Embed Size (px)

Citation preview

GLOBAL OUTLOOK

December 2017

ECONOMIC WATCH

Global Economic Watch | December 2017

The sustainability of the global growth is more evident

Official GDP growth figures are revised upwards in 3Q17 to 1.02% QoQ from 0.93% QoQ,

which implies slightly higher figures for 4Q17 than a month ago (BBVA-GAIN: 1.04% QoQ).

Strong confidence indicators, but hard data still fail to catch up. Further gains in manufacturing

surveys and steady service confidence up to November, but industrial output and retail sales

improved only slightly in October. Global trade recovery continues, but at a slower pace.

Solid economic momentum growth in developed markets (DM):

US: improving confidence and solid labour market support growth momentum in Q4. Upside

short-term bias from tax reform.

EZ: increasing global demand adds to strengthening domestic factors and reduced political

uncertainty, suggesting that strong momentum will be maintained in coming months.

Mixed signals from emerging markets (DM):

China: Growth moderation continues due to the authorities’ policy initiatives.

Latam: Activity recovery underway, supported by increasing demand, higher confidence and

better external environment.

Global headline inflation accelerated mildly in November driven by volatile components while

core pressures remained broadly unchanged and subdued.

2

Global Economic Watch | December 2017

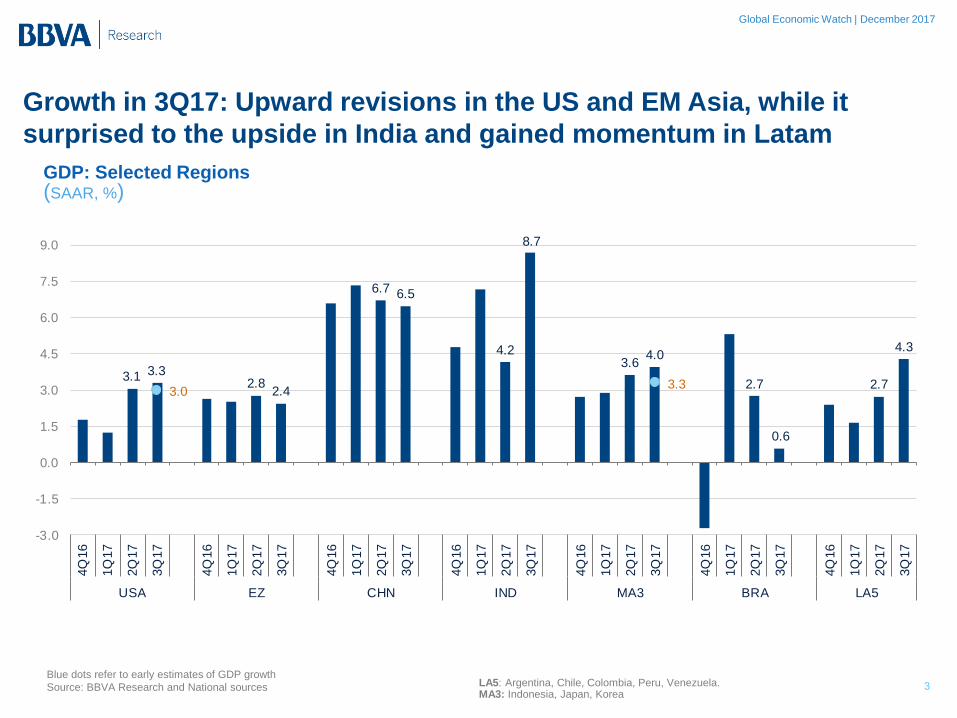

GDP: Selected Regions (SAAR, %)

Blue dots refer to early estimates of GDP growth

Source: BBVA Research and National sources

3

3.1 3.32.8

2.4

6.7 6.5

4.2

8.7

3.64.0

2.7

0.6

2.7

4.3

3.03.3

-3.0

-1.5

0.0

1.5

3.0

4.5

6.0

7.5

9.0

4Q

16

1Q

17

2Q

17

3Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

16

1Q

17

2Q

17

3Q

17

USA EZ CHN IND MA3 BRA LA5

Growth in 3Q17: Upward revisions in the US and EM Asia, while it

surprised to the upside in India and gained momentum in Latam

LA5: Argentina, Chile, Colombia, Peru, Venezuela. MA3: Indonesia, Japan, Korea

Global Economic Watch | December 2017

Global GDP growth momentum to continue in the Q4 (around 1% QoQ)

World GDP Growth

Forecast based on BBVA-GAIN (%, QoQ) World GDP Growth: Change in forecast

QoQ, %

Source: BBVA Research and CPB 4

* Forecast and nowcast based on BBVA-GAIN

0.4

0.6

0.8

1.0

1.2

Dec-1

2

Jun-1

3

Dec-1

3

Jun-1

4

Dec-1

4

Jun-1

5

Dec-1

5

Jun-1

6

Dec-1

6

Jun-1

7

Dec-1

7

CI 20% CI 40% CI 60%

Point Estimates Period average

0.80

0.981.04 1.02

0.931.04

0.96

Off

icia

l da

ta

Last

mon

th

Cu

rre

nt

Est.

Last

mon

th

4Q16 1Q17 2Q17 3Q17 4Q17

Nowcast

Global Economic Watch | December 2017

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

WLD DM EM

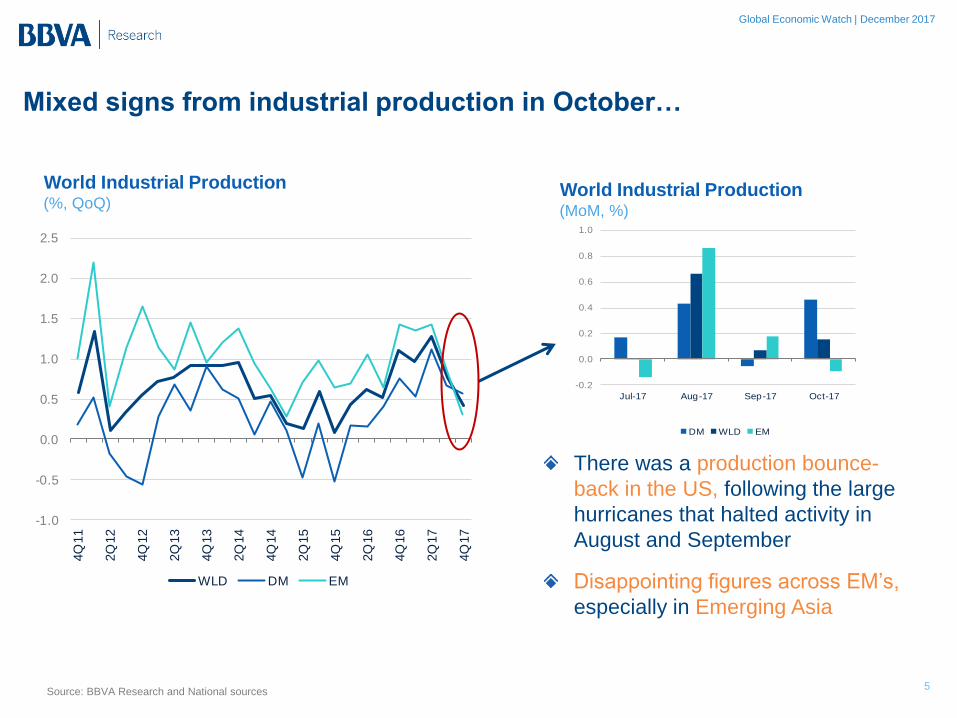

Mixed signs from industrial production in October…

World Industrial Production

(%, QoQ) World Industrial Production (MoM, %)

Source: BBVA Research and National sources 5

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Jul-17 Aug-17 Sep-17 Oct-17

DM WLD EM

There was a production bounce-

back in the US, following the large

hurricanes that halted activity in

August and September

Disappointing figures across EM’s,

especially in Emerging Asia

Global Economic Watch | December 2017

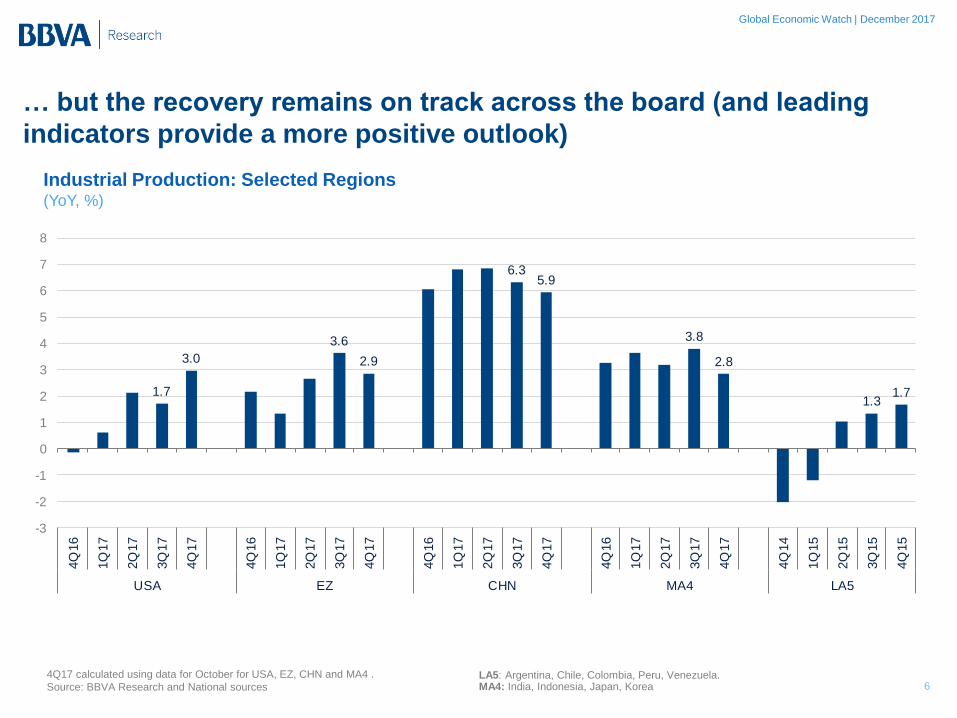

… but the recovery remains on track across the board (and leading

indicators provide a more positive outlook)

Industrial Production: Selected Regions (YoY, %)

6 4Q17 calculated using data for October for USA, EZ, CHN and MA4 .

Source: BBVA Research and National sources LA5: Argentina, Chile, Colombia, Peru, Venezuela. MA4: India, Indonesia, Japan, Korea

1.7

3.0

3.6

2.9

6.35.9

3.8

2.8

1.31.7

-3

-2

-1

0

1

2

3

4

5

6

7

8

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

USA EZ CHN MA4 LA5

Global Economic Watch | December 2017

48

49

50

51

52

53

54

55

56

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

DM WLD EM

Global manufacturing confidence improved again in November

suggesting strong activity in the coming months

World Manufacturing PMI

(Level ± 50)

World Manufacturing PMI (Level ± 50)

Source: BBVA Research and Markit 7

According to PMI’s, strong demand

continued to test capacity, leading

firms to reach the highest staffing

levels registered by the survey

Meanwhile, the rates of inflation in

input costs and output charges

edged higher (especially in

developed economies)

49

50

51

52

53

54

55

56

57

Aug-17 Sep-17 Oct-17 Nov-17

DM WLD EM

Global Economic Watch | December 2017

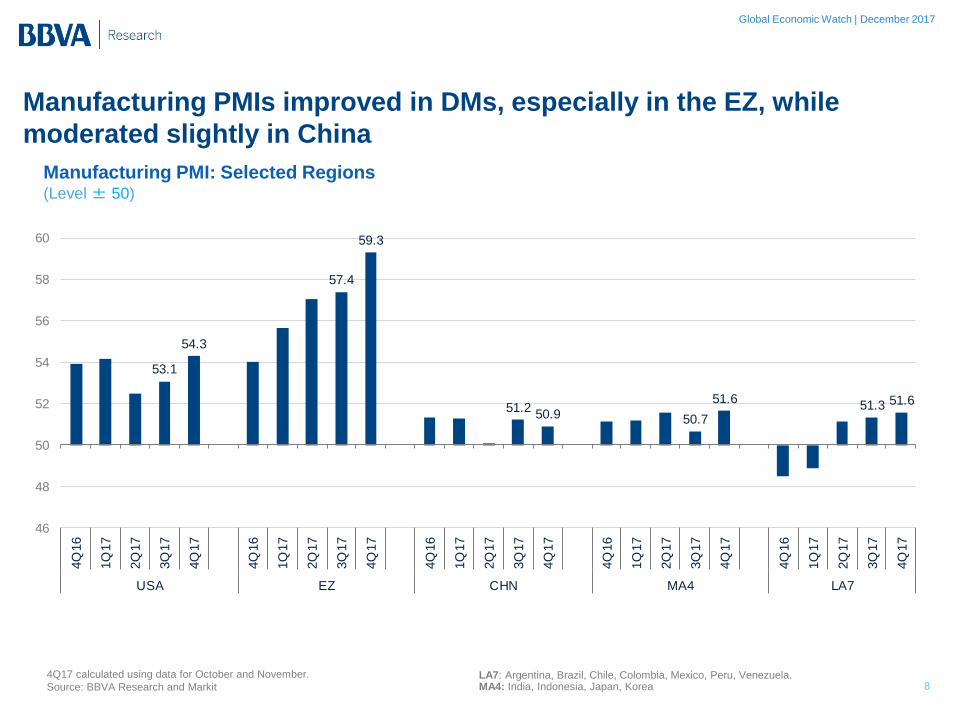

Manufacturing PMIs improved in DMs, especially in the EZ, while

moderated slightly in China

Manufacturing PMI: Selected Regions (Level ± 50)

8 LA7: Argentina, Brazil, Chile, Colombia, Mexico, Peru, Venezuela. MA4: India, Indonesia, Japan, Korea

4Q17 calculated using data for October and November.

Source: BBVA Research and Markit

53.1

54.3

57.4

59.3

51.250.9 50.7

51.651.3 51.6

46

48

50

52

54

56

58

60

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

USA EZ CHN MA4 LA7

Global Economic Watch | December 2017

Global services PMIs fell mildly in November, but consolidated the

gains over the quarter…

World Services PMI

(Level ± 50)

World Services PMI (Level ± 50)

Source: BBVA Research and Markit 9

November services confidence

continue to show an expansion at a

solid and stable pace underpinned

by rising new orders

Price pressures also intensified

during November as input costs

and output charges rates

accelerated

49

50

51

52

53

54

55

56

Aug-17 Sep-17 Oct-17 Nov-17

DM WLD EM

48

49

50

51

52

53

54

55

56

57

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

DM WLD EM

Global Economic Watch | December 2017

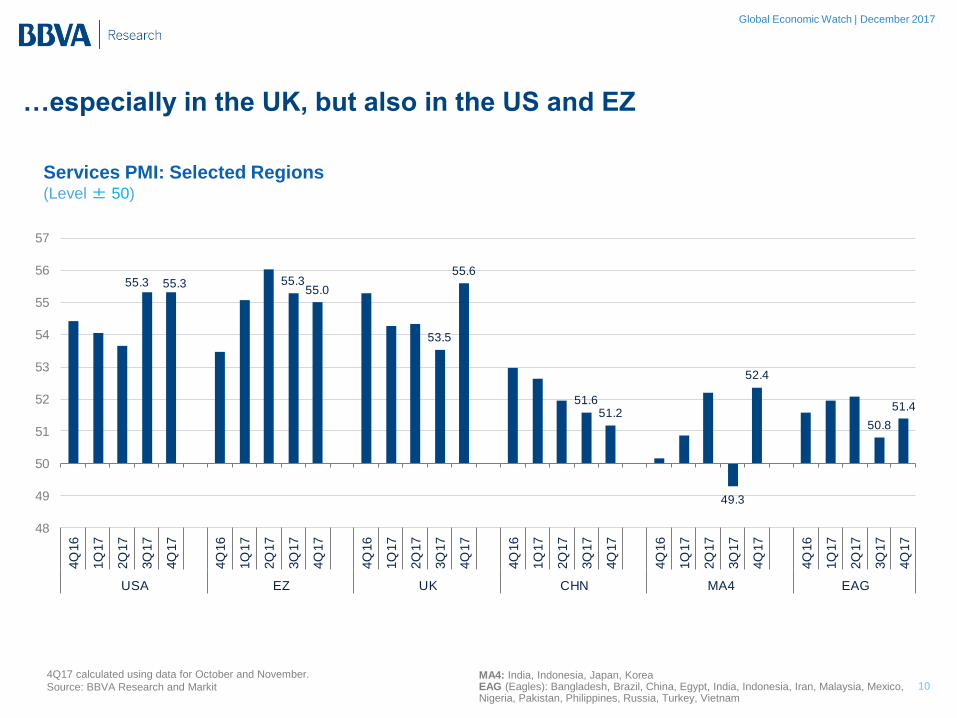

…especially in the UK, but also in the US and EZ

Services PMI: Selected Regions (Level ± 50)

10 MA4: India, Indonesia, Japan, Korea EAG (Eagles): Bangladesh, Brazil, China, Egypt, India, Indonesia, Iran, Malaysia, Mexico, Nigeria, Pakistan, Philippines, Russia, Turkey, Vietnam

4Q17 calculated using data for October and November.

Source: BBVA Research and Markit

55.3 55.3 55.355.0

53.5

55.6

51.651.2

49.3

52.4

50.8

51.4

48

49

50

51

52

53

54

55

56

57

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

USA EZ UK CHN MA4 EAG

Global Economic Watch | December 2017

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

DM WLD EM

DM: Avg 2000-16

EM: Avg 2000-16

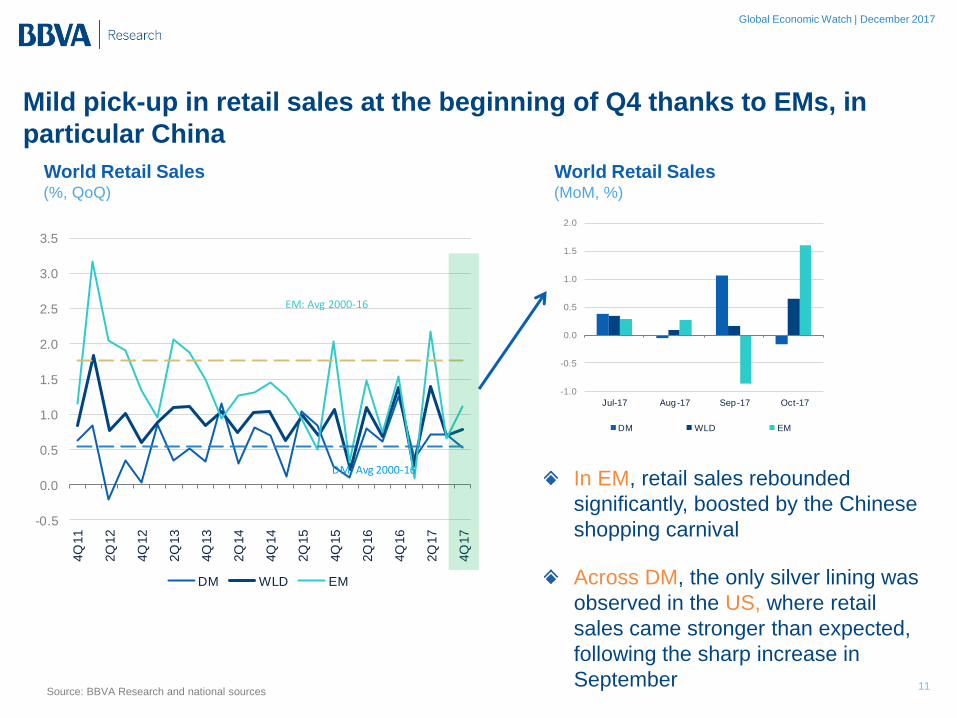

Mild pick-up in retail sales at the beginning of Q4 thanks to EMs, in

particular China

World Retail Sales

(%, QoQ)

World Retail Sales (MoM, %)

Source: BBVA Research and national sources 11

In EM, retail sales rebounded

significantly, boosted by the Chinese

shopping carnival

Across DM, the only silver lining was

observed in the US, where retail

sales came stronger than expected,

following the sharp increase in

September

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Jul-17 Aug-17 Sep-17 Oct-17

DM WLD EM

Global Economic Watch | December 2017

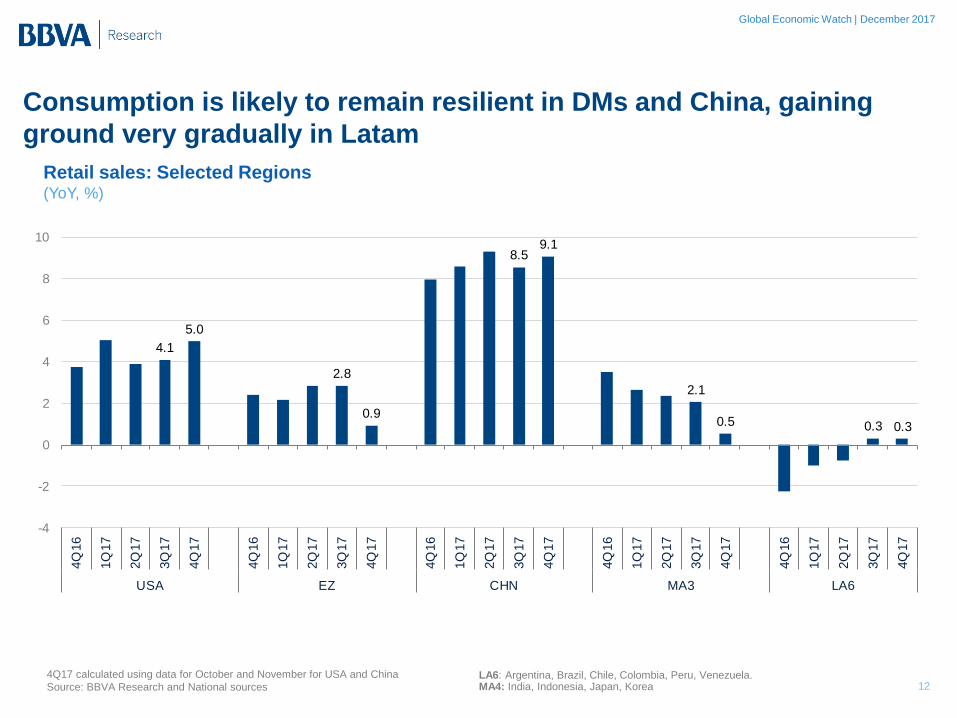

Consumption is likely to remain resilient in DMs and China, gaining

ground very gradually in Latam

Retail sales: Selected Regions (YoY, %)

12 4Q17 calculated using data for October and November for USA and China

Source: BBVA Research and National sources LA6: Argentina, Brazil, Chile, Colombia, Peru, Venezuela. MA4: India, Indonesia, Japan, Korea

4.1

5.0

2.8

0.9

8.59.1

2.1

0.5 0.3 0.3

-4

-2

0

2

4

6

8

10

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

USA EZ CHN MA3 LA6

Global Economic Watch | December 2017

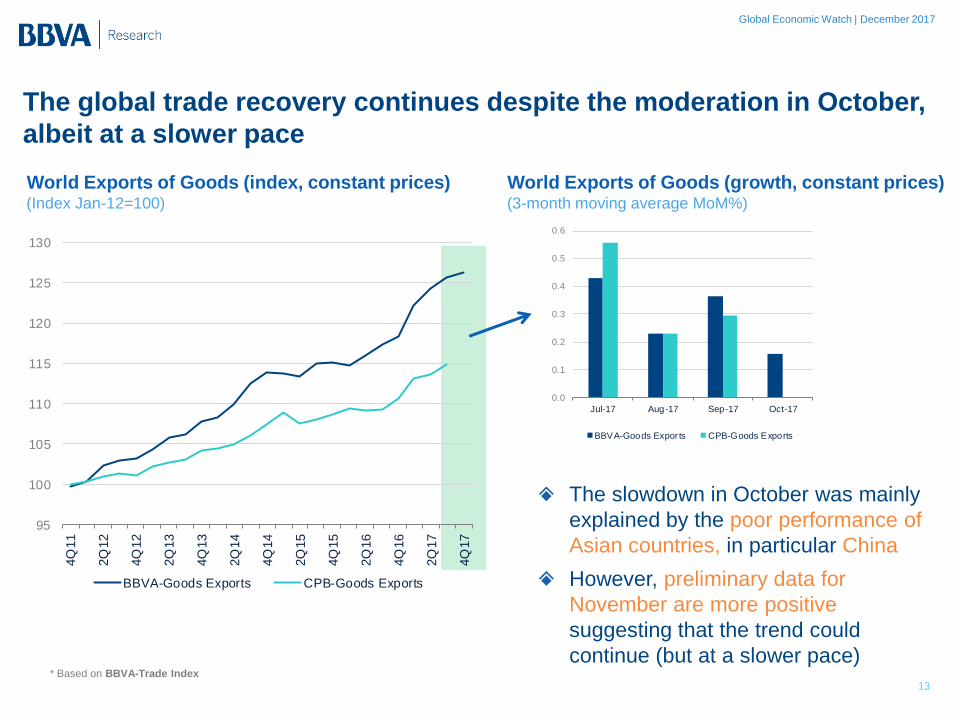

The global trade recovery continues despite the moderation in October,

albeit at a slower pace

World Exports of Goods (index, constant prices) (Index Jan-12=100)

13

* Based on BBVA-Trade Index

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Jul-17 Aug-17 Sep-17 Oct-17

BBVA-Goods Expor ts CPB-Goods Exports

The slowdown in October was mainly

explained by the poor performance of

Asian countries, in particular China

However, preliminary data for

November are more positive

suggesting that the trend could

continue (but at a slower pace)

World Exports of Goods (growth, constant prices) (3-month moving average MoM%)

95

100

105

110

115

120

125

130

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

BBVA-Goods Exports CPB-Goods Exports

Global Economic Watch | December 2017

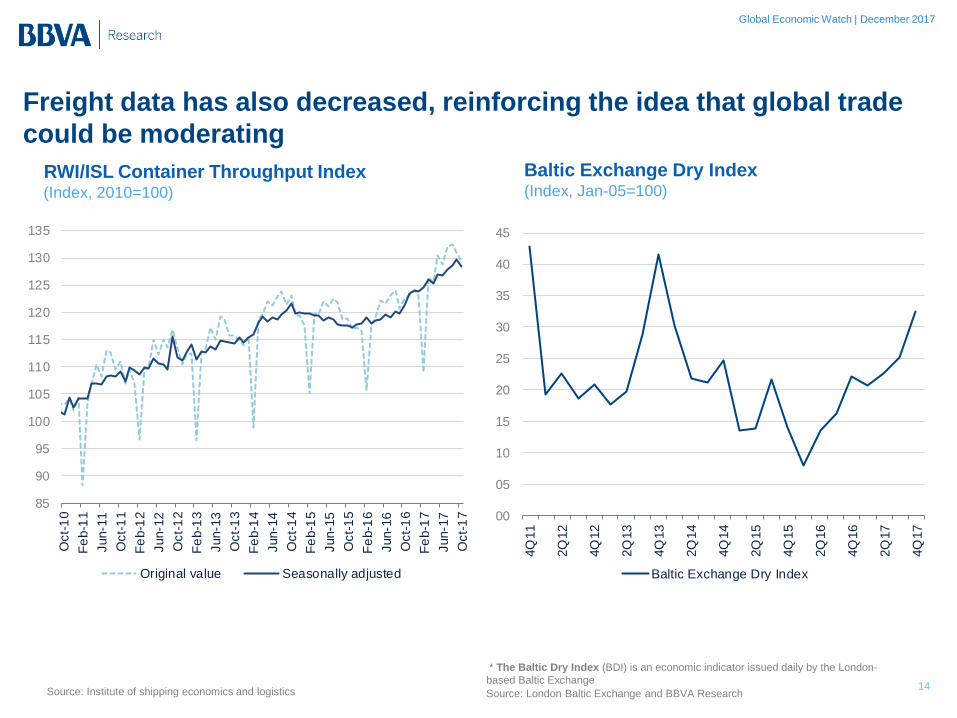

Freight data has also decreased, reinforcing the idea that global trade

could be moderating

RWI/ISL Container Throughput Index

(Index, 2010=100)

Baltic Exchange Dry Index (Index, Jan-05=100)

Source: Institute of shipping economics and logistics 14

* The Baltic Dry Index (BDI) is an economic indicator issued daily by the London-

based Baltic Exchange

Source: London Baltic Exchange and BBVA Research

85

90

95

100

105

110

115

120

125

130

135

Oct-

10

Fe

b-1

1

Jun-1

1

Oct-

11

Fe

b-1

2

Jun-1

2

Oct-

12

Fe

b-1

3

Jun-1

3

Oct-

13

Fe

b-1

4

Jun-1

4

Oct-

14

Fe

b-1

5

Jun-1

5

Oct-

15

Fe

b-1

6

Jun-1

6

Oct-

16

Fe

b-1

7

Jun-1

7

Oct-

17

Original value Seasonally adjusted

00

05

10

15

20

25

30

35

40

45

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

Baltic Exchange Dry Index

Global Economic Watch | December 2017

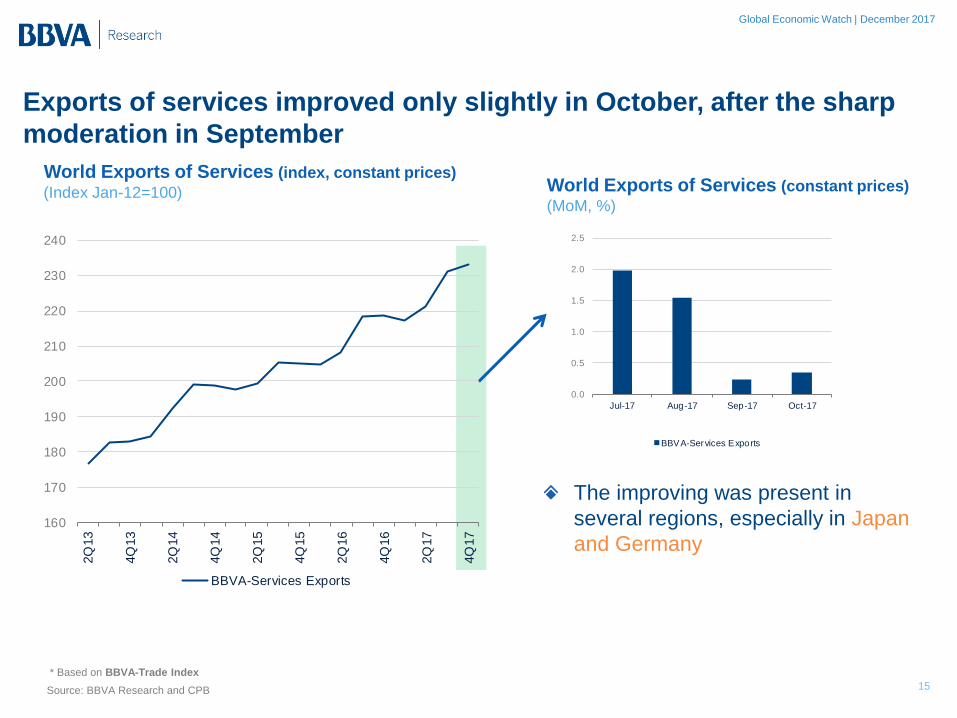

Exports of services improved only slightly in October, after the sharp

moderation in September

World Exports of Services (index, constant prices)

(Index Jan-12=100) World Exports of Services (constant prices) (MoM, %)

15

The improving was present in

several regions, especially in Japan

and Germany

Source: BBVA Research and CPB

* Based on BBVA-Trade Index

0.0

0.5

1.0

1.5

2.0

2.5

Jul-17 Aug-17 Sep-17 Oct-17

BBVA-Services Exports

160

170

180

190

200

210

220

230

240

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

BBVA-Services Exports

Global Economic Watch | December 2017

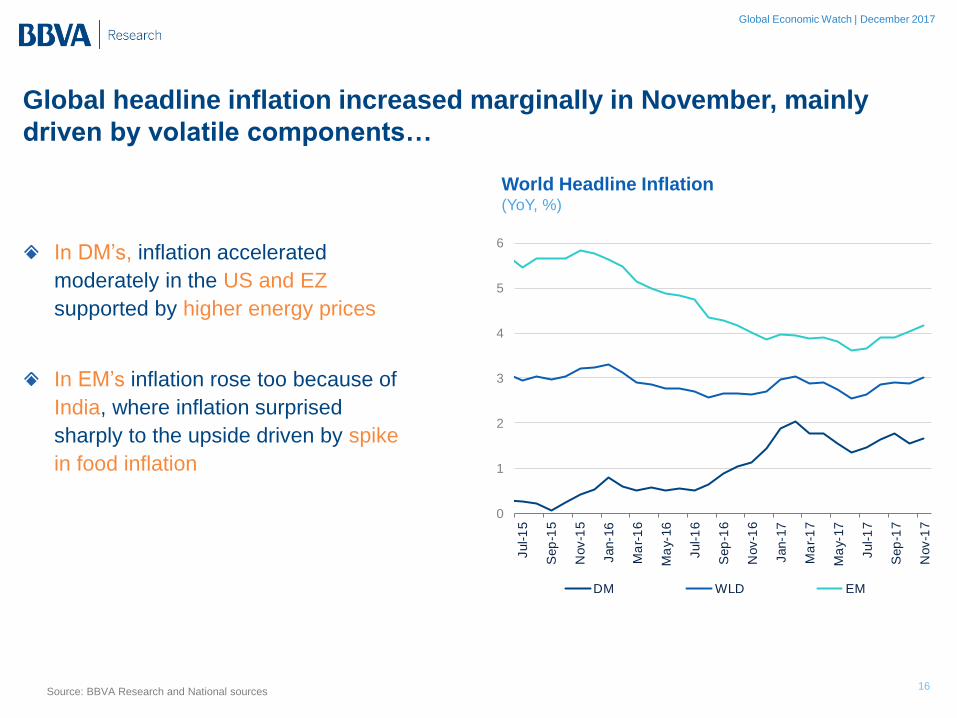

Global headline inflation increased marginally in November, mainly

driven by volatile components…

World Headline Inflation (YoY, %)

Source: BBVA Research and National sources 16

0

1

2

3

4

5

6

Jul-1

5

Sep

-15

Nov-1

5

Jan-1

6

Ma

r-1

6

Ma

y-16

Jul-1

6

Sep

-16

Nov-1

6

Jan-1

7

Ma

r-1

7

Ma

y-17

Jul-1

7

Sep

-17

Nov-1

7

DM WLD EM

In DM’s, inflation accelerated

moderately in the US and EZ

supported by higher energy prices

In EM’s inflation rose too because of

India, where inflation surprised

sharply to the upside driven by spike

in food inflation

Global Economic Watch | December 2017

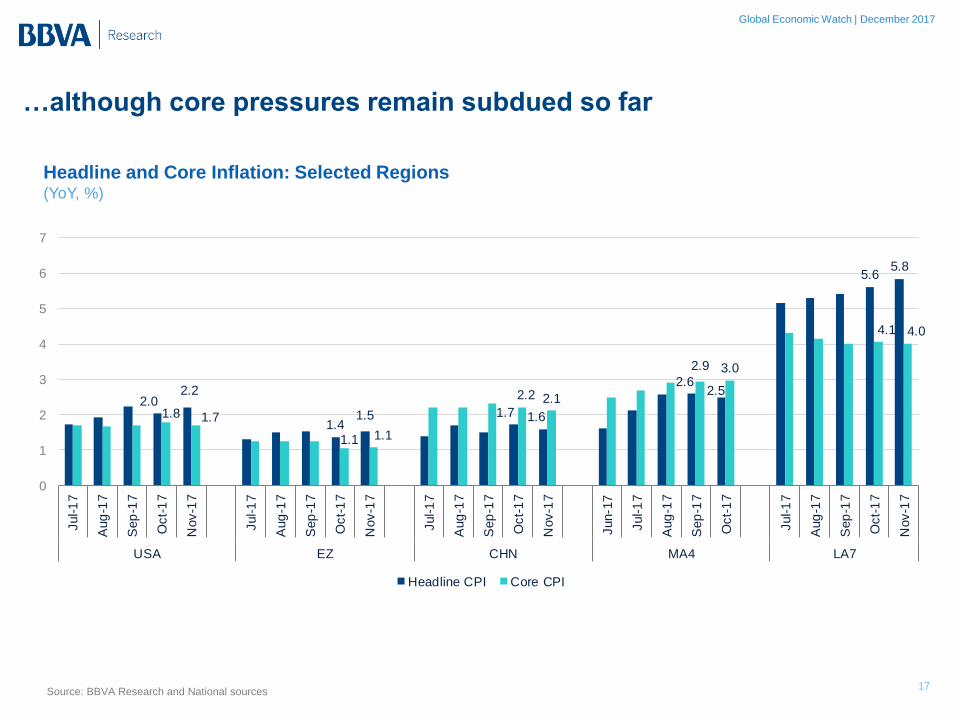

…although core pressures remain subdued so far

Headline and Core Inflation: Selected Regions (YoY, %)

Source: BBVA Research and National sources 17

2.02.2

1.41.5 1.7 1.6

2.62.5

5.65.8

1.8 1.7

1.1 1.1

2.2 2.1

2.9 3.0

4.1 4.0

0

1

2

3

4

5

6

7

Jul-1

7

Aug

-17

Sep

-17

Oct-

17

Nov-1

7

Jul-1

7

Aug

-17

Sep

-17

Oct-

17

Nov-1

7

Jul-1

7

Aug

-17

Sep

-17

Oct-

17

Nov-1

7

Jun-1

7

Jul-1

7

Aug

-17

Sep

-17

Oct-

17

Jul-1

7

Aug

-17

Sep

-17

Oct-

17

Nov-1

7

USA EZ CHN MA4 LA7

Headline CPI Core CPI

GLOBAL OUTLOOK

December 2017

ECONOMIC WATCH