Embed Size (px)

Citation preview

1

Published May 2015

15.0 International audit issues – Under review

(Revised January 2014)

Disclaimer

Hyperlinks to external or unaffiliated websites are for information purposes only. The Canada

Revenue Agency (CRA) is not responsible for the content or practices of such websites. While

efforts are made to ensure that hyperlinks are current and up-to-date, it is not guaranteed.

15.1.0 Introduction – Under review

(Revised January 2014)

This chapter deals with international audit issues as well as issues that affect international

taxpayers.

15.2.0 Income of a non-resident – Under review

(Revised January 2014)

15.2.1 Overview

A non-resident person is subject to income tax under Part I of the Income Tax Act (ITA) where

the non-resident person was:

• employed in Canada;

• carried on a business in Canada; or

• disposed of taxable Canadian property at any time in the year or a previous year.

A brief discussion of the treatment of income from each of these sources follows.

15.2.2 Part XIII tax

(Revised November 2013)

A non-resident person is subject to income tax under Part XIII of the ITA on certain types of

income arising in Canada, including dividends, interest, rents and royalties.

For more information, go to 15.3.0, Part XIII tax on income from Canada of non-resident

persons.

15.2.3 Part XIV tax

Non-resident corporations that earn income from carrying on business in Canada are subject to

tax under Part XIV of the ITA that is in addition to tax payable under Part I.

15.2.4 Income earned in Canada from an office or employment

(Revised November 2013)

Non-resident individuals that are regularly and continuously employed in Canada during the year

are subject to tax under paragraph 2(3)(a) of the ITA on income earned in the year as described

in subparagraph 115(1)(a)(i).

Subsection 115(2) applies in certain circumstances and deems certain types of non-resident

persons to have been employed in Canada for the purposes of subsection 2(3).

A non-resident individual that has earned employment income during the year must calculate the

amount and file an income tax return according to the same rules that apply to resident

2

Published May 2015

employees. Therefore, the non-resident's income includes the value of any benefits received or

enjoyed in connection with employment in Canada. In addition, the individual must file an

income tax return if, during a calendar year, employment income was earned in Canada resulting

in income tax payable under Part I for that year.

Treaties do not generally override the statutory provisions referred to above; exceptions to the

Canada-US treaty include exemption from Part I tax in Canada for any US resident that:

• earns less than $10,000 in respect of an employment in Canada; and

• is present in Canada for fewer than 184 days during the year and the remuneration is not

expensed from Part I taxes in Canada.

15.2.5 Income from business carried on in Canada

(Revised November 2013)

Income earned by a non-resident from carrying on a business in Canada is:

• included in taxable income under subparagraph 115(1)(a)(ii) of the ITA;

• taxable under paragraph 2(3)(b) of the ITA; and

• subject to withholdings in accordance with Section 105 of the Income Tax Regulations

(Regulation 105).

Whether a business is being carried on in Canada is generally a question of fact based on

common law factors connecting a business to a particular place and on the definition in section

253 of the ITA of "extended meaning of carrying on business" in Canada.

Where it is not obvious whether an individual is an employee subject to income tax under

paragraph 2(3)(a) of the ITA or taxable as a contractor under paragraph 2(3)(b) as having

"carried on a business in Canada," certain tests may be applied to make that determination.

For more information, go to 15.2.9, Agent or servant vs. independent contractor.

15.2.6 Common law factors connecting a business to a particular place

(Revised November 2013)

Common law has identified several factors that connect a business to a particular place. The

place where profit-producing contracts (for example, sales contracts) are entered into is generally

recognized as an important factor in determining where a business is carried on. However, the

courts have frequently looked beyond the conclusion of sales contracts citing the fact that

business income is attributable to the sum total of business activity not merely to the completion

of the sale.

Accordingly, depending on the facts of a case, one or more of the following factors may be

important in determining whether a non-resident person is carrying on business in Canada:

• place of delivery of goods

• place where services are rendered

• place of payment for the goods or services

• place where purchases are made in connection with goods or services

• place of manufacture or production

3

Published May 2015

• place from which transactions are solicited

• location of an inventory of goods

• location of a bank account relating to the business

• place where the non-resident's name and business are listed in a directory

• location of a branch office

• place where agents or employees of the non-resident are located

15.2.7 Carrying on business "with" vs. "in" Canada

(Revised November 2013)

Generally, non-resident corporations that export goods to Canadian customers are considered to

be carrying on business "with" Canada, not "in" Canada if the place of delivery is the only factor

that indicates that business activity is being carried on in Canada. For example, unless sales

orders are procured through an agent in Canada, a corporation merely selling goods into Canada

would not be considered to be carrying on business in Canada and is not subject to the T2 filing

requirements or to income tax in Canada.

For more information, go to Tax Guide 4012, T2 Corporation – Income Tax Guide, at www.cra-

arc.gc.ca/E/pub/tg/t4012/README.html.

Where services are rendered to customers situated in Canada, such activity will normally be

considered to be carrying on business in Canada only if work is performed in Canada.

15.2.8 Extended meaning of "Carrying on business in Canada"

Section 253 of the ITA deems a non-resident to be carrying on business in Canada regarding the

activities and dispositions specified in the section. This extended meaning applies to a non-

resident person and certain trusts whose beneficiaries are non-residents in a tax year that:

• produce, grow, mine, create, manufacture, fabricate, improve, pack, preserve, or

construct, in whole or in part, anything in Canada, whether or not for export;

• solicit orders or offer anything for sale in Canada through an "agent or servant;" or

• dispose of a Canadian resource property, timber resource property or real property that is

not a capital property.

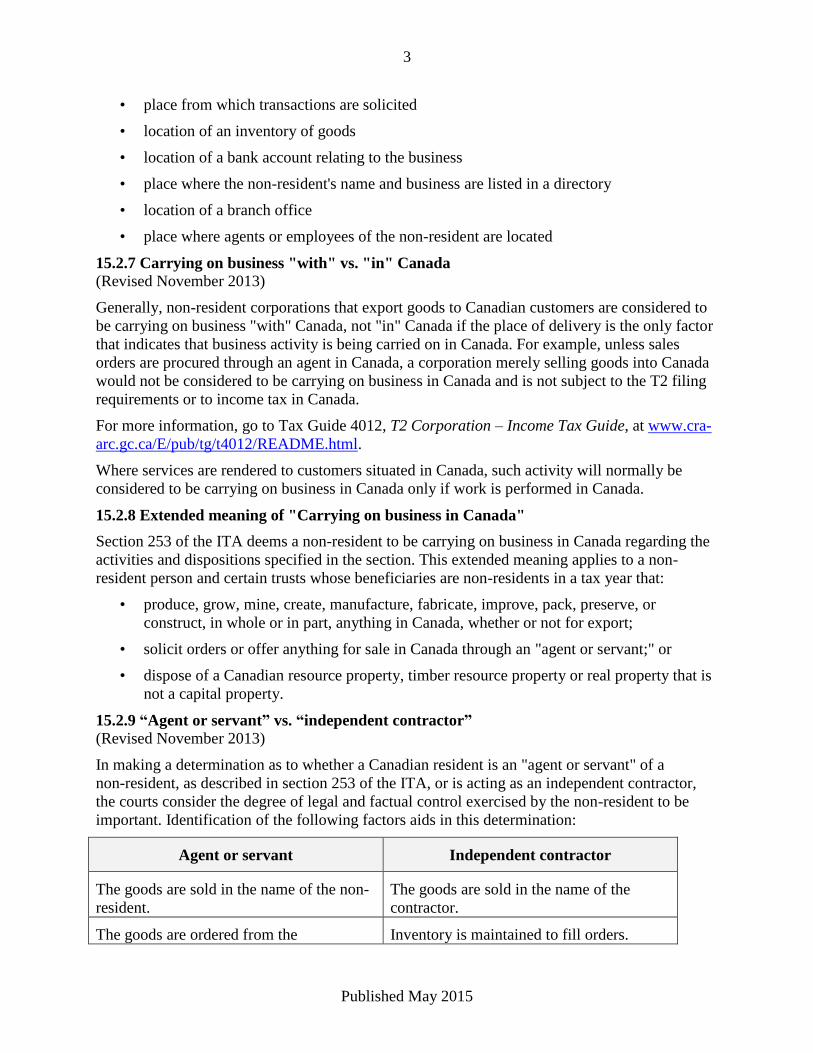

15.2.9 “Agent or servant” vs. “independent contractor”

(Revised November 2013)

In making a determination as to whether a Canadian resident is an "agent or servant" of a

non-resident, as described in section 253 of the ITA, or is acting as an independent contractor,

the courts consider the degree of legal and factual control exercised by the non-resident to be

important. Identification of the following factors aids in this determination:

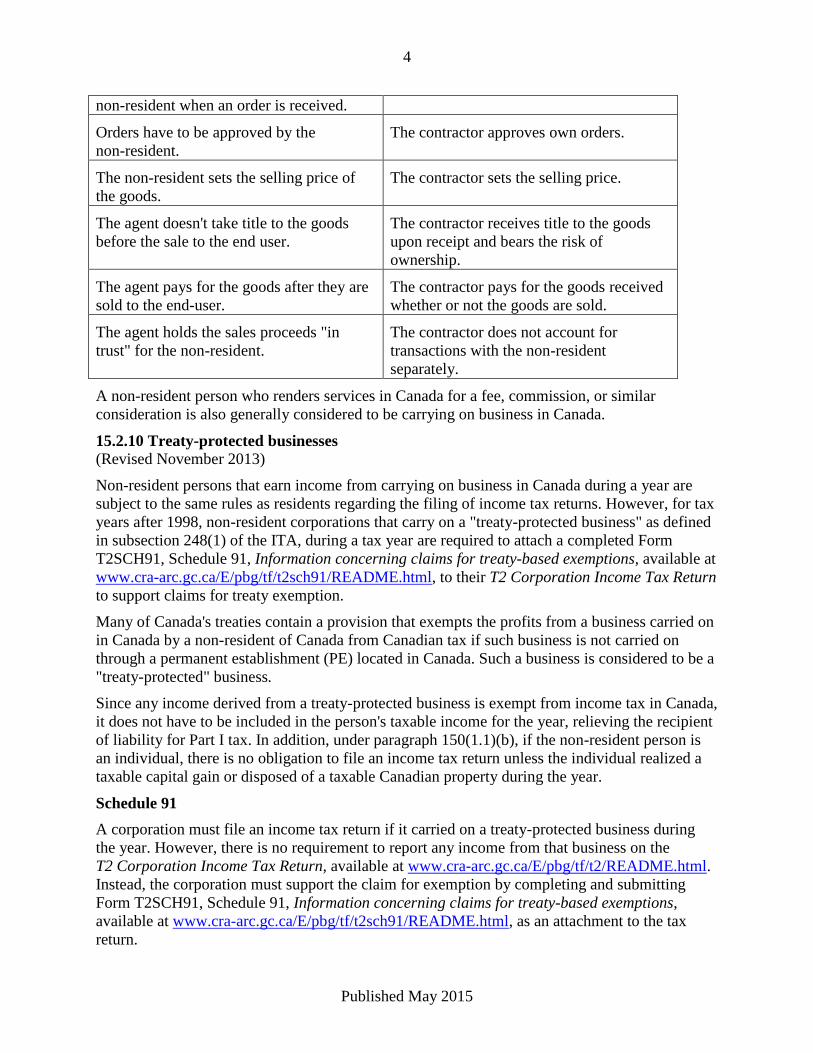

Agent or servant Independent contractor

The goods are sold in the name of the non-

resident.

The goods are sold in the name of the

contractor.

The goods are ordered from the Inventory is maintained to fill orders.

4

Published May 2015

non-resident when an order is received.

Orders have to be approved by the

non-resident.

The contractor approves own orders.

The non-resident sets the selling price of

the goods.

The contractor sets the selling price.

The agent doesn't take title to the goods

before the sale to the end user.

The contractor receives title to the goods

upon receipt and bears the risk of

ownership.

The agent pays for the goods after they are

sold to the end-user.

The contractor pays for the goods received

whether or not the goods are sold.

The agent holds the sales proceeds "in

trust" for the non-resident.

The contractor does not account for

transactions with the non-resident

separately.

A non-resident person who renders services in Canada for a fee, commission, or similar

consideration is also generally considered to be carrying on business in Canada.

15.2.10 Treaty-protected businesses

(Revised November 2013)

Non-resident persons that earn income from carrying on business in Canada during a year are

subject to the same rules as residents regarding the filing of income tax returns. However, for tax

years after 1998, non-resident corporations that carry on a "treaty-protected business" as defined

in subsection 248(1) of the ITA, during a tax year are required to attach a completed Form

T2SCH91, Schedule 91, Information concerning claims for treaty-based exemptions, available at

www.cra-arc.gc.ca/E/pbg/tf/t2sch91/README.html, to their T2 Corporation Income Tax Return

to support claims for treaty exemption.

Many of Canada's treaties contain a provision that exempts the profits from a business carried on

in Canada by a non-resident of Canada from Canadian tax if such business is not carried on

through a permanent establishment (PE) located in Canada. Such a business is considered to be a

"treaty-protected" business.

Since any income derived from a treaty-protected business is exempt from income tax in Canada,

it does not have to be included in the person's taxable income for the year, relieving the recipient

of liability for Part I tax. In addition, under paragraph 150(1.1)(b), if the non-resident person is

an individual, there is no obligation to file an income tax return unless the individual realized a

taxable capital gain or disposed of a taxable Canadian property during the year.

Schedule 91

A corporation must file an income tax return if it carried on a treaty-protected business during

the year. However, there is no requirement to report any income from that business on the

T2 Corporation Income Tax Return, available at www.cra-arc.gc.ca/E/pbg/tf/t2/README.html.

Instead, the corporation must support the claim for exemption by completing and submitting

Form T2SCH91, Schedule 91, Information concerning claims for treaty-based exemptions,

available at www.cra-arc.gc.ca/E/pbg/tf/t2sch91/README.html, as an attachment to the tax

return.

5

Published May 2015

15.2.11 Withholding of Part I tax – Income from carrying on a business in Canada

Regulation 105 and paragraph 153(1)(g) of the ITA require any person paying a non-resident

person for services rendered in Canada (other than for regular and continuous employment

services) to withhold 15% of the gross payment. However, most tax treaties between Canada and

other countries provide for some relief from this requirement. The withholding does not

represent a final tax and must be remitted by the 15th of the following month.

The non-resident must file an income tax return (T1 or T2) in Canada, regardless of whether a

waiver has been received and pay income tax under Part I if applicable. Refunds may be issued if

a business is carried on in Canada with no fixed base or PE if an exemption is provided under a

tax treaty.

In accordance with subsection 227(8.4) of the ITA, where a person has failed to make a

withholding under Regulation 105 from a payment to a non-resident recipient, such person

becomes liable to pay the tax.

15.2.12 Disposition of taxable Canadian property by a non-resident

(Revised November 2013)

Taxable capital gains or other income arising from the disposition of taxable Canadian property

by a non-resident are:

• taxable under paragraph 2(3)(c) of the ITA;

• included in taxable income under subparagraph 115(1)(a)(iii); and

• subject to withholdings in accordance with section 116.

Withholding of income tax on dispositions of taxable Canadian property

Section 116 requires a non-resident person disposing of taxable Canadian property to notify the

CRA of the dispositions and to make a payment or provide acceptable security on account of tax

on any gain or income arising from the disposition.

Once this notification/payment has been confirmed, the CRA will issue a certificate to both

parties to the transaction confirming that the non-resident has complied with the section 116

requirements. The certificate identifies the vendor, purchaser, and the property disposed of and

confirms the amount of the certificate limit if it is a proposed disposition or the proceeds of

disposition if it is an actual disposition.

For more information, go to Income Tax Information Circular IC72-17R6, Procedures

concerning the disposition of taxable Canadian property by non-residents of Canada – Section

116, at www.cra-arc.gc.ca/E/pub/tp/ic72-17r6/README.html.

However, if the final amount payable for the property exceeds the certificate limit, the purchaser

must withhold and remit 25 %i1 of the amount of the excess. In the case of properties the

dispositions of which are generally accorded income rather than capital gains treatment, such as

a Canadian resource property, timber resource or non-capital real property, the withholding rate

for such excess is 50% (subsections 116(5.2) and 116(5.3)).

If the vendor does not notify the CRA, the purchaser is liable to remit to the Receiver General

within 30 days after the end of the month in which the purchaser acquired the property, the tax

on the amount payable by the purchaser calculated at the applicable rate. This requirement is

6

Published May 2015

waived if it can be demonstrated that, after reasonable inquiry, the purchaser had no reason to

believe that the vendor was a non-resident. The purchaser acquiring the property may recover

any such tax remitted by deducting it from any amount payable to the vendor.

In addition, the purchaser becomes liable for any related penalties and interest arising under

subsections 227(9) and 227(9.3) for failure to remit.

15.2.13 Treaty-protected property

(Revised November 2013)

Non-residents are subject to Part I tax on income from the disposition of taxable Canadian

property. However, Canada's tax treaties provide that while dispositions by non-residents of a

real property or PE property situated in Canada are taxable in Canada, other taxable Canadian

property is considered to be treaty-protected property. Any income or gain from the disposition

of such property may be taxed only in the country of residence.

Schedule 91

A corporation must file an income tax return for the year if it disposed of a taxable Canadian

property during the year. However, if the taxable Canadian property was a treaty-protected

property, there is no requirement to include any gain or income from that disposition in the

calculation of income earned in Canada. Instead, the corporation must support its claim for

exemption by completing Form T2SCH91, Schedule 91, Information concerning claims for

treaty-based exemptions, available at www.cra-arc.gc.ca/E/pbg/tf/t2sch91/README.html, and

filing the schedule as an attachment to the return.

15.2.14 Waivers of withholding tax

If the CRA is satisfied that there is no tax liability or a lesser tax liability than provided for in

the legislation, withholding tax may be waived on payments made to non-residents for the

following:

• non-resident employee remuneration

• fees, commissions, or other amounts for services performed in Canada

• business income in Canada (no Part XIII tax if taxable under Part I)

• salary paid by an eligible employer to an employee working overseas at least six months

(overseas employment tax credit)

• payments under the Student Work Abroad Program (SWAP); foreign students studying

full time and working in Canada may not be subject to withholding if the total income

earned in the year is less than the non-refundable tax credit base amount

• payments subject to treaty-based waivers – non-resident corporations that do not derive

income from a PE in Canada, non-resident individuals that do not derive income from a

fixed base regularly available in Canada, employment income in Canada less than the

threshold amount ($10,000 for US residents)

15.2.15 Tax calculations

(Revised November 2013)

Individuals

7

Published May 2015

A non-resident individual is liable for income tax at the rates set out in subsection 117(2) of the

ITA that are the same rates applicable to an individual who is resident in Canada. A non-resident

individual is also liable for Part I.1 surtax.

Section 118.94 stipulates that 90% of the total income of a non-resident must be included in

computing taxable income earned in Canada for the non-resident to be entitled to deduct most of

the non-refundable tax credits in computing income tax payable for the year.

Corporations

Non-resident corporations subject to income tax in Canada are taxed at the same rate as resident

corporations. The normal rules for determining the amount of taxable income earned in a

province by a corporation are modified by subsection 413(1) of the Income Tax Regulations

applicable to non-resident corporations. In computing the taxable income earned in a province, a

non-resident corporation that has a PE in a province, excludes salaries and gross revenue

attributable to a PE outside Canada and includes only taxable income earned in Canada.

For purposes of determining the taxable income earned in a province, “permanent establishment”

is defined in subsection 400(2) of the Income Tax Regulations as a fixed place of business,

including an office, a branch, a mine, a workshop, and so on. However, it should be noted that

this definition of “permanent establishment” differs from the one found in tax treaties.

A non-resident corporation may claim the same tax credits under Division E (computation of tax)

as a resident corporation, except for the small business deduction in section 125 and the foreign

tax deduction under section 126.

15.2.16 Audit considerations

(Revised January 2014)

Income from an office or employment in Canada

The verification of the propriety of payroll deductions and remittances is the responsibility of

payroll auditors and is not normally addressed by business audit. However, during the audit of

corporations carrying on business in Canada, the auditor may determine that certain non-resident

employees are temporarily employed in Canada.

The auditor should verify that the employer has undertaken to account for the time that each

employee was employed in Canada and has made reasonable salary allocations to Canada when

preparing T4 slips for such employees.

In addition, non-resident employees may receive equalization payments to compensate them for

relatively higher personal tax rates than payable in their resident country. Such equalization

payments constitute employment remuneration and are subject to withholdings under section 102

of the Income Tax Regulations.

If the audit reveals that withholdings have not been made and T4 slips not prepared, all related

documentation should be referred to the Trust Account Examination Section, Revenue

Collections Division.

Services rendered in Canada by a non-resident

The review of disbursements by a non-resident corporation carrying on business in Canada may

reveal non-payroll amounts paid to individuals for services rendered in Canada relating to that

business. The nature of the relationship between the corporation and the individual should be

8

Published May 2015

reviewed to determine whether the individual is an employee or a sub-contractor. If the

individual is providing regular and continuous service under the control of the corporation the

matter should be referred to payroll audit. If it is determined that the individual is an independent

contractor and is a non-resident, the application of Regulation 105 should be considered.

The auditor should be aware of the following examples of payments to individuals for

non-employment services:

• fees or other amounts paid to:

• entertainers – including actors and actresses

• athletes – including boxers, wrestlers, tennis players, golfers, and team players

• traveling theatrical groups, ballet, orchestras and variety shows, circuses and

carnivals

• lecturers

• consultants

• fees paid under service contracts relating to drilling operations in Canada, including

offshore drilling

• fees paid under service contracts for custom combining

Payments for services rendered in Canada by a non-resident in other than regular and continuous

employment are subject to a withholding of 15%. This requirement to withhold tax applies

regardless of any tax treaty between Canada and the recipient’s country of residence.

In addition, the auditor should:

• Obtain the T4A-NR return and slips to reconcile applicable payments to non-residents.

• Review the supplier master listing (including address details), if available, to identify

potential non-resident payees that might be subject to withholding tax treatment (under

either Part XIII or Regulation 105).

• Where potential candidates for withholdings are identified, review the supplier file to

determine the nature and dollar volume of the payments.

• If possible, use audit software to isolate and summarize payments by supplier number and

by account charged to quantify payments to specific suppliers and identify the nature of

those payments.

Documentation, including copies of invoices, contracts and cancelled cheques relating to any

questionable payments should be given to the International Tax Section at the tax services office

(TSO) together with an explanatory memorandum.

The Non-Resident unit may initiate a concurrent joint audit of the Canadian resident payer based

on the documentation provided and assess withholding taxes as required.

Dispositions of taxable Canadian property

(Revised January 2014)

During the audit of Canadian resident persons or non-resident persons carrying on business in

Canada auditors should:

9

Published May 2015

• Review supporting documentation relating to significant purchases of property from

non-residents.

• Determine whether the property is taxable Canadian property subject to the requirements

in section 116.

• If the property is subject to section 116, establish whether the vendor has obtained a

certificate of compliance (Form T2062 or T2062A) relating to the disposition. A copy of

the certificate should be in the permanent document folder. A copy may also be obtained

from the Dispositions Unit, International Tax Section at the applicable TSO or from the

taxpayer.

• Examine documentation relating to the transaction including any purchase agreement,

correspondence, cancelled cheque, etc.

• If the vendor was a non-resident and a certificate of compliance was not obtained, gather

available evidence indicating that the purchaser should have been aware the vendor was a

non-resident.

If a certificate relating to the disposition is unavailable and compliance cannot otherwise be

verified, forward all documentation including records of taxpayer discussions concerning the

transaction, together with an explanatory memorandum, to the International Tax Section at the

TSO for issuance of a purchaser liability assessment if necessary.

15.2.17 Assessment procedures

(Revised November 2013)

Where potential assessments of residents for unremitted Part I withholdings are identified, refer

the adjustments to the International Section of the applicable TSO for processing. Such referrals

should be in the form of a written memorandum outlining the nature and the amount of the

transactions requiring assessment and should be supported by copies of all applicable

documentation. This procedure should also be followed for other potential Part I tax assessments

of non-residents.

Where it is determined that a non-resident has earned income under section 115 during a tax year

and has not filed an income tax return for that year, a memorandum outlining all relevant details

should be referred to the Non-Filer/Non-Registrant Section of the International Tax Services

Office.

All referrals should be noted in the Audit Report and cross-referenced to a copy of the applicable

memorandum included in the audit working papers.

15.2.18 References

(Revised November 2013)

Income Tax Act

• Sections 2, 115, and 116

Income Tax Regulations

• Sections 102 and 105

Income Tax Information Circulars

10

Published May 2015

• IC72-17R6, Procedures concerning the disposition of taxable Canadian property by non-

residents of Canada – Section 116, at www.cra-arc.gc.ca/E/pub/tp/ic72-

17r6/README.html

• IC75-6R2, Required withholding from amounts paid to non-residents providing services

in Canada, at www.cra-arc.gc.ca/E/pub/tp/ic75-6r2/README.html

Income Tax Interpretation Bulletins

• IT81R, Partnerships – Income of non-resident partners, at www.cra-

arc.gc.ca/E/pub/tp/it81r/README.html

• IT168R3, Athletes and players employed by football, hockey, and similar clubs, at

www.cra-arc.gc.ca/E/pub/tp/it168r3/README.html

• IT173R2, Capital gains derived in Canada by residents of the United States, at www.cra-

arc.gc.ca/E/pub/tp/it173r2/README.html

• IT173R2SR, Capital gains derived in Canada by residents of the United States, at

www.cra-arc.gc.ca/E/pub/tp/it173r2sr/README.html

• IT262R2, Losses of non-residents and part-year residents, at www.cra-

arc.gc.ca/E/pub/tp/it262r2/README.html

• IT420R3, Non-residents – Income earned in Canada, at www.cra-

arc.gc.ca/E/pub/tp/it420r3/README.html

• IT420R3SR, Non-residents – Income earned in Canada, at www.cra-

arc.gc.ca/E/pub/tp/it420r3sr/README.html

Tax Guides

• T4001, Employer's guide - Payroll deductions and remittances, at

www.cra-arc.gc.ca/E/pub/tg/t4001/README.html

• T4058, Non-residents and income tax, at

www.cra-arc.gc.ca/E/pub/tg/t4058/README.html

• T4061, NR4 - Non-resident tax withholding, remitting, and reporting, at

www.cra-arc.gc.ca/E/pub/tg/t4061/README.html

Communiqués

• ITD-99-04, Regulation 105 Treaty-Based Waiver Guidelines

• ITD-99-05, Non-resident Athletes Employed in Canada – Signing Bonuses

• ITD-05-06, The Dudney Decision: Effects on Fixed Base or Permanent Establishment

Audits and Regulation 105 Treaty-based Waiver Guidelines

• ITD-02-02, International Waivers Program Update on Various Issues

15.3.0 Part XIII tax on income from Canada of non-resident persons – Under review

(Revised January 2014)

15.3.1 Legislative authority

(Revised November 2013)

11

Published May 2015

Subsection 212(1) of the ITA imposes income tax of 25% on certain amounts paid or credited (or

deemed paid or credited) to non-residents by residents (or deemed residents) of Canada. The

specific items on which tax is imposed are found in paragraphs 212(1)(a) through 212(1)(v) and

subsection 212(2). Under section 215, the resident payer must withhold and remit this tax.

The statutory rate of withholding tax of 25% may be reduced by the relevant tax treaty between

Canada and the country of residence of the non-resident.

15.3.2 Income taxed under Part XIII

(Revised November 2013)

The more common sources of income that are paid to non-residents, and from which Part XIII

tax is withheld, include:

• management fees;

• interest;

• rents;

• royalties; and

• dividends.

For more information, go to Income Tax Information Circular IC77-16R4, Non-resident income

tax, at www.cra-arc.gc.ca/E/pub/tp/ic77-16r4/README.html.

15.3.3 Withholding and reporting obligations of the payer

(Revised November 2013)

In accordance with subsection 215(1) of the ITA, the resident payer, such as a tenant paying rent

or a mortgagor or other debtor paying interest to a non-resident, must withhold non-resident tax

at source from the amount paid or credited, and remit it to the Receiver General for Canada.

Under subsection 215(6), a person who fails to withhold and remit where required, is liable to

pay the tax that should have been withheld. However, that person is entitled to withhold or

otherwise recover from further payments to the non-resident any amount so paid as tax.

The payer must prepare an NR4 Summary annually. Accompanying information slips, including

the full name and address of the payer and payee, the gross amount of income paid and the

amount of non-resident tax withheld, must be submitted with the NR4 Summary. Copies 2 and 3

of the NR4 slips are to be delivered to the recipient by March 31 following the end of the

calendar year. As the amount withheld represents a final tax, there is no requirement for filing of

an income tax return by the non-resident income recipient.

15.3.4 Treaty reduction of Part XIII tax rate

(Revised November 2013)

The statutory Part XIII tax rate is 25% and is usually reduced by the relevant tax treaty between

Canada and the non-resident's country of residence. Accordingly, it is recommended that

auditors check with the International Tax Section of their TSO to confirm the applicable rate

prior to processing a Part XIII assessment.

For more information, go to Income Tax Information Circular IC76-12R6, Applicable rate of

part XIII tax on amounts paid or credited to persons in countries with which Canada has a tax

12

Published May 2015

convention, at www.cra-arc.gc.ca/E/pub/tp/ic76-12r6/README.html, for a schedule of non-

resident withholding tax rates for treaty countries.

This may be used as a guide to verify the correct rate for withholding of Part XIII tax from

payments made to non-residents of Canada. However, as treaties are re-negotiated frequently and

new treaties entered into, reference to the actual treaty texts is advisable.

15.3.5 Election by a non-resident to be taxed under Part I

(Revised November 2013)

Under sections 216 and 217 of the ITA, non-residents may obtain a tax benefit by electing to be

taxed under Part I on certain types of income that would otherwise be subject to Part XIII tax.

Non-resident election to report rents and timber royalties as Part I income

A non-resident person that has received rent or timber royalty payments upon which Part XIII

tax has been withheld may elect under subsection 216(1) to file a Canadian income tax return,

(T1, T2, or T3 as applicable) and report the amounts in question as income subject to tax under

Part I. In such a case, the person would calculate the tax under Part I based on the net rental or

royalty income calculated as if a resident of Canada. As the net income from rental property in

particular tends to be quite low, it is generally advantageous to the non-resident owner to file an

election and report the net rental income (or loss) under Part I. The applicable return must be

filed within two years after the end of the tax year during which the amount was received or

credited.

Subsection 216(4) permits an agent or other person acting on behalf of the non-resident to elect

to withhold tax based on the net amount of rents and royalties where the non-resident has filed an

undertaking with the minister to do the following:

• file Form NR6, Undertaking to file an income tax return by a non-resident receiving rent

from real property or receiving a timber royalty, available at www.cra-

arc.gc.ca/E/pbg/tf/nr6/README.html, every year before the first rental payment is due

for the year;

• agree to file an income tax return and pay any Part I tax payable; and

• file the return within six months after the end of the year.

The International Tax Services Office (ITSO) keeps a record of all approved NR6 applications.

ITSO currently runs a default program that matches the NR6 undertakings with filed returns.

When no return is filed, ITSO will usually issue an assessment under Part XIII based on the

gross rental payments. The assessment is usually issued against the agent for failure to remit.

In certain circumstances, the Section 216 late-filing policy and/or the taxpayer relief provisions

may be applied to allow a non-resident to late-file a section 216 return. Any requests to late-file

such a return should be forwarded to the ITSO. The objective of the policy is to allow a one-time

opportunity to re-enter the system as though they had filed on time, thus avoiding the onerous

liability of the Part XIII tax. It is intended to promote voluntary compliance with Part XIII and to

encourage non-residents to come forward and correct deficiencies to comply with their legal

obligations.

13

Published May 2015

For more information, go to Income Tax Interpretation Bulletin IT393R2, Election re: tax on

rents and timber royalties non-residents, at www.cra-arc.gc.ca/E/pub/tp/it393r2/README.html,

or Communiqué ITD-02-03, Section 216 Late-Filing Policy.

Election respecting certain payments

Section 217 allows a non-resident who receives certain Canadian source income referred to in

the section as "Canadian benefits" to elect not to be taxed under Part XIII on that income. The

income is included in the computation of the non-resident's taxable income earned in Canada that

is subject to Part I tax. The non-resident may decide to elect under section 217 if the Part XIII tax

otherwise payable on the income is greater than the potential Part I tax liability. A non-resident

person's "Canadian benefits" for a tax year include superannuation or pension benefits

(CPP/QPP), death benefits, employment insurance (EI) benefits, retiring allowances, registered

supplementary unemployment benefit plan payments, registered retirement savings plan (RRSP)

payments, deferred profit sharing plan (DPSP) payments, and registered retirement income fund

(RRIF) payments.

A return under Part I must be filed within six months after the end of the calendar year in which

the income was received or credited. The person making the election is deemed to have been

employed in Canada in the year, and is deemed to have taxable income earned in Canada equal

to the greater of:

• the amount described in subparagraph 217(3)(b)(i), that is essentially the amount that

would be the non-resident person's taxable income earned in Canada if section 115

included "Canadian benefits;" and

• the amount described in subparagraph 217(3)(b)(ii), that is the non-resident person's net

income for the year, less any deductions in computing taxable income that are applicable

to the person's Canadian-source Part I income excluding the "Canadian benefits."

For more information, go to Pamphlet T4145, Electing under section 217 of the Income Tax Act,

at www.cra-arc.gc.ca/E/pub/tg/t4145/README.html.

15.3.6 Non-resident beneficiaries of trusts

(Revised November 2013)

Part XIII tax is payable on Canadian-resident estate or trust income that is allocated to non-

resident beneficiaries. The income is considered to have been allocated if it would have been

included in the person's income under Part I had the person been resident in Canada. However, if

such income is attributable to capital gains, it loses its source identity (and 50%ii2 inclusion rate)

if it is paid or allocated to a non-resident beneficiary unless the trust is a mutual fund trust.

Payments that flow through a trust, other than capital, are generally re-characterized and deemed

to be trust income, and are therefore not entitled to any exemption from Part XIII that may have

been applicable to the income prior to such re-characterization.

For a list of exceptions to this general rule and more information, see lesson 6 of learning

product TD1115-000, Part XIII Non-Resident Tax – Legislation, or go to Income Tax

Interpretation Bulletin IT465R, Non-resident beneficiaries of trusts, at www.cra-

arc.gc.ca/E/pub/tp/it465r/README.html.

15.3.7 Audit considerations relating to Part XIII tax

(Revised November 2013)

14

Published May 2015

When reviewing expense items during the audit of businesses carried on in Canada, the auditor

should pay special attention to certain high-risk accounts including royalties, interest expense,

dividend payments, and rent expense to determine the country of residence of income recipients.

In this regard, the following records and documentation should be reviewed:

• royalty agreements;

• loan agreements;

• share register; and

• lease agreements relating to physical facilities and equipment.

Other audit steps

• If available, review the master supplier list (including address details), to identify

potential non-resident payees that might be subject to withholding tax under Part XIII or

Regulation 105. Before doing this step, the auditor should be familiar with major

suppliers of inventory so the review can be restricted to suppliers outside this category.

Where potential candidates for withholdings are identified, the supplier file should be

reviewed to determine the nature and amount of the payments.

• Alternatively, audit software may be used to isolate and summarize payments by supplier

number and by the account charged in order to quantify and determine the type of

payments made to specific suppliers.

• Auditors should access the NR4 return (internally or from the taxpayer) and reconcile

audit findings to the NR slips.

• Where discrepancies are found, the International section at the TSO should be consulted

regarding adjustments that may be required.

When payments or credits to non-residents are discovered during an audit, the auditor must

ensure that the correct amount of Part XIII tax is withheld and remitted.

When auditors discover a failure to withhold in connection with this type of transaction, they

must discuss the file with the Non-Resident Section as quickly as possible to decide who will

finalize this audit issue.

For more information, go to 10.11.13, Consultation and referrals on non-residents.

15.3.8 Other Income Tax Interpretation Bulletins relating to Part XIII tax

(Revised November 2013)

• IT76R2, Exempt portion of pension when employee has been a non-resident, at www.cra-

arc.gc.ca/E/pub/tp/it76r2/README.html

• IT155R3, Exemption from non-resident tax on interest payable on certain bonds,

debentures, notes, hypothecs, or similar obligations, at www.cra-

arc.gc.ca/E/pub/tp/it155r3/README.html

• IT155R3SR, Exemption from non-resident tax on interest payable on certain bonds,

debentures, notes, hypothecs, or similar obligations, at www.cra-

arc.gc.ca/E/pub/tp/it155r3sr/README.html

15

Published May 2015

• IT303, Know-how and similar payments to non-residents, at www.cra-

arc.gc.ca/E/pub/tp/it303/README.html

• IT303SR, Know-how and similar payments to non-residents, at www.cra-

arc.gc.ca/E/pub/tp/it303sr/README.html

• IT361R3, Exemption from Part XIII tax on interest payments to non-residents, at

www.cra-arc.gc.ca/E/pub/tp/it361r3/README.html

• IT393R2, Election re: tax on rents and timber royalties non-residents, at www.cra-

arc.gc.ca/E/pub/tp/it393r2/README.html

• IT465R, Non-resident beneficiaries of trusts, at www.cra-

arc.gc.ca/E/pub/tp/it465r/README.html

• IT468R, Management or administration fees paid to non-residents, at www.cra-

arc.gc.ca/E/pub/tp/it468r/README.html

• IT494, Hire of ships and aircraft from non-residents, at www.cra-

arc.gc.ca/E/pub/tp/it494/README.html

• IT528, Transfers of funds between registered plans, at www.cra-

arc.gc.ca/E/pub/tp/it528/README.html

15.4.0 Residency – Under review

(Revised January 2014)

15.4.1 Overview

(Revised November 2013)

Subsection 2(1) of the ITA requires that every person who is resident in Canada shall pay an

income tax on taxable income for each tax year.

Subsection 2(3) stipulates that for a person who is not resident in Canada, income tax is payable

on that person's "taxable income earned in Canada for the year" if that person at any time in the

year or a previous year:

• was employed in Canada;

• carried on a business in Canada; or

• disposed of a taxable Canadian property.

Since "resident" is not defined in the ITA, reference must be made to the applicable

jurisprudence for guidance in this regard; the ITA includes the following deeming provisions

applicable to specific situations:

• Subsection 250(1) – applies mainly to individuals setting out situations where a person is

deemed to be resident in Canada for income tax purposes.

• Subsection 250(4) – describes situations where corporations are deemed to be resident in

Canada for income tax purposes.

• Subsection 250(5) – applies to corporations or individuals identifying situations where

persons are deemed not to be resident in Canada for income tax purposes.

16

Published May 2015

• Under subsection 250(5.1), a corporation that obtains articles of continuance in Canada is

deemed for Canadian income tax purposes to have been incorporated in Canada. In such

a case, a corporation previously considered to be a non-resident of Canada under

common law principles, may be deemed resident in Canada under subsection 250(4).

Specific rules are also provided in section 128.1 where a person has become a resident of Canada

(immigrated) or ceased to be a resident of Canada (emigrated) during the year.

Residency of individuals

Jurisprudence indicates that a detailed review of an individual's personal circumstances may be

required to determine residency. An individual will generally be considered a resident of Canada

if the individual habitually lives in Canada as evidenced by the location of family, personal

residence, holdings of financial and other properties, social ties, etc. Also, the permanence and

purpose of stays abroad as well as the frequency and duration of visits to Canada are factors to be

considered.

For more information, go to Income Tax Folio S5-F1-C1, Determining an individual's residence

status, at www.cra-arc.gc.ca/tx/tchncl/ncmtx/fls/s5/f1/s5-f1-c1-eng.html.

If requested, the International Tax Services Office (ITSO) will make a residency determination

for a taxpayer, who will be asked to complete Form NR74, Determination of Residency Status

(Entering Canada), available at www.cra-arc.gc.ca/E/pbg/tf/nr74/README.html, or Form

NR73, Determination of Residency Status (Leaving Canada), available at www.cra-

arc.gc.ca/E/pbg/tf/nr73/README.html.

Residency determinations are filed according to account number at the ITSO and copies can be

obtained for specific individuals. Alternatively, if a determination has not been made, the auditor

may use the NR74 or NR73 questionnaires as a guide to determine whether an individual is

resident in Canada.

Individuals deemed resident

In addition to common law criteria, subsection 250(1) specifically deems a person to be a

resident of Canada in certain circumstances including those persons (and their children and

dependents) who were members of the Canadian forces, ambassadors, provincial agents-general

or other diplomatic staff living abroad, Canadians working abroad under a prescribed

international development assistance program, and more particularly, persons who sojourned in

Canada for 183 days or more in the year.

An individual that sojourns, (that is, is temporarily present, for one or more periods in Canada

totalling 183 days or more in any calendar year) is deemed to be resident in Canada for the entire

year. For this to occur, the individual must also be a resident of another country during those

same time periods. Consequently, a resident of Canada who becomes a non-resident in the last

half of a calendar year cannot be considered a resident of Canada for the entire year.

However, if an individual emigrates to another country sometime during the first half of a

calendar year, or in a previous year, but returns often enough to have "sojourned" in Canada for

the required 183 days or more during the year and the individual was otherwise not a resident,

the individual would be deemed to be resident in Canada for the entire year.

Individuals deemed to be non-resident by virtue of a treaty

17

Published May 2015

Where both Canada and another country consider a person resident of their respective countries,

the tax treaty, if any, with that country will usually provide a tiebreaker rule that determines, for

purposes of the treaty, the country in which the person is resident.

To ensure that a person's status in Canada is consistent with the status accorded under the treaty,

subsection 250(5) treats the person in such a case as a non-resident for all purposes of the ITA if

that person is considered a resident of the other country under the treaty.

15.4.2 Residency of corporations

(Revised November 2013)

If a corporation is not incorporated in Canada, common law has generally established that a

corporation is resident in the country in which its "central management and control" is exercised

as evidenced by such factors as where the Board of Directors meets and holds its meetings,

where the officers and directors reside etc.

By virtue of the deeming provisions in subsection 250(4) of the ITA, a corporation is generally

deemed to be resident in Canada throughout a tax year if it was incorporated in Canada after

April 26, 1965. In the case of corporations incorporated before that date, if they are otherwise

incorporated in Canada and if they are otherwise resident under common law principles or

carried on business in Canada are also deemed to be resident. Certain foreign business

corporations incorporated before April 9, 1959 are also deemed resident in Canada under specific

circumstances.

For more information, see paragraphs 15 and 16, "Corporate Residence," in Income Tax

Interpretation Bulletin IT391R, Status of corporations, at www.cra-

arc.gc.ca/E/pub/tp/it391r/README.html.

15.4.3 Trusts

(Revised November 2013)

As stated in Income Tax Interpretation Bulletin IT447, Residence of a trust or estate, at

www.cra-arc.gc.ca/E/pub/tp/it447/README.html, "residence of a trust or estate is a question of

fact to be determined according to the circumstances in each case. However, a trust is generally

considered to reside where the trustee, executor, administrator, heir or other legal representative

who manages the trust or controls the trust assets resides."

15.4.4 Immigration – Becoming resident in Canada

(Revised November 2013)

Subsection 128.1(1) of the ITA provides rules that apply when a taxpayer becomes resident in

Canada. The "particular time" at which residence occurs is very important as the events that are

deemed under this subsection to take place are timed by reference to that moment. The events

include the beginning and ending of an immigrating corporation's tax years and fiscal periods as

well as dispositions and re-acquisitions of property owned by an immigrant.

Determining the particular time when a taxpayer became resident may be problematic if, for

example:

• An individual commuted between residences and worked in two jurisdictions for a period

of time before gradually becoming rooted in one.

18

Published May 2015

• The management of a corporation is split between two jurisdictions both in terms of the

location of meetings and the residence of management employees.

A review of jurisprudence may be helpful in both cases.

A corporation will generally be considered to have become resident in Canada if:

• It was incorporated outside Canada and was managed from that outside jurisdiction but

restructures its operations such that the central management and control is now exercised

within Canada.

• It obtains articles of continuance in Canada and is deemed for Canadian tax purposes

under subsection 250(5.1) to have been incorporated in Canada.

In such a case, a corporation previously considered to be a non-resident of Canada under

common law principles, may be deemed resident in Canada under subsection 250(4).

Income tax effects of becoming a resident in Canada

When a corporation or trust immigrates to Canada, paragraph 128.1(1)(a) deems its tax year to

have ended immediately before the "particular time" of immigration and deems a new tax year to

have begun at the "particular time" of immigration. The immigrating corporation or trust may

select a new fiscal period at that time.

Immigrating corporations or trusts are deemed under paragraph 128.1(1)(b), to have disposed of

each property owned immediately before the time of immigration for proceeds equal to the

property's fair market value (FMV) and, under paragraph 128.1(1)(c), to have reacquired each

such property at a cost equal to the proceeds of disposition.

The same rules apply to individuals becoming resident in Canada except that certain properties

described in subparagraphs 128.1(1)(b)(i) through (v) are exempted from the provisions.

For income tax purposes, the deeming provisions give rise to a gain or loss that is considered to

have been realized during the year that ended at the time of immigration. Accordingly, since the

taxpayer is a non-resident throughout that year, section 115 applies and only gains on

dispositions of taxable Canadian property will generally be subject to income tax.

In addition, the reacquisition of each previously owned property at FMV is reflected in the

immigrating taxpayer's property valuations for purposes of capital cost allowance (CCA),

inventory, and computation of capital gain or loss on future disposition.

A "paid-up capital adjustment" under subsection 128.1(2) may also be required to reflect the

deemed acquisitions.

For more information, go to Pamphlet T4055, Newcomers to Canada, at www.cra-

arc.gc.ca/E/pub/tg/t4055/README.html.

15.4.5 Emigration – Ceasing to be resident in Canada

(Revised November 2013)

An individual will generally be considered as having ceased to be resident in Canada when that

individual habitually lives in some other country as evidenced by the location of family, personal

residence, holdings of financial and other properties, social ties etc.

A corporation may be considered to have emigrated from Canada if:

19

Published May 2015

• It restructures its operations such that the central management and control is no longer

exercised within Canada and the corporation is not otherwise deemed to be resident in

Canada under subsection 250(4) of the ITA.

• It obtains articles of continuance in a foreign jurisdiction and under subsection 250(5.1),

is deemed for Canadian income tax purposes to have been incorporated in that

jurisdiction. In such a case, a corporation previously deemed resident in Canada under

subsection 250(4), would no longer qualify.

• It becomes a resident in another country and not resident in Canada under a tax treaty

with the other country. Such a corporation is deemed not to be resident in Canada in

accordance with subsection 250(5).

• It is deemed to have ceased to be resident in Canada in accordance with subsection

128.2(2) by merging with another corporation to form a corporation not resident in

Canada.

In addition, a person who is resident in Canada is deemed under subsection 250(5), to be a non-

resident of Canada if such person is a resident of another country and not of Canada under a tax

treaty with that country.

Income tax effects of ceasing to be a resident in Canada

When a corporation or trust emigrates from Canada, paragraph 128.1(4)(a) deems its tax year to

have ended immediately before the particular time of emigration and deems a new tax year to

have commenced at the particular time of emigration. The emigrating corporation or trust may

select a new fiscal period.

A corporation or trust that ceases to be resident in Canada is deemed by paragraph 128.1(4)(b) to

have disposed of all of its property at the time immediately before the deemed year end, for

proceeds equal to the property's FMV. Where the taxpayer is an individual, subparagraphs

128.1(4)(b)(i) through (vi) exempt certain types of property from the deemed disposition.

Generally, Canada has a continuing right to tax these properties upon their ultimate disposition.

Properties include taxable Canadian property, inventory used in a Canadian business, rights to

receive pension or similar payments and employee stock options that are subject to section 7.

In addition to any Part I tax that may result from the deemed disposition of property, section

219.1 imposes an additional 25% tax under Part XIV (commonly referred to as the "departure

tax") when a corporation ceases to be resident in Canada. This tax is levied on the difference

between the FMV of the corporation's property and the total of its paid-up capital and debts.

Applicable tax treaty provisions may reduce the rate of tax.

Emigrant individuals, other than trusts, may elect under subparagraph 128.1(4)(b)(iv) not to be

treated as having disposed of capital property provided that adequate security is given for the tax

that would otherwise have been payable. Under paragraph 128.1(4)(e), such property is treated as

taxable Canadian property until it is disposed of or the taxpayer once again becomes resident in

Canada. Section 114 provides rules for computing the taxable income of an individual who is

resident in Canada for a period or periods in a tax year, and who is non-resident for the rest of

the year.

For more information, go to Tax Guide T4056, Emigrants and income tax, at

www.cra-arc.gc.ca/E/pub/tg/t4056/README.html.

20

Published May 2015

15.4.6 For future use

15.4.7 Audit considerations

(Revised November 2013)

Residency of individuals

The term "resident" is not defined in the ITA. The Courts have held that an individual is resident

in Canada for tax purposes if Canada is the place where, in the settled routine of life, the

individual regularly, normally or customarily lives. In making this determination, all of the

relevant facts in each case must be considered. In the case of individuals, useful documents for

review include:

• historical T1 filings;

• vehicle registrations and insurance premium billings;

• personal residence property tax bills;

• personal residence utility bills;

• health insurance premium statements or provincial health card;

• credit card statements; and

• lease agreements for vehicle or apartment.

In addition, the auditor should note the spouse or common law partner's place of employment

and corroborate the information with T1 filings.

Where deemed residency under the 183-day sojourning rule is in question, the auditor may verify

the time spent in Canada by reference to:

• hotel bills paying particular attention to check-in/check-out dates;

• airline tickets noting the dates of arrival and departure;

• the rental period in automobile and apartment rental agreements; and

• meeting and conference agendas, consulting agreements or other correspondence

specifying the length of time.

15.5.0 Foreign-based information and documentation – Under review

(Revised January 2014)

15.5.1 Overview

(Revised November 2013)

Section 231.6 of the ITA came into effect on September 13, 1988. It was implemented as a result

of difficulties encountered when information in the possession and control of non-residents,

particularly those residing in countries where no treaty provisions for exchange of information

apply, was not voluntarily provided by the Canadian taxpayer and was not obtainable by the

minister. More specifically, the CRA was experiencing problems with taxpayer compliance

where cross-border transactions and transfer pricing were involved.

The section was introduced to enable the minister to serve notice on any Canadian residents or

non-residents carrying on business in Canada, to require that they provide foreign-based

information or documentation that may be relevant to the administration or enforcement of the

21

Published May 2015

ITA. The section applies to information and documentation available or located in all foreign

countries not only with respect to treaty partners.

Section 231.6 is an extension of the powers given to the minister under section 231.2 that

requires any person to provide any information or document to specifically include information

and documents located outside of Canada. There is no stipulation that section 231.6 is operative

only after section 231.2 has failed. Situations may arise where certain foreign-based information

is available in Canada (or copies thereof). In such situations, a decision will need to be made as

to whether to issue a requirement under section 231.2 or 231.6. The ultimate decision will

depend on the circumstances. It is advisable that TSO staff contact their regional international

tax advisor to discuss the case.

The law is broad enough to allow service of a requirement on third parties such as with respect to

information held abroad by an unrelated party. However, the CRA intends to use such powers

only in exceptional circumstances; Headquarters, International Tax Directorate should be

involved in any such request.

The authority to serve a requirement under section 231.6 has been delegated to the Directors of

the TSO and to certain Assistant Directors and Managers. This delegation of authority is

contained in the document, "Delegation of the Minister of National Revenue's Powers and

Duties," that was signed on September 27, 1999. It supersedes the delegation of the minister's

powers and duties under Section 900 of the Income Tax Regulations.

Where the requested information or document is located in a treaty country with which an

Exchange of Information provision is available, the CRA has the option of proceeding by way of

a specific request for information from that treaty partner. The circumstances of each case will

dictate which route the CRA should take to obtain the information.

15.5.2 Potential conflict with foreign laws

The ITA does not include a specific reference to foreign non-disclosure laws. Including such a

clause in the legislation could place a person in a conflict position where that person would have

to break the foreign law to comply with Canadian law.

For example, in the 1985 Supreme Court of Canada case Spencer v. The Queen, the issue was

whether a Canadian resident and citizen, who had previously been a manager of a Bahamian

branch of a Canadian bank, could be compelled to testify for the Crown in a prosecution under

the ITA against a client of the bank. The appellant contended that to do so would make him

liable for prosecution under a Bahamian statute and that this would be an infringement of his

rights under section 7 of the Canadian Charter of Rights and Freedoms. The court held that

section 7 of the Charter did not apply because the infringement of Mr. Spencer's liberty or

security, if any, did not result from the operation of the Canadian law, but solely from the

operation of a Bahamian law. To allow Mr. Spencer to refuse to give evidence would permit a

foreign country to frustrate the administration of justice in Canada.

Although a foreign jurisdiction may forbid disclosure of certain information in that jurisdiction,

this prohibition should not stop the CRA from issuing a requirement under section 231.2 of the

ITA for that information in Canada and should not preclude the taxpayer involved from

providing such information available in Canada for Canadian income tax purposes. Where the

requirement is served on a resident who has to ask an employee of a non-resident affiliate to

obtain and disclose the required information, the situation is much more difficult.

22

Published May 2015

Situations are examined on a case-by-case basis.

15.5.3 Definition of "foreign-based information or document"

(Revised November 2013)

"Foreign-based information or document" is defined by subsection 231.6(1) of the ITA as being

any information or document that is available or located outside Canada and that may be relevant

to the administration or enforcement of the ITA including the collection of any amount payable

under the ITA by any person.

The term "document" includes money, a security and a record. The term "record" is defined in

section 248 to include an account, agreement, book, chart or table, diagram, form, image,

invoice, letter, map, memorandum, plan, return, statement, telegram, voucher, and any other

thing containing information, whether in writing or in any other form.

With respect to the application of the transfer pricing rules contained in section 247, the general

principles on existing documentation in subsection 247(4) also apply to foreign-based

documentation. This means that the taxpayer's documentation may include foreign-based

information or documents to the extent that it is relevant in determining arm's length prices.

For example, in determining what constitutes a reasonable arm's length price for inter-company

transactions, it may be necessary to obtain information concerning comparable uncontrolled

prices, costs incurred to produce a product or supply a service, resale margins derived by a

distributor, or profitability of a specific operation from a foreign jurisdiction. This information

may be obtained from offshore studies that might have been undertaken and used in the

determination of the transfer price.

The documentation requirements of subsection 247(4) are inclusive, but not prescriptive. The

taxpayer is required to make a reasonable effort to provide information and penalty provisions

are in place to ensure that complete and accurate information is maintained. Section 247 may be

a strategic option to section 231.6 for transfer pricing.

15.5.4 Requirement to provide foreign-based information

(Revised November 2013)

Notwithstanding any other provision of the ITA, the minister may, by notice, serve requirements

for foreign-based information or documents in person, by registered mail or certified mail on a

person resident in Canada or a non-resident person carrying on business in Canada.

If there is a question as to whether a particular entity is carrying on business in Canada, the

requirement may still be issued. The onus will be on the taxpayer to convince the court that the

taxpayer is not carrying on business, and therefore not subject to the requirement.

Subsection 231.6(3) of the ITA sets out a list of what must be included in a notice/requirement

referred to in subsection 231.6(2). The notice must contain:

• a reasonable time period of at least 90 days for compliance. In all cases, a reasonable time

period has to be given according to the type of documents requested and their location;

• a clear description of the information or documentation being sought in order to ensure

that the person served with the requirement can determine with reasonable certainty what

must be provided. The description should include the type of document, for example

“itemized invoice,” or describe the contents as precisely as possible. A description that is

23

Published May 2015

too general may allow the person served with the requirement to either selectively

provide only the information or documents that are advantageous to the person’s case, or

apply to have the requirement varied or set aside. This is also relevant when determining

substantial compliance under subsection 231.6(8).

• the consequences under subsection 231.6(8) for failure to comply.

It is advisable to add a reference as to where and to whom the information should be provided.

When preparing a requirement under section 231.6, it is advisable to contact the regional

international tax advisor to discuss the case. To promote consistency a template is provided. For

more information, go to Appendix A-10.1.19, Requirement for foreign-based information

(Combined).

It is also strongly recommended that any officer preparing a requirement consult with Justice

legal counsel to ensure that the requirement is complete and accurate in all respects and to avoid

potential problems that could result in rendering the requirement invalid.

For example, errors have occurred in something as seemingly simple as the computation of the

90-day period. Note that subsection 27(1) of the Interpretation Act states that where there is a

reference to “at least” a number of days between two events, the days on which the events occur

are excluded from the calculation. With respect to serving a requirement, if the events include

the date the requirement is served, and the date the documents are required to be provided, then a

period of 92 days would be calculated as the time limit. If the requirement is worded to the effect

that the taxpayer must comply before the ninety-first day following the day of the service of the

requirement, then the requirement will not meet the provision of paragraph 231.6(3)(a) of the

ITA and could be submitted by the taxpayer to a court for review.

15.5.5 Judicial review of foreign information requirement

(Revised November 2013)

Where a notice for foreign-based information is served, subsection 231.6(4) of the ITA permits

the person served with the notice to apply to a judge for a review of the requirement. Application

must be made within 90 days of the date the notice is served.

For purposes of this review, a judge includes a judge of a superior court having jurisdiction in the

province where the matter arises or a judge of the Federal Court.

Subsection 231.6(5) sets out the powers of a judge on hearing an application for review under

subsection 231.6(4). It is within a judge's jurisdiction to confirm or vary the requirement, or to

set aside the requirement if it is considered to be unreasonable.

If, for example, the time period set forth in the notice was not reasonable in the circumstances,

the judge could increase the time period, vary the description of the information or documents

being sought, or set aside the requirement if the judge is satisfied that it is unreasonable.

Subsection 231.6(6) provides that for purposes of paragraph 231.6(5)(c), a requirement is not to

be considered unreasonable where the foreign-based information or document being sought is

under the control of, or available to, a related non-resident person, merely because that person is

not controlled by the person served with the notice under subsection 231.6(2). This provision is

intended to prevent a Canadian taxpayer from being excused from providing information simply

by saying it does not have the power to force its parent or sister corporation to provide it. Apart

24

Published May 2015

from this specific limitation, the reasonableness of a requirement in any situation will depend on

the particular circumstances.

A requirement could be held to be unreasonable where the information or document is under the

control of or available to an unrelated non-resident person, such as a third party.

Subsection 231.6(7) provides that the time that elapses between a person's application for review

of a requirement by a judge and its final disposition will not be included in computing the time

permitted for production of the information or document as set out in the notice (that is, if the

taxpayer applies for a review, the 90-day time limit stops until the application is decided).

In addition, the review will extend the statutory time limit (currently six or seven years under

subparagraph 152(4)(b)(iii)) for making assessments or reassessments relating to cross-border

transactions between a taxpayer and a non-arm's length non-resident person.

The six or seven-year limit applies only to the extent that the reassessment relates to the

transaction with the non-resident person. The amendment to subsection 152(4) is effective for

transactions entered into, payments made and reimbursements received after April 27, 1989.

15.5.6 Consequence of failure

(Revised November 2013)

Under subsection 231.6(8) of the ITA, failure to provide substantially all the documents or

information covered by a notice allows the minister to bring a motion to prohibit the introduction

into evidence of any such information or documentation in an appeal or other civil proceeding

relating to the ITA. For example, if a person provides five out of ten documents required, that

person may be prohibited from introducing into evidence any of the ten documents required,

including those that were provided to the minister. Therefore, it is important to make the

requirement as comprehensive and specific as possible in order to prevent taxpayers from

selectively providing only the information or documents that are advantageous while refusing to

provide the information or documents that could assist the minister in arriving at a proper

assessment.

It is not the quantity of the documents supplied, but rather their relevance that should be taken

into account in assessing whether there has been substantial compliance. The determination will

ultimately be made at the court proceeding during which the person served with the notice

wishes to introduce the documents as evidence.

Although not required by any provision of the ITA, in the appropriate circumstances the

possibility of prosecution under section 238 could also be set out in the requirement. Any person

failing to substantially comply with the requirement could be guilty of an offence under section

238 and liable to fines and/or imprisonment in addition to any penalty otherwise provided (that

is, non-admissibility).

Subsection 238(1) deals with offences and provides that failure to comply with "any of sections

230 to 232" is an offence, subject on summary conviction to a fine from $1,000 to $25,000, or

imprisonment for a term of up to 12 months, or both. Since the main objective of serving the

requirement under subsection 231.6(2) is to obtain the foreign-based information and documents,

rather than render them inadmissible, it may be more effective to use the provisions of section

238 and seek a fine and a compliance order under subsection 238(2). However, prosecution steps

will not be automatic for non-compliance. In the rare circumstance that prosecution under section

238 is being contemplated by the TSO where the taxpayer has failed to substantially comply with

25

Published May 2015

the requirement, the Director of the TSO may wish to consult with Headquarters, International

Advisory Services Section, International Tax Division, International and Large Business

Directorate and with Justice counsel.

In addition, subsection 247(4) deems that taxpayers who do not assemble basic documentation

by their filing date (documentation-due date) have not made reasonable efforts for purposes of

the penalty provisions contained in subsection 247(3). Therefore, the provisions in section 247

that relate to contemporaneous documentation and penalties, although not the primary focus in

relation to issuing requirements for foreign-based information, may be used as an alternative

means of obtaining (foreign-based) information or documentation with respect to cross-border

transactions between related parties.

15.5.7 Documentation submitted after the requirement due date

(Revised November 2013)

If a taxpayer submits sufficient documentation (such that the standard of substantial compliance

contained in subsection 231.6(8) of the ITA is met), but it is submitted after the due date

stipulated in the requirement, it may be advisable to accept the documentation, since the

objective of issuing the requirement was to obtain such information.

If the documentation received after the due date is ignored, and in accordance with subsection

231.6(8) precluded from evidence, the judge may not support this position. In addition, the

information may be provided to the Appeals Branch if the taxpayer appeals the reassessment or it

may be presented by the other tax jurisdiction under the exchange of information provisions if

the case goes to Competent Authority. Therefore, every available avenue (including for example,

treaty requests) should be pursued to obtain information at the audit stage and documentation

should be accepted even if it is submitted late. Each situation must be examined on a case-by-

case basis.

For example, the taxpayer has made every effort to obtain the requested information, but due to

circumstances beyond the taxpayer's control, the information is not obtained within the time

limits set out in the requirement. When the information is subsequently obtained by the taxpayer

and provided to the CRA, the minister should accept it, even if the due date has passed.

There may be circumstances where it is reasonable not to accept the documentation. For

example, where the taxpayer is clearly not co-operating and two years have gone by with only

minimal compliance, it may be reasonable not to accept information that is submitted after the

due date. It is recommended that TSO staff contact their regional international tax advisor to

discuss the case.

Although it may be contrary to the spirit of section 231.6, there are no explicit provisions

contained in the section to prevent the taxpayer from providing any information/documentation

to the Appeals Branch for examination, even if the taxpayer did not comply with the requirement

at the audit stage. However, when the required information is provided after the due date,

Appeals can bring a motion under subsection 231.6(8) to prohibit the taxpayer from using that,

or any other information in court on the grounds that the taxpayer provided incomplete

information and/or did not provide the information by the stipulated due date. While Appeals

must examine the information, no matter if it is submitted past the due date, they are not obliged

to take the information into account when determining whether or not to uphold the

reassessment.

26

Published May 2015

Section 231.6 is not limited to information available to related non-residents. However, if the

requested information is available only to unrelated third parties and it is not provided within the

time frame specified in the requirement, the question is whether the prohibition from using the

information in court would apply if the taxpayer was initially unsuccessful in obtaining the

documentation after exercising due diligence, but subsequently obtains the information. This will

have to be determined on a case-by-case basis.

For example, this situation may be encountered when dealing with licensors, licensees, suppliers

or customers. It is possible that a requirement could be held to be unreasonable where the