Embed Size (px)

Citation preview

Global Research

October 2008

Equities

Saudi International Petrochemical Co. (SIPCHEM)Saud

i Arab

ia

Crystallizing Growth

Global Investment House KSCCSharq, Global TowerP.O. Box 28807 Safat13149 KuwaitTel: (965) 2295 1000Fax: (965) 2295 1005E-mail: [email protected]://www.globalinv.net

Global Investment House stock market indices can be accessedfrom the Bloomberg page GLOHand from Reuters Page GLOB

Omar M. El-Quqa, CFAExecutive Vice [email protected] No:(965) 2295 1110

Faisal Hasan, CFAHead of [email protected] No:(965) 22951270

Syed Taimure AkhtarFinancial [email protected] No:(965) 22951278

Hettish KumarFinancial [email protected] No:(965) 22951281

Global Research - Saudi Arabia Global Investment House

�Saudi International Petrochemical Company - SIPCHEMOctober 2008

Tickers:SIPCHEM AB (Bloomberg)2310.SE (Reuters)

Listing:Saudi Stock Exchange (Tadawul)

Current Price:SR22.5 (18th October 2008)

October 2008

BUY

Saudi International Petrochemical Company (SIPCHEM)

Investment Summary

- Saudi International Petrochemical Company (SIPCHEM) was registered as a joint stock company in the Kingdom of Saudi Arabia on 22nd December 1999 and got its commercial license on 6th February, 2000. The principle activity of the Company is to own, establish, operate and manage industrial projects in the petrochemical and chemical fields. The Company had started its commercial operations with the manufacturing of three products Methanol, Malice anhydride-Ma and Butanediol-BDO. However, the Company is in the process of enhancing its manufacturing capabilities, mainly in chemical products.

- SIPCHEM went public following an initial public offer (IPO) and got listed on Saudi Stock Exchange (Tadawul) in November 2006. The Company, after approval from Capital Market Authority (CMA), issued 45mn shares at SR55 per share. By the end of 2006, a major portion of the Company’s shares were held by the general public, which accounted for 47.2%.

- SIPCHEM has a total of 6 affiliates, out of which, at present, only two affiliates are under operations. However, the remaining three are under developmental process while the other one is related to the marketing and distribution of chemicals and petrochemical products. Based on the current product range, methanol is the only petrochemical product of the Company, which is categorized under oxygenate products. The remaining products of the Company are (i) Butanediol-BDO and (ii) Maleic Anhydride-Ma. However, after the completion of new production lines of its new affiliates; the product range of the Company will expand to the other chemicals, which includes (i) Vinyl acetate monomer-VAM and (ii) Acetic Acid-AA along with the other olefins products like ethylene, propylene and polymers. Moreover, during 2007, the existing capacity of methanol production accounts for 89.5%, while the remainder capacity is allocated for the production of BDO and Ma, which comprise 4.5% and 6.1% of the total capacity respectively.

- According to the management of SIPCHEM, the completion of Acetyl complex is expected in mid 2009 and we have taken the production commencement from 3Q2009. In order to finance the project, the Company has issued 66.5% right shares at a premium of SR5 per share. Acetyl complexes comprise of three companies i.e. (i) International Acetyl Complex-IAC, from where SIPCHEM will get 400,000 tons of acetate acid-AA and 50,000 tons of AAn, (ii) International Vinyl Acetate Company-IVAC, which will produce 300,000 tons of vinyl acetate monomer-VAM & consume 80% production of IAC and

Global Research - Saudi Arabia Global Investment House

2 October 2008Saudi International Petrochemical Company - SIPCHEM

-5.0

10.015.020.025.030.035.040.045.050.0

-

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0

12,000.0

SIPCHEM TASI

Jan-0

7

Feb

-07

Mar

-07

Apr-

07

May

-07

Jun-0

7

Jul-

07

Aug-0

7

Sep

-07

Oct

-07

Nov-0

7

Dec

-07

Jan-0

8

Feb

-08

Mar

-08

Apr-

08

May

-08

Jun-0

8

Jul-

08

Aug-0

8

Sep

-08

Oct

-08

Mar

ket

Pri

ce (

SR

)

TA

SI

(iii) International Gas Companies-IGC to produce carbon monoxide-CO. Furthermore, these complexes are very well integrated with each other and with methanol producing plant. This will result in an improvement in the gross margins (excluding depreciation) of the Company, going forward.

- Upon the completion of the Acetyl complex in 3Q2009, the management has a plan to set up polyolefin complex, which is designed to produce 1.3mn tins of ethylene and propylene with the capacity to produce 800,000 tons of polymers. The status of the project is still unclear.

- We expect the sales revenue of SIPCHEM to show a growth of 19.7% in 2008 over the sales revenues of SR1.5bn in 2007. The growth in sale revenues is expected to continue in 2009 and is forecasted to be up by 11.1% to reach at SR2.0bn in 2009, which is mainly due to the expected commencement of production from Acetyl complex in 3Q2009. Furthermore, the growth in 2008 & 2009 sales revenue will increase at a CAGR of 12.5%, during 2007-11, while the bottom line is expected to increase at a CAGR of 10.1%, during 2007-11.

- We valued SIPCHEM using the weighted average valuation approach, with an 80% weight to the DCF technique and 20% to value derived from the relative valuation technique. Based on the weighted average valuation approach, we have reached a fair value for SIPCHEM of SR35.3. The current market price of SR22.5 per share as of 18th October 2008, offers a potential upside of 56.4%. We, therefore, initiate our coverage of SPICHEM with a “BUY” recommendation.

Table 01: Investment Indicators

CMP (SR)Shares in issue

(mn)

Market Cap

(SR mn)

52-week price range

(SR)

22.55* 333.3 7,517 50.99 / 19.75

YearRevenues Net Profit EPS BVPS ROE P/E P/BV

(SR Mn) (SR Mn) (SR) (SR) (%) (x) (x)

2009E 2,031.1 658.0 2.0 16.1 10.7 11.4 1.4

2008E 1,828.3 611.2 1.8 15.5 12.3 12.3 1.5

2007A 1,527.7 594.0 1.8 15.7 17.3% 24.7 2.8

2006A 1,334.0 493.7 1.5 14.4 18.6% 15.9 1.6

Source: Annual Reports and Global Research *Historical P/E & P/BV multiples pertain to respective year-end prices, while those for future years are based on closing prices on the Tadawul as of 18th October, 2008.

Chart 01: Share Price Performance Chart

Source: Zawya & Global Research

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM �

Company Overview

BackgroundSaudi International Petrochemicals Company was registered as a joint stock company in the Kingdom of Saudi Arabia on 22nd December 1999 and got its commercial license on 6th February, 2000. At present, the Company has a paid-up capital of SR3.3bn (US$880mn). SIPCHEM actively develops and invests in petrochemical and chemical industries, both basic and intermediate, to produce chemicals used to manufacture a multitude of products that improve the lives of people worldwide. Moreover, the principle activity of the Company is to own, establish, operate and manage industrial projects in the petrochemical and chemical fields. The Company had started its commercial operation with the manufacturing of three products Methanol, Malice anhydride-Ma and butanediol-BDO.

The Company has a total of 6 affiliates, out of which only two affiliates are under manufacturing operations. At present, however, 3 are under developmental process while one is related to the marketing and distribution of chemicals and petrochemical products. Based on the current product range, methanol is the only petrochemical product of the Company, which is categorized under oxygenate products. The remaining products of the Company are (i) BDO and (ii) Ma. However, after the completion of new production facilities of it affiliates’ the product range of the Company will expand to the other chemicals, to include (i) VAM and (ii) AA and other olefins products.

Table 02: Designed Production Capacities

Tons 2006 2007 2008E 2009E 2010E 2011E

Methanol 691,600 691,600 650,000 650,000 650,000 650,000

Butanediol 24,899 34,619 40,433 40,433 40,433 40,433

Malice Anhydride 46,772 46,772 56,126 56,126 56,126 56,126

Acetic Acid + Acetic Anhydride - - - 187,500* 375,000 375,000

Vinyl Acetate Monomer - - - 123,750* 247,500 247,500

Carbon Monoxide - - - 127,500* 255,000 255,000

Total 763,270 772,990 746,558 1,185,308 1,624,058 1,624,058

Source: APPC & Global Research*Six months production from Acetyl Complex

In order to attain sustainable growth, the Company, in 2H2006, started construction of a major Acetyls Complex which consisted of an Acetic Acid plant (450,000 tons of AA & AAn), Vinyl Acetate Monomer plant (300,000 tons) and Carbon Monoxide plant (330,000 tons). The complex is expected to commence production by 3Q2008. In addition, the Company is also developing an integrated olefins derivatives complex which will consist of nine plants producing value-added performance chemicals with a production capacity of 1.3mn tons of ethylene and propylene, which will be used to produce 800,000 tons of polymers. The SR 20 billion project is scheduled to start in 2013-14.

Global Research - Saudi Arabia Global Investment House

� October 2008Saudi International Petrochemical Company - SIPCHEM

Chart 02: SIPCHEM Expansion (Investment in US$)

Source: SIPCHEM Management & Global Research

ManagementThe board of directors of the company is led by Mr. Abdulaziz Abdullah Hamad Al Zamil. Mr. Abdulaziz Abdullah Hamad is the acting chairman of the Company’s board.

Table 03: Board of DirectorsNames Position in SIPCHEM

Mr. Abdulaziz Abdullah Hamad Al Zamil Chairman

Mr. Reyadh S. Ahmed Member

Mr. Abdullah S. Bahamdan Member

Mr. Abdulrahman A. Al-Turki Member

Dr. Abdulrahman A. Al-Zamil Member

Dr. Saleh H. Al-Humaidan Member

Mr. Mohammad A. Al-Ghurair Member

Mr. Ibrahim M. Al-Humaidan Member

Dr. Abdulaziz A. Al-Gwaiz Member

Mr. Fahad S. Al-Rajhi Member

Ahmed Al-Ohali Member

Source: Company Website

The senior management of the company is headed by Mr. Ahmed Abdul Aziz Al Ohali. Mr. Ohali’s career started with SABIC National Methanol Company (IBN SINA) in September 1981 and he took a two year assignment with Celanese Chemical Company, in Houston, Texas, shortly afterwards. Mr. Al Ohali progressed within the company during his 15 years service into technical and executive positions. Mr. Al Ohali left SABIC in early 1996 to join the private industry world. He successfully started a medium sized private business in the non-woven films called Saudi German Non-Woven Products and was its Managing Director. During 1999, Mr. Al Ohali participated in setting up SIPCHEM, and became its president.

01000200030004000500060007000

Investments

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Capital Increasefrom SR500mn to650mn

Methanol Start-Up

BDO start-up capitalincreased to SR1.5bn Initial Public Offering Bonus shares Issued 33%

Right sharesissued 65.6%

Acetyl Start-up

PolyolefinsComplex

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM �

Table 04: Senior Management

Names Position in SIPCHEM

Mr. Ahmad Abdulaziz Al Ohali President & CEO

Mr. Abdulrahman A. Al-Saif President IDC & IMC

Mr. Abdullah S. Al-Saadoon President Acetyl Complex

Mr. Mehdi Aftab V.P, Major Projects

Mr. Abdullatif M. Bhairi V.P, Planning & Development Projects

Mr. Kevin J. Hayes V.P, Corporate Finance

Mr. Alber E Biggs G.M, Maintenance & Technical Services

Rashid M. Al-Dossari G.M, Public Relations & Corporate Affairs

Khaled S. Al-Dossari G.M, Finance & Accounting

Abdullah N. Al-Jaber G.M, Administration & Human Resources

Source: Company Website

Shareholding and LiquidityThe Company went in public following an initial public offering (IPO) and got listed on the Saudi Stock Exchange (Tadawul) in November 2006. The Company on the approval of Capital Market Authority (CMA) had issued 45mn shares at SR55 per share.

Table 05: SIPCHEM Shareholders (By the Year End 2007)

Shareholder Holding

Zamil Group Holding-Saudi Arabia 10.2%

National Industries Group Holdings-Kuwait 8.3%

Olayan Financing Company-Saudi Arabia 6.8%

Public Pension Agency –Saudi Arabia 6.5%

Al Ghurair Investment 3.7%

Sara Development Company 1.5%

Individuals, Corporate and Financial Institutions 14.9%

Public 47.2%

Source: Zawya

By the end of 2007, a major portion of the Company’s shares were held by the general public, which accounted for 47.2%. In addition, by the end of 2007, the Company had further increased its issued number of shares from 150mn to 200mn through the issuance of bonus shares. Furthermore, the Company has recently issued right shares, which are 66.5% of the capital at the end of 2007, and it has raised the Company’s share capital to 333mn shares. The other notable shareholders are (i) Zamil Group Holding Company which owns 10.2% (ii) National Industries Group Holding, which owns 8.3% and (iii) Olayan Financing Company, which owns 6.8% of the total paid-up capital. Rest of the shares are held by several government and private owned corporations and agencies.

Global Research - Saudi Arabia Global Investment House

� October 2008Saudi International Petrochemical Company - SIPCHEM

Table 06: Stock Liquidity

Year Volume Market Price (Year End) Market Cap (SR mn)

2006 9,446,097 23.6 3,540

2007 3,992,250 44.1 8,820

2008 2,351,851 22.5* 7,517

Source: TADAWUL, Global Research * Market price as 18th October 2008

SPICHEM Affiliates / SubsidiariesThe Company, at present, has six affiliates / subsidiaries out of which five are manufacturing units while one is used to carry out marketing & distribution activities of the Company. Currently, only two manufacturing affiliates / subsidiaries of the Company are operational alongwith the marketing affiliate / subsidiary.

International Methanol Company-IMCIMC is a limited liability company established in 2003 in Saudi Arabia, owned 65% by SPICHEM and 35% by Japan-Arabia Methanol Company Limited (JAMC), a special purpose subsidiary owned by a consortium of Japanese companies including Mitsui & Company Limited (Mitsui) (55%), Mitsubishi Corporation (Mitsubishi) (15%), Daicel Chemical Industries Limited (Daicel) (15%) and Iino Kaiun Kaisha Limited (Iino) (15%). IMC owns and operates a Methanol Plant in Jubail, Saudi Arabia. The Methanol plant at IMC commenced its commercial production in 4Q2004. IMC produces 1mn tons of methanol by using natural gas as a primary raw material, for which SIPCHEM signed a supply agreement with Saudi Aramco.

IMC operates proven steam methane reforming and methanol synthesis technology licensed by Jacobs Engineering UK Limited (Jacobs). The Plant also incorporates a range of process proven proprietary technologies including Johnson Matthey catalyst systems (included in approximately 60% of worldwide methanol production capacity) and a Methanol Casale S.A. Axial Radial Converter (ARC). JAMC, which is a shareholder of IMC, markets about 80% of the Company Methanol output outside the Middle East, whereas the Company is marketing the remaining balance in the Middle East.

International Diol Company-IDC International Diol Company is a limited liability company established in 2002 in Saudi Arabia. SIPCHEM owns a majority of the shares of IDC, in a joint venture with the Public Pension Agency GOSI, Huntsman Corp., Davy Process Technology, Sabih Tahir Darwish Al Masri, and A.S. Albabtain & Company. IDC had successfully started it initial production in 4Q2005 and is now going on stream with a total capacity of 75,000 tons to meet the growing demand for butanediol (BDO) and derivatives in the world and domestic markets.

International Diol Company’s product line comprises of specialty chemicals such as Butanediol (BDO), Tetrahydrofuran (THF) and Gamma-butyrolactone (GBL). The BDO production technology is provided by Davy Process Technology Limited of the United Kingdom. Upstream technology is provided by Huntsman Corporation and UOP LLC. Vinmar International Limited, USA and Will & Co B.V., of the Netherlands are providing the marketing services. The BDO and THF market have been very receptive of the new product.

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM �

International Acetyl Company –IACIAC is a limited liability company registered in January, 2006, owned 87% by SIPCHEM, 10% by Helm Arabia and 3% by Ministry of Endowments. IAC is intended to build, own and operate the Acetic Acid (AA) plant. Helm Arabia is a special purpose company established in Hamburg, Germany between Helm AG of Germany, a leading multinational producer and distributor of petrochemical products and Thales International Offsites, a subsidiary of Thales Company of France, a leading international electronics and systems group, serving government and business customers worldwide. The plant is designed to produce up to 400,000 tons of acetic acid and up to 50,000 tons of acetic anhydride, which will start commercial operation in 3Q2009. The feedstock, namely methanol, carbon monoxide and hydrogen will be provided internally by other SIPCHEM affiliates, viz. International Methanol Company (IMC) and Industrial Gases Company (IGC), thus ensuring an uninterrupted supply of feedstock.

International Vinyl Acetyl Company –IVACSIPCHEM has 87% stakes in IVAC, which is a limited liability company registered in January 2006. Reminder shares are held by Helm Arabia (10%) and Ministry of Endowmens (3%). IVAC is intended to build, own and operate the Vinyl Acetate Monomer (VAM) plant. Helm Arabia is a special purpose company established in Hamburg, Germany between Helm AG of Germany and Thales International Offsites. In addition, Helm AG of Germany is a leading multinational producer and distributor of petrochemical products and Thales International Offsite, a subsidiary of Thales Company of France, a leading international electronics and systems group, serving government and business customers worldwide.

The IVAC plant is designed to produce up to 330,000 tons of VAM and will start commercial operation in 3Q2009. The feedstock, Acetic Acid, will be provided internally from the complex of IAC, thus ensuring an uninterrupted supply of feedstock. DuPont, a multinational science and technology company, has agreed to supply technology.

International Gas Company-IGCIGC was established as a joint venture between SIPCHEM, National Power Company-NPC and Ministry of Endowments. The affiliate / subsidiary got registered in May2005. SIPCHEM holds a 72% stakes in IGCL while the remaining stakes of 25% are held by NPC and the remainder 3% by Ministry of Endowments. The plant is designed to produce 345,000 tons of Carbon Monoxide-CO, which is expected to start commercial operation in 3Q2009. Saudi Aramco has agreed to supply SIPCHEM the natural gas, which will also be used as feedstock for IGC plant.

Global Research - Saudi Arabia Global Investment House

8 October 2008Saudi International Petrochemical Company - SIPCHEM

Petrochemicals Overview

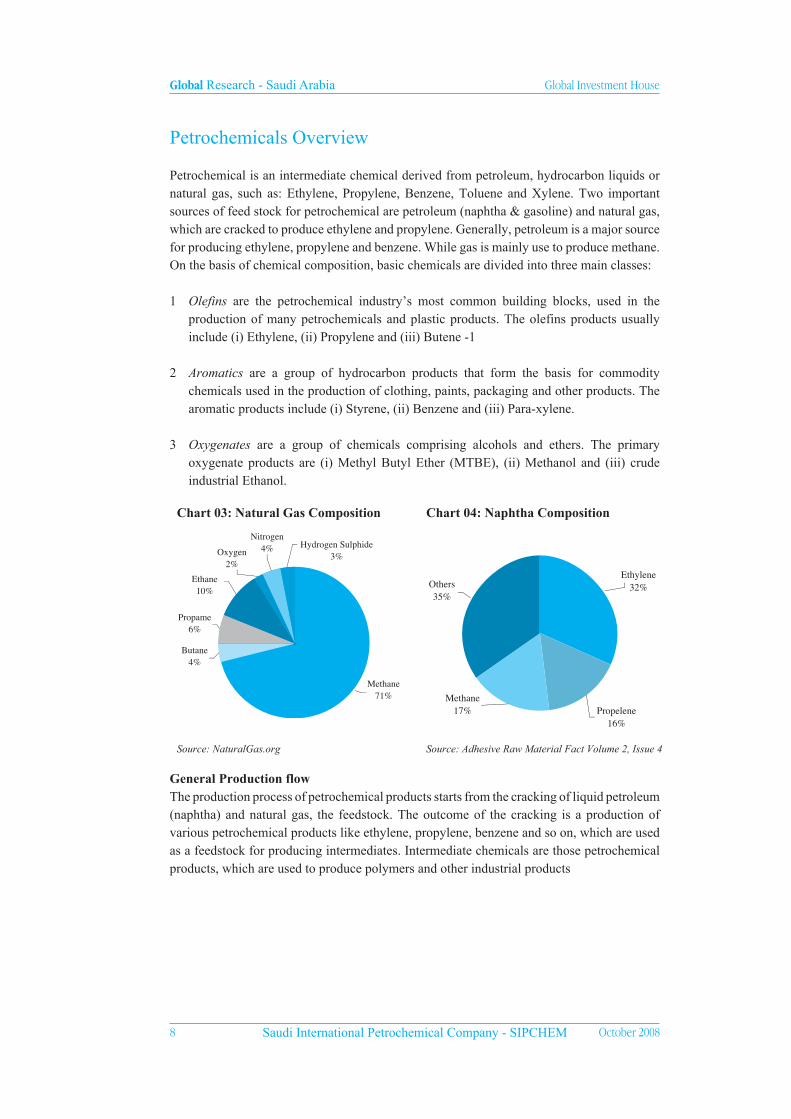

Petrochemical is an intermediate chemical derived from petroleum, hydrocarbon liquids or natural gas, such as: Ethylene, Propylene, Benzene, Toluene and Xylene. Two important sources of feed stock for petrochemical are petroleum (naphtha & gasoline) and natural gas, which are cracked to produce ethylene and propylene. Generally, petroleum is a major source for producing ethylene, propylene and benzene. While gas is mainly use to produce methane. On the basis of chemical composition, basic chemicals are divided into three main classes:

1 Olefins are the petrochemical industry’s most common building blocks, used in the production of many petrochemicals and plastic products. The olefins products usually include (i) Ethylene, (ii) Propylene and (iii) Butene -1

2 Aromatics are a group of hydrocarbon products that form the basis for commodity chemicals used in the production of clothing, paints, packaging and other products. The aromatic products include (i) Styrene, (ii) Benzene and (iii) Para-xylene.

3 Oxygenates are a group of chemicals comprising alcohols and ethers. The primary oxygenate products are (i) Methyl Butyl Ether (MTBE), (ii) Methanol and (iii) crude industrial Ethanol.

Chart 03: Natural Gas Composition Chart 04: Naphtha Composition

Source: NaturalGas.org Source: Adhesive Raw Material Fact Volume 2, Issue 4

General Production flowThe production process of petrochemical products starts from the cracking of liquid petroleum (naphtha) and natural gas, the feedstock. The outcome of the cracking is a production of various petrochemical products like ethylene, propylene, benzene and so on, which are used as a feedstock for producing intermediates. Intermediate chemicals are those petrochemical products, which are used to produce polymers and other industrial products

Ethylene32%

Propelene16%

Methane17%

Others35%

Hydrogen Sulphide3%

Nitrogen4%Oxygen

2%Ethane10%

Propame6%

Butane4%

Methane71%

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM �

Figure 01: Production Flow Diagram

Cru

de O

il

Gas

Prim

ary

Feed

Sto

ck

Seco

ndar

y Fe

ed S

tock

Proc

essi

ng U

nit

Bas

ic C

hem

ical

Inte

rmed

iate

s

Poly

mer

s, r

aw m

ater

ial f

or in

dust

ries

Gas

olin

e

Nap

htha

Ben

zene

Bas

ic C

hem

ical

Proc

essi

ng U

nit

Gas

olin

e

Gas

Oil

(Die

sel)

Nap

hta

Ker

osen

e

Eth

ane

Prop

ane

But

ane

Met

hane

Olefins

Eth

ylen

e

Prop

ylen

e

But

ene

Aro

mat

ics

Styr

ene

Ben

zene

Para

-Xyl

ene

Oxy

gena

tes

Met

hano

l

Met

hyl T

ertia

ry B

utyl

Eth

er

(MTB

E)

Crud

e Ind

ustri

al E

than

ol

I n t e r m e d i a t e s

P o l y m e r s

I n d u s t r i a l U s e s

Sour

ce:

Indu

stry

Sou

rces

& G

loba

l Res

earc

h

Global Research - Saudi Arabia Global Investment House

�0 October 2008Saudi International Petrochemical Company - SIPCHEM

3.3%4.2%4.1%

5.0%4.8%

1.7%

-2002 2003 2004 2005 2006 2007

0.0%1.0%2.0%3.0%4.0%5.0%6.0%

World Petrochemical Demand Growth Rate

20,00040,00060,00080,000

100,000120,000140,000

000 t

ons

Grot

h rate

4.0% 4.2%4.1%5.0%5.1%

1.1%

-20,00040,00060,00080,000

100,000120,000140,000

2002 2003 2004 2005 2006 20070.0%1.0%2.0%3.0%4.0%5.0%6.0%

World Petrochemical Production Growth Rate

000 t

ons

Grot

h rate

1.7% 1.6%

5.3% 5.3%

2.5%

5.2%

90,000.0100,000.0110,000.0120,000.0130,000.0

2002 2003 2004 2005 2006 20070.0%

2.0%

4.0%

6.0%

World Petrochemical Capacity Growth

000

tons

Gro

th ra

te

World Petrochemical Industry

Ease in capacity expansionGlobal petrochemical capacity increased at a CAGR of 3.3% to 128.4mn tons, during 2002-07. The major increase in petrochemical production capacity was witnessed in 2005 and 2006. However, in 2007 the growth was limited to 2.5% due to higher feedstock prices than 2005 and 2006.

Chart 05: World Petrochemical Capacity

Source: Global Research, Bloomberg & Industry Sources

Demand for petrochemical productsDemand is a driving force to increase capacity and improve capacity utilization, which results in an increase in production. The demand of petrochemical products has increased at a CAGR of 4% during 2002-07, with a sufficient world capacity to meet the existing demand. The rising prices of ethylene, propylene, and other basic petrochemical products have limited the demand growth between 4%-5% during the last 3-years.

Chart 06: World Petrochemical Demand (000 tons)

Source: Global Research, Bloomberg & Industry Sources

Higher capacity utilization leads to an increase in productionOver the last five years, the world capacity utilization has reached 90.3% in 2007, which is 3.3% higher than the capacity utilization in 2002. The improvement in capacity utilization has led the world production to increase at a 5-year CAGR of 3.9% to 117.7mn tons in 2007. The year-on-year production growth, during the last 3 years, remained at an average level of 4.5%-5%, as compared to a marginal growth of 1.1% in 2003.

Chart 07: World Petrochemical Production

Source: Global Research, Bloomberg & Industry Sources

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM ��

Capacity Expansion in ChinaChina, the world’s third largest petrochemicals market, is currently undergoing extensive expansions in ethylene capacities, adding almost 6.6mn tons of ethylene between 2008 and 2012. Ethylene capacities in China are planned to increase by 11.4mn to 11.6mn tons between 2008 and 2016.

China’s ethylene output will go up from 9.6mn tons in 2006 to 14 -18 mn tons by 2010. It is worth noting that most Chinese crackers will be naphtha based, which will result in a rapid growth in the heavy feedstock consumption and consequently this will exert upward pressure on the international naphtha prices.

Table 07: Chinese Ethylene Expansions

Company LocationCapacity

(1,000 mt)

Startup

Year

Projects Underway

Fujian Refining and Petrochemical Company Ltd(JV with Exxon)

Quangzhou 800 1Q2009

PETROCHINA

PetroChina Dushanzi PetroChemical Dushanzi, Xinjiang 1,000 2008

PetroChina Fushun PetroChemical Fushun, Liaoning 800 2010

PetroChina Chengdu Ethylene Project (New plant) Chengdu, Sichuan 800 2012

SINOPEC

Sinopec Zhenhai Refining & Chemical Co. Ltd Zhenhai, Zhejiang 800 - 1000 2009

Sinopec Tianjin Petrochemical Tianjin 800 2010

Sinopec Wuhan Co. Wuhan, Hubei 800 2012

In Early Planning

Sinopec Shanghai Chemical Park Ethylene Project Shanghai 1,000 2014+

Dalian Ethylene Project Dalian, Liaoning 1,000 2015+

Formosa Ningbo Ethylene Project Ningbo, Zhejiang 1,000 2015+

MTO

China Shenhua Group MTO Plant * Erdos,Inner Mongolia 600 2012

Shaanxi Yulin MTO Project * Yulin, Shaanxi 1,000 2013

Shenhua Dow * Shaanxi 1,000 2013+

Total 11,400 – 11,600

* Production will be 50% ethylene and 50% propyleneSource: The Gulf Petrochemicals and Chemicals Directory, Volume I

Alternative Feedstock Experiments in China Currently, China is undertaking extensive experiments to produce chemicals from coal in an attempt to find alternative cheap feedstock post the naphtha price surge. Coal represents almost 70% of the Chinese energy mix. Under this process, coal is converted to synthesis gas “syngas”, which can be then converted to different chemicals, among which is methanol. The methanol is converted to olefins (MTO) ethylene and propylene. Mostly in the planning stage, there are 12 to 14 MTO projects, with some under construction, that are based on coal.

Global Research - Saudi Arabia Global Investment House

�2 October 2008Saudi International Petrochemical Company - SIPCHEM

-1.002.003.004.005.006.007.008.009.00

2001 2002 2003 2004 2005 2006 2007 2008E 2009E 2010E 2011E

-10.0020.0030.0040.0050.0060.0070.0080.00

2001 2002 2003 2004 2005 2006 2007

Feed Stock PricesGas pricesCrude oil prices are used as a benchmark to set gas-well head price in the international markets. However, gas prices are highly subsidized in certain regions of the world, mainly the Middle-East, North Africa, and South Asia. The gas-well head prices, in these regions, are subject to have pre-determined discounts. At the same time, gas well head prices in the international markets, have shot up by 44.2% from US$4.4 per mmbtu in 2001 to US$6.3 per mmbtu in 2007.

Chart 08: Prices of Gas (US$ per mmbtu)

Source: EIA & Global Research

Crude oil pricesOver the period of the last 6 years, the basket price of OPEC crude oil has surged by 192.5% from US$23.01 per barrel in 2002 to US$67.31 per barrel in 2007. The increase in crude oil prices over the period of 5 years are mainly due to the following reasons:

• Global political uncertainty

• High global economic growth

• Lack of refining capacity which caused a shortage of refined products.

Chart 09: OPEC Historical Crude Oil Prices (US$ per barrel)

Source: OPEC

The average basket prices of OPEC crude oil prices were recorded at US$113.5 per barrel, in 3Q2008. The recent upward rally in the price of crude oil, which was started in the 4Q2007, has ended during the 3Q2008, which is mainly due to the ongoing global financial crisis. Going forward, we expect crude oil prices to ease down from the current level (3Q2008) to US$80.8 per barrel in 2011. This assumption is based on the following factors:

• Recovery of the financial market from the ongoing financial crisis.

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM ��

-

20.00

40.00

60.00

80.00

100.00

120.00

2007 2008E 2009E 2010E 2011E

Crude Oil US / bbl

• Slowdown in economic development and shifting towards gas base industries

• New refining capacity will come online by 2011, which will fulfill the shortage of refined products.

Chart 10: Forecasted OPEC Crude Oil Prices (US$ per barrels)

Source: OPEC& Global Research

Naphtha is a major feedstock for ethylene and propylene production. The natural gas, mainly ethane and propane, is also used in the manufacturing of these petrochemicals, despite the fact that the main component of the natural gas is the methane, which is primarily used for energy. Naphtha is a direct outcome of crude oil refining, hence the prices of naphtha is much correlated to the prices of crude oil.

World Petrochemical OutlookBased on our expectations, crude oil price will remain on the high side. Even after an expected relaxation, the average price is forecasted to remain in the range of US$80-US$90 per barrel in 2011 as compared to 3Q2008 average prices of US$113.5 per barrel. Since the prices of petroleum products and gas feedstock are derived from crude oil prices, we expect the price of international feedstock to remain high as well. The higher feedstock prices will not allow the global petrochemical industry to expand their margins, as the price of petrochemical products is subject to feedstock prices. Consequently, we expect a major expansion in petrochemical capacities will happen in those areas of the world where feedstock is available at cheap rates, including the MENA region and China. The capacity expansion in MENA and China is mainly due to the following:

•Effort of economic diversification i.e. shifts from oil based economies to industrial based economies.

•Plenty of gas reserves, which accounted for 51.9% of the world reserves. This enables these countries to supply gas at cheap rates. Moreover, the region has plenty of crude oil reserves, which enables the government to supply petroleum products with some specific discounts.

•Extraction of petrochemical products from coal has encouraged China to consider massive expansion in its petrochemical capacities. However, the effort is under process.

Prices of MethanolThe price of methanol has surged by 191.7% to US$472.6 pet ton in 2007 as compared to US$162 per ton in 2001. The increase in the price of methanol during the period of 2001-

Global Research - Saudi Arabia Global Investment House

�� October 2008Saudi International Petrochemical Company - SIPCHEM

0

100

200

300

400

500

600

2007 2008E 2009E 2010E 2011E

Methanol Prices

-

100.0

200.0

300.0

400.0

500.0

2001

2002

2003

2005

2006

2007

2004

07 is mainly because of higher gas prices, which have been increased due to higher crude oil prices. Moreover, methanol is derived from methane which is mainly obtained from the cracking of natural gas while sometime from naphtha. The availability of natural gas at high subsidize price of US$0.75 per mmbtu has further strengthened the margin of Saudi petrochemical units.

Chart 11: Historical Average Prices of Methanol (US$ per ton)

Source: Methanex

Goring forward, the expected future prices of methanol is based on the movement of our expected crude oil prices, which will also affect the price of natural gas in international market. Based on our expectations, the price of methanol will surge by 11.1% in 2008 to reach at US$525.1 per tons as compared to the average prices in 2007. However, we expect a gradual decline in the average prices of methanol to US$304.1 per ton in 2011, in line with our expected prices of crude oil.

Chart 12: Forecasted Average Prices of Methanol (US$ per ton)

Source: Methanex & Global Research

Implications…Methanol is used in manufacturing a wide variety of chemical products such as formaldehyde and Acetic Acid. Methanol, as a hydrogen carrier is being considered for fuel cell application and as an alternate fuel. Methanol was once known as wood alcohol, because it was originally produced as a by-product of the distillation of wood.

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM ��

MENA Petrochemical Industry

Petrochemical hubAs of 2007, the MENA region’s combined petrochemical production capacity reached 84.7mn tons, which represents 66% of total world capacity. This indicates that the region is the largest petrochemical producer in world.

Chart 13: Share of MENA in World’s Capacity 2007

Source: Zawya & Global Research

Saudi Arabia: The largest petrochemical playerIn 2007, Saudi Arabia occupied 52.8% of the total MENA capacity, through SABIC. SABIC is not only a major player in Saudi Arabia, but the company has a vital position in the international market. In 2007, SABIC accounted for 53.9% of the total Saudi Arabia’s capacity, 28.4% of MENA and 18.7% of the world. Next to Saudi Arabia, Iran, through National Petrochemical Company, has claimed 20.2% and Qatar has 11.3% of MENA capacity.

Table 08: Country-Wise MENA Capacity (000 tons)

Country 2007 Share

Saudi Arabia 44,686 52.8%

Iran 17,145 20.2%

Qatar 9,585 11.3%

Egypt 3,057 3.6%

Kuwait 2,133 2.5%

UAE 1,441 1.7%

Rest of MENA 6,628 7.8%

Total MENA Capacity 84,675 100%

Source: Zawya

Capacity Expansion in MENAMENA region has planned for a massive expansion of petrochemical capacity of different grades with an estimated cost of US$90.7bn (SR332.8bn). Based on the given expansion plans, the production capacity in MENA region will increase to 90.9mn tons in 2008 and 104.1mn tons in 2009. Going forward, we expect the production capacity will increase to 114.6mn tons by 2011, at a 4-year CAGR of 8.2%. Major capacity expansion in petrochemicals of different grades is expected in Saudi Arabia, which will account for 61.3% in 2008 followed by Kuwait which is expected to contribute by 25.5%. In addition, after 2011, production capacity in MENA region will further increase by 3.4mn tons in 2012, due to upcoming capacity expansion in Saudi Arabia and Qatar.

MENA66%

Rest of the world34%

Global Research - Saudi Arabia Global Investment House

�� October 2008Saudi International Petrochemical Company - SIPCHEM

14. 5%

7.3%

4. 0%7.4%

-20.0040.0060.0080.00

100.00120.00140.00

2008E 2009E 2010E 2011E

0.0%

5.0%

10.0%

15.0%

20.0%

Total Capacity Expansion Growth In Capacity Expansion

Chart 14: MENA Capacity Expansion

Source: Zawya & Global Research

Product-wise capacity expansionThe total expected increase of 31.2mn tons, till 2011, in the petrochemical products capacities of different grades, in the MENA region, is based on the addition of (i) 16.9mn tons of basic chemical-olefins, (ii) 5.6mn tons of basic chemical-Aromatics and (iii) 8.8mn tons of basic chemical-oxygenates.

Table 09: Grade-Wise Capacity Expansion in MENA (Tons)

2008E 2009E 2010E 2011E

Basic-Olefins 2,982,500 6,837,500 3,629,250 3,409,750

Basic-Aromatic 1,848,750 2,566,250 1,200,000 -

Basic-Oxygenate 1,339,000 3,643,000 2,788,000 1,020,000

Expected Expansion 6,170,250 13,046,750 7,617,250 4,429,750

Source: Zawya & Global Research

Country-wise capacity expansionSaudi Arabia – Capacity expansionSaudi Arabia is expected to make an addition of 3.84mn tons of basic chemical of different grades out of the total additions in regional capacities of 6.27mn tons in 2008. The contribution, however, will increase to 6.54mn tons in 2009, and will taper down to 4.2mn tons in 2010.

Table 10: Saudi Arabia Additional Capacity (Tons)

2008E 2009E 2010E 2011E

Basic-Olefins 2,232,500 5,437,500 3,600,000 1,900,000

Basic-Aromatic 573,750 191,250 600,000 -

Basic-Oxygenate 1,039,000 913,000 - -

Expected Expansion 3,845,250 6,541,750 4,200,000 1,900,000

Total Expected Expansion 6,170,250 13,046,750 7,617,250 4,429,750

Contribution in Expansion 62.3% 50.1% 55.1% 42.9%

Source: Zawya & Global Research

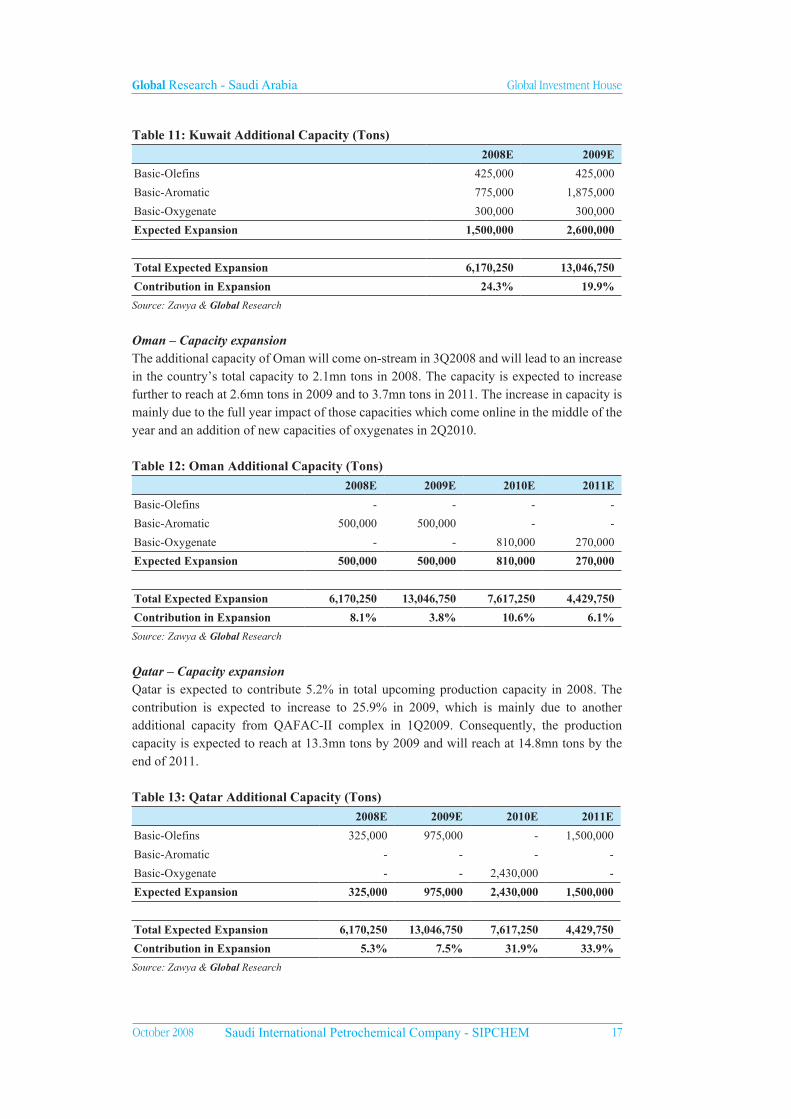

Kuwait – Capacity expansionBased on the given expansion plan, production capacities of basic chemicals in Kuwait will increase by 1.5mn tons in 2008 and 2.7mn tons in 2009. This will increase the country’s capacity from 2.1mn tons in 2007 to 6.3mn tons in 2009.

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM ��

Table 11: Kuwait Additional Capacity (Tons)

2008E 2009E

Basic-Olefins 425,000 425,000

Basic-Aromatic 775,000 1,875,000

Basic-Oxygenate 300,000 300,000

Expected Expansion 1,500,000 2,600,000

Total Expected Expansion 6,170,250 13,046,750

Contribution in Expansion 24.3% 19.9%

Source: Zawya & Global Research

Oman – Capacity expansionThe additional capacity of Oman will come on-stream in 3Q2008 and will lead to an increase in the country’s total capacity to 2.1mn tons in 2008. The capacity is expected to increase further to reach at 2.6mn tons in 2009 and to 3.7mn tons in 2011. The increase in capacity is mainly due to the full year impact of those capacities which come online in the middle of the year and an addition of new capacities of oxygenates in 2Q2010.

Table 12: Oman Additional Capacity (Tons)

2008E 2009E 2010E 2011E

Basic-Olefins - - - -

Basic-Aromatic 500,000 500,000 - -

Basic-Oxygenate - - 810,000 270,000

Expected Expansion 500,000 500,000 810,000 270,000

Total Expected Expansion 6,170,250 13,046,750 7,617,250 4,429,750

Contribution in Expansion 8.1% 3.8% 10.6% 6.1%

Source: Zawya & Global Research

Qatar – Capacity expansionQatar is expected to contribute 5.2% in total upcoming production capacity in 2008. The contribution is expected to increase to 25.9% in 2009, which is mainly due to another additional capacity from QAFAC-II complex in 1Q2009. Consequently, the production capacity is expected to reach at 13.3mn tons by 2009 and will reach at 14.8mn tons by the end of 2011.

Table 13: Qatar Additional Capacity (Tons)

2008E 2009E 2010E 2011E

Basic-Olefins 325,000 975,000 - 1,500,000

Basic-Aromatic - - - -

Basic-Oxygenate - - 2,430,000 -

Expected Expansion 325,000 975,000 2,430,000 1,500,000

Total Expected Expansion 6,170,250 13,046,750 7,617,250 4,429,750

Contribution in Expansion 5.3% 7.5% 31.9% 33.9%

Source: Zawya & Global Research

Global Research - Saudi Arabia Global Investment House

�8 October 2008Saudi International Petrochemical Company - SIPCHEM

Table 14: MENA Capacity Expansion (Tons)

Country Basic-Olefins Basic-Aromatic Basic-Oxygenate Expected Production

Saudi Arabia 252,000 2Q2008

Saudi Arabia 50,000 2Q2008

Saudi Arabia 950,000 4Q2008

Saudi Arabia 1,700,000 2010

Saudi Arabia 3,800,000 3Q2010

Saudi Arabia 230,000 715,000 2Q2008

Saudi Arabia 2,100,000 2012

Saudi Arabia 1,285,000 4Q2008

Saudi Arabia 600,000 2010

Saudi Arabia 1,200,000 2009

Saudi Arabia 1,700,000 3Q2008

Kuwait 850,000 450,000 600,000 3Q2008

Kuwait 1,100,000 3Q2008

Kuwait 1,100,000 1Q2009

UAE 600,000 2010

Egypt 350,000 4Q2009

Oman 1,080,000 2Q2010

Oman 1,000,000 3Q2008

Qatar 1,300,000 4Q2008

Qatar 2,430,000 1Q2010

Qatar 1,500,000 2011

Qatar 880000 600000 2012

Qatar 1,300,000 2012

Algeria 1,000,000 4Q2010

Algeria 1,400,000 2012

Bahrain 1,728,000 2010

Source: Zawya & Global Research

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM ��

Saudi Petrochemical Industry

IntroductionSaudi Arabia is a key player in the global petrochemical industry commanding a 34.8% and 52.8% of the world and MENA petrochemical production capacity in 2007, respectively. The major part of Saudi Arabia’s petrochemical production is exported. The Saudi petrochemical industry is mainly concentrated in the industrial cities of Jubail and Yanbu.

Chart 15: Saudi Arabia Share in World Chart 16: Saudi Arabia Share in Region 2007 2007

Source: Global Research

Feedstock a competitive edgeThe Kingdom’s petrochemical industry enjoys high profit margins, mainly due to a natural competitive advantage of availability of low cost feedstock, on account of vast crude oil and natural gas resources. The cost of natural gas for the Saudi Arabian petrochemical industry is just US$0.75/mmbtu, which is far below than the international prices.

Table 15: Gross Margins on Petrochemical Products in Saudi Arabia

2008E 2009E 2010E 2011E

Ethylene Average High High High

Propylene Average High High High

MTBE Low Low Low Low

Styrene Average Average Average Average

Benzene High High High High

Paraxylene Low Low Low Low

Mono Ethylene Glycol Average Low Low Low

Di Ethylene Glycol Average Average Average Average

Teri Ethylene Glycol Average Average Average Average

Purified Terephthalic Acid - PTA Low High High High

Ethylene Di Chloride High High High High

Caustic Soda Low Average High High

Vinyl Chloride Monomer - VCM Average Average Average Average

Polyethylene Average Average Average Average

Polypropylene Average Average Average Average

Polyvinyl Chloride - PVC High High High High

Polyethylene Terephthalate Resin - PET High Average Average Low

Polystyrene - PS Low Low Low Low

Source: Global ResearchNote: High Return = 50%, Average Return = 20%-50%, Low Return = Below 20%

MENA47%Saudi Arabia

53%

Rest of the World65%

Saudi Arabia35%

Global Research - Saudi Arabia Global Investment House

20 October 2008Saudi International Petrochemical Company - SIPCHEM

The WTO agreement confirmed Saudi Arabia has the right to retain low feedstock prices on the grounds that its hydrocarbon resources are a natural advantage and low prices are not classed as a subsidy. The agreement also allows a dual pricing system, where domestic users pay less than the export price for feedstock, under the reasoning that domestic customers do not require export infrastructure or export marketing.

Major Players

Saudi Arabian Basic Industries (SABIC)SABIC is the world’s leading petrochemical producing company and was established by the Saudi government in 1976 in furtherance of a government policy to diversify the Saudi industrial base outside the oil sector and in order to make use of crude oil-associated gases at well-heads which had, until that point, been flared off. The intention was to build a chain of basic, large-scale industries located close to or with easy access to gas resources and to develop export-oriented non-oil businesses of strategic importance to Saudi Arabia, including hydrocarbon-based chemicals and basic metal industries.

Now SABIC has a total 21 petrochemical affiliates and YANSAB is one of them. The affiliates of SABIC are distinguished in six strategic business units (SBUs), organized by products. These are: Basic Chemicals, Intermediates, Polymers, Specialized Products, Fertilizers, and Metals. Each of these is headed by a Vice-President. These six business units make four different kinds of products:

1 Chemicals – Basic Chemicals, Intermediates and Specialized Products (three SBUs)

2 Plastics – Polymers (one SBU)

3 Fertilizers (one SBU)

4 Metals (one SBU)

Table 16: SABIC’s Affiliates

Name of Affiliates LocationHolding of

SABIC

Arabian Petrochemical Company Saudi Arabia 100.00%

SABIC Asia Pacific Singapore Singapore 100.00%

SABIC Industries Investments Company Saudi Arabia 100.00%

SABIC Innovative Plastics United States 100.00%

SABIC Luxembourg Luxembourg 100.00%

SABIC Sukuk Company Saudi Arabia 100.00%

SABIC UK Petrochemicals UK 100.00%

Saudi Iron and Steel Company Saudi Arabia 100.00%

Saudi European Petrochemical Company Saudi Arabia 80.00%

Jubail United Petrochemical Company Saudi Arabia 75.00%

National Industrial Gases Company Saudi Arabia 70.00%

Yanbu National Petrochemicals Company Saudi Arabia 56.00%

Arabian Industrial Fibers Company Saudi Arabia 53.90%

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM 2�

Al Jubail Fertilizer Company Saudi Arabia 50.00%

Al Jubail Petrochemical Company Saudi Arabia 50.00%

Eastern Petrochemical Company Saudi Arabia 50.00%

National Chemical Fertilizer Company Saudi Arabia 50.00%

National Methanol Company Saudi Arabia 50.00%

Saudi Methanol Company Saudi Arabia 50.00%

Saudi Petrochemical Company Saudi Arabia 50.00%

Saudi Yanbu Petrochemical Company Saudi Arabia 50.00%

Saudi Arabian Fertilizer Company Saudi Arabia 42.99%

Saudi Kayan Petrochemical Company Saudi Arabia 35.00%

Gulf Petrochemical Industries Company Bahrain 33.33%

Gulf Aluminum Rolling Mill Company Bahrain 30.28%

Maaden Phosphate Company Saudi Arabia 30.00%

Power and Water Utility Company for Jubail and Yanbu Saudi Arabia 24.81%

Aluminum Bahrain [Via SABIC Industries Investments Company] Bahrain 20.00%

National Chemical Carriers Saudi Arabia 20.00%

Source: Zawya

Saudi Chemical CompanySaudi Chemical’s line of production includes the latest generation, safest, and world wide commonly used civil explosives and non-electrical detonators, which are KEMULEX, PRILLEX, and SANEL, respectively. KEMULEX is an emulsion type explosive characterized by its high detonation velocity and good waterproof properties and packaged in special plastic cartridges with different sizes that meet the clients’ needs. PRILLEX is a dry blasting agent, which is composed of Ammonium Nitrates and Fuel Oil (ANFO).

Saudi Chemical Company also manufactures non-electric detonators “SANEL” that provide the precious control and accuracy that reduces blasting vibration and improves fragmentation for all kind of blasting. SANEL is produced in a wide range of delay times, lengths, and models for different types of use. In addition, the company offers wide variety of Electrical Detonators, and Detonating Cords, in addition to all accessories for rock blasting and oil exploration shooting.

Progress continues and Saudi Chemical proceeds along the path of ongoing improvement, advancing in all aspects that go beyond expectation to provide domestic and global supplies of most modern explosives. This resulted in new production line for ENVIROSEIS, the latest in seismic explosives specially designed for seismic exploration. Proudly, ENVIROSEIS is now used for oil and gas exploration in Saudi Arabia. It is worth mentioning that the company’s activity is not limited to production of civil explosives only, but also will be extended to include military explosives in manufacturing and demilitarization processes. Sahara Petrochemical CompanySince its establishment in 2004, Sahara’s management team has been successfully working on two projects, Al Waha Petrochemical Company, its first majority owned subsidiary and on its affiliated participation in Saudi Olefins and Polyolefins Company (SEPC), both of which are expected to become operational by the fourth quarter of 2008.

Global Research - Saudi Arabia Global Investment House

22 October 2008Saudi International Petrochemical Company - SIPCHEM

8.3%

5.2%

5.5%12.3%

-

2008E 2009E 2010E 2011E

0.0%

5.0%

10.0%

15.0%

Capacity Expansion Growth

Al Waha Petrochemical Company (Al-Waha) is located in the Industrial City of Jubail in the Eastern Province of the Kingdom of Saudi Arabia. The affiliate (Al-Waha) was established in September of 2006, as Sahara’s first majority owned industrial project subsidiary. Al Waha is a limited liability joint venture company, which is to construct, own and operate a world scale petrochemical complex for the production of 460,000 tons of propylene that will serve as feedstock for the production of 450,000 tons of polypropylene. The polypropylene will be sold both within the region and into international markets.

Sahara, together with Tasnee Petrochemical Company (Tasnee) 50.6% stake owner and the Basell group of companies (Basell) holding 25% stake, formed a new company to develop, finance, construct, commission, own, manage and operate a world-scale petrochemical complex for the production of some 1,000,000 tons of ethylene, 80% of which will be used as the primary feedstock for the production of approximately 800,000 tons of polyethylene. The Saudi Ethylene and Polyethylene Company (SEPC) is also located in Al-Jubail Industrial City, Saudi Arabia with commercial operations set to begin in the fourth quarter of 2008.

Capacity expansionDuring the last 4 years, the growth in Saudi Arabia’s economy is mainly due to higher crude oil prices. This depicts a serious threat for the country in case of ease in crude oil prices. In order to minimize this risk the government of Saudi Arabia has promoted non-oil industries. Consequently, a massive expansion in petrochemical has been taken into account, which will increase at a CAGR of 7.8% during the period from 2007 to 2011.

Chart 17: Saudi Arabia Capacity Expansion

Source: Zawya and Global Research

Major new capacities in Saudi Arabia are expected to locate in Jubail industrial area. In our valuations, we have not incorporated the upcoming capacity of SIPCHEM’s olefins complex, as it will come online in 2012 with a designed capacity of 2.1mn tons.

Major capacity expansion – Company WiseMajor additional petrochemical capacity in Saudi Arabia is expected from Saudi Kayan Petrochemical Company (KAYAN), which will come on line on 3Q2010. KAYAN is expected to contribute by 23% in the total Saudi Arabia expansion of 16.5mn tons. However, the capacity from Eastern Petrochemical (SHARQ) and YANSAB will contribute to 24.3%, with a combined capacity of 4mn tons.

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM 2�

Table 17: Capacity Expansion by Company

Name Basic-Olefins Basic-Aromatic Basic-Oxygenate Expected Production

Saudi European-IBN ZAHR 950,000 - - 4Q2008

Sino-Saudi Petrochemical Project 1,700,000 - - 2010

Saudi Kayan 3,800,000 - - 3Q2010

Sharq-Eastern Petrochemical 2,000,000 - - 3Q2008

YANSAB 2,005,000 - - 4Q2008

SIPCHEM-Olefins 2,100,000 - - 2012

Sahara/Tanesse-Saudi Ethylene &

Propylene Plant1,285,000 4Q2008

Petrokemya-PVC and Offsite - - - 2010

Sadaf-Styrene Plant-Saudi

Petrochemical- 600,000 - 2010

Delta Oil 1,200,000 - - 2009

Source: Zawya & Global Research

Global Research - Saudi Arabia Global Investment House

2� October 2008Saudi International Petrochemical Company - SIPCHEM

SIPCHEM Competitors’ Profile

Based on the, current, production mix of the Company, we have identified the following potential competitors in local and regional market.

•Saudi Methanol Company (Ar-Razi)

•Egyptian Methanex Methanol Company (EMETHANEX)

•National Methanol Company (Ibn Sina)

•Oman Methanol Company (OMC)

•Salalah Methanol Company (SMC)

Saudi Methanol Company-Ar Razi The company was formed in 1979 in Saudi Arabia under a 50-50 joint venture between SABIC and Japanese companies (led by Japan Saudi Arabia Methanol Company). This was the first joint venture of SABIC. The basic activity of Ar Razi is to produce chemical grade methanol with a designed capacity of 3.3mn tons. However, the additional capacity of 1.7mn tons of methanol will lead the overall production capacity of the complex to 5mn tons by the end of 2008. Moreover, the expansion cost was estimated at SR2.2bn (US$600mn) for the complex. Egyptian Methanex Methanol Company-EMETHANEXEMETHANEX was established as a limited liability company in 2005. The plant of the company is under developmental stage and is designed to produce 1.3mn tons of Methanol per year. The majority of the shareholding is held by Methanex Corporation, which accounts for 60% of the total stakes. The remainder stakes are held by (i) Egyptian Natural Gas Holding Company (12%), (ii) Egyptian Petrochemicals Holding Limited (12%), Egyptian Natural Gas Company (9%) and Arab Petroleum Investments Corporation (7%). The present shareholding structure shows an undisrupted supply of gas to the plant at subsidize rate of US$2.5-US$2.75 pet mmbtu.

National Methanol Company-Ibn Sina Ibn Sina is a joint venture of (i) SABIC, which holds 50% stakes, (ii) Duke Energy Corporation, holds 25% stakes and (iii) Hoechst Celanese Chemicals, holds 25% stakes. The company has a designed capacity to produce 2.1mn tons of Methanol and MTBE.

Oman Methanol Company-OMCOMC is a joint venture between Methanol Holding International Limited-MHIL of Trinidad, Oman Methanol Holding Company, which is a division of Omar Zawawi Establishment (OMZEST) Group & MAN Ferrostaal Methanol Holding Limited. The project has the backing of MHIL, which already has four methanol plants in Trinidad and Tobago and is in the process of constructing the world’s largest methanol plant with a production capacity of 1.9mn tons.

OMC has constructed a methanol producing complex with a design producing capacity

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM 2�

of 1.1mn tons in the Sohar Industrial Port area, which will use Johnson Matthey LPM technology as originally developed by ICI. The complex is managed and operated by Oman Plants Services Company-OPSC, which is a joint venture between Oman Mechanical Services Company, a part of The OMZEST Group and Industrial Plant Services Limited, a Trinidadian company which manages and operates Methanol Holding Trinidad Limited’s methanol plants in Trinidad. Salalah Methanol Company-SMCSMC is a subsidiary of Oman Oil Company-OOC and was established in 2006 with the principle activities (i) to produce 1.2mn tons of methanol, (ii) water desalination and (iii) waste water treatment. Currently, the petrochemical complex of SMC is under developmental phase and is expected to start commercial production of by the end of 2009.

Global Research - Saudi Arabia Global Investment House

2� October 2008Saudi International Petrochemical Company - SIPCHEM

-1,000.02,000.03,000.04,000.05,000.06,000.07,000.0

2004 2005 2006 2007-20.040.060.080.0100.0120.0140.0160.0180.0

Longtermloans - LHS Assetbase _ LHS Depriciation - RHS Financial Cost - RHS

72.4%72.7%

77.6%

71.5%

-200.0400.0600.0800.0

1,000.01,200.01,400.01,600.01,800.0

2004 2005 2006 200768.0%70.0%72.0%74.0%76.0%78.0%80.0%

Gross Profit (excluding depriciation Cost) Gross Profit Margins

SIPCHEM Financial Overview

Growth in sales revenue Since inception, the sale revenues of the Company have increased at a CAGR of 274%, during 2004-07. The increase in the sale revenues of the Company during the last 3 years are mainly due to (i) commencement of production of methanol, through IMC in mid 2004, (ii) start-up of BDO in late 2005, through its affiliates IDL. Moreover, the increase in the average prices of methanol and BDO, on account of higher crude oil prices, has also fueled the sales revenue of the Company.

High gross marginsHistorically, the gross margins (excluding depreciation cost) of the Company remained higher since inception, at an average level of 73.5%. The major reason of high gross margins is the availability of feed stock gas at highly subsidize rate of US$0.75 per mmbtu and butane (from naphtha) at 30%-35% lower than the average prices in international market.

Chart 18: Gross Profit (SR mn) & Gross Margins (Excluding Depreciation Cost)

Source: Company Reports & Global Research

Increase in asset-base inflates financial & depreciation chargesThe consistent efforts to expand the manufacturing operation of the Company through (i) establishment of IMC and IDL in 2005 and 2006 respectively and (ii) planned development of Acetyl complex by 2009 have led the management to go for long-term loans. Consequently, the asset base of the Company has been increased from SR2.2bn in 2004 to SR5.4bn in 2007 which has led the depreciation cost to reach at SR164.1bn in 2007.

Chart 19: Long-Term Loans, Asset Base, Depreciation & Financial Cost (SR mn)

Source: Company Reports & Global Research

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM 2�

71.1%73.1%79.2%

100.6%

44.8%

78.3%

37.0% 38.9%

-200.0400.0600.0800.0

1,000.01,200.0

2004 2005 2006 20070.0%20.0%40.0%60.0%80.0%100.0%120.0%

EBITDA EBITDA MarginProfitability Profitability Margin

Surge in profitabilityRapid increase in the sale revenues of the Company has eliminated the impact of higher depreciation and financial cost, which has led profitability to increase at a CAGR of 359.8%, during 2004-07, and reached at SR593.9mn in 2007. However, the net profit margin has declined to 38.9% in 2007 as compared to 78.3% in 2004. Furthermore, the EBITDA of the Company has surged to SR1,087mn in 2007 as compared to SR7.8mn in 2004, with the average EBITDA margins 81% during the same period.

Chart 20: Profitability & EBITDA (SR mn)

Source: Company Reports & Global Research

Major concernsThe prime risk of the company is on the supply of feedstock, which includes naphtha (propane) and natural gas. As Saudi Aramco is the only supplier of feedstock to the Company, the risk of constant supplies of raw material from Saudi Aramco is associated with the Company.

SIPCHEM is enjoying the benefit of getting Naphtha and natural gas, as a feed stock at subsidized rates like other Saudi Arabian petrochemical complexes. This provides the competitive edge to the Company on regional competitors.

SIPCHEM has to face stiff competition within the country with Ar-Razi and Ibn-Sina methanol producing complexes, as both of these complexes are the affiliates / subsidiaries of SABIC. Thus, the Company has to face stiff competition with SABIC on a local, regional and international basis. The Company is enjoying the benefit of having a BDO producing complex, and is one of the few petrochemical companies in Saudi Arabia.

Production growthBy the end of 2007, the production of the Company had reached 772,990 tons out of which methanol production accounted for 89.5%, while BDO production recorded at 34,619 tons and the remainder is Ma production. The production in 2008 is expected to decline by 3.4% due to the expectations of lower capacity utilization i.e. at 100% with the domination of methanol production. The completion of the Acetyl complex in 3Q2009 will lead production to grow at a CAGR of 20.4%, during 2007-11. Furthermore, by the end of 2011, the Company will be able to expand its product-line by adding AA, AAn, VAM and CO. Despite the, expected commencement of production from Acetyl complex, methanol is expected to remain the Company’s main product till 2011, though the share of methanol is expected to dilute and reach at 40% in overall production of the Company.

Global Research - Saudi Arabia Global Investment House

28 October 2008Saudi International Petrochemical Company - SIPCHEM

-3.5%

25.0%11.1%

19.7%14.5%

83.7%

-500.0

1,000.01,500.02,000.02,500.03,000.0

2006 2007 2008E 2009E 2010E 2011E-20.0%0.0%20.0%40.0%60.0%80.0%100.0%

Sales Revenue Sales Growth

3.6%

-26.0%

1.3% -3.4%

58.8%37.0%

0.0%

-200,000400,000600,000800,000

1,000,0001,200,000

2005 2006 2007 2008E 2009E 2010E 2011E-30.0%-10.0%10.0%30.0%50.0%70.0%90.0%

Methanol-IMCCarbon Monoxide

BDO-Beutaidiol-IDLAcetic Acid & Acetic Anhydride

Malice anhydrideVinyl Actate Monomer

Production Growth

Chart 21: Production Growth (Tons)

Source: Company Reports & Global Research

Sale revenues growthThe price of crude oil is expected to remain on the higher side, despite an expected relaxation in prices in 2009, which will force the price of methanol, VAM and BDO to remain on the higher side as compared to the average prices by the end of 2007. While the prices of methanol is expected to relax down to US$304.1 per ton by 2011 as compared to US$472.6 per ton in 2007. However, YoY basis, our expected average prices of methanol is expected to depict a decline of 34.2% in 2009, 7.1% in 2010 and 5.2% in 2011. Moreover, the completion of Acetyl Complex by 3Q2009, will help the Company to register a growth in sales revenue, which is expected to increase at a CAGR of 12.5%, during 2007-11.

Chart 22: Sales Revenues (SR mn)

Source: Company Annual Reports & Global Research

Sales revenue mixCurrently, the sales revenue of the Company is mainly composed on the sales of methanol, which constitute 68.3% in 2007, which is mainly due to the higher contribution in the overall production of the Company. The contribution in 2008 is expected to remain at same level as it recorded in 2007, since no new production is expected to come online during the year. However, upon the completion of acetyl complex, in 3Q2009, the product line of the Company will expand and utilize 70% production of methanol as a feed stock for IAC. Thus, the contribution from methanol will decline to 35.2% in 2009, which will further get diluted in 2010 and reach 21.2% in 2011 with an increasing contribution of VAM in total sales. Furthermore, we expect 80% of AA production will use as the feed stock for the production of VAM.

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM 2�

9.1%9.7%

6.8%7.0%9.1%

10.2%9.2%

-100.0200.0300.0400.0500.0600.0700.0800.0900.0

1,000.0

2005 2006 2007 2008E 2009E 2010E 2011E0.0%

2.0%

4.0%6.0%

8.0%

10.0%12.0%

Profitability ROAA

19.0%18.6% 17.3%

12.3%10.7%

14.3%12.6%

-

200.0

400.0

600.0

800.0

1,000.0

2005 2006 2007 2008E 2009E 2010E 2011E0.0%

5.0%

10.0%

15.0%

20.0%

Profitability ROAA

62.7%70.2%

57.8%

-200.0400.0600.0800.0

1,000.01,200.01,400.01,600.0

2007 2008E 2009E 2010E 2011E0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%

58.3%60.0%

Growth Profit Growth Margins

Chart 23: Sales Revenue Mix 2008E Chart 24: Sales Revenue Mix 2011E

Source: Global Research

Improving gross profit marginsThe gross margin of the Company is expected to shown an improvement and will reach 70.5% by the end of 2008 from 62.7% in 2007. This is mainly due to the expected increase in methanol prices in international market with the feedstock availability at US$0.75 per mmbtu in Saudi Arabia. Furthermore, the completion of acetyl complex in 3Q2009 will increase the depreciation cost, which will result in a contraction in gross profit margins for the Company and limited GP margins in the range of 57%-60%.

Chart 25: Improving Gross Profit (SR mn) & Margins

Source: Global Research

Improving ProfitabilityThe Company is expected to register after tax profit of SR611.2mn (translating into EPS of SR1.8) in 2008 as compared to SR593.9mn in 2007. The increase in 2008 profitability is mainly due to the improvement in gross margins. Furthermore, we expect the return on average assets (ROAA) of the Company will remain at 7.0% in 2008 as compared to 9.1% in 2007. This is mainly due to a higher CAPEX on account of Acetyl Complex. The return on average equity (ROAE), on the other hand, is expected to dilute from 17.3% in 2007 to 12.3% in 2008, which is mainly due to higher equity-base following rights issue. However, the completion of Acetyl Complex will lead the profitability of the Company to increase at a CAGR of 10.2%, during 2007-11.

Chart 26: Profitability (SR mn) & ROA Chart 27: Profitability (SR mn) & ROE

Source: Company Reports & Global Research

Malice Anhydride23.4%

Methano-IMC68.3%

BDO-Beutaidiol-IDL8.3%

Methano-IMC 21.2%

BDO-Beutaidiol-IDL5.0%

Malice Anhydride15.3%Carbon Monoxide 15.3%

Vinyl Acetate Monomer34.5%

Global Research - Saudi Arabia Global Investment House

�0 October 2008Saudi International Petrochemical Company - SIPCHEM

Acetyl Complex & Impact On Profitability

The future growth of SIPCHEM is based on the timely completion of the Acetyl Complex. The complex comprises of three plants which are vertically integrated with each other and also the methanol plant as well. Hence, the feedstock of the additional capacity is internal generated, which will help the Company to reduce costs (excluding depreciation).

Figure 02: Acetyl Complex Production Flow

Source: SIPCHEM Prospectus & Global Research

We have conducted a sensitivity analysis of the commencement of production from acetyl complex by using different time scenario.

Table 18: Acetyl Complex Commissioning (EPS in SR)-Scenario AnalysisBase

Assumption*

Commencement

in 1Q2010

Commencement

in 3Q2010

Commencement

in 1Q2011

Commencement

in 3Q2011

2008E 1.8 1.8 1.8 1.8 1.8

2009E 2.0 0.9 0.9 0.9 0.9

2010E 2.8 2.8 1.7 0.6 0.6

2011E 2.6 2.6 2.6 2.6 1.6

* Expected commencement of production from acetyl complex in 3Q2009Source: Global Research

Complexes Feed Stocks

CO Plant 300,000 tons AA plant 450,000 tons VAM 300,000 tons

Methanol Ethylene OxygenNatural Gas

Common Utilities

Port Facilities

H2 65,000

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM ��

Polyolefins Complex

The next expansion plan of the Company is the establishment of envisaged olefins complex, which will comprise a world scale ethane/propane cracker manufacturing facilities for producing various derivatives including polymers, speciality chemicals, engineering plastics, fabricated plastics and value added downstream products. The project was initially expected to come online by the end of 2012 and now the status of this project is unclear, so we have not taken the impact of this project in our valuation.

Figure 03: SIPCHEM Polyolefins Complex Production Flow

Prim

ary

Seco

ndar

y

Ole

fins

Cra

cker

By

Pro

duct

s

Eth

ylen

e 1m

n to

ns

Pro

pyle

ne 2

20,0

00 t

ons

Am

mon

ia 6

00,0

00 t

ons

AC

N 2

00,0

00

tons

PAN

50,

000

tons

Car

bon

Fib

er

3,00

0 t

ons

LD

PE

400

,000

ton

s

HD

PE

400

,000

ton

s

VA

M 3

30,0

00 t

ons

MM

A 2

50,0

00 t

ons

PM

MA

30,

000

tons

Sodi

um C

yani

de

50,0

00 t

ons

HD

Pip

e 15

,000

to

ns

HD

Flil

ms

20,0

00 t

ons

HD

Pal

lets

30

,000

ton

s

PV

A

PV

OH

40,

000

tons

EV

OH

15,

000

tons

Sour

ce:

SIP

CH

EM

Pro

spec

tus

& G

loba

l Res

earc

h

Global Research - Saudi Arabia Global Investment House

�2 October 2008Saudi International Petrochemical Company - SIPCHEM

9M-2008 Financial Results

SIPCHEM has reported a net profit of SR502.1mn in 9M-2008, against the net profit of SR339.9mn in corresponding period last year. The improvement in profitability is mainly due to the increase in methanol prices from US$401.0 per ton to US$579.0 per ton, with the subsidized prices of feedstock gas at US$0.75 per mmbtu. Consequently, the Company has shown an improvement in gross margins, which had recorded at 61.6%, in 9M-2008, as compared to 58.0% in the corresponding period last year.

Table 19: 9M-2008 Income Statement

SR ‘000’ 9M-2007 9M-2008 Change

Net Sales 1,025,648 1,472,076 43.5%

Cost of Sales (430,772) (565,603) 31.3%

Gross Profit 594,876 906,473 52.4%

Selling, General & Administrative Expenses (37,359) (45,055) 20.6%

Operating Income 557,516 861,417 54.5%

Financial Charges (71,766) (62,779) -12.5%

Other Income 5,335 11,388 113.5%

Investment Income 25,829 31,049 20.2%

Net Expenses of pre-operating expenses + Provision for project

developmental cost(623) (54,639) 8670.3%

Minority Interest (160,168) (259,742) 62.2%

Net Profit Before Zakat 356,123 526,694 47.9%

Zakat (16,229) (24,636) 51.8%

Net Profit After Zakat 339,893 502,058 47.7%

Source: Company Accounts

The balance sheet size of the company, during 9M-2008, has increased by 23.4% from the reported size of SR7.8bn by the end of 2007. During the period, share capital of the company has increased from SR2bn to SR3.3bn, which is mainly due to issuance of right shares at SR15 per share with SR5 per share as a premium to finance the acetyl project. On the other hand, the obligation of the Company has shown a decline of 9.1%, during the period under review, to SR3.5bn from SR3.8bn by the end of 2007, thus improving the current ratio to 2.4x, in 9M-2008, as compared to 0.92x by the end of 2007.

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM ��

Table 20: 9M-2008 Balance Sheet

SR ‘000’ 2007 9M-2008

Assets

Total Current Assets 1,995,522 2,215,316

Total Fixed Assets 5,755,300 7,076,267

Other Assets - 273,699

Total Assets 7,750,822 9,565,282

Liabilities & Equity

Total Current Liabilities 2,164,335 905,812

Total Non-Current Liabilities 1,694,328 2,602,643

Provisions - -

Total Liabilities & Provisions 3,858,663 3,508,454

Minority Interest 895,292 926,416

Shareholders’ Equity

Share Capital 2,000,000 3,333,333

Statutory Reserves 176,947 860,828

General Reserves 275,000 275,000

Retained Earnings 544,920 661,249

Total Shareholders’ Equity 2,996,867 5,130,410

Total Liabilities & Shareholders> Equity 7,750,822 9,565,282

Source: Company Accounts

Global Research - Saudi Arabia Global Investment House

�� October 2008Saudi International Petrochemical Company - SIPCHEM

Valuation and Recommendation

Discounted Cash Flows MethodologyOur DCF model is based on a 4-year (FY2008-FY2011) explicit forecast period for the Free Cash Flow (FCF). The terminal value is estimated using the constant growth Gordon Growth Model (GGM). The forecasted cash flow and the terminal value is then discounted at the company Weighted Average Cost of Capital (WACC). In our DCF valuation, we have used the following assumptions:

1. Risk Free Rate (RFR) of 5.4%.

2. Equity risk premium of 5.5%.

3. Beta of 1.05.

4. A terminal growth rate of 3.0%.

5. A target cost of debt of 7%.

Using the above assumptions, we have derived a cost of equity for the Company at 11.4%, by using Capital Assets Pricing Model, and a WACC of 10.0%, resulting in a fair value of SR35.9 per share.

Table 21: DCF Calculations

(SR Mn) 2008 (E) 2009 (E) 2010 (E) 2011 (E)

FCF (713) 910 399 1,095

Discounted Cash Flow (679) 789 314 784

Terminal Value 15,083

Primary Value 1,209

Terminal Value (discounted) 11,185

Total Enterprise Value 12,375

Debt (2365) (As of 2008E)

Add: Investments & cash equivalents 1,960 (As of 2008E)

Total Equity Value 11,970

Shares Outstanding (’000) 333,333

Fair Value Per Share 35.9

Source: Global Research

Sensitivity AnalysisWe provide below a sensitivity analysis table, which shows the probable value given different growth rate assumption and WACC. The shaded area represents the most probable outcomes.

Table 22: Sensitivity Analysis Terminal Growth Rates

1.50% 2.50% 3.00% 3.50% 4.50%

WA

CC

8.48% 40.0 46.7 51.0 56.1 70.2

9.48% 34.3 39.3 42.3 45.8 55.0

10.48% 29.9 33.7 35.9 38.5 44.9

11.48% 26.4 29.3 31.1 33.0 37.8

12.48% 23.5 25.8 27.2 28.7 32.4

Source: Global Research

Global Research - Saudi Arabia Global Investment House

October 2008 Saudi International Petrochemical Company - SIPCHEM ��

Relative Valuation For relative valuation, we have made a comparison of SIPCHEM with selected regional and international players.

Table 23: Relative Comparison

Company Name Country Name

Market

Price

(Local)

Adjusted

Market

Price

(US$)

Adjusted

Market

Cap

(US$mn)

EV/

EBITDA

2008

Mitsui Chemicals Inc JAPAN 352.0 3.6 2,814.2 7.3

FMC Corp UNITED STATES 36.3 37.3 2,786.9 8.4

JSR Corp JAPAN 1,055.0 10.6 2,725.0 6.2

Teijin Ltd JAPAN 266.0 2.7 2,644.1 6.4

Lubrizol Corp UNITED STATES 37.0 37.9 2,567.6 5.6

Umicore BELGIUM 14.8 20.4 2,551.3 9.9

Fertilizantes Fosfatados SA BRAZIL 11.8 5.7 2,434.4 13.4

Braskem SA BRAZIL 9.9 4.8 2,312.2 7.3

Sinofert Holdings Ltd HONG KONG 2.5 0.3 2,336.7 11.1

Albemarle Corp UNITED STATES 23.5 24.1 2,202.2 8.6

Hitachi Chemical Co Ltd JAPAN 1,013.0 10.2 2,130.6 4.2

China BlueChemical Ltd CHINA 3.4 0.5 2,086.5 6.6

Hercules Inc UNITED STATES 17.8 18.2 2,056.8 5.9

Showa Denko KK JAPAN 160.0 1.6 2,016.0 5.7

Yantai Wanhua Polyurethanes C CHINA 8.1 1.2 2,018.0 18.6

Valspar Corp UNITED STATES 19.5 20.0 1,997.2 7.9

RPM International Inc UNITED STATES 14.8 15.2 1,961.1 7.3

Terra Industries Inc UNITED STATES 20.5 21.1 1,934.2 3.7

Ube Industries Ltd/Japan JAPAN 181.0 1.8 1,843.5 6.9

Makhteshim-Agan Industries Lt ISRAEL 1,620.0 4.4 1,925.6 8.6

Mitsubishi Gas Chemical Co In JAPAN 367.0 3.7 1,791.1 6.7

Symrise AG GERMANY 10.7 14.7 1,732.1 9.0

IRPC PCL THAILAND 2.9 0.1 1,690.8 7.7

Ashland Inc UNITED STATES 25.4 26.1 1,642.5 3.4

Nufarm Ltd AUSTRALIA 12.3 8.7 1,624.9 11.7

PTT Chemical PCL THAILAND 36.5 1.1 1,639.1 6.8

Altana AG GERMANY 8.5 11.6 1,632.8 6.7

Huabao International Holdings HONG KONG 4.0 0.5 1,628.7 11.9

Clariant AG SWITZERLAND 7.8 7.0 1,622.4 5.5

Lanxess AG GERMANY 14.1 19.4 1,613.4 4.8

Arkema SA FRANCE 19.0 26.2 1,602.4 5.8

Cabot Corp UNITED STATES 24.3 24.9 1,602.2 5.7

Air Water Inc JAPAN 847.0 8.5 1,583.5 5.6

Kaneka Corp JAPAN 443.0 4.5 1,565.1 4.8

Saudi International Petrochem SAUDI ARABIA 22.3 6.1 2,020.9

Source: Bloomberg * As on 19th October 2008

Global Research - Saudi Arabia Global Investment House

�� October 2008Saudi International Petrochemical Company - SIPCHEM

The comparison is made on sector EV/EBITDA of 2008, which is calculated at 7.4. By employing the sector EV/EBITDA on the Company’s EBITDA, our fair value of the Company arrives at SR32.7. Consolidated Fair ValueIn order to arrive at a consolidated fair value for the Company, we have assigned 80% weightage to the value arrived from DCF base valuation and 20% to the relative value. On the basis of this, our consolidated value for the Company comes at SR35.3.

Table 24: Consolidated Fair Value