Embed Size (px)

Citation preview

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 1/48

Georgia Transport Sector Assessment, Strategy,

and Road MapTRANSPORT AND COMMUNICATIONS. Georgia

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 2/48

Georgia ransport

Sector Assessment, Strategy,and Road Map

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 3/48

© 2014 Asian Development Bank

All rights reserved. Published in 2014.Printed in the Philippines

ISBN 978-92-9254-411-9 (Print), 978-92-9254-412-6 (PDF)Publication Stock No. RP 136127-3

Cataloging-In-Publication Data

Asian Development Bank. Georgia transport sector assessment, strategy, and road map.Mandaluyong City, Philippines: Asian Development Bank, 2014.

1. Georgia 2. ransport sector. 3. Assessment. I. Asian Development Bank.

Te views expressed in this publication are those of the authors and do not necessarily reect the views and policies of the AsianDevelopment Bank (ADB) or its Board of Governors or the governments they represent.

ADB does not guarantee the accuracy of the data included in this publication and accepts no responsibility for any consequenceof their use.

By making any designation of or reference to a particular territory or geographic area, or by using the term “country” in thisdocument, ADB does not intend to make any judgments as to the legal or other status of any territory or area.

ADB encourages printing or copying information exclusively for personal and noncommercial use with proper acknowledgment ofADB. Users are restricted from reselling, redistributing, or creating derivative works for commercial purposes without the express,written consent of ADB.

Asian Development Bank 6 ADB Avenue, Mandaluyong City 1550 Metro Manila, Philippines

el +63 2 632 4444Fax +63 2 636 2444www.adb.org

For orders, please contact:Public Information CenterFax +63 2 636 [email protected]

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 4/48

Contents

ables and Figures iv

Currency Equivalents v

Abbreviations v

Acknowledgments vi

Executive Summary vii

I. Introduction 1

II. Sector Assessment: Current Status and Strategic Issues 2

A. Sector Performance 2

B. Strategic Issues 4

C. Cross-Sector Issues 17

D. Conclusions 21

III. Current Sector Strategies 23

A. Government Strategy 23

B. ADB Strategy, Support, and Experience 23

C. Other Development Partner Support 24

D. ADB’s Forward Strategy and Program 24

IV. ransport Sector Road Map and Results Framework 26

Appendixes

1. List of Stakeholders Consulted in June–September 2012 27

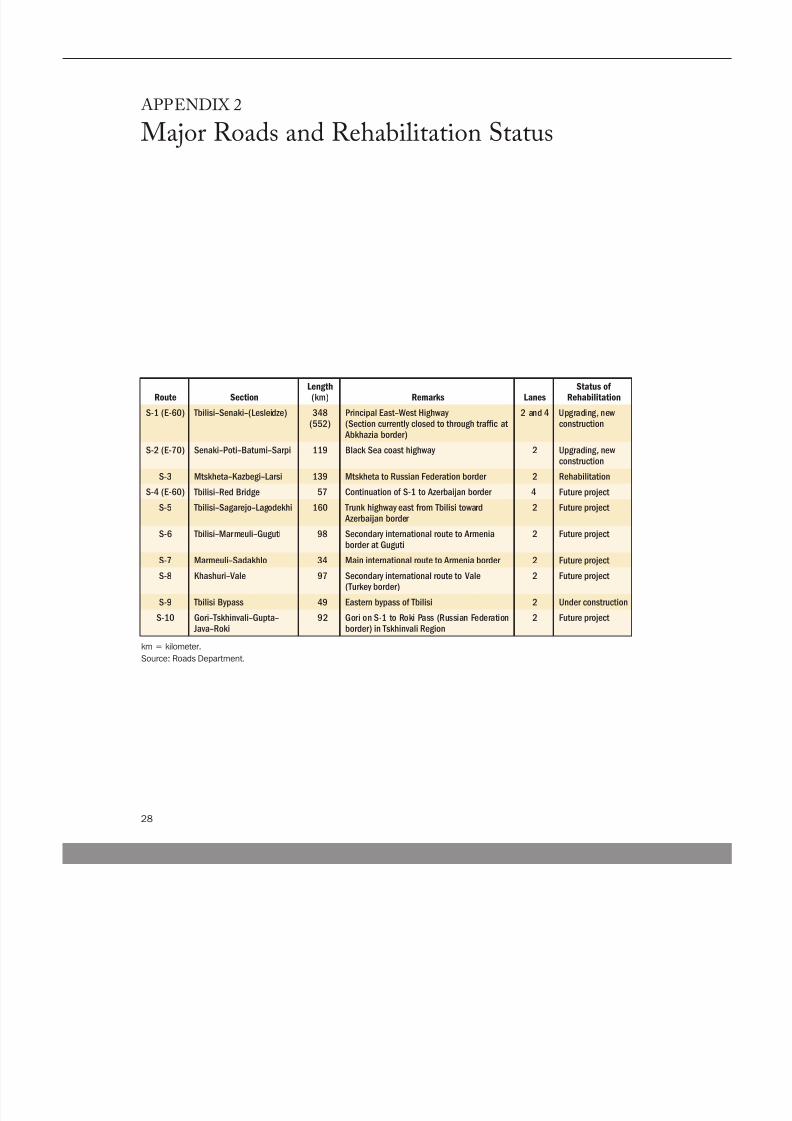

2. Major Roads and Rehabilitation Status 28

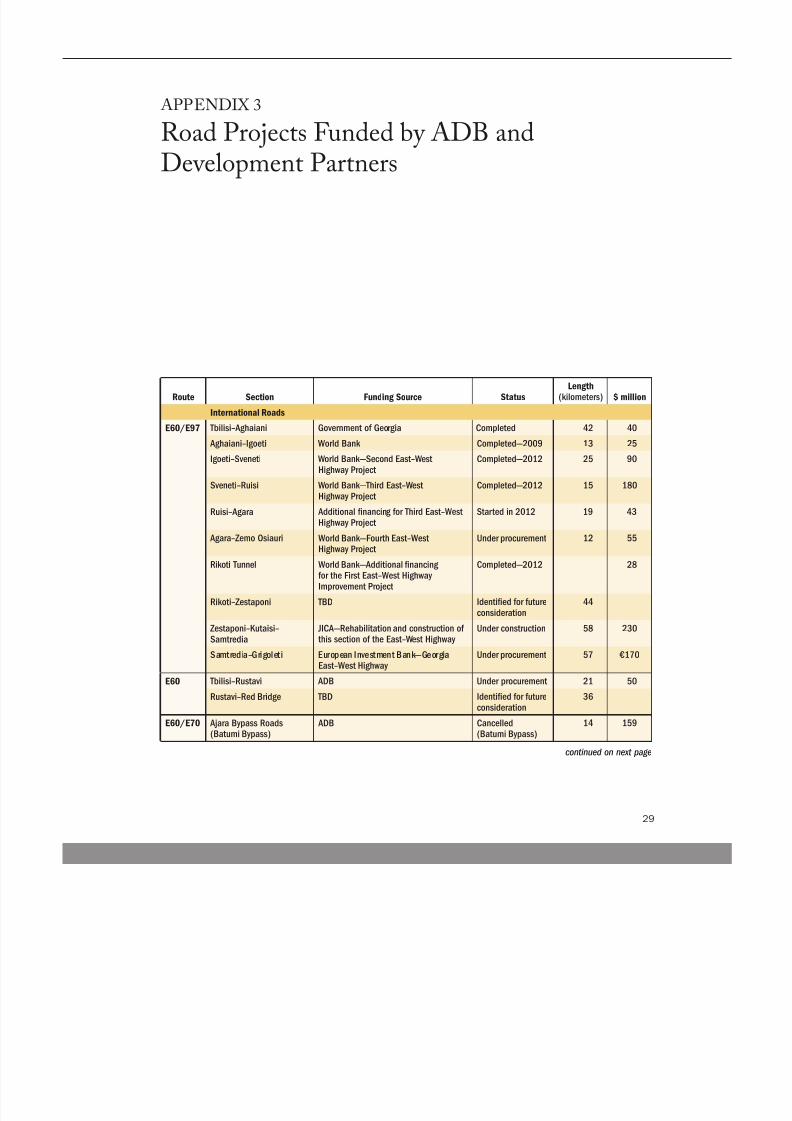

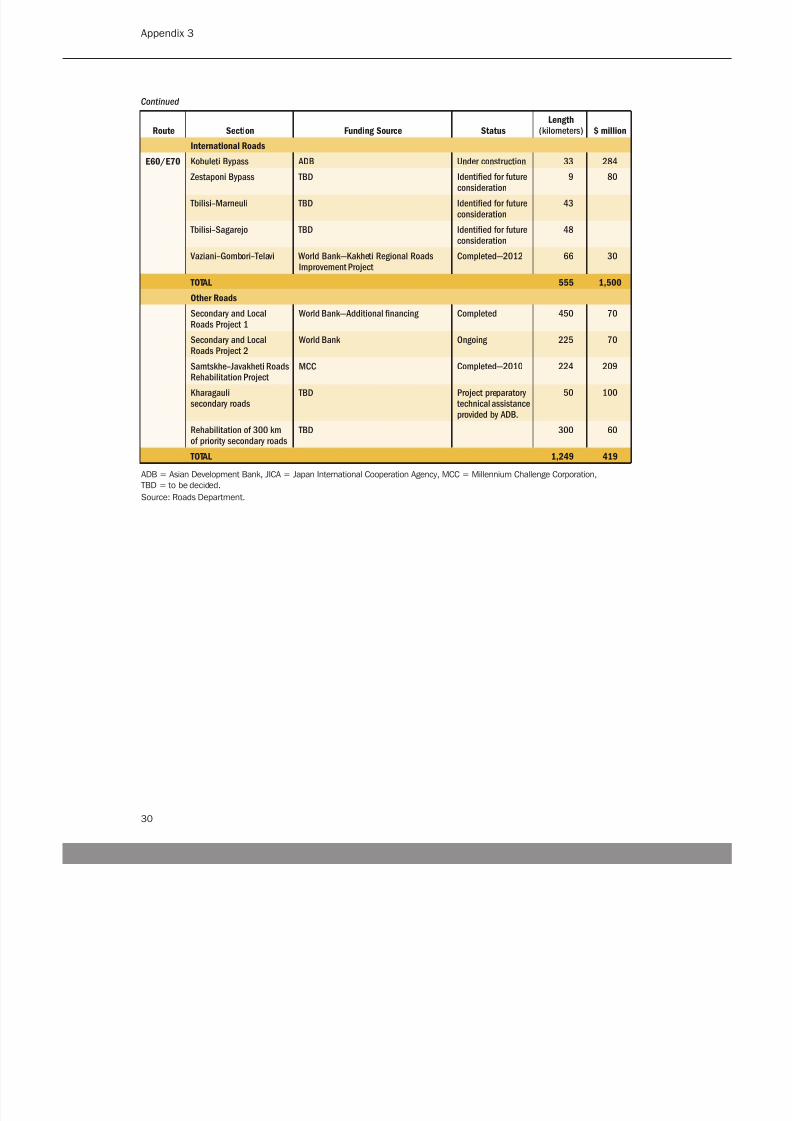

3. Road Projects Funded by ADB and Development Partners 29

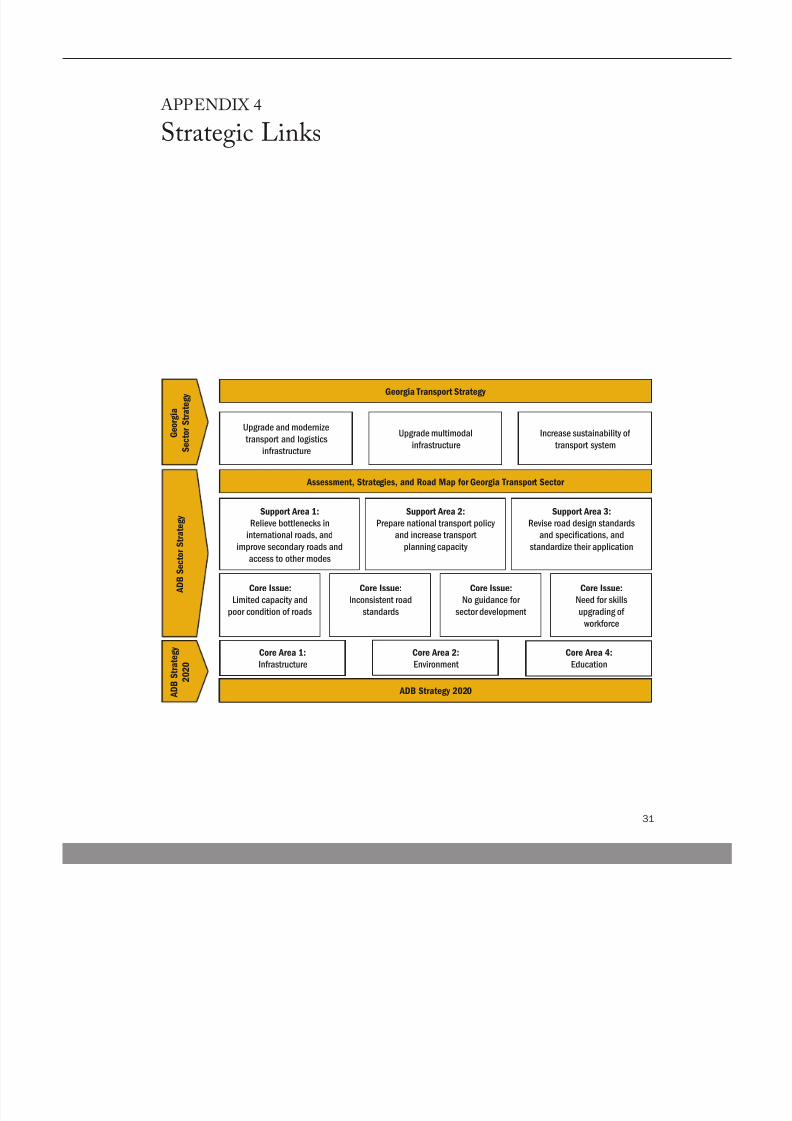

4. Strategic Links 31

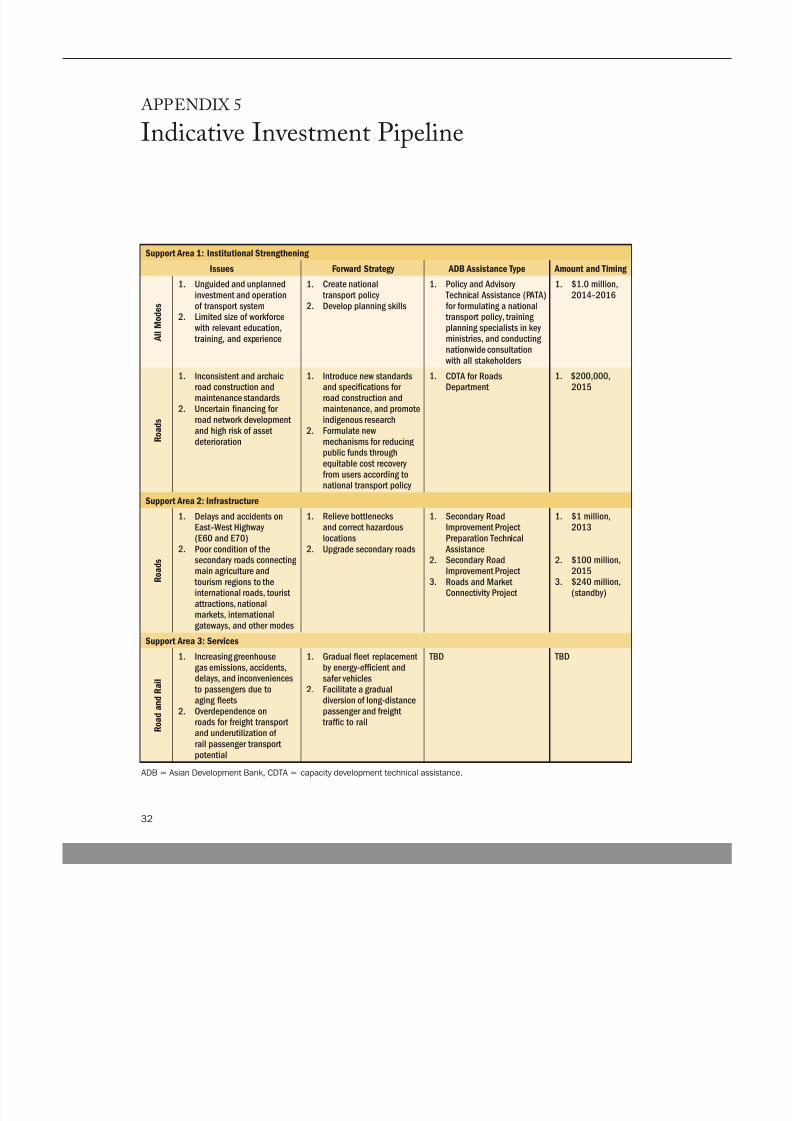

5. Indicative Investment Pipeline 32

References 33

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 5/48

iv

ables and Figures

Tables

1. ransport Sector Governance Framework 5

2. ransport Sector Strengths, Weaknesses, Opportunities, and Risks 22

Figures

1. System-Wide raffic Growth in Georgia, Year-to-Year Percentage to 2011 3

2. Skills, Experience, and raining Required of Ministry of Economy andSustainable Development Staff 6

3. Condition of International Roads in Georgia 9

4. Passengers and Freight Handled at Georgia’s Airports 16

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 6/48

v

Abbreviations

Currency Equivalents(as of 27 December 2013)

ADB – Asian Development Bank BP – British PetroleumEWH – East–West Highway GDP – gross domestic product JICA – Japan International Cooperation Agency km – kilometerL A – Land ransport Agency MCC – Millennium Challenge CorporationMESD – Ministry of Economy and Sustainable DevelopmentMRDI – Ministry of Regional Development and InfrastructureM A – Maritime ransport Agency teu – twenty-foot equivalent unit RACECA – ransport Corridor Europe–Caucasus–AsiaUS – United States

Currency Unit – lari (GEL)GEL1.00 = $0.577$1.00 = GEL1.732

In this publication, “$” refers to US dollars.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 7/48

vi

Acknowledgments

Tis report was initiated by Prianka Seneviratne, principal transport specialist, Central and West Asia Department (CWRD), Asian Development Bank, and by consultant Amal Kumarage.Klaus Gerhaeusser (director general, CWRD), Hong Wang (deputy director general, CWRD),and Kathie Julian (resident representative, Georgia Resident Mission) provided guidance andadvice. Xiaohong Yang (director, CWRD’s ransport and Communications Division [CW C])and Narendra Singru (senior transport specialist, CW C) supported the nalizing of the report.Staff members of the Ministry of Economy and Sustainable Development, Ministry of RegionalDevelopment and Infrastructure, and Georgian Railway; port operators; academics from theGeorgian echnical University; and ADB staff members provided information and suggestionsduring the preparation of this report. Muriel Ordoñez (operations communications specialist,CWRD), consultant James Unwin and his editorial team, and Nancy Bustamante (senior operationsassistant, CW C) helped publish the report.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 8/48

vii

Executive Summary

Tis sector assessment, strategy, and road map was prepared to guide the dialogue betweenthe Asian Development Bank (ADB) and theGovernment of Georgia on transport sectordevelopment and the country partnershipstrategy, 2014–2017. Urban transport is notcovered in this assessment, since it forms part ofthe urban sector development.

It reveals that Georgia, since 2005, hasrevised regulations and legislation on manyaspects of transport-related infrastructureand services to facilitate rapid developmentof its transport sector. Increased economicactivity, following these reforms, has led to

more intensive use of the sector, particularly forinternational links, and the sector’s contributionto gross domestic product has been growingabout 10% annually. All modes of internationaltransport (i.e., road, rail, air, water, andpipelines) indicate growth in demand, rangingfrom 5%–15% a year. However, improvementsin overall national mobility are not as visible

as in international sections of the network.In fact, rural bus services, passenger rail, andsecondary and local roads do not meet thedemand or expectations of the economy. Lackof transport options is considered a contributorto the high national unemployment rate, whichstood at 15.2% in 2011. Workforce limitationsare also hampering sector improvements, as lessthan 30% of key staff members in the Ministryof Economy and Sustainable Developmentand the Ministry of Regional Developmentand Infrastructure have the required practicalexperience and specialized education intransport.

Annual capital investment in all modesof transport reached $362 million in 2011,including $131 million of foreign directinvestment. Much of this has gone intoimproving Georgia’s international roads,following attempts to make Georgia’s transportsystem an integral part of the ransportCorridor Europe–Caucasus–Asia and the

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 9/48

viii

Executive Summary

Central Asia Regional Economic Cooperationcorridors and a regional logistics hub.

In its national plans, the government hasthree aims related to transport: (i) make Georgiaa regional and logistics hub, and businessplatform; (ii) upgrade multimodal infrastructure;and (iii) develop professional and highereducation centers. However, the capacity of themajor seaports on the west coast will remainconstrained until the rail and road capacitiesin the east–west corridor are increased. Accordingly, improvement of the East–WestHighway (EWH), which requires removingsome of the bottlenecks and introducing

advanced traffic management systems, remainsthe priority for public investment.

Placing EWH improvement at the topof the investment list is justied because it isthe fastest and shortest surface transport linkbetween the east and west of the country, andis important for the cohesiveness and securityof the country. It is also the only alternativeto the railway, which runs parallel in closeproximity, in the case of an emergency. Further,

inclusion of the north–south internationalroad improvements in the investment pipelineis rational because imminent resumptionof trade with the Russian Federation willrequire more road capacity. Te governmentis also proposing spending more to improvesecondary roads, because more than 70% ofthem are in poor condition, reducing freightand passenger transport services in some ruralareas, and resulting in high unemployment

and poverty. Lastly, improving maintenanceefficiency through new forms of procurementsuch as performance-based contract work, anddeveloping the transport-related workforce withmore knowledge and advanced skills, addressesthe need to increase sector productivity. Although this strategy addresses some criticaldeciencies of the sector, its ability to be

implemented is dependent on nancing, modalintegration and public transport, and thecreation of a cohesive national transport policy.

ADB has strongly supported Georgia’ssector priorities. It provided a $500 millionmultitranche nancing facility for improvingabout 200 kilometers (km) of secondary roadsand for building the Roads Department’scapacity to manage road assets and to improvesafety. Te rst and third tranches amountto about $260 million, which are currentlybeing used for project 1, constructing a new30 km two-lane road and upgrading 2 km ofa two-lane road to a four-lane road by passing

Kobuleti, a Black Sea resort. Tis road isscheduled to be operational in 2016.

Te European Bank for Reconstructionand Development, European Union,

Japan International Cooperation Agency,Millennium Challenge Corporation, and

World Bank have also assisted road networkdevelopment, especially the EWH. ADB

works closely with these development partnersthrough frequent meetings and information

exchanges. More coordination should occur,however, on general issues such as on jointneeds assessments, which can be extendedto avoid duplication, especially of capacitydevelopment initiatives.

ADB’s forward strategy for the sector willbe to continue supporting Georgia’s efforts todevelop an efficient, sustainable transport systemin line with its vision of making the nation aninternational gateway and to promote inclusive

growth. o this end, ADB plans to nanceimprovements to international and secondaryroads that can bring benets to the populationand businesses of Georgia. It will coordinate

with other development partners to speed upproject delivery and maximize impact. Further,to ensure inclusive growth, ADB plans toassist in linking the international roads to local

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 10/48

ix

Executive Summary

regional centers through selected secondaryroad improvements.

Given the urgent need for better directionfor the sector, particularly the need fornding sustainable, multimodal solutions,

ADB plans to provide technical assistancefor developing a national transport policy

and the transport planning capacity ofassociated government institutions. ADB alsointends to provide technical assistancefor modernizing technical standards andspecications in the roads subsector, and foraddressing critical gaps in implementing thesemodernized standards.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 11/48

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 12/48

1

Tis assessment, strategy, and road map wasprepared to guide the Asian Development Bank(ADB) in allocating and programming its

assistance1 to increase the efficiency of Georgia’stransport system in line with the country’spriorities, Strategy 2020 (ADB 2008b), andthe Sustainable ransport Initiative (ADB2010b). It addresses key international2 anddomestic passenger and freight transport issuesunder three broad categories—institutions,infrastructure, and services. It further servesto guide ADB’s continuing dialogue with thegovernment on transport sector development.

Te assessment used four approachesto gather information and involve sector

1 The country partnership strategy for Georgia, 2014–2017,is under development.

2 In this report, travel between the countries of theCaucasus is termed international travel. Travel within thecountry, including between provinces (which are commonlyknown in Georgia as regions), is termed domestic ornational travel.

Chapter 1Introduction

stakeholders in the preparation and validationof the strategy and road map. First, itundertook a detailed review of the literature

and an analysis of secondary data to determinetrends and Georgia’s comparative transportadvantages. Second, it consulted governmentagencies, particularly the Ministry of Economyand Sustainable Development (MESD) andthe Ministry of Regional Development andInfrastructure (MRDI), and private ownersand operators of transport infrastructure andservices to verify the feasibility of the strategy(Appendix 1). Tird, it invited educators and

multilateral and bilateral lenders to take partin discussions. Finally, it held consultative

workshops in June and September 2012 to reacha consensus with stakeholders; the initial focus

was on the assessment ndings and later on thestrategy and road map.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 13/48

2

Chapter 2Sector Assessment:Current Status and Strategic Issues

A. Sector Performance

Georgia’s transport system comprises

ve modes—road, rail, sea, air, and pipelines. All provinces, cities, towns, and neighboringcountries are connected either directly orindirectly by at least one of these modes. o improve these connections and to tapinto the benets of providing an efficientconduit for international travel and tradebetween Central Asia and Europe, successivegovernments in Georgia since 2005 haverevised rules and regulations on the supply

of transport infrastructure and services. Teyhave restructured institutions and delegated toline agencies the authority for modernizing thetransport system. Tis has helped draw privatecapital into aviation (airports and airlines),maritime services (ports and shipping), roadtransport (all freight and intercity passenger),and pipelines (oil and gas from Azerbaijan and

Kazakhstan). Te railway is now a state-ownedenterprise with the authority to raise capital inthe open market, leaving the road network as

the only physical asset owned and operated in atraditional, public-sector manner.

ransport system use has risen, mainlydue to the increased supply that followedreforms. otal freight movement up to 2011 wasgrowing at about 3.5% a year, while rail andbus passenger traffic was increasing at about1.5% a year. Railways currently carry about 40%of total freight. Since 2008, freight handledby ports has increased by about 10% a year,

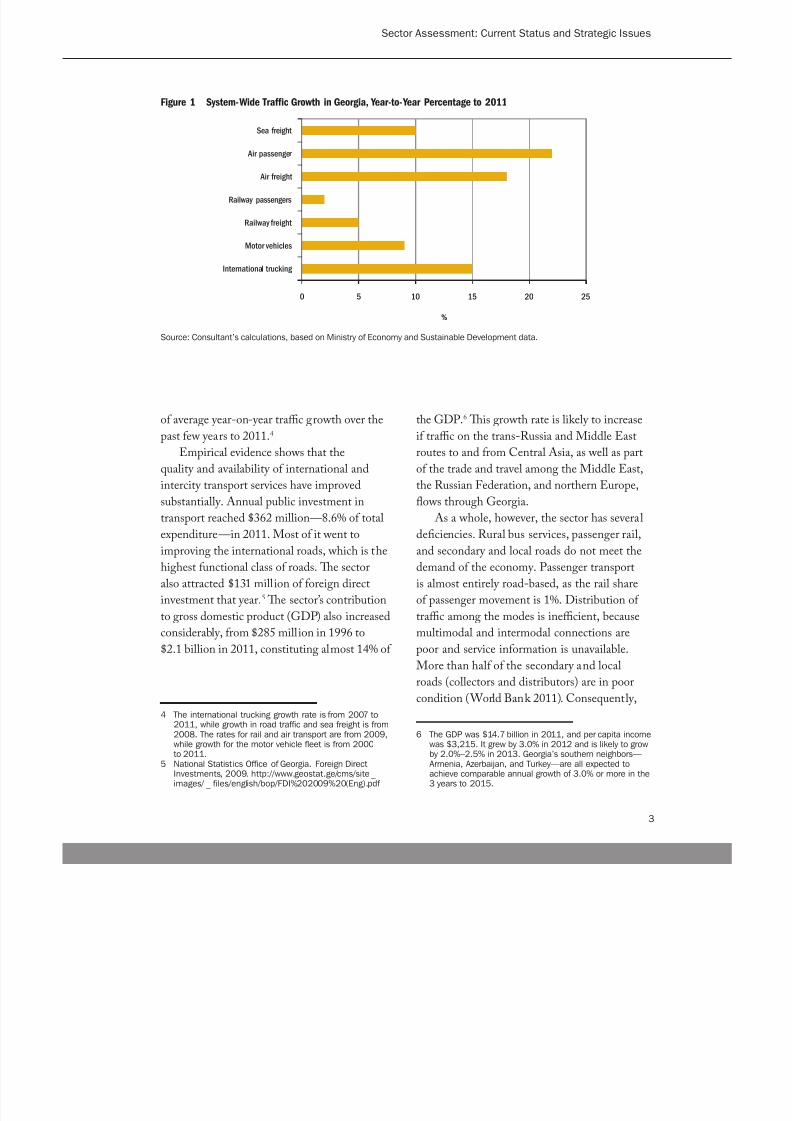

while traffic at the airports has grown by 15%.Cross-border truck movements grew at nearly15% a year, rising from 182,400 in 2007 to291,000 in 2011.3 Figure 1 provides a snapshot

3 Consultants’ calculations based on data provided by the Transport Policy Depar tment, MESD.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 14/48

3

Sector Assessment: Current Status and Strategic Issues

0 5 10 15 20 25

International trucking

Motor vehicles

Railway freight

Railway passengers

Air freight

Air passenger

Sea freight

%

Figure 1 System-Wide Traf c Growth in Georgia, Year-to-Year Percentage to 2011

Source: Consultant’s calculations, based on Ministry of Economy and Sustainable Development data.

of average year-on-year traffic growth over thepast few years to 2011.4

Empirical evidence shows that thequality and availability of international andintercity transport services have improved

substantially. Annual public investment intransport reached $362 million—8.6% of totalexpenditure—in 2011. Most of it went toimproving the international roads, which is thehighest functional class of roads. Te sectoralso attracted $131 million of foreign directinvestment that year.5 Te sector’s contributionto gross domestic product (GDP) also increasedconsiderably, from $285 million in 1996 to$2.1 billion in 2011, constituting almost 14% of

4 The international trucking growth rate is from 2007 to2011, while growth in road traffic and sea freight is from2008. The rates for rail and air transport are from 2009,while growth for the motor vehicle fleet is from 2000to 2011.

5 National Statist ics Office of Georgia. Foreign DirectInvestments, 2009. http://www.geostat.ge/cms/site _images/ _ files/english/bop/FDI%202009%20(Eng).pdf

the GDP. 6 Tis growth rate is likely to increaseif traffic on the trans-Russia and Middle Eastroutes to and from Central Asia, as well as partof the trade and travel among the Middle East,the Russian Federation, and northern Europe,

ows through Georgia. As a whole, however, the sector has several

deciencies. Rural bus services, passenger rail,and secondary and local roads do not meet thedemand of the economy. Passenger transportis almost entirely road-based, as the rail shareof passenger movement is 1%. Distribution oftraffic among the modes is inefficient, becausemultimodal and intermodal connections arepoor and service information is unavailable.

More than half of the secondary and localroads (collectors and distributors) are in poorcondition (World Bank 2011). Consequently,

6 The GDP was $14.7 billion in 2011, and per capita incomewas $3,215. It grew by 3.0% in 2012 and is likely to growby 2.0%–2.5% in 2013. Georgia’s southern neighbors—Armenia, Azerbaijan, and Turkey—are all expected toachieve comparable annual growth of 3.0% or more in the3 years to 2015.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 15/48

4

Georgia Transport Sector Assessment, Strategy, and Road Map

economic and social development has beengeographically skewed, and people andbusinesses in rural areas still lack access toreliable, affordable transport. wo-thirdsof rural households engage in agriculturalproduction for subsistence, which provides41% of their income, instead of trade outside ofthe community, partly due to lack of transport(JICA 2012 and USAID 2011a).

Lack of transport options is considereda contributor, in part, to the high nationalunemployment rate, which stood at 15.2%in 2011 (National Statistics Office of Georgia2013). Although about 47% of the value

addition in the sector is around the capitalcity, bilisi, the city actually has the highestunemployment rate in the country, at 29.2% in2011 (USAID 2011b). In fact, all of Georgia’scities have unemployment rates ve timesthose of depressed and isolated rural areasdue to outward migration of younger people(footnote 5). A Gini coefficient of 42 in 2011,compared with 37.1 in 1996, reects risingincome inequality.

ransport and logistics are 2 of 10 areasthat the government identied for improvementin its 2011–2015 plan to boost economic growth(Government of Georgia 2011b). Its goal wasto make these improvements by investingin high-quality transport infrastructure andtrade facilitation (European Commission 2010).It recognized that making the transport systeman integral part of the ransport CorridorEurope–Caucasus–Asia ( RACECA)7 and the

7 Georgia is located along an important international andregional corridor, TRACECA, and is well placed to absorbgrowing transport demands. The TRACECA corridorthrough Georgia is the shortest route between Europeand Azerbaijan, Armenia, and the Central Asian Republicsthrough its Black Sea ports. TRACECA is envisaged as analternative to both the northern corridor running throughthe Russian Federation and Belarus and the southerncorridor running through Iran and Turkey. Due to itsintermodal nature, TRACECA would only be competitivewhen connected and operated efficiently to reduce traveltime and costs.

Central Asia Regional Economic Cooperationcorridors (ADB 2012) is vital for sustaininginvestments in other thrust areas; thus, it signed22 bilateral agreements on freight and passengertravel. Te new administration, while retainingthe 2011 plan, hopes to also focus on improvinginternational roads extending from the north tothe south, as well as secondary roads connectingregional centers to international roads.Initiatives such as performance-based roadmaintenance and traffic and safety management

will be implemented with more vigor.

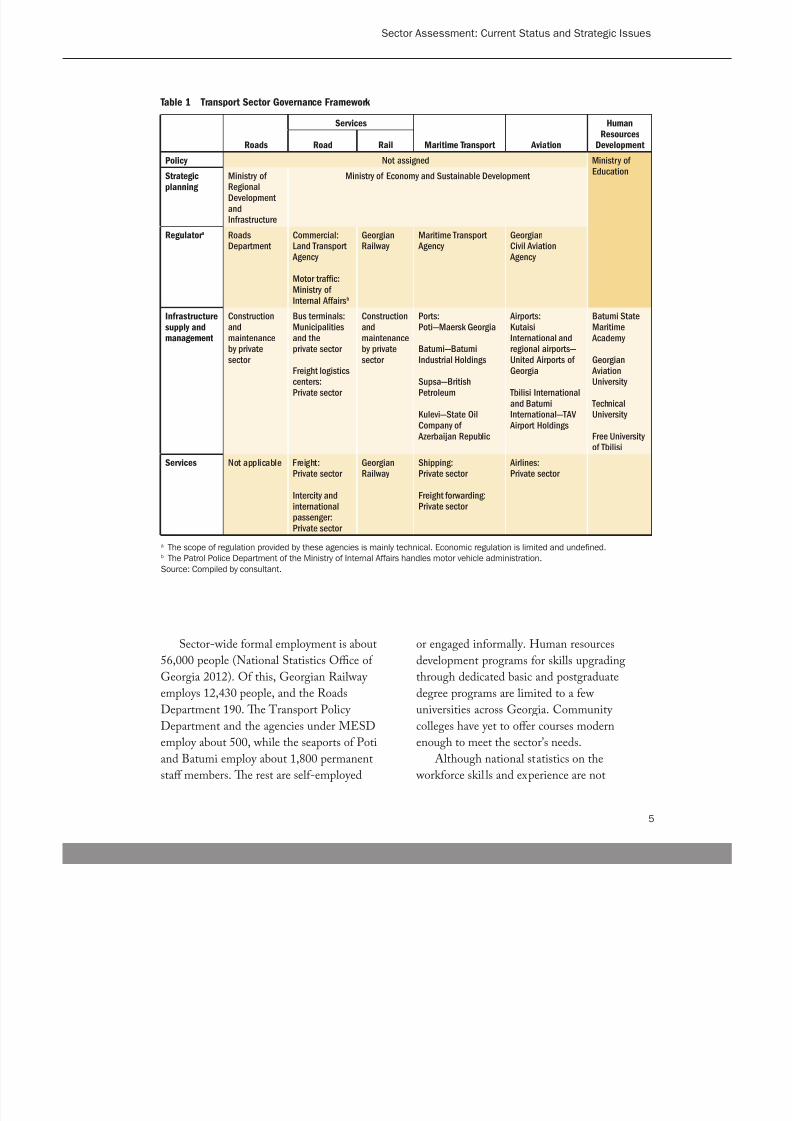

B. Strategic Issues1. Sector Governance

MESD has jurisdiction over road transport,maritime transport, railways, and aviationinfrastructure and services, with its ransportPolicy Department serving as the coordinatingbody. Te Roads Department of MRDIbuilds and operates roads classied asinternational and secondary. Local authorities

are responsible for the other roads in thenetwork, which are classied as local roads. Te Land ransport Agency (L A), Maritime ransport Agency (M A), and Georgian Civil Aviation Agency are the technical regulators.Georgian Railway is state-owned. Privatecompanies operate all the country’s ports andtwo major airports, while the state-ownedUnited Airports of Georgia operates thenewest international airport in Kutaisi, and allregional airports. Te Georgia Civil Aviation

Agency oversees safety in this sector, anddevelops regulations and procedures. Pipelineregulation rests with the Georgian Oil and GasCorporation, another joint stock company ofthe government. able 1 summarizes the sectororganizational structure.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 16/48

5

Sector Assessment: Current Status and Strategic Issues

Table 1 Transport Sector Governance Framework

Roads

Services

Maritime Transport Aviation

HumanResources

DevelopmentRoad Rail

Policy Not assigned Ministry ofEducationStrategic

planning Ministry ofRegionalDevelopmentandInfrastructure

Ministry of Economy and Sustainable Development

Regulator a RoadsDepartment

Commercial:Land Transport

Agency

Motor traf c:Ministry ofInternal Affairs b

GeorgianRailway

Maritime Transport Agency

GeorgianCivil Aviation

Agency

Infrastructuresupply andmanagement

Constructionandmaintenanceby privatesector

Bus terminals:Municipalitiesand theprivate sector

Freight logisticscenters:Private sector

Constructionandmaintenanceby privatesector

Ports:Poti—Maersk Georgia

Batumi—BatumiIndustrial Holdings

Supsa—BritishPetroleum

Kulevi—State OilCompany of

Azerbaijan Republic

Airports:KutaisiInternational andregional airports—United Airports ofGeorgia

Tbilisi Internationaland BatumiInternational—TAV

Airport Holdings

Batumi StateMaritime

Academy

Georgian AviationUniversity

TechnicalUniversity

Free Universityof Tbilisi

Services Not applicable Freight:Private sector

Intercity andinternationalpassenger:Private sector

GeorgianRailway

Shipping:Private sector

Freight forwarding:Private sector

Airlines:Private sector

a The scope of regulation provided by these agencies is mainly technical. Economic regulation is limited and undefined.b The Patrol Police Department of the Ministry of Internal Affairs handles motor vehicle administration.Source: Compiled by consultant.

Sector-wide formal employment is about56,000 people (National Statistics Office ofGeorgia 2012). Of this, Georgian Railwayemploys 12,430 people, and the RoadsDepartment 190. Te ransport PolicyDepartment and the agencies under MESDemploy about 500, while the seaports of Potiand Batumi employ about 1,800 permanentstaff members. Te rest are self-employed

or engaged informally. Human resourcesdevelopment programs for skills upgradingthrough dedicated basic and postgraduatedegree programs are limited to a fewuniversities across Georgia. Communitycolleges have yet to offer courses modernenough to meet the sector’s needs.

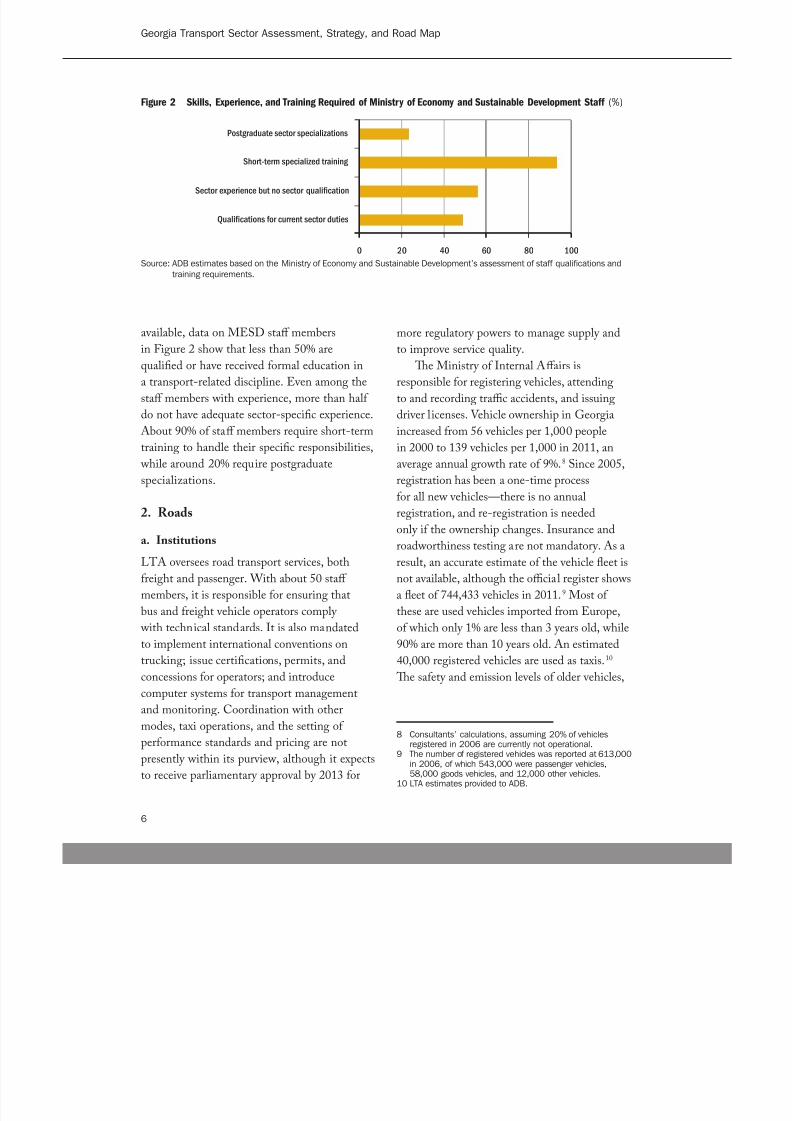

Although national statistics on the workforce skil ls and experience are not

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 17/48

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 18/48

7

Sector Assessment: Current Status and Strategic Issues

particularly buses and trucks, are among thecurrent concerns of MESD.

Te Roads Department is responsiblefor planning, designing, constructing, andmaintaining secondary and internationalroads. It has a large portfolio of projects inthe preconstruction and construction stages(ADB 2009c). Most of its work, except someplanning and programming work, is outsourcedto national and international private companies.It has evolved into a contract administrator andmanager of the network, but lacks sufficientexpertise and personnel to deliver projectsefficiently. Such capacity gaps are being plugged

using consultants in parallel to continuedcapacity building within the department.

Local authorities oversee the roads in cities,towns, and villages. In addition to havinginsufficient technical staff, these authoritieslack a formal organizational arrangement andconsistent funding for maintaining existingassets in good condition.

b. Services

i. Intercity Buses

Regulatory reforms in 2005 and 2006, whichremoved market-entry requirements for privateoperators, have increased the supply of intercitybus services. Tese vehicles are operatedmostly by owner–drivers, and according toinformal schedules and tariffs. An estimated25,000 buses andmarshtukas (minibuses) nowprovide services on 450 urban and 650 intercity

routes. Services on the 36 international routesare provided by 82 operators, mostly foreigncompanies (Government of Georgia, L A).On both intercity and international routes,passengers have few choices in terms of speed,frequency, and comfort of service.

Fares and schedules, except on servicesbetween the main bus stations (e.g., bilisi and

Batumi), are neither managed nor published.On a regular service, the fare is GEL20.Corporate operators and standard proceduresfor managing bus routes have not been putin place, and bus stations are poorly designedand lack convenient access and intermodalintegration. Te municipalities own andoperate bus stations in the main cities andtowns, and charge a portion of the fare forstation use and route capacity control, limitingthe operating frequencies and number ofoperators (Ade ransport 2012). axis also offercompeting intercity services on a shared basisfrom the same terminals.

Despite the relative increase in services,rural communities and small towns areinadequately served, and there is neithera policy on public service obligations norminimum service requirements. Safety andenvironmental standards are not monitored,and penalties for noncompliance are unclearand inconsistently applied. Te lack of suchpolicies and rules and the spread of informalpractices have hindered development of

new services (ADB 2009d). L A specialistsbelieve that high costs and limited nancingare preventing owners from upgrading their

vehicles and eets. Inadequate nancial supportalso partly explains why foreign operatorsdominate international routes. L A, withbilateral assistance from the Government ofFrance, initiated a study in 2012 to examine theproblems of public transport in Georgia.

ii. Freight Services

Georgia has simplied procedures at its bordersand eliminated almost all causes of delay andcorruption for trucks entering and leaving thecountry. In 2011, L A issued permits accordingto bilateral agreements governing cross-bordertruck movements to 102 freight service providers,

who collectively owned 40,000 trucks. Tese

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 19/48

8

Georgia Transport Sector Assessment, Strategy, and Road Map

providers are mostly foreign companies—the largest being Mediterranean ShippingCompany—which made 183,000 crossings toand from Georgia during 2011, according toL A. A GEL200 toll is levied on foreign trucks with containers transiting the country. Tistoll appears to be based on an agreed protocolbetween Georgia and Azerbaijan in October2005 to charge $0.28 per container kilometer(Ziyadov n.d.). Georgia’s neighbors do not levyany charges, but the cost and delay at the bordersoffset this savings to truckers.

Secondary data on national freightoperations—such as eet size, vehicle types,

and tariffs—are not available. According tonational logistics academics, most nationalfreight operators are individual truckers whoseservices are completely unregulated and marketentry unhindered. Te services are poor andfragmented, and, like the buses, customershave no formal sources of information on theiravailability and cost. An ADB study (2009d)found competition to be intense, with rates ofGEL0.20–GEL0.27 per ton-kilometer

(ton-km) charged for hauls of 100–500 km.

c. Infrastructure

i. Physical Network and Performance

Te road network is about 22,000 km, and roaddensity, at 318 km per 1,000 km2, is higher thanthat of Armenia (279 km per 1,000 km2) and Azerbaijan (223 km). Roads are functionallyclassied as international, secondary(interprovincial), and local (municipal). As previously stated, the Roads Departmentmanages international and secondary roads(6,835 km), and district administrations andcities manage local roads (around 15,000 km).11

11 In 2007, the Roads Department transferred local roadsto 69 local governments as part of broader public sectorreform aimed at decentralizing government functions.

Five international roads totaling 859 kmare used mainly by transit traffic. About 95 kmof those are four-lane, and the rest, includingthe secondary and local roads, are two-lane.12

wo of these ve roads, the E60 and E70of the European network, form Georgia’sEast–West Highway (EWH)—part of theEurope–Asia corridor through the Caucasus.

Tey run north from the urkey border at Sarpi,serving the Black Sea ports of Batumi andPoti, then east past Kutaisi (Georgia’s second-largest city) to bilisi, and then southeast to theborder with Azerbaijan at Red Bridge, a totaldistance of more than 400 km. Te other three

international roads run south from bilisi tothe Armenia border at Sadakhlo, Guguti, andnear Ninotsminda. Georgia is a signatory to anumber of international transport agreementsfor the continued development of an integratedroad transport network that not only facilitatescross-border transit traffic but also contributes toregional cooperation and integration.

Te E60 carries more than 60% of theinternational freight moved by roads.13 otal

traffic on this road is increasing at around10% a year, in part due to road improvements,streamlined border-crossing procedures, andharmonized standards and documents. Averagedaily traffic on its Rikoti and Samtredia sectionsincreased to 9,000–10,700 vehicles by 2011,from 5,900–7,000 vehicles in 2007. Even thoughthe feasibility study of rehabilitation optionsfor these sections in 2008 forecast 17,000–20,000 vehicles a day by 2030, the currentgrowth rate suggests that that volume oftraffic will be reached by 2018 (JBIC 2012).

As such, continuing highway investment forraising the capacity will become expensive

12 The typical geometry of these roads, classified as Class 2and 3, is 3.5-meter travel lanes and at least 1.0 meter ofpaved shoulders.

13 This is equal to an estimated 6.4 million tons transitingthis highway (World Bank 2011).

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 20/48

9

Sector Assessment: Current Status and Strategic Issues

Figure 3 Condition of International Roads in Georgia

Source: Government of Georgia, Roads Department (2011).

2004

2009

Y e a r

%

2010

2011

GoodSatisfactory Damaged or bad

0 908070605040302010

and unsustainable unless policy interventionsmanage demand.

Te length of international roads in goodcondition increased to 84% in 2011 from 34%in 2004 (Figure 3). A road asset managementsystem is expected to be operational in 2013,

which will help plan and program maintenanceand rehabilitation works, enable the selectionof cost-effective design standards, andprovide condition and travel time data bothfor road users and for project monitoring andevaluation (World Bank 2011). As of now,about 1,100 km of international and secondaryroads (Appendix 2) have been programmed forimprovement. Te World Bank is supportinga program of multiyear, performance-basedcontracts for maintaining secondary roads, andthe lessons from these contracts will be usedto extend the concept over the entire network.However, it concluded that annual expenditureon maintenance is too low to keep the entirenetwork in good condition (ADB 2009d).

In addition to inadequate maintenance,the poor condition of roads is attributed to

overburdened foreign trucks (ADB 2009d). Tis occurs despite national regulationsthat conform to Europe-wide limits,14 andsurveillance through permanent weighbridgesat the border crossings and seven mobile bridgesoperated by the police. Offenders are ned a at

fee of GEL500. Te pavement damage causedby a typical multi-axle truck is about $0.50per km (based on United States [US] rates).

Accordingly, a truck crossing Georgia, travelingabout 400 km, will cause $200 of damage pertrip, meaning that the current $120 toll coversonly 60% of the damage caused.

Further, construction and maintenancecost more in Georgia than in its neighbors.For example, in 2010, the tender price fortopsoil removal was 17% higher than the

Azerbaijan price. ack coating was 46% moreexpensive than in Azerbaijan, and prime coating

was 250% more expensive (yet only half the cost

14 The upper loading limit for each nondrive axle is 10.0 tons,and 11.5 tons for each drive axle; the total limit is 44.0tons for articulated, multi-axle vehicles.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 21/48

10

Georgia Transport Sector Assessment, Strategy, and Road Map

of the material in Armenia).15 However, someitems were substantially cheaper. For instance,crushed-stone base course material was 6 timesmore expensive in Azerbaijan and 18 times morein Armenia. Yet overall, costs in Georgia arehigher due to cost-insensitive design standardsand specications. For example, the volumespecied for reinforcement steel in concrete boxculverts on high-volume highways in Georgia isabout 30% higher than in the US.

Te 2010 revisions to national standardsand specications have not included anymodern measures to address climate change,the environment, or sustainability issues,

except for seismic considerations. Tere are nospecications for warm-mix asphalt, which cansave energy, reduce the carbon footprint, andlast a long time.

ii. Financing

Road construction and maintenance arenanced from government revenue and donorfunds. Te share of public expenditure on roadsincreased from about 37% in 2009 to 47% in

2011. Te share of GDP spent on maintenanceand rehabilitation in 2010 increased to2.4%, amounting to about $265 million(World Bank 2011). About 75% of this hasbeen nanced through ADB, the EuropeanUnion, Millennium Challenge Corporation(MCC), and World Bank. ADB’s contributionsince 2009 has been through a $500 millionmultitranche nancing facility for improving thehighways that connect Georgia to its neighbors

and institutional capacity building (Governmentof Georgia 2011b).16 A road fund, nanced fromtaxes on fuel, transit tolls, and a road-use levyon individuals and enterprises, was reportedly

15 ADB estimates, which are based on only one bid in eachcountry in 2010.

16 Includes one loan of $150 million, which was canceledafter signing.

liquidated in 2005 after 10 years in existence(World Bank 2011).

Different sources have provided estimatesof the investment needed to modernize andmaintain Georgia’s road network. ADB’s2009 estimate was $3 billion (Governmentof Georgia 2011b).17 Te 20-year investmentneeds assessment of the World Bank in 2012puts the gure at about $3.4 billion, $2.0 billionfor clearing the backlog of maintenance over10 years, $450 million for routine and periodicmaintenance in the subsequent 10 years(World Bank 2011), and $1.0 billion formodernizing the remaining parts of the EWH,

along with the rehabilitation of secondaryroads (Government of Georgia, L A).18 Tegovernment intends to raise the needed fundsfrom its development partners, but lacks aformal project assessment process and a rminvestment plan, aside from the one mentionedin Appendix 3 (United Nations and WorldBank 2010). Consultant support is used for duediligence at project appraisal.

Recovery of part of the investment costs

from users remains an unexplored optionto supplement budgetary allocations andborrowings. Despite differences in the numberof foreign transit trucks on the road networkreported by various government agencies,if taken as 150,000 trucks per year, about$18 million can be recovered from the currenttransit fee of $120 per truck. Tis fee could beincreased to recover a larger share of the cost.Moreover, current legislation that precludes

the levying of charges on roads where there areno alternative routes can be adjusted to allowtime-of-day-based charges, for example, and can

17 Comprised $1.851 million for the EWH, $594 million forother international roads, and $500 million for secondaryand local roads.

18 In 2007, the Roads Department transferred local roads to69 local governments as part of a broader public sectorreform aimed at decentralizing government functions.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 22/48

11

Sector Assessment: Current Status and Strategic Issues

be used for managing demand on the EWH.Risk-based design, procurement, construction,and maintenance principles are another optionfor reducing costs.

3. Railways

a. Institutions

Georgian Railway’s core business is trainoperations, and it has three subsidiariesspecializing in container handling, construction,and property management. MESD, whichserves as its supervisory body, appoints a chiefexecutive officer, three executive directors,and a board of directors to oversee operations.Operations are divided into three strategicbusiness units: freight, passenger, andinfrastructure. Each unit is a separate protcenter under an executive director reportingto the chief executive and is responsible to theboard of directors. Te freight and passengerunits make an internal ledger payment to theinfrastructure unit for track use. Te freightunit, being the only unit that is protable, pays

taxes and dividends to the government. Te freight unit earned over $286 million

in 2011 (RZD Information Agency 2012).In addition to nonsovereign bilateral andmultilateral bank loans, the company raisedfunds through a $500 million bond issue in

June 2012. Georgian Railway went for an initialpublic offering (IPO) to sell 25% of its shares in2012 but the IPO was not completed. Althoughit intends to complete it in the near future,

there is no denite timeline for completion. Te IPO had been expected to raise around$250 million for developing the internationalfreight operations (Antidze 2012). However,there is no clear, stated vision and strategy toalign development with the national transportstrategy or integration with other modes.

b. Infrastructure

Of the 1,326 km rail network, 293 km is doubletrack and 1,251 km is electried (GeorgianRailway 2012). About 80% of the network isin mountainous terrain, and segments of themain line traverse narrow gorges, where anyexpansion will be costly and slow. Most of thenetwork is designed for an axle load of 23 tons

with speeds of 100 km per hour for passengertrains and 80 km per hour for freight trains.Most tunnels and bridges are 100 or more yearsold. Te rail eet, composed of 171 electric and134 diesel locomotives, and the rolling stock ofaround 7,000 must also be modernized.19

Te track between the Azerbaijan borderand Poti, a mostly double-track electriedline of 385 route-km, and a mostly single-track electried line of 104 route-km betweenSamtredia and Batumi, carries oil for export—most of rail freight traffic. However, theoperating speed on the east–west corridor isonly 33 km per hour. Improvements are eitherunder way or planned to increase speed andconnectivity. One is the reestablishment of the

bilisi–Kars line, connecting Azerbaijan and urkey through bilisi, for which Azerbaijanhas provided Georgia with a $220 millionloan. Besides rehablitaiton of the existing line,the project intends to add 27 km to Georgia’snetwork. Its opening is slated for 2015, initiallycarrying about 1.2 million people and 3.5 milliontons of cargo annually. It will enable increasedtrade between urkey and eastern countries.

Other investments include upgrading and

rehabilitating track and rolling stock. Tis will permit operating speeds to increase to100 km per hour, especially on the line between

bilisi and Batumi. Construction of a 68 kmnew line—including 6 km of double track and8 km of single track that pass through tunnels

19 Based on ADB discussions with Georgian Railway officials.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 23/48

12

Georgia Transport Sector Assessment, Strategy, and Road Map

in the mountainous section from Khashurito Zestafoni, which is a major bottleneckon the bilisi–Batumi line—is scheduledto be completed by 2016. Te travel timeafter reconstruction and the introduction ofnew rolling stock is expected to fall to about3.50 hours from the current 4.75 hours. Freightcapacity is estimated to increase to 45 milliontons per year by 2016. However, activities havebeen temporarily halted on an earlier plan for acentral bilisi bypass, nanced by the EuropeanBank for Reconstruction and Development(Georgian Railway 2012).

c. Services Te railway carried 20.1 million tons of freight in2012. Out of the total revenue of approximately$284.5 million, freight contributed 95%, of which half came from transporting oil fromKazakhstan and Azerbaijan to Georgia portson the Black Sea. Freight traffic has grown atabout 5% since 2009, despite a slight drop in2012, and passenger traffic at about 2% per year,but rail transport is still losing market share to

road transport. Te net operating prot in 2012dropped by nearly 80% due to a bond buybackand depreciation of the lari against the mainforeign currencies.

About 37,000 twenty-foot equivalentunit (teu) containers were transported by railalong the east–west corridor in 2011, compared with an estimated 150,000 by road.20 Doubletracking from Samtredia to Poti and Batumi—in addition to the rehabilitation of the othersections—will benet both modes and helpchange these shares. Te level of service on theEWH will be sustained when more dry cargoshifts from road to rail, and rail’s revenue willincrease, while costs to the environment will fallas greenhouse gas emissions decline.

20 Based on truck movement data provided by MESD,assuming 1.5 teu per truck and 80% containers.

Private industries strongly support thedevelopment of railway freight capacity sincecost, if not for the delay, is considered tobe half that of trucking for certain cargoes.Moreover, sufficient non-oil freight is expectedto ow to and from Central Asia to sustainthe investments. Several railways, seaports,and cargo companies are implementing the“Viking Plan,” a joint operation to transportcontainers by rail from Europe through Latvia,Belarus, and Ukraine across the Black Seato Georgia and Central Asia. Te simpliedcustoms formalities allow a container train totravel 1,734 km in just 52 hours. Te traffic

using this service has increased 50% since itstarted in 2010 (Pavilenene 2011). However,the railways do not have major contracts forfreight movement with logistics providerssuch as the Poti Industrial Free Port or the

bilisi Logistics Center.Passenger traffic in 2011 was 3.3 million,

of which only 3% were tourists. Internationalpassenger services are limited to overnight trainsfrom bilisi to Baku (daily; about 15 hours)

and Yerevan (every other day; about 12 hours),operated by Azerbaijan (Azerbaijan Railways)and Armenia railways (South Caucasus Railway).

Te current one-way fares from Yerevan to bilisi are $18–$36, and from Baku to bilisi,$35–$70, depending on the class of service.Daily domestic services are available from bilisito most regional capitals. Te overnight sleeperfrom Batumi to bilisi has air-conditionedrst- and second-class compartments and takes

8 hours, while the day train takes 4 hours and45 minutes.21 Te current one-way fare on theovernight sleeper is about $25 for a shared cabin.Most regional and commuter services, which link

21 Georgian Railway. http://www.railway.ge; Lonely Planet2013; and Railway Transport. Transport to/from Russia,Uzbekistan, Kazakhstan, CIS, SNG, and Mongolia. http:// www.railwaytransport.eu/?gclid=CPrXk9mB0bACFUZd3wod807CXg

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 24/48

13

Sector Assessment: Current Status and Strategic Issues

provincial and rural areas to several main cities,operate mostly once a day. Tere is no publicservice obligation to the government or specictargets to develop passenger services, althoughthe cost of operations is met by freight servicesurpluses. However, the fares are competitive

with road transport, except in regional services, which are priced below bus fares as a publicservice obligation.

4. Maritime Transport

a. Institutions

M A was established in April 2011 with a

mandate to create a sustainable maritime systemin Georgia. Its immediate tasks are to buildindustry capacity, intensify cooperation withinternational maritime authorities, enable theBatumi State Maritime Academy to regainauthority to issue certicates of competency forseafarers, and help the Georgian shipping eetobtain technical certicates for internationaloperations. Te loss of competency certicationrights and vessel operating licenses has reduced

the eet size to only 6 in 2012 from 375 in 2006,and caused 3,700 seafarers to lose their jobs. Te Batumi State Maritime Academy,

formed in 1921, is now a state-ownedenterprise. It can produce up to 250 seafarersper year, including engineers and technicians.

Te academy is negotiating with a privateeducation provider to offer a wider program andis preparing to satisfy audit requirements setby the International Maritime Organization.

It expects this joint venture to increase studentenrollment from 1,400 to 4,000, attracting 500foreign students. It is also preparing for an auditfor recertication of its courses.

b. Infrastructure

About 22 million tons, including 300,000 teu, were handled by the four ports in 2011: Poti,

7.2 million tons; Batumi, 6.8 million tons;Kulevi, 3.4 million tons; and Supsa, 4.0 milliontons. Tis amounted to about 340 vessels amonth on average. State earnings from portoperations are not published, but the operators’nancial reports show prots before taxes.

Te Port of Batumi’s 2011 revenue was about$30 million. Pre-tax annual prot has remainedat about $8 million since 2009. Te four portsprovide direct and indirect employment to about30,000 people.

i. Port of Poti

Te Port of Poti is operated by APM erminals,

a subsidiary of Maersk Shipping of Denmark, which in 2011 paid the RAK Investment Authority of the United Arab Emirates$300 million for an 80% stake in the port.

Te RAK Investment Authority purchased theport from the government in 2009 and investedin port infrastructure and the adjacent PotiIndustrial Free Zone.

Te port spans 30 hectares and consists of14 berths extending over 2.9 km. Container

cargo constitutes 27% of the volume handled, while bulk cargo (36%), liquid cargo (16%),break bulk (10%), and roll-on and roll-off traffic(11%) make up the rest. About 46% of the cargois transit traffic, while imports make up 37%and exports 17%. otal cargo handled grew at10% a year from 2009 to 2011, and the numberof containers handled increased 47% from172,000 teu to 254,000 teu. Te port’s currentcontainer handling capacity is estimated at

450,000 teu. APM erminals plans to invest$100 million over 5 years in expansion andmodernization of the port. Tis may addressthe 13-meter approach channel draft limitation,

which restricts ship size. However, road andrail capacity remains a concern. Only about30% of containers are moved by rail, which has

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 25/48

14

Georgia Transport Sector Assessment, Strategy, and Road Map

a direct spur from the main line to the berthsand Poti Free Industrial Zone. Tis strengthensthe need for better planning and coordinationamong the modes to maximize the return on theinvestments.

ii. Port of Batumi

Te Port of Batumi is owned and operatedby Batumi Industrial Holdings, a subsidiaryof Kaz ransOil of Kazakhstan, under a 49- year agreement signed with the governmentin 2008. Te port has ve separate berthsfor oil, containers, rail ferry, dry cargo, andpassengers, and a conventional buoy mooring

for larger vessels with a depth of 13.6 meters. Te capacities of the oil and dry cargo berthsare 15.0 million tons and 2.1 million tons,respectively. Te two container berths have acombined capacity of 300,000 teu per year,but their drafts are only 11.7 meters. Te ferryberth can accept 108 eight-wheel rail wagons,is completely automated, and can handle about0.7 million tons of cargo per year.

Te agreement requires the port to handle

6.0 million tons of cargo every year. It handled5.3 million tons of oil, 1.5 million tons of bulkdry cargo, and 45,442 teu in 2011. However,Batumi Industrial Holdings has now leased twocontainer berths and one ferry berth to BatumiInternational Container erminals, a subsidiaryof Manila-based International ContainerServices. Te oil berths have been leased toBatumi Oil erminals until 2019.

Te total area of the port is 13.6 hectares, of

which only 3.6 hectares have been developed. Terefore, the port has space for furtherexpansion, although the immediate need is forimproving handling equipment and berths. A new container yard of 15 hectares with newrail and road access is expected to be completedin 2013. Tis will increase container berthcapacity to 400,000 teu. However, the port is in

the heart of Batumi, which is being promotedfor tourism. Batumi Industrial Holdings isnegotiating to transfer the passenger ferryoperations to the city of Batumi in exchangefor other land for the port. Regardless, accessis a constraint. Without a grade-separatedinterchange at the port entrance, conictsbetween port access and through traffic willincrease as the port expands. As is the case forPoti, the port’s capacity will remain constraineduntil the rail and road capacities in the east–westcorridor are increased.

iii. Port of Supsa

Te Port of Supsa is an offshore oil terminal,owned and operated by British Petroleum(BP). Opened in 1999, Supsa is the terminusof the 833 km Baku– bilisi–Supsa pipeline,also known as the Western Route ExportPipeline or the Western Early Oil Pipeline,from BP’s Sangachal terminal south of Baku.

Te International Finance Corporationinvested $30 million in the Georgia portionof the pipeline in 1998. BP has since invested

more than $5 billion to develop other majoroil and gas pipelines that cross Georgia: theBaku– bilisi–Ceyhan pipeline, with a capacityof 1 million barrels of oil per day; SouthCaucasus Pipeline, carrying 650 million cubicmeters of gas per day; and the Western Exportpipeline from Baku to Supsa (Government ofGeorgia, Ministry of Economy and SustainableDevelopment 2007).

iv. Port of Kulevi

Tis port, constructed in 2000, is an oil-exporting terminal owned and operated bya consortium comprising the State EnergyCompany of Azerbaijan Republic (51%),Middle East Petroleum (34%), and variousGeorgian investors (15%). Te port has twoberths (13.6 meters and 6.13 meters deep),

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 26/48

15

Sector Assessment: Current Status and Strategic Issues

which can accommodate 100,000-ton and40,000-ton vessels. A buoy mooring located4 km offshore with a draft of 17.1 meters canaccommodate vessels of 100,000–120,000 tons(World Bank 2008a). A 10 km spur connectsthe port to the main east–west railway. Teport handled 3.3 million tons of crude oil andrened products in 2011. Its total capacity is10 million tons of oil per year—transportedfrom Azerbaijan by rail—and the terminal canaccommodate up to 168 railway tank cars.

c. Services

Shipping services are provided by a few

foreign companies. Te largest operator is theMediterranean Shipping Company, whichprovides global transshipment and relay servicesmainly through Istanbul. Scheduled passengerservices operate, several of them directly,from Batumi and Poti to Bulgaria, Romania,

urkey, and Ukraine ( akaishvili 2012). Whilethe Batumi passenger terminal capacity isabout 180,000 passengers a year, only 21,520passengers used it in 2011. Te government

signed a memorandum of understanding inNovember 2011 with Royal Caribbean CruiseLines for reconstruction of the passengerterminal, allowing it to host large cruise ships(containing 3,000–5,000 passengers) by 2014.22

Tis will signicantly increase cruise touristthroughput, which was only 2,900 in 2011.23 Some companies also offer limited roll-on androll-off services to Romania, largely for used-

vehicle imports from Europe.

22 Autonomous Republic of Ajara, Ministry of Finance andEconomy. Batumi Invest. http://www.investinbatumi.ge

23 Commersant. http://www.commersant.ge

5. Aviation

a. Institutional

Te Georgian Civil Aviation Agency isresponsible for certifying and licensing aircraftsand airline crew members, and ensuring thataircraft, aviation services, and airports conformto international and European standards.

Te agency’s 56 staff members are alsoresponsible for ensuring the supply of skilled

workers for all aspects of aviation. Georgia hasentered into 16 bilateral air service agreementsand adopted the Open Skies policy with11 European Union countries since 2010. In

2013, Georgia became the 40th member of theEuropean Organisation for the Safety of AirNavigation.

SAKAERONAVIGA SIA, a limitedliability company, has been responsible formanaging Georgia’s airspace since 1999.It monitors and provides aviation servicesand ight safety in the takeoff and landingzones of international airports in Batumi,Kutaisi, Mestia, and bilisi. Most aircraft and

avionics maintenance works are performed byinternational companies. Georgian AviationUniversity, a nationally accredited institution,awards undergraduate and graduate degreesin aviation engineering and management, as

well as associate degrees and certicates intechnical and administrative subjects. Afterbeing part of the rst institute of highereducation in the Caucasus region that wasestablished in 1917, the university is aspiring

to become the region’s center of excellencein aviation after it was granted autonomousstatus in 2005. Te opportunities for acquiringtechnician-level accreditation, however, arelimited, and this may impact the aviationindustry’s growth in the long term.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 27/48

16

Georgia Transport Sector Assessment, Strategy, and Road Map

b. Infrastructure

United Airports of Georgia, a state-ownedenterprise in operation since April 2011, ownsall airports in Georgia. Operations of twointernational airports are outsourced. AV

Airports Holdings, a urkish partnership, wasawarded a concession for operating the bilisiand Batumi airports starting in October 2005. Te initial agreement was for AV to design,nance, construct, maintain, and operatethe landside facilities, and provide ground-handling services, customs and noncustomsstores, and catering services at the two airportsfor 11.5 years. AV built a new terminal andimproved the runway, which opened in February

2007. Operations in the Batumi airport startedin May 2007.24 Te concession period has beenextended twice since 2005, and the currentconcession extends up to November 2037.

Te airport in bilisi can handle up to2.8 million passengers and 160,000 tons of

24 Government of Georgia, Georgian National InvestmentAgency. http://www.investingeorgia.org

freight per year. It has two parallel runways,one of which is an International Civil AviationOrganization Code E runway. Several airlinesoffer scheduled services to bilisi from Europe,the Middle East, and Central Asia. Flights are

also available from bilisi to Batumi, Kutaisi,and Mestia. Because it has both road and railaccess, bilisi is also well positioned to serve thetourism industry with minor improvements tofacilitate air–road–rail transfers. Te airport inBatumi can handle 600,000 passengers a year.It has one Code E runway, and is served bymostly scheduled regional carriers and urkish

Airlines. Batumi also serves as an internationalgateway to border towns in urkey. For example,

passengers on Pegasus Airlines can purchase aticket to Batumi from 56 destinations with landtransport to Hopa in urkey.

Since the improvements were completed at bilisi and Batumi, annual passenger traffichas almost doubled to more than 1.3 million in2012 (Figure 4). Of these, bilisi handled about1.2 million passengers, Batumi about 170,000,

Figure 4 Passengers and Freight Handled at Georgia’s Airports

Source: Consultant’s computation based on statistics provided by the Ministry of Economy and Sustainable Development.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

0

200,000

400,000 N u m

b e r o

f P a s s e n

g e r s

Year

F r e

i g h t H a n

d l e d ( t o n s )

600,000

800,000

1,000,000

1,200,000

1,400,000

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

Air Passengers Air Freight

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 28/48

17

Sector Assessment: Current Status and Strategic Issues

Kutaisi 13,000, and Mestia 3,000. Freight trafficincreased by about 7% a year since 2004 to reach165,000 tons in 2011, with bilisi handling thebulk. Although it is unlikely that this rate ofgrowth will continue, there is sufficient landsidecapacity at both bilisi and Batumi to servetraffic until around 2020.

Kutaisi, which was a regional airport, wasupgraded to international standards, opened fortraffic in September 2012, and handled nearly13,000 passengers that year. It is in Kopitnari,about 14 km west of Kutaisi, the country’ssecond-largest city, which was slated to be thenew capital until the government changed

in 2013. It serves low-cost regional carriersand commuter service operators from bilisi.However, public transport from the airport toKutaisi and bilisi is limited and informal.

Queen amar Airport in Mestia is servedby about ve ights a week from bilisi. Anew airport is being constructed in Zugdidi,

while the airport in Poti, which was closedin the 1990s, will also be developed. Tere isan aerodrome for small airplanes at Senaki.

RAKIA, the owner of the Poti Free IndustrialZone, plans to develop a private cargo airportto attract air–sea traffic to Poti and serve theindustrial zone traffic.

c. Air Services

In 2012, 23 registered airlines operated inGeorgia, offering scheduled and charterservices from Batumi, Kutaisi, and bilisi to12 international destinations.25 Privately owned

Airzena Georgian Airlines, the national agcarrier with a eet of seven aircraft,26 had thelargest market share in 2011, at 21%, followedby urkish Airlines with 17%. Aerosvit, aUkrainian airline, had 11%, followed by Pegasus

25 Computed from data provided by United Airports ofGeorgia.

26 Georgian Airways. http://www.georgian-airways.com

at 9%, and Belavia and Lufthansa, each with 6%of the market. FlyGeorgia is the latest Georgianairline to enter the market, offering scheduledights to ehran and Amsterdam. In June2012, the largest low-budget airline of Centraland Eastern Europe, Wizz Air, and United

Airports of Georgia signed a memorandum forregular Kutaisi–Kiev ights three times a week.It expects to carry about 40,000 passengers in2013.27 Domestic air travel, however, is limited.Passenger traffic on the Kutaisi–Batumi route

was only 38,654 passengers in 2011.

6. Pipelines

Georgia hosts two international pipelines:the Baku–Supsa line connected to the Supsaterminal, with a capacity of about 7 million tonsof oil per year, and the Baku– bilisi–Ceyhanline, connected to Kulevi. Te transport cost ofusing these two lines, which form the westernroute for moving Azerbaijan’s oil to worldmarkets, is reportedly half that of the northernroute via the Russian Federation (IMF 2004).

Tis competitive edge, through transit fees andin-kind payments in gas, has been a source ofnontax revenue for the country.

C. Cross-Sector Issues

1. Policy and Planning

Te transport sector lacks an explicit policyto guide its development in an integrated,inclusive manner. Coordination of modesis now done through the Commission of

ransport, chaired by the Prime Minister.It meets only when called by MESD todiscuss matters related to proposed legislation,foreign funding, project implementation, and

27 Government of Georgia, MESD. http://www.economy.ge

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 29/48

18

Georgia Transport Sector Assessment, Strategy, and Road Map

technical standards, and is inadequate to fosterdevelopment. Consequently, each agencyand mode’s vision, mission, and strategy areindependent. Tis deciency, part of which hasbeen highlighted recently by the World Bank,has caused the sector to remain without threefundamental prerequisites for development(World Bank 2012a):

(i) a development strategy with aneconomically justied road map for eachmode and nancing arrangements,

(ii) regulators with authority to fostercompetition and ensure good-qualitypassenger and freight services, and

(iii) a workforce with the right skills mix andexperience.

2. Sustainability

Te government has yet to start implementingcorrective measures proposed by MESD againstthe potential impacts of increasing travel andtrade resulting from transport development.28 For instance, aspects that have an impact on

climate change—such as energy use, greenhousegas emissions, and renewable material use inconstruction and maintenance—are not fullyconsidered in investment decisions. Althoughsome steps have been taken in the rightdirection, they are often not fully realized. Forexample, ambient air quality is now monitoredat seven stations in ve cities, but is inadequatefor effective monitoring of air pollution bymotor vehicles (Government of Georgia,Ministry of Environment Protection 2011), and

28 These include (i) developing public transport, (ii) reducingtravel distances, (iii) optimizing traffic flow, (iv) enforcingimport limits on the age of old vehicles, (v) improvingfuel quality, (vi) creating incentives for fuel-efficientcommercial vehicles, (vii) reintroducing roadworthinesstesting, (viii) conducting stricter enforcement of vehicleemissions, and (ix) developing electric transport systems.

These measures are expected to reduce carbon dioxideemissions by 4%–7%, carbon monoxide by 20%, and nitricoxide emissions by 40%.

meaningless if the corrective measures are notimplemented (World Bank 2011a; Governmentof Georgia, MESD 2010). In addition, designand supervision consultants, contractors,and materials suppliers are without nationalguidance on climate change requirements exceptfor project-related environmental managementplans, which are more in line with the safeguardpolicies of the donors than climate change.

Inadequate investment in asset preservationhas caused many roads to deteriorate.

Although the newly created assets are receivingconsiderable attention and are being constructedto higher standards, there is no long-term

plan to keep them in good condition withtimely maintenance. Investment is also lackingin research and development for producingconstruction materials and methods to suit localconditions.

ransport demand management plansto enable better distribution of traffic amongthe modes are also absent. Such plans wouldinclude information systems to assist travelers inplanning trips using the best mix of modes and

for enhancing safety in the context of a programalready in place to reduce road accidents. TeNational Road Safety Action Plan sets out thestrategy for cutting accidents (Governmentof Georgia, MESD 2010) by improvingroad geometry, conducting safety studiesand educational campaigns, and increasingenforcement.

Te plan has yet to be fully implemented.However, after peaking in 2008 at 10 times that

of European countries, the total number of roadaccidents fell 25%, and fatalities declined 39%by 2011 (National Statistics Office of Georgia2012).29 Tis improvement can be attributedin part to the introduction of increased policesurveillance that has reduced drunk driving

29 Also based on data from the Ministry of Internal Affairs.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 30/48

19

Sector Assessment: Current Status and Strategic Issues

and improved road conditions—parts of theroad safety plan. Nonetheless, the accidentrate remains high. Te plan is unlikely to havea major impact, mainly because the proposedmeasures have not been fully researched andcustomized to the local conditions. Moreover,some prerequisites for their success, such asdriver insurance, emergency medical services,and vehicle standards are neither present in thecurrent legislation nor are they planned.

Tere is no information on the safety recordof other modes. However, it is reasonableto assume that basic safety and emergencypreparedness measures are in place at the

ports and airports, and for maritime andaviation services, as they are mandatory underinternational conventions. Similar mandatorymeasures must be put in place for the railway.

3. Logistics Services

Te most active logistical operation is used- vehicle trading. Georgia serves as marketplacefor used vehicles, imported mainly from

Germany, for buyers in Azerbaijan and Armenia. Tis has created informal jobs andhelped keep export gures high. Other logisticaloperations are limited to trucking, shipping,and port handling, provided mainly by foreigncompanies. Processing, packaging, warehousing,or distribution services are informal anduncoordinated. Tere are no proper markets orstorage facilities, and large amounts of wasteoccur in rural agriculture production areas(USAID 2011a). Waste can be attributed in partto the poor condition of the roads. Buyers andfreight operators are unable or nd it too costlyto reach the sources. When they do, damageoccurs in transit due to poor packaging and lackof refrigeration.

Te goal to make Georgia an internationalgateway and the EWH a logistics corridor

is achievable with good planning andperseverance. Georgia’s exports by value in 2011comprised motor vehicles and parts (22.3%),iron and steel (20.0%), beverages (8.3%),fertilizer (6.6%), and fruit and nuts (6.4%),30 all of which indicate that greater industrial

value addition is possible. Te governmentoffers incentives for developers of logisticscenters in the form of free land and assistance.Legislation on establishing industrial zonesattracts investment (EU–Georgia BusinessCouncil 2007). Preference is given—in parallelto the traditional self-sufficient agriculture—tomodern primary production and processing

enterprises, and agricultural and logisticscenters. All are intended to enable producers,exporters, importers, and distributors to havestorage facilities, primary processing, sorting,packaging, retail and wholesale outlets,container warehouses, and laboratories (USAID2011a). Tese incentives help address twocritical issues—poverty and food security.

Hence, donors and private developershave shown considerable interest. Te bilisi

Logistics Center has been developed as a joint venture on a budget of $26 million–$38 million.31 Its aim is to use the direct railway connection toGeorgia’s seaports with Azerbaijan and Armeniato provide a unique combination of rail servicesfor containers and warehousing in an area of91,500 square meters (Georgia oday2012). TePort of Poti has set up the Poti Free IndustrialZone of around 8,000 square meters. Some145 companies and individuals have registeredto use the zone for various logistics services,and 10 have started operations, performing

warehousing and distribution functions or

30 Provided by the Transport Policy Department, and basedon data from the National Statistics Office of Georgia.

31 This is supported by the Economic Prosperity Initiative ofthe Government of the US and was launched in April 2012to become a core for a multimodal transport system inthe Caucasus and to serve as the main logistics center for

Tbilisi and eastern Georgia.

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 31/48

20

Georgia Transport Sector Assessment, Strategy, and Road Map

virtual operations.32 Te government has alsoinvited investors to participate in a $7 million venture for a 4.7-ton fruit and vegetable coldstorage facility serving the bilisi–Rustavi area.

Te Japan International Cooperation Agency (JICA) has studied the feasibility of theconcept ofmichi-no-eki , or roadside stations, which are used in rural Japan by local farmers,food processors, and artisans to reach buyers.Such points of sale are also expected to addressthe problem of the declining rural population(footnote 5). Te success of the concept alsodepends on the quality and cost of accessibilityfrom the production areas to such stations. Te

World Bank has observed informal stationsemerging along rehabilitated secondary roads. A cost-effective extension to this is to networkthe supply chain by connecting the smallerlogistics centers to larger centers located alongthe EWH.

4. Transport for Tourism

Te government is aiming to attract 5.0 million

visitors per year by 2015,

compared with2.8 million in 2011 (Government of Georgia,Ministry of Environment Protection 2011).However, to support this target, transportdevelopment must be linked to tourism. Mosttourist areas lack good-quality, all-weatheraccess. Public and private transport fromairports and railway terminals are unknownto visitors and residents, and are slow andunreliable (Government of Georgia, Ministryof Environment Protection 2011).

5. Users with Special Needs

Inclusive growth requires provision of mobilityto all segments of the population. One part of

32 Other centers have been created or are planned, butinformation on their operating status is unavailable.

this is paying equal attention to the transportneeds of women, children, senior citizens, andpeople with disabilities. Te current design andoperation policies and standards must be revisedto meet their needs. For instance, bus andtrain stations and airports must have signs andfacilities to aid disadvantaged users. ransportneeds for implementing the government’s genderequality action plan must also be formallyconsidered in investment decisions (Governmentof Georgia 2011a).

6. Workforce

Workforce issues in the transport sector havereceived limited attention. Donor assistance hasbeen used for occasional training of governmentofficials and private contractors, and facilityand curriculum improvements at educationalestablishments. However, these activities arenot sufficiently based on sound knowledge of

workforce needs. MESD and MRDI staff donot have sufficient transport sector skills neededto manage the expanding transport network.

Tose who have obtained formal degrees andlicenses from nationally and internationallyaccredited institutions need opportunities forcontinuing education and career advancementsin the sector.

Te World Bank and ADB continueto provide short-term training for RoadsDepartment staff members to developspecic skills that can help them moreeffectively execute their roles. However, the

department needs more skills and experiencein planning and programming, developingpublic–private partnerships, communicating

with road users and the public (Governmentof Georgia, L A 2012), quality control andquality assurance, risk management and valueengineering, and general project management.It cannot depend entirely on consultants,

8/13/2019 Georgia Transport Sector Assessment, Strategy, and Road Map

http://slidepdf.com/reader/full/georgia-transport-sector-assessment-strategy-and-road-map 32/48

21

Sector Assessment: Current Status and Strategic Issues

because certain tasks cannot be outsourced andthe national consulting rms are experiencinga shortage of skilled staff members. Te RoadsDepartment needs a forward-looking humanresources development plan to attract and retainstaff with advanced skills. However, universitiesin Georgia lack faculty and resources to producegraduates with such skills.

Skilled labor and semiskilled labor arealso in short supply despite countrywide highunemployment. Vocational education andtraining opportunities for young people arelacking even in the cities, making labor costsrise. Wage demand by road construction

workers in eastern Georgia in October 2012 was more than 50% higher than the nationalaverage. Tese factors, in concert with thepressure on contractors from the governmentfor faster project delivery, are pushing upconstruction costs to uneconomical levels,and affecting quality and productivity asevidenced by the premature failure of severalrecently rehabilitated roads. Moreover, foreigncontractors fear that they will be unable to meet

the national labor quotas (e.g., at least 70% ofcontract workers must be Georgian nationals)stipulated in some contracts, and therefore incurdelay costs.

Batumi State Maritime Academy,Free bilisi University, Georgian AviationUniversity, and Georgian echnical Universitycurrently offer degrees in transport-related