Embed Size (px)

Citation preview

Y

Tcm

Ja

b

a

ARRA

KBPSOM

1

e(cbWuaoothe

h1

ARTICLE IN PRESSG ModelMARE-553; No. of Pages 12

Management Accounting Research xxx (2015) xxx–xxx

Contents lists available at ScienceDirect

Management Accounting Research

journa l homepage: www.e lsev ier .com/ locate /mar

he impact of participation in strategic planning on managers’reation of budgetary slack: The mediating role of autonomousotivation and affective organisational commitment

olien De Baerdemaeker a,∗, Werner Bruggeman a,b

Department of Accountancy, Corporate Finance, and Taxation, Ghent University, Sint-Pietersplein 7, 9000 Ghent, BelgiumVlerick Business School, Reep 1, 9000 Ghent, Belgium

r t i c l e i n f o

rticle history:eceived 6 August 2014eceived in revised form 22 May 2015ccepted 20 June 2015

eywords:udgetary slackarticipationtrategy

a b s t r a c t

This study investigates the impact of participative strategic planning on managers’ creation of budgetaryslack. Specifically, we draw on self-determination and organisational commitment theory to examinewhether and how the degree of managerial participation in strategic planning relates to the creation ofbudgetary slack. The hypotheses are empirically tested with survey data obtained from 247 managersin a cross-section of West-European organisations. The results from a structural equation model, withcontrols for budget participation and slack detection, suggest that increased participation in strategicplanning leads to lower budgetary slack creation through the suggested path of heightened affectiveorganisational commitment. In addition, the results indicate that budget participation decreases the

rganizational commitmentotivation

creation of budgetary slack through the mediating effect of autonomous budget motivation, suggestingthat both elements of the organisational planning process are related to the creation of budgetary slack.Our study contributes to the growing research exploring the interface between accounting and strategyby recognizing the importance of participative strategic planning for understanding managers’ creationof budgetary slack.

© 2015 Elsevier Ltd. All rights reserved.

. Introduction

Budgetary slack, defined as the deliberate incorporation ofxcess resources in the budget that make the budget easier to attainMerchant, 1985), is one of the most investigated budgeting out-omes. Not only does evidence indicate that there is considerableudgetary slack in organisations (e.g. Merchant, 1985; Schoute andiersma, 2007), it also remains one of the primary controversial,

nsolved issues in budgetary control. There is a considerable liter-ture that discusses possible antecedents of budgetary slack (for anverview, see Derfuss, 2012; Dunk and Nouri, 1998). The majorityf this prior literature investigated the effect of budget participa-ion (BP) on the creation of budgetary slack. These empirical studies,

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

owever, have resulted in contradictory findings. BP seems a nec-ssary but not sufficient explanation for budgetary slack creation,

∗ Corresponding author.E-mail address: [email protected] (J. De Baerdemaeker).

ttp://dx.doi.org/10.1016/j.mar.2015.06.002044-5005/© 2015 Elsevier Ltd. All rights reserved.

which establishes a need to identify and test the effect of additionalexplanatory variables (Webb, 2001).

This study focuses on managers’ participation in strategic plan-ning (PSP) as an additional explanation for the creation of budgetaryslack. The identification of PSP as a possible antecedent of bud-getary slack creation is based on the fact that the budget is anindistinguishable part of an organisation’s planning process (e.g.Covaleski et al., 2003; Hansen et al., 2003; Merchant and Van derStede, 2011). This planning process not only includes budgeting butalso strategic planning (e.g. Frezatti et al., 2011). Focus in extantresearch on a manager’s immediate budget setting and BP hasneglected the possible effect of strategic planning on budgetaryslack creation. This omission may be significant as it may, at leastpartially, explain the inconsistencies in the research findings con-cerning the effect of BP on managers’ budgetary slack creation. Thisresearch aims to extend prior research’s focus by studying the effectof strategic planning on budgetary slack creation, over and beyond

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

BP’s effect in order to capture the whole planning process and assuch further our understanding of the antecedents of budgetaryslack creation. In particular, as recent work on strategic manage-

ING ModelY

2 gemen

msso

bCmwdwhm

rbaoataeutBapb1aaoytsaoabtaMbttdhp

proyod

2

2

cvpd

One of the main reasons why managers create slack is to protectthemselves and the organisation’s core from uncertainty (Cyertand March, 1963). PSP can lower the uncertainty experienced (and,

1 We recognize that the creation of budgetary slack in itself is not undesirableper se (e.g. Davila and Wouters, 2005; Marginson and Ogden, 2005; Van der Stede,2000) and that it is only detrimental to the organisation to the extent that it resultsin the expropriation of resources (Church et al., 2012). Judging the (un) desirability

ARTICLEMARE-553; No. of Pages 12

J. De Baerdemaeker, W. Bruggeman / Mana

ent (e.g. Floyd and Wooldridge, 2000; Kaplan and Norton, 2001)uggests that strategy should be planned in a participative way, thistudy aims to clarify whether and how PSP relates to the creationf budgetary slack.

As understanding managerial behaviour requires insights fromoth psychology-based and economic-based theories, we followovaleski et al.’s (2003) suggestion and adopt a psychology-basedanagement accounting research approach. More specifically,e use insights from organisational commitment and self-

etermination theory (SDT) to broaden our understanding ofhether and how PSP relates to budgetary slack. To test our

ypotheses, we conducted a survey which was completed by 247anagers from a cross-section of West-European organisations.

The contribution of this paper to management accountingesearch is threefold. First, our study results contribute to theudgetary slack literature by demonstrating that PSP reduces themount of budgetary slack created through enhanced affectiverganisational commitment, after controlling for the effect of BPnd slack detection. As such, we deepen our understanding ofhe factors that drive budgetary slack. Second, we show that BPlso decreases the creation of budgetary slack through height-ned autonomous budget motivation. Taken together, in order tonderstand the creation of budgetary slack in a specific situa-ion, we should take into account both the level of BP and PSP.oth elements are part of an organisation’s planning process andre related to budgetary slack creation, albeit through a differentath. Third, our study extends the line of research on the interfaceetween accounting and strategy (Dent, 1990; Langfield-Smith,997) by focusing on the relationship between the level of PSPnd the creation of budgetary slack. Surprisingly, few managementccounting research has been published on PSP despite it beingf interest in the academic and professional literature in recentears (Kaplan and Norton, 2008; Wooldridge et al., 2008). In addi-ion to the contributions to management accounting research, thistudy also has the potential to inform the practice of managementccounting. In particular, our results demonstrate the importancef personal variables such as affective organisational commitmentnd autonomous motivation to understand managers’ budgetingehaviour. Indeed, it are not the formal management control sys-ems in itself but it are their effects on these personal variables thatre primordial to understand managers’ budgetary slack creation.oreover, our study gives practitioners an understanding of how

udgeting and strategy may interact. Specifically, we show thathe way managers are involved in the strategy process determinesheir budgetary slack creation. When trying to influence subor-inate managers’ budgeting behaviour, top management shouldence take a holistic approach and consider both elements of thelanning process.

The remainder of this study is organised as follows. Section 2rovides the theoretical background of the constructs used in ouresearch model and develops the hypotheses. Section 3 describesur research method, and Section 4 presents the results of the anal-sis of our survey data. In Section 5, we summarise the conclusionsf our research, discuss the limitations, and suggest some fruitfulirections for future research.

. Theoretical background and hypothesis development

.1. Managers’ creation of budgetary slack

The traditional concern is that managers have an incentive to

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

reate budgetary slack by withholding or misrepresenting their pri-ate information in an attempt to control for resources, to achieveersonal aspirations, or in order to maximise the expected rewardsependent upon budget attainment (Dunk, 1993; Nouri, 1994).

PRESSt Accounting Research xxx (2015) xxx–xxx

Consequently, a manager’s budget demand not necessarily reflectsreal organisational necessities (Hopwood, 1974).1

The majority of slack-related studies have focused on BP as themain explanation for the creation of budgetary slack (e.g. Merchant,1985; Nouri and Parker, 1996; Onsi, 1973). BP refers to “a processin which the subordinate is involved in, and has influence over, thedetermination of his budget” (Anthony and Govindarajan, 2007; p.380). There is, however, little consistent evidence on the effect ofBP on the creation of budgetary slack. While some studies reportthat the relationship is negative (Dunk, 1993; Merchant, 1985; Onsi,1973), others report a positive relationship (Lowe and Shaw, 1968;Lukka, 1988) or an insignificant one (Collins, 1978).

These mixed results have led to the use of other approaches suchas agency models (e.g. Young, 1985) and the use of contingency fac-tors to predict the creation of budgetary slack (for an overview, seeDerfuss, 2012; Dunk and Nouri, 1998). Although these approacheshave helped gain insight into the creation of budgetary slack, muchremains unexplained, establishing the need to identify and testthe effect of additional explanatory variables (Webb, 2001; Yuen,2004). Such an additional explanation suggested by prior bud-geting research is the organisation’s strategy (e.g. Merchant andManzoni, 1989; Van der Stede, 2000, 2001) as research increasinglyacknowledges both budgeting and strategy as parts of the organi-zational planning process (e.g. Cadez and Guilding, 2008; Frezattiet al., 2011). Whereas prior empirical studies incorporating strategyin budgetary slack research have focused on the effect of genericstrategies2 (Derfuss, 2012; Van der Stede, 2000, 2001), we focus onthe effect of PSP.

2.2. Participation in strategic planning and its relationship withbudgetary slack

Strategy, defined as ‘the determination of the basic long-termgoals and objectives of an enterprise, and the adoption of courses ofaction [. . .] necessary for carrying out these goals’ (Chandler, 1962;p. 13) was traditionally treated as a dichotomy: strategy planningwas the sole responsibility of top management and strategy imple-mentation the task of all other managerial levels (e.g. Ansoff, 1965;Anthony, 1965). This traditional division of work was challenged asenvironmental uncertainty increased in recent decades: we haveobserved a shift in focus in the strategic management literaturefrom top management to other managerial levels in the organisa-tion. We may even say that there is currently a widespread feelingthat top management is no longer in a position to make strate-gic decisions on its own. Recent work on strategic management(e.g. Floyd and Wooldridge, 2000; Kaplan and Norton, 2001, 2008)therefore suggests that in today’s business environment, strategyshould be planned in a participative way.

Although there is strong theoretical and empirical support for apositive relationship between PSP and organisational performance(Bourgeois and Brodwin, 1984; Wooldridge and Floyd, 1990), priorliterature is less clear on the potential impact of PSP on budgetaryslack. First, PSP can be argued to decrease budgetary slack creation.

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

of budgetary slack, however, goes beyond the scope of this paper.2 We use the phrase “generic strategies” to refer to Porter’s distinction between

three types of strategies: low cost, differentiation, and focus. In particular, “generic”reflects the choices companies make regarding both the type of competitive advan-tage (low cost or differentiation) and the scope (narrow or industry-wide focus).

ARTICLE IN PRESSG ModelYMARE-553; No. of Pages 12

J. De Baerdemaeker, W. Bruggeman / Management Accounting Research xxx (2015) xxx–xxx 3

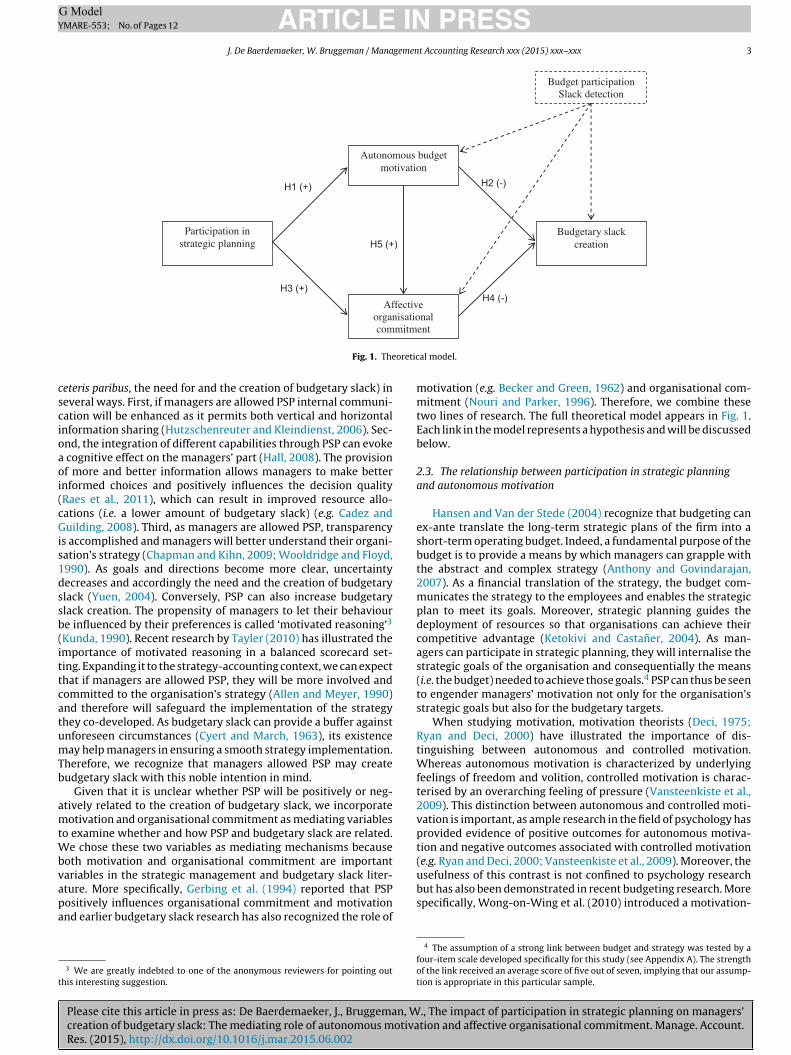

Participation in strategic planning

Autonomous budget motivation

Affective organisation al

mitm

Budgetary slackcreation

H1 (+)

H3 (+)

H2 (-)

H4 ( -)

H5 (+)

Budget participationSla ck dete ction

oretic

cscioaoi(cGis1dssb(ittcatumTb

amtWbvapa

t

usefulness of this contrast is not confined to psychology research

com

Fig. 1. The

eteris paribus, the need for and the creation of budgetary slack) ineveral ways. First, if managers are allowed PSP internal communi-ation will be enhanced as it permits both vertical and horizontalnformation sharing (Hutzschenreuter and Kleindienst, 2006). Sec-nd, the integration of different capabilities through PSP can evoke

cognitive effect on the managers’ part (Hall, 2008). The provisionf more and better information allows managers to make better

nformed choices and positively influences the decision qualityRaes et al., 2011), which can result in improved resource allo-ations (i.e. a lower amount of budgetary slack) (e.g. Cadez anduilding, 2008). Third, as managers are allowed PSP, transparency

s accomplished and managers will better understand their organi-ation’s strategy (Chapman and Kihn, 2009; Wooldridge and Floyd,990). As goals and directions become more clear, uncertaintyecreases and accordingly the need and the creation of budgetarylack (Yuen, 2004). Conversely, PSP can also increase budgetarylack creation. The propensity of managers to let their behavioure influenced by their preferences is called ‘motivated reasoning’3

Kunda, 1990). Recent research by Tayler (2010) has illustrated themportance of motivated reasoning in a balanced scorecard set-ing. Expanding it to the strategy-accounting context, we can expecthat if managers are allowed PSP, they will be more involved andommitted to the organisation’s strategy (Allen and Meyer, 1990)nd therefore will safeguard the implementation of the strategyhey co-developed. As budgetary slack can provide a buffer againstnforeseen circumstances (Cyert and March, 1963), its existenceay help managers in ensuring a smooth strategy implementation.

herefore, we recognize that managers allowed PSP may createudgetary slack with this noble intention in mind.

Given that it is unclear whether PSP will be positively or neg-tively related to the creation of budgetary slack, we incorporateotivation and organisational commitment as mediating variables

o examine whether and how PSP and budgetary slack are related.e chose these two variables as mediating mechanisms because

oth motivation and organisational commitment are importantariables in the strategic management and budgetary slack liter-

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

ture. More specifically, Gerbing et al. (1994) reported that PSPositively influences organisational commitment and motivationnd earlier budgetary slack research has also recognized the role of

3 We are greatly indebted to one of the anonymous reviewers for pointing outhis interesting suggestion.

ent

al model.

motivation (e.g. Becker and Green, 1962) and organisational com-mitment (Nouri and Parker, 1996). Therefore, we combine thesetwo lines of research. The full theoretical model appears in Fig. 1.Each link in the model represents a hypothesis and will be discussedbelow.

2.3. The relationship between participation in strategic planningand autonomous motivation

Hansen and Van der Stede (2004) recognize that budgeting canex-ante translate the long-term strategic plans of the firm into ashort-term operating budget. Indeed, a fundamental purpose of thebudget is to provide a means by which managers can grapple withthe abstract and complex strategy (Anthony and Govindarajan,2007). As a financial translation of the strategy, the budget com-municates the strategy to the employees and enables the strategicplan to meet its goals. Moreover, strategic planning guides thedeployment of resources so that organisations can achieve theircompetitive advantage (Ketokivi and Castaner, 2004). As man-agers can participate in strategic planning, they will internalise thestrategic goals of the organisation and consequentially the means(i.e. the budget) needed to achieve those goals.4 PSP can thus be seento engender managers’ motivation not only for the organisation’sstrategic goals but also for the budgetary targets.

When studying motivation, motivation theorists (Deci, 1975;Ryan and Deci, 2000) have illustrated the importance of dis-tinguishing between autonomous and controlled motivation.Whereas autonomous motivation is characterized by underlyingfeelings of freedom and volition, controlled motivation is charac-terised by an overarching feeling of pressure (Vansteenkiste et al.,2009). This distinction between autonomous and controlled moti-vation is important, as ample research in the field of psychology hasprovided evidence of positive outcomes for autonomous motiva-tion and negative outcomes associated with controlled motivation(e.g. Ryan and Deci, 2000; Vansteenkiste et al., 2009). Moreover, the

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

but has also been demonstrated in recent budgeting research. Morespecifically, Wong-on-Wing et al. (2010) introduced a motivation-

4 The assumption of a strong link between budget and strategy was tested by afour-item scale developed specifically for this study (see Appendix A). The strengthof the link received an average score of five out of seven, implying that our assump-tion is appropriate in this particular sample.

ING ModelY

4 gemen

be

febanfitpsspsr(ett2aLhfPbmeentbmmf

Hm

2b

lbpwp(gMiaiia2pgtg

Hb

ARTICLEMARE-553; No. of Pages 12

J. De Baerdemaeker, W. Bruggeman / Mana

ased model of participative budgeting to explain the mixedvidence concerning the relationship between BP and performance.

Within SDT, it is maintained that autonomous motivation can beostered through a need-supportive environment (Vansteenkistet al., 2010). A need-supportive environment sustains the threeasic psychological needs innate to all humans: the need forutonomy, the need for competence, and the need for related-ess. The need for autonomy refers to feeling strong-willed and

ully endorsing one’s actions. People want to experience choicen their behaviour (Vansteenkiste et al., 2010) and be the initia-ors of their own actions (Deci, 1975). As a specific instance ofarticipative decision-making, PSP can provide managers with aense of willpower and choice (Deci et al., 1989) and therebyatisfy their need for autonomy. The second basic need, com-etence, concerns feeling effective in one’s interactions with theocial and physical environment (Deci, 1975). People have a natu-al tendency to explore, manipulate, and master their environmentVansteenkiste et al., 2010). Therefore, they feel competent if theyxperience opportunities to exercise and express their capaci-ies (Deci and Ryan, 2004). PSP can give managers the feelinghat they are better able to control their environment (Chenhall,003; Hutzschenreuter and Kleindienst, 2006), their work (Shieldsnd Shields, 1998), and the decision-making process (Locke andatham, 1990). Being invited to participate in strategic planningence signals trust in the manager’s competence. Lastly, the need

or relatedness denotes caring for and feeling cared for by others.eople search for close relationships and want to feel as though theyelong to a social group (Baumeister and Leary, 1995). Allowinganagers PSP increases the level of consensus among managers,

nhances internal communication, and creates a climate of sharedffort (Papadakis et al., 1998), which all satisfy the need for related-ess. Based upon these findings, we expect that the satisfaction ofhe three basic needs through PSP will encourage internalisation ofoth the organisational goals and the resources needed to imple-ent those goals, such that the manager experiences autonomousotivation to achieve the budgetary targets. Hypothesis H1 tests

or this positive relationship:

1. Higher levels of PSP increase managers’ autonomous budgetotivation.

.4. The relationship between autonomous motivation andudgetary slack

Managers can engage in similar behaviours for different under-ying reasons (Grant et al., 2011). They may constrain theirudgetary slack creation because of social pressure, accountabilityressure, or pressure to reveal private information they otherwiseould not (Covaleski et al., 2003). However, individuals who feel

ressured fail to maintain their effort and performance over timeGrant, 2008). Conversely, autonomous motivation predicts greateroal-directed effort and goal attainment (Sheldon and Elliot, 1998).anagers having autonomous budget motivation understand the

mportance of budget attainment which is central to their decisionsbout how best to meet these budgetary targets. Prior research hasllustrated autonomous motivation’s strong relationship with pos-tive work outcomes, such as performance, creativity, persistence,nd initiative (e.g. Ryan and Deci, 2000; Wong-On-Wing et al.,010). This implies that autonomously motivated managers willut more effort in looking for creative solutions to attain the bud-etary targets “as they are” and will be less inclined to make theargets easier to attain (i.e. they will be less inclined to create bud-

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

etary slack). Therefore, we formulate the following hypothesis:

2. Higher levels of autonomous budget motivation decreaseudgetary slack creation.

PRESSt Accounting Research xxx (2015) xxx–xxx

2.5. The relationship between participation in strategic planningand affective organisational commitment

PSP spurs not only motivation but also affective commitment tothe organisation (Freeman, 1989; Shields and Shields, 1998). Affec-tive organisational commitment refers to employees’ emotionalattachment to the organisation and is characterised by (1) a strongbelief in and acceptance of the organisational goals and values and(2) a willingness to exert substantial effort on the organisation’sbehalf (e.g. Mowday et al., 1979).

Employees develop a deep sense of affective organisationalcommitment if they are in a business environment that providesthem chances to participate in decision-making (Searfoss andMonczka, 1973). PSP, as a specific form of participative decision-making, is positively related to the satisfaction of the manager’sneed for autonomy and competence and satisfaction of those needsis identified as an antecedent of affective organisational com-mitment (e.g. Greguras and Dieffendorff, 2009). Applying thesenotions to a strategic management context, ample research illus-trates that PSP leads to greater acceptance of organisational goalsand hence fosters affective organisational commitment (e.g. Kimand Mauborgne, 1998; Korsgaard et al., 1995). Indeed, PSP enhancesaffective organisational commitment as it provides managers anopportunity to make organisational decisions and commits them tothese decisions (Mathieu and Zajac, 1990). The following hypothe-sis tests for this positive relationship:

H3. Higher levels of PSP increase managers’ affective organisa-tional commitment.

2.6. The relationship between affective organisationalcommitment and budgetary slack

The possibility of creating budgetary slack can instil a conflictof interest, as slack creation may be beneficial for the manager butmay run against the interests of the organisation as a whole (Kramerand Hartmann, 2011). Managers with strong affective commitmentwill act in the interests of the organisation just as they would intheir own because they have come to perceive the interests as iden-tical (Kim and Mauborgne, 1998). These managers align with theorganisational goals and feel positive about them. Conversely, man-agers with low organisational commitment are primarily driven bysatisfying their individual goals and ambitions.

Nouri (1994) and Nouri and Parker (1996) found that man-agers’ level of affective organisational commitment influences theirattempt to create budgetary slack. Strongly affectively committedmanagers understand the potential dysfunctional effects of bud-getary slack for their organisation and will be inclined to act inthe general interest of the organisation. Therefore, the amount ofbudget slack they create will be low. Conversely, managers witha low level of affective organisational commitment may exhibit ahigh degree of budgetary slack creation because as rational eco-nomic individuals, this is often in their best interest (Lowe andShaw, 1968). Hypothesis 4 tests for this negative relationship:

H4. Higher levels of affective organisational commitmentdecrease budgetary slack creation.

2.7. The relationship between autonomous motivation andaffective organisational commitment

Motivation is one of the bases through which commitmentdevelops. Researchers have argued that autonomous motivation

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

and affective organisational commitment should be related to eachother (e.g. Gagné et al., 2008). More specifically, Bono and Judge(2003) demonstrated a positive relationship between autonomousreasons for pursuing work goals and affective organisational com-

IN PRESSG ModelY

gement Accounting Research xxx (2015) xxx–xxx 5

mgrtiaiiIogftm3Gtmcabai

Hm

3

3

owtrgmsafip

WbcJajwnwntrab2

w

(u

p

Table 1Respondents by tenure, age, gender, education, role, and company size.

Characteristics of sample n Mean %

Panel A: respondent profileTenureYears in organisation 244 13.10Years in current function 247 6.17Age 245 46.92

GenderMale 214 87Female 31 13

EducationSecondary education or less 15 6Bachelor 65 26Master 156 63PhD 11 5

RoleFinance 16 6General management 50 20Manufacturing 37 14Marketing 26 11R&D 26 11Sales 49 20Supply chain 41 17Other 2 1

Panel B: company profileNumber of employees0–250 72 30251–500 38 15501–1000 22 91001–5000 34 14

ARTICLEMARE-553; No. of Pages 12

J. De Baerdemaeker, W. Bruggeman / Mana

itment. They asked respondents to identify important job-relatedoals, such as budget attainment, and found that autonomouseasons for pursuing those goals were positively related to affec-ive organisational commitment. While Bono and Judge (2003)mplicitly considered budget attainment as one possible work goalmongst others, we specifically tap into this issue and expand thedea that managers’ motivation for budget attainment may havemplications for their overall organisational affective commitment.ndeed, in his hierarchical motivation model Vallerand (1997) rec-gnizes that motivation exists at three levels of generality: thelobal, contextual, and situational levels. One of the motivationaleatures concerns the bottom-up influence of situational on con-extual motivation. Applying this to our setting, we know that all

anagers in our sample have budget responsibility5 (see Section.1 for more detailed information about our sampling approach).iven the importance of budget attainment within their work set-

ing, we believe that managers experiencing autonomous budgetotivation are more likely to experience affective organisational

ommitment. In other words, stretching Vallerand’s (1997) hier-rchical model, we believe that managers’ situational autonomousudget motivation will relate to them feeling affectively committedt the contextual level of the organisation. This positive expectations tested through the following hypothesis:

5. Higher levels of autonomous budget motivation increaseanagers’ affective organisational commitment.

. Research method

.1. Data collection

To test our hypotheses, we conducted a survey study to increaseur study’s comparability with previous research and because weanted to study managerial behaviour in a real-life business con-

ext. The target population of this research is managers with budgetesponsibilities, a key condition for examining the creation of bud-etary slack (e.g. Merchant, 1985; Onsi, 1973). Typically, generalanagers have these responsibilities, as do marketing, sales, R&D,

upply chain and production managers.6 Moreover, these managersre uniquely positioned to evaluate the value of information to therm and should therefore occupy a central position in the strategiclanning process (Floyd and Wooldridge, 1992).

For the random sample, we obtained contact information from aest-European commercial mailing list provider whose total num-

er of e-mail addresses approximates 300,000.7 Given the aboveriteria of function, 2,301 invitations were mailed to managers inanuary 2013, of which 256 failed to reach the respondent due ton invalid e-mail address, the respondent left the firm for anotherob, or had retired. To increase the response rate, each participant

as promised confidentiality and a follow-up was administered toon-respondents two weeks after the initial mail-out. Respondentsere provided both material (i.e. a chance to win a gastronomic din-

er for two) and non-material compensation (i.e. feedback abouthe study) (Moore and Tarnai, 2002). Of the 2,045 invitations thateached the respondents, 249 responses were returned, yielding

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

response rate of 12.18%. This response rate is in line with otherehavioural management accounting research (e.g. Chenhall et al.,011; Moores and Yuen, 2001). We compared the demographics

5 In particular, 65% of the managers reported having full P&L responsibility,hereas the other 35% had either expense or revenue responsibility.6 Our sample also comprises 6% finance managers. We did an additional analysis

results not reported here) without these managers and our inferences remainednchanged.7 Although not all managers were represented in this commercial mailing list, it

rovided the advantage of targeting the right people to complete our survey.

5001–10,000 19 810,001+ 58 24

and mean responses on all constructs of early (i.e. the respondentswho answered after the initial mail-out) and late (i.e. the respon-dents who answered after the reminder) respondents. The �2 andtwo-sample t-tests revealed no systematic differences (p > 0.05).Therefore, non-response bias is unlikely to affect the results.

As all data are self-reported, common method bias (CMB)may influence the observed correlations between the constructs(Podsakoff et al., 2003). A priori, we attempted to reduce the poten-tial effects of CMB by safeguarding the respondents’ anonymityand by assuring them that there were no right or wrong answers.A posteriori, we conducted Harman’s one-factor test on the fourconceptually crucial variables in our theoretical model (i.e. PSP,autonomous motivation, affective organisational commitment, andbudgetary slack). A four-factor solution rather than a single fac-tor occurred, and the first factor explained only 19% of the totalvariance. These results indicate that CMB is unlikely to contami-nate the research results (Podsakoff et al., 2003). Second, followingthe recommendations of Widaman (1985), we included a com-mon method factor in the structural equation model. While themethod factor did slightly improve the model fit (CMINDF = 2.57and NNFI = 0.93), it was not significant. Given the small magnitudeand insignificance of the common method factor, we contend thatCMB is unlikely to be a serious concern for this study, implying thatother factors account for the observed variance. Moreover, poten-tial response bias was investigated by manually going througheach individual filled-in questionnaire and by inspecting the vari-ance across all items. For two respondents, an answer pattern wasrecorded.8 Therefore, we decided to remove these respondents

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

from further analyses, yielding 247 usable responses. The charac-teristics of the final sample are displayed in Table 1.

8 They chose the neutral option for almost every item.

ARTICLE IN PRESSG ModelYMARE-553; No. of Pages 12

6 J. De Baerdemaeker, W. Bruggeman / Management Accounting Research xxx (2015) xxx–xxx

Table 2Descriptive statistics, correlation matrix, and discriminant validity coefficients (n = 247) for participation in strategic planning, autonomous budget motivation, affectiveorganisational commitment, the creation of budgetary slack, and the control variables.

Variable Mean s.d. Min Max Cronbach (1) (2) (3) (4) (5) (6)PSP (1) 5.56 0.95 1.90 7 0.93 0.75AM (2) 5.38 0.99 1 7 0.85 0.23** 0.71AOC (3) 5.63 0.98 1 7 0.87 0.42** 0.25** 0.74SLACK (4) 3.06 1.11 1 6.33 0.70 −0.27** −0.32** −0.29** 0.66BP (5) 5.57 1.04 1 7 0.89 0.45** 0.18** 0.26** −0.26** 0.77DETECT (6) 5.32 1.11 1.67 7 0.81 0.28** 0.17** 0.28** −0.18** 0.24** 0.77

**, Correlation is significant at the 0.01 level (two-tailed test), respectively. Correlations between the different constructs are below the diagonal. The square root of the AVEvP ctive

p

3

stvvttraoNiAatt

3

rSti2cttcpn(iarpetvft

h

fmmaf

alue for each of the constructs in along the diagonal (in bold).SP – participation in strategic planning; AM – autonomous motivation; AOC – affearticipation; and DETECT – slack detection.

.2. Variable measurement

For all variables in our study, the survey items were scored on aeven-point Likert-type scale ranging from one (strongly disagree)o seven (strongly agree) unless stated otherwise. We used pre-iously validated scales whenever possible to ascertain constructalidity. To check on the relevance of these measures, our ques-ionnaire was submitted to the scrutiny of six faculty colleagues,hree part-time MBA students, and 21 managers with budgetesponsibility9 for pre-testing. Final measures were then developednd refined. Furthermore, we conducted empirical tests (i.e. rangef responses, Cronbach’s alpha, and factor analyses) as suggested byunnally (1978) to further establish content and construct valid-

ty. An overview of the survey items is provided in Appendix A.ppendix B depicts the factor analyses used to construct the vari-bles in this study. Descriptive statistics of the constructs based onhe equally weighted average scores of multi-item variables andhe correlation matrix are presented in Table 2.

.2.1. Participation in strategic planning (PSP)Given the novelty of PSP in management accounting survey

esearch, we designed a new instrument specifically for this study.pecial attention has been paid to the conceptual specification ofhe construct. PSP, as a practice-informed construct, is given mean-ng by listing its theoretical properties found in practice (Bisbe et al.,007). The process of specifying this construct’s exact meaningonsists of a twofold approach. First, we elaborate on the defini-ion of ‘participation’ and ‘strategic planning’. Participation referso both the ‘involvement of employees in and their influence over’ertain organisational decisions (Anthony and Govindarajan, 2007;. 10, emphasis added). Strategic planning focuses on ‘the determi-ation of the basic long-term goals and objectives of an enterprise’Chandler, 1962; p. 13). Allowing managers PSP thus implies involv-ng them in and allowing them to influence the long-term goalsnd objectives of the organisation (Freeman, 1989). As such, weecognise both the quantity and quality aspect of managementarticipation in the strategy process, as recommended by Gerbingt al. (1994). Second, we engaged in a thorough examination ofhe strategic management literature and conducted in-depth inter-

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

iews with three senior managers and one middle manager10 toully grasp the process of strategic planning in both theory and prac-ice. Further support was provided for the validity of the theoretical

9 The target respondents for the pretest phase were excluded from the actualypothesis testing sample.10 Senior manager A (54 year, male) has been the CEO of a playing card companyor 18 years. Senior manager B (60 year, male) has been in his function of general

anager in a civic and social organisation for 15 years. Senior manager C (51 year,ale) is since five years responsible for the strategy process in the same organisation

s senior manager B. Middle manager D (51 year, female) works already 21 yearsor a telecommunication company and is since two years after sales manager.

organisational commitment; SLACK – the creation of budgetary slack; BP – budget

definition, as illustrated by the following quote given by one of theinterviewees:

‘Strategic planning is looking for an answer to the “what” question:what do we want to achieve? Strategy implementation, conversely,focuses on the “how” question: once we have decided what we wantto do, we need to decide upon how to achieve these goals.’

We used thematic analysis procedures to systematically iden-tify patterns that organise both the published and oral informationon the strategic planning process in a meaningful way. AppendixC provides a non-exhaustive overview of the analysed quotationsfrom published work. Different themes referring to different PSPproperties were developed and clustered into one code when thethemes had similar contents or were closely conceptually related(Boyatzis, 1998). The output of this procedure are two codes rep-resenting the building blocks of the strategic planning process,namely, the visioning process and the strategic positioning pro-cess, which is in line with research by Merchant and Van der Stede(2011). The visioning process entails answering abstract questions ofexistence. In particular, the interviewees mentioned such questionsas ‘What type of organisation are we?’, ‘What type of organisationdo we want to be?’; and ‘What type of business do we want to bein?’, reflecting Johnson and Scholes’ (1989) definition of corporatestrategy. The strategic positioning process refers to preparing anal-yses and making decisions about the strategic position of the firm,as reflected in Porter’s (1985, p.1) notion of competitive strategy:strategy is ‘the search for a favourable competitive position in anindustry’. Interviewees cited external and internal analyses, anddecisions about products, markets, product-market combinations,and the firm’s/business unit’s competitive advantage. To measureparticipation in the two sub strategy processes identified in theinterviews, we adapted the BP measure,11 which was developed byMilani (1975) and tested extensively in prior research (e.g. Chenhall,2003; Dunk, 1993; Leach-López et al., 2007). The item pool included12 items: six items measuring participation in the visioning processand six items measuring participation in the strategic positioningprocess (see Appendix A). More specifically, we asked respondentsto indicate their extent of involvement in and influence over (a)the determination of the basic long-term goals, objectives, andfuture opportunities of their organisational entity12 (i.e. the vision-ing process), and (b) the identification, preparation, and evaluation

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

of options (i.e. the strategic positioning process). Although the mea-surement properties of this 12-item PSP scale are good, scale itemstwo and eight could be viewed as rather communication by the

11 The original phrase referring to the budgeting process was replaced by ‘vision’or ‘long-term goals and objectives’ to refer to the visioning process and was replacedby ‘strategic position’ when measuring the amount of participation in the strategicpositioning process.

12 We used the phrase ‘organisational entity’ to refer to the specific unit the respon-dents is working in. For example, an organisational entity can be a business unit, adepartment.

ING ModelY

gemen

scaPani(etmia

3

wtto‘ita

3

dttA(oaoTarc

3

asaadMfdaCabda2‘

‘sr

s

4.1.1. Analysis of the measurement modelThe first step in the analysis was to develop a measurement

model. This model aims to specify the relationships between

15 We also controlled for perceived environmental uncertainty, organisationalstrategy, and some background variables (i.e. number of years working in the organi-

ARTICLEMARE-553; No. of Pages 12

J. De Baerdemaeker, W. Bruggeman / Mana

uperior instead of subordinate participation and thus we recal-ulated the measure without these items. The exploratory factornalysis reveals that the ten remaining questions used to measureSP load on one factor with an explained variance of 61%. The reli-bility of the 10-item construct is strong ( = 0.93). Since this is aew measure, we correlated it to an established measure of partic-

pation in strategic decision making (Floyd and Wooldridge, 1992)nine-item scale, 43% variance explained, = 0.83) and found, asxpected, a significant positive correlation (r = 0.40, p < 0.01). Ashe measurement properties of the specific measurement instru-

ent were better than those of the Floyd and Wooldridge (1992)nstrument, we decided to use the former as input for the statisticalnalyses.

.2.2. Autonomous budget motivation (AM)The adapted Motivation At Work Scale by Gagné et al. (2013)

as used to measure the manager’s autonomous budget motiva-ion. However, a change was made specifically for the purpose ofhis study. The original stem of the question reading ‘Why do your would you put effort into your current job?’ was changed to

Why do you or would you put effort into attaining your organ-sational entity’s budget?’ The exploratory factor analysis revealshat AM is uni-dimensional with an explained variance of 58% and

Cronbach’s alpha coefficient of 0.85.

.2.3. Affective organisational commitment (AOC)To assess AOC, the eight-item Affective Commitment Scale (ACS)

eveloped by Allen and Meyer (1990) was employed.13 This ques-ionnaire has been widely used in research and has been showno have acceptable levels of reliability and validity (Meyer andllen, 1991). Exploratory factor analysis reveals that two items

‘I would be very happy to spend the rest of my career with thisrganisation’14 and ‘I think that I could easily become as attached tonother organisation as I am to this one’) did not load significantlyn the factor and were dropped from the measurement model.he final exploratory analysis indicates that the six retained itemsre uni-dimensional and explain 60% of the variance. In the cur-ent study, the Cronbach’s alpha coefficient for the revised six-itemonstruct is 0.87.

.2.4. Budgetary slack (SLACK)In line with Dunk (1993), Van der Stede (2000), and Indjejikian

nd Matejka (2006), the definition of budgetary slack used in thistudy focuses on the ease with which budgetary targets can bechieved. Budgetary slack occurs when managers ‘negotiate highlychievable targets’ (Van der Stede, 2000; p. 609), i.e. targets that areeliberately lower than their best-guess forecast about the future.anagers can create budgetary slack by intentionally overstating

uture costs or understating future revenues (Merchant and Vaner Stede, 2011; Onsi, 1973). This lowers the budgetary targets setnd makes it easier for the manager to attain the required targets.onversely, a budget contains little slack if it requires consider-ble effort and a high degree of efficiency (Simons, 1987). To reflectudgetary slack creation, we used the measurement instrument

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

eveloped by Dunk (1993). Considerable evidence of the validitynd reliability of this scale has been compiled (e.g. Van der Stede,000). It is clear from the exploratory factor analysis that the item

budgets set for my organisational entity are safely attainable’ does

13 In some items, the original word ‘organisation’ was replaced by the wordorganisational entity’. Similar changes were made to the original commitment mea-urement scale by Aranya and Ferris (1984) and Wong-on-Wing et al. (2010), whoeplaced the word ‘organisation’ with ‘profession’ and ‘bank’, respectively.14 This item was also deleted in the study of Viator and Pasewark (2005) due toignificant cross-loadings.

PRESSt Accounting Research xxx (2015) xxx–xxx 7

not load adequately on the factor. Therefore, we deleted this itemfor further analyses. The remaining three items load on the samefactor, which explains 62% of the variance. The reliability of thethree-item construct is acceptable ( = 0.70). The construct is cor-related to two alternative measures for the creation of budgetaryslack (Van der Stede’s (2000) and Onsi’s (1973) measure, respec-tively) to ensure that the Dunk (1993) measure is working plausiblyin our sample. As expected, the results show positive and significantcorrelations (r = 0.79, p < 0.01 and r = 0.23, p < 0.01, respectively).Dunk’s (1993) measure is retained for further empirical analyses asit has better measurement properties than Van der Stede’s (2000)and Onsi’s (1973) measure in this specific sample.

3.2.5. Control variablesWe used two control variables in this study.15 First, we con-

trolled for BP. Although results are mixed, the large amount ofresearch on the relationship between BP and budgetary slack indi-cates the importance of controlling for it. BP was measured usingthe six-item measurement instrument developed by Milani (1975).Second, prior research revealed that a superior’s ability to detectslack (DETECT) is negatively related to a manager’s creation ofbudgetary slack (Merchant, 1985; Onsi, 1973), as ‘slack cannotbe created where it is easily detected’ (Merchant, 1985; p. 203).DETECT was measured by the three-item measure developed byOnsi (1973). The exploratory factor analyses reveal that BP andDETECT are uni-dimensional with explained variances of 65% and72%, respectively, and their Cronbach’s alphas are 0.89 and 0.81,respectively.

4. Research results and discussion

4.1. Statistical method

We used structural equation modelling (SEM) to examine therole of autonomous budget motivation and affective organisationalcommitment in the relationship between PSP and SLACK.16 Anadvantage of SEM is that it can simultaneously evaluate the pro-posed hypotheses and test the measurement reliability (Smith andLangfield-Smith, 2004). We conducted our analyses in LISREL 9.1according to the two-step approach recommended by Andersonand Gerbing (1988). This approach has been employed in a numberof recent accounting studies (e.g. Hartmann and Slapnicar, 2009;Wong-On-Wing et al., 2010). A structural equation model using themaximum likelihood (ML) method17 in which AM and AOC mediatethe relation between PSP and SLACK was estimated, controlling forthe effects of BP and DETECT on both the dependent and mediatingvariables.

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

sation/current function, age, and gender). As our analyses (results not reported here)indicated that none of these control variables were correlated with the dependentvariable, we decided to omit them from further analyses (Becker, 2005).

16 As we reviewed the tolerance and variance inflation factors for each construct,no evidence of multicollinearity was found. Furthermore, we plotted the residualsand performed White’s test, but no signs of heteroscedasticity were apparent.

17 In preliminary tests, we discovered that our data are not multivariate normallydistributed, as is the case with most data of perceptual nature (Hunton and Gibson,1999). We tested normality by investigating the skewness and kurtosis indexes asso-ciated with each of the survey items and conducted Shapiro–Wilk’s test. Althoughresults indicated that the measures were not normally distributed, we used themaximum likelihood (ML) method, as it performs well even under conditions ofnon-normality (Boomsma and Hoogland, 2001).

ARTICLE IN PRESSG ModelYMARE-553; No. of Pages 12

8 J. De Baerdemaeker, W. Bruggeman / Management Accounting Research xxx (2015) xxx–xxx

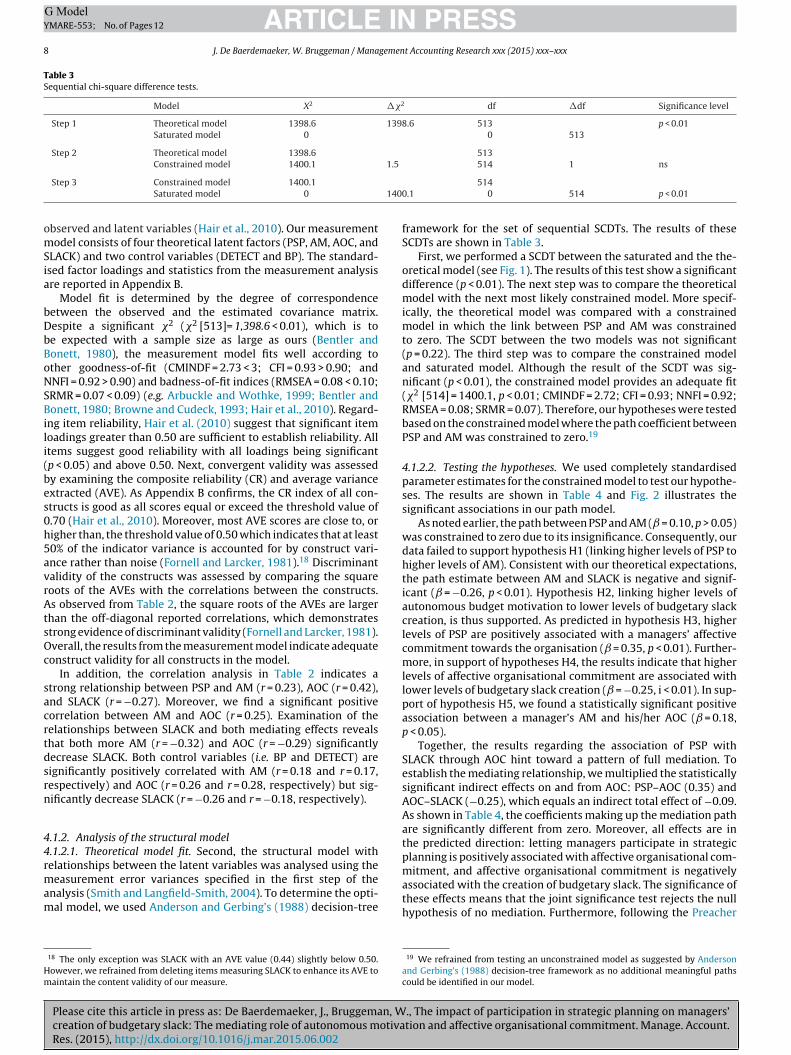

Table 3Sequential chi-square difference tests.

Model X2 ��2 df �df Significance level

Step 1 Theoretical model 1398.6 1398.6 513 p < 0.01Saturated model 0 0 513

Step 2 Theoretical model 1398.6 513Constrained model 1400.1 1.5 514 1 ns

140

omSia

bDbBoNSBili(bes0h5avrAtsOc

sacrtdsrn

44rmam

Hm

Step 3 Constrained model 1400.1

Saturated model 0

bserved and latent variables (Hair et al., 2010). Our measurementodel consists of four theoretical latent factors (PSP, AM, AOC, and

LACK) and two control variables (DETECT and BP). The standard-sed factor loadings and statistics from the measurement analysisre reported in Appendix B.

Model fit is determined by the degree of correspondenceetween the observed and the estimated covariance matrix.espite a significant �2 (�2 [513]= 1,398.6 < 0.01), which is toe expected with a sample size as large as ours (Bentler andonett, 1980), the measurement model fits well according tother goodness-of-fit (CMINDF = 2.73 < 3; CFI = 0.93 > 0.90; andNFI = 0.92 > 0.90) and badness-of-fit indices (RMSEA = 0.08 < 0.10;RMR = 0.07 < 0.09) (e.g. Arbuckle and Wothke, 1999; Bentler andonett, 1980; Browne and Cudeck, 1993; Hair et al., 2010). Regard-

ng item reliability, Hair et al. (2010) suggest that significant itemoadings greater than 0.50 are sufficient to establish reliability. Alltems suggest good reliability with all loadings being significantp < 0.05) and above 0.50. Next, convergent validity was assessedy examining the composite reliability (CR) and average variancextracted (AVE). As Appendix B confirms, the CR index of all con-tructs is good as all scores equal or exceed the threshold value of.70 (Hair et al., 2010). Moreover, most AVE scores are close to, origher than, the threshold value of 0.50 which indicates that at least0% of the indicator variance is accounted for by construct vari-nce rather than noise (Fornell and Larcker, 1981).18 Discriminantalidity of the constructs was assessed by comparing the squareoots of the AVEs with the correlations between the constructs.s observed from Table 2, the square roots of the AVEs are larger

han the off-diagonal reported correlations, which demonstratestrong evidence of discriminant validity (Fornell and Larcker, 1981).verall, the results from the measurement model indicate adequateonstruct validity for all constructs in the model.

In addition, the correlation analysis in Table 2 indicates atrong relationship between PSP and AM (r = 0.23), AOC (r = 0.42),nd SLACK (r = −0.27). Moreover, we find a significant positiveorrelation between AM and AOC (r = 0.25). Examination of theelationships between SLACK and both mediating effects revealshat both more AM (r = −0.32) and AOC (r = −0.29) significantlyecrease SLACK. Both control variables (i.e. BP and DETECT) areignificantly positively correlated with AM (r = 0.18 and r = 0.17,espectively) and AOC (r = 0.26 and r = 0.28, respectively) but sig-ificantly decrease SLACK (r = −0.26 and r = −0.18, respectively).

.1.2. Analysis of the structural model

.1.2.1. Theoretical model fit. Second, the structural model withelationships between the latent variables was analysed using the

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

easurement error variances specified in the first step of thenalysis (Smith and Langfield-Smith, 2004). To determine the opti-al model, we used Anderson and Gerbing’s (1988) decision-tree

18 The only exception was SLACK with an AVE value (0.44) slightly below 0.50.owever, we refrained from deleting items measuring SLACK to enhance its AVE toaintain the content validity of our measure.

5140.1 0 514 p < 0.01

framework for the set of sequential SCDTs. The results of theseSCDTs are shown in Table 3.

First, we performed a SCDT between the saturated and the the-oretical model (see Fig. 1). The results of this test show a significantdifference (p < 0.01). The next step was to compare the theoreticalmodel with the next most likely constrained model. More specif-ically, the theoretical model was compared with a constrainedmodel in which the link between PSP and AM was constrainedto zero. The SCDT between the two models was not significant(p = 0.22). The third step was to compare the constrained modeland saturated model. Although the result of the SCDT was sig-nificant (p < 0.01), the constrained model provides an adequate fit(�2 [514] = 1400.1, p < 0.01; CMINDF = 2.72; CFI = 0.93; NNFI = 0.92;RMSEA = 0.08; SRMR = 0.07). Therefore, our hypotheses were testedbased on the constrained model where the path coefficient betweenPSP and AM was constrained to zero.19

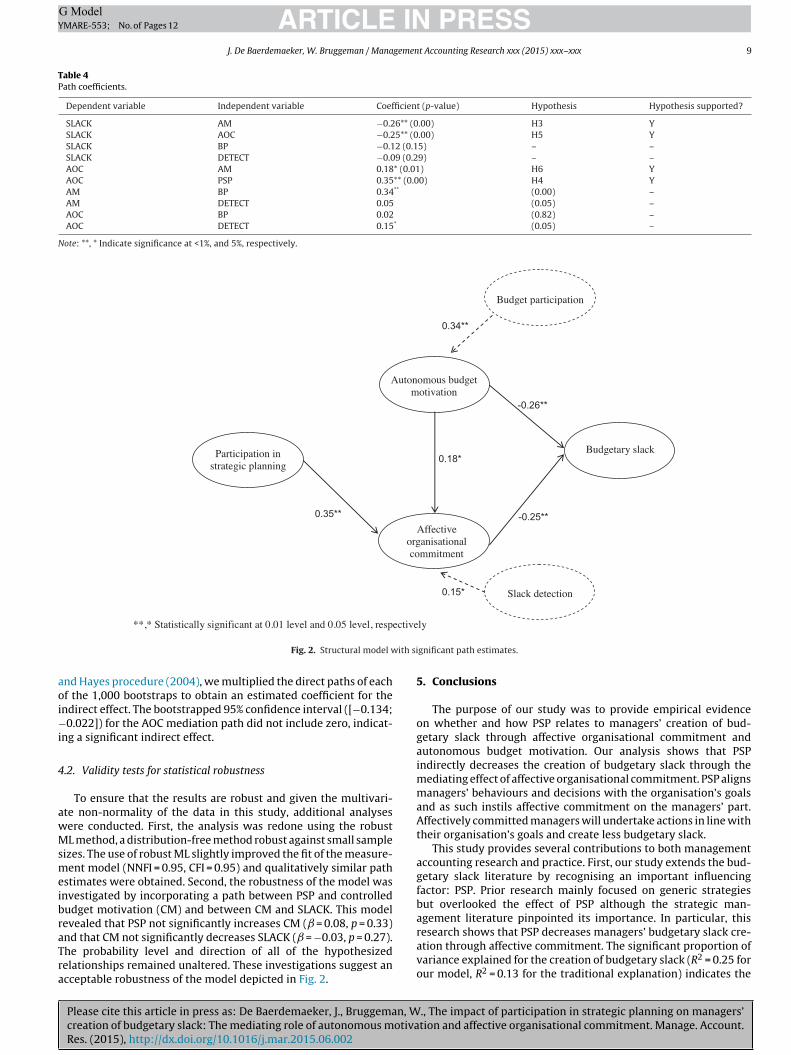

4.1.2.2. Testing the hypotheses. We used completely standardisedparameter estimates for the constrained model to test our hypothe-ses. The results are shown in Table 4 and Fig. 2 illustrates thesignificant associations in our path model.

As noted earlier, the path between PSP and AM ( = 0.10, p > 0.05)was constrained to zero due to its insignificance. Consequently, ourdata failed to support hypothesis H1 (linking higher levels of PSP tohigher levels of AM). Consistent with our theoretical expectations,the path estimate between AM and SLACK is negative and signif-icant ( = −0.26, p < 0.01). Hypothesis H2, linking higher levels ofautonomous budget motivation to lower levels of budgetary slackcreation, is thus supported. As predicted in hypothesis H3, higherlevels of PSP are positively associated with a managers’ affectivecommitment towards the organisation ( = 0.35, p < 0.01). Further-more, in support of hypotheses H4, the results indicate that higherlevels of affective organisational commitment are associated withlower levels of budgetary slack creation ( = −0.25, i < 0.01). In sup-port of hypothesis H5, we found a statistically significant positiveassociation between a manager’s AM and his/her AOC ( = 0.18,p < 0.05).

Together, the results regarding the association of PSP withSLACK through AOC hint toward a pattern of full mediation. Toestablish the mediating relationship, we multiplied the statisticallysignificant indirect effects on and from AOC: PSP–AOC (0.35) andAOC–SLACK (−0.25), which equals an indirect total effect of −0.09.As shown in Table 4, the coefficients making up the mediation pathare significantly different from zero. Moreover, all effects are inthe predicted direction: letting managers participate in strategicplanning is positively associated with affective organisational com-mitment, and affective organisational commitment is negatively

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

associated with the creation of budgetary slack. The significance ofthese effects means that the joint significance test rejects the nullhypothesis of no mediation. Furthermore, following the Preacher

19 We refrained from testing an unconstrained model as suggested by Andersonand Gerbing’s (1988) decision-tree framework as no additional meaningful pathscould be identified in our model.

ARTICLE IN PRESSG ModelYMARE-553; No. of Pages 12

J. De Baerdemaeker, W. Bruggeman / Management Accounting Research xxx (2015) xxx–xxx 9

Table 4Path coefficients.

Dependent variable Independent variable Coefficient (p-value) Hypothesis Hypothesis supported?

SLACK AM −0.26** (0.00) H3 YSLACK AOC −0.25** (0.00) H5 YSLACK BP −0.12 (0.15) – –SLACK DETECT −0.09 (0.29) – –AOC AM 0.18* (0.01) H6 YAOC PSP 0.35** (0.00) H4 YAM BP 0.34** (0.00) –AM DETECT 0.05 (0.05) –AOC BP 0.02 (0.82) –AOC DETECT 0.15* (0.05) –

Note: **, * Indicate significance at <1%, and 5%, respectively.

ective

Participation in strategic planning

Autonomous budget motivation

Affective organisation alcom mitment

Budgetary slack0.18*

0.35**

-0.26 **

Budget participation

0.34**

-0.25 **

Sla ck dete ction0.15*

ith si

aoi−i

4

awMsmeibraTra

**,* Statistic ally s ignificant at 0.01 level and 0.05 level, resp

Fig. 2. Structural model w

nd Hayes procedure (2004), we multiplied the direct paths of eachf the 1,000 bootstraps to obtain an estimated coefficient for the

ndirect effect. The bootstrapped 95% confidence interval ([−0.134;0.022]) for the AOC mediation path did not include zero, indicat-

ng a significant indirect effect.

.2. Validity tests for statistical robustness

To ensure that the results are robust and given the multivari-te non-normality of the data in this study, additional analysesere conducted. First, the analysis was redone using the robustL method, a distribution-free method robust against small sample

izes. The use of robust ML slightly improved the fit of the measure-ent model (NNFI = 0.95, CFI = 0.95) and qualitatively similar path

stimates were obtained. Second, the robustness of the model wasnvestigated by incorporating a path between PSP and controlledudget motivation (CM) and between CM and SLACK. This modelevealed that PSP not significantly increases CM ( = 0.08, p = 0.33)

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

nd that CM not significantly decreases SLACK ( = −0.03, p = 0.27).he probability level and direction of all of the hypothesizedelationships remained unaltered. These investigations suggest ancceptable robustness of the model depicted in Fig. 2.

ly

gnificant path estimates.

5. Conclusions

The purpose of our study was to provide empirical evidenceon whether and how PSP relates to managers’ creation of bud-getary slack through affective organisational commitment andautonomous budget motivation. Our analysis shows that PSPindirectly decreases the creation of budgetary slack through themediating effect of affective organisational commitment. PSP alignsmanagers’ behaviours and decisions with the organisation’s goalsand as such instils affective commitment on the managers’ part.Affectively committed managers will undertake actions in line withtheir organisation’s goals and create less budgetary slack.

This study provides several contributions to both managementaccounting research and practice. First, our study extends the bud-getary slack literature by recognising an important influencingfactor: PSP. Prior research mainly focused on generic strategiesbut overlooked the effect of PSP although the strategic man-agement literature pinpointed its importance. In particular, this

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

research shows that PSP decreases managers’ budgetary slack cre-ation through affective commitment. The significant proportion ofvariance explained for the creation of budgetary slack (R2 = 0.25 forour model, R2 = 0.13 for the traditional explanation) indicates the

ING ModelY

1 gemen

iottrloadielsowtac(agFmttmcvstpamsia

t(cdtOt(ehpomprbmwotswdwsmuir

ARTICLEMARE-553; No. of Pages 12

0 J. De Baerdemaeker, W. Bruggeman / Mana

mportance of PSP, autonomous budget motivation, and affectiverganisational commitment in explaining budgetary slack in addi-ion to the traditional explanatory variables. Second, we believehat this study contributes to the growing amount of researchecognising that the budgeting process cannot be studied in iso-ation, as budgeting and strategic planning are both part of therganisational planning process (e.g. Covaleski et al., 2003; Kramernd Hartmann, 2011). Based on our study, it appears that BP is notirectly related with managers’ creation of budgetary slack, but that

t only indirectly decreases budgetary slack through the mediatingffect of autonomous budget motivation. PSP, on the other hand,owers the creation of budgetary slack through affective organi-ational commitment. It is therefore important to study the effectf both parts of the planning process simultaneously to understandhat exactly drives budgetary slack. Third, this study contributes to

he growing research exploring the interface between accountingnd strategy (Dent, 1990). Although strategy has gained signifi-ant importance in the management and organisational literatureLangfield-Smith, 1997), according to the best of our knowledge, noccounting research has investigated the impact of PSP despite therowing amount of strategic management research on this topic.ourth, this study also has some implications for the practice ofanagement accounting. In particular, our results demonstrate

he importance of personal variables such as affective organisa-ional commitment and autonomous motivation to understand

anagers’ budgeting behaviour. It are not the formal managementontrol systems in itself but it are their effects on these personalariables that are important to understand managers’ budgetarylack creation. Top management should therefore not only focus onhe design of a participatory system – being it either in the strategiclanning or budgeting process – but they should also understandnd manage the psychological effects it evokes on the subordinateanager’s part. Moreover, our study gives practitioners an under-

tanding of how budgeting and strategy can be related. Hence, itllustrates the importance and the benefits of managing the strategynd budgeting processes in an integrated way.

The results of this study are subject to a number of limita-ions. First, the proposed model considers two mediating factorsi.e. autonomous budget motivation and affective organisationalommitment) in the relationship between PSP and SLACK. There areoubtlessly alternative explanations that have not been captured inhe model tested here to keep the scope of this work manageable.ther underlying mechanisms that have been examined in rela-

ion to the creation of budgetary slack include perceived fairnesse.g. Wentzel, 2004), trust (e.g. Langevin and Mendoza, 2013), andthics (e.g. Stevens, 2002). The inclusion of these variables couldave produced different results. Future research should exploreossible other mediating mechanisms between PSP and SLACK. Sec-nd, the use of the PSP measurement instrument for the first timeay impede the results of our study. Although the psychometric

roperties of our measurement instrument were satisfying, futureesearch should further validate and refine it. Third, by choosingudgetary slack as a dependent variable, we are unable to deter-ine whether slack is desirable or not (Van der Stede, 2001). Ase cannot test whether the presence of budgetary slack is good

r bad for performance, future research should attempt to testhe good and bad conditions more explicitly. In addition to thesetudy-specific limitations, there are some limitations associatedith cross-sectional survey research in general. First, this study

epends on participants’ self-reported measures. Although stepsere taken to ensure reliability and tests show that there is no rea-

on to expect CMB or non-response bias, the possibility of noisy

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

easures cannot be eliminated. Although there is support for these of self-assessment (Venkatraman and Ramanujam, 1987) and

ts use allows us to compare our study with earlier budgetary slackesearch, a multi-method approach would improve the validity

PRESSt Accounting Research xxx (2015) xxx–xxx

of the results by confirming self-assessments with external mea-sures. Second, a cross-sectional study can only provide presumptiveevidence about causality. Alternative methods (e.g. experiment,longitudinal field research) may provide more information aboutthe directional relationships.

Notwithstanding these limitations, this study provides evidenceon the relationship between PSP and the creation of budgetaryslack. As the current study is the first to examine this relation-ship, many opportunities exist for further research in this area.One avenue for future research is to focus on other consequencesof PSP. Involving managers in strategic planning can, for example,also impact managerial and organisational performance. Further-more, the consequences as well as antecedents of PSP must beinvestigated. Possible antecedents, such as environmental com-plexity and the organisation’s competitive strategy, should bestudied (Hutzschenreuter and Kleindienst, 2006). Another avenueto explore is whether fostering autonomous budget motivationcan offset the positive effects of lower information asymmetry(due to PSP) on job tension (Jaworski and Young, 1992). Futureresearch could also investigate the impact of other characteristicsof the strategy process (e.g. the degree of formality, the degree ofopenness of top management to subordinate managers’ PSP) onbudgeting outcomes.

While further research is needed before definitive conclusionscan be drawn, the findings of our study suggest that studying thewhole planning process (i.e. both budgeting and strategic planning)is useful for understanding the creation of budgetary slack. Theantecedents of budgetary slack creation may be more complex anddiverse than assumed since budgetary slack creation relates to thebroader planning context than merely the direct budgeting setting.

Acknowledgements

We wish to express our gratitude to Sally Widener, FrankHartmann, Sophie Hoozée, Klaus Derfuss, Anne Boomsma, PascalLangevin and Patricia Everaert for their constructive comments onearlier drafts of this paper. We acknowledge the most valuablecomments from two anonymous reviewers and the associate editorTheresa Libby. We are grateful for helpful comments from the par-ticipants of the 9th International Management Control ResearchConference (Nyenrode, September 2013), the participants of the7th Performance Measurement and Management Control Confer-ence (Barcelona, September 2013), as well as the participants of the37th European Accounting Association Annual Congress (Tallinn,May 2014). The first author gratefully acknowledges the financialsupport provided by a BOF research fund of Ghent University (con-tract number B/12354/01) and a special research grant from theNational Bank of Belgium.

Appendix A. Supplementary data

Supplementary data associated with this article can be found, inthe online version, at http://dx.doi.org/10.1016/j.mar.2015.06.002

References

Allen, N.J., Meyer, J.P., 1990. The measurement and antecedents of affective,continuance and normative commitment to the organization. J. Occup. Psychol.63, 1–18.

Anderson, J.C., Gerbing, D.W., 1988. Structural equation modeling: a review andrecommended two-step approach. Psychol. Bull. 103, 411–423.

Ansoff, H.I., 1965. Corporate Strategy: An Analytic Approach to Business Policy for

., The impact of participation in strategic planning on managers’tion and affective organisational commitment. Manage. Account.

Growth and Expansion. McGraw-Hill, New York (N.Y.).Anthony, R.N., 1965. Planning and Control Systems: A Framework for Analysis.

Harvard Business School, Boston (Mass.).Anthony, R.N., Govindarajan, V., 2007. Management Control Systems, 12th ed.

McGraw-Hill, Boston, Massachusetts.

ING ModelY

gemen

A

A

B

BB

B

B

B

B

B

B

B

C

C

C

C

C

C

C

C

C

D

DD

D

D

D

D

D

F

F

F

F

F

G

G

G

ARTICLEMARE-553; No. of Pages 12

J. De Baerdemaeker, W. Bruggeman / Mana

ranya, N., Ferris, K.R., 1984. A reexamination of accountants’organizational-professional conflict. Account. Rev. 59, 1–15.

rbuckle, J., Wothke, W., 1999. AMOS 4 User’s Reference Guide. SmallwatersCorporation, Chicago.

aumeister, R., Leary, M.R., 1995. The need to belong: desire for interpersonalattachments as a fundamental human motivation. Psychol. Bull. 117, 497–529.

ecker, S., Green, D., 1962. Budgeting and employee behavior. J. Bus. 35, 392–402.ecker, T.E., 2005. Potential problems in the statistical control of variables in

organizational research: a qualitative analysis with recommendations. Organ.Res. Methods 8, 274–289.

entler, P.M., Bonett, D.D., 1980. Significance tests and goodness of fit in theanalysis of covariance structures. Psychol. Bull. 88, 588–606.

isbe, J., Batista-Foguet, J.-M., Chenhall, R.H., 2007. Defining managementaccounting constructs: a methodological note on the risks of misspecification.Account. Organ. Soc. 32, 789–820.

ono, J.E., Judge, T.A., 2003. Self-concordance at work: toward understanding themotivational effects of transformational leaders. Acad. Manage. J. 46, 554–571.

oomsma, A., Hoogland, J.J., 2001. The robustness of LISREL modeling revisited.Structural equation models: present and future. A Festschrift in honor of KarlJöreskog, 139–168.

ourgeois, L.J., Brodwin, D.R., 1984. Strategic implementation: five approaches toan elusive phenomenon. Strategic Manage. J. 5, 241–264.

oyatzis, R.E., 1998. Transforming Qualitative Information: Thematic Analysis andCode Development. Sage, Thousand Oaks (Calif.).

rowne, M.W., Cudeck, R., 1993. Alternative ways of assessing model fit. In: Bollen,K.A., Long, J.S. (Eds.), Testing Structural Equation Models. Sage, Newbury Park,CA, pp. 136–162.

adez, S., Guilding, C., 2008. An exploratory investigation of an integratedcontingency model of strategic management accounting. Account. Organ. Soc.33, 836–863.

handler, A.D., 1962. Strategy and Structure: Chapters in the History of theIndustrial Enterprise. MIT Press, Cambridge (Mass.).

hapman, C.S., Kihn, L.-A., 2009. Information system integration, enabling controland performance. Account. Organ. Soc. 34, 151–169.

henhall, R.H., 2003. Management control systems design within its organizationalcontext: findings from contingency-based research and directions for thefuture. Account. Organ. Soc. 28, 127–168.

henhall, R.H., Kallunki, J.-P., Silvola, H., 2011. Exploring the relationships betweenstrategy, innovation, and management control systems: the roles of socialnetworking, organic innovative culture, and formal controls. J. Manage.Account. Res. 23, 99–128.

hurch, B.K., Hannan, R.L., Kuang, X.J., 2012. Shared interest and honesty in budgetreporting. Account. Organ. Soc. 37, 155–167.

ollins, F., 1978. The interaction of budget characteristics and personality variableswith budgetary response attitudes. Account. Rev. 53, 324–335.

ovaleski, M.A., Evans III, J.H., Luft, J.L., Shields, M.D., 2003. Budgeting research:three theoretical perspectives and criteria for selective integration. J. Manage.Account. Res. 15, 3–49.

yert, R.M., March, J.G., 1963. Behavioral Theory of the Firm. Prentice Hall,Englewood Cliffs, NJ.

avila, T., Wouters, M., 2005. Managing budget emphasis through the explicitdesign of conditional budgetary slack. Account. Organ. Soc. 30, 587–608.

eci, E.L., 1975. Intrinsic Motivation. Plenum Press, New York (N.Y.).eci, E.L., Connell, J.P., Ryan, R.M., 1989. Self-determination in a work organization.

J. Appl. Psychol. 74, 580–590.eci, E.L., Ryan, R.M., 2004. Handbook of Self-Determination Research. University

of Rochester, Rochester (N.Y.).ent, J.F., 1990. Strategy, organization and control: Some possibilities for

accounting research. Account. Organ. Soc. 15, 3–25.erfuss, K., 2012. Budget slack: some meta-analytic evidence. In: 8th Conference

on New Directions in Management Accounting, Brussels, Belgium.unk, A.S., 1993. The effect of budget emphasis and information asymmetry on the

relation between budgetary participation and slack. Account. Rev. 68, 400–410.unk, A.S., Nouri, H., 1998. Antecedents of budget slack: a literature review and

synthesis. J. Account. Lit. 17, 72–96.loyd, S.W., Wooldridge, B., 1992. Middle management involvement in strategy

and its association with strategic type. Strategic Manage. J. 13, 153–167.loyd, S.W., Wooldridge, B., 2000. Building Strategy from the Middle:

Reconceptualizing Strategy Process. Sage, London.ornell, C., Larcker, D.F., 1981. Evaluating structural equation models with

unobservable variables and measurement error. J. Market. Res. 18, 39–50.reeman, E.B., 1989. Effectiveness of strategic planning: a multidimensional view.

Acad. Manage. Proc. 1, 12–16.rezatti, F., Aguiar, A.B., Guerreiro, R., Gouvea, M.A., 2011. Does management

accounting play role in planning process. J. Bus. Res. 64, 242–249.agné, M., Chemolli, E., Forest, J., Koestner, R., 2008. A temporal analysis of the

relation between organisational commitment and work motivation. Psychol.Belgica 48, 219–241.

agné, M., Forest, J., Vansteenkiste, M., Crevier-Braud, L., Van den Broeck, A.,Aspeli, A.K., Battistelli, A., Bellerose, J., Benabou, C., Chemolli, E., Güntert, S.T.,Halvari, H., Johnson, P., Indiyastuti, D.L., Ndao, A., Martin-Albo, J., Molstad, M.,

Please cite this article in press as: De Baerdemaeker, J., Bruggeman, Wcreation of budgetary slack: The mediating role of autonomous motivaRes. (2015), http://dx.doi.org/10.1016/j.mar.2015.06.002

Naudin, M., Ntalianis, F., Nunez, J.L., 2013. The multi-dimensional workmotivation scale: validation evidence in seven languages and nine countries.

erbing, D.W., Hamilton, J.G., Freeman, E.B., 1994. A large-scale second-orderstructural equation model of the influence of management participation onorganizational planning benefits. J. Manage. 20, 859–885.

PRESSt Accounting Research xxx (2015) xxx–xxx 11

Grant, A.M., 2008. Does intrinsic motivation fuel the prosocial fire? Motivationalsynergy in predicting persistence, performance, and productivity. J. Appl.Psychol. 93, 48.

Grant, A.M., Nurmohamed, S., Ashford, S.J., Dekas, K., 2011. The performanceimplications of ambivalent initiative: the interplay of autonomous andcontrolled motivations. Organ. Behav. Hum. Decis. Process. 116, 241–251.

Greguras, G.J., Dieffendorff, J.M., 2009. Different fits satisfy different needs: linkingperson-environment fit to employee commitment and performance usingself-determination theory. J. Appl. Psychol. 94, 465–477.

Hair, J.F.J., Black, W.C., Babin, B.J., Anderson, R.E., 2010. Multivariate Data Analysis:A Global Perspective, 7th ed. Pearson Education, Inc., Upper Saddle River, NewJersey.

Hall, M., 2008. The effect of comprehensive performance measurement systems onrole clarity, psychological empowerment and managerial performance.Account. Organ. Soc. 33, 141–163.

Hansen, S.C., Otley, D.T., Van der Stede, W.A., 2003. Practice developments inbudgeting: an overview and research perspective. J. Manage. Account. Res. 15,95–116.

Hansen, S.C., Van der Stede, W.A., 2004. Multiple facets of budgeting: anexploratory analysis. Manage. Account. Res. 15, 415–439.

Hartmann, F., Slapnicar, S., 2009. How formal performance evaluation affects trustbetween superior and subordinate managers. Account. Organ. Soc. 34,722–737.

Hopwood, A., 1974. Accounting and Human Behaviour. Haymarket, London.Hunton, J.E., Gibson, D., 1999. Soliciting user-input during the development of an

accounting information system: investigating the efficacy of group discussion.Account. Organ. Soc. 24, 597–618.

Hutzschenreuter, T., Kleindienst, I., 2006. Strategy-process research: what have welearned and what is still to be explored. J. Manage. 32, 673–720.

Indjejikian, R.J., Matejka, M., 2006. Organizational slack in decentralized firms: therole of business unit controllers. Account. Rev. 81, 849–872.

Jaworski, B.J., Young, S.M., 1992. Dysfunctional behavior and management control:an empirical study of marketing managers. Account. Organ. Soc. 17, 17–35.