Embed Size (px)

Citation preview

Gaining A New Perspective Or History Repeating Itself

Ganpat Mani, President & CEO

1

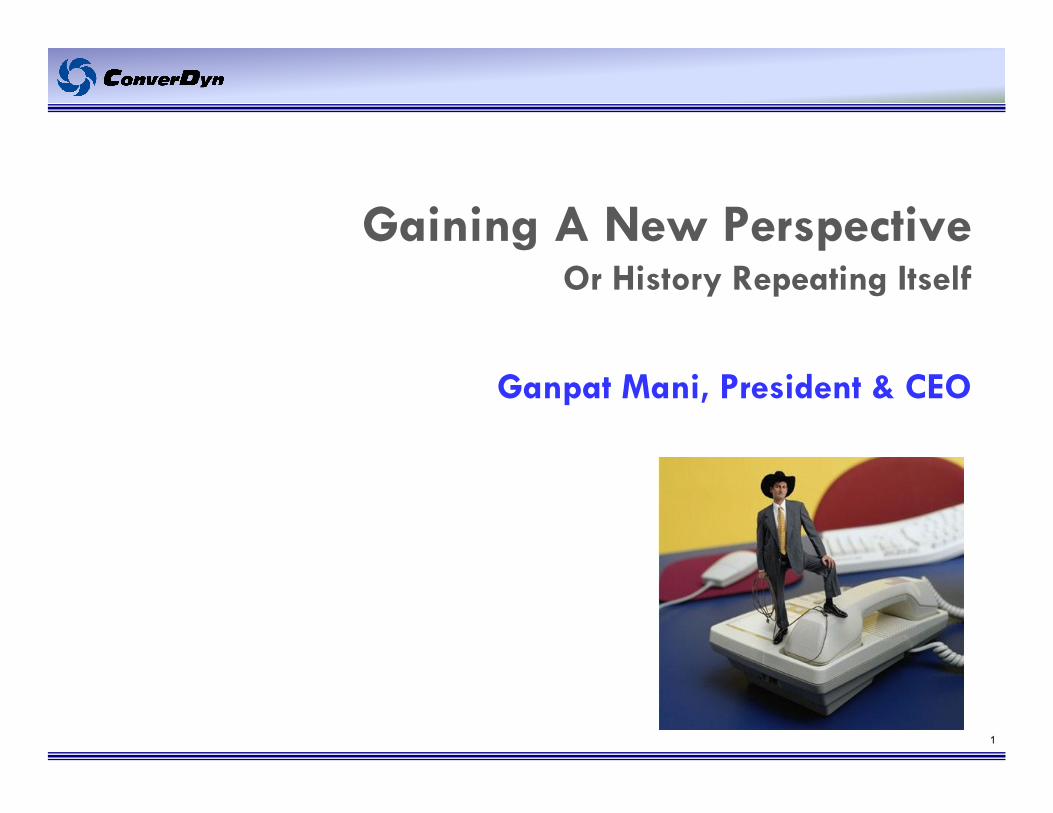

C t M tComponent Movement

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Conversion U308 SWU

2005 2006 2007 2008 2009

2Source: Tradetech

U & SWU: upward movement. Conversion: painfully flat!

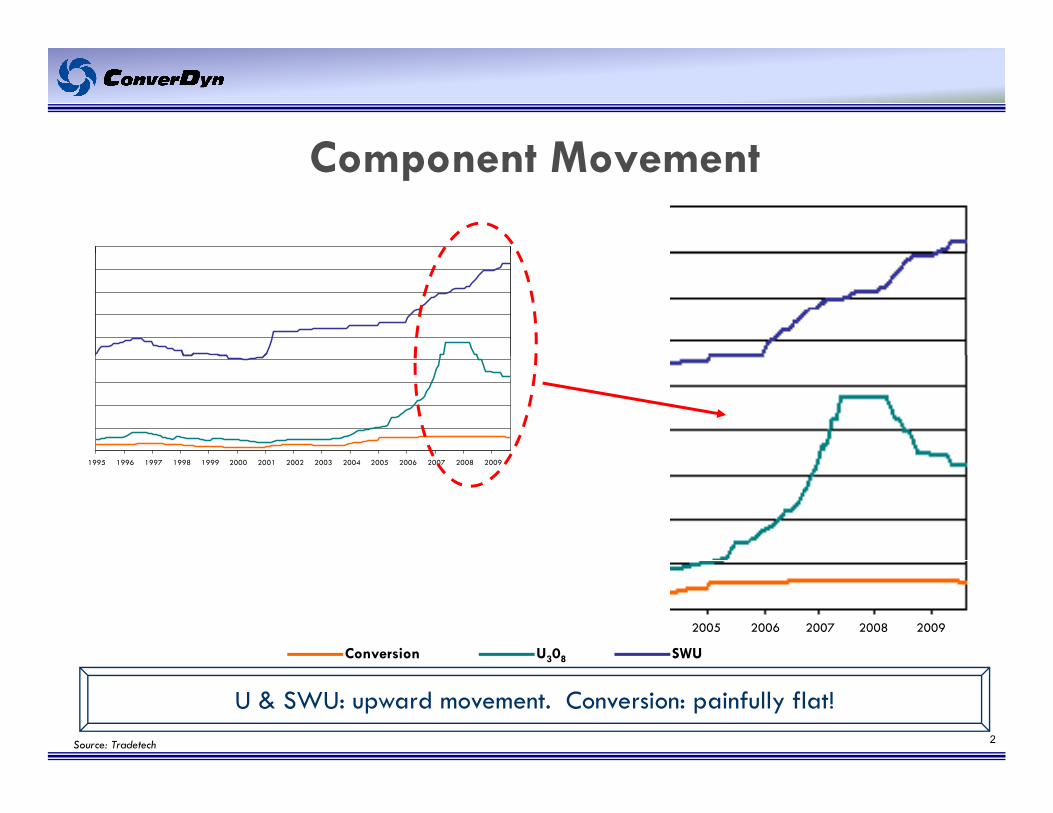

Conversion Market Movement – Phase 1

$7 $14Actual $ per kgU as UF6

Conversion Market Movement Phase 1Historical vs Current

$5

$6

$10

$12

$3

$4

$6

$8

$1

$2

$3

$2

$4

$6

1998 – USECPrivatization

1995 – First Ru HEU reaches market

2000 – USEC Inventory Committed

$0

$1

$0

$2

1992 2000 2002 to Present

(1.8 M kgU as UF6)

1992-2000 2002 to Present

3Source: TradeTech, NA Spot Price Jan 1992-Feb 1996, NA Long Term Price Feb 1996-present

Large scale entry of secondary supplies

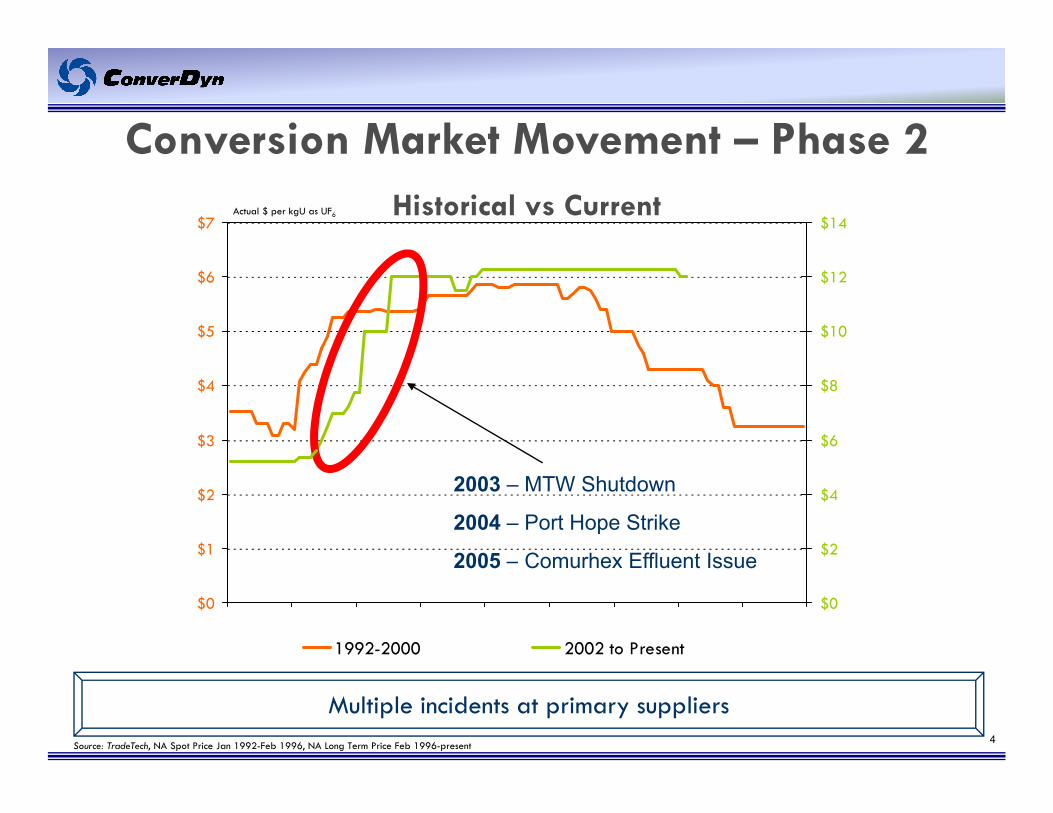

Conversion Market Movement – Phase 2

$7 $14Actual $ per kgU as UF6

Conversion Market Movement Phase 2Historical vs Current

$5

$6

$10

$12

$3

$4

$6

$8

$1

$2

$2

$42003 – MTW Shutdown

2004 – Port Hope Strike

2005 Comurhex Effluent Issue

$0 $0

1992-2000 2002 to Present

2005 – Comurhex Effluent Issue

4Source: TradeTech, NA Spot Price Jan 1992-Feb 1996, NA Long Term Price Feb 1996-present

Multiple incidents at primary suppliers

Russian SupplyEffect of Russian HEU Supply on

Conversion Industry: PAST –

Russian Supply

• Reduced demand for primary conversion

• Reduced capital investment by primary converters

• BNFL announced plan to exit

•One way trade

Effect of Russian HEU and Commercial Supply on Conversion Industry: PRESENT –

• Increased HEU uncertainty post 2013 – if, when, how much?

–Domenici Amendment impactp

•Russian penetration of current and future markets

–Ex: Japan, China, India, US

U t i t i i k f it l i t t b i

5

• Uncertainty increases risk of capital investment by primary converters

•Still one way trade

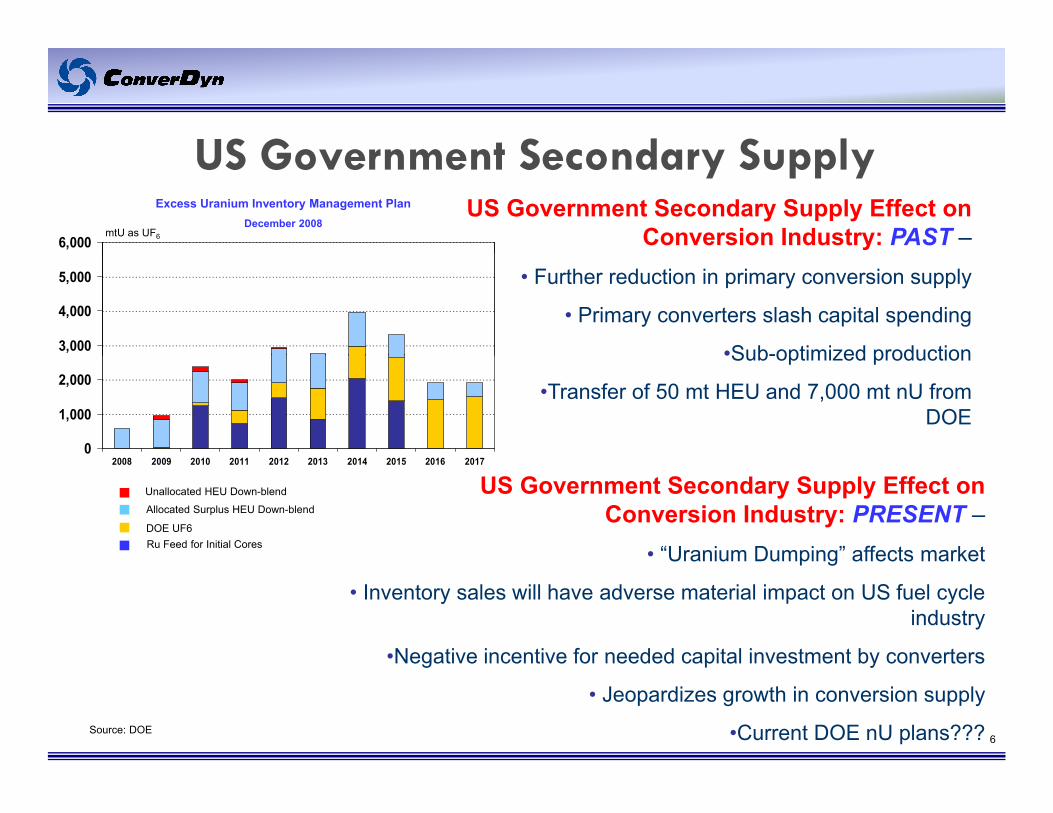

US Government Secondary SupplyUS Government Secondary Supply Effect on

Conversion Industry: PAST –Excess Uranium Inventory Management Plan

December 2008mtU as UF6

US Government Secondary Supply

6,000

• Further reduction in primary conversion supply

• Primary converters slash capital spending

•Sub-optimized production3,000

4,000

5,000

•Sub-optimized production

•Transfer of 50 mt HEU and 7,000 mt nU from DOE

0

1,000

2,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

US Government Secondary Supply Effect on Conversion Industry: PRESENT –

• “Uranium Dumping” affects market

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Unallocated HEU Down-blend

Allocated Surplus HEU Down-blend

DOE UF6Ru Feed for Initial Cores Uranium Dumping affects market

• Inventory sales will have adverse material impact on US fuel cycle industry

•Negative incentive for needed capital investment by converters

6

Negative incentive for needed capital investment by converters

• Jeopardizes growth in conversion supply

•Current DOE nU plans???Source: DOE

Supply DisruptionsSupply Disruptions Effect on Conversion

Industry: PAST –

Supply Disruptions

• Demonstrated that primary production is fragile

• Depletion of inventories

• Supplier incidents raised market awareness of needSupplier incidents raised market awareness of need for capital improvements

Supply Disruptions Effect on Conversion Industry: PRESENT –

•Inventories held as UF66

• Ample supply

• Some market recognition of need for capital improvements

7

p

•Insufficient incentives offered by market for supply growth

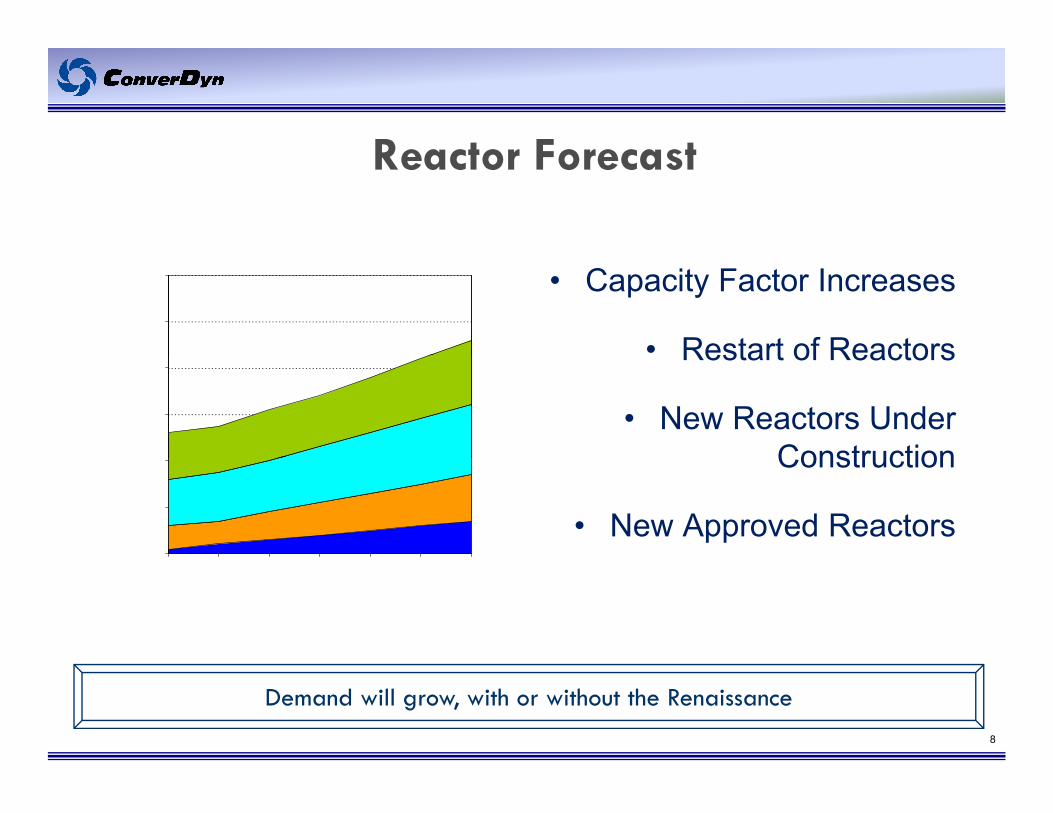

Reactor ForecastReactor Forecast

• Capacity Factor Increases

• Restart of Reactors50

60

Restart of Reactors

• New Reactors Under Construction20

30

40

Construction

• New Approved Reactors0

10

20

2009 2011 2013 2015

8

Demand will grow, with or without the Renaissance

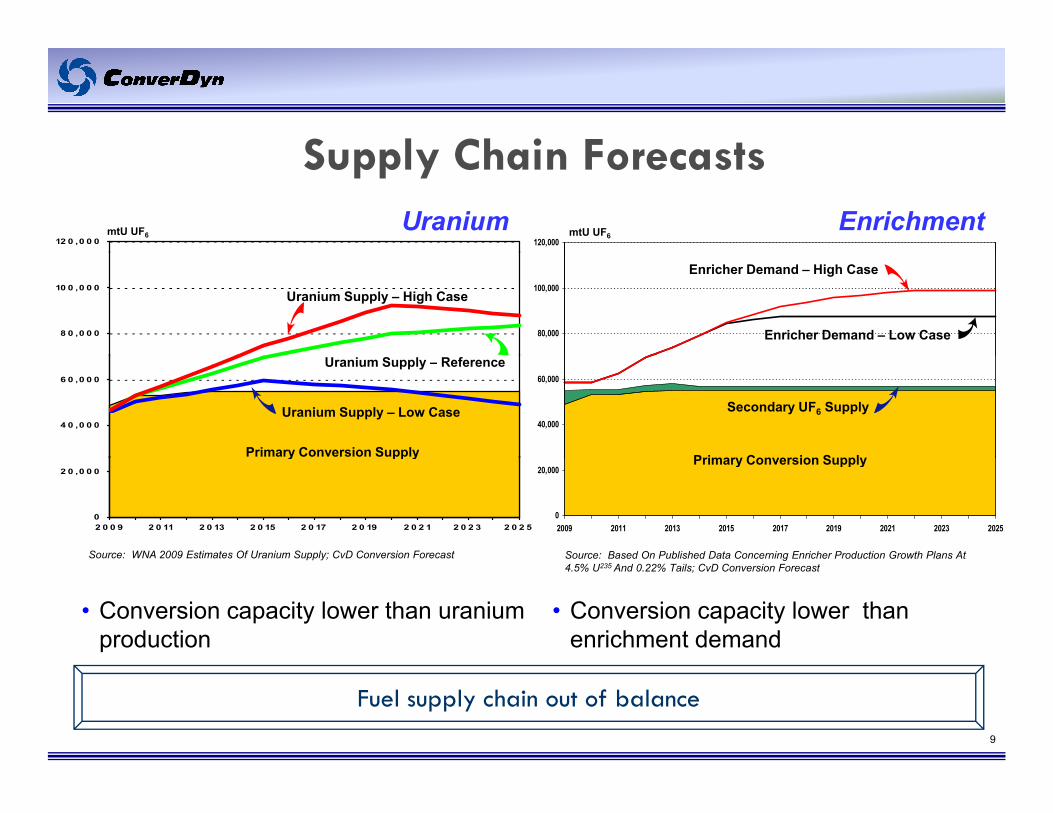

Supply Chain Forecasts

12 0 ,0 0 0

Uranium Enrichment120,000

mtU UF6 mtU UF6

Supply Chain Forecasts

8 0 ,0 0 0

10 0 ,0 0 0Uranium Supply – High Case

80,000

100,000

Enricher Demand – Low Case

Enricher Demand – High Case

4 0 ,0 0 0

6 0 ,0 0 0

Uranium Supply – Low Case40,000

60,000

Primary Conversion Supply

Secondary UF6 Supply

Primary Conversion Supply

Uranium Supply – Reference

0

2 0 ,0 0 0

2 0 0 9 2 0 11 2 0 13 2 0 15 2 0 17 2 0 19 2 0 2 1 2 0 2 3 2 0 2 50

20,000

2009 2011 2013 2015 2017 2019 2021 2023 2025

y pp y Primary Conversion Supply

Source: WNA 2009 Estimates Of Uranium Supply; CvD Conversion Forecast Source: Based On Published Data Concerning Enricher Production Growth Plans At

• Conversion capacity lower than enrichment demand

• Conversion capacity lower than uranium production

g4.5% U235 And 0.22% Tails; CvD Conversion Forecast

9

Fuel supply chain out of balance

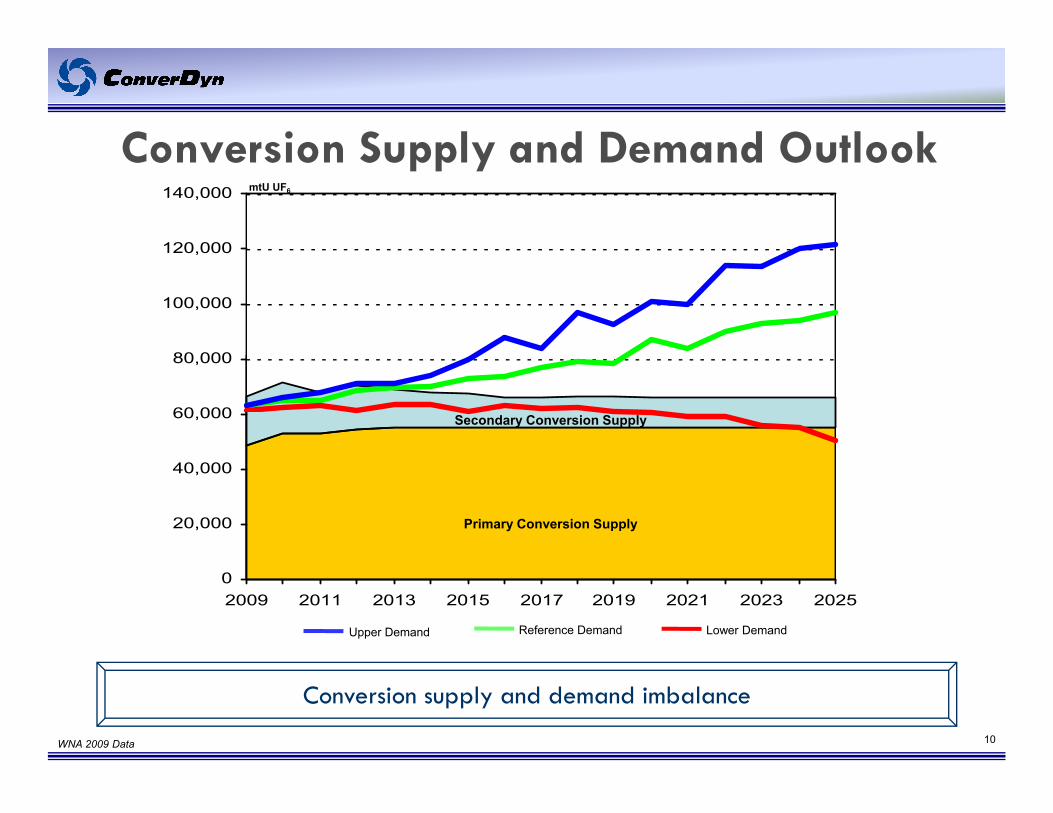

Conversion Supply and Demand OutlookConversion Supply and Demand Outlook

120,000

140,000 mtU UF6

80 000

100,000

120,000

60,000

80,000

Secondary Conversion Supply

20,000

40,000

Primary Conversion Supply

02009 2011 2013 2015 2017 2019 2021 2023 2025

Lower DemandReference DemandUpper Demand

WNA 2009 Data

Conversion supply and demand imbalance10

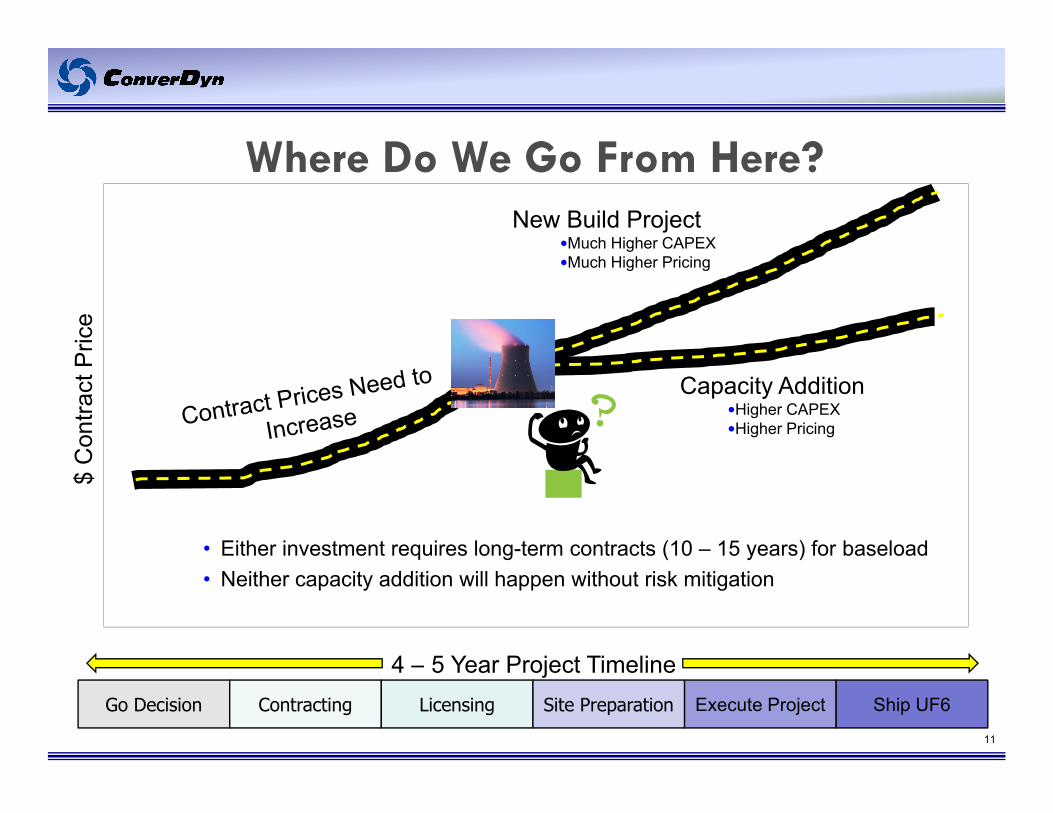

Wh D W G F H ?New Build Project

•Much Higher CAPEX

Where Do We Go From Here?

•Much Higher Pricing

Pric

eC

ontra

ct P

Capacity Addition•Higher CAPEX•Higher Pricing

$ C

• Either investment requires long-term contracts (10 – 15 years) for baseload

4 5 Year Project Timeline

• Neither capacity addition will happen without risk mitigation

11

Go Decision Contracting Licensing Site Preparation Execute Project Ship UF6

4 – 5 Year Project Timeline

Capacity Addition Or New Build

Conversion Expansion: Maintain

Capacity Addition Or New Build

Existing Plants –• Increased capital investment for maintenance

reliability and performance improvements

• Added staff and management positions

• Some support through direct customer participation

Conversion Expansion: New Build –•Stronger market signals needed

• Shared risk and margin protection

• Government intentions must be clear and firm

12

• Government intentions must be clear and firm

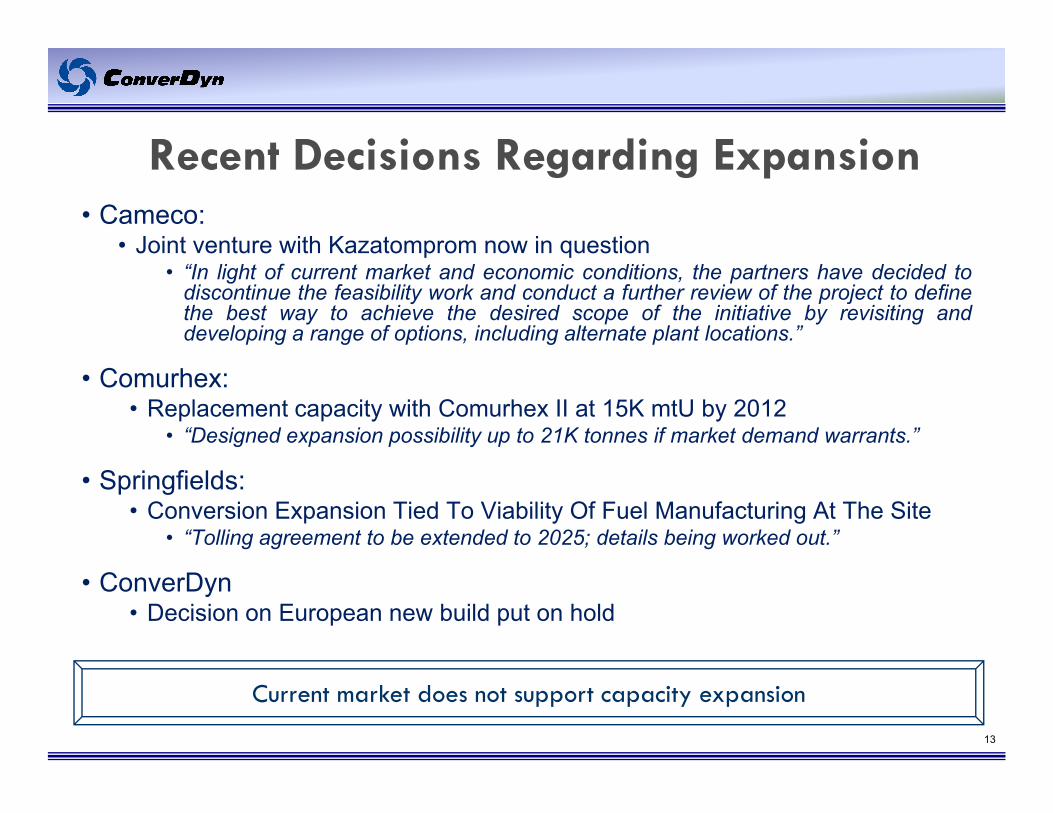

Recent Decisions Regarding ExpansionRecent Decisions Regarding Expansion• Cameco:

• Joint venture with Kazatomprom now in questionJoint venture with Kazatomprom now in question• “In light of current market and economic conditions, the partners have decided to

discontinue the feasibility work and conduct a further review of the project to definethe best way to achieve the desired scope of the initiative by revisiting anddeveloping a range of options, including alternate plant locations.”

• Comurhex:• Replacement capacity with Comurhex II at 15K mtU by 2012

• “Designed expansion possibility up to 21K tonnes if market demand warrants.”

• Springfields:• Conversion Expansion Tied To Viability Of Fuel Manufacturing At The Site

• “Tolling agreement to be extended to 2025; details being worked out.”

• ConverDyn• Decision on European new build put on hold

13

Current market does not support capacity expansion

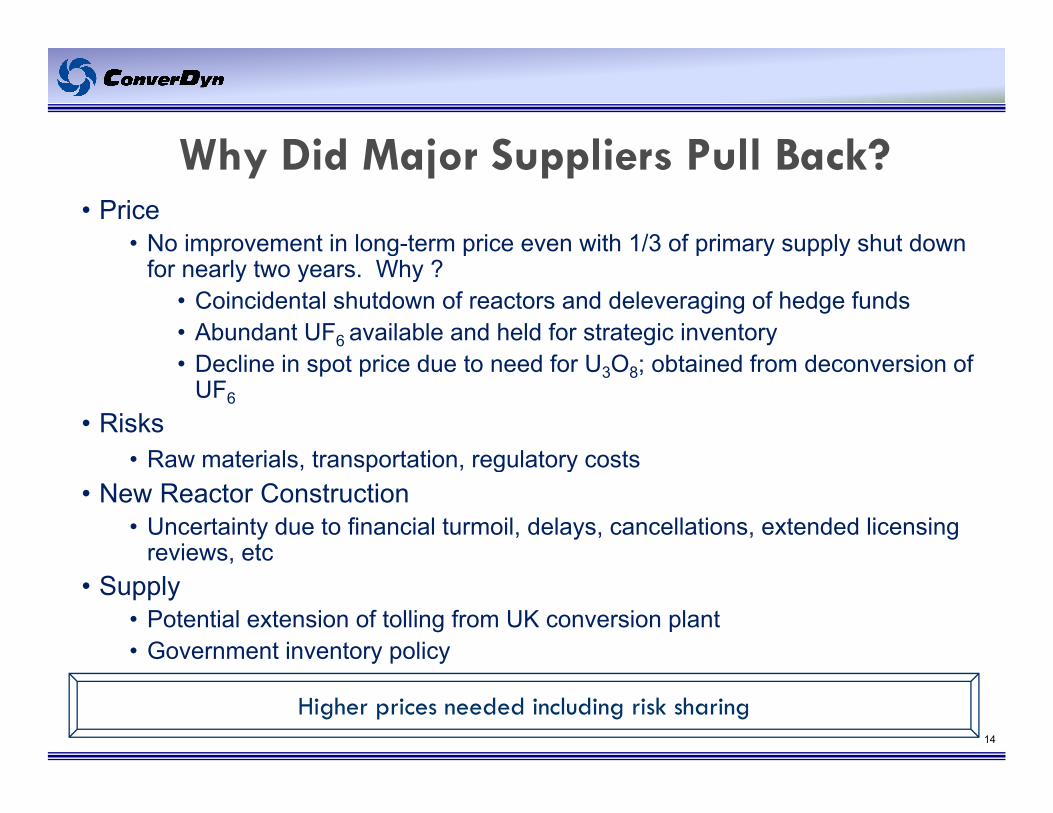

Why Did Major Suppliers Pull Back?Why Did Major Suppliers Pull Back?• Price

• No improvement in long-term price even with 1/3 of primary supply shut down p g p p y pp yfor nearly two years. Why ?

• Coincidental shutdown of reactors and deleveraging of hedge funds • Abundant UF6 available and held for strategic inventory

D li i t i d t d f U O bt i d f d i f• Decline in spot price due to need for U3O8; obtained from deconversion of UF6

• Risks• Raw materials transportation regulatory costs• Raw materials, transportation, regulatory costs

• New Reactor Construction• Uncertainty due to financial turmoil, delays, cancellations, extended licensing

reviews, etce e s, etc• Supply

• Potential extension of tolling from UK conversion plant• Government inventory policy

14

Higher prices needed including risk sharing

y p y

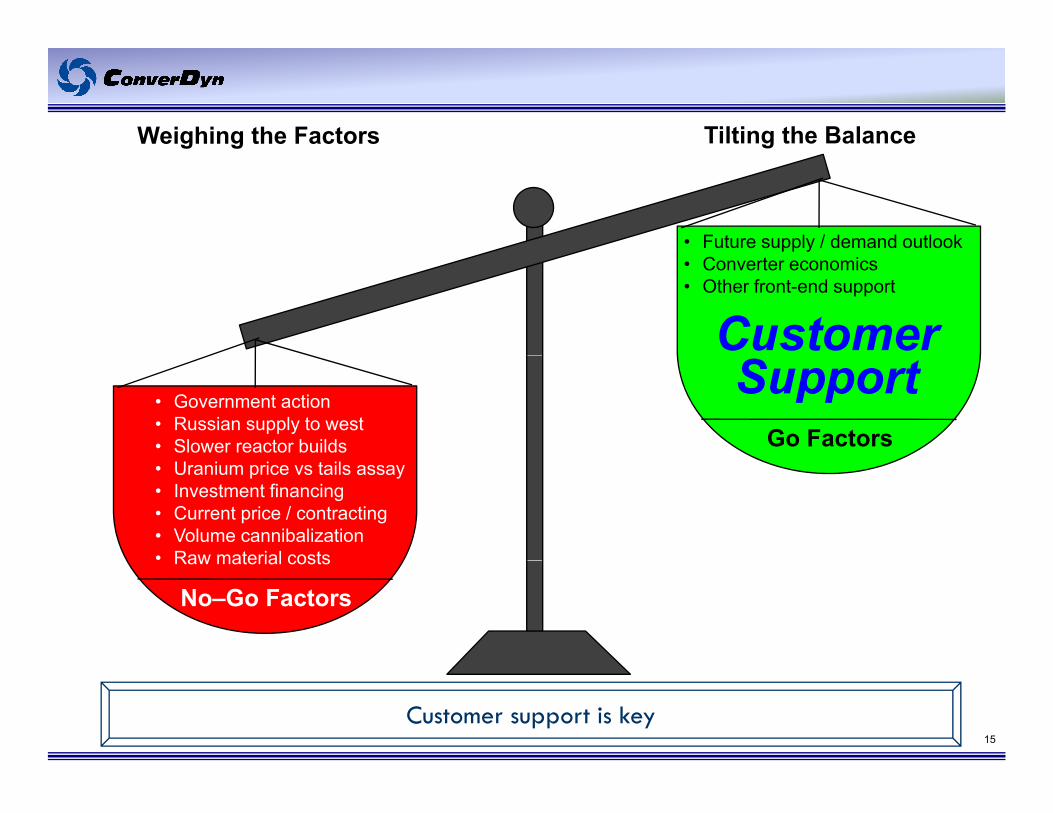

Weighing the Factors Tilting the Balance

• Future supply / demand outlook• Converter economics• Other front-end support

Customer• Government action• Russian supply to west• Slower reactor builds Go Factors

Support• Uranium price vs tails assay• Investment financing• Current price / contracting• Volume cannibalization• Raw material costsRaw material costs

No–Go Factors

15

Customer support is key

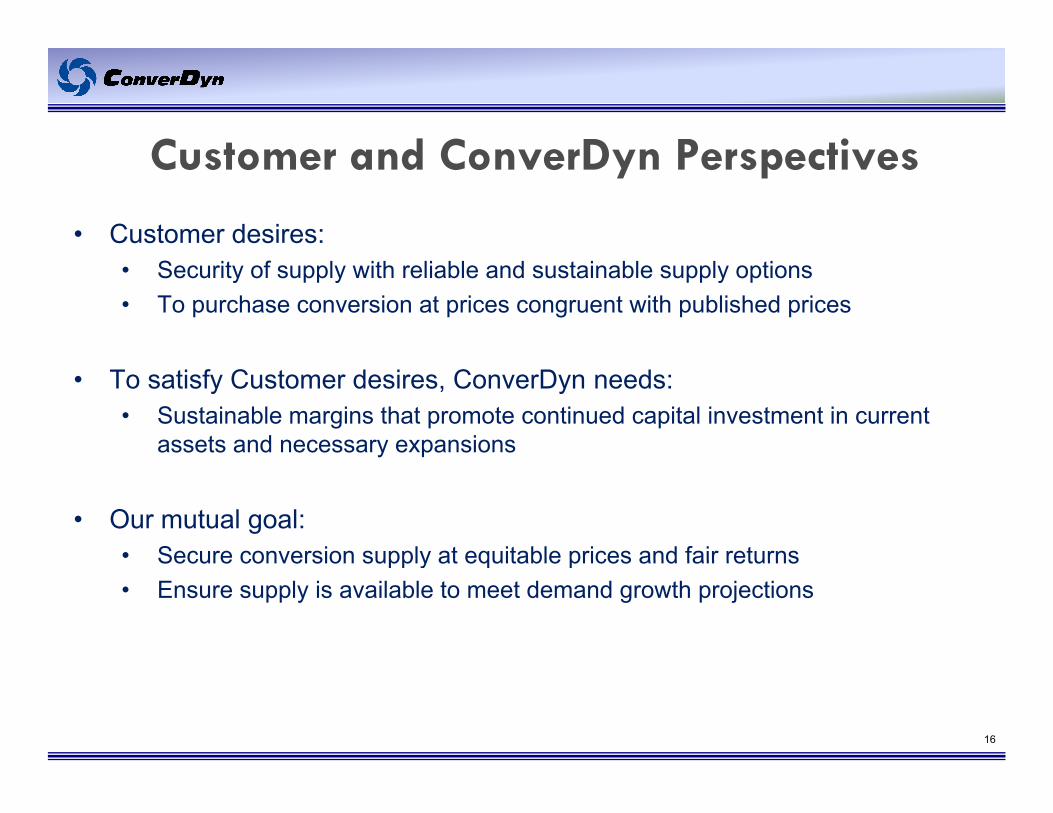

Customer and ConverDyn PerspectivesCustomer and ConverDyn Perspectives

• Customer desires:• Security of supply with reliable and sustainable supply options• To purchase conversion at prices congruent with published prices

• To satisfy Customer desires, ConverDyn needs:• Sustainable margins that promote continued capital investment in current

assets and necessary expansions

• Our mutual goal:• Secure conversion supply at equitable prices and fair returnsSecure conversion supply at equitable prices and fair returns• Ensure supply is available to meet demand growth projections

16

Closing CommentsConverter’s Challenge:

Closing Comments

• Supply / Demand analysis supports more conversion needed to meet uranium and SWU requirements for planned reactors

C i i i f ibl k• Capacity expansion is not feasible at current marketconditions

17

![pv s^zq{s]`kgu - Wing On Travel · iX8*X5;23:2534: 305}5}412}-*/ 0=46IPL}*}~ ~~~} 3~+ [jxaw^bxo^nr^tiy^lm^fh^zd^ec\ pv_s^zq{s]`kgu:>B=C29ED 1/18 4P/ XI_C\ Z;/35E](https://img.pdfslide.net/doc/110x75/5eb478d4ca47825da31dbc09/pv-szqskgu-wing-on-travel-ix8x5232534-3055412-046ipl-3.jpg)