Embed Size (px)

Citation preview

GCC supply chain and logistics conference 2015, Muscat

Presentation by

Kim Fejfer

CEO, APM Terminals

Oman - Positioned To Win in a Dynamic World

April 15, 2015

APM Terminals: part of Maersk Group with a long and rich history in Oman

2

APM Terminals: A balanced global network serving all major markets

Agenda

1. Economic Trends

2. Container Shipping Trends

3. Oman – How to Win

4. Conclusion

4

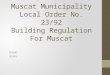

World Economy – Developed markets recover but growth still driven by emerging markets

5

Source: IMF, Jan 2015

*All GDP taken at constant prices

GDP Growth Rate

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

World Developed

Economies

Emerging

Economies

2014 2015 2016

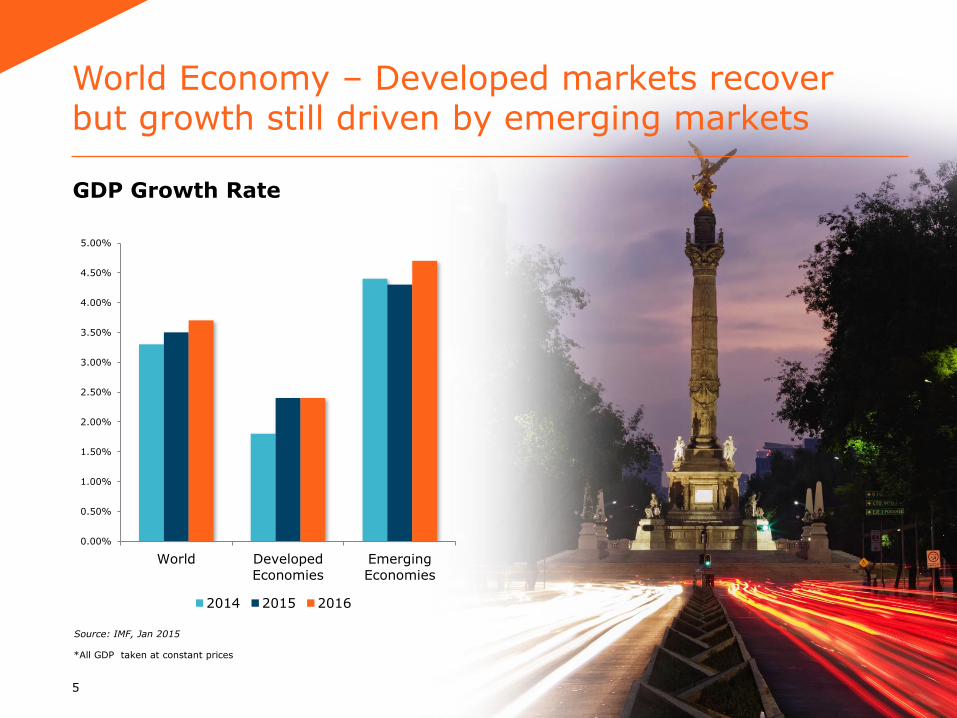

World Economy – Developed markets recover but …………

6

GDP Growth Rate

Source: IMF, Jan 2015

*All GDP taken at constant prices

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

USA Euro Area Germany France Italy

2014 2015 2016

World Economy – Emerging markets drive growth but oil producing countries under pressure

7

GDP Growth Rate

Source: IMF, Jan 2015

*All GDP taken at constant prices

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Brazil Russia India China GCC

2014 2015 2016

Container Shipping Trends

• Ever larger container ships

• Carrier alliances

• Freight rate instability

• Pure Transhipment hubs under pressure

• Stringent Environmental Guidelines

8

0

4

8

12

Annualised in m

illion t

eu

Independent Alliance

Source: Drewry Research

10

12

14

16

18

20

22

2012 2016

Fle

et

Capacity -

Million T

eu N

om

inal

>10,000 teu 7,500 - 9,999 TEU < 7,500 TEU

Source: Alphaliner November 2014

Capacity Deployment Pattern: Asia-Europe

Larger containerships adding global fleet capacity:

9

Vessel Size by Capacity (TEUs)

(Source: Alphaliner Februaury 2015)

There are currently 138 Ultra-Large Container Ships (10,000 TEU+) on order

Number of Vessels on Order

138

92

24 18

78

56

40

7

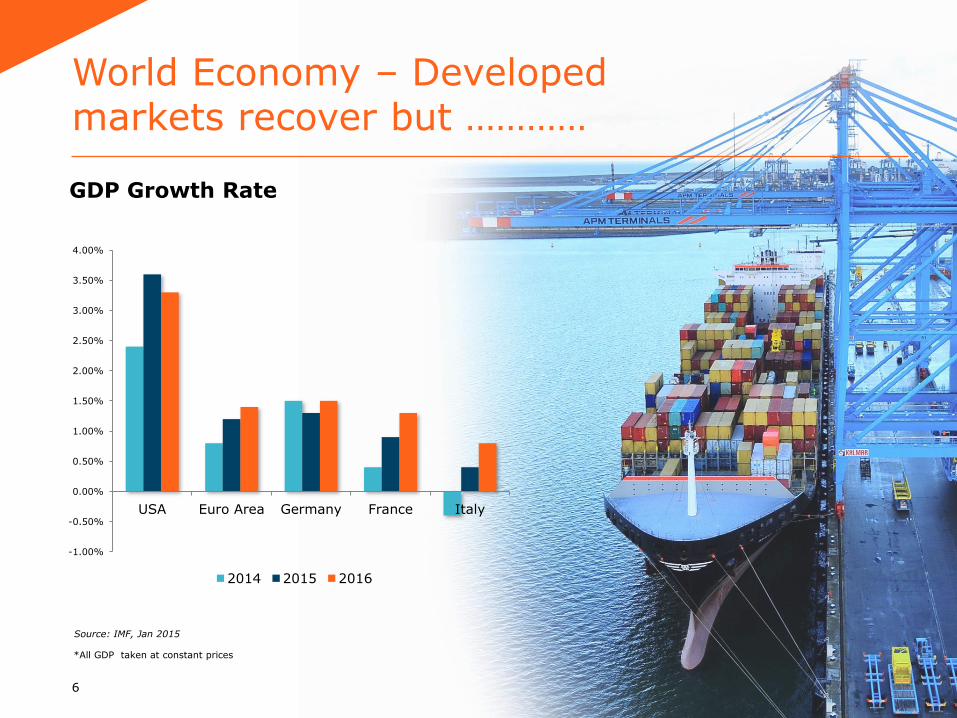

Container shipping Trends – Impact on Ports Infrastructure

10

Bigger ships

• Cascading of vessels

• Fewer port calls and less frequency

• Increasing Capex and Opex for ports

Carrier Alliances

• Concentration of volumes

• Market risk for terminals

Liners’ weak financials

• Pressure on terminals • Mergers and acquisition in liner industry

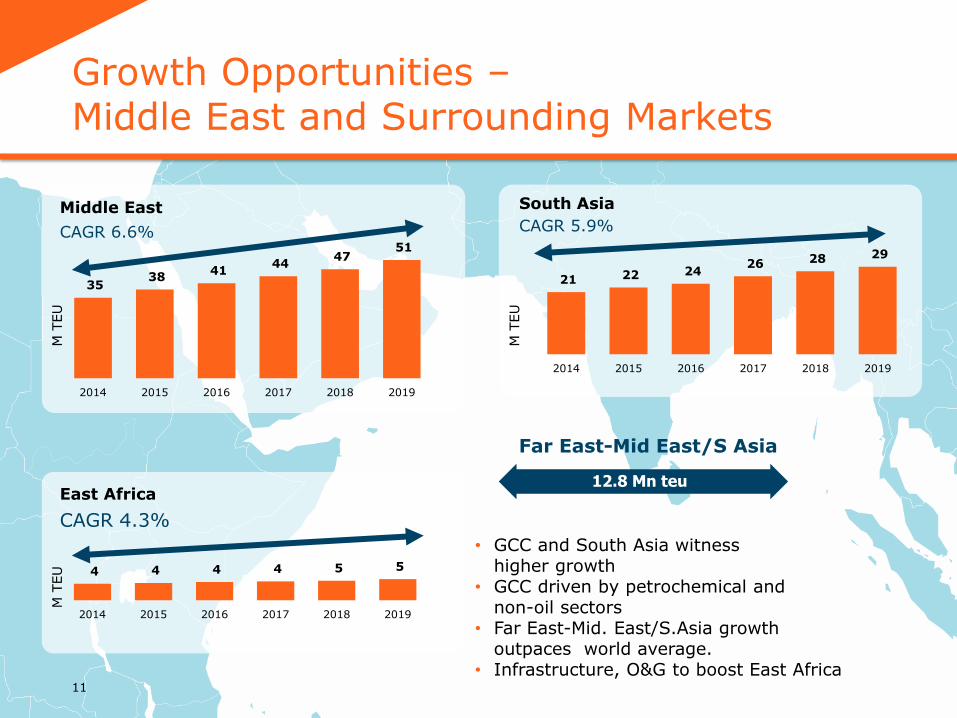

Growth Opportunities – Middle East and Surrounding Markets

11

• GCC and South Asia witness higher growth

• GCC driven by petrochemical and non-oil sectors

• Far East-Mid. East/S.Asia growth outpaces world average.

• Infrastructure, O&G to boost East Africa

21 22 24 26 28 29

2014 2015 2016 2017 2018 2019

4 4 4 4 5 5

2014 2015 2016 2017 2018 2019

35 38

41 44

47 51

2014 2015 2016 2017 2018 2019

CAGR 6.6% CAGR 5.9%

CAGR 4.3%

M T

EU

M

TEU

M T

EU

Far East-Mid East/S Asia

12.8 Mn teu

South Asia Middle East

East Africa

Oman- Opportunities to win

12

Robust regional trade growth

Development of GCC rail

Regional Focus on manufacturing

and other non-oil sectors

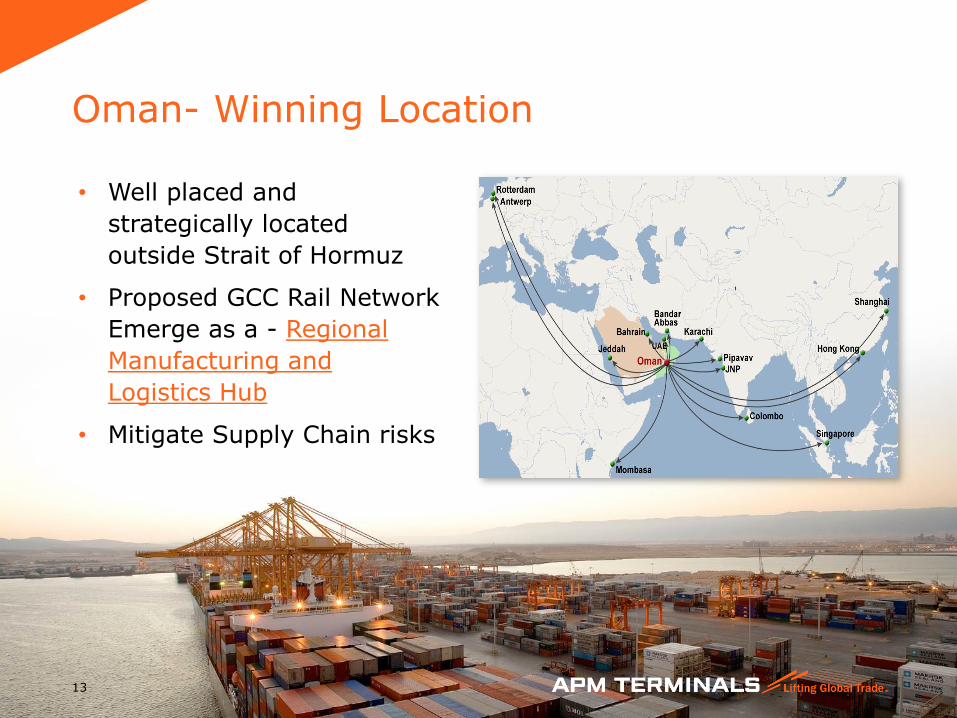

Oman- Winning Location

• Well placed and

strategically located

outside Strait of Hormuz

• Proposed GCC Rail Network

Emerge as a - Regional

Manufacturing and

Logistics Hub

• Mitigate Supply Chain risks

13

Oman – Create an environment to win

14

• Business regulatory environment

• Reduce barriers to trade

• Robust legal framework to build confidence

Countries Ease of Doing Business Trading Cross Borders Enforcing contracts

Singapore 1 1 1

UAE 22 8 121

Saudi Arabia 49 92 108

Oman 66 60 130

Ease of Doing Business – Global rankings

Source: Doing Business 2015, World Bank Group

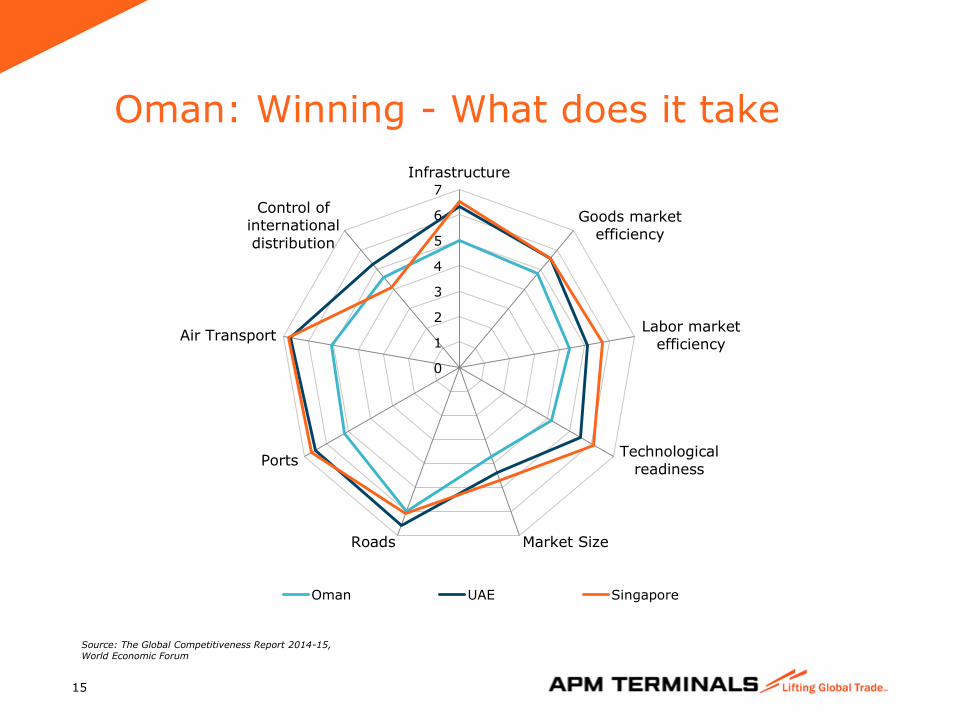

Oman: Winning - What does it take

15

0

1

2

3

4

5

6

7

Infrastructure

Goods marketefficiency

Labor marketefficiency

Technologicalreadiness

Market SizeRoads

Ports

Air Transport

Control ofinternational

distribution

Oman UAE Singapore

Source: The Global Competitiveness Report 2014-15, World Economic Forum

Oman - Road to Win

• Develop and improve

logistics infrastructure

• Strengthen existing free

trade and industrial zones

16

• Ease of doing business

• Skill development

• Investment in technology

Conclusion – Sure Oman will Win

17

• Global economy rebalance

• Emerging markets

to lead growth

• Strategically located to serve key

growth markets

• Changing industry trends resulting

in intense competition in logistics

and port sector

• Oman can improve its

competitiveness to emerge as

Regional Manufacturing and

Logistics Hub

Thank you

www.apmterminals.com