Embed Size (px)

Citation preview

4 Investments & Acquisitions — May 2015 7 U.S. General Purpose Cards 1Q 2015 vs. 1Q 2014 9 Credit Card Debt in the U.S. 1984–2014

11 Largest Merchant Acquirers in Europe 2014

2 – 4 Fast Facts 5 Luxury Cards from OT 6 Merchant Processing

Fees in the U.S.

7 First Quarter Card Results in the U.S.

10 Zooz’s Insight for Web Merchants

INSIDE CHARTS

Investments & Acquisitions — May 2015Turn to page 4 for a list of 62 mergers, acquisitions, and corporate financing deals that occurred in May 2015.Prior issues: 1063, 1061, 1059, 1057, 1055, 1054, 1053

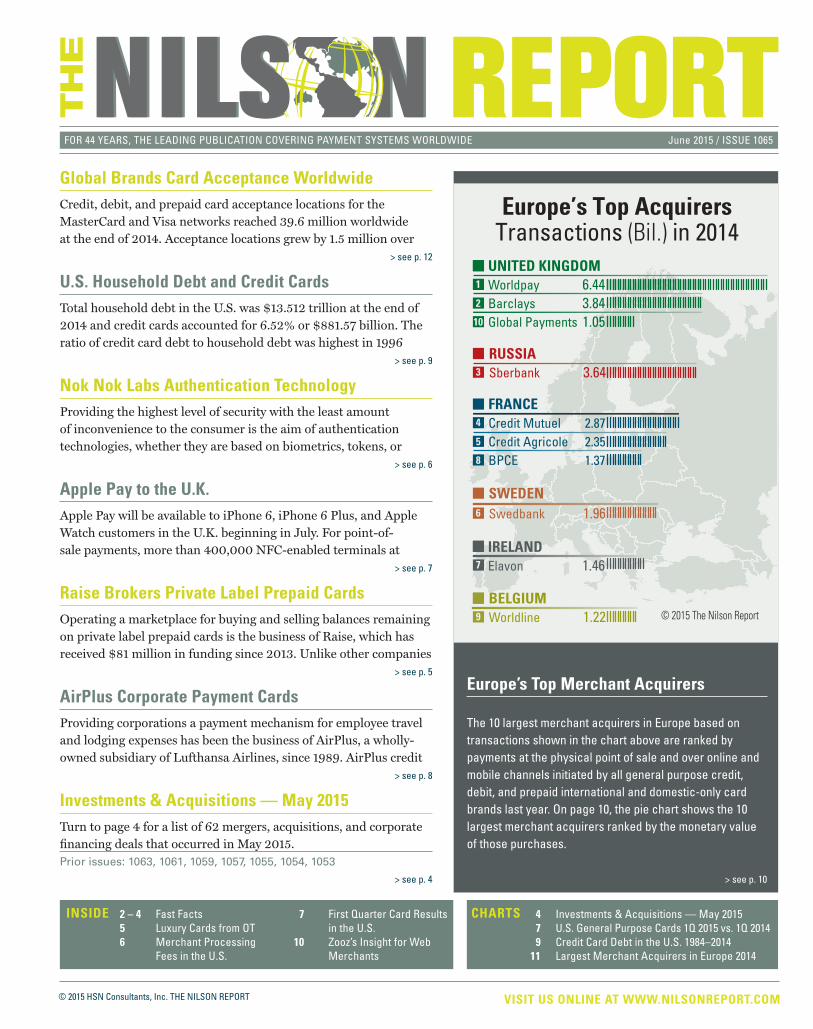

Europe’s Top Merchant Acquirers

The 10 largest merchant acquirers in Europe based on transactions shown in the chart above are ranked by payments at the physical point of sale and over online and mobile channels initiated by all general purpose credit, debit, and prepaid international and domestic-only card brands last year. On page 10, the pie chart shows the 10 largest merchant acquirers ranked by the monetary value of those purchases.

Nok Nok Labs Authentication TechnologyProviding the highest level of security with the least amount of inconvenience to the consumer is the aim of authentication technologies, whether they are based on biometrics, tokens, or

Raise Brokers Private Label Prepaid CardsOperating a marketplace for buying and selling balances remaining on private label prepaid cards is the business of Raise, which has received $81 million in funding since 2013. Unlike other companies

AirPlus Corporate Payment CardsProviding corporations a payment mechanism for employee travel and lodging expenses has been the business of AirPlus, a wholly-owned subsidiary of Lufthansa Airlines, since 1989. AirPlus credit

Apple Pay to the U.K.Apple Pay will be available to iPhone 6, iPhone 6 Plus, and Apple Watch customers in the U.K. beginning in July. For point-of-sale payments, more than 400,000 NFC-enabled terminals at

Global Brands Card Acceptance WorldwideCredit, debit, and prepaid card acceptance locations for the MasterCard and Visa networks reached 39.6 million worldwide at the end of 2014. Acceptance locations grew by 1.5 million over

U.S. Household Debt and Credit CardsTotal household debt in the U.S. was $13.512 trillion at the end of 2014 and credit cards accounted for 6.52% or $881.57 billion. The ratio of credit card debt to household debt was highest in 1996

© 2015 The Nilson Report

Europe’s Top AcquirersTransactions (Bil.) in 2014

UNITED KINGDOMWorldpay 6.44Barclays 3.84Global Payments 1.05

2

10

1

FRANCECredit Mutuel 2.87Credit Agricole 2.35BPCE 1.37

5

8

4

SWEDENSwedbank 1.966

IRELANDElavon 1.467

BELGIUMWorldline 1.229

RUSSIASberbank 3.643

> see p. 4

> see p. 12

> see p. 10

> see p. 9

> see p. 6

> see p. 7

> see p. 5

> see p. 8

VISIT US ONLINE AT WWW.NILSONREPORT.COM © 2015 HSN Consultants, Inc. THE NILSON REPORT

FOR 44 YEARS, THE LEADING PUBLICATION COVERING PAYMENT SYSTEMS WORLDWIDE June 2015 / ISSUE 1065

Topics include: how payment collections and estimations tools and strategies are transforming RCM, best practices in online and mobile patient payments, bundled payments – a new understanding of financial operations & new models of servicing members & patients, payment alternatives: virtual, check, ACH, virtual card, credit/debit cards & cash, bringing the treasury department into the revenue cycle, revenue cycle best practices, how insurers are achieving the elusive healthcare payments/servicing victory, case study: partnership in operational excellence and transparency, considerations of outsourcing revenue cycle operations. Speakers represent: Aetna, Apex Revenue Technologies, Blue Shield of California, BNY Mellon Treasury Service, Carolinas HealthCare System, Citi Retail Services, Commerce Bank, Dimensions Healthcare System, Fifth Third Bank, Flagler Hospital, Horizon Blue Cross Blue Shield, InstaMed, Johns Hopkins Health System, Parallon Revenue Cycle Services, UnitedHealthcare, Wells Fargo, WEX, and more. Cost ranges from $695 to $1,695. (Use code NILSON300.) Contact Kathleen Daffner at Strategic Solutions Network, (203) 209-0520, [email protected]. Register at www.hcpaymentsinnovations.com.

FEATURED CONFERENCE$300Subscribers to The Nilson Report will receive a $300 discount.

Conf

eren

ce li

nks

at w

ww

.nils

onre

port

.com

6TH ANNUAL HEALTHCARE PAYMENTS INNOVATIONS 2015

Two-Day ConferenceJuly 27-28, 2015The Hyatt Regency, Boston, Massachusetts

SAVE

BANK OF AMERICA MERCHANT SERVICES, the 4th largest U.S. acquirer ranked by active merchants, will offer those customers that process less than $1 million annually in American Express card trans-actions participation in Amex’s OptBlue program. OptBlue merchants receive a single statement from their acquirer inclusive of all card pay-ments including Amex. Tim Tynan is CEO at Bank of America Merchant Services, (212) 515-0299, [email protected], www.bankofamerica.com/merchant. Ed Jay is EVP of Merchant Services – Americas at American Express, (212) 640-0791, [email protected], www.americanexpress.com.

VISA will accept airline-supplied flight manifests to refute “friendly fraud” payment card chargebacks beginning October 15, 2015. The rules change will enable airlines to recoup millions of dollars lost annually when a cardholder claims fraud on a valid transaction. Manifests confirm that the passenger name matches the cardholder name. Ramon Martin is Global Head of Merchant Solutions at Visa, (212) 521-3977, [email protected], www.visa.com. Jennifer Watkins is Director of Credit Card Services and Fraud Prevention at ARC, (703) 341-1018, [email protected], www.arccorp.com.

U.S. COURT OF APPEALS for the Second Circuit has declined to halt a District Court’s injunction commanding American Express to drop a requirement in its acceptance agreements forbidding merchants from asking Amex cardholders for card payment from another brand. The Court of Appeals hasn’t yet decided if it will accept Amex’s appeal for a new trial, which aims to overturn a February 19, 2015 anti-competi-tion ruling made by the District Court.

BLUESNAP has added to its payment gateway fraud detection and sales boosting technology from Kount. The technology can analyze hundreds of data points per transaction and deliver a predictive fraud assessment within an average of 350 milliseconds. Bill Sobo is CFO and Global Head of Risk at BlueSnap, (781) 790-5016, [email protected], www.bluesnap.com. Jack Alton is SVP Sales at Kount, (208) 489-2701, [email protected], www.kount.com.

EVO PAYMENTS INT’L will purchase P.O.S. Transact, the merchant acquiring business of Deutsche Postbank. Postbank and EVO have also signed a long-term strategic marketing agreement. In 2013, EVO purchased Deutsche Card Services from Deutsche Bank. James Kelly is CEO at EVO, (770) 709-7310, jim.kelly@ evopayments.com, www.evopayments.com.

TSYS Chip Card on Demand is a card manufacturing service that allows chips to be added to EMV-capable magnetic stripe cards or customized cards from TSYS Card Shop during the production process. Issuers can continue to issue magnetic-stripe-only cards, reducing the need for management of chip inventories, applet changes, and chip specifica-tions. Bob Kellum is Group Executive, Output Services at TSYS, (706) 649-4155, [email protected], www.tsys.com.

VERIFONE will connect its point-of-sale gateway to Visa’s CyberSource global merchant payment management platform. Merchants obtain a single source to protect customer payment data, fight fraud, and inte-grate digital and offline payment systems. Adam Williams is Strategic Alliance Account Executive, Business Development at CyberSource, (512) 535-2331, [email protected], www.cybersource.com. Vin D’Agostino is EVP of Commerce Enablement at Verifone, (212) 364-5626, vin.d’[email protected], www.verifone.com.

CORRECTION: Matthew Katz is CEO, not CFO at Verifi, (323) 655-5789, [email protected].

ICAP PATENT BROKERAGE is offering for sale patents disclosing a multipurpose, multicard reader with storage, display, and transmission capabilities from inventor Adrian Gluck. The sale is part of the Internet of Things IP Auction. Bidding deadline is July 30, 2015. Dean Becker is CEO at ICAP, (561) 573-0405, [email protected], www.icappatentbrokerage.com.

JCPENNEY, a private label credit card client of Synchrony Financial, will offer Apple Pay to its cardholders. Tokenization for Apple Pay transactions will be handled by the MasterCard Digital Enablement Service. Tom Quindlen is CEO of Retail Card at Synchrony Financial, (203) 585-6560, [email protected], www.synchronyfinancial.com. Linda Kirkpatrick is Group Head, Key Merchants at MasterCard, (914) 249-1804, linda_kirkpatrick@ mastercard.com, www.mastercard.com.

FAST FACTS

2 VISIT US ONLINE AT WWW.NILSONREPORT.COM Order Back Issues / Preview Upcoming Conferences / View Newsletter Archive

CASHLESS PAYMENTS SUMMIT 2015: June 25-26, 2015. The Emperors Palace Hotel, Johannesburg, South Africa. Estimated attendance: 50. Cost for the two-day conference is $692. Subscribers to The Nilson Report will receive a 20% discount. (Use code NRB.) Contact Grace Gambiza at Mogorosi Communications, 27 (11) 325-2485, [email protected]. Register at http://www.mogorosicommunications.co.za.

MPOS WORLD 2015: June 30-July 1, 2015. The Kap Europa, Frankfurt, Germany. Estimated attendance: 300. Cost for the two-day conference is $850. Contact David Vesely at Empiria Group, 421 (245) 248-931, david.vesely@ empiriagroup.eu. Register at www.mpos-world.com.

MOBILE PAYMENTS CONFERENCE 2015 (MPC): August 31-September 2, 2015. Hyatt Regency McCormick Place, Chicago, Illinois. Estimated attendance: 300. Cost for the three-day conference is $699 until June 30 ($799 until August 30, and $899 on-site). Subscribers to The Nilson Report will receive a 20% discount. (Use code MPC15NIL.) Contact Robin Albright at MP Associates, (303) 530-4562, [email protected]. Register at http://mobilepaymentconference.com

CONFERENCES & SEMINARS

See

links

at w

ww

.nils

onre

port

.com

MOBEY FORUM has produced a white paper called “Mobile Corporate Banking: a Key Component in a Bank’s Omni-Channel Strategy.” It dis-cusses findings from a survey of 79 banks from around the world and can be downloaded from http://www.mobeyforum.org/whitepaper/corporate-mobile-banking-and-banks-omnichannel-strategy/.

XPRESS-PAY.COM, owned by Systems East, offers merchants online, IVR, and mobile wallet payment products. The company now uses CoCard as its processor. James Buttino is President at Systems East, (607) 753-6156, [email protected], www.systemseast.com. Andrew Anderson is Owner at CoCard Anderson, (802) 459-4262, [email protected], www.cocardmerchantaccounts.com.

COUPA SOFTWARE, provider of cloud-based applications for accounts payable, procurement, expense management, and sourcing & inventory, is in a strategic alliance with MasterCard. Their first joint service is MasterCard in Control for Commercial Payments virtual card payments embedded in the Coupa Procure-to-Pay platform. Rob Bernshteyn is CEO at Coupa, (650) 485-8680, [email protected], www.coupa.com. Edward Glassman is Group Executive, Global Commercial Products, MasterCard, (914) 249-3129, [email protected], www.mastercard.com.

NORTH AMERICAN BANCARD (NAB), the 22nd largest U.S. acquirer, will offer its online merchants PayItSimple’s instant install-ment payments service on Visa and MasterCard credit card purchases. NAB’s front-end gateway, Velocity, will provide PayItSimple with a single interface to all of NAB’s merchants. NAB serves 394,126 active merchants. Alon Feit is CEO at PayItSimple, (972) 524-44-8084, [email protected], www.payitsimple.com. Pat Ward is VP Channel Sales at NAB, (248) 269-6000, [email protected], www.nabancard.com.

MASHREQ has become the first bank in the Central Europe, Middle East, and Africa region to offer credit and debit cardholders Visa Checkout, a one-click digital payment service that makes online purchases simpler and faster. The bank is based in the UAE. Nimish Dwivedi is Head of Payments at Mashreq, 971 (4) 608-3693, [email protected], www.mashreq.com. Marcello Baricordi is General Manager UAE and Global Accounts Lead, MENA at Visa, 971 (4) 457-7200, [email protected], www.visa.com.

UKRAINIAN PROCESSING CENTER (UPC), the largest independent payment processor in Ukraine, will deploy Authentic, the payment platform from the Alaric unit of NCR. UPC, part of the Raiffeisen banking group, supports 30+ banks in Ukraine and customers in Central and Eastern Europe. It manages 7,700+ ATMs, nearly 60,000 POS terminals, and processes up to 60 million trans-actions a month. Sergey Vetrenko is COO at UPC, 380 (44) 247-4977, [email protected], www.upc.ua. Steve Nogalo is VP & General Manager Payments Software at NCR, (937) 445-4200, [email protected], www.ncr.com.

Seventh Edition

a 2015 Nilson Report PublicationWorldwide

Largest

© HSN Consultants Inc. 2015 THE NILSON REPORT, www.nilsonreport.com/specialreport. Reproducing or allowing reproduction

or dissemination of any portion of this document in any manner is a copyright violation subject to substantial fines.

Card Issuers

Merchant Acquirersand

in

Asia/Pacific, United States, Europe, Latin America, Middle East/Africa, and Canada

Over 1,000 Card Issuersfrom 115 countries in all world regions

7th Edition

275 Merchant Acquirersfrom 65 countries in all world regions

Figures include cardsin circulationand spending for

credit & debit card issuers

Pre-order Todaywww.nilsonreport.com/specialreport

FAST FACTS

© 2015 HSN Consultants, Inc. THE NILSON REPORT 3JUNE 2015 / ISSUE 1065 / THE NILSON REPORT

UL has automated card testing to execute the entire Visa Contactless Payment Specification test plan in one run without any manual user interaction. Maxim Dyachenko is Manager Service Line Test Tools at UL, 31 (71) 581-3636, [email protected], www.ul.com.

UNIONPAY cardholders will gain access to 45,000 point-of-sale locations in Portugal beginning July 1, 2015, through a contract with local acquirer Unicre. Joao Serra Amaral is Subdirector, New Channels, Direccao Redunicre, Merchant Acquiring Division at Unicre, 351 (21) 350-9692, [email protected], www.redunicre.pt.

MICROPROSS’S MP500 TCL3 test system has received validation for EMVCo L1 PICC & Mobile analog testing for contactless smart cards and mobile devices. Philippe Bacle is CEO, 33 (3) 2074-6630, [email protected], www.micropross.com.

WIRECARD SINGAPORE will provide card payment processing for more than 2,000 taxis in Singapore. Taxis will accept MasterCard, American Express, JCB, UnionPay, Diners, NETS Debit, FlashPay, and EZ-Link cards. Jeffry Ho is Managing Director, Singapore at Wirecard, (65) 6690 6688, [email protected], www.wirecard.com.

Affi rmLE Series B1 $275.0 U.S. BitbondCR angel funding2 $0.7 Germany Bitcoin BrainsCR BitNational3 $2.0 Canada BorderfreeEC Pitney Bowes3 $395.0 U.S./U.K. Cardtronics U.K.MT Loomis4 $28.0 U.K. Citrus PayMP Series C5 $25.0 India ClearentPR undisclosed round6 $25.0 U.S. CompoSecureCM undisclosed round7 * U.S. ContactMT Qiwi3 * Russia Credit SesamePF Series D8 $16.0 U.S. CryexCR undisclosed round9 $10.0 Sweden Digital CCCR undisclosed round10 $2.6 Australia DLRSCP Tall Group3 * No. Ireland DropletMP seed funding11 $0.9 U.K. Edo InteractiveLO Series E12 $20.0 U.S. eGifterPD undisclosed round13 $3.5 U.S. EverCompliantSE Series A14 $3.5 Israel FANSMP Optimal Payments3 $13.0 Canada FeedzaiSE Series B15 $17.5 U.S. First PerformanceSO MasterCard16 * U.S. Fraud MetrixSE Series B17 $30.0 China GE CapitalCC Coles18 * Australia GoldMoneyCR BitGold3 $41.1 Canada IDcheckerSE Mitek3 $10.6 Netherlands IngenicoHW Fosyn19 * China IngogoMP crowdfunding20 $9.2 Australia Intelligent Point of SaleSD angel funding10 $0.8 U.K. ItBitCR undisclosed round10 $25.0 U.S. IyzicoEC Series B21 $6.2 Turkey KantoxFX undisclosed round22 $10.9 U.K. MartMobiMP Snapdeal3 * India MoneseMP seed funding23 $1.8 U.K./Estonia NerdWalletLE Series A24 $64.0 U.S. Net ElementMP Series A10 $5.5 U.S. Net ElementMP Senior Convertible Notes10 $5.0 U.S. NewgenPR angel funding25 * India NXT-IDCM undisclosed round10 $1.6 U.S. OmiseMP Series A26 $2.6 Thailand PaidyEC Series A27 $8.3 Japan

Payfi rmaPR Series A28 $10.4 Canada PayItSimpleLE undisclosed round29 $10.0 U.S. PayOnlineEC NetElement3 $8.4 Russia PayzerMP Series A30 $4.2 U.S. PostbankMA EVO Pay. Int’l31 * Germany RapidaPR Qiwi3 * Russia Ripple LabsSE Series A32 $28.0 U.S. SavingStarLO undisclosed round10 $3.1 U.S. SeergateEC MyECheck3 * Israel SeglanMP Tag Systems33 * Spain Shenzhen 1card1Tech.CM Hengbao34 * China SparkBasePD Factor435 * U.S. SquarePR undisclosed round36 * U.S. Strongroom SolutionSO Avid Xchange3 * U.S. TiltCF undisclosed round10 * U.S. Transact24PR Net1 UEPS37 * Hong Kong TravelersBoxPR undisclosed round38 $4.5 Turkey Tugboat YardsEC Facebook3 * U.S. UnfraudSE seed funding39 $0.1 Italy VouchLE Series A40 $6.0 U.S. WePayEC Series D41 $40.0 U.S. WeveMP O23 * U.K. Ziddy.comEC angel funding42 $0.5 Singapore

*Terms not disclosed. (1) Includes $75 mil. in equity and $200 million to fund loans from Spark Capital and others. (2) Led by Point Nine Capital. (3) Acquisition. (4) Purchased only the cash-in-transit business. (5) Including Peter Thiel. (6) From FTV Capital. (7) From LLR Partners. (8) Led by Syncora Alternative Investments. (9) Led by White Star Capital. (10) Undisclosed investors. (11) From Crowdcube. (12) Led by Baird Capital. (13) Including 94Bits. (14) Including Nyca Partners. (15) Led by Oak HC/FT. (16) Purchased equity stake. (17) Including CBC Capital. (18) Purchased the other 50% of its in-house credit card portfo-lio. (19) Purchased 20% of Ingenico’s Fujian Landi stake. (20) From Venture Crowd. (21) Led by Int’l Finance Corp. (22) From Partech. (23) Including seedcamp. (24) Led by Institutional Venture Partners. (25) From Jan Manten. (26) Led by Sinar Mas Digital Ventures. (27) Led by Arbor Ventures. (28) Led by Dundee Capital Markets. (29) From Simple Mgmt. (30) Led by Grotech Ventures. (31) Purchased its P.O.S. Transact merchant acquiring portfolio. (32) Including IDG Capital. (33) Purchased undisclosed equity position. (34) Purchased 51% of the equity. (35) Purchased 11,000 private label prepaid card accounts. (36) Including Victory Park Capital. (37) Purchased 43.88%. (38) Led by iAngles. (39) Led by TIM Ventures. (40) Led by First Round Capital. (41) Led by FTV Capital. (42) From Bachchan family. Company categories: BP = bill payment, CC = credit card, CF = crowd funding, CM = card manufacturing, CP = check printer, CR = cryptocurrency, EC = ecommerce, FX = foreign exchange, HW = hardware, LE = lending, LO = loyalty/coupons, MA = merchant acquiring, MP = mobile payments, MT = money transfer, PD = prepaid, PF = personal fi nance, PR = processor, SE = security, SO = software.

© 2015 The Nilson Report

AmountCompany Buyer/Investor (mil.) Country

AmountCompany Buyer/Investor (mil.) Country

Investments & Acquisitions May 2015

FAST FACTS

4 VISIT US ONLINE AT WWW.NILSONREPORT.COM Order Back Issues / Preview Upcoming Conferences / View Newsletter Archive

Oberthur Technologies (OT), the third largest payment card manufacturer in the world, offers

Smart Premiere, a range of luxury payment cards issuers can offer affluent customers. Smart Premiere cards can be produced with precious metals (gold, silver, or titanium), or jewels (including diamonds). They are also available in unusual

shapes, and can be delivered in partnership with luxury brands such as high-end car manufacturers. OT handles most of the manufacturing of Smart Premiere cards.

For special materials or designs involving engraving for example, it sometimes subcontracts the fabrication to outside firms.

Oberthur offers issuers consulting services to help them refresh designs for high-net-worth

individuals or to create entirely new designs. It delivers a full range of packaging options to enhance its Smart Premiere product line,

which has the same functionality as normal payment cards.Nicolas Raffin is Head of Strategic Marketing

at Oberthur Technologies in Colombes Cedex,

France, 33 (1) 7814-7000, [email protected],

www.oberthur.com.

that see opportunities to generate revenue from the estimated $100 billion a year in unwanted prepaid

card balances, Raise does not buy and then sell cards. It performs a service like eBay or Stub Hub, taking a 15% commission from sellers.

The private label prepaid card market has three components — purchased as gifts, issued as store credit, and issued as a merchandiser’s credit. Collectively, new value exceeds $400 billion annually. More than 3,000 different brands of private label cards have been brokered since Raise launched in February 2013. Since that time,

Raise has handled two million transactions. It estimates that the market for buying/selling prepaid card balances is less than 1% penetrated.

Raise settles with sellers by way of an ACH deposit, paper check, or deposit to a PayPal account. It batches all transactions and sends them to Wells Fargo for ACH, PayPal, or check disbursement.

Relationships with processors and program managers enable Raise to facilitate value exchanges in real time and to confirm that sellers are offering legitimate cards. It plans on expanding those relationships to gain access to more merchants. Their support is needed for redemption of prepaid balances that can only be used online.

Raise launched an app for iOS mobile users in the fourth quarter of 2014, and an Android app earlier this year. It already

has more than one million mobile users. Currently, 94% of all business handled by Raise is digital. Buyers receive a barcode representing prepaid value that integrates with a retailer’s POS system for redemption.

Funds raised in its Series B round completed in February of this year will be used over the next two years to establish Raise as a brand, for marketing, to hire software engineers, and to support new customer acquisition efforts.

It will also begin a credit program that will allow customers to sell their unwanted card balances and buy another brand of prepaid card. George Bousis is CEO at Raise

in Chicago, Illinois, (312) 548-

1091, [email protected],

www.raise.com.

Sellers could potentially offer $100 bil. in unwanted prepaid funds.

Luxury Cards from OT for Affluent Cardholders

Raise Brokers Private Label Prepaid Cardsfrom page 1...

© 2015 HSN Consultants, Inc. THE NILSON REPORT 5JUNE 2015 / ISSUE 1065 / THE NILSON REPORT

passwords. Nok Nok Labs has used $31.5 million in venture funding since 2011 to build authentication infrastructure

card issuers and others can deploy to handle every kind of authentication certified by the FIDO Alliance, a consortium of almost 200 major organizations.

FIDO Alliance standards enhance authentication reliability and leverage a device’s components — camera, embedded secure element (eSE), SIM card, geolocation service, fingerprint sensor, microphone, and Trusted Execution Environment. Those standards favor, but are not limited to, using biometric authentication, incorporating

asymmetric cryptography, and accommodating the user’s existing device or one provided by their employer. FIDO members include representatives from Visa, MasterCard, Discover, NTT Docomo, Microsoft, Google, Gemalto, Oberthur, Alibaba, PayPal, G&D, Bank of America, Wells Fargo, and Samsung.

Smartphones are reaching ubiquity in developed markets, eSEs are available to give strong hardware protection to authentication credentials, governments including the European Union, Singapore, and Hong Kong are demanding stronger protection for digital transactions, and Apple and Samsung devices have made fingerprint biometrics acceptable to consumers through their newest handheld devices.

The first Nok Nok Labs product reached the market in 2012 — a server with out-of-band authentication software as well as SDKs for iOS and Android devices that issuers and others could use to upgrade their mobile banking apps to add FIDO-certified authentication for login and payments. Nok Nok can also help clients with system integration if they need to connect the Nok Nok

Authentication Server to their legacy customer identification platforms. Clients include Alipay, PayPal, MedImpact, and NTT Docomo.

Nok Nok’s out-of-band authentication relies on QR codes and push notifications to a user’s mobile device or computer. The

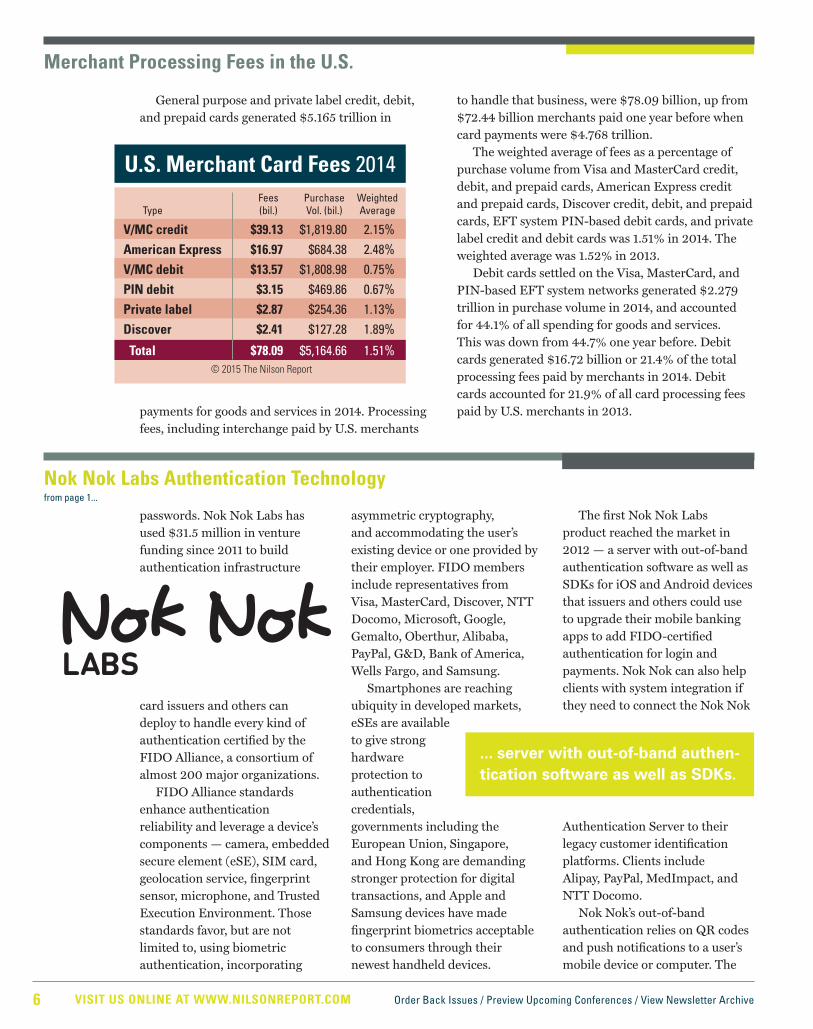

General purpose and private label credit, debit, and prepaid cards generated $5.165 trillion in

payments for goods and services in 2014. Processing fees, including interchange paid by U.S. merchants

to handle that business, were $78.09 billion, up from $72.44 billion merchants paid one year before when card payments were $4.768 trillion.

The weighted average of fees as a percentage of purchase volume from Visa and MasterCard credit, debit, and prepaid cards, American Express credit and prepaid cards, Discover credit, debit, and prepaid cards, EFT system PIN-based debit cards, and private label credit and debit cards was 1.51% in 2014. The weighted average was 1.52% in 2013.

Debit cards settled on the Visa, MasterCard, and PIN-based EFT system networks generated $2.279 trillion in purchase volume in 2014, and accounted for 44.1% of all spending for goods and services. This was down from 44.7% one year before. Debit cards generated $16.72 billion or 21.4% of the total processing fees paid by merchants in 2014. Debit cards accounted for 21.9% of all card processing fees paid by U.S. merchants in 2013.

... server with out-of-band authen-tication software as well as SDKs.

U.S. Merchant Card Fees 2014 Fees Purchase Weighted Type (bil.) Vol. (bil.) Average

V/MC credit $39.13 $1,819.80 2.15%American Express $16.97 $684.38 2.48%V/MC debit $13.57 $1,808.98 0.75%PIN debit $3.15 $469.86 0.67%Private label $2.87 $254.36 1.13%Discover $2.41 $127.28 1.89%

Total $78.09 $5,164.66 1.51%© 2015 The Nilson Report

Nok Nok Labs Authentication Technology from page 1...

Merchant Processing Fees in the U.S.

6 VISIT US ONLINE AT WWW.NILSONREPORT.COM Order Back Issues / Preview Upcoming Conferences / View Newsletter Archive

Visa, MasterCard, American Express, and Discover brand consumer and commercial credit, debit, and prepaid cards issued in the U.S. generated $1.108 trillion in purchase volume in the first quarter of 2015, up 7.6% over the same period in 2014.

Credit card purchase volume of $642.91 billion grew by 8.0%. Visa was up 12.2%, American Express was up 6.3%, MasterCard was up 6.1%, and Discover was down 11.4%.

Credit card cash volume of $22.83 billion from balance

transfers, ATMs, over the counter, and paper checks increased 3.1%. As a percentage of total volume, cash volume was 3.43%. One year earlier it was 3.59%.

Debit and prepaid card purchase volume of $465.43 billion increased 6.9%.

MasterCard debit and prepaid card spending was up 8.1%. Visa debit and prepaid card spending increased 6.3%.

Credit cards generated 36.04% of all purchase transactions at merchants, up from 35.46%. Purchase transactions using Visa credit cards accounted for 53.28% of all credit card transactions, up 212 basis points over the first quarter of 2014. MasterCard credit card purchase transactions held a 23.67% share, down 87 basis points. American Express’s market share of all credit card purchase transactions was 16.35%, down 47 basis points, and Discover’s 6.71% share was down 78 basis points.

authentication can be used for branches, websites, ATMs, mobile apps, point of sale, and customer service. No authentication secrets are stored on Nok Nok servers. Point of sale includes

compatibility with host card emulation and tokenization.

Nok Nok Labs can serve customers anywhere in the world. It prices its products on a per-end-user, per-year basis, not on a per-transaction or per-device basis.

Jamie Cowper is Senior Director,

Business Development at

Nok Nok Labs, Inc. in Palo Alto,

California, (650) 433-1300,

www.noknok.com.

250,000 locations in the U.K. will accept Apple Pay transactions billed to American Express, MasterCard, and Visa credit and debit cards. Within apps, Apple Pay transactions can also be made from iPad

Air 2 and iPad mini 3 devices. More than 40% of smartphones in the U.K. are Apple devices.

The first batch of issuers to offer Apple Pay to their cardholders will be First Direct, HSBC, NatWest,

U.S. General Purpose Cards 1Q 2015 vs. 1Q 2014 Dollar Volume (bil.) Purch. Trans. Brand Total Chg. Purchases Chg. Cash Chg. (bil.) Chg.

Visa Credit $315.52 12.2% $302.13 12.2% $13.39 12.2% 3.62 15.1%

American Express Credit $169.20 6.3% $168.17 6.3% $1.03 –1.8% 1.11 7.4%

MasterCard Credit $152.28 5.4% $146.22 6.1% $6.06 –10.2% 1.61 6.6%

Discover Credit $28.74 –10.8% $26.39 –11.4% $2.35 –2.9% 0.46 –1.1%

CREDIT CARD TOTALS $665.74 7.9% $642.91 8.0% $22.83 3.1% 6.80 10.5%

Visa Debit & Prepaid $431.51 5.6% $324.74 6.3% $106.77 3.5% 8.56 7.1%

MasterCard Debit & Prepaid $186.62 7.6% $140.69 8.1% $45.93 6.0% 3.51 9.3%

DEBIT CARD TOTALS $618.13 6.2% $465.43 6.9% $152.70 4.2% 12.07 7.7%

CREDIT & DEBIT TOTALS $1,283.86 7.1% $1,108.33 7.6% $175.53 4.1% 18.86 8.7%

Visa Totals $747.03 8.3% $626.87 9.1% $120.16 4.4% 12.18 9.3%

MasterCard Totals $338.90 6.6% $286.91 7.1% $51.99 3.8% 5.12 8.4%

VISA & MC TOTALS $1,085.92 7.8% $913.78 8.5% $172.15 4.2% 17.30 9.1%

Includes all consumer and commercial credit, debit, and prepaid cards. American Express and Discover include business from third-party issuers. Figures include PIN-based debit fi gures for Visa (Interlink) and MasterCard to match their reporting. © 2015 The Nilson Report

First Quarter Card Results in the U.S.

> see p. 8

Apple Pay to the U.K. from page 1...

© 2015 HSN Consultants, Inc. THE NILSON REPORT 7JUNE 2015 / ISSUE 1065 / THE NILSON REPORT

card accounts generated $14.35 billion (€12.7 billion) in purchase

volume last year — 80% of that spending was billed to a lodge or

“ghost” account for which there is no plastic card. That spending is cleared over the payment network owned by UATP. Payment cards are issued by 21 airlines worldwide for use on the UATP network. A total of 260 airlines worldwide accept UATP cards for payment. AirPlus issues the UATP card for Lufthansa, United Airlines, Singapore Airlines, AirChina, and four other airlines. The remaining 20% of AirPlus lodge account and card spending in 2014 was billed to virtual MasterCard and Visa cards.

Europe is AirPlus’s biggest market. It has applied for an

e-money license in Europe where it issues its MasterCard cards in 11 countries. Outside Europe it has partnerships with credit card issuers in 18 countries including First National of Omaha in the U.S. Those banks issue Visa and MasterCard cards in their home countries to employees of AirPlus corporate customers. Card accounts are issued in 70 countries.

Spending billed to AirPlus accounts grew by 7.5% last year even as corporate travel worldwide fell by 3.6%. AirPlus owns the customer relationships worldwide, takes all credit risk, issues

Nationwide Building Society, Royal Bank of Scotland, Santander, and Ulster Bank. By the end of the third quarter of this year, Bank of Scotland, Coutts, Halifax, Lloyds Bank, MBNA, M&S Bank, and TSB Bank will

join that group. U.K. issuers will use

tokenization services from American Express, MasterCard, and Visa Europe for all Apple Pay transactions.

Not participating in Apple Pay at this time is Barclaycard, the largest

credit card issuer and second largest debit card issuer in the U.K. As is the case with other U.K. card issuers, most active Barclaycard credit and debit cards have contact and contactless chips, which already gives them access to all NFC-enabled POS terminals that will be available to Apple Pay smartphones.

There are 59 million contactless credit and debit cards in the U.K. generating nearly 50 million transactions monthly.

Other mobile payment services to launch in the U.K. by year-end are Samsung Pay (see issue 1064) and Zapp, a mobile payment service of VocaLink. Zapp payments will initiate from a user’s mobile banking app. First Direct, HSBC, Metro Bank, Nationwide, and Santander have committed to Zapp,

which will be available for online payments this year and NFC-based payments at the point of sale next year.

U.S. Apple Pay users already have access to all NFC-enabled POS terminals worldwide, including 2.6 million in Europe, owing to a 2013 agreement by American Express, MasterCard, and Visa to use a global common standard to generate tokens for all mobile payments based on EMV contactless protocols. All Apple Pay transactions at the point of sale use tokens that comply with EMV contactless protocols. U.K. Apple Pay customers will have access to the same global NFC-enabled POS terminal base.

Adyen, Braintree, CyberSource, DataCash, First Data, Global Payments, Judo Payments, Simplify,

Stripe, and Worldpay are acquirers and gateway providers that will offer merchants Apple Pay for in-app purchases. Mark Barnett is President, U.K. & Ireland at MasterCard

in London, U.K., 44 (207) 557-6818, mark_barnett@

mastercard.com, www.mastercard.com.

Jeremy Nicholds is Executive Director of Mobile at Visa

Europe in London, U.K., 44 (207) 795-5495, nicholdj@

visa.com, www.visa.com.

Issuers will use token vaults from Amex, MasterCard, and Visa Europe.

AirPlus Corporate Payment Cards from page 1...

Apple Pay to the U.K. from page 7...

8 VISIT US ONLINE AT WWW.NILSONREPORT.COM Order Back Issues / Preview Upcoming Conferences / View Newsletter Archive

statements, processes accounts, and handles settlement. Its business grows by following the

multinationals among its 43,000 corporate clients to all of the countries in which they operate. AirPlus gains new corporate

customers faster in markets where employee travel is booked by agencies that receive payment

from corporations by paper check or bank transfers. China, where AirPlus

has four offices, is its fastest growing market.

Last year 143 million transactions billed to AirPlus

cards earned the company revenue of $361.6 million (€320 million), up 7.4%. Earnings before taxes more than doubled to $45.6 million (€40.4 million). Patrick Diemer is Managing

Director at AirPlus International in

Neu-Isenburg, Germany, 49 (610)

220-4118, [email protected],

www.airplus.com.

Prior issues: 1002, 990, 975, 972

at 10.05%. Card debt is comprised of outstanding receivables tied to general purpose and private label credit accounts. Debt on credit cards is a subset of total consumer credit, which was $3.317 trillion at the end of 2014.

Total consumer credit is reported in the Federal Reserve Statistical Release, Z.1, Financial Accounts of the United States, Flow of Funds, Balance Sheets, and Integrated Macroeconomic Accounts, Table D.3, Credit Market Debt Outstanding by Sector. Card debt is compiled by The Nilson Report from its surveys of financial institutions and other credit card lenders.

Credit card debt accounted for 26.58% of total consumer credit at the end of 2014. This is the lowest level of card debt to total consumer credit since 1990 when it was 29.42%. Card debt was highest in 1997, when it was 40.95% of consumer credit.

Total consumer credit is comprised of installment and noninstallment unsecured personal loans, both closed and open-ended. The Federal Reserve does not count mortgage debt and low-value bank loans as consumer credit. However, total household debt includes consumer credit added to mortgage debt and low-value bank loans.

Mortgage debt (and select other loans) of $10.195 trillion in 2014 increased by $123.30 billion in 2014. Credit card debt increased by $38.23 billion, while total consumer credit grew by $218.40 billion.

Total U.S. household debt of $13.512 trillion in 2014 was up $341.70 billion from $13.170 trillion at year-end 2013. The average debt for each of the 123.2 million U.S. households at year-end 2014 was $109,650. One year before the average household debt was $107,549.

Consumer credit equaled 24.55% of household debt at the end of 2014, up from 23.53% the prior year. Consumer credit per household was $26,919. Not counted by the Federal Reserve as consumer credit are rent payments and automobile leases.

Credit card debt per household was $7,154 at year-end 2014, up from $6,887 in 2013.

Prior issues: 1043, 1020, 997, 974, 952, 926, 903

The lowest level of card debt to total consumer credit since 1990.

...143 mil. transactions generated $14.35 bil. in purchase volume.

5.6%

20.4% 25.5%

37.0%

40.9%38.2% 36.8%

30.7%26.6%

5.5%

6.8%

10.1%9.8%

6.8%

7.1%

6.1%

6.5%

$12

$9

$6

$3

as a % ofHousehold Debt(Trillion)

‘94‘92‘90‘88‘86‘84 ‘96 ‘98 ‘00 ‘02 ‘04 ‘06 ‘08 ‘10 ‘12 ‘14

‘94‘92‘90‘88‘86‘84 ‘96 ‘98 ‘00 ‘02 ‘04 ‘06 ‘08 ‘10 ‘12 ‘14

$3

$2

$1

as a % ofConsumer Credit(Trillion)

©2015 The Nilson Report

Credit Card Debtin the U.S. 1984–2014

7.2%

9.0%

U.S. Household Debt and Credit Cards from page 1...

© 2015 HSN Consultants, Inc. THE NILSON REPORT 9JUNE 2015 / ISSUE 1065 / THE NILSON REPORT

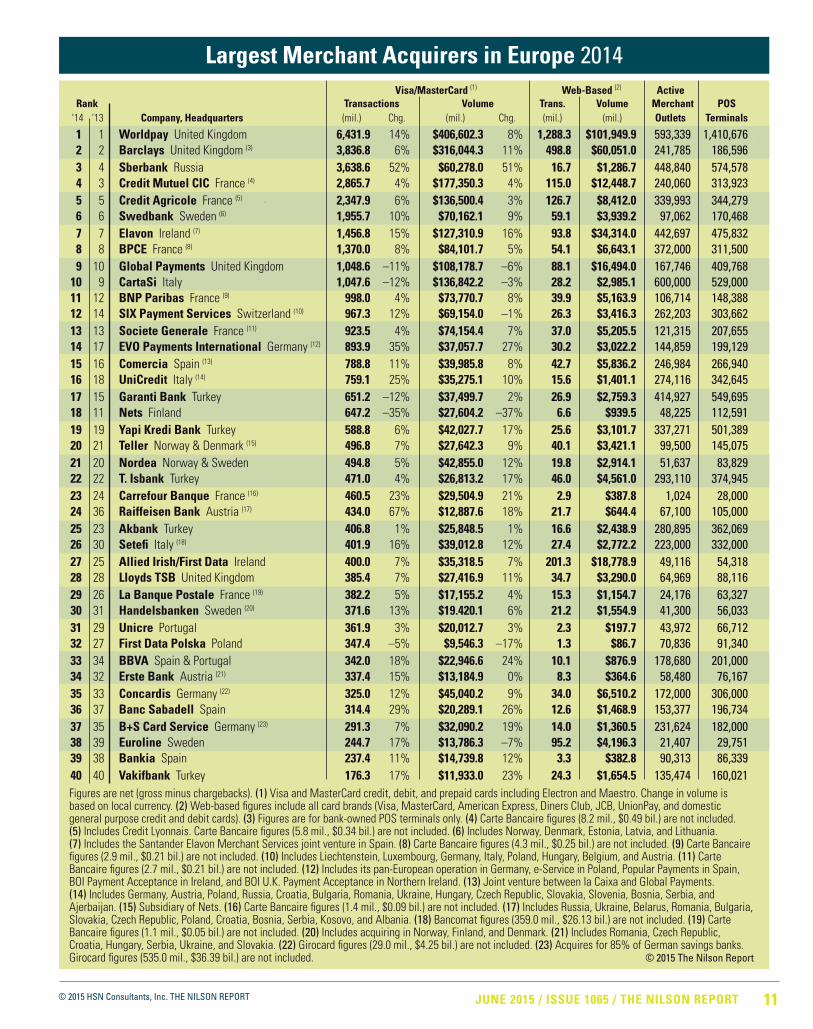

Europe’s 40 largest acquirers of Visa (including Electron), MasterCard, and Maestro bank card transactions in 2014 are

ranked on page 11. Collectively, the top 40 handled 40.90 billion transactions from 7.9 million active merchant outlets. Purchase

volume of Visa, MasterCard, and Maestro transactions was $2.567 trillion.

Web-based and mobile transactions are also shown in the top 40 table. This group handled 3.27 billion transactions valued at $338.39 billion. Visa and MasterCard purchases included in the Web-based columns are also counted in the Visa/MasterCard columns.

Other Web and mobile activity counted includes purchases on all international and domestic general purpose credit and debit cards. Those transactions are not included in the Visa/MasterCard columns.

The Visa/MasterCard columns in the top 40 table do not include 50.4 million transactions handled by this group generated by American Express, Diners Club, Discover, JCB, and UnionPay credit cards, valued at $10.70 billion.

Domestic debit transactions processed by this group are also not shown in the Visa/MasterCard columns in the top 40 table. Domestic debit brands include Girocard (564.0 million) in Germany, Pago Bancomat (359.0 million) in Italy, and Carte Bancaire (26.3 million) in France. Collectively, they reached 949.3 million last year and generated $68.40 billion in purchase volume at merchants.

More than 1,000 retailers and technology companies selling across national borders use the

Smart Routing payments platform from Zooz to manage card and alternative payments to maximize acceptance rates at the lowest cost.

The platform determines in real time how to clear a payment from among multiple acquirers.

Over the last year Zooz has worked on taking all data gathered from its customers about card products, cardholders, national markets, seasonality, and much more to create a service it calls Insights. Merchants can use Insights to support a variety of

business decisions including how to increase sales, cut fraud fighting costs, reach out to particular issuers to help authorize more sales, gain benchmarks for payment types, redesign aspects of their payment page to reduce consumer friction, view a buyer’s spending pattern, and more.

The Insights dashboard will be offered free of charge to existing Zooz customers, most of which are based in Europe.

Zooz uses a direct sales staff to sign new merchant customers. It opened a sales office in the U.K. earlier this year and expects to open one in California before the end of the year. Oren Levy is CEO at Zooz in Ra’anana, Israel, 972 (73)

726-9669, [email protected], www.zooz.com.

Prior issues: 1045, 996

The 40 largest acquirers handled 40.90 bil. card transactions.

Top 10 Acquirers in Europe Ranked by Purchase Volume

on General Purpose Cards (Bil.)Worldpay•$407.80

SocieteGenerale•$74.36

BPCE•$84.35

Worldline•$86.66

GlobalPayments•$108.74

•Barclays$316.06

•CreditMutuel$177.84

•CreditAgricole$137.55

•CartaSi$136.84

•Elavon$127.92

Notes: Figures include all European business except for exclusions noted below. Volume is net (gross minus chargebacks) for Visa, MasterCard, Maestro, American Express, JCB, Diners Club, Discover, UnionPay, and domestic brands.Credit Mutuel, Credit Agricole, BPCE and Societe Generale include Carte Bancaire figures. Elavon includes the Santander Elavon Merchant Services joint venture in Spain and the partnership with Santander in the U.K. Global Payments does not include the UCS Russia business or the La Caixa joint venture in Spain. Worldline includes Bancontact/Mister Cash figures. © 2015 The Nilson Report

10

7 5

39

8

6

4

21

Europe’s Top Merchant Acquirers from page 1

Zooz’s Insight for Web Merchants

10 VISIT US ONLINE AT WWW.NILSONREPORT.COM Order Back Issues / Preview Upcoming Conferences / View Newsletter Archive

Visa/MasterCard (1) Web-Based (2) Active Rank Transactions Volume Trans. Volume Merchant POS ‘14 ‘13 Company, Headquarters (mil.) Chg. (mil.) Chg. (mil.) (mil.) Outlets Terminals

1 1 Worldpay United Kingdom 6,431.9 14% $406,602.3 8% 1,288.3 $101,949.9 593,339 1,410,676 2 2 Barclays United Kingdom (3) 3,836.8 6% $316,044.3 11% 498.8 $60,051.0 241,785 186,596 3 4 Sberbank Russia 3,638.6 52% $60,278.0 51% 16.7 $1,286.7 448,840 574,578 4 3 Credit Mutuel CIC France (4) 2,865.7 4% $177,350.3 4% 115.0 $12,448.7 240,060 313,923 5 5 Credit Agricole France (5) 2,347.9 6% $136,500.4 3% 126.7 $8,412.0 339,993 344,279 6 6 Swedbank Sweden (6) 1,955.7 10% $70,162.1 9% 59.1 $3,939.2 97,062 170,468 7 7 Elavon Ireland (7) 1,456.8 15% $127,310.9 16% 93.8 $34,314.0 442,697 475,832 8 8 BPCE France (8) 1,370.0 8% $84,101.7 5% 54.1 $6,643.1 372,000 311,500 9 10 Global Payments United Kingdom 1,048.6 –11% $108,178.7 –6% 88.1 $16,494.0 167,746 409,768 10 9 CartaSi Italy 1,047.6 –12% $136,842.2 –3% 28.2 $2,985.1 600,000 529,000 11 12 BNP Paribas France (9) 998.0 4% $73,770.7 8% 39.9 $5,163.9 106,714 148,388 12 14 SIX Payment Services Switzerland (10) 967.3 12% $69,154.0 –1% 26.3 $3,416.3 262,203 303,662 13 13 Societe Generale France (11) 923.5 4% $74,154.4 7% 37.0 $5,205.5 121,315 207,655 14 17 EVO Payments International Germany (12) 893.9 35% $37,057.7 27% 30.2 $3,022.2 144,859 199,129 15 16 Comercia Spain (13) 788.8 11% $39,985.8 8% 42.7 $5,836.2 246,984 266,940 16 18 UniCredit Italy (14) 759.1 25% $35,275.1 10% 15.6 $1,401.1 274,116 342,645 17 15 Garanti Bank Turkey 651.2 –12% $37,499.7 2% 26.9 $2,759.3 414,927 549,695 18 11 Nets Finland 647.2 –35% $27,604.2 –37% 6.6 $939.5 48,225 112,591 19 19 Yapi Kredi Bank Turkey 588.8 6% $42,027.7 17% 25.6 $3,101.7 337,271 501,389 20 21 Teller Norway & Denmark (15) 496.8 7% $27,642.3 9% 40.1 $3,421.1 99,500 145,075 21 20 Nordea Norway & Sweden 494.8 5% $42,855.0 12% 19.8 $2,914.1 51,637 83,829 22 22 T. Isbank Turkey 471.0 4% $26,813.2 17% 46.0 $4,561.0 293,110 374,945 23 24 Carrefour Banque France (16) 460.5 23% $29,504.9 21% 2.9 $387.8 1,024 28,000 24 36 Raiffeisen Bank Austria (17) 434.0 67% $12,887.6 18% 21.7 $644.4 67,100 105,000 25 23 Akbank Turkey 406.8 1% $25,848.5 1% 16.6 $2,438.9 280,895 362,069 26 30 Setefi Italy (18) 401.9 16% $39,012.8 12% 27.4 $2,772.2 223,000 332,000 27 25 Allied Irish/First Data Ireland 400.0 7% $35,318.5 7% 201.3 $18,778.9 49,116 54,318 28 28 Lloyds TSB United Kingdom 385.4 7% $27,416.9 11% 34.7 $3,290.0 64,969 88,116 29 26 La Banque Postale France (19) 382.2 5% $17,155.2 4% 15.3 $1,154.7 24,176 63,327 30 31 Handelsbanken Sweden (20) 371.6 13% $19.420.1 6% 21.2 $1,554.9 41,300 56,033 31 29 Unicre Portugal 361.9 3% $20,012.7 3% 2.3 $197.7 43,972 66,712 32 27 First Data Polska Poland 347.4 –5% $9,546.3 –17% 1.3 $86.7 70,836 91,340 33 34 BBVA Spain & Portugal 342.0 18% $22,946.6 24% 10.1 $876.9 178,680 201,000 34 32 Erste Bank Austria (21) 337.4 15% $13,184.9 0% 8.3 $364.6 58,480 76,167 35 33 Concardis Germany (22) 325.0 12% $45,040.2 9% 34.0 $6,510.2 172,000 306,000 36 37 Banc Sabadell Spain 314.4 29% $20,289.1 26% 12.6 $1,468.9 153,377 196,734 37 35 B+S Card Service Germany (23) 291.3 7% $32,090.2 19% 14.0 $1,360.5 231,624 182,000 38 39 Euroline Sweden 244.7 17% $13,786.3 –7% 95.2 $4,196.3 21,407 29,751 39 38 Bankia Spain 237.4 11% $14,739.8 12% 3.3 $382.8 90,313 86,339 40 40 Vakifbank Turkey 176.3 17% $11,933.0 23% 24.3 $1,654.5 135,474 160,021Figures are net (gross minus chargebacks). (1) Visa and MasterCard credit, debit, and prepaid cards including Electron and Maestro. Change in volume is based on local currency. (2) Web-based fi gures include all card brands (Visa, MasterCard, American Express, Diners Club, JCB, UnionPay, and domestic general purpose credit and debit cards). (3) Figures are for bank-owned POS terminals only. (4) Carte Bancaire fi gures (8.2 mil., $0.49 bil.) are not included. (5) Includes Credit Lyonnais. Carte Bancaire fi gures (5.8 mil., $0.34 bil.) are not included. (6) Includes Norway, Denmark, Estonia, Latvia, and Lithuania. (7) Includes the Santander Elavon Merchant Services joint venture in Spain. (8) Carte Bancaire fi gures (4.3 mil., $0.25 bil.) are not included. (9) Carte Bancaire fi gures (2.9 mil., $0.21 bil.) are not included. (10) Includes Liechtenstein, Luxembourg, Germany, Italy, Poland, Hungary, Belgium, and Austria. (11) Carte Bancaire fi gures (2.7 mil., $0.21 bil.) are not included. (12) Includes its pan-European operation in Germany, e-Service in Poland, Popular Payments in Spain, BOI Payment Acceptance in Ireland, and BOI U.K. Payment Acceptance in Northern Ireland. (13) Joint venture between la Caixa and Global Payments. (14) Includes Germany, Austria, Poland, Russia, Croatia, Bulgaria, Romania, Ukraine, Hungary, Czech Republic, Slovakia, Slovenia, Bosnia, Serbia, and Ajerbaijan. (15) Subsidiary of Nets. (16) Carte Bancaire fi gures (1.4 mil., $0.09 bil.) are not included. (17) Includes Russia, Ukraine, Belarus, Romania, Bulgaria, Slovakia, Czech Republic, Poland, Croatia, Bosnia, Serbia, Kosovo, and Albania. (18) Bancomat fi gures (359.0 mil., $26.13 bil.) are not included. (19) Carte Bancaire fi gures (1.1 mil., $0.05 bil.) are not included. (20) Includes acquiring in Norway, Finland, and Denmark. (21) Includes Romania, Czech Republic, Croatia, Hungary, Serbia, Ukraine, and Slovakia. (22) Girocard fi gures (29.0 mil., $4.25 bil.) are not included. (23) Acquires for 85% of German savings banks. Girocard fi gures (535.0 mil., $36.39 bil.) are not included. © 2015 The Nilson Report

Largest Merchant Acquirers in Europe 2014

© 2015 HSN Consultants, Inc. THE NILSON REPORT 11JUNE 2015 / ISSUE 1065 / THE NILSON REPORT

2013. Locations include physical and online merchant outlets, ATMs, bank branches, and other outlets where cardholders can obtain cash.

The second largest card acceptance network in the world is operated by Discover Financial Services. Its network of 31.0 million locations increased by 5.3 million locations in 2014. Discover is owner of Diners Club International. Acceptance locations in the Discover Network are open to Diners Club cards. Discover’s network growth in 2014 came from a network-to-network link to UnionPay. The companies

have a reciprocal sharing agreement. As each grows, so does the other. Other Discover Network growth came from acquirers including Atos (Belgium), Societe Generale (France), GlobalCollect (worldwide), Global Payments (U.K.), BBL (Thailand), and Alipay (China).

South Korea-based BC Card is the largest acquirer in the Asia-Pacific region measured by the number of Visa, MasterCard, JCB, UnionPay, BC Card, and other transactions handled in 2014. It also issues cards with the Visa, MasterCard, and BC Card brands. It licenses the BC Card brand to other issuers, mostly in South Korea. BC Cards carry bank

identification numbers (BINs) issued by Discover, and have access to all of the acceptance locations available in the Discover Network.

RuPay debit cards issued in India also carry BINs provided by Discover, giving those cardholders global acceptance on the Discover Network. Financial institution members of the National Payments Corporation of India (NPCI) issue RuPay cards, which compete against Visa and MasterCard. RuPay credit cards will be introduced in 2016. RuPay debit cards exceeded 120 million at year-end 2014. NPCI

and UnionPay are discussing a network-to-network link. The RuPay

domestic network links 1 million POS terminals and 20,000 online merchants.

Japan-based JCB issues credit cards in Japan and licenses card issuing to financial institutions in other countries. All cardholders have access to 27.9 million acceptance locations worldwide, an increase of 11.8% or nearly 3 million over year-end 2013. Approximately 70% of JCB acceptance locations are outside Japan. Adyen and European Merchant Services added JCB card acquiring in Europe last year. Redeban Multicolor, Colombia’s largest acquirer, added JCB card acceptance in 2014.

China-based UnionPay has 27.8 million acceptance locations worldwide — one-third are in China where acceptance locations now exceed 9.5 million. Locations outside of China are in more than 140 countries. UnionPay has the fastest growing acceptance network among all global brands.

American Express’s network of merchant acceptance locations, ATMs, and over-the-counter acceptance locations is now 18.7 million worldwide. Growth in 2014 was the strongest in the company’s history and occurred in the U.S. and all other regions.

Prior issues: 1036, 1014

JCB’s merchant acceptance network grew 11.7% over the prior year.

Global AcceptanceLocations

* Estimate. © 2015 The Nilson Report

Brand (mil.)

Visa & MasterCard 39.6Discover/Diners 31.0BC Card 31.0RuPay 31.0JCB 27.9UnionPay 27.8American Express 18.7*

Global Brands Card Acceptance Worldwide from page 1...

12 VISIT US ONLINE AT WWW.NILSONREPORT.COM Order Back Issues / Preview Upcoming Conferences / View Newsletter Archive

© 2015 HSN Consultants, Inc. THE NILSON REPORT All Rights Reserved. Reproducing or allowing reproduction or dissemination of any portion of this newsletter in any manner for any purpose is strictly prohibited and may violate the intellectual property rights of HSN Consultants, Inc. dba The Nilson Report.

David Robertson, PublisherJune 16, 2015

![Surprise Me If You Can: Serendipity in Health Informationstatic.tongtianta.site/paper_pdf/7247e7d2-4bfa-11e9-b101... · 2019. 3. 21. · “filter bubbles” [40] and “blind spots”](https://img.pdfslide.net/doc/110x75/5fe0b9e24d40e15dec1ab7fa/surprise-me-if-you-can-serendipity-in-health-2019-3-21-aoefilter-bubblesa.jpg)