Embed Size (px)

Citation preview

Global Transfer Pricing ConferenceRegulatory developments in Canada

October 2016

www.pwc.com/transferpricing

The new normal – full TransParency

Global Transfer Pricing Conference │ October 2016

Today’s presenters

PwC │ 2

Gord JansCanada

Olivier Paul-HusCanada

Lav ChadhaCanada

Shiraj KeshvaniCanada

Global Transfer Pricing Conference │ October 2016

Agenda

PwC │ 3

Introduction1

TPM 17 and RevenuQuébec audit 2

TP dispute resolution 4

Panel Q&A 5

Global Transfer Pricing Conference │ October 2016

BEPS in action3

Global Transfer Pricing Conference │ October 2016

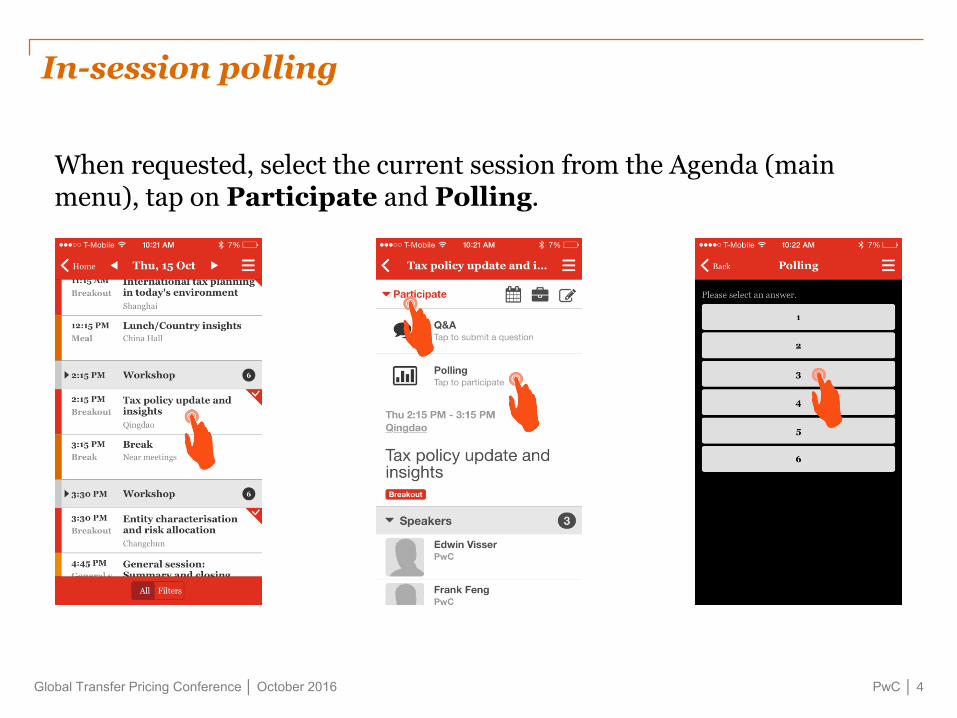

In-session polling

When requested, select the current session from the Agenda (main menu), tap on Participate and Polling.

PwC │ 4

TPM 17 and Revenu Québec audit

1

Global Transfer Pricing Conference │ October 2016

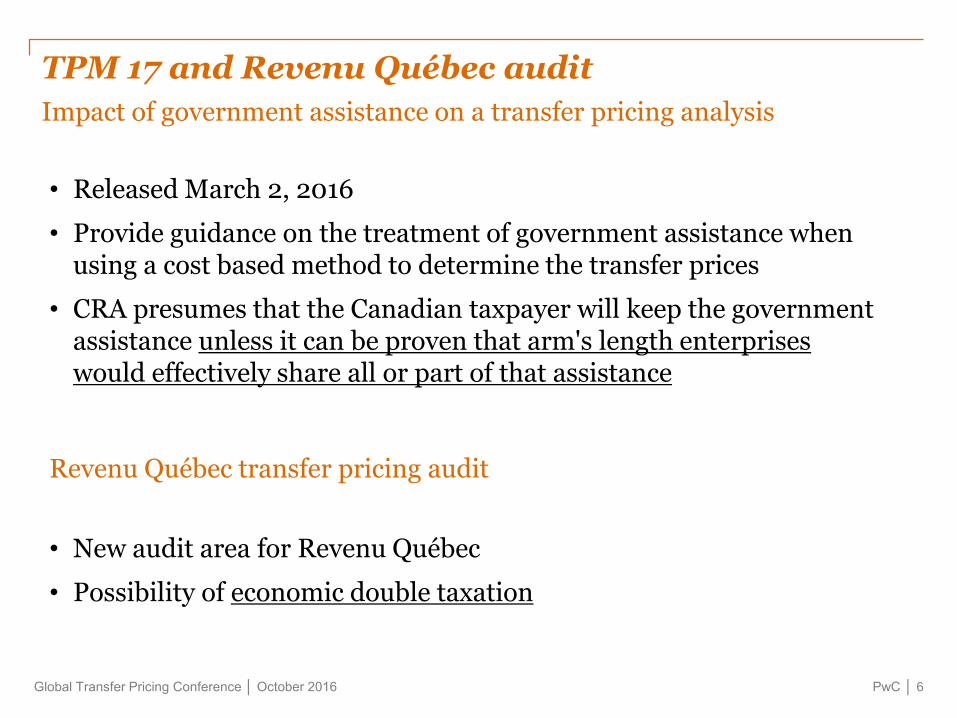

TPM 17 and Revenu Québec audit

PwC │ 6

Impact of government assistance on a transfer pricing analysis

• Released March 2, 2016

• Provide guidance on the treatment of government assistance when using a cost based method to determine the transfer prices

• CRA presumes that the Canadian taxpayer will keep the government assistance unless it can be proven that arm's length enterprises would effectively share all or part of that assistance

Revenu Québec transfer pricing audit

• New audit area for Revenu Québec

• Possibility of economic double taxation

Global Transfer Pricing Conference │ October 2016

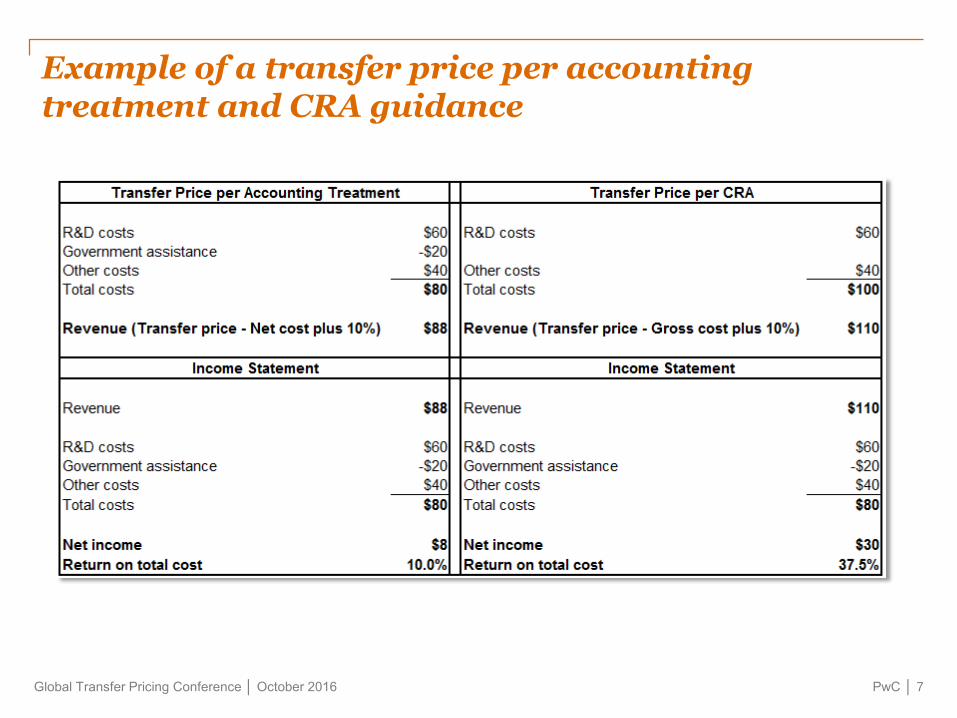

Example of a transfer price per accountingtreatment and CRA guidance

PwC │ 7

Global Transfer Pricing Conference │ October 2016

Polling question 1

A. Reduce the cost base by the amount of

governmental assistance

B. Do not reduce the cost base by the

amount of governmental assistance.

C. This situation does not apply to us

D. PwC participant

How is your company treating

governmental assistance under

a cost plus transfer pricing

policy?

PwC │ 8

Global Transfer Pricing Conference │ October 2016

Polling question 2

A. Yes

B. No

C. PwC participant

Has your company ever

faced a provincial transfer pricing

audit?

PwC │ 9

BEPS in action

2

Global Transfer Pricing Conference │ October 2016

BEPS in action

PwC │ 11

Canada’s influence seen in BEPS Guidelines

“The OECD developed a “responsible response” with its 15-point action plan to combat BEPS. [However] much of what it contains is heavily influenced by Canadian practice.”

“For us very much we see the [new] OECD guidelines as a clarification and extension of what has always existed in Canada to other jurisdictions”

Assistant Commissioner, Large Business and Investigation Branch, CRA.

Global Transfer Pricing Conference │ October 2016

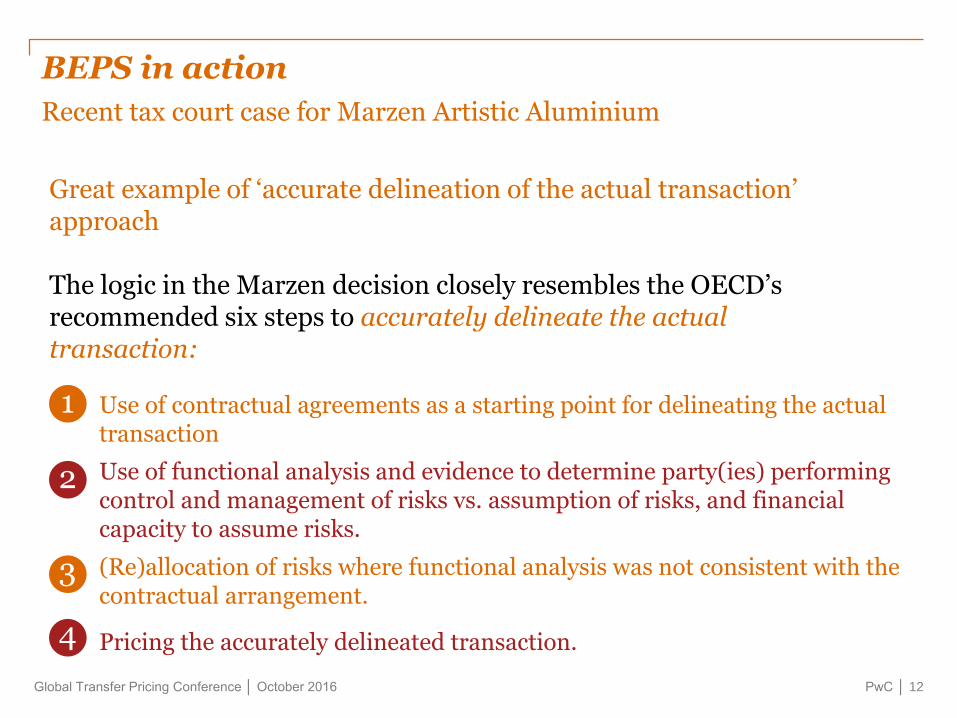

BEPS in action

PwC │ 12

Recent tax court case for Marzen Artistic Aluminium

Great example of ‘accurate delineation of the actual transaction’ approach

The logic in the Marzen decision closely resembles the OECD’s recommended six steps to accurately delineate the actual transaction:

Use of contractual agreements as a starting point for delineating the actual transaction

1

Use of functional analysis and evidence to determine party(ies) performing control and management of risks vs. assumption of risks, and financial capacity to assume risks.

2

(Re)allocation of risks where functional analysis was not consistent with the contractual arrangement.

3

Pricing the accurately delineated transaction.4

Global Transfer Pricing Conference │ October 2016

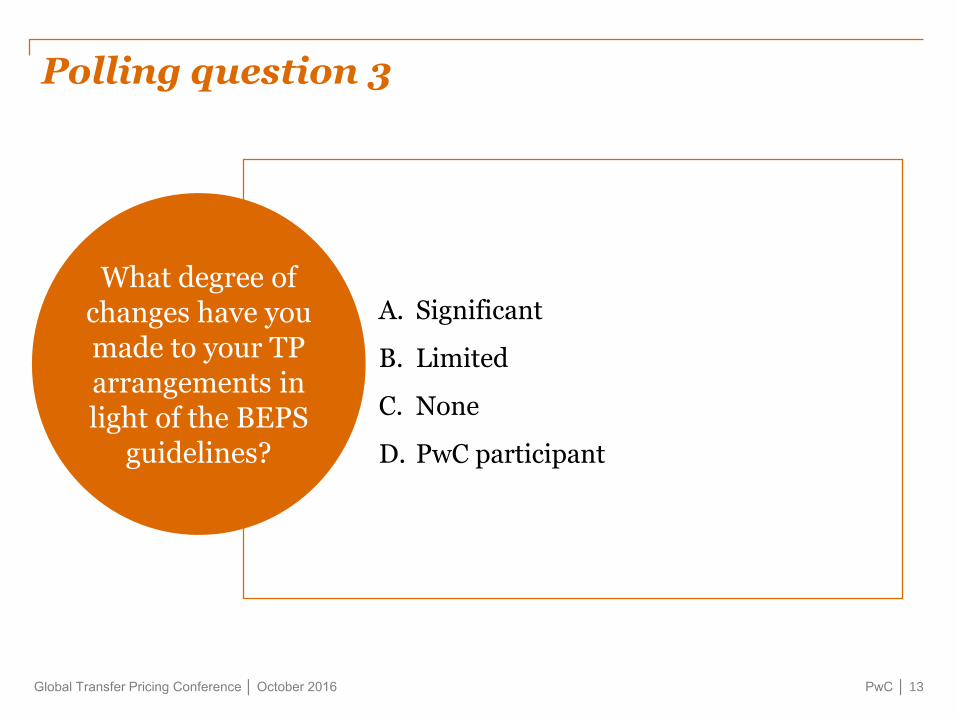

Polling question 3

A. Significant

B. Limited

C. None

D. PwC participant

What degree of changes have you made to your TP arrangements in light of the BEPS

guidelines?

PwC │ 13

TP dispute resolution

3

Global Transfer Pricing Conference │ October 2016

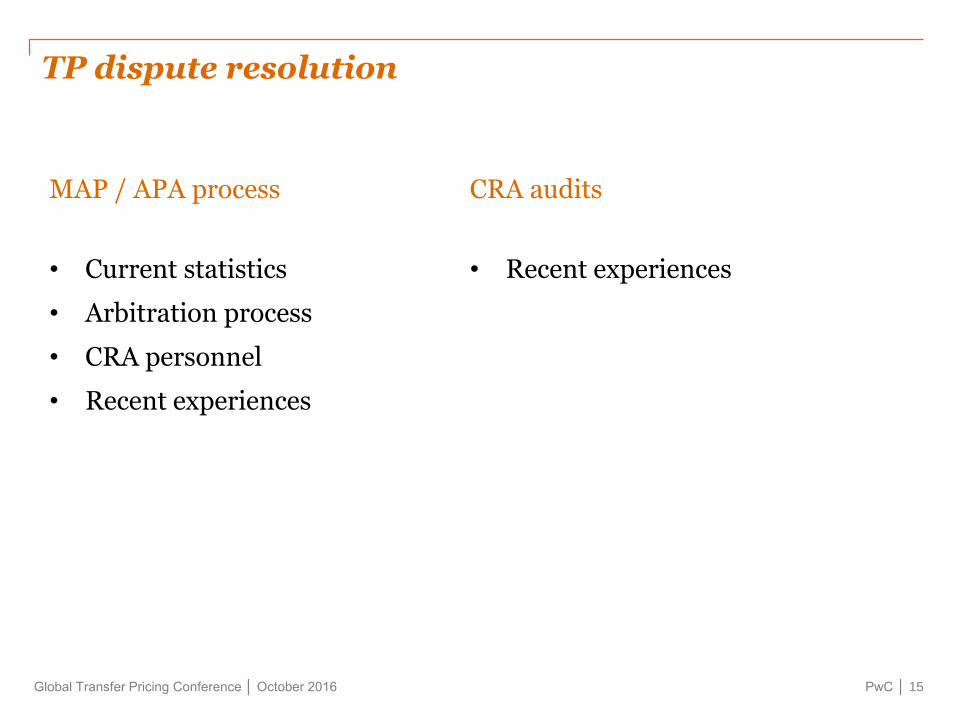

TP dispute resolution

PwC │ 15

MAP / APA process

• Current statistics

• Arbitration process

• CRA personnel

• Recent experiences

CRA audits

• Recent experiences

Global Transfer Pricing Conference │ October 2016

Polling question 4

A. Very comfortable

B. Somewhat comfortable

C. Not at all comfortable

D. PwC participant

How comfortable are you that your

business documents (i.e. evidence) aligns

to your TP documentation?

PwC │ 16

Global Transfer Pricing Conference │ October 2016

In-session Q&A

PwC │ 17

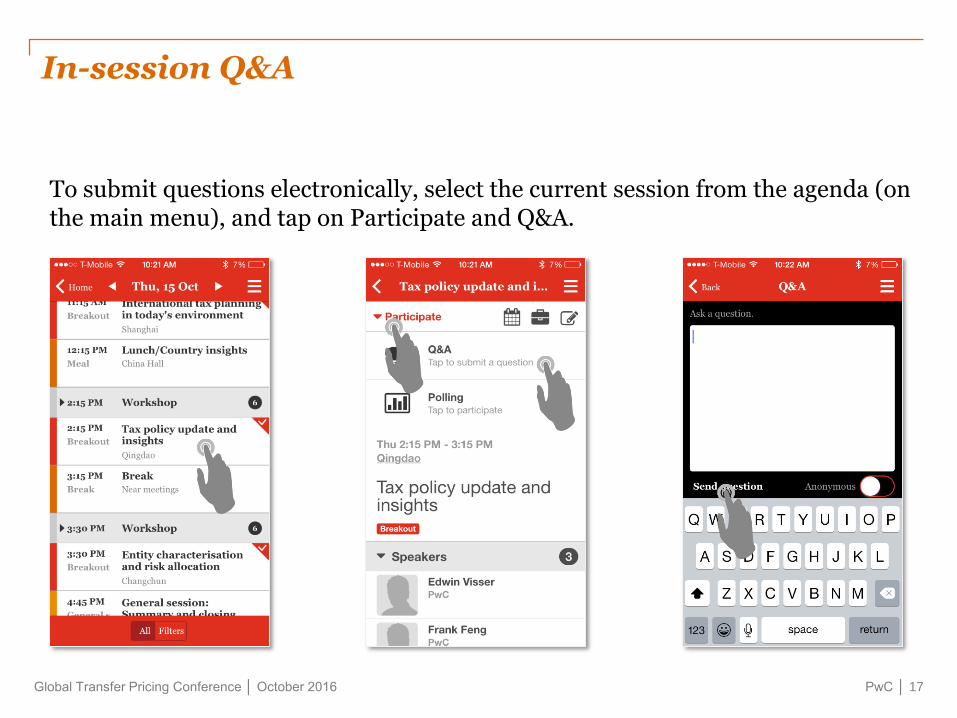

To submit questions electronically, select the current session from the agenda (on the main menu), and tap on Participate and Q&A.

Global Transfer Pricing Conference │ October 2016

Panel Q&A

PwC │ 18

Global Transfer Pricing Conference │ October 2016

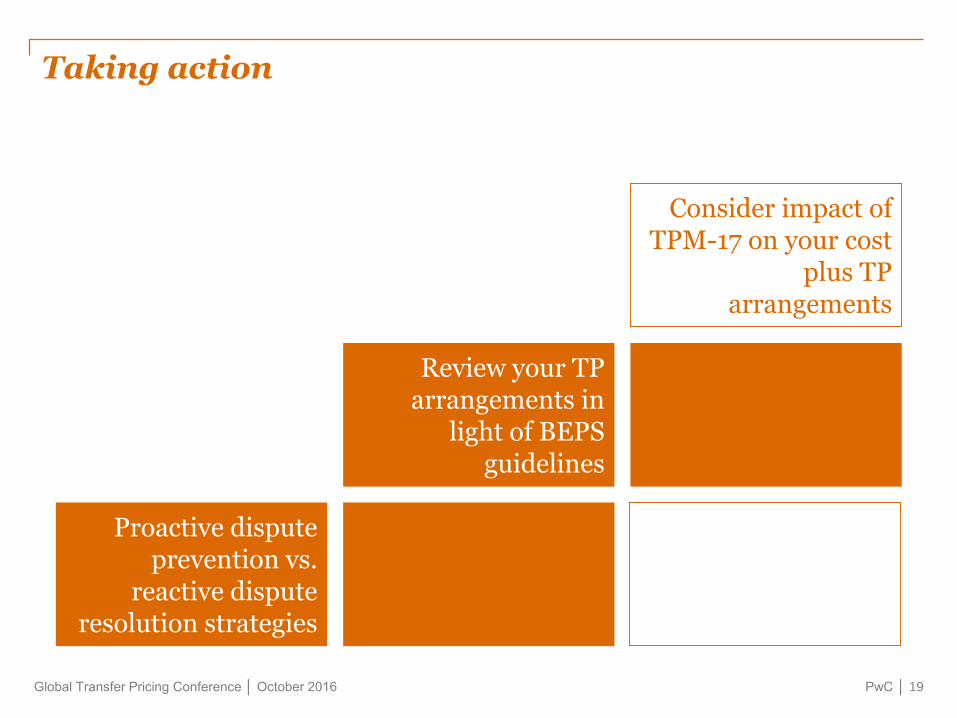

Taking action

Proactive dispute prevention vs.

reactive dispute resolution strategies

Review your TP arrangements in

light of BEPS guidelines

Consider impact of TPM-17 on your cost

plus TP arrangements

PwC │ 19

Global Transfer Pricing Conference │ October 2016

What did you think?

PwC │ 20

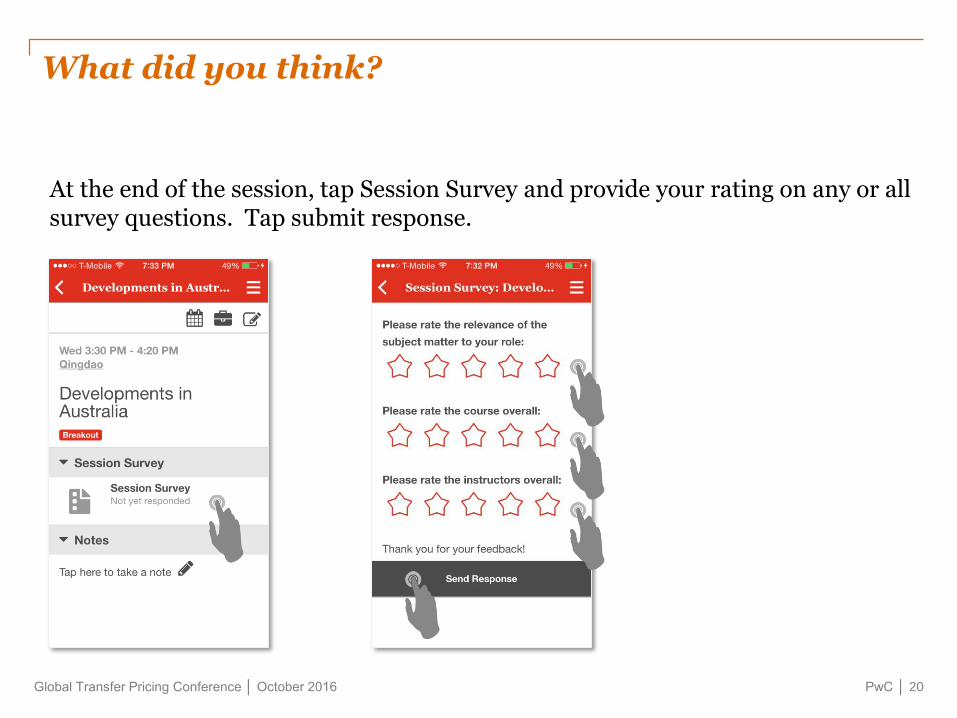

At the end of the session, tap Session Survey and provide your rating on any or all survey questions. Tap submit response.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the

information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the

accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC does not accept or assume any liability,

responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or

for any decision based on it.

© 2016 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see

www.pwc.com/structure for further details.

Design services 30335_PRES_09/16

Thank you