Embed Size (px)

Citation preview

GE2250 Understand Global Project for Business and Engineering Professionals

Instructor: Jiayu Chen Ph.D.

Project Cost Estimation and Budgeting

© Jiayu Chen, Ph.D. 2

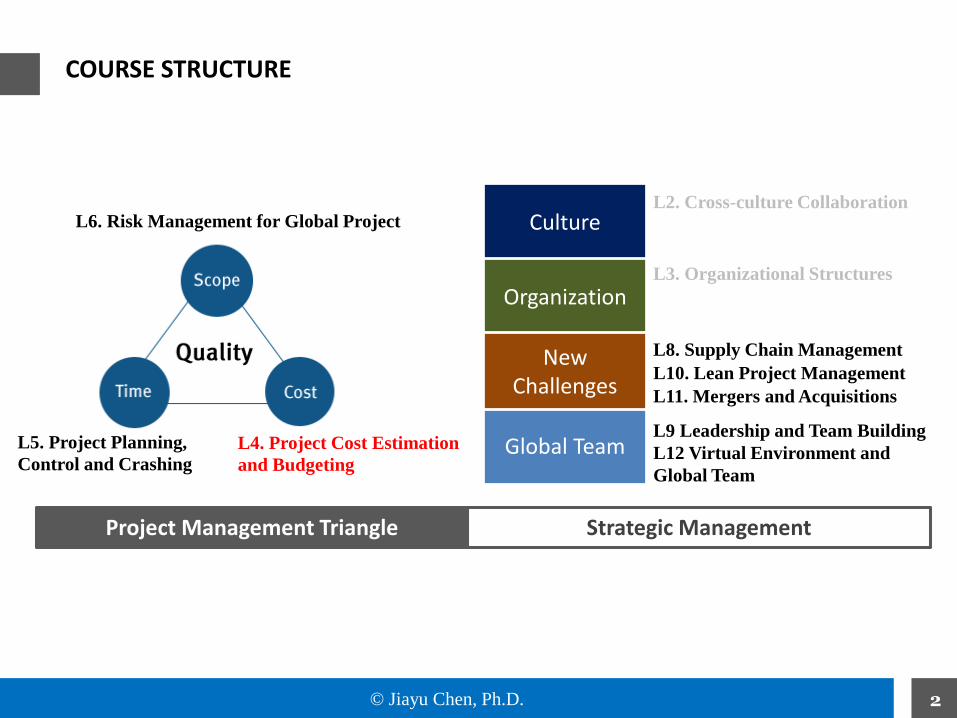

COURSE STRUCTURE

L4. Project Cost Estimation

and Budgeting

L5. Project Planning,

Control and Crashing

L6. Risk Management for Global Project

Project Management Triangle Strategic Management

L2. Cross-culture Collaboration

L3. Organizational Structures

Culture

Organization

Global Team

New Challenges

L8. Supply Chain Management

L10. Lean Project Management

L11. Mergers and Acquisitions

L9 Leadership and Team Building

L12 Virtual Environment and

Global Team

© Jiayu Chen, Ph.D. 3

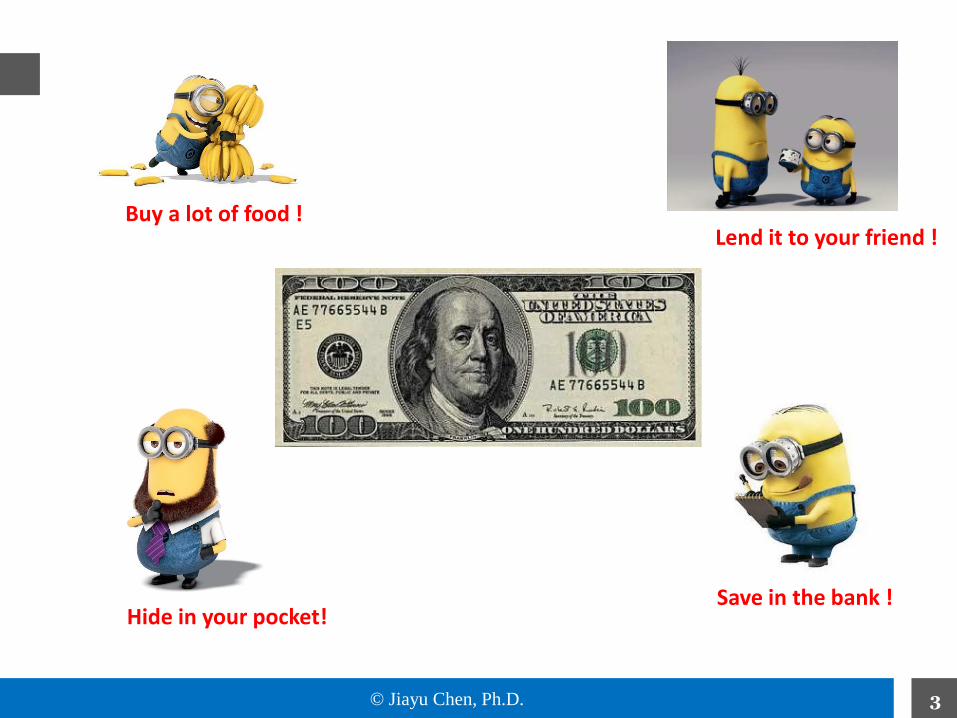

Buy a lot of food !

Hide in your pocket!Save in the bank !

Lend it to your friend !

© Jiayu Chen, Ph.D. 4

INVESTMENT

Any currency have both purchasing power and earning power!

Investment Activity

The act of committing money or capital to an endeavor with the expectation of

obtaining an additional income or profit.

Simple Problems:

Can generally be worked in one's head without extensive analysis…

• Should I buy a subway pass or pay daily rates?

• Should I buy the textbook for 3129 or an iPod?

© Jiayu Chen, Ph.D. 5

Why Bother Investing?

INVESTMENT

• The rule of 7-10 and 10-7

• Inflation

• Future security

• Large purchase

© Jiayu Chen, Ph.D. 6

• Must be organized and analyzed.

• Sufficiently important to justify serious thought and action.

• The economic aspects are significant.

• Single criteria decision making is generally adequate.

However there are some decisions much difficult to make!Because investment for projects are much complex.

INVESTMENT

© Jiayu Chen, Ph.D. 7

INVESTMENT

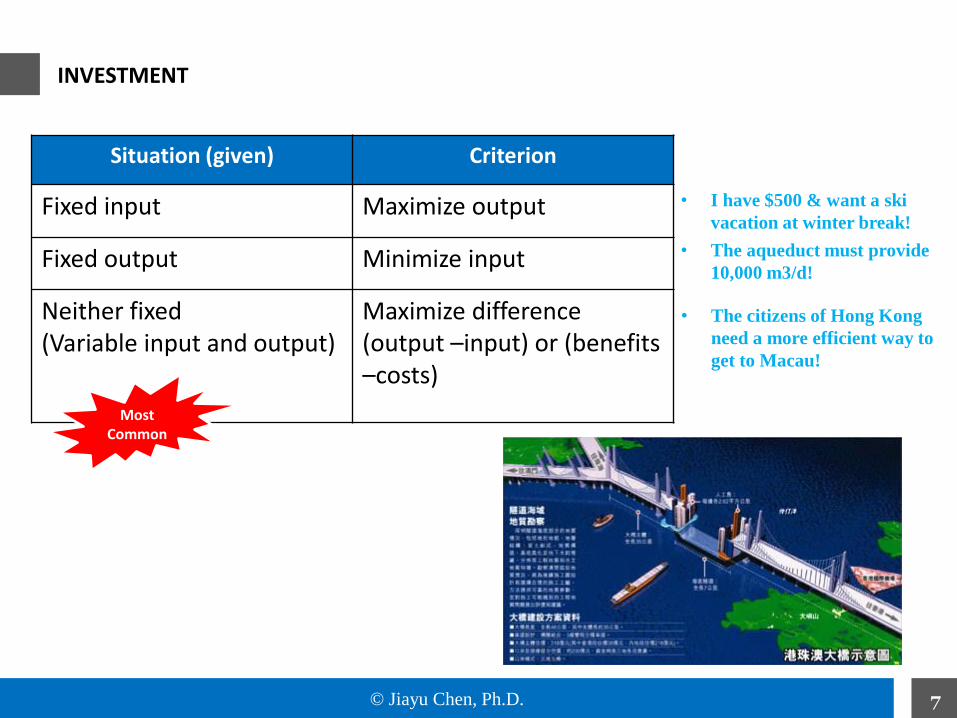

Situation (given) Criterion

Fixed input Maximize output

Fixed output Minimize input

Neither fixed(Variable input and output)

Maximize difference(output –input) or (benefits –costs)

• I have $500 & want a ski

vacation at winter break!

• The aqueduct must provide

10,000 m3/d!

• The citizens of Hong Kong

need a more efficient way to

get to Macau!

Most Common

© Jiayu Chen, Ph.D. 8

ENGINEERING ECONOMICS

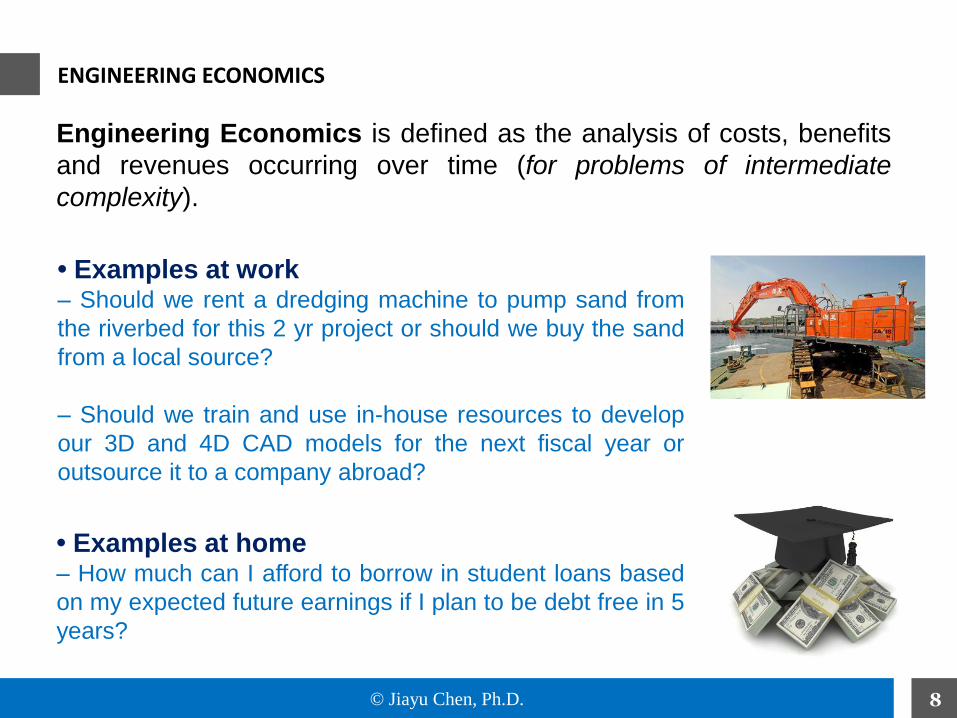

Engineering Economics is defined as the analysis of costs, benefits

and revenues occurring over time (for problems of intermediate

complexity).

• Examples at work– Should we rent a dredging machine to pump sand from

the riverbed for this 2 yr project or should we buy the sand

from a local source?

– Should we train and use in-house resources to develop

our 3D and 4D CAD models for the next fiscal year or

outsource it to a company abroad?

• Examples at home– How much can I afford to borrow in student loans based

on my expected future earnings if I plan to be debt free in 5

years?

© Jiayu Chen, Ph.D. 9

Money is a valuable commodity !

– Can be leased or rented (borrowed)

You’re probably renting some money to or from a bank right now!

– Amount borrowed/loaned is the Principal, P

– Amount paid for its use is called Interest, I

– Interest for 1 time period is called interest rate, i

TIME VALUE

If I borrow $100 (=P) for 1 year, and I pay

back a total of $109 (=P+I),

then the interest paid for 1 year (=I) = $9

and the interest rate (i) = $9 $100 = 9%

© Jiayu Chen, Ph.D. 10

Time Value of Money

© Jiayu Chen, Ph.D. 11

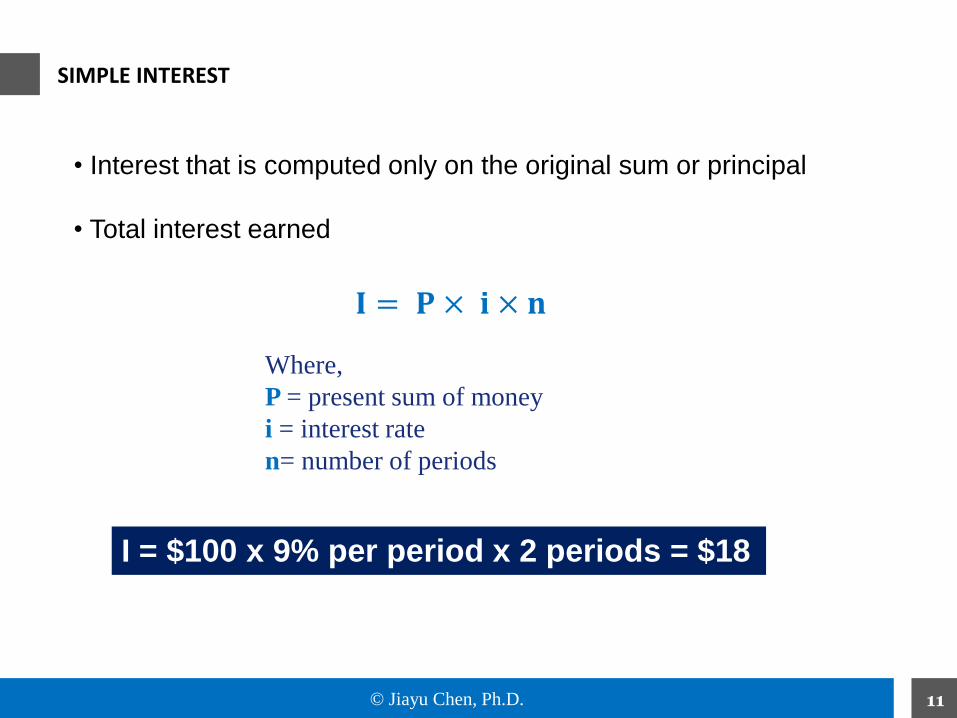

• Interest that is computed only on the original sum or principal

• Total interest earned

𝐈 = 𝐏 × 𝐢 × 𝐧

SIMPLE INTEREST

I = $100 x 9% per period x 2 periods = $18

Where,

P = present sum of money

i = interest rate

n= number of periods

© Jiayu Chen, Ph.D. 12

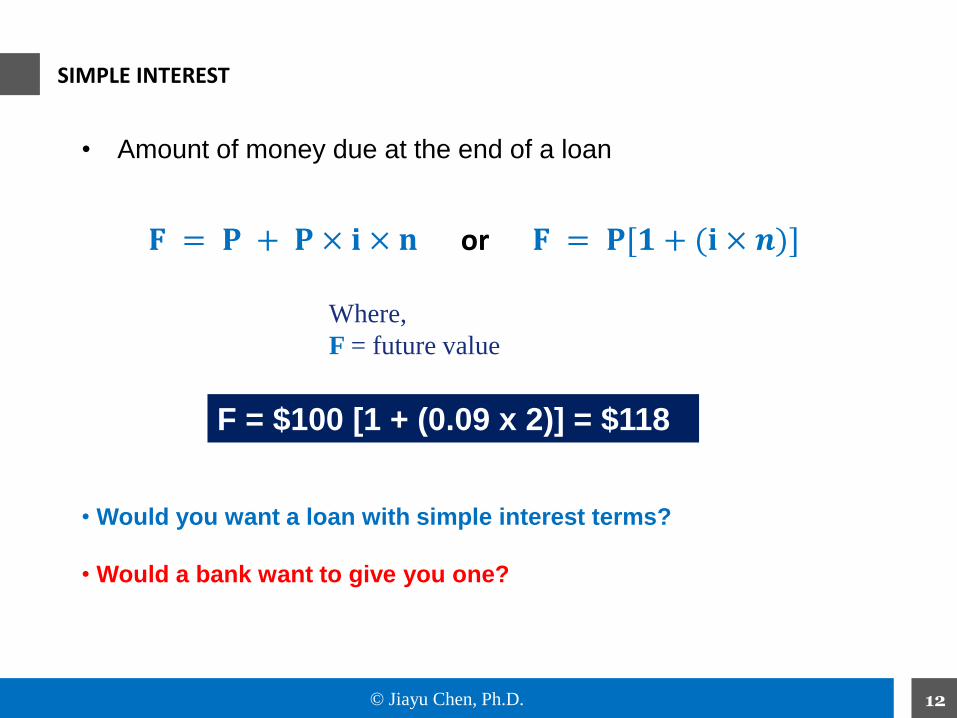

SIMPLE INTEREST

• Amount of money due at the end of a loan

• Would you want a loan with simple interest terms?

• Would a bank want to give you one?

𝐅 = 𝐏 + 𝐏 × 𝐢 × 𝐧 or 𝐅 = 𝐏[𝟏 + (𝐢 × 𝒏)]

Where,

F = future value

F = $100 [1 + (0.09 x 2)] = $118

© Jiayu Chen, Ph.D. 13

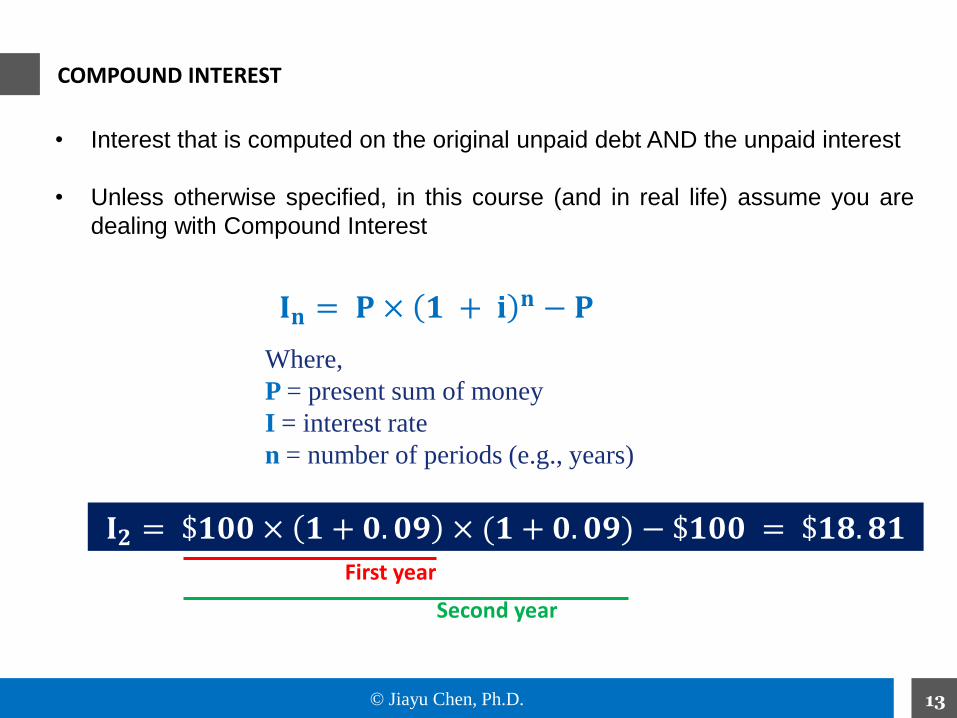

COMPOUND INTEREST

• Interest that is computed on the original unpaid debt AND the unpaid interest

• Unless otherwise specified, in this course (and in real life) assume you are

dealing with Compound Interest

𝐈𝐧 = 𝐏 × 𝟏 + 𝐢𝐧 − 𝐏

Where,

P = present sum of money

I = interest rate

n = number of periods (e.g., years)

𝐈𝟐 = $𝟏𝟎𝟎 × 𝟏 + 𝟎. 𝟎𝟗 × (𝟏 + 𝟎. 𝟎𝟗) − $𝟏𝟎𝟎 = $𝟏𝟖. 𝟖𝟏

First year

Second year

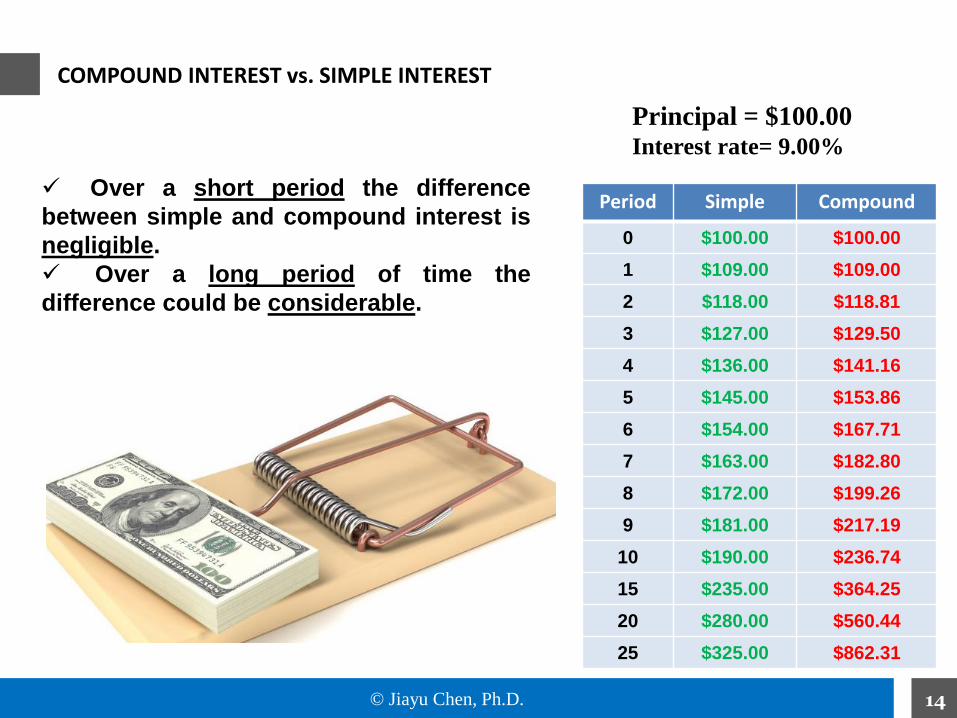

© Jiayu Chen, Ph.D. 14

Period Simple Compound

0 $100.00 $100.00

1 $109.00 $109.00

2 $118.00 $118.81

3 $127.00 $129.50

4 $136.00 $141.16

5 $145.00 $153.86

6 $154.00 $167.71

7 $163.00 $182.80

8 $172.00 $199.26

9 $181.00 $217.19

10 $190.00 $236.74

15 $235.00 $364.25

20 $280.00 $560.44

25 $325.00 $862.31

COMPOUND INTEREST vs. SIMPLE INTEREST

Principal = $100.00 Interest rate= 9.00%

Over a short period the difference

between simple and compound interest is

negligible.

Over a long period of time the

difference could be considerable.

© Jiayu Chen, Ph.D. 15

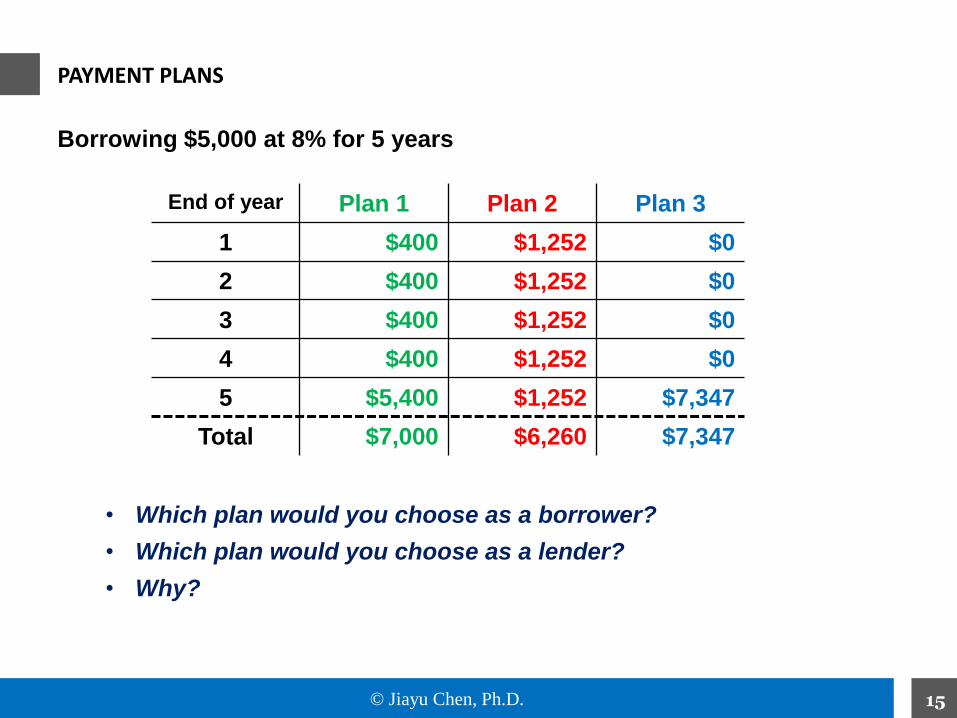

PAYMENT PLANS

Borrowing $5,000 at 8% for 5 years

• Which plan would you choose as a borrower?

• Which plan would you choose as a lender?

• Why?

End of year Plan 1 Plan 2 Plan 3

1 $400 $1,252 $0

2 $400 $1,252 $0

3 $400 $1,252 $0

4 $400 $1,252 $0

5 $5,400 $1,252 $7,347

Total $7,000 $6,260 $7,347

© Jiayu Chen, Ph.D. 16

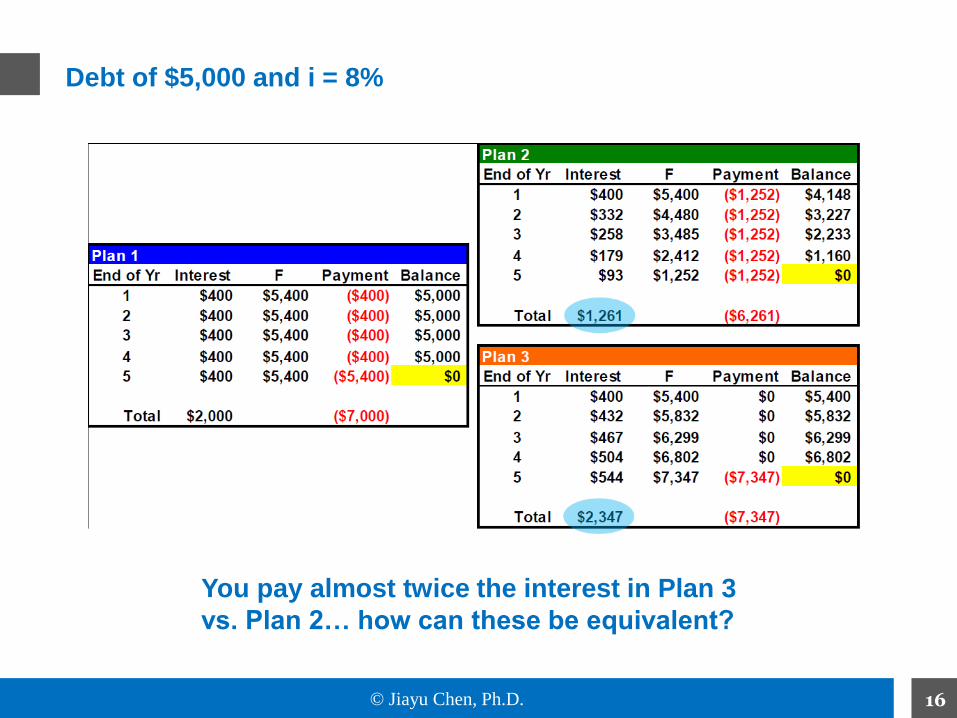

Debt of $5,000 and i = 8%

You pay almost twice the interest in Plan 3

vs. Plan 2… how can these be equivalent?

© Jiayu Chen, Ph.D. 17

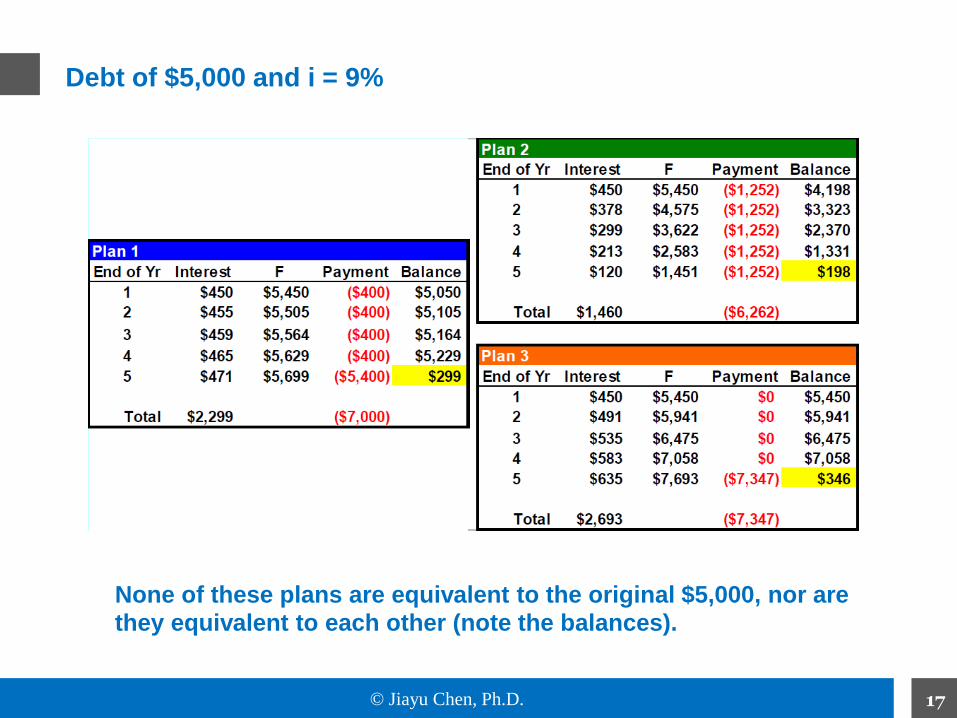

Debt of $5,000 and i = 9%

None of these plans are equivalent to the original $5,000, nor are

they equivalent to each other (note the balances).

© Jiayu Chen, Ph.D. 18

EVALUATION – Cash Flows

Present Value is the value of a sum of money in today’s

dollars–Future sums are discounted when moved backward in time(i.e., to the present)

Future Value is the value of a sum of money at a specified

time and interest rate–Present sums are compounded when moved forward in time(i.e., to the future)

Cash flows are equivalent if they are of equal value at a particular point in time

and a particular interest rate–All 3 plans are equivalent to $5,000 now at 8%

© Jiayu Chen, Ph.D. 19

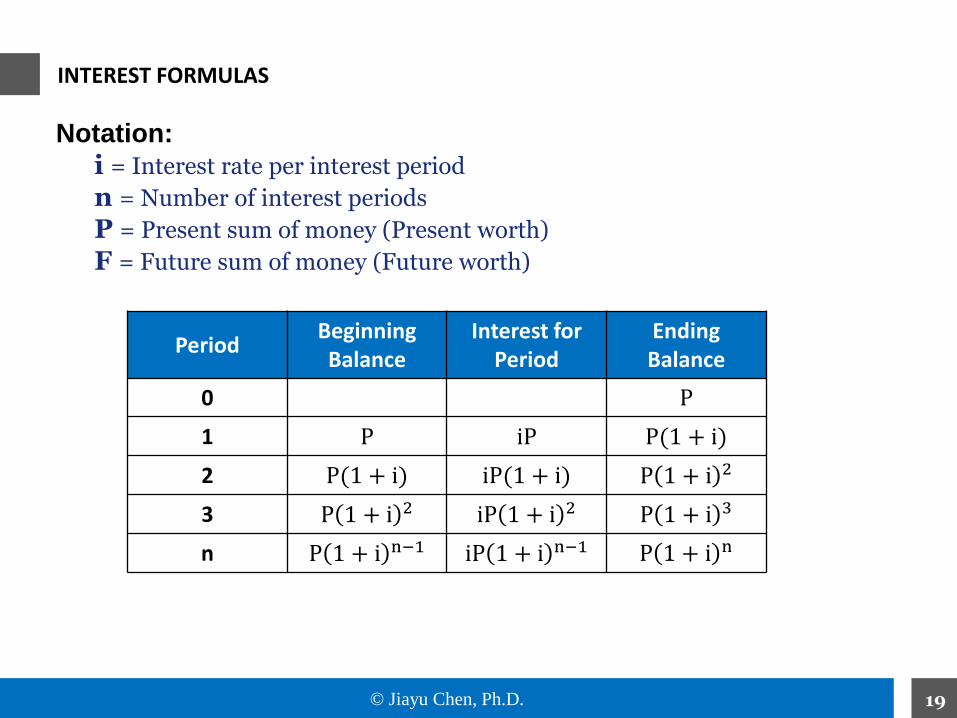

INTEREST FORMULAS

Notation:

i = Interest rate per interest period

n = Number of interest periods

P = Present sum of money (Present worth)

F = Future sum of money (Future worth)

PeriodBeginning Balance

Interest for Period

Ending Balance

0 P

1 P iP P(1 + i)

2 P(1 + i) iP(1 + i) P 1 + i 2

3 P 1 + i 2 iP 1 + i 2 P 1 + i 3

n P 1 + i n−1 iP 1 + i n−1 P 1 + i n

© Jiayu Chen, Ph.D. 20

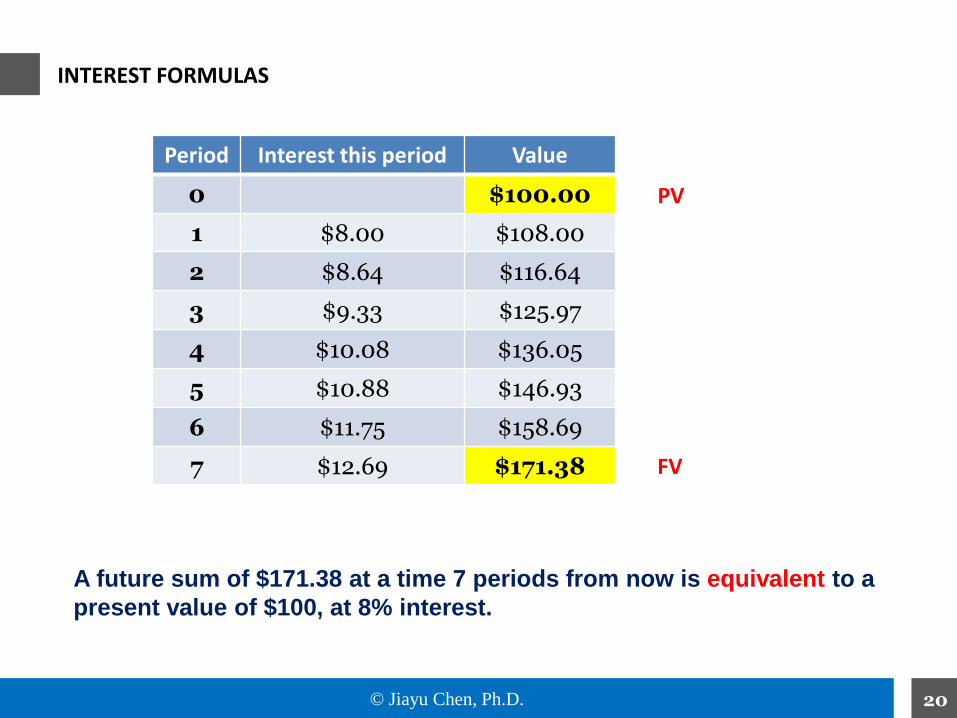

INTEREST FORMULAS

Period Interest this period Value

0 $100.00

1 $8.00 $108.00

2 $8.64 $116.64

3 $9.33 $125.97

4 $10.08 $136.05

5 $10.88 $146.93

6 $11.75 $158.69

7 $12.69 $171.38

A future sum of $171.38 at a time 7 periods from now is equivalent to a

present value of $100, at 8% interest.

PV

FV

© Jiayu Chen, Ph.D. 21

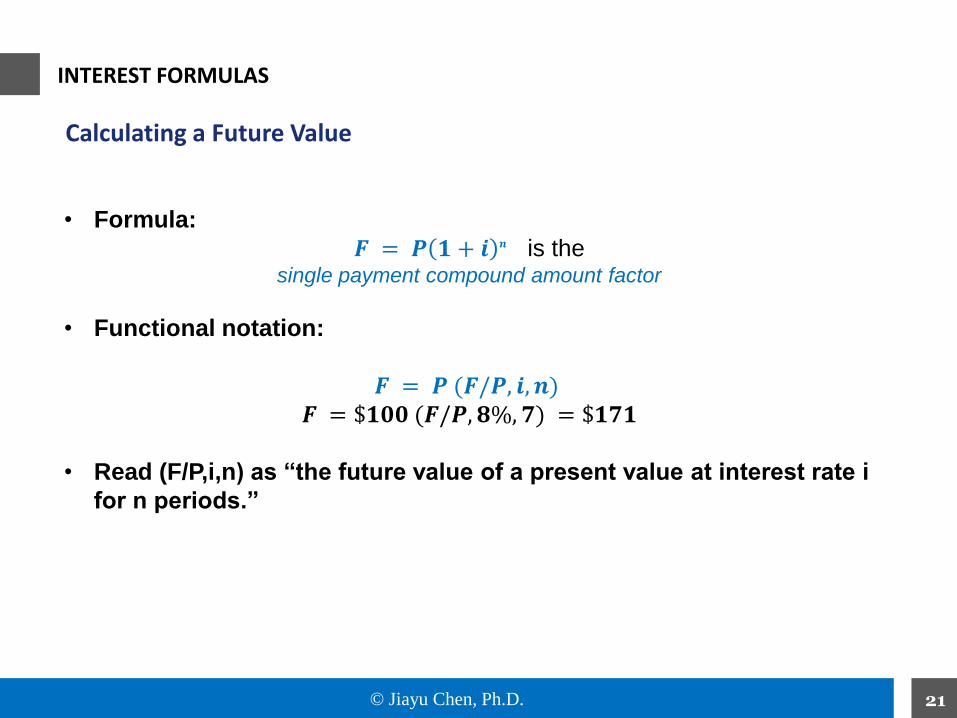

• Formula:

𝑭 = 𝑷 𝟏 + 𝒊 𝒏 is the single payment compound amount factor

• Functional notation:

𝑭 = 𝑷 (𝑭/𝑷, 𝒊, 𝒏)𝑭 = $𝟏𝟎𝟎 (𝑭/𝑷, 𝟖%, 𝟕) = $𝟏𝟕𝟏

• Read (F/P,i,n) as “the future value of a present value at interest rate i

for n periods.”

INTEREST FORMULAS

Calculating a Future Value

© Jiayu Chen, Ph.D. 22

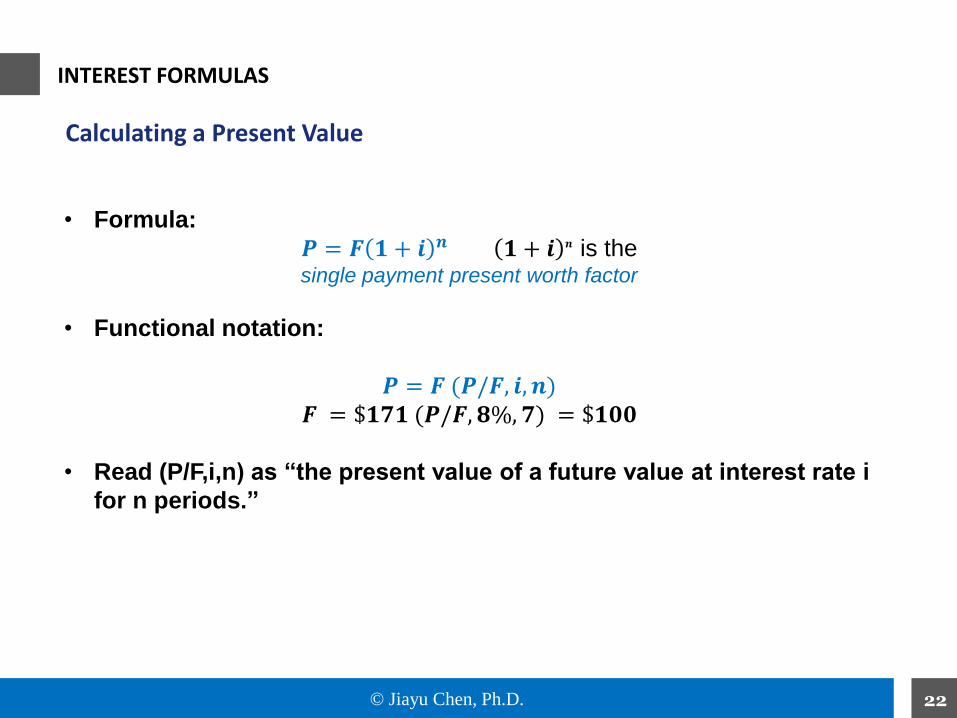

INTEREST FORMULAS

Calculating a Present Value

• Formula:

𝑷 = 𝑭 𝟏 + 𝒊 𝒏 𝟏 + 𝒊 𝒏 is the single payment present worth factor

• Functional notation:

𝑷 = 𝑭 (𝑷/𝑭, 𝒊, 𝒏)𝑭 = $𝟏𝟕𝟏 (𝑷/𝑭, 𝟖%, 𝟕) = $𝟏𝟎𝟎

• Read (P/F,i,n) as “the present value of a future value at interest rate i

for n periods.”

© Jiayu Chen, Ph.D. 23

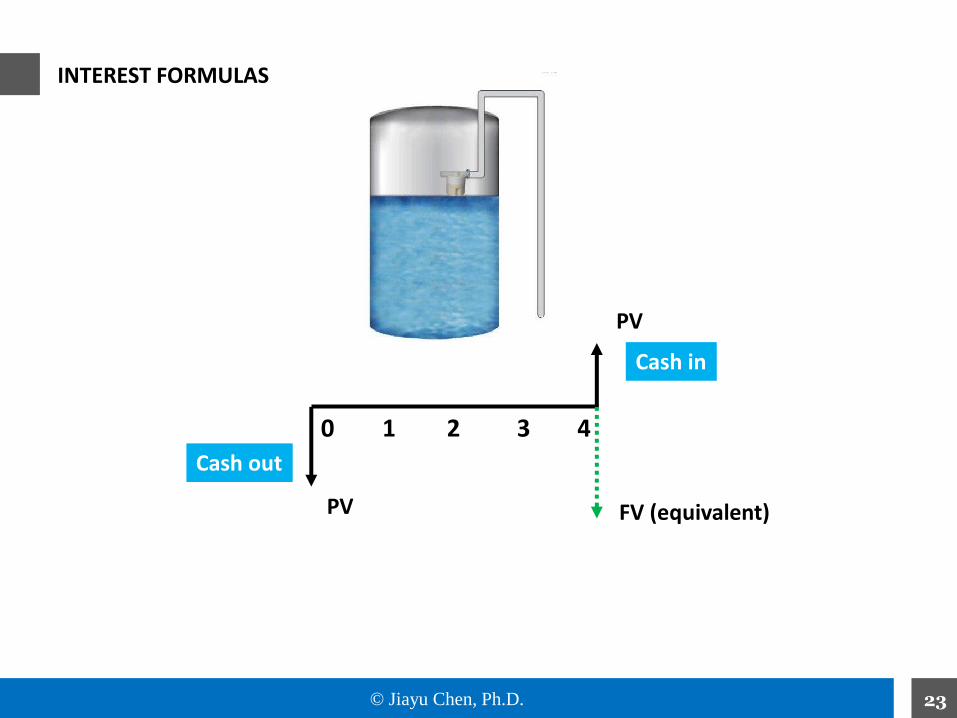

0 1 2 3 4

INTEREST FORMULAS

Cash out

Cash in

PV FV (equivalent)

PV

© Jiayu Chen, Ph.D. 24

• An understanding of “P” and “F” calculations is fundamental tounderstanding cash flows.

• However, in reality cash flows are often more complex:

– Cash flows can be repeated over many periods

e.g., Car payments

– Cash flows can increase or decrease over many periods

e.g., Maintenance costs

– Interest rates can be identified on an annualized basis but

calculated on shorter intervals

e.g., Credit cards

– Interest rates can be compounded continuously (vs. annually)

e.g., Rarely used in practice… useful in financial modeling as

theoretical maximum

CASH FLOWS

© Jiayu Chen, Ph.D. 25

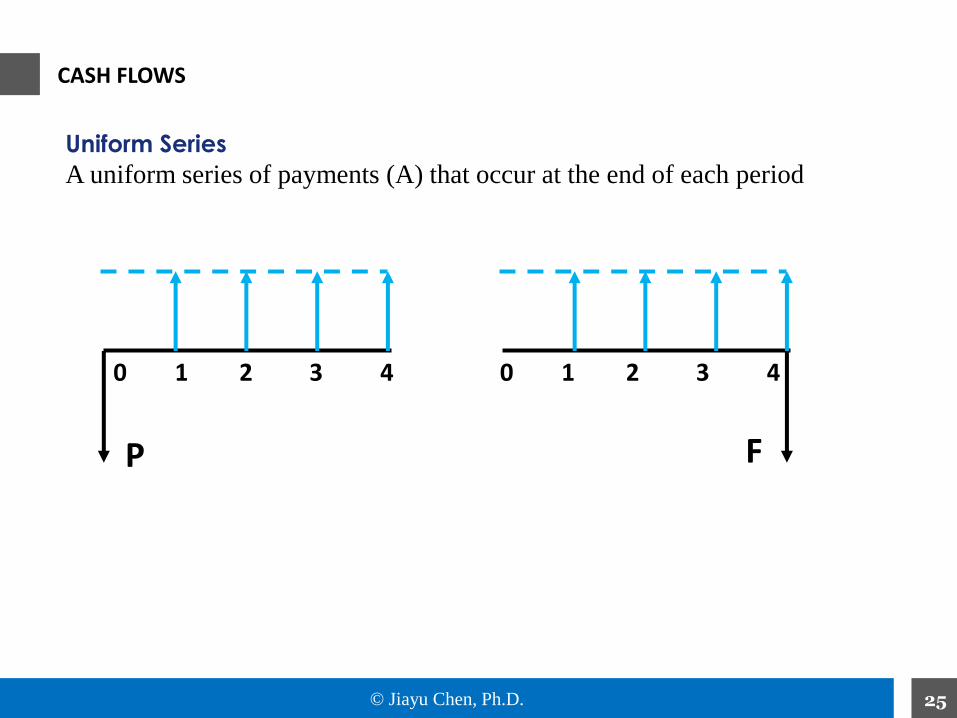

CASH FLOWS

Uniform Series

A uniform series of payments (A) that occur at the end of each period

P F

0 1 2 3 4 0 1 2 3 4

© Jiayu Chen, Ph.D. 26

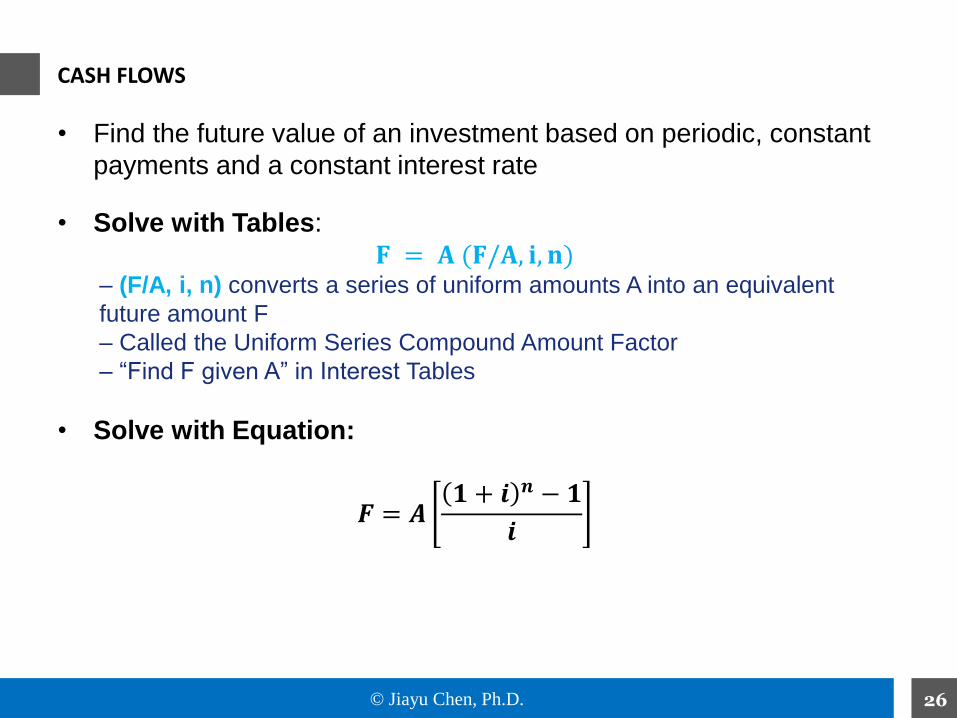

CASH FLOWS

• Find the future value of an investment based on periodic, constant

payments and a constant interest rate

• Solve with Tables:

𝐅 = 𝐀 (𝐅/𝐀, 𝐢, 𝐧)– (F/A, i, n) converts a series of uniform amounts A into an equivalent

future amount F

– Called the Uniform Series Compound Amount Factor

– “Find F given A” in Interest Tables

• Solve with Equation:

𝑭 = 𝑨𝟏 + 𝒊 𝒏 − 𝟏

𝒊

© Jiayu Chen, Ph.D. 27

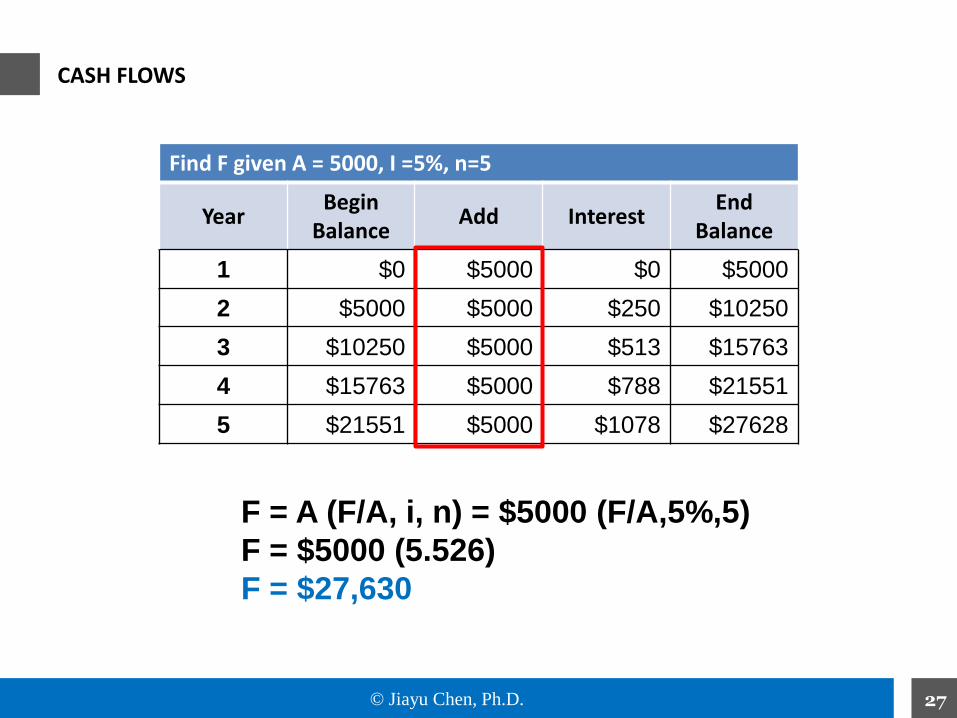

CASH FLOWS

Find F given A = 5000, I =5%, n=5

YearBegin

BalanceAdd Interest

End Balance

1 $0 $5000 $0 $5000

2 $5000 $5000 $250 $10250

3 $10250 $5000 $513 $15763

4 $15763 $5000 $788 $21551

5 $21551 $5000 $1078 $27628

F = A (F/A, i, n) = $5000 (F/A,5%,5)

F = $5000 (5.526)

F = $27,630

© Jiayu Chen, Ph.D. 28

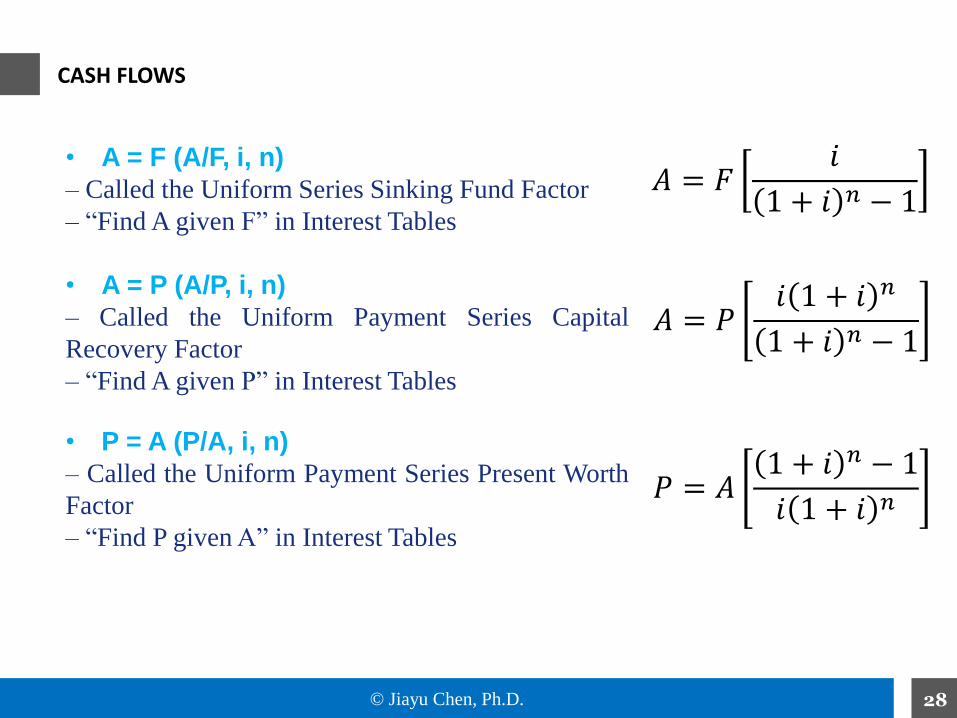

• A = F (A/F, i, n)

– Called the Uniform Series Sinking Fund Factor

– “Find A given F” in Interest Tables

• A = P (A/P, i, n)

– Called the Uniform Payment Series Capital

Recovery Factor

– “Find A given P” in Interest Tables

• P = A (P/A, i, n)

– Called the Uniform Payment Series Present Worth

Factor

– “Find P given A” in Interest Tables

CASH FLOWS

𝐴 = 𝐹𝑖

1 + 𝑖 𝑛 − 1

𝐴 = 𝑃𝑖 1 + 𝑖 𝑛

1 + 𝑖 𝑛 − 1

𝑃 = 𝐴1 + 𝑖 𝑛 − 1

𝑖 1 + 𝑖 𝑛

© Jiayu Chen, Ph.D. 29

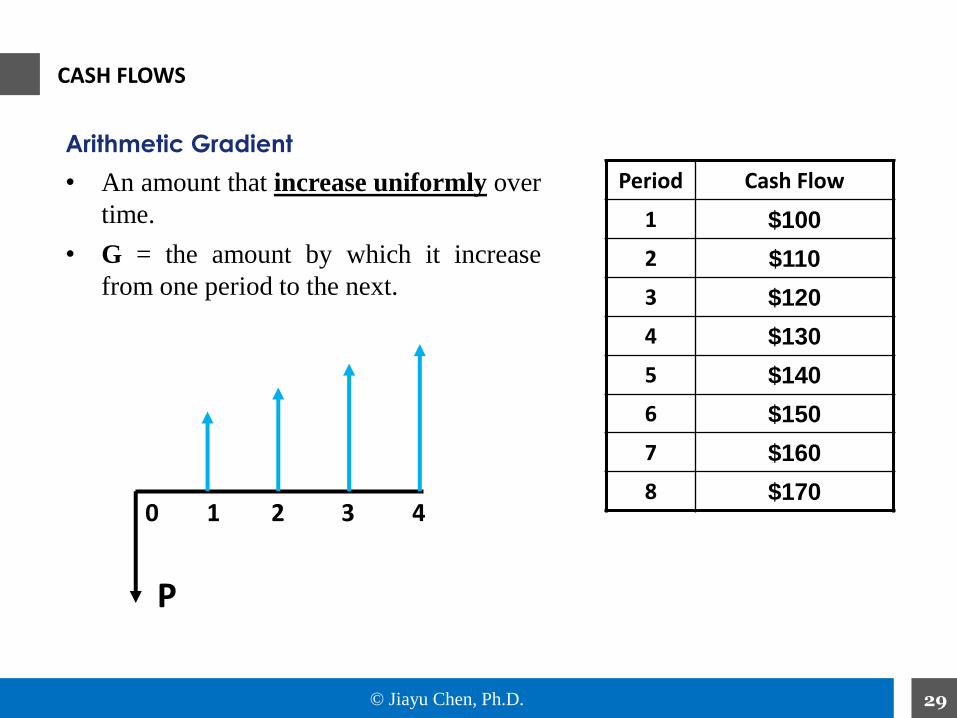

CASH FLOWS

Arithmetic Gradient

• An amount that increase uniformly over

time.

• G = the amount by which it increase

from one period to the next.

Period Cash Flow

1 $100

2 $110

3 $120

4 $130

5 $140

6 $150

7 $160

8 $170

P

0 1 2 3 4

© Jiayu Chen, Ph.D. 30

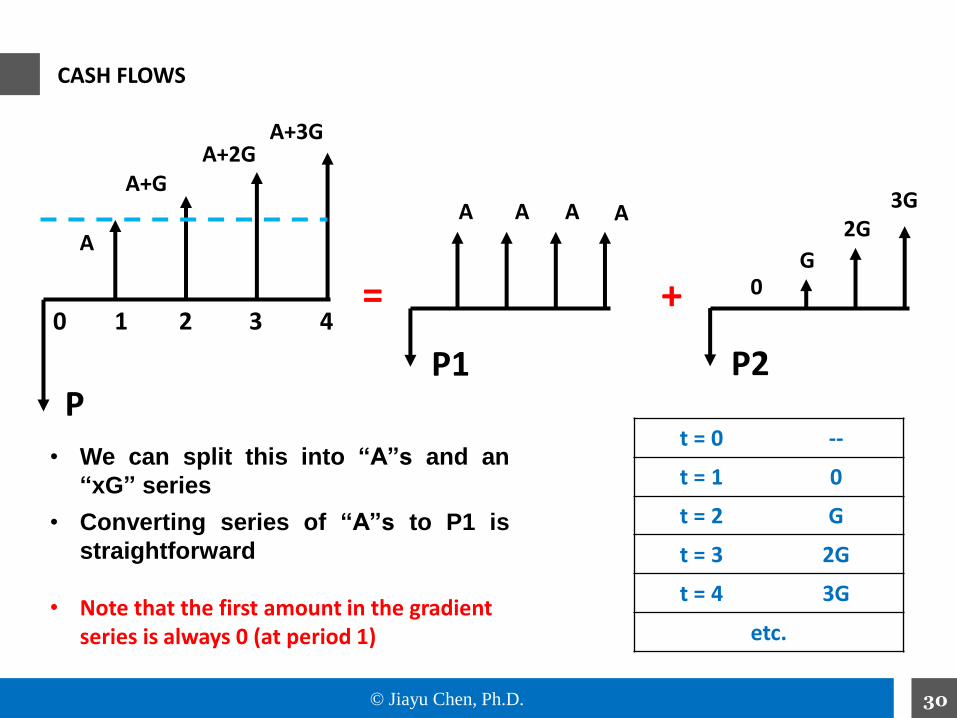

CASH FLOWS

P

0 1 2 3 4

A

A+GA+2G

A+3G

P1

A A A A

P2

0G

2G3G

= +

• We can split this into “A”s and an

“xG” series

• Converting series of “A”s to P1 is

straightforward

• Note that the first amount in the gradient series is always 0 (at period 1)

t = 0 --

t = 1 0

t = 2 G

t = 3 2G

t = 4 3G

etc.

© Jiayu Chen, Ph.D. 31

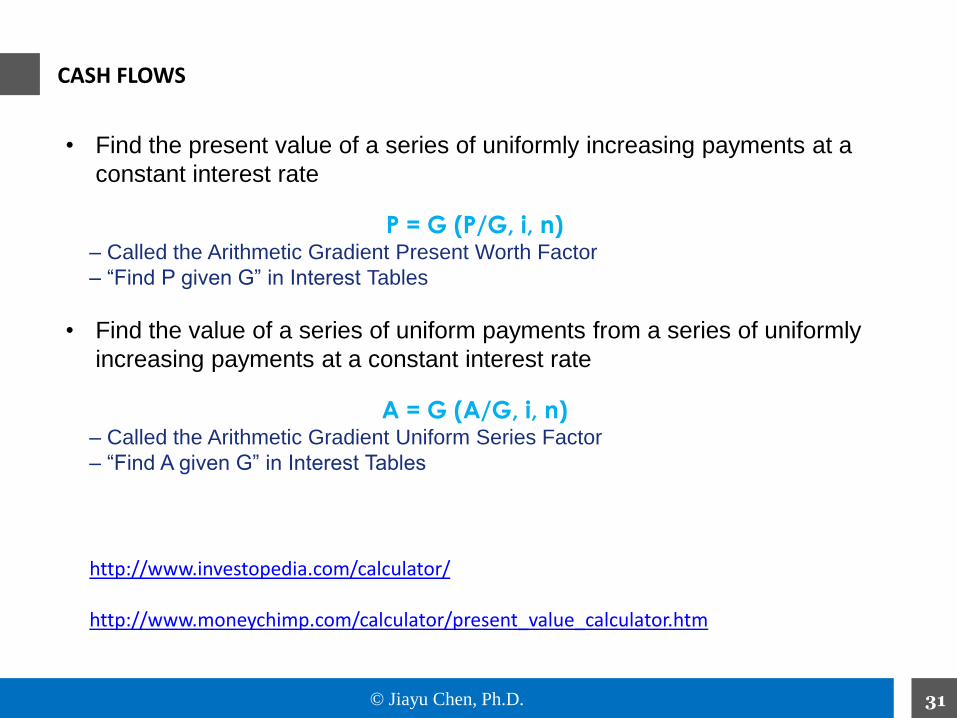

http://www.investopedia.com/calculator/

http://www.moneychimp.com/calculator/present_value_calculator.htm

• Find the present value of a series of uniformly increasing payments at a

constant interest rate

P = G (P/G, i, n)– Called the Arithmetic Gradient Present Worth Factor

– “Find P given G” in Interest Tables

• Find the value of a series of uniform payments from a series of uniformly

increasing payments at a constant interest rate

A = G (A/G, i, n)– Called the Arithmetic Gradient Uniform Series Factor

– “Find A given G” in Interest Tables

CASH FLOWS

© Jiayu Chen, Ph.D. 32

CASH FLOWS

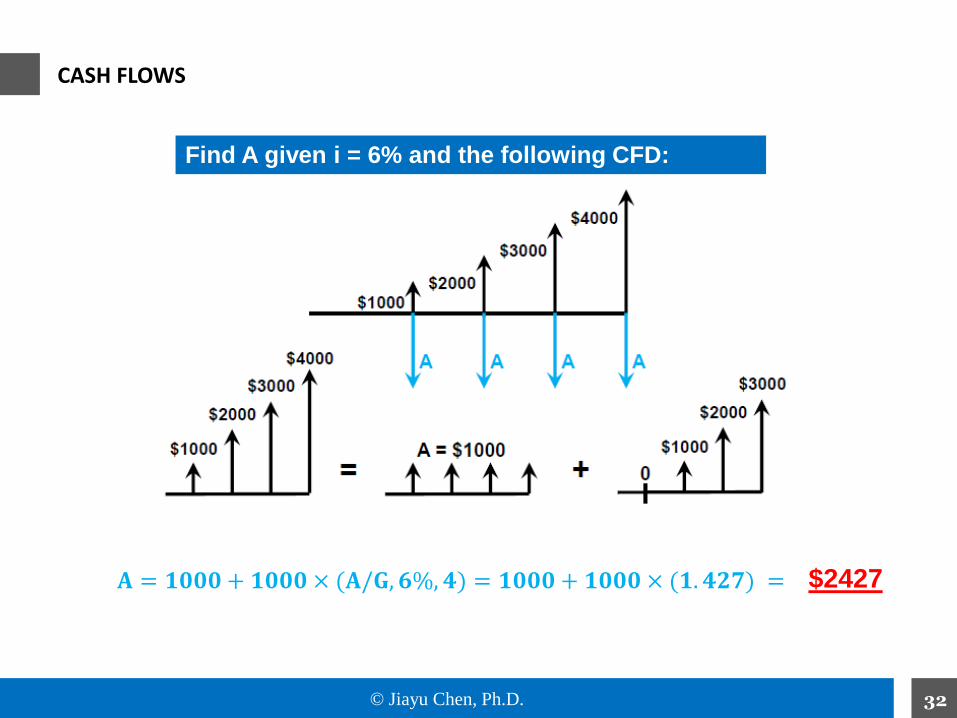

Find A given i = 6% and the following CFD:

𝐀 = 𝟏𝟎𝟎𝟎 + 𝟏𝟎𝟎𝟎 × (𝐀/𝐆, 𝟔%, 𝟒) = 𝟏𝟎𝟎𝟎 + 𝟏𝟎𝟎𝟎 × (𝟏. 𝟒𝟐𝟕) = $2427

© Jiayu Chen, Ph.D. 33

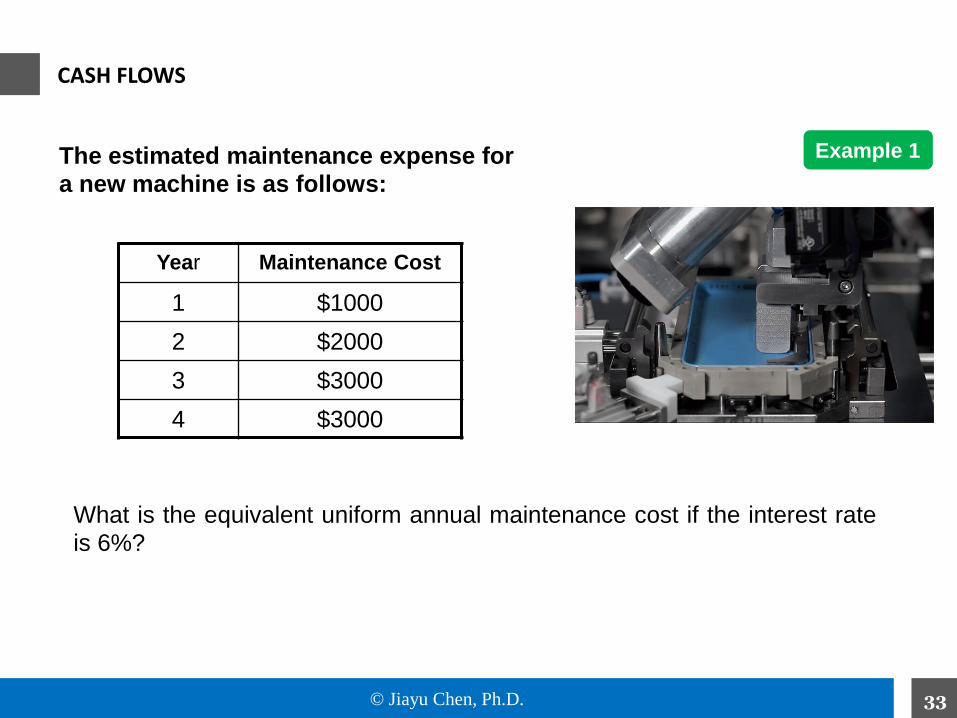

CASH FLOWS

The estimated maintenance expense for

a new machine is as follows:

Year Maintenance Cost

1 $1000

2 $2000

3 $3000

4 $3000

What is the equivalent uniform annual maintenance cost if the interest rate

is 6%?

Example 1

© Jiayu Chen, Ph.D. 34

ANALYSIS PERIOD

• Sometimes called the planning horizon

• What is the useful life of each alternative?

– Depends on technology and business

• Three possibilities:

1.Useful life of each alternative equals the analysis period.

2.Alternatives have useful lives different from the analysis period.

3.Analysis period is infinite (n = ∞)

© Jiayu Chen, Ph.D. 35

ANALYSIS PERIOD

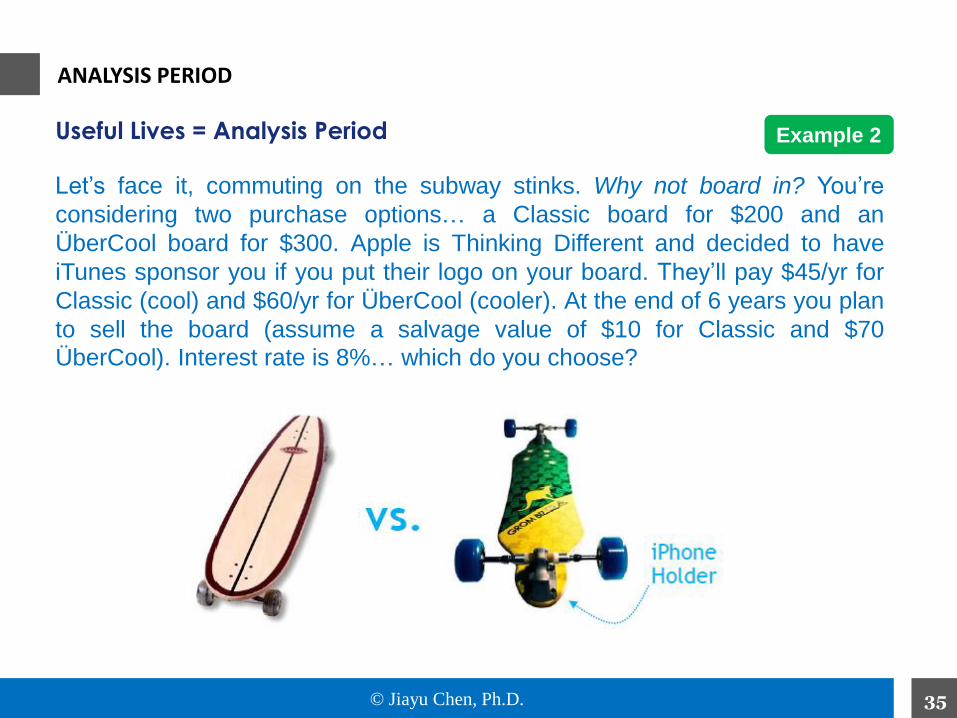

Useful Lives = Analysis Period

Let’s face it, commuting on the subway stinks. Why not board in? You’re

considering two purchase options… a Classic board for $200 and an

ÜberCool board for $300. Apple is Thinking Different and decided to have

iTunes sponsor you if you put their logo on your board. They’ll pay $45/yr for

Classic (cool) and $60/yr for ÜberCool (cooler). At the end of 6 years you plan

to sell the board (assume a salvage value of $10 for Classic and $70

ÜberCool). Interest rate is 8%… which do you choose?

Example 2

© Jiayu Chen, Ph.D. 36

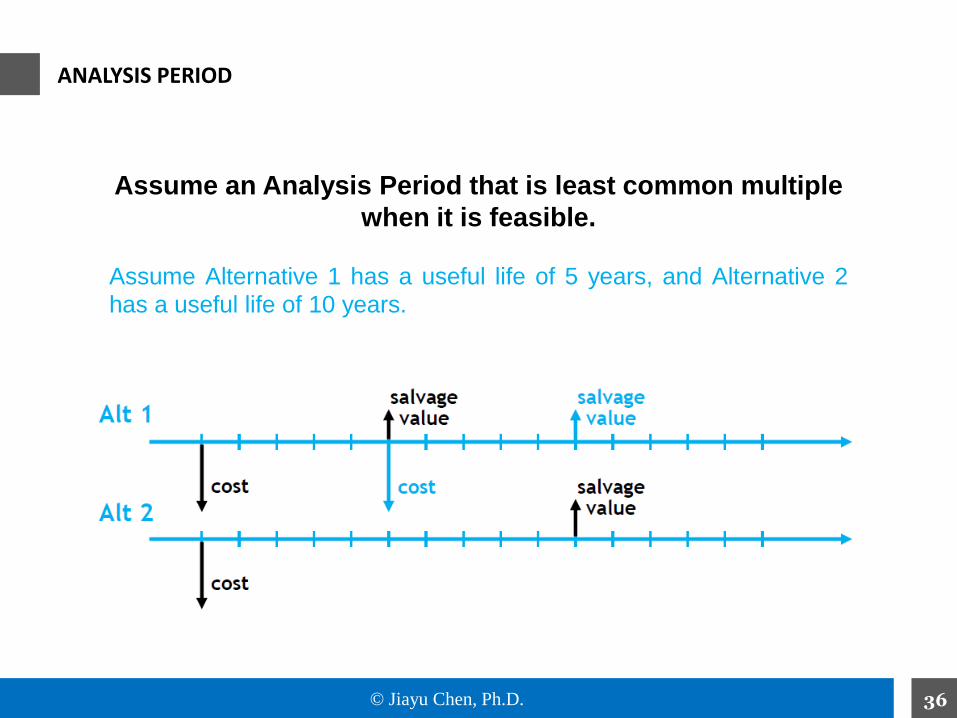

Assume an Analysis Period that is least common multiple

when it is feasible.

Assume Alternative 1 has a useful life of 5 years, and Alternative 2

has a useful life of 10 years.

ANALYSIS PERIOD

© Jiayu Chen, Ph.D. 37

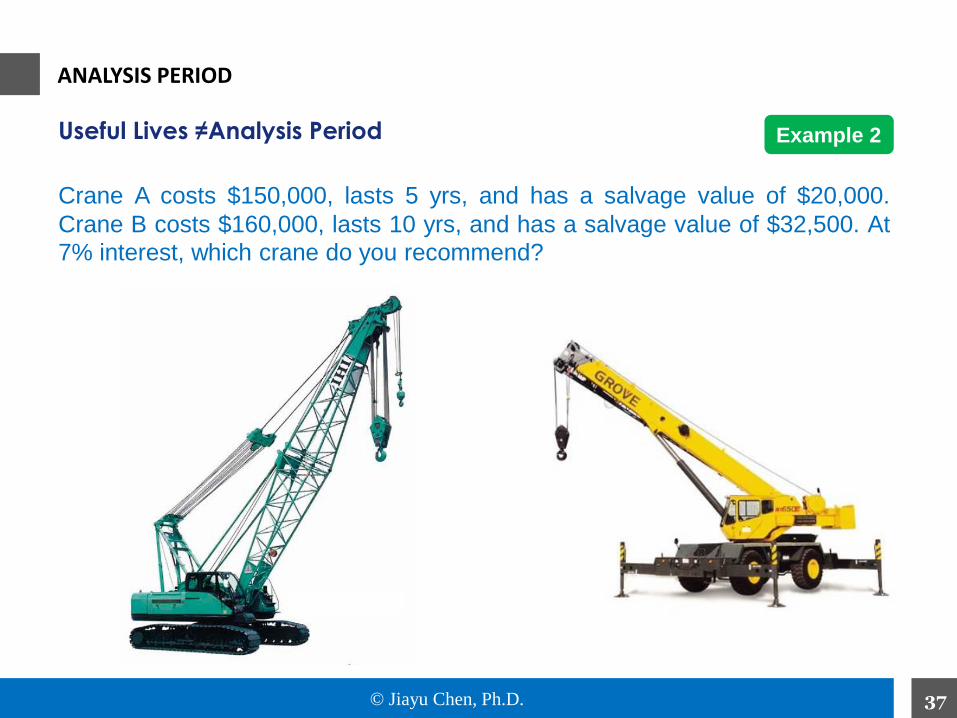

ANALYSIS PERIOD

Useful Lives ≠Analysis Period

Crane A costs $150,000, lasts 5 yrs, and has a salvage value of $20,000.

Crane B costs $160,000, lasts 10 yrs, and has a salvage value of $32,500. At

7% interest, which crane do you recommend?

Example 2

© Jiayu Chen, Ph.D. 38

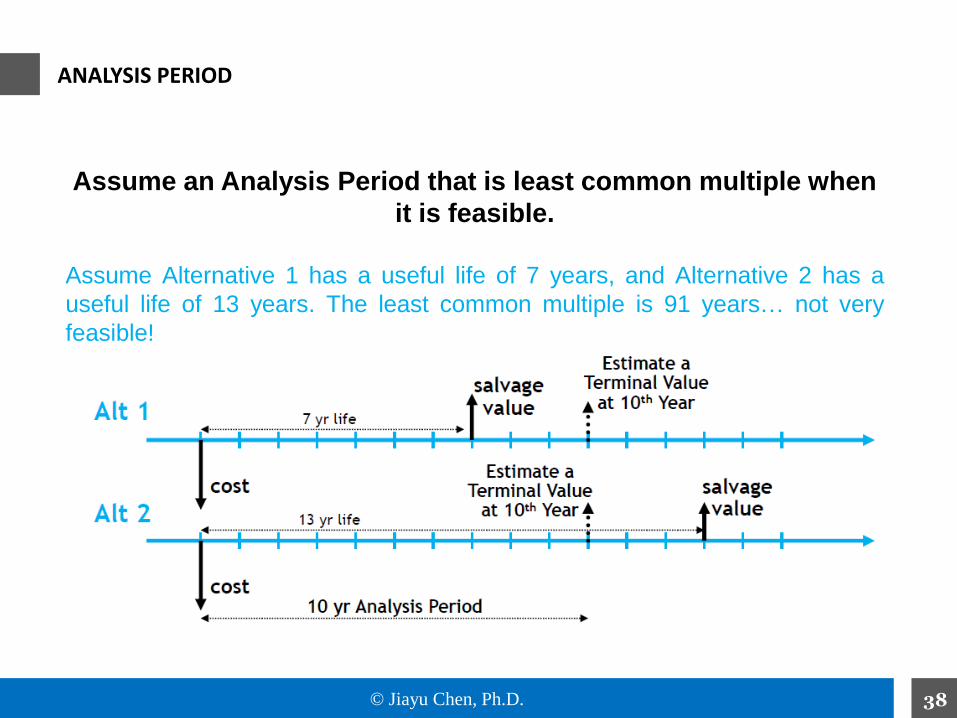

Assume an Analysis Period that is least common multiple when

it is feasible.

Assume Alternative 1 has a useful life of 7 years, and Alternative 2 has a

useful life of 13 years. The least common multiple is 91 years… not very

feasible!

ANALYSIS PERIOD

© Jiayu Chen, Ph.D. 39

Project Investment

© Jiayu Chen, Ph.D. 40

ANNUAL WORTH ANALYSIS / PRESENT VALUE ANALYSIS

• Similar process to Present Worth Analysis

• Convert cash flows to equivalent

– EUAB = Equivalent Uniform Annual Benefit

– EUAC = Equivalent Uniform Annual Cost

– EUAW = Equivalent Uniform Annual Worth EUAB-EUAC

• The Analysis Period or Planning Horizon is an important consideration

• However, unlike Present Worth Analysis, it is not necessary to compute

each alternative over the same period in most cases.

© Jiayu Chen, Ph.D. 41

ANNUAL WORTH ANALYSIS

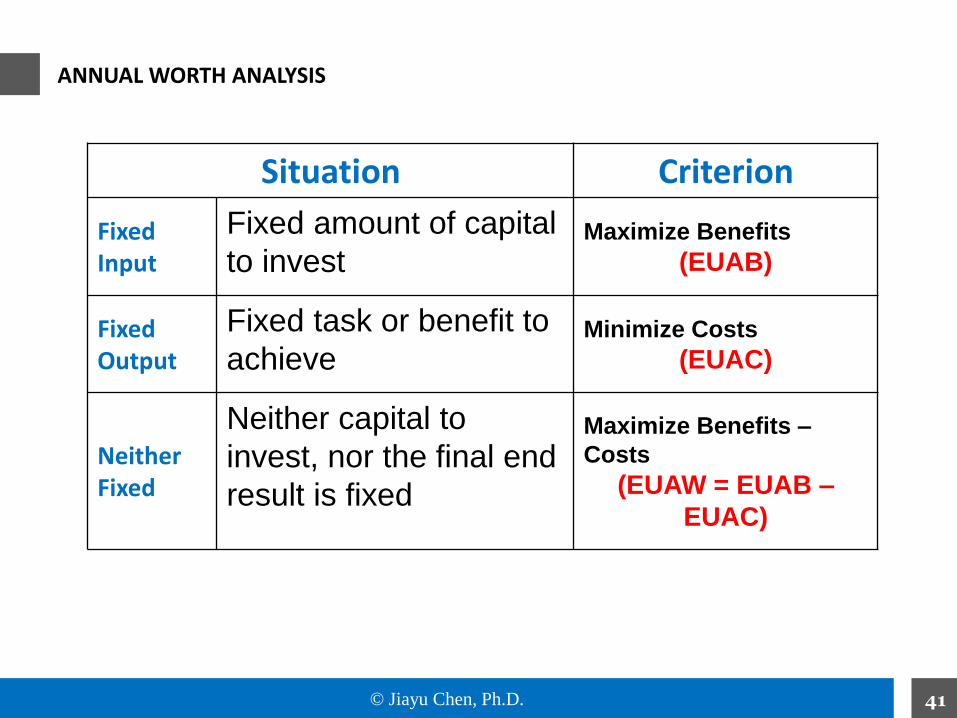

Situation Criterion

Fixed Input

Fixed amount of capital

to investMaximize Benefits

(EUAB)

Fixed Output

Fixed task or benefit to

achieveMinimize Costs

(EUAC)

Neither Fixed

Neither capital to

invest, nor the final end

result is fixed

Maximize Benefits –

Costs

(EUAW = EUAB –

EUAC)

© Jiayu Chen, Ph.D. 42

ANNUAL WORTH ANALYSIS

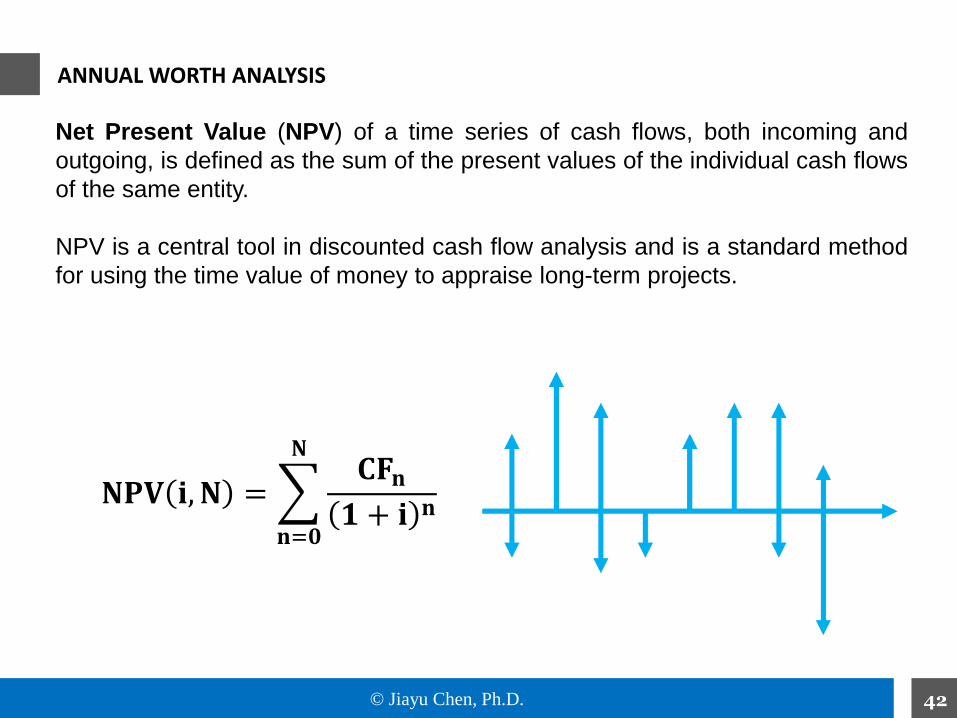

Net Present Value (NPV) of a time series of cash flows, both incoming and

outgoing, is defined as the sum of the present values of the individual cash flows

of the same entity.

NPV is a central tool in discounted cash flow analysis and is a standard method

for using the time value of money to appraise long-term projects.

𝐍𝐏𝐕 𝐢, 𝐍 =

𝐧=𝟎

𝐍𝐂𝐅𝐧𝟏 + 𝐢 𝐧

© Jiayu Chen, Ph.D. 43

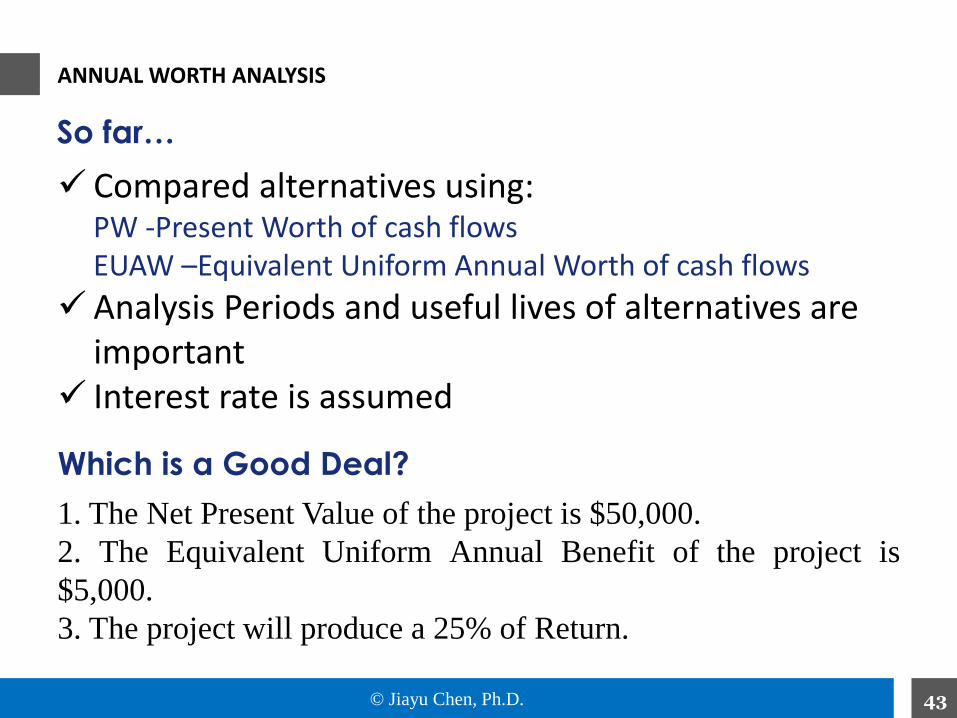

Compared alternatives using:PW -Present Worth of cash flowsEUAW –Equivalent Uniform Annual Worth of cash flows

Analysis Periods and useful lives of alternatives are important

Interest rate is assumed

ANNUAL WORTH ANALYSIS

So far…

Which is a Good Deal?

1. The Net Present Value of the project is $50,000.

2. The Equivalent Uniform Annual Benefit of the project is

$5,000.

3. The project will produce a 25% of Return.

© Jiayu Chen, Ph.D. 44

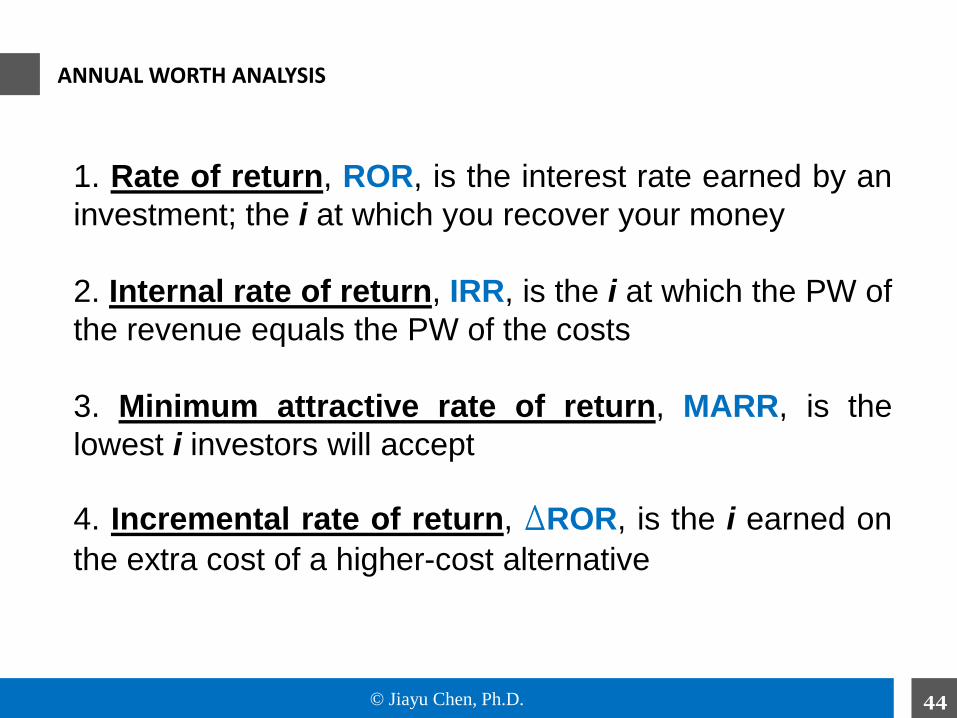

ANNUAL WORTH ANALYSIS

1. Rate of return, ROR, is the interest rate earned by an

investment; the i at which you recover your money

2. Internal rate of return, IRR, is the i at which the PW of

the revenue equals the PW of the costs

3. Minimum attractive rate of return, MARR, is the

lowest i investors will accept

4. Incremental rate of return, DROR, is the i earned on

the extra cost of a higher-cost alternative

© Jiayu Chen, Ph.D. 45

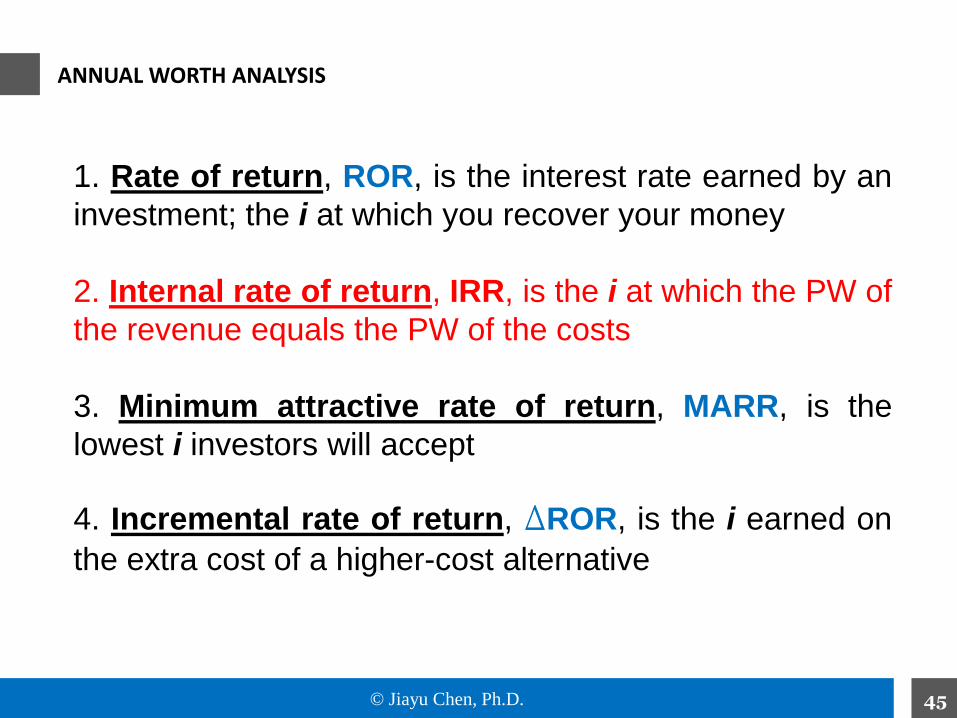

ANNUAL WORTH ANALYSIS

1. Rate of return, ROR, is the interest rate earned by an

investment; the i at which you recover your money

2. Internal rate of return, IRR, is the i at which the PW of

the revenue equals the PW of the costs

3. Minimum attractive rate of return, MARR, is the

lowest i investors will accept

4. Incremental rate of return, DROR, is the i earned on

the extra cost of a higher-cost alternative

© Jiayu Chen, Ph.D. 46

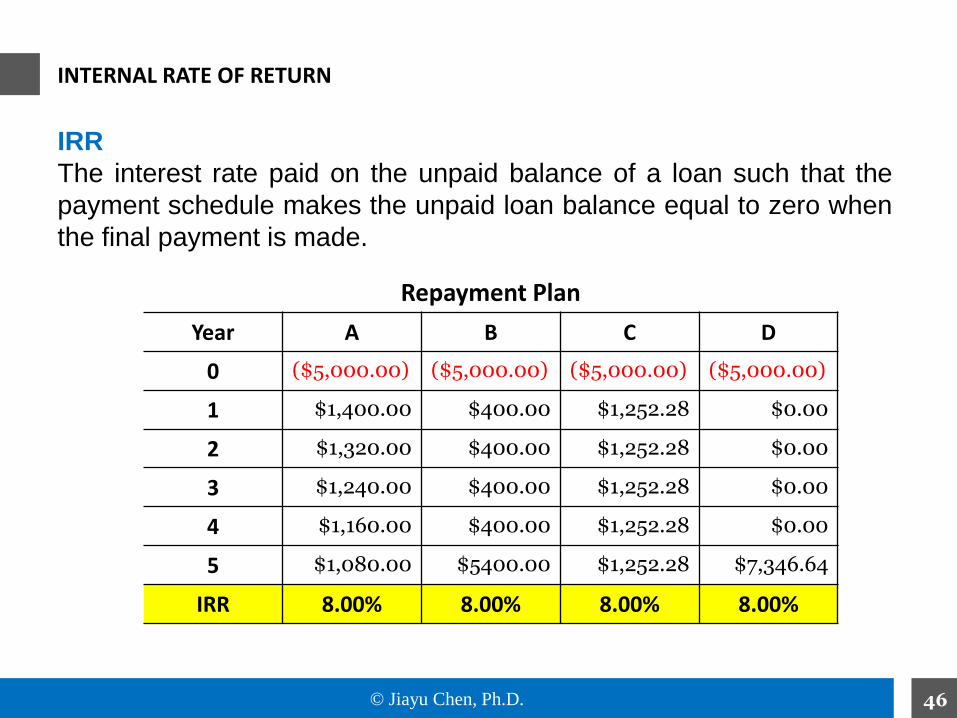

INTERNAL RATE OF RETURN

IRR

The interest rate paid on the unpaid balance of a loan such that the

payment schedule makes the unpaid loan balance equal to zero when

the final payment is made.

Repayment Plan

Year A B C D

0 ($5,000.00) ($5,000.00) ($5,000.00) ($5,000.00)

1 $1,400.00 $400.00 $1,252.28 $0.00

2 $1,320.00 $400.00 $1,252.28 $0.00

3 $1,240.00 $400.00 $1,252.28 $0.00

4 $1,160.00 $400.00 $1,252.28 $0.00

5 $1,080.00 $5400.00 $1,252.28 $7,346.64

IRR 8.00% 8.00% 8.00% 8.00%

© Jiayu Chen, Ph.D. 47

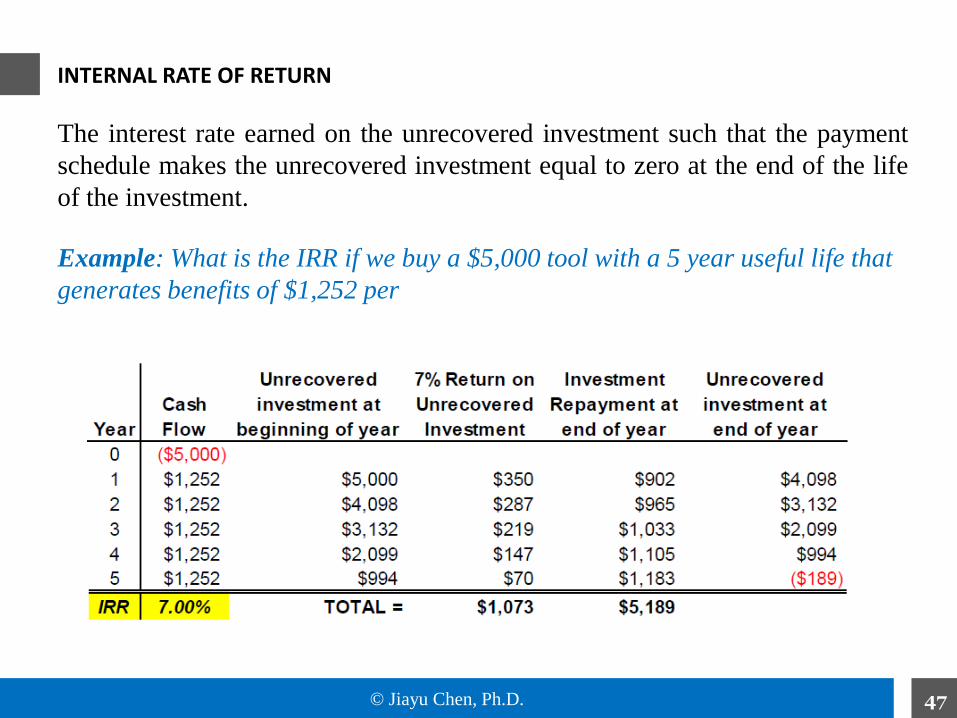

INTERNAL RATE OF RETURN

The interest rate earned on the unrecovered investment such that the payment

schedule makes the unrecovered investment equal to zero at the end of the life

of the investment.

Example: What is the IRR if we buy a $5,000 tool with a 5 year useful life that

generates benefits of $1,252 per year?

© Jiayu Chen, Ph.D. 48

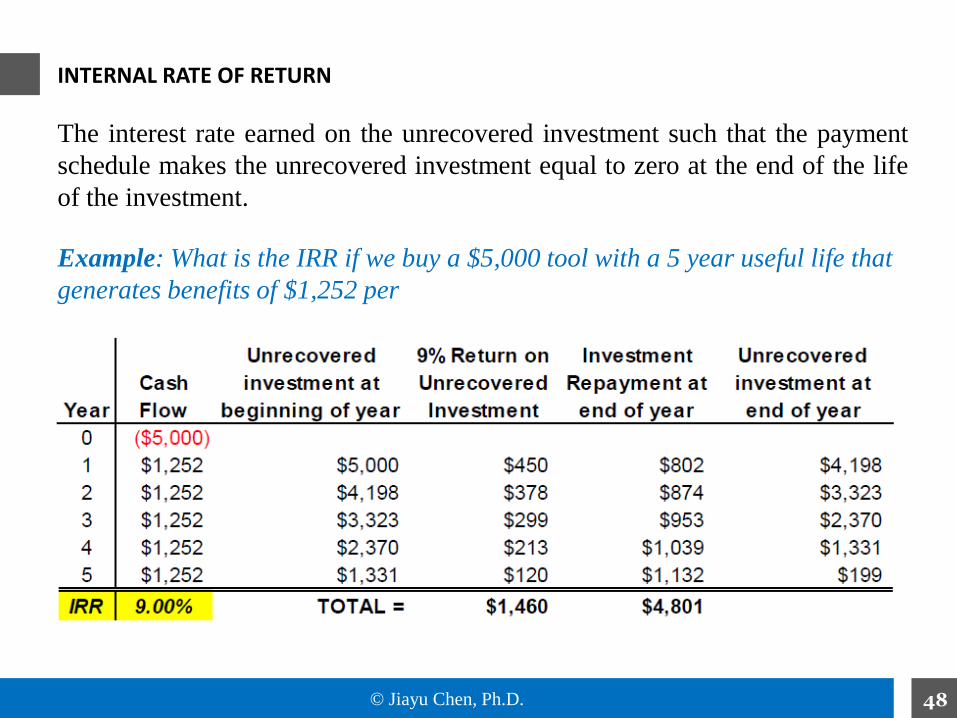

INTERNAL RATE OF RETURN

The interest rate earned on the unrecovered investment such that the payment

schedule makes the unrecovered investment equal to zero at the end of the life

of the investment.

Example: What is the IRR if we buy a $5,000 tool with a 5 year useful life that

generates benefits of $1,252 per year?

© Jiayu Chen, Ph.D. 49

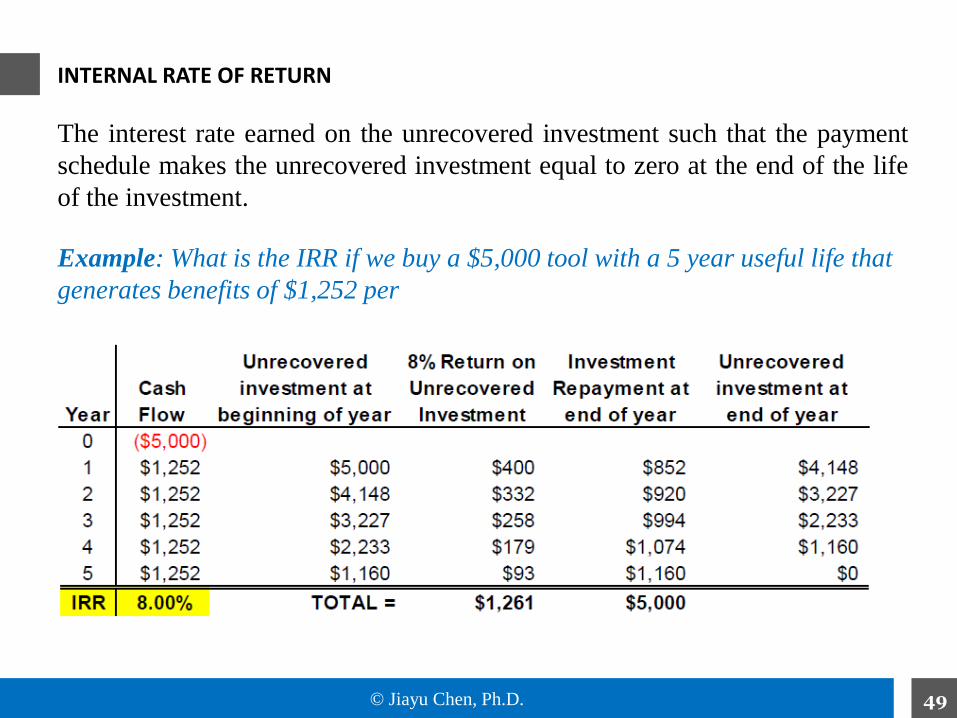

INTERNAL RATE OF RETURN

The interest rate earned on the unrecovered investment such that the payment

schedule makes the unrecovered investment equal to zero at the end of the life

of the investment.

Example: What is the IRR if we buy a $5,000 tool with a 5 year useful life that

generates benefits of $1,252 per year?

© Jiayu Chen, Ph.D. 50

• MARR is the lowest i investors will accept

• IRR ≥MARR to proceed

• When two alternatives have equal first costs (or initial investments),

choose the one with higher IRR.

• If alternatives have IRR ≥MARR and different costs, then look at the cost

of each and decide whether the incremental investment is worthwhile

INTERNAL RATE OF RETURN

Minimum Attractive Rate of Return (MARR)

Make sure you understand a positive NPV and MARR

© Jiayu Chen, Ph.D. 51

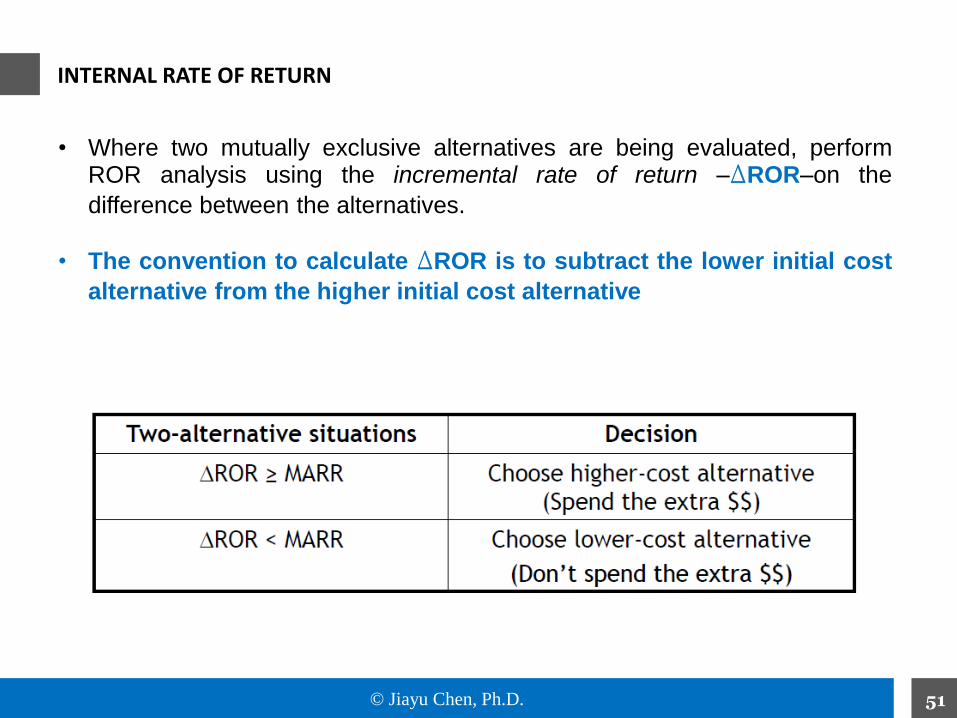

INTERNAL RATE OF RETURN

• Where two mutually exclusive alternatives are being evaluated, performROR analysis using the incremental rate of return –DROR–on the

difference between the alternatives.

• The convention to calculate DROR is to subtract the lower initial cost

alternative from the higher initial cost alternative

© Jiayu Chen, Ph.D. 52

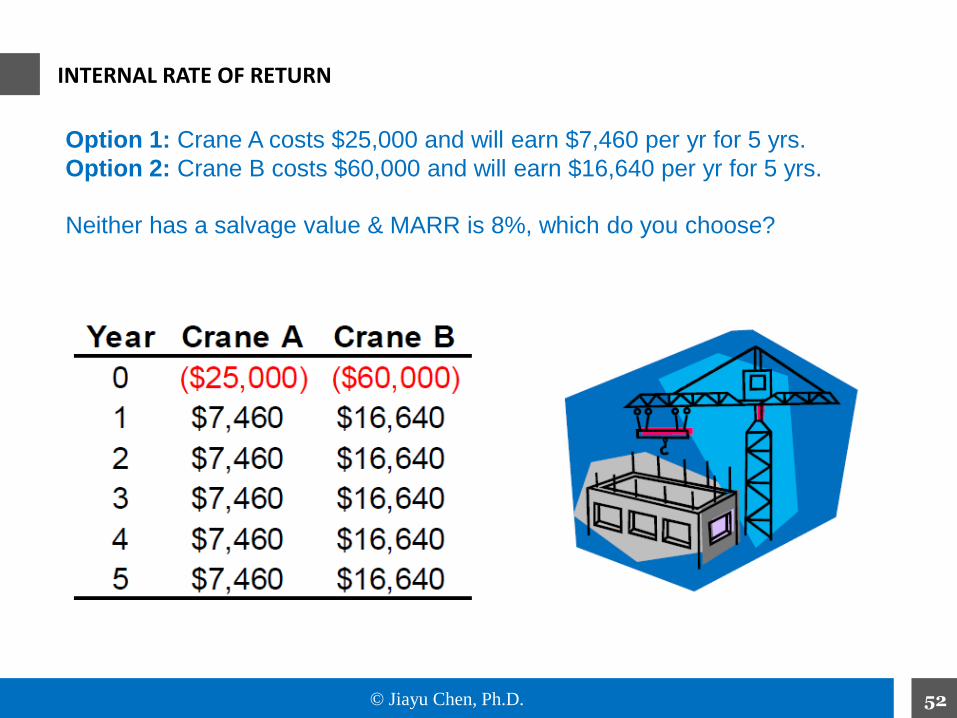

Option 1: Crane A costs $25,000 and will earn $7,460 per yr for 5 yrs.

Option 2: Crane B costs $60,000 and will earn $16,640 per yr for 5 yrs.

Neither has a salvage value & MARR is 8%, which do you choose?

INTERNAL RATE OF RETURN

© Jiayu Chen, Ph.D. 53

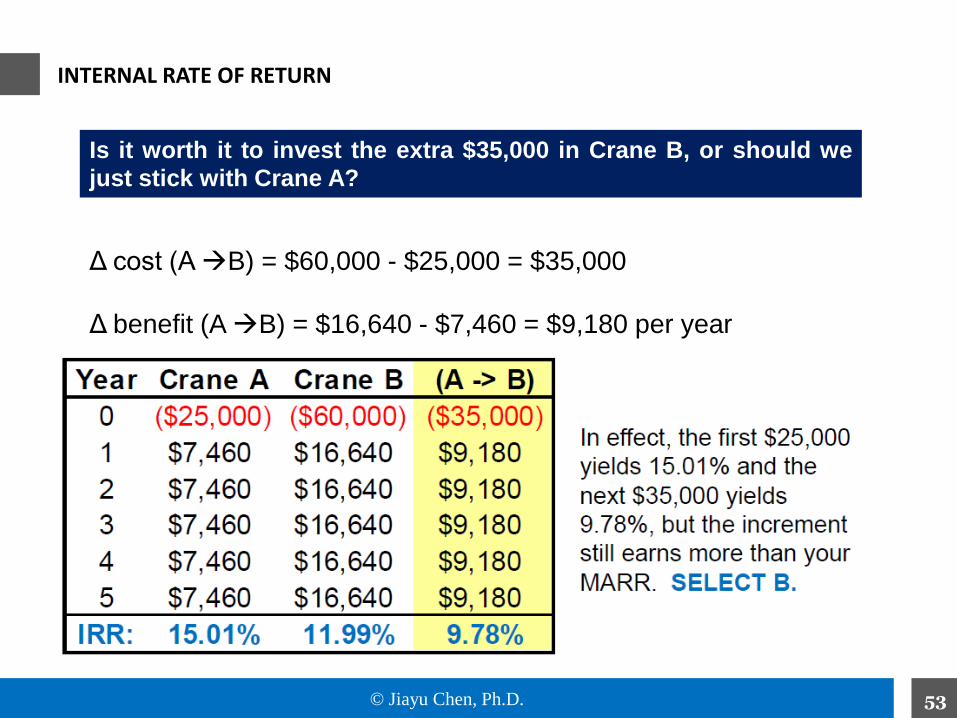

INTERNAL RATE OF RETURN

Is it worth it to invest the extra $35,000 in Crane B, or should we

just stick with Crane A?

Δ cost (A B) = $60,000 - $25,000 = $35,000

Δ benefit (A B) = $16,640 - $7,460 = $9,180 per year

© Jiayu Chen, Ph.D. 54

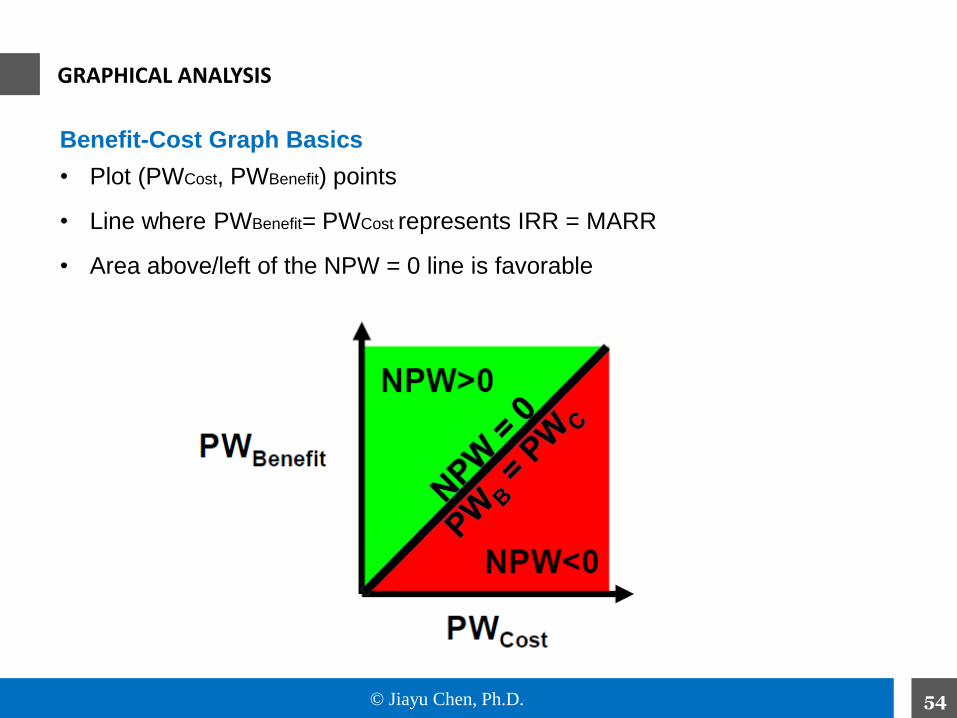

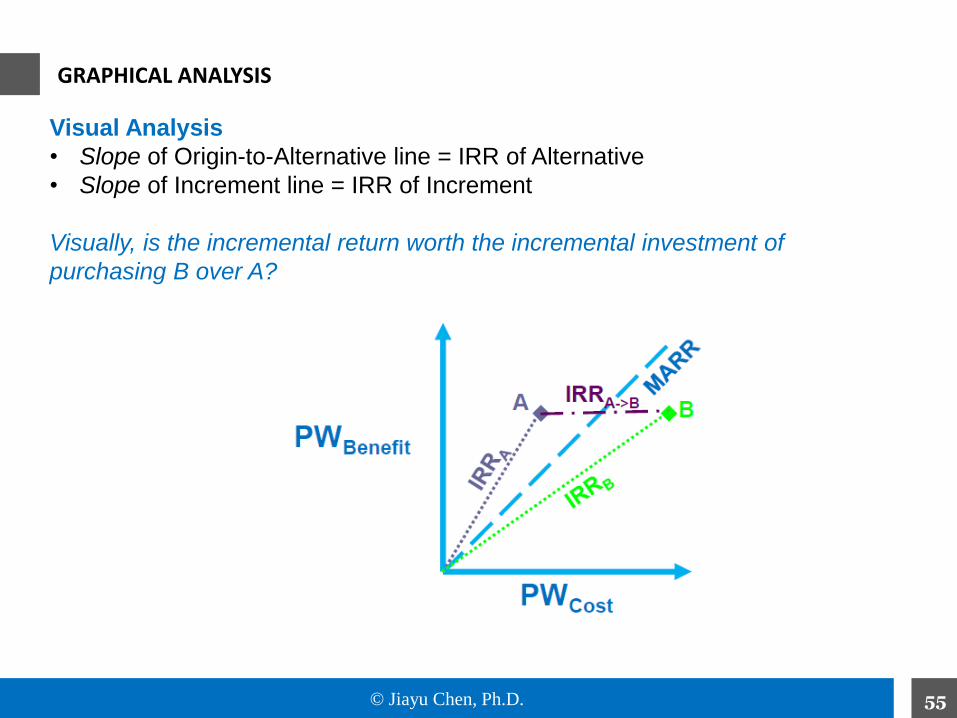

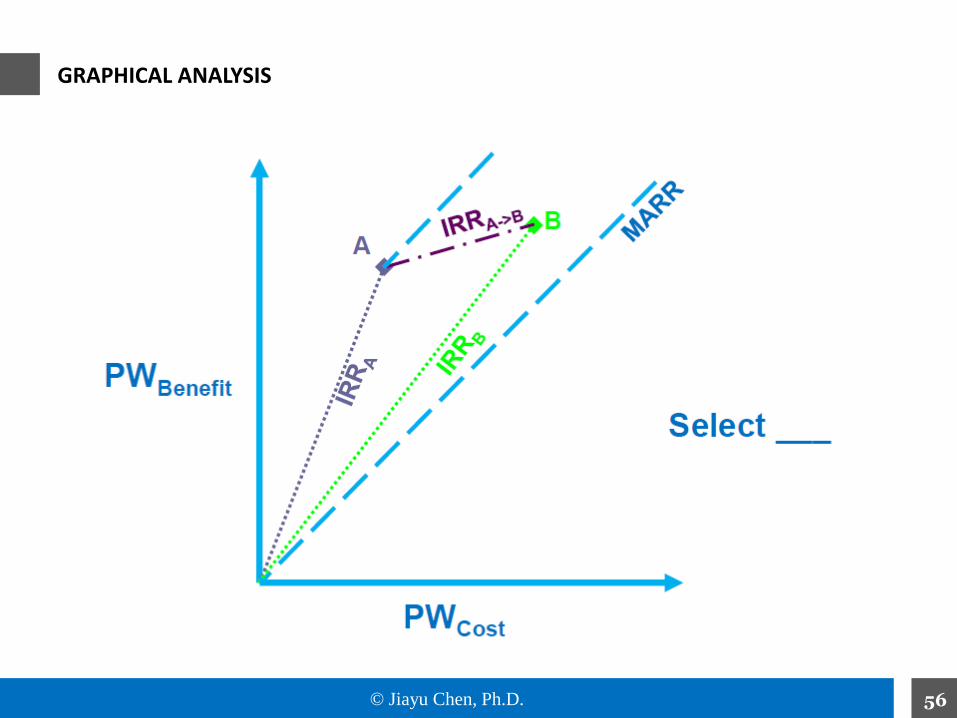

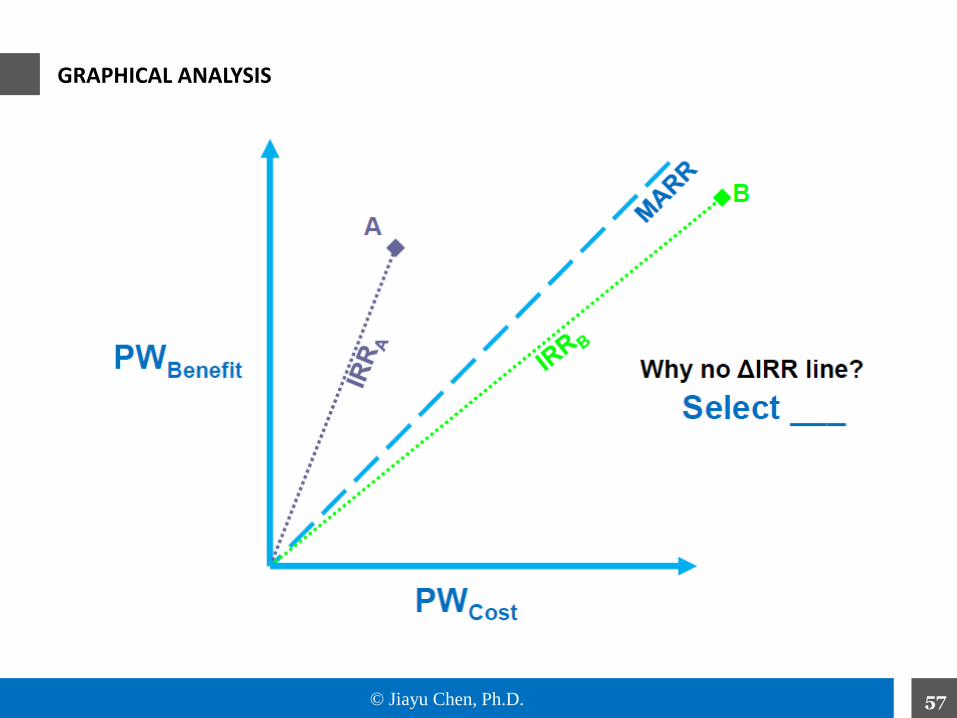

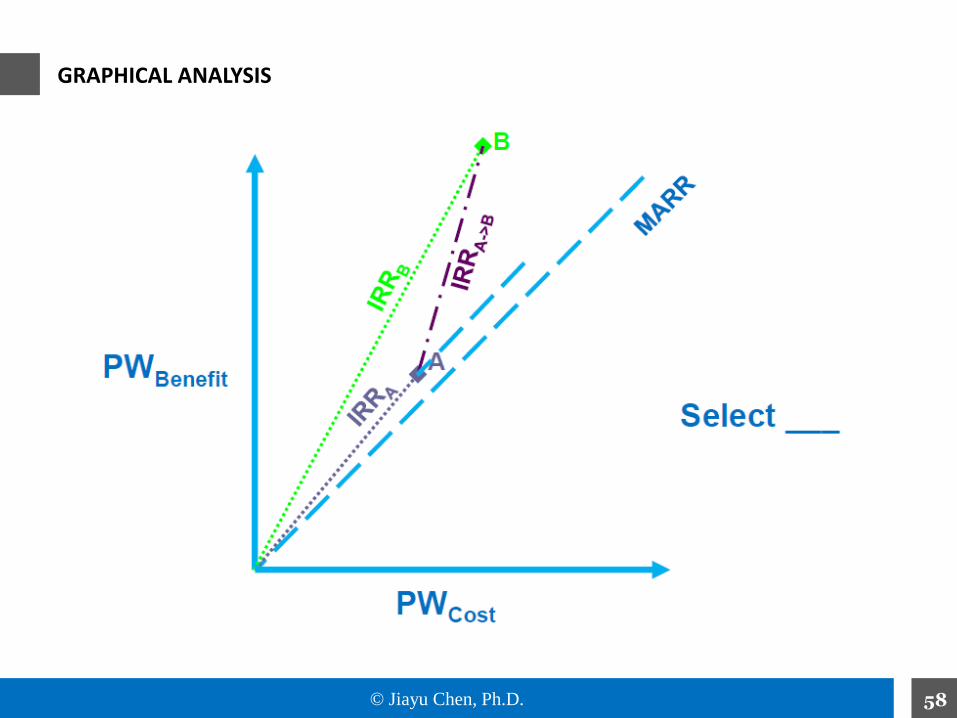

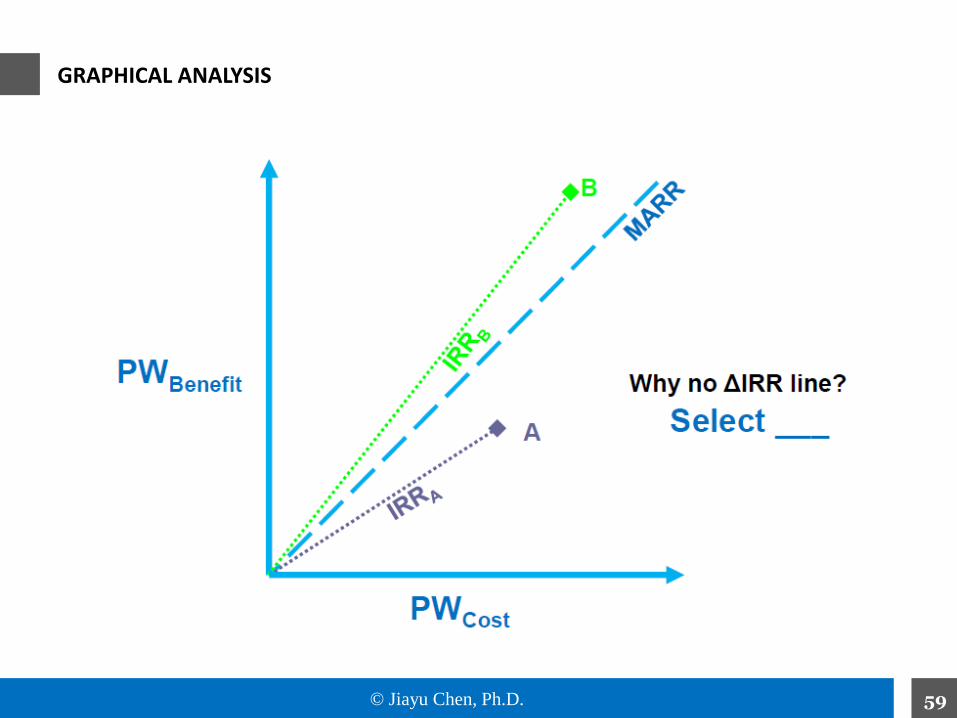

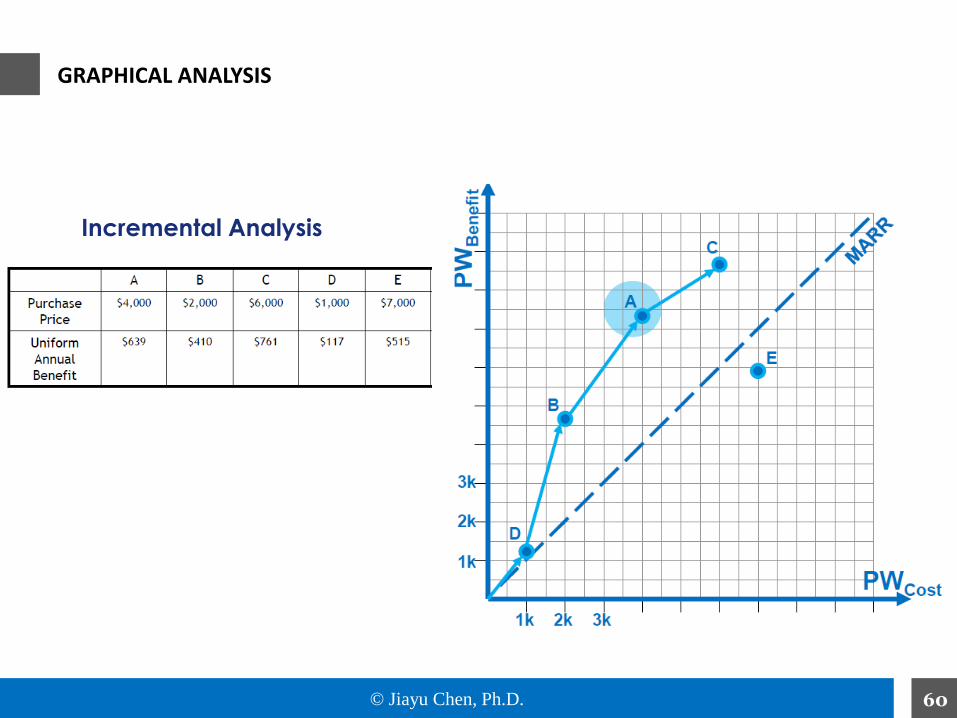

Benefit-Cost Graph Basics

• Plot (PWCost, PWBenefit) points

• Line where PWBenefit= PWCost represents IRR = MARR

• Area above/left of the NPW = 0 line is favorable

GRAPHICAL ANALYSIS

© Jiayu Chen, Ph.D. 55

Visual Analysis

• Slope of Origin-to-Alternative line = IRR of Alternative

• Slope of Increment line = IRR of Increment

Visually, is the incremental return worth the incremental investment of

purchasing B over A?

GRAPHICAL ANALYSIS

© Jiayu Chen, Ph.D. 56

GRAPHICAL ANALYSIS

© Jiayu Chen, Ph.D. 57

GRAPHICAL ANALYSIS

© Jiayu Chen, Ph.D. 58

GRAPHICAL ANALYSIS

© Jiayu Chen, Ph.D. 59

GRAPHICAL ANALYSIS

© Jiayu Chen, Ph.D. 60

Incremental Analysis

GRAPHICAL ANALYSIS

© Jiayu Chen, Ph.D. 61

RATIONING

• Until now all worthwhile projects were funded

– In reality companies have more projects than resources to complete them

• Until now options were interdependent (i.e., we selected one winner

from mutual exclusive alternatives)

– Now we will evaluate independent projects

• How do we ration capital among independent projects?

– Rate of Return or Present Worth methods

© Jiayu Chen, Ph.D. 62

RATIONING

© Jiayu Chen, Ph.D. 63

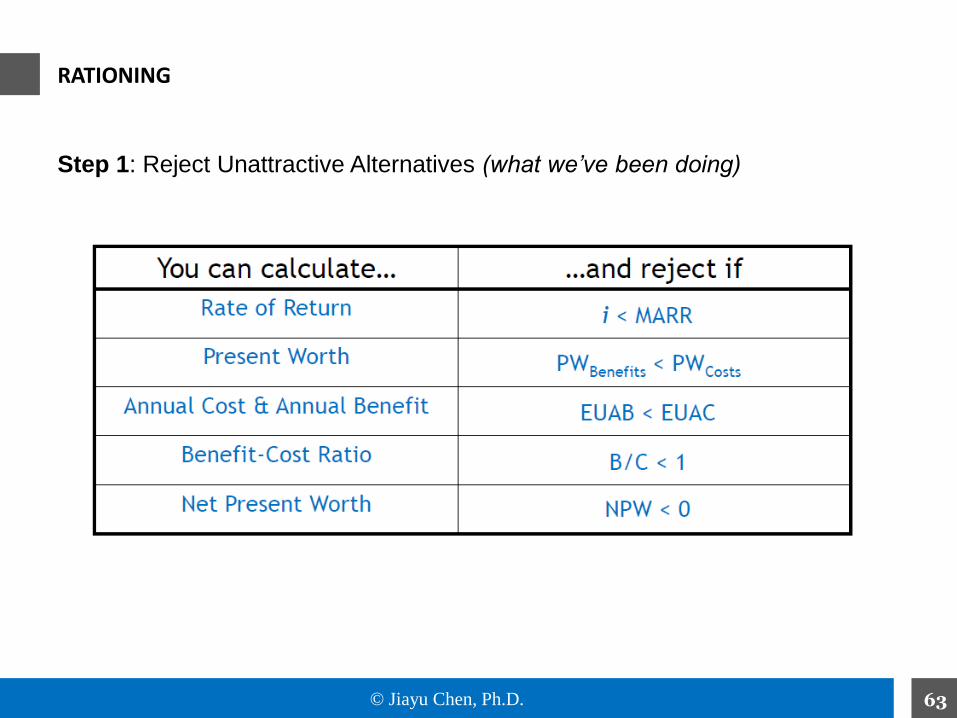

Step 1: Reject Unattractive Alternatives (what we’ve been doing)

RATIONING

© Jiayu Chen, Ph.D. 64

RATIONING

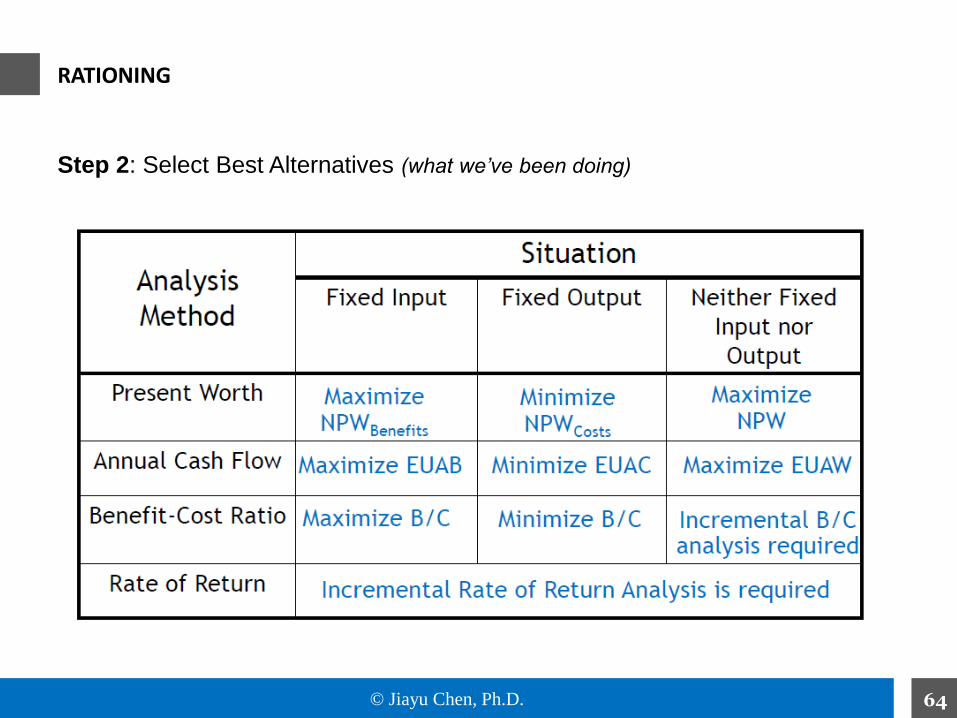

Step 2: Select Best Alternatives (what we’ve been doing)

© Jiayu Chen, Ph.D. 65

RATIONING

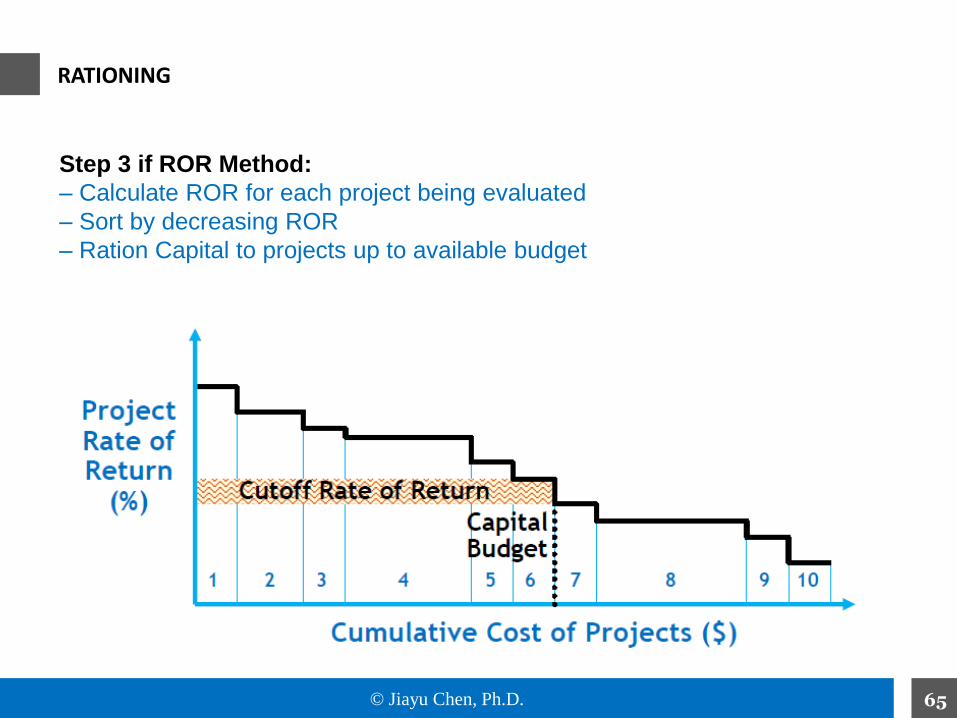

Step 3 if ROR Method:

– Calculate ROR for each project being evaluated

– Sort by decreasing ROR

– Ration Capital to projects up to available budget

© Jiayu Chen, Ph.D. 66

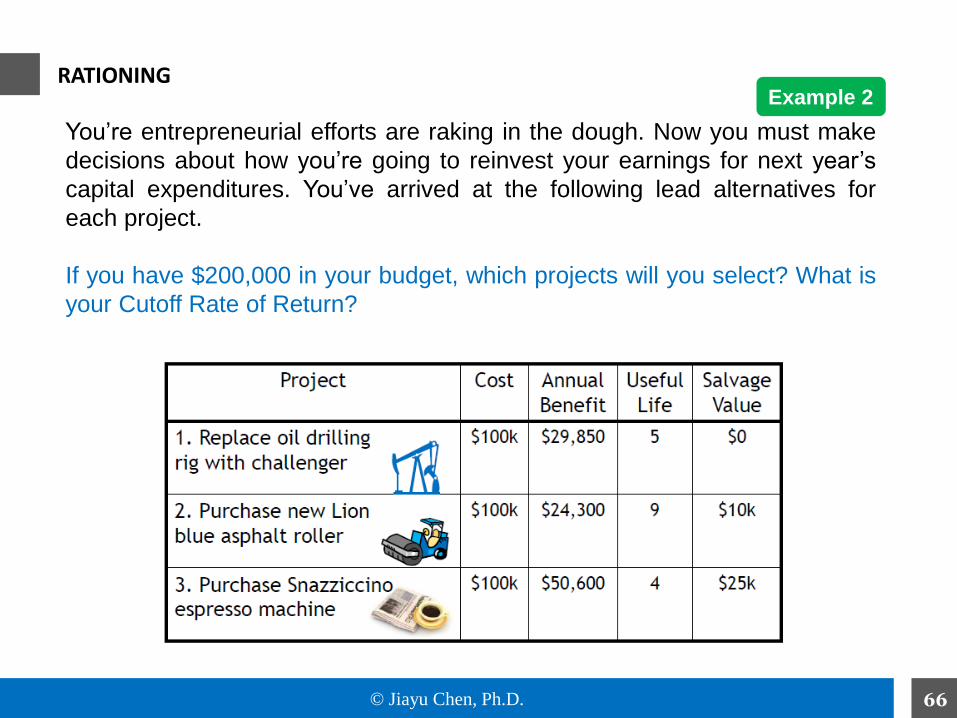

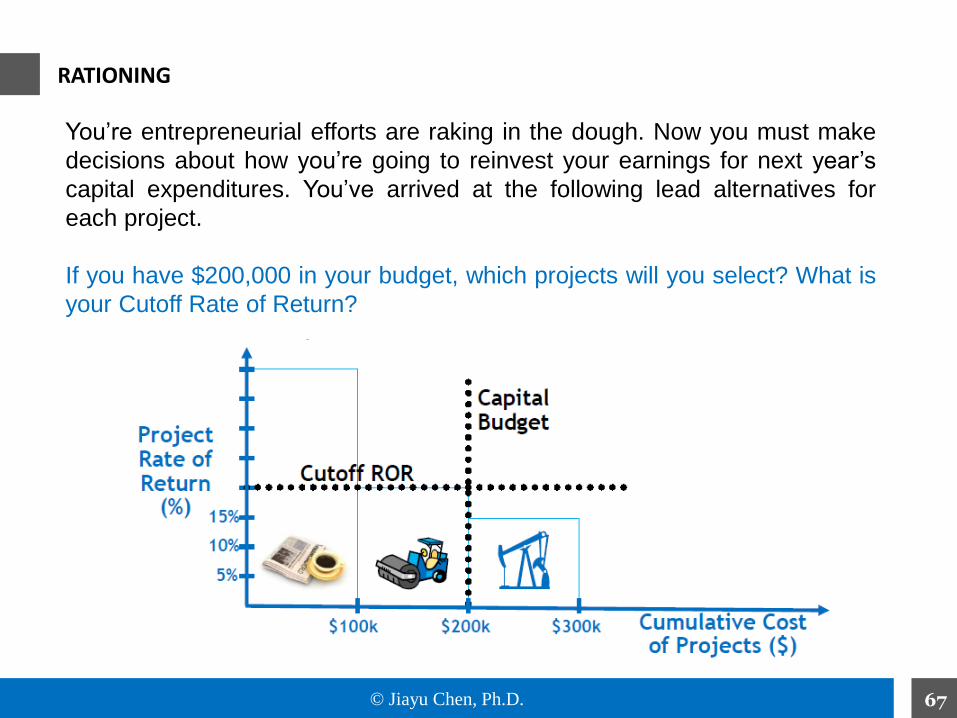

You’re entrepreneurial efforts are raking in the dough. Now you must make

decisions about how you’re going to reinvest your earnings for next year’s

capital expenditures. You’ve arrived at the following lead alternatives for

each project.

If you have $200,000 in your budget, which projects will you select? What is

your Cutoff Rate of Return?

RATIONING Example 2

© Jiayu Chen, Ph.D. 67

You’re entrepreneurial efforts are raking in the dough. Now you must make

decisions about how you’re going to reinvest your earnings for next year’s

capital expenditures. You’ve arrived at the following lead alternatives for

each project.

If you have $200,000 in your budget, which projects will you select? What is

your Cutoff Rate of Return?

RATIONING

© Jiayu Chen, Ph.D. 68

Step 3 if PV Method:

– At times the question the budget committee will ask how to rank the projects

(as opposed to just deciding which projects to fund)

– Divide the Net Present Value by the Present Value of the Costs at the

Minimum Attractive Rate of Return to arrive at a ratio as follows:

NPV PVCost

– Place the projects in order of decreasing NPV PVCost ratio values in order to

determine the projects’ rank order

(highest ratio is highest rank)

RATIONING

© Jiayu Chen, Ph.D. 69

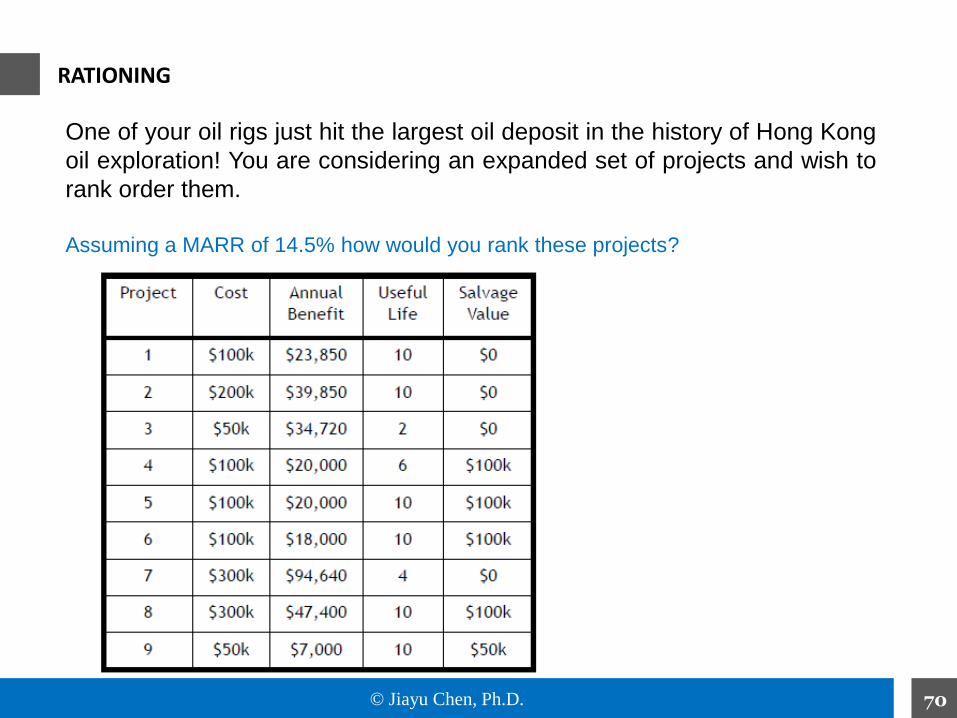

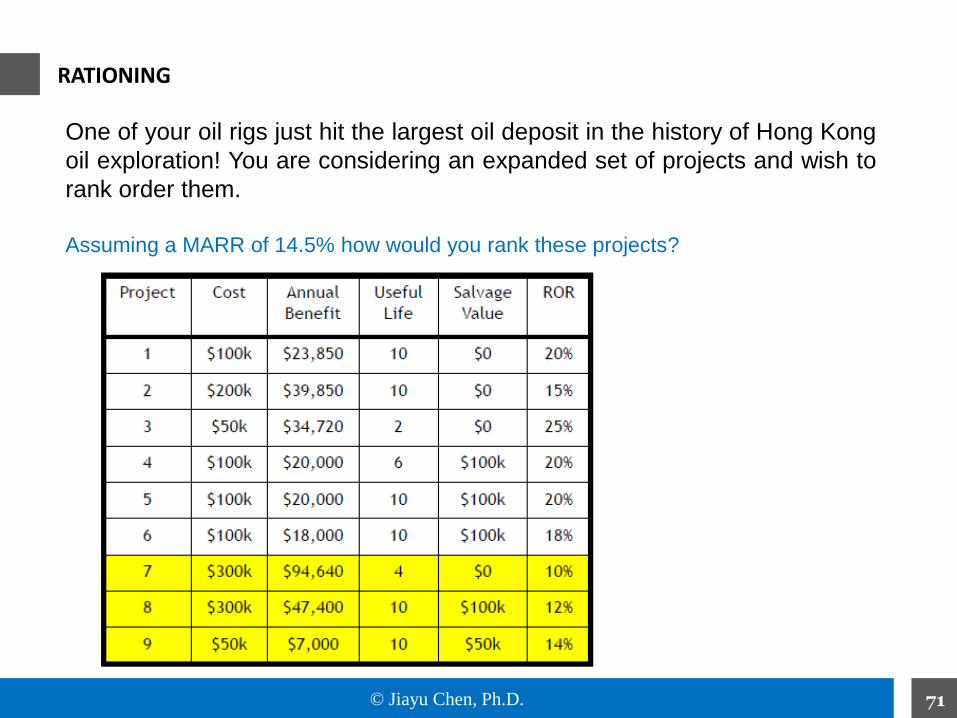

One of your oil rigs just hit the largest oil deposit in the history of Hong Kong

oil exploration! You are considering an expanded set of projects and wish to

rank order them.

Assuming a MARR of 14.5% how would you rank these projects?

RATIONING

© Jiayu Chen, Ph.D. 70

RATIONING

One of your oil rigs just hit the largest oil deposit in the history of Hong Kong

oil exploration! You are considering an expanded set of projects and wish to

rank order them.

Assuming a MARR of 14.5% how would you rank these projects?

© Jiayu Chen, Ph.D. 71

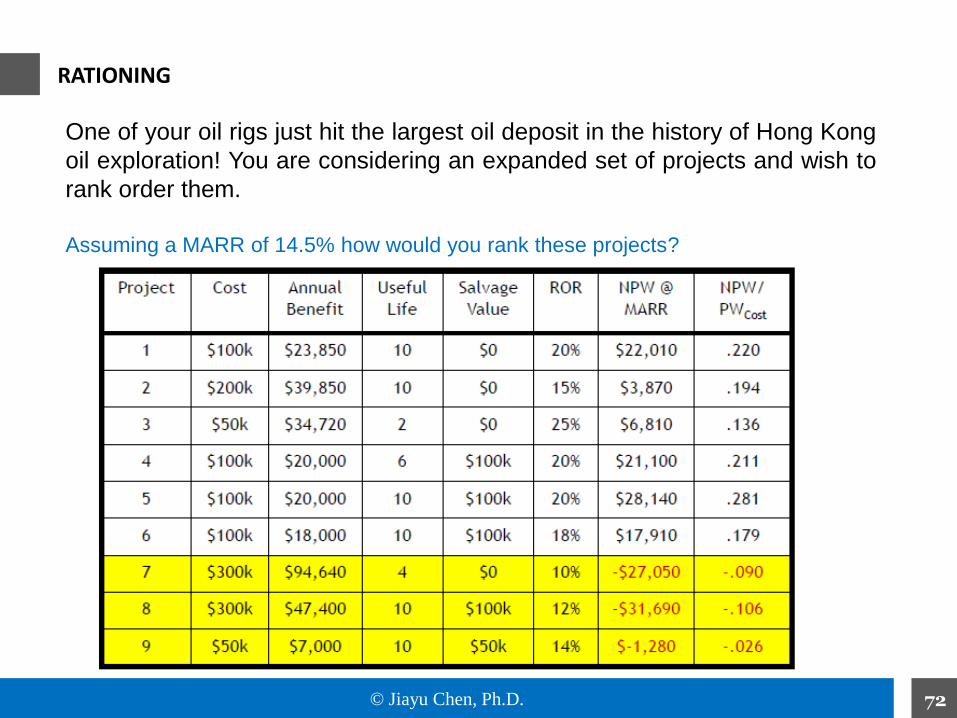

RATIONING

One of your oil rigs just hit the largest oil deposit in the history of Hong Kong

oil exploration! You are considering an expanded set of projects and wish to

rank order them.

Assuming a MARR of 14.5% how would you rank these projects?

© Jiayu Chen, Ph.D. 72

RATIONING

One of your oil rigs just hit the largest oil deposit in the history of Hong Kong

oil exploration! You are considering an expanded set of projects and wish to

rank order them.

Assuming a MARR of 14.5% how would you rank these projects?

© Jiayu Chen, Ph.D. 73

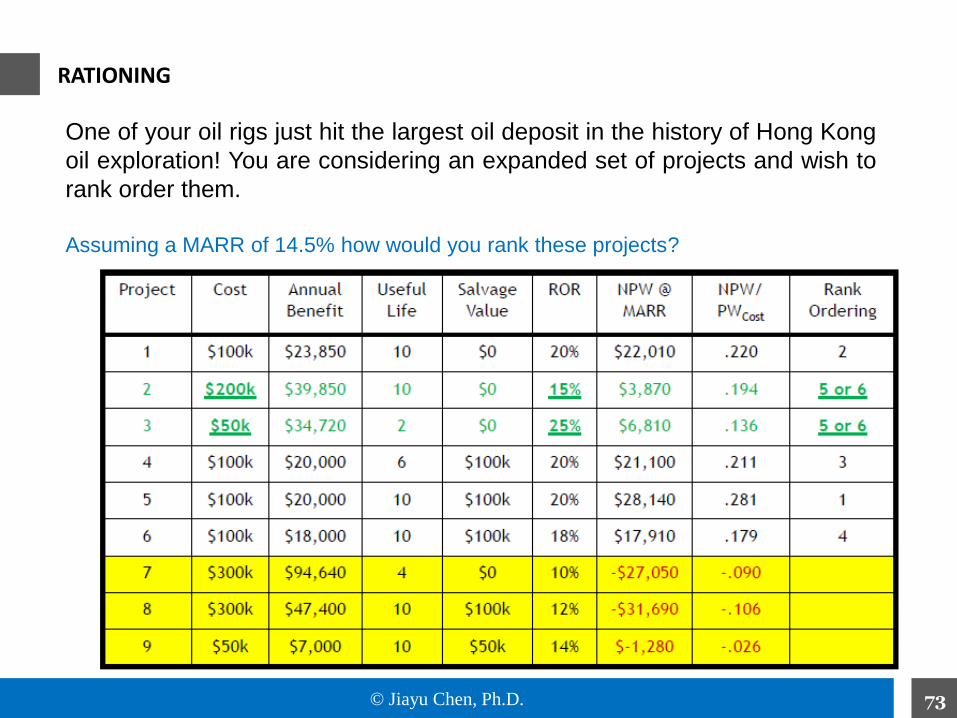

RATIONING

One of your oil rigs just hit the largest oil deposit in the history of Hong Kong

oil exploration! You are considering an expanded set of projects and wish to

rank order them.

Assuming a MARR of 14.5% how would you rank these projects?

© Jiayu Chen, Ph.D. 74

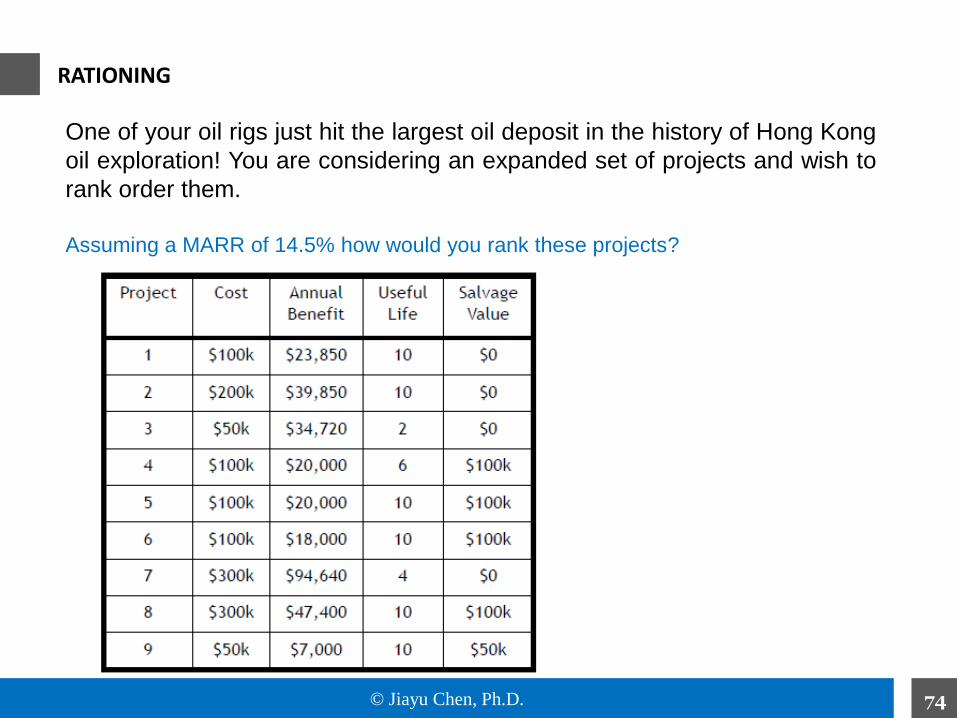

RATIONING

One of your oil rigs just hit the largest oil deposit in the history of Hong Kong

oil exploration! You are considering an expanded set of projects and wish to

rank order them.

Assuming a MARR of 14.5% how would you rank these projects?

© Jiayu Chen, Ph.D. 75

It is a decline in value resulting from…

– Decline in market value of an asset

– Decline in value of an asset to its owner(due to

obsolescence or deterioration)

DEPRECIATION

Depreciation is a systematic allocation of the cost of an asset over its

depreciable life.

Depreciation vs. Expense !

© Jiayu Chen, Ph.D. 76

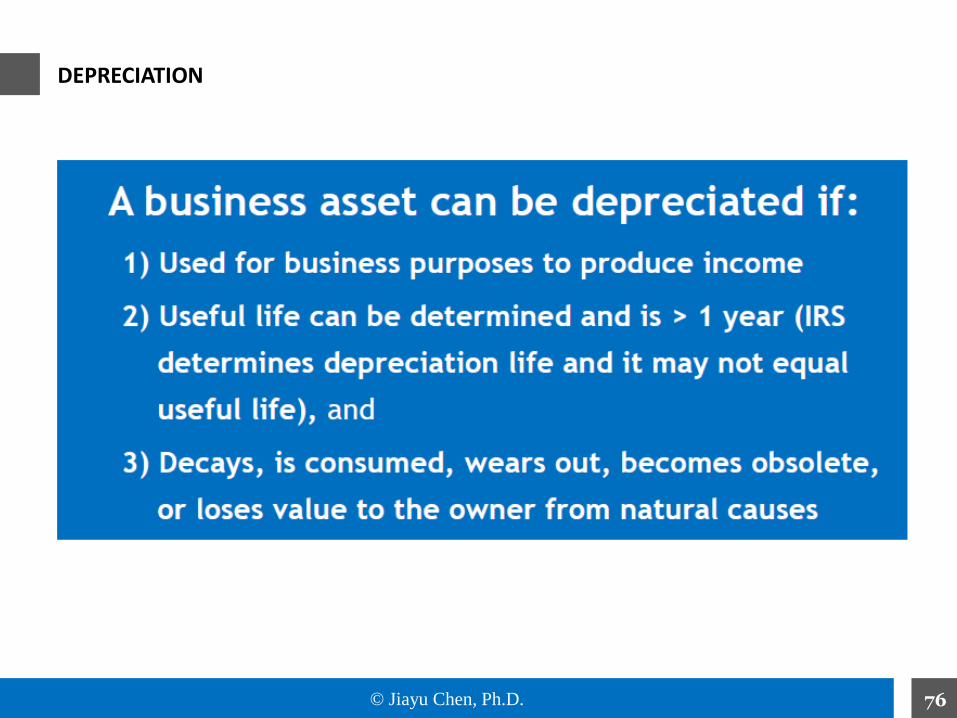

DEPRECIATION

© Jiayu Chen, Ph.D. 77

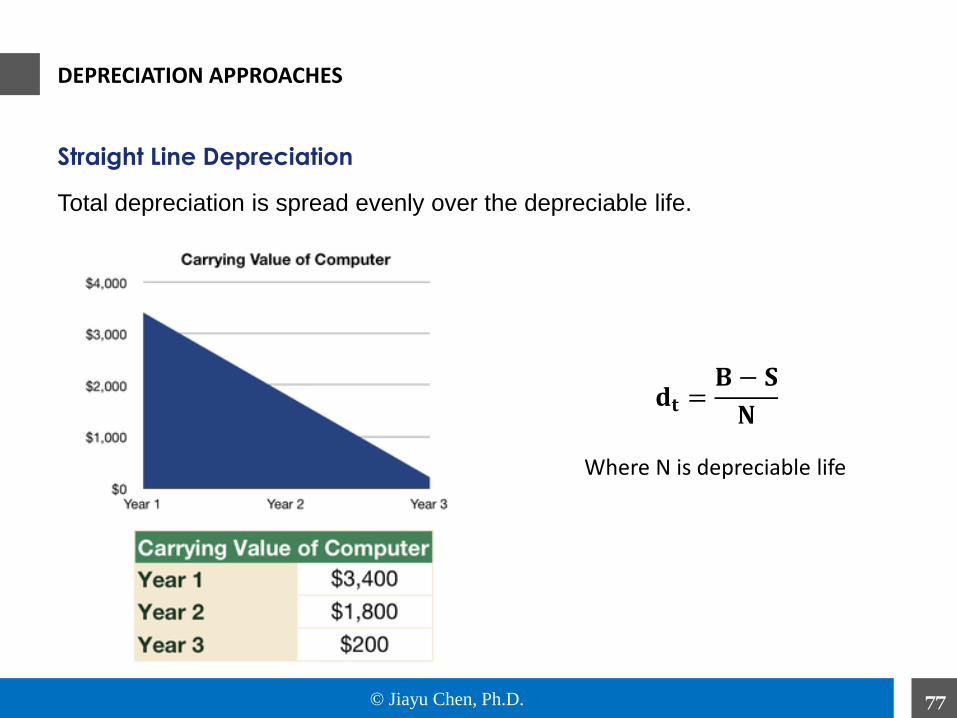

Total depreciation is spread evenly over the depreciable life.

Straight Line Depreciation

DEPRECIATION APPROACHES

𝐝𝐭 =𝐁 − 𝐒

𝐍

Where N is depreciable life

© Jiayu Chen, Ph.D. 78

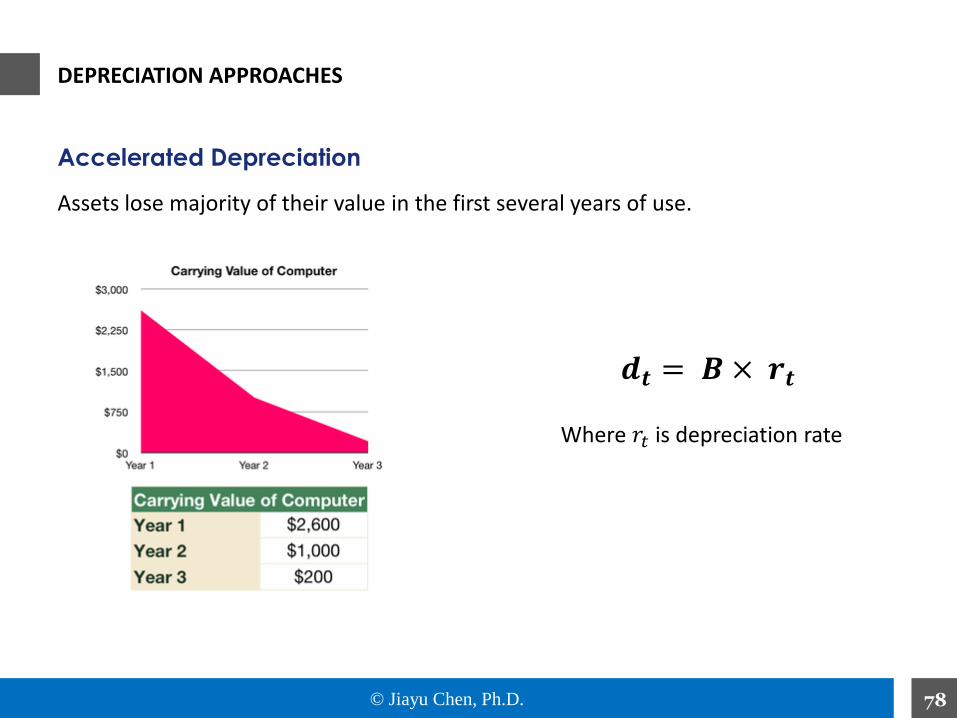

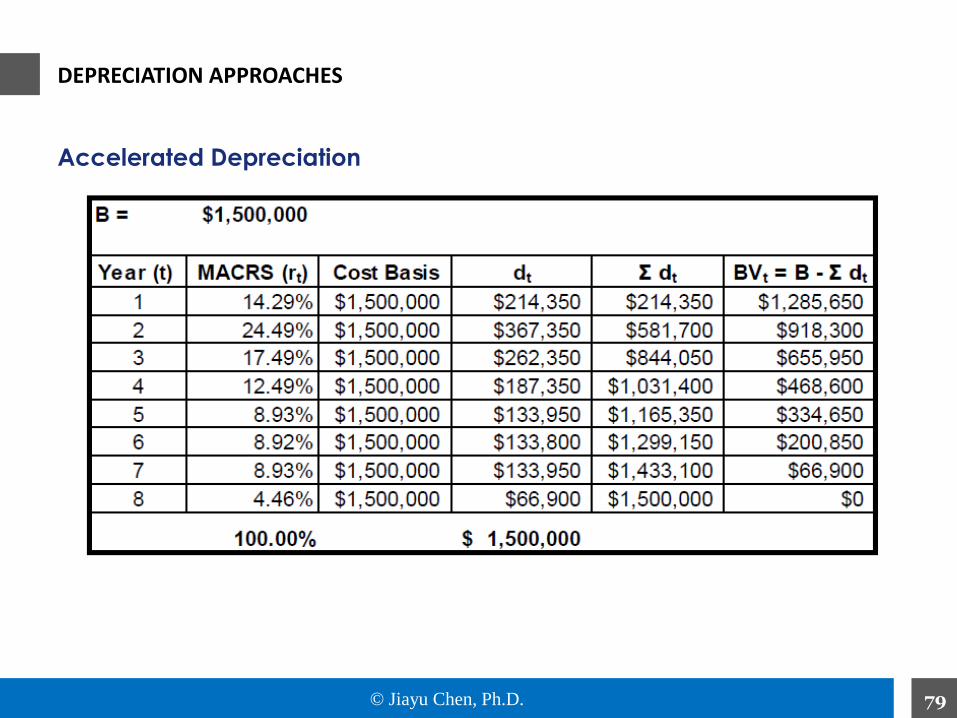

DEPRECIATION APPROACHES

Assets lose majority of their value in the first several years of use.

Accelerated Depreciation

𝒅𝒕 = 𝑩 × 𝒓𝒕

Where 𝑟𝑡 is depreciation rate

© Jiayu Chen, Ph.D. 79

Accelerated Depreciation

DEPRECIATION APPROACHES

© Jiayu Chen, Ph.D. 80

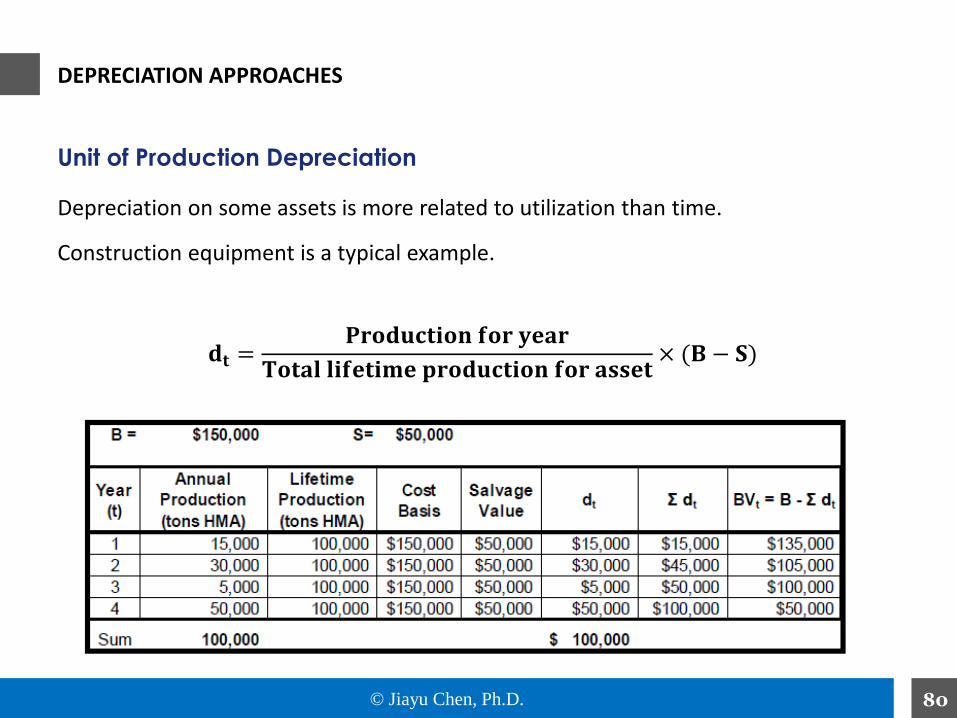

Unit of Production Depreciation

DEPRECIATION APPROACHES

Depreciation on some assets is more related to utilization than time.

Construction equipment is a typical example.

𝐝𝐭 =𝐏𝐫𝐨𝐝𝐮𝐜𝐭𝐢𝐨𝐧 𝐟𝐨𝐫 𝐲𝐞𝐚𝐫

𝐓𝐨𝐭𝐚𝐥 𝐥𝐢𝐟𝐞𝐭𝐢𝐦𝐞 𝐩𝐫𝐨𝐝𝐮𝐜𝐭𝐢𝐨𝐧 𝐟𝐨𝐫 𝐚𝐬𝐬𝐞𝐭× (𝐁 − 𝐒)

© Jiayu Chen, Ph.D. 81Thank You!