Embed Size (px)

Citation preview

Globalization in thefinancial services industry

The pace has been most rapid at thewholesale, bank-to-bank and bank-to-multinational level; at the retailcustomer level, globalization will soonquicken, particularly in Europe.

Christine Pavel and John N. McElravey

Globalization can be definedas the act or state of becomingworldwide in scope or appli-cation. Apart from this geo-graphical application, globali-

zation can also be defined as becoming univer-sal. For the financial services industry, thissecond meaning implies both a harmonizationof rules and a reduction of barriers that willallow for the free flow of capital and permit allfirms to compete in all markets.

This article looks at how global the finan-cial services industry already is, and will likelybecome, by examining the nature and trends ofglobalization in the industry. It will also drawlessons from global nonfinancial industries andfrom recent geographic expansion of bankingfirms within the United States.

Financial globalization is being driven byadvances in data processing and telecommuni-cations, liberalization of restrictions on cross-border capital flows, deregulation of domesticcapital markets, and greater competitionamong these markets for a share of the world'strading volume. It is growing rapidly, butprimarily at the intermediary, rather than thecustomer, level. Its effects are felt at the cus-tomer level mainly because prices and interestrates are influenced by worldwide economicand financial conditions, rather than becausedirect customer access to suppliers has in-creased. However, globalization at the cus-tomer level will soon become apparent, at leastin Europe after 1992, when European Commu-nity banking firms will be allowed to crossnational borders.

Trends in other industries and lessonsfrom interstate banking in the United Statessuggest that as financial globalization pro-gresses, financial services will become moreintegrated, more competitive, and more con-centrated. Also, firms that survive will be-come more efficient, and consumers of finan-cial services will benefit considerably. Recip-rocity is likely to be an important factor forthose countries not already part of a regionalcompact, as it has been for interstate bankingto proceed in the United States.

International commercial banking

The international banking market consistsof the foreign sector of domestic banking mar-kets and the unregulated offshore markets. Ithas undergone important structural changesover the last decade.

Like domestic banking, internationalbanking involves lending and deposit taking.The primary distinction between the two typesof banking lies in their customer bases. Since1982, international lending and deposit takinghave both been growing at roughly 15 percentannually. At year-end 1988, foreign loans andforeign liabilities at the world's banks eachtotalled more than $5 trillion. The extent,nature, and growth of international banking,however, are not the same in all countries.

When she wrote this article, Christine Pavel was anecnomist at the Federal Reserve Bank of Chicago.She is now an assistant vice president at CiticorpNorth America Inc. John N. McElravey is an asso-ciate economist at the Federal Reserve Bank ofChicago.

FEDERAL RESERVE BANK OF CHICAGO

billions of dollars

1,200 —

1987

1981

400

200

0West Switzerland U.K. Luxembourg Hong Singapore Cayman All

Germany Kong Islands other

SOURCE: International Monetary Fund, international Financial Statistics; and various central bank statistical releases.

1,000

800

600

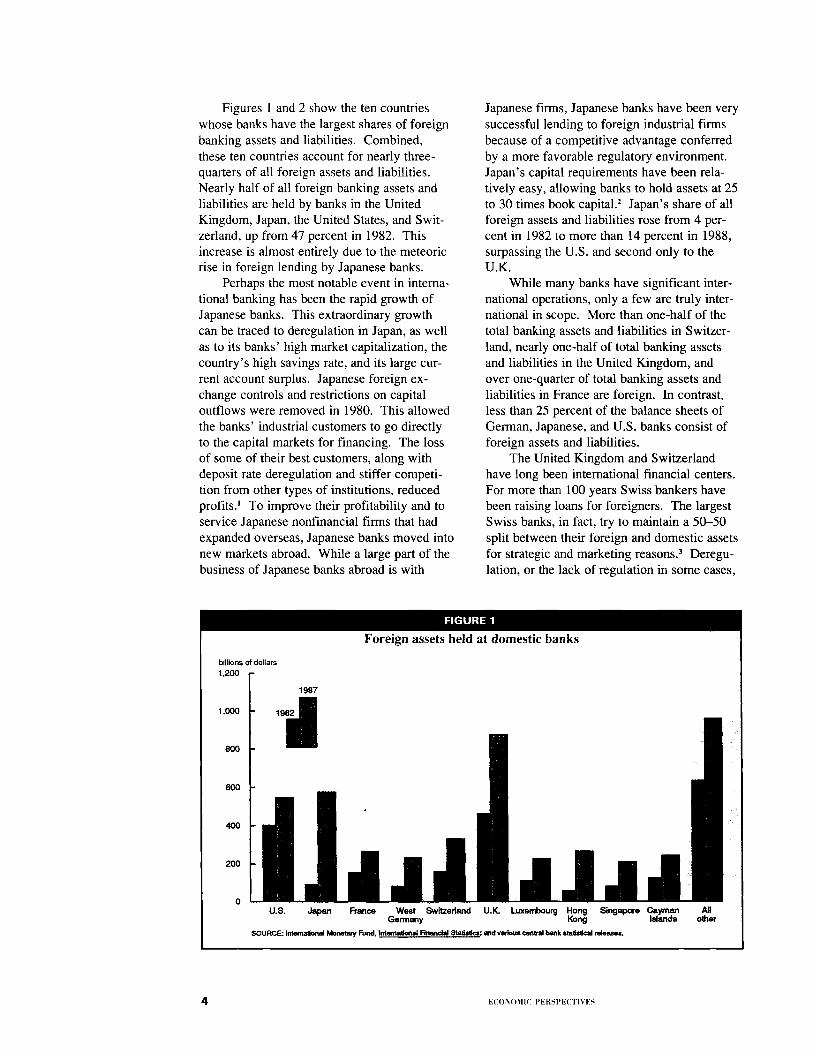

Figures 1 and 2 show the ten countrieswhose banks have the largest shares of foreignbanking assets and liabilities. Combined,these ten countries account for nearly three-quarters of all foreign assets and liabilities.Nearly half of all foreign banking assets andliabilities are held by banks in the UnitedKingdom, Japan, the United States, and Swit-zerland, up from 47 percent in 1982. Thisincrease is almost entirely due to the meteoricrise in foreign lending by Japanese banks.

Perhaps the most notable event in interna-tional banking has been the rapid growth ofJapanese banks. This extraordinary growthcan be traced to deregulation in Japan, as wellas to its banks' high market capitalization, thecountry's high savings rate, and its large cur-rent account surplus. Japanese foreign ex-change controls and restrictions on capitaloutflows were removed in 1980. This allowedthe banks' industrial customers to go directlyto the capital markets for financing. The lossof some of their best customers, along withdeposit rate deregulation and stiffer competi-tion from other types of institutions, reducedprofits.' To improve their profitability and toservice Japanese nonfinancial firms that hadexpanded overseas, Japanese banks moved intonew markets abroad. While a large part of thebusiness of Japanese banks abroad is with

Japanese firms, Japanese banks have been verysuccessful lending to foreign industrial firmsbecause of a competitive advantage conferredby a more favorable regulatory environment.Japan's capital requirements have been rela-tively easy, allowing banks to hold assets at 25to 30 times book capital. 2 Japan's share of allforeign assets and liabilities rose from 4 per-cent in 1982 to more than 14 percent in 1988,surpassing the U.S. and second only to theU.K.

While many banks have significant inter-national operations, only a few are truly inter-national in scope. More than one-half of thetotal banking assets and liabilities in Switzer-land, nearly one-half of total banking assetsand liabilities in the United Kingdom, andover one-quarter of total banking assets andliabilities in France are foreign. In contrast,less than 25 percent of the balance sheets ofGerman, Japanese, and U.S. banks consist offoreign assets and liabilities.

The United Kingdom and Switzerlandhave long been international financial centers.For more than 100 years Swiss bankers havebeen raising loans for foreigners. The largestSwiss banks, in fact, try to maintain a 50-50split between their foreign and domestic assetsfor strategic and marketing reasons.' Deregu-lation, or the lack of regulation in some cases,

FIGURE 1

Foreign assets held at domestic banks

4

ECONOMIC PERSPECTIVES

billions of dollars1,200 —

1987

1,000

800

600

400

200

0

1982

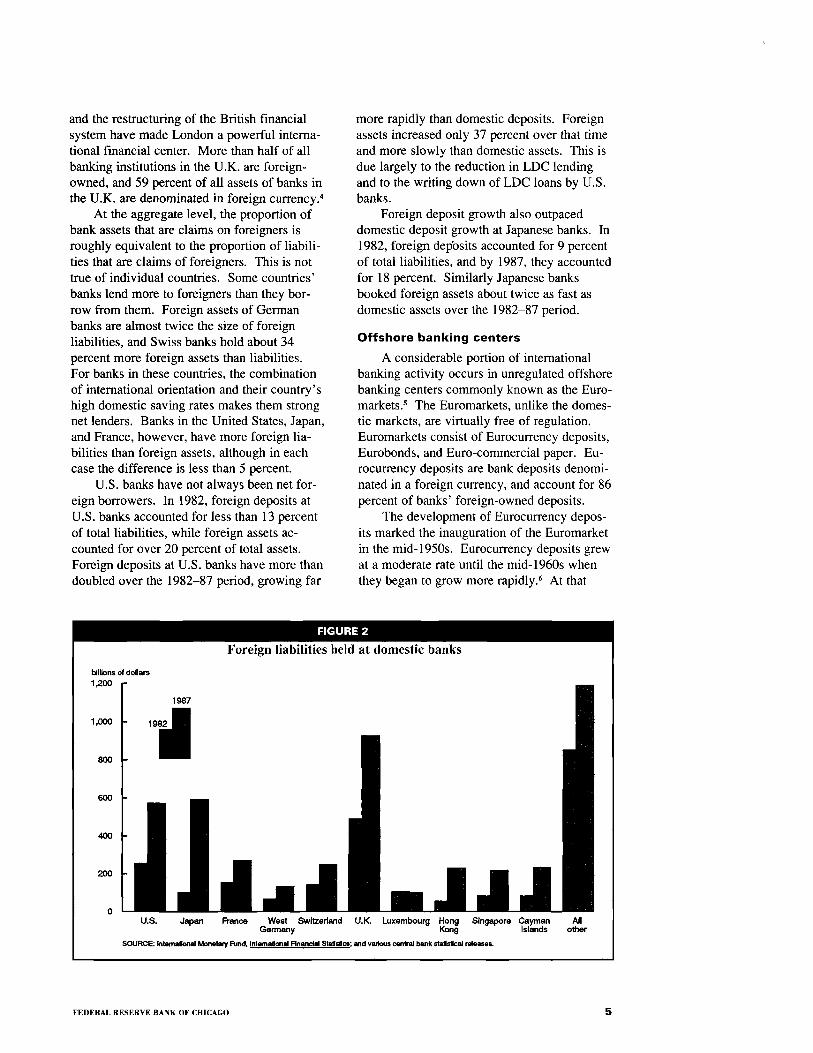

and the restructuring of the British financialsystem have made London a powerful interna-tional financial center. More than half of allbanking institutions in the U.K. are foreign-owned, and 59 percent of all assets of banks inthe U.K. are denominated in foreign currency.°

At the aggregate level, the proportion ofbank assets that are claims on foreigners isroughly equivalent to the proportion of liabili-ties that are claims of foreigners. This is nottrue of individual countries. Some countries'banks lend more to foreigners than they bor-row from them. Foreign assets of Germanbanks are almost twice the size of foreignliabilities, and Swiss banks hold about 34percent more foreign assets than liabilities.For banks in these countries, the combinationof international orientation and their country'shigh domestic saving rates makes them strongnet lenders. Banks in the United States, Japan,and France, however, have more foreign lia-bilities than foreign assets, although in eachcase the difference is less than 5 percent.

U.S. banks have not always been net for-eign borrowers. In 1982, foreign deposits atU.S. banks accounted for less than 13 percentof total liabilities, while foreign assets ac-counted for over 20 percent of total assets.Foreign deposits at U.S. banks have more thandoubled over the 1982-87 period, growing far

more rapidly than domestic deposits. Foreignassets increased only 37 percent over that timeand more slowly than domestic assets. This isdue largely to the reduction in LDC lendingand to the writing down of LDC loans by U.S.banks.

Foreign deposit growth also outpaceddomestic deposit growth at Japanese banks. In1982, foreign deposits accounted for 9 percentof total liabilities, and by 1987, they accountedfor 18 percent. Similarly Japanese banksbooked foreign assets about twice as fast asdomestic assets over the 1982-87 period.

Offshore banking centers

A considerable portion of internationalbanking activity occurs in unregulated offshorebanking centers commonly known as the Euro-markets. 5 The Euromarkets, unlike the domes-tic markets, are virtually free of regulation.Euromarkets consist of Eurocurrency deposits,Eurobonds, and Euro-commercial paper. Eu-rocurrency deposits are bank deposits denomi-nated in a foreign currency, and account for 86percent of banks' foreign-owned deposits.

The development of Eurocurrency depos-its marked the inauguration of the Euromarketin the mid-1950s. Eurocurrency deposits grewat a moderate rate until the mid-1960s whenthey began to grow more rapidly. 6 At that

FIGURE 2

Foreign liabilities held at domestic banks

U.S. Japan France West Switzerland U.K. Luxembourg Hong Singapore CaymanGermany Kong Islands

SOURCE: International Monetary Fund, International Financial Statistics; and various central bank statistical releases.

Allother

FEDERAL RESERVE BANK OF CHICAGO

5

FIGURE 3

Eurocurrency deposits

Eurodollar share(right scale)

4

3

0

time, the U.S. government imposed severecontrols on the movement of capital, which"deflected a substantial amount of borrowingdemand to the young Eurodollar market.'"These U.S. capital controls were dismantled in1974, but the oil crisis of the 1970s helped tofuel the continued growth of the Eurocurrencymarket. The U.S. oil embargo made oil-ex-porting countries fearful of placing their fundsin domestic branches of U.S. banks. In thelate 1970s and early 1980s, high interest ratesbolstered the growth of Eurocurrency deposits,which are free of interest-rate ceilings and notsubject to reserve requirements or depositinsurance premiums. From 1975 to 1980,Eurocurrency deposits grew over threefold.

Since 1980, Eurocurrency deposits havecontinued to grow quite rapidly, reaching agross value of $4.5 trillion outstanding in 1987and a net value of nearly $2.6 trillion (net ofinterbank claims). Eurodollar deposits, how-ever, have not grown as rapidly. During theearly 1980s, Eurodollars represented over 80percent of all Eurocurrency deposits outstand-ing, but by 1987, they represented only 66percent (see Figure 3). The declining impor-tance of Eurodollar deposits can be explained,at least partially, by the decline in the cost ofholding noninterest-bearing reserves againstdomestic deposits in the United States. 8

Many Eurocenters have developedthroughout the world. They have developedwhere local governments allow them to thrive,i.e., where regulation is favorable to offshore

markets. Consequently, some countries withrelatively small domestic financial markets,such as the Bahamas, have become importantEurocenters. Similarly, some countries withmajor domestic financial markets have no orvery small offshore markets. In the UnitedStates, for example, the offshore market wasprohibited until 1981 when International Bank-ing Facilities (IBFs) were authorized.

Japan did not permit an offshore market todevelop until late in 1986. Until then the"Asian dollar" market consisted primarily ofthe Eurocenters of Singapore, Bahrain, andHong Kong. Now Japan's offshore market isabout $400 billion in size, over twice as largeas the U.S. offshore market, but still smallerthan that in the United Kingdom.'

The interbank market

The international lending activities ofmost banks, aside from the money centers, areconcentrated heavily in the area of providing avariety of credit facilities to banks in othercountries. Consequently, a large proportion ofbanks' foreign assets and liabilities are claimson or claims of foreign banks. Eighty percentof all foreign assets are claims on otherbanks.'° This ratio varies somewhat by coun-try; however, since 1982, it has been increas-ing for all the major industrialized countries.

Similarly, nearly 80 percent of all banks'foreign liabilities are claims of other banks."In Japan, 99 percent of all foreign liabilities atbanks are deposits of foreign banks. Swissbanks are the exception, where only 28 percentof foreign liabilities are claims of banks.

The Swiss have a long history of provid-ing banking services directly to foreign corpo-rate and individual customers, which explainstheir relatively low proportion of interbankclaims. A favorable legal and regulatory cli-mate aided the development of a system thatcaters to foreigners, especially those wishingto shelter income from taxes. Confidentialityis recognized as a right of the bank customer,and stiff penalties can be imposed on bankofficials who violate that right. In effect, noinformation about a client can be given to anythird party."

Since a very large portion of foreign de-posits are Eurocurrency deposits, it is no sur-prise that about half of all Eurocurrency de-posits are interbank claims. Eurocurrency

6

ECONOMIC PERSPECTIVES

deposits are frequently re-lent to other, oftensmaller, banks in the interbank market. 13

The Japanese have become very largeborrowers in the interbank market in responseto domestic restrictions on prices and volumesof certain activities. Japanese banks operatingoverseas have been funding their activities byborrowing domestically (from nonresidents) inone market (e.g., the U.K.), and lending thefunds through the interbank market to affiliatesin other countries (e.g., the U.S.). 14

Foreign exchange trading

Foreign exchange (forex) trading is an-other important international banking activity.Informal estimates place daily foreign ex-change trading at $400 billion.° Like the loanmarkets, forex markets are primarily interbankmarkets. The primary players involved in theUnited States are the large money center andregional commercial banks, Edge Act corpora-tions, and U.S. branches and agencies of for-eign banks. Forex trading also involves somelarge nonbank financial firms, primarily largeinvestment banks and foreign exchange bro-kers. However, according to the Federal Re-serve Bank of New York's U.S. Foreign Ex-change Market Survey for April 1989, 82 per-cent of the forex trading volume of banks waswith other banks. Foreign exchange trading inNew York grew at about 40 percent annuallysince 1986 to reach more than $130 billion byApril 1989. In contrast, foreign trade (importsplus exports) has been growing at only about 6percent annually since 1982 (3 percent on aninflation-adjusted basis).

The German mark is the most activelytraded currency, followed by the Japanese yen,British pound, Swiss franc, and Canadiandollar. Since 1986, however, the Germanmark has lost some ground to the Japanese yenand the Swiss franc."

The explosion of forex trading can, atleast partly, be explained by the high rate ofgrowth in cross-border financial transactions.Capital and foreign exchange controls werereduced or eliminated in a number of countriesduring the 1980s.

An international banking presence

There are several ways that commercialbanks engage in international bankingactivities—through representative offices,agencies, foreign branches, and foreign sub-

sidiary banks and affiliates. In addition, in theUnited States, commercial banks may operateInternational Banking Facilities (IBFs) andEdge Act corporations, which unlike the othermeans, do not involve a physical presenceabroad. The primary difference among thesetypes of foreign offices centers on how cus-tomer needs are met (often because of regula-tion). For example, agencies of foreign banksare essentially branches that cannot acceptdeposits from the general public, whilebranches, as well as subsidiary banks, canoffer a full range of banking services.

U.S. branches and agencies of foreignbanks devote well over half of their assets toloans, about the same proportion as the domes-tic offices of U.S. commercial banks. U.S.commercial banks, however, hold a muchlarger proportion of their assets in securitiesand a much smaller proportion in customer'sliability on acceptances!' This latter situationreflects the international trade financings ofU.S. foreign offices.

U.S. offices of foreign banks competewith domestic banks primarily in commerciallending and, to a lesser extent, in real estatelending.° However, a significant portion ofthe commercial loans held at U.S. offices offoreign banks were purchased from U.S.banks, rather than originated by the foreignoffices themselves.°

Both U.S. offices of foreign banks anddomestic offices of U.S. commercial banksprimarily fund their operations with depositsof individuals, partnerships and corporations(IPC).20 Offices of foreign banks currentlygather 23 percent of these deposits from for-eigners, and nearly all of these deposits are ofthe nontransaction type.

The presence of foreign banks in theUnited States has been increasing. The ratioof foreign offices to domestic offices in theUnited States has increased from 2.8 percent in1981 to 4.4 percent in 1987. Similarly, theratio of assets of foreign banking offices in theUnited States to assets of U.S. domestic bankshas increased over 5 percentage points since1981 to nearly 21 percent in 1987. 21

The presence of U.S. banks abroad, how-ever, has been falling since 1985. At thattime, U.S. banks operated nearly 1,000 foreignbranches. 22 Similarly, the number of U.S.banks with foreign branches peaked at 163 in1982 and began to fall in 1986. By 1988, the

FEDERAL RESERVE BANK OF CHICAGO 7

number of banks with foreign branches hadfallen to 147. On an inflation-adjusted basis,total assets of foreign branches of U.S. banksfell 12 percent since 1983 to $506 billion in1988. The number of IBFs and Edge ActCorporations has also been waning. Edge Actsnumbered 146 in 1984 and were down to 112by 1988. 23 This retrenchment reflects thelessening attractiveness of foreign operationsas losses on LDC loans have mounted.

Implications of Europe after 1992

The presence of foreign banking firms inEuropean domestic markets will likely in-crease over the next few years as the 12 Euro-pean Community states become, at least eco-nomically, a "United States of Europe." TheEC plans to issue a single license that willallow banks to expand their networks through-out the Community, governed by their homecountry's regulations. 24

Since banking powers will be determinedby the rules of the home country, banks fromcountries with more liberal banking laws oper-ating in countries with more restrictive bank-ing laws will have an advantage over theirdomestic competitors. Consequently, the mostefficient form of banking will prevail. Coun-tries with more fragmented banking systemswill need to liberalize for their banks to com-pete with banks from countries with universalbanking.

While reciprocity will not be importantfor nations within the EC, it will be an issuefor banks from countries outside the EC, espe-cially those from Japan and the U.S. As finan-cial services companies in Europe begin tooperate with fewer restrictions, there will becompetitive pressure on the U.S. and Japan toremove the barriers between commercial andinvestment banking. To be most efficient,firms operating in various markets want simi-lar powers in each market. The EC, as previ-ously noted, solved this problem with a Com-munity banking license. Thus, the EC's ef-forts at regulatory harmonization may hastenthe demise of Glass-Steagall in the U.S. andArticle 65 in Japan. 25

The implications for European bankingwill be similar to the experience in the UnitedStates following the introduction of interstatebanking in the early to mid-1980s. Since thattime, the U.S. commercial banking industryhas been consolidating on nationwide, re-

gional, and statewide bases through mergersand acquisitions. Acquiring firms tend to belarge, profitable organizations with expertisein operating geographically dispersed net-works, while targets tend to be smaller, al-though still relatively large firms, in attractivebanking markets. Large, poorly-capitalizedfirms will also find themselves to be potentialtakeover targets.

What these lessons imply for Europe in1992 is that the largest and strongest organiza-tions with the managerial talent to operate ageographically dispersed organization willbecome Europe-wide firms, while smallerfirms will have a more regional focus andothers will survive as niche players. In addi-tion, just as different state laws have slowedthe process of nationwide banking in theUnited States, language and cultural barrierswill slow the process in Europe as well. Theoverall result of a more globally integratedfinancial sector in Europe, and elsewhere, willbe that the organizations that survive will bemore efficient, and customers will be betterserved. Also, it is very likely that the 1992experience will improve European banks'ability to compete outside of Europe.

Size is not, and will not be, a sufficientingredient for survival. In general, firms inprotected industries, such as airlines, tend tobe inefficient. Large banking organizationsbased in states with restrictive branching andmultibank holding company laws tended to beless efficient than their peers in states thatallow branches and, therefore, more competi-tion. In addition, commercial banking organi-zations that operated in unit banking states hadlittle expertise in operating a decentralizedorganization, and tended to focus primarily onlarge commercial customers. Consequently,these banking firms have not acquired banksfar from home.

The process of consolidation has alreadybegun within European countries and withinEurope as firms prepare for a single Europeanbanking market. Unlike the Unites States'experience of outright mergers and acquisi-tions, however, the European experience cen-ters on forming "partnerships." Partnershipshave been formed Europe-wide, even thoughthe most recent directive on commercial bank-ing permits branching, because of the difficul-ties in managing an organization that spans

8

CONOMIC PERSPECTIVES

several cultures and languages. Apparently,financial services firms want to get their feetwet first, rather than plunge into Europeanbanking and risk drowning before 1992 ar-rives. But also, until regulations among coun-tries become more uniform, partnerships andjoint ventures allow financial firms to arbi-trage regulations.

The formation of partnerships and jointventures is not only a European phenomenon.Indeed, U.S. firms have entered into suchagreements with European and Japanese com-panies. For example, Wells Fargo and NikkoSecurities have formed a joint venture to oper-ate a global investment management firm, andMerrill Lynch and Societe Generale are dis-cussing a partnership to develop a Frenchasset-backed securities market.

The experience of nonfinancial firmssuggests that this arrangement can be a goodway to establish an international presence. Forexample, in 1984, Toyota and General Motorsentered into a joint manufacturing venture inCalifornia. Through this venture, the Japanesewere able to acquaint themselves with Ameri-can workers and suppliers before opening theirown plants in the U.S. Since then, Toyota hasopened two more manufacturing plants on itsown in North America, and there is specula-tion in the auto industry that they will buyGM's share of the joint venture once theagreement ends in 1996. 26

Another case of international expansionthrough joint ventures can be found in thepetroleum industry. Oil companies from someoil-producing countries have been quite activein recent years buying stakes in refining andmarketing operations in the United States andEurope. These acquisitions give producers anoutlet for their crude in important retail mar-kets, and refiners get a reliable source. SaudiArabia purchased a 50 percent stake in Tex-aco's eastern and Gulf Coast refining andmarketing operations in November 1988. Thestate-owned oil companies from Kuwait andVenezuela have joint ventures with Europeanoil companies as well.27 If joint ventures be-tween financial services firms are as successfulas nonfinancial ones have been, then globalfinancial integration will benefit.

International securities markets

International securities include securitiesthat are issued outside the issuer's home coun-

try. Some of these securities trade on foreignexchanges. Issuance and trading of interna-tional securities have grown considerably since1986, as has the amount of such securitiesoutstanding.

Greater demand for international financ-ing is stimulating important changes in finan-cial markets, especially in Europe. Regula-tions and procedures designed to shield domes-tic markets from foreign competition aregradually being dismantled. London's posi-tion as an international market was strength-ened by the lack of sophistication of manyother European markets. Greater demand forequity financing in Europe has been encour-aged by private companies, and by govern-ments privatizing large public-sector corpora-tions. These measures to deregulate and,therefore, improve the efficiency, regulatoryorganizations, and settlement procedures are aresponse to competition from other markets,and the explosion of securities trading in the1980s. 29

It is estimated that the world bond marketsat the end of 1988 consisted of about $9.8trillion of publicly issued bonds outstanding, anearly $2 trillion increase since 1986. 29 Atyear-end 1988, two-thirds of all bonds out-standing were obligations of central govern-ments, their agencies, and state and local gov-ernments. This figure varies considerablyacross countries. Over two-thirds of bondsdenominated in the U.S. dollar and the Japa-nese yen are government obligations, but lessthan one-third of bonds denominated in theGerman mark are government obligations, andonly 10 percent of bonds denominated in theSwiss franc represent government debt."

The international bond market includesforeign bonds, Eurobonds, and Euro-commer-cial paper. Foreign bonds are bonds issued ina foreign country and denominated in thatcountry's currency. Eurobonds are long-termbonds issued and sold outside the country ofthe currency in which they are denominated.Similarly, Euro-commercial paper is a short-term debt instrument that is issued and soldoutside the country of the currency in which itis denominated.

The Japanese are the biggest issuers ofEurobonds because it is easier and cheaperthan issuing corporate bonds in Japan. Japa-nese companies issued 21 percent of all Eu-

FEDERAL RESERVE BANK OF CHICAGO 9

Total publicly issued

Total international bonds

UK French Canadian -

sterling franc dollar

robonds in 1988. 3 ' Ministry of Finance (MOF)regulations and the underwriting oligopoly ofthe four largest Japanese securities firms keepthe issuance cost in the domestic bond markethigher than in the Euromarket. The ministrywould like to bring this bond market activityback to Japan, so it has been slowly liberaliz-ing the rules for issuing yen bonds and samuraibonds (yen bonds issued by foreigners in Ja-pan). So far, the impact of these changes hasbeen small. 32

International bonds accounted for almost10 percent of bonds outstanding at the end of1988 and over three-quarters are denominatedin the U.S. dollar, Japanese yen, German markand U.K. sterling (see Figure 4). These coun-tries represent four of the largest economiesand financial markets in the world.

The importance of international bondmarkets has increased considerably for manycountries. As Table 1 shows, internationalbonds account for nearly half of all bondsdenominated in the Swiss franc and over one-third of all bonds denominated in the Austra-lian dollar. International bonds account forover 21 percent of bonds denominated in theBritish pound, up dramatically from less than 1percent in 1980. The rise in importance ofinternational bonds for these currencies can, at

least in part, be explained by the budget sur-pluses in the countries in which these curren-cies are denominated and, therefore, theslower growth in the debt obligations of thesecountries' governments.

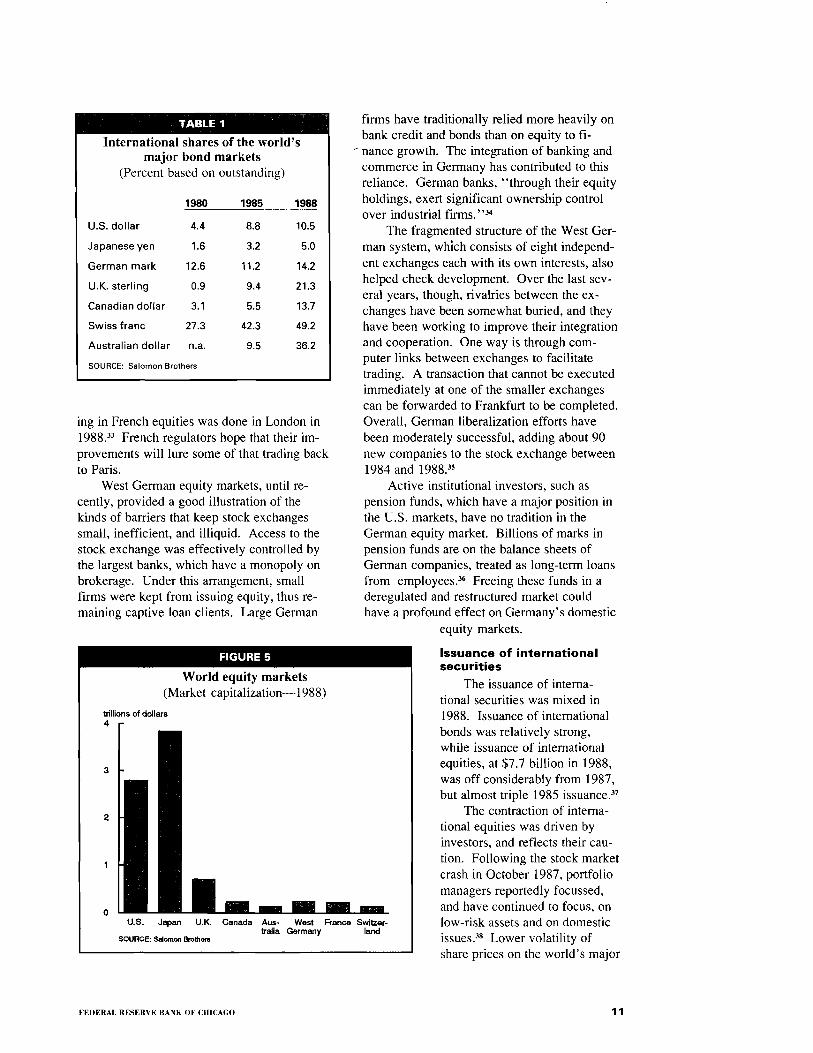

The value of world equity markets, at $9.6trillion in 1988, is about equal to the value ofworld bond markets. Three countries—theUnited States, Japan, and the UnitedKingdom—account for three quarters of thetotal capitalization on world equity markets,and they account for nearly half of the 15,000equity issues listed on the world's stock ex-changes (see Figure 5).

American, Japanese, and British equitymarkets are the largest and most active.American and British markets are very open toforeign investors, but significant barriers toforeign competitors still exist in Japan.

Stocks have, historically, played a rela-tively minor role in corporate financing inmany European countries. Various regulatoryand traditional barriers to entry made thesebourses financial backwaters. The stock ex-changes in Switzerland, West Germany,France, and Italy have only recently takensteps to modernize in order to compete againstexchanges in the U.S. and the U.K. It wasestimated that about 20 percent of daily trad-

Market shares o otal publicly issued bonds: year-end 1988(Based on outstanding)

SOURCE: Salomon Brothers

1 0

ECONOMIC PERSPECTIVES

TABLE 1

International shares of the world'smajor bond markets

(Percent based on outstanding)

1980 1985 1988

U.S. dollar 4.4 8.8 10.5

Japanese yen 1.6 3.2 5.0

German mark 12.6 11.2 14.2

U.K. sterling 0.9 9.4 21.3

Canadian dollar 3.1 5.5 13.7

Swiss franc 27.3 42.3 49.2

Australian dollar n.a. 9.5 36.2

SOURCE: Salomon Brothers

FIGURE 5

World equity markets(Market capitalization-1988)

U.S. Japan U.K. Canada Aus- West France Switzer-tralia Germany land

SOURCE: Salomon Brothers

ing in French equities was done in London in1988. 33 French regulators hope that their im-provements will lure some of that trading backto Paris.

West German equity markets, until re-cently, provided a good illustration of thekinds of barriers that keep stock exchangessmall, inefficient, and illiquid. Access to thestock exchange was effectively controlled bythe largest banks, which have a monopoly onbrokerage. Under this arrangement, smallfirms were kept from issuing equity, thus re-maining captive loan clients. Large German

firms have traditionally relied more heavily onbank credit and bonds than on equity to fi-nance growth. The integration of banking andcommerce in Germany has contributed to thisreliance. German banks, "through their equityholdings, exert significant ownership controlover industrial firms.' '34

The fragmented structure of the West Ger-man system, which consists of eight independ-ent exchanges each with its own interests, alsohelped check development. Over the last sev-eral years, though, rivalries between the ex-changes have been somewhat buried, and theyhave been working to improve their integrationand cooperation. One way is through com-puter links between exchanges to facilitatetrading. A transaction that cannot be executedimmediately at one of the smaller exchangescan be forwarded to Frankfurt to be completed.Overall, German liberalization efforts havebeen moderately successful, adding about 90new companies to the stock exchange between1984 and 1988."

Active institutional investors, such aspension funds, which have a major position inthe U.S. markets, have no tradition in theGerman equity market. Billions of marks inpension funds are on the balance sheets ofGerman companies, treated as long-term loansfrom employees. 36 Freeing these funds in aderegulated and restructured market couldhave a profound effect on Germany's domestic

equity markets.

Issuance of internationalsecurities

The issuance of interna-tional securities was mixed in1988. Issuance of internationalbonds was relatively strong,while issuance of internationalequities, at $7.7 billion in 1988,was off considerably from 1987,but almost triple 1985 issuance. 37

The contraction of interna-tional equities was driven byinvestors, and reflects their cau-tion. Following the stock marketcrash in October 1987, portfoliomanagers reportedly focussed,and have continued to focus, onlow-risk assets and on domesticissues." Lower volatility ofshare prices on the world's major

FEDERAL RESERVE BANK OF CHICAGO

1 1

exchanges, however, would likely aid a re-bound in the appetite for and in the issuance ofinternational equities.

Some important structural changes tookplace in international financial markets be-tween 1985 and 1987. A sharp increase in is-suance for the U.K. translated into substan-tially greater market share of internationalequity issuance, from 3.7 percent in 1985 to33.0 percent in 1987. This increased share ofinternational activity reflects the deregulationand restructuring of the London markets thatoccurred in the fall of 1986, improving theirplace as an international marketplace for secu-rities. Even with the retrenchment in 1988,London maintained its leading role, with twicethe issuance of second-place U.S. 39

Over this same three-year period, Switzer-land's international equity issuance translatedinto a substantially smaller market share, fall-ing from 40.7 percent to 6.0 percent. Thissharp decline in market share, from undisputedleader to fourth, reveals Switzerland's failureto keep pace with deregulation in other coun-tries. For years, a cartel system dominated byits three big banks has set prices and practicesin the stock markets. It is only recently thatcompetition from markets abroad has forcedthe cartel to liberalize its system.40

In contrast to the international equitiesmarkets, issuance of international bonds wasvery strong in 1988, following a sharp contrac-tion in 1987 entirely due to a 25.5 percentdecline in Eurobond issuance.41 Eurobondsaccount for about 80 percent of internationalbond issues, and nearly two-thirds of all inter-national issues are denominated in threecurrencies—the U.S. dollar, Swiss franc, andthe Deutschemark. Nearly 60 percent of inter-national bonds are issued by borrowers inJapan, the United Kingdom, the United States,France, Canada, and Germany.

The long-time importance of the UnitedStates and the U.S. dollar in the internationalbond market has been dwindling. In 1985, 54percent of all Eurobonds were denominated inU.S. dollars, but by 1988 only 42 percent werein U.S. dollars.

Similarly, U.S. borrowers issued 24 per-cent of all international bonds in 1985, butissued only 8 percent in 1988. The impetusbehind this decline lies in part with the inves-tors who prefer low-risk securities and are

leery of U.S. bonds because of the perceivedincrease in "event risk" associated withrestructurings and leveraged buyouts. Also, nodoubt, developments such as the adoption ofRule 415 by the Securities and ExchangeCommission (shelf registration) have encour-aged U.S. firms to issue domestic securities bymaking it less costly to do so.

Trading in international securities

The United States is a major center ofinternational securities trading. Foreign trans-actions in U.S. markets exceed U.S. transac-tions in foreign markets by a ratio of almost 7to 1. This is a result of several factors. TheUnited States has the largest and most devel-oped securities markets in the world. U.S.equity markets are virtually free of controls onforeign involvement. SEC regulations ondisclosure dissipate much uncertainty concern-ing the issuers of publicly listed securities inthe United States while less, or inadequate,regulation in other countries makes invest-ments more risky in those foreign markets.The market for U.S. Treasury securities hasalso been very attractive to foreign investors.In fact, large purchases of these securities bythe Japanese have helped finance the U.S.government budget deficit.

Both foreign transactions in U.S. marketsand U.S. transactions in foreign markets havebeen increasing at a very rapid pace. Foreigntransactions in U.S. equity securities in U.S.markets plus such transactions in foreign equi-ties in U.S. markets grew at almost 50 percentannually to exceed $670 billion in 1987. 42

Foreign transactions in U.S. stocks on U.S.equity markets have been increasing fasterthan domestic transactions; in 1988, foreigntransactions accounted for 13 percent of thevalue of transactions on U.S. markets, up from10 percent in 1986 (see Table 2).

Foreign transactions have increased insecurities markets abroad as well; however,they have not, in general, kept pace with do-mestic trading. Consequently, foreign transac-tions as a percentage of all transactions hasdeclined over the 1986-88 period for Japan,Canada, Germany, and the United Kingdom.Nevertheless, transactions by U.S. residents inforeign equity markets were estimated at about$188 billion in 1987, nearly 12 times as muchas in 1982. 43

12

ECO:NOMIC PERSPECTIVES

TABLE 2

Foreign transactions in domestic equitymarkets: Share of domestic trading

(Percent of total volume)

1985 1988

Japan 8.7 6.5

Canada 29.5 21.6

Germany 29.9 8.7

U.S. 9.7 13.1

U.K. 37.3 20.8

France 38.0 43.5

Switzerland 4.6 6.3

SOURCE: Salomon Brothers

FIGURE 6

Foreign transactions in U.S. bond marketstrillions of dollars

1982 1983 1984 1985 1986 1987SOURCE: Board of Governors of the Federal Reserve System andU.S. Department of the Treasury

1988

4 -

U.S. corporate securities

3 - Foreign corporate securities

U.S. Treasury securities

2

0

Foreign transactions in U.S. bonds andforeign bonds in U.S. markets in 1988 in-creased to more than 13 times their 1982 level(see Figure 6). This trading boom was fueledmainly by growth in transactions for U.S.Treasury bonds, which accounted for about 84percent of total foreign bond transactions in1988, up from 63 percent in 1982. Thesetransactions in U.S. Treasury bonds accountedfor almost three-quarters of all foreign securi-ties transactions in U.S. markets in 1988.

Bond transactions in other countries bynonresidents also increased dramatically. InGermany, for example, the value of such trans-actions increased by 300 percent over the

1985-88 period and now account for over halfof the value of all transactions in German bondmarkets." Foreign bond transactions by U.S.residents reached an estimated $380 billion in1987, six times greater than the 1982 figure.

Derivative products

Globalization has affected derivativefinancial products in two ways. First, it hasspurred the creation and rapid growth of inter-nationally-related financial products, such asEurodollar futures and options and foreigncurrency futures and options as well as futuresand options on domestic securities that tradeglobally, such as U.S. Treasury securities.Trading hours on some U.S. futures and op-tions exchanges have been expanded to sup-port cross-border trading of underlying assets,such as Treasury securities. Second, globali-zation has lead to the establishment of futuresand options exchanges worldwide. Once theexclusive domain of U.S. markets, especiallyin Chicago, financial derivative products arenow traded in significant volumes throughoutEurope and Asia.

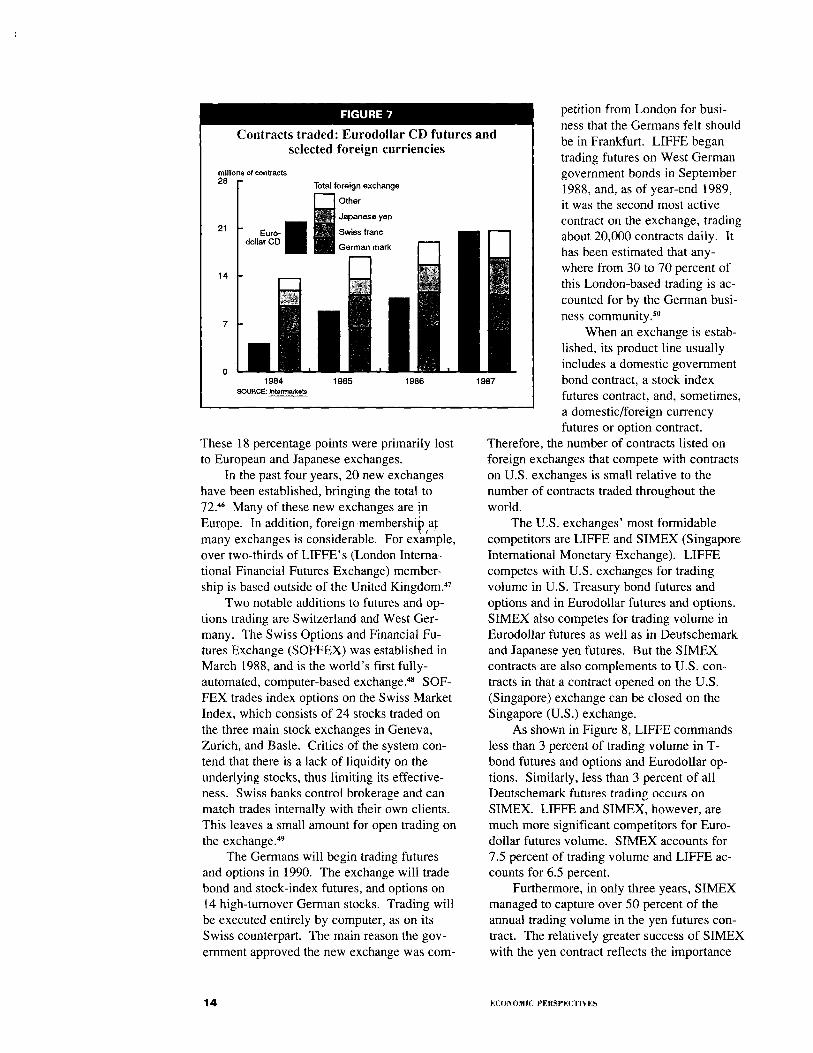

The number of futures contracts on Euro-dollar CDs and on foreign currencies as wellas the number of open positions has increasedrapidly (see Figure 7). The number of futurescontracts on Eurodollar CDs traded worldwideincreased almost 70 percent annually since1983 to reach over 25 million in 1988. Thiscompares with a 20 to 25 percent annual

growth rate for Eurodollars."Similarly, nearly 40 million fu-tures and options contracts onvarious foreign currencies weretraded worldwide in 1988, upfrom 14 million in 1983. Thisgrowth rate is roughly equivalentto that of forex trading.

The rapid increase in thevolume of trading of internation-ally-linked futures and optionscontracts has largely benefitedU.S. exchanges, which are thelargest and sometimes the onlyexchanges where such productsare traded. Nevertheless, theshare of exchange traded futuresand options volume commandedby the U.S. exchanges hasdropped from 98 percent in 1983to about 80 percent in 1988.

FEDERAL RESERVE BANK OF CHICAGO

13

FIGURE 7

Contracts traded: Eurodollar CD futures andselected foreign curriencies

Euro-dollar II CD

21

14

1984SOURCE: Intermark.Is

millions of contracts28 Total foreign exchange

Other11111 Japanese yenlaN Swiss franc

I . I

German mark

7

01985 1986 1987

These 18 percentage points were primarily lostto European and Japanese exchanges.

In the past four years, 20 new exchangeshave been established, bringing the total tor .46z Many of these new exchanges are inEurope. In addition, foreign membership atmany exchanges is considerable. For example,over two-thirds of LIFFE' s (London Interna-tional Financial Futures Exchange) member-ship is based outside of the United Kingdom.'"

Two notable additions to futures and op-tions trading are Switzerland and West Ger-many. The Swiss Options and Financial Fu-tures Exchange (SOFFEX) was established inMarch 1988, and is the world's first fully-automated, computer-based exchange." SOF-FEX trades index options on the Swiss MarketIndex, which consists of 24 stocks traded onthe three main stock exchanges in Geneva,Zurich, and Basle. Critics of the system con-tend that there is a lack of liquidity on theunderlying stocks, thus limiting its effective-ness. Swiss banks control brokerage and canmatch trades internally with their own clients.This leaves a small amount for open trading onthe exchange."

The Germans will begin trading futuresand options in 1990. The exchange will tradebond and stock-index futures, and options on14 high-turnover German stocks. Trading willbe executed entirely by computer, as on itsSwiss counterpart. The main reason the gov-ernment approved the new exchange was corn-

petition from London for busi-ness that the Germans felt shouldbe in Frankfurt. LIFFE begantrading futures on West Germangovernment bonds in September1988, and, as of year-end 1989,it was the second most activecontract on the exchange, tradingabout 20,000 contracts daily. Ithas been estimated that any-where from 30 to 70 percent ofthis London-based trading is ac-counted for by the German busi-ness community."

When an exchange is estab-lished, its product line usuallyincludes a domestic governmentbond contract, a stock indexfutures contract, and, sometimes,a domestic/foreign currencyfutures or option contract.

Therefore, the number of contracts listed onforeign exchanges that compete with contractson U.S. exchanges is small relative to thenumber of contracts traded throughout theworld.

The U.S. exchanges' most formidablecompetitors are LIFFE and SIMEX (SingaporeInternational Monetary Exchange). LIFFEcompetes with U.S. exchanges for tradingvolume in U.S. Treasury bond futures andoptions and in Eurodollar futures and options.SIMEX also competes for trading volume inEurodollar futures as well as in Deutschemarkand Japanese yen futures. But the SIMEXcontracts are also complements to U.S. con-tracts in that a contract opened on the U.S.(Singapore) exchange can be closed on theSingapore (U.S.) exchange.

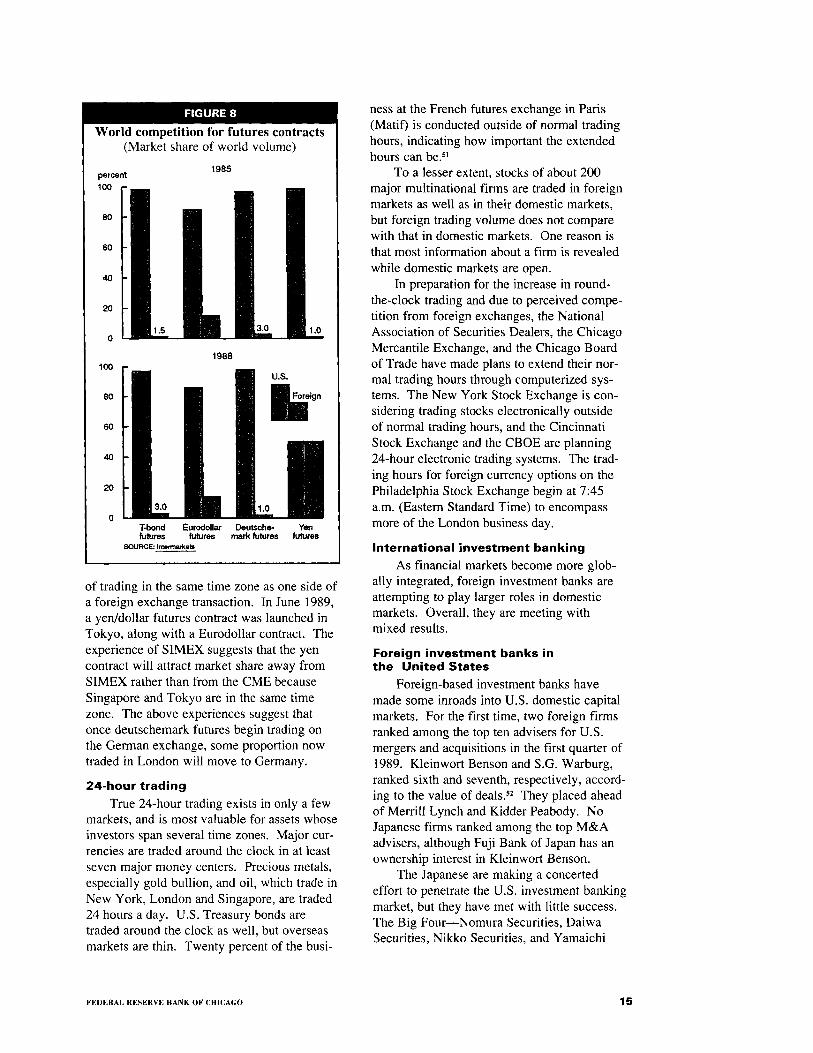

As shown in Figure 8, LIFFE commandsless than 3 percent of trading volume in T-bond futures and options and Eurodollar op-tions. Similarly, less than 3 percent of allDeutschemark futures trading occurs onSIMEX. LIFFE and SIMEX, however, aremuch more significant competitors for Euro-dollar futures volume. SIMEX accounts for7.5 percent of trading volume and LIFFE ac-counts for 6.5 percent.

Furthermore, in only three years, SIMEXmanaged to capture over 50 percent of theannual trading volume in the yen futures con-tract. The relatively greater success of SIMEXwith the yen contract reflects the importance

14

ECONOMIC PERSPECTIVES

FIGURE 8

World competition for futures contracts(Market share of world volume)

T-bond Eurodollar Deutsche- Yenfutures futures mark futures futures

SOURCE: Intermarkets

of trading in the same time zone as one side ofa foreign exchange transaction. In June 1989,a yen/dollar futures contract was launched inTokyo, along with a Eurodollar contract. Theexperience of SIMEX suggests that the yencontract will attract market share away fromSIMEX rather than from the CME becauseSingapore and Tokyo are in the same timezone. The above experiences suggest thatonce deutschemark futures begin trading onthe German exchange, some proportion nowtraded in London will move to Germany.

24-hour trading

True 24-hour trading exists in only a fewmarkets, and is most valuable for assets whoseinvestors span several time zones. Major cur-rencies are traded around the clock in at leastseven major money centers. Precious metals,especially gold bullion, and oil, which trade inNew York, London and Singapore, are traded24 hours a day. U.S. Treasury bonds aretraded around the clock as well, but overseasmarkets are thin. Twenty percent of the busi-

ness at the French futures exchange in Paris(Matif) is conducted outside of normal tradinghours, indicating how important the extendedhours can be. 51

To a lesser extent, stocks of about 200major multinational firms are traded in foreignmarkets as well as in their domestic markets,but foreign trading volume does not comparewith that in domestic markets. One reason isthat most information about a firm is revealedwhile domestic markets are open.

In preparation for the increase in round-the-clock trading and due to perceived compe-tition from foreign exchanges, the NationalAssociation of Securities Dealers, the ChicagoMercantile Exchange, and the Chicago Boardof Trade have made plans to extend their nor-mal trading hours through computerized sys-tems. The New York Stock Exchange is con-sidering trading stocks electronically outsideof normal trading hours, and the CincinnatiStock Exchange and the CBOE are planning24-hour electronic trading systems. The trad-ing hours for foreign currency options on thePhiladelphia Stock Exchange begin at 7:45a.m. (Eastern Standard Time) to encompassmore of the London business day.

International investment banking

As financial markets become more glob-ally integrated, foreign investment banks areattempting to play larger roles in domesticmarkets. Overall, they are meeting withmixed results.

Foreign investment banks inthe United States

Foreign-based investment banks havemade some inroads into U.S. domestic capitalmarkets. For the first time, two foreign firmsranked among the top ten advisers for U.S.mergers and acquisitions in the first quarter of1989. Kleinwort Benson and S.G. Warburg,ranked sixth and seventh, respectively, accord-ing to the value of deals. 52 They placed aheadof Merrill Lynch and Kidder Peabody. NoJapanese firms ranked among the top M&Aadvisers, although Fuji Bank of Japan has anownership interest in Kleinwort Benson.

The Japanese are making a concertedeffort to penetrate the U.S. investment bankingmarket, but they have met with little success.The Big Four—Nomura Securities, DaiwaSecurities, Nikko Securities, and Yamaichi

FEDERAL RESERVE BANK OF CHICAGO 15

Securities Company—expanded in the UnitedStates in the mid-1980s, but have scaledback personnel due to unprofitable U.S. opera-tions. Two of the Big Four—Nomura andYamachi—have been trying to model theirU.S. operations as identifiable Wall Streetcompanies, and not just subsidiaries of Tokyofirms, by their appointment of Americans tohead their U.S. operations. Nomura'sstrengths have been its primary dealership inU.S. government securities and U.S. stocktrading unit, primarily for Japanese purchase.Nomura's weaknesses, however, are its lackof financial product development and its trad-ing skills.

The Japanese have been more successfulin U.S. derivative markets. In April 1988,Nikko Securities became the first Japanesesecurities firm to acquire a clearing member-ship at the Chicago Board of Trade (CBOT).Since then, fifteen others have joined theCBOT. The Chicago Mercantile Exchange(CME) has seventeen Japanese companies asmembers. Nikko, Daiwa, and Yamaichi aremembers of both the CBOT and CME. Re-cently, Nomura announced a cooperativeagreement with Refco, one of the world'slargest futures merchants. Consummation ofthe deal will assist Nomura in learning futurestrading.

U.S. investment banks'activities abroad

Merger and acquisition activity has beenslowing in the United States, prompting WallStreet firms to look to foreign markets. Ac-cording to a 1988 survey, U.S. firms accountedfor slightly more than half of all cross-bordermerger and acquisition activity. The mostactive U.S. investment banks were ShearsonLehman Hutton (57 deals), Goldman Sachs(46), and First Boston (34)."

U.S. investment banks represented about12 percent of all mergers and acquisitions forEuropean clients in 1988. The most activeU.S. firms in this category were Security Pa-cific Group (37 deals), Shearson Lehman Hut-ton (26), and Goldman Sachs (22). SecurityPacific has acquired two foreign investmentbanks, one Canadian and one British?'

U.S. firms expect to find some business inAsia as well. The newly formed investmentbank, Wasserstein Perella, for example, re-cently dispatched merger and acquisition

teams to Japan to set up the Tokyo joint ven-ture, Nomura Wasserstein Perella.

In the area of securities underwriting, U.S.firms are quite strong. Seven of the top tenunderwriters of debt and equity securitiesworldwide are U.S. firms; however, only threeU.S. firms rank among the top underwriters ofnon-U.S. securities. Merrill Lynch was the topunderwriter of all debt and equity offeringsworldwide during the first half of 1989. 5'

The strength of U.S. firms abroad lies pri-marily in Europe. Foreign securities firms inTokyo have found it difficult to establish them-selves. Thirty-six of the 51 Tokyo branches offoreign securities houses lost a total of $164million for the six months ending March 1989. 56

As a result of these losses, many foreign firmshave cut back their Tokyo operations, concen-trating on a particular product or service.Twenty-two out of the 115 Tokyo stock ex-change members are foreign firms. Another 29foreign securities houses have opened branchoffices in Tokyo. Nevertheless, the Big Fourdominate the Tokyo exchange, accounting foralmost 50 percent of daily business. The for-eign firms account for only 4.5 percent of thisdaily business. 57

Three American investment banks, Salo-mon Brothers, Merrill Lynch, and First Boston,have been able to develop profitable operationsin the Tokyo market. All three American firmsattribute their success in part to a well-trainedstaff, and to hiring Japanese college graduatesto fill positions. Salomon posted a $53.6 mil-lion pretax profit as of March 31, 1989. It alsomade a $300 million capital infusion, which hashelped to make Salomon a challenger to the BigFour in bond trading.'"

The U.S. government has been pressuringfor greater access for U.S. firms to Japanesecapital markets since 1984. For instance, Japa-nese government securities are predominantlysold through closed syndicates, in which foreignfirms account for only about 8 percent of thetotal. Change has been slower than foreigninvestment banks and governments would like,but some progress has been made. The Japa-nese sold 40 percent of its 10-year bonds at anopen auction in April 1989. 56

Conclusion

Financial markets and financial services arebecoming more globally integrated. As busi-nesses expand into new markets around the

16 E4:1) \ 01111: PERSPECII‘ES

world, there is greater demand for financing tofollow them. All major areas of internationalfinance have grown far more rapidly than for-eign trade in recent years. Trading of securi-ties in U.S. markets by nonresidents, tradingvolume of foreign currency futures and op-tions, and foreign exchange trading have beengrowing at 40 percent or more a year. Thisrapid growth of international financial transac-tions reflects the growth in cross-border capitalflows.

The major markets for domestic as well asinternational financial services are the UnitedStates, Japan, and the United Kingdom, al-though it is beginning to make more sense totalk about the dominant markets as the UnitedStates, Japan, and Europe. The reduction ofregulatory barriers and harmonization of rulesamong countries have allowed more firms tocompete in more markets around the world.These markets are also competing againsteach other for a share of the world's tradingvolume.

Today, a very large part of financial glo-balization involves financial intermediariesdealing with other, foreign, financial interme-

diaries. Consequently, prices in one marketare affected by conditions in other markets,but, with a few exceptions, of which commer-cial lending is the most notable, customers donot have direct access to more suppliers.Again, this could change as Europe movestoward economic and financial unification.

Lessons from industries such as automo-biles and petroleum, as well as lessons fromgeographic expansion in the United States,indicate that the financial services industrywill become more consolidated, with firmsfrom a handful of countries garnering substan-tial market share. International joint ventureswill be common and often precursors to out-right acquisitions. For smaller firms to surviveas global competitors, they will have to findand service a market niche.

As the financial services industry andfinancial markets become more globally inte-grated, the most efficient and best organizedfirms will prevail. Also, countries with themost efficient—but not necessarily theleast—regulation will become the world'smajor international financial centers.

FOOTNOTES

1 "Japanese Finance," Survey, The Economist, December10, 1988, pp. 3 and 10.

2 Ibid.

3Thomas H. Hanky, et. al., "The Swiss Banks: UniversalBanks Poised to Prosper as Global Deregulation Unfolds,"Salomon Brothers Stock Research, June 1986.

4See David T. Llewellyn, Competition, Diversification, andStructural Change in the British Financial System, 1989,unpublished xerox, p. 1.

5Christopher M. Korth, "Intemational Financial Markets,"in William H. Baughn and Donald R. Mandich, eds., TheInternational Banking Handbook, Dow Jones-Irwin, 1983,pp. 9-13.

6During the Cold War, the U.S. dollar was the only univer-sally accepted currency, and the Russians wanted to main-tain their intemational reserves in dollars, but not at Ameri-can banks for fear that the U.S government might freeze thefunds. Therefore, the Russians found some British, Frenchand German banks that would accept deposits in dollars.See Korth, p. 11.

7 Christopher M. Korth, "The Eurocurrency Markets," inBaughn and Mandich, p. 26.

8 Herbert L. Baer and Christine A. Pavel, "Does regulationdrive innovation?," Economic Perspectives, Vol. 12, No. 2,March/April 1988, pp. 3-15, Federal Reserve Bank ofChicago.

9"Japanese banking booms offshore," The Economist,November 26, 1988, p. 87.

°International Financial Statistics, International MonetaryFund, various years.

11 Ibid.

I2This does not apply in criminal cases, bankruptcy, or debtcollection. The disclosure of secret information to foreignauthorities is not allowed, unless provided for in an interna-tional treaty. In such a case, which is an exception, theforeign authorities could obtain only the informationavailable to Swiss authorities under similar circumstances.See Peat, Marwick, Mitchell & Co., Banking in Switzerland,1979, pp. 35-6.

13 Eurobanks have specific rates at which they are preparedeither to borrow or lend Eurofunds. In London, this rate isknown as LIBOR (the London Interbank Offer Rate).LIBOR dominates the Eurocurrency market.

"Henry S. Terrell, Robert S. Dohner, and Barbara R.Lowrey, "The Activities of Japanese Banks in the United

FEDERAL RESERVE, BANK OF CHICAGO 17

Kingdom and in the United States, 1980-88," Federal

Reserve Bulletin, February 1990, p. 43.

"Michael R. Sesit and Craig Tones, "What if They TradedAll Day and Nobody Came?," Wall Street Journal, June 14,1989, p. Cl.

16 U.S. Foreign Exchange Market Survey, Federal ReserveBank of New York, April 1989, pp. 5-7.

'Report of Assets and Liabilities of U.S. Branches andAgencies of Foreign Banks," Table 4.30, Federal ReserveBulletin, June 1989, Board of Governors of the FederalReserve System; and Annual Statistical Digest, Board ofGovernors of the Federal Reserve System, Table 68.

"Ibid.

"Senior Loan Officer Opinion Survey on Bank LendingPractices for August 1989, Board of Governors of theFederal Reserve System.

20 See footnote 17.

21 Annual Report, Board of Governors of the Federal Re-serve System, Banking Supervision and Regulation Sec-tion, various years; authors' calculations from Report ofCondition and Income tapes, Board of Governors of theFederal Reserve System, various years.

22Ibid.

"Ibid.

24"European banking: Cheque list," The Economist, June24, 1989, pp. 74-5.

25 The Glass-Steagall Act is the law that separates commer-cial banking from investment banking in the U.S. Article65 is its Japanese equivalent.

26James B. Treece, with John Hoerr, "Shaking Up Detroit,"Business Week, August 14, 1989, pp. 74-80.

"Standard and Poor's Oil Industry Survey, August 3,1989, p. 26.

28"European Stock Exchanges," A supplement to Euro-money, August 1987, pp. 2-5.

29Rosario Benvides, "How Big is the World Bond Mar-ket?-1989 Update" International Bond Markets, SalomonBrothers, June 24, 1989.

30Ibid.

31"Look east, young Eurobond," The Economist, September16, 1989, pp. 83-4; "Japanese paper fills the void," Asupplement to Euromoney, March 1989, p. 2.

32See The Economist, Sept. 16, 1989, pp. 83-4.

33"La grande bourn," The Economist, October 1, 1988,pp. 83-4.

34Christine M. Cumming and Lawrence M. Sweet, "Finan-cial Structure of the G-7 Countries: How Does the United

States Compare?," Federal Reserve Bank of New York,Quarterly Review, Winter 1987/88, pp. 15-16.

35"Sweeping away Frankfurt's old-fashioned habits," TheEconomist, January 28, 1989, pp. 73-4.

36 Ibid

"Financial Market Trends, OECD, February 1989, pp.85-6.

38 Ibid.

39Ibid.

40"A smooth run for Switzerland's big banks," The Econo-

mist, June 17, 1989, pp. 87-8.

41 World Financial Markets, J.P. Morgan & Co., November29, 1988.

42"Foreign Transactions in Securities," Table 3.24, FederalReserve Bulletin, June 1989, Board of Governors of theFederal Reserve System.

43Ibid.

"Various central bank statistical releases.

45The underlying instrument is worth $1 million.

46"US exchanges fight for market share," A supplement toEuromoney, July 1989, p. 9.

47Elizabeth R. Thagard, "London's Jump," Intermarkets,

May 1989, p. 22.

48See A supplement to Euromoney, August 1987, p. 28.

49Ginger Szala, "Financial walls tumble for Germaninvestors," Futures, January 1990, p. 44.

50Ibid., p. 42.

51See Thagard, p. 23.

52Ted Weissberg, "Wall Street Seeks Global Merger Mar-ket: IDD's First-quarter M&A Rankings," InvestmentDealers Digest, May 8, 1989, pp. 17-21.

""The World Champions of M&A," Euromoney, February1989, pp. 96-102.

54Ibid.

"Philip Maher, "Merrill Lynch Holds on to Top Interna-tional Spot," Investment Dealers Digest, July 10, 1989,pp. 23-25.

56"Japan proving tough for foreign brokerage," ChicagoTribune, September 11, 1989, section 4, pp. 1-2

58Ibid.

59Ibid.

18 ECO:NOM IC PERS PECTIN ES

![CEO] dm Mot... · 2014-02-02 · (2 lthh th ltrtr tt th r p (nrhtdn xt pr rr th l th prdtd rlt hv fnd tht th ptnt hvn L, nldn th p t 0 dptr f pr, hv ll ttnd t lt 2040 r bttr ndd vl](https://img.pdfslide.net/doc/110x75/5e7b58e8e503d517894909fc/ceo-dm-mot-2014-02-02-2-lthh-th-ltrtr-tt-th-r-p-nrhtdn-xt-pr-rr-th-l-th.jpg)

![SD servicio nombres docu examen2 - UPM · 2019. 4. 9. · d urrw vhuyhuv qhw =rqd d qlf hv =rqd hv hlqvwhlq ffxsp xsp hv =rqd xsp hv ]dsh il xsp hv =rqd il xsp hv qv jqx ruj =rqd](https://img.pdfslide.net/doc/110x75/613bce56f8f21c0c826934b2/sd-servicio-nombres-docu-examen2-upm-2019-4-9-d-urrw-vhuyhuv-qhw-rqd-d-qlf.jpg)