Embed Size (px)

Citation preview

Global Preferred Securities Portfolio, Series 1

The unit investment trust named above (the “Portfolio”), included in Van Kampen Unit Trusts, Series 1049,invests in a portfolio of preferred securities. Of course, we cannot guarantee that the Portfolio will achieve itsobjective.

October 22, 2010

You should read this prospectus and retain it for future reference.

The Securities and Exchange Commission has not approved or disapproved of the Unitsor passed upon the adequacy or accuracy of this prospectus.

Any contrary representation is a criminal offense.

INVESCO

Investment Objective. The Portfolio seeks anattractive level of current income.

Principal Investment Strategy. The Portfolioseeks to achieve its objective by investing in aportfolio consisting of preferred securities issuedprimarily by financial institutions such as banks andinsurance companies. The portfolio was selected byCohen & Steers Capital Management, Inc., the“Portfolio Consultant”. In selecting the Portfolio,Cohen & Steers weighed many factors, includingindustry and company trends and fundamentals aswell as the broader economic backdrop. The bankingand insurance industr ies are highly regulated.Preferred securities, which provide regulatory capitalbenefits to the companies in these industries, can besignificantly impacted by changes in regulations.While the final outcome of regulatory changes cannotbe predicted, Cohen & Steers considered the currentregulatory environment in selecting the securities inthe portfolio. Cohen & Steers implemented valuationscreens which considered, among other things,security call features, premiums and discounts, andliquidity. Paramount in the selection process wasfundamental credit qual i ty and divers i f icat ionconsiderations. As of the Initial Date of Deposit,certain securities included in the Portfolio are ratedbelow-investment grade by both Standard & Poor’sand Moody’s Investors Service, Inc. See “RiskFactors--High Yield Security Risk”.

Recent regulatory reforms in the United States,and pending reforms overseas, may potentiallychange the role that certain preferred securities mayserve in financial institutions’ regulatory capital. Thesechanges may negatively impact the prices of somepreferred securities, particularly those trading abovetheir par values as the new reforms increase thepossibility of near-term redemption. In addition,certain preferred securities may be less attractive forissuing banks, which is believed to be likely to resultin a significant reduction in the issuance and, overtime, availability of these types of securities andpotentially many outstanding issues being redeemed.

Should an issuer call or redeem a preferred securityduring the life of the Portfolio, the monthly income onyour Units may be reduced, and in certain cases, thevalue of your Units may decrease. However, othersecurities may be positively affected, particularlythose trading at discounts to par value. Suchsecurities may experience an increase in marketvalue from issuers’ redemption activity. A longer-termconsequence of the regulatory reforms, which are tobe phased in over a period of a few years, is thepotential for certain preferred securit ies in thePortfolio to become more scarce and potentially lessliquid. In addition, other proposals to update capitalrequirements for banks globally, if finalized andadopted in the United States, would further limit theattractiveness to issuing banks of a broader range ofpreferred security types and possibly have moresignificant consequences, including a smaller marketof issues and less liquidity. It is not possible to predictthe impact of these reforms and proposals on thePortfolio. See “Preferred Securities”.

The preferred securities selected for the Portfolioconsist of traditional preferred securities and hybrid-preferred securities. Traditional preferred securitiesmay be issued by an entity taxable as a corporationand pay fixed or floating rate dividends. However,these claims are subordinated to more seniorcreditors, including senior debt holders. A companymust pay dividends on its preferred securities beforepaying any dividends on its common stock, and theclaims of preferred securities holders are ahead ofcommon stockholders’ c la ims on assets in acorporate liquidation.

Hybrid-preferred securities, including trust preferredsecurities, are debt instruments that have characteristicssimilar to those of traditional preferred securities. Hybrid-preferred securities may be issued by corporations,generally in the form of interest-bearing notes withpreferred securities characteristics, or by an affiliatedtrust or partnership of the corporation, generally in theform of preferred interests in subordinated debenturesor similarly structured securities. The hybrid-preferred

2

Global Preferred Securities Portfolio

3

securities market consists of both fixed and adjustablecoupon rate securities that are either perpetual in natureor have stated maturity dates. Hybrid-preferred holdersgenerally have claims to assets in a corporate liquidationthat are senior to those of traditional preferred securitiesbut subordinate to those of senior debt holders. Certainsubordinated debt and senior debt issues that havepreferred characteristics are also considered to be partof the broader preferred securities market.

The Portfolio will invest in both over-the-counter(“OTC”) and exchange-traded preferred securities. OTCissues are often referred to in the financial industry as“capital securities.” Certain Portfolio securities may paydividends that are not eligible for the corporatedividends received deduction (“DRD”) for corporationsor for treatment as qualified dividend income (“QDI”) forindividuals while other Portfolio securities may paydividends eligible for the DRD for corporations or fortreatment as QDI for individuals. There can be noassurance that favorable tax treatment of QDI willcontinue following December 31, 2010. See “Taxation”.

The preferred securities selected for the Portfoliogenerally pay a fixed rate of return during the life of thePortfolio and are sold on the basis of current yield.Although the underlying securities may pay quarterly orsemi-annual distributions of income, the Portfolio isdesigned to make monthly distributions to Unitholders.The preferred securities in the Portfolio may be calledor redeemed during the life of the Portfolio.

The Portfolio Consultant. Founded in 1986,Cohen & Steers Capital Management Inc. is amanager of high income equity portfolios specializingin U.S. REITs, global real estate securities, preferredsecurities, utilities, value equity securities and otherhigh dividend paying common stocks. As of June 30,2010, Cohen & Steers Capital Management Inc. had$26.2 billion in assets under management. Cohen &Steers manages separate account portfolios forinstitutional investors, including some of the world’slargest pension funds and endowments. In addition,the firm manages open- and closed-end mutual funds

for both retail and institutional investors. Cohen &Steers is among the largest REIT managers in theU.S. and employs a significant research and tradingstaff. Many investors have come to view Cohen &Steers as an important source for income-orientedinvestment products. Cohen & Steers also acts asSupervisor of the Portfolio. As described above,Cohen & Steers advises other cl ients such asinvestment companies and other accounts. Many ofthese client accounts are “managed” accounts. ThePortfolio is not a managed fund and will generally notsell or replace Securities. Please refer to “Objectivesand Securities Selection” for a discussion of Cohen &Steers’ activities regarding the advisory accounts ofits other clients and the effect these activities mayhave on the Securities in the Portfolio.

William Scapell, CFA, former director of preferredsecurities research at Merrill Lynch, heads the firm’spreferred securities research and investment team.Mr. Scapell and his team of analysts cover the $200billion U.S. corporate preferred market, researching abroad scope of domest ic and foreign issuersencompassing media, telecommunications, utilities,insurance, banking and finance, and real estate. Thefirm’s preferred securities investment professionalsare distinguished by the breadth of their experienceand the depth of their industry knowledge.

Principal Risks. As with all investments, you canlose money by investing in this Portfolio. The Portfolioalso might not perform as well as you expect. This canhappen for reasons such as these:

• Prices of the securities in the Portfoliowill fluctuate. The value of your investmentmay fall over time.

• The value of preferred securities mayfall if interest rates, in general, rise. Noone can predict whether interest rates will riseor fall in the future.

• An issuer may be unable to makedividend or interest payments in the

4

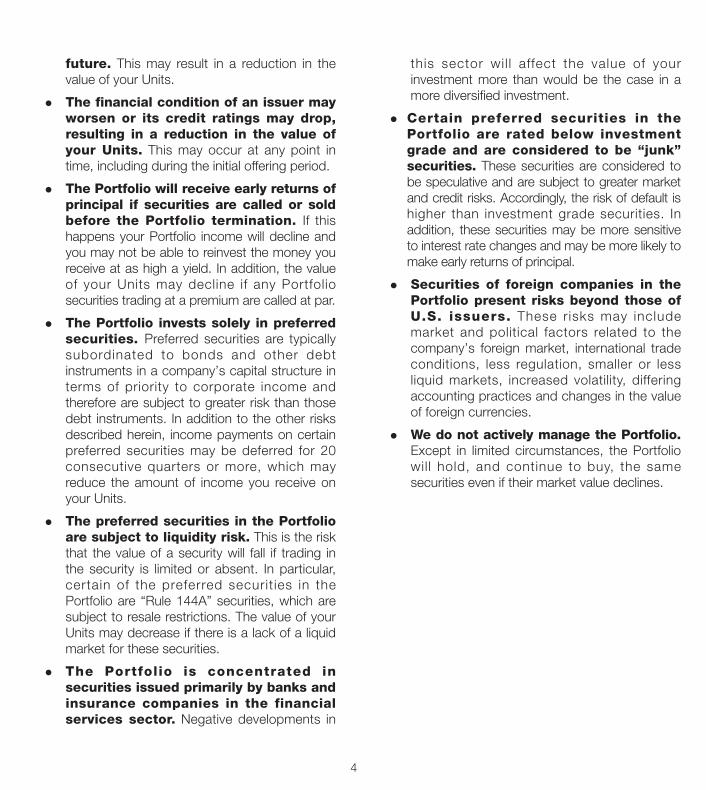

future. This may result in a reduction in thevalue of your Units.

• The financial condition of an issuer mayworsen or its credit ratings may drop,resulting in a reduction in the value ofyour Units. This may occur at any point intime, including during the initial offering period.

• The Portfolio will receive early returns ofprincipal if securities are called or soldbefore the Portfolio termination. If thishappens your Portfolio income will decline andyou may not be able to reinvest the money youreceive at as high a yield. In addition, the valueof your Units may decline if any Portfoliosecurities trading at a premium are called at par.

• The Portfolio invests solely in preferredsecurities. Preferred securities are typicallysubordinated to bonds and other debtinstruments in a company’s capital structure interms of priority to corporate income andtherefore are subject to greater risk than thosedebt instruments. In addition to the other risksdescribed herein, income payments on certainpreferred securities may be deferred for 20consecutive quarters or more, which mayreduce the amount of income you receive onyour Units.

• The preferred securities in the Portfolioare subject to liquidity risk. This is the riskthat the value of a security will fall if trading inthe security is limited or absent. In particular,certain of the preferred securit ies in thePortfolio are “Rule 144A” securities, which aresubject to resale restrictions. The value of yourUnits may decrease if there is a lack of a liquidmarket for these securities.

• The Portfolio is concentrated insecurities issued primarily by banks andinsurance companies in the financialservices sector. Negative developments in

this sector wi l l affect the value of yourinvestment more than would be the case in amore diversified investment.

• Certain preferred securities in thePortfolio are rated below investmentgrade and are considered to be “junk”securities. These securities are considered tobe speculative and are subject to greater marketand credit risks. Accordingly, the risk of default ishigher than investment grade securities. Inaddition, these securities may be more sensitiveto interest rate changes and may be more likely tomake early returns of principal.

• Securities of foreign companies in thePortfolio present risks beyond those ofU.S. issuers. These r isks may includemarket and political factors related to thecompany’s foreign market, international tradeconditions, less regulation, smaller or lessliquid markets, increased volatility, differingaccounting practices and changes in the valueof foreign currencies.

• We do not actively manage the Portfolio.Except in limited circumstances, the Portfoliowil l hold, and continue to buy, the samesecurities even if their market value declines.

5

Fee Table

The amounts below are estimates of the direct and indirectexpenses that you may incur based on a $10 Public Offering Price perUnit. Actual expenses may vary.

As a % of Public Amount Offering Per 100Sales Charge Price Units _________ _________

Initial sales charge 1.000% $10.000Deferred sales charge 2.000 20.000Creation and development fee 0.500 5.000 ______ ______Maximum sales charge 3.500% $35.000 ______ ______ ______ ______

As a % Amount of Net Per 100 Assets Units _________ _________

Estimated Organization Costs 0.364% $3.500 ______ ______ ______ ______

Estimated Annual Expenses Trustee’s fee and operating expenses 0.171% $1.642Supervisory fee 0.075 0.721Bookkeeping and administrative fees 0.015 0.150 ______ ______

Total 0.261% $2.513* ______ ______ ______ ______

Example

This example helps you compare the cost of the Portfolio with otherunit trusts and mutual funds. In the example we assume that the expensesdo not change and that the Portfolio’s annual return is 5%. Your actualreturns and expenses will vary. The amounts are the same regardless ofwhether you sell your investment at the end of a period or continue to holdyour investment. Based on these assumptions, you would pay thefollowing expenses for every $10,000 you invest in the Portfolio:

1 year $ 410

2 years 435

3 years (Life of Portfolio) 462

* The estimated annual expenses are based upon the estimated trust sizefor the Portfolio determined as of the initial date of deposit. Becausecertain of the operating expenses are fixed amounts, if the Portfolio doesnot reach the estimated size, or if the value of the Portfolio or number ofoutstanding units decline over the life of the trust, or if the actual amountof the operating expenses exceeds the estimated amounts, the actualamount of the operating expenses per 100 units would exceed theestimated amounts. In some cases, the actual amount of operatingexpenses may substantially differ from the amounts reflected above.

The maximum sales charge is 3.50% of the Public Offering Price perUnit. The initial sales charge is the difference between the total salescharge (maximum of 3.50% of the Public Offering Price) and the sum ofthe remaining deferred sales charge and the total creation anddevelopment fee. The deferred sales charge is fixed at $0.200 per Unit andaccrues daily from December 10, 2010 through May 10, 2011. YourPortfolio pays a proportionate amount of this charge on the 10th day ofeach month beginning in the accrual period until paid in full. Thecombination of the initial and deferred sales charges comprises the“transactional sales charge”. The creation and development fee is fixed at$0.05 per Unit and is paid at the earlier of the end of the initial offeringperiod or six months following the Initial Date of Deposit. The Portfolioassesses the Supervisory Fee as a percentage of the daily net asset value(0.075%). Other annual expenses are assessed as dollar amounts per Unit.

Essential Information

Unit Price at Initial Date of Deposit $10.0000

Unit Redemption Price at Initial Date of Deposit1 $9.560

Initial Date of Deposit October 22, 2010

Mandatory Termination Date October 22, 2013

Estimated Net Annual Income2 $0.64333 per Unit

Estimated Initial Distribution2 $0.03 per Unit

Record Dates 10th day of November 2010 and each month thereafter

Distribution Dates 25th day of November 2010 and each month thereafter

CUSIP Numbers Cash – 37950X109

Wrap Fee Cash – 37950X117

1 After the first settlement date (October 27, 2010) you will pay accruedinterest from this date to your settlement date less incomedistributions.

2 As of close of business day prior to Initial Date of Deposit. The actualdistributions you receive will vary from the estimated amount due tochanges in the Portfolio’s fees and expenses, in actual income receivedby the Portfolio, currency fluctuations and with changes in the Portfoliosuch as the acquisition or liquidation of securities. See “Rights ofUnitholders--Estimated Distributions.”

6

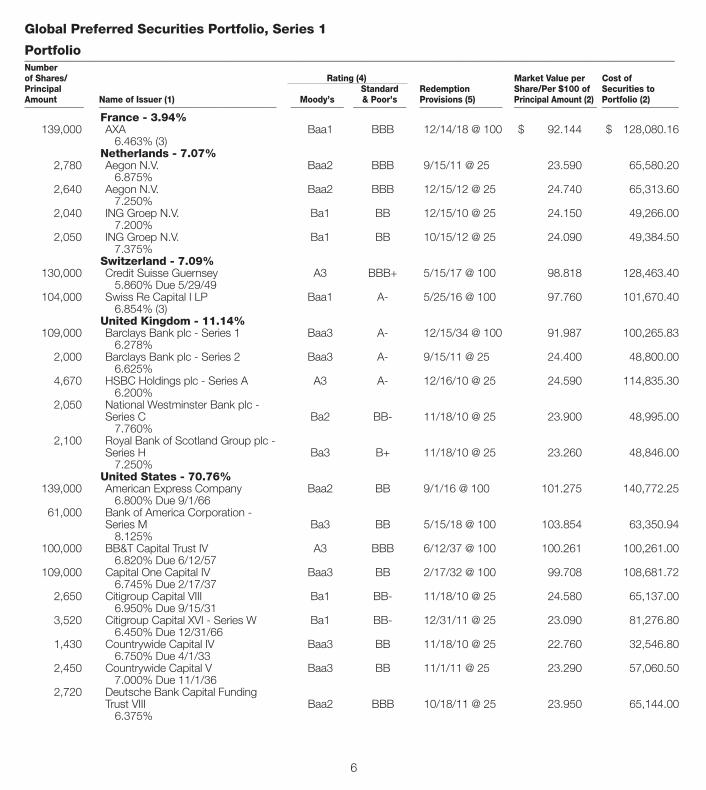

Global Preferred Securities Portfolio, Series 1

Portfolio______________________________________________________________________________________________________________Number of Shares/ Rating (4) Market Value per Cost ofPrincipal Standard Redemption Share/Per $100 of Securities toAmount Name of Issuer (1) Moody’s & Poor’s Provisions (5) Principal Amount (2) Portfolio (2) __________ ______________________________ _________ _________ ______________ ______________ _____________ France - 3.94% 139,000 AXA Baa1 BBB 12/14/18 @ 100 $ 92.144 $ 128,080.16 6.463% (3) Netherlands - 7.07% 2,780 Aegon N.V. Baa2 BBB 9/15/11 @ 25 23.590 65,580.20 6.875% 2,640 Aegon N.V. Baa2 BBB 12/15/12 @ 25 24.740 65,313.60 7.250% 2,040 ING Groep N.V. Ba1 BB 12/15/10 @ 25 24.150 49,266.00 7.200% 2,050 ING Groep N.V. Ba1 BB 10/15/12 @ 25 24.090 49,384.50 7.375% Switzerland - 7.09% 130,000 Credit Suisse Guernsey A3 BBB+ 5/15/17 @ 100 98.818 128,463.40 5.860% Due 5/29/49 104,000 Swiss Re Capital I LP Baa1 A- 5/25/16 @ 100 97.760 101,670.40 6.854% (3) United Kingdom - 11.14% 109,000 Barclays Bank plc - Series 1 Baa3 A- 12/15/34 @ 100 91.987 100,265.83 6.278% 2,000 Barclays Bank plc - Series 2 Baa3 A- 9/15/11 @ 25 24.400 48,800.00 6.625% 4,670 HSBC Holdings plc - Series A A3 A- 12/16/10 @ 25 24.590 114,835.30 6.200% 2,050 National Westminster Bank plc - Series C Ba2 BB- 11/18/10 @ 25 23.900 48,995.00 7.760% 2,100 Royal Bank of Scotland Group plc - Series H Ba3 B+ 11/18/10 @ 25 23.260 48,846.00 7.250% United States - 70.76% 139,000 American Express Company Baa2 BB 9/1/16 @ 100 101.275 140,772.25 6.800% Due 9/1/66 61,000 Bank of America Corporation - Series M Ba3 BB 5/15/18 @ 100 103.854 63,350.94 8.125% 100,000 BB&T Capital Trust IV A3 BBB 6/12/37 @ 100 100.261 100,261.00 6.820% Due 6/12/57 109,000 Capital One Capital IV Baa3 BB 2/17/32 @ 100 99.708 108,681.72 6.745% Due 2/17/37 2,650 Citigroup Capital VIII Ba1 BB- 11/18/10 @ 25 24.580 65,137.00 6.950% Due 9/15/31 3,520 Citigroup Capital XVI - Series W Ba1 BB- 12/31/11 @ 25 23.090 81,276.80 6.450% Due 12/31/66 1,430 Countrywide Capital IV Baa3 BB 11/18/10 @ 25 22.760 32,546.80 6.750% Due 4/1/33 2,450 Countrywide Capital V Baa3 BB 11/1/11 @ 25 23.290 57,060.50 7.000% Due 11/1/36 2,720 Deutsche Bank Capital Funding Trust VIII Baa2 BBB 10/18/11 @ 25 23.950 65,144.00 6.375%

7

Global Preferred Securities Portfolio, Series 1

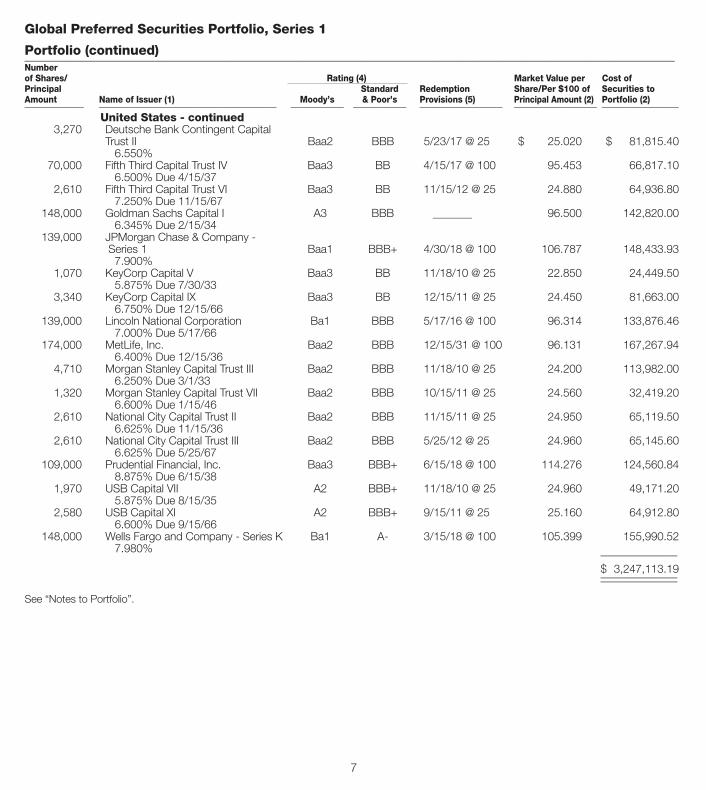

Portfolio (continued)______________________________________________________________________________________________________________Number of Shares/ Rating (4) Market Value per Cost ofPrincipal Standard Redemption Share/Per $100 of Securities toAmount Name of Issuer (1) Moody’s & Poor’s Provisions (5) Principal Amount (2) Portfolio (2) __________ ______________________________ _________ _________ ______________ ______________ _____________ United States - continued 3,270 Deutsche Bank Contingent Capital Trust II Baa2 BBB 5/23/17 @ 25 $ 25.020 $ 81,815.40 6.550% 70,000 Fifth Third Capital Trust IV Baa3 BB 4/15/17 @ 100 95.453 66,817.10 6.500% Due 4/15/37 2,610 Fifth Third Capital Trust VI Baa3 BB 11/15/12 @ 25 24.880 64,936.80 7.250% Due 11/15/67 148,000 Goldman Sachs Capital I A3 BBB _______ 96.500 142,820.00 6.345% Due 2/15/34 139,000 JPMorgan Chase & Company - Series 1 Baa1 BBB+ 4/30/18 @ 100 106.787 148,433.93 7.900% 1,070 KeyCorp Capital V Baa3 BB 11/18/10 @ 25 22.850 24,449.50 5.875% Due 7/30/33 3,340 KeyCorp Capital IX Baa3 BB 12/15/11 @ 25 24.450 81,663.00 6.750% Due 12/15/66 139,000 Lincoln National Corporation Ba1 BBB 5/17/16 @ 100 96.314 133,876.46 7.000% Due 5/17/66 174,000 MetLife, Inc. Baa2 BBB 12/15/31 @ 100 96.131 167,267.94 6.400% Due 12/15/36 4,710 Morgan Stanley Capital Trust III Baa2 BBB 11/18/10 @ 25 24.200 113,982.00 6.250% Due 3/1/33 1,320 Morgan Stanley Capital Trust VII Baa2 BBB 10/15/11 @ 25 24.560 32,419.20 6.600% Due 1/15/46 2,610 National City Capital Trust II Baa2 BBB 11/15/11 @ 25 24.950 65,119.50 6.625% Due 11/15/36 2,610 National City Capital Trust III Baa2 BBB 5/25/12 @ 25 24.960 65,145.60 6.625% Due 5/25/67 109,000 Prudential Financial, Inc. Baa3 BBB+ 6/15/18 @ 100 114.276 124,560.84 8.875% Due 6/15/38 1,970 USB Capital VII A2 BBB+ 11/18/10 @ 25 24.960 49,171.20 5.875% Due 8/15/35 2,580 USB Capital XI A2 BBB+ 9/15/11 @ 25 25.160 64,912.80 6.600% Due 9/15/66 148,000 Wells Fargo and Company - Series K Ba1 A- 3/15/18 @ 100 105.399 155,990.52 7.980% _____________

$ 3,247,113.19 _____________ _____________

See “Notes to Portfolio”.

8

Notes to Portfolio

(1) The Securities are initially represented by “regular way” contracts for the performance of which cash or an irrevocable letter ofcredit has been deposited with the Trustee. Contracts to acquire Securities were entered into on October 21, 2010 and havea settlement date of October 26, 2010 (see “The Portfolio”). Shown under this heading is the issuer name, stated incomedistribution rate of each Security expressed as a percentage of par or stated value, and scheduled maturity date of eachSecurity, if any.

(2) The value of each Security is determined on the bases set forth under “Public Offering--Unit Price” as of the close of theNew York Stock Exchange on the business day before the Initial Date of Deposit. In accordance with FASB AccountingStandards Codification (“ASC”), ASC 820, Fair Value Measurements and Disclosures, a number of the Portfolio’sinvestments may be classified as Level 1, which refers to security prices determined using quoted prices in active marketsfor identical securities. A number of the Portfolio’s investments may be classified as Level 2, which refers to securityprices determined using other significant observable inputs. Observable inputs are inputs that other market participantswould use in pricing a security. These may include quoted market prices for similar securities, interest rates, prepaymentspeeds and credit risk. Other information regarding the Securities, as of the Initial Date of Deposit, is as follows:

Profit Cost to (Loss) To Sponsor Sponsor ______________ ______________

$ 3,238,505 $ 8,608

(3) This preferred security is a restricted security that may only be resold pursuant to Rule 144A under the Securities Act of1933, as amended. See “Liquidity Risk”.

(4) “NR” indicates that the rating service did not provide a rating for that security. For a brief description of the ratings see“Description of Security Ratings” in the Information Supplement.

(5) The Securities are first redeemable on such date and at such price as listed in this column. The Securities may beredeemable at declining prices thereafter but not below the par or stated value. The Securities may be subject to optionalredemption provisions, such as a “make whole” call option which may be exercised in whole or in part at any time at theoption of the issuer, at prices of par or stated value. A “make whole” redemption price is generally equal to the sum ofthe principal amount of the Securities, a “make whole” amount, and any accrued and unpaid interest to the date ofredemption. The “make whole” amount is generally equal to the excess, if any, of (i) the aggregate present value as ofthe date of redemption of principal being redeemed and the amount of interest (exclusive of interest accrued to the dateof redemption) that would have been payable if redemption had not been made, determined by discounting theremaining principal and interest at a specified rate (which varies among particular securities and is generally equal to anaverage of yields on U.S. Treasury obligations with maturities corresponding to the remaining life of the Security plus apremium rate) from the dates on which the principal and interest would have been payable if the redemption had notbeen made, over (ii) the aggregate principal amount of the Securities being redeemed. Optional redemption provisionsgenerally will occur at times when the redeemed Securities have an offering side evaluation which represents a premiumover par or stated value. To the extent that the Securities were acquired at a price higher than the redemption price, thiswill represent a loss of capital when compared with the Public Offering Price of the Units when acquired.

Distributions to Unitholders will generally be reduced by the amount of dividends, interest payments or other incomewhich otherwise would have been paid with respect to redeemed Securities, and any principal amount received on suchredemption after satisfying any redemption requests for Units received by the Portfolio will be distributed to Unitholders.Certain of the Securities have provisions which would allow for their redemption prior to the earliest stated call datepursuant to the occurrence of certain extraordinary events, including changes in federal regulations governing the capitaltreatment of certain preferred securities (see “Preferred Securities”).

9

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Unitholders of Van Kampen Unit Trusts, Series 1049:

We have audited the accompanying statement of condition and the related portfolio of Global PreferredSecurities Portfolio, Series 1 (included in Van Kampen Unit Trusts, Series 1049) as of October 22, 2010. Thestatement of condition is the responsibility of the Sponsor. Our responsibility is to express an opinion on suchstatement of condition based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting OversightBoard (United States). Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the statement of condition is free of material misstatement. The trust is not requiredto have, nor were we engaged to perform an audit of its internal control over financial reporting. Our auditincluded consideration of internal control over financial reporting as a basis for designing audit proceduresthat are appropriate in the circumstances, but not for the purpose of expressing an opinion on theeffectiveness of the trust’s internal control over financial reporting. Accordingly, we express no such opinion.An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in thestatement of condition, assessing the accounting principles used and significant estimates made by thesponsor, as well as evaluating the overall statement of condition presentation. Our procedures includedconfirmation with The Bank of New York Mellon, Trustee, of cash or an irrevocable letter of credit depositedfor the purchase of Securities as shown in the statement of condition as of October 22, 2010. We believethat our audit of the statement of condition provides a reasonable basis for our opinion.

In our opinion, the statement of condition referred to above presents fairly, in all material respects, thefinancial position of Global Preferred Securities Portfolio, Series 1 (included in Van Kampen Unit Trusts, Series1049) as of October 22, 2010, in conformity with accounting principles generally accepted in the UnitedStates of America.

/s/ GRANT THORNTON LLP

New York, New YorkOctober 22, 2010

10

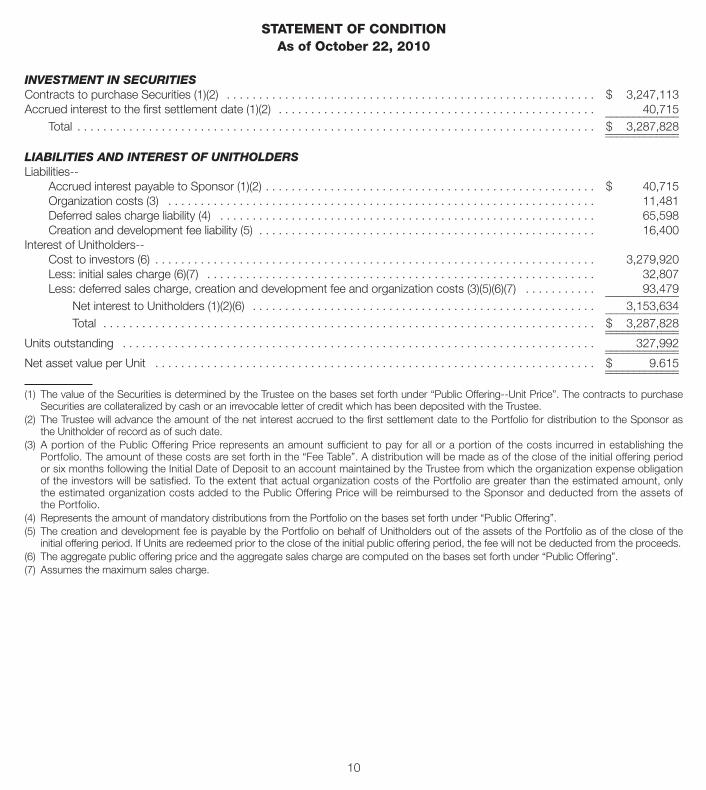

STATEMENT OF CONDITIONAs of October 22, 2010

INVESTMENT IN SECURITIESContracts to purchase Securities (1)(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 3,247,113Accrued interest to the first settlement date (1)(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40,715 _____________ Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 3,287,828 _____________ _____________

LIABILITIES AND INTEREST OF UNITHOLDERSLiabilities-- Accrued interest payable to Sponsor (1)(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 40,715 Organization costs (3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11,481 Deferred sales charge liability (4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65,598 Creation and development fee liability (5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16,400Interest of Unitholders-- Cost to investors (6) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,279,920 Less: initial sales charge (6)(7) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32,807 Less: deferred sales charge, creation and development fee and organization costs (3)(5)(6)(7) . . . . . . . . . . . 93,479 _____________ Net interest to Unitholders (1)(2)(6) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,153,634 _____________ Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 3,287,828 _____________ _____________Units outstanding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 327,992 _____________ _____________Net asset value per Unit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 9.615 _____________ _____________

(1) The value of the Securities is determined by the Trustee on the bases set forth under “Public Offering--Unit Price”. The contracts to purchaseSecurities are collateralized by cash or an irrevocable letter of credit which has been deposited with the Trustee.

(2) The Trustee will advance the amount of the net interest accrued to the first settlement date to the Portfolio for distribution to the Sponsor asthe Unitholder of record as of such date.

(3) A portion of the Public Offering Price represents an amount sufficient to pay for all or a portion of the costs incurred in establishing thePortfolio. The amount of these costs are set forth in the “Fee Table”. A distribution will be made as of the close of the initial offering periodor six months following the Initial Date of Deposit to an account maintained by the Trustee from which the organization expense obligationof the investors will be satisfied. To the extent that actual organization costs of the Portfolio are greater than the estimated amount, onlythe estimated organization costs added to the Public Offering Price will be reimbursed to the Sponsor and deducted from the assets ofthe Portfolio.

(4) Represents the amount of mandatory distributions from the Portfolio on the bases set forth under “Public Offering”.(5) The creation and development fee is payable by the Portfolio on behalf of Unitholders out of the assets of the Portfolio as of the close of the

initial offering period. If Units are redeemed prior to the close of the initial public offering period, the fee will not be deducted from the proceeds.(6) The aggregate public offering price and the aggregate sales charge are computed on the bases set forth under “Public Offering”.(7) Assumes the maximum sales charge.

THE PORTFOLIO

The Portfolio was created under the laws of the Stateof New York pursuant to a Trust Indenture and TrustAgreement (the “Trust Agreement”), dated the date ofthis prospectus (the “Initial Date of Deposit”), amongVan Kampen Funds Inc., as Sponsor, Cohen & SteersCapital Management, Inc., as Supervisor, and The Bankof New York Mellon, as Trustee.

The Portfolio offers investors the opportunity topurchase Units representing proportionate interests in aportfolio of securities. The Portfolio may be an appropriatemedium for investors who desire to participate in aportfolio of securities with greater diversification than theymight be able to acquire individually.

On the Initial Date of Deposit, the Sponsor depositeddelivery statements relating to contracts for the purchaseof the Securities and cash or an irrevocable letter ofcredit in the amount required for these purchases withthe Trustee. In exchange for these contracts, the Trusteedelivered to the Sponsor documentation evidencing theownership of Units of the Portfolio. Unless otherwiseterminated as provided in the Trust Agreement, thePortfolio will terminate on the Mandatory TerminationDate and any remaining Securities will be liquidated ordistributed by the Trustee within a reasonable time. Asused in this prospectus the term “Securities” means thesecurities (including contracts to purchase thesesecurities) listed under “Portfolio” and any additionalsecurities deposited into the Portfolio.

Additional Units of the Portfolio may be issued atany time by depositing in the Portfolio (i) additionalSecurit ies, ( i i ) contracts to purchase Securit iestogether with cash or irrevocable letters of credit or (iii)cash (or a letter of credit or the equivalent) withinstructions to purchase additional Securities. Asadditional Units are issued by the Portfol io, theaggregate value of the Securities will be increased andthe fractional undivided interest represented by eachUnit may be decreased. The Sponsor may continue tomake additional deposits into the Portfolio followingthe Initial Date of Deposit provided that the additionaldeposits will be in amounts which will maintain, asnear ly as pract icable, the same percentage

relationship among the number of shares or principalamount of each Security in the Portfolio that existedimmediately prior to the subsequent deposit. Investorsmay experience a dilution of their investments and areduction in their anticipated income because offluctuations in the prices of the Securities between thetime of the deposit and the purchase of the Securitiesand because the Portfolio will pay the associatedbrokerage or acquisit ion fees. Due to purchaserequirements in certain preferred securities markets,including limited trading volume and best pricing forround lots among other reasons, and market valuefluctuations, the Portfolio may not be able to invest ineach Security on any subsequent date of deposit inthe same proportion as existed on the Initial Date ofDeposit or immediately prior to the subsequentdeposit of Securities. This could increase the potentialfor dilution of investments and variances in anticipatedincome. Purchases and sales of Securities by yourPortfolio may impact the value of the Securities. Thismay especially be the case during the initial offering ofUnits, upon Portfolio termination and in the course ofsatisfying large Unit redemptions.

Each Unit of your Portfolio initially offered representsan undivided interest in the Portfolio. At the close of theNew York Stock Exchange on the Init ial Date ofDeposit, the number of Units may be adjusted so thatthe Public Offering Price per Unit equals $10. Thenumber of Units, fractional interest of each Unit in yourPortfolio and the estimated distributions per Unit willincrease or decrease to the extent of any adjustment.To the extent that any Units are redeemed by theTrustee or additional Units are issued as a result ofadditional Securities being deposited by the Sponsor,the fractional undivided interest in your Portfoliorepresented by each unredeemed Unit will increase ordecrease accordingly, although the actual interest inyour Portfolio will remain unchanged. Units will remainoutstanding until redeemed upon tender to the Trusteeby Unitholders, which may include the Sponsor, or untilthe termination of the Trust Agreement.

In order to acquire certain securities, it may benecessary for the Sponsor or Trustee to pay amountscovering accrued interest on the securities which exceed

A-1

A-2

the amounts which will be made available through cashfurnished by the Sponsor on the Date of Deposit. Thiscash may exceed the interest which would accrue to thefirst settlement date. The Trustee has agreed to pay forany amounts necessary to cover any excess and will bereimbursed when funds become available from interestpayments on the related securities.

The Portfolio consists of (a) the Securities (includingcontracts for the purchase thereof) l isted under“Portfolio” as may continue to be held from time to timein the Portfolio, (b) any additional Securities acquiredand held by the Portfolio pursuant to the provisions ofthe Trust Agreement and (c) any cash held in the relatedIncome and Capital Accounts. Neither the Sponsor northe Trustee shall be liable in any way for any contractfailure in any of the Securities.

OBJECTIVE AND SECURITIES SELECTION

The objective of the Portfolio is described on page 2.There is no assurance that the Portfolio will achieve itsobjective.

The Portfolio Consultant is not an affiliate of theSponsor. The Sponsor did not select the Securitiesfor the Portfolio. The Portfolio Consultant may use thelist of Securities in its independent capacity as aninvestment adviser and distribute this information tovar ious indiv iduals and ent i t ies. The Port fo l ioConsultant may recommend or effect transactions inthe Securities. This may have an adverse effect on theprices of the Securities. This also may have an impacton the price the Portfolio pays for the Securities andthe price received upon Unit redemptions or Portfoliotermination. The Portfolio Consultant may act asagent or principal in connection with the purchaseand sale of securities, including the Securities. ThePortfolio Consultant also issues reports and makesrecommendations on the Securities. The PortfolioConsultant’s research department may receivecompensation based on commissions generated byresearch and/or sales of Units.

Neither the Portfolio Consultant nor the Sponsormanage the Portfolio. You should note that the PortfolioConsultant applied the selection criteria to the Securities

for inclusion in the Portfolio prior to the Initial Date ofDeposit. After this time, the Securities may no longermeet the selection criteria. Should a Security no longermeet the selection criteria, we will generally not removethe Security from the Portfolio. In offering the Units to thepublic, neither the Sponsor nor any broker-dealers arerecommending any of the individual Securities but ratherthe entire pool of Securities in the Portfolio, taken as awhole, which are represented by the Units.

RISK FACTORS

All investments involve risk. You should understandthese risks before you invest. If the value of thesecurities falls, the value of your Units will also fall. Youcan lose money by investing in the Portfolio. No onecan guarantee that the Portfolio will achieve its objectiveor that your investment return will be positive over anyperiod. The Information Supplement, which is availableupon request, contains a more detailed discussion ofrisks related to your investment.

Preferred Securities. The Portfolio investsexclusively in preferred securities, including hybrid andtrust preferred securities. You should understand thesesecurities before you invest. Hybrid-preferred securitiesare preferred securities typically issued by corporations,generally in the form of interest-bearing notes and may beperpetual in duration or may have a stated maturity. Trustpreferred securities are similar to hybrid securities, but aretypically issued by an affiliated business trust of acorporation, generally in the form of beneficial interests insubordinated debentures or similarly structured securities.The maturity and distribution payments of the preferredsecurities generally coincide with the maturity and interestpayments on the underlying obligations. Whiledistributions received from certain preferred securities inthe Portfolio may be treated as ordinary income for federalincome tax purposes, distributions received from otherpreferred securities in the Portfolio may be designated asqualified dividend income for federal income tax purposes(see “Taxation”). The securities underlying certain preferredsecurities may be equity type securities which payperiodic dividends. The hybrid-preferred securities in thePortfolio typically feature a fixed maturity date, may deferinterest payments for up to 20 quarters without invoking a

default, and make income payments that typically are fullytaxable as interest income, rather than as dividendincome, for federal income tax purposes. Thesecurities underlying hybrid-preferred securities aretypically a type of subordinated debt instrument, suchas a note or debenture.

Preferred securities’ prices fluctuate for severalreasons including changes in investors’ perception ofthe financial condition of an issuer, the general conditionof the market for preferred securities, or when political,regulatory or economic events affecting the issuersoccur. These securities are also sensitive to interest ratefluctuations, as the cost of capital rises and borrowingcosts increase in a rising interest rate environment andthe risk that a preferred security may be called forredemption in a falling interest rate environment.

Hybrid and trust preferred securities with a statedmaturity date usually mature on the maturity date of theunderlying interest-bearing notes or subordinateddebentures and may be redeemed or liquidated prior tothe stated maturity date of such instruments for anyreason on or after their stated call date or upon theoccurrence of certain circumstances at any time. In afalling interest rate environment, a preferred securitymay be subject to increased risk of being called forearly redemption by the issuer. Certain tax or regulatoryevents may trigger the redemption of the interest-bearing notes, preferred securities or subordinateddebentures by the issuing corporation and result inprepayment of the hybrid and trust preferred securitiesprior to their stated maturity date.

The Dodd-Frank Wall Street Reform and ConsumerProtection Act (the "Dodd-Frank Act"), signed into law inJuly 2010, and other proposed regulatory changes mayhave a profound impact on preferred securities. TheDodd-Frank Act contains provisions which will makecertain hybrid and trust preferred securities lessattractive for issuing banks, which is believed to be likelyto result in a significant reduction in the issuance and,over time, availability of these types of securities andpotentially, in many outstanding issues being redeemed.These changes may negatively impact the prices ofsome securities, particularly those trading above theirpar values as the new legislation increase the possibility

of near-term redemption. Any such issuer redemptionsamong the preferred securities in the Portfolio maycause the value of your Units to decline, andfurthermore, may decrease the amount of income youmay receive on your Units. However, other securitiesmay be positively affected by potential near-termredemptions, particularly those trading at discounts topar value. Such securities may experience an increase inmarket value from issuers' redemption activity.

A longer-term consequence of the relevant provisionsof the Dodd-Frank Act, which are to be phased in over aperiod of a few years, is the potential for some types ofpreferred securities in which the Portfolio invests tobecome more scarce and potentially less liquid. Inaddition, proposals of the Basel Committee on BankingSupervision (“Basel Committee”) to update capitalrequirements for banks globally, if finalized and adopted inthe United States, would further limit the attractiveness toissuing banks of a broader range of preferred securitytypes and possibly have more significant consequences,including a smaller market of issues and less liquidity. It isnot possible to predict the impact of the Dodd-Frank Actor Basel Committee proposals on the Portfolio.

Hybrid and trust preferred securit ies are alsosubject to unique risks which include the fact thatdistributions will only be paid by a preferred security ifthe interest payments on the underlying obligations aremade, which interest payments are dependent on thefinancial condition of the issuer and, in certain cases,may be subject to deferral. During any deferral period,the Portfolio may have to recognize income as if thePortfolio had received current interest payments. Insuch a case, the Portfolio will be required to satisfydistribution requirements based on such income eventhough it would not have received cash with which topay such distributions. In addition, the underlyingobligations, and thus the hybrid and trust preferredsecurities, may be pre-paid after a stated call date oras a result of certa in tax or regulatory events.Preferred securities are typically subordinated tobonds and other debt instruments in a company’scapital structure, in terms of priority to corporateincome, and therefore will be subject to greater creditrisk than those debt instruments.

A-3

Certain of the preferred securities in the Portfolio offera fixed rate coupon through a particular future date,after which the rate is reset to a floating coupon rate.The coupon rates on any such securit ies in thePortfolio, however, are not scheduled to reset during thelife of the Portfolio, and will remain fixed for the durationof the Portfolio. Unlike the other securities in thePortfolio, these particular preferred securities are tradedover-the-counter, and the Trustee will evaluate thesesecurities using only the prices supplied by Standard &Poor’s Securities Evaluations (the “pricing service”).

Market Risk. Market risk is the risk that the value ofthe securities in the Portfolio will fluctuate. This couldcause the value of your Units to fall below your originalpurchase price or below the par value. Market valuefluctuates in response to various factors. These caninclude changes in interest rates, inflation, the financialcondition of a security’s issuer, perceptions of the issueror insurer, or ratings on a security. Even though theSupervisor supervises your Portfolio, you shouldremember that no one manages your Portfolio. ThePortfolio will not sell a security solely because themarket value falls as is possible in a managed fund.

Interest Rate Risk. Interest rate risk is the risk thatsecurities in the Portfolio will decline in value because ofa rise in interest rates. Generally, securities that payfixed rates of return will increase in value when interestrates decline and decrease in value when interest ratesrise. Typically, securities that pay fixed rates of returnwith longer periods before maturity are more sensitive tointerest rate changes.

Credit and Distribution Payment Risk. Creditand distribution payment risk is the risk that an issuer ofa security in the Portfolio is unable or unwilling to makedividend, interest and/or principal payments. Thepreferred securities in the Portfolio are subject to uniquerisks which include the fact that distributions will only bepaid by the security if interest payments on theunderlying obl igations are made. Such interestpayments are dependent on the financial condition ofthe issuer. Distributions for certain preferred securitiesmay not be paid at all or, in certain cases, may bedeferred without default. If distributions received by thePortfolio are insufficient to cover expenses, redemptions

or other Portfolio costs, it may be necessary for thePortfolio to sell Securities to cover such expenses,redemptions or other costs. Any such sales may resultin capital gains or losses to you. See “Taxation”.

Call Risk. Call risk is the risk that the issuer prepays or“calls” a security before its stated maturity. An issuer mightcall a security if interest rates fall and the security pays ahigher interest rate or if it no longer needs the money forthe original purpose. If an issuer calls a security, thePortfolio will distribute the principal to you but your futureincome distributions will fall. The Portfolio does not offerreinvestment of distributions into additional Units, andconsequently, you might not be able to reinvest thisprincipal at as high a yield. A security’s call price could beless than the price the Portfolio paid for the security andcould be below the security’s par value. This means thatyou could receive less than the amount you paid for yourUnits. If enough securities in the Portfolio are called, thePortfolio could terminate early. Some or all of thesecurities may also be subject to extraordinary optional ormandatory redemptions if certain events occur, such ascertain changes in tax laws, the substantial damage ordestruction by fire or other casualty of the project forwhich the proceeds of the securities were used, andvarious other events. The call provisions are described ingeneral terms in the “Portfolio” under “RedemptionProvisions”.

Liquidity Risk. Liquidity risk is the risk that the valueof a security will fall if trading in the security is limited orabsent. In particular, certain securities in the Portfolio are“Rule 144A” restricted securities pursuant to theSecurities Act of 1933, as amended (“1933 Act”), andmay be subject to enhanced liquidity risk. Rule 144Asecurities are restricted securities that may only be resoldin accordance with the applicable provisions of the 1933Act. Rule 144A establishes a “safe harbor” from theregistration requirements of the 1933 Act for resale ofcertain securities to qualified institutional buyers.

Restricted securities may be sold only in privatelynegotiated transactions or in a public offering withrespect to a registration statement which is in effectunder the 1933 Act. The restricted securities in thePortfolio may not be readily marketable at the time thePortfolio may be seeking to sell such securities, such as

A-4

for a request for redemption. An insufficient number ofqualified institutional buyers interested in purchasingrestricted securities held by the Portfolio may adverselyaffect the marketability of such securities, and theTrustee might be unable to dispose of such Portfoliosecurities promptly or at reasonable prices. Whereregistration is required for the resale of a restrictedsecurity, the Portfolio may be obligated to pay all or partof the registration expenses and a considerable periodmay elapse from the time the Trustee attempts to sellsuch restricted Portfolio securities and the time theTrustee may be permitted to sell the restricted Portfoliosecurities under an effective registration statement. Dueto the potential for delays on resale and uncertainty invaluation associated with restricted securities, theTrustee may experience difficulty satisfying redemptionswithin seven days.

Whether or not the securities in the Portfolio arelisted on an exchange, the securities may delist fromthe exchange or principally trade in an over-the-counter market. As a result, the existence of a liquidtrading market could depend on whether dealers willmake a market in the securities. We cannot guaranteethat dealers will maintain a market or that a liquidtrading market will exist for any security. The value ofthe securities could fall if trading markets are limitedor absent.

Financial Services Issuers. The Portfolio investsexclusively in the preferred securities of financialservices companies or related subsidiaries. Anynegative impact on this industry will have a greaterimpact on the value of Units than on a portfoliodiversif ied over several industr ies. You shouldunderstand the risks of this industry before you invest.

The effects of the global financial crisis that began tounfold in 2007 continue to manifest in nearly all thesub-divisions of the financial services industry. Financiallosses and write downs among investment banks andsimilar institutions reached significant levels in 2008. Theimpact of these losses among traditional banks,investment banks, broker/dealers and insurers has forceda number of large such institutions into either liquidation orcombination, while drastically increasing the credit risk,and possibility of default, of bonds issued by such

institutions faced with these troubles. Many of theinstitutions are having difficulty in accessing credit marketsto finance their operations and in maintaining appropriatelevels of equity capital. In some cases, U.S. and foreigngovernments have acted to bail out or provide support toselect institutions, however the risk of default by suchissuers has nonetheless increased substantially.

In response to the financial crisis, the Dodd-FrankAct was enacted into federal law in large part to provideincreased regulation of financial institutions. The Dodd-Frank Act includes significant reforms and refinementsto modernize existing laws to address emerging risksand issues in the nation’s evolving financial system. Italso establishes entirely new regulatory regimes,including in areas such as systemic risk regulation, over-the-counter derivatives market oversight, and federalconsumer protection.

The Dodd-Frank Act will have broad impact onvirtually all participants in the financial services industryfor years to come, including banks, thrifts, depositoryinstitution holding companies, mortgage lenders,insurance companies, industrial loan companies, broker-dealers and other securities and investment advisoryfirms, private equity and hedge funds, consumers, andnumerous federal agencies and the federal regulatorystructure. These regulatory changes may have adverseeffects on certain issuers in your Portfolio, such asdecreased profits or revenues. The Sponsor is unable topredict the ultimate impact of the Dodd-Frank Act, andany resulting regulation, on the securities in your Portfolioor on the financial services industry in general.

While the U.S. and foreign governments, and theirrespective government agencies, have taken steps toaddress problems in the financial markets and withfinancial institutions, there can be no assurance thatthe risks associated with investment in financialservices company issuers will decrease as a result ofthese steps.

The Portfolio invests significantly in banks. Banks andtheir holding companies are especially subject to theadverse effects of economic recession; volatile interestrates; portfolio concentrations in geographic markets andin commercial and residential real estate loans; and

A-5

competition from new entrants in their fields of business.In addition, banks and their holding companies areextensively regulated at both the federal and state leveland may be adversely affected by increased regulation.Economic conditions in the real estate markets havedeteriorated and have had a substantial negative effectupon banks because they generally have a portion of theirassets invested in loans secured by real estate.

Banks are highly dependent on net interest margin.Bank profitability is largely dependent on the availabilityand cost of capital funds, and can fluctuate significantlywhen interest rates change or due to increasedcompetition. Banks had received significant consumermortgage fee income as a result of activity in mortgageand refinance markets. As initial home purchasing andrefinancing activity subsided as a result of increasinginterest rates and other factors, this income diminished.Banks and their holding companies are subject toextensive federal regulation and, when such institutionsare state-chartered, to state regulation as well. Suchregulations impose strict capital requirements andlimitations on the nature and extent of businessactivities that banks may pursue. Furthermore, bankregulators have a wide range of discretion in connectionwith their supervisory and enforcement authority andmay substantially restrict the permissible activities of aparticular institution if deemed to pose significant risksto the soundness of such institution or the safety of thefederal deposit insurance fund. Regulatory actions,such as increases in the minimum capital requirementsapplicable to banks and increases in deposit insurancepremiums required to be paid by banks and thrifts tothe Federal Deposit Insurance Corporation (“FDIC”), cannegatively impact earnings and the ability of a companyto pay dividends or make interest payments. Neitherfederal insurance of deposits nor governmentalregulations, however, insures the solvency or profitabilityof banks or their holding companies, or insures againstany risk of investment in the securities issued by suchinstitutions.

Banks face competition from nontraditional lendingsources as regulatory changes have permitted newentrants to offer various f inancial products.Technological advances such as the Internet allow

these nontraditional lending sources to cut overheadand permit the more efficient use of customer data.Banks continue to face tremendous pressure frommutual funds, brokerage firms and other financialservice providers in the competition to furnish servicesthat were traditionally offered by banks.

Companies involved in the insurance, reinsurance andrisk management industry underwrite, sell or distributeproperty, casualty and business insurance. Many factorsaffect insurance, reinsurance and risk managementcompany profits, including interest rate movements, theimposition of premium rate caps, a misapprehension ofthe risks involved in given underwritings, competition andpressure to compete globally, weather catastrophes orother disasters and the effects of client mergers. Alreadyextensively regulated, insurance companies’ profits maybe adversely affected by increased governmentregulations or tax law changes.

Companies engaged in investment management andbroker-dealer activities are subject to volatility in theirearnings and share prices that often exceeds the volatilityof the equity market in general. Adverse changes in thedirection of the stock market, investor confidence, equitytransaction volume, the level and direction of interest ratesand the outlook of emerging markets could adverselyaffect the financial stability, as well as the security prices,of these companies. Additionally, competitive pressures,including increased competition with new and existingcompetitors, the ongoing commoditization of traditionalbusinesses and the need for increased capitalexpenditures on new technology could adversely impactthe profit margins of companies in the investmentmanagement and brokerage industries. Companiesinvolved in investment management and broker-dealeractivities are also subject to extensive regulation bygovernment agencies and self-regulatory organizations,and changes in laws, regulations or rules, or in theinterpretation of such laws, regulations and rules couldadversely affect the security prices of such companies.

High-Yield Security Risk. Certain of the preferredsecurities held by your Portfolio are high-yield securitiesor unrated securities. High-yield, high risk securities aresubject to greater market fluctuations and risk of lossthan securities with higher investment ratings. The value

A-6

of these securit ies wil l decline signif icantly withincreases in interest rates, not only because increasesin rates generally decrease values, but also becauseincreased rates may indicate an economic slowdown.An economic slowdown, or a reduction in an issuer’screditworthiness, may result in the issuer being unableto maintain earnings at a level sufficient to maintaininterest and principal payments.

High-yield or “junk” securities, the generic names forsecurities rated below “BBB” by Standard & Poor’s or“Baa” by Moody’s, are frequently issued by corporationsin the growth stage of their development or byestablished companies who are highly leveraged orwhose operations or industr ies are depressed.Securities rated below BBB or Baa are consideredspeculative as these ratings indicate a quality of lessthan investment grade. Because high-yield securitiesare general ly subordinated obl igations and areperceived by investors to be riskier than higher ratedsecurities, their prices tend to fluctuate more thanhigher rated securities and are affected by short-termcredit developments to a greater degree.

The market for high-yield securities is smaller andless liquid than that for investment grade securities.High-yield securities are generally not listed on anational securit ies exchange but trade in theover-the-counter markets. Due to the smaller, less liquidmarket for high-yield securities, the bid-offer spread onsuch securities is generally greater than it is forinvestment grade securities and the purchase or sale ofsuch securities may take longer to complete.

Foreign Securities. Because the Portfolio investssignificantly in foreign securities, the Portfolio involvesadditional risks that differ from an investment indomestic securities. These risks include the risk oflosses due to future pol it ical and economicdevelopments, international trade conditions, foreignwithholding taxes and restr ict ions on foreigninvestments or exchange of securities, foreign currencyfluctuations or restriction on exchange or repatriation ofcurrencies.

The political, economic and social structures of someforeign countries may be less stable and more volatile

than those in the U.S. Investments in these countries maybe subject to the risks of internal and external conflicts,currency devaluations, foreign ownership limitations andtax increases. It is possible that a government may takeover the assets or operations of a company or imposerestrictions on the exchange or export of currency or otherassets. Some countries also may have different legalsystems that may make it difficult for the Portfolio to voteproxies, exercise investor rights, and pursue legalremedies with respect to its foreign investments.Diplomatic and political developments, including rapid andadverse political changes, social instability, regionalconflicts, terrorism and war, could affect the economies,industries, and securities and currency markets, and thevalue of the Portfolio’s investments, in non-U.S. countries.No one can predict the impact that these factors couldhave on the Portfolio’s securities.

The purchase and sale of the foreign securities mayoccur in foreign securities markets. Certain of the factorsstated above may make it impossible to buy or sell themin a timely manner or may adversely affect the valuereceived on a sale of securities. Custody of certain of thesecurities in the Portfolio may be maintained by a globalcustody and clearing institution which has entered into asub-custodian relationship with the Trustee. In addition,round lot trading requirements exist in certain foreignsecurities markets. These round lot trading requirementscould cause the proportional composit ion anddiversification of the Portfolio’s securities to vary whenthe Portfolio purchases additional securities or sellssecurities to satisfy expenses or Unit redemptions. Thiscould have a material impact on investmentperformance and portfolio composition. Brokeragecommissions and other fees generally are higher forforeign securit ies. Government supervision andregulation of foreign securities markets, currencymarkets, trading systems and brokers may be less thanin the U.S. The procedures and rules governing foreigntransactions and custody (holding of the Portfolio’sassets) also may involve delays in payment, delivery orrecovery of money or investments.

Foreign companies may not be subject to the samedisclosure, accounting, auditing and financial reportingstandards and practices as U.S. companies. Thus,

A-7

there may be less information publicly available aboutforeign companies than about most U.S. companies.

Certain foreign securities may be less liquid (harderto sell) and more volatile than many U.S. securities.This means the Portfolio may at times be unable tosel l foreign secur i t ies in a t imely manner or atfavorable prices. See “Liquidity Risk”.

Because securities of foreign issuers not listed on aU.S. securities exchange generally pay dividends andtrade in foreign currencies, the U.S. dollar value of thesesecurities and dividends will vary with fluctuations inforeign exchange rates. Most foreign currencies havefluctuated widely in value against the U.S. dollar forvarious economic and political reasons. To determinethe value of foreign securities or their dividends, theTrustee will estimate current exchange rates for therelevant currencies based on activity in the variouscurrency exchange markets. However, these marketscan be quite volatile depending on the activity of thelarge international commercial banks, various centralbanks, large multi-national corporations, speculatorsand other buyers and sellers of foreign currencies.Since actual foreign currency transactions may not beinstantly reported, the exchange rates estimated by theTrustee may not reflect the amount the Portfolio wouldreceive in U.S. dollars, had the Trustee sold anyparticular currency in the market. The value of theSecurities in terms of U.S. dollars, and therefore thevalue of your Units, will decline if the U.S. dollardecreases in value relative to the value of the currenciesin which the Securities trade.

Additional Units. The Sponsor may createadditional Units of the Portfolio by depositing into thePortfolio additional securities or cash with instructionsto purchase additional securities. Some of the securitiesheld by your Portfolio may have limited trading volume.The Trustee, with directions from the Sponsor, willendeavor to purchase securities with deposited cash assoon as practicable, reserving the right to purchasethose securities over several business days followingeach deposit in an effort to reduce the effect of thesepurchases on the market price for those securities. Tothe extent the price of a security increases or decreasesbetween the time cash is deposited with instructions to

purchase the security and the time cash is used topurchase the security, Units may represent less or moreof that security and more or less of the other securitiesin the Portfolio. This could result in the Portfolio’s failureto participate in any appreciation of certain securitiesbefore the cash is fully invested.

Reduced Diversification. The Portfolio involvesthe risk that the Portfolio will become smaller and lessdiversified as securities are sold, are called or mature.This could increase your risk of loss and increase yourshare of Portfolio expenses.

Quality Risk. Security quality risk is the risk that asecurity will fall in value if a rating agency decreases thesecurity’s rating.

Tax and Legislation Risk. Tax legislation proposedby the President or Congress, tax regulations proposedby the U.S. Treasury or positions taken by the InternalRevenue Service could affect the value of the trust bychanging the taxation or tax characterizations of theportfolio securities, or other income paid by or related tosuch securities. Congress has considered such proposalsin the past and may do so in the future. No one canpredict whether any legislation will be proposed, adoptedor amended by Congress and no one can predict theimpact that any other legislation might have on thePortfolio or its portfolio securities, or on the tax treatmentof your Portfolio or of your investment in the Portfolio.

No FDIC Guarantee. An investment in yourPortfolio is not a deposit of any bank and is not insuredor guaranteed by the Federal Deposit InsuranceCorporation or any other government agency.

PUBLIC OFFERING

General. Units are offered at the Public OfferingPrice which consists of the net asset value per Unit plusorganization costs plus the sales charge. The net assetvalue per Unit is the value of the securities, cash, anyaccrued interest, and other assets in your Portfolioreduced by the liabilities of the Portfolio divided by thetotal Units outstanding. The maximum sales chargeequals 3.50% of the Public Offering Price per Unit(3.63% of the aggregate offering price of the Securities)at the time of purchase.

A-8

You pay the initial sales charge at the time you buyUnits. The initial sales charge is the difference betweenthe total sales charge percentage (maximum of 3.50%of the Public Offering Price per Unit) and the sum of theremaining fixed dollar deferred sales charge and thetotal fixed dollar creation and development fee. Theinitial sales charge will be approximately 1.00% of thePublic Offering Price per Unit depending on the PublicOffering Price per Unit. The deferred sales charge isfixed at $0.200 per Unit. Your Portfolio pays thedeferred sales charge in installments as described in the“Fee Table”. If any deferred sales charge payment dateis not a business day, we will charge the payment onthe next business day. If you purchase Units after theinitial deferred sales charge payment, you will only paythat portion of the payments not yet collected. If youredeem or sell your Units prior to collection of the totaldeferred sales charge, you will pay any remainingdeferred sales charge upon redemption or sale of yourUnits. The initial and deferred sales charges are referredto as the “transactional sales charge”. The transactionalsales charge does not include the creation anddevelopment fee which compensates the Sponsor forcreating and developing your Portfolio and is describedunder “Expenses”. The creation and development fee isfixed at $0.05 per Unit. Your Portfolio pays the creationand development fee as of the close of the initialoffering period as described in the “Fee Table”. If youredeem or sell your Units prior to collection of thecreation and development fee, you will not pay thecreation and development fee upon redemption or saleof your Units. Because the deferred sales charge andcreation and development fee are fixed dollar amountsper Unit, the actual charges wil l exceed thepercentages shown in the “Fee Table” if the PublicOffering Price per Unit falls below $10 and will be lessthan the percentages shown in the “Fee Table” if thePublic Offering Price per Unit exceeds $10. In no eventwill the maximum total sales charge exceed 3.50% ofthe Public Offering Price per Unit.

Since the deferred sales charge and creation anddevelopment fee are fixed dollar amounts per Unit, yourPortfolio must charge these amounts per Unit regardlessof any decrease in net asset value. However, if the Public

Offering Price per Unit falls to the extent that themaximum sales charge percentage results in a dollaramount that is less than the combined fixed dollaramounts of the deferred sales charge and creation anddevelopment fee, your initial sales charge will be a creditequal to the amount by which these fixed dollar chargesexceed your sales charge at the time you buy Units. Insuch a situation, the value of securities per Unit wouldexceed the Public Offering Price per Unit by the amount ofthe initial sales charge credit and the value of thosesecurities will fluctuate, which could result in a benefit ordetriment to Unitholders that purchase Units at that price.The initial sales charge credit is paid by the Sponsor andis not paid by the Portfolio. The “Fee Table” shows thesales charge calculation at a $10 Public Offering Price perUnit and the following examples illustrate the sales chargeat prices below and above $10.

If the Public Offering Price per Unit fell to $7, themaximum sales charge would be $0.245 (3.50% of thePublic Offering Price per Unit), which consists of an initialsales charge of -$0.005, a deferred sales charge of$0.200 and a creation and development fee of $0.05. Ifthe Public Offering Price per Unit rose to $13, themaximum sales charge would be $0.455 (3.50% of thePublic Offering Price per Unit), consisting of an initial salescharge of $0.205, a deferred sales charge of $0.200 andthe creation and development fee of $0.05.

Beginning on October 22, 2011, the secondarymarket sales charge will be 3.00% and will not includedeferred payments. The actual sales charge that maybe paid by an investor may differ slightly from the salescharges shown herein due to rounding that occurs inthe calculation of the Public Offering Price and in thenumber of Units purchased.

The minimum purchase is 100 Units (25 Units forretirement accounts) but may vary by selling firm.Certain broker-dealers or selling firms may charge anorder handling fee for processing Unit purchases.

Reducing Your Sales Charge. The Sponsor offersa variety of ways for you to reduce the sales charge thatyou pay. It is your financial professional’s responsibility toalert the Sponsor of any discount when you purchaseUnits. Before you purchase Units you must also inform

A-9

your financial professional of your qualification for anydiscount or of any combined purchases to be eligible for areduced sales charge. You may not combine discounts.Since the deferred sales charge and creation anddevelopment fee are fixed dollar amounts per Unit, yourPortfolio must charge these amounts per Unit regardlessof any discounts. However, if you are eligible to receive adiscount such that your total sales charge is less than thefixed dollar amounts of the deferred sales charge andcreation and development fee, you will receive a creditequal to the difference between your total sales chargeand these fixed dollar charges at the time you buy Units.

Large Quantity Purchases. You can reduce yoursales charge by increasing the size of your investment.If you purchase the amount of Units of the Portfolioshown in the table below during the initial offeringperiod, the sales charge will be as follows:

Transaction SalesAmount Charge______________ ____________

Less than $50,000 . . . . . . . . . . . . . . . . . . . 3.50%$50,000 - $99,999 . . . . . . . . . . . . . . . . . . 3.25$100,000 - $249,999 . . . . . . . . . . . . . . . . . 3.00$250,000 - $499,999 . . . . . . . . . . . . . . . . 2.75$500,000 - $999,999 . . . . . . . . . . . . . . . . 2.50$1,000,000 or more . . . . . . . . . . . . . . . . . 1.55

Except as described below, these quantity discountlevels apply only to purchases of a single Portfolio madeby the same person on a single day from a singlebroker-dealer. We apply these sales charges as apercent of the Public Offering Price per Unit at the timeof purchase. We also apply the different purchase levelson a Unit basis using a $10 Unit equivalent. Forexample, if you purchase between 5,000 and 9,999Units of the Portfolio, your sales charge will be 3.25% ofyour Public Offering Price per Unit.

For purposes of achieving these levels you maycombine purchases of Units of the Portfolio withpurchases of units of any other Van Kampen-sponsoredunit investment trust in the initial offering period whichare not already subject to a reduced sales charge. Inaddition, Units purchased in the name of your spouseor children under 21 living in the same household asyou will be deemed to be additional purchases by you

for the purposes of calculating the applicable quantitydiscount level. The reduced sales charge levels will alsobe applicable to a trustee or other fiduciary purchasingUnits for a single trust, estate (including multiple trustscreated under a single estate) or fiduciary account. Tobe el igible for aggregation as described in thisparagraph, all purchases must be made on the sameday through a single broker-dealer or selling agent. Youmust inform your broker-dealer of any combinedpurchases before your purchase to be eligible for areduced sales charge.

Fee Accounts. Investors may purchase Units throughregistered investment advisers, certified financialplanners and registered broker-dealers who in eachcase either charge periodic fees for brokerage services,f inancial planning, investment advisory or assetmanagement services, or provide such services inconnection with the establishment of an investmentaccount for which a comprehensive “wrap fee” charge(“Wrap Fee”) is imposed (“Fee Accounts”). If Units of thePortfolio are purchased for a Fee Account and thePortfolio is subject to a Wrap Fee (i.e., the Portfolio is“Wrap Fee Eligible”), then the purchase will not besubject to the transactional sales charge but will besubject to the creation and development fee that isretained by the Sponsor. Please refer to the sectioncalled “Fee Accounts” for additional information onthese purchases. The Sponsor reserves the right to limitor deny purchases of Units described in this paragraphby investors or selling firms whose frequent tradingactivity is determined to be detrimental to the Portfolio.

Rollovers and Exchanges. During the initial offeringperiod of the Portfol io, unitholders of any VanKampen-sponsored unit investment trusts andunitholders of unaffiliated unit investment trusts mayutilize their redemption or termination proceeds fromsuch a trust to purchase Units of the Portfolio offered inthis prospectus at the Public Offering Price per Unit less1.00%. In order to be eligible for the sales chargediscounts applicable to Unit purchases made withredemption or termination proceeds from other unitinvestment trusts, the termination or redemptionproceeds used to purchase Units of the Portfolio mustbe derived from a transaction that occurred within 30

A-10

days of your Unit purchase. In addition, the discountswill only be available for investors that utilize the samebroker-dealer (or a different broker-dealer withappropriate notification) for both the Unit purchase andthe transaction resulting in the receipt of the terminationor redemption proceeds used for the Unit purchase.You may be required to provide appropriatedocumentation or other information to yourbroker-dealer to evidence your eligibility for thesereduced sales charge discounts. An exchange does notavoid a taxable event on the redemption or terminationof an interest in a trust.

Employees. Employees, officers and directors(including their spouses and children under 21 living inthe same household, and trustees, custodians orfiduciaries for the benefit of such persons) of VanKampen Funds Inc. and its affiliates, and dealers andtheir affiliates may purchase Units at the Public OfferingPrice less the applicable dealer concession. Al lemployee discounts are subject to the policies of therelated selling firm. Only employees, officers anddirectors of companies that allow their employees toparticipate in this employee discount program areeligible for the discounts.

Unit Price. The Public Offering Price of Units willvary from the amounts stated under “EssentialInformation” in accordance with fluctuations in theprices of the underlying Securities in the Portfolio. Theinitial price of the Securities upon deposit by theSponsor was determined by the Trustee, utilizing pricesreceived from the pricing service in connection withPortfolio securities which are traded over-the-counter.The Trustee will generally determine the value of theSecurities as of the Evaluation Time on each businessday and will adjust the Public Offering Price of Unitsaccordingly. The Evaluation Time is the close of theNew York Stock Exchange on each business day. Theterm “business day”, as used herein and under “Rightsof Unitholders--Redemption of Units”, means any dayon which the New York Stock Exchange is open forregular trading. The Public Offering Price per Unit willbe effect ive for al l orders received pr ior to theEvaluation Time on each business day. Orders receivedby the Sponsor prior to the Evaluation Time and orders