Embed Size (px)

Citation preview

Global Competitiveness, Market Demand

and the US Plastics Processing Industry

Platts Asian Petrochemicals Markets Conference 2016

Grand Hyatt Pudong

Shanghai, China

August 30-31, 2016

Presented By:

Michael D. Taylor

Vice President, International Affairs and Trade

Agenda Introduction to SPI

Shale Gas – A Game Changer

Overview of the U.S. Plastics Industry

Trade Flows in Plastics

SPI Plastics Market Watch

Key End Market Demand

Global Manufacturing Competitiveness

Q&A

SPI – The Plastics Industry

Trade Association

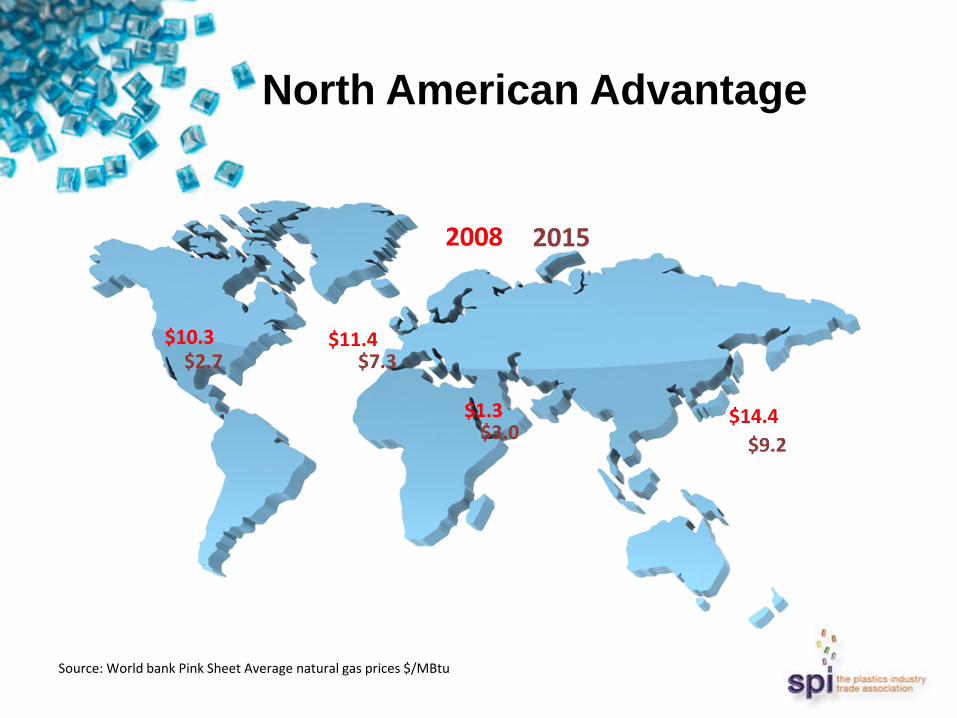

North American Advantage

Source: World bank Pink Sheet Average natural gas prices $/MBtu

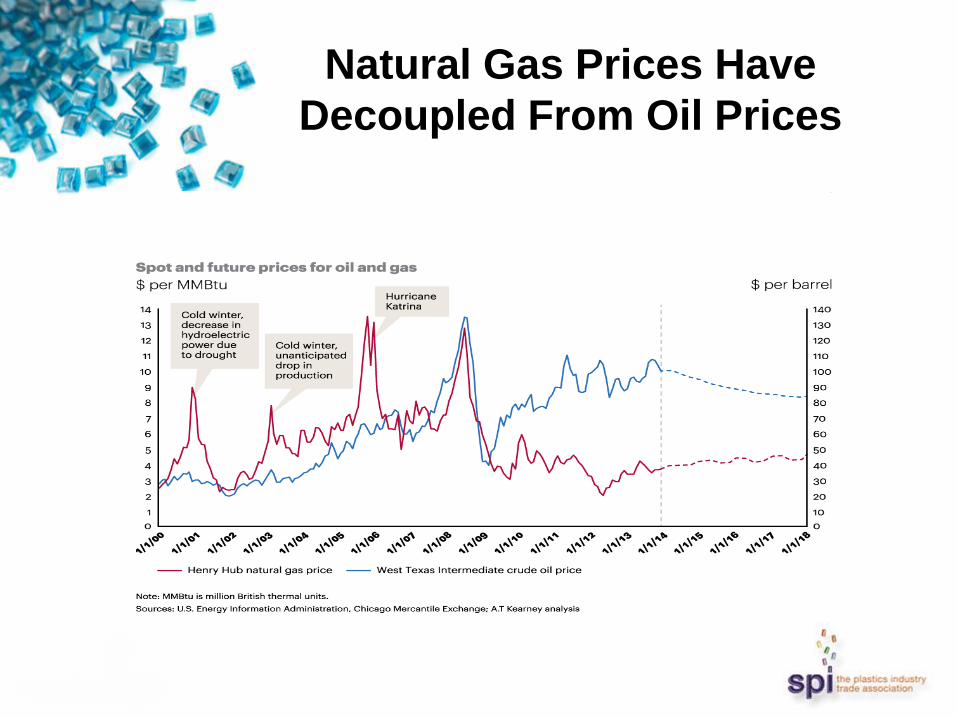

Natural Gas Prices Have

Decoupled From Oil Prices

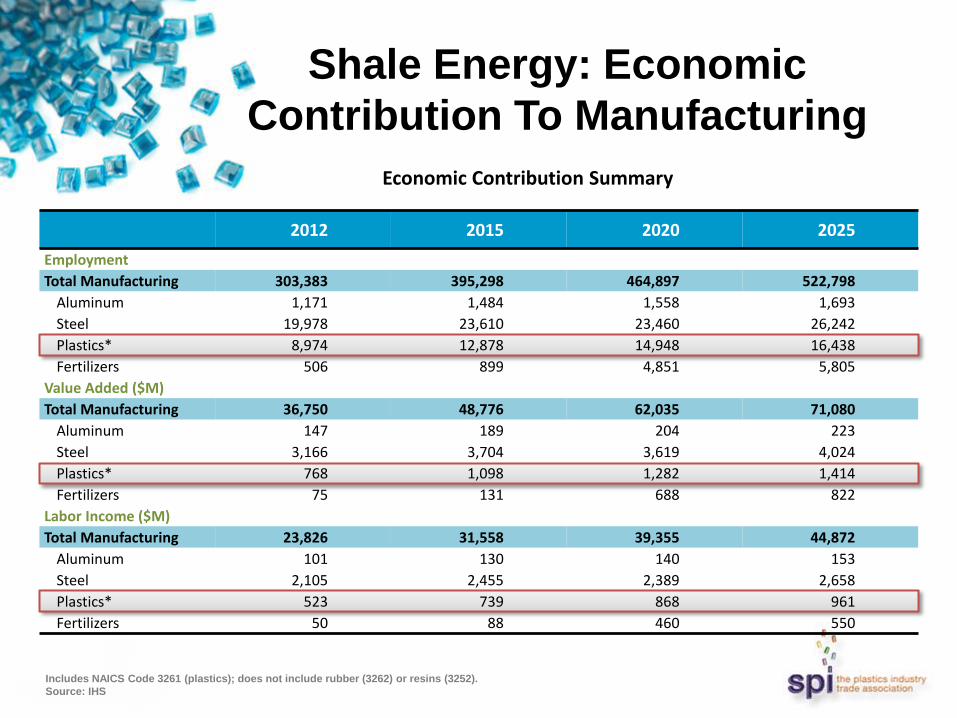

Shale Energy: Economic

Contribution To Manufacturing

2012 2015 2020 2025

Employment

Total Manufacturing 303,383 395,298 464,897 522,798

Aluminum 1,171 1,484 1,558 1,693

Steel 19,978 23,610 23,460 26,242

Plastics* 8,974 12,878 14,948 16,438

Fertilizers 506 899 4,851 5,805

Value Added ($M)

Total Manufacturing 36,750 48,776 62,035 71,080

Aluminum 147 189 204 223

Steel 3,166 3,704 3,619 4,024

Plastics* 768 1,098 1,282 1,414

Fertilizers 75 131 688 822

Labor Income ($M)

Total Manufacturing 23,826 31,558 39,355 44,872

Aluminum 101 130 140 153

Steel 2,105 2,455 2,389 2,658

Plastics* 523 739 868 961

Fertilizers 50 88 460 550

Economic Contribution Summary

Includes NAICS Code 3261 (plastics); does not include rubber (3262) or resins (3252).

Source: IHS

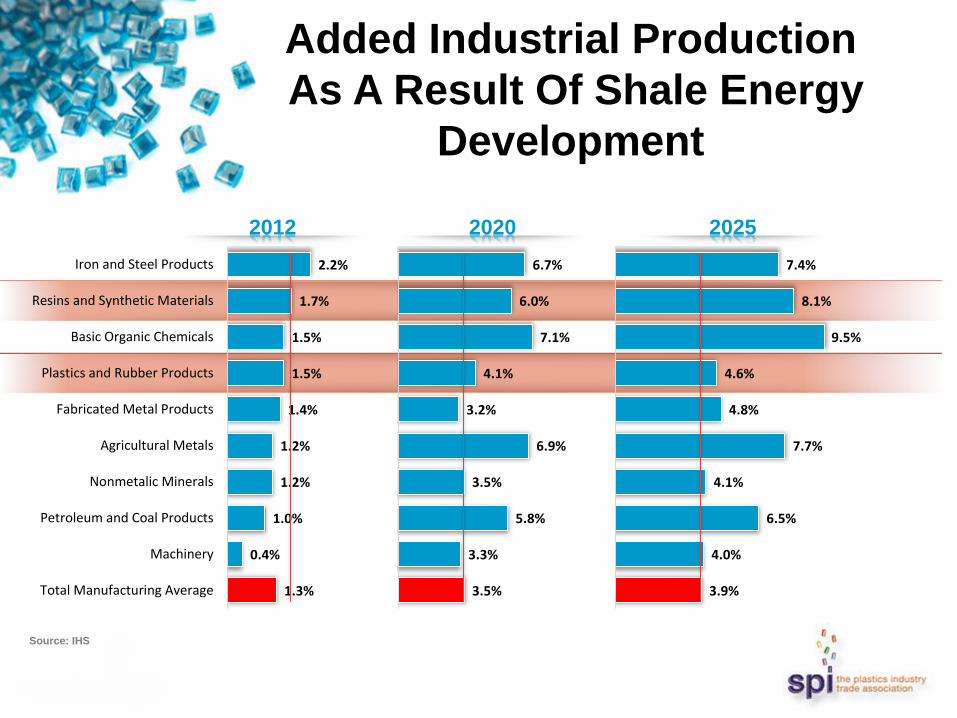

Added Industrial Production

As A Result Of Shale Energy

Development

Source: IHS

2.2%

1.7%

1.5%

1.5%

1.4%

1.2%

1.2%

1.0%

0.4%

1.3%

Iron and Steel Products

Resins and Synthetic Materials

Basic Organic Chemicals

Plastics and Rubber Products

Fabricated Metal Products

Agricultural Metals

Nonmetalic Minerals

Petroleum and Coal Products

Machinery

Total Manufacturing Average

2012

6.7%

6.0%

7.1%

4.1%

3.2%

6.9%

3.5%

5.8%

3.3%

3.5%

2020

7.4%

8.1%

9.5%

4.6%

4.8%

7.7%

4.1%

6.5%

4.0%

3.9%

2025

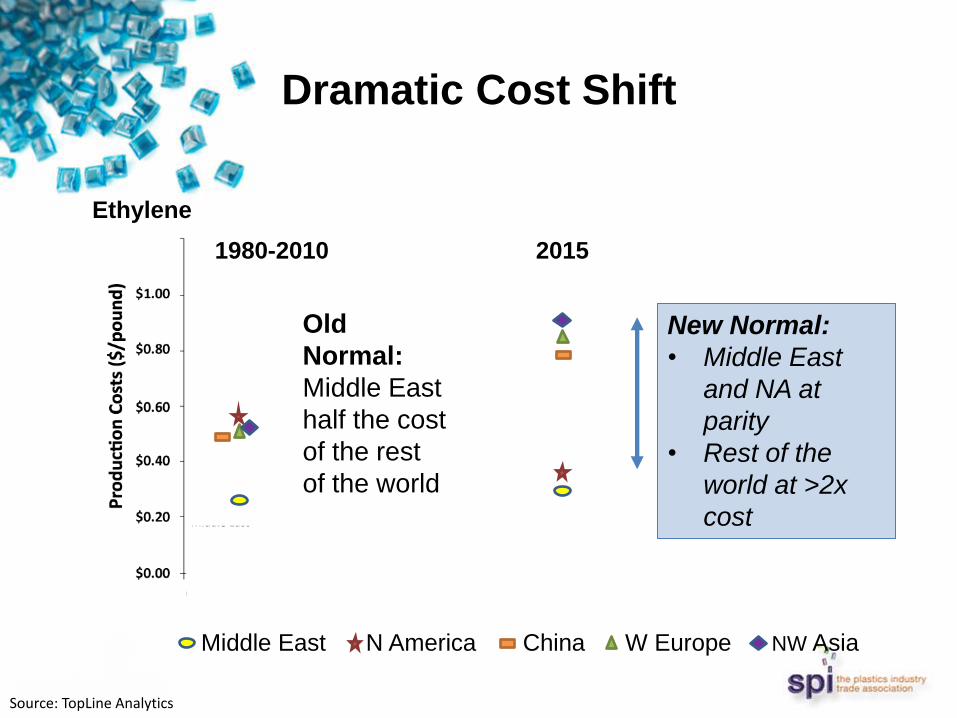

Dramatic Cost Shift

Ethylene

1980-2010

Middle East N America China W Europe NW Asia

Old

Normal:

Middle East

half the cost

of the rest

of the world

2015

New Normal:

• Middle East

and NA at

parity

• Rest of the

world at >2x

cost

Source: TopLine Analytics

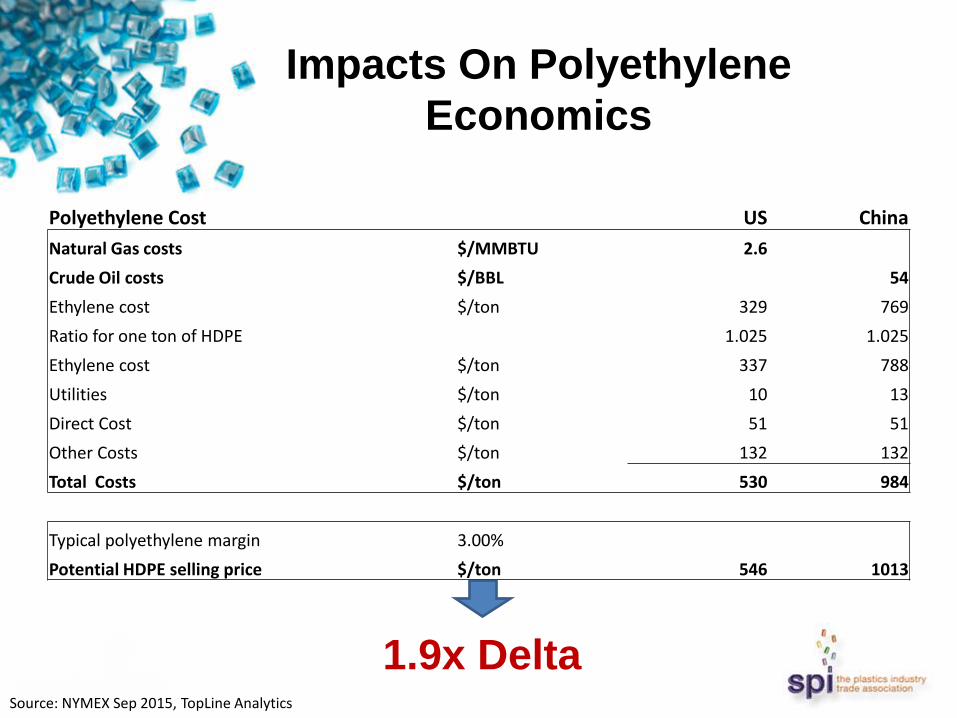

Impacts On Polyethylene

Economics

1.9x Delta Source: NYMEX Sep 2015, TopLine Analytics

Polyethylene Cost US China

Natural Gas costs $/MMBTU 2.6

Crude Oil costs $/BBL 54

Ethylene cost $/ton 329 769

Ratio for one ton of HDPE 1.025 1.025

Ethylene cost $/ton 337 788

Utilities $/ton 10 13

Direct Cost $/ton 51 51

Other Costs $/ton 132 132

Total Costs $/ton 530 984

Typical polyethylene margin 3.00%

Potential HDPE selling price $/ton 546 1013

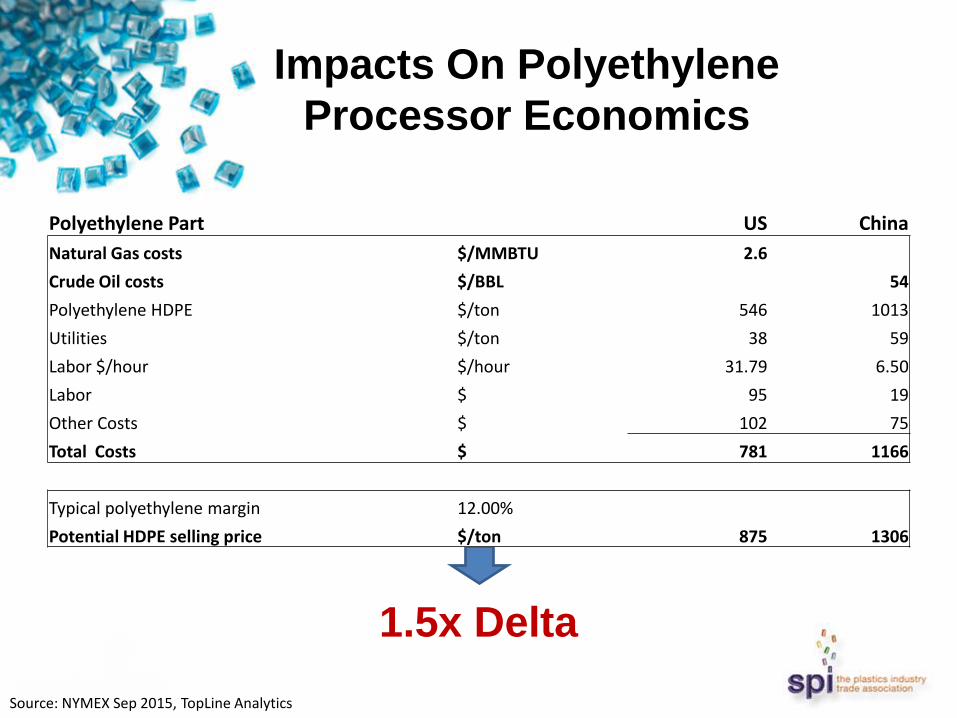

Impacts On Polyethylene

Processor Economics

1.5x Delta

Source: NYMEX Sep 2015, TopLine Analytics

Polyethylene Part US China

Natural Gas costs $/MMBTU 2.6

Crude Oil costs $/BBL 54

Polyethylene HDPE $/ton 546 1013

Utilities $/ton 38 59

Labor $/hour $/hour 31.79 6.50

Labor $ 95 19

Other Costs $ 102 75

Total Costs $ 781 1166

Typical polyethylene margin 12.00%

Potential HDPE selling price $/ton 875 1306

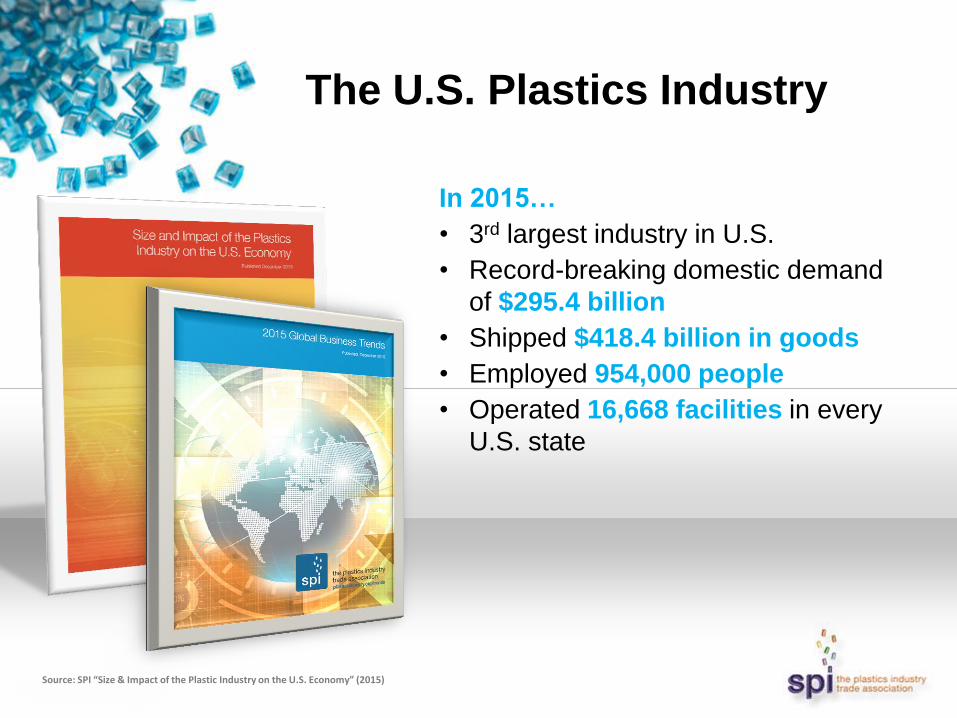

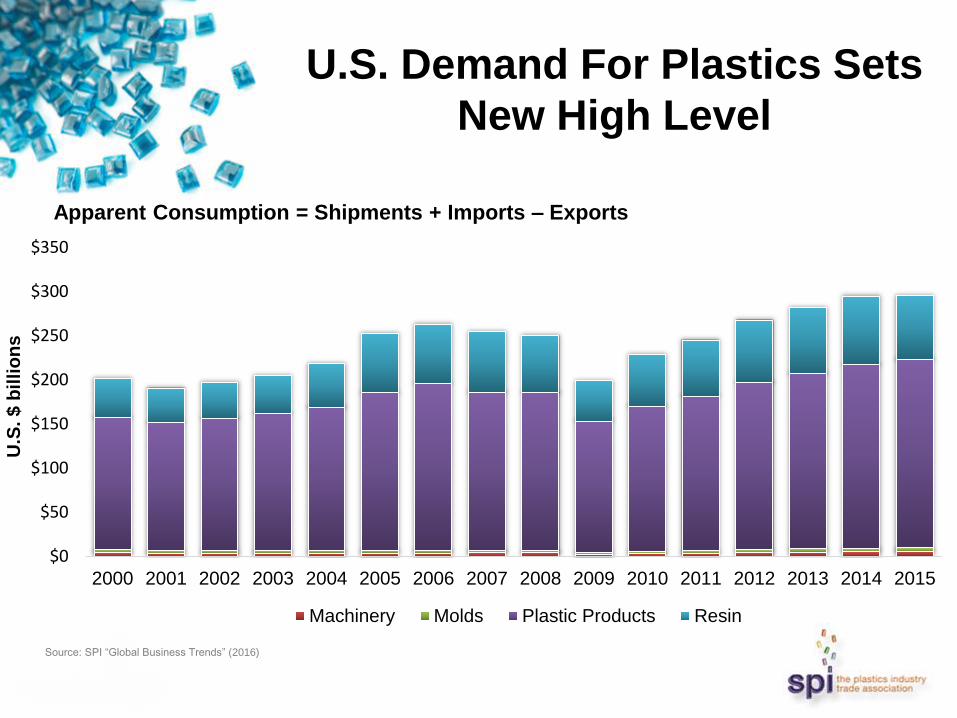

The U.S. Plastics Industry

In 2015…

• 3rd largest industry in U.S.

• Record-breaking domestic demand

of $295.4 billion

• Shipped $418.4 billion in goods

• Employed 954,000 people

• Operated 16,668 facilities in every

U.S. state

Source: SPI “Size & Impact of the Plastic Industry on the U.S. Economy” (2015)

U.S. Demand For Plastics Sets

New High Level

$0

$50

$100

$150

$200

$250

$300

$350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

U.S

. $

bil

lio

ns

Machinery Molds Plastic Products Resin

Apparent Consumption = Shipments + Imports – Exports

Source: SPI “Global Business Trends” (2016)

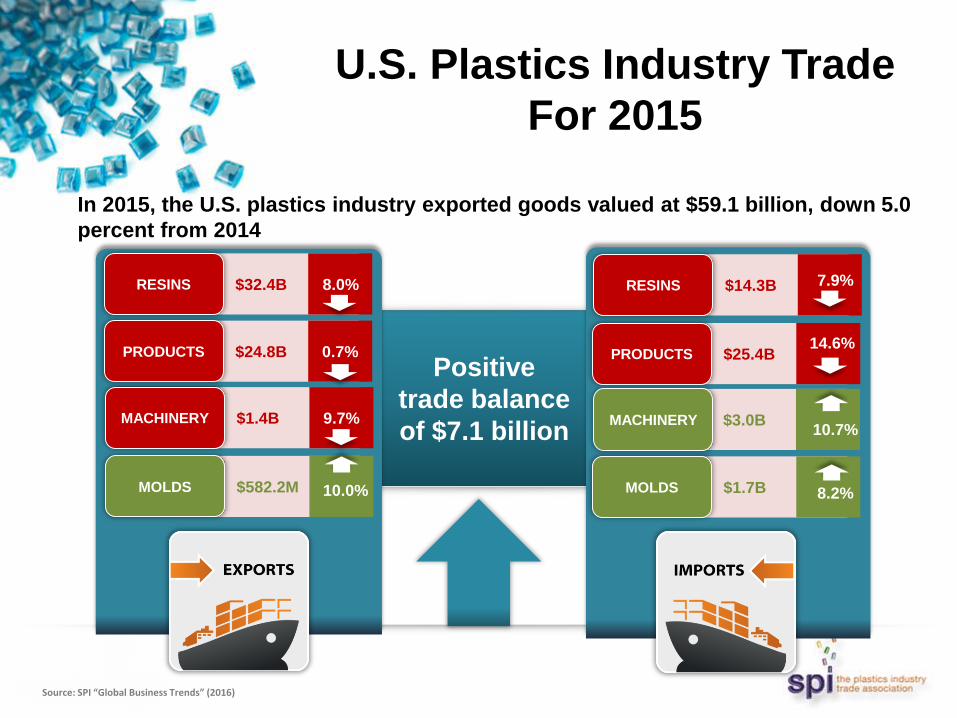

Positive

trade balance

of $7.1 billion

U.S. Plastics Industry Trade

For 2015

In 2015, the U.S. plastics industry exported goods valued at $59.1 billion, down 5.0

percent from 2014

$32.4B RESINS 8.0%

$24.8B PRODUCTS 0.7%

$582.2M MOLDS 10.0%

$1.4B MACHINERY 9.7%

$14.3B RESINS 7.9%

$25.4B PRODUCTS

$3.0B MACHINERY

$1.7B MOLDS

14.6%

10.7%

8.2%

Source: SPI “Global Business Trends” (2016)

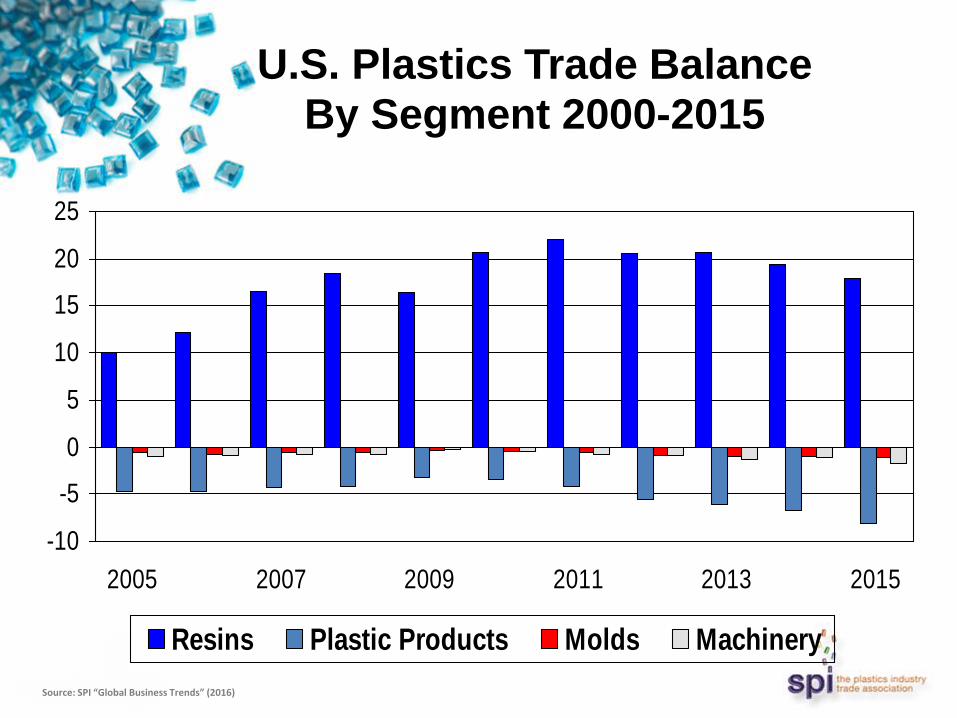

-10

-5

0

5

10

15

20

25

2005 2007 2009 2011 2013 2015

Resins Plastic Products Molds Machinery

U.S. Plastics Trade Balance By Segment 2000-2015

Source: SPI “Global Business Trends” (2016)

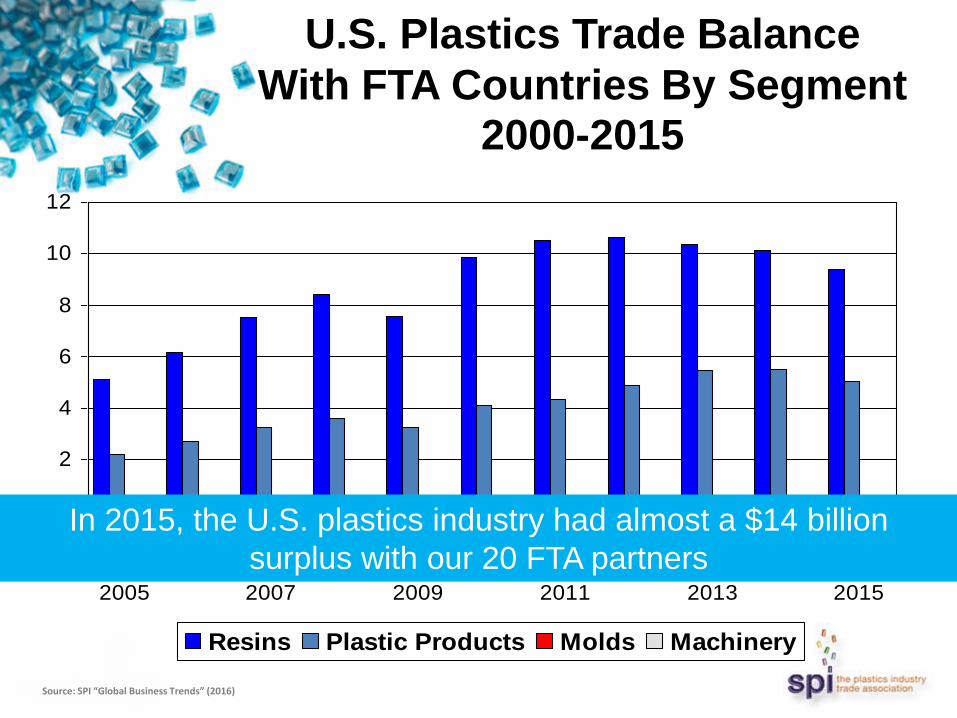

-2

0

2

4

6

8

10

12

2005 2007 2009 2011 2013 2015

Resins Plastic Products Molds Machinery

U.S. Plastics Trade Balance

With FTA Countries By Segment 2000-2015

In 2015, the U.S. plastics industry had almost a $14 billion

surplus with our 20 FTA partners

Source: SPI “Global Business Trends” (2016)

PMW Reports Released: Automotive & Transportation, Healthcare &

Medical Devices, Packaging, Building & Construction, Auto Recycling

Scheduled Reports: Bioplastics, Bottling, Consumer Electronics

SPI Plastics Market Watch

To Get Your Complimentary Copies: www.plasticsindustry.org/marketwatch

Continued Growth In Housing

Market Forecasted

2012 2013 2014 2015 2016 2017 2018

Housing Activity

(000)

Total Housing Starts 784 928 1,001 1,108 1,182 1,313 1,425

Single Family 537 620 647 713 806 930 1,057

Multifamily 247 308 355 395 376 383 368

New Single Family

Sales 368 430 440 503 574 685 779

Existing Single

Family Home Sales 4,125 4,475 4,338 4,627 4,816 4,923 4,965

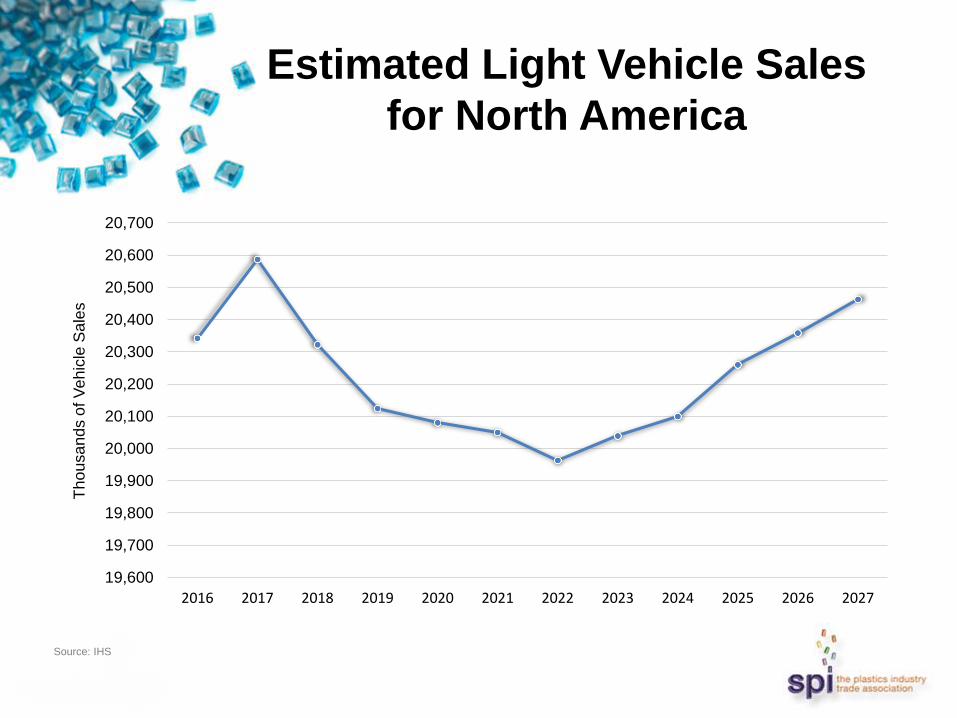

Estimated Light Vehicle Sales

for North America

19,600

19,700

19,800

19,900

20,000

20,100

20,200

20,300

20,400

20,500

20,600

20,700

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Th

ou

sa

nd

s o

f V

eh

icle

Sa

les

Source: IHS

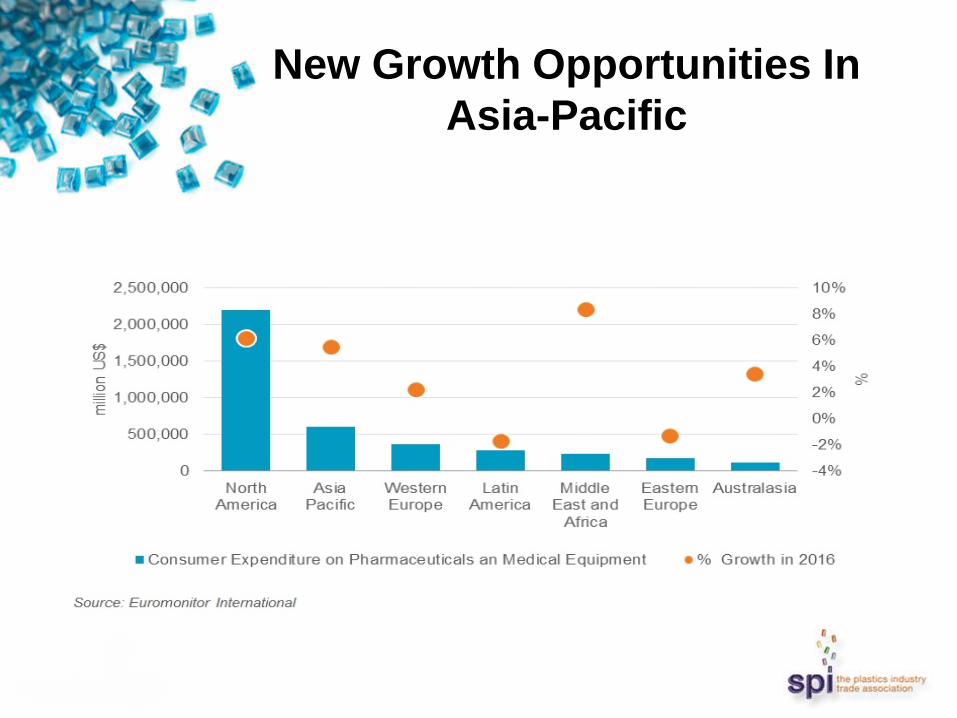

New Growth Opportunities In

Asia-Pacific

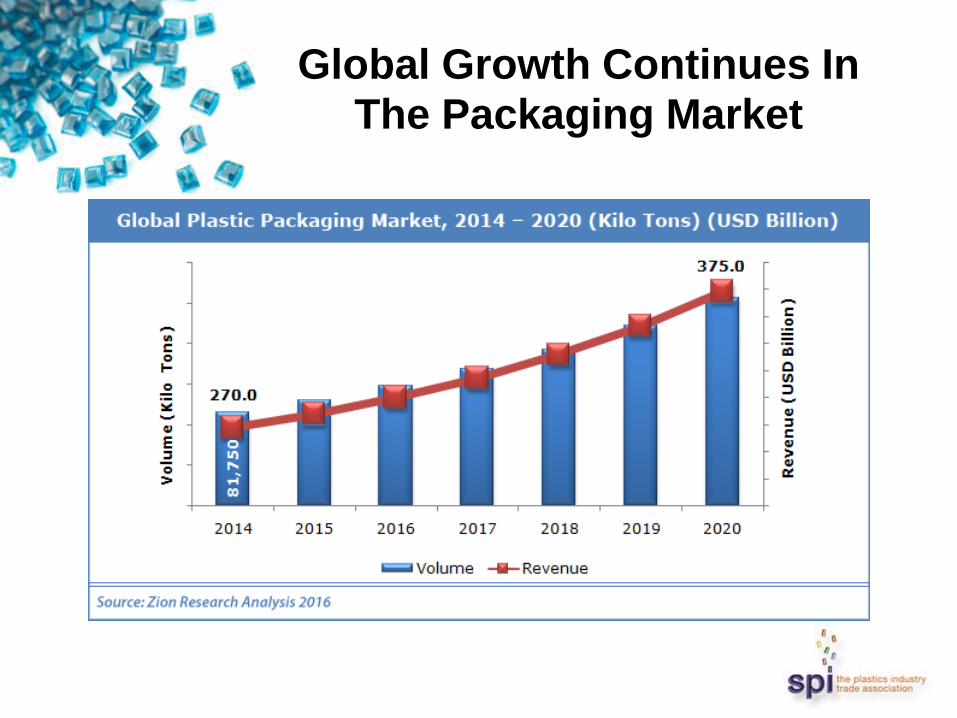

Global Growth Continues In The Packaging Market

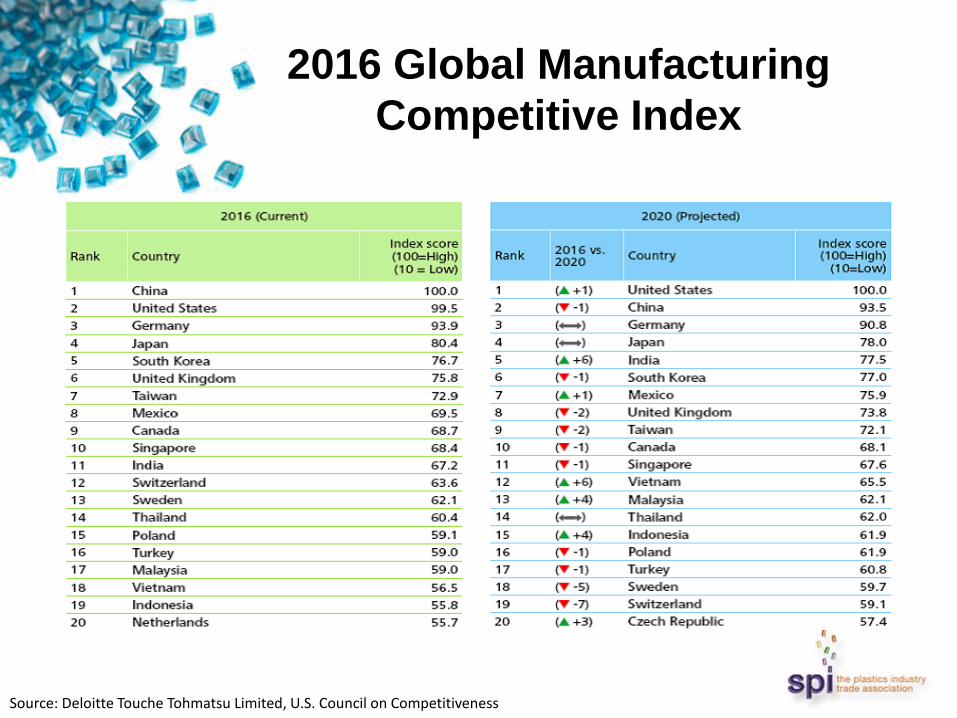

2016 Global Manufacturing

Competitive Index

Source: Deloitte Touche Tohmatsu Limited, U.S. Council on Competitiveness

Shifting Dynamics Among

Global Manufacturing Nations

• As the digital and physical worlds converge within

manufacturing, executives indicate the path to

manufacturing competitiveness is through advanced

technologies.

• Shift to higher value, advanced manufacturing tilts the

advantage to developed nations in the future.

• Two regional clusters of strength emerge.

• BRIC breaks down.

• The rise of the “Mighty Five“ (Malaysia, India, Thailand,

Indonesia and Vietnam or MITI-V).

Concluding Thoughts

• Manufacturing renaissance?

• Transformed global energy situation

• Reshoring

• Skilled labor shortage

• Advanced manufacturing, smart manufacturing, innovation, productivity

• Additive manufacturing

• Whither free trade?

• Risks – Known

– Unknown

Thank You!

谢谢 Merci Vielen Dank

Grazie ありがとうございました 감사합니다

Obrigado Спасибо Gracias Teşekkürler

Questions & Answers

Michael Taylor

Vice President, International Affairs & Trade

+1 202-974-5232