Embed Size (px)

Citation preview

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 1/48

MARKET CONDITIONS IN CONSTRUCTION

GILBANE BUILDING COMPANY

Q2 MAY 2012

C O N S T R U C T I O N E C O N O M I C S

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 2/48

© 2012 by Gilbane Building Company

Gilbane and Cost Advisor are trademarks of Gilbane Building Company

All other trademarks are the property of their respective companies

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 3/48

Gilbane Building Company

Market Conditions In Construction – May 2012

iiiT A B L E O F C O N T E N T S

Summary 1

Construction Starts 3

Construction Spending 5

Inflation Adjusted Volume 11

Jobs/Unemployment 12

Jobs/Productivity 15

Construction Costs General 18

Material Price Movement 18

Cement / Concrete 20

Structural Steel 21

Copper 23

Producer Price Index 24The Baltic Dry Index 26

Architectural Billings Index 27

Consumer Inflation / Deflation 28

Construction Inflation Forecast 29

Some Signs Ahead 29

ENR Index 30

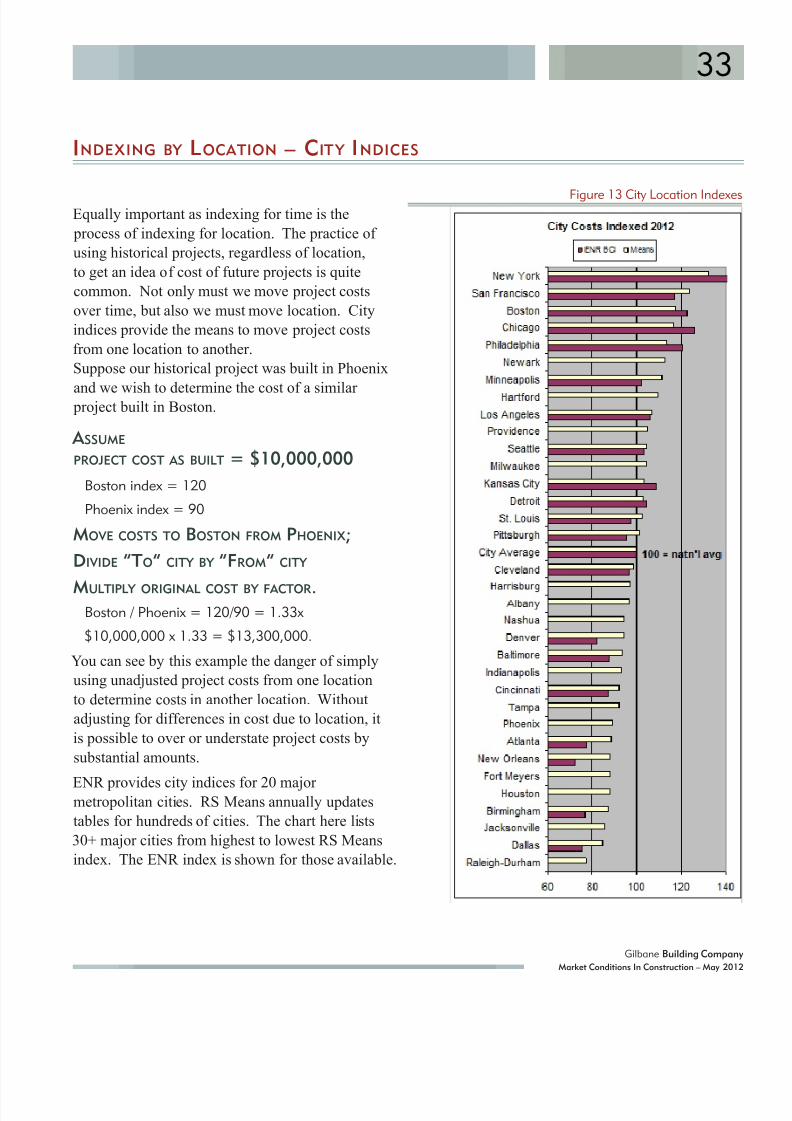

Indexing by Location – City Indices 33

Selling Price 34

Indexing – Addressing the Fluctuation in Margins 36

Escalation – What Should We Carry? 39Data Sources: 44

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 4/48

T A B L E O F C O N T E N T S

Gilbane Building Company

Market Conditions In Construction – May 2012

v T A B L E S A N D G R A P H S

Table 1 Total Construction Starts 2009-2012 3

Table 2 Total Construction Spending 2006 - 2012 7

Table 3 Construction Spending Public/Private 9

Table 4 Construction Spending Educational Healthcare 10

Table 5 Construction Spending Adjusted to 2012 11

Table 6 BLS 2012 April Construction Employment All Employees 13

Table 7 Construction Employees Major States 14

Table 8 Productivity Inflation Adjusted 15

Table 9 BLS PPI Markets 19

Table 10 BLS Actual Cost Buildings 19

Table 11 BLS Actual Cost Trades 20

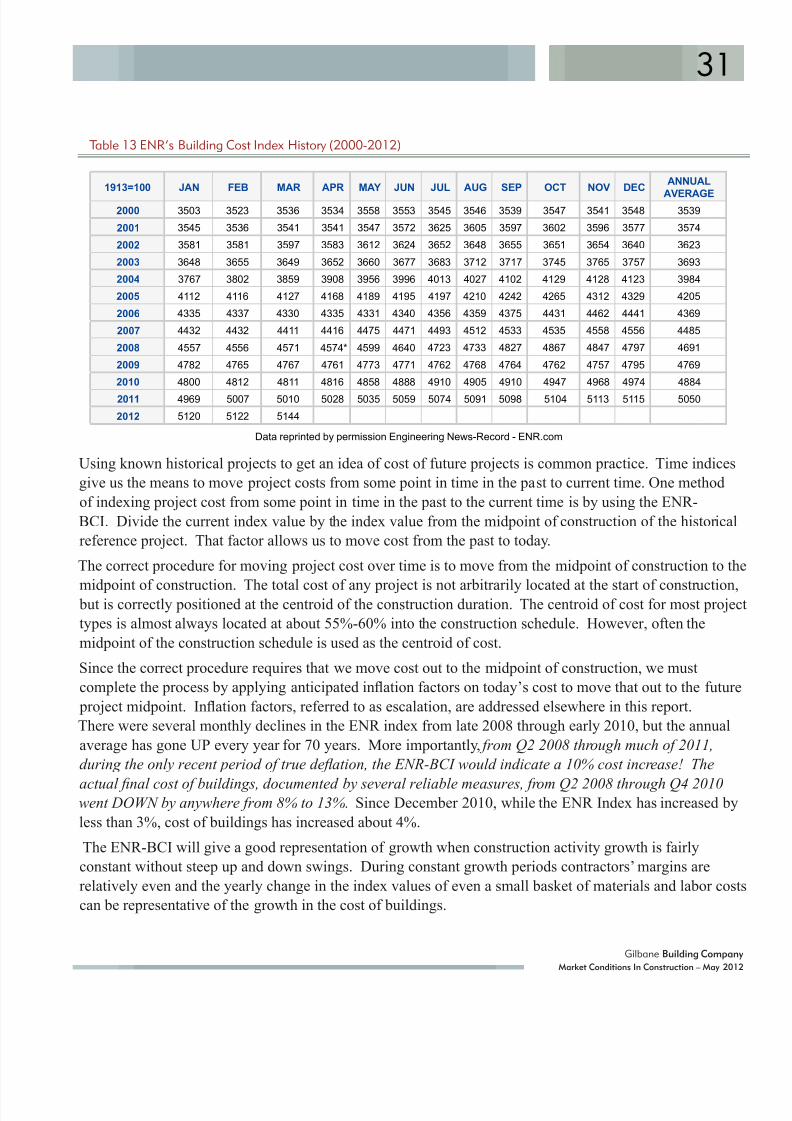

Table 12 BLS PPI Construction Related Materials 24Table 13 ENR’s Building Cost Index History (2000-2012) 31

Table 14 BLS PPI Markets 34

Table 15 BLS Actual Cost Trades 34

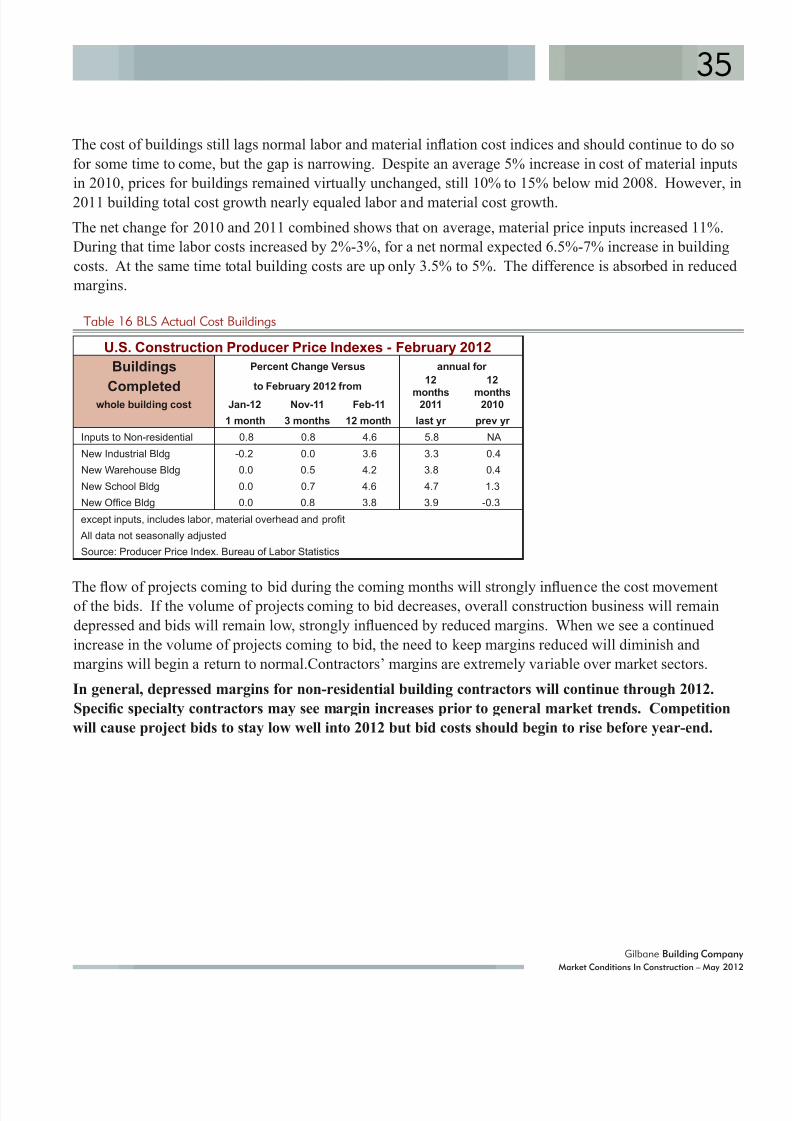

Table 16 BLS Actual Cost Buildings 35

Figure A: Architectural Billings Index 1

Figure B: Non-residentual Spending Growth 2

Figure C: Inflation/Escalation 2011-2014 2

Figure 1 Construction Starts Moving Average 4

Figure 2 Construction Starts Trend 4Figure 3 Construction Spending Non-residential 8

Figure 4 Construction Spending Adjusted to 2012 12

Figure 5 Jobs per billion dollars spending adjusted 15

Figure 6 Productivity Changes 2003-2012 16

Figure 7 PCA Cement Consumption 21

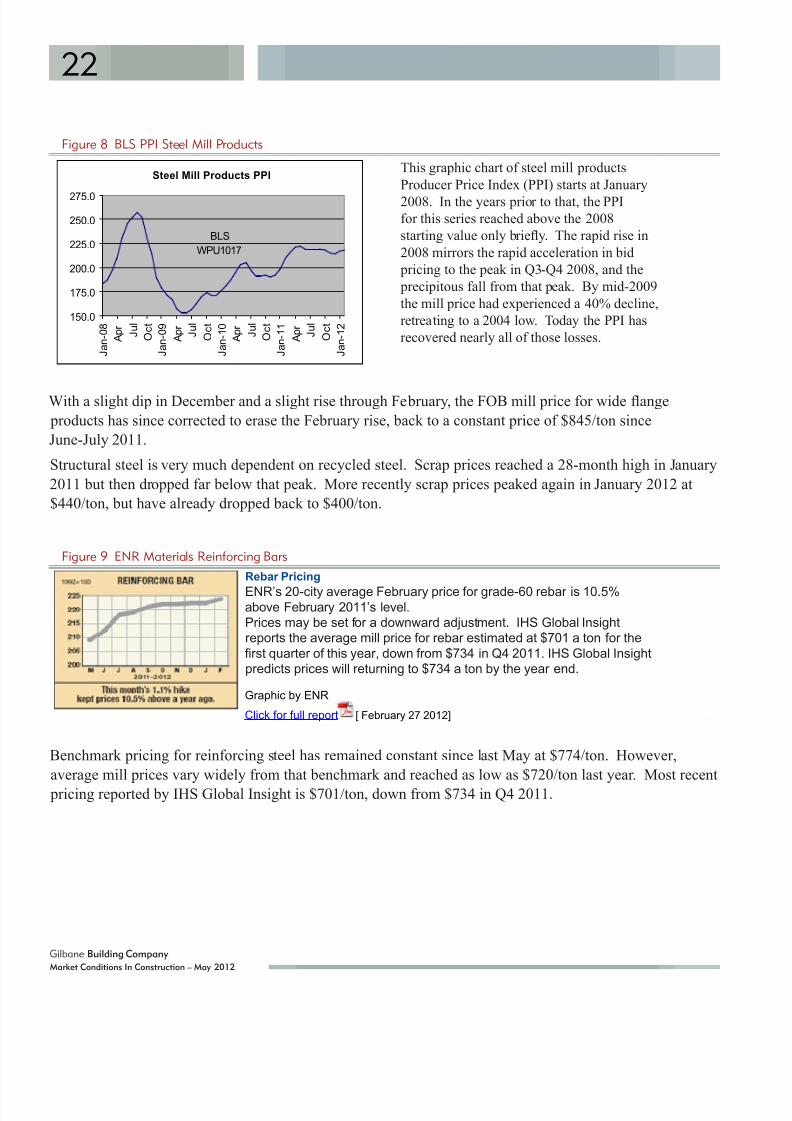

Figure 8 BLS PPI Steel Mill Products 22

Figure 9 ENR Materials Reinforcing Bars 22

Figure 10 Baltic Dry Index BDI 26

Figure 11 Architectural Billings Index ABI 27

Figure 12 Moore Inflation Predictor Consumer Inflation 28Figure 13 City Location Indexes 33

Figure 14 Escalation Growth vs. Margin Cost 37

Figure 15 Escalation Minimum and Potential 42

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 5/48

Gilbane Building Company

Market Conditions In Construction – May 2012

1

SUMMARY

SOME

ECONOMIC

FACTORS

AND

MARKET

FACTORS

SPECIFIC

TO

CONSTRUCTION

ARE

POSITIVE

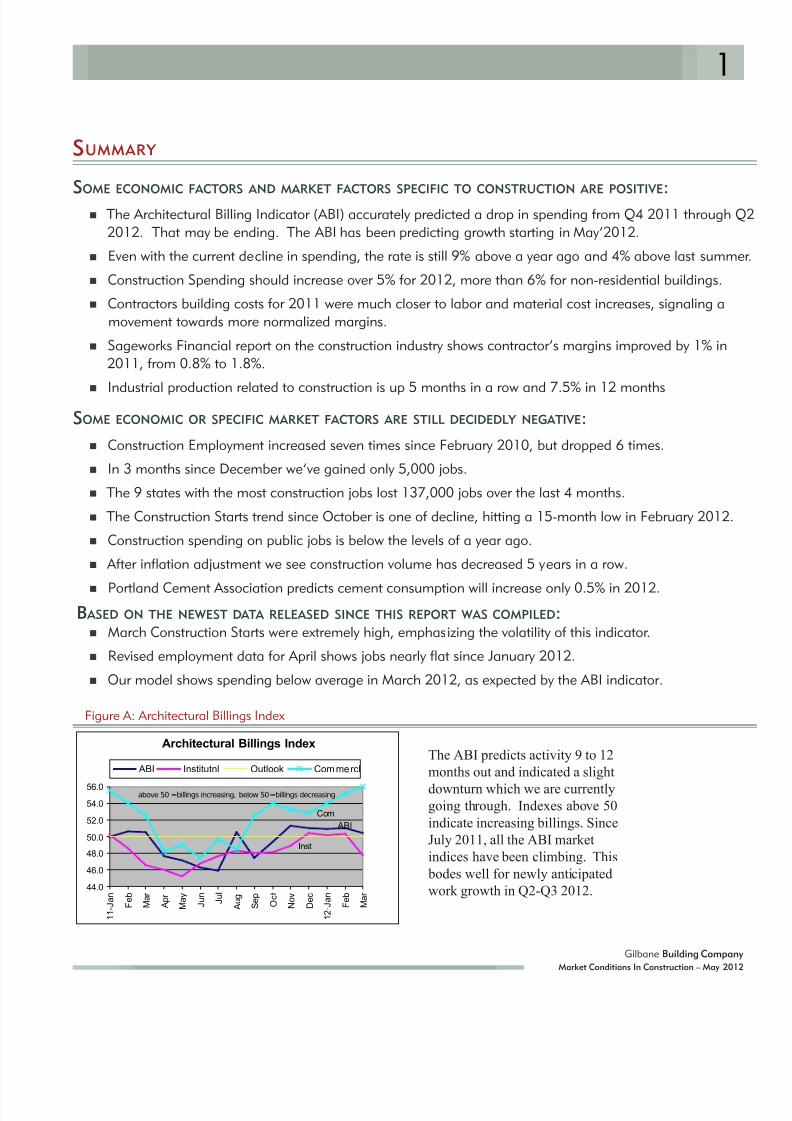

: The Architectural Billing Indicator (ABI) accurately predicted a drop in spending from Q4 2011 through Q

2012. That may be ending. The ABI has been predicting growth starting in May’2012.

Even with the current decline in spending, the rate is still 9% above a year ago and 4% above last summe

Construction Spending should increase over 5% for 2012, more than 6% for non-residential buildings.

Contractors building costs for 2011 were much closer to labor and material cost increases, signaling amovement towards more normalized margins.

Sageworks Financial report on the construction industry shows contractor’s margins improved by 1% in2011, from 0.8% to 1.8%.

Industrial production related to construction is up 5 months in a row and 7.5% in 12 months

SOME ECONOMIC OR SPECIFIC MARKET FACTORS ARE STILL DECIDEDLY NEGATIVE:

Construction Employment increased seven times since February 2010, but dropped 6 times.

In 3 months since December we’ve gained only 5,000 jobs.

The 9 states with the most construction jobs lost 137,000 jobs over the last 4 months.

The Construction Starts trend since October is one of decline, hitting a 15-month low in February 2012.

Construction spending on public jobs is below the levels of a year ago.

After inflation adjustment we see construction volume has decreased 5 years in a row.

Portland Cement Association predicts cement consumption will increase only 0.5% in 2012. B ASED ON THE NEWEST DATA RELEASED SINCE THIS REPORT WAS COMPILED:

March Construction Starts were extremely high, emphasizing the volatility of this indicator.

Revised employment data for April shows jobs nearly flat since January 2012.

Our model shows spending below average in March 2012, as expected by the ABI indicator.

Figure A: Architectural Billings Index

Architectural Billings Index

ABI

Inst

Com

44.0

46.0

48.0

50.0

52.0

54.0

56.0

1 1 - J a n

F e b

M a r

A p r

M a y

J u n

J u l

A u g

S e p

O c t

N o v

D e c

1 2 - J a n

F e b

M a r

above 50 =billings increasing, below 50 =billings decreasing

ABI Institutnl Outlook Com mercl

The ABI predicts activity 9 to 12

months out and indicated a slight

downturn which we are currentlygoing through. Indexes above 50

indicate increasing billings. Since

July 2011, all the ABI market

indices have been climbing. This

bodes well for newly anticipated

work growth in Q2-Q3 2012.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 6/48

2

Gilbane Building Company

Market Conditions In Construction – May 2012

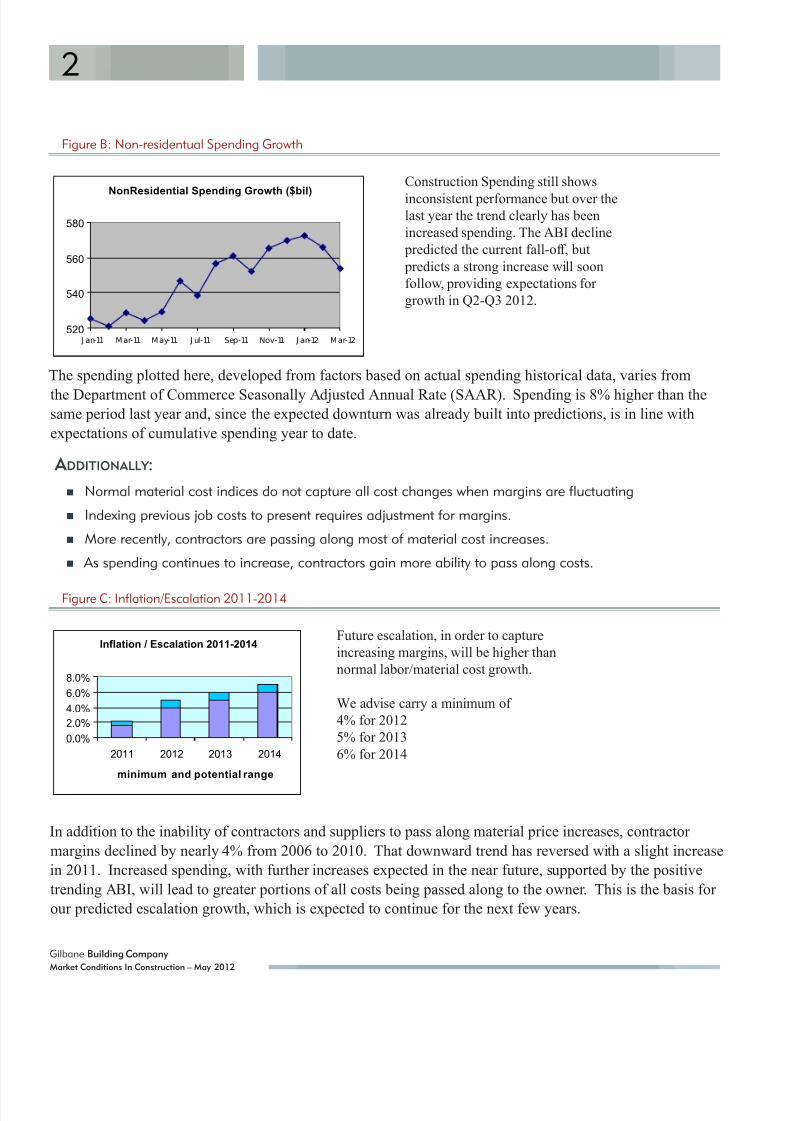

Figure B: Non-residentual Spending Growth

NonResidential Spending Growth ($bil)

520

540

560

580

J an-11 Mar-11 May-11 J ul-11 Sep-11 Nov-11 J an-12 Mar-12

The spending plotted here, developed from factors based on actual spending historical data, varies from

the Department of Commerce Seasonally Adjusted Annual Rate (SAAR). Spending is 8% higher than thesame period last year and, since the expected downturn was already built into predictions, is in line with

expectations of cumulative spending year to date.

A DDITIONALLY :

Normal material cost indices do not capture all cost changes when margins are fluctuating

Indexing previous job costs to present requires adjustment for margins.

More recently, contractors are passing along most of material cost increases.

As spending continues to increase, contractors gain more ability to pass along costs.

Figure C: Inflation/Escalation 2011-2014

Inflation / Escalation 2011-2014

0.0%

2.0%

4.0%

6.0%

8.0%

2011 2012 2013 2014

minimum and potential range

In addition to the inability of contractors and suppliers to pass along material price increases, contractor

margins declined by nearly 4% from 2006 to 2010. That downward trend has reversed with a slight increase

in 2011. Increased spending, with further increases expected in the near future, supported by the positive

trending ABI, will lead to greater portions of all costs being passed along to the owner. This is the basis for

our predicted escalation growth, which is expected to continue for the next few years.

Construction Spending still shows

inconsistent performance but over thelast year the trend clearly has been

increased spending. The ABI decline

predicted the current fall-off, but

predicts a strong increase will soon

follow, providing expectations for

growth in Q2-Q3 2012.

Future escalation, in order to capture

increasing margins, will be higher than

normal labor/material cost growth.

We advise carry a minimum of

4% for 2012

5% for 2013

6% for 2014

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 7/48

3

Gilbane Building Company

Market Conditions In Construction – May 2012

CONSTRUCTION STARTS

Construction Starts published data gives monthly actual data and a seasonal adjusted annual rate (SAAR)

for each set of monthly Starts values. But the monthly values for Starts uctuate wildly. In fact, one ofthe most important things we can say about Construction Starts is that they can be extremely variable from

month to month, presumably dependent on the exact date that any new project gets listed.

SAAR based on monthly data in 2011 had variation from $380 billion to $470 billion (2010 varied from

$380billion to $450 billion). And yet, 2010 and 2011 nished within 2% of each other at $412 billion vs.

$421 billion. Any given month of data is far too volatile to predict the annual total. In the last two years of

data there have been at least 4 occasions when consecutive months have varied by an average 20% and as

high a difference as 25%. This causes unrealistic peaks and valleys in the data. Therefore, we do not use

month to month data to predict annual outcome.

One way to look at the data is to calculate a forecast based on the latest month, last 3 months and last 6months. One month trend data is always too volatile to predict the year, but shows the current monthly

trend; 3-month trends smooth out the data and give a near term trend and better prediction; and 6-month

trends atten the data even more and show a smoothed long-term trend.

Historically, we see only 7% of annual Starts in some months while we nd other months have 10% of

the annual Starts for the year. We see lowest Starts in November through February and highest Starts in

Jun through October It is not unusual to see huge increases or decreases in volume from month to month.

Historically, for non-residential buildings, there are 20% more Starts in Jun than in May and 30% more

Starts in October than November The SAAR factors are weakest during these periods and therefore at times

during the year the SAAR report can produce signicant variation from actual data and historical averages.

Our forecasting model is based on the actual data and historical averages.

Table 1 Total Construction Starts 2009-2012

TOTAL CONSTRUCTION STARTS Forecast 2012 based on

Actual Actual Actual 1 month 3 month Trend2009 2010 2011 actuals actuals predicion

Non-residential Buildings $ 167,955 $ 152,033 $ 154,782 $ 135,716 $ 141,140 $ 160,000

-9.5% 1.8% -12.3% -8.8% 3.4%

Residential Buildings $ 111,851 $ 119,360 $ 123,444 $ 146,499 $ 141,234 $ 145,000

6.7% 3.4% 18.7% 14.4% 17.5%

Non-building Construction $ 141,899 $ 141,078 $ 143,195 $ 117,342 $ 117,817 $ 120,000

-0.6% 1.5% -18.1% -17.7% -16.2%

Total Construction $ 421,705 $ 412,471 $ 421,421 $ 399,557 $ 400,191 $ 425,000

percent change yoy -2.2% 2.2% -5.2% -5.0% 0.8%

dollars in millions Feb’2012 Dec/Jan/Febforecast based on historical cumulative factors

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 8/48

4

Gilbane Building Company

Market Conditions In Construction – May 2012

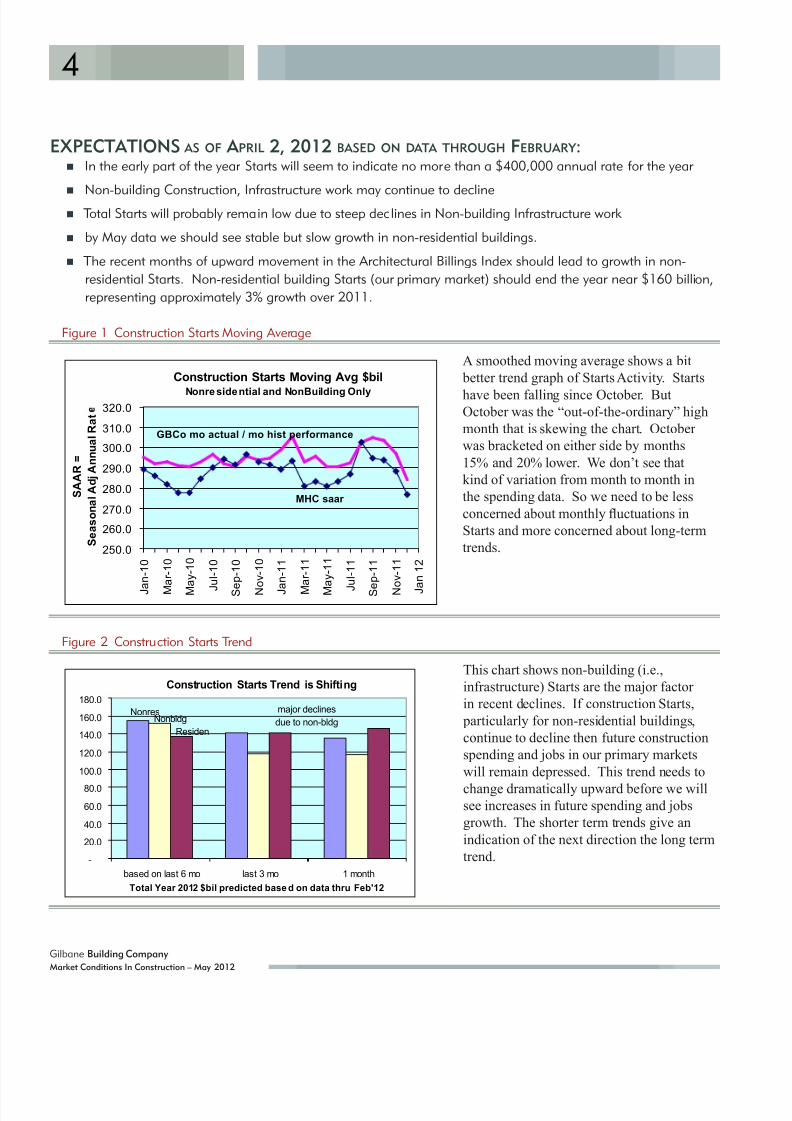

EXPECTATIONS AS OF A PRIL 2, 2012 BASED ON DATA THROUGH FEBRUARY : In the early part of the year Starts will seem to indicate no more than a $400,000 annual rate for the year

Non-building Construction, Infrastructure work may continue to decline

Total Starts will probably remain low due to steep declines in Non-building Infrastructure work

by May data we should see stable but slow growth in non-residential buildings.

The recent months of upward movement in the Architectural Billings Index should lead to growth in non-

residential Starts. Non-residential building Starts (our primary market) should end the year near $160 billion,

representing approximately 3% growth over 2011.

Figure 1 Construction Starts Moving Average

Construction Starts Moving Avg $bil

Nonresidential and NonBuilding Only

MHC saar

250.0

260.0

270.0

280.0

290.0

300.0

310.0

320.0

J a n - 1 0

M

a r - 1 0

M

a y - 1 0

J

u l - 1 0

S e p - 1 0

N o v - 1 0

J a n - 1 1

M

a r - 1 1

M

a y - 1 1

J

u l - 1 1

S e p - 1 1

N o v - 1 1

J a n 1 2

GBCo mo actual / mo hist performance

S A A R =

S e a s o n a l A d j A n n u a l R a t

Figure 2 Construction Starts Trend

Construction Starts Trend is Shifting

NonresNonbldg

major declines

due to non-bldgResiden

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

based on last 6 mo last 3 mo 1 month

Total Year 2012 $bil predicted base d on data thru Feb'12

A smoothed moving average shows a bit

better trend graph of Starts Activity. Starts

have been falling since October. ButOctober was the “out-of-the-ordinary” high

month that is skewing the chart. October

was bracketed on either side by months

15% and 20% lower. We don’t see that

kind of variation from month to month in

the spending data. So we need to be less

concerned about monthly uctuations in

Starts and more concerned about long-term

trends.

This chart shows non-building (i.e.,

infrastructure) Starts are the major factor

in recent declines. If construction Starts,

particularly for non-residential buildings,

continue to decline then future construction

spending and jobs in our primary markets

will remain depressed. This trend needs to

change dramatically upward before we willsee increases in future spending and jobs

growth. The shorter term trends give an

indication of the next direction the long term

trend.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 9/48

5

Gilbane Building Company

Market Conditions In Construction – May 2012

Inationary inuences have the effect of reducing the value of new Starts, and so, Starts at a rate lower than

the real ination rate would mean construction Starts in terms of building volume (not in terms of revenue)

are actually falling. If ination for the year comes in at 4%, then Starts need to be greater than 4% to realize

any growth.

CONSTRUCTION SPENDING

WHAT SHOULD WE EXPECT FOR 2012? HOW ARE WE DOING SO FAR ?

DOESN’T SOUND GOOD, DOES IT? OK, ’LET’S TAKE A LOOK .

Quoted from a February 7, 2012 post in my Gilbane blog

“it is widely agreed by many expert economists that we may experience a slowdown in the coming months…

(note- at this point December spending data had just been released).”

Quoted from a March 5, 2012 post in my Gilbane blog

“Earlier in 2011 the Architectural Billings Index showed work on the (architect’s) books declining. That

signaled an expected drop in construction 9 to 12 months out. We may be currently seeing this in the

declining new Starts….that could continue through April 2012….last year’s declining ABI billings indicated

Starts and spending would be lower for a period.”

Quoted from my Q4’2011 economics report

“The Architectural Billings Index has been signaling all year that we should expect further declines in

spending. A reliable indicator of work 9 to 12 months out, new Starts and spending results will always lag

the ABI.”

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 10/48

Gilbane Building Company

Market Conditions In Construction – May 2012

6

First: It cannot be said this drop was UNEXPECTED. I’ve been

predicting the drop for a few months. Two leading indicators showed

an expected decline in Q1’ 2012 and previously reported jobs movement

followed suit. Now if the drop continues for 4 to 6 more months, that’s

unexpected.

Second: the Department of Commerce SAAR factor for January appears

to give a somewhat “too high” expectation for that month. On top of that,

December was an unusually strong month. So this is skewing the data

upon which all other news services report.

Third: January and February were the ONLY months that showed declines

in the last 7 months, and that’s undoubtedly because Q4’ 2011 was so

unusually strong and set a very high comparable. Furthermore, January

and February show spending at almost exactly the same rate, and bothstill show spending at a rate comfortably above Q3’ 2011.

My statistical monthly averages show from January to February the

monthly decline was only 0.2%, spending combined is 8% higher than the

same period last year and is within 0.1% of expectations cumulative year

to date. Since the bottom, spending has increased 9 out of 12 months and

the current rate for Jan-February is well above the rate last June, July, and

-August On an ination-adjusted basis, we’ve just had the best December,

January, and February period since ‘2008-’2009. It would appear so far

we are right on track.

The recently release CIRT (Construction Industry Round table) SentimentIndex Report, issued by FMI, representing collective input from

approximately 100 non-residential construction executives, includes these

data and responses: 42% of executives expect spending to improve only

modestly, from 0.5% to 2.5%, 26% expect little to no growth and 27%

expect spending declines. I do not share that sentiment.

I PRECICT THAT 2012 SPENDING FOR ALL CONSTRUCTION WILL BE $832 BILLION, A GROWTH OF 5.4%.

Given the most recent trends that take into consideration the 2011

midyear downturn in the ABI and a Q4 drop in new Starts, but thatmonthly spending rates increased in 9 out of the last 12 months,after factoring in an expected slowdown in the first quarter, my modelpredicts total spending will climb slowly for the remainder of the year,reflecting a growing ABI and slightly stronger economy, and will end the year 2012 at $832 billion spending for all construction, 5.4%above 2011. That represents a growth of only 2.2% after inflation.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 11/48

7

Gilbane Building Company

Market Conditions In Construction – May 2012

Table 2 Total Construction Spending 2006 - 2012

U.S. Total Construction Spending Summarytotals in billions U.S. dollars

Actual Forecast

2006 2007 2008 2009 2010 2011 2012

Non-residential Buildings 339.4 403.7 438.0 375.5 288.5 277.8 294.9

% change year over year 12.5% 18.9% 8.5% -14.3% -23.2% -3.7% 6.2%

Non-building heavy engr 207.9 248.3 271.8 273.3 266.4 266.6 274.9

12.4% 19.4% 9.5% 0.6% -2.5% 0.1% 3.1%

Residential 619.9 500.3 357.7 254.3 248.7 244.9 262.4

0.4% -19.3% -28.5% -28.9% -2.2% -1.5% 7.1%

Total 1167.2 1152.3 1067.5 903.1 803.6 789.2 832.2

5.7% -1.3% -7.4% -15.4% -11.0% -1.8% 5.4%

Residential includes new, remodeling, renovation and replacement work.

Source: U.S. Census Bureau, Department of Commerce.

Forecast 2012 - GBCo

Historically, the period of June through October shows the highest monthly rates of spending during the

year, all 5 months each over 9% of annual volume, with the highest monthly volume being reached in

August. Long-term averages show that spending in December, January and February each account for only

±7% of the annual volume. For example, in January and Feb, the lowest activity months of the year, history

leads us to expect to spend 7.0% of the total for the year. In August we expect to spend 9.5% of the total for

the year. If we see spending of $70 billion in January and $95 billion in August, this increase by $25 billion per month from January to August is seasonal, not an indication of growth. It simply indicates the rate

of spending in each of those months has reached the expected seasonal average rate for that month. Both

monthly values would predict the same year end total. We must use caution to not consider these increases

as an improvement in the rate of spending. The monthly rate-of-spending trends are holding through this

winter.

The months November through March have a high standard deviation from average and can produce wide

uctuations in year end data predicted from monthly data. However, the months of May through September

have a very low standard deviation and monthly data from that period gives a much more reliable year-end

prediction. Unfortunately, that means the current data for the past 4 months is among the least reliable to

predict the entire year.

Historical monthly activity can also be used to develop cumulative year-to-date data activity. This

eliminates some of the monthly uctuations and the total annual prediction gains more weight each month.

By September each year for 10 years, we had realized on average 75% total annual spending, with a

standard deviation of less than ±1%.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 12/48

8

Gilbane Building Company

Market Conditions In Construction – May 2012

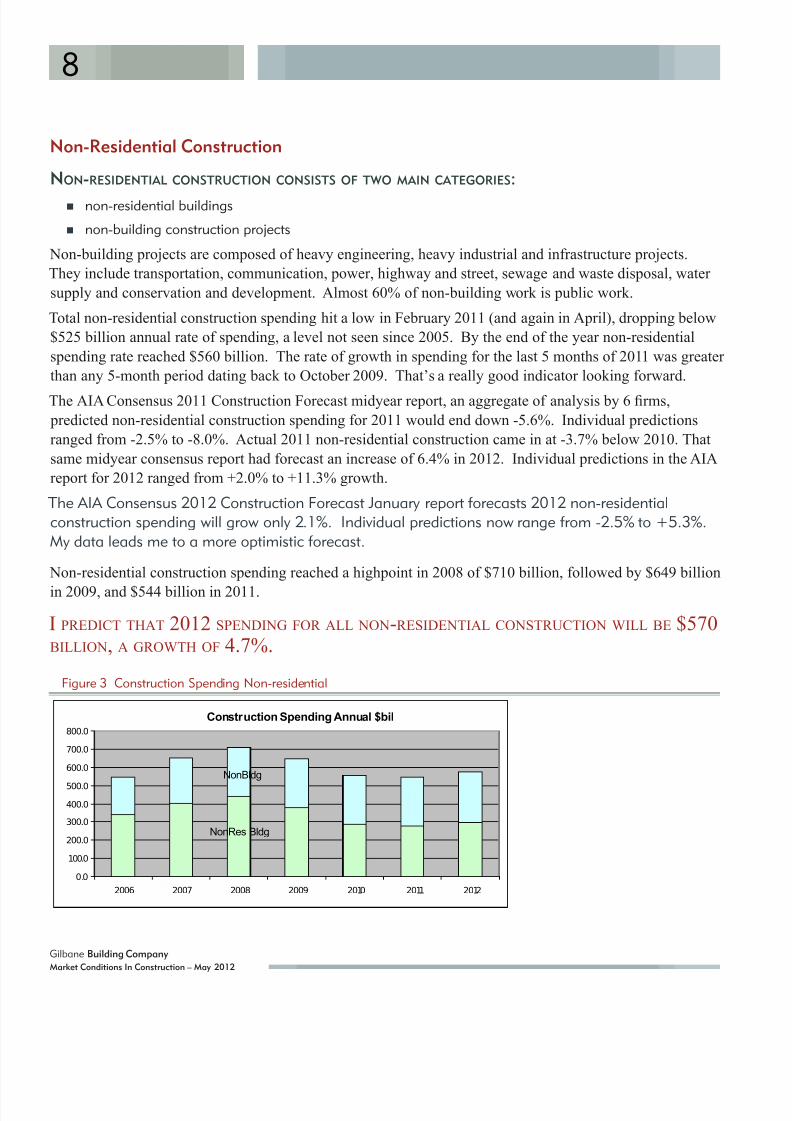

Non-Residential Construction

NON-RESIDENTIAL CONSTRUCTION CONSISTS OF TWO MAIN CATEGORIES:

non-residential buildings

non-building construction projects

Non-building projects are composed of heavy engineering, heavy industrial and infrastructure projects.

They include transportation, communication, power, highway and street, sewage and waste disposal, water

supply and conservation and development. Almost 60% of non-building work is public work.

Total non-residential construction spending hit a low in February 2011 (and again in April), dropping below

$525 billion annual rate of spending, a level not seen since 2005. By the end of the year non-residential

spending rate reached $560 billion. The rate of growth in spending for the last 5 months of 2011 was greater

than any 5-month period dating back to October 2009. That’s a really good indicator looking forward.

The AIA Consensus 2011 Construction Forecast midyear report, an aggregate of analysis by 6 rms,

predicted non-residential construction spending for 2011 would end down -5.6%. Individual predictions

ranged from -2.5% to -8.0%. Actual 2011 non-residential construction came in at -3.7% below 2010. That

same midyear consensus report had forecast an increase of 6.4% in 2012. Individual predictions in the AIA

report for 2012 ranged from +2.0% to +11.3% growth.

The AIA Consensus 2012 Construction Forecast January report forecasts 2012 non-residentialconstruction spending will grow only 2.1%. Individual predictions now range from -2.5% to +5.3%.My data leads me to a more optimistic forecast.

Non-residential construction spending reached a highpoint in 2008 of $710 billion, followed by $649 billion

in 2009, and $544 billion in 2011.

I PREDICT THAT 2012 SPENDING FOR ALL NON-RESIDENTIAL CONSTRUCTION WILL BE $570BILLION, A GROWTH OF 4.7%.

Figure 3 Construction Spending Non-residential

Construction Spending Annual $bil

NonRes Bldg

NonBldg

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

2006 2007 2008 2009 2010 2011 2012

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 13/48

9

Gilbane Building Company

Market Conditions In Construction – May 2012

THE RECENTLY RELEASED CIRT SENTIMENT INDEX REPORT, REPRESENTING COLLECTIVE INPUT FROM NON-RESIDENTIAL CONSTRUCTION EXECUTIVES INCLUDES THESE RESPONSES:

More than 70% of executives expect the strongest increase of the year in Industrial/Petrochemical. Approx. 50% expect next strongest yearly increases in manufacturing and healthcare, but approximately

50% expect manufacturing and healthcare to remain the same or decline.

The educational sector still has the worst overall outlook 1 and 3 years out.

Non-Residential Buildings

Non-residential “buildings” construction spending reached a highpoint in 2008 at $438 billion, followed by

$376 billion in 2009, and $278 billion for 2011.

I PREDICT THAT 2012 SPENDING FOR NON-RESIDENTIAL BUILDINGS WILL BE $295 BILLION,

A GROWTH OF 6.2%.Private construction is predominantly residential. 97% of all residential work is private and constitutes

just under half of all private work. (A historical note: in 2005-2006, residential work constituted 70% of all

private work and more than half of all construction spending. For the last 3 years residential comprises

just less than 50% of private work and only 30% of all construction). Manufacturing (8%) and Commercial

(7.5%) are the next largest private “buildings” sectors. Non-buildings make up a large portion of private

work; ALL Power (17%) and Communication work (3.5%) is private work.

Private Construction spending reached a highpoint in 2006 at $912 billion and in 2011 was $506 billion.

I PREDICT THAT 2012 PRIVATE CONSTRUCTION SPENDING WILL BE $555 BILLION, AN INCREASE OF 9.8%, BUT STILL 40% BELOW THE PEAK .

Table 3 Construction Spending Public/Private

U.S. Total Construction Spendingtotals in billions U.S. dollars

Actual Forecast

2006 2007 2008 2009 2010 2011 2012

Private 911.8 863.4 758.8 588.1 500.4 505.7 555.0

% change year over year 4.8% -5.3% -12.1% -22.5% -14.9% 1.1% 9.8%

Public 255.4 288.9 308.7 315.0 303.2 283.5 277.2

9.0% 13.1% 6.9% 2.0% -3.7% -6.5% -2.2%

Total 1167.2 1152.3 1067.5 903.1 803.6 789.2 832.2

5.7% -1.3% -7.4% -15.4% -11.0% -1.8% 5.4%

Source: U.S. Census Bureau, Department of Commerce.

Forecast 2012 - GBCo

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 14/48

10

Gilbane Building Company

Market Conditions In Construction – May 2012

The largest public construction markets are Highway and Educational. Those two markets alone represent

more than half of all public construction, followed by Transportation, a distant third, and Waste Disposal

fourth. All other markets together make up less than 30% of public work. Slight increases show up

in Highway from September through January, and Waste Disposal from October through February

Educational has been showing a steady decline for 6 months and Transportation, after deep drops since

2010, has been at since August.

Public Construction spending reached a highpoint in 2009 at $315 billion and in 2011 was $284 billion.

I PREDICT THAT 2012 PUBLIC CONSTRUCTION SPENDING WILL BE $277 BILLION, A DROP OF 2.2%, 12% BELOW THE 2009 PEAK .

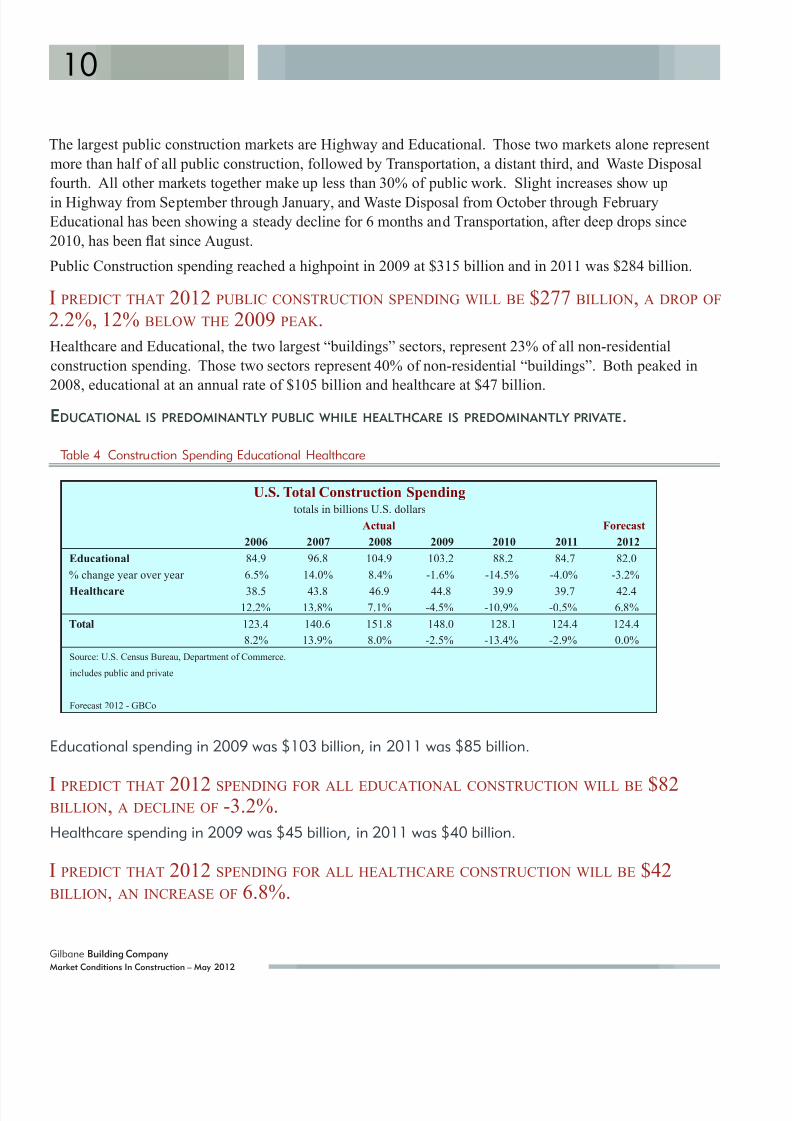

Healthcare and Educational, the two largest “buildings” sectors, represent 23% of all non-residential

construction spending. Those two sectors represent 40% of non-residential “buildings”. Both peaked in

2008, educational at an annual rate of $105 billion and healthcare at $47 billion.EDUCATIONAL IS PREDOMINANTLY PUBLIC WHILE HEALTHCARE IS PREDOMINANTLY PRIVATE.

Table 4 Construction Spending Educational Healthcare

U.S. Total Construction Spendingtotals in billions U.S. dollars

Actual Forecast

2006 2007 2008 2009 2010 2011 2012

Educational 84.9 96.8 104.9 103.2 88.2 84.7 82.0

% change year over year 6.5% 14.0% 8.4% -1.6% -14.5% -4.0% -3.2%

Healthcare 38.5 43.8 46.9 44.8 39.9 39.7 42.4

12.2% 13.8% 7.1% -4.5% -10.9% -0.5% 6.8%

Total 123.4 140.6 151.8 148.0 128.1 124.4 124.4

8.2% 13.9% 8.0% -2.5% -13.4% -2.9% 0.0%

Source: U.S. Census Bureau, Department of Commerce.

includes public and private

Forecast 2012 - GBCo

Educational spending in 2009 was $103 billion, in 2011 was $85 billion.

I PREDICT THAT 2012 SPENDING FOR ALL EDUCATIONAL CONSTRUCTION WILL BE $82BILLION, A DECLINE OF -3.2%.

Healthcare spending in 2009 was $45 billion, in 2011 was $40 billion.

I PREDICT THAT 2012 SPENDING FOR ALL HEALTHCARE CONSTRUCTION WILL BE $42BILLION, AN INCREASE OF 6.8%.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 15/48

11

Gilbane Building Company

Market Conditions In Construction – May 2012

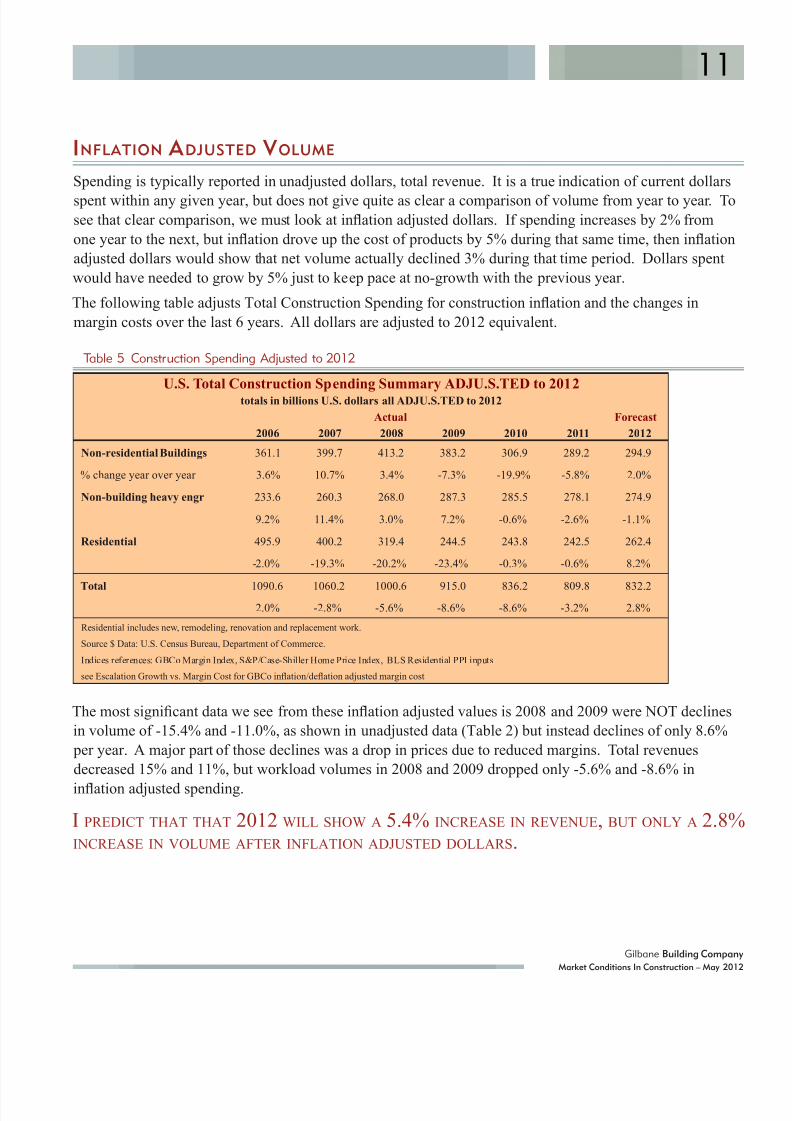

INFLATION A DJUSTED V OLUME

Spending is typically reported in unadjusted dollars, total revenue. It is a true indication of current dollars

spent within any given year, but does not give quite as clear a comparison of volume from year to year. Tosee that clear comparison, we must look at ination adjusted dollars. If spending increases by 2% from

one year to the next, but ination drove up the cost of products by 5% during that same time, then ination

adjusted dollars would show that net volume actually declined 3% during that time period. Dollars spent

would have needed to grow by 5% just to keep pace at no-growth with the previous year.

The following table adjusts Total Construction Spending for construction ination and the changes in

margin costs over the last 6 years. All dollars are adjusted to 2012 equivalent.

Table 5 Construction Spending Adjusted to 2012

U.S. Total Construction Spending Summary ADJU.S.TED to 2012totals in billions U.S. dollars all ADJU.S.TED to 2012

Actual Forecast

2006 2007 2008 2009 2010 2011 2012

Non-residential Buildings 361.1 399.7 413.2 383.2 306.9 289.2 294.9

% change year over year 3.6% 10.7% 3.4% -7.3% -19.9% -5.8% 2.0%

Non-building heavy engr 233.6 260.3 268.0 287.3 285.5 278.1 274.9

9.2% 11.4% 3.0% 7.2% -0.6% -2.6% -1.1%

Residential 495.9 400.2 319.4 244.5 243.8 242.5 262.4

-2.0% -19.3% -20.2% -23.4% -0.3% -0.6% 8.2%

Total 1090.6 1060.2 1000.6 915.0 836.2 809.8 832.2

2.0% -2.8% -5.6% -8.6% -8.6% -3.2% 2.8%

Residential includes new, remodeling, renovation and replacement work.

Source $ Data: U.S. Census Bureau, Department of Commerce.

Indices references: GBCo Margin Index, S&P/Case-Shiller Home Price Index, BLS Residential PPI inputs

see Escalation Growth vs. Margin Cost for GBCo ination/deation adjusted margin cost

The most signicant data we see from these ination adjusted values is 2008 and 2009 were NOT declines

in volume of -15.4% and -11.0%, as shown in unadjusted data (Table 2) but instead declines of only 8.6%

per year. A major part of those declines was a drop in prices due to reduced margins. Total revenues

decreased 15% and 11%, but workload volumes in 2008 and 2009 dropped only -5.6% and -8.6% in

ination adjusted spending.

I PREDICT THAT THAT 2012 WILL SHOW A 5.4% INCREASE IN REVENUE, BUT ONLY A 2.8%INCREASE IN VOLUME AFTER INFLATION ADJUSTED DOLLARS.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 16/48

12

Gilbane Building Company

Market Conditions In Construction – May 2012

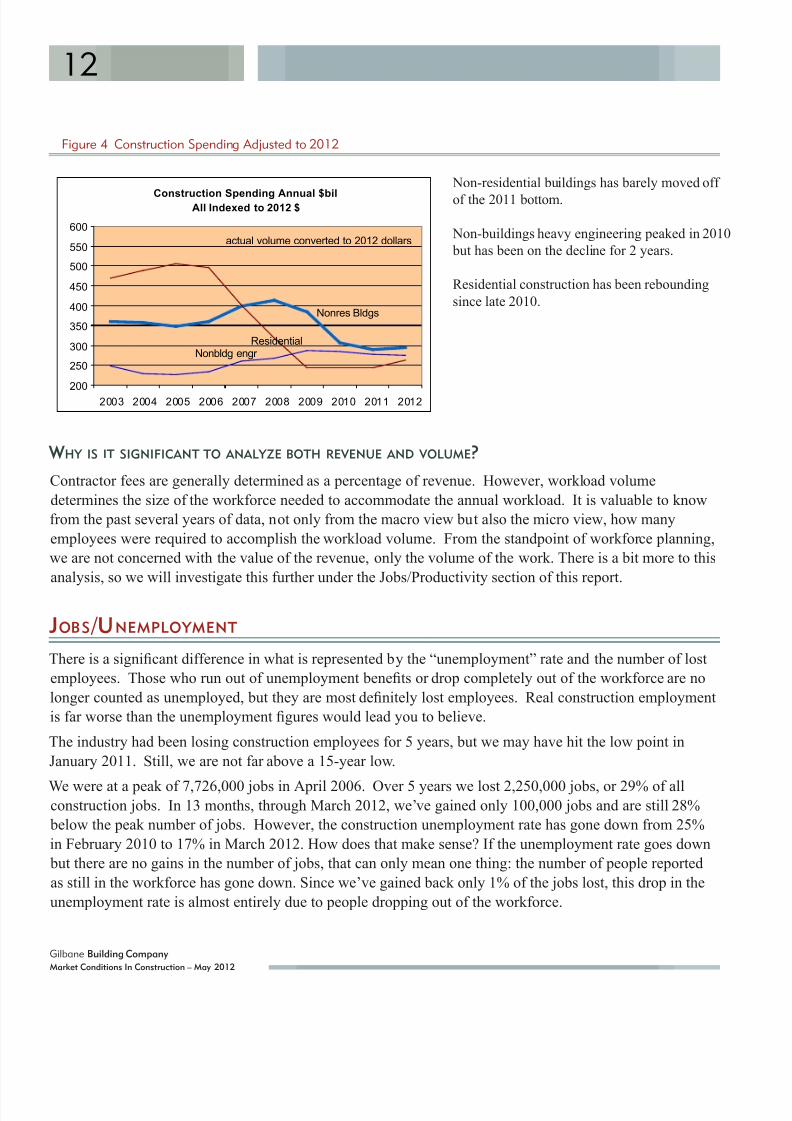

Figure 4 Construction Spending Adjusted to 2012

Construction Spending Annual $bilAll Indexed to 2012 $

Nonres Bldgs

Nonbldg engr Residential

200

250

300

350

400

450

500

550

600

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

actual volume converted to 2012 dollars

WHY IS IT SIGNIFICANT TO ANALYZE BOTH REVENUE AND VOLUME?

Contractor fees are generally determined as a percentage of revenue. However, workload volume

determines the size of the workforce needed to accommodate the annual workload. It is valuable to know

from the past several years of data, not only from the macro view but also the micro view, how many

employees were required to accomplish the workload volume. From the standpoint of workforce planning,

we are not concerned with the value of the revenue, only the volume of the work. There is a bit more to this

analysis, so we will investigate this further under the Jobs/Productivity section of this report.

JOBS /UNEMPLOYMENT

There is a signicant difference in what is represented by the “unemployment” rate and the number of lost

employees. Those who run out of unemployment benets or drop completely out of the workforce are no

longer counted as unemployed, but they are most denitely lost employees. Real construction employment

is far worse than the unemployment gures would lead you to believe.

The industry had been losing construction employees for 5 years, but we may have hit the low point in

January 2011. Still, we are not far above a 15-year low.

We were at a peak of 7,726,000 jobs in April 2006. Over 5 years we lost 2,250,000 jobs, or 29% of allconstruction jobs. In 13 months, through March 2012, we’ve gained only 100,000 jobs and are still 28%

below the peak number of jobs. However, the construction unemployment rate has gone down from 25%

in February 2010 to 17% in March 2012. How does that make sense? If the unemployment rate goes down

but there are no gains in the number of jobs, that can only mean one thing: the number of people reported

as still in the workforce has gone down. Since we’ve gained back only 1% of the jobs lost, this drop in the

unemployment rate is almost entirely due to people dropping out of the workforce.

Non-residential buildings has barely moved off

of the 2011 bottom.

Non-buildings heavy engineering peaked in 2010

but has been on the decline for 2 years.

Residential construction has been rebounding

since late 2010.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 17/48

13

Gilbane Building Company

Market Conditions In Construction – May 2012

While many workers are lost, the rst workers to be lost are typically those that represent the least value

to an organization, however, not all of the lost workers are “wanted turnover”. As the workload dwindled,

some of the workers that were let go or dropped out of the workforce had many years experience and were

highly trained. As a result, when work volume picks up there are going to be both general worker shortages

and as well as at least some shortage of these more valuable skilled workers. Over the next few years, when

work volume does pick up, this industry is going to be faced with a lack of available workers and shortage

of skilled, experienced workers. Both of those issues are going to DRIVE COSTS UP and QUALITY

DOWN due to the need to pay a premium for skilled workers and the necessity of training new workers in

their job and company procedures.

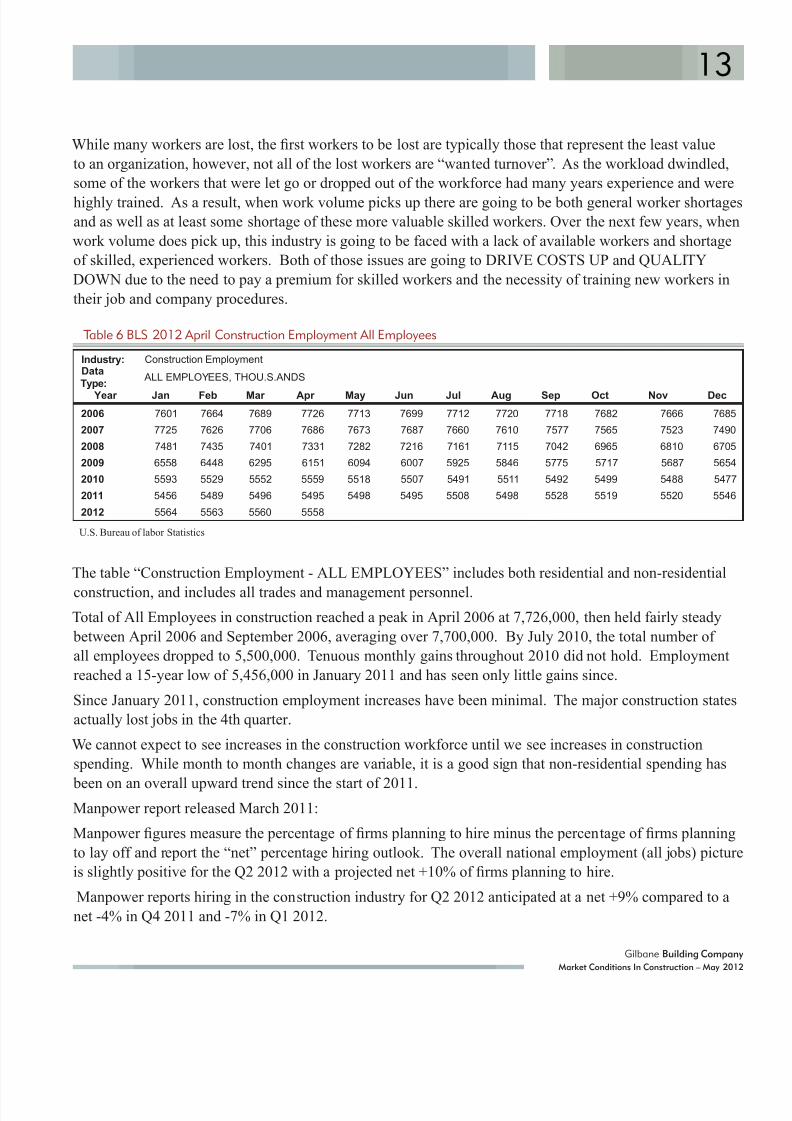

Table 6 BLS 2012 April Construction Employment All Employees

Industry: Construction Employment DataType:

ALL EMPLOYEES, THOU.S.ANDS

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2006 7601 7664 7689 7726 7713 7699 7712 7720 7718 7682 7666 7685

2007 7725 7626 7706 7686 7673 7687 7660 7610 7577 7565 7523 7490

2008 7481 7435 7401 7331 7282 7216 7161 7115 7042 6965 6810 6705

2009 6558 6448 6295 6151 6094 6007 5925 5846 5775 5717 5687 5654

2010 5593 5529 5552 5559 5518 5507 5491 5511 5492 5499 5488 5477

2011 5456 5489 5496 5495 5498 5495 5508 5498 5528 5519 5520 5546

2012 5564 5563 5560 5558

U.S. Bureau of labor Statistics

The table “Construction Employment - ALL EMPLOYEES” includes both residential and non-residential

construction, and includes all trades and management personnel.

Total of All Employees in construction reached a peak in April 2006 at 7,726,000, then held fairly steady

between April 2006 and September 2006, averaging over 7,700,000. By July 2010, the total number of

all employees dropped to 5,500,000. Tenuous monthly gains throughout 2010 did not hold. Employment

reached a 15-year low of 5,456,000 in January 2011 and has seen only little gains since.

Since January 2011, construction employment increases have been minimal. The major construction states

actually lost jobs in the 4th quarter.

We cannot expect to see increases in the construction workforce until we see increases in construction

spending. While month to month changes are variable, it is a good sign that non-residential spending has

been on an overall upward trend since the start of 2011.Manpower report released March 2011:

Manpower gures measure the percentage of rms planning to hire minus the percentage of rms planning

to lay off and report the “net” percentage hiring outlook. The overall national employment (all jobs) picture

is slightly positive for the Q2 2012 with a projected net +10% of rms planning to hire.

Manpower reports hiring in the construction industry for Q2 2012 anticipated at a net +9% compared to a

net -4% in Q4 2011 and -7% in Q1 2012.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 18/48

14

Gilbane Building Company

Market Conditions In Construction – May 2012

Manpower survey gures released in September 2011 indicated construction employment would decrease in

the fourth quarter That prediction was on target, with the top 9 states losing over 150,000 during the fourth

quarter.

Table 7 Construction Employees Major States

State Construction Employment # of Jobs

Four states account for 33% of ALL construction jobs.

current 12 mo last 4 mo

Texas 563,000 3,000 (41,000)

California 567,000 (3,000) (18,000)

Florida 319,000 (22,000) (15,000)

New York 301,000 (1,000) (25,000)

1,750,000 (23,000) (99,000)

Only ve other states have more than 150,000 construction jobs:current 12 mo last 4 mo

Pennsylvania 231,000 13,000 -

Illinios 190,000 (9,000) (29,000)

Virginia 182,000 500 (1,000)

North Carolina 177,000 6,000 1,000

Ohio 177,000 5,000 (9,000)

957,000 15,500 (38,000)

Where are the jobs?

Together these top 9 states make up 50%

of the national construction workforce.

The last (winter) report showed these

nine states combined had 39,000 more

jobs than a year ago. That has reversed

dramatically, showing the weakness in

jobs growth. Now they have 8,000 LESS

jobs than a year ago. And one year ago

total construction jobs had reached a 15

year low. The bad news is this group of

9 states lost 137,000 jobs in the 4 months

from Sep 2011 through Jan 2012. The

good news is the losses appear to have

been stemmed with the addition of 20,000

jobs in January.The big drop most probably reects the expected downturn

that was previously signaled by the falling ABI “work on the

boards” and construction Starts, among other indicators inthe middle of last year. National construction employment

totals increased by only 100,000 jobs during the same one year

period. Texas, which had been a jobs leader for the later half

of 2011, took the biggest drop.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 19/48

15

Gilbane Building Company

Market Conditions In Construction – May 2012

JOBS /PRODUCTIVITY

A long-term trend in productivity can be found by comparing the annual spending to the annual average

workforce. For this purpose we must use the ination adjusted spending, which will eliminate material,wage and margin ination/deation from the equation. Productivity is a measure of units per worker, not $

put in place per worker. This adjustment gives total spending in constant dollars and allows a comparison

to equal units. Therefore the following productivity analysis is based on put-in-place revenues, ination

adjusted to 2012 dollars, compared to actual manpower.

Table 8 Productivity Inflation Adjusted

Productivity Infation Adjusted 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Total Unadjusted $ Spending

848891 991 1,104 1,167 1,152 1,068 903 804 789 832

5.1% 11.2% 11.4% 5.7% -1.3% -7.4% -15% -11% -1.8% 5.4%

Total Spending 2012 $ 1,071 1,080 1,077 1,083 1,091 1,060 1,001 915 836 810 832

0.8% -0.2% 0.5% 0.7% -2.8% -5.6% -8.6% -8.6% -3.2% 2.8%

# jobs avg / yr mil lions 6,715 6,736 6,973 7,333 7,690 7,627 7,162 6,013 5,518 5,504 5,666

# jobs per billion$ unadjusted 7,919 7,558 7,033 6,641 6,588 6,619 6,709 6,658 6,867 6,974 6,808

# jobs per billion 2012 $ 6,268 6,238 6,472 6,774 7,051 7,194 7,158 6,572 6,599 6,797 6,808

productivity change 0.5% -3.6% -4.5% -3.9% -2.0% 0.5% 8.9% -0.4% -2.9% -0.2%

At rst glance, Figure 5 seems to indicate the number of jobs supported by $1 billion dollars of spending

declined from 2002 to 2006 (the thin black line). Fewer workers to perform the same unit volume of work

would indicate an increase in productivity. If productivity was increasing, then each succeeding year it

would take fewer workers to produce the same work volume and the number of jobs would be declining.But you can see that line would go counter to expectations. It shows increasing productivity in times

of increasing workload. What’s missing in that analysis is the dollar volume of work put in place is not

ination adjusted, so it indicates work $ value, but not true work unit volume.

Figure 5 Jobs per billion dollars spending adjusted

JOBS per $bil ajusted to 2012$

#jobs per$bi

unadjustedl #jobs per $bil

in 2012$

5,500

6,000

6,500

7,000

7,500

8,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

# of Jobs needed to support $1 billion spending

To get the real picture of

productivity changes we must

adjust all dollars to the same

point in time, here adjusted to

2012$. Once we’ve done that,we see the adjusted data in Figure

5 (the thicker blue line) shows

productivity declining in lock-step

with rapid volume growth and

improving as work volume drops.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 20/48

16

Gilbane Building Company

Market Conditions In Construction – May 2012

From 2003 through 2007, the number of workers needed to put in place $1 billion of spending

increased. In other words, productivity decreased during that period when spending and jobs were on

the rapid growth trend. That result is perfectly in line with expectations during rapid growth. As we

approached peak employment in 2006-2007 we also approached peak spending, but the number of jobs

supported by $1 billion of spending was increasing. In 2002 through 2004, $1 billion of spending supported

just under 6,500 jobs. By the peak activity in 2006-2007, it required 7,300 jobs to put-in-place $1 billion

in spending, (less work value per employee). Productivity declined to its lowest point in 2005. But work

volume reversed and by the end of 2009, productivity increases were so signicant that $1 billion of

spending supported only 6,600 jobs. Today $1 billion in spending supports 6,800 jobs.

Figure 6 Productivity Changes 2003-2012

Productivity Changes

annual change

cum since 2007

since 2005

since 2006

-7.0%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

values above 0% = productivity gains

values below 0% = productivity declines

From 2007 through 2010, the number of workers needed to put in place $1 billion of spending

declined. This indicates each worker accomplished more work. In other words, productivity increased

during that entire period when spending and jobs were on the decline. Those are clear indications that

productivity will be increasing. Out of necessity, and with diminished workload providing no other options,

workers and management nd ways to improve. But that can and always does reach a limit. At some point,

longer hours and additional work burden causes productivity to decline. Also, a return to volume growth

results in an easing of performance. It appears the trend reversed in 2011. After 4 years of mostly work

output increases, the work output declined dramatically in 2011.

Over a period of 5 years (since 2006) the net gain in productivity is 4%. That means that it would take 4%

less workforce to put in place the equivalent volume of work today as it would have taken in 2006. That

also means if we were to maintain that 4% productivity advantage, then at some point in the future, when

work volume does return to previous peak levels, it would require 4% less total workforce to accomplish

that workload.

It is well known that productivity

decreases in times of increasing

activity,. Productivity generally

increases as available work declines.

(Applied Cost Engineering, Chapter

5, Clark and Lorenzoni, Marcel

Dekker, Inc., 1985). This graphic,

Productivity Changes, portrays this

concept almost perfectly.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 21/48

17

Gilbane Building Company

Market Conditions In Construction – May 2012

As workload begins to increase in coming years, net productivity gains will decline somewhat. This net

affect cannot go unaddressed. The results of productivity declines are either decreased total output (if

workforce remains constant) or increased workforce needed (if total workload remains constant). Even with

the drop in 2011, fewer workers are needed currently to accomplish the same work volume as compared to

any time since 2005. However, that is already changing.

Realistically, I would expect that over the next few years, each year work volume increases we will

experience some slight erosion from the productivity gains. That means when we do once again recover to

the spending levels of years past, we will not recover to the number of jobs in years past. This erosion can

be offset by signicant technological and process advancements. I expect some of what we saw in 2009 can

be attributed to those two issues.

Earlier I asked, Why is it significant to analyze both revenue and volume?

Contractor fees are often determined as a percentage of revenue. However, workload volume is used for

planning the size of the workforce needed to accommodate the annual workload. It is valuable to know

from the past several years of data how many employees were required to accomplish the workload volume.

From the viewpoint of workforce determination, we should not be concerned with the value of the revenue,

only the volume of the work.

A S AN EXAMPLE:

At the peak of construction, a building cost $12 million and took 100 men/yr to build. Today that samebuilding could potentially cost as little as $10 million to build. Does it take 20% less men/yr to build it? No,certainly not. That would be the fallacy of trying to determine jobs needed based on revenue.

The building has not changed, only its cost changed. It still has the same amount of steel and concrete and

brick and windows. The only thing we can say is we’ve had an improvement of 4% in productivity. Therefore the workforce today will be 4% lower. Using revenue as a basis we might be led to think we need 20% fewerworkers. That points to the value to base workers needed on inflation adjusted volume, not direct annualrevenue.

How quickly can we recover from a 30% decline in the workforce?

The most rapid expansion in the workforce during the last 10 years was the period from mid-2003 to

mid-2006. In that 36-month period, the construction labor workforce expanded by 1,000,000 jobs, 15%.

Therefore, during the strongest period of expansion in the last 10 years, the workforce expanded by only

15% over 3 years, or an average of 28,000 jobs per month. What’s signicant is that ination adjusted

volume increased by only 10%. Such a signicant workforce expansion led to measurable lost productivity.Even if we could realize a similar rate of growth, which was associated with a high rate of economic

expansion, it would take 6 years to recover more than 2 million lost jobs. At this accelerated rate the

workforce would not return to previous levels before 2017. That is a very unlikely scenario, since it would

require uninterrupted elevated economic expansion. It is highly unlikely we will see the workforce return

to previous levels within 6 years. Furthermore, if we experience uninterrupted economic expansion at this

level for the next 6 years, productivity is going to plummet erasing all of the gains realized in the last few

years and more.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 22/48

18

Gilbane Building Company

Market Conditions In Construction – May 2012

The rate of employment growth may be a valid concern for the following reason; if spending and jobs are

to remain balanced and return to normal, then both the rate of expansion in construction spending and the

rate of growth in the workforce needs to be approximately equal in the coming years. If the rate of spending

growth exceeds a normal the rate of growth, it will produce an extremely active market, there will be worker

shortages and productivity will drop. Also, when that occurs, it leads to rapidly increasing prices and

elevated margins.

CONSTRUCTION COSTS GENERAL

Industrial production related to construction is up 5 months in a row and is up over 7.5% in 12 months since

February 2011.

Fabricated metal products industry reported production is up, prices paid are lower and Backlog of

Orders is up.

Of items used in construction, copper, copper wire, copper pipe, aluminum, diesel fuel and plastics are all

still UP in price over the last 3 months. Structural shapes are down in price over 3 months.

Concrete and steel, the major drivers of building structure cost, are both experiencing low cost increases.

Concrete contractor pricing is up less than 1.5% over the year and more recently is down. Fabricated

structural products are up less than 2.5% over the year.

In March, Ken Simonson, AGC Chief Economist, said he expects materials prices to range from 4% to 9%

during the year, but to end at 5% to 6% increases for the year 2012. Labor is expected to nish the year up

1.5% to 2.5%.

Manufacturing capacity utilization had been uctuating between 76% and 77% since November 2010. In

July it increased just above 77%, by October it was approaching 78% and since December it has been near

79%. Typically, the capacity utilization index needs to be consistently above 80 before we see an expansion

of construction spending in the manufacturing sector. Spending in this sector is still down 23% from last

year. That will keep prices in that sector depressed.

M ATERIAL PRICE MOVEMENT

The overall Producer Price Index (PPI) for February 2012 shows cost for construction materials are up 4.4%

in the last 12 months. Costs for material inputs to non-residential construction are up 4.6% in the last 12months. Prices for completed buildings are up on average 4.0%.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 23/48

19

Gilbane Building Company

Market Conditions In Construction – May 2012

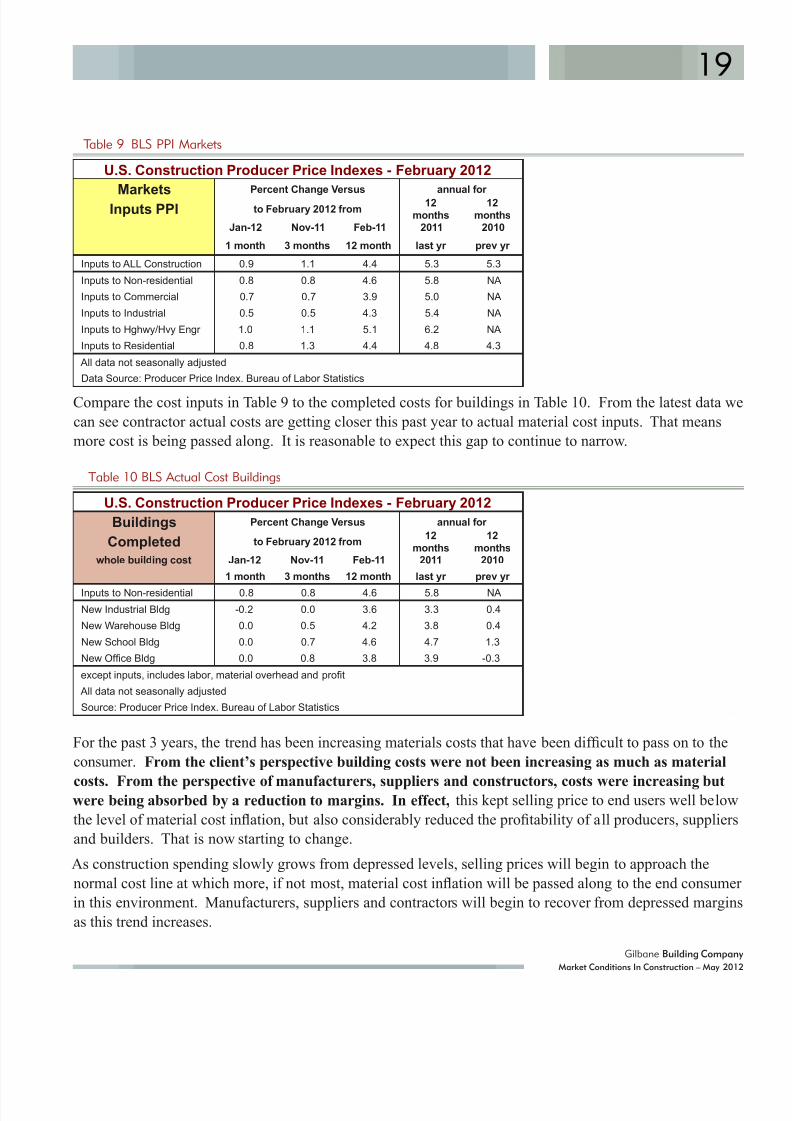

Table 9 BLS PPI Markets

U.S. Construction Producer Price Indexes - February 2012

MarketsPercent Change Versus annual for

Inputs PPI to February 2012 from12

months12

months Jan-12 Nov-11 Feb-11 2011 2010

1 month 3 months 12 month last yr prev yr

Inputs to ALL Construction 0.9 1.1 4.4 5.3 5.3

Inputs to Non-residential 0.8 0.8 4.6 5.8 NA

Inputs to Commercial 0.7 0.7 3.9 5.0 NA

Inputs to Industrial 0.5 0.5 4.3 5.4 NA

Inputs to Hghwy/Hvy Engr 1.0 1.1 5.1 6.2 NA

Inputs to Residential 0.8 1.3 4.4 4.8 4.3

All data not seasonally adjusted

Data Source: Producer Price Index. Bureau of Labor Statistics

Compare the cost inputs in Table 9 to the completed costs for buildings in Table 10. From the latest data we

can see contractor actual costs are getting closer this past year to actual material cost inputs. That means

more cost is being passed along. It is reasonable to expect this gap to continue to narrow.

Table 10 BLS Actual Cost Buildings

U.S. Construction Producer Price Indexes - February 2012

Buildings Percent Change Versus annual for

Completed to February 2012 from12

months12

monthswhole building cost Jan-12 Nov-11 Feb-11 2011 2010

1 month 3 months 12 month last yr prev yr

Inputs to Non-residential 0.8 0.8 4.6 5.8 NA

New Industrial Bldg -0.2 0.0 3.6 3.3 0.4

New Warehouse Bldg 0.0 0.5 4.2 3.8 0.4

New School Bldg 0.0 0.7 4.6 4.7 1.3

New Ofce Bldg 0.0 0.8 3.8 3.9 -0.3

except inputs, includes labor, material overhead and prot

All data not seasonally adjusted

Source: Producer Price Index. Bureau of Labor Statistics

For the past 3 years, the trend has been increasing materials costs that have been difcult to pass on to the

consumer. From the client’s perspective building costs were not been increasing as much as material

costs. From the perspective of manufacturers, suppliers and constructors, costs were increasing butwere being absorbed by a reduction to margins. In effect, this kept selling price to end users well below

the level of material cost ination, but also considerably reduced the protability of all producers, suppliers

and builders. That is now starting to change.

As construction spending slowly grows from depressed levels, selling prices will begin to approach the

normal cost line at which more, if not most, material cost ination will be passed along to the end consumer

in this environment. Manufacturers, suppliers and contractors will begin to recover from depressed margins

as this trend increases.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 24/48

20

Gilbane Building Company

Market Conditions In Construction – May 2012

Table 11 BLS Actual Cost Trades

U.S. Construction Producer Price Indexes - February 2012

TradesPercent Change Versus annual for

Non-residential to February 2012 from12

months12

monthswhole trade bid cost Jan-12 Nov-11 Feb-11 2011 2010

1 month 3 months 12 month last yr prev yr

Inputs to Non-residential 0.8 0.8 4.6 5.8 NA

Concrete -0.2 -0.5 1.1 1.3 0.4

Roong 0.0 0.7 4.2 4.3 -1.9

Electrical 0.8 1.2 4.1 3.8 1.1

Plumbing / HVAC -0.1 0.8 4.3 3.6 1.7

except inputs, includes labor, material overhead and prot

All data not seasonally adjusted

Source: Producer Price Index. Bureau of Labor Statistics

I expect whole building costs to rise, but a bit slower than material/labor ination.

Indicators are pointing to growth signs and that will eventually lead to a more normal bidding environment.

That in turn will allow builders to pass along ever greater percentages of cost increases. Concrete trades

over the last year increased prices only about 1%, but Roong Electrical and Plumbing / HVAC trades all

increased prices on average 4%.

NOTABLE MATERIALS CHANGES OVER THE LAST 12 MONTHS THROUGH FEBRUARY :

diesel fuel +14%

gypsum products +15%

copper and brass shapes -11%

steel pipe +10%

asphalt paving +11%

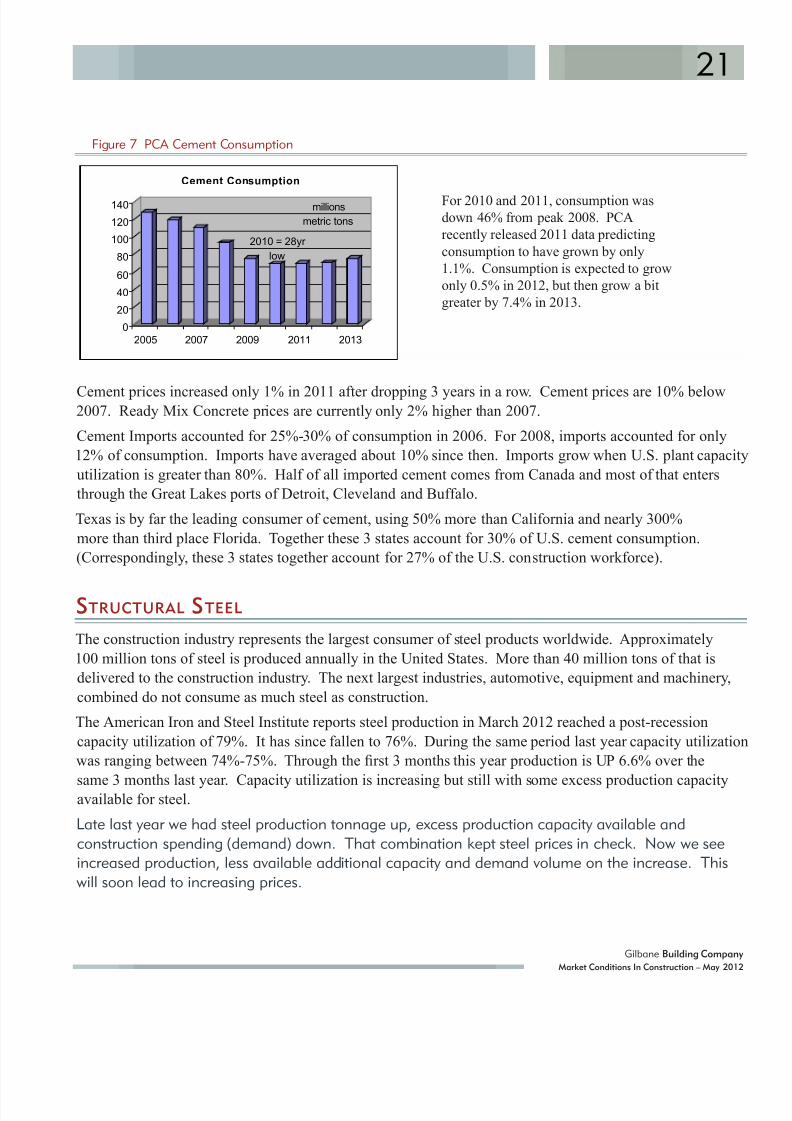

CEMENT / CONCRETE

Portland Cement Association (PCA) reports the volume of cement demand as an indicator of economic

activity. It is a reliable coincident indicator.

Nearly two-thirds of U.S. cement consumption occurs in the six months between May and October. Rising

consumption and prices leading into summer can lead to large shifts in demand and seasonal pricing andis not an indicator of long term growth but only reects periodic seasonal uc0tuating consumption rates.

Look at total annual volumes for trends.

Cement ProductionIn 2008 U.S. cement plants were operating at a capacity utilization of 82%. In Fall 2011, cement plant

capacity utilization, considered depressed, was 60%. The rate of decline in consumption helps explain the

60% capacity utilization. In 2010, cement production and consumption hit a 28-year low.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 25/48

21

Gilbane Building Company

Market Conditions In Construction – May 2012

Figure 7 PCA Cement Consumption

millions

metric tons

2010 = 28yr

low

0

20

40

60

80

100

120

140

2005 2007 2009 2011 2013

Cement Consumption

Cement prices increased only 1% in 2011 after dropping 3 years in a row. Cement prices are 10% below2007. Ready Mix Concrete prices are currently only 2% higher than 2007.

Cement Imports accounted for 25%-30% of consumption in 2006. For 2008, imports accounted for only

12% of consumption. Imports have averaged about 10% since then. Imports grow when U.S. plant capacity

utilization is greater than 80%. Half of all imported cement comes from Canada and most of that enters

through the Great Lakes ports of Detroit, Cleveland and Buffalo.

Texas is by far the leading consumer of cement, using 50% more than California and nearly 300%

more than third place Florida. Together these 3 states account for 30% of U.S. cement consumption.

(Correspondingly, these 3 states together account for 27% of the U.S. construction workforce).

STRUCTURAL STEEL

The construction industry represents the largest consumer of steel products worldwide. Approximately

100 million tons of steel is produced annually in the United States. More than 40 million tons of that is

delivered to the construction industry. The next largest industries, automotive, equipment and machinery,

combined do not consume as much steel as construction.

The American Iron and Steel Institute reports steel production in March 2012 reached a post-recession

capacity utilization of 79%. It has since fallen to 76%. During the same period last year capacity utilization

was ranging between 74%-75%. Through the rst 3 months this year production is UP 6.6% over the

same 3 months last year. Capacity utilization is increasing but still with some excess production capacityavailable for steel.

Late last year we had steel production tonnage up, excess production capacity available andconstruction spending (demand) down. That combination kept steel prices in check. Now we seeincreased production, less available additional capacity and demand volume on the increase. Thiswill soon lead to increasing prices.

For 2010 and 2011, consumption wasdown 46% from peak 2008. PCA

recently released 2011 data predicting

consumption to have grown by only

1.1%. Consumption is expected to grow

only 0.5% in 2012, but then grow a bit

greater by 7.4% in 2013.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 26/48

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 27/48

23

Gilbane Building Company

Market Conditions In Construction – May 2012

COPPER

Copper material prices hit an all-time high of $4.60/lb in February 2011, up 25% from October 2010. By

September 2011 the price dropped back to $3.10/lb. The price as of April 4, 2012 was just under $3.85/lb,15% below where it was a year ago.

WHAT MAKES COPPER SO IMPORTANT TO WATCH?

Copper is a leading economic indicator that has rarely (if ever) failed to indicate the direction of world

economies. When copper rises in price, world economies are leading into expansion. When copper drops

in price, a decline in world economies very quickly follows. Copper prices and the U.S. workforce move

almost perfectly together. Also, because copper is so widely used in buildings, and manufacturing facilities

must be built to see a big increase in production, copper demand precedes and is an excellent predictor of

industrial production 12 months out.

For a visual representation of the copper prices, visit:

http://metalprices.com/PubCharts/PublicCharts.aspx?metal=cu&type=L&weight=LB&days=60&size=M&bg=&cs=1011&cid=0

What drives copper prices up or down? Unlike some other metals, it is not speculation. Quite often it is

demand. Increasing demand = increasing prices. When demand wanes, prices drop. Analysts predict

copper will average $4.00/lb in 2012.

WHAT AFFECT DO COPPER PRICE CHANGES HAVE ON THE COST OF OUR PROJECTS?

ROUGHLY SPEAKING, COPPER MATERIAL IS ABOUT:

10% of an Electrical contract or 1% of cost of project

5% of an HVAC contract or 0.6% of cost of project

10% of a Plumbing contract or 0.3% of cost of project

So, for an average project, copper material can represent approximately 2% of the total cost of the project.

Therefore, a 25% increase in the cost of copper will increase the cost of a project by 0.5%.

There may be exceptions. For example, if copper is 2% of the total cost of the typical project, it is probably

4% to 5% of total cost on a heavy mechanical/electrical project, like a data center. So a 25% increase in the

cost of copper increases the total cost of a data center by 1% to 1.5%. For a copper roof, material is 65% of

total cost and can represent ~1% of typical project cost.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 28/48

24

Gilbane Building Company

Market Conditions In Construction – May 2012

PRODUCER PRICE INDEX

The February 2012 2011 Producer Price Index for Material Inputs to Construction increased 1.1% over the

last 3 months and is up 4.4% over the past 12 months.

The February 2012 PPI for Material Inputs to Non-residential Construction decreased 0.8% over the last 3months and is up 4.6% over the past 12 months.

PPI for Trade Contractors nal costs and Whole Building nal costs is UP, but up only about 4% in 12

months. See Materials Price Movement for Contractor Installed Prices and Finished Building Prices.

Table 12 BLS PPI Construction Related Materials

U.S. Construction Producer Price Indexes - February 2012

Materials Percent Change Versus annual for

to February 2012 from12

months

12

months Jan-12 Nov-11 Feb-11 2011 2010

1 month 3 months 12 month last yr prev yr

Summary

Inputs to ALL Construction 0.9 1.1 4.4 5.3 5.3

Inputs to Non-residential 0.8 0.8 4.6 5.8 NA

Commodities

Cement -2.4 1.3 2.2 1.1 -6.0

Iron & Steel Scrap -6.2 3.5 -4.5 11.1 38.9

Manufactured Materials

Diesel Fuel 3.0 -2.0 14.5 20.2 26.4

Asphalt Paving 2.5 4.3 11.3 8.4 4.4

Asphalt Roong -0.5 -2.4 -1.9 2.6 1.9

Ready Mix Concrete -0.2 1.0 1.5 0.6 -1.2

Concrete Block & Brick -0.1 0.3 1.8 1.1 -1.1

Precast Conc Products 0.1 0.2 0.1 2.6 1.0

Building Brick 0.2 -3.4 -2.9 -2.6 -0.3

Copper / Brass Mill Shapes 5.9 4.7 -11.2 -9.3 11.8

Aluminum Mill Shapes 1.9 -0.8 -0.8 0.1 11.6

Steel Mill Products 0.6 1.3 4.0 11.3 12.5

Steel Pipe and Tube -0.8 4.9 10.0 12.1 19.6

Fab. Structural Steel 1.9 1.2 2.5 4.4 1.9

Fab. Bar Joists and Rebar 2.4 0.7 1.4 2.8 -0.3

Gypsum Products 5.1 12.0 15.2 -1.5 3.2

Insulation Materials 0.4 3.3 5.0 5.4 4.6Lumber and Plywood 1.7 2.3 -0.7 -0.8 5.7

Sheet Metal Products -0.5 -2.1 2.4 5.8 4.0

All data not seasonally adjusted

Source: Producer Price Index. Bureau of Labor Statistics

The primary factor keeping total costs down right now is high level of competition for a slowly increasing

volume of new work. The price asked for subcontract work and for nished buildings is slowly starting to

catch up with the rate of material cost increases.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 29/48

25

Gilbane Building Company

Market Conditions In Construction – May 2012

THE PPI FOR ITEMS THAT CONTRIBUTED THE MOST TO THE 3 MONTH AND YEARLY CHANGE INCLUDED:

Diesel fuel prices dropped 2% recently but climbed 14% over the last year Asphalt paving is up 4% in 3 months and up 11% over the year

Gypsum products rose 12% in 3 months and 15% over the year

Steel pipe and tube rose 5% in 3 months and but rose 10% over the year

Is the PPI for Construction Materials = Escalation? NO!

IS THE MOVEMENT OF THE PPI A GOOD INDICATOR OF FUTURE ESCALATION? NO!

Indexes like the PPI MTRLS deal ONLY with materials costs or prices charged at the producer level. They

do not include delivery, equipment, installation, or markups. In fact, they do not even reect the retail pricecharged to contractors. Nor do they reect the cost of services provided by the GC or CM.

Total project cost encompasses all of these other costs. Trade Contractor PPI and Whole Building PPI

doesn’t give us any details about the retail price of the materials used, but it does include all of the

contractors costs incurred for delivery, equipment for installation, labor for installation and markups on the

nal product delivered to the consumer, the building.

The PPI for construction materials IS NOT an indicator of construction ination. It is missing the selling

price. In 2010, the PPI for construction inputs was up 5.3% but the selling price was at. In 2009 PPI for

Inputs was at but construction ination as measured by cost of buildings was down 8%-10%.

Construction Starts and construction spending are still near 10-year lows, and therefore there is little workavailable out for bid, forcing contractors to remain extremely competitive. As a result, they areunable

to pass on all cost increases to clients. This has the effect of keeping selling price low, reducing both

contractors and producers margins. In some cases margins may be reduced to a loss just to get work.

Construction cost escalation is moving closer to track in line with the PPI for construction materials. But it

will take continued increases in the levels of activity to enforce the narrowing of the gap between the two.

I do not expect cost escalation to track in-line with PPI for at least 1 to 2 years. Until then, do notbase building cost growth on the increase in construction materials PPI.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 30/48

26

Gilbane Building Company

Market Conditions In Construction – May 2012

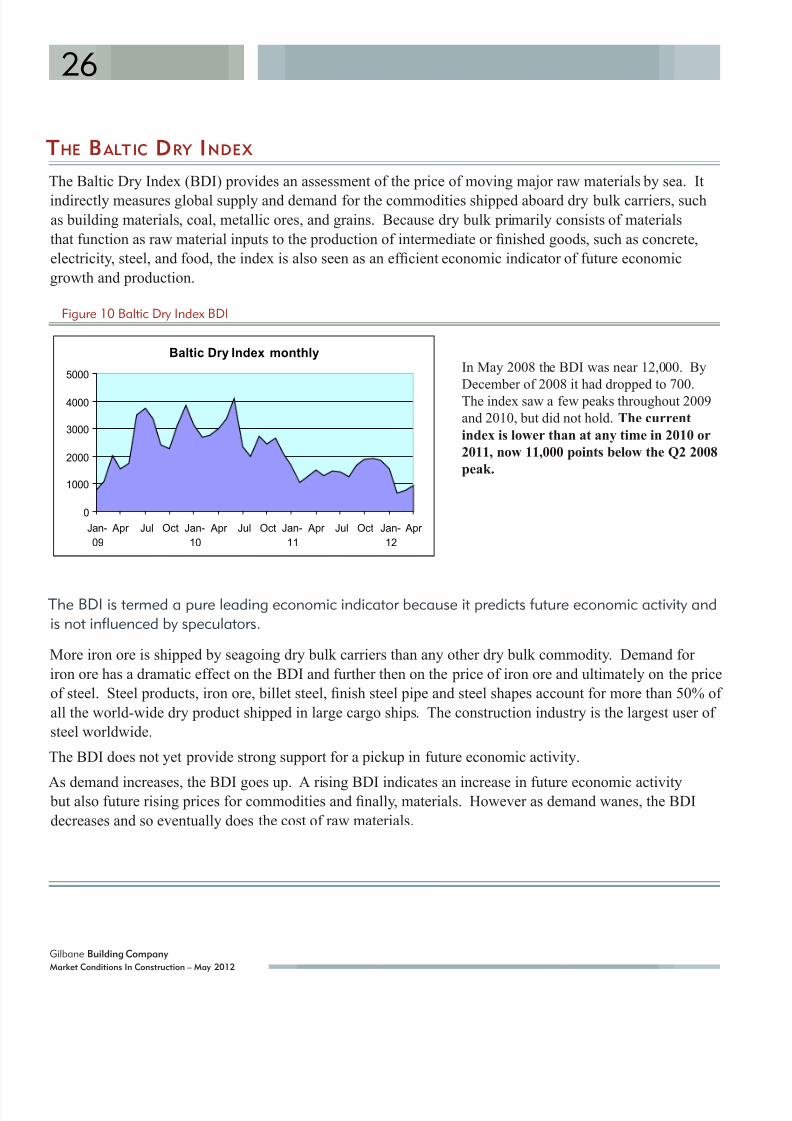

THE B ALTIC DRY INDEX

The Baltic Dry Index (BDI) provides an assessment of the price of moving major raw materials by sea. It

indirectly measures global supply and demand for the commodities shipped aboard dry bulk carriers, suchas building materials, coal, metallic ores, and grains. Because dry bulk primarily consists of materials

that function as raw material inputs to the production of intermediate or nished goods, such as concrete,

electricity, steel, and food, the index is also seen as an efcient economic indicator of future economic

growth and production.

Figure 10 Baltic Dry Index BDI

Baltic Dry Index monthly

0

1000

2000

3000

4000

5000

Jan-

09

Apr Jul Oct Jan-

10

Apr Jul Oct Jan-

11

Apr Jul Oct Jan-

12

Apr

The BDI is termed a pure leading economic indicator because it predicts future economic activity andis not influenced by speculators.

More iron ore is shipped by seagoing dry bulk carriers than any other dry bulk commodity. Demand for

iron ore has a dramatic effect on the BDI and further then on the price of iron ore and ultimately on the price

of steel. Steel products, iron ore, billet steel, nish steel pipe and steel shapes account for more than 50% of

all the world-wide dry product shipped in large cargo ships. The construction industry is the largest user of

steel worldwide.

The BDI does not yet provide strong support for a pickup in future economic activity.

As demand increases, the BDI goes up. A rising BDI indicates an increase in future economic activity but also future rising prices for commodities and nally, materials. However as demand wanes, the BDI

decreases and so eventually does the cost of raw materials.

In May 2008 the BDI was near 12,000. By

December of 2008 it had dropped to 700.

The index saw a few peaks throughout 2009

and 2010, but did not hold. The current

index is lower than at any time in 2010 or

2011, now 11,000 points below the Q2 2008

peak.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 31/48

27

Gilbane Building Company

Market Conditions In Construction – May 2012

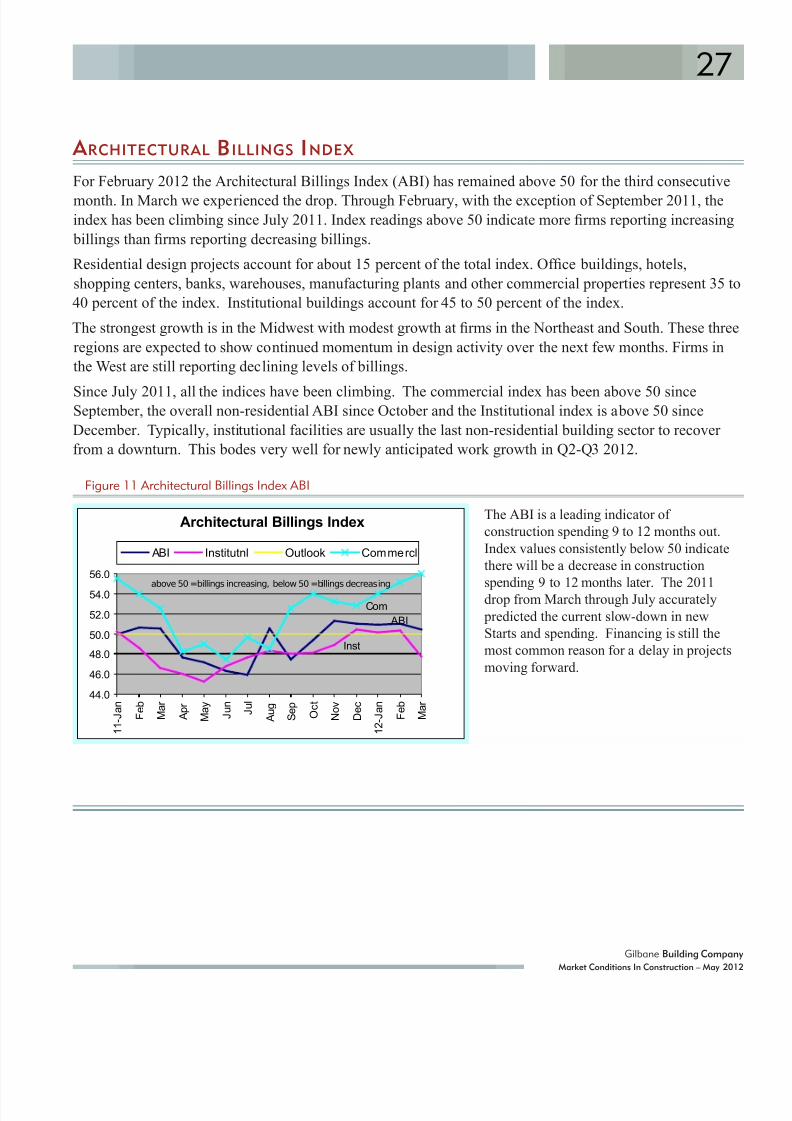

A RCHITECTURAL B ILLINGS INDEX

For February 2012 the Architectural Billings Index (ABI) has remained above 50 for the third consecutive

month. In March we experienced the drop. Through February, with the exception of September 2011, theindex has been climbing since July 2011. Index readings above 50 indicate more rms reporting increasing

billings than rms reporting decreasing billings.

Residential design projects account for about 15 percent of the total index. Ofce buildings, hotels,

shopping centers, banks, warehouses, manufacturing plants and other commercial properties represent 35 to

40 percent of the index. Institutional buildings account for 45 to 50 percent of the index.

The strongest growth is in the Midwest with modest growth at rms in the Northeast and South. These three

regions are expected to show continued momentum in design activity over the next few months. Firms in

the West are still reporting declining levels of billings.

Since July 2011, all the indices have been climbing. The commercial index has been above 50 sinceSeptember, the overall non-residential ABI since October and the Institutional index is above 50 since

December. Typically, institutional facilities are usually the last non-residential building sector to recover

from a downturn. This bodes very well for newly anticipated work growth in Q2-Q3 2012.

Figure 11 Architectural Billings Index ABI

Architectural Billings Index

ABI

Inst

Com

44.0

46.0

48.0

50.0

52.0

54.0

56.0

1 1 - J a n

F e b

M a r

A p r

M a y

J u n

J u l

A u g

S e p

O c t

N o v

D e c

1 2 - J a n

F e b

M a r

above 50 =billings increasing, below 50 =billings decreasing

ABI Institutnl Outlook Commercl

The ABI is a leading indicator of

construction spending 9 to 12 months out.

Index values consistently below 50 indicate

there will be a decrease in construction

spending 9 to 12 months later. The 2011drop from March through July accurately

predicted the current slow-down in new

Starts and spending. Financing is still the

most common reason for a delay in projects

moving forward.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 32/48

28

Gilbane Building Company

Market Conditions In Construction – May 2012

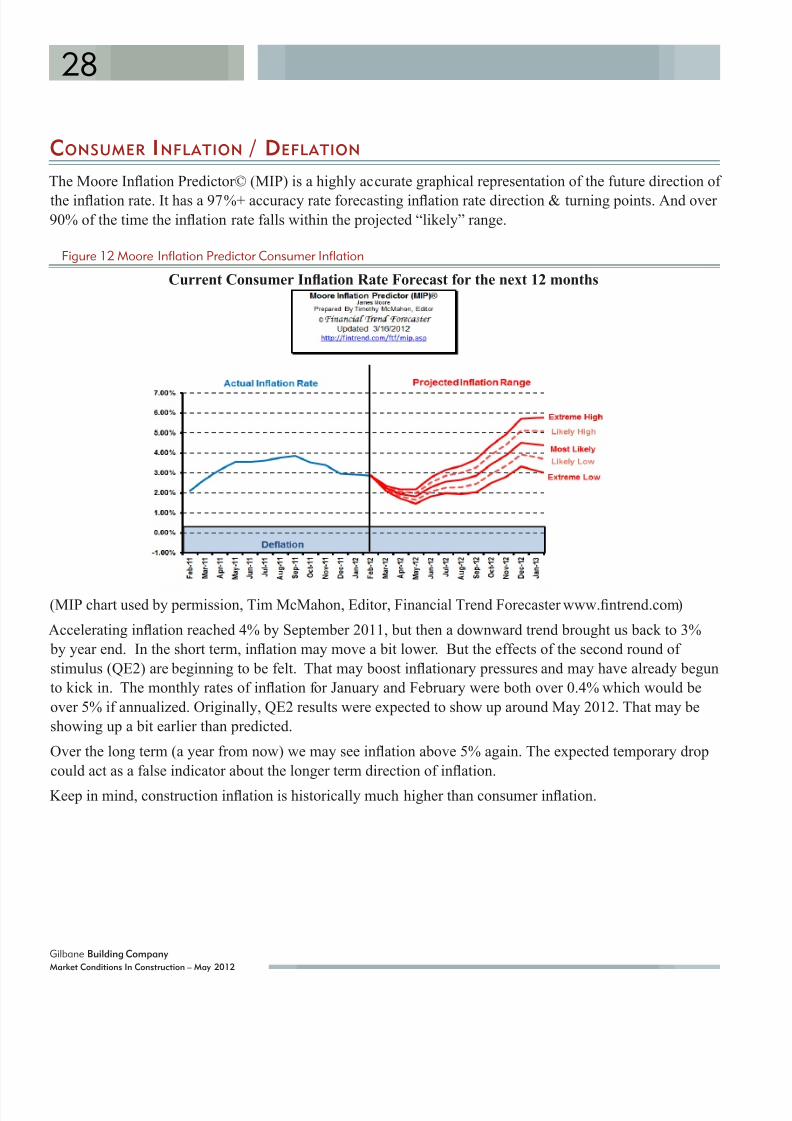

CONSUMER INFLATION / DEFLATION

The Moore Ination Predictor© (MIP) is a highly accurate graphical representation of the future direction of

the ination rate. It has a 97%+ accuracy rate forecasting ination rate direction & turning points. And over90% of the time the ination rate falls within the projected “likely” range.

Figure 12 Moore Inflation Predictor Consumer Inflation

Current Consumer Ination Rate Forecast for the next 12 months

(MIP chart used by permission, Tim McMahon, Editor, Financial Trend Forecaster www.ntrend.com)

Accelerating ination reached 4% by September 2011, but then a downward trend brought us back to 3%

by year end. In the short term, ination may move a bit lower. But the effects of the second round of

stimulus (QE2) are beginning to be felt. That may boost inationary pressures and may have already begun

to kick in. The monthly rates of ination for January and February were both over 0.4% which would be

over 5% if annualized. Originally, QE2 results were expected to show up around May 2012. That may be

showing up a bit earlier than predicted.

Over the long term (a year from now) we may see ination above 5% again. The expected temporary drop

could act as a false indicator about the longer term direction of ination.

Keep in mind, construction ination is historically much higher than consumer ination.

8/10/2019 GBCo Market Conditions Spring 2012

http://slidepdf.com/reader/full/gbco-market-conditions-spring-2012 33/48

29

Gilbane Building Company

Market Conditions In Construction – May 2012

CONSTRUCTION INFLATION FORECAST

Construction ination, based on several decades of trends, is double consumer ination. Since mid-2009that long term trend has not held up. Recent construction ination continues to be inuenced primarily by

bid margins which have been low due to low work volume. If it holds true that long-term trends eventually

return to the norm, we may be headed for some serious construction ination down the road.

From January through April 2011 consumer ination shot up to 3%. At that time expectations were that

consumer ination would continue to climb through the year, potentially to a range just above 5% with a

drop back to 3% expected by May 2012. We see now that it reached near 4% by September and returned to

3% by year end and may go lower by May. But that short-term downward trend should then turn upwards

and move closer to 5% a year from now.

Normally we would expect construction ination to come in near double that range. Construction materials

currently are below that trend. However, keep in mind, because of current low demand, prices are being

held down. Construction materials ination is low year to date, but increased signicantly in the latest

month. As demand increases in coming months, construction ination may climb rapidly.

Until construction spending returns to normal, I expect total construction escalation cost passed on to

owners might be somewhat subdued, perhaps no more than 4%. Subdued nished building prices will be

inuenced by aggressive bidding. This will change quickly as bidding volume increases.

SOME S IGNS A HEAD

The Institute for Supply Management (ISM) report released April 2, 2012, shows the national Purchasing

Manager’s Index (PMI) is 53.4%. It is growing stronger. PMI values above 42.5 indicate overall economic

expansion. Index values above 50 indicate expansion in the manufacturing sector. Fabricated metal

products industry reported production is up, prices paid are lower and Backlog of Orders is up.

The ISM Non Manufacturing Index (NMI) measures economic activity in several industries (including

construction) not covered in the manufacturing sector. The NMI for March is 56.0, down from February,

but still growing, although at a slower rate. The New Orders and Backlog Indexes declined for the month.

A respondent from the construction industry commented, “We are starting to see the private sector building

again.”

Industrial production related to construction is up 5 months in a row and is up over 7.5% in 12 months since

February 2011.

The Conference Board Leading Economic Index (LEI) is up 5 months in a row through February. After 5