Embed Size (px)

Citation preview

Global Forces Shaping Urban Mobility

Club of Amsterdam – Future of Mobility - January 30th 2014

Rohit Talwar - CEO – Fast Future Research

www.fastfuture.com [email protected] Twitter @fastfuture

Contents

• Presentation p. 3

• About Fast Future p. 34

• Image Sources p. 43

• Background Notes p. 48

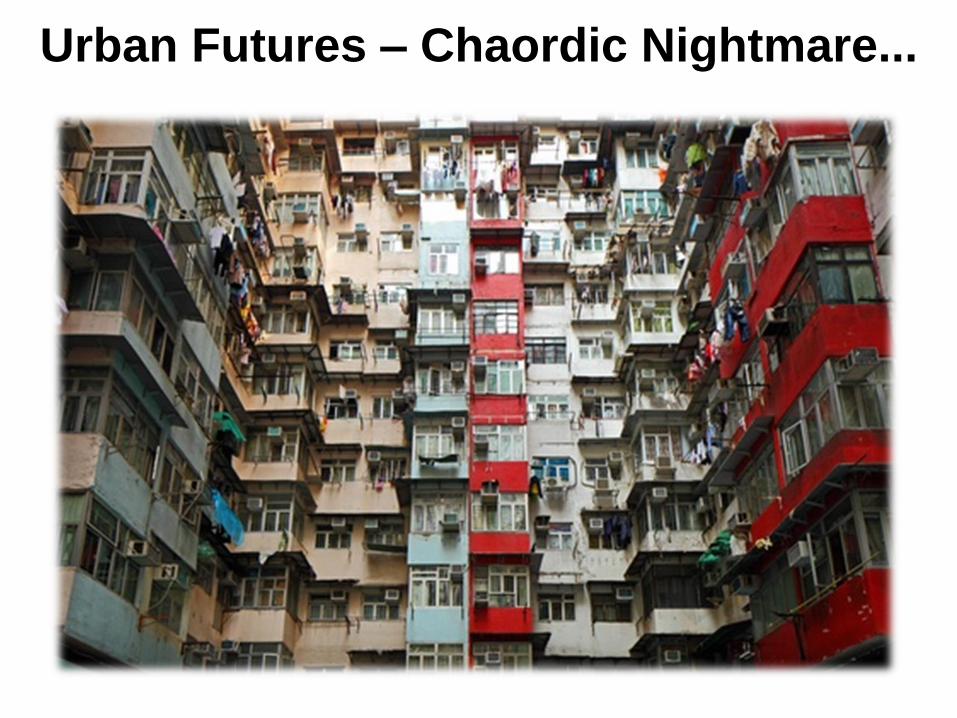

Urban Futures – Chaordic Nightmare...

...or Resource-Efficient Utopia

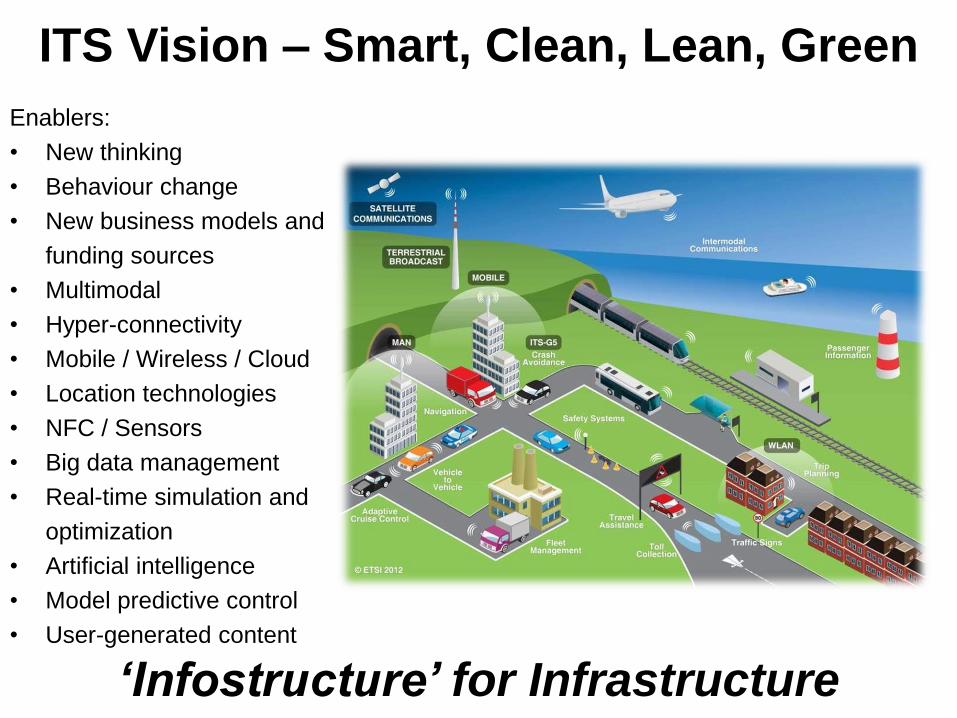

ITS Vision – Smart, Clean, Lean, Green

Enablers:

• New thinking

• Behaviour change

• New business models and

funding sources

• Multimodal

• Hyper-connectivity

• Mobile / Wireless / Cloud

• Location technologies

• NFC / Sensors

• Big data management

• Real-time simulation and

optimization

• Artificial intelligence

• Model predictive control

• User-generated content

‘Infostructure’ for Infrastructure

The Future is Being Created Now...

Economic and Political Uncertainty

and Turbulence are the ‘New Normal’

Continued Global Shifts Of

Influence, Wealth and

Power to Emerging Markets

Socio-Demographic Shifts are

Reshaping Society

Free education is a game changer

Sustainability Issues Will Play a

Bigger Role in Decision Making

Assets: ‘Usership’ vs. Ownership

Citizens Have an Expanded Role e.g.

Crowd Funded Bridge - Rotterdam

Rapid Execution e.g. Superfast Construction

Ark Hotel - Dongting Lake - China

Our Technologies are Evolving From

Desktop, Portable and Mobile ...

...to Wearable...

...to Embedded...

... to Grown and Grafted...

…and totally Connected via

‘The Internet of Everything’

“What happens when the smartest thing in the room is the room itself?”

Madeleine Albright

Speech / gesture / image recognition, integrated analytics, knowledge management,

image / video / voice mining, client self-service, intelligent documents, expertise

systems, collaboration, secure email, virtual assistants, intelligent agents and

collective intelligence

Artificial Intelligence is Going

Mainstream

Automation is Accelerating…

....and eliminating jobs

Science is Opening up New Horizons

‘Magic’ and Science are Blurring

The biological era is emerging

Challenges - Developing Viable

Green / Electric Vehicle Strategies

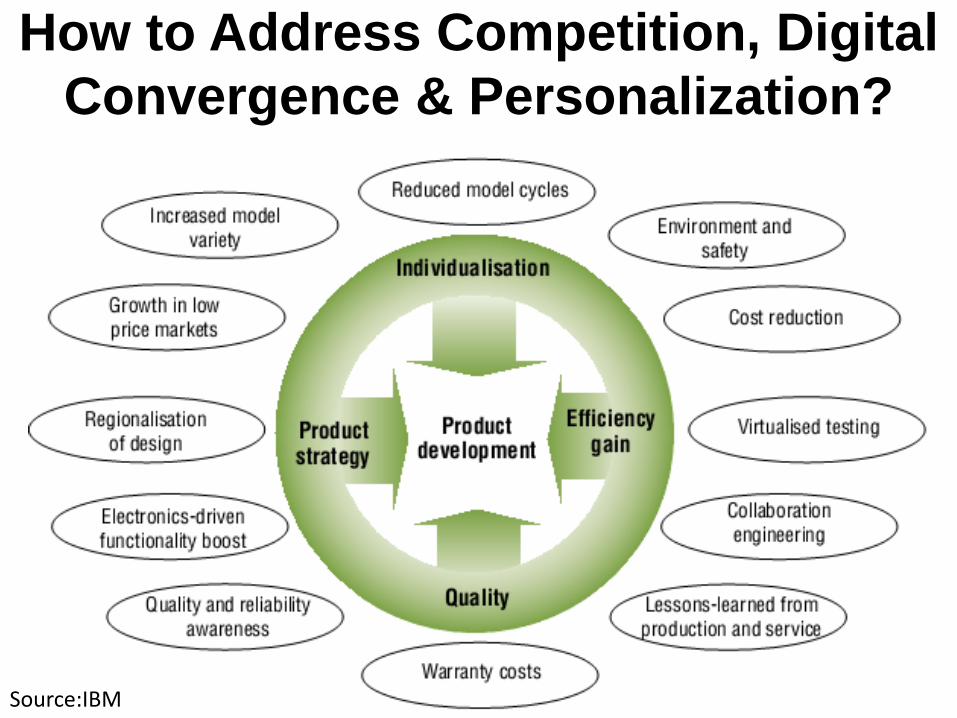

How to Address Competition, Digital

Convergence & Personalization?

Source:IBM

How do we Balance Value,

Innovation and Speed?

What New Business Models are we

Exploring?

Whole System Change for Driverless

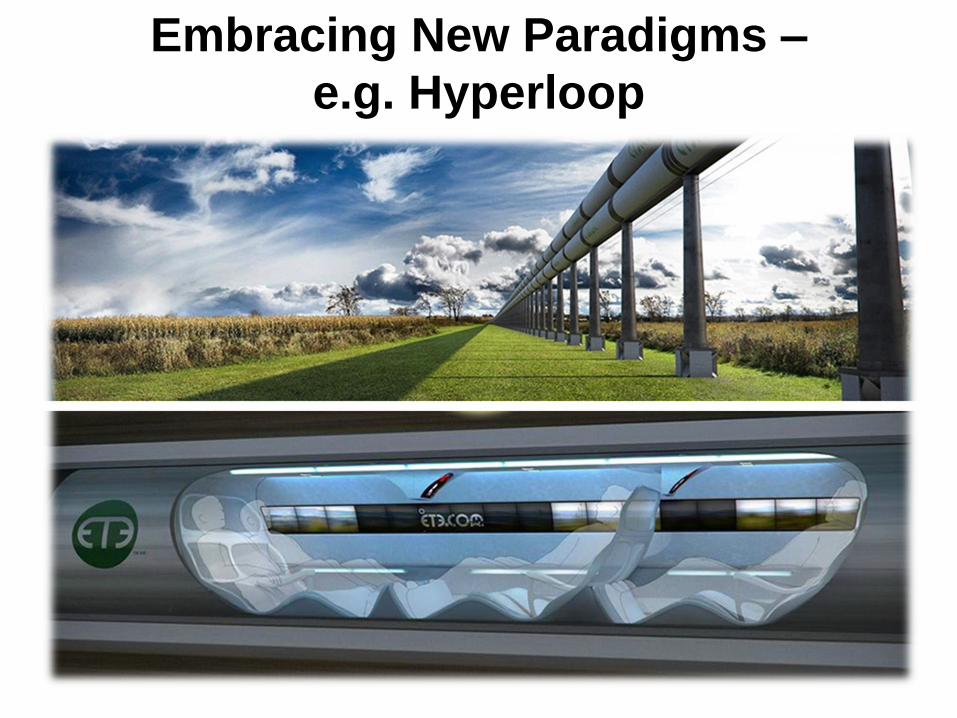

Embracing New Paradigms –

e.g. Hyperloop

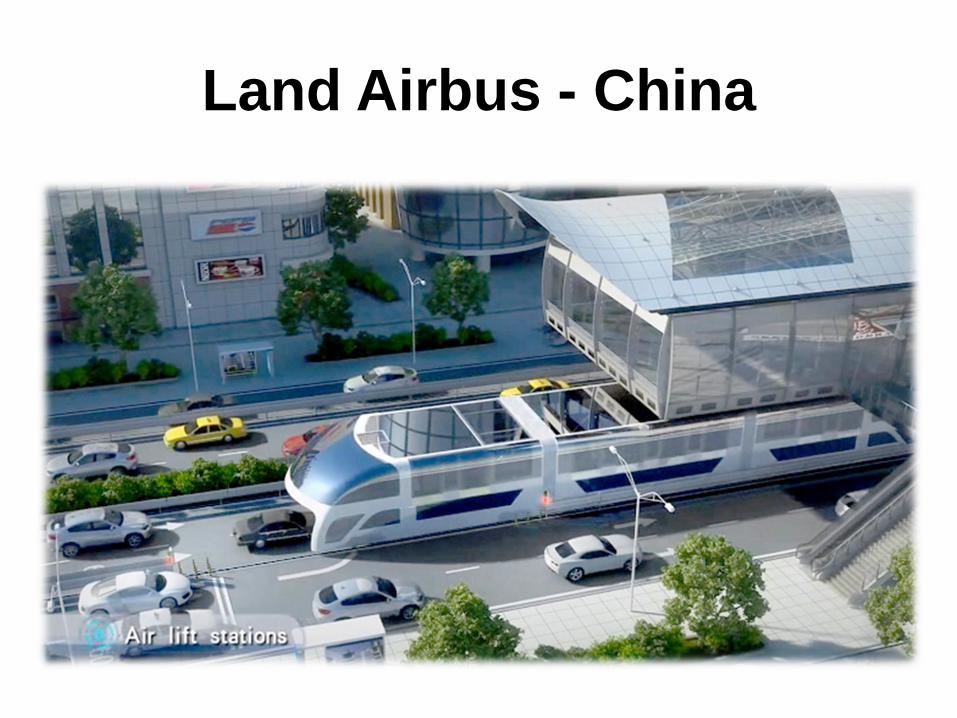

Land Airbus - China

String Theory

(High Tension Cables)

Tubular Rails

Human-powered Mass Transport (E.g. Shweeb - Agroventures New Zealand)

Conclusions

• What is our planning

horizon?

• Which forces, factors and

assumptions are we building

into our strategies?

• How robust is our thinking in

the face of alternative

scenarios?

• Where can we disrupt, what

could disrupt us?

About Fast Future

Fast Future –

Core Services

• Live Events - Speeches, briefings and workshops for executive management and boards of governments, investment funds, development agencies , companies, airlines, airports, hotels, venues, CVB’s and associations

• Future Insights - Customised research on emerging trends, future scenarios, technologies and new markets

• Immersion - ‘Deep dives’ on future trends, market developments, emerging issues and technology advances

• Strategy - Development of strategies and business plans

• Innovation - Creation of business models and innovation plans

• Engagement - Consultancy and workshop facilitation

Fast Future • Research, consulting, speaking, leadership

• 5-20 year horizon - focus on ideas, developments, people,

trends and forces shaping the future

• Clients

– ING, ABN Amro, Laing O’Rourke

– Marks and Spencer

– Airports - Aeroports de Paris / Schiphol Group

– Vancouver Airport Services

– Industry Associations – ICCA, ASAE, PCMA, MPI

– Corporates - GE, Nokia, Pepsi, IBM, Intel, Orange,

O2, Siemens, Samsung, GSK, SAPE&Y, KPMG,

Amadeus, Sabre, Travelport, Travelex, ING,

Santander, Barclays, Citibank, DeutscheBank

– Governments - Dubai, Finland, Nigeria, Singapore,

UK, US

– Convention Bureaus – Seoul, Sydney, London, San

Francisco, Toronto, Abu Dhabi, Durban, Athens,

Slovenia, Copenhagen

– Convention Centres – Melbourne,

Adelaide, Qatar, QEIICC

– Hotels - Accor Group, Preferred,

– Intercontinental

– PCO’s - Congrex, Kenes

Our Services Bespoke research; Identification &

Analysis of Future Trends, Drivers &

Shocks

Accelerated Scenario

Planning, Timelining &

Future Mapping

Identification of

Opportunities for

Innovation and Strategic

Investment Strategy Creation &

Development of

Implementation

Roadmaps

Design & Facilitation of

Innovation, Incubation

& Venturing

Programmes

Expert Consultations &

Futures Think Tanks

Personal Futuring for

Leaders and Leadership

Teams

Public Speaking, In-

Company Briefings,

Seminars and

Workshops

Example Projects • Public and private client research e.g. :

– Reinventing the Airport Ecosystem

– Development of Market Scenarios, emerging trends and strategies for key clients

– Government and OECD Scenario Projects – e.g. Migration 2030, Future of Narcotics, Chemical Sector, Family 2030

– Scenarios for the global economy for 2030 and the implications for migration

– Designing Your Future (Published August 2008) – book written for the American Society of Association Executives & The

Center for Association Leadership

– Global Economies – e.g. The Future of China – the Path to 2020

– The Shape of Jobs to Come – Emerging Science and Technology Sectors and Careers

– Winning in India and China

– The Future of Human Resources

– Exploiting the Future Potential of Social Media in UK Small to Medium Enterprises

– Convention 2020 – the Future of Business Events

– Future Convention Cities Initiative – Maximising Long-term Economic Impact of Events

– One Step Beyond – Future trends and challenges for the events industry

– Hotels 2020: Beyond Segmentation – Future Hotel Strategies

– The Future of Travel and Tourism in the Middle East – a Vision to 2020

– Future of Travel and Tourism Investment in Saudi Arabia

Hotels 2020 – Objectives

• Identify key drivers of change

for the globally branded hotel

sector over the next decade

• Examine the implications for:

Hotel strategy

Brand portfolio

Business models

Customer targeting

Innovation

• Global strategic foresight study to help the meetings industry prepare for

the decade ahead - Industry-wide sponsors

• Multiple outputs Nov 2009 – December 2011

• Current studies on future strategies for venues and destinations

Convention 2020

Rohit Talwar • Global futurist and founder of Fast Future Research.

• Award winning speaker on future insights and strategic

innovation – addressing leadership audiences in 40 countries on

5 continents

• Author of Designing Your Future

• Profiled by UK’s Independent Newspaper as one of the Top 10

Global Future Thinkers

• Led futures research, scenario planning and strategic

consultancy projects for clients in telecommunications,

technology, pharmaceuticals, banking, travel and tourism,

environment, food and government sectors

• Clients include 3M, BBC, BT, BAe, Bayer, Chloride, DTC De

Beers, DHL, EADS, Electrolux, E&Y, GE, Hoover, Hyundai, IBM,

ING, Intel, KPMG, M&S, Nakheel, Nokia, Nomura, Novartis,

OECD, Orange, Panasonic, Pfizer, PwC, Samsung, Shell,

Siemens, Symbian, Yell , numerous international associations

and governments agencies in the US, UK, Finland, Dubai,

Nigeria, Saudi Arabia and Singapore.

• To receive Fast Future’s newsletters please email

• 50 key trends

• 100 emerging trends

• 10 major patterns of change

• Key challenges and choices for

leaders

• Strategic decision making framework

• Scenarios for 2012

• Key futures tools and techniques

• Published August 2008

• Price £49.95 / €54.95/ $69.95

• Email invoice request to

Designing Your Future Key Trends, Challenges and Choices

Image Sources

Image Sources p.1

Page:

1. http://2.bp.blogspot.com/-i2lsRx2NtUI/UeL7jdKNBuI/AAAAAAAAAPs/GhbgGozH1NU/s1600/CiudadFuturo.jpg

3. http://cdn.theatlanticcities.com/img/upload/2013/05/06/shutterstock_132797276/largest.jpg

4. http://img.photobucket.com/albums/v303/wreckless13/Zeitgeist/TVP2010A/aircraft.jpg

5. http://www.etsi.org/images/files/membership/ETSI_ITS_09_2012.jpg

6. http://www.yourformula.eu/wp-content/uploads/2012/09/shutterstock_97807763.jpg

7. Left, right:

http://img.timeinc.net/time/magazine/archive/covers/2009/1101091207_400.jpg

http://tctechcrunch2011.files.wordpress.com/2013/05/bitcoin.png%3Fw%3D640

8. http://upload.wikimedia.org/wikipedia/commons/6/61/Map_of_emerging_markets.JPG

9. Clockwise:

http://inclusionparadox.com/wp-content/uploads/2010/04/Multi-generational_Latino.jpg

http://batonrouge.myhomecareblog.com/files/2011/07/active_seniors4.jpg

http://discoverwebsbest.files.wordpress.com/2011/06/khan-academy.jpg

10. http://www.wallpaperex.com/wallpapers/green_environmental_issues_mac_wallpapers_hd_634101_jpeg-wide.jpg

Image Sources p.2

11. Left, right:

http://3008docklands.com.au/article/neighbourhood/1490

http://www.answers.com/topic/cloud-computing

12. http://inhabitat.com/rotterdams-wooden-luchtsingel-footbridge-is-a-fantastic-piece-of-crowdfunding-architecture/

13. http://www.dailymail.co.uk/news/article-2083883/Ark-Hotel-construction-Chinese-built-30-storey-hotel-scratch-15-days.html

14. Left, right:

http://quietfurybooks.com/blog/wp-content/uploads/2012/09/original-cell-phone.jpg

http://www.universalexports.net/Movies/Graphics/18-gadgets/cellphone2.jpg

15. Clockwise:

http://cdn2.ubergizmo.com/wp-content/uploads/2013/01/Google_Glass_features_in_flux.jpeg

http://naturescrusaders.files.wordpress.com/2010/07/brain-computer-alsno-lead-art1.jpg

http://dustinkirk.com/blogpicsBig/Emotiv_Headset.jpg

17. http://www.mondolithic.com/wp-content/uploads/2010/02/You-Are-Only-Coming-Through-In-Waves.jpg

18. http://smartdesignworldwide.com/thinking/wp-content/uploads/internetofthings_480x324_final.jpg

19. http://overthemoonscifi.files.wordpress.com/2012/06/brain-mind.jpeg

Image Sources p.3

20. http://gizmaestro.com/wp-content/uploads/2011/09/Foxconns-Future-Robots.jpg

21. Clockwise:

http://www.midwich.com/common/userfiles/midwich/cube-cubeX.png

http://www.printedelectronicsworld.com/images/v5/articles/820x615/main3149.jpg

http://www.rumormillnews.com/pix5/nbic8.jpg

http://crnano.org/srg-iii-pov-animation2.gif

22. Top, bottom:

http://www.newsyaps.com/wp-content/uploads/2013/03/digital-brain.jpg

http://www.pakalertpress.com/wp-content/uploads/2012/06/Transhuman-Symbolism-in-Prometheus.png

23. Clockwise:

http://www.urdesign.it/wp-content/uploads/2013/08/2-armadillo-t-kaist-unveils-foldable-micro-electric-car.jpg

http://www.urdesign.it/wp-content/uploads/2013/08/1-armadillo-t-kaist-unveils-foldable-micro-electric-car.jpg

http://carinpicture.com/wp-content/uploads/2012/07/Audi-Urban-Concept-Spyder-2011-Photo-09-800x600.jpg

http://ucnauri.com/category/%E1%83%A3%E1%83%AA%E1%83%9C%E1%83%90%E1%83%A3%E1%83%A0%E1%83%98/page/11

Image Sources p.4

24. ftp://ftp.software.ibm.com/software/plm/de/challenges_automotive.pdf

25. http://i.co.uk/wp-content/uploads/2012/01/carInternet.png

26. http://www.businessmodelsinc.com/new-business-models-in-the-car-industry/

27. http://www.instablogsimages.com/1/2011/10/03/bmw_autonomous_car_dtcci.jpg

28. http://s3files.core77.com/blog/images/2013/05/high-speed-tube-01.jpg

29. http://assets.inhabitat.com/wp-content/blogs.dir/1/files/2013/09/Land-Airbus-TBS-China-1.jpg

30. http://www.gizmag.com/future-transport/22959/

31. http://www.gizmag.com/future-transport/22959/

32. http://www.gizmag.com/future-transport/22959/

33. Top, bottom:

http://ichef.bbci.co.uk/wwfuture/624_351/images/live/p0/0x/b6/p00xb6yp.jpg

http://www.huffingtonpost.co.uk/2013/11/06/milton-keynes-driverless-pods_n_4223397.html

Background Notes

Urbanisation Trends

• The UN forecasts that between 2011 and 2050, the world population is

expected to increase by 2.3 billion, passing from 7.0 billion to 9.3 billion.

• The population living in urban areas is projected to grow by 2.6 billion,

increasing from 3.6 billion in 2011 to 6.3 billion 2050.

• The urban areas of the world are expected to absorb all the population

growth expected over the next four decades.

• As a result, the world rural population is projected to start decreasing in

about a decade .

Source: UN, World Urbanisation Prospects (2011): http://esa.un.org/unup/pdf/WUP2011_Highlights.pdf

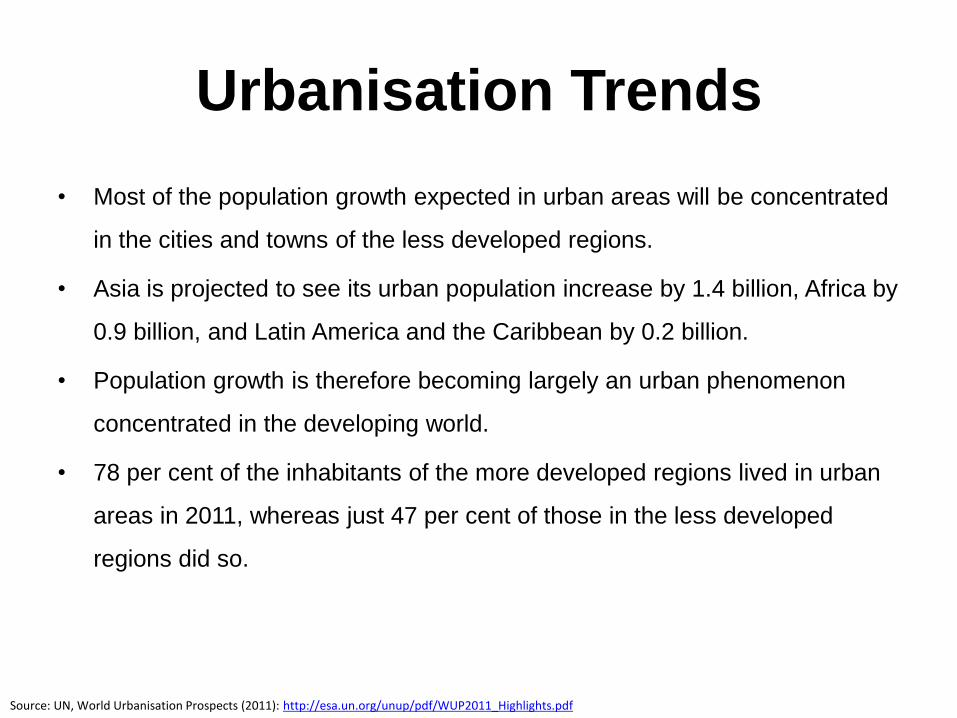

Urbanisation Trends

• Most of the population growth expected in urban areas will be concentrated

in the cities and towns of the less developed regions.

• Asia is projected to see its urban population increase by 1.4 billion, Africa by

0.9 billion, and Latin America and the Caribbean by 0.2 billion.

• Population growth is therefore becoming largely an urban phenomenon

concentrated in the developing world.

• 78 per cent of the inhabitants of the more developed regions lived in urban

areas in 2011, whereas just 47 per cent of those in the less developed

regions did so.

Source: UN, World Urbanisation Prospects (2011): http://esa.un.org/unup/pdf/WUP2011_Highlights.pdf

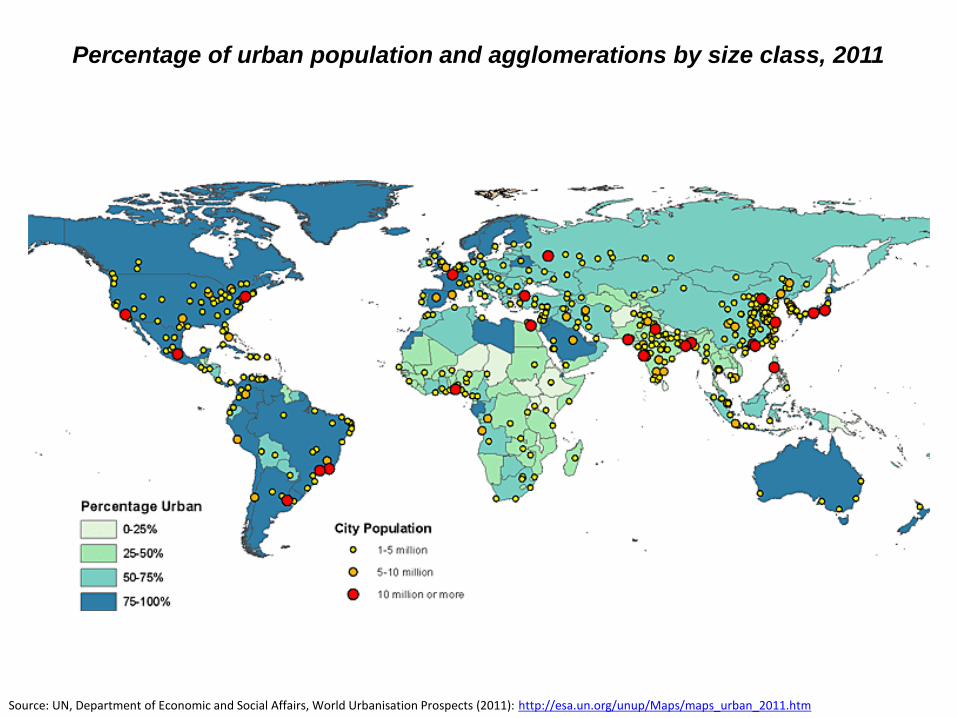

Source: UN, Department of Economic and Social Affairs, World Urbanisation Prospects (2011): http://esa.un.org/unup/Maps/maps_urban_2011.htm

Percentage of urban population and agglomerations by size class, 2011

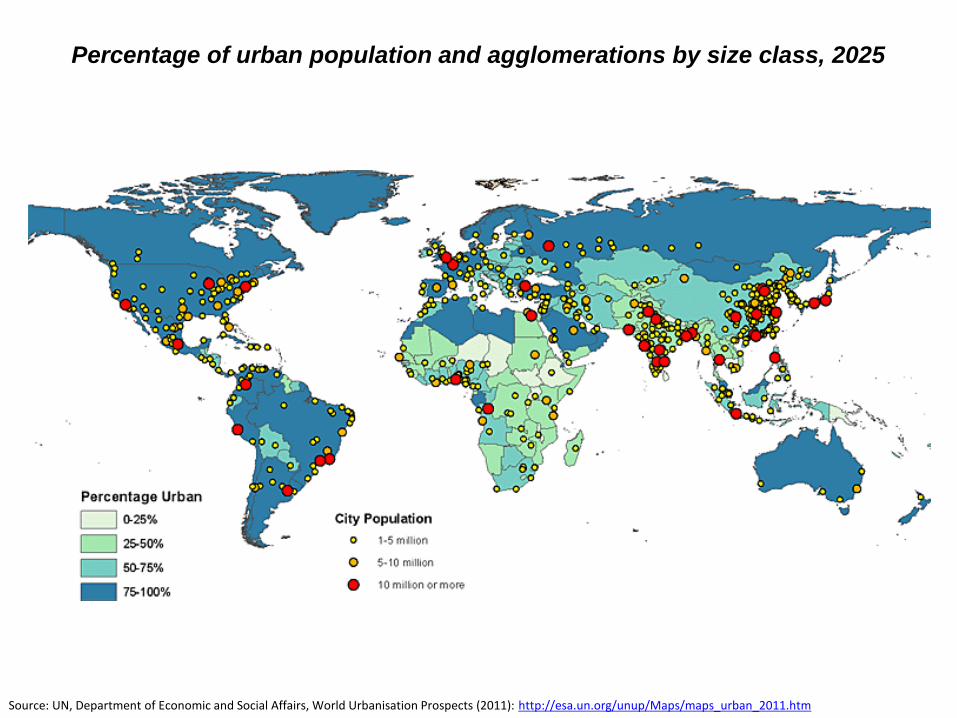

Percentage of urban population and agglomerations by size class, 2025

Source: UN, Department of Economic and Social Affairs, World Urbanisation Prospects (2011): http://esa.un.org/unup/Maps/maps_urban_2011.htm

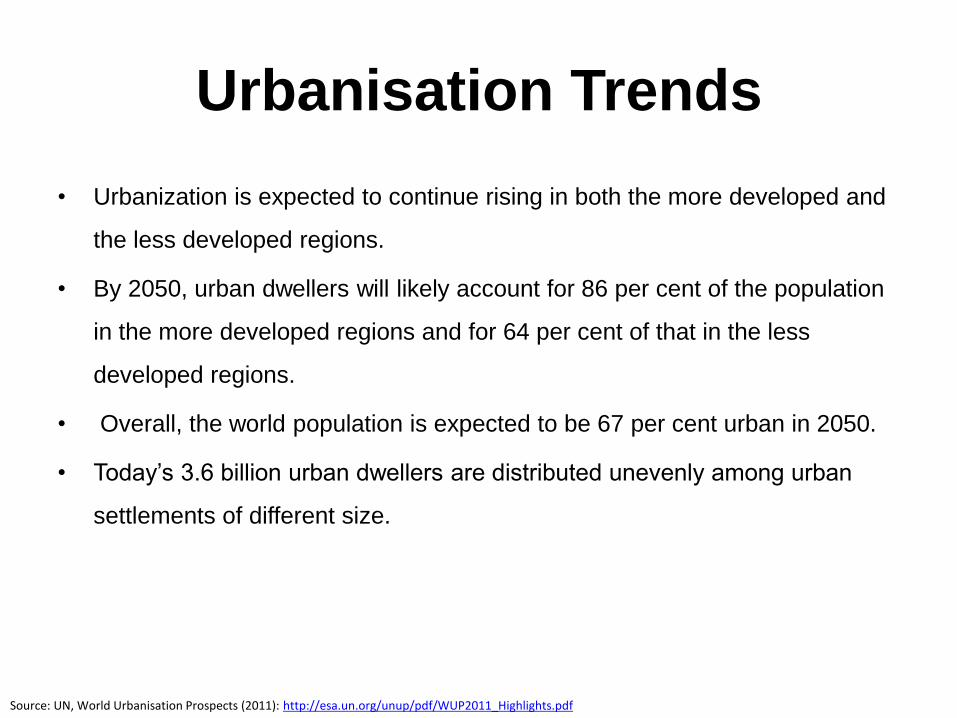

Urbanisation Trends

• Urbanization is expected to continue rising in both the more developed and

the less developed regions.

• By 2050, urban dwellers will likely account for 86 per cent of the population

in the more developed regions and for 64 per cent of that in the less

developed regions.

• Overall, the world population is expected to be 67 per cent urban in 2050.

• Today’s 3.6 billion urban dwellers are distributed unevenly among urban

settlements of different size.

Source: UN, World Urbanisation Prospects (2011): http://esa.un.org/unup/pdf/WUP2011_Highlights.pdf

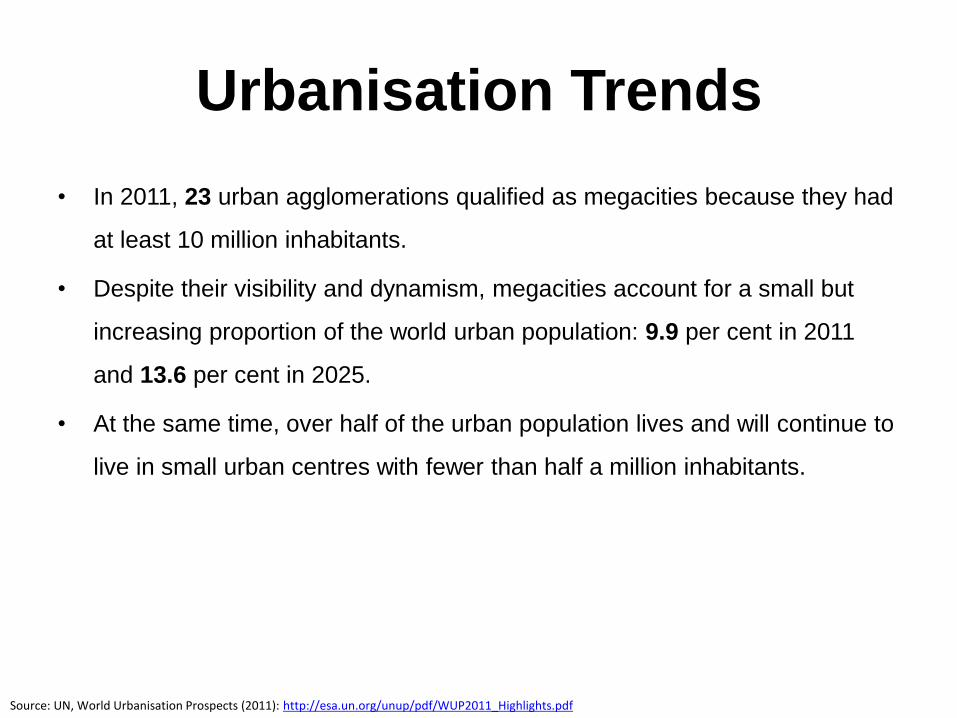

Urbanisation Trends

• In 2011, 23 urban agglomerations qualified as megacities because they had

at least 10 million inhabitants.

• Despite their visibility and dynamism, megacities account for a small but

increasing proportion of the world urban population: 9.9 per cent in 2011

and 13.6 per cent in 2025.

• At the same time, over half of the urban population lives and will continue to

live in small urban centres with fewer than half a million inhabitants.

Source: UN, World Urbanisation Prospects (2011): http://esa.un.org/unup/pdf/WUP2011_Highlights.pdf

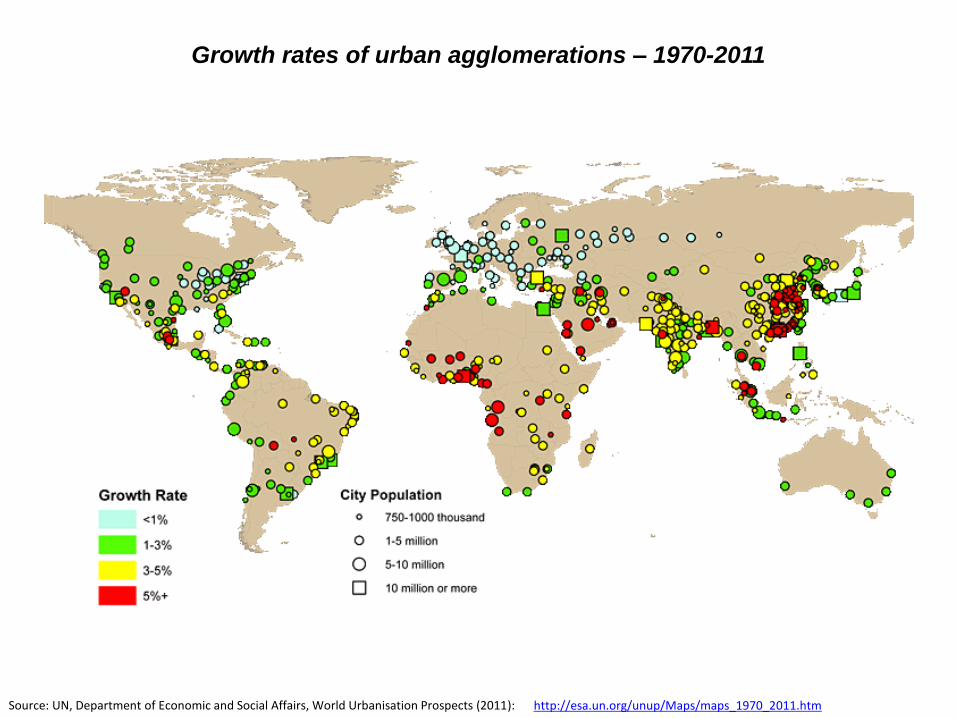

Growth rates of urban agglomerations – 1970-2011

Source: UN, Department of Economic and Social Affairs, World Urbanisation Prospects (2011): http://esa.un.org/unup/Maps/maps_1970_2011.htm

Source: UN, Department of Economic and Social Affairs, World Urbanisation Prospects (2011):

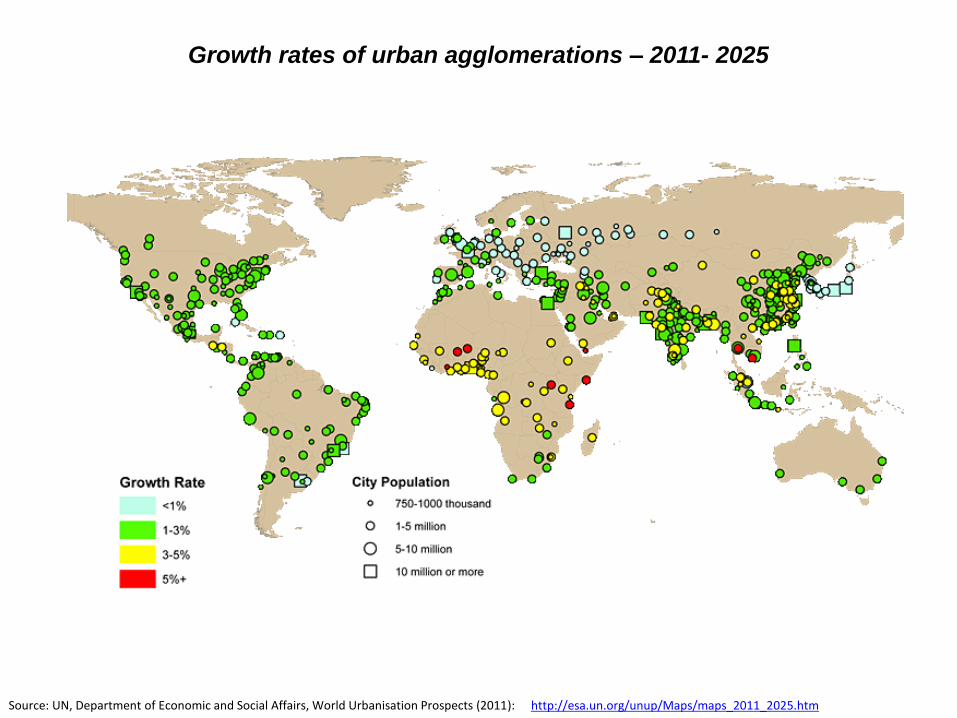

Growth rates of urban agglomerations – 2011- 2025

http://esa.un.org/unup/Maps/maps_2011_2025.htm

Growth Rates of Urban

Agglomeration

• The annual growth rates of urban agglomerations in the past (1970-2011

period) were higher than the growth rates that are projected for the future

(2011 to 2025 period).

• The growth of urban agglomerations will slow down, because many of them

have already reached a population of 1 million or more or have become

mega-cities with 10 or more million inhabitants.

Source: UN, Department of Economic and Social Affairs, World Urbanisation Prospects (2011): http://esa.un.org/unup/Maps/maps_2011_2025.htm

Intelligent Transport in Europe

• The future of mobility:

• A future based on 100% clean mobility is considered to be further out than

2030, but some of its main ingredients are already coming together and will

become increasingly evident in the years to come. Several socio-economic

trends, which include demographic and life-style changes, increasing

urbanization, shifting balance of the global economy and exponential growth

of connectivity between people and devices, will have an overwhelming

impact on how transport is used, its quality of delivery to the customer; and

its efficiency, and will result in the gradual emergence of new vehicle

concepts and new mobility patterns.

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Intelligent Transport in Europe

• Intelligent Transport Systems and rapidly evolving ICT technologies are

expected to play a key role in transforming transportation and delivering

safe, efficient, sustainable and seamless transport options for freight and

people across Europe.

• According to recent estimations, despite two decades of increasing

connectivity over high-tech networks, only 1 percent of what could be

connected in the world actually is, but in the coming years this number is

expected to go up dramatically.

• High-speed communication networks, crowdsourcing, cloud storage, social

networks, "internet of things/vehicles", advanced data analytics,

multiplication of mobile applications

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Intelligent Transport in Europe

• and massive amounts of data made available by proliferation of sensors are

the connectivity components will provide many new opportunities for personal

mobility and for transport of goods.

• The establishment of an integrated transport "info-structure", relying notably

on vehicle to vehicle (V2V) and vehicle to infrastructure (V2I)

communications, but also on the availability of open and quality transport

data, can provide substantial improvements for the performance of transport

networks and raise its efficiency.

• Automated and progressively autonomous applications will continue to evolve

in road transport both at tactical and strategic levels, offering the potential to

significantly improve not only traffic flows but also the safety level.

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Intelligent Transport in Europe

• On the way to more autonomous driving functions and vehicle systems, fault

tolerance and reliability of safety critical sensors, actuators, controllers, and

communication devices will be still areas of technological research.

• At a strategic level, navigation systems will evolve towards incorporation of

true predictive traffic information and optimal individual routing. Technologies

improving the Human Machine Interface (HMI) aspects will play a crucial role.

• Technological trends:

• Major scientific and technological trends that will impact the transport field can

be found in the ICT domain and constitute key enablers for the roll-out of

“intelligent” transport applications. Some of these include:

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Intelligent Transport in Europe

• Wireless networks: especially cellular networks and mobile

communications will be in a central role in the service provision to mobile

devices and to support V2I communication.

• Mobile devices: smartphones, tablets and other mobile devices provide the

most convenient way to interact with many of the traffic related services,

especially in a multi-modal traffic context and will continue to proliferate.

They will also provide the basis for a wealth of customised innovative

mobility solutions for various end-users (such as car/ride-sharing, parking

space location etc).

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Intelligent Transport in Europe

• Location technologies based on highly accurate, dynamically updated

maps are central enablers to contextualize services and collected data and

will be key for advanced tracking of vehicles, passengers and freights.

• Near Field Communications (NFC) use will grow in mobile payment and

expand to other areas.

• Sensors will be everywhere to observe the environment, provide data and

control systems. The envisioned Internet of Things and Machine to Machine

related technologies will emerge to manage the increasing complexity of

sensor networks.

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Intelligent Transport in Europe

• Massive data management, data fusion and data mining will be in the

heart of many traffic services; in addition, real-time requirements and

localisation computing puts pressure on computing power.

• Real-time simulation and optimization, artificial intelligence, model

predictive control alongside with management of uncertainty in transport

system simulation and modelling will lie at the heart of dynamic traffic

management and will require ever increased levels of robustness and fault

tolerance.

• User-generated content will play a more and more important role in

providing dynamic information.

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Intelligent Transport in Europe

• Cloud computing in its various forms provides solutions for the computing

and data intensive tasks.

• Innovative, contextual and safe user interaction is one of the most important

features of services in traffic context and new solutions utilizing, e.g.

multimodal and ergonomic user interfaces will be developed.

• Challenges and barriers for the successful deployment of intelligent

transport:

• Innovation amongst information services and network providers has

generally outpaced innovation in the regulatory environment, in

management structures and within transport service providers.

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Intelligent Transport in Europe

• All this requires strong political leadership and buy-in from transport

operators. New rules and management structures must be flexible enough to

evolve rapidly. At the same time location-based and traffic related services

have to provide robust built-in data privacy and security solutions and issues

related to liability must be solved.

• Additionally, integration of currently separated services will be one of the key

issues to be solved in the future. All these requirements shall be addressed at

an EU level with an integrated approach towards R&I activities, by tackling

simultaneously basic and applied research, proof of concept and

demonstration activities towards full scale deployment. Improved access to

risk finance, especially for SMEs, will be of key importance.

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Intelligent Transport in Europe

• The European, national and regional regulative framework should take all

these elements into account in view of developing and enacting truly

comprehensive and cohesive strategy in regards of roll-out of smart mobility

solutions by 2030.

• the Commission has initiated a process to develop a Strategic Transport

Technology Plan with its Communication Research and Innovation for

Europe's Future Mobility.

• It should form the basis for identifying strategic priorities for EU funding

schemes for research and innovation activities influencing transport system

development and deployment.

Source: Futurium, Smart Mobility-Intelligent Transport: http://ec.europa.eu/digital-agenda/futurium/en/content/smart-mobility-intelligent-transport

Transport 2050

• The European Commission has adopted a comprehensive strategy for a

competitive transport system that will increase mobility, remove major barriers in

key areas and fuel growth and employment. At the same time, the proposals will

dramatically reduce Europe's dependence on imported oil and cut carbon

emissions in transport by 60% by 2050.

• By 2050, key goals will include:

• No more conventionally-fuelled cars in cities.

• 40% use of sustainable low carbon fuels in aviation; at least 40% cut in shipping

emissions.

• A 50% shift of medium distance intercity passenger and freight journeys from

road to rail and waterborne transport.

• All of which will contribute to a 60% cut in transport emissions by the middle of

the century.

Source: Futurium, Transport 2050: http://ec.europa.eu/digital-agenda/futurium/en/content/transport-2050-commission-outlines-ambitious-plan-increase-mobility-and-reduce-emissions

Transport 2050

• The Transport 2050 roadmap to a Single European Transport Area sets out

to remove major barriers and bottlenecks in many key areas across the

fields of transport infrastructure and investment, innovation and the internal

market.

• The aim is to create a Single European Transport Area with more

competition and a fully integrated transport network which links the different

modes and allows for a profound shift in transport patterns for passengers

and freight. To this purpose, the roadmap puts forward 40 concrete

initiatives for the next decade.

Source: Futurium, Transport 2050: http://ec.europa.eu/digital-agenda/futurium/en/content/transport-2050-commission-outlines-ambitious-plan-increase-mobility-and-reduce-emissions

Transport 2050

• The Transport 2050 roadmap sets different goals for different types of journey -

within cities, between cities, and long distance.

• Urban transport:

• A big shift to cleaner cars and cleaner fuels is required. 50% shift away from

conventionally fuelled cars by 2030, phasing them out in cities by 2050.

• Halve the use of ‘conventionally fuelled’ cars in urban transport by 2030; phase

them out in cities by 2050; achieve essentially CO2-free movement of goods in

major urban centres by 2030.

• By 2050, move close to zero fatalities in road transport. In line with this goal, the

EU aims at halving road casualties by 2020. Make sure that the EU is a world

leader in safety and security of transport in aviation, rail and maritime.

Source: Futurium, Transport 2050: http://ec.europa.eu/digital-agenda/futurium/en/content/transport-2050-commission-outlines-ambitious-plan-increase-mobility-and-reduce-emissions

Challenges of Urban Mobility

• Hyper-mobility – the notion that more travel at faster speeds covering longer

distances generates economic prosperity – is a distinguishing feature of

urban areas.

• By 2005 approximately 7.5 billion trips were made each day in cities

worldwide. In 2050, there may be three to four times as many passenger-

kilometres travelled as in 2000.

• Mobility flows have become a key dynamic of urbanization, with the

associated infrastructure constituting the backbone of urban form.

• Despite the increasing level of urban mobility worldwide, access to places,

activities and services has become increasingly difficult and less convenient

in terms of time, cost and comfort.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

Challenges of Urban Mobility

• Current urbanization patterns are causing unprecedented challenges to

urban mobility systems, particularly in developing countries.

• These areas accounted for less than 40 per cent of the global population

growth in the early 1970s, this share has now increased to 86 per cent, and

is projected to increase to more than 100 per cent within the next 15 years.

• The world’s poorest regions that will experience the greatest urban

population increase. These are the regions that will face the greatest

challenges in terms of coping with increasing demands for improved

transport infrastructure.

• Projections indicate that Africa will account for less than 5 per cent of the

global investments in transport infrastructure during the next few decades.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

Challenges of Urban Mobility

• Influences of decentralized urban growth on mobility and travel

worldwide:

• Dispersal of growth from the urban centre, as a form of decentralization,

when poorly planned is at the hearth of unfolding patterns of urban

development that are environmentally, socially and economically

unsustainable.

• With dispersal come: lower densities, separation of land uses and urban

activities, urban fragmentation, segregation by income and social class,

consumption of precious resources such as farmland and open space and

more car-dependent systems.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

Challenges of Urban Mobility

• Urban dispersal has an unmistakable and profound influence on travel.

Spread-out growth not only lengthens journeys by separating trip origins

and destinations, but also increases the use of private motorized vehicles.

• In developed countries, suburban living has contributed to rising

motorization rates and the environmental problems related to car

dependency.

• When urban dispersal is driven almost exclusively by market forces and is

largely unplanned, car dependency, energy consumption, environmental

degradation and social problems in urban areas are further exacerbated.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

Challenges of Urban Mobility

• Overregulation of urban development (e.g. zoning codes that require

significant supplies of off-street parking) can also induce car-dependent

sprawl by suppressing market preferences.

• Trends both in developed and various developing countries suggest

that many young adults want to live incompact, walkable

neighbourhoods.

• Urban sprawl is increasingly prevalent in developing countries. From 1970

to 2000, the physical expansion of all urban areas in Mexico was nearly four

times more than their urban population growth.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

Mobility and Urban Form

• In Cairo (Egypt), Sana’a (Yemen), Panama City (Panama) and Caracas

(Venezuela), sprawl is blamed for consuming scarce agricultural lands and

dramatically increasing municipal costs for infrastructure and service

delivery.

• Global urban density patterns and trends

• Asian and African cities are, on average, around 35 per cent denser than

cities in Latin America, 2.5 times denser than European cities, and nearly 10

times denser than cities in North America and Oceania.

• 39 of the world’s 100densest urban areas were situated in Asia in 2010.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

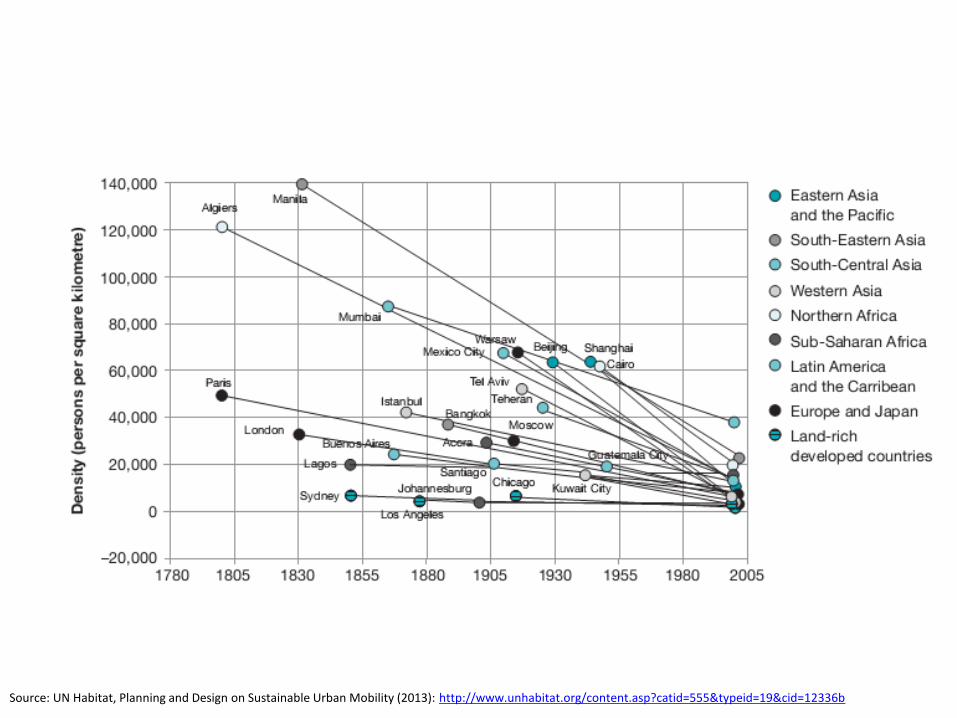

Mobility and Urban Form

• Cities of developing countries

have been sprawling more rapidly

than those in developed countries.

• From 1990 to 2000, average

urban densities fell from 3545 to

2835 people per square kilometre

in developed countries compared

to a drop from 9860 to 8050

people per square kilometre in

developing ones.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

Mobility and Urban Form

• Planning the accessible city:

• Coordinating and integrating urban transport and land development is

imperative to creating sustainable urban futures. Successfully linking the

two is a signature feature of ‘compact cities’ or ‘smart growth.

• Successful integration means making the connections between transport

and urban development work in both directions.

• The coordinated planning of urban mobility and land development starts

with a collective vision of the future city, shared by city government and

major stakeholders of civil society.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

Mobility and Urban Form

• Well-planned cities, such as Singapore, Stockholm (Sweden) and Curitiba

(Brazil), crafted cogent visions of the future to shape transportation

investments and achieve the best outcomes, whether measured in

economic prosperity, energy resourcefulness, cleanliness of the natural

environment or quality of life.

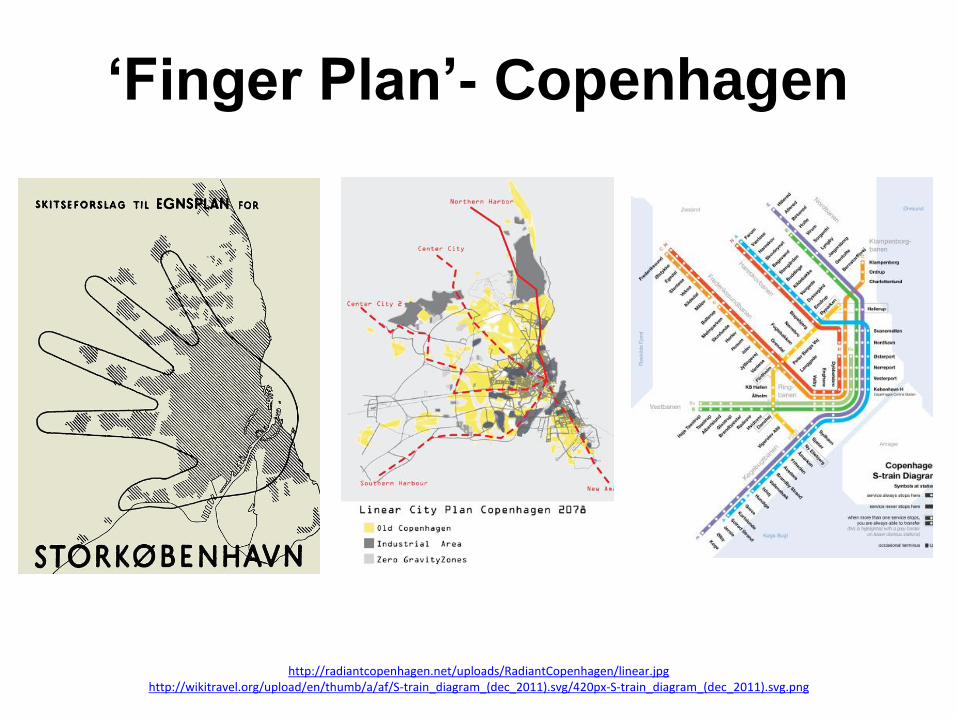

• The city of Copenhagen (Denmark) and its celebrated ‘Finger Plan’ is a

text-book example of a long-term planning vision, which shaped rail

investments and urban growth.

• A five-finger hand became the metaphor for defining where growth would

and would not occur.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

Mobility and Urban Form

• Each finger was oriented to a traditional Danish market town within the orbit

of metropolitan Copenhagen. The construction of rail-based public transport

was purposed to steer growth along the desired growth axes, in advance of

travel demand.

• Also, greenbelt wedges set aside as agricultural preserves, open space and

natural habitats were designated and major infrastructure was directed

away from the districts.

Source: UN Habitat, Planning and Design on Sustainable Urban Mobility (2013): http://www.unhabitat.org/content.asp?catid=555&typeid=19&cid=12336b

‘Finger Plan’- Copenhagen

http://radiantcopenhagen.net/uploads/RadiantCopenhagen/linear.jpg http://wikitravel.org/upload/en/thumb/a/af/S-train_diagram_(dec_2011).svg/420px-S-train_diagram_(dec_2011).svg.png

Regenerative Urbanisation

• The World Future Council (WFC) believes that a new model of urbanisation,

powered by renewable energy and defined by a regenerative, mutually

beneficial relationship between cities, rural areas and ecosystems, is

urgently needed.

• The Council advocates for going beyond sustainable cities to regenerative

cities.

• A long term target for cities should be ‘regenerating’ the same amount of

resources as they absorb - both in terms of cities’ ecological footprint and

the ecological burden of all materials used.

• In the following five cities, some aspects of regenerative urbanisation are

already a reality.

Source: World Future Council, 28/06/2012: http://power-to-the-people.net/2012/06/5-cases-of-regenerative-urbanisation/

Multimodal System – The Future

of Transport

• Eco-Business (2013) reports that time and traffic conditions in Singapore

are becoming rather unpredictable. There is growing on-road congestion

and a dilemma around balancing the increasing driving aspirations of

Singaporeans and the limited space available in the country. The rise of

commuters is also leading to overcrowding and delays – of trains and

buses.

• The government is placing emphasis on providing solutions and devising

policies to address both private and public transport concerns but another

issue has to be addressed as well: the commuter mind-set.

Source: Eco-Business, 22/04/2013:http://www.eco-business.com/opinion/singapores-transport-future-could-be-multimodal-system/

Multimodal System – The Future

of Transport

• To meet the demand for greater transportation capacities and address

mobility issues, new and attractive concepts are needed to simplify

intermodal travel and make it easier for travellers to optimise the usage of

various transport modes to reach their destination safe and conveniently.

• Challenges in Singapore:

• In the public’s best interest, the government is increasing the cost of vehicle

ownership. Limiting cars on the road and improving traffic flow, however,

have not been the end results. Instead, drivers tend to drive more frequently

to get the most out of their hefty investment.

• Singapore had to think of a better solution.

Source: Eco-Business, 22/04/2013:http://www.eco-business.com/opinion/singapores-transport-future-could-be-multimodal-system/

Multimodal System – The Future

of Transport

• In contrast, Singapore has the advantage of a widespread MRT or rail

network. This pushes the MRT as the primary means of transportation for

public commuters.

• Individuals who cannot afford a car but still want the convenience of

individual transport opt for taxis, but taxi bookings are often difficult during

peak periods.

• In order for Singapore to maintain an efficient transport network with

sustainable levels of road traffic, the country has to think of ways to

incorporate the benefits of both public and private transport.

Source: Eco-Business, 22/04/2013:http://www.eco-business.com/opinion/singapores-transport-future-could-be-multimodal-system/

Multimodal System – The Future

of Transport

• Siemens has developed an Integrated Mobility Platform (IMP) that takes

into account all the modes of transport and suggests the most feasible and

economic option for commuters.

• Operators can easily combine complementary mobility services with their

own portfolio. With this pool, the single platform facilitates the planning,

booking and billing of multimodal travel.

• Travellers are then presented with the modes of transportation and best

available fares, provided by the real-time information and mobile payment

systems of the platform. Options also enable the traveller to switch to

alternative modes of travel in the event of delays.

Source: Eco-Business, 22/04/2013:http://www.eco-business.com/opinion/singapores-transport-future-could-be-multimodal-system/

Multimodal System – The Future

of Transport • Germany is already taking a step forward in the use of multimodal transport.

As part of the Berlin-Brandenburg Electromobility Showcase, it was

announced that a central IT platform is being developed for the integration

of the various mobility services across different operators and thus enabling

the offering of seamless end-to-end connections for commuters.

• Part of the convenience of a multimodal transportation scheme is how

customers only need to pay a flat rate based on usage. The IMP has a

central billing process for all the mobility services used.

• Eco-Business suggests that the availability of multimodal travel can be a

catalyst for shifting mobility behaviour towards a stronger acceptance of

public transport.

Source: Eco-Business, 22/04/2013:http://www.eco-business.com/opinion/singapores-transport-future-could-be-multimodal-system/

Renewable Urban Transport –

Calgary • The WFC argues that land use planning, favouring compact urban

settlements will be critical to low-carbon urban development.

• In these settlements daily needs for products and services could be

supplied by non-motorised forms of mobility.

• However, in the short and medium term, cities have little choice but to

pursue alternative mobility options including public transit systems utilizing

regionally supplied renewable energy.

• Calgary’s light rail transit (LRT) system, the CTrain, runs on electricity

generated entirely by twelve wind turbines in the province.

Source: World Future Council, 28/06/2012: http://power-to-the-people.net/2012/06/5-cases-of-regenerative-urbanisation/

Renewable Urban Transport –

Calgary • It carries the highest volume of any LRT in North America, with over 280

000 passengers every weekday.

• It comprises 44 kilometres of double track, 155 light rail vehicles, 37

stations, and over 13 000 park-and-ride stalls.

• It is currently the only 100% renewable energy-powered light rail system in

North America.

• Cities that base their transport systems on renewable energy are likely to be

more environmentally, socially and economically resilient than cities with

transport based on fossil fuels.

Source: World Future Council, 28/06/2012: http://power-to-the-people.net/2012/06/5-cases-of-regenerative-urbanisation/

Scenarios

• The High-tech scenario - describes a world in which high-tech products

simplify many areas of daily life. Devices are controlled by voice, eye,

gesture and other sensors. People live in a highly interconnected world and

are a part of networking ecosystems.

• There is strong competition between content and infrastructure providers.

People expect and receive 24/7 service. It is easy to swap applications and

switch providers. For the automotive sector, this scenario foresees a wide

array of car features allowing drivers to stay connected to their networks

while driving, use the Internet (cloud-based services) and personalize the

MMI.

Source: Roland Berger (2011), Automotive Landscape to 2025: http://www.rolandberger.com/media/pdf/Roland_Berger_Automotive_Landscape_2025_20110228.pdf

Scenarios

• Complex E/E systems in active and passive safety, driving assistance and

auto diagnostics are commonplace. In marketing, technologies such as

CRM play a major role in helping OEMs to go beyond the product.

• The key success factors to surviving the High-tech scenario are

powerful R&D processes. This enables quick innovation and easy

collaboration with changing partners from the automotive and non-

automotive sectors. Module-based approaches allow features to be

upgraded fast. Strong configuration management is a prerequisite. Plants

must be highly flexible and allow frequent updates and personalization

• of products.

Source: Roland Berger (2011), Automotive Landscape to 2025: http://www.rolandberger.com/media/pdf/Roland_Berger_Automotive_Landscape_2025_20110228.pdf

Scenarios

• The Budget scenario – describes a world in which the purchasing power

of customers is strongly reduced due to taxes and inflation combined with

low income growth.

• Globalization creates scarcity of employment and raw material costs rise.

Cars are less affordable and the money spent on cars is in competition with

other spending. Leasing and finance schemes are the norm and pay-per-

use models establish themselves for many products. New low-cost brands

emerge.

• The main features for cars in the Budget scenario are a high degree of

simple, no-frills technology and limited standard equipment levels, enabling

a low-cost position.

Source: Roland Berger (2011), Automotive Landscape to 2025: http://www.rolandberger.com/media/pdf/Roland_Berger_Automotive_Landscape_2025_20110228.pdf

Scenarios

• New low-cost brands emerge and players from outside the automotive

industry enter the market selling affordable cars under their own label, e.g.

Walmart.

• The key success factors to surviving the Budget scenario are reducing

the costs of development and production to an absolute minimum. Standard

platforms will be the norm for producing global products with limited

equipment. Multi-badging allows OEMs to address local markets with

different brands and players while sharing the same product base.

Engineering and production will take place in low-cost centres with a high

level of local sourcing. Cost is the main driver and development and

production of many modules and even complete vehicles is outsourced.

Source: Roland Berger (2011), Automotive Landscape to 2025: http://www.rolandberger.com/media/pdf/Roland_Berger_Automotive_Landscape_2025_20110228.pdf

Scenarios

• The Sustainability scenario describes a world in which consumer

behaviour is strongly influenced by regulation, legislation and tax, but at the

same time by rating recommendations. Transportation is restricted.

• Sustainability is partially imposed by law, partially the result of a changing

attitude to the environment on the part of consumers. People are highly

educated and use the transparency offered by the media to buy long-term

durability and high quality. The marketplace for second-hand products

grows.

• For the automotive sector, this means that vehicles must comply with all

current and future legislation.

Source: Roland Berger (2011), Automotive Landscape to 2025: http://www.rolandberger.com/media/pdf/Roland_Berger_Automotive_Landscape_2025_20110228.pdf

Scenarios

• Brands can gain a competitive edge by offering the most sustainable

product and a high share of electrified cars. OEMs become new mobility

solution services working together with other providers.

• The key success factors to surviving the Sustainability scenario are

R&D activities aimed at creating innovation through green tech. Successful

products will be zero or low-emission vehicles and mobility solutions,

allowing intelligent traffic management.

Source: Roland Berger (2011), Automotive Landscape to 2025: http://www.rolandberger.com/media/pdf/Roland_Berger_Automotive_Landscape_2025_20110228.pdf

Intelligent Infrastructure

Scenarios

• The Foresight Project on Intelligent Infrastructure Systems (IIS) examines

how, over the next 50 years, the UK can apply science and technology to

the design and implementation of intelligent infrastructure for robust,

sustainable and safe transport, and its alternatives.

• The IIS report describes four scenarios and ‘systems maps’ that were

developed to investigate how science and technology might be applied to

infrastructure over the next 50 years.

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

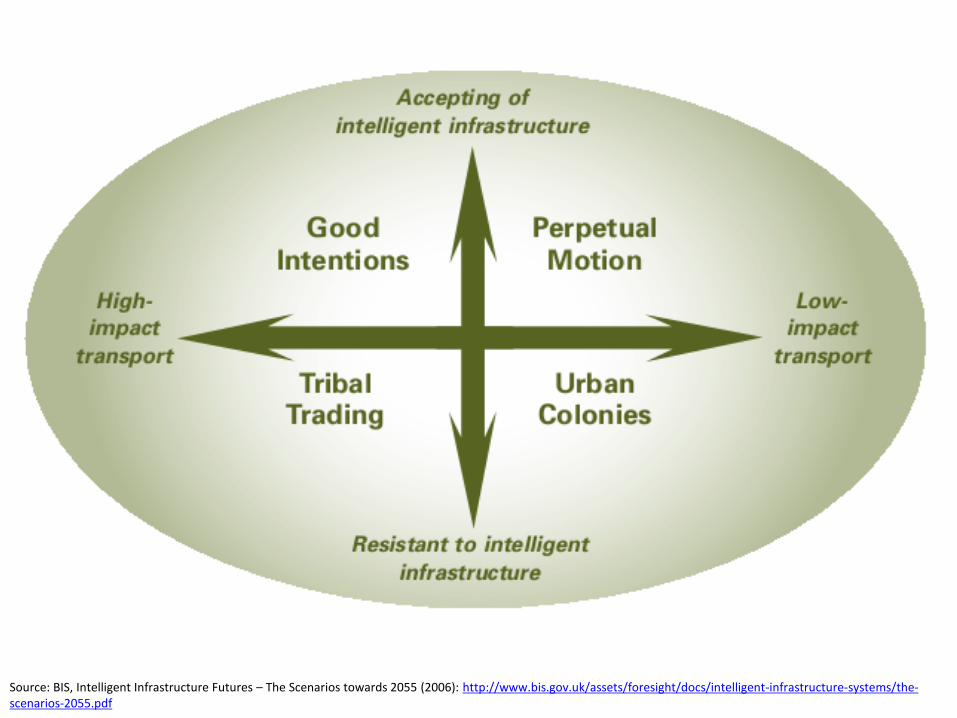

Intelligent Infrastructure

Scenarios

• Scenario 1 – Perpetual Motion

• Perpetual Motion describes a society driven by constant information,

consumption and competition. In this world, instant communication and

continuing globalisation have fuelled growth: demand for travel remains

strong.

• New, cleaner, fuel technologies are increasingly popular. Road use is

causing less environmental damage, although the volume and speed of

traffic remains high. Aviation relies on carbon fuels and remains expensive.

It is increasingly replaced by ‘telepresencing’ technology(for business) and

rapid train systems (for travel).

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

Intelligent Infrastructure

Scenarios

• Energy supply is a precondition for the ‘always on’ world of Perpetual

motion.

• Technology in all its aspects is a large but not exclusive part of the picture,

and the human capacity to cope with such a world resists full-scale

adoption. In this scenario, technology achieves levels of interoperability,

resilience and ubiquity that renders it effective and trustworthy.

• Problems still exist, arguably because technology is applied without regard

to the design of the physical environment or its waste footprint. People are

also too busy to think about efficient use.

• Crime adapts to a more connected world, as does law enforcement.

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

Intelligent Infrastructure

Scenarios

• Scenario 2 – Urban Colonies

• In this scenario, investment in technology primarily focuses on minimising

environmental impacts. Good environmental practice is at the heart of the

UK’s economic and social policies; sustainable buildings, distributed power

generation and new urban planning policies have created compact,

sustainable cities.

• Transport is permitted only if green and clean. Car use is still energy-

expensive and is restricted. Public transport – electric and low-energy – is

efficient and widely used.

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

Intelligent Infrastructure

Scenarios • Competitive cities have the IT infrastructure needed to link high-value

knowledge businesses, but there is poor integration of IT supporting

transport systems. Rural areas have become more isolated, effectively

acting as food and bio-fuel sources for cities.

• Urban Colonies identifies that improved urban design, organising ourselves

to minimise the need for travel, has a contribution to make. The scenario is

a response to environmental concerns but is also driven by suspicion about

intelligent technologies, which requires to find alternatives to travel.

• The overall economic focus is more city-based than global, with medium

economic growth. Societal benefits accrue from a society integrated more at

the local level.

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

Intelligent Infrastructure

Scenarios

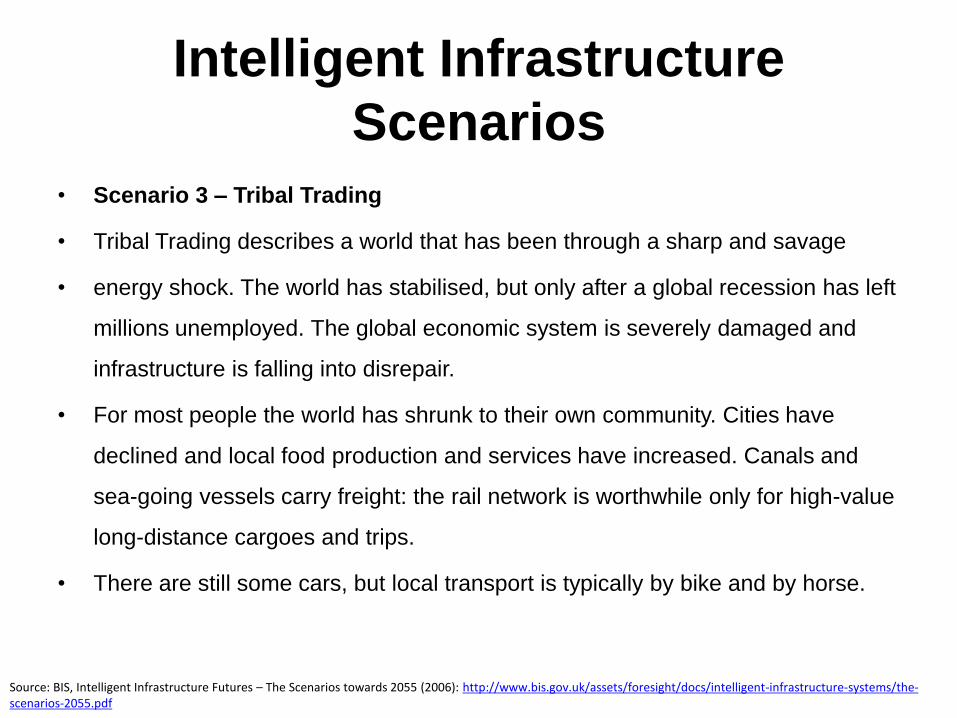

• Scenario 3 – Tribal Trading

• Tribal Trading describes a world that has been through a sharp and savage

• energy shock. The world has stabilised, but only after a global recession has left

millions unemployed. The global economic system is severely damaged and

infrastructure is falling into disrepair.

• For most people the world has shrunk to their own community. Cities have

declined and local food production and services have increased. Canals and

sea-going vessels carry freight: the rail network is worthwhile only for high-value

long-distance cargoes and trips.

• There are still some cars, but local transport is typically by bike and by horse.

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

Intelligent Infrastructure

Scenarios

• The power of the state has been eroded, although it does what it can. There

are many local conflicts over resources, lawlessness and mistrust are high.

• Intelligent infrastructure is not on the agenda in this scenario. This is a world

of opportunities not grasped and challenges ignored until too late.

• Some places fare better than others, but universally the focus is on making

the most of the resources available, particularly locally, and being patient.

• Technology is limited to that which is robust and able to cope with

fluctuations in energy supply, and legacy infrastructure is patched and

patched again.

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

Intelligent Infrastructure

Scenarios

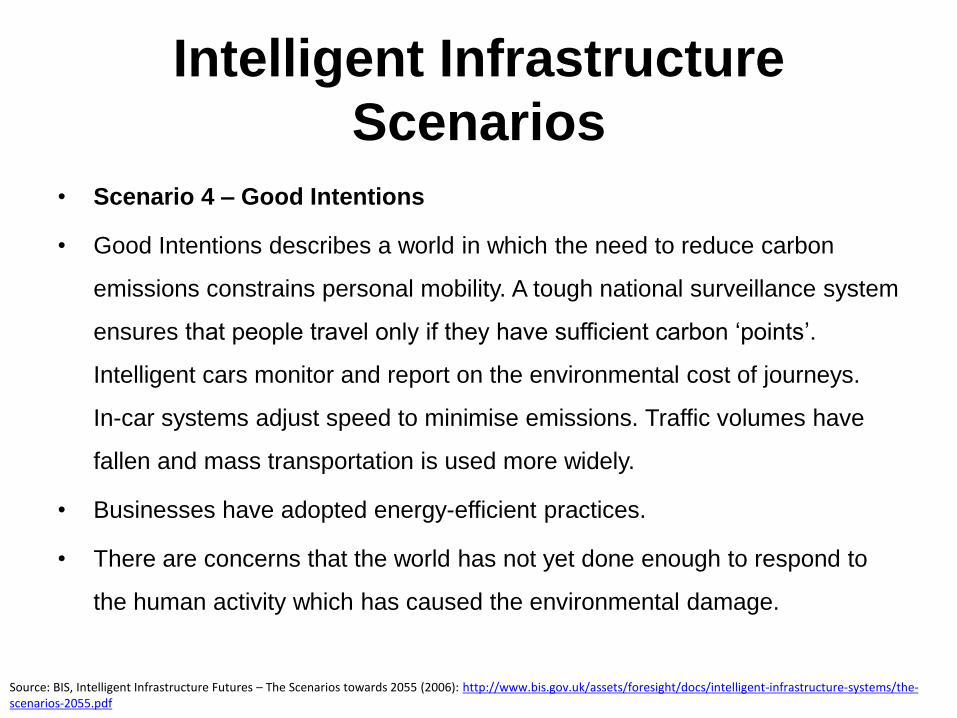

• Scenario 4 – Good Intentions

• Good Intentions describes a world in which the need to reduce carbon

emissions constrains personal mobility. A tough national surveillance system

ensures that people travel only if they have sufficient carbon ‘points’.

Intelligent cars monitor and report on the environmental cost of journeys.

In-car systems adjust speed to minimise emissions. Traffic volumes have

fallen and mass transportation is used more widely.

• Businesses have adopted energy-efficient practices.

• There are concerns that the world has not yet done enough to respond to

the human activity which has caused the environmental damage.

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

Intelligent Infrastructure

Scenarios

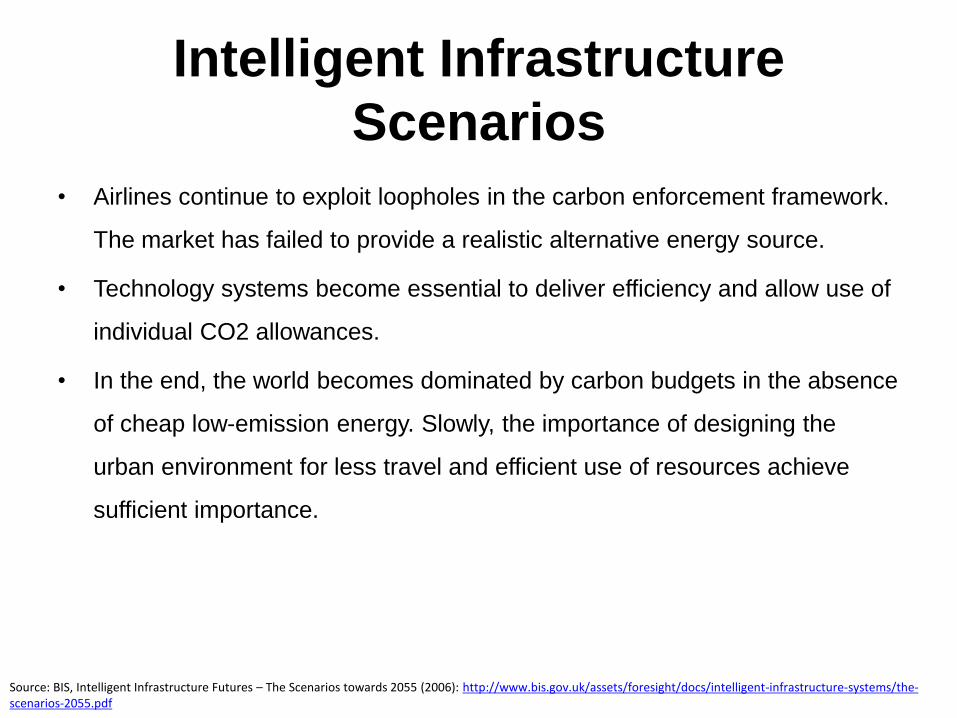

• Airlines continue to exploit loopholes in the carbon enforcement framework.

The market has failed to provide a realistic alternative energy source.

• Technology systems become essential to deliver efficiency and allow use of

individual CO2 allowances.

• In the end, the world becomes dominated by carbon budgets in the absence

of cheap low-emission energy. Slowly, the importance of designing the

urban environment for less travel and efficient use of resources achieve

sufficient importance.

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

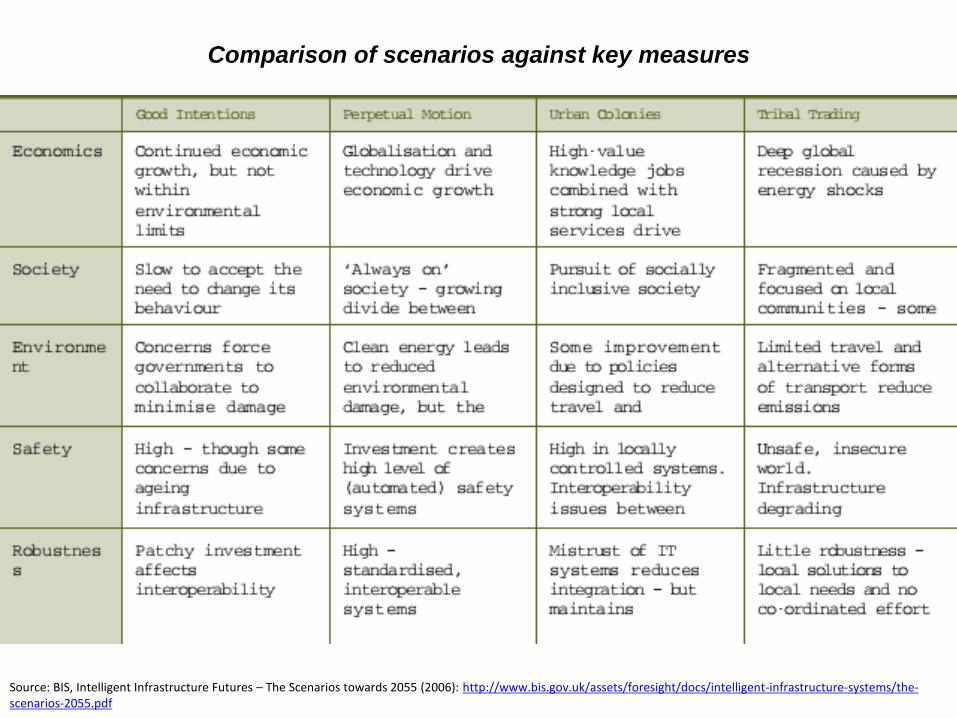

Comparison of scenarios against key measures

Source: BIS, Intelligent Infrastructure Futures – The Scenarios towards 2055 (2006): http://www.bis.gov.uk/assets/foresight/docs/intelligent-infrastructure-systems/the-scenarios-2055.pdf

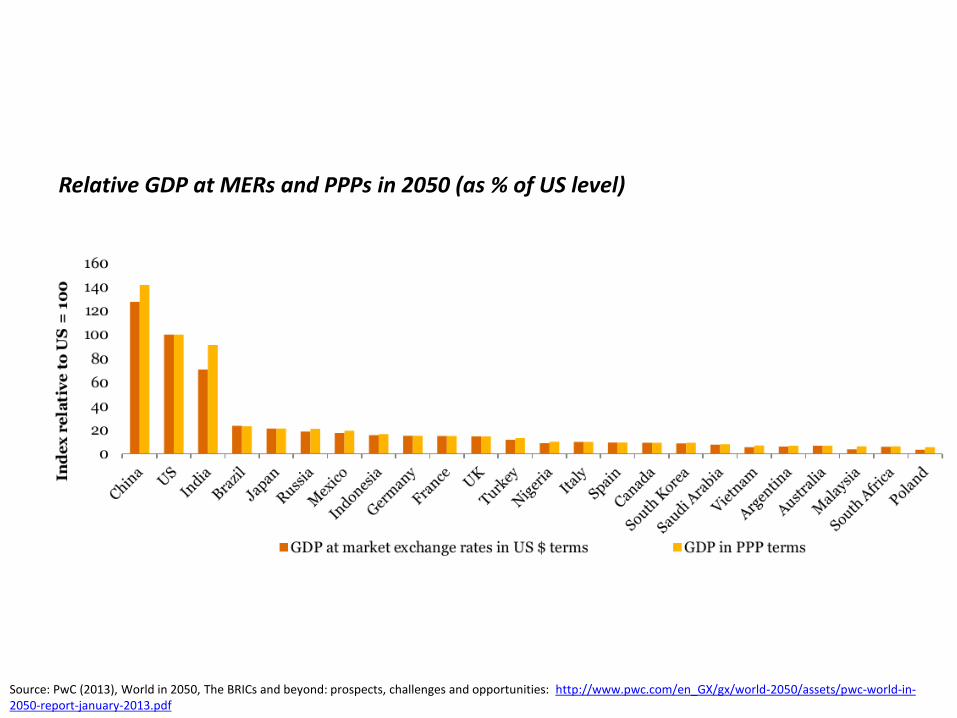

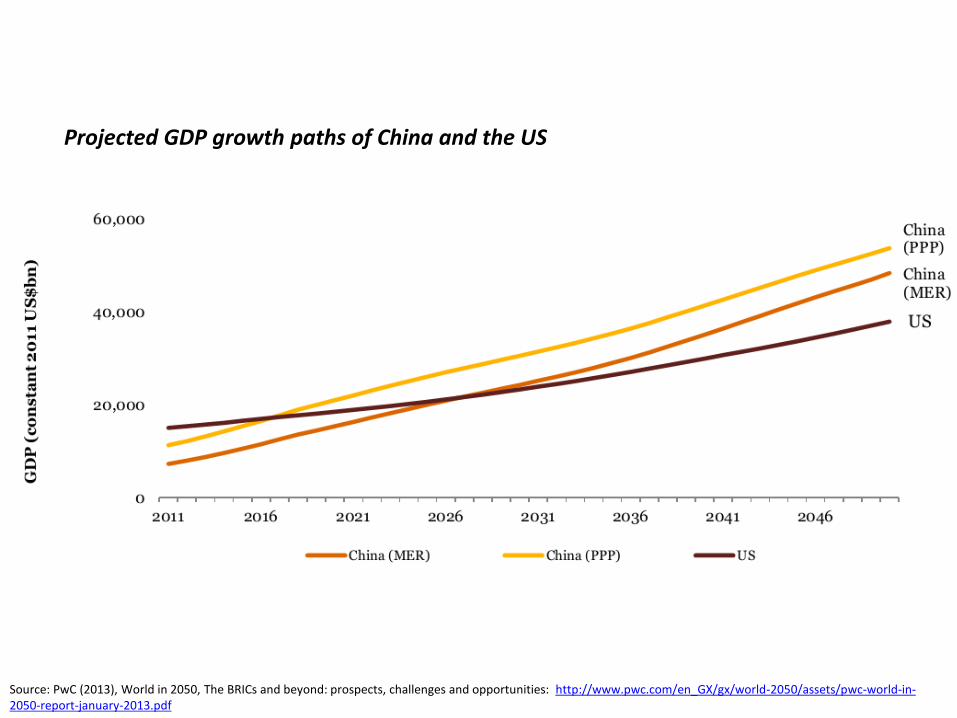

The World in 2050

• Research undertaken by PwC suggests that the world economy is projected

to grow at an average rate of just over 3% per annum from 2011 to 2050,

doubling in size by 2032 and nearly doubling again by 2050.

• China is projected to overtake the US as the largest economy by 2017 in

purchasing power parity (PPP) terms and by 2027 in market exchange rate

terms.

• India is expected to become the third ‘global economic giant’ by 2050, a

long way ahead of Brazil, which we expect to move up to 4th place ahead of

Japan.

• Outside the G20, Vietnam, Malaysia and Nigeria all have strong long-term

growth potential.

Source: PwC (2013), World in 2050, The BRICs and beyond: prospects, challenges and opportunities: http://www.pwc.com/en_GX/gx/world-2050/assets/pwc-world-in-2050-report-january-2013.pdf

The World in 2050

• China’s growth rate is expected to meet the government’s new 7% target for

the current decade, but will cool down progressively during the period 2021

– 2050 as its economy matures.

• A rapidly aging population and rising real labour costs are expected to see

China transition from being an export-orientated economy to more of a

consumption driven economy.

• Chinese exporters will find themselves competing more on the basis of

quality rather than price in their key US and EU export markets.

Source: PwC (2013), World in 2050, The BRICs and beyond: prospects, challenges and opportunities: http://www.pwc.com/en_GX/gx/world-2050/assets/pwc-world-in-2050-report-january-2013.pdf

Relative GDP at MERs and PPPs in 2050 (as % of US level)

Source: PwC (2013), World in 2050, The BRICs and beyond: prospects, challenges and opportunities: http://www.pwc.com/en_GX/gx/world-2050/assets/pwc-world-in-2050-report-january-2013.pdf

Projected GDP growth paths of China and the US

Source: PwC (2013), World in 2050, The BRICs and beyond: prospects, challenges and opportunities: http://www.pwc.com/en_GX/gx/world-2050/assets/pwc-world-in-2050-report-january-2013.pdf

Source: PwC (2013), World in 2050, The BRICs and beyond: prospects, challenges and opportunities: http://www.pwc.com/en_GX/gx/world-2050/assets/pwc-world-in-2050-report-january-2013.pdf

Car Sharing Business Model

• Roland Berger (2011) suggests that new business models will not be only

about selling cars but also about integrating software and hardware, or

different hardware modules.

• One example is mobility services, such as car sharing. Car sharing is a

business that will have to be taken seriously by 2025

• Given that one shared vehicle can replace up to 38 cars, OEMs will have to

try to integrate this new business into their model and generate other

alternative sources of revenue before somebody else does.

• C2E and C2C communication could represent future revenue pools as well.

Source: Roland Berger (2011), Automotive Landscape to 2025: http://www.rolandberger.com/media/pdf/Roland_Berger_Automotive_Landscape_2025_20110228.pdf

Car Sharing Business Model

• The rising proportion of corporate vehicle owners such as companies with

car fleets, car hire firms, municipalities and car sharing companies will make

it harder to achieve premium prices. Margins will be eroded and there will

be more direct sales.

• This will weaken the car retailers' position. At the same time, retailers are

crucial for customer contact and will become increasingly vital as customers'

needs become more individualized.

Source: Roland Berger (2011), Automotive Landscape to 2025: http://www.rolandberger.com/media/pdf/Roland_Berger_Automotive_Landscape_2025_20110228.pdf

Electric Vehicle Business Model

• Electric vehicles will also require new business models.

• The economics of electric vehicles open up new ways for consumers to

think about and pay for mobility.

• They could, for example, purchase, finance or lease a vehicle without the

battery and then have the battery supplied by somebody else. Or they could

buy, finance or lease the battery together with the vehicle.

• Drivers could pay a monthly flat rate that covers use of the car including the

battery, charging of the battery and maintenance. Or they could pay a

higher monthly fee and in addition receive value-added services such as

navigation on demand, parking access, music downloads, and so on.

Source: Roland Berger (2011), Automotive Landscape to 2025: http://www.rolandberger.com/media/pdf/Roland_Berger_Automotive_Landscape_2025_20110228.pdf

The Connected Car – Changing

Business Models

• By 2022, the connected car market will comprise an estimated 700 million

connected cars plus 1.1 billion aftermarket connected devices providing

services such as navigation, usage-based insurance, stolen vehicle

recovery and infotainment.

• Telefónica Digital has published a report that identifies the opportunities and

challenges in stimulating collaboration between the automotive and mobile

industries which will together build this new market.

• The report suggests that the industries need to harmonise their work

practices and business models.

Source: Latelier, 2/7/2013: http://www.atelier.net/en/trends/articles/mobile-and-automotive-industries-new-business-models-needed-promote-collaboration_422528

The Connected Car – Changing

Business Models

• Overcoming the disconnect between mobile and automotive industry

lifecycles – The report suggests that mobile operators and automotive

manufacturers must now start to draw up their business models in

collaboration with each other because their approaches and aims vary

considerably today.

• For instance, while Automotive Original Equipment Manufacturers typically

look for local connectivity solutions, BMW and Nissan take a global

approach to the market and so need to be able to secure suitable

agreements to provide global, or at least regional, coverage.

Source: Latelier, 2/7/2013: http://www.atelier.net/en/trends/articles/mobile-and-automotive-industries-new-business-models-needed-promote-collaboration_422528

The Connected Car – Changing

Business Models

• Another challenge for the connected car market is the difference in life-cycle

between the mobile and automotive industries. New features, such as

operating system upgrades and new applications, are provided almost

constantly for the smartphone, whereas automobile manufacturers work on

five-year cycles.

• The advent of new business models – The connected car is about to

cause an upheaval in the traditional dealership model. It offers a unique

opportunity for manufacturers to engage directly with their customers.

Branded app stores, upgrades to software solutions over-the-air, and

sharing of vehicle data all provide automotive OEMs with opportunities to

maintain brand awareness among customers.

Source: Latelier, 2/7/2013: http://www.atelier.net/en/trends/articles/mobile-and-automotive-industries-new-business-models-needed-promote-collaboration_422528

The Connected Car – Changing

Business Models

• The question of who pays for connected car services is an issue that is not

yet resolved.

• Consumers are used to making a one-off payment when purchasing a

vehicle, but embedded connection entails an additional bill to be paid for

actual connectivity.

• This means that new business models need to be created.

• One suggestion from General Motors is that operators could for example

recognise vehicles as a second device on a customer’s data plan for a low

monthly fee.

Source: Latelier, 2/7/2013: http://www.atelier.net/en/trends/articles/mobile-and-automotive-industries-new-business-models-needed-promote-collaboration_422528

The Connected Car – Changing

Business Models

• New technologies give rise to new business models that streamline that

sales process and engage with customers.

• CSC (2012),citing McKinsey’s 2012 Automotive Report suggests that ‘’Most

companies have conducted major programs to boost productivity and

improve operations, but haven't put sales under the same microscope. Yet

there's a much bigger gap between best and worst companies when it

comes to selling than to areas like supply chain management, finance or

purchasing.’’

Source: CSC (2012), The Connected Car –Changing Business Models for Automotive: http://www.w3.org/2012/08/web-and-automotive/slides/webandauto-day2-CSC.pdf

The Connected Car – Changing

Business Models

• Challenges:

• Current supply chain

• Lifecycle of automobiles

• Opportunities:

• Streamline sales processes

• Provide stock visibility

• Integrate with social media

Source: CSC (2012), The Connected Car –Changing Business Models for Automotive: http://www.w3.org/2012/08/web-and-automotive/slides/webandauto-day2-CSC.pdf

Driverless Public Transport –

Milton Keynes

• The Independent (2013) reports that Milton Keynes has announced plans to

deploy a driverless public transport system – 100 pods alongside an

accompanying smartphone app that can be used to book and pay for

journeys.

• Each pod will have enough space for two passengers and luggage and will

travel up to speeds of 12mph.

• The pods are powered by electronic motors and will initially be given their

own lanes, though there are plans to remove these once residents have

become accustomed to the technology.

Source: The Independent, 06/11/2013: http://www.independent.co.uk/life-style/gadgets-and-tech/news/milton-keynes-introducing-driverless-public-transport-pods-by-2017-8925119.html

Driverless Public Transport –

Milton Keynes

• The pods will be used to ferry passengers between the train station and

shopping centres and offices a mile away, a journey will cost £2.

• It is expected that the project will generate £1m of revenue in the first year,

and will cost £65 million in total.

• Twenty trial pods will be introduced in 2015 with steering wheels or joysticks

to control them. The full, driverless system will hit the streets later in 2017.

• John Bint, Milton Keynes Council’s cabinet member for transport and

highways believes that the system will ease parking problems and pollution

in the city, but notes that as the pod is neither a nor a taxi the council needs

to “work out how it’s going to be permitted.’’

Source: The Independent, 06/11/2013: http://www.independent.co.uk/life-style/gadgets-and-tech/news/milton-keynes-introducing-driverless-public-transport-pods-by-2017-8925119.html

Armadillo-T

• Researchers from the Korea Advanced Institute of Science and Technology

have developed a prototype for an EV folding car.

• The Armadillo-T starts off small, about the size of a smart car, and gets

smaller, reducing its overall length to just 65 inches after parking.

• A smartphone activation system is supposed to prevent the car from folding

if the driver is inside.

• The car’s aesthetics are a disadvantage at the moment.

Source: Autoweek, 22/08/2013: http://www.autoweek.com/article/20130822/carnews/130829958

Concept Ideas for EVs

• Next Geencar reports that car manufacturers are investing significant time

and money into research and development of plug-in vehicles.

• Due to the increasing pressures on road space and fuel economy, a

segment that will certainly offer several electric options will be small

quadricycle urban mobility vehicles.

• Many manufacturers have designed concept ideas for single or two-seater

urban vehicles – some of which will reach the market and some of which will

remain as just ideas.

Source: Next greencar, 3/9/2012: http://www.nextgreencar.com/news/5566/Top-10-electric-concept-cars

Nissan Pivo 2

• Nissan has developed a bubble-shaped, three-seater all-electric car called

the Pivo, which is short for pivot.

• It was introduced in 2005 at the Tokyo Motor Show. The third version was

unveiled in 2011, and uses a lithium-ion battery with a greater range.

• The most striking design feature is that the cabin sits on a wheeled platform

and can swivel through 360 degrees, making manoeuvring and parking less

of an effort.

Source: Next greencar, 3/9/2012: http://www.nextgreencar.com/news/5566/Top-10-electric-concept-cars

Audi Urban Spyder Concept

• Audi have taken their Urban Spyder concept a step. Production was

expected to begin in 2013 with the aim to offer the go-kart style electric

quadricycle to selected markets for around £8,000.

• The 7.1 kWh lithium-ion batteries will power twin electric motors at the rear

wheels to return a range of around 30 miles, top speed of 60 mph and

acceleration to 40 mph in 6 seconds.

• To reduce weight, the shell is made from carbon fibre reinforced plastics

and aluminium.

Source: Next greencar, 3/9/2012: http://www.nextgreencar.com/news/5566/Top-10-electric-concept-cars

Kia POP

• Kia POP is a three seater electric concept city car that was first presented at

the 2010 Paris Motor Show.

• Its design was inspired by pictures of space shuttles, and its glass roof

gives it a futuristic appearance.

• Only 3000mm long, it is intended to be easy to park and drive around town.

It uses a 50 kW electric motor with 190 Nm torque, powered by lithium

polymer gel batteries – returning a full driving range of around 99 miles.

• Although Kia expect to take the POP to production, as of 2012 timing was

not confirmed.

Source: Next greencar, 3/9/2012: http://www.nextgreencar.com/news/5566/Top-10-electric-concept-cars

Driverless Public Transport –

Milton Keynes • The pods have been designed by Ultra Global, a company that installed a

system of driverless pods in Heathrow’s Terminal 5.

• The pods in Milton Keynes will have no guideway, and will instead use a

combination of GPS, high definition cameras and ultrasonic sensors to

navigate and avoid pedestrians, similar to the technology used in self-

driving cars.

• They will also include large touchscreens that allow passengers to browse

the internet or check their emails.

Source: The Independent, 06/11/2013: http://www.independent.co.uk/life-style/gadgets-and-tech/news/milton-keynes-introducing-driverless-public-transport-pods-by-2017-8925119.html

Large-scale Trial of Driverless

Cars in Gothenburg

• The Telegraph (2013) reports that Volvo plans to introduce 100 driverless

cars on public roads as part of the world’s first large-scale autonomous

driving pilot.

• The cars will drive in normal, everyday road conditions, surrounded by

pedestrians and other traffic, and will even be able to self-park.

• Volvo is working alongside the Swedish Transport Administration, The

Swedish Transport Agency, Lindholmen Science Park and the City of

Gotehenburg, with the goal of placing both it and Sweden as leaders in the

development of future mobility.

Source: The Telegraph, 02/12/2013: http://www.telegraph.co.uk/motoring/news/10484839/Large-scale-trial-of-driverless-cars-to-begin-on-public-roads.html

Large-scale Trial of Driverless

Cars in Gothenburg • The pilot scheme is called “Drive Me - Self-driving cars for sustainable

mobility” and will underway in 2014 with customer research and further

development of current technology.

• The cars themselves won’t appear until 2017, when they will drive on about

30 miles of public road in and around Gothenburg.

• Håkan Samuelsson, President and CEO of the Volvo Car Group says that

Autonomous vehicles are an integrated part of Volvo Cars’ as well as the

Swedish government’s vision of zero traffic fatalities. This public pilot

represents an important step towards this goal’’.

• The pilot will also establish infrastructure requirements for autonomous

driving.

Source: The Telegraph, 02/12/2013: http://www.telegraph.co.uk/motoring/news/10484839/Large-scale-trial-of-driverless-cars-to-begin-on-public-roads.html

Hyperloop - The Future of Travel

• Hyperloop is a conceptual system that could transport passengers in pods

at near-supersonic speed – the vision of billionaire entrepreneur Elon Musk.

• This transport concept could provide a viable alternative to short-haul travel,

high-speed rail and travelling by car.

• Hyperloop could reduce the journey time between Los Angeles and San

Francisco to just 30 minutes, compared to 75 minutes by plane and 5.5

hours by car.

• The concept is based on pods travelling through a low-pressure tube that

would be suspended above the ground.

Source: Future Travel Experience, 15/08/2013: http://www.futuretravelexperience.com/2013/08/hyperloop-the-future-of-travel-or-pure-science-fiction/

Hyperloop - The Future of Travel

• Pods would have a compressor on the front to pass the air to the rear and

some of the air would be used to create a cushion underneath the pod on

which it could ride. Electric induction motors at the beginning, middle and

end points of the tube would be used to accelerate and decelerate the pods.

• Musk believes the whole system could run on solar power, ticket prices

should be as low as $20.

• The Hyperloop could reduce travel times greatly and provide excellent

passenger experience. However, one of the biggest challenges is that much

of the technology that is needed for Hyperloop to become a reality doesn’t

yet exist.

Source: Future Travel Experience, 15/08/2013: http://www.futuretravelexperience.com/2013/08/hyperloop-the-future-of-travel-or-pure-science-fiction/

Hyperloop - The Future of Travel

• Development costs for the project are estimated at $6Bn - ten-times less than

the cost of the high-speed rail link between San Francisco and LA. Much more

than that would be needed for developing and testing new technologies.

• Also, the preliminary concept envisages a system of tubes and capsules that

would travel directly above the California highway between LA and San

Francisco.

• It is not clear how long will it take to convince the government and the public

that a building a futuristic transport system directly above a highway is a

sensible and safe idea.

Source: Future Travel Experience, 15/08/2013: http://www.futuretravelexperience.com/2013/08/hyperloop-the-future-of-travel-or-pure-science-fiction/

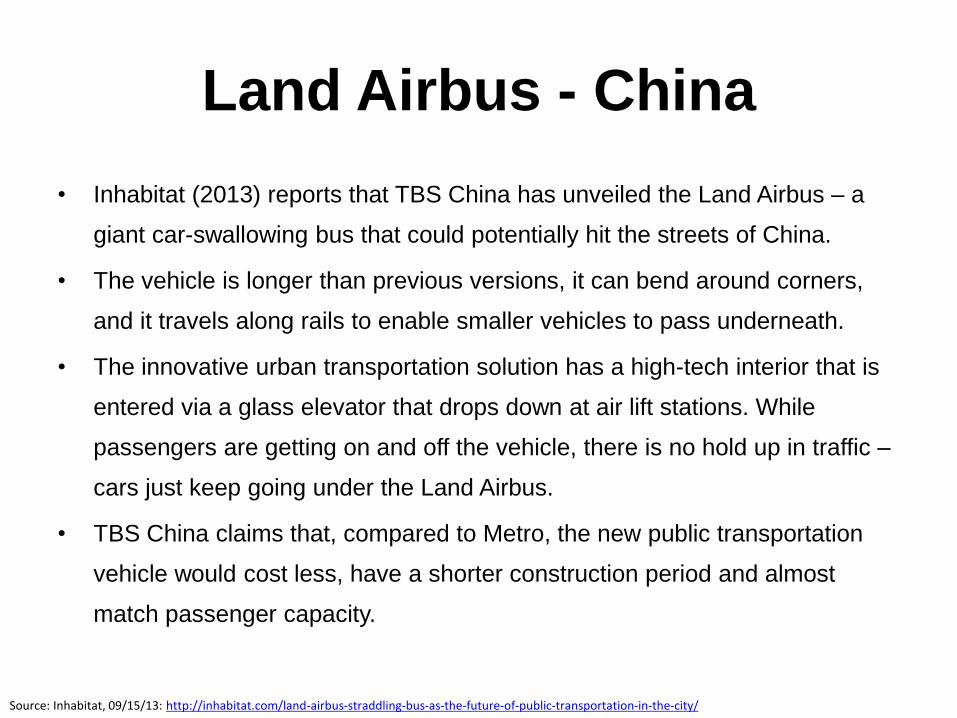

Land Airbus - China

• Inhabitat (2013) reports that TBS China has unveiled the Land Airbus – a

giant car-swallowing bus that could potentially hit the streets of China.

• The vehicle is longer than previous versions, it can bend around corners,

and it travels along rails to enable smaller vehicles to pass underneath.

• The innovative urban transportation solution has a high-tech interior that is

entered via a glass elevator that drops down at air lift stations. While

passengers are getting on and off the vehicle, there is no hold up in traffic –

cars just keep going under the Land Airbus.

• TBS China claims that, compared to Metro, the new public transportation

vehicle would cost less, have a shorter construction period and almost

match passenger capacity.

Source: Inhabitat, 09/15/13: http://inhabitat.com/land-airbus-straddling-bus-as-the-future-of-public-transportation-in-the-city/

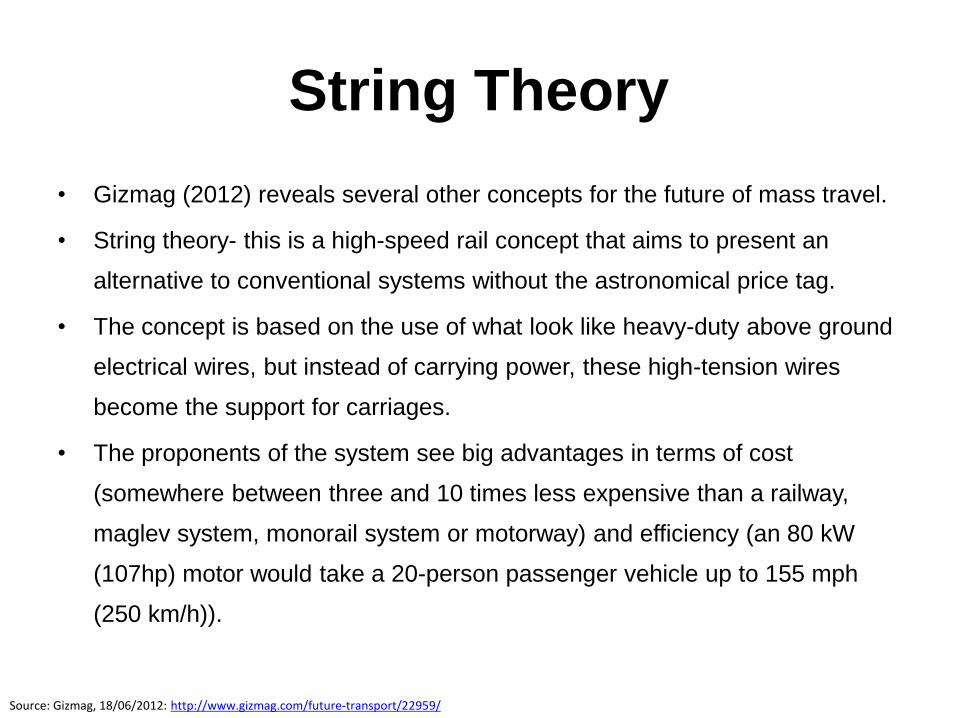

String Theory

• Gizmag (2012) reveals several other concepts for the future of mass travel.

• String theory- this is a high-speed rail concept that aims to present an

alternative to conventional systems without the astronomical price tag.

• The concept is based on the use of what look like heavy-duty above ground

electrical wires, but instead of carrying power, these high-tension wires

become the support for carriages.

• The proponents of the system see big advantages in terms of cost

(somewhere between three and 10 times less expensive than a railway,

maglev system, monorail system or motorway) and efficiency (an 80 kW

(107hp) motor would take a 20-person passenger vehicle up to 155 mph

(250 km/h)).

Source: Gizmag, 18/06/2012: http://www.gizmag.com/future-transport/22959/

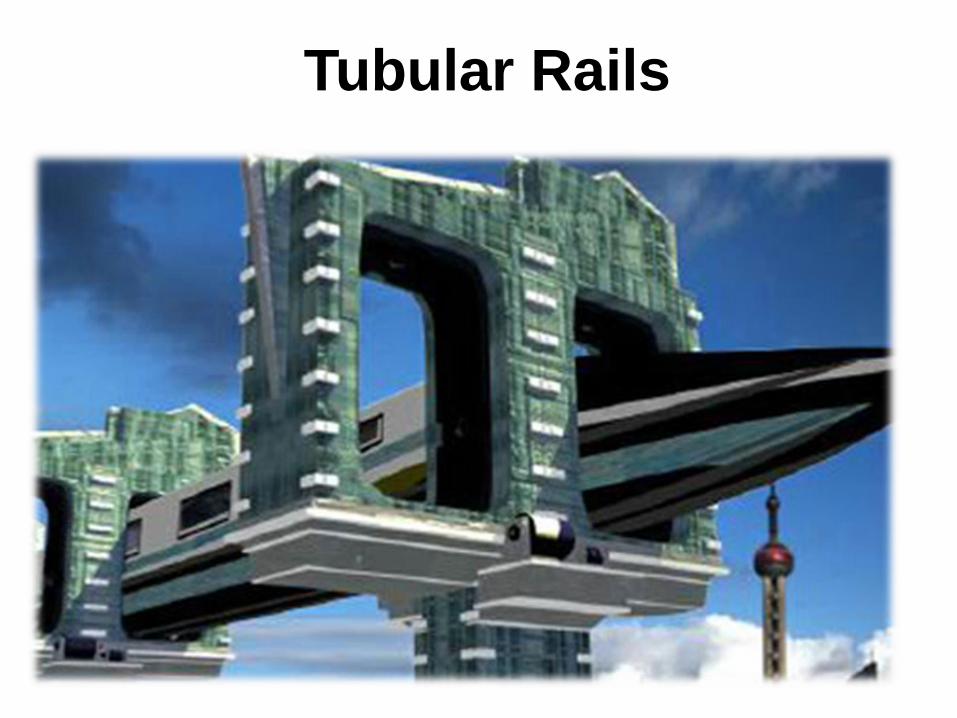

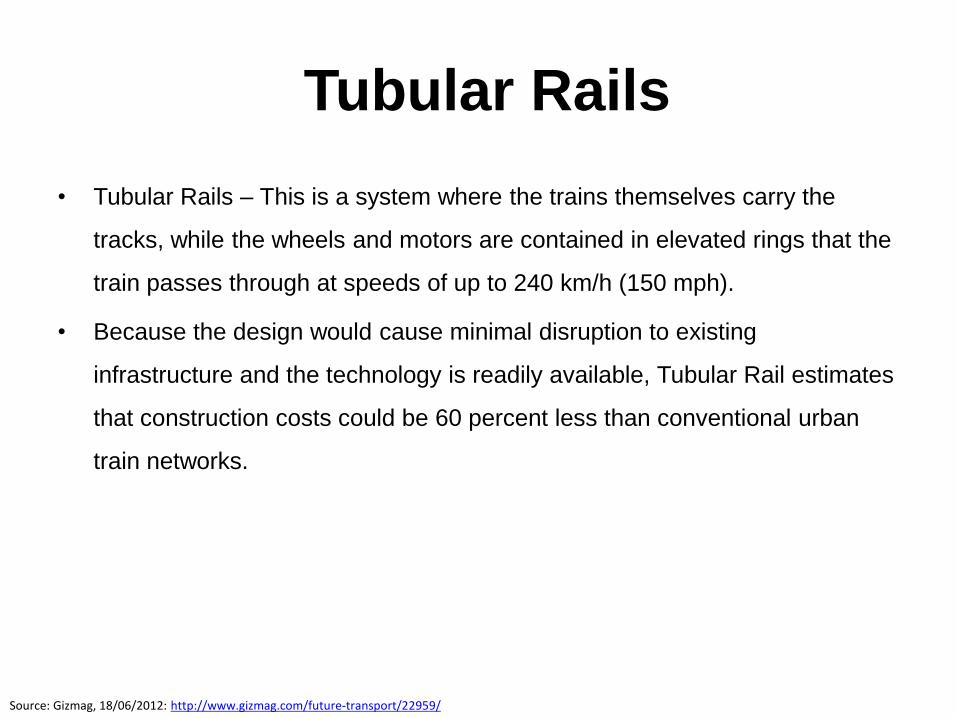

Tubular Rails

• Tubular Rails – This is a system where the trains themselves carry the

tracks, while the wheels and motors are contained in elevated rings that the

train passes through at speeds of up to 240 km/h (150 mph).

• Because the design would cause minimal disruption to existing

infrastructure and the technology is readily available, Tubular Rail estimates

that construction costs could be 60 percent less than conventional urban

train networks.

Source: Gizmag, 18/06/2012: http://www.gizmag.com/future-transport/22959/

Human-powered Mass Transport

• Shweeb is a human-powered monorail system that uses bicycle pods

suspended from tracks to create a very efficient option for getting from A to

B.

• Currently people can ride the Shweeb at the Agroventures in New Zealand,

reaching speeds of up to 45 km/h (28 mph).