Embed Size (px)

Citation preview

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Global Methanol Market

Review

Dewey Johnson

Sr. Director Chemical Market Research

June 2012

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Presentation Agenda

•Methanol global and regional balance

•Methanol global trade

•Methanol price mechanisms and regional feedstock

costs

•Key methanol derivatives

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

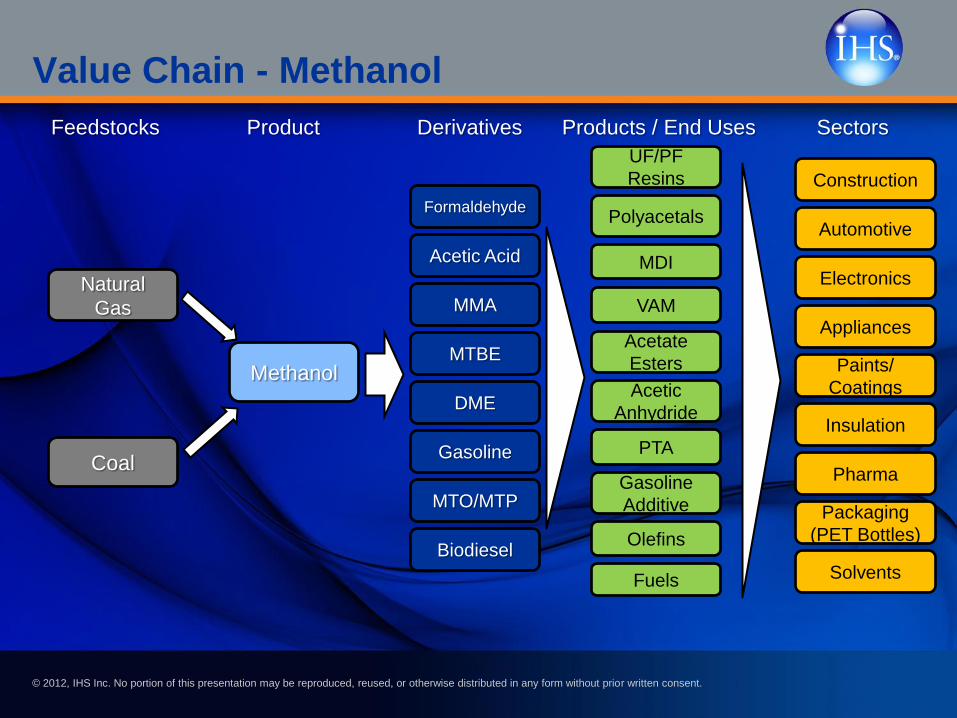

Value Chain - Methanol

Feedstocks Product Derivatives Products / End Uses Sectors

Natural

Gas

Methanol

Formaldehyde

Acetic Acid

MMA

MTBE

DME

Gasoline Coal

Construction

Automotive

Electronics

Appliances

Paints/

Coatings

Insulation

Pharma

Packaging

(PET Bottles)

MTO/MTP

Biodiesel

UF/PF

Resins

MDI

VAM

Gasoline

Additive

Polyacetals

Acetate

Esters

Acetic

Anhydride

Olefins

Fuels

PTA

Solvents

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 4

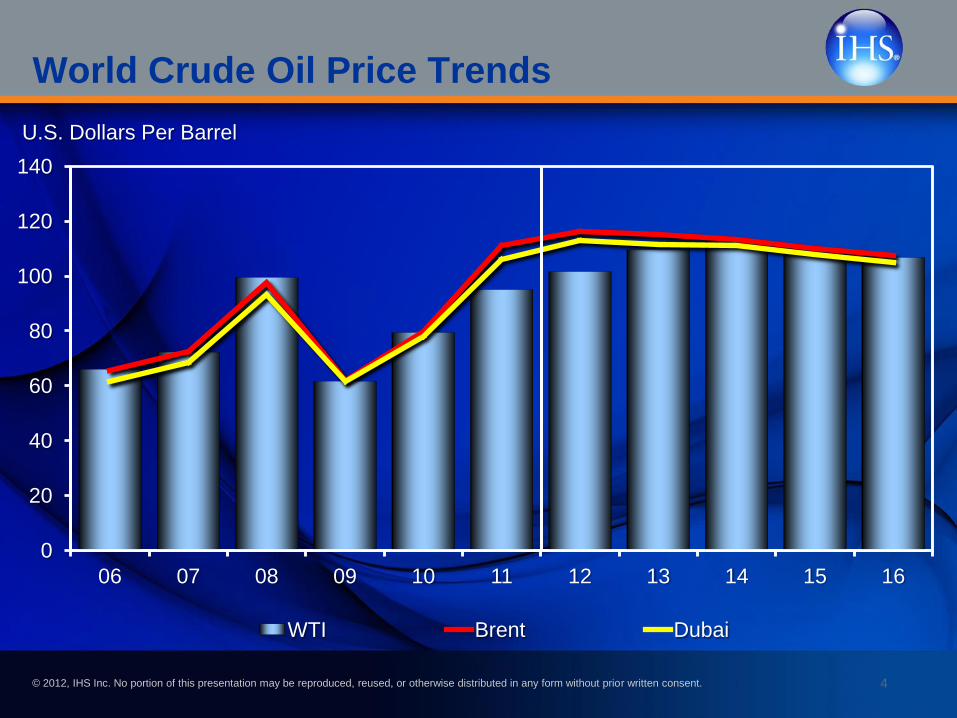

World Crude Oil Price Trends

0

20

40

60

80

100

120

140

06 07 08 09 10 11 12 13 14 15 16

WTI Brent Dubai

U.S. Dollars Per Barrel

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

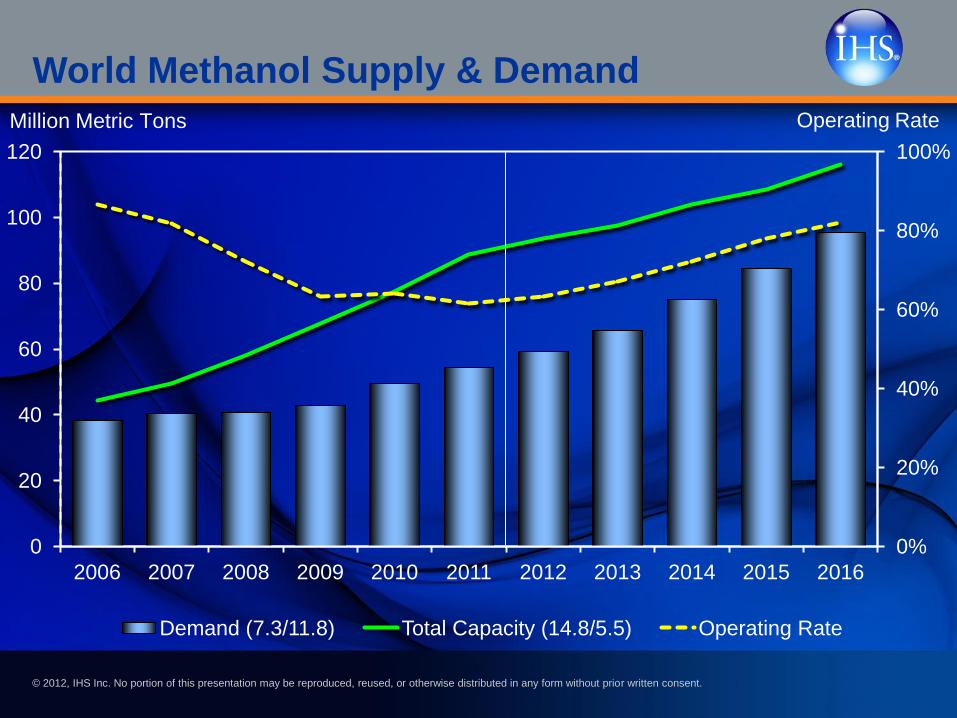

World Methanol Supply & Demand

0%

20%

40%

60%

80%

100%

0

20

40

60

80

100

120

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Demand (7.3/11.8) Total Capacity (14.8/5.5) Operating Rate

Million Metric Tons Operating Rate

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

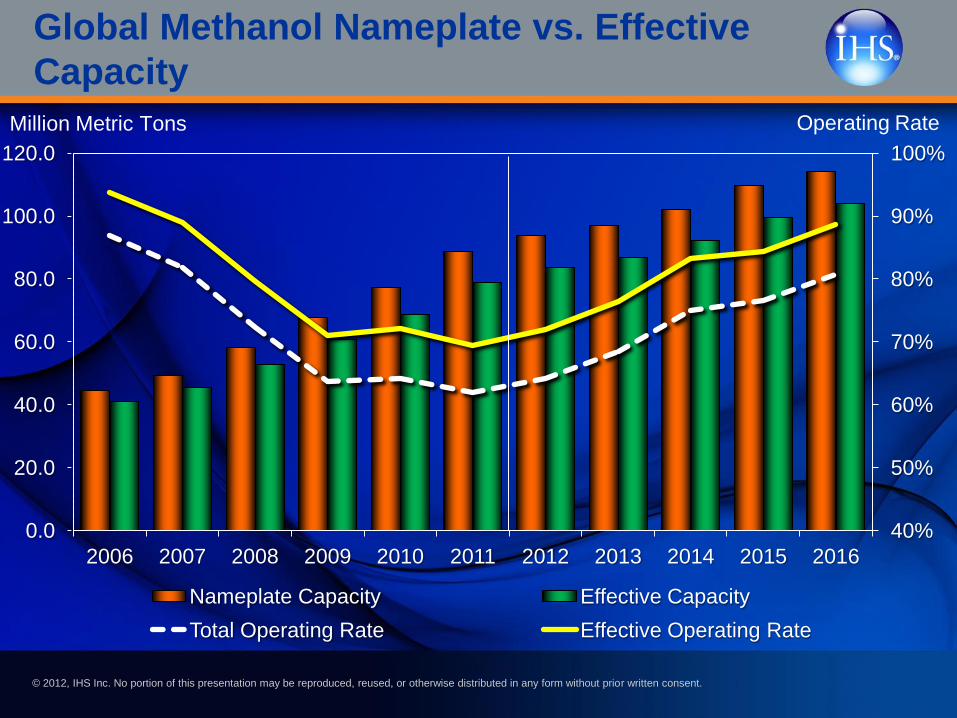

40%

50%

60%

70%

80%

90%

100%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Nameplate Capacity Effective Capacity

Total Operating Rate Effective Operating Rate

Million Metric Tons Operating Rate

Global Methanol Nameplate vs. Effective

Capacity

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

7

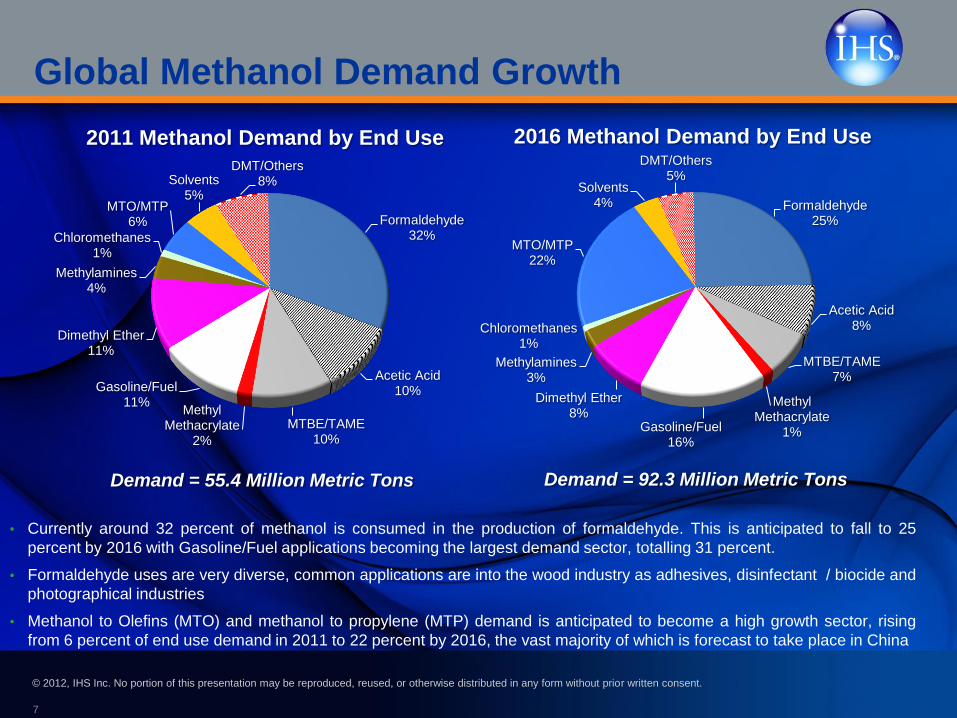

Formaldehyde 32%

Acetic Acid 10%

MTBE/TAME 10%

Methyl Methacrylate

2%

Gasoline/Fuel 11%

Dimethyl Ether 11%

Methylamines 4%

Chloromethanes 1%

MTO/MTP 6%

Solvents 5%

DMT/Others 8%

Demand = 55.4 Million Metric Tons

2011 Methanol Demand by End Use

Formaldehyde 25%

Acetic Acid 8%

MTBE/TAME 7%

Methyl Methacrylate

1% Gasoline/Fuel 16%

Dimethyl Ether 8%

Methylamines 3%

Chloromethanes 1%

MTO/MTP 22%

Solvents 4%

DMT/Others 5%

Demand = 92.3 Million Metric Tons

2016 Methanol Demand by End Use

• Currently around 32 percent of methanol is consumed in the production of formaldehyde. This is anticipated to fall to 25

percent by 2016 with Gasoline/Fuel applications becoming the largest demand sector, totalling 31 percent.

• Formaldehyde uses are very diverse, common applications are into the wood industry as adhesives, disinfectant / biocide and

photographical industries

• Methanol to Olefins (MTO) and methanol to propylene (MTP) demand is anticipated to become a high growth sector, rising

from 6 percent of end use demand in 2011 to 22 percent by 2016, the vast majority of which is forecast to take place in China

Global Methanol Demand Growth

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.0

20.0

40.0

60.0

80.0

100.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Formaldehyde Acetic Acid MTBE/TAME

Methyl Methacrylate Gasoline/Fuel Dimethyl Ether

Methylamines Chloromethanes MTO/MTP

Solvents DMT/Others Operating Rate

Million Metric Tons Operating Rate

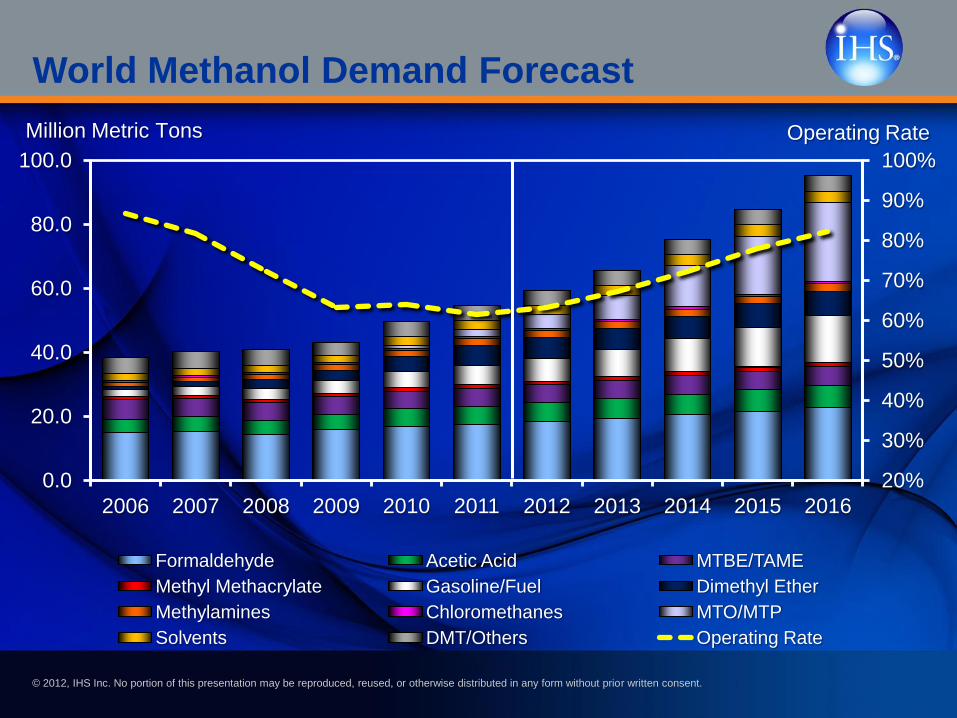

World Methanol Demand Forecast

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

9

0

20

40

60

80

100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

N. America S. America Europe CIS & Baltics

Africa/Middle East Indian Subc. NE Asia SE Asia

Million Metric Tons

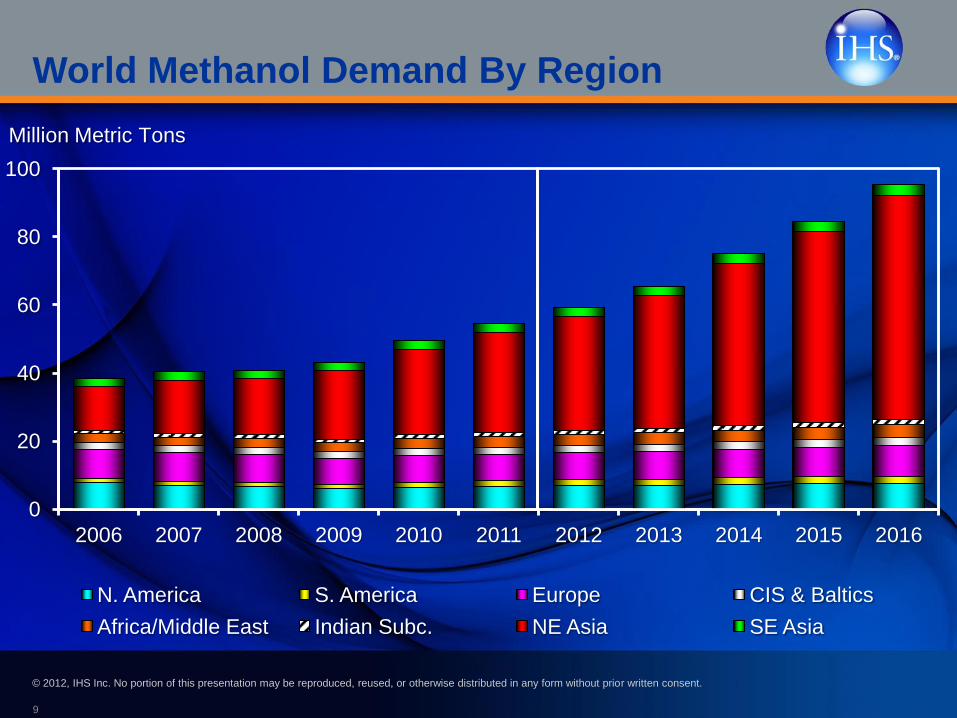

World Methanol Demand By Region

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 10

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

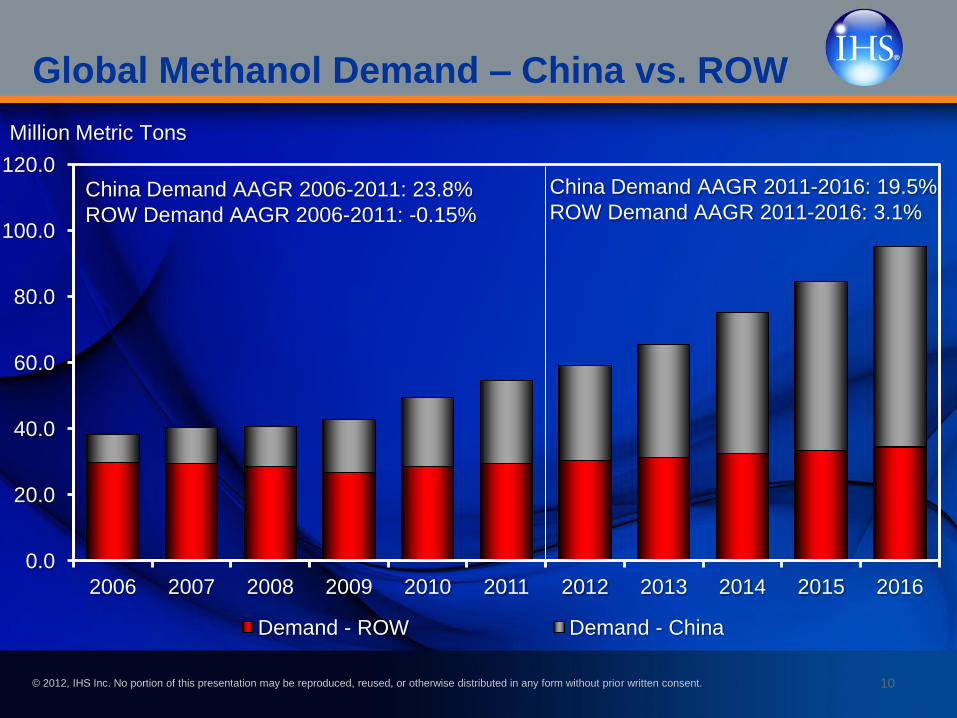

Demand - ROW Demand - China

Million Metric Tons

China Demand AAGR 2006-2011: 23.8%

ROW Demand AAGR 2006-2011: -0.15%

China Demand AAGR 2011-2016: 19.5%

ROW Demand AAGR 2011-2016: 3.1%

Global Methanol Demand – China vs. ROW

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 11

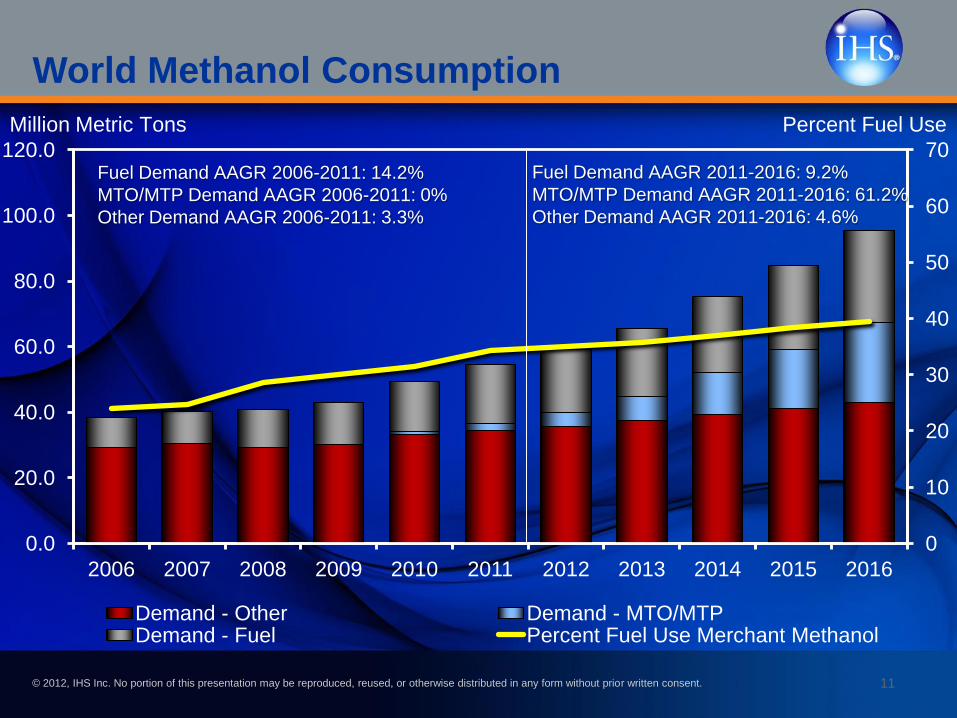

World Methanol Consumption

0

10

20

30

40

50

60

70

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Demand - Other Demand - MTO/MTP Demand - Fuel Percent Fuel Use Merchant Methanol

Million Metric Tons Percent Fuel Use

Fuel Demand AAGR 2006-2011: 14.2%

MTO/MTP Demand AAGR 2006-2011: 0%

Other Demand AAGR 2006-2011: 3.3%

Fuel Demand AAGR 2011-2016: 9.2%

MTO/MTP Demand AAGR 2011-2016: 61.2%

Other Demand AAGR 2011-2016: 4.6%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

West Europe

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

13

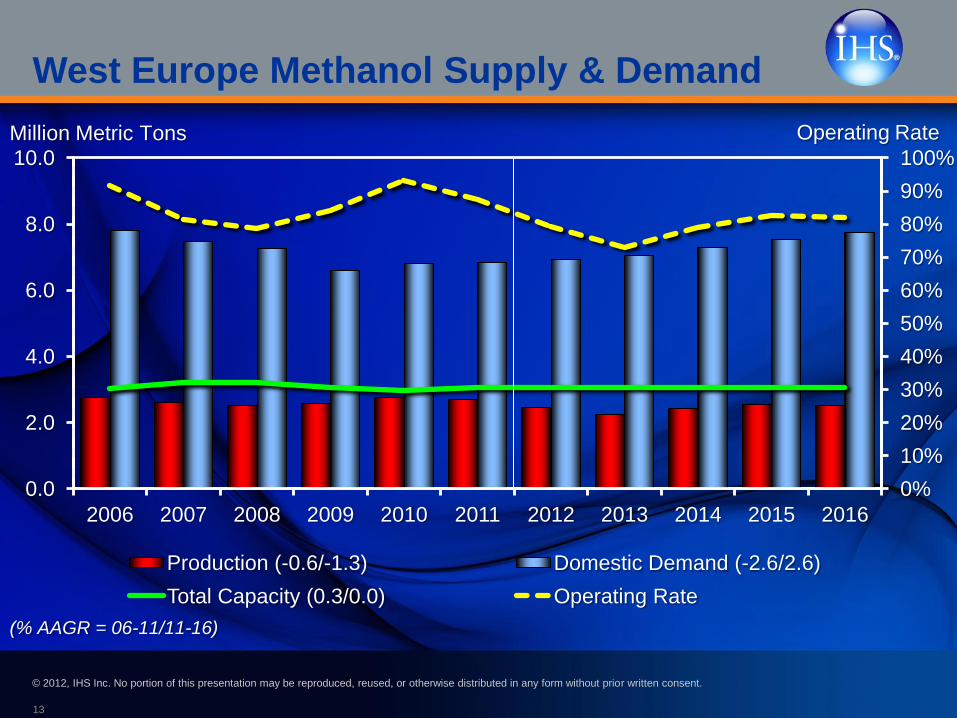

West Europe Methanol Supply & Demand

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.0

2.0

4.0

6.0

8.0

10.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Production (-0.6/-1.3) Domestic Demand (-2.6/2.6)

Total Capacity (0.3/0.0) Operating Rate

Million Metric Tons Operating Rate

(% AAGR = 06-11/11-16)

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Middle East

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

15

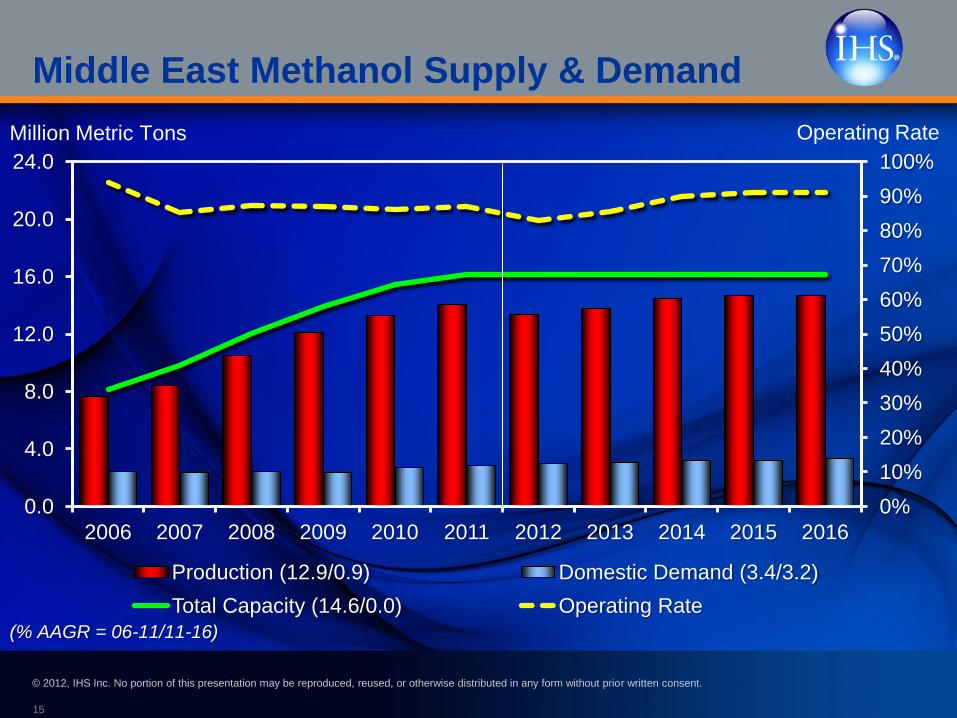

Middle East Methanol Supply & Demand

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.0

4.0

8.0

12.0

16.0

20.0

24.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Production (12.9/0.9) Domestic Demand (3.4/3.2)

Total Capacity (14.6/0.0) Operating Rate

Million Metric Tons Operating Rate

(% AAGR = 06-11/11-16)

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Asia

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

17

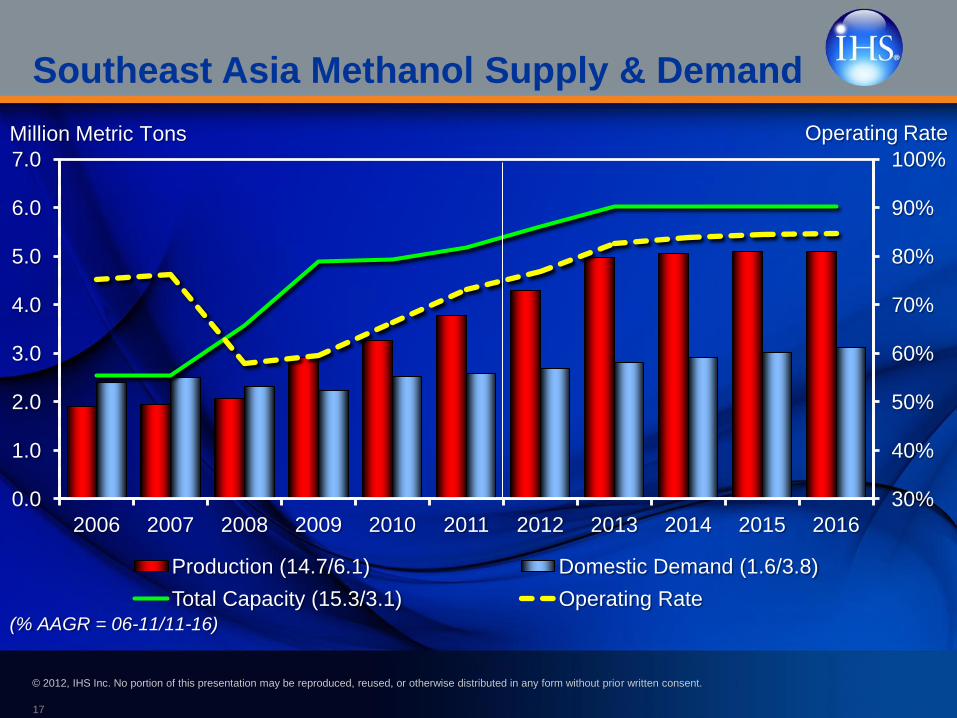

Southeast Asia Methanol Supply & Demand

30%

40%

50%

60%

70%

80%

90%

100%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Production (14.7/6.1) Domestic Demand (1.6/3.8)

Total Capacity (15.3/3.1) Operating Rate

Million Metric Tons Operating Rate

(% AAGR = 06-11/11-16)

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

18

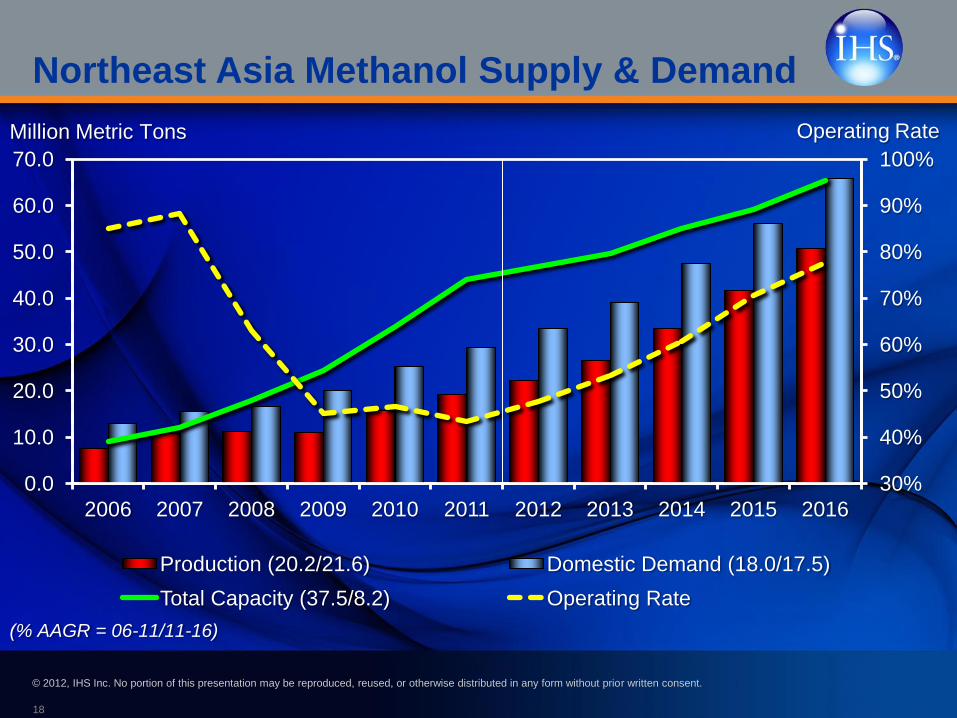

Northeast Asia Methanol Supply & Demand

30%

40%

50%

60%

70%

80%

90%

100%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Production (20.2/21.6) Domestic Demand (18.0/17.5)

Total Capacity (37.5/8.2) Operating Rate

Million Metric Tons Operating Rate

(% AAGR = 06-11/11-16)

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Numerous Coal to Olefin Projects Are Coming

Shenhua Baotou

MTO: 600 KTA

On-stream: Aug 2010

Shenhua Ningmei

MTP: 500 KTA

Q2/2011

2nd Phase MTP: 500 KTA

Mid/2014

Datang Intl

MTP: 500 KTA

Q1/2012

Zhongyuan PC

MTO: 200 KTA

On-stream: Oct 2011

Shaanxi Yanchang

MTO: 900 KTA

Mid/2014

Yankuang

MTO: 600 KTA

End 2014

Shanxi Coking

MTO: 600 KTA

End 2014

Sinopec

MTO: 600 KTA

End 2014

Shenhua/Dow JV

Integrated complex

2016

CPI/Total JV

MTO: 800 KTA

2016

Shenhua

MTO: 600 KTA

2016

Yili Meidianhua

MTO: 600 KTA

2016

Yulin Energy & Chem

MTO: 600 KTA

Q2/2013

Pucheng Clean Energy

MTO: 680 KTA

Mid/2013

Zhejiang Heyuan

MTO: 600 KTA

Q1/2013

Wison

MTO: 300 KTA

End 2012

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Americas

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

21

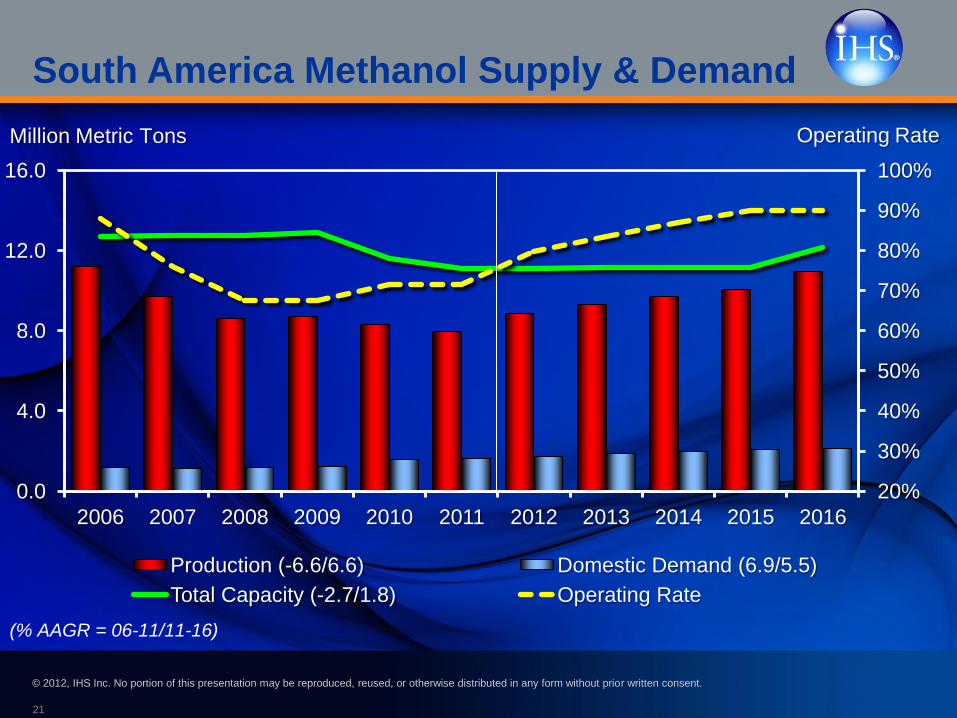

South America Methanol Supply & Demand

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.0

4.0

8.0

12.0

16.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Production (-6.6/6.6) Domestic Demand (6.9/5.5)

Total Capacity (-2.7/1.8) Operating Rate

Million Metric Tons Operating Rate

(% AAGR = 06-11/11-16)

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

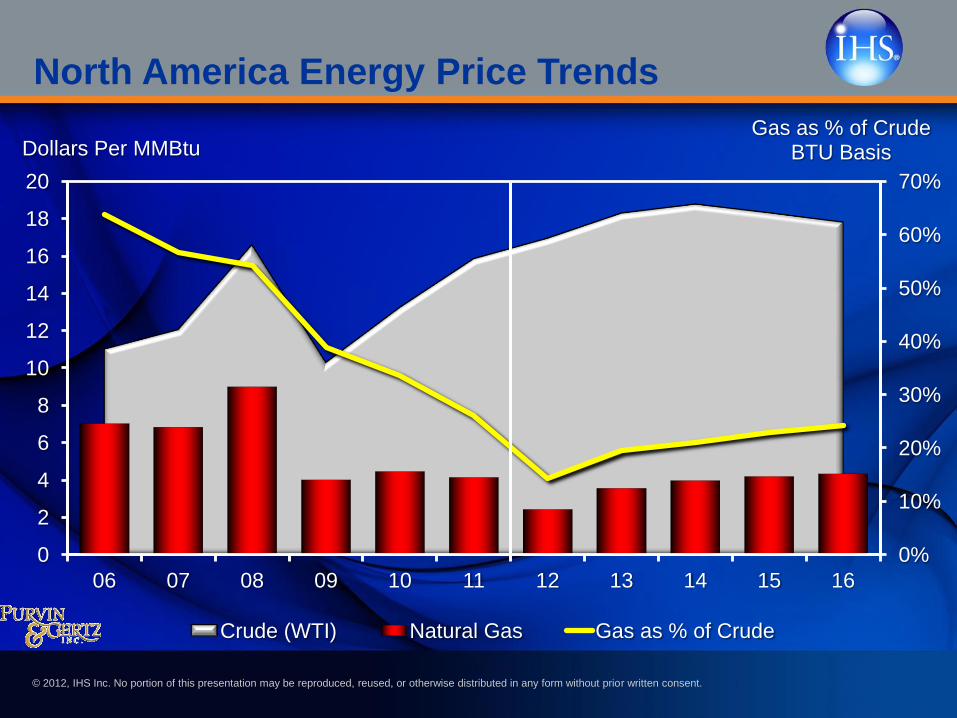

North America Energy Price Trends

0%

10%

20%

30%

40%

50%

60%

70%

0

2

4

6

8

10

12

14

16

18

20

06 07 08 09 10 11 12 13 14 15 16

Gas as % of Crude BTU Basis Dollars Per MMBtu

Crude (WTI) Natural Gas Gas as % of Crude

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

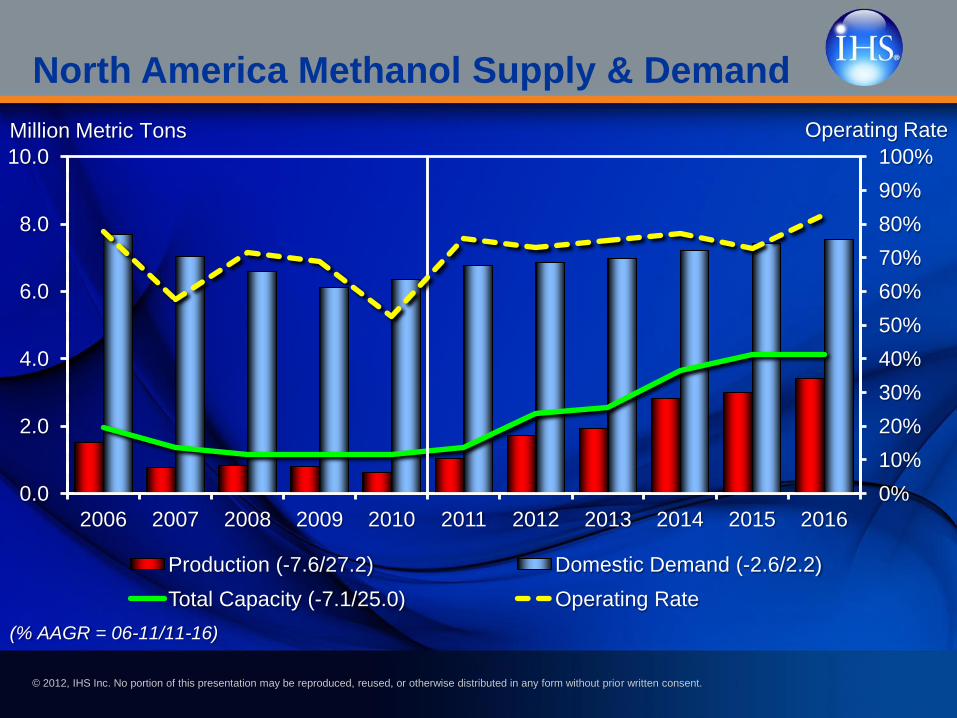

North America Methanol Supply & Demand

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.0

2.0

4.0

6.0

8.0

10.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Production (-7.6/27.2) Domestic Demand (-2.6/2.2)

Total Capacity (-7.1/25.0) Operating Rate

Million Metric Tons Operating Rate

(% AAGR = 06-11/11-16)

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0%

20%

40%

60%

80%

100%

0

2

4

6

8

10

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Formaldehyde Acetic Acid MTBE/TAME

Methyl Methacrylate Gasoline/Fuel Methylamines

Solvents DMT/Others Operating Rate

Million Metric Tons Operating Rate

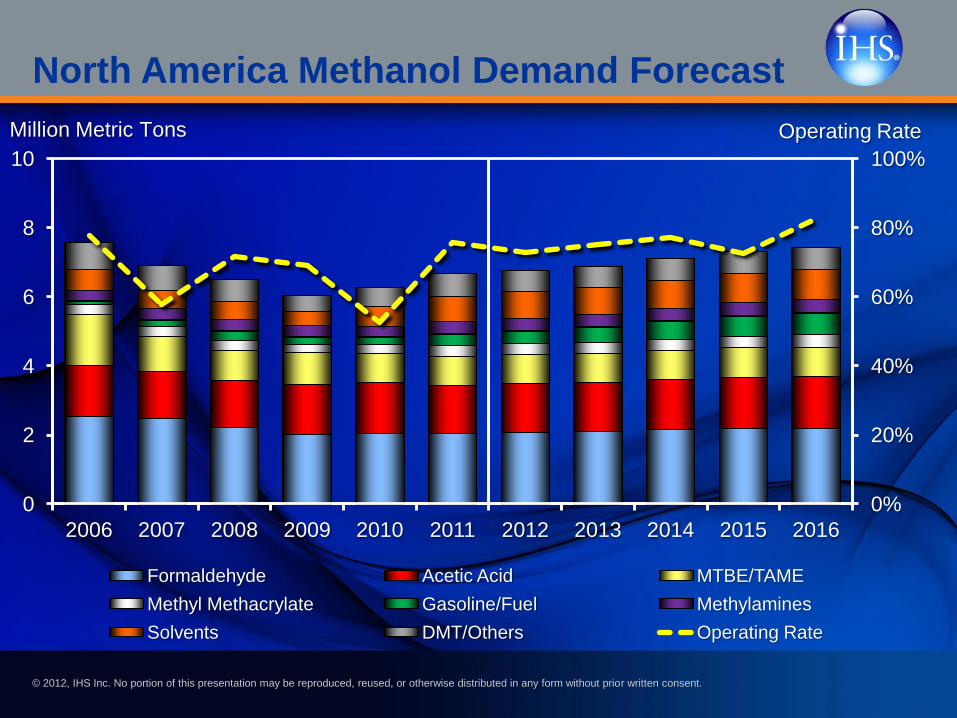

North America Methanol Demand Forecast

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

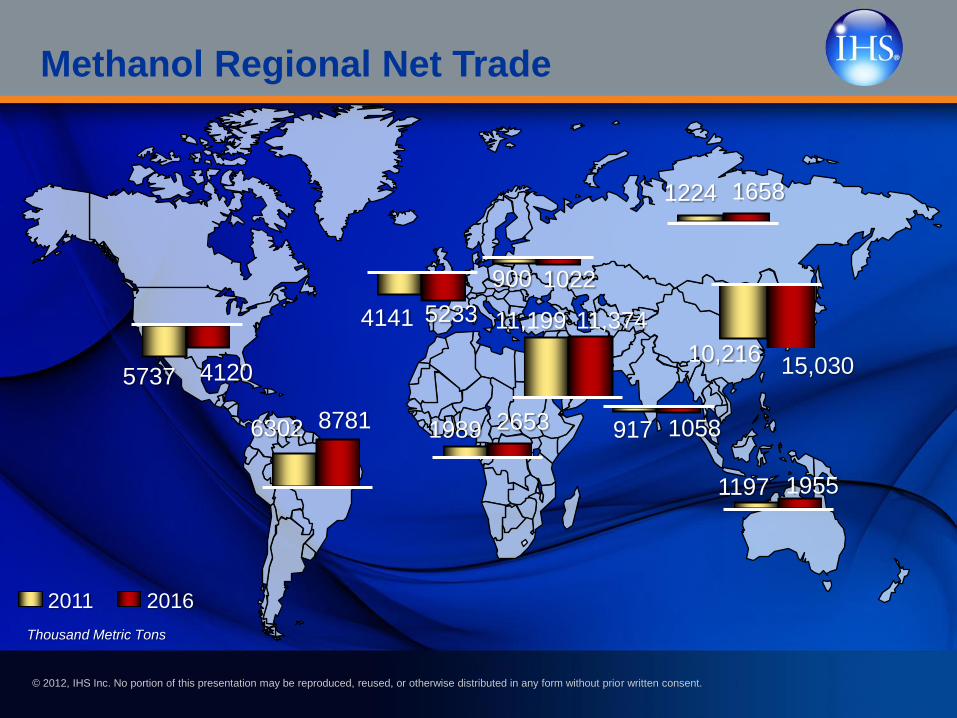

Methanol Regional Net Trade

2011 2016

Thousand Metric Tons

5737 4120

6302 8781 1989 2653

4141 5233

1224 1658

900 1022

11,199 11,374

10,216 15,030

1197 1955

917 1058

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Price

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

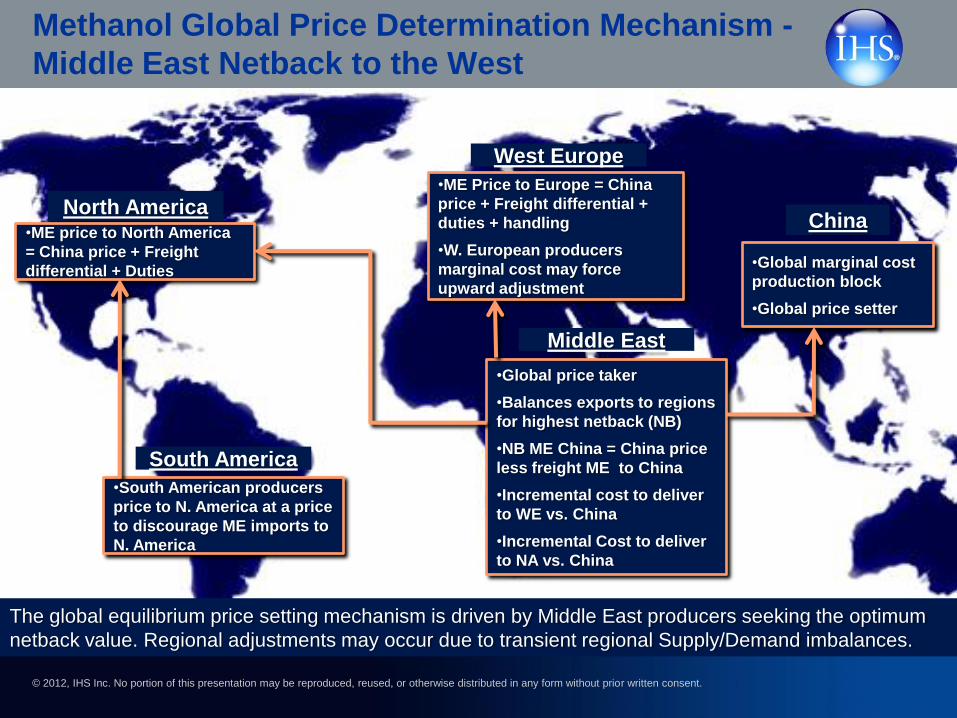

North America •ME price to North America

= China price + Freight

differential + Duties

South America

•South American producers

price to N. America at a price

to discourage ME imports to

N. America

West Europe

•ME Price to Europe = China

price + Freight differential +

duties + handling

•W. European producers

marginal cost may force

upward adjustment

Middle East

•Global price taker

•Balances exports to regions

for highest netback (NB)

•NB ME China = China price

less freight ME to China

•Incremental cost to deliver

to WE vs. China

•Incremental Cost to deliver

to NA vs. China

China

•Global marginal cost

production block

•Global price setter

The global equilibrium price setting mechanism is driven by Middle East producers seeking the optimum

netback value. Regional adjustments may occur due to transient regional Supply/Demand imbalances.

Methanol Global Price Determination Mechanism -

Middle East Netback to the West

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

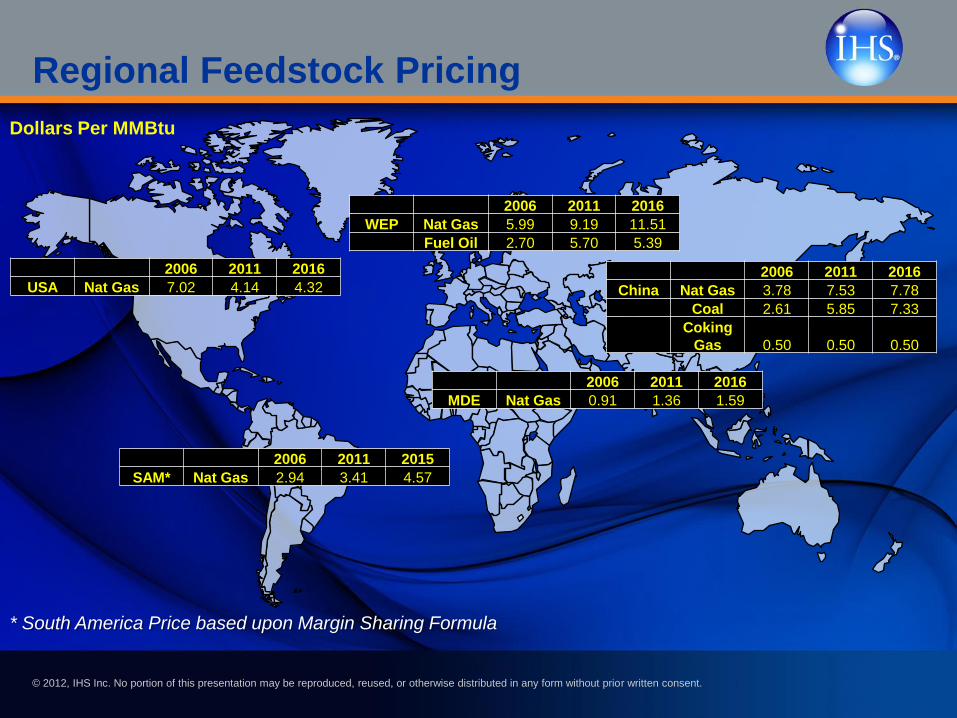

Regional Feedstock Pricing

2006 2011 2016

USA Nat Gas 7.02 4.14 4.32

2006 2011 2015

SAM* Nat Gas 2.94 3.41 4.57

2006 2011 2016

WEP Nat Gas 5.99 9.19 11.51

Fuel Oil 2.70 5.70 5.39

2006 2011 2016

MDE Nat Gas 0.91 1.36 1.59

2006 2011 2016

China Nat Gas 3.78 7.53 7.78

Coal 2.61 5.85 7.33

Coking

Gas 0.50 0.50 0.50

Dollars Per MMBtu

* South America Price based upon Margin Sharing Formula

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

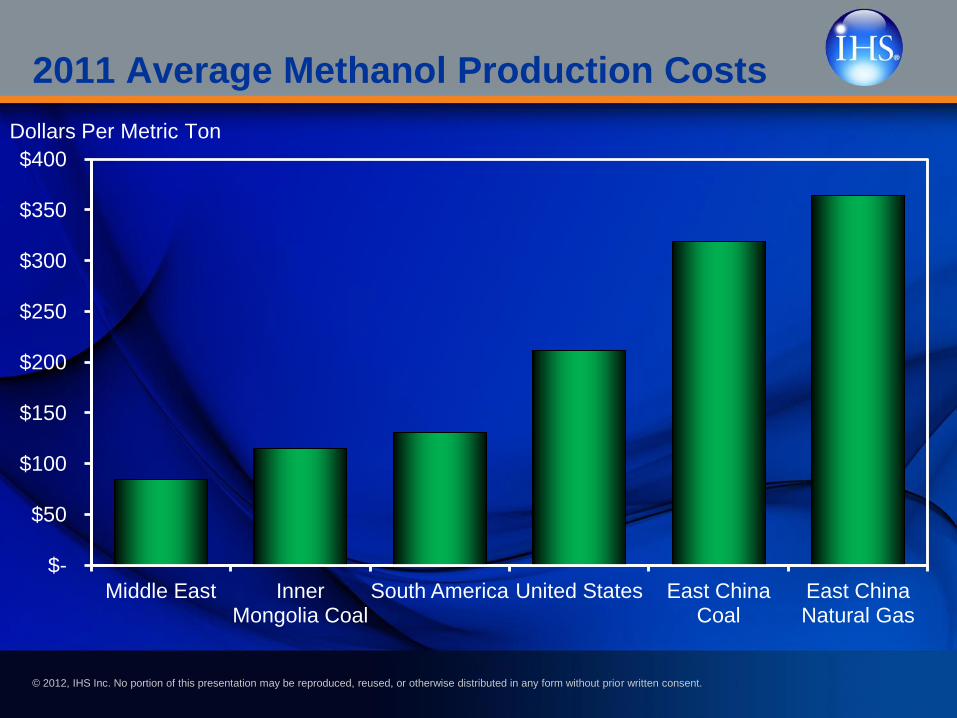

2011 Average Methanol Production Costs

$-

$50

$100

$150

$200

$250

$300

$350

$400

Middle East Inner Mongolia Coal

South America United States East China Coal

East China Natural Gas

Dollars Per Metric Ton

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

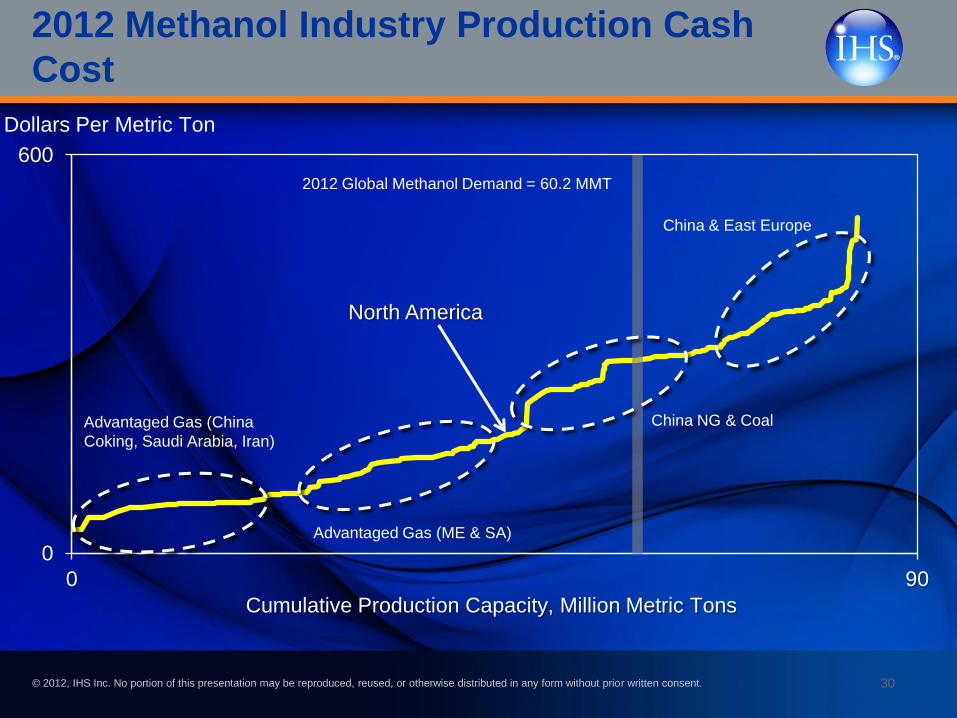

2012 Methanol Industry Production Cash

Cost

30

0

600

0 90

Cumulative Production Capacity, Million Metric Tons

Dollars Per Metric Ton

China & East Europe

China NG & Coal

Advantaged Gas (ME & SA)

Advantaged Gas (China

Coking, Saudi Arabia, Iran)

2012 Global Methanol Demand = 60.2 MMT

North America

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 31

0

100

200

300

400

500

600

700

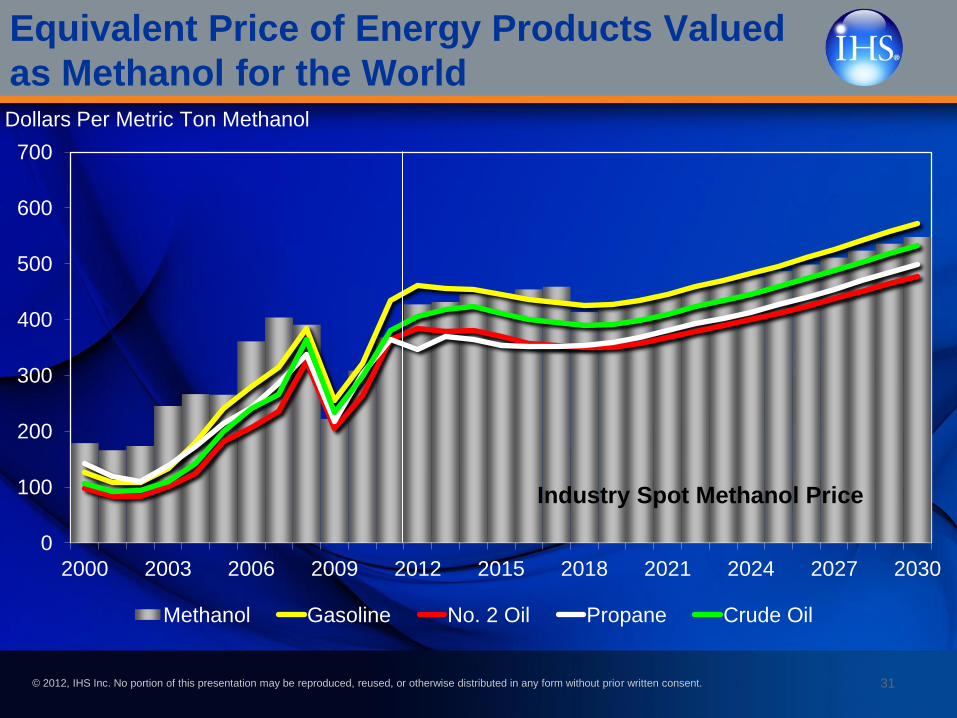

2000 2003 2006 2009 2012 2015 2018 2021 2024 2027 2030

Methanol Gasoline No. 2 Oil Propane Crude Oil

Industry Spot Methanol Price

Dollars Per Metric Ton Methanol

Equivalent Price of Energy Products Valued

as Methanol for the World

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 32

0

100

200

300

400

500

600

700

2000 2003 2006 2009 2012 2015 2018 2021 2024 2027 2030

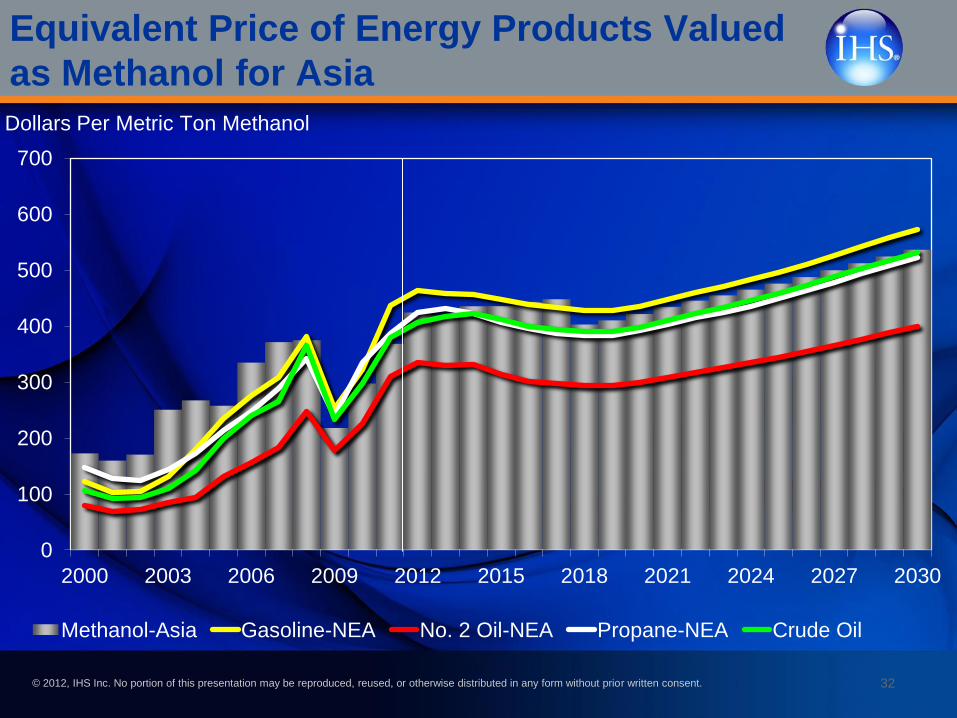

Methanol-Asia Gasoline-NEA No. 2 Oil-NEA Propane-NEA Crude Oil

Dollars Per Metric Ton Methanol

Equivalent Price of Energy Products Valued

as Methanol for Asia

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0

20

40

60

80

100

120

140

160

180

200

0

100

200

300

400

500

600

700

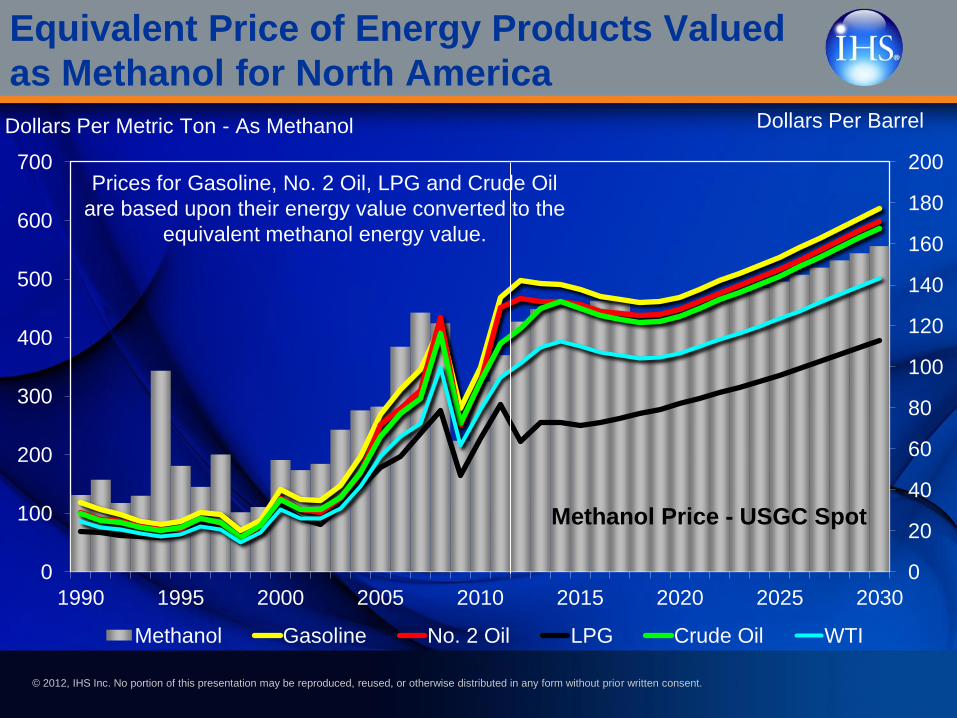

1990 1995 2000 2005 2010 2015 2020 2025 2030

Methanol Gasoline No. 2 Oil LPG Crude Oil WTI

Methanol Price - USGC Spot

Dollars Per Barrel Dollars Per Metric Ton - As Methanol

Prices for Gasoline, No. 2 Oil, LPG and Crude Oil

are based upon their energy value converted to the

equivalent methanol energy value.

Equivalent Price of Energy Products Valued

as Methanol for North America

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

34

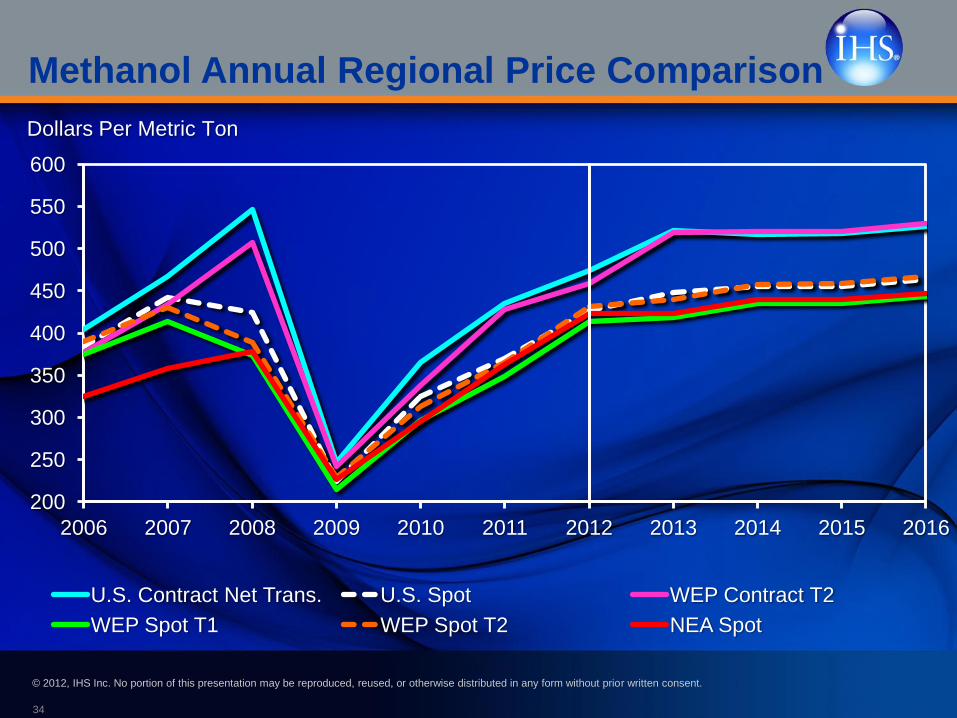

Methanol Annual Regional Price Comparison

200

250

300

350

400

450

500

550

600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

U.S. Contract Net Trans. U.S. Spot WEP Contract T2

WEP Spot T1 WEP Spot T2 NEA Spot

Dollars Per Metric Ton

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Five Key Points for the Methanol Industry

• Methanol demand tracks GDP on average 1.7x

• Conventional derivatives drive base demand

– Fuels have potential for step-out growth

– Energy differentials drive fuels applications

• MTO/MTP bring potential balance shocks

• Economic volatility creates price volatility through end-use demand patterns, inventory management, and credit availability

• Process technology advancing with feedstocks diversity, increased scale, yield improvement, and integration options

• Feed stock dynamics affect supply location

– End-use options for feedstocks

– Sustainability criteria for option selection

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 36

Methanol Derivatives

•Formaldehyde

•Acetyls

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 37

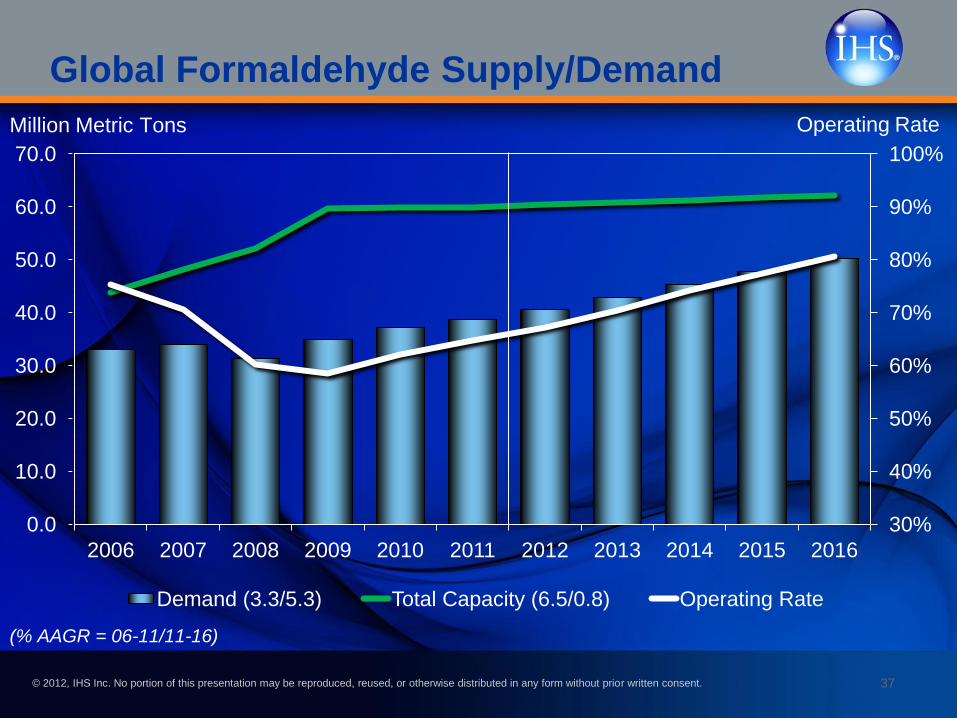

Global Formaldehyde Supply/Demand

30%

40%

50%

60%

70%

80%

90%

100%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Demand (3.3/5.3) Total Capacity (6.5/0.8) Operating Rate

Million Metric Tons Operating Rate

(% AAGR = 06-11/11-16)

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

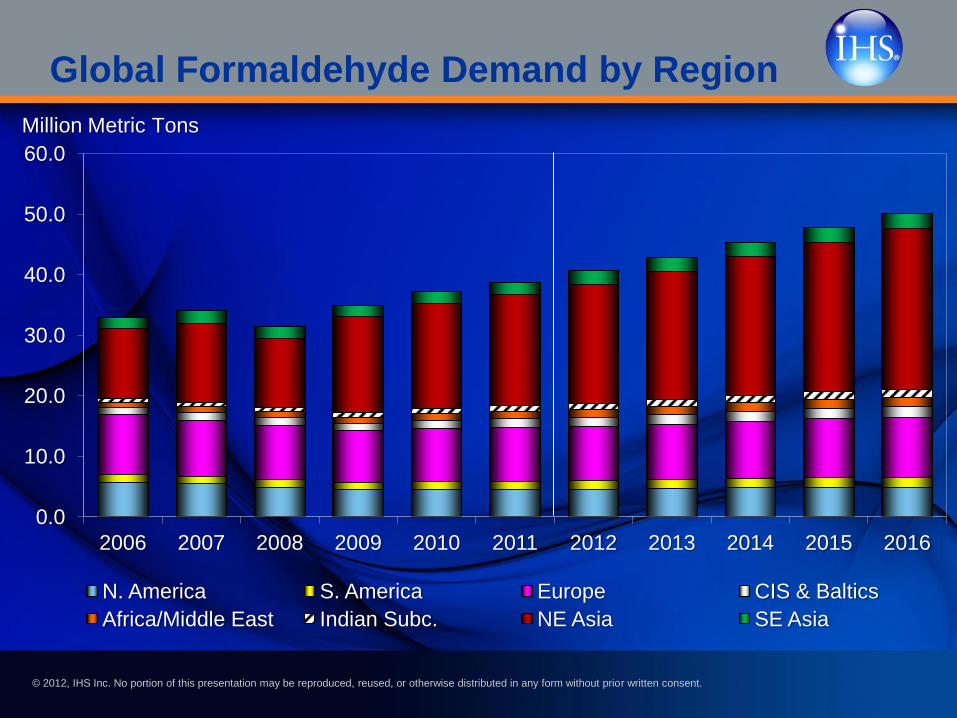

Global Formaldehyde Demand by Region

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

N. America S. America Europe CIS & Baltics

Africa/Middle East Indian Subc. NE Asia SE Asia

Million Metric Tons

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

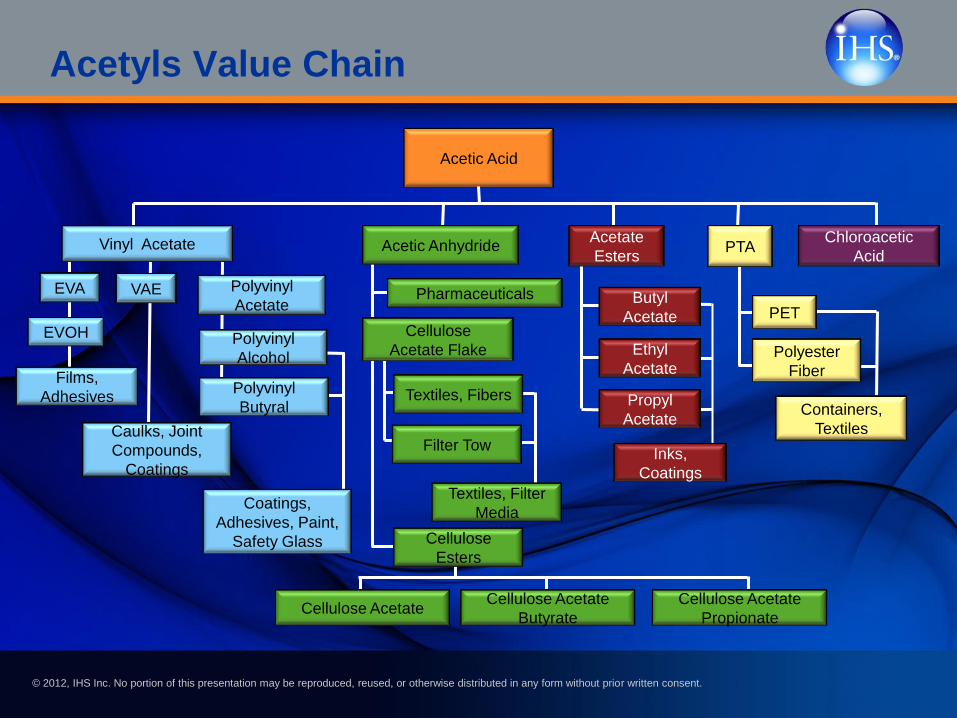

Acetic Acid

EVA VAE

EVOH

Polyvinyl

Acetate

Polyvinyl

Alcohol

Polyvinyl

Butyral

Films,

Adhesives

Caulks, Joint

Compounds,

Coatings

Coatings,

Adhesives, Paint,

Safety Glass

Vinyl Acetate Chloroacetic

Acid

Butyl

Acetate

Ethyl

Acetate

Propyl

Acetate

Inks,

Coatings

Acetate

Esters

PET

Polyester

Fiber

Containers,

Textiles

PTA

Pharmaceuticals

Cellulose

Acetate Flake

Textiles, Fibers

Filter Tow

Textiles, Filter

Media

Acetic Anhydride

Cellulose

Esters

Cellulose Acetate Cellulose Acetate

Butyrate

Cellulose Acetate

Propionate

Acetyls Value Chain

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

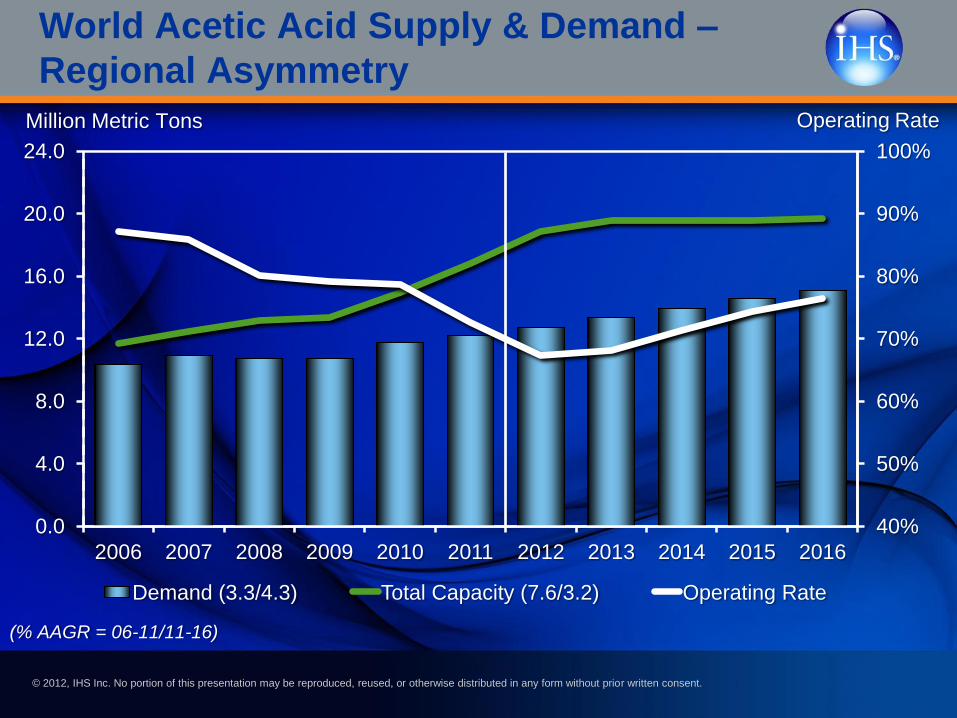

World Acetic Acid Supply & Demand –

Regional Asymmetry

40%

50%

60%

70%

80%

90%

100%

0.0

4.0

8.0

12.0

16.0

20.0

24.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Demand (3.3/4.3) Total Capacity (7.6/3.2) Operating Rate

Million Metric Tons Operating Rate

(% AAGR = 06-11/11-16)

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

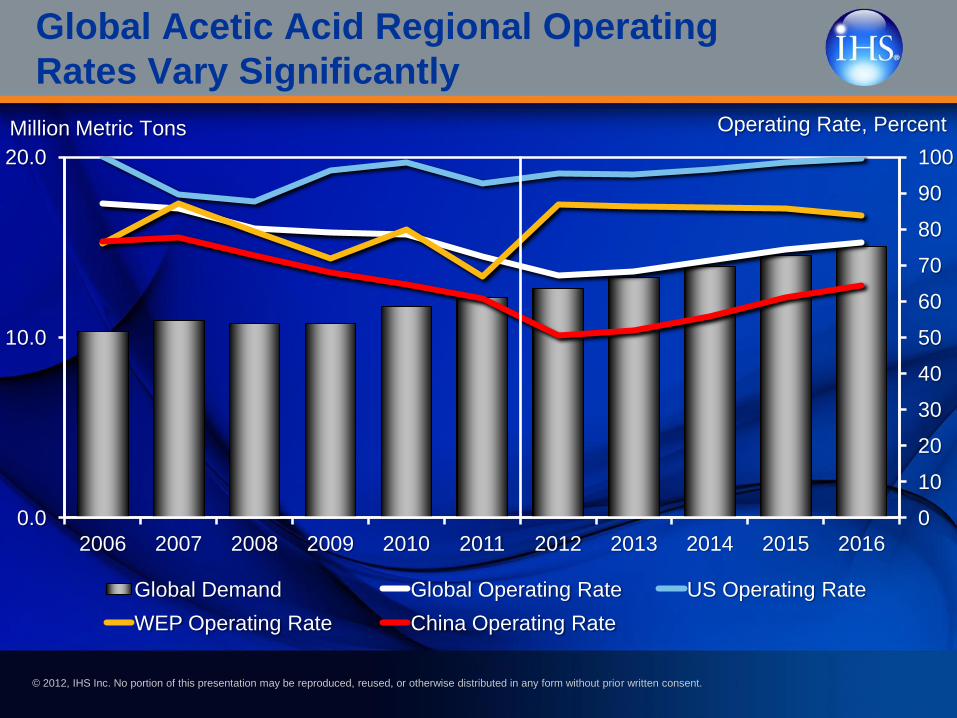

Global Acetic Acid Regional Operating

Rates Vary Significantly

0

10

20

30

40

50

60

70

80

90

100

0.0

10.0

20.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Global Demand Global Operating Rate US Operating Rate

WEP Operating Rate China Operating Rate

Million Metric Tons Operating Rate, Percent

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

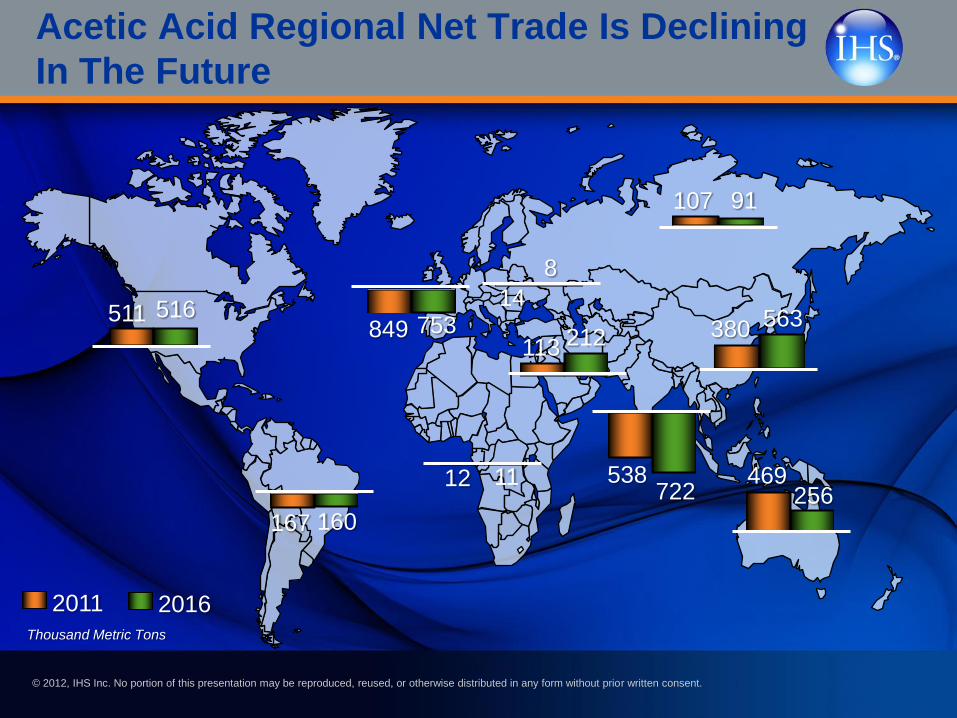

Acetic Acid Regional Net Trade Is Declining

In The Future

2011 2016 Thousand Metric Tons

511 516

167 160

12 11

849 753

107 91

14

8

113 212 380 563

469 256

538 722

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

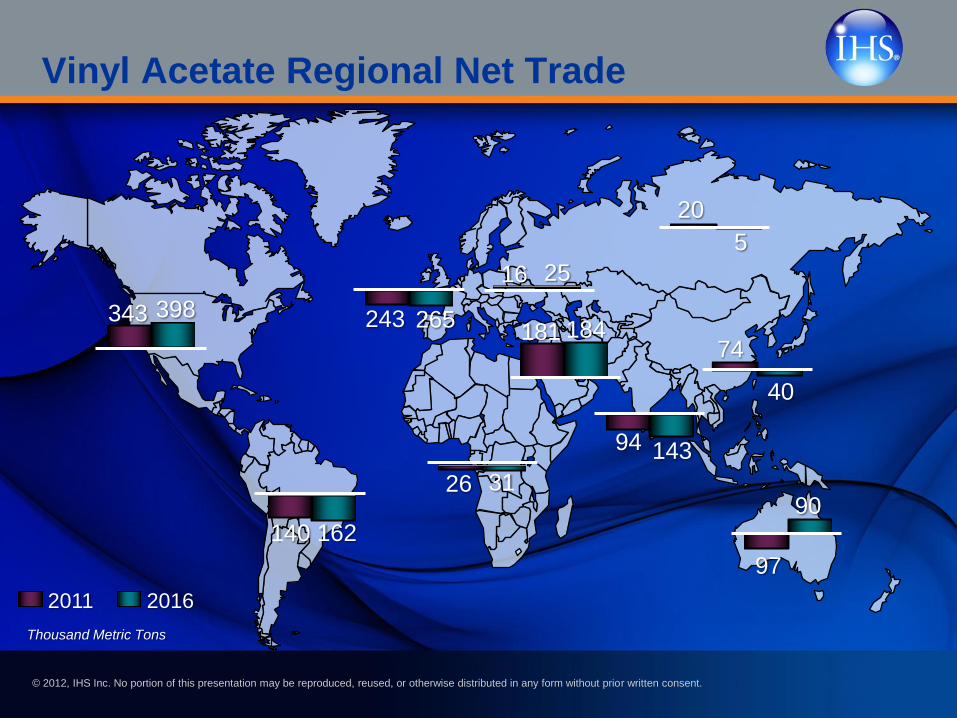

Vinyl Acetate Regional Net Trade

2011 2016

Thousand Metric Tons

343 398

140 162

26 31

243 265

20

5

16 25

181 184 74

40

97

90

94 143

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Acetyls Value Chain-Conclusions

•Acetic Acid & VAM market dynamics driven by: Cost position

Regional discipline.

• Acetyls economics driven by Feedstock position, Scale &

Integration, Technology.

•Methanol will tighten through 2016. Iranian trade position &

feedstock cost shifts will have greatest effects on supply

balance and price.

• Coal to ethanol through acetic acid is a potential growth

engine for the acetyls chain.