Embed Size (px)

Citation preview

1

Gifts vs. Grants

Thursday, May 3rd, 2012

2

Policies & Guidance

Temple University Gift Acceptance Policyhttp://policies.temple.edu/getdoc.asp?policy_no=05.60.01

Temple University Exchange Transactions, Contributions and Sponsored Projectshttp://www.temple.edu/controller/Procedure-AwardSetUp-GRPR01.06ExchangeTransactionsCon.pdf

3

LanguageDonor - gifts/grantsSponsor - grants/contracts etc.Contribution - Gift (restricted or

unrestricted)Exchange Transaction - Grant,

Contract, or other (restricted only)

4

Definitions/Considerations

CASE Management StandardsPrivate or Public Foundation or Institution Institutional Practice

5

Standards and Regulations Government Accounting Standards Board

(GASB) Financial Accounting Standards Board

(FASB) Internal Revenue Service (IRS) Office of Management and Budget (OMB

A-21)

6

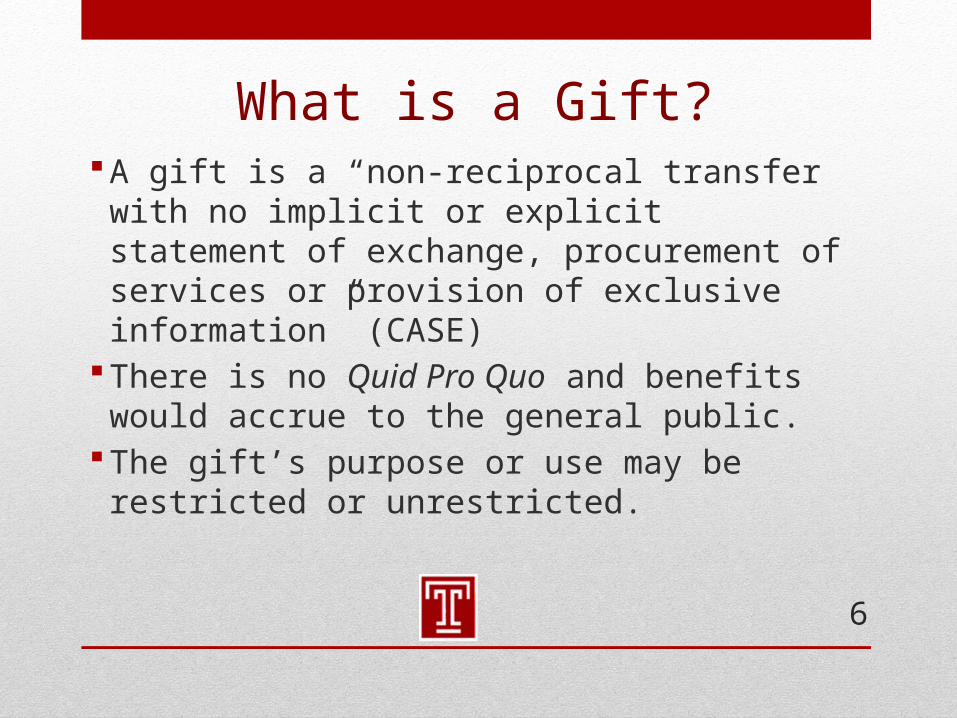

What is a Gift? A gift is a “non-reciprocal transfer with no

implicit or explicit statement of exchange, procurement of services or provision of exclusive information” (CASE)

There is no Quid Pro Quo and benefits would accrue to the general public.

The gift’s purpose or use may be restricted or unrestricted.

7

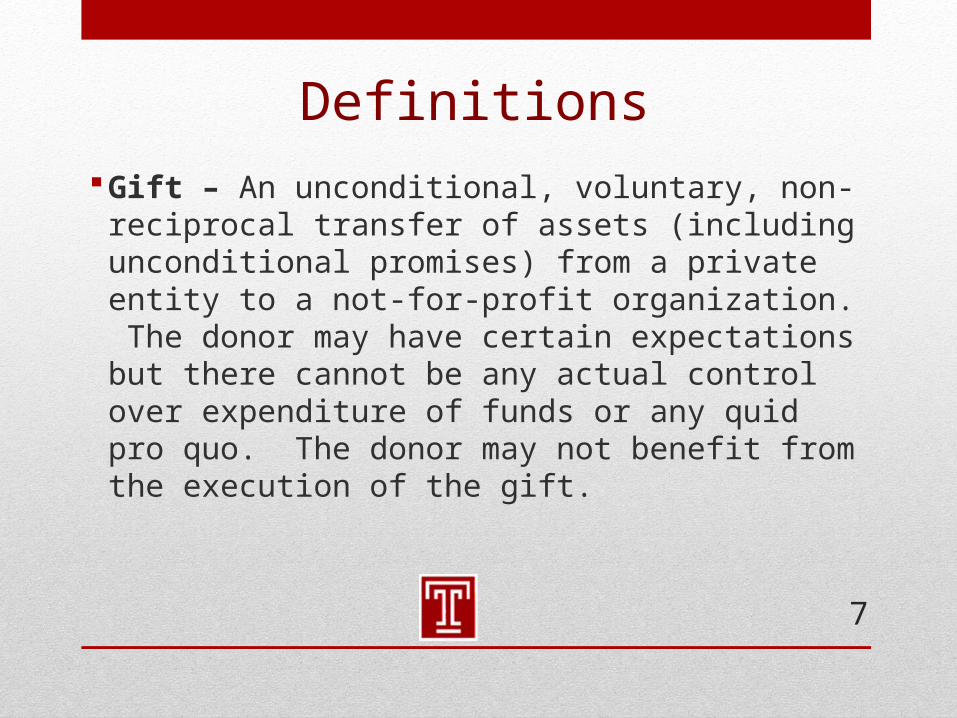

Definitions Gift – An unconditional, voluntary, non-

reciprocal transfer of assets (including unconditional promises) from a private entity to a not-for-profit organization. The donor may have certain expectations but there cannot be any actual control over expenditure of funds or any quid pro quo. The donor may not benefit from the execution of the gift.

8

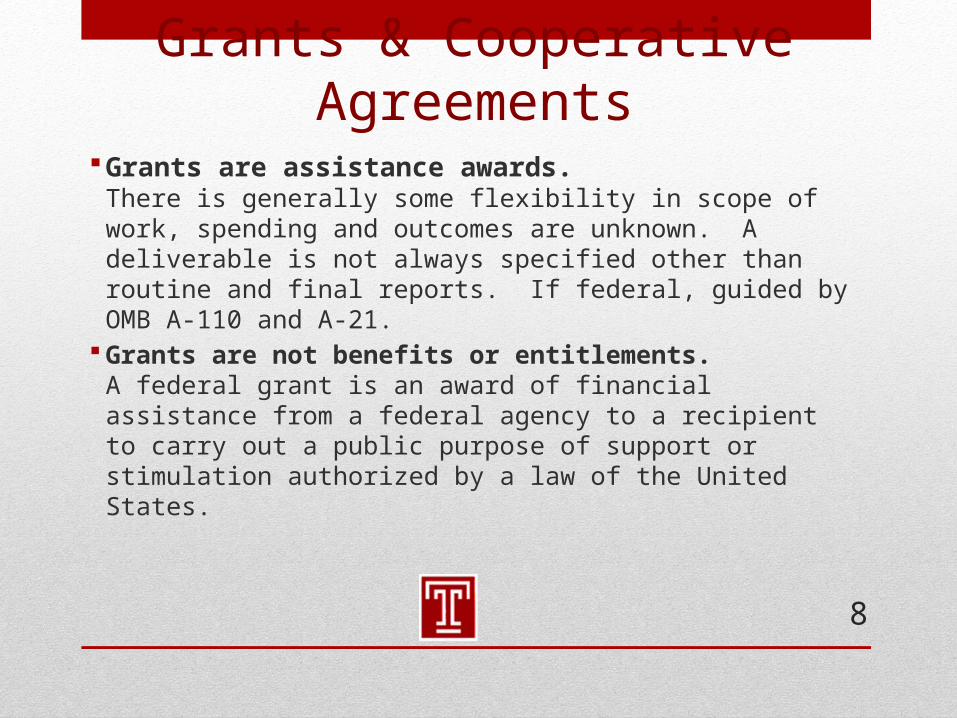

Grants & Cooperative Agreements Grants are assistance awards.

There is generally some flexibility in scope of work, spending and outcomes are unknown. A deliverable is not always specified other than routine and final reports. If federal, guided by OMB A-110 and A-21.

Grants are not benefits or entitlements.A federal grant is an award of financial assistance from a federal agency to a recipient to carry out a public purpose of support or stimulation authorized by a law of the United States.

9

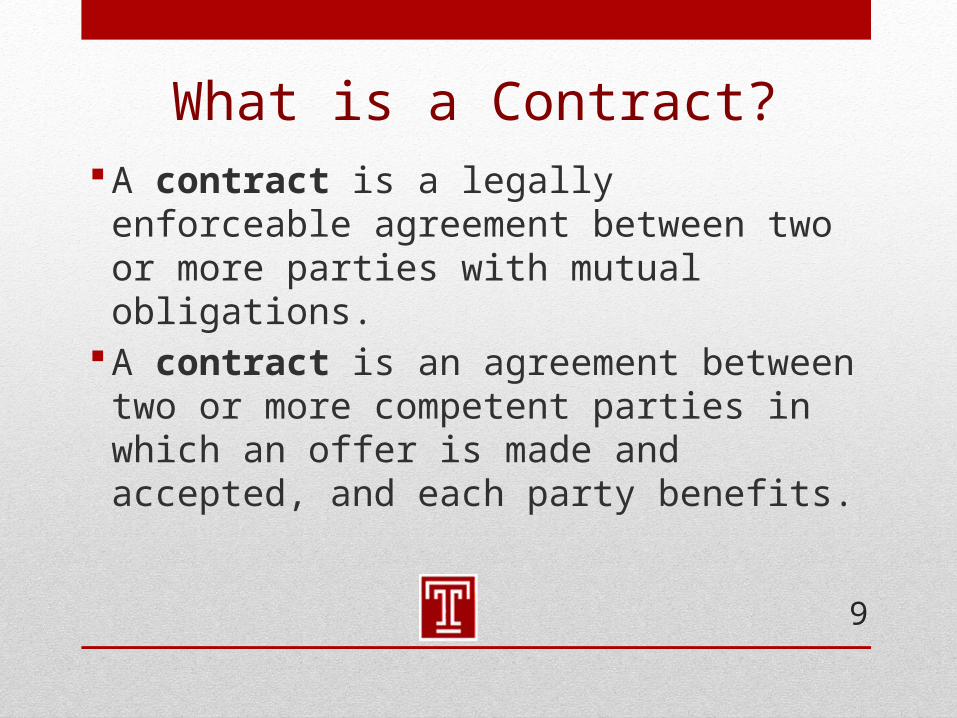

What is a Contract?A contract is a legally enforceable

agreement between two or more parties with mutual obligations.

A contract is an agreement between two or more competent parties in which an offer is made and accepted, and each party benefits.

10

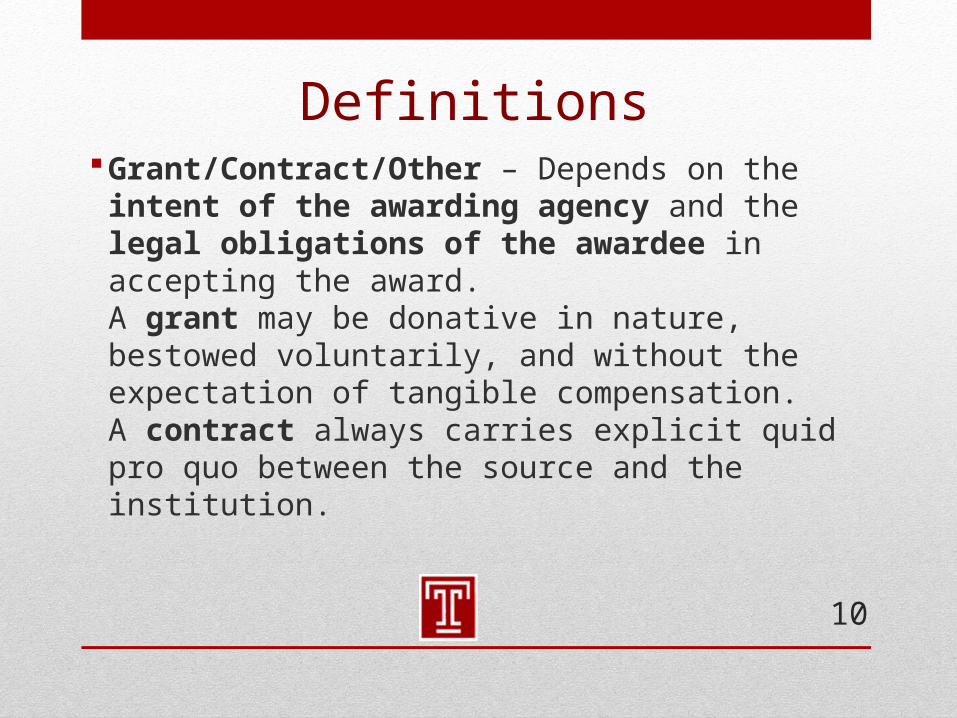

Definitions Grant/Contract/Other – Depends on the intent

of the awarding agency and the legal obligations of the awardee in accepting the award.A grant may be donative in nature, bestowed voluntarily, and without the expectation of tangible compensation.A contract always carries explicit quid pro quo between the source and the institution.

11

Other Considerations Lack of indirect cost on a project does not

make it a gift. Gifts may be used to match federal dollars –

but then must be used according to federal cost principles.

In rare instances, a sponsor can provide both a restricted gift and a sponsored project for the same purpose.

12

How Do I Know – Sponsored Projects?1. Government sponsor2. Delivery of goods, services etc.3. Performance milestones4. IP interest (patent, copyright etc.)5. A contract: insurance, warranty, other contract clauses etc.6. Funding rescission clause7. Patient care costs/routine care8. Testing services9. Quid Pro Quo with sponsor

13

How Do I Know – Gifts?1. Primary beneficiary is the general

public – not the donor.2. Irrevocable3. Donor has no expectation of economic

or other tangible benefit4. Detailed financial generally not

required

14

eRA Routing Review & Approval

Institutional Advancement reviews all corporate industry & foundation sponsored proposal submissions.

15

Characteristics of a Grant, Contract and Gift for Sponsored Research

Gifts Description: Funds or goods that are given

voluntarily to Temple University with no reciprocal obligations. Absence of any quid pro quo expectations.

May be restricted or unrestricted funds – donor may define the purpose or a specific area of research that the gift is being provided for

Unexpended funds are not required to be returned

No specific period of performance No quid pro quo The transfer of funds or goods is irrevocable No formal financial accounting requirements

beyond a general report of expenditures No budgetary restrictions No formal requirement that research results

be reported to the Sponsor Imposes no requirement regarding

disposition of either tangible property (e.g., equipment) or intangible property (e.g., inventions, copyrights or rights in data)

Donor(s) may be individuals, companies, corporations or foundations

Qualifies as charitable contribution for donor’s taxes

Grant• Description: An arrangement under which

there is a transfer of funds, property, services or anything of value from the sponsor to the institution to assist the institution in reaching a particular institutional goal or public purpose.

• PI defines the project – usually fairly loosely – Scope of Work or Proposal is cited in award

• Sponsor retains the right to revoke the award and unused funds revert back to sponsor

• Has a defined period of performance• Reports are normally on an annual basis• Supports further knowledge in a particular

subject area or field of research• Temple University owns IP• Publications are not restricted• “Best efforts” are used in completing

research• Benefit is normally to grantee/PI by

furthering their own purposes or programs• IRS includes scholarships, fellowships,

internships, prizes, and awards• May qualify as charitable contribution

depending on source of funds

Contract

• Description: A mechanism for the procurement of a specific service or product with specific obligations for both the buyer and the seller. Creates a quid pro quo relationship.

• Sponsor or Sponsor and PI jointly define Scope of Work

• Sponsor retains the right to terminate the contract

• Reports are often done more frequently than annually

• Publication may require review/approval of the sponsor

• Benefit is normally to the sponsor – anticipates and economic benefit as a result of the activity to be conducted

• Contractor generally is required to produce a work product or deliverable (it’s possible this is only a report of findings)

• Contractors are paid only if the deliverable is accomplished

• Most involve some supervision or control by sponsor (on expenditures and/or deliverable)

• Provides expertise/knowledge to solve a problem

16

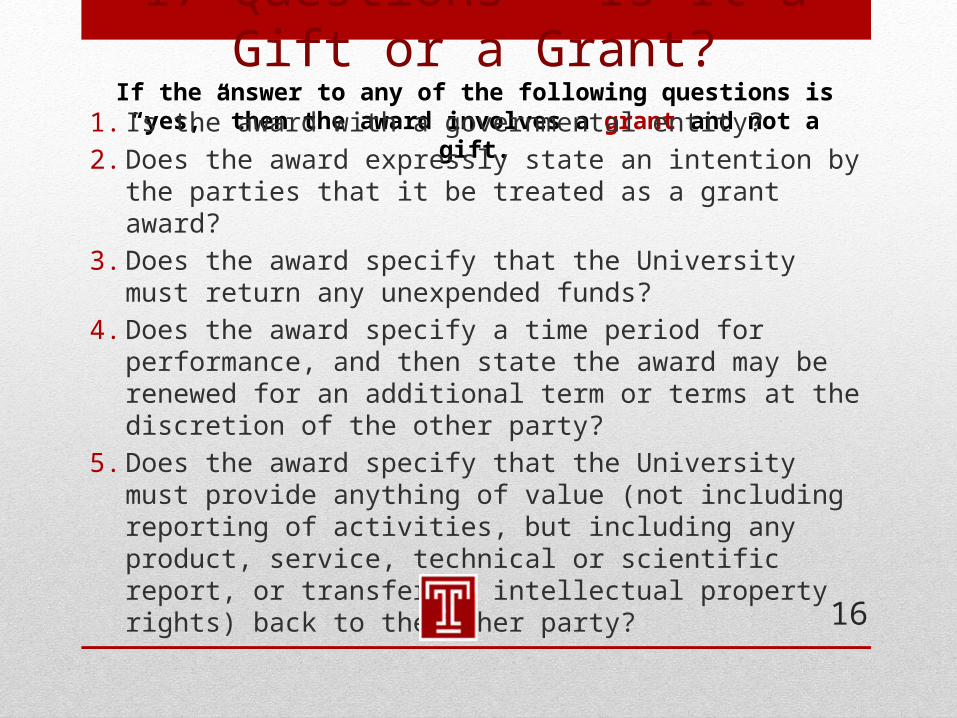

17 Questions – Is It a Gift or a Grant?If the answer to any of the following questions is “yes,” then the award

involves a grant and not a gift.

1. Is the award with a governmental entity?2. Does the award expressly state an intention by the parties that it be

treated as a grant award?3. Does the award specify that the University must return any

unexpended funds?4. Does the award specify a time period for performance, and then

state the award may be renewed for an additional term or terms at the discretion of the other party?

5. Does the award specify that the University must provide anything of value (not including reporting of activities, but including any product, service, technical or scientific report, or transfer of intellectual property rights) back to the other party?

17

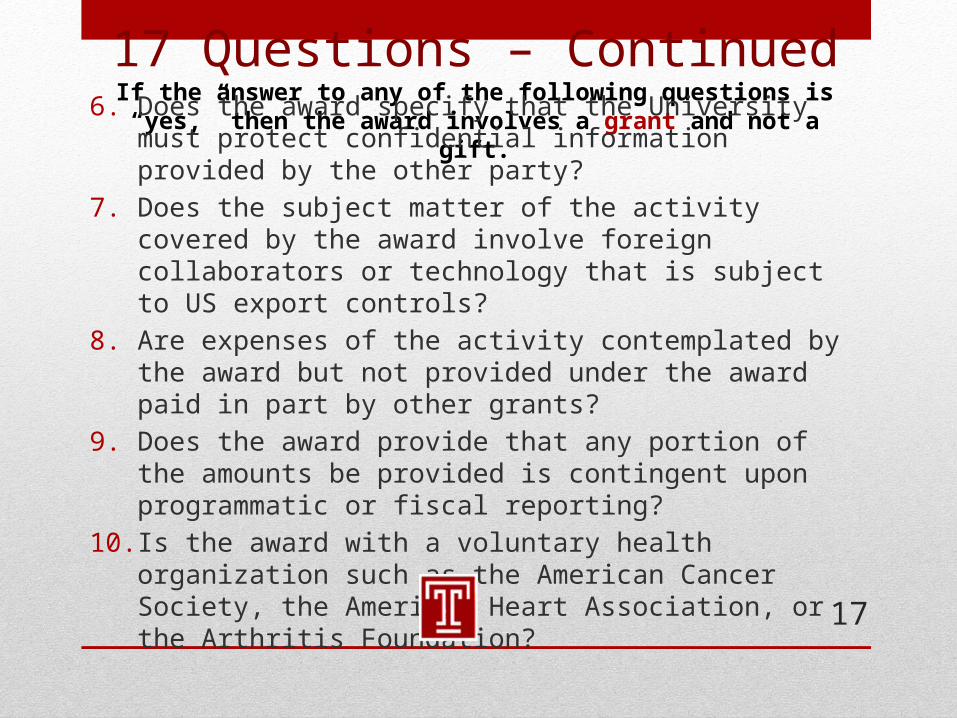

17 Questions – ContinuedIf the answer to any of the following questions is “yes,” then the award

involves a grant and not a gift.

6. Does the award specify that the University must protect confidential information provided by the other party?

7. Does the subject matter of the activity covered by the award involve foreign collaborators or technology that is subject to US export controls?

8. Are expenses of the activity contemplated by the award but not provided under the award paid in part by other grants?

9. Does the award provide that any portion of the amounts be provided is contingent upon programmatic or fiscal reporting?

10. Is the award with a voluntary health organization such as the American Cancer Society, the American Heart Association, or the Arthritis Foundation?

18

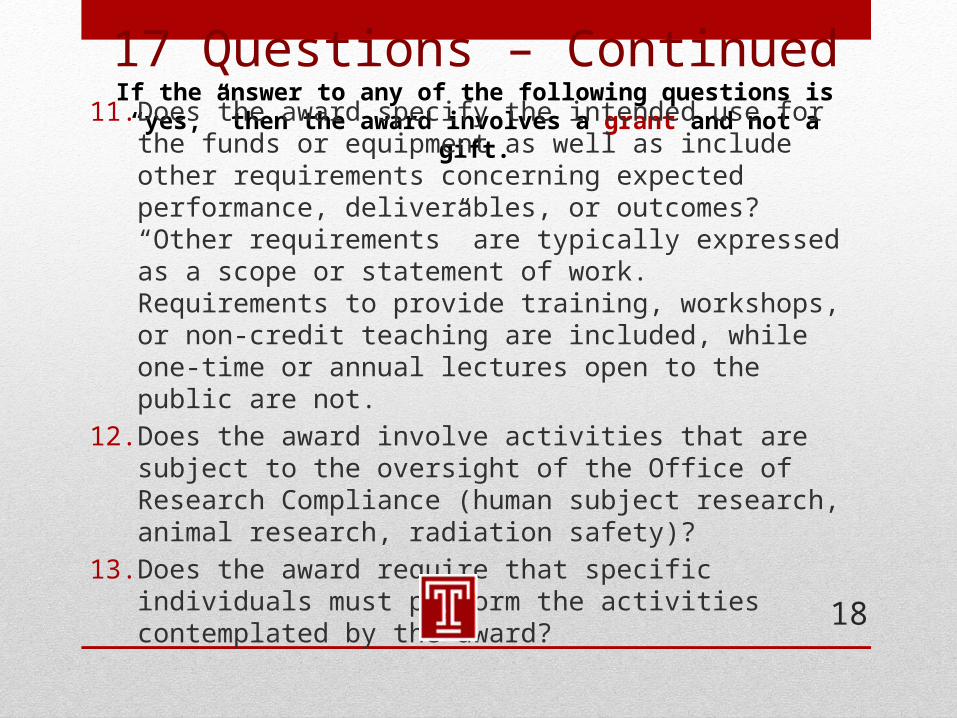

17 Questions – ContinuedIf the answer to any of the following questions is “yes,” then the award

involves a grant and not a gift.

11. Does the award specify the intended use for the funds or equipment as well as include other requirements concerning expected performance, deliverables, or outcomes? “Other requirements” are typically expressed as a scope or statement of work. Requirements to provide training, workshops, or non-credit teaching are included, while one-time or annual lectures open to the public are not.

12. Does the award involve activities that are subject to the oversight of the Office of Research Compliance (human subject research, animal research, radiation safety)?

13. Does the award require that specific individuals must perform the activities contemplated by the award?

19

17 Questions – ContinuedIf the answer to any of the following questions is “yes,” then the award

involves a grant and not a gift.

14. Does the award limit the publication rights of the individual faculty undertaking the activities contemplated by the award in any way, including any duty of notice to the other party in advance of publication?

15. Does the award provide for the payment of indirect or administrative costs from the other party?

20

17 Questions – ContinuedIf the answer to any of the following questions is “yes,” then the award

involves a gift and not a grant.

16. Does the award merely specify the intended use for the funds or equipment provided, and not include any other requirements concerning performance, deliverables, or outcomes except for reporting back to the other party?

17. Does the award specify that the funds provided are to be used for endowments or capital projects?

If none of the preceding questions have resolved the issue, the matters should be referred to the Offices of Sponsored Programs and Institutional

Advancement for a decision.