Embed Size (px)

Citation preview

Global Oil Markets and Hedging Are Trends Your Friend?

EnerCom March 2016 – Fredrik Sagen Andersen

Non-OPEC to painfully balance the oil market by moving from record growth in 2014 to production declines in 2016

2

3

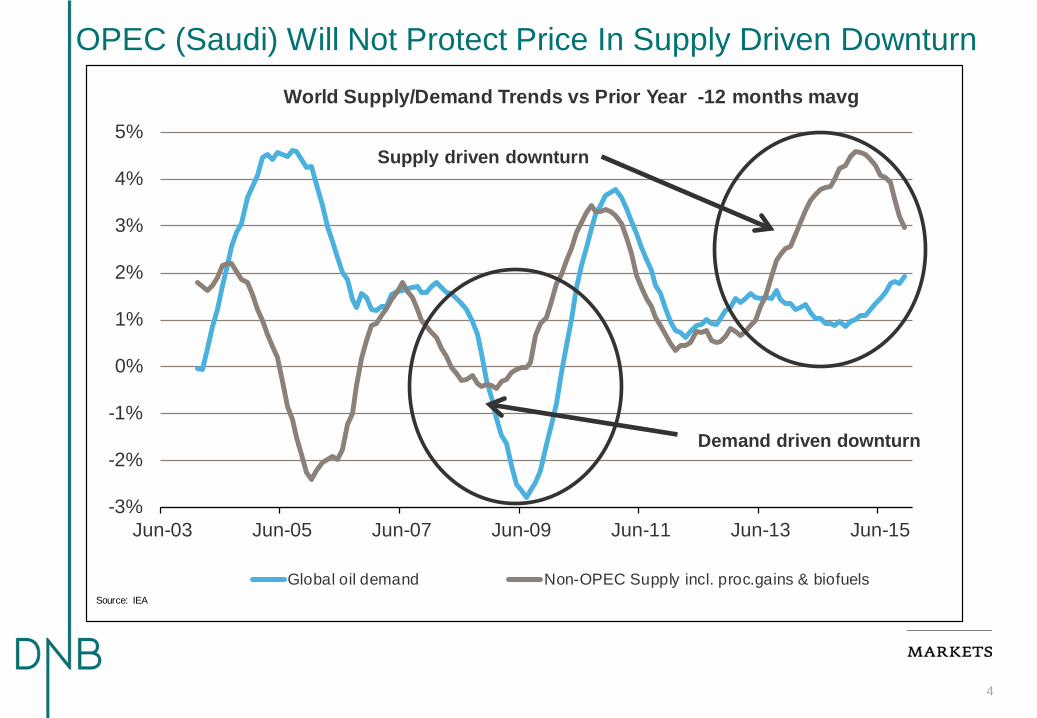

OPEC (Saudi) Will Not Protect Price In Supply Driven Downturn

4

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Jun-03 Jun-05 Jun-07 Jun-09 Jun-11 Jun-13 Jun-15

World Supply/Demand Trends vs Prior Year -12 months mavg

Global oil demand Non-OPEC Supply incl. proc.gains & biofuelsSource: IEA

Supply driven downturn

Demand driven downturn

Bearish Headlines

5

6

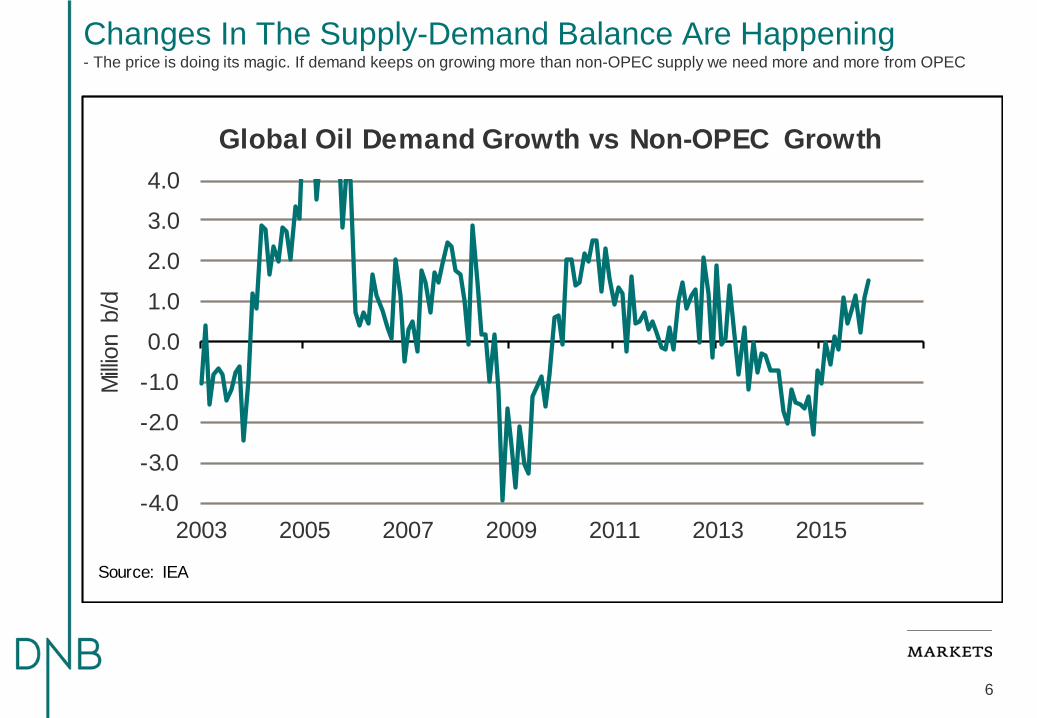

Changes In The Supply-Demand Balance Are Happening - The price is doing its magic. If demand keeps on growing more than non-OPEC supply we need more and more from OPEC

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2003 2005 2007 2009 2011 2013 2015

Milli

on b

/dGlobal Oil Demand Growth vs Non-OPEC Growth

Source: IEA

7

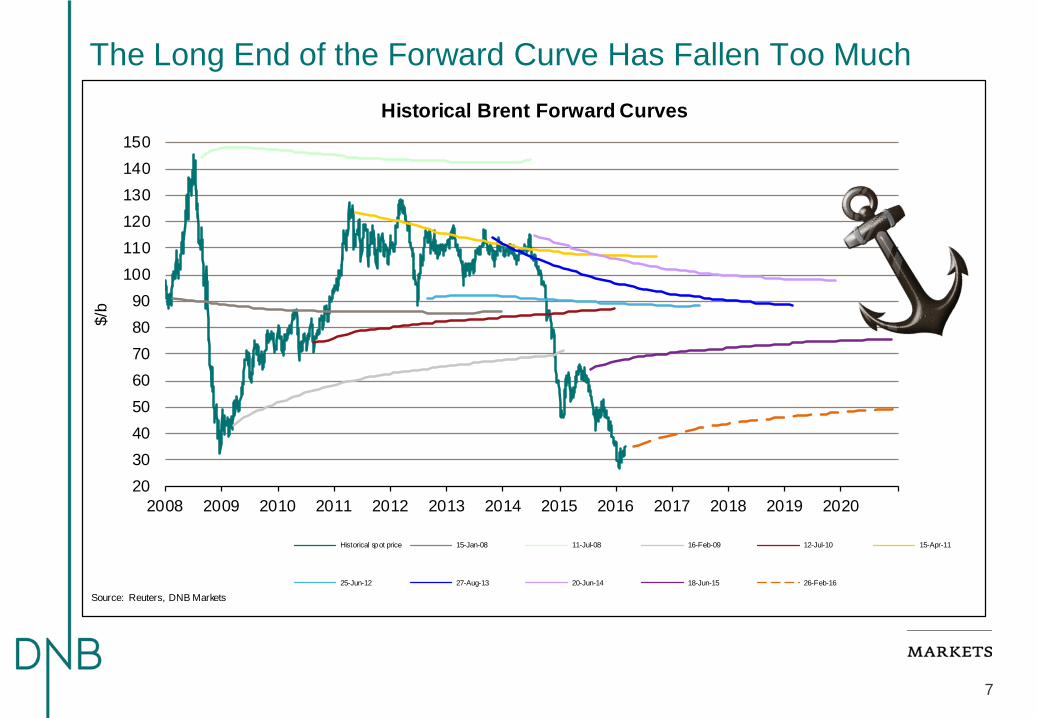

The Long End of the Forward Curve Has Fallen Too Much

2030405060708090

100110120130140150

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

$/b

Historical Brent Forward Curves

Historical spot price 15-Jan-08 11-Jul-08 16-Feb-09 12-Jul-10 15-Apr-11

25-Jun-12 27-Aug-13 20-Jun-14 18-Jun-15 26-Feb-16

Source: Reuters, DNB Markets

8

The Headline Oversupply Not Visible In Time Spreads - The graph below suggest that the last drop in oil prices is sentiment driven and not fundamentally driven

20

30

40

50

60

70

80

90

100

110

120

130

Jan/2009 Jan/2010 Jan/2011 Jan/2012 Jan/2013 Jan/2014 Jan/2015 Jan/2016

$/b

Modelled Brent Price Based On Time Spread (1 vs 3)(Based on daily correlation since 2009)

Modeled Brent Price, 20 days rolling avg Real Brent Price

-5

-4

-3

-2

-1

0

1

2

3

4

5

25

45

65

85

105

125

145

165

Jan-2007 Jan-2009 Jan-2011 Jan-2013 Jan-2015

$/b

time

spre

ad

$/b

flat p

rice

Brent Price vs Structure of FWD-Curve(Brent 1-3 as leading indicator for Flat Price)

Real Brent Price Brent Fwd Structure

9

Short Sellers Have Been In Command the Last Year

20

25

30

35

40

45

50

55

60

65

70

-350

-300

-250

-200

-150

-100

-50

0

Jan-15 Jul-15 Jan-16

$/b

Mill

ion

barre

ls

Non-Commercial Short Positions vs WTI

Source: CFTC

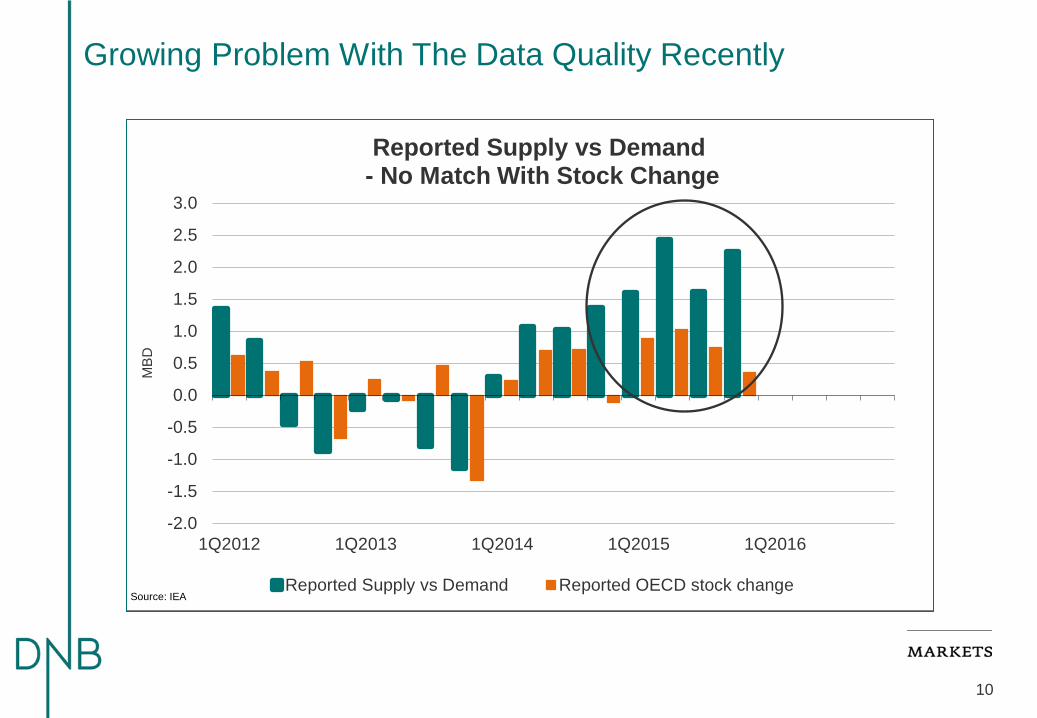

10

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1Q2012 1Q2013 1Q2014 1Q2015 1Q2016

MBD

Reported Supply vs Demand- No Match With Stock Change

Reported Supply vs Demand Reported OECD stock changeSource: IEA

Growing Problem With The Data Quality Recently

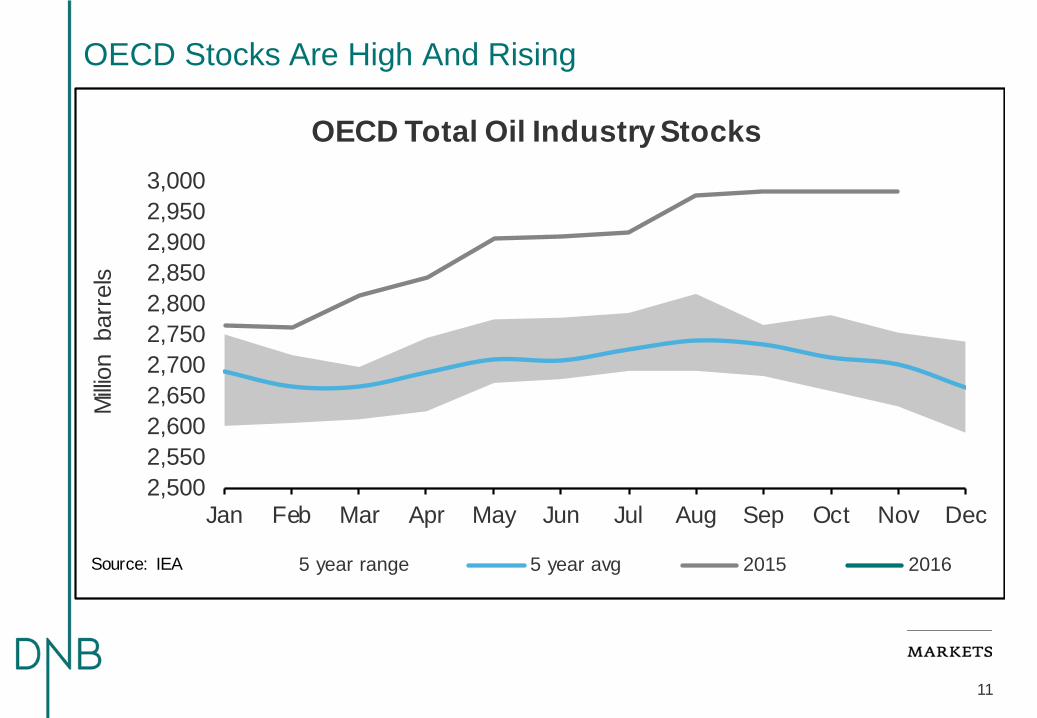

11

2,5002,5502,6002,6502,7002,7502,8002,8502,9002,9503,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Milli

on b

arre

lsOECD Total Oil Industry Stocks

5 year range 5 year avg 2015 2016Source: IEA

OECD Stocks Are High And Rising

12

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

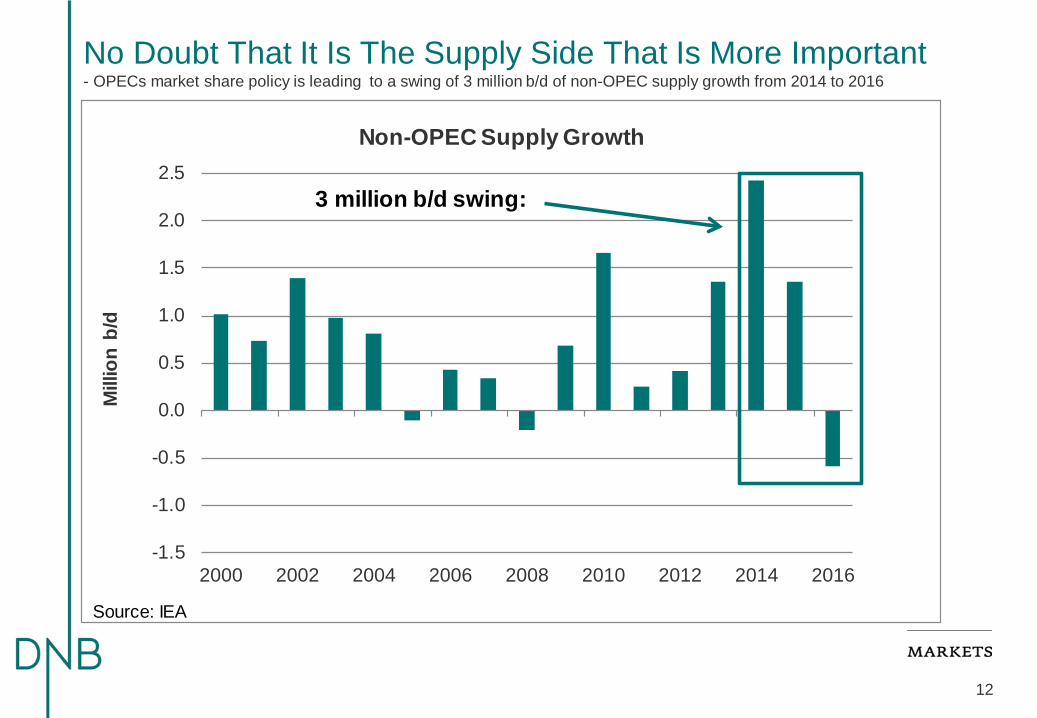

2000 2002 2004 2006 2008 2010 2012 2014 2016

Mill

ion

b/d

Non-OPEC Supply Growth

Source: IEA

3 million b/d swing:

No Doubt That It Is The Supply Side That Is More Important - OPECs market share policy is leading to a swing of 3 million b/d of non-OPEC supply growth from 2014 to 2016

13

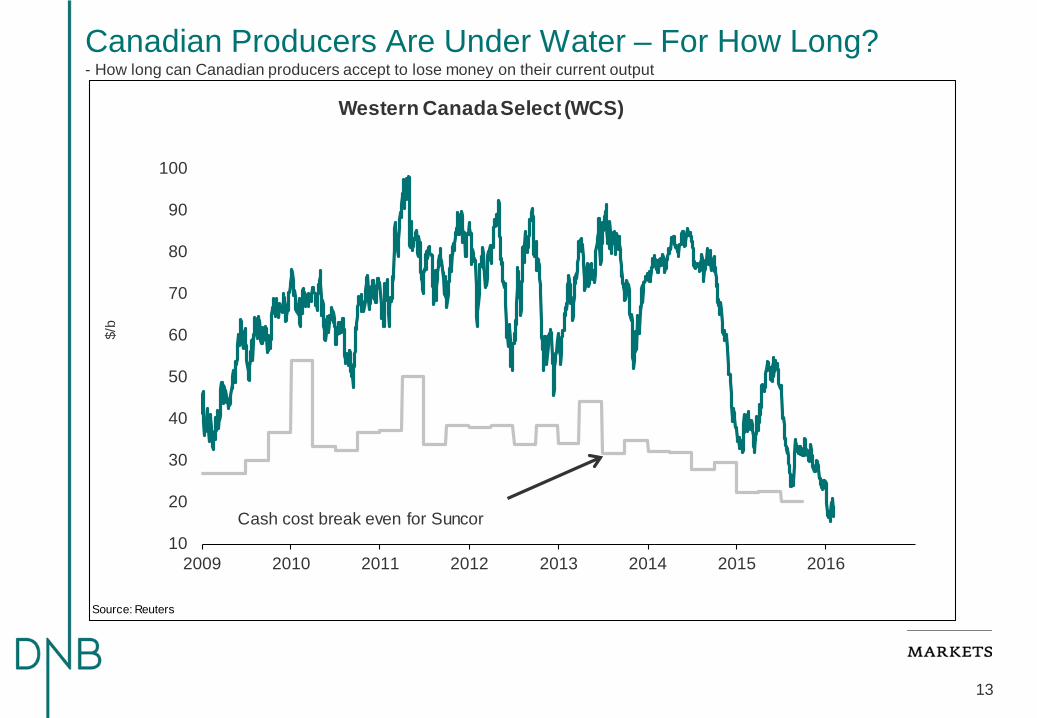

Canadian Producers Are Under Water – For How Long? - How long can Canadian producers accept to lose money on their current output

10

20

30

40

50

60

70

80

90

100

2009 2010 2011 2012 2013 2014 2015 2016

$/b

Western Canada Select (WCS)

Source: Reuters

Cash cost break even for Suncor

14

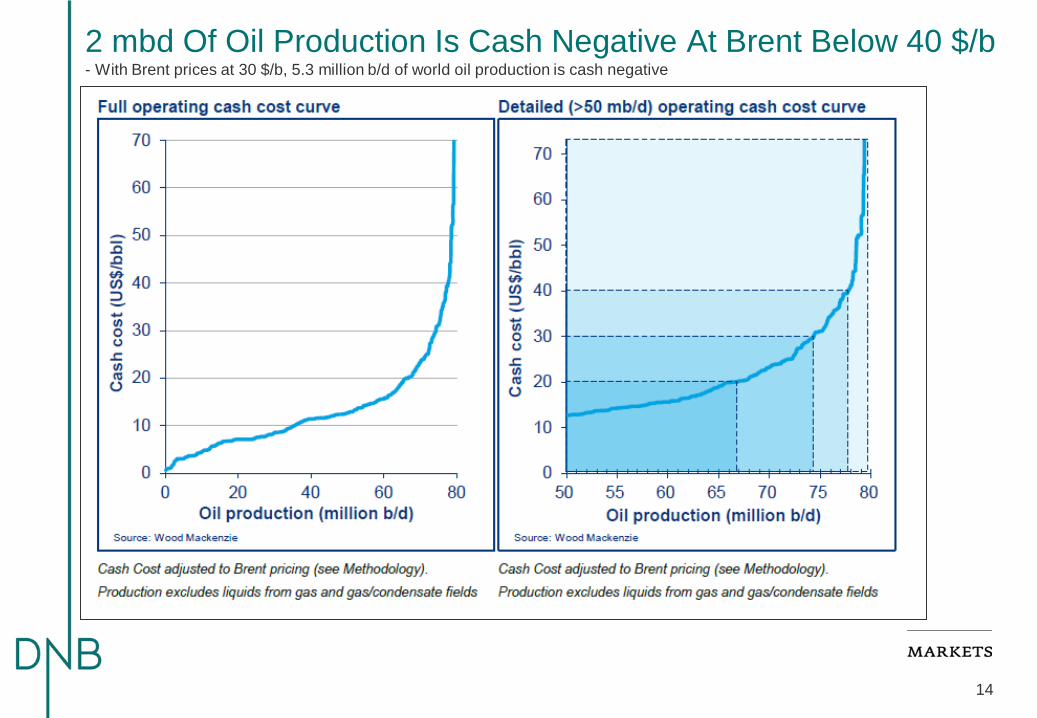

2 mbd Of Oil Production Is Cash Negative At Brent Below 40 $/b - With Brent prices at 30 $/b, 5.3 million b/d of world oil production is cash negative

15

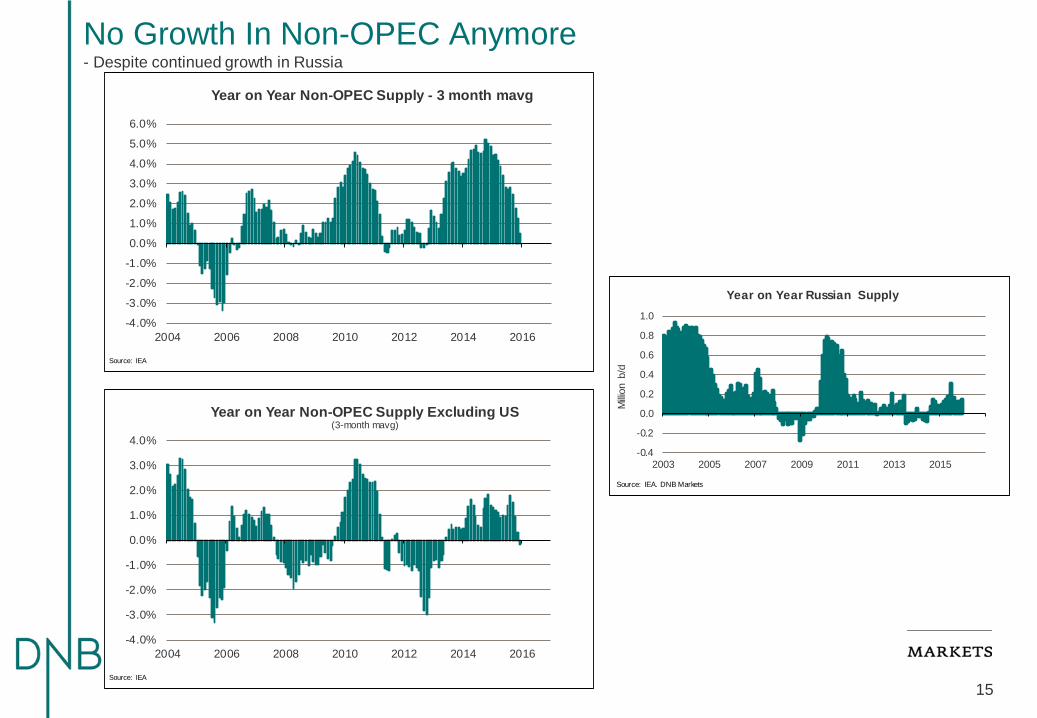

No Growth In Non-OPEC Anymore - Despite continued growth in Russia

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2004 2006 2008 2010 2012 2014 2016

Year on Year Non-OPEC Supply - 3 month mavg

Source: IEA

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2004 2006 2008 2010 2012 2014 2016

Year on Year Non-OPEC Supply Excluding US(3-month mavg)

Source: IEA

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

2003 2005 2007 2009 2011 2013 2015

Milli

on b

/d

Year on Year Russian Supply

Source: IEA, DNB Markets

16

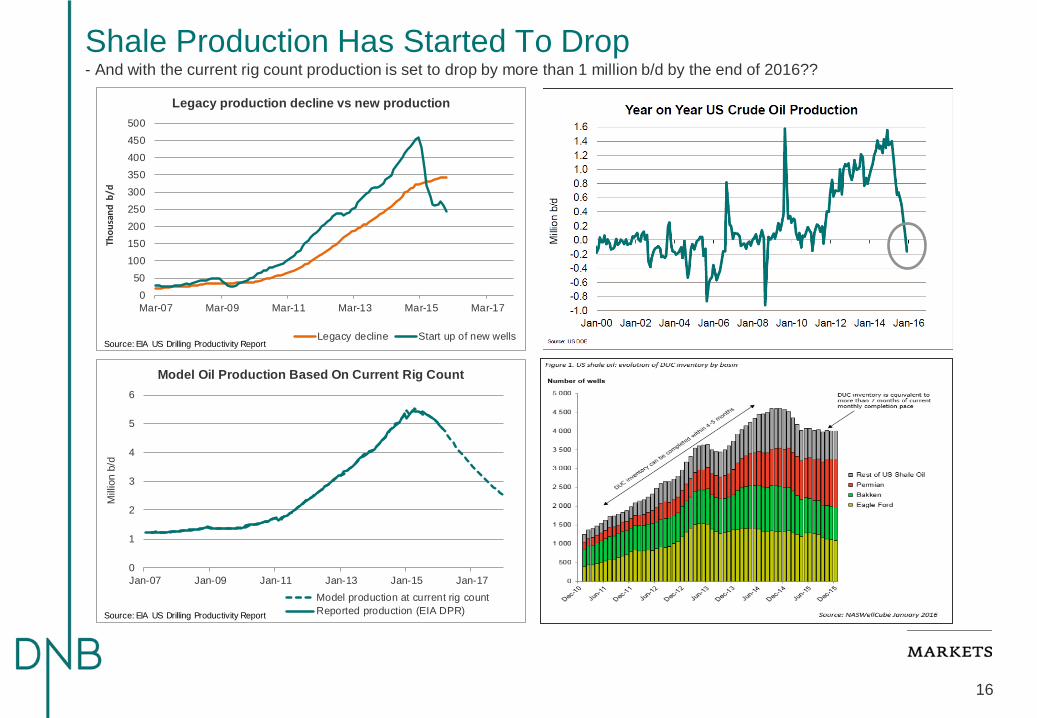

Shale Production Has Started To Drop - And with the current rig count production is set to drop by more than 1 million b/d by the end of 2016??

050

100150200250300350400450500

Mar-07 Mar-09 Mar-11 Mar-13 Mar-15 Mar-17

Thou

sand

b/d

Legacy production decline vs new production

Legacy decline Start up of new wellsSource: EIA US Drilling Productivity Report

0

1

2

3

4

5

6

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15 Jan-17

Mill

ion

b/d

Model Oil Production Based On Current Rig Count

Model production at current rig countReported production (EIA DPR)Source: EIA US Drilling Productivity Report

17

Enormous Cuts In Global Oil Spending Will Continue in 2016 - This sets the stage for lower production/lower production growth in the future

18

Accelerating Decline Rates In Russia - Source: IEA

19

Source: DNB Markets, Rystad Energy

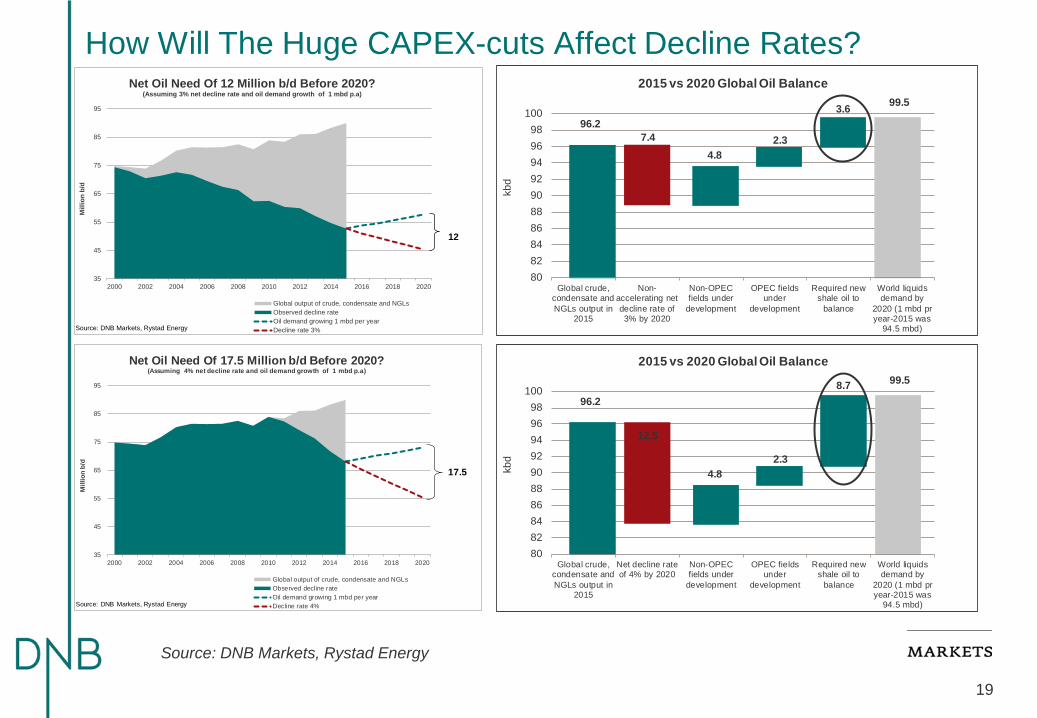

How Will The Huge CAPEX-cuts Affect Decline Rates?

35

45

55

65

75

85

95

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mill

ion

b/d

Net Oil Need Of 12 Million b/d Before 2020?(Assuming 3% net decline rate and oil demand growth of 1 mbd p.a)

Global output of crude, condensate and NGLsObserved decline rateOil demand growing 1 mbd per yearDecline rate 3%

12

Source: DNB Markets, Rystad Energy

99.5

7.44.8

2.3

3.696.2

80828486889092949698

100

Global crude,condensate andNGLs output in

2015

Non-accelerating netdecline rate of3% by 2020

Non-OPECfields under

development

OPEC fieldsunder

development

Required newshale oil to

balance

World liquidsdemand by

2020 (1 mbd pryear-2015 was

94.5 mbd)

kbd

2015 vs 2020 Global Oil Balance

35

45

55

65

75

85

95

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mill

ion

b/d

Net Oil Need Of 17.5 Million b/d Before 2020?(Assuming 4% net decline rate and oil demand growth of 1 mbd p.a)

Global output of crude, condensate and NGLsObserved decline rateOil demand growing 1 mbd per yearDecline rate 4%

17.5

Source: DNB Markets, Rystad Energy

99.5

12.5

4.82.3

8.796.2

80828486889092949698

100

Global crude,condensate andNGLs output in

2015

Net decline rateof 4% by 2020

Non-OPECfields under

development

OPEC fieldsunder

development

Required newshale oil to

balance

World liquidsdemand by

2020 (1 mbd pryear-2015 was

94.5 mbd)

kbd

2015 vs 2020 Global Oil Balance

20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Milli

on b

/d

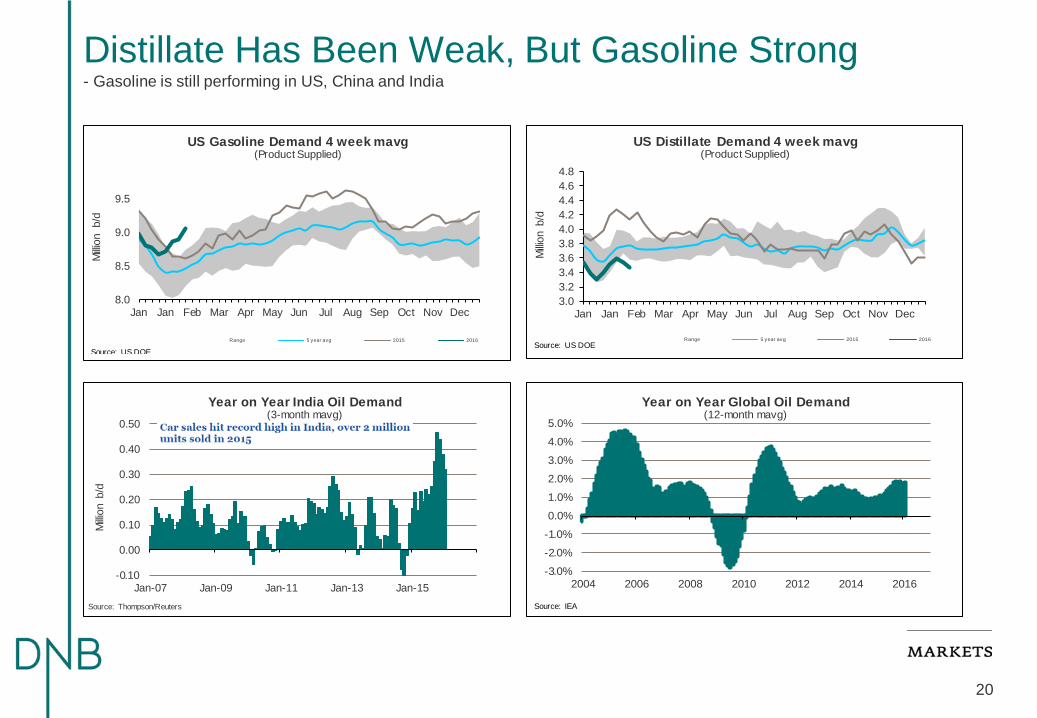

Year on Year India Oil Demand(3-month mavg)

Source: Thompson/Reuters

-3.0%-2.0%-1.0%0.0%1.0%2.0%3.0%4.0%5.0%

2004 2006 2008 2010 2012 2014 2016

Year on Year Global Oil Demand(12-month mavg)

Source: IEA

8.0

8.5

9.0

9.5

Jan Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Milli

on b

/d

US Gasoline Demand 4 week mavg(Product Supplied)

Range 5 year avg 2015 2016

Source: US DOE

3.03.23.43.63.84.04.24.44.64.8

Jan Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Milli

on b

/d

US Distillate Demand 4 week mavg(Product Supplied)

Range 5 year avg 2015 2016Source: US DOE

Distillate Has Been Weak, But Gasoline Strong - Gasoline is still performing in US, China and India

21

2930

2950

2970

2990

3010

3030

3050

3070

3090

3110

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

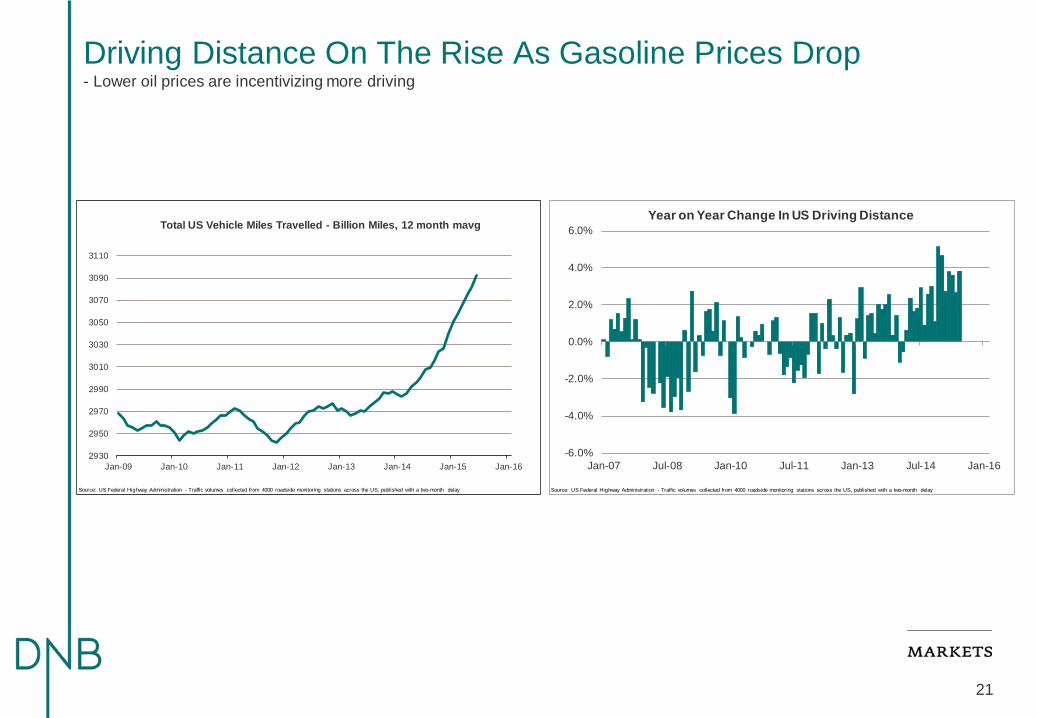

Total US Vehicle Miles Travelled - Billion Miles, 12 month mavg

Source: US Federal Highway Administration - Traffic volumes collected from 4000 roadside monitoring stations across the US, published with a two-month delay

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Jan-07 Jul-08 Jan-10 Jul-11 Jan-13 Jul-14 Jan-16

Year on Year Change In US Driving Distance

Source: US Federal Highway Administration - Traffic volumes collected from 4000 roadside monitoring stations across the US, published with a two-month delay

Driving Distance On The Rise As Gasoline Prices Drop - Lower oil prices are incentivizing more driving

22

8

10

12

14

16

18

20

22

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

Jul-08 Jul-10 Jul-12 Jul-14

Annu

aliz

ed M

illion

Car

s So

ld

Ligh

t Tru

cks

Mar

ket S

hare

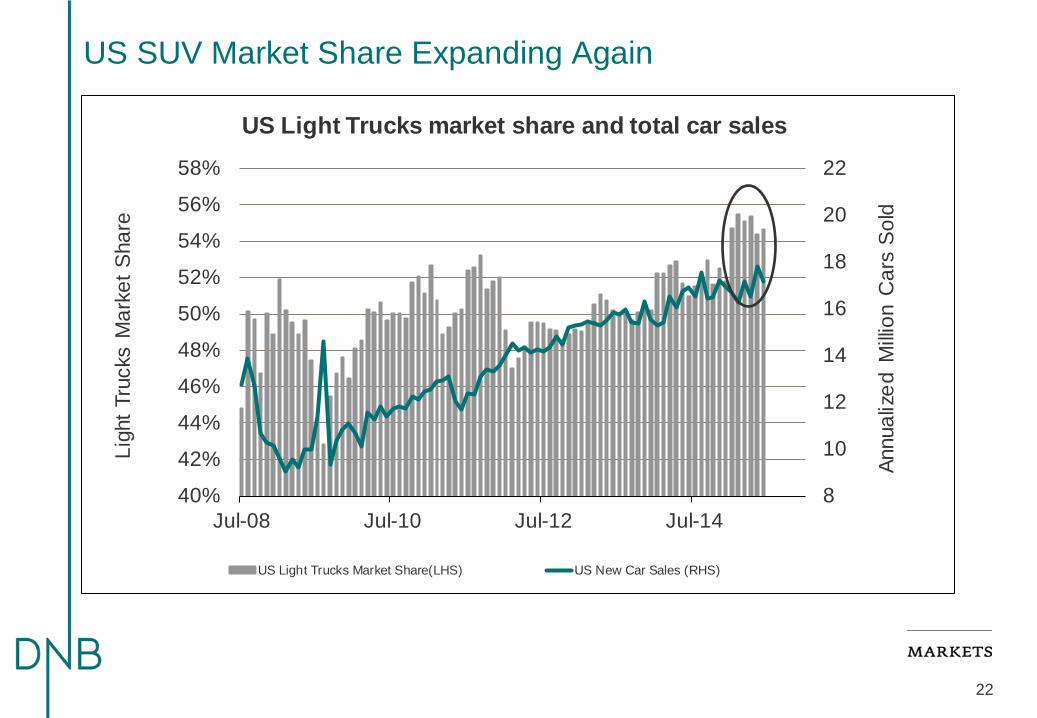

US Light Trucks market share and total car sales

US Light Trucks Market Share(LHS) US New Car Sales (RHS)

US SUV Market Share Expanding Again

23

How to Explain Chinese Gasoline Demand - With Chinese SUV sales up 58% in 2015 it is maybe not that strange that gasoline demand is performing strongly

0

100

200

300

400

500

600

700

Jan-05 Jan-08 Jan-11 Jan-14

Thou

sand

s of

SU

Vs s

old

per m

onth

Chinese SUV sales

Source: ThompsonReuters Datastream

The 2016 Oil Price Score Card

24

2016 Oil Price Scorecard Comments Oil Price Weight

Overall Outlook

The market still looks over supplied in 2016 but the call on OPEC is increasing by 1.6 million b/d according to IEA. The upside is capped by falling production costs, large US spare capacity in the form of available oil rigs/drilled uncompleted wells and OPECs market share strategy. But OPEC spare capacity is very low and non-OPEC supply growth will fade soon while geopolitical risk is high and rising.

Average price

55 $/b

Fundamentals

Global Fundamental BalanceThe global supply-demand balance is still looking over supplied for 2016, but much less over supplied than in 2015 as the call on OPEC is increasing by 1.6 million b/d in the latest IEA forecast. The problem is however that OPEC looks to produce more than the call.

BEARISH HIGH

Crude vs Product Balance (Margins)Refinery margins will probably be weaker in 2016 than in 2015 as particularly the Middle East is bringing on new capacity and as oil demand growth will be weaker in 2016 than in 2015. For the first and last quarter of 2016 the weak diesel market may lead to refinery run cuts, but we believe margins will be strong during the gasoline season.

BEARISH LOW

OECD Stock levels Stock levels are record high, but we do not believe the market will run out of storage capacity BEARISH MEDIUM

OPEC Spare CapacityCore OPEC spare capacity is low at only 2.3% of global oil demand according to IEA data. In reality the spare capacity is probably even lower since Saudi is probably producing close to capacity.

BULLISH HIGH

US Oil Statistics - Fundamentals US oil production growth which was 1.6 million b/d in 2014 and about 0.8 million b/d in 2015 is forecast to drop to negative in 2016 and US crude stocks will draw down in 2016. BULLISH HIGH

Global Demand GrowthGlobal oil demand growth is positively affected by the lower prices in 2015 but this effect is seen to fade in 2016. We have factored in weaker global demand growth for 2016, but the higher starting point of OECD oil demand next year means year on year growth will still be decent for OECD also in 2016.

NEUTRAL MEDIUM

OPEC SupplyOPEC (Saudi) is seen to contiunue its policy of targeting market share instead of price. And we estimate that Iran will increase its output from the current 2.9 million b/d to about 3.6 million b/d by the summer, starting the ramp up in Q1-2016.

BEARISH HIGH

Non-OPEC Supply Total non-OPEC supply growth is seen negative in 2016, down from a record growth of 2.2 million b/d in 2014 and 1.2 million b/d in 2015. BULLISH MEDIUM

Political Risk

Venezuela, Iraq, Iran, Saudi, Nigeria, Russia, Israel, MENA, Brazil, etc

Political risk is on the rise. Key risk is from countries like Venezuela, Iraq, Libya, Brazil. The Iran deal will probably bring meaningfully more OPEC barrels to the market, but generally the sunni-shiite conflict and IS has increased the total risk in the Middle East and weak economic conditions in countries like Venezuela and Brazil is threatening the social stability. There is a non-negligible risk related to conflict/power struggle inside the Saudi Royal family and the escalating tension between Iran and Saudi Arabia after Saudi executed an important Shia cleric.

BULLISH HIGH

Other Factors

Financial Money Flow

Total financial net oil length is significantly down since the peak. There is hence room room for a rebuild of positions if the sentiment should change. Triggers could be geopolitics, a strong gasoline season, accellerating decline rates, write downs of resources from shale oil companies, etc. A stronger USD has provided headwinds for the oil price since 2014, but this effect is probaly fading for 2016 as we do not believe in a further strengthening of the USD for the coming year.

BULLISH LOW

25

Long Term Oil Price Forecast – Current (The forecast is for the average of the rolling 1st month ICE Brent future contract)

Historical HistoricalNominal $/b Real (2015) $/b

2001 24.4 32.72002 25.0 32.92003 28.8 37.12004 38.3 48.02005 54.5 66.12006 65.1 76.52007 72.4 82.72008 97.3 106.92009 61.7 68.12010 79.5 86.32011 111.3 117.12012 111.7 115.12013 108.7 110.42014 99.5 101.52015 53.6 53.6

Price target ForecastNominal $/b Real (2015) $/b

3 months 456 months 55

12 months 6524 months 702019-2023 60-80

0

20

40

60

80

100

120

140

1996 1999 2002 2005 2008 2011 2014 2017 2020

$/b

Spot Brent History & FWD looking

New normalized price range in 2015 USD FWD (nominal)

Forecast nominal HistoricalSource: Reuters, DNB Markets

100-120 range gone (forever?)

26

“The time to repair the roof is when the sun is shining”

John F. Kennedy, SotU 1962

27

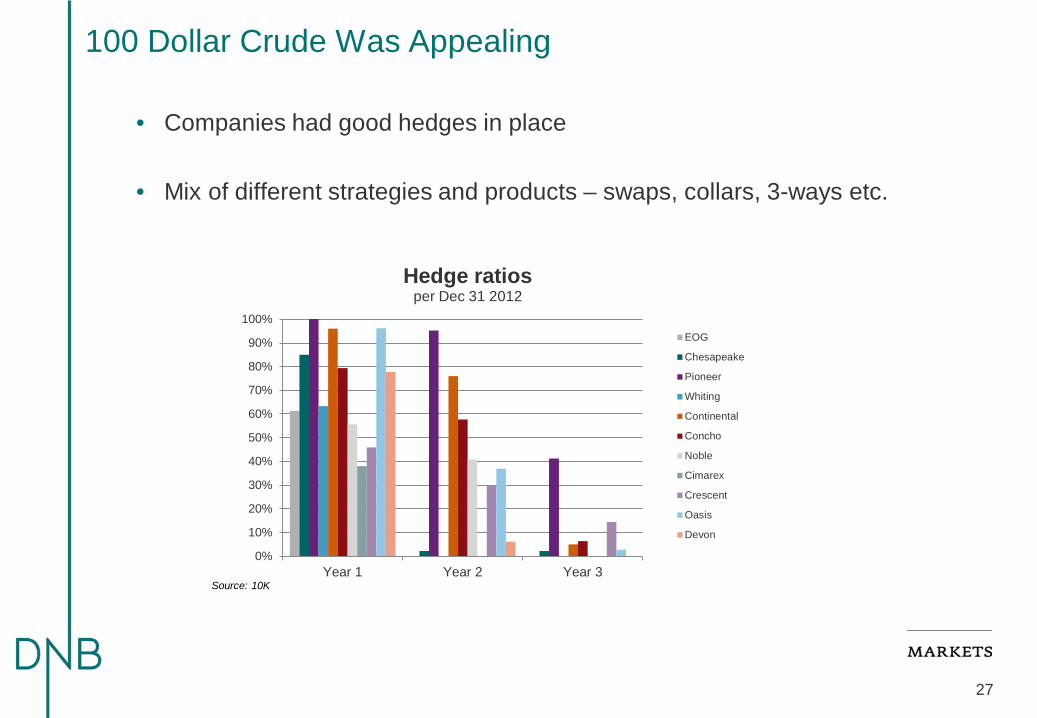

100 Dollar Crude Was Appealing

• Companies had good hedges in place

• Mix of different strategies and products – swaps, collars, 3-ways etc.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Year 1 Year 2 Year 3

Hedge ratios per Dec 31 2012

EOG

Chesapeake

Pioneer

Whiting

Continental

Concho

Noble

Cimarex

Crescent

Oasis

Devon

Source: 10K

28

Hedge Ratios Dropped With Falling Prices

0%

10%

20%

30%

40%

50%

60%

70%

80%

Year 1 Year 2 Year 3

Hedge ratio 2013 2014 2015 2016

Source: 10K (EOG, CHK, PXD, WLL, CLR, CXO, NBL, XEC, CPG, OAS, DVN)

• Those same companies sharply reduced their hedged volume

• Hedge ratios lowest when hedges were needed the most?

29

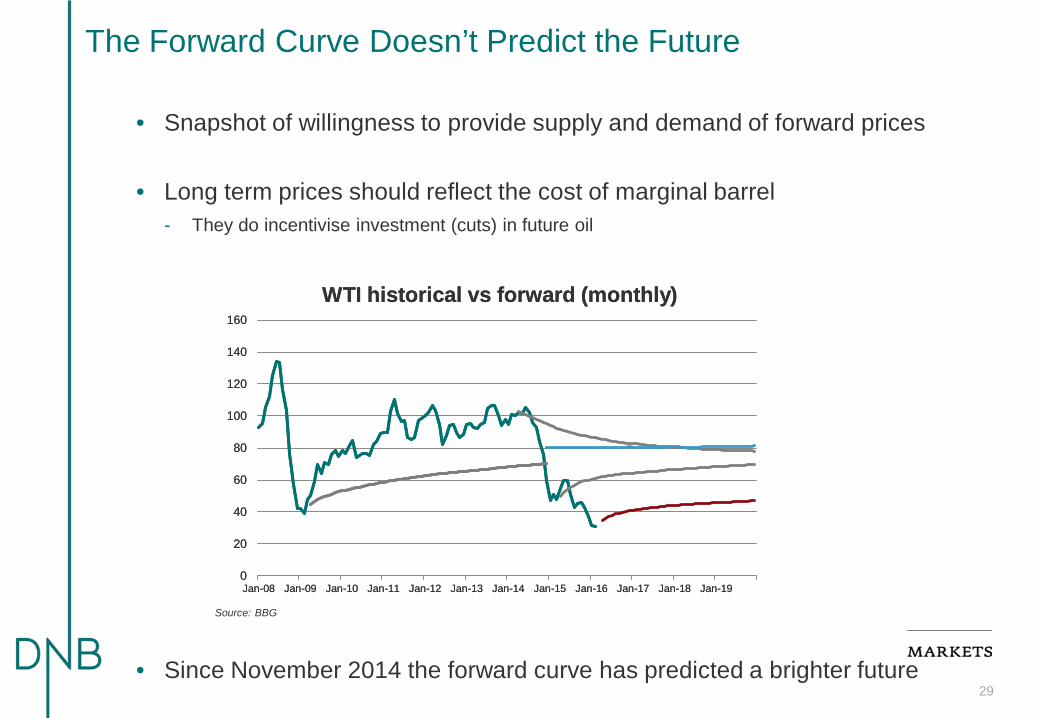

• Snapshot of willingness to provide supply and demand of forward prices

• Long term prices should reflect the cost of marginal barrel - They do incentivise investment (cuts) in future oil

• Since November 2014 the forward curve has predicted a brighter future

The Forward Curve Doesn’t Predict the Future

0

20

40

60

80

100

120

140

160

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

WTI historical vs forward (monthly)

0

20

40

60

80

100

120

140

160

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

WTI historical vs forward (monthly)

0

20

40

60

80

100

120

140

160

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

WTI historical vs forward (monthly)

0

20

40

60

80

100

120

140

160

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

WTI historical vs forward (monthly)

Source: BBG

30

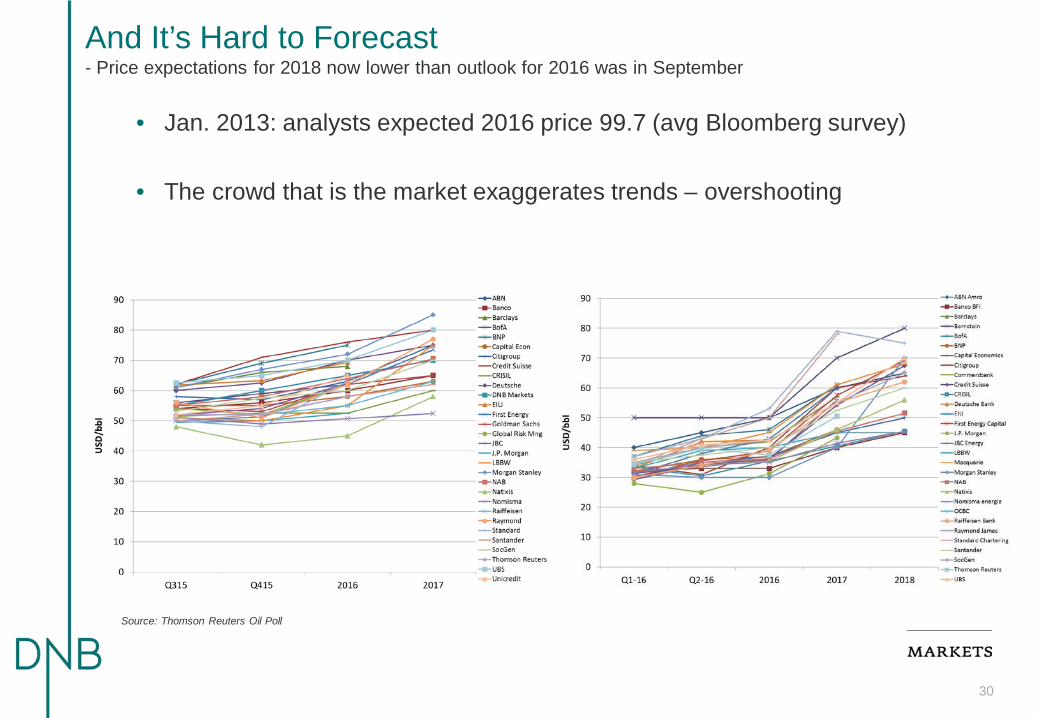

And It’s Hard to Forecast - Price expectations for 2018 now lower than outlook for 2016 was in September

Source: Thomson Reuters Oil Poll

• Jan. 2013: analysts expected 2016 price 99.7 (avg Bloomberg survey)

• The crowd that is the market exaggerates trends – overshooting

31

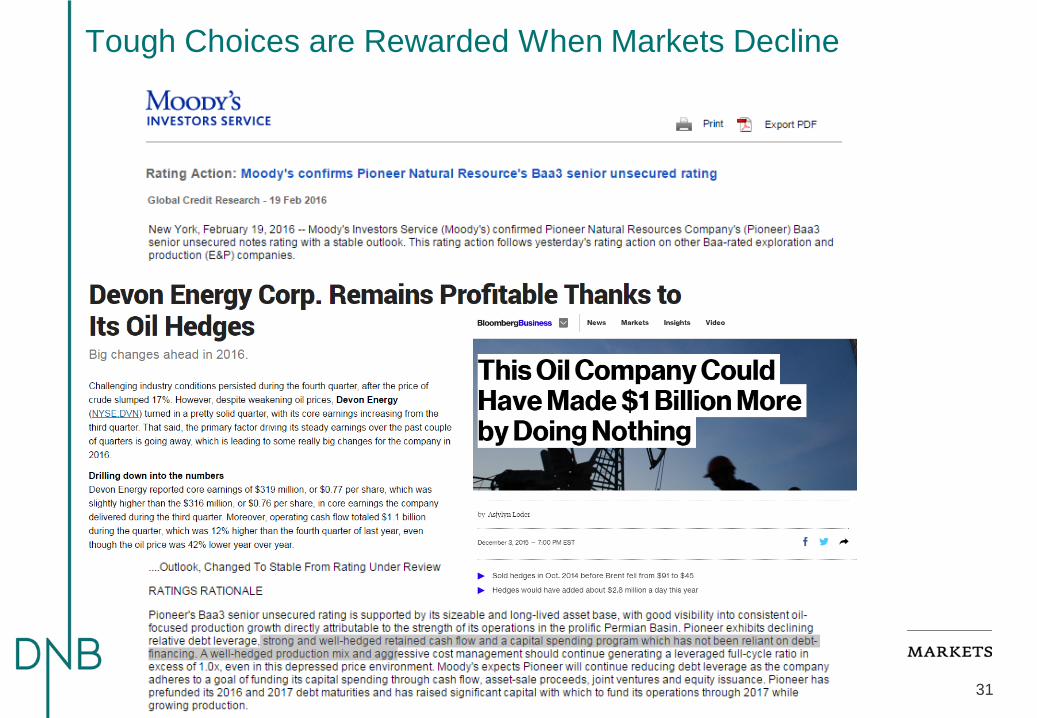

Tough Choices are Rewarded When Markets Decline

32

Opportunistic vs Apocalyptic Hedging

• Should not be about picking the tops and bottoms

• Markets are not rational, cash flow must be protected

• Consider risks of hedge losses in high price scenarios vs risk of bankruptcy in a weak market

• Cost of hedging rises considerably when it’s most crucial - 40 put for 2018 is 5.5 USD/bbl now - 40 put for 2016 was 10 cents/bbl two years ago

• Firm strategy – flexible execution

Normal hedge ratio

60 %40 %25 %15 %37-48 months

Hedging ratios50-70%30-50%0-40%0-30%

Time0-12 months

13-24 months25-36 months

33

• Trends typically overshoot in commodities – prepare to outlast them

• Hedges aren’t supposed to always be profitable

• Maintain financial flexibility through smoothing out revenue - Maintain capacity when times are tough - Avoid firesales - More time to adjust strategy, reorganise, negotiate with creditors - Solid hedging policy can reduce finance costs and increase debt capacity - Stability in financial ratios, rating and financing costs

Summary