Embed Size (px)

Citation preview

Global Potential for Prepaid Cards

Overview of Key Markets

© Edgar, Dunn & Company, 2013

Introduction to Edgar, Dunn & Company

© Edgar, Dunn & Company, 2013

3

Edgar, Dunn & Company

Edgar, Dunn & Company (EDC) is a director-owned management consulting company established in 1978

Recognised industry leaders in payments

Financial services focus with payments specialisation

Collaborative consulting approach

Today we serve clients in more than 30 countries on six continents from offices located in North America, Europe and Asia

San Francisco

Sydney

London

Atlanta

Frankfurt

Singapore

Paris

Global Thought Leaders in Payments

Mexico City

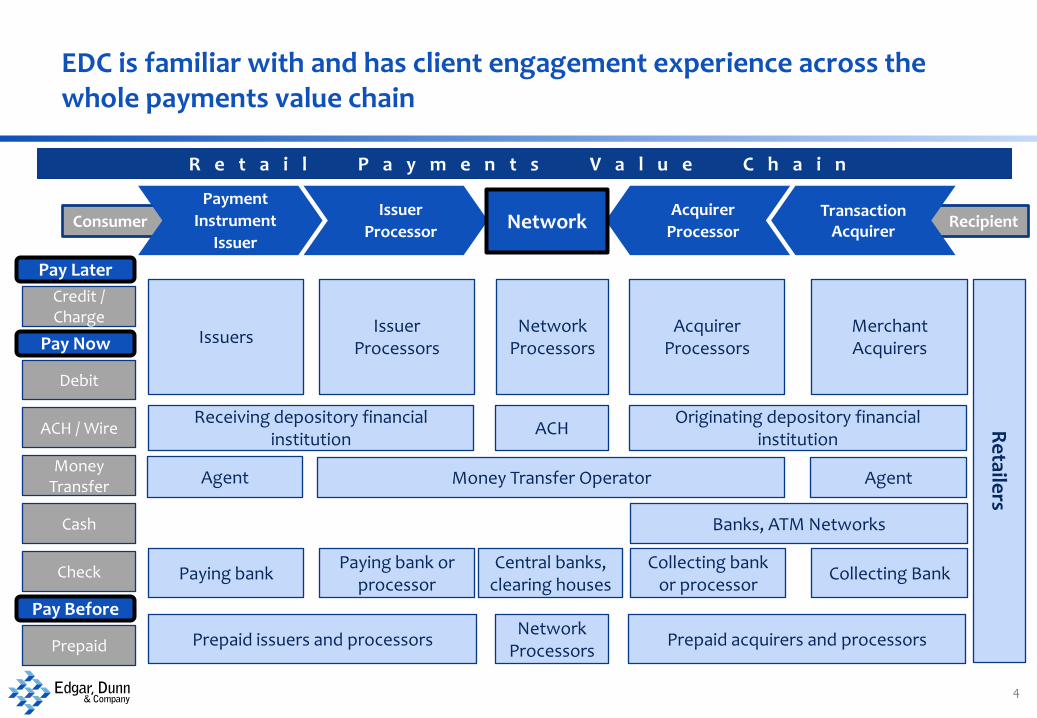

Recipient Consumer

4

Payment

Instrument

Issuer

Issuer

Processor

Acquirer

Processor Transaction

Acquirer

Debit

Credit / Charge

ACH / Wire

Money Transfer

Cash

Check

Prepaid

Pay Later

Pay Now

Pay Before

Acquirer Processors

Receiving depository financial institution

Originating depository financial institution

ACH

Agent Money Transfer Operator Agent

Banks, ATM Networks

Central banks, clearing houses

Collecting Bank Collecting bank

or processor Paying bank or

processor Paying bank

Prepaid issuers and processors

R e t a i l P a y m e n t s V a l u e C h a i n

Merchant Acquirers

Issuer Processors

Network Processors

Issuers

Prepaid acquirers and processors Network

Processors

EDC is familiar with and has client engagement experience across the whole payments value chain

Network

Re

tailers

EDC’s Advisory Services cover multiple functional areas and include conducting strategic analysis and providing critical business guidance to organisations throughout the payments value chain

5

Strategy

Financial Analysis & Profitability

Customer segmentation analysis

Portfolio profitability analysis

Loyalty program development

Cost studies

Pricing studies

Risk Management

Proposition Development

Operations

PAYMENTS

VALUE

CHAIN

Corporate and business unit strategy development

Enterprise-wide and product-specific programs

Merger and acquisition support

Competitive positioning & brand strategy

Channel strategy

Risk management strategies, including chip

Credit and fraud risk policies

Fraud prevention & detection

Benchmarking & best practices

Back-office process improvement

Third-party processor evaluation

Review of business processes

Outsourcing strategies

Portfolio migration and implementation

Regulatory and network compliance

Market entry strategies

New product strategies

Market opportunity assessment

Implementation planning and support

Introduction

$822 billion projected prepaid opportunity 20171

The global prepaid industry is fragmented between financial institutions, retailers and speciality companies

Two main drivers have supported the global growth of prepaid: Functionality to support unbanked and

underbanked segments

1. Youth

2. GPR

Functionality to support distribution of value 1. Gift

2. Government benefit

3. Corporate Prepaid (travel, procurement, etc.)

6 1BCG

Image: www.theguardian.com

7

Europe – UK, Italy, France, Germany

Middle East - UAE, Iran, Turkey

Latin America – Brazil, Mexico, Chile

North America – USA, Canada

Asia-Pacific – India, China, Australia

Africa – South Africa, Egypt, Kenya

Overview of Key Markets by Region

Europe

UK, Italy, France, Germany

© Edgar, Dunn & Company, 2013

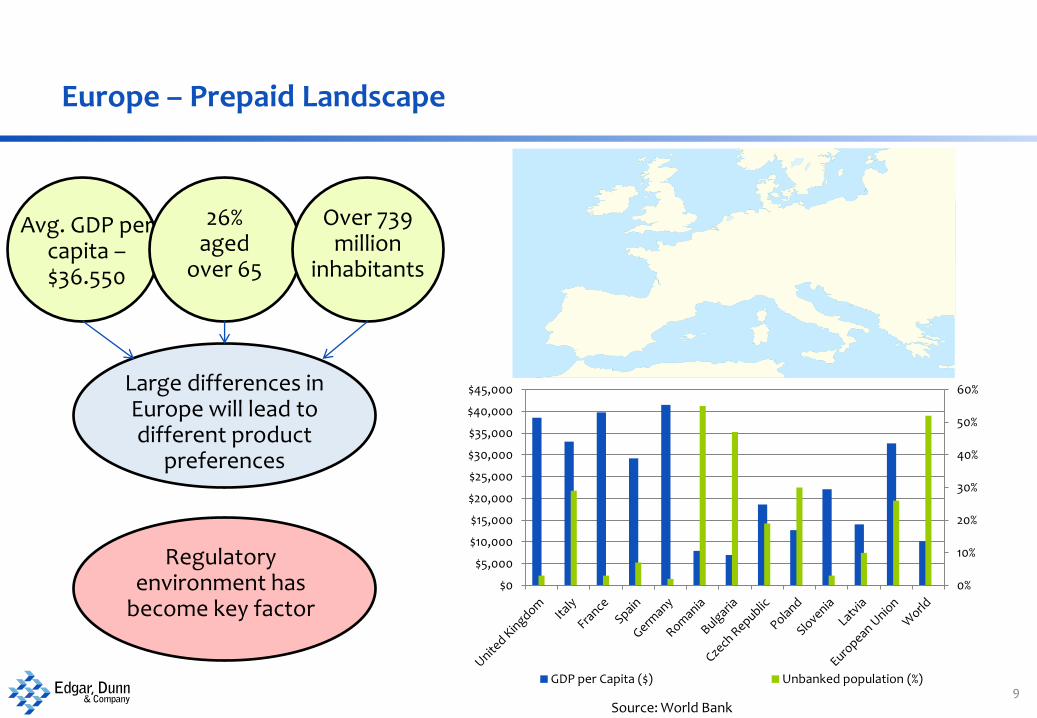

Europe – Prepaid Landscape

9

0

10,000

20,000

30,000

40,000

50,000

US $ GDP pr. Capita

Large differences in Europe will lead to different product

preferences

Regulatory environment has

become key factor

Avg. GDP per capita – $36.550

26% aged

over 65

Over 739 million

inhabitants

0%

10%

20%

30%

40%

50%

60%

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

GDP per Capita ($) Unbanked population (%)

Source: World Bank

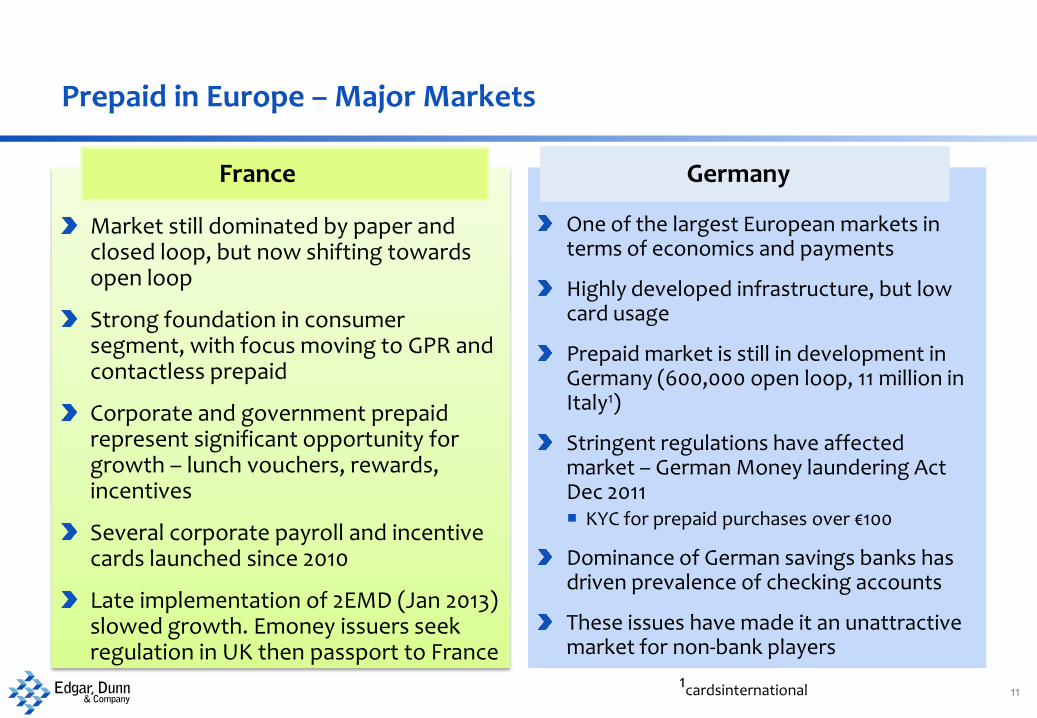

Prepaid Cards in Europe – Major Markets

10

One of the largest prepaid markets

15 million people do not have bank accounts (29%), largest absolute number in Europe1

Cost of basic banking is high and cultural factors see consumers with a high propensity to use cash

General purpose cards dominate the market

Main growth expected to be in payroll and corporate T & E

Dec 2011 law passed stipulating payments over €1,000 ($1,300) must be electronic, in attempt to reduce tax avoidance

Gift cards is the largest market worth an estimated £4.7billion2

In 2011 sales of gift cards and vouchers to corporations exceeded sales to consumers

Now more than 230 different prepaid cards available, up from 50 in 2007

Youth cards have become incorporated into general purpose (citizen card)

Prepaid cards generally need a niche to succeed in the UK Travel cards meet a need for UK travellers –

cards loaded with Euros don’t attract foreign currency transaction fees where debit and credit do

Italy

United Kingdom

1world bank

2UKGCVA

Prepaid in Europe – Major Markets

Market still dominated by paper and closed loop, but now shifting towards open loop

Strong foundation in consumer segment, with focus moving to GPR and contactless prepaid

Corporate and government prepaid represent significant opportunity for growth – lunch vouchers, rewards, incentives

Several corporate payroll and incentive cards launched since 2010

Late implementation of 2EMD (Jan 2013) slowed growth. Emoney issuers seek regulation in UK then passport to France

11

One of the largest European markets in terms of economics and payments

Highly developed infrastructure, but low card usage

Prepaid market is still in development in Germany (600,000 open loop, 11 million in Italy1)

Stringent regulations have affected market – German Money laundering Act Dec 2011 KYC for prepaid purchases over €100

Dominance of German savings banks has driven prevalence of checking accounts

These issues have made it an unattractive market for non-bank players

Germany

France

1cardsinternational

Prepaid Cards in Europe - Consumer

12

Youth Cards/GPR

European youth population – 55 million

Large potential market for retailers as there is an increase in spending power among youth.

Loyalty and brand recognition from early age

Convergence with mobile phones and loyalty

Gift Cards

62% and 72% of German and British consumers have bought a gift card1

Once customers have tried prepaid cards, they come back1

Reloadable opportunities

Transit

Transit cards expected to grow to $54 billion2

Prepaid transit cards can incorporate other functionalities3

T&E

Banks in well developed countries are active in issuing travel cards

UK and Germany are expected to account for 27% and 23% of the European travel market respectively by 20174

1Card World “German Consumers Warming to Prepaid”

2BCG

3Paybefore “Europe’s Changing Prepaid Landscape”

4VRL Financial news “The Prepaid Travel and Transit Opportunity

Prepaid Cards in Europe - Government

13

Post Offices

Poste Italiane

Poste Romania

Municipalities

Banks

National Healthcare

Social benefits receivers

Asylum Seekers

Prepaid not yet used for cash management

Typically prepaid cards are intended for specific purpose so closed or semi closed loop

Government to Government

Government payments are largely dominated by bank transactions – However, some prepaid initiatives appear to thrive

Programme Managers Card type Users

Typically issued in cooperation with

domestic banks or post offices

Both open and closed loop cards are issued by

governments

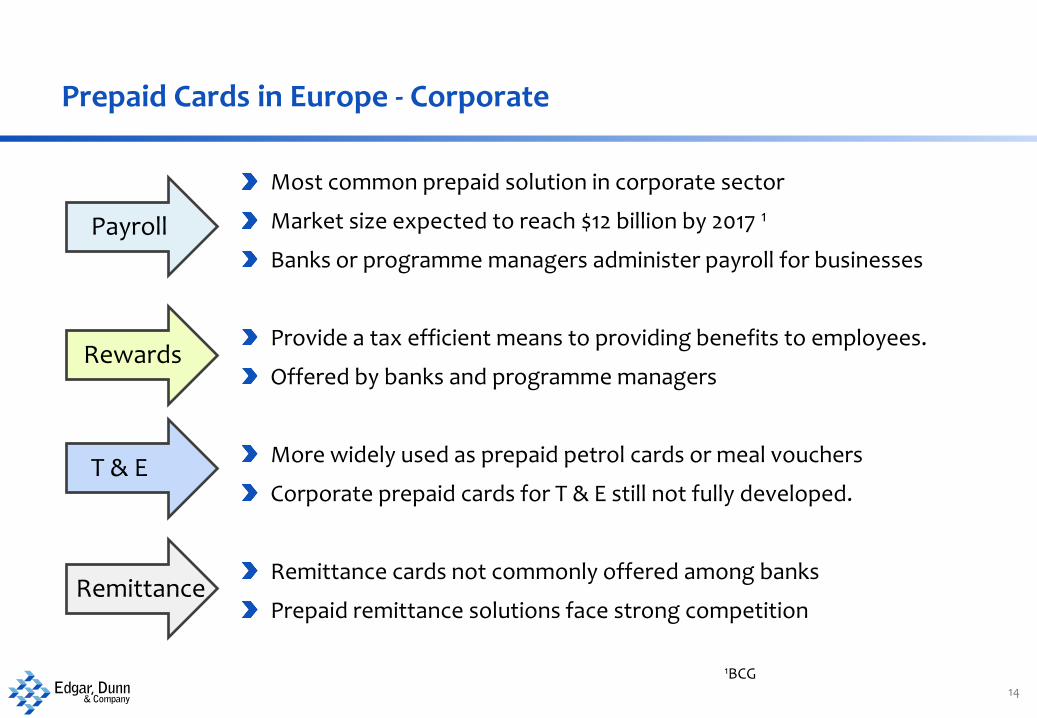

Prepaid Cards in Europe - Corporate

14

Most common prepaid solution in corporate sector

Market size expected to reach $12 billion by 2017 1

Banks or programme managers administer payroll for businesses

Provide a tax efficient means to providing benefits to employees.

Offered by banks and programme managers

More widely used as prepaid petrol cards or meal vouchers

Corporate prepaid cards for T & E still not fully developed.

Remittance cards not commonly offered among banks

Prepaid remittance solutions face strong competition

Payroll

Rewards

T & E

Remittance

1BCG

Regulation of Prepaid - Europe

15

Regulatory environment Impact on the prepaid market

Germany is one of largest markets in terms of economics and payments

Concerns about money laundering means customers have to be present at POS for KYC and due diligence checks

Payroll must be paid via a bank account making prepaid propositions superfluous

Italian legislation is helping propel toward prepaid, issuing a mandate that transactions over $1300 must be electronic

Well defined and open regulatory environment provides a potential competitive

Image: www.theguardian.com

Prepaid in Europe – Major Regulatory Changes Proposed

Standardisation of Payment Regulation across the EU and EEA

Amend and replace PSD I

Principal aims: Level the playing field for payment

providers

Increase consumer protection

Improving transaction security

Reduce ambiguity in PSD I

Achieve greater consistency across the EU in payment regulation

16

Regulated caps on cross-border 4 party scheme interchange rates

Extension to domestic interchange rates after 2 years

Removal of certain scheme rules Accept all cards rule

Definition of merchant location

Increased transparency about levels of interchange fees and acquiring fees

Interchange Regulation

PSD II

Adoption proposed by Spring 2014 – appears highly ambitious, as there are European Parliament due Summer 2014

“The subject matter of the proposals is technically complex and not always fully understood by those drafting the legislation” – Hogan Lovells, August 2013

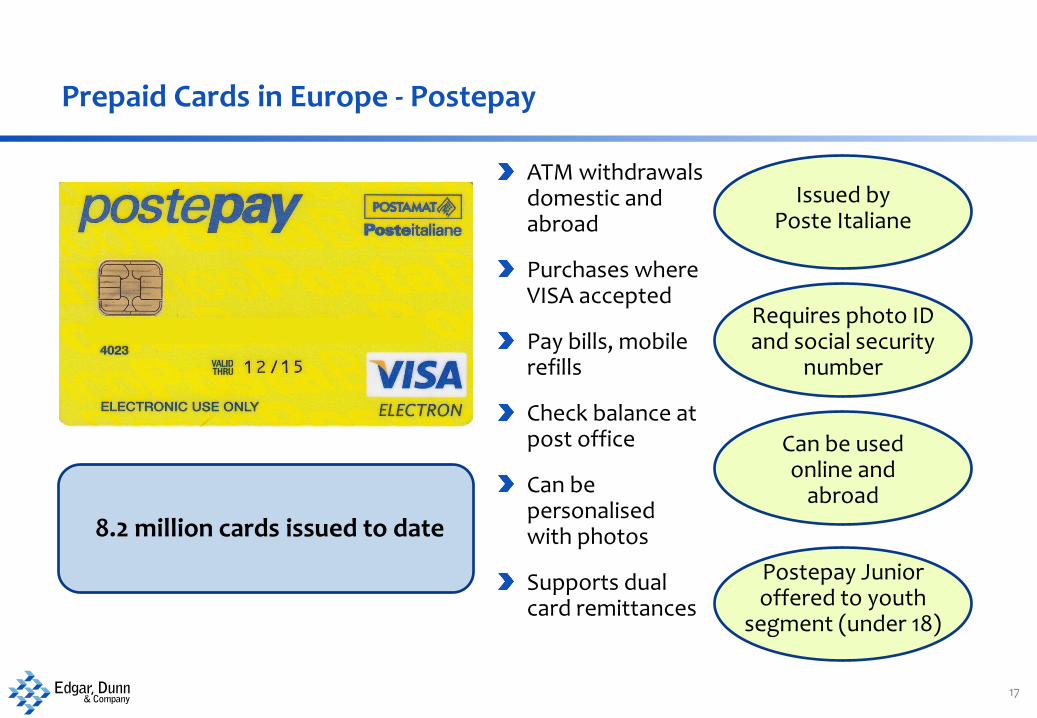

Prepaid Cards in Europe - Postepay

17

Issued by Poste Italiane

Requires photo ID and social security

number

Can be used online and

abroad

Postepay Junior offered to youth

segment (under 18)

8.2 million cards issued to date

ATM withdrawals domestic and abroad

Purchases where VISA accepted

Pay bills, mobile refills

Check balance at post office

Can be personalised with photos

Supports dual card remittances

Prepaid cards in Europe - CitizenCard

18

Acts as ID through the card’s PASS hologram (endorsed by the Home Office, Police and Trading Standards)

Cash loaded by bank transfer, at post office or PayPoint retailer

Can be used at VISA terminal online or the high street

P2P enabled

Open loop general purpose

for youth

Offers PASS proof of age

Can load between £10 and £5,000

Offers discounts at retailers and ‘refer and earn incentive’

Issued by Valitor

Middle East

UAE, Egypt and Turkey

© Edgar, Dunn & Company, 2013

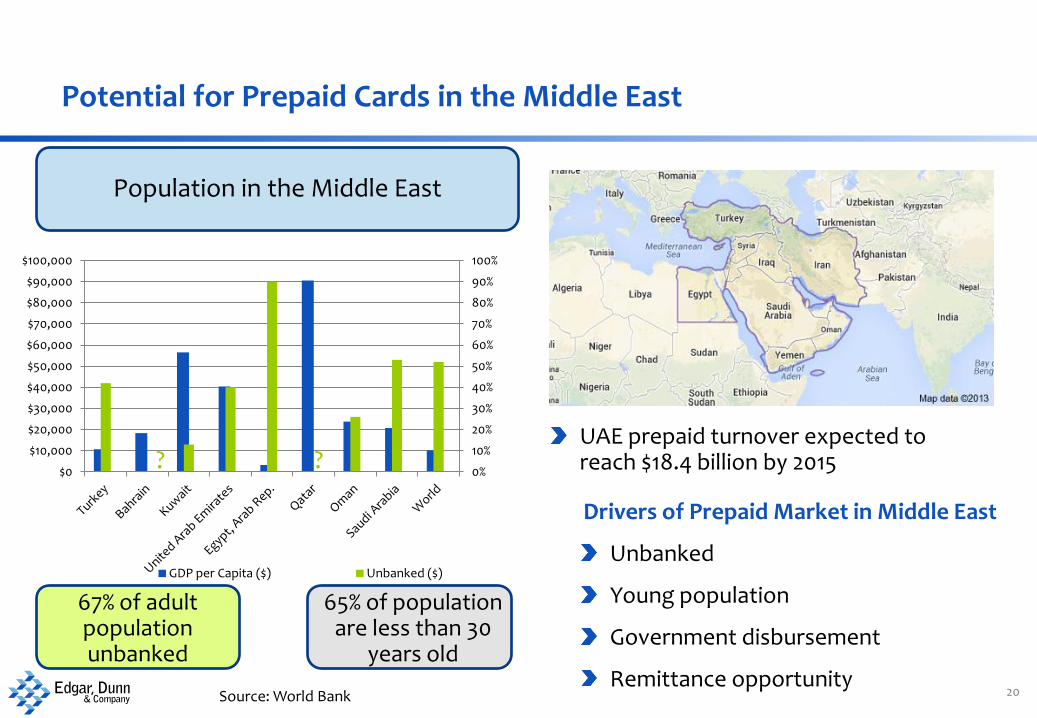

Potential for Prepaid Cards in the Middle East

20

UAE prepaid turnover expected to reach $18.4 billion by 2015

Drivers of Prepaid Market in Middle East

Unbanked

Young population

Government disbursement

Remittance opportunity

Population in the Middle East

67% of adult population unbanked

65% of population are less than 30

years old

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

GDP per Capita ($) Unbanked ($)

? ?

Source: World Bank

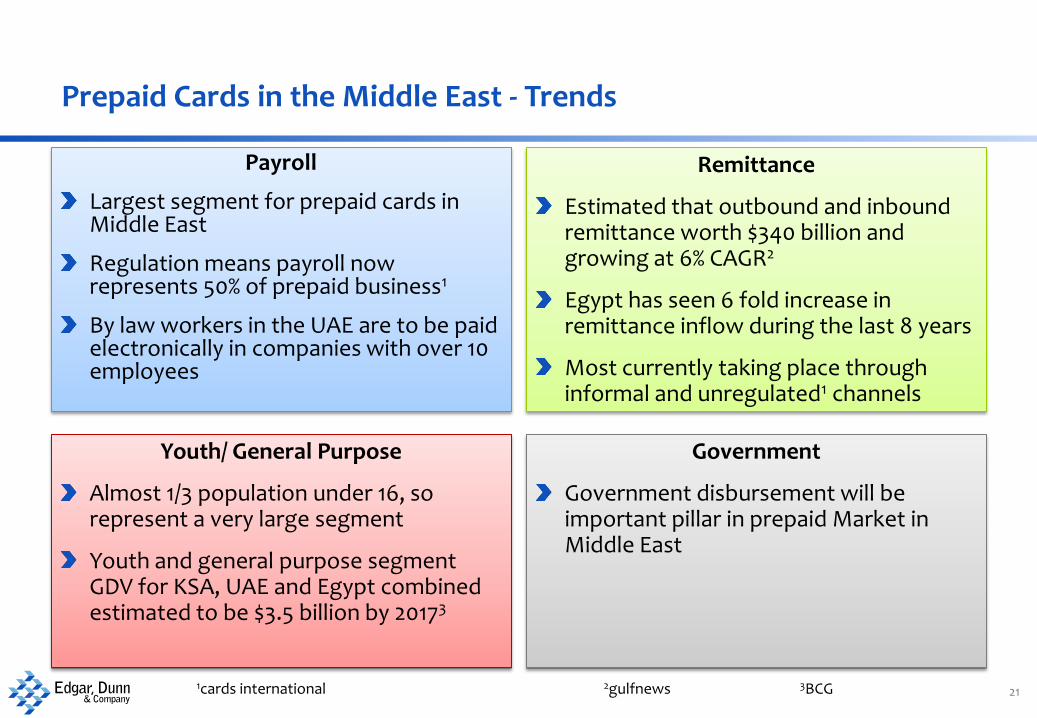

Prepaid Cards in the Middle East - Trends

21

Payroll

Largest segment for prepaid cards in Middle East

Regulation means payroll now represents 50% of prepaid business1

By law workers in the UAE are to be paid electronically in companies with over 10 employees

Remittance

Estimated that outbound and inbound remittance worth $340 billion and growing at 6% CAGR2

Egypt has seen 6 fold increase in remittance inflow during the last 8 years

Most currently taking place through informal and unregulated1 channels

Government

Government disbursement will be important pillar in prepaid Market in Middle East

Youth/ General Purpose

Almost 1/3 population under 16, so represent a very large segment

Youth and general purpose segment GDV for KSA, UAE and Egypt combined estimated to be $3.5 billion by 20173

1cards international 2gulfnews 3BCG

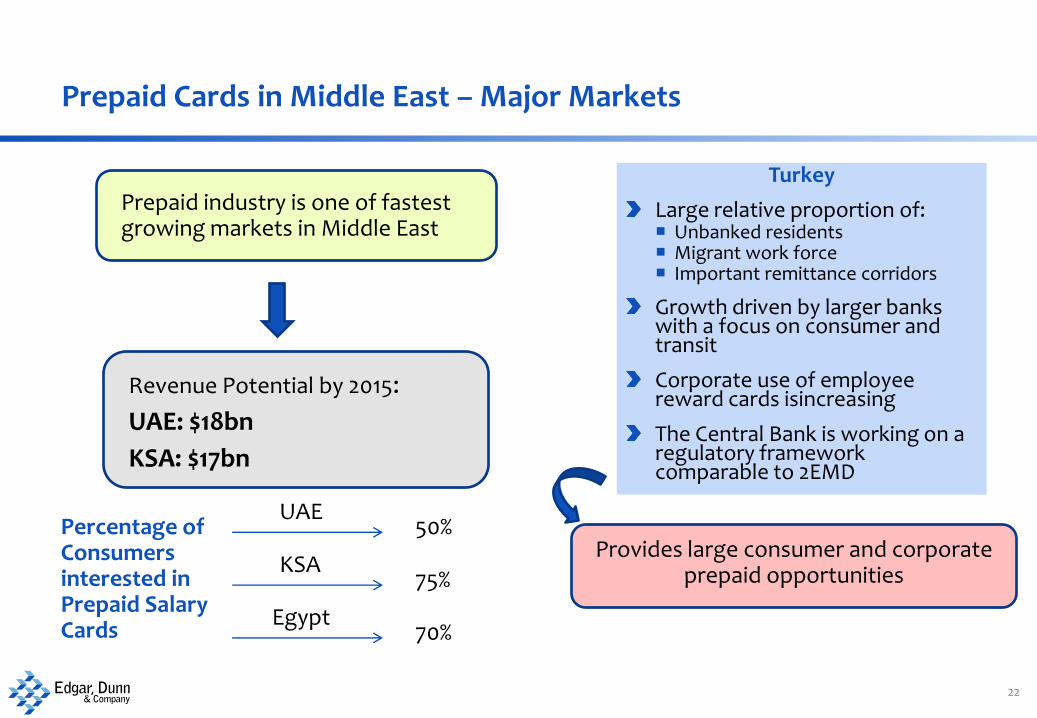

Prepaid Cards in Middle East – Major Markets

22

Percentage of Consumers interested in Prepaid Salary Cards

Turkey

Large relative proportion of: Unbanked residents Migrant work force Important remittance corridors

Growth driven by larger banks with a focus on consumer and transit

Corporate use of employee reward cards isincreasing

The Central Bank is working on a regulatory framework comparable to 2EMD

Prepaid industry is one of fastest growing markets in Middle East

Revenue Potential by 2015:

UAE: $18bn

KSA: $17bn

UAE

KSA

Egypt

50%

75%

70%

Provides large consumer and corporate prepaid opportunities

Prepaid Cards in Middle East – Obstacles to growth

23 23

Lack of regulatory frameworks in most markets Only Saudi Arabia has developed prepaid card regulations Regulation requiring electronic payroll settlement in UAE supports issuance of

prepaid cards

Distribution and Infrastructure Accessibility of prepaid services to customer Increasing number of POS and ATM

Education Issuers and consumers

Payroll cards for migrant workers often require extensive training of the workers

Usage of remittance services is slow to pick up

Revenue Models Competition and Profitability

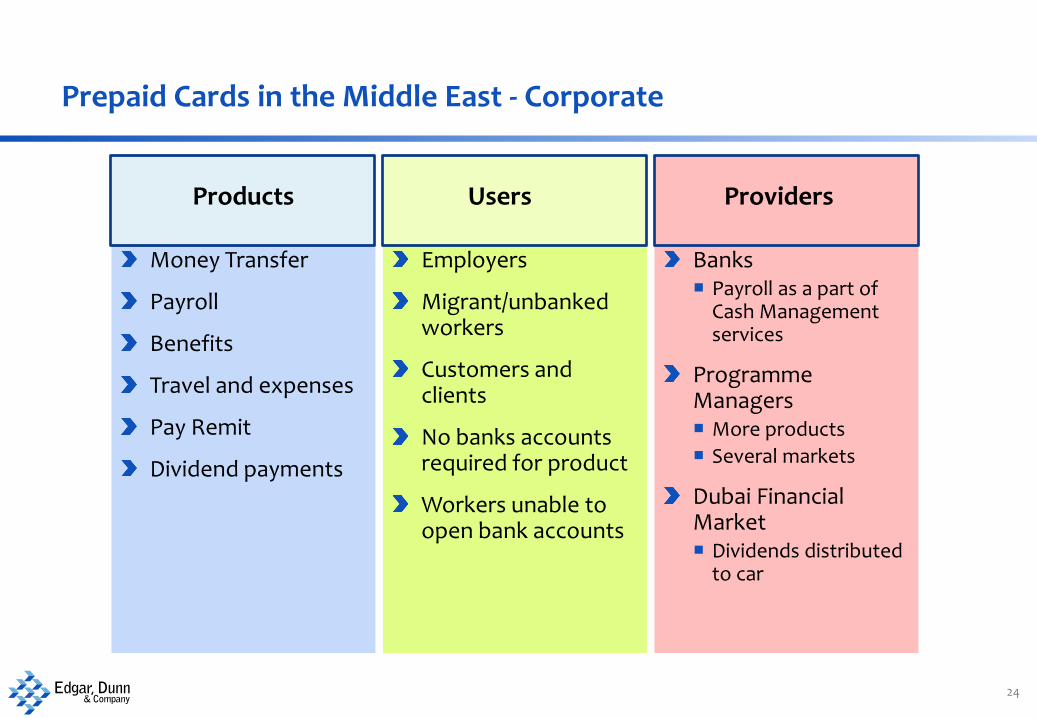

Prepaid Cards in the Middle East - Corporate

24

Money Transfer

Payroll

Benefits

Travel and expenses

Pay Remit

Dividend payments

Banks Payroll as a part of

Cash Management services

Programme Managers More products

Several markets

Dubai Financial Market Dividends distributed

to car

Employers

Migrant/unbanked workers

Customers and clients

No banks accounts required for product

Workers unable to open bank accounts

Products Users Providers

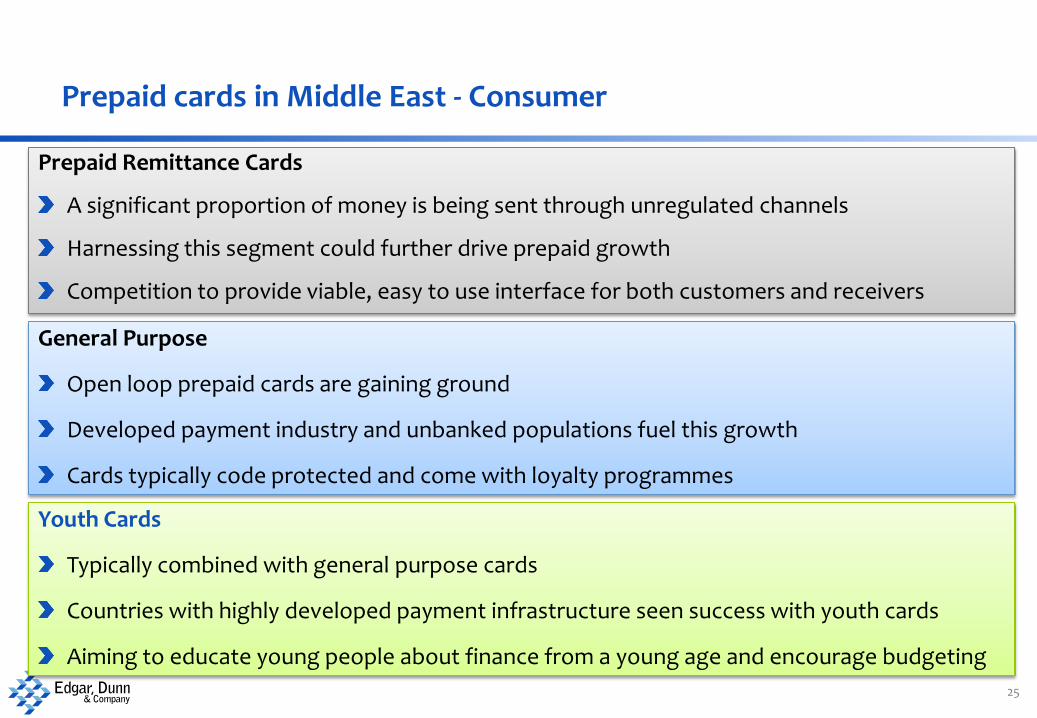

Prepaid cards in Middle East - Consumer

25

Prepaid Remittance Cards

A significant proportion of money is being sent through unregulated channels

Harnessing this segment could further drive prepaid growth

Competition to provide viable, easy to use interface for both customers and receivers

General Purpose

Open loop prepaid cards are gaining ground

Developed payment industry and unbanked populations fuel this growth

Cards typically code protected and come with loyalty programmes

Youth Cards

Typically combined with general purpose cards

Countries with highly developed payment infrastructure seen success with youth cards

Aiming to educate young people about finance from a young age and encourage budgeting

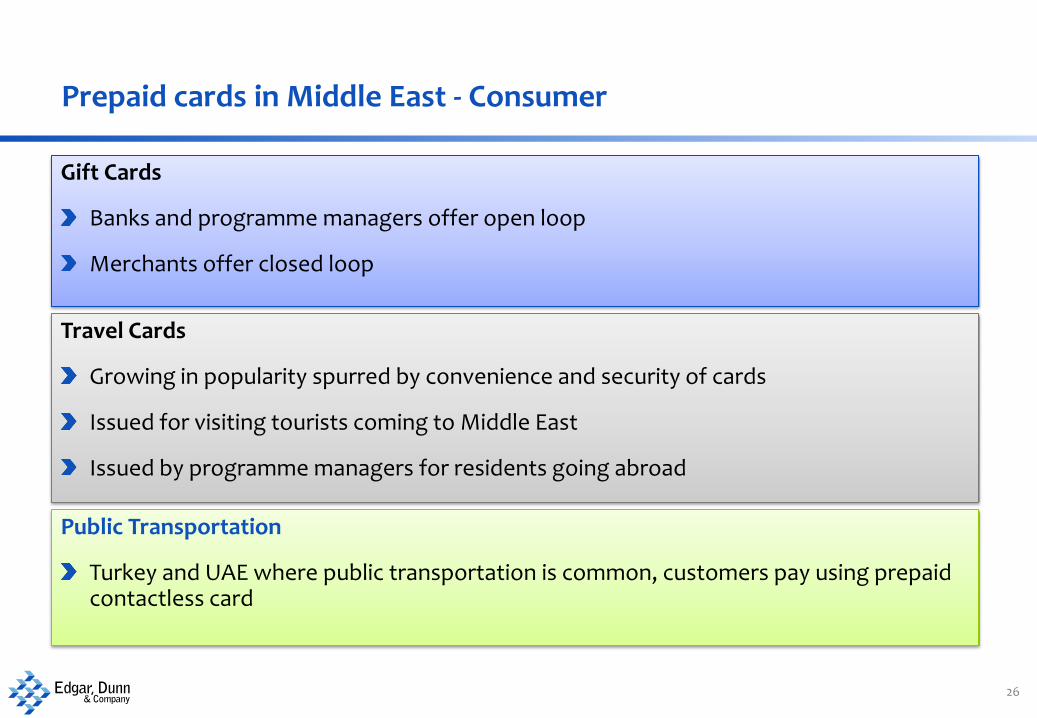

Prepaid cards in Middle East - Consumer

26

Gift Cards

Banks and programme managers offer open loop

Merchants offer closed loop

Travel Cards

Growing in popularity spurred by convenience and security of cards

Issued for visiting tourists coming to Middle East

Issued by programme managers for residents going abroad

Public Transportation

Turkey and UAE where public transportation is common, customers pay using prepaid contactless card

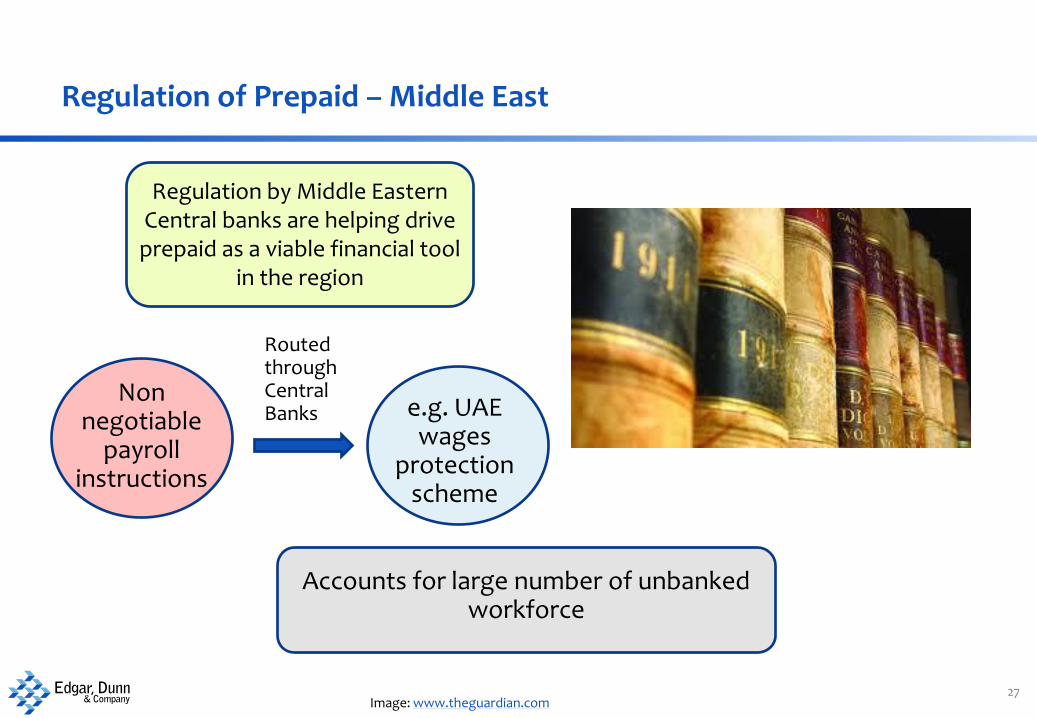

Regulation of Prepaid – Middle East

27

Regulation by Middle Eastern Central banks are helping drive prepaid as a viable financial tool

in the region

Non negotiable

payroll instructions

Routed through Central Banks e.g. UAE

wages protection

scheme

Accounts for large number of unbanked workforce

Image: www.theguardian.com

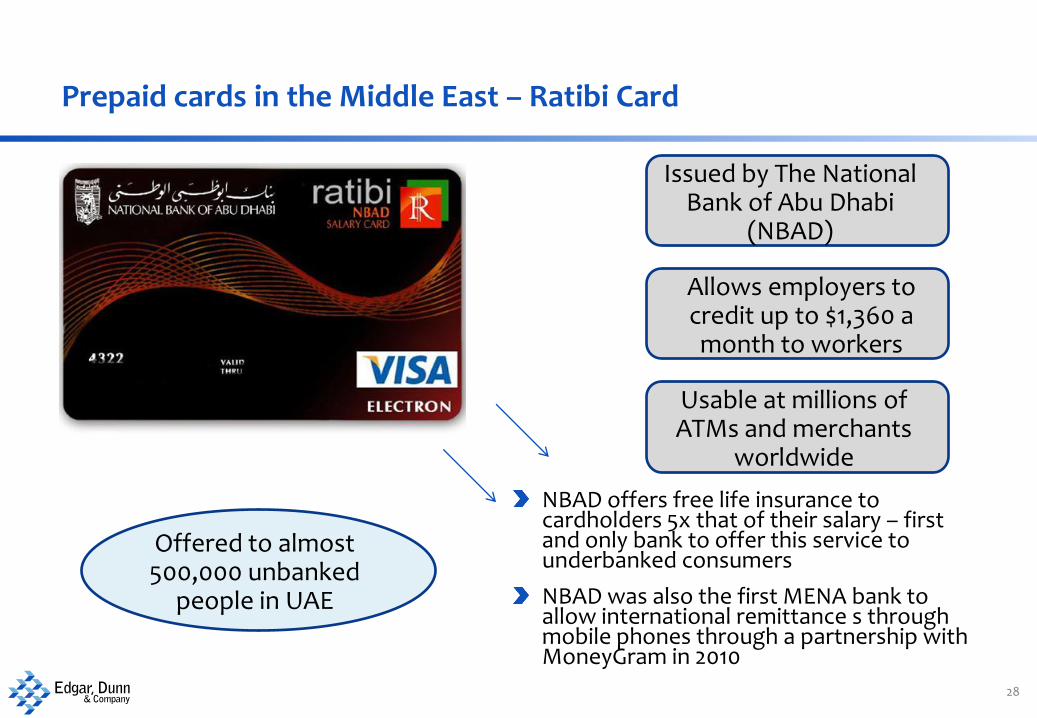

Prepaid cards in the Middle East – Ratibi Card

28

NBAD offers free life insurance to cardholders 5x that of their salary – first and only bank to offer this service to underbanked consumers

NBAD was also the first MENA bank to allow international remittance s through mobile phones through a partnership with MoneyGram in 2010

Issued by The National Bank of Abu Dhabi

(NBAD)

Offered to almost 500,000 unbanked

people in UAE

Allows employers to credit up to $1,360 a month to workers

Usable at millions of ATMs and merchants

worldwide

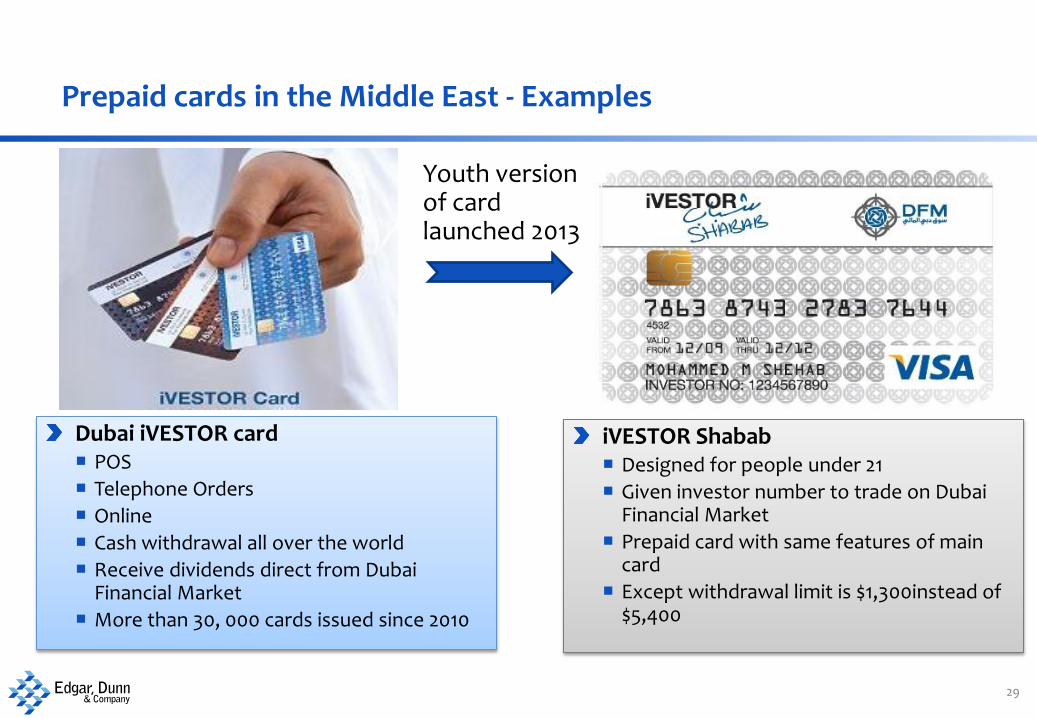

Prepaid cards in the Middle East - Examples

29

Dubai iVESTOR card POS

Telephone Orders

Online

Cash withdrawal all over the world

Receive dividends direct from Dubai Financial Market

More than 30, 000 cards issued since 2010

iVESTOR Shabab Designed for people under 21

Given investor number to trade on Dubai Financial Market

Prepaid card with same features of main card

Except withdrawal limit is $1,300instead of $5,400

Youth version of card launched 2013

Latin America

Overview of Key Markets

© Edgar, Dunn & Company, 2013

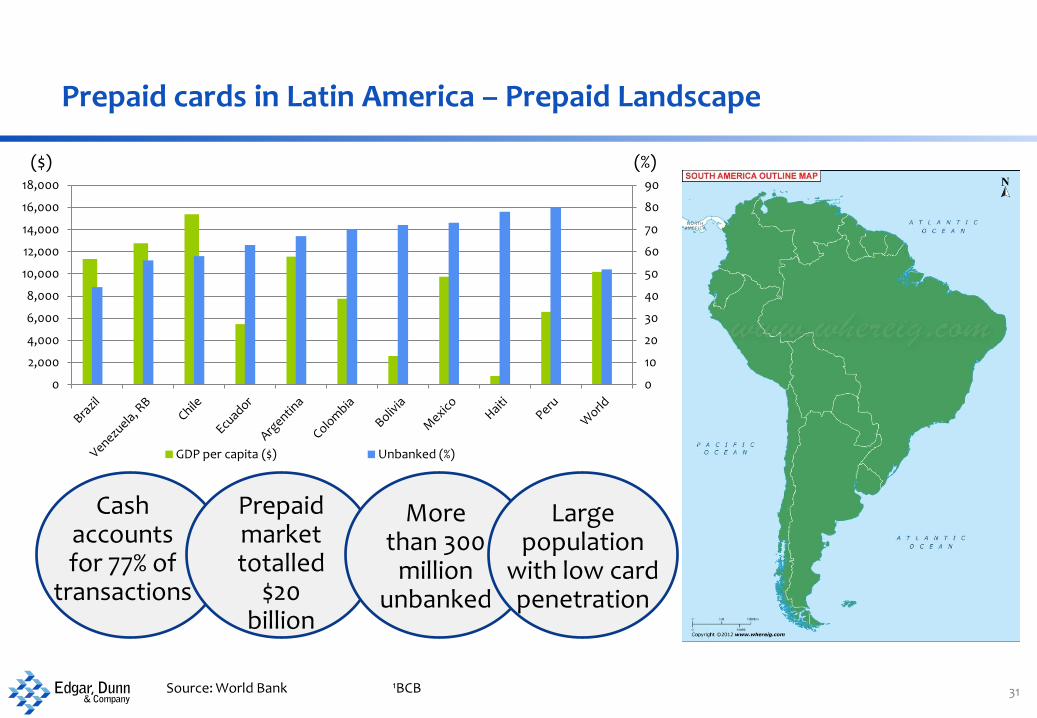

Prepaid cards in Latin America – Prepaid Landscape

31

Cash accounts for 77% of

transactions

Prepaid market totalled

$20 billion

0

10

20

30

40

50

60

70

80

90

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

GDP per capita ($) Unbanked (%)

($) (%)

More than 300

million unbanked

Large population

with low card penetration

1BCB Source: World Bank

Prepaid cards in Latin America – Prepaid Trends

Mexico – Prepaid Cards

2007 2011

32

7.82 million open loop

cards

12.7 million

4 million open loop

government 6.7 million

1.1 million closed loop

4.5 million

Major retailers issue their own

prepaid gift cards

55% of retailers in Mexico and 47% in

Chile issue gift cards1

Brazil’s gift card segment is not very developed

Some merchants offer less restriction on gift

increasing value

Market worth 150-175 $billion

by 20151

Low Value

High Volume Basic financial services cost %5-10 of minimum

monthly wage2 1Speers and associates

2World Bank

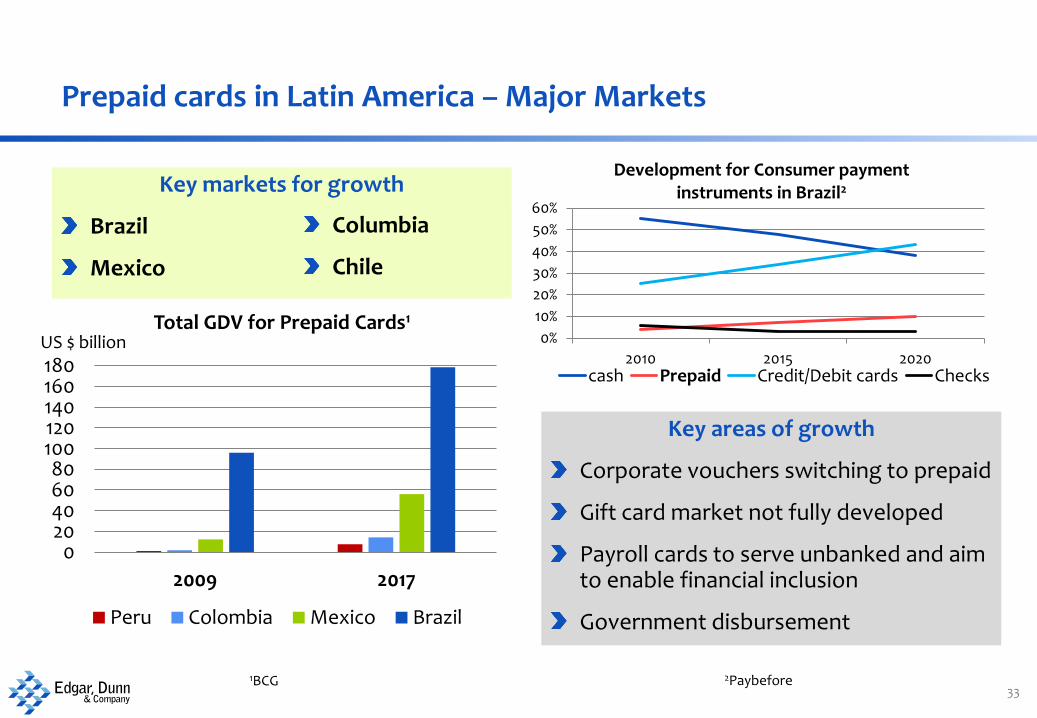

Prepaid cards in Latin America – Major Markets

33

Key markets for growth

Brazil

Mexico

Key areas of growth

Corporate vouchers switching to prepaid

Gift card market not fully developed

Payroll cards to serve unbanked and aim to enable financial inclusion

Government disbursement

0%

10%

20%

30%

40%

50%

60%

2010 2015 2020

Development for Consumer payment instruments in Brazil2

cash Prepaid Credit/Debit cards Checks

0 20 40 60 80

100 120 140 160 180

2009 2017

US $ billion Total GDV for Prepaid Cards1

Peru Colombia Mexico Brazil

2Paybefore

1BCG

Columbia

Chile

Prepaid cards in Latin America - Government

34

Brazilian government uses prepaid cards to pay welfare benefits

to consumers

Benefits distributed through Bolsa Familia*

social services programme to 12 million

households

70

90

110

130

2009 2017

US $ bn Total GDV for government programmes1

Brazil

Mexican government has recently moved towards distribution of social

benefits via prepaid cards

6.5 million

families

$99 billion

0

5

10

15

2009 2017

US $ bn Total GDV for government programmes1

Peru

Colombia

Mexico

1BCG

Prepaid cards in Latin America - Corporate

35

In Brazil employers are obliged by the government to

give employees meal vouchers

Corporate paper vouchers are being replaced with Visa

prepaid cards

70,000 employers and 3.2 million

workers use Visa Vale

Recently, banks and branded networks are included in these solutions, creating widely

accepted closed loop solutions

Initially programme managers operate directly between employers and merchants and

restaurants

Programme managers are very active in this segment

Thus consumers learn to use banking products

Prepaid cards for rewards and incentives are gaining popularity

Banks and micro finance institutions starting to cooperate

Micro finance loans are distributed through prepaid cards

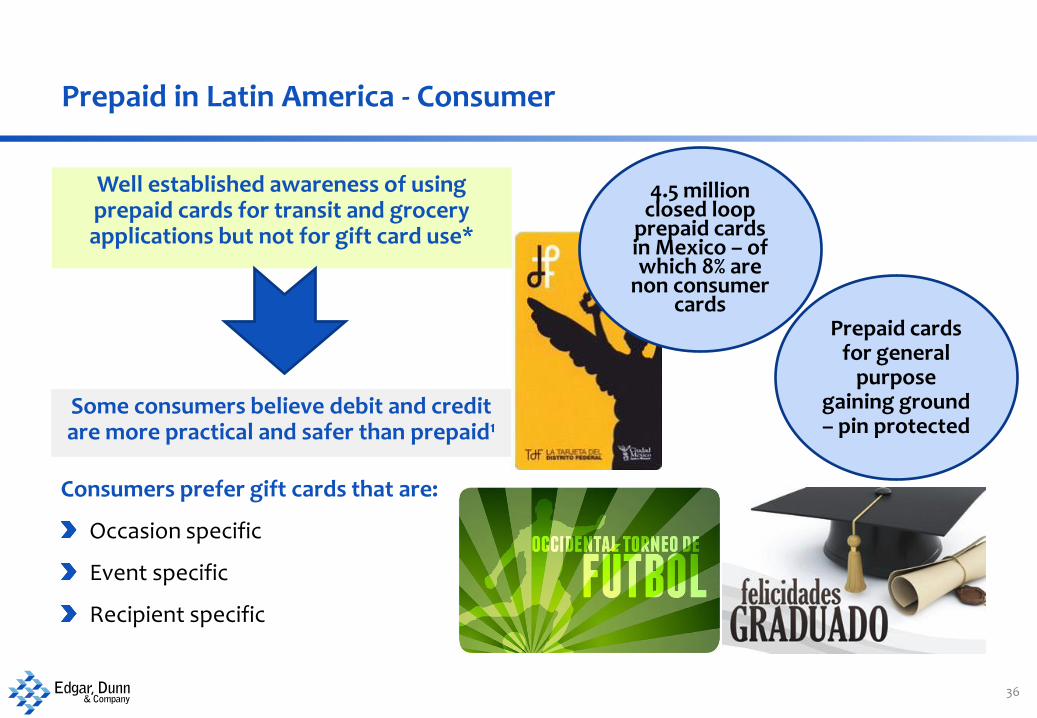

Prepaid in Latin America - Consumer

36

Well established awareness of using prepaid cards for transit and grocery applications but not for gift card use*

Some consumers believe debit and credit are more practical and safer than prepaid1

Consumers prefer gift cards that are:

Occasion specific

Event specific

Recipient specific

4.5 million closed loop

prepaid cards in Mexico – of which 8% are

non consumer cards

Prepaid cards for general

purpose gaining ground – pin protected

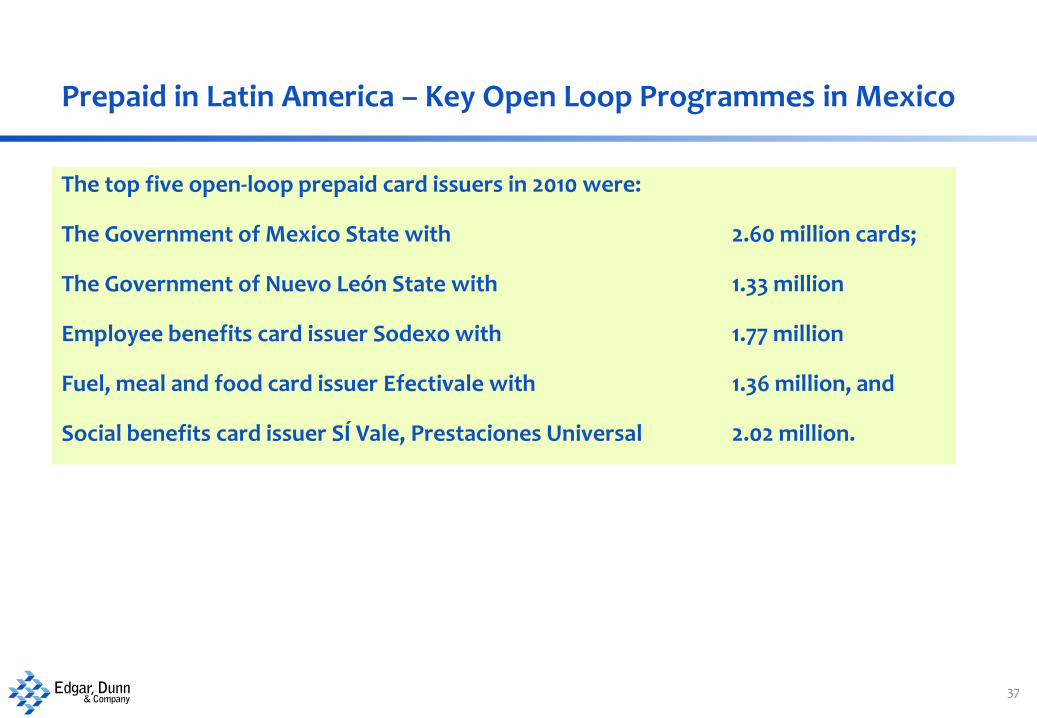

Prepaid in Latin America – Key Open Loop Programmes in Mexico

37

The top five open-loop prepaid card issuers in 2010 were:

The Government of Mexico State with 2.60 million cards;

The Government of Nuevo León State with 1.33 million

Employee benefits card issuer Sodexo with 1.77 million

Fuel, meal and food card issuer Efectivale with 1.36 million, and

Social benefits card issuer SÍ Vale, Prestaciones Universal 2.02 million.

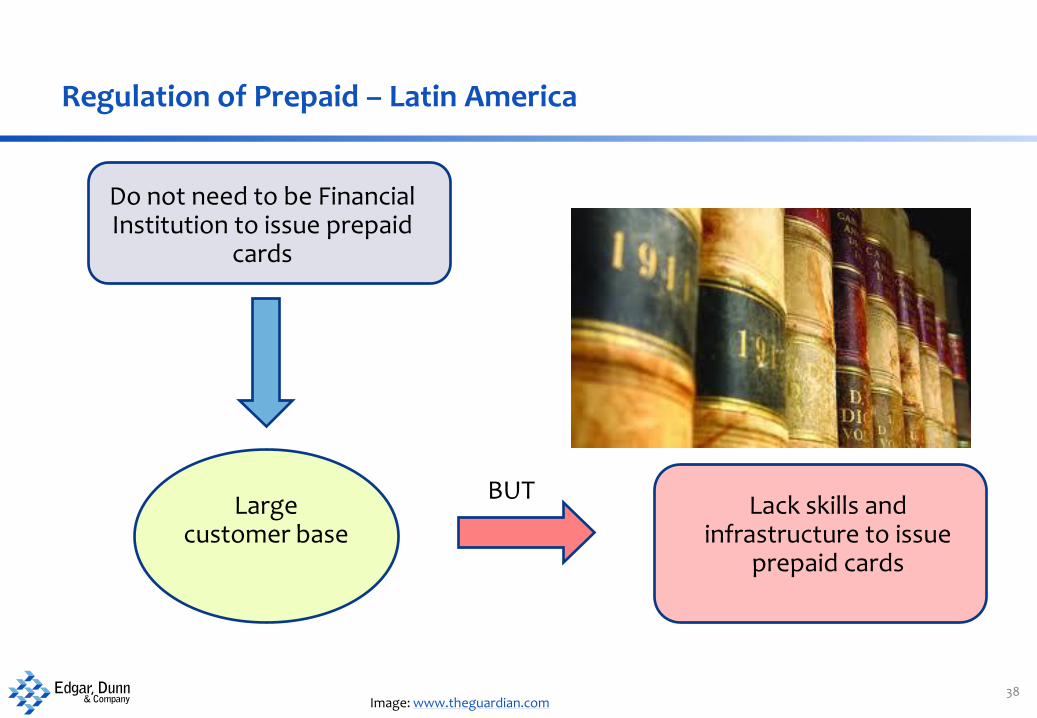

Regulation of Prepaid – Latin America

38

Do not need to be Financial Institution to issue prepaid

cards

Large customer base

Lack skills and infrastructure to issue

prepaid cards

BUT

Image: www.theguardian.com

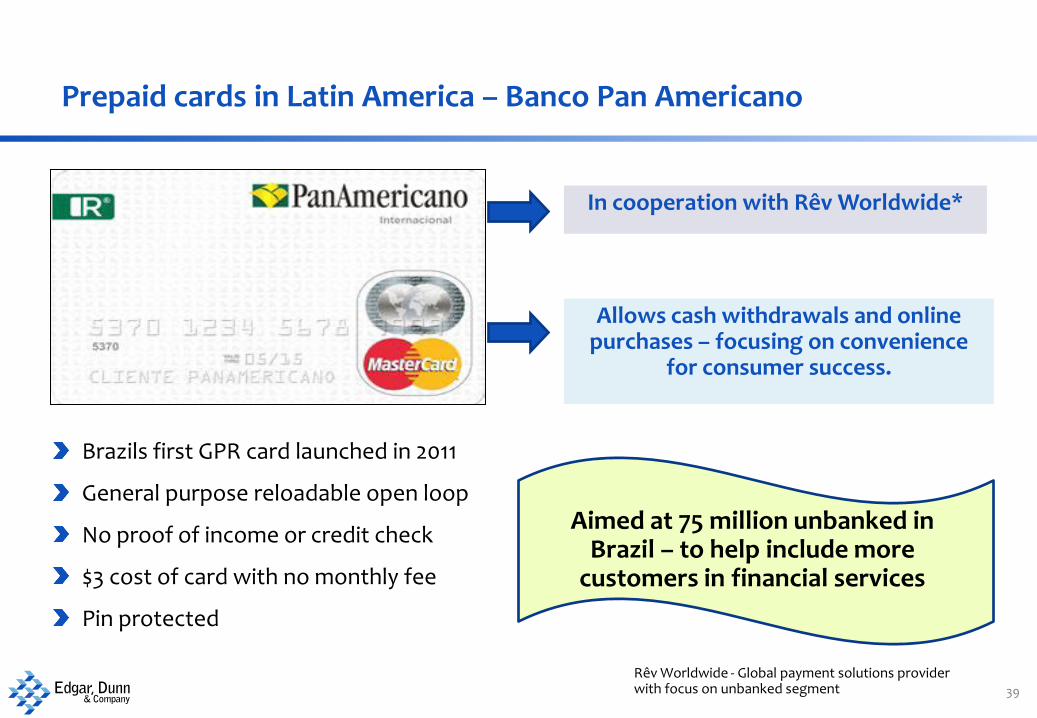

Prepaid cards in Latin America – Banco Pan Americano

39

Brazils firts GPR card launched in 2011

General purpose reloadable open loop

No proof of income or credit check

In cooperation with Rêv Worldwide*

Brazils first GPR card launched in 2011

General purpose reloadable open loop

No proof of income or credit check

$3 cost of card with no monthly fee

Pin protected

Allows cash withdrawals and online purchases – focusing on convenience

for consumer success.

Aimed at 75 million unbanked in Brazil – to help include more

customers in financial services

Rêv Worldwide - Global payment solutions provider with focus on unbanked segment

Prepaid cards in Latin America – MiFon MasterCard Prepaid Card

40

Allows users to withdraw funds from any of the 6,200 Banorte ATMs and send

money from one account to another using their mobile phone

Targeted at unbanked Mexicans, Mifon cards can be bought and reloaded at retail locations without the need to visit a Banorte Branch

Cardholders can carry out P2P transfers and make payments to merchants and utility companies from MiFon account via SMS

Partnership with Rêv Worldwide and Banorte – Mexico's 3rd largest bank

MasterCard Prepaid Debit Card linked to a mobile phone

account

© 2013 Edgar, Dunn & Company

Thank You

41

Edgar, Dunn & Company Candlewick House 120 Cannon Street London EC4N 6AS

Tel +44 207 283 1114 Fax +44 207 283 1007

Peter Sidenius Director