98

FY 2013

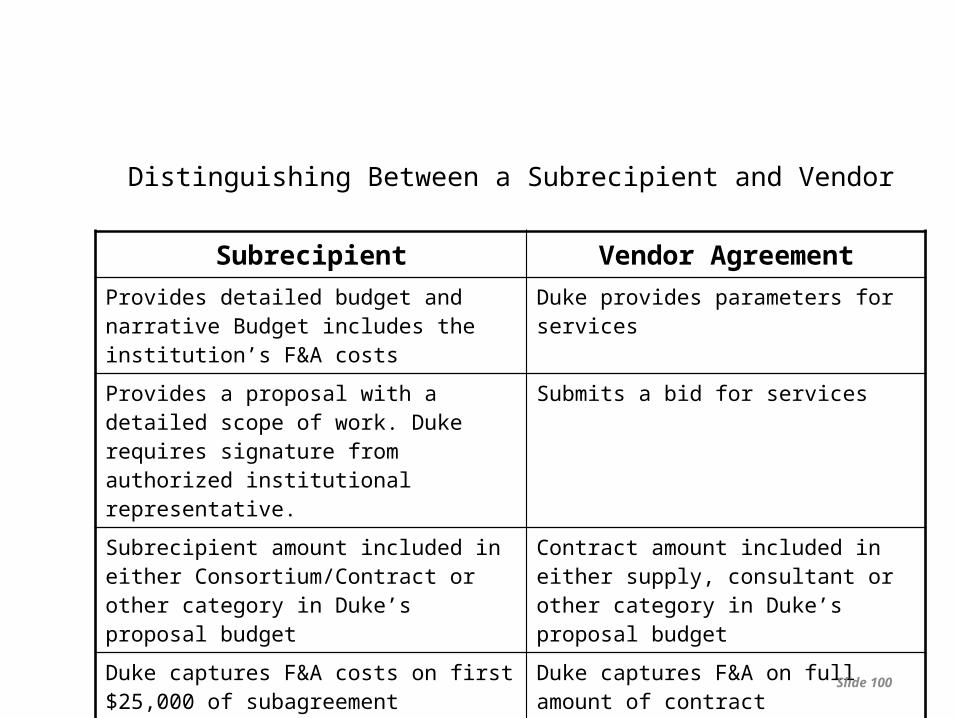

Distinguishing Between a Subrecipient and Vendor

Subrecipient Vendor Agreement

Subrecipient services are uniquely designed in response to each project, and not provided commercially

Vendor provides the goods and services commercially

Subrecipient technical lead is usually a scientific collaborator or possibly a co-investigator on the proposed project

Vendor operates in a competitive environment

Subrecipient retains rights to intellectual property

Vendor retains no rights to intellectual property

Subrecipient participates in development and execution of scope of work

Vendor provides the goods or services ancillary to the operation of the federal program

Slide 99

FY 2013

Distinguishing Between a Subrecipient and Vendor

Subrecipient Vendor Agreement

Provides detailed budget and narrative Budget includes the institution’s F&A costs

Duke provides parameters for services

Provides a proposal with a detailed scope of work. Duke requires signature from authorized institutional representative.

Submits a bid for services

Subrecipient amount included in either Consortium/Contract or other category in Duke’s proposal budget

Contract amount included in either supply, consultant or other category in Duke’s proposal budget

Duke captures F&A costs on first $25,000 of subagreement

Duke captures F&A on full amount of contract

Slide 100

FY 2013

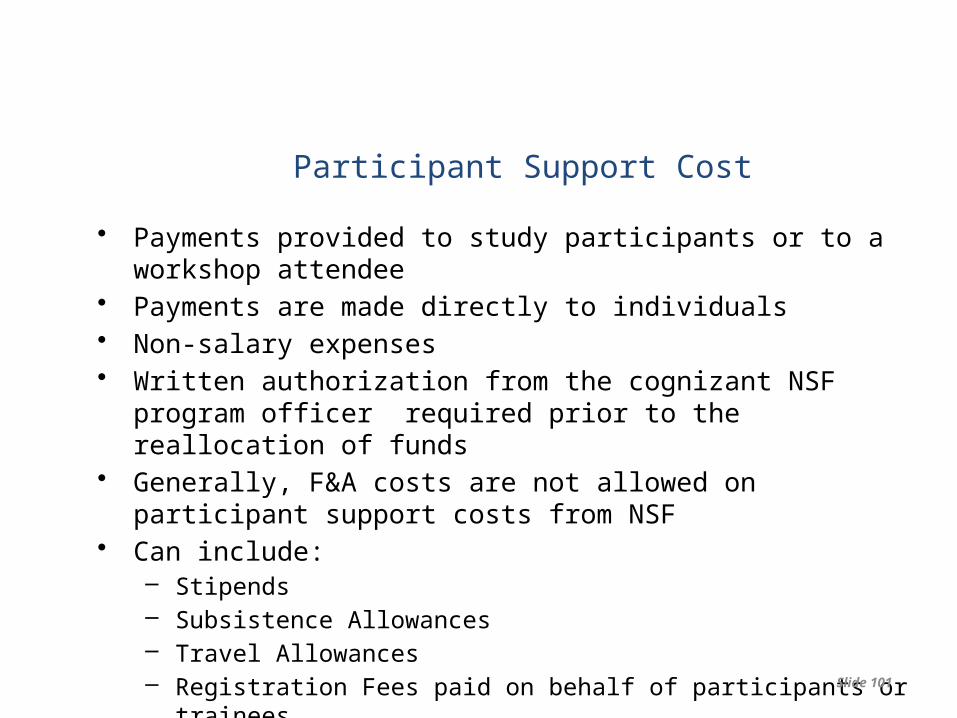

Participant Support Cost

• Payments provided to study participants or to a workshop attendee• Payments are made directly to individuals• Non-salary expenses• Written authorization from the cognizant NSF program officer

required prior to the reallocation of funds• Generally, F&A costs are not allowed on participant support costs

from NSF• Can include:

– Stipends– Subsistence Allowances– Travel Allowances– Registration Fees paid on behalf of participants or trainees

Slide 101

FY 2013

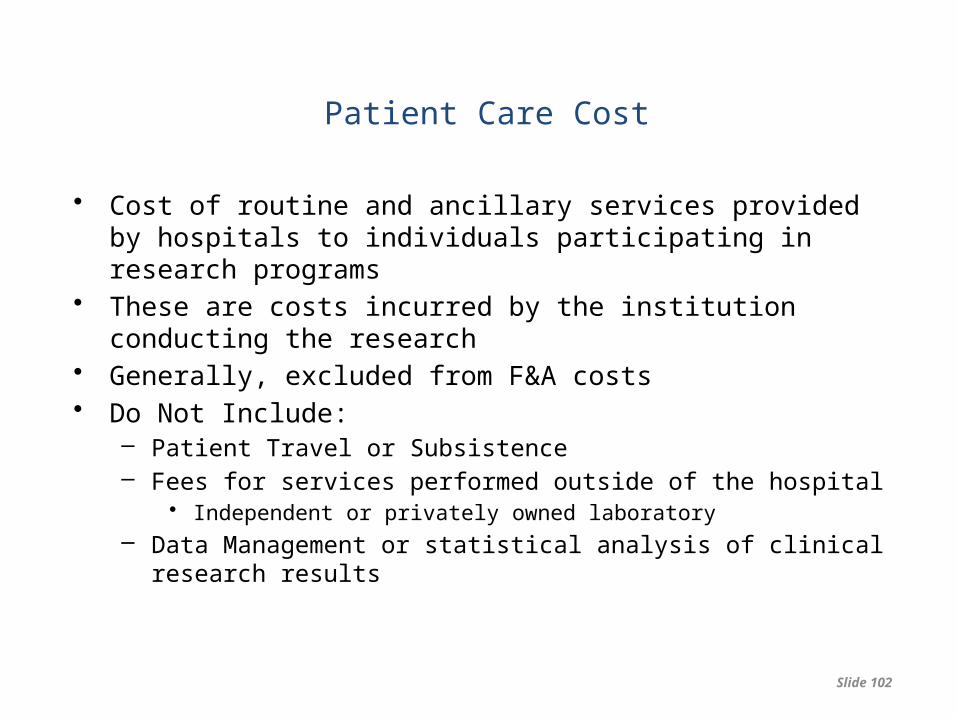

Patient Care Cost

• Cost of routine and ancillary services provided by hospitals to individuals participating in research programs

• These are costs incurred by the institution conducting the research

• Generally, excluded from F&A costs• Do Not Include:

– Patient Travel or Subsistence– Fees for services performed outside of the hospital

• Independent or privately owned laboratory– Data Management or statistical analysis of clinical research results

Slide 102

FY 2013

Publication Cost

• Costs of documenting, preparing, publishing, disseminating and sharing research findings and supporting material

• Page charges for scientific journals or publications

• Publication or sharing of research results supported by the project

Slide 103

FY 2013

• Non-supply costs

• Animal care/per diems (check current rates)

• Subject costs (payment, meals, parking)

• Vendor services

• Shared Facilities and Service Centers fees

• Service Contracts on equipment related to project

• Caution: No indirect/unallowable items• Caution: Each sponsor may categorize ODC’s differently. Read

the Program Announcement for what is allowed and how to reflect it on the budget

Other Direct Costs (ODC)

Slide 104

FY 2013

Now that we’ve reviewed the direct costing basics, let’s review special budget

considerations…

FY 2013

Special Budget Considerations: Cost Share

• Cost sharing is the portion of project or program cost not borne by the sponsor.

• Cost sharing occurs when either a sponsor requires or the University commits funds beyond those awarded by the sponsoring agency to support a particular grant or contract.

• Cost sharing is a legally binding commit made during proposal submission. If project is awarded, the cost sharing commitment must be fulfilled

• It can be borne by Duke or a third party contributor

106

FY 2013 Slide 107

Special Budget Considerations: Cost Share

• Types:– Mandatory– Voluntary

• Only charges that would be allowable as direct costs to the recipient grant are allowable as cost sharing.

• Duke discourages participation in cost share unless it is specifically required by the sponsor

• Must be incurred during the award period• Cannot be committed as cost sharing on any other project or

program

Refer to ORA/ ORS for guidance on cost share.

GAP 200.140 Cost Sharing On Sponsored Projects

FY 2013

Common Examples of Cost Sharing• Salaries

– Effort with no salary– Salary over the NIH Salary cap

• Equipment purchases where Duke is providing full or partial funding for equipment required for a specific project

• Reduced F&A rate from negotiated Duke rate (example: 28% for clinical trials)

108 Slide 108

FY 2013

Special Budget Considerations: Salary Cap

• Salary cap is a limitation imposed by a sponsor on the amount of salary that can be directly charged to a sponsored project.

– National Institutes of Health (NIH) is one of several agencies within DHHS that imposes a salary cap on all positions

– The cap is based only on institutional base salary– The current rate is $179,700 for a 12-month appointment. The rate is

adjusted to $134,775 for a 9-month appointment.• Salary above cap must be cost-shared

– DHHS Salary Cap Worksheet: https://finance.duke.edu/research/forms-resources/forms/index.php#NIH

The rules on salaries and wages can vary, depending on the sponsor.

109 Slide 109

FY 2013

Salary Cost Sharing Formulas

1. Determining Salary Cost Share:a. Actual Salary x Percentage of Committed Effort = Actual Salary

Committedb. Allowable Salary Request x Percentage of Committed Effort =

Allowable Requested Salaryc. Actual Salary Committed - Allowable Requested Salary = Cost

Shared Salary

Slide 110

FY 2013

Special Budget Considerations: NSF 2-Month Restriction

• 2-month salary limit (known as “two-ninths rule”) from all National Science Foundation (NSF) funding sources combined

Ex.: $200,000 annual salary (9-month appt)

$200,000 ÷ 9 months = $22,222 per month

$22,222 x 2-month limit = $44,444 total salary allowed by NSF

The rules on salaries and wages can vary, depending on the sponsor.

NSF Grant Proposal Guide: http://www.nsf.gov/pubs/policydocs/pappguide/nsf11001/gpg_2.jsp#IIC2gia

111 Slide 111

FY 2013

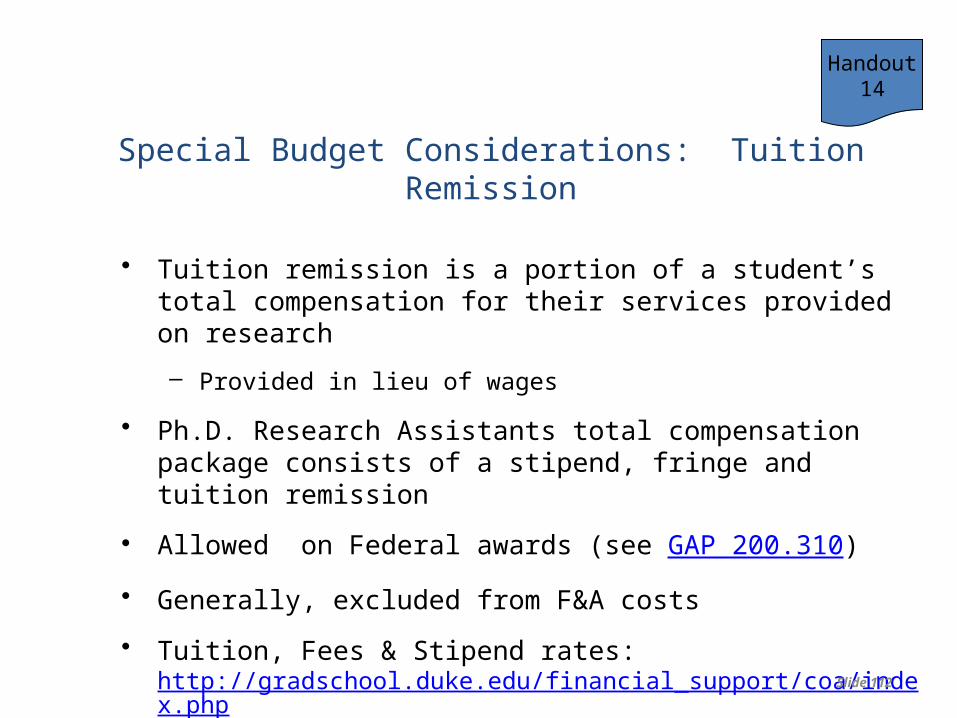

Special Budget Considerations: Tuition Remission

• Tuition remission is a portion of a student’s total compensation for their services provided on research

– Provided in lieu of wages

• Ph.D. Research Assistants total compensation package consists of a stipend, fringe and tuition remission

• Allowed on Federal awards (see GAP 200.310)

• Generally, excluded from F&A costs

• Tuition, Fees & Stipend rates: http://gradschool.duke.edu/financial_support/coa/index.php

Handout14

Slide 112

FY 2013

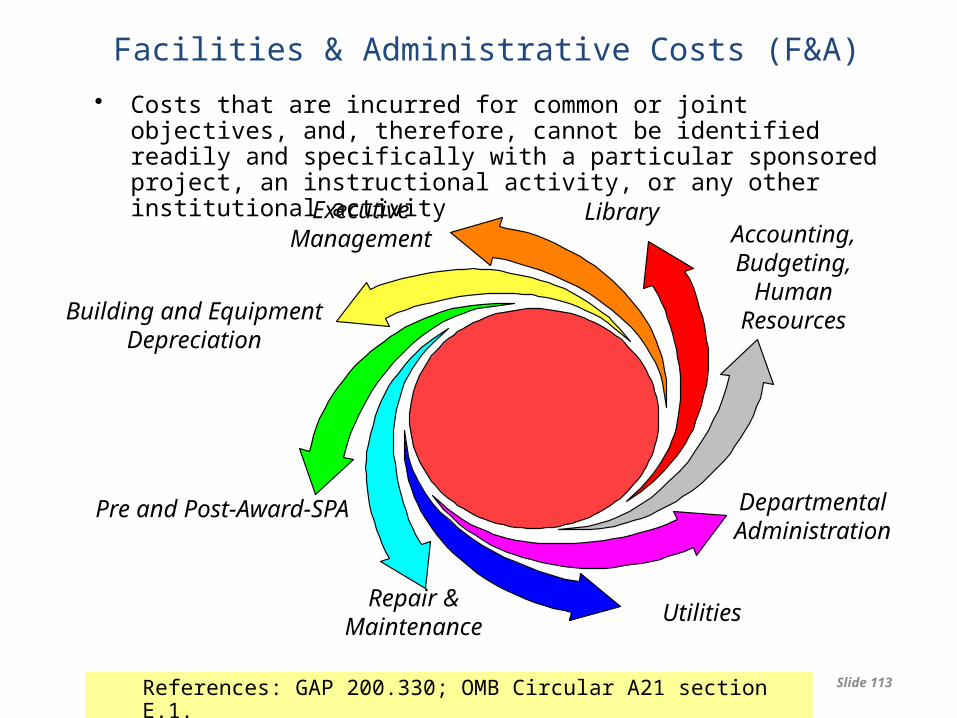

Utilities

Not directlyassignableto any one

activity

Building and Equipment Depreciation

Accounting, Budgeting,

Human Resources

Pre and Post-Award-SPA

ExecutiveManagement

Library

Departmental Administration

Repair & Maintenance

Facilities & Administrative Costs (F&A)

• Costs that are incurred for common or joint objectives, and, therefore, cannot be identified readily and specifically with a particular sponsored project, an instructional activity, or any other institutional activity

Slide 113References: GAP 200.330; OMB Circular A21 section E.1.

FY 2013

Direct Cost vs. F&AThis list is only a summary; a comprehensive list can be found at the Office of Management and

Budget Circular (OMB) A-21.

Direct (Allowable as Budgeted Items) F&A (Not Allowable as Direct Costs)

Salaries/Wages & Fringe Benefits:Faculty, other professionals, technicians, post doc associates, research associates, graduate and undergraduate students

Salaries/Wages & Fringe Benefits:Clerical and administrative assistants, fiscal manager, secretaries, and directors (special rules apply if allowable)

Materials and Supplies:Project related research and scientific supplies. Any equipment or software that does not qualify under the equipment definition

Office Supplies:Pens, pencils, paper, staples, transparencies, toner cartridges, diskettes, printer paper, word processing and spreadsheet programs

Equipment:Equipment used for scientific, technical, and research purposes that costs greater than $5,000 and has a useful life of at least one year

Equipment:General office equipment such as copiers, printers, office computers, and fax machines

Facilities:Project specific space rental for off-campus facilities from a third party. Use of specialized equipment for which there is a commonly applied charge

Facilities:Utilities, building use, grounds maintenance, renovations, and alterations of University property whether on- or off-campus

Travel:Transportation, lodging, subsistence, and related items incurred by employees who are in travel status on official business of the institution related to the project

Travel:Costs of entertainment, and any costs directly associated with such costs (such as tickets to shows or sports events, meals, lodging, rentals, transportation, and gratuities)

Slide 114

FY 2013

Direct or F&A?

DirectSterile tubes used in water collection samples to measure Ph levels in NC streams

Grant manager salary A book on drug interactionsand toxicity

Patient care expenses related to clinical trials

iPads for field research to monitor hibernation patterns in male grizzly bears in Montana.

F&A

Sample tubes are directly related to research.

Generally, library expenses Are part of the F&A base, and booksAre considered an F&A expense.

Likely that pt. care is a direct cost

For more information on direct and F&A Costs, consult OMB circular A-21, sections D and E

Generally, grant manager salaries are considered an F&Acost.

Field research is an unlikecircumstance and in this instance, an iPad may be a direct charge.

Computers are typically treated as general purpose, and should be recorded as F&A

Slide 115

FY 2013

Unallowable (Always) Allowable

Directly Charge to Project Include in F&A Calculation(Indirectly Charge to Project)

Alcoholic beverages Salary of PI Laboratory space

Fundraising Laboratory Technician Office administrative support

Alumni activities Research supplies Office supplies

Travel related to project Computers, telephones, postage

116

Direct vs. F&A vs. Unallowable

Take home message: Both direct and F&A costs must be allowable Slide 116

FY 2013

Consistently Allocating Costs

• Although costs may be charged as either direct costs or F&A costs, they must be treated consistently for all work of the organization under similar circumstances, regardless of the source of funding, so as to avoid duplicate charges

• How is “consistently treated” determined?– Has the institution specifically defined the accounting practice for assigning

this cost?– Has the institution spelled out criteria for deviations in this practice?– Is the institution applying the accounting practice each time the cost is

assigned?

Costs that are easily identified with the basics of day-to-day operations (telephone, postage, office space, clerical support) are generally not allowable as direct charges

Slide 117

FY 2013

Subrecipients and F&A

• Circular A-21 stipulates that the prime institution can collect F&A on the first $25,000 of a subcontract.

• Prime institution recovers F&A costs on the first $25,000 of each subcontract– There are exceptions to this requirement depending on sponsor or

program (example: USDA Cooperative agreements)– Prime institution incorporates the cost of the subcontract into the

proposal and recovers indirects only on the first $25,000 of each subcontract.

Slide 118

FY 2013

Guidance on Direct Charging Administrative and Clerical Costs

• Costs normally treated as F&A costs cannot be charged directly to a sponsored project unless the specific activities related to the project are clearly different in type or significantly different in scale from the Institutions norm. Costs normally charged as F&A costs may be charged directly when "unlike or unusual" circumstances exist.

Reference: GAP 200.360 Charging Clerical and/or Administrative Expenses to Federally Funded Projects

• Remember your basic costing guidelines – Items such as office supplies, postage, local telephone costs, and memberships shall normally be treated as F&A costs. (A-21: F.6.b)

• Review your budget during award set-up and complete a CAS form if necessary

Slide 119

FY 2013

Guidance on Direct Charging Administrative and Clerical Costs

• Administrative and clerical salaries should normally be treated as F&A costs per A-21. It may be appropriate to charge administrative and clerical salaries to a Federal award under the following circumstances:– A major project (as defined in OMB A-21 Exhibit C) or activity explicitly

budgeted for administrative or clerical services; and– Employees involved can be specifically identified with the project or activity;

and– Costs are incurred in unlike circumstances, i.e., the actual activities direct

charged are not the same as the actual activities normally included in the institution's F&A cost pool.

• Non-salary CAS expenses must be incurred in unlike circumstances.

Slide 120

FY 2013

Direct Cost Exceptions: Duke Policy

• A Direct Cost Exception form is required each time new or incremental funding is awarded, whether for an already existing WBSE or a new WBSE

• The University has adopted a policy that departments must be able to justify CAS-related expenses of at least $500 PER G/L GROUP/CATEGORY– This means that CAS charges totaling less than $500 per G/L group or

category in a budget period cannot be requested and cannot be charged. If costs less then $500 are posted to a WBSE those charges are required to be removed or written off

• The CAS/Rebudget form will be accessible via Duke@Work effective January 30, 2014

Handout 15

Slide 121

FY 2013

Direct Cost Exceptions: Pre-Award Guidance

What to do during proposal development:

• Discuss budget items with PI. If any appear to be CAS expenses:– Ensure requests meet CAS requirements for major project (salary only) and

unlike circumstances (non-salary)– Ensure the requested budget is ≥ $500– Alert PI that further justification may be required if project is awarded– Plan to submit CAS form at time of award

Slide 122

FY 2013

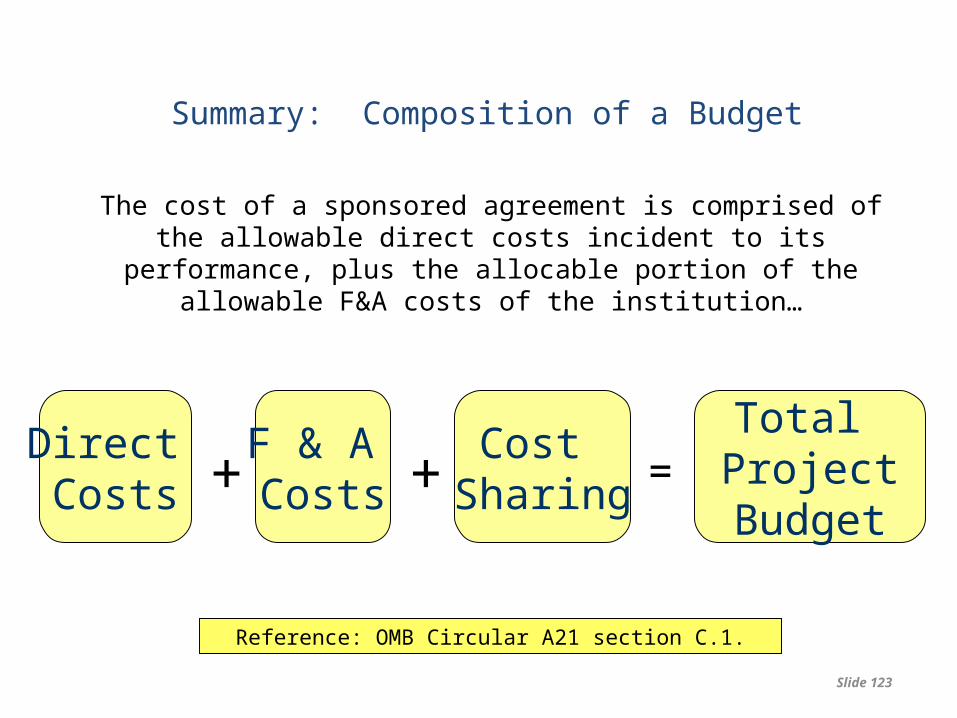

Summary: Composition of a Budget

The cost of a sponsored agreement is comprised of the allowable direct costs incident to its performance, plus the allocable portion of

the allowable F&A costs of the institution…

Reference: OMB Circular A21 section C.1.

Slide 123

Direct Costs

F & A Costs

Cost Sharing

Total ProjectBudget

++ =

FY 2013

Budget Review– Exercise

Handout 16 is a budget for a DHHS-sponsored project routed to a pre-award office for approval. There are numerous problems with this budget. Can you locate them? Work in pairs to see if you can identify the discrepancies.

Some items to remember…

• Cost Sharing

• Sponsor guidelines

• Appointment types

• Subrecipient F&ASlide 124

Handouts 16 & 17

FY 2013

Institutional Clearance

Slide 125

FY 2013

Proposal Review and Clearance

• After submitting a proposal via SPS, your pre-award office will review to ensure the submission conforms do sponsor and Duke guidelines

• Your next class will cover the internal review process in detail

Slide 126

FY 2013

Proposal Submission & Sponsor Review

Slide 127

FY 2013

Submission Guidelines

• After receiving approval by your pre-award office, your PI can submit the proposal to the sponsor

• Varies by sponsor and opportunity

• Generally, Federal sponsors require electronic submission via grants.gov, Fastlane, or other electronic system

• Paper submissions can be specific (postmark or receipt, express or regular mail, etc.)

• READ GUIDELINES CAREFULLY!!!!

Slide 128Slide 128

FY 2013

Grants.duke

SPS

Electronic Submissions

Slide 129Slide 129

FY 2013

Proposal Review Process

Most sponsors:• Check to ensure proposals meet the requirements outlined in

the Funding Opportunity Announcement (FOA) and are compliant with formatting rules.

• Assign proposals to a review group.

• Communicate with PIs about score/ranking (funding indicators), and feedback.

130

Handout18

Slide 130

FY 2013

Proposal Review Process

Site Visits:• Generally associated with large or complex projects• Agencies may schedule one or more site visits to review

resources and expertise before award is granted• Find out if the site visit includes a review of Duke’s financial

policies and procedures

• Get the appropriate Duke offices [Office of Research Administration (ORA)/Office of Research Support (ORS)/Office of Sponsored Programs (OSP)] involved

131 Slide 131

FY 2013

Award Negotiations & Acceptance

Slide 132

FY 2013

Pre-Award Costs: NIH Guidance• A grantee may, at its own risk and without NIH prior approval, incur obligations and

expenditures to cover costs up to 90 days before the beginning date of the initial budget period of a new or competing continuation award if such costs:

– Are necessary to conduct the project, and– Would be allowable under the grant, if awarded, without NIH prior approval

• If specific expenditures would otherwise require prior approval, the grantee must obtain NIH approval before incurring the cost. NIH prior approval is required for any costs to be incurred more than 90 days before the beginning date of the initial budget period of a new or competing continuation award.

• Grantees may incur pre-award costs before the beginning date of a non-competing continuation award without regard to the time parameters stated above.

• The incurrence of pre-award costs in anticipation of a competing or non-competing award imposes no obligation on NIH either to make the award or to increase the amount of the approved budget if an award is made for less than the amount anticipated and is inadequate to cover the pre-award costs incurred.

• NIH expects the grantee to be fully aware that pre-award costs result in borrowing against future support and that such borrowing must not impair the grantee’s ability to accomplish the project objectives in the approved time frame or in any way adversely affect the conduct of the project.

You will learn more about Pre-Award Costs in your next class. Slide 133

FY 2013

Pre-Award Costs: NSF Guidance

• Grantees may incur allowable pre-award costs within the 90 day period immediately preceding the effective date of the grant providing:

– The approval of the pre-award spending is made and documented in accordance with the grantee’s procedures; and

– The advanced funding is necessary for the effective and economical conduct of the project

• Pre-award expenditures are made at the grantee's risk. Grantee authority to approve pre-award costs does not impose an obligation on NSF: (1) in the absence of appropriations; (2) if an award is not subsequently made; or (3) if an award is made for a lesser amount than the grantee anticipated.

• Requests for pre-award costs for periods exceeding 90 calendar days must be submitted electronically via use of the Notification and Request module in FastLane. Pre-award expenditures prior to funding of an increment within a continuing grant are not subject to this limitation or approval requirement, but are subject to paragraph above.

If your project has a different federal sponsor, consult the FDP matrix or other sponsor guidelines to determine of pre-award spending is allowable

You will learn more about Pre-Award Costs in your next class. Slide 134

FY 2013

Pre-Award Costs: Duke Process

1. Principal Investigator determines that pre-award spending is necessary for the conduct of the research

2. Principal Investigator in conjunction with the Grant Manager completes the WBSE Request Form (SOM/SON) (Campus) and submits to the appropriate Pre-award Office.

– SOM/SON: Utilize the administrative action request form on the ORA website to submit the WBSE request

3. The Pre-award Office reviews the form to determine:– If sponsor approval is required – If request is consistent with sponsor guidelines– Request default Cost Center as back-up

4. Department is notified of approval5. Approved form is forwarded to OSP to set up the WBSE

You will learn more about Pre-Award Costs in your next class. Slide 135

FY 2013

Pre-award CostsSubrecipients

• Subagreements under parent code within Duke or subrecipients should not be given approval for Pre-Award costs.

– In most cases, the Pre-award Offices will not issue subcontract agreements without having the Prime Award in hand

136 You will learn more about Pre-Award Costs in your next class.

Slide 136

FY 2013

Review: Learning Objectives

• Upon completion of this class participants will be able to:– Understand and apply basic Federal regulations towards charging costs to

Federal awards– Able to understand basic compliance rules of allowability, allocability,

consistency, and reasonableness– Ability to distinguish and apply charges based on allowable and unallowable

costs– Ability to distinguish differences between direct charges and F&A costs – Understand basic concept of charging Administrative and Clerical costs to

Federal awards– Locate and have a basic understanding of guidance cited in funding

announcements– Identify and advise the PI of administrative requirements and proposal

elements related to proposal preparation

Slide 137

FY 2013

Review: Learning Objectives

– Ability to understand and apply basic knowledge of who funds sponsored research and the basic funding mechanisms used by sponsors

– Ability to understand and apply guidance on funding opportunity announcements from different sponsors

– Awareness of various search engines and resources at Duke in order to find funding opportunities for PIs

– Ability to understand the basic concepts and terminology related to proposal development

– Understand and be able to advise PIs of required proposal elements (Biosketch, Other Support, Facilities & Resources) for proposal preparation

– Understand how to include collaborations and subcontractors in proposal budgets and submissions

– Ability to advise the PI of submission requirement (paper vs. electronic)

Slide 138

FY 2013

Questions?

Slide 139Slide 139