Embed Size (px)

Citation preview

positive property report2012ISSUE 9

Page 1

Gladstone:The BesT Is YeT To Come

positive property report 2012ISSUE 9

positive property report2012ISSUE 9

View Positive Properties Now

Page 2

Introduction

Crawford Property Group

Crawford Property Group are your positively geared property experts, specialising in cash flow earning property Australia-wide.

Positive Property is now the investment vehicle of choice and of fers many benefits including; passive income, high rental returns and the ability to build a successful por t folio much quicker!

Crawford Property Group is your positive property destination and can help with market knowledge, education, property selection and management of your new investment property.

What are you waiting for, explore our site and star t your investment journey today. Search our positive properties, accurate market information, market updates, success stories, best financial options and the right advice.

positive property report2012ISSUE 9

View Positive Properties Now

Page 3

The Best is Yet to Come – Gladstone ..........................................................................................................4

Key report findings ....................................................................................................................................................5

Macroeconomic Investment Story ...............................................................................................................................5

Why YOU should invest in Gladstone ............................................................................................................................7

Queensland’s Premier Industrial City .........................................................................................................8

History being repeated, only magnified ......................................................................................................................12

Australia’s Super-Infrastructure Town .....................................................................................................14

$105bn in planned and committed projects ...............................................................................................................16

Diversity of development ..........................................................................................................................................17

LNG Projects – Over 30 years life..............................................................................................................................18

$226m in civil infrastructure projects ........................................................................................................................19

Strong Population Growth .........................................................................................................................20

Leading Professor of Regional Economics predicts 8,100 new dwellings required ........................................................23

Lack of supply .........................................................................................................................................................25

Massive capital growth forecast ................................................................................................................................28

Australia’s $555bn resources boom only 1/3 through .................................................................................................29

Three phases of the commodities boom ....................................................................................................................31

The Great Chinese Urbanisation ...............................................................................................................33

Japanese Turning Away from Nuclear to LNG .............................................................................................................36

Rising demand for coking and thermal coal ...............................................................................................................38

Demand for coking coal to soar 80% by 2025 ...........................................................................................................38

Demand for thermal coal also to rise 30% by 2030 ....................................................................................................39

LNG – the World’s New Energy Source .....................................................................................................40

Queensland coal production could triple by 2020, with coking coal production to rise 100% .........................................43

300% increase in East Australian LNG production ......................................................................................................44

Contents

positive property report2012ISSUE 9

View Positive Properties Now

Page 4

The Best is Yet to Come – Gladstone

This report details one of Australia’s super-infrastructure boom towns, Gladstone, Queensland’s most important industrial town – which boasts a staggering $105bn in approved and planned infrastructure projects. With over $65bn in projects currently under construction, the last two years have seen rents soar by over 60% and median house values rise 22%.

The future looks even brighter, with a renowned Queensland Professor of Regional Economic (relied upon by Federal and State Governments) forecasting Gladstone to experience hundreds of thousands in capital growth over the next five years.

positive property report2012ISSUE 9

View Positive Properties Now

Page 5

Key report findings:

Gladstone – Multi-billion dollar, multi-industry1. Gladstone is Queensland’s oldest and largest industrial centre. Located 550km north of Brisbane,

it is the home of the world’s 3rd largest alumina refinery and 5th largest coal por t, Australia’s 4th largest por t and power station, and Australia’s largest alumina smelter and cement plant;

2. Gladstone has experienced three major property booms in the last 25-years, all following small billion dollar infrastructure projects, and a four th boom has begun following commencement of three massive liquefied natural gas (‘LNG’) projects;

3. The city boasts over $105bn ($65bn under construction) of infrastructure projects, the largest concentration of multi-billion dollar projects in Australia representing four separate commodities – alumina, coking coal, LNG and thermal coal – with future billion dollar projects to see a fur ther two commodities (nickel and iron ore) make the city the most diversified industrial city in Australia;

4. $226m in civil infrastructure projects are commit ted or proposed to accommodate the rapid population expansion forecast for Gladstone;

5. Gladstone’s population is expected to soar by more than 21,000 (or 33%) by 2018, as over 9,000 new, permanent jobs are created ( in addition to some 8,000 construction jobs);

6. The surge in the population is creating demand for an estimated 8,100 new dwellings by 2018 and the required average construction rate of 1,013 per annum far exceeds historical construction rates;

7. The combination of thousands of highly paid construction workers, new permanent jobs and demand for new housing is forecast to see median house prices rise by between $200,000 and $350,000 between 2012 and 2018.

Macroeconomic Investment Story 8. Australia is the midst of an unprecedented boom that has seen its terms of trade reach 150-

year highs. While a colossal $100bn has been spent on commodity infrastructure projects in Australia, a pipeline of $268bn in approved projects are underway or soon to commence;

9. While the first phase of the commodities boom (prices) has peaked, the boom actually has three distinct phases. The second and greatest phase, in terms of job creation, is the investment phase and with $260bn of approved projects we are only one third of the way through this phase;

positive property report2012ISSUE 9

View Positive Properties Now

Page 6

10. The longevity of the commodities boom is underpinned by the greatest economic event in the world’s history – the urbanisation of China and the emerging world, which will drive unprecedented demand for coking coal, thermal coal and the new ‘clean’ source of energy, LNG;

11. Chinese demand for steel is to double by 2025, which is forecast to drive global imports of coking coal by 80% in the same time;

12. Chinese energy demand is also set to increase global demand for thermal coal and Asian demand for LNG to both rise 30% by 2017;

13. Queensland coal exports are expected to rise by 200% by 2020, while QLD LNG production will jump over 300% to make it one of the largest LNG export hubs in the world.

our research confirms that Gladstone has:

• A shortage of rental stock

• very strong rental growth

• rising demand for new housing (to the tune of 900 dwellings a year)

• A rise in the number of properties selling

the economy is booming with some $30 billion worth of major engineering projects under construction in the resource and energy sectors.

michael matusik

Courier Mail

positive property report2012ISSUE 9

View Positive Properties Now

Page 7

Why YOU should invest in Gladstone

Largest concentration of multi-billion dollar infrastructure projects in Australia (worth a staggering $105bn)

Population to soar by 21,000 residents (33% increase in population) by 2018

New infrastructure projects will create more than 9,000 new permanent jobs (in addition to over 8,000 construction workers required for the major projects)

8,100 new residential dwellings will be required by 2018

Supply very unlikely to meet the average demand of 1,013 new dwellings per year

The resulting shortfall in supply forecast by leading Queensland university to see median house prices rise by an astonishing $200,000 and $350,000 between 2012 and 2018

positive property report2012ISSUE 9

View Positive Properties Now

Page 8

Queensland’s Premier Industrial City

Just like the New South Wales port city of Newcastle, Gladstone is ‘the’ industrial hub of Queensland. Unlike Newcastle, which suffered the devastation of the 1999 BHP closure of their steelworks and near 12% unemployment rates, Gladstone has ridden a succession of economic booms as industry after industry has established itself in the city. In fact, Gladstone is the state’s preferred location for major, heavy industry.

positive property report2012ISSUE 9

View Positive Properties Now

Page 9

Beginning in 1925 with its first coal exports, growth began in earnest for Gladstone in 1967 with the establishment of the city’s first alumina refinery (Queensland Alumina Refinery) – which initially produced 600,000 tonnes of alumina per annum and now produces nearly four million per annum, making it the third largest refinery in the world.

In 1976, Australia’s four th largest power station (and Queensland’s largest) was constructed in Gladstone to power the emerging industry. This was followed by the construction of Australia’s largest cement plant in 1981 and then the establishment the Rio Tinto Boyne Smelter in 1982 to develop aluminium, which both led to the creation of thousands of new jobs.

The Gladstone campus of the Central Queensland University opened in 1994 – making another milestone in the rise of the city’s importance. This was followed in 1997 by the $1bn expansion of the Boyne Smelter, which doubled its capacity and lif ted total employment to 1,480 workers.

True diversification of the city was achieved in that year as well, with the construction of the massive $0.7bn RG Tanna Coal Terminal which has grown to become the fif th largest coal exporting terminal in the world.

More was to come and in 2002, the alumina industry expanded with the $1.5bn Rio Tinto ( then Comalco) Stage 1 construction of the Yarwun Alumina Refinery. This was followed in 2007 by the $2.3bn commencement of the Yarwun Alumina Refinery Stage 2 expansion. Thousands of jobs were created.

Image: Boyne Smelter near Tannum Sands (25mins from Gladstone CBD)

positive property report2012ISSUE 9

View Positive Properties Now

Page 10

October 2010 brought the largest game changer to Gladstone’s economy, with the approval of BG Groups’ $20bn Queensland Curtis LNG (‘QCLNG’) project on Curtis Island, across the harbour from Gladstone. Then in January 2011, Santos approved its $18.5bn Gladstone LNG (‘GLNG’) project also on Curtis Island. Simultaneously, 2011 saw the approval of the $1.3bn Western Basin Dredging project to open the harbour for more ship traf fic and the $2.5bn approval of the Wiggins Island Coal Terminal Stage 1 project.

The crowning glory for Gladstone then followed, with Origin approving the first stage of its $23bn Australia Pacific LNG (‘APLNG’) project in July 2011 with the second stage further approved a year later.

Today, these three LNG projects employ over 8,200 workers in Gladstone - many located in mining camps on Curtis Island but many more jobs created by the economic multiplier ef fect of the projects – making today the busiest economic period in the city’s history.

Image: Rio Tinto’s Yarwun Alumina Refinery, Gladstone

positive property report2012ISSUE 9

View Positive Properties Now

Page 11

Image: Cur tis Island LNG, Gladstone

Australia is forecast to become the world’s biggest LNG producer within the next seven or eight years, overtaking Qatar, indonesia and Malaysia. Australia has known reserves likely to last the next 100 years, and new discoveries are happening regularly.

Australia now has seven of the world’s 10 largest LNG projects. resources Minister Martin Ferguson said recently: “By 2017, based on proposed and committed new projects, Australia’s LNG production capacity is projected to quadruple.

Terry Ryder

Property Observer

positive property report2012ISSUE 9

View Positive Properties Now

Page 12

History being repeated, only magnified

Gladstone is no stranger to property booms over the last 25 years. During this period, three massive property booms occurred on the back of three separate $1.0bn to $2.3bn infrastructure projects, being the:

1. 1988-1991 boom (14% pa growth peak)The 1987 approvals of the $1.0bn Boyne Smelter and $0.7bn RG Tanna Coal Terminal expansions brought thousands of workers into Gladstone and created such an economic boom that property prices surged by over 11% pa for four years straight (peaking at 14% pa in 1989).

2. 2002-2006 boom (23% pa growth peak)Gladstone’s $1.5bn second alumina refinery ( Yarwun Stage 1) commenced construction in 2002, star ting the city’s second property boom that lasted five years and saw prices rise between 10% and 23% pa (peaking at 23% pa in 2003).

3. 2007-2008 (24% pa growth peak)The city’s third boom occurred as the second boom began to ease, with the $2.3bn Yarwun Stage 2 expansion commencing construction in 2007 and continuing into 2008 as growth hit a 25-year record high of 24% pa in 2007 and a solid 12% pa in 2008.

Char t 1: Median House Values, Gladstone

positive property report2012ISSUE 9

View Positive Properties Now

Page 13

While the Global Financial Crisis had a very significant impact across property markets in Australia, Gladstone proved extraordinarily resilient. While negative growth was experienced through 2009 and 2010, it was negligible – a fall of 2% pa followed by a fur ther easing of 1%.

What underpinned the health of the property market in Gladstone was the imminent approval of some $60bn in LNG projects that would transform the city into one of the largest LNG hubs in the world.

Fourth boom (2011 onwards)The late 2010 approval of the $20bn QCLNG saw the property market reignite, as Gladstone’ four th property booms commenced.

Median house rents jumped by 44% within the year and median house values rose by 15% as QCLNG was followed by approval of the $18.5bn GLNG and first stage of the $23bn APLNG mega projects plus and approval of the smaller $2.5bn Wiggins Island Coal Terminal Stage 1 and $1.3bn Western Basin Dredging projects.

As thousands of workers poured into Gladstone, the second stage of APLNG was also approved and median rents rose a further 14% and median house values continued to rise – up a further 11% pa in 2012.

Today, hundreds of workers continue to come into the city each month and with over $65bn in commenced infrastructure projects – an amazing 11 times the value of all previous infrastructure projects that drove the three previous property booms – the conditions that have created previous booms are now many times magnified.

Indeed, a study titled Gladstone Population and Housing study – Social Impact Study (2012) (‘CQU Gladstone Report’ ) by esteemed Professor John Rolfe, Professor of Regional Economics at the Central Queensland University has predicted that Gladstone will experience a rise in median house prices of between $200,000 and $350,000 between 2012-18.

Char t 2: Predicted Median House Price (Low Range Scenario), GladstoneSource: Central Queensland Universi t y (G ladstone Populat ion & Housing S tudy – Social Impact Analysis, 2012)

there is much more to Gladstone than construction. two out of every five jobs in Gladstone are associated with manufacturing, with a further 30 per cent related to services and retail.

this is one regional area that has good reason to be on an investor’s radar.

michael matusik

Courier Mail

positive property report2012ISSUE 9

View Positive Properties Now

Page 14

Gladstone: Australia’s Super-Infrastructure Town

The scale of investment in Gladstone is unprecedented in Australia’s history. Indeed, with over $105bn in infrastructure projects committed and planned, Gladstone towers over its rival towns nationwide by a factor of two to three times.

positive property report2012ISSUE 9

View Positive Properties Now

Page 15

Indeed, Gladstone meets all the investor criteria:

High rentals

Strong capital growth potential

Optimistic future

Gladstone is on a path of growth that is making property investors sit up and take notice. As the focus of four major coal seam gas to LNG developments worth approximately $75 billion – each with multi-billion dollar, long term sales contracts for decades of LNG production – Gladstone also has $65bn of approved projects under construction – more than the total approved and commit ted projects of Por t Hedland, Australia’s second largest super-infrastructure boom town.

Better yet, Gladstone is not a one commodity boom town like those in the Pilbara, WA ( iron ore), the Bowen Basin, QLD (coking coal) or emerging Galilee Basin, QLD (thermal coal). I t is even bet ter than the Surat Basin, QLD and towns like Chinchilla that have two commodities (thermal coal and LNG).

No, Gladstone doesn’t just have two commodity industries. Not even three. It has an unheard of four commodity industries – coking coal, thermal coal, alumina and LNG – of fering the best diversification of any other infrastructure mining boom town in Australia.

However, Gladstone isn’t stopping at ‘just’ four global commodities. It is posed to go to six!

The proposed $6.1bn Gladstone Pacific Nickel Plant and $4.0bn Boulder Steel Plant will not only employ a cumulative 8,500 or so construction workers but will see nickel and iron ore join the impressive stable of industries in the city por t, making it Australia’s most diversified industrial city.

Char t 3: Commit ted and Planned Infrastructure Projects, $bnSource: Omega Investments

positive property report2012ISSUE 9

View Positive Properties Now

Page 16

$105bn in planned and committed projects

Gladstone has a breathtaking 18 major projects planned and commit ted, with 17 of these valued over $1.0bn and in total cumulatively valued at a staggering $105bn:

In totality, these projects have the potential to create over 22,000 construction jobs and some 5,000 operational worker positions.

Table 1: Major Planned and Commit ted Infrastructure Projects, Gladstone Source: Omega Investments

positive property report2012ISSUE 9

View Positive Properties Now

Page 17

Diversity of development

The very at tractive feature of Gladstone is that it doesn’t have all of its eggs in the one basket. Its projects span a variety of industries, from the established four commodities to the proposed nickel and steel ( iron ore) production industries.

This diversity will ensure Gladstone’s status as a major infrastructure hotspot into the future and of fer security for its long-term growth prospects.

Map 1: Location of Exist ing and Future Industry – Gladstone

positive property report2012ISSUE 9

View Positive Properties Now

Page 18

LNG Projects – Over 30 years life

The par ticularly exciting aspect of the emerging LNG industry is the nature of the economics of LNG developments. Specifically, these projects are long term with 20-year supply contracts in place that mean they cannot be shut down and mothballed like a conventional mine.

This is due to the huge debt levels reached in building the large, multi-billion dollar projects that will take decades to pay of f.

Recently Santos highlighted the long term nature of LNG projects, when it highlighted that a ‘smaller’ LNG project of only $6-7bn will have a payback period (that is, when all debt and equity has been repaid) of a staggering 22 years. So the proponents of the LNG projects are not expecting to make any money until more than 20 years in the future (of course, it will then be super profits once payback is achieved).

Char t 4: Example of LNG Project Cash Flow – Long Haul Operation

Image: Refinery

positive property report2012ISSUE 9

View Positive Properties Now

Page 19

Table 2: Civil Infrastructure Projects – Gladstone, $m Source: Gladstone Por t Corp, Gladstone Regional Council, Press Search

Image: Concept of Stockland Gladstone Expansion

$226m in civil infrastructure projects

The billions of dollars in major infrastructure projects and the accompanying economic and population growth has led to over $226m in civil infrastructure projects being proposed or commit ted – ranging from the $125m expansion of the local Stockland shopping centre to the proposed $30m construction of the Pioneer Drive Bridge Extension (near the seaside community of Tannum Sands) to a $10m upgrade of the local airpor t’s instrument landing system (following a recently completed $65m upgrade of the landing strip and terminal).

positive property report2012ISSUE 9

View Positive Properties Now

Page 20

Strong Population Growth

In 2001, the population of the Gladstone Local Government Area (LGA) was 46,369. Over the next decade, fuelled by the commodities boom and the Yarwun Stage 1 and 2 expansions, the city’s population hit 59,402 by 2011 (according to the latest census data). This represented an average population growth rate of 2.5% per annum between 2001 and 2011 – significantly faster than the Australian average of 1.4% per annum.

positive property report2012ISSUE 9

View Positive Properties Now

Page 21

According to the central population forecast of the Queensland Office of Economic and Statistical Research (‘OESR’), Gladstone’s population is expected to surge by approximately 22,000 over the next decade – rising some 35% to hit 85,000 by 2021. This represents an average growth rate of 3.3%, well above the rate of growth of the last decade and is reflective of the transformation the city is experiencing from the billions in dollars of major infrastructure projects under construction and proposed.

Char t 6: Gladstone Population Forecast Source: OESR 2011c (note that populat ion est imates are for 30 June each year )

Char t 5: Historic Population Growth - Gladstone Source: Australian Bureau of S tat ist ics, Regional Populat ion Growth, Australia (3218.0). Compiled and presented by .id the populat ion exper ts

YearCha

nge

in n

umbe

r of

peo

ple

positive property report2012ISSUE 9

View Positive Properties Now

Page 22

In the CQU Gladstone Report, Professor of Regional Economics at the Central Queensland University (‘CQU’) John Rolfe predicts that the OESR central forecast is actually conservative.

Fur ther, under the CQU central forecast, Gladstone’s population is expected to reach the OESR’s population 2021 target three years earlier by 2018 – with 21,000 more people in Gladstone by 2018 (a 33% rise) rather than the comparable 2018 OESR forecast of 18,700 (a 29% rise).

Importantly, Professor Rolfe stated, “the cumulative impact of all confirmed projects will see solid rental and sales prices increase over a much longer period of some seven or more years”. This would significantly outlast Gladstone’s earlier booms, which typically lasted two to three years.

If Gladstone’s history has taught us anything, it’s that the region responds favourably to infrastructure spending. So it’s exciting to wonder what may result from the $65 billion worth of infrastructure projects that have been confirmed or commenced in the last 24 months.

Representing 11 times the capital expenditure total of Gladstone’s previous two booms, the money pouring into the region is ramping up expectations of strong future growth.

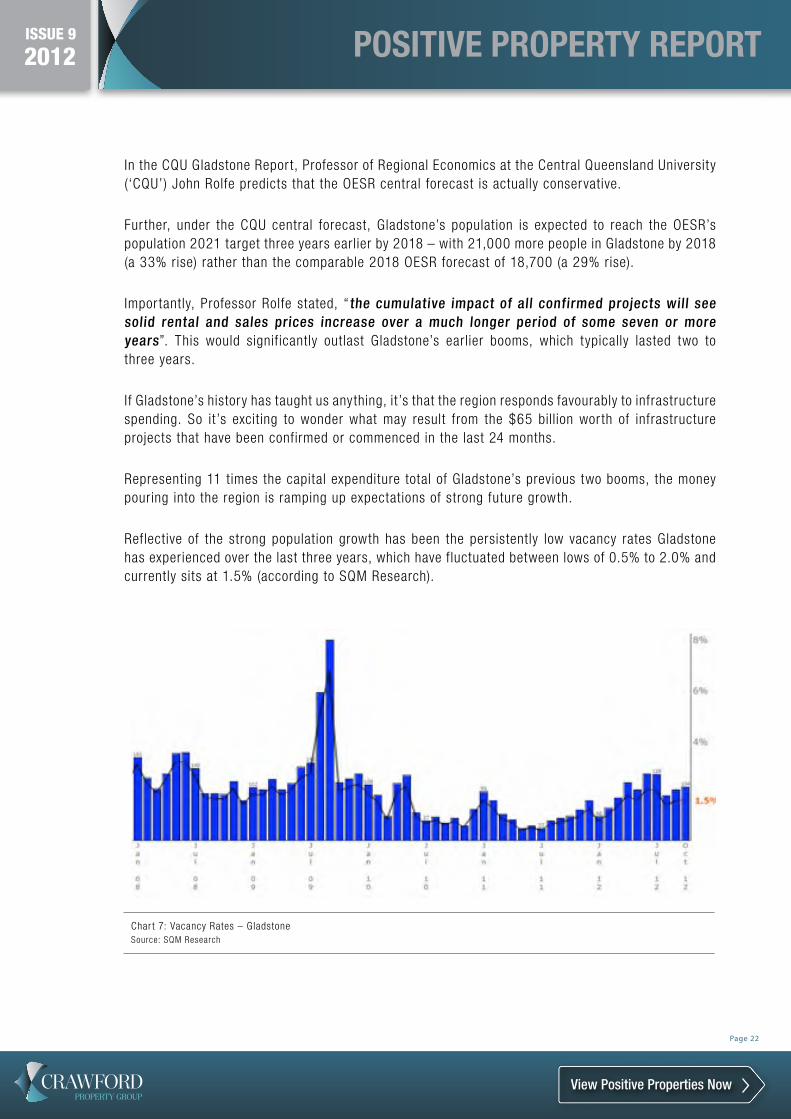

Reflective of the strong population growth has been the persistently low vacancy rates Gladstone has experienced over the last three years, which have fluctuated between lows of 0.5% to 2.0% and currently sits at 1.5% (according to SQM Research).

Char t 7: Vacancy Rates – Gladstone Source: SQM Research

positive property report2012ISSUE 9

View Positive Properties Now

Page 23

Leading Professor of Regional Economics predicts 8,100 new dwellings required

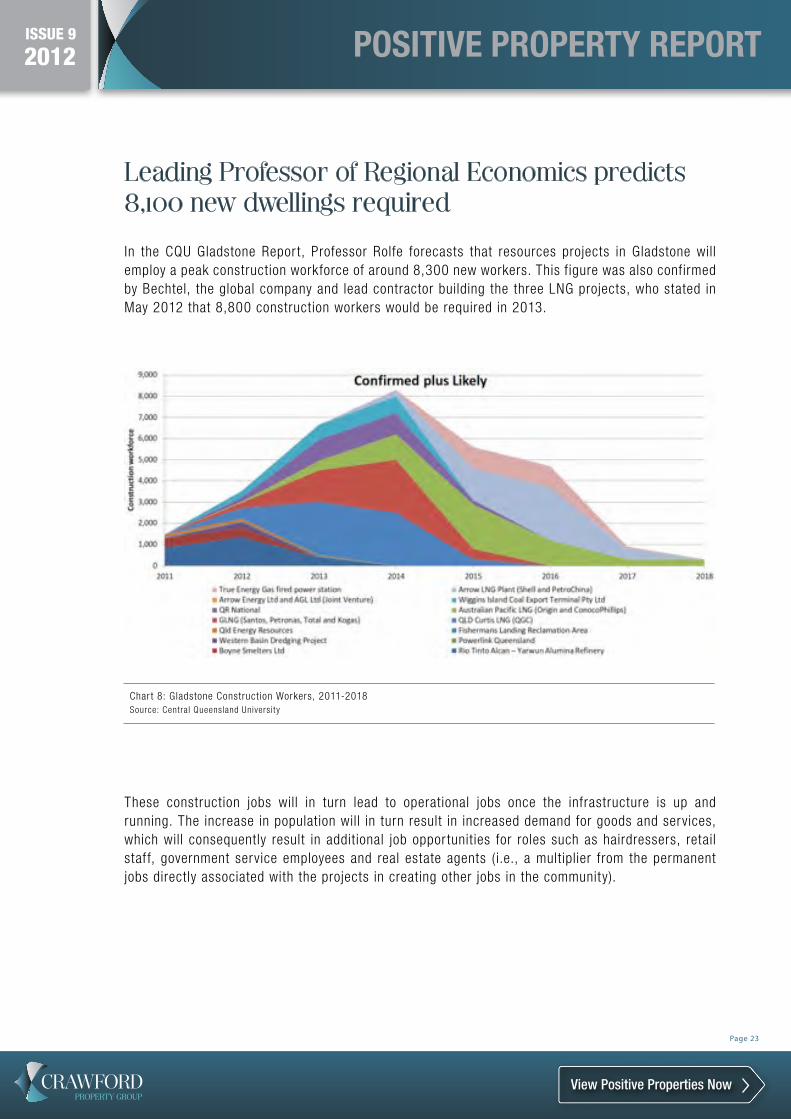

In the CQU Gladstone Report, Professor Rolfe forecasts that resources projects in Gladstone will employ a peak construction workforce of around 8,300 new workers. This figure was also confirmed by Bechtel, the global company and lead contractor building the three LNG projects, who stated in May 2012 that 8,800 construction workers would be required in 2013.

These construction jobs will in turn lead to operational jobs once the infrastructure is up and running. The increase in population will in turn result in increased demand for goods and services, which will consequently result in additional job opportunities for roles such as hairdressers, retail staf f, government service employees and real estate agents ( i.e., a multiplier from the permanent jobs directly associated with the projects in creating other jobs in the community).

Char t 8: Gladstone Construction Workers, 2011-2018 Source: Central Queensland Universit y

positive property report2012ISSUE 9

View Positive Properties Now

Page 24

We have industry, we have jobs, we just can’t accommodate those people that are coming to the city. Gladstone’s Curtis island gas hub is destined to have 7000 new workers, and all must be accommodated.

We just can’t keep pace with the development as it’s happening.

Gail sellers

Gladstone Mayor, Climate Spectator

Specifically, the CQU Gladstone Report forecasts that about 1,700 operational workers will be directly employed by the major resources projects by 2018, which will be followed by about 7,300 additional job opportunities – creating a total of 9,000 new, permanent jobs for Gladstone and 21,000 new Gladstone residents (well above existing government forecasts) by 2018.

This population increase will of course also lead to a rise in demand for residential dwellings. Specifically, Professor Rolfe is forecasting demand for approximately 8,100 new properties between 2011 and 2018.

21,000 New Residents

9,000 New Permanent Jobs

8,100 New Properties

5 5 5

2018 Forecasts – Gladstone

positive property report2012ISSUE 9

View Positive Properties Now

Page 25

Lack of supply

Now, 8,100 new residential dwellings won’t just drop out of the sky – there will be significant challenges building such a large number of new dwellings. In fact, one of the key accelerators of property values in towns like Por t Hedland or Moranbah is the limited ability to build new dwellings (be it due to flooding issues, native title, limited land supply, lack of workers due to major projects soaking up all available workers).

While Gladstone doesn’t have a limited availability of land, what will drive up prices is the tremendous underlying challenges in building enough housing to meet supply in Gladstone.

Over the last 15 years, the number of residential dwellings approved ( ie, as ready for construction) by the Gladstone Regional Council has averaged 528 dwellings pa – rising to 590 dwellings pa for the last 10 years.

Table 3: Dwellings Approved by Gladstone Regional Council Source: Australian Bureau of S tat ist ics, Building Approvals, Australia (8731.0). Compiled and presented by .id

positive property report2012ISSUE 9

View Positive Properties Now

Page 26

To build 8,100 dwellings between 2011 and 2018 (the forecast period for the CQU Gladstone Report) would require 1,013 dwellings to be constructed each year – that is 72% more than the 10 year average and just below the all-time high of 1,110 in 2012!

While dwelling approvals in 2012 were suf ficient to meet that year’s demand, 2011 fell well shor t (at 681 dwellings) and it is very unlikely that an average dwelling rate 72% higher than the 10 year average can be sustained for another six years.

Image: Housing Estate

positive property report2012ISSUE 9

View Positive Properties Now

Page 27

Image: Coal Terminal

The demand for housing is therefore almost cer tain to outstrip supply in Gladstone, at least in the medium term. It is anticipated that significant gaps between supply and demand will continue over the next few years, especially since much of the construction labour force will be employed by the resource development projects themselves. These employees will be at tracted to the higher wages on of fer within the resources industry, leaving a gap in the residential dwelling construction workforce at the very time it is needed most.

positive property report2012ISSUE 9

View Positive Properties Now

Page 28

Massive capital growth forecast

And of course, when supply fails to meet demand, prices rise. Therefore, this predicted lack of supply in the housing market is likely to push property prices up in Gladstone.

According to Professor Rolfe’s forecast modelling, median house prices in Gladstone are expected to rise by almost 60% from their current median price of $457,000 to between $657,000 and $819,000 by 2018.

This all cer tainly bodes well for investors:

• $105bn in infrastructure projects, with $65bn approved and commenced.

• Previous property booms of 20% per annum growth on the back of $1.5-2.3bn projects

• 33% population growth forecast by 2018 to fuel demand for property

• Over 8,100 dwellings required at a rate of over 1,000 per annum, 65% over the last nine year annual average and larger than the all-time high, and this is required each and every year to 2018

• CQU forecast that median house prices will rise by between $200,000 and $350,000 by 2018

It is clear that the best is yet to come for Gladstone.

Table 4: Median House Prices – Gladstone (Central Case): 2011-2018 Source: CQU

positive property report2012ISSUE 9

View Positive Properties Now

Page 29

Australia’s $555bn resources boom only 1/3 through

As the global demand for coal, LNG, iron ore and other natural resources skyrockets, Australia now finds itself in the middle of the biggest resources boom it’s experienced since Federation. The combined value of projects is now five times more than it was in 2005, with $555 billion commit ted or proposed to be invested.

In its history, Australia has experienced three boom periods of exports that led to significantly high levels of trade surpluses, or positive terms of trade. The first was in the 1920s; the second in the 50s; and the third we are living through right now.

Char t 9: Planned and Commit ted Infrastructure Projects ($bn) Source: Omega Investments

Char t 10: Australian Terms of Trade Source: ABS; Gil l i t zer & Kearns (2005); RBA

positive property report2012ISSUE 9

View Positive Properties Now

Page 30

All three booms have been linked to rising global economies and industrialisation, which has naturally increased the demand for commodities. But the biggest distinction between what happened then, and what is happening now, is the type of commodities that are driving our economy forward.

The first two booms in the 1920s and the 1950s were related to ‘sof t’ commodities, namely organic products such as wheat and livestock, and par ticularly wool. The current boom, while also a response to rising demand for commodities due to urbanisation, is principally being driven by demand for ‘hard’ or inorganic commodities such as coal and LNG.

These impressive growth rates have been driven by an amazing $100bn in cumulative infrastructure projects spent across Australia since the boom began. A boom that has seen mining become by far the highest paid industry in the nation. However, investors need to know that even greater things are ahead.

Specifically, there is $268bn in approved and commenced projects currently underway – more than 150% greater than the combined value of projects built since the boom began. Indeed, Professor Quentin Graf ton, Chief Economist of the Federal Government’s Bureau of Resources and Energy Economics (‘BREE’) recently told at tendees in September 2012 at the annual Australian National Conference on Resources and Energy that, “Australia is still only about a third of the way ( in value terms) through the investment phase of the boom.”

Char t 11: Infrastructure Projects – Spend to Date vs Future Approved Spending Source: BREE

positive property report2012ISSUE 9

View Positive Properties Now

Page 31

Three phases of the commodities boom

As iron ore and coal prices began decreasing in 2012, the newspapers couldn’t jump on the story quick enough. “The commodities boom is over!” they declared. “The mining boom is done and dusted!”

While it’s true that commodity prices did retract, the reality of the situation is that the commodities boom is anything but over. In fact, it has barely begun. Mainstream media may be peddling fear with their reporting on a fall in Chinese growth, but the facts and figures present a dif ferent story.

While China’s growth is slowing, it is still travelling strongly at 8%, despite troubles in Europe and the US. The reality is that China has become so big that it cannot grow as fast as it may have once done, however this does not mean that it will produce smaller waves. The vast Chinese economy will continue to bring waves of prosperity to Australia for years to come.

Confirms, China’s growth is doing anything but stalling, Federal Treasurer Wayne Swan has said,

“China is now 40% larger than in 2008, so its growth rate can be 20% lower for it to make the same contribution to global GDP growth.”

“We are only par t of the way through the current mining boom, which can be characterised as three overlapping phases: a boom in prices, then investment, and then in exports.”

While Mr Swan says we have passed the peak in prices, the second and third phases still have a way to run.

“In the 2012 June quarter, business investment as a per cent of GDP reached its highest point in 40 years at 17.1%, and we expect it to rise fur ther over the next year or so,” Mr Swan adds.

The Federal Treasurer is not alone in his thinking, with Professor Quentin Graf ton, Chief Economist of the Federal Government’s Bureau of Resources and Energy Economics (‘BREE’) telling at tendees at the 2012 Australian National Conference on Resources and Energy:

• The investment phase began before the 2011 price peak and has yet to reach its maximum.

• Projects that have passed final approvals and final investment decisions currently amount to over $260bn – more than two and a half times that spent since the commodities boom commenced.

Therefore, even if there were to be no new additions to the Major Projects list, Australia is still only about a third of the way ( in value terms) through the investment phase of the boom.

“There’s about $260 billion investments on the books… which indicates there’s a large pipeline of investment underway in Australia,” Professor Graf ton adds.

positive property report2012ISSUE 9

View Positive Properties Now

Page 32

“We’ll expect a very large increase in volume over the next decade, and that volume increase will leave at a higher level than we were before the boom. So in other words, we’ll have prosperity in the context of much higher volumes for some time to come, even though prices will eventually, and already are, moderating.”

And JP Morgan Australia chief economist Stephen Walters says that although “the first phase of the mining boom – the sustained rise in commodity prices that boosted growth in national income – has probably ended, the mining boom in itself is not over”.

He confirms that across the country, “resources firms plan to spend another $120 billion by June 2013”.

Char t 12: Phases of the Australian Mining Boom

Commodity prices have increased by 400% since 2003

Approved infrastructure project spending has risen by 600%

This is going to drive export volumes in 2017 to levels that are 250% higher than when the boom started.

positive property report2012ISSUE 9

View Positive Properties Now

Page 33

The Great Chinese Urbanisation

The global economy is expected to grow by around $50 trillion US dollars by 2025 – essentially meaning the economy will double in size over the next two decades. Across this period, the primary driving force fuelling the global economy will be urbanisation.

Like industrialisation before it, urbanisation is producing a tidal wave of economic growth and driving the booming commodities industry.

positive property report2012ISSUE 9

View Positive Properties Now

Page 34

The global trend of urbanisation is significantly contributing to the increase in demand for resources, while new forces in the global economy – namely China, India, South Korea and Indonesia – are all on a path of development and growth that is seeing their need for steel, coal and LNG soar.

Leading this growth is China, a country that is urbanising so fast, it is forecast to see its economy grow by a breathtaking 150% between 2011 and 2025. That’s triple the growth rate of the United States and the Europe Union according to recent analysis by the world’s largest economics organisation, Global Insight!

The dramatic impact of industrialisation and urbanisation in China is visually best demonstrated by the growth and change of Shanghai, China’s largest and most modern city over the last 20 years.

Char t 13: GDP Change Between 2011 and 2025 (2005 real PPP US$ tr il l ion)

GDP per capita

positive property report2012ISSUE 9

View Positive Properties Now

Page 35

Char t 14: Major Chinese Cit ies

Photo: Shanghai Cit y – 20 years ago and today

According to the United Nations, about 60% of the world’s population will be living in urban centres by 2030, compared to 34% in 1960, and 52% today. Leading the charge is China, which is experiencing mass migration from rural farmlands to urban centres. It’s believed that almost 255 million people will move to China’s urban regions over the next 15 years, stimulating the creation of 37 cities about the size of Per th over the next decade or so. China is also a major player in coal consumption and is experiencing strong demand for energy (thermal coal) and steel production (coking coal).

positive property report2012ISSUE 9

View Positive Properties Now

Page 36

Over the next 20 years, the world’s rural population is forecast to stay constant at around three billion. However, the United Nations’ Department of Economic and Social Af fairs predicts that the number of people living in urban regions will increase significantly.

In fact, it’s expected to increase by around one billion people in just two decades – a whopping 28% increase in the world’s urban (high commodity consuming) population.

Japanese Turning Away from Nuclear to LNG

Japan is also adding to the global demand for resources. In response to the earthquake and tsunami disaster of March 2011 and the subsequent destruction of the Fukushima Daiichi nuclear power plant, Japan shut down its final nuclear reactor in May this year.

The country is now looking to Australia’s LNG and coal assets to fill the energy gap, according to Masayuki Naoshima, vice-president of the Japanese upper house.

“Australia is one of the most important countries for Japan in terms of natural resources supply,” he said. “After the earthquake, our demand for LNG and coal has increased, and our investment in natural resources will increase in the future.”

Char t 15: Global Urbanisation (bill ion people) Source: United Nations (Populat ion Division, Depar tment of Economic and Social Af fairs)

positive property report2012ISSUE 9

View Positive Properties Now

Page 37

While much has been made of the ‘slow down’ of growth in China, Chinese growth has been writ ten-of f time and time again over the last decade. In fact, over the last ten years China has proved consensus economic forecasts wrong nine times out of ten – with Chinese growth far outper forming forecasts.

The reality is that China is much stronger economically than its critics claim and has many times the capacity to stimulate its economy than the US or Europe. Indeed, in September 2012, China launched a US$150bn stimulus program to build infrastructure projects across 18 of its cities. During the GFC, it launched an even larger US$500bn stimulus program that drove commodity demand through the roof.

Unlike US stimulus spending that ends up on Wall Street and the casino speculation of its investment bankers, Chinese stimulus packages actually build ‘real’ things – things that require immense amount of coking coal (for steel making), thermal coal and LNG (both for electricity production).

Char t 16: Chinese GDP Growth Forecasts Source: ABS; CEIC; Consensus Economics; RBA

positive property report2012ISSUE 9

View Positive Properties Now

Page 38

Rising demand for coking and thermal coal

Demand for coking coal to soar 80% by 2025

The urbanisation of China - and other developing countries such as India, South Korea, Malaysia and Indonesia – is creating an immense thirst for coking coal for steel manufacturing and thermal coal for the generation of electricity.

Specifically, the production of steel in China alone is currently nearly equal to the rest of the world combined at a staggering 650Mt per year. With 37 new cities being built in China alone over the next 15 years it is expected that its steel production will reach a mammoth 1.1bn Mt by 2025.

This demand for steel is forecast by the global commodities research and consultancy firm, Wood McKenzie, to translate into a lif t in coking coal imports by 80% from 250Mt per annum in 2011 to nearly 450Mt per annum by 2020.

Char t 17: Global steel production Source: CEIC; World Steel Associat ion

positive property report2012ISSUE 9

View Positive Properties Now

Page 39

Demand for thermal coal also to rise 30% by 2030

Rising energy demand – par ticularly from China – will also see approximately a 30% increase in thermal coal seaborne demand globally according to Wood Mackenzie.

Char t 19: Seaborne thermal coal demand

Char t 18: Annual seaborne coking coal demand (million tonnes) Source: IEA , Macquarie Bank

positive property report2012ISSUE 9

View Positive Properties Now

Page 40

LNG – the world’s new energy source

While the commodity booms in Moranbah and Port Hedland have been driven by coal and iron ore, Gladstone is being super charged by billions of dollars’ worth of infrastructure projects to do with a completely different energy resource.

Global energy usage is rapidly rising, led increasingly by LNG, which is seen as the “cleaner” alternative to coal and a safer option to nuclear power. Indeed, LNG is forecast to represent around 25% of global energy usage by 2030, nearly surpassing coal and oil.

positive property report2012ISSUE 9

View Positive Properties Now

Page 41

LNG exists above coal deposits and is environmentally a much cleaner source of energy than traditional “dir ty” coal. Global demand is soaring and the modest production of LNG in the Bowen Basin will be eclipsed by the Surat Basin, which will then be piped and shipped internationally from Gladstone.

Global energy forecasts have been radically changed since the March 2011 tsunami in Japan, which resulted in the world’s second most serious nuclear reactor incident.

In May 2011, Germany announced it would immediate shut down 8 of its 17 nuclear reactors, with plans to close the remaining 9 sites over the next decade.

In May 2012, Japan backed up the growing anti-nuclear sentiment by announcing that it had shut down the last of its 50 nuclear power plants (although, two have since reopened).

This global shif t has heralded a new era in how the world will be powered, and has seen Asian priced LNG rise to levels more than double that of five years ago.

Char t 20: Share of Global Energy Consumption Source: BP Energy Outlook

Char t 21: Regional Gas Prices Source: Argus Metals L imited, Argus Global, E IA

positive property report2012ISSUE 9

View Positive Properties Now

Page 42

LNG is now seen as replacing nuclear energy in the future, with Japan being the main importer of LNG in the Asian region and China rapidly expanding its imports. The urbanisation of China in par ticular is leading to a significant increase in its demand for energy, as it follows the path of industrialisation the West has travelled.

Char t 22: LNG impor ts in Asia-Pacif ic Region Source: Bureau of Resources and Energy Economics

Char t 23: Per Capita Energy Consumption, Millions Brit ish Thermal Units Per Person Source: IEA , Global Insight, McKinsey analysis

positive property report2012ISSUE 9

View Positive Properties Now

Page 43

Queensland coal production could triple by 2020, with coking coal production to rise 100%

In 2011, saleable exports of coal mined in Queensland (not all coal exported is classed as saleable) totalled 162.5Mt, and was principally comprised of coking coal (116.3Mt) produced in Queensland’s Bowen Basin – with over 83Mt exported out of Gladstone.

According to the Queensland Resources Council, following a modest 50% growth in coal production over the previous eight years, the large scale expansion of mines in the Bowen Basin will see production increase by 100% by 2020.

The construction of a new railway and the opening of several new mines, led by the $7bn flagship Wandoan coal mine by Xstrata, will see a massive increase in thermal coal mining in the Surat Basin (up 100% by 2020). These mines will export from the massive new multi-billion dollar Wiggins Island Coal Terminal being built in Gladstone.

Char t 24: Queensland Coal Production – Mtpa Source: ABS, DEEDI, QRC survey results

Note: P = projections based on QRC survey results

positive property report2012ISSUE 9

View Positive Properties Now

Page 44

300% increase in East Australian LNG production

The impact of the three LNG projects in Gladstone will be to see a tripling of LNG production on the East Coast of Australia, making Gladstone of the largest LNG hubs in the world.

Interest ingly the LNG produced in Gladstone wil l be so called ‘unconvent ional’ gas, meaning that i t is more dif f icult to ex tract – due to i t being sealed in coal deposits located in the Surat Basin to the west of Gladstone.

Char t 25: East Australian LNG Production Source: Santos

Diagram 1: Conventional vs Unconventional Gas

positive property report2012ISSUE 9

View Positive Properties Now

Page 45

Ryan Crawford has been involved in the property investment industry for over 10 years, making the transition from successful investor to real estate professional. Developed in 2008 Crawford Property Group was created to provide an innovative solution to real estate investing in the Pilbara and Australia-wide. With their core focus on positive investment property and wealth creation, Crawford Property Group has fast become the network of choice when choosing to invest in positive property. From the dynamic website to their smart investor list, Crawford Property Group are dedicated to providing the most up to date information and properties in positively geared hotspots Australia-wide. Ryan is a firm believer in the positive power of real estate investing and offers his service and advice as a seasoned investor, with a sizable portfolio in the Pilbara and throughout the state. Ryan is the CEO of the Crawford Property Group.

www.crawfordpropertygroup.com.au

Flynn De Freitas is the Principal of Omega Investments and one of Australia’s leading infrastructure spot ting specialist. He has extensive experience researching and working on major residential subdivisions in Australia’s hot test areas and, as a result, he of fers a unique insider’s perspective on boom town property markets.

Omega Investments focuses on “infrastructure spot ting”, rather than property hot spot ting: that is, investment in high yield, high growth residential properties located in regional boom towns of Australia with a major impending or commenced infrastructure project.

An active and successful residential property investor specialising in infrastructure towns, Flynn is a former investment banker with US-based Merrill Lynch and management consultant for the international consultancy McKinsey & Company. He has also worked extensively in the Australian retail banking industry.

He has also spent four years working for a private property developer, focusing on mining town developments. This experience has helped him develop his extensive knowledge and understanding of towns exposed to the commodities boom.

Biographies

Crawford Property Group

positive property report

2012ISSUE 9

Visit us at: www.crawfordpropertygroup.com.au