Embed Size (px)

Citation preview

Global Trends AffectingGlobal Trends Affectingthe U.S. Forest Sectorthe U.S. Forest Sector

Jim L. BowyerUniversity of Minnesota

Department of Bio-based ProductsSt. Paul, MN

Global Trends Affecting the U.S. ForestGlobal Trends Affecting the U.S. ForestSectorSector

nn Global mega-trends that will impact theGlobal mega-trends that will impact the forest sector forest sectornn National trends important to forestry National trends important to forestrynn Implications of global and national trends Implications of global and national trends

for the forest products industry of the N.E. for the forest products industry of the N.E.nn The emerging bio-economy The emerging bio-economynn The bio-economy, bio-energy and the N.E. The bio-economy, bio-energy and the N.E. forest products industry forest products industry –– threat or threat or opportunity? opportunity?nn Positioning for the future Positioning for the future

Global Mega-Trends thatGlobal Mega-Trends thatwill Impact the Forestwill Impact the Forest

SectorSector

Global Mega-TrendsGlobal Mega-Trends

nn Globalization Globalization

nn Expansion of the global economy Expansion of the global economy

nn Growth of energy demand and Growth of energy demand and

the approach of peak petroleum the approach of peak petroleum

nn Increasing interest in bio-energy Increasing interest in bio-energy

nn Growth of global fiber supplies Growth of global fiber supplies

nn Rising global competition Rising global competition

Global Mega-TrendsGlobal Mega-Trends

nn GlobalizationGlobalization

nn Expansion of the global economy Expansion of the global economy

nn Growth of energy demand and Growth of energy demand and

the approach of peak petroleum the approach of peak petroleum

nn Increasing interest in bio-energy Increasing interest in bio-energy

nn Growth of global fiber supplies Growth of global fiber supplies

nn Rising global competition Rising global competition

Global Mega-TrendsGlobal Mega-Trends

nn Globalization Globalization

nn Expansion of the global economyExpansion of the global economy

nn Growth of energy demand and Growth of energy demand and

the approach of peak petroleum the approach of peak petroleum

nn Increasing interest in bio-energy Increasing interest in bio-energy

nn Growth of global fiber supplies Growth of global fiber supplies

nn Rising global competition Rising global competition

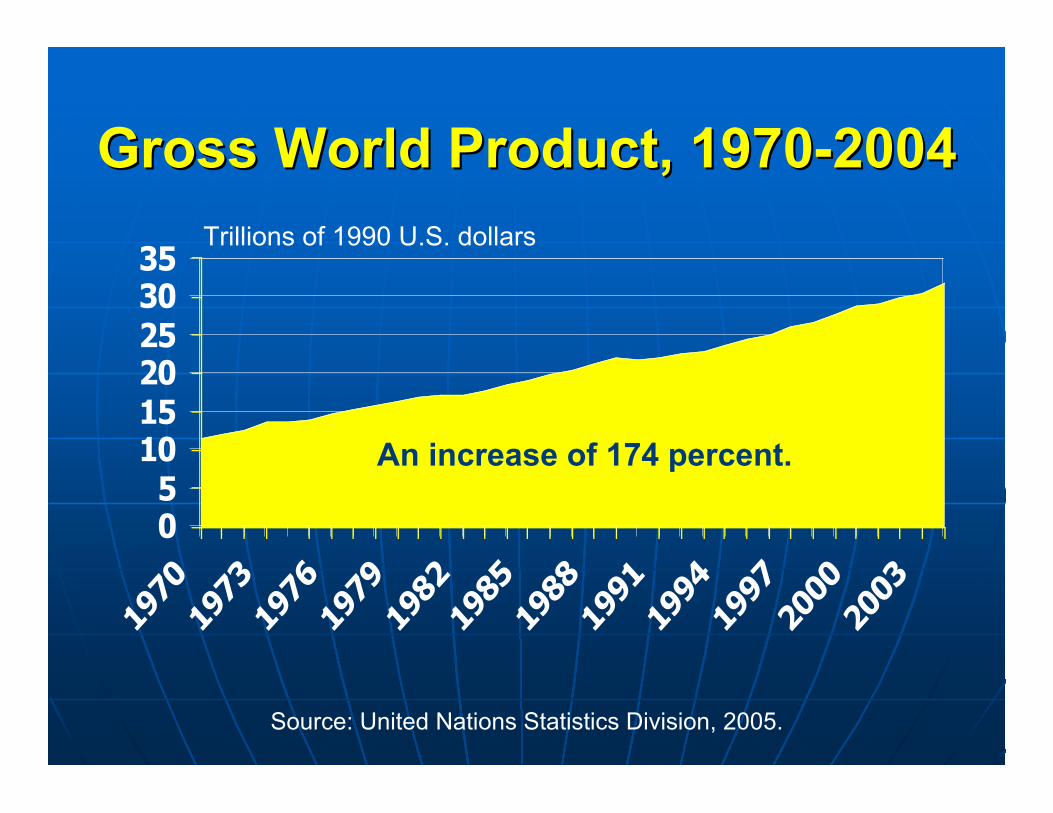

Gross World Product, 1970-2004Gross World Product, 1970-2004

05

101520253035

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

Trillions of 1990 U.S. dollars

Source: United Nations Statistics Division, 2005.

An increase of 174 percent.

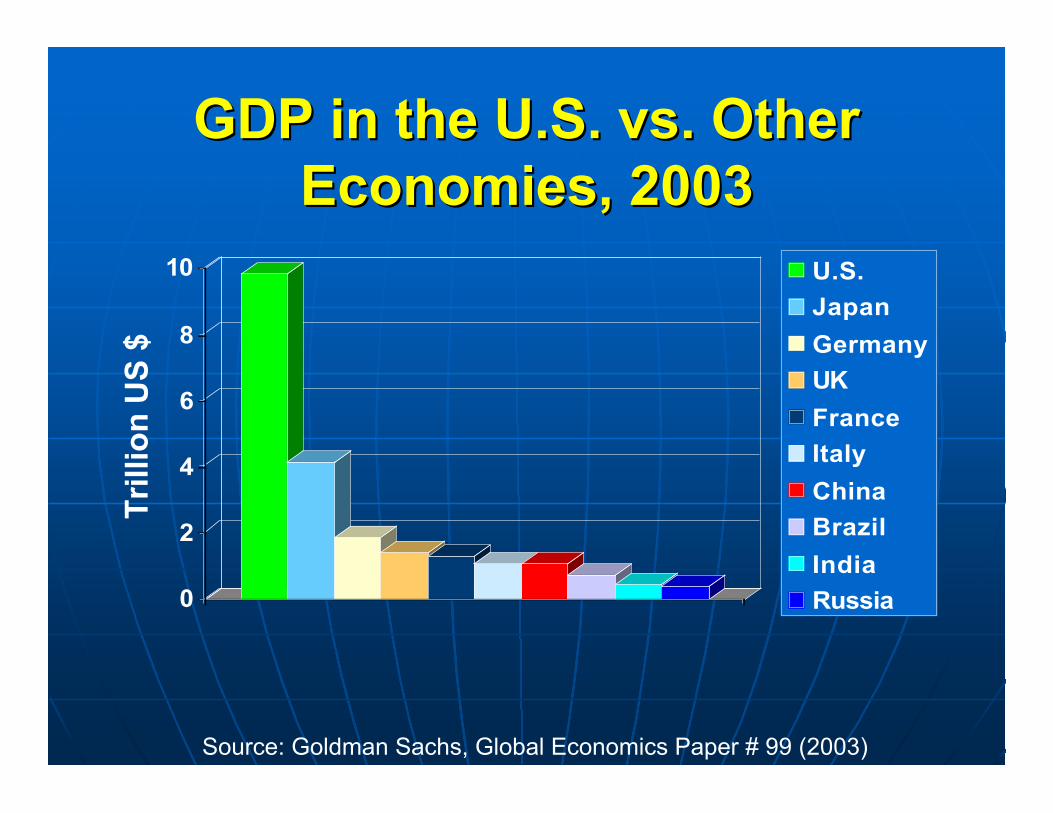

GDP in the U.S. vs. OtherGDP in the U.S. vs. OtherEconomies, 2003Economies, 2003

0

2

4

6

8

10 U.S.

Japan

Germany

UK

France

Italy

China

Brazil

India

Russia

Source: Goldman Sachs, Global Economics Paper # 99 (2003)

Tri

llio

n U

S $

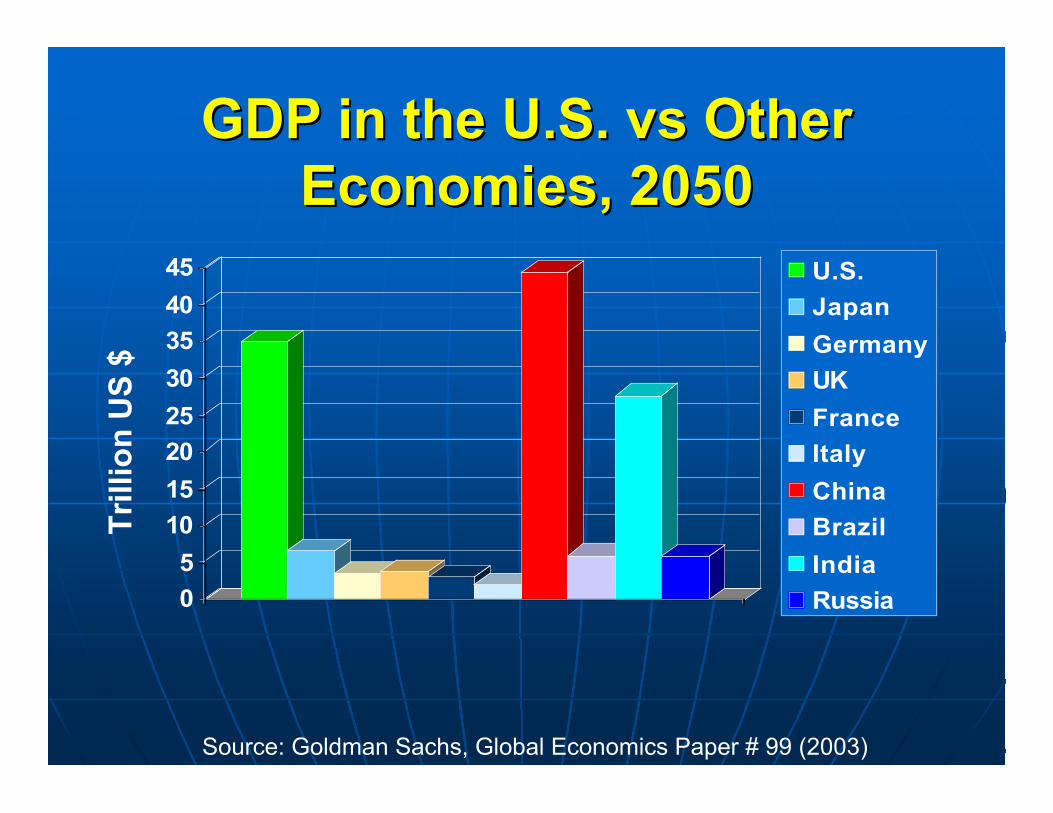

GDP in the U.S. GDP in the U.S. vsvs Other OtherEconomies, 2050Economies, 2050

0

5

10

15

20

25

30

35

40

45 U.S.

Japan

Germany

UK

France

Italy

China

Brazil

India

Russia

Source: Goldman Sachs, Global Economics Paper # 99 (2003)

Tri

llio

n U

S $

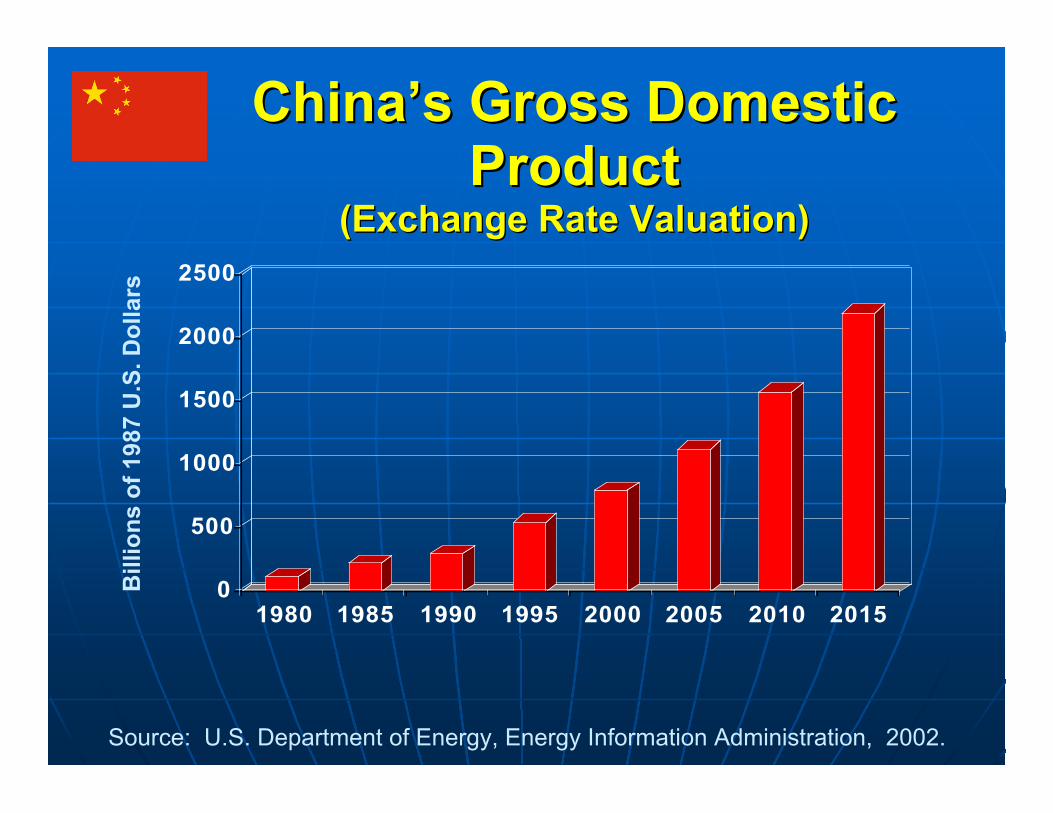

ChinaChina’’s Gross Domestics Gross DomesticProductProduct

(Exchange Rate Valuation)(Exchange Rate Valuation)

0

500

1000

1500

2000

2500

1980 1985 1990 1995 2000 2005 2010 2015

Bill

ion

s o

f 19

87 U

.S. D

olla

rs

Source: U.S. Department of Energy, Energy Information Administration, 2002.

The result is unprecedentedThe result is unprecedentedgrowth of consumptiongrowth of consumption

worldwide.worldwide.

Considering the combinedConsidering the combinedeffect of population growtheffect of population growth

and economic growth withinand economic growth withindeveloping nations, developing nations, demanddemand

forfor new housing unitsnew housing unitsglobally over the next 50globally over the next 50

years is likely to exceed years is likely to exceed oneonebillion.billion.

Global Mega-TrendsGlobal Mega-Trends

nn GlobalizationGlobalization

nn Expansion of the global economy Expansion of the global economy

nn Growth of energy demand andGrowth of energy demand and

the approach of peak petroleum the approach of peak petroleum

nn Increasing interest in bio-energy Increasing interest in bio-energy

nn Growth of global fiber supplies Growth of global fiber supplies

nn Rising global competition Rising global competition

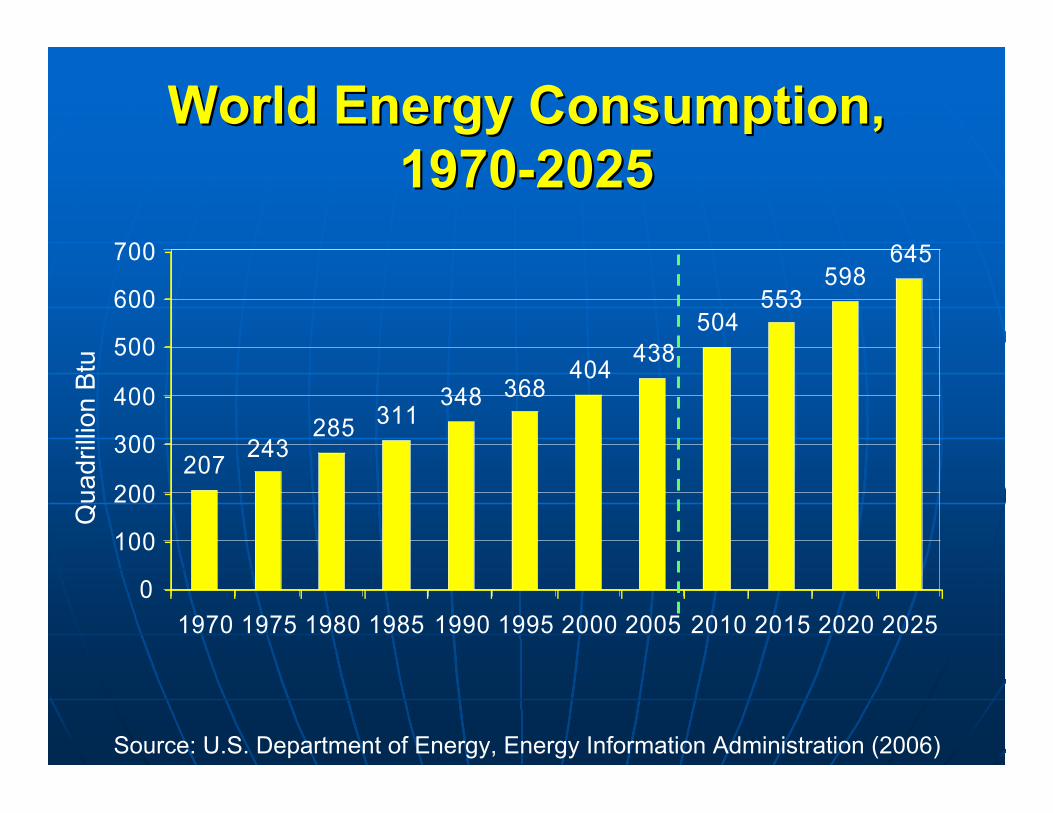

World Energy Consumption,World Energy Consumption,1970-20251970-2025

207243

285 311348 368

404

645598

553504

438

0

100

200

300

400

500

600

700

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Qua

drill

ion

Btu

Source: U.S. Department of Energy, Energy Information Administration (2006)

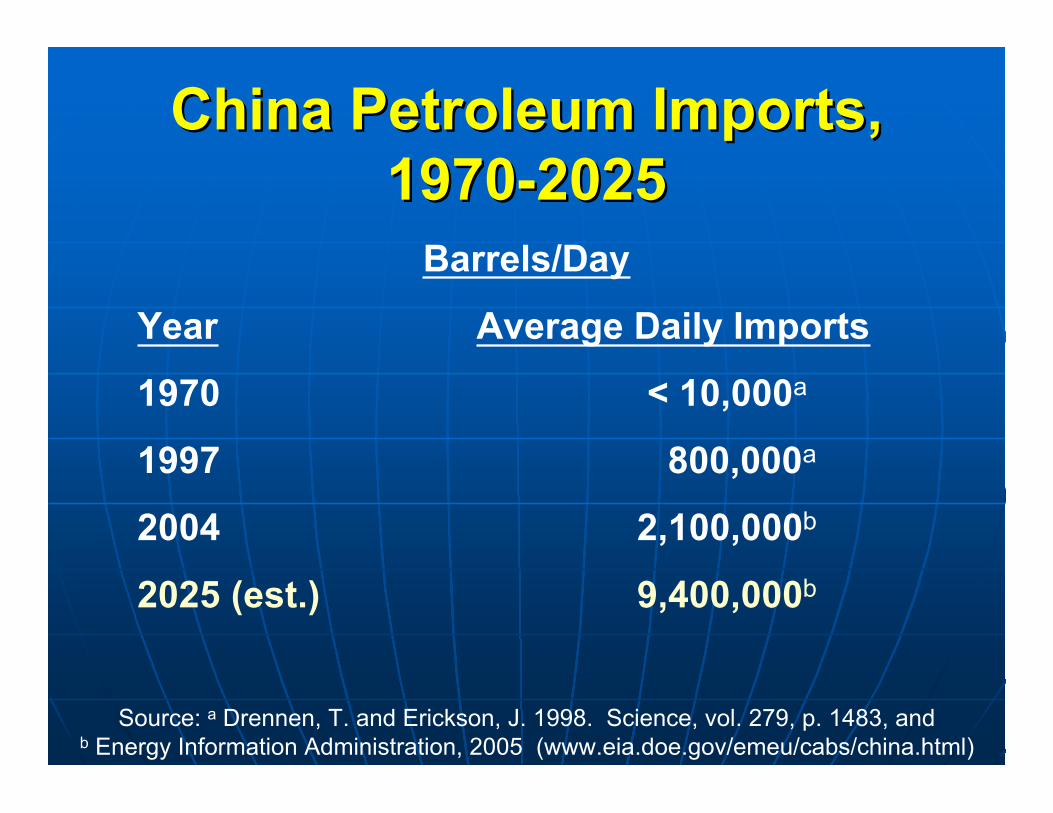

China Petroleum Imports,China Petroleum Imports,1970-20251970-2025

Barrels/Day

Year Average Daily Imports

1970 < 10,000a

1997 800,000a

2004 2,100,000b

2025 (est.) 9,400,000b

Source: a Drennen, T. and Erickson, J. 1998. Science, vol. 279, p. 1483, andb Energy Information Administration, 2005 (www.eia.doe.gov/emeu/cabs/china.html)

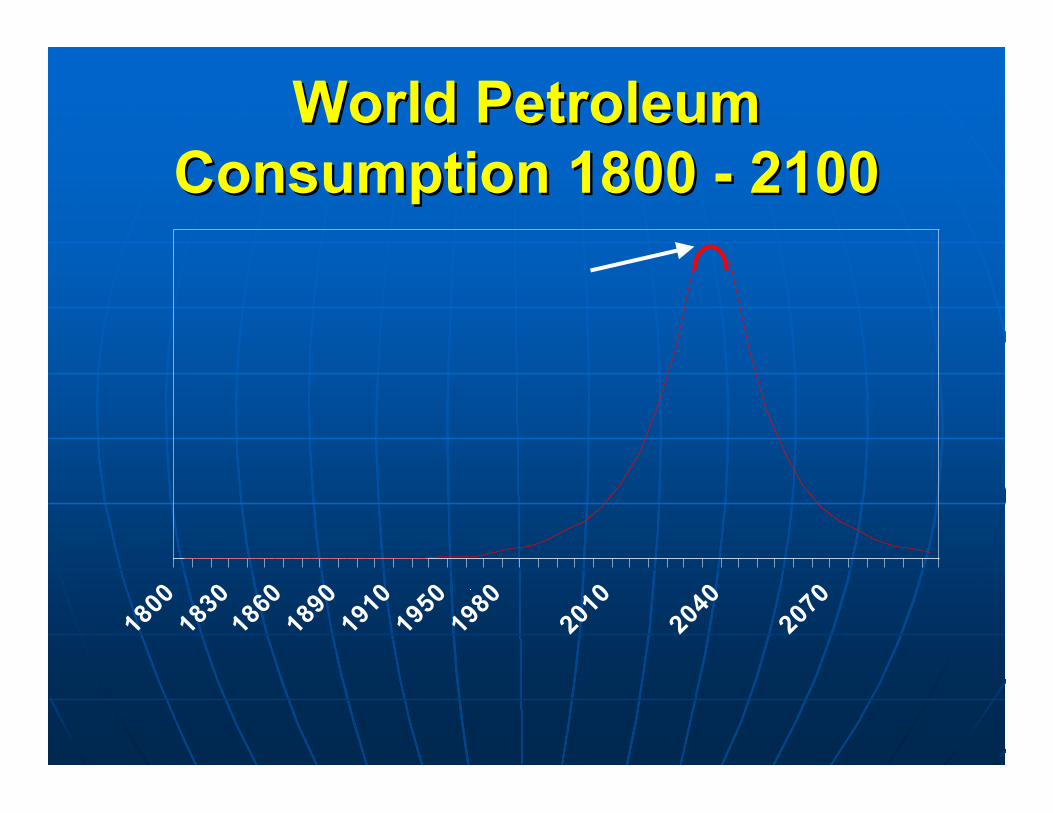

World PetroleumWorld PetroleumConsumption 1800 - 2100Consumption 1800 - 2100

18001830

18601890

19101950

19802010

20402070

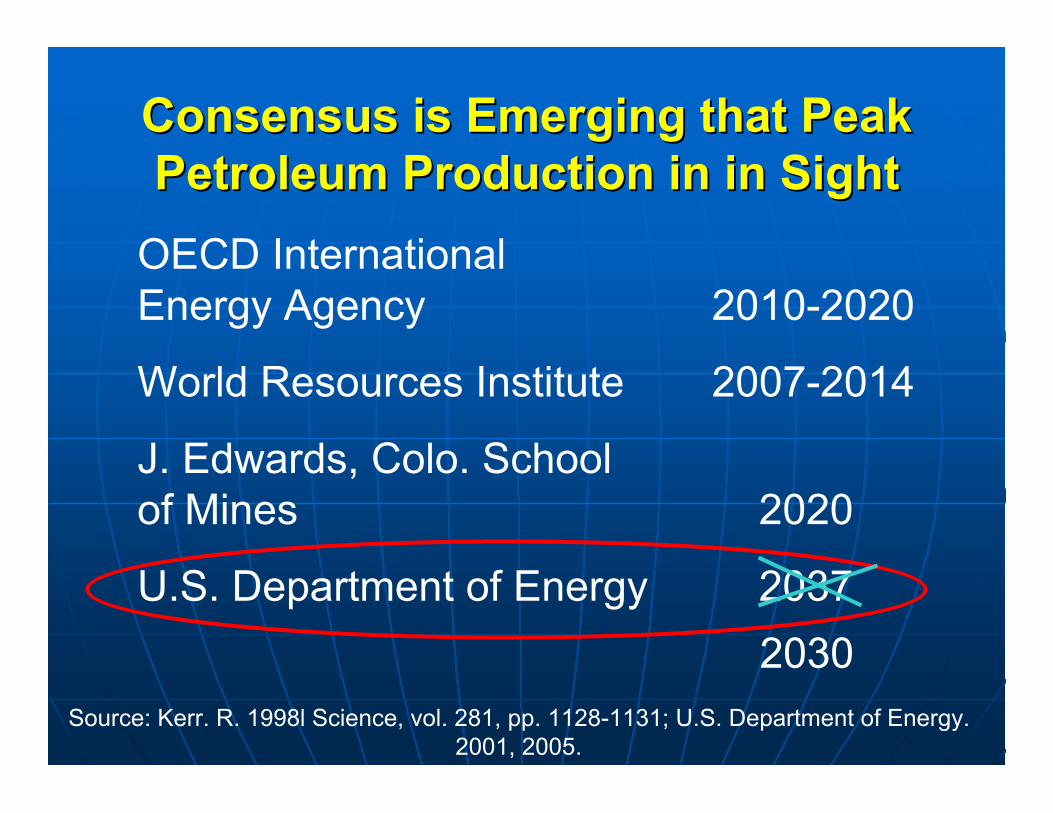

Consensus is Emerging that PeakConsensus is Emerging that PeakPetroleum Production in in SightPetroleum Production in in Sight

OECD InternationalEnergy Agency 2010-2020

World Resources Institute 2007-2014

J. Edwards, Colo. Schoolof Mines 2020

U.S. Department of Energy 2037

2030Source: Kerr. R. 1998l Science, vol. 281, pp. 1128-1131; U.S. Department of Energy.

2001, 2005.

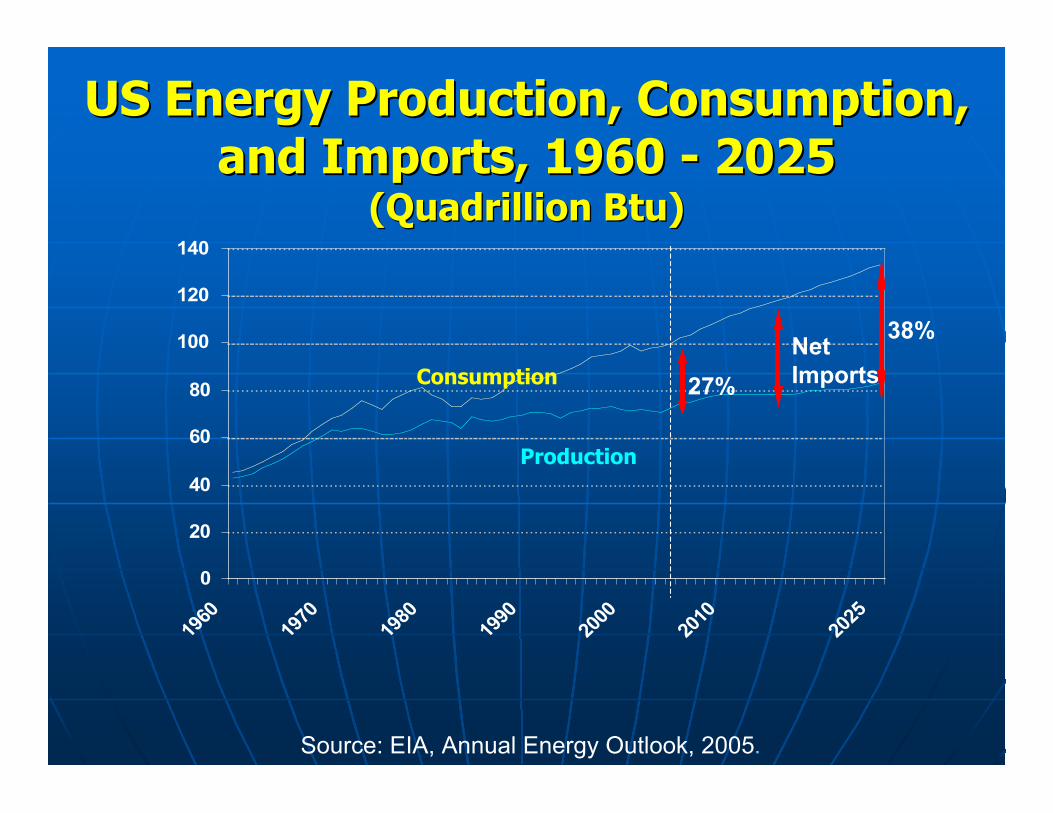

US Energy Production, Consumption,US Energy Production, Consumption,and Imports, 1960 - 2025and Imports, 1960 - 2025

(Quadrillion Btu)(Quadrillion Btu)

0

20

40

60

80

100

120

140

1960

1970

1980

1990

2000

2010

2025

Source: EIA, Annual Energy Outlook, 2005.

Consumption

Production

NetImports27%

38%

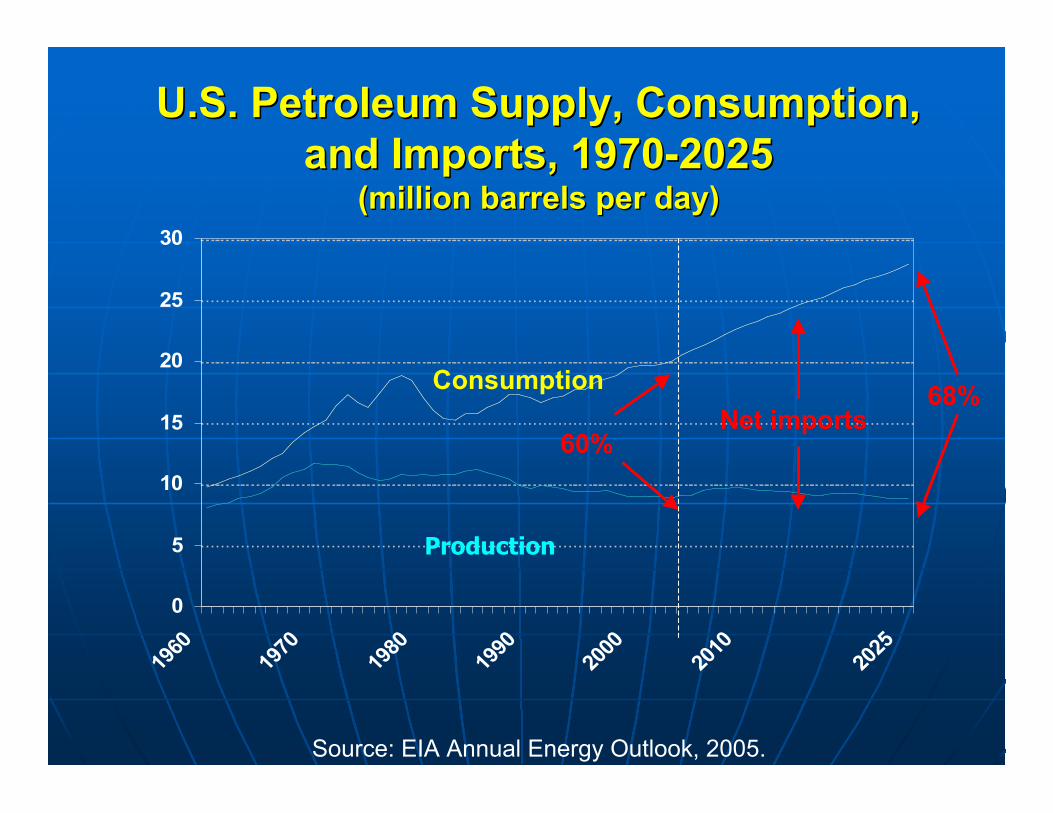

U.S. Petroleum Supply, Consumption,U.S. Petroleum Supply, Consumption,and Imports, 1970-2025and Imports, 1970-2025

(million barrels per day)(million barrels per day)

0

5

10

15

20

25

30

1960

1970

1980

1990

2000

2010

2025

Source: EIA Annual Energy Outlook, 2005.

Production

Consumption

Net imports60%

68%

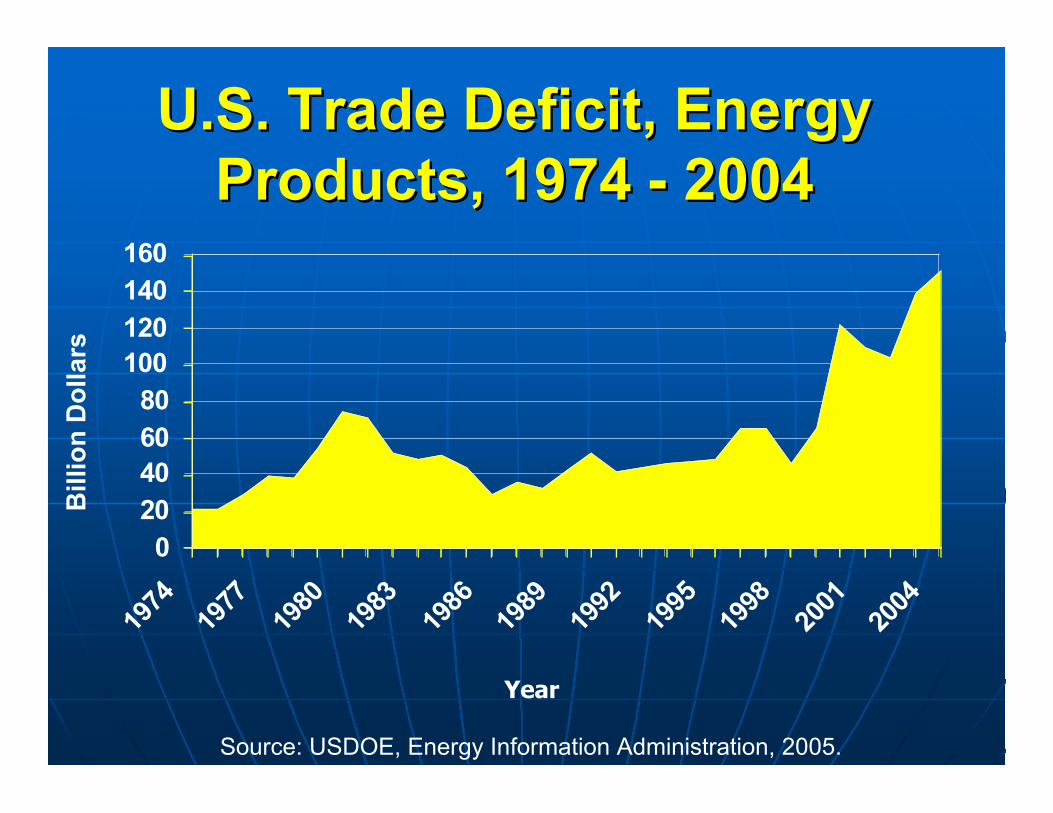

U.S. Trade Deficit, EnergyU.S. Trade Deficit, EnergyProducts, 1974 - 2004Products, 1974 - 2004

020406080

100120140160

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Bill

ion

Do

llars

Year

Source: USDOE, Energy Information Administration, 2005.

Global Mega-TrendsGlobal Mega-Trends

nn GlobalizationGlobalization

nn Expansion of the global economy Expansion of the global economy

nn Growth of energy demand and Growth of energy demand and

the approach of peak petroleum the approach of peak petroleum

nn Increasing interest in bio-energyIncreasing interest in bio-energy

nn Growth of global fiber supplies Growth of global fiber supplies

nn Rising global competition Rising global competition

Bio-Energy SourcesBio-Energy Sources - Trees - Grasses - Agricultural Crops - Agricultural Residues - Animal Wastes - Municipal Solid Waste

Bio-Energy OptionsBio-Energy Options

nn HydrogenHydrogen

nn EthanolEthanol

nn BiodieselBiodiesel

nn Replacement forReplacement forfossil fuels infossil fuels inelectricityelectricitygenerationgeneration

nn Steam generationSteam generationfor district heatingfor district heating

Bio-Energy OptionsBio-Energy Options

nn HydrogenHydrogen

nn EthanolEthanol

nn BiodieselBiodiesel

nn Replacement forReplacement forfossil fuels infossil fuels inelectricityelectricitygenerationgeneration

nn Steam generationSteam generationfor district heatingfor district heating

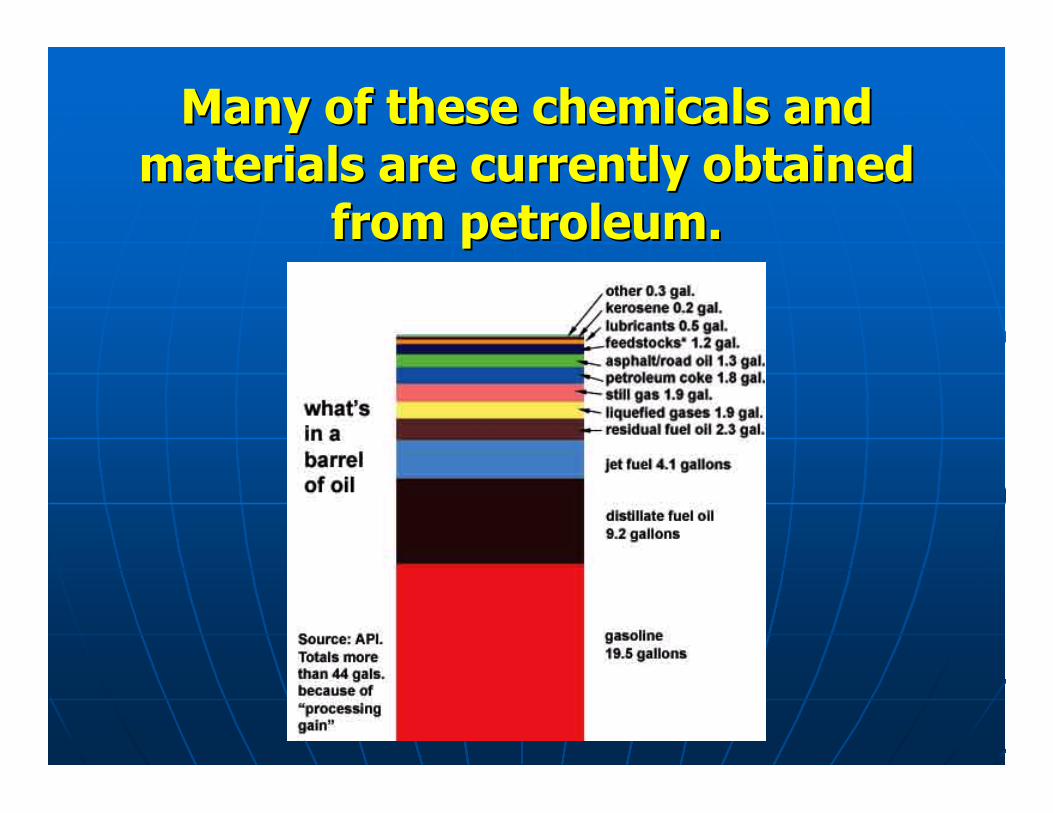

Beyond energy, there areBeyond energy, there areopportunities for producingopportunities for producinga wide range of chemicalsa wide range of chemicalsand industrial and industrial feedstocksfeedstocks

from biomass.from biomass.

Bio-Energy OptionsBio-Energy Optionsnn HydrogenHydrogen

nn EthanolEthanol

nn BiodieselBiodiesel

nn Replacement forReplacement forfossil fuels infossil fuels inelectricity generationelectricity generation

nn Steam generation forSteam generation fordistrict heatingdistrict heating

nn OlefinsOlefins

Many of these chemicals andMany of these chemicals andmaterials are currently obtainedmaterials are currently obtained

from petroleum.from petroleum.

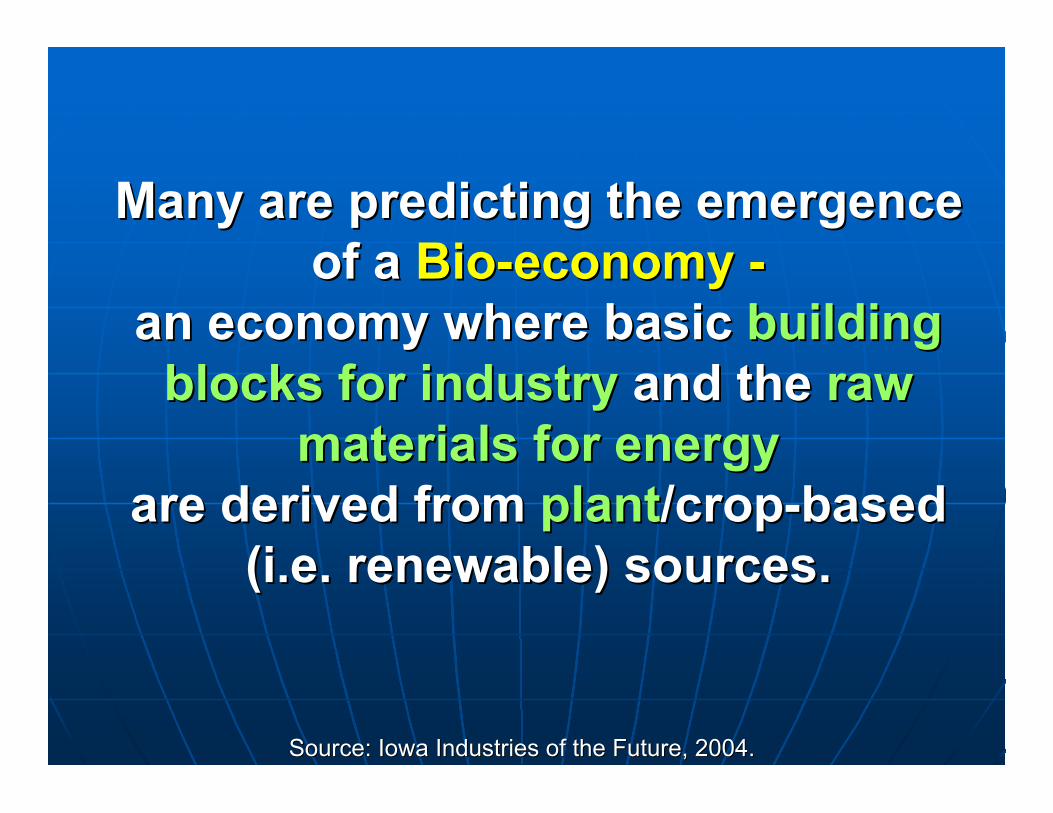

Many are predicting the emergenceMany are predicting the emergenceof aof a Bio-economy - Bio-economy -

an economy where basic an economy where basic buildingbuildingblocks for industryblocks for industry and the and the rawraw

materials for energymaterials for energyare derived from are derived from plantplant/crop-based/crop-based

(i.e. renewable) sources.(i.e. renewable) sources.

Source: Iowa Industries of the Future, 2004.Source: Iowa Industries of the Future, 2004.

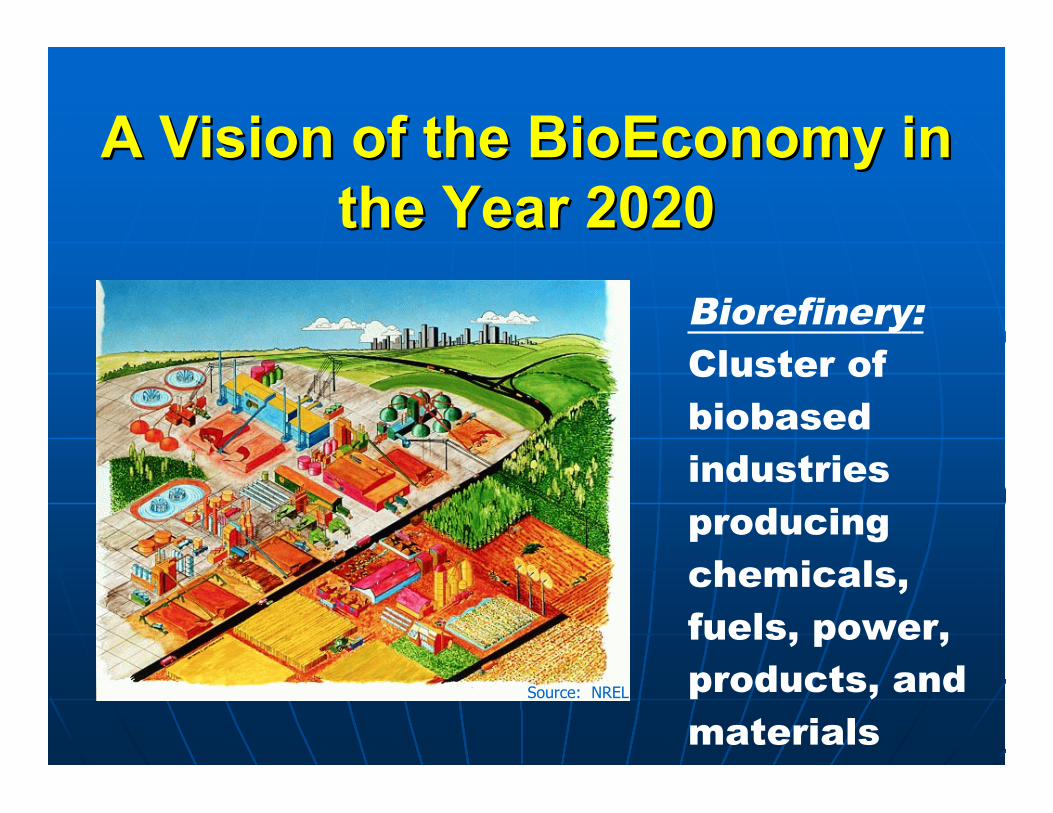

A Vision of the BioEconomy inA Vision of the BioEconomy inthe Year 2020the Year 2020

Biorefinery:Cluster ofbiobasedindustriesproducingchemicals,fuels, power,products, andmaterials

Source: NREL

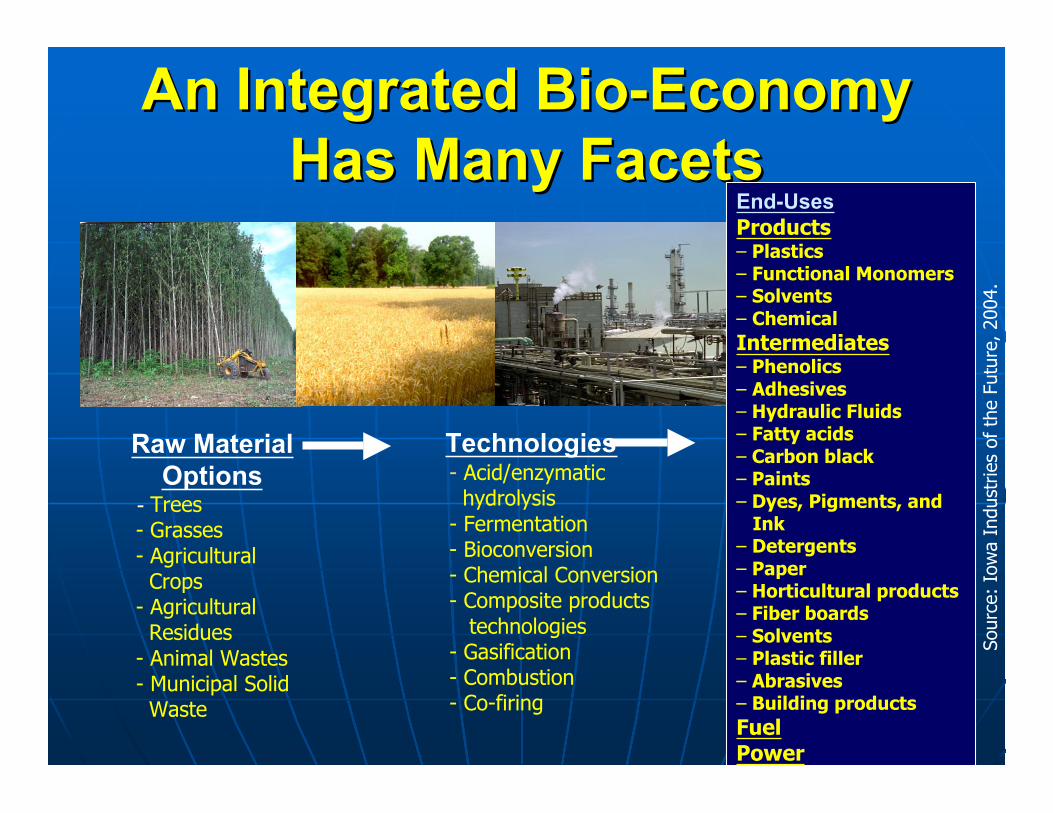

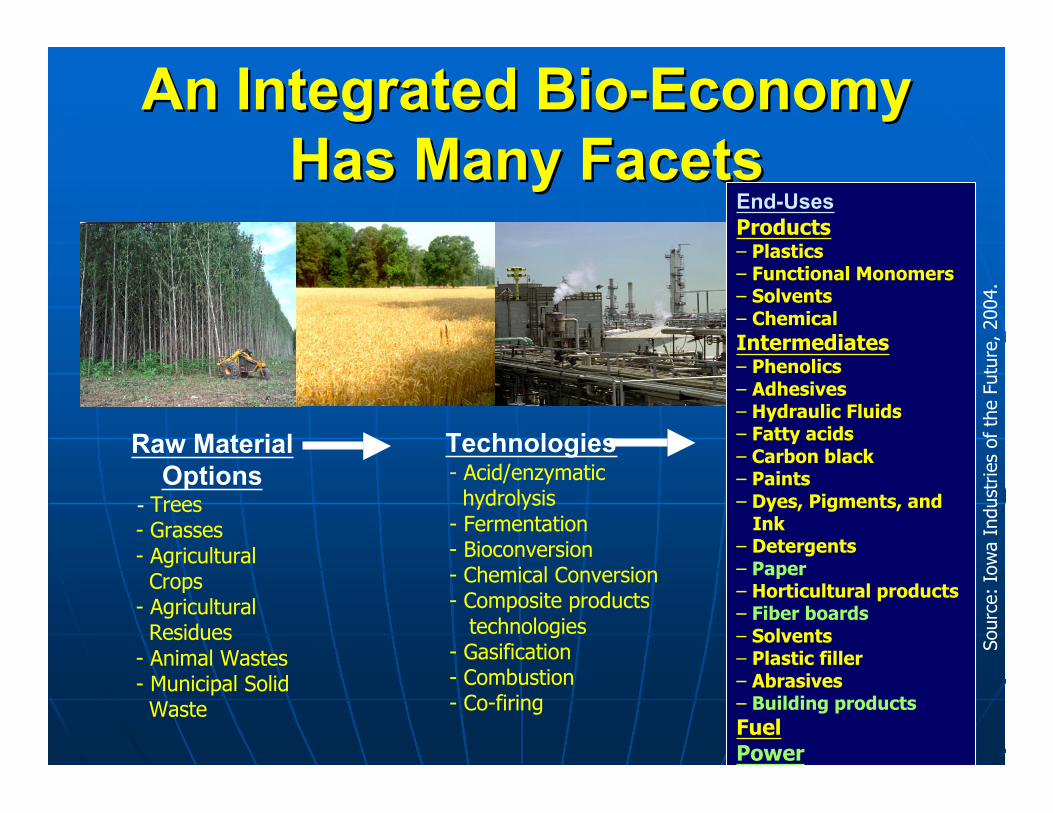

An Integrated Bio-EconomyAn Integrated Bio-EconomyHas Many FacetsHas Many Facets

Raw MaterialOptions

- Trees - Grasses - Agricultural Crops - Agricultural Residues - Animal Wastes - Municipal Solid Waste

Technologies- Acid/enzymatic hydrolysis- Fermentation- Bioconversion- Chemical Conversion- Composite products technologies- Gasification- Combustion- Co-firing

Sour

ce:

Iow

a In

dust

ries

of t

he F

utur

e, 2

004.

End-UsesProducts– Plastics– Functional Monomers– Solvents– ChemicalIntermediates– Phenolics– Adhesives– Hydraulic Fluids– Fatty acids– Carbon black– Paints– Dyes, Pigments, and Ink– Detergents– Paper– Horticultural products– Fiber boards– Solvents– Plastic filler– Abrasives– Building productsFuelPower

An Integrated Bio-EconomyAn Integrated Bio-EconomyHas Many FacetsHas Many Facets

Raw MaterialOptions

- Trees - Grasses - Agricultural Crops - Agricultural Residues - Animal Wastes - Municipal Solid Waste

Technologies- Acid/enzymatic hydrolysis- Fermentation- Bioconversion- Chemical Conversion- Composite products technologies- Gasification- Combustion- Co-firing

Sour

ce:

Iow

a In

dust

ries

of t

he F

utur

e, 2

004.

End-UsesProducts– Plastics– Functional Monomers– Solvents– ChemicalIntermediates– Phenolics– Adhesives– Hydraulic Fluids– Fatty acids– Carbon black– Paints– Dyes, Pigments, and Ink– Detergents– Paper– Horticultural products– Fiber boards– Solvents– Plastic filler– Abrasives– Building productsFuelPower

In the future, products nowIn the future, products nowderived from petroleum willderived from petroleum willbe made from a variety ofbe made from a variety of

biochemicalsbiochemicals and andbiofeedstocksbiofeedstocks arising from arising from

biorefineriesbiorefineries..

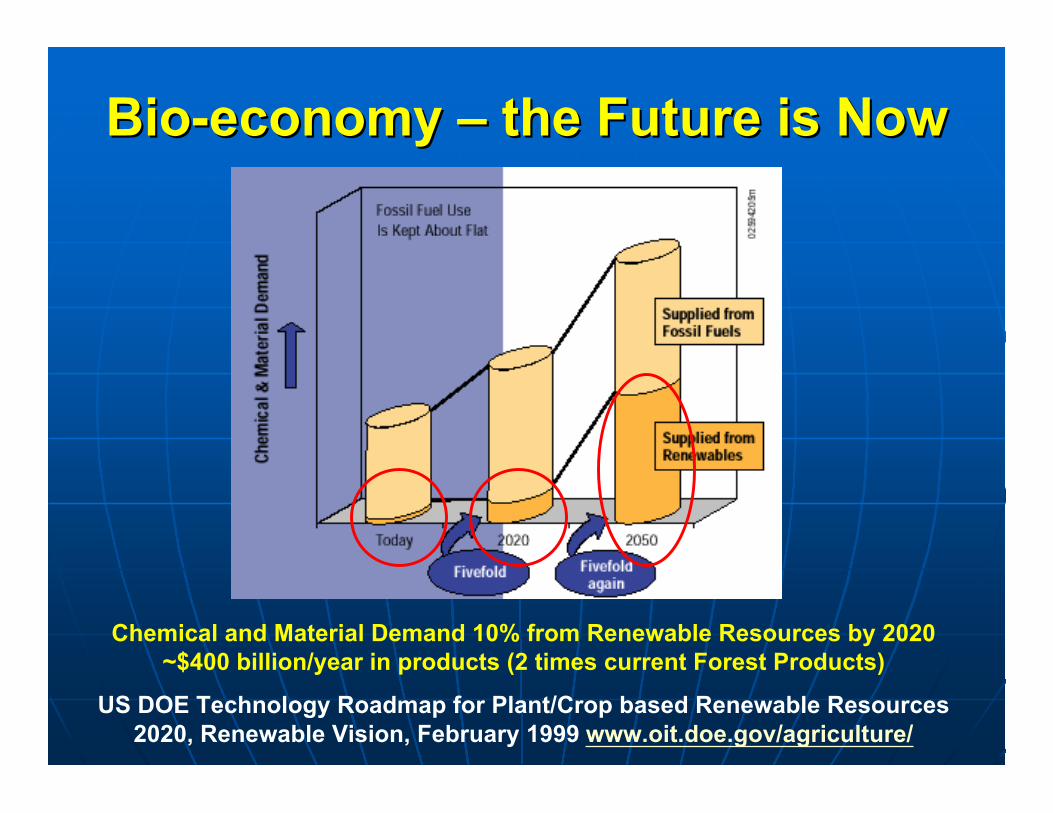

Chemical and Material Demand 10% from Renewable Resources by 2020~$400 billion/year in products (2 times current Forest Products)

US DOE Technology Roadmap for Plant/Crop based Renewable Resources2020, Renewable Vision, February 1999 www.oit.doe.gov/agriculture/

Bio-economy Bio-economy –– the Future is Now the Future is Now

Increasing economicIncreasing economicimportance of biomassimportance of biomasshas major implicationshas major implicationsfor the forest productsfor the forest products

industry.industry.

Global Mega-TrendsGlobal Mega-Trends

nn GlobalizationGlobalization

nn Expansion of the global economy Expansion of the global economy

nn Growth of energy demand and Growth of energy demand and

the approach of peak petroleum the approach of peak petroleum

nn Increasing interest in bio-energy Increasing interest in bio-energy

nn Growth of global fiber suppliesGrowth of global fiber supplies

nn Rising global competition Rising global competition

Growth of Global Fiber SuppliesGrowth of Global Fiber Supplies

vv PlantationsPlantationsvv Re-emergence of the forest Re-emergence of the forest sector of Russia and Eastern sector of Russia and Eastern Europe Europevv Increasing Availability ofIncreasing Availability of Tropical Timber Tropical Timber

Growth of Global Fiber SuppliesGrowth of Global Fiber Supplies

vv PlantationsPlantationsvv Re-emergence of the forestRe-emergence of the forest sector of Russia and Eastern sector of Russia and Eastern Europe Europevv Increasing Availability of Increasing Availability of Tropical Timber Tropical Timber

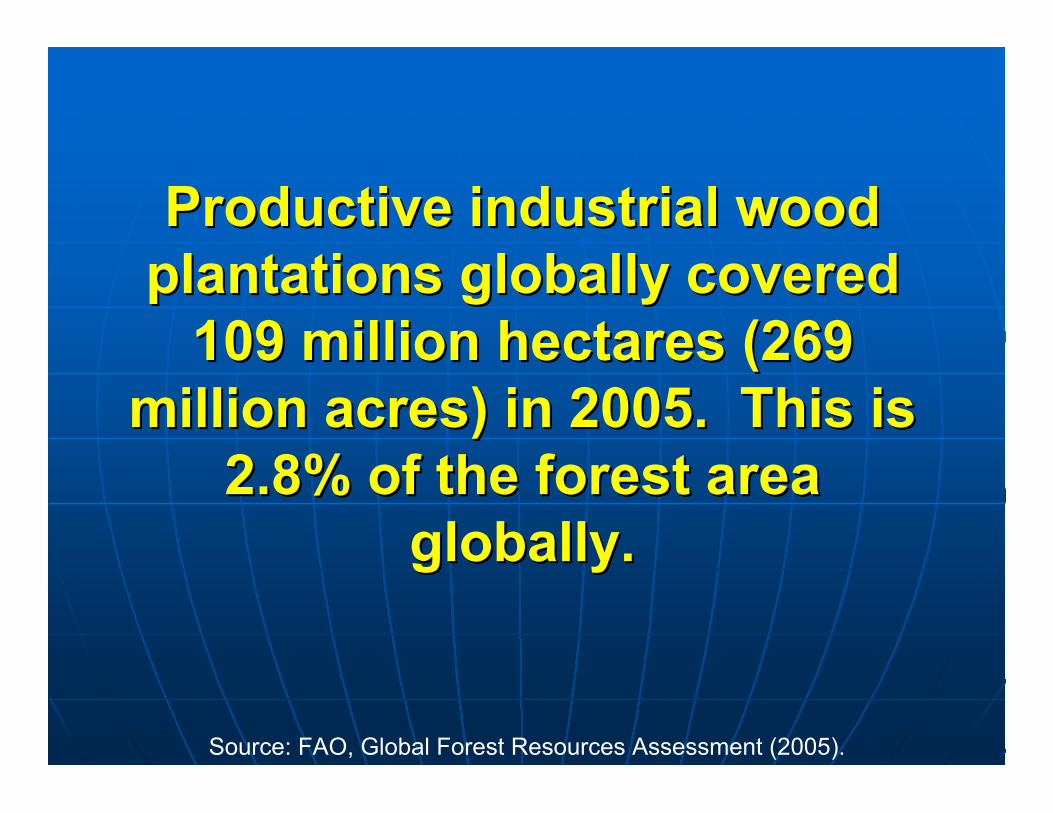

Productive industrial woodProductive industrial woodplantations globally coveredplantations globally covered

109 million hectares (269109 million hectares (269million acres) in 2005. This ismillion acres) in 2005. This is

2.8% of the forest area2.8% of the forest areaglobally.globally.

Source: FAO, Global Forest Resources Assessment (2005).

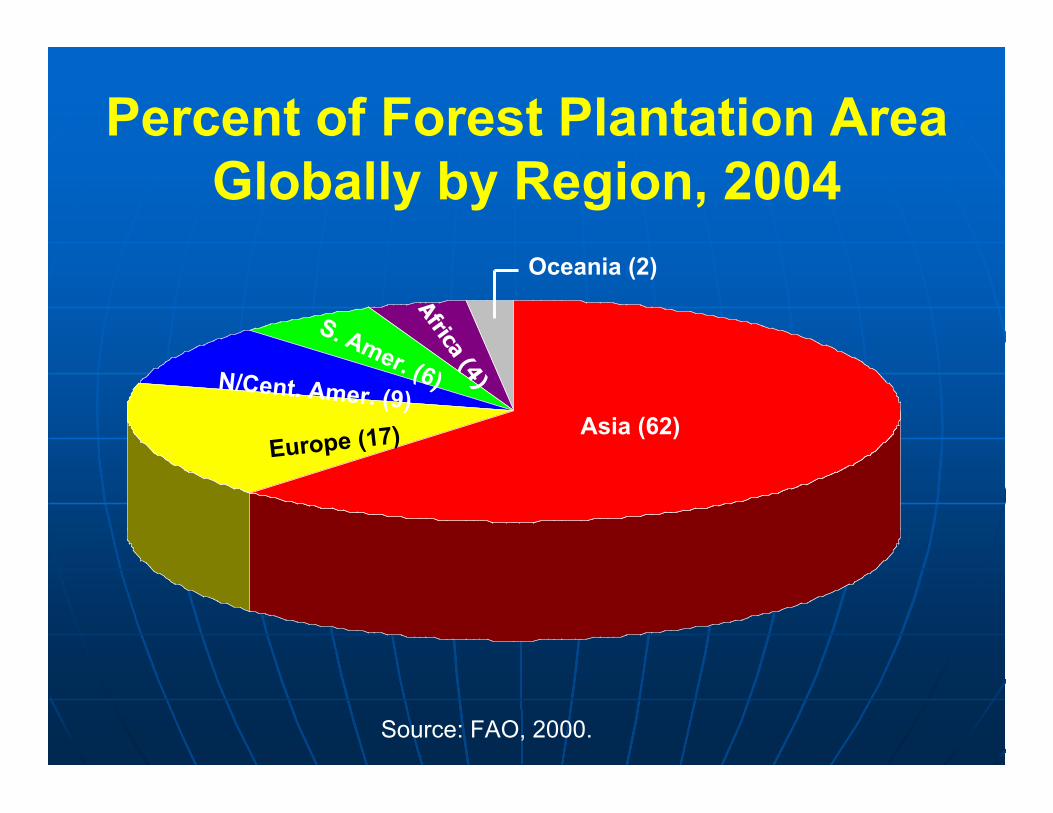

Percent of Forest Plantation AreaGlobally by Region, 2004

Source: FAO, 2000.

Asia (62)Europe (17)

N/Cent. Amer. (9)

S. Amer. (6)

Africa (4)

Oceania (2)

0

10

20

30

40

50

Percent

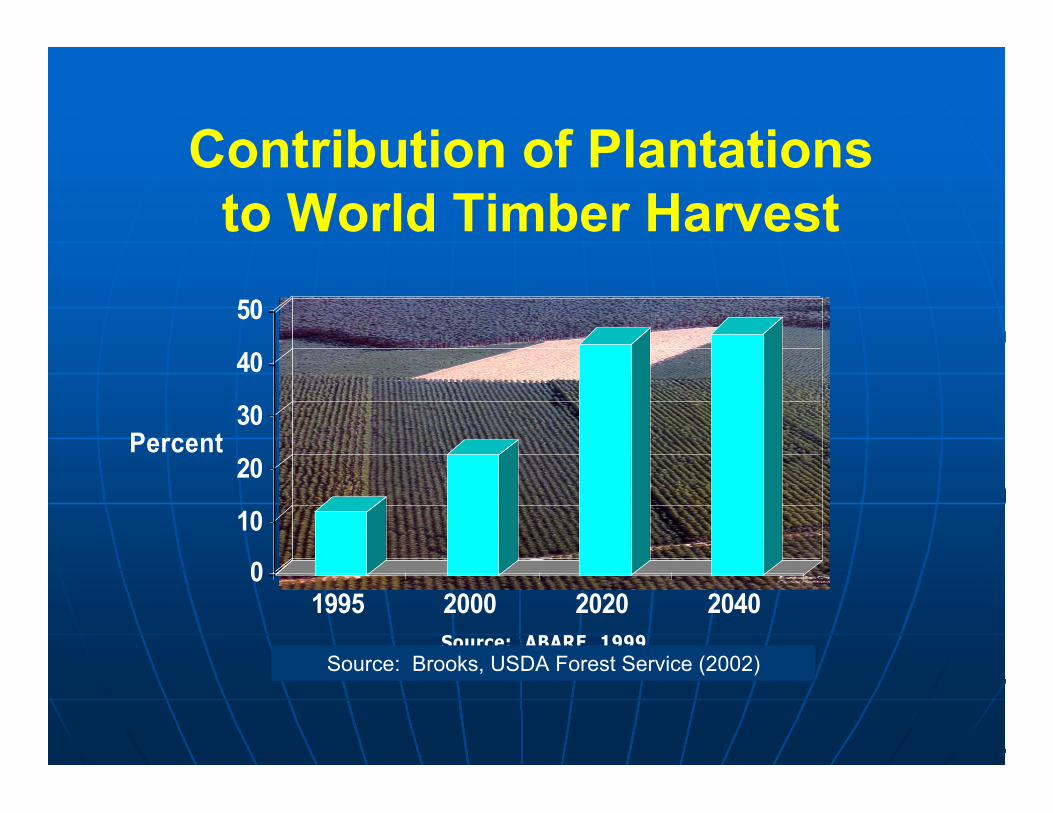

1995 2000 2020 2040Source: ABARE 1999

Contribution of Plantationsto World Timber Harvest

Source: Brooks, USDA Forest Service (2002)

The impact of thisThe impact of thisdevelopment on thedevelopment on the

forest products industryforest products industryglobally will be profound.globally will be profound.

Growth of Global Fiber SuppliesGrowth of Global Fiber Supplies

vv Plantations Plantationsvv Re-emergence of the forest Re-emergence of the forest sector of Russia and Eastern sector of Russia and Eastern Europe Europevv Increasing Availability of Increasing Availability of Tropical Timber Tropical Timber

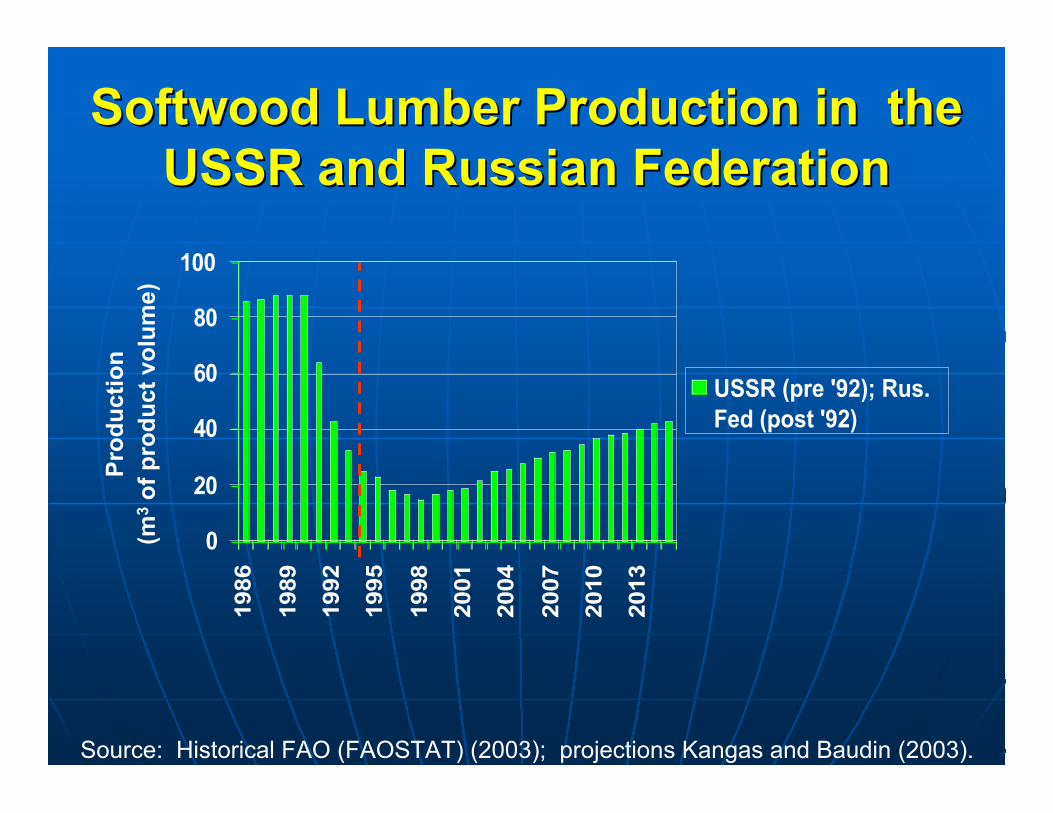

Softwood Lumber Production in theSoftwood Lumber Production in theUSSR and Russian FederationUSSR and Russian Federation

0

20

40

60

80

1001986

1989

1992

1995

1998

2001

2004

2007

2010

2013

USSR (pre '92); Rus.Fed (post '92)

Pro

du

ctio

n(m

3 o

f p

rod

uct

vo

lum

e)

Source: Historical FAO (FAOSTAT) (2003); projections Kangas and Baudin (2003).

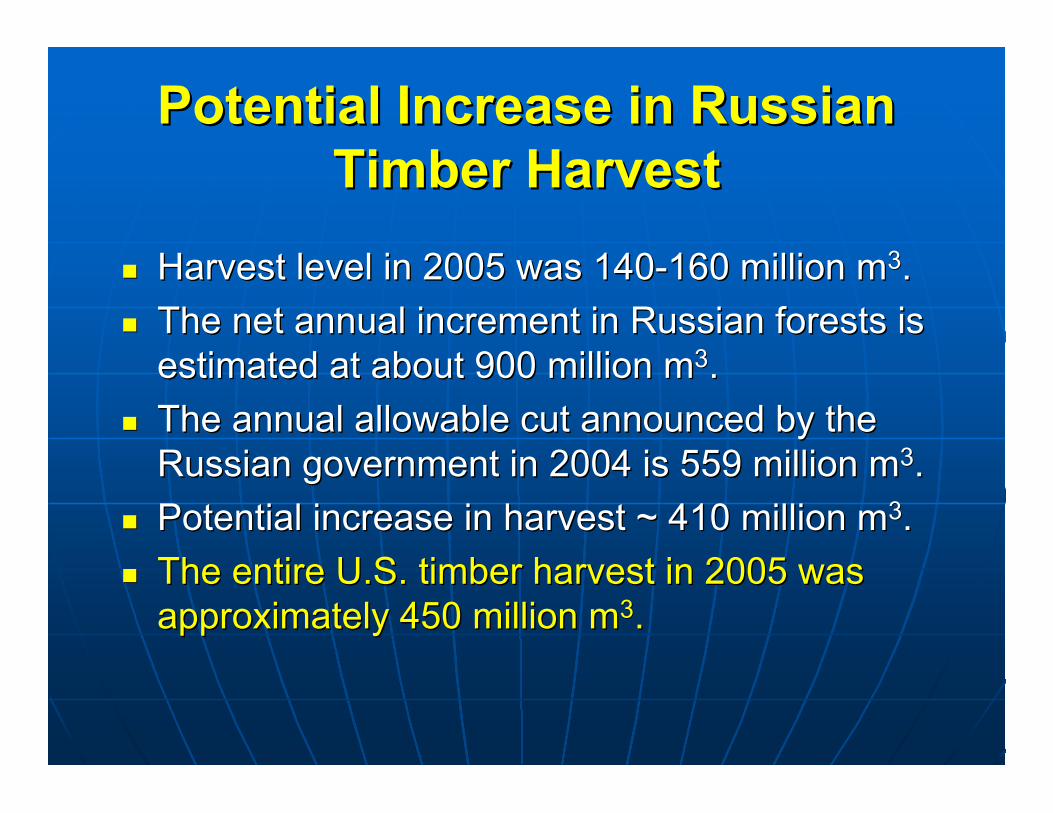

Potential Increase in RussianPotential Increase in RussianTimber HarvestTimber Harvest

nn Harvest level in 2005 was 140-160 million mHarvest level in 2005 was 140-160 million m33..

nn The net annual increment in Russian forests isThe net annual increment in Russian forests isestimated at about 900 million mestimated at about 900 million m33..

nn The annual allowable cut announced by theThe annual allowable cut announced by theRussian government in 2004 is 559 million mRussian government in 2004 is 559 million m33..

nn Potential increase in harvest ~ 410 million mPotential increase in harvest ~ 410 million m33..

nn The entire U.S. timber harvest in 2005 wasThe entire U.S. timber harvest in 2005 wasapproximately 450 million mapproximately 450 million m33..

Russian Foreign Trade in Paper andRussian Foreign Trade in Paper andTimber Products, 1994-2003Timber Products, 1994-2003

0

1

2

3

4

5

6

7

8

1994 1996 1998 2000 2002 2003

Foreign Trade

Exports

Imports

($ B

illio

n U

.S. )

Source: UNECE, Timber Committee and European Forestry Commission Market Discussions,2004.

Recent and Coming SawmillRecent and Coming SawmillInvestment in Russia, Investment in Russia, BalticsBaltics, and, and

E. Europe (2002-2006)E. Europe (2002-2006)nn Proposed for RussiaProposed for Russia - 40 sawmills - 40 sawmills

nn Proposed for Proposed for BalticsBaltics & E. & E. EurEur. . - -15 sawmills15 sawmills

Total Total ’’02 02 –– ’’06 06 55 sawmills 55 sawmills

Source: R. Taylor, Taylor & Associates Ltd., 2004.

A total of 8.5 million m3 (3.7 billion bf – net; or ~ 6billion board feet (nominal) so far.

About U.S. $2.5 billion in non-pulp wood productsinvestments between 2002 and 2006.

Growth of Global Fiber SuppliesGrowth of Global Fiber Supplies

vv Plantations Plantationsvv Re-emergence of the forestRe-emergence of the forest sector of Russia and Eastern sector of Russia and Eastern Europe Europevv Increasing Availability ofIncreasing Availability of Tropical Timber Tropical Timber

Global Mega-TrendsGlobal Mega-Trends

nn GlobalizationGlobalization

nn Expansion of the global economy Expansion of the global economy

nn Growth of energy demand and Growth of energy demand and

the approach of peak petroleum the approach of peak petroleum

nn Increasing interest in bio-energy Increasing interest in bio-energy

nn Growth of global fiber supplies Growth of global fiber supplies

nn Rising global competitionRising global competition

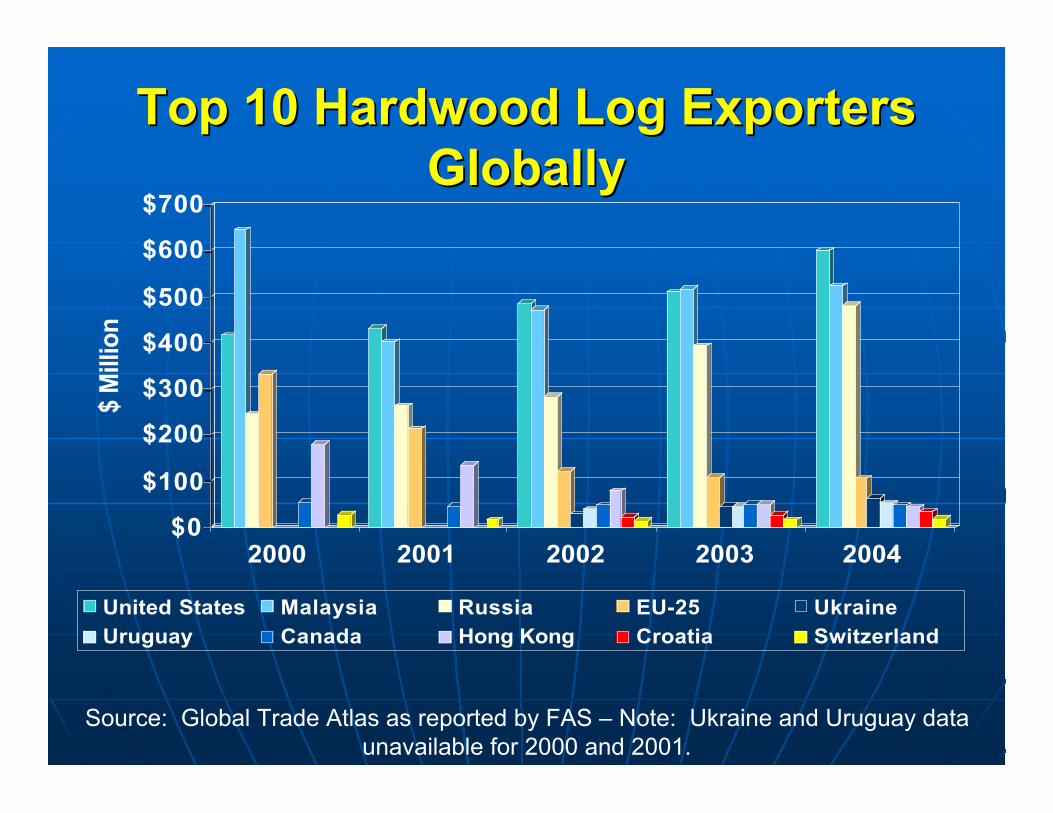

Top 10 Hardwood Log ExportersTop 10 Hardwood Log ExportersGloballyGlobally

$0

$100

$200

$300

$400

$500

$600

$700

$ M

illio

n

2000 2001 2002 2003 2004

United States Malaysia Russia EU-25 UkraineUruguay Canada Hong Kong Croatia Switzerland

Source: Global Trade Atlas as reported by FAS – Note: Ukraine and Uruguay dataunavailable for 2000 and 2001.

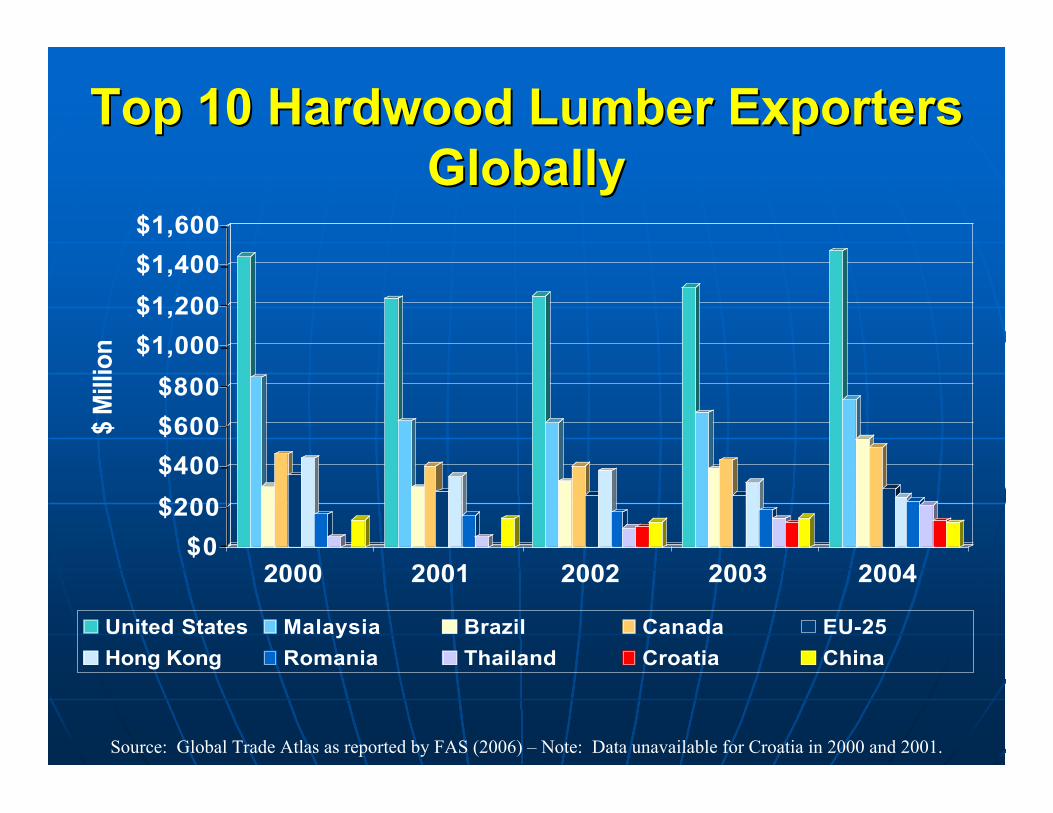

Top 10 Hardwood Lumber ExportersTop 10 Hardwood Lumber ExportersGloballyGlobally

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$ M

illio

n

2000 2001 2002 2003 2004

United States Malaysia Brazil Canada EU-25

Hong Kong Romania Thailand Croatia China

Source: Global Trade Atlas as reported by FAS (2006) – Note: Data unavailable for Croatia in 2000 and 2001.

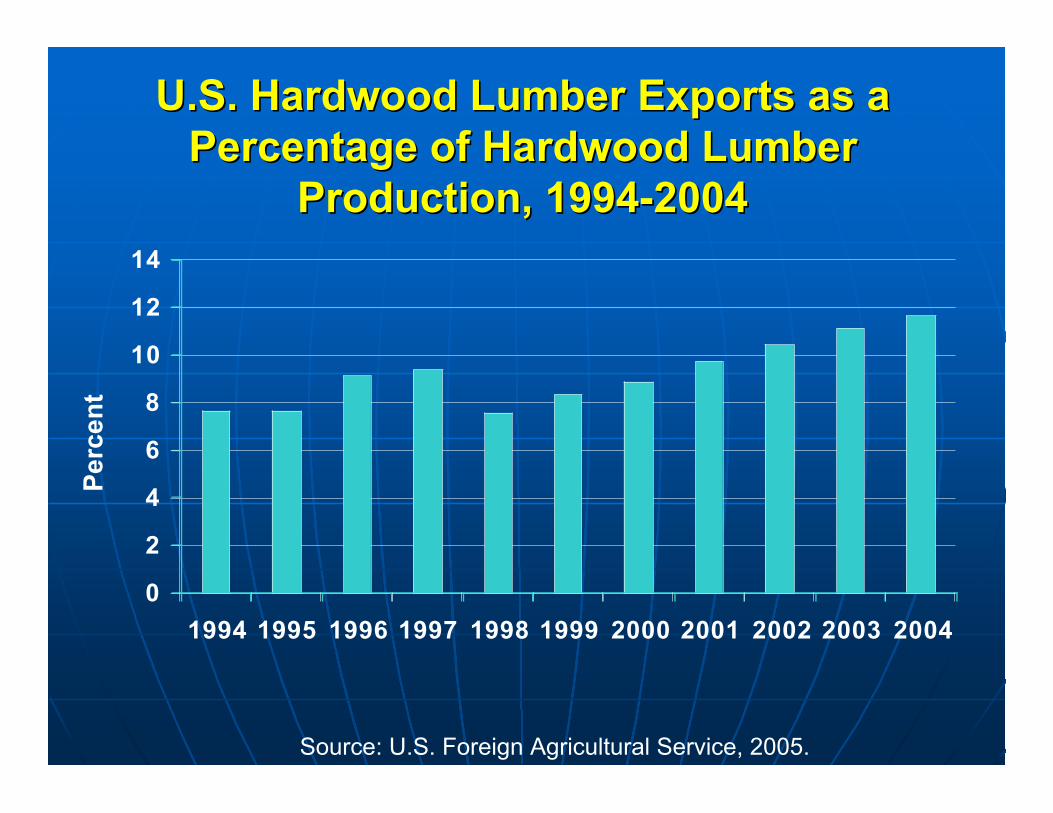

U.S. Hardwood Lumber Exports as aU.S. Hardwood Lumber Exports as aPercentage of Hardwood LumberPercentage of Hardwood Lumber

Production, 1994-2004Production, 1994-2004

0

2

4

6

8

10

12

14

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Per

cen

t

Source: U.S. Foreign Agricultural Service, 2005.

U.S. Hardwood Lumber Exports byU.S. Hardwood Lumber Exports byDestination, 1994Destination, 1994

0

50

100

150

200

250

300

350

Mill

ion

Bo

ard

Fee

t

Source: U.S. Foreign Agricultural Service, 2004.

Can

ada

Jap

an

Tai

wan

Ital

y

Ger

man

y

Bel

g./L

ux.

Mex

ico

Ko

rea

Sp

ain

UK

China?

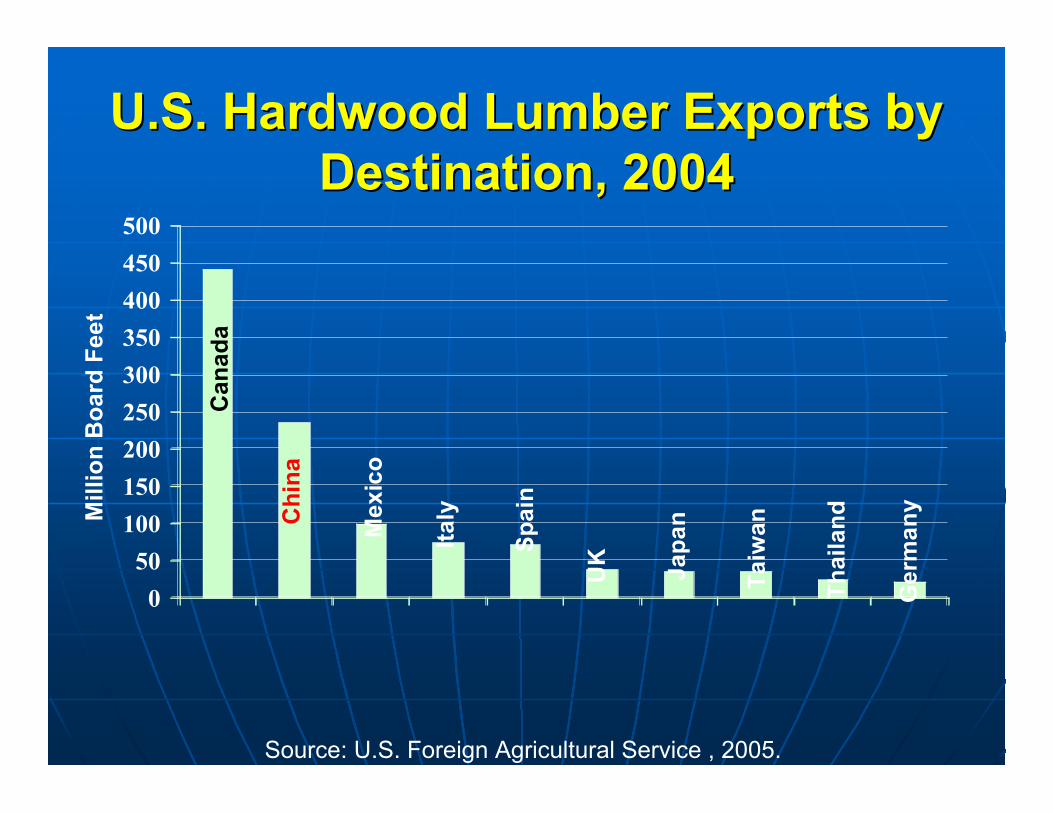

U.S. Hardwood Lumber Exports byU.S. Hardwood Lumber Exports byDestination, 2004Destination, 2004

0

50

100

150

200

250

300

350

400

450

500

Mill

ion

Bo

ard

Fee

t

Source: U.S. Foreign Agricultural Service , 2005.

Can

ada

Ch

ina

Mex

ico

Sp

ain

Ital

y

Jap

an

UK

Ger

man

y

Th

aila

nd

Tai

wan

0

500

1000

1500

2000

2500

3000

3500

4000

4500

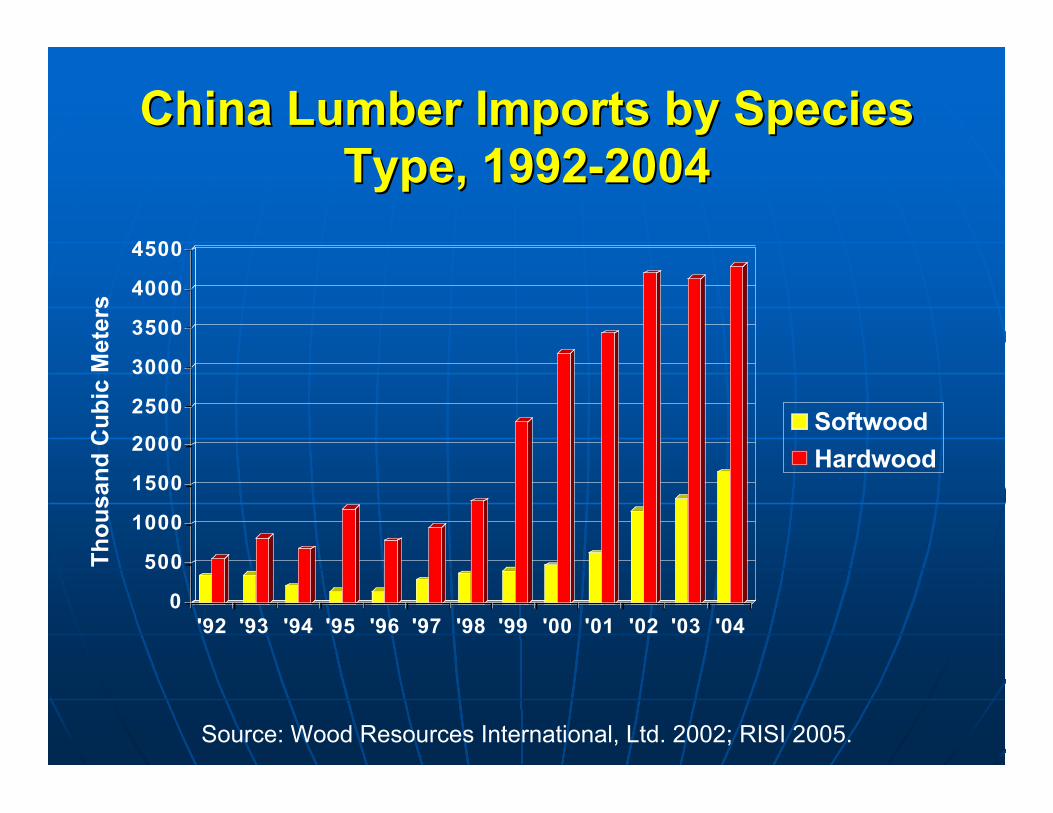

'92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04

Softwood

Hardwood

Source: Wood Resources International, Ltd. 2002; RISI 2005.

China Lumber Imports by SpeciesChina Lumber Imports by SpeciesType, 1992-2004Type, 1992-2004

Th

ou

san

d C

ub

ic M

eter

s

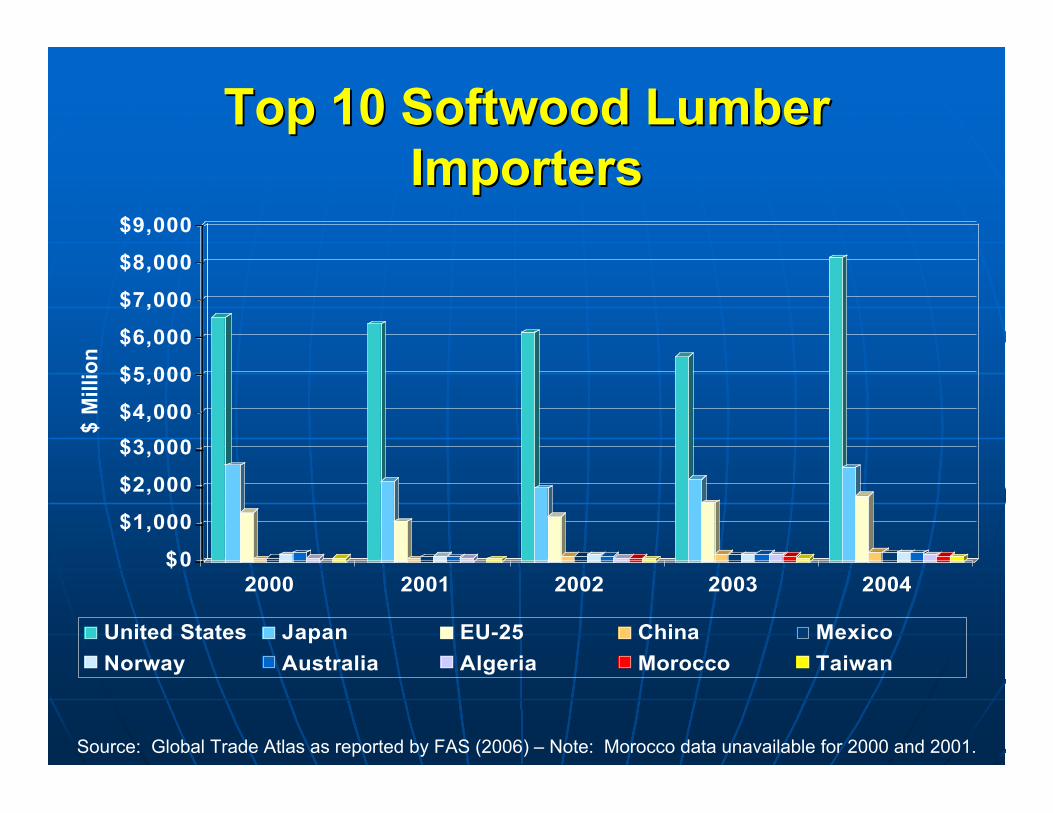

Top 10 Softwood LumberTop 10 Softwood LumberImportersImporters

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$ M

illio

n

2000 2001 2002 2003 2004

United States Japan EU-25 China Mexico

Norway Australia Algeria Morocco Taiwan

Source: Global Trade Atlas as reported by FAS (2006) – Note: Morocco data unavailable for 2000 and 2001.

0

2000

4000

6000

8000

10000

12000

14000

16000

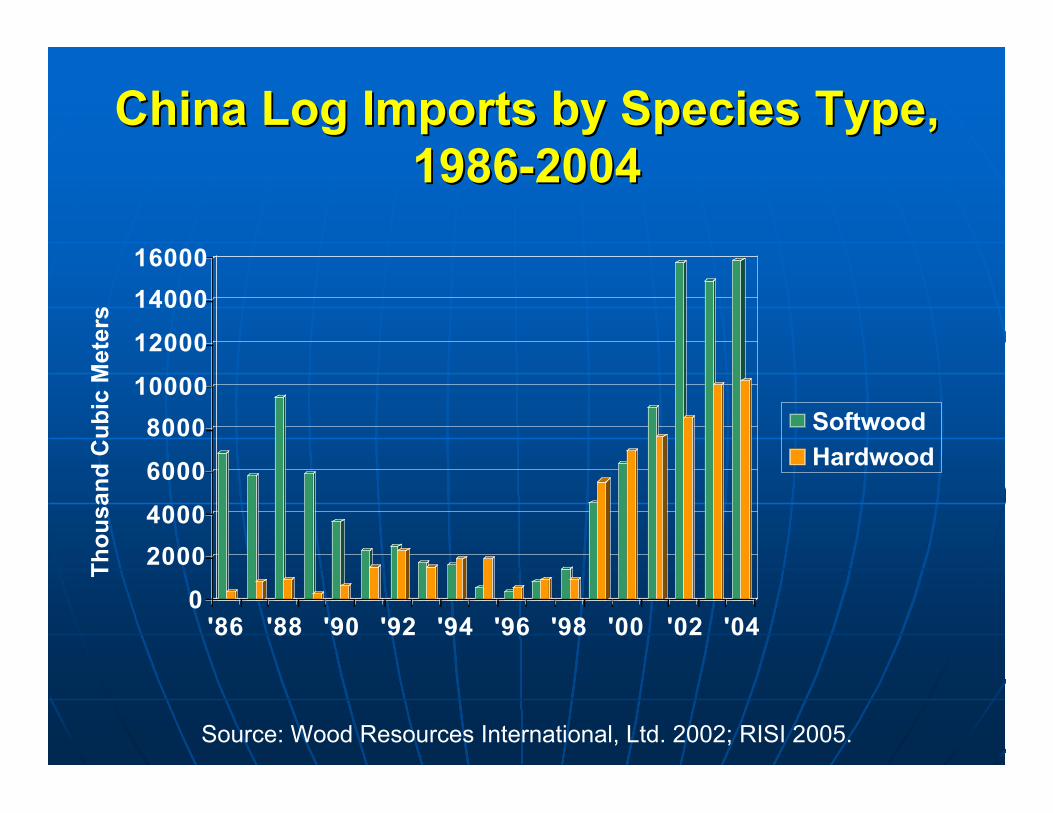

'86 '88 '90 '92 '94 '96 '98 '00 '02 '04

Softwood

Hardwood

Source: Wood Resources International, Ltd. 2002; RISI 2005.

China Log Imports by Species Type,China Log Imports by Species Type,1986-20041986-2004

Th

ou

san

d C

ub

ic M

eter

s

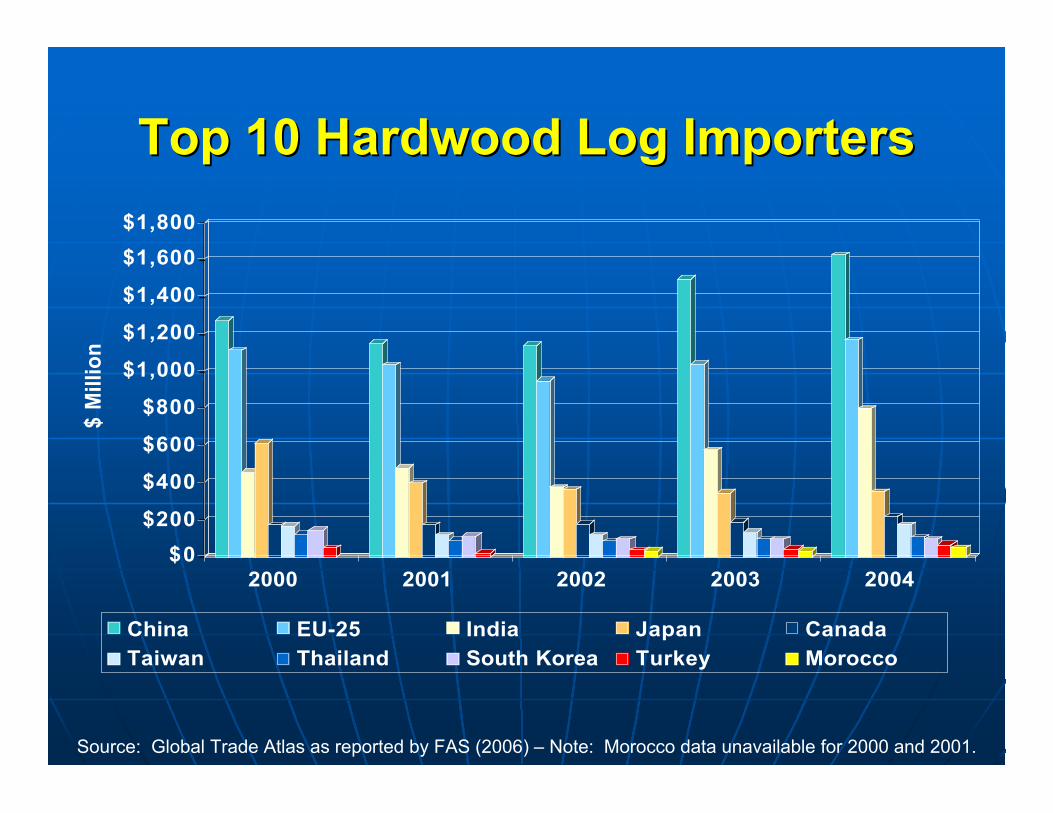

Top 10 Hardwood Log ImportersTop 10 Hardwood Log Importers

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$ M

illio

n

2000 2001 2002 2003 2004

China EU-25 India Japan CanadaTaiwan Thailand South Korea Turkey Morocco

Source: Global Trade Atlas as reported by FAS (2006) – Note: Morocco data unavailable for 2000 and 2001.

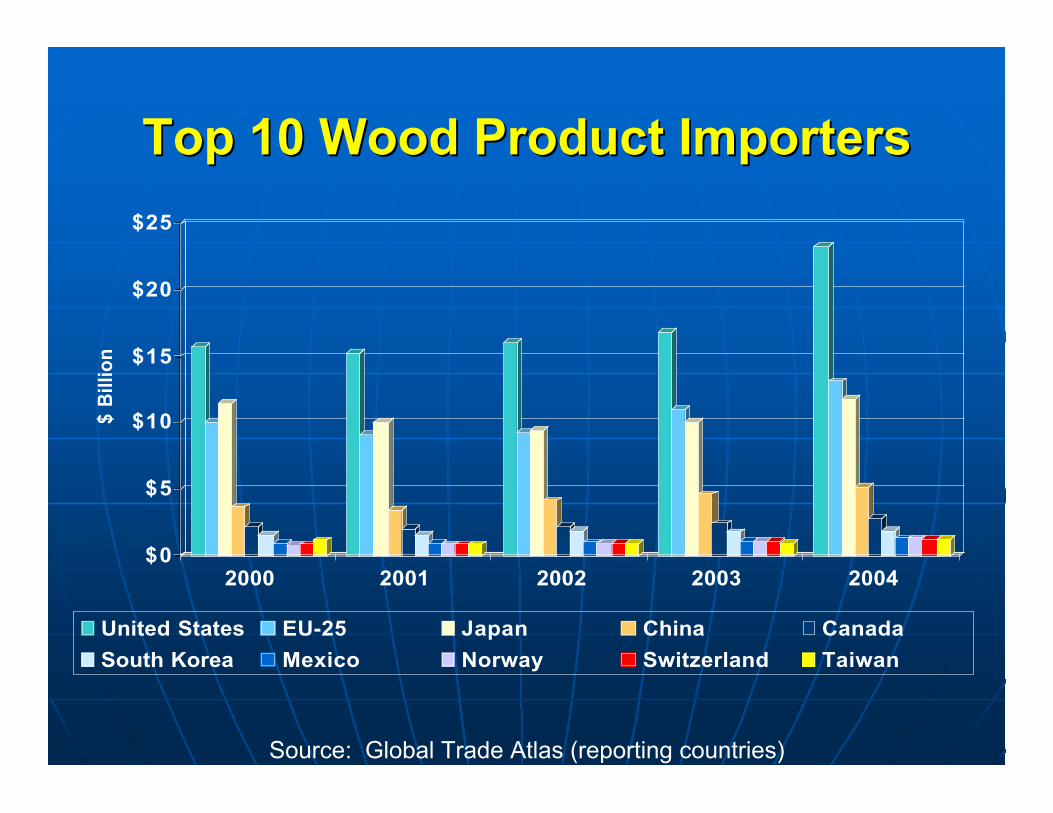

Top 10 Wood Product ImportersTop 10 Wood Product Importers

$0

$5

$10

$15

$20

$25

$ B

illio

n

2000 2001 2002 2003 2004

United States EU-25 Japan China Canada

South Korea Mexico Norway Switzerland Taiwan

Source: Global Trade Atlas (reporting countries)

0

20

40

60

80

100

120

Paper

& P

Bd.

OSB & P

lywoo

d

SW L

br

HH Fur

n

HW L

br

HW F

loor

ing

HW M

oldi

ng

1990

2002

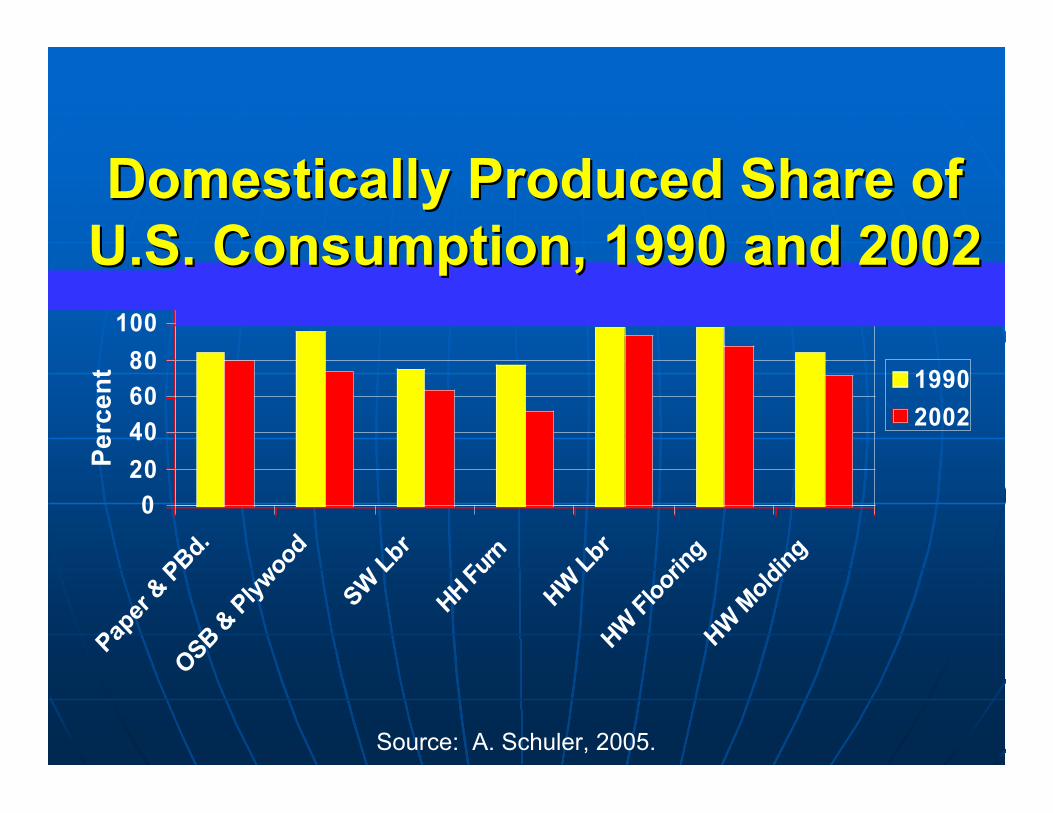

Source: A. Schuler, 2005.

Per

cen

t

Domestically Produced Share ofDomestically Produced Share ofU.S. Consumption, 1990 and 2002U.S. Consumption, 1990 and 2002

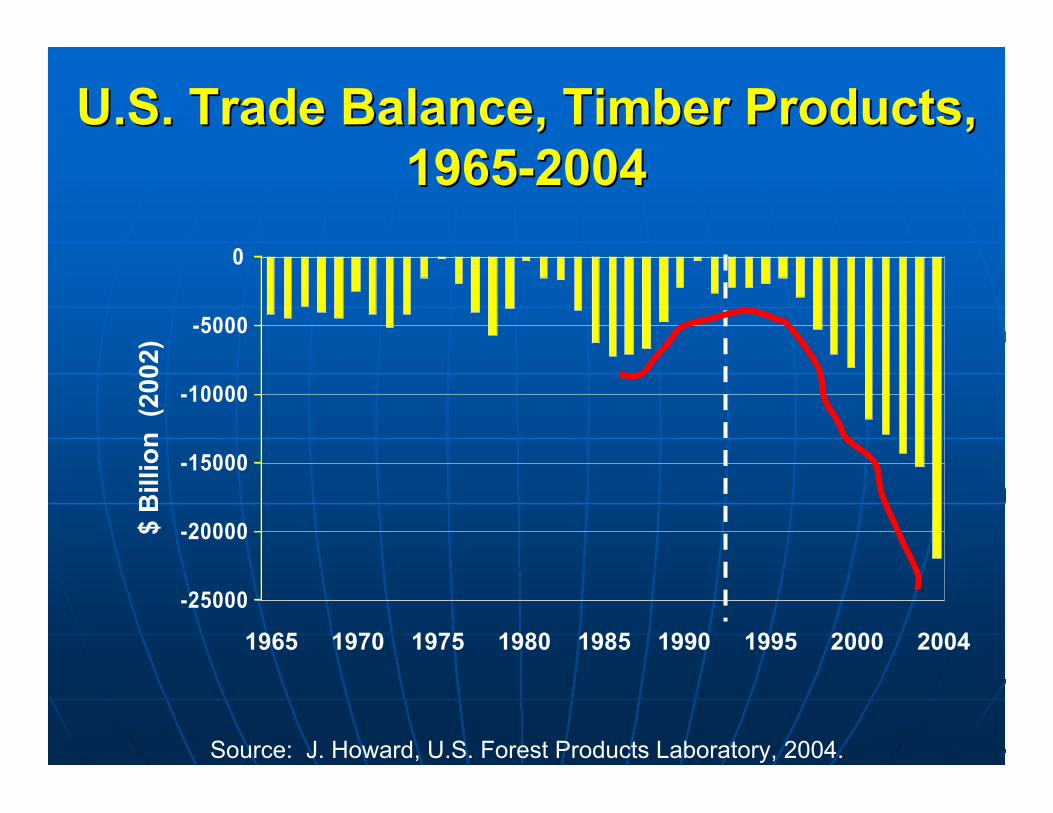

U.S. Trade Balance, Timber Products,U.S. Trade Balance, Timber Products,1965-20041965-2004

-25000

-20000

-15000

-10000

-5000

0

$ B

illio

n (

2002

)

Source: J. Howard, U.S. Forest Products Laboratory, 2004.

1965 1970 1975 1980 1985 1990 1995 2000 2004

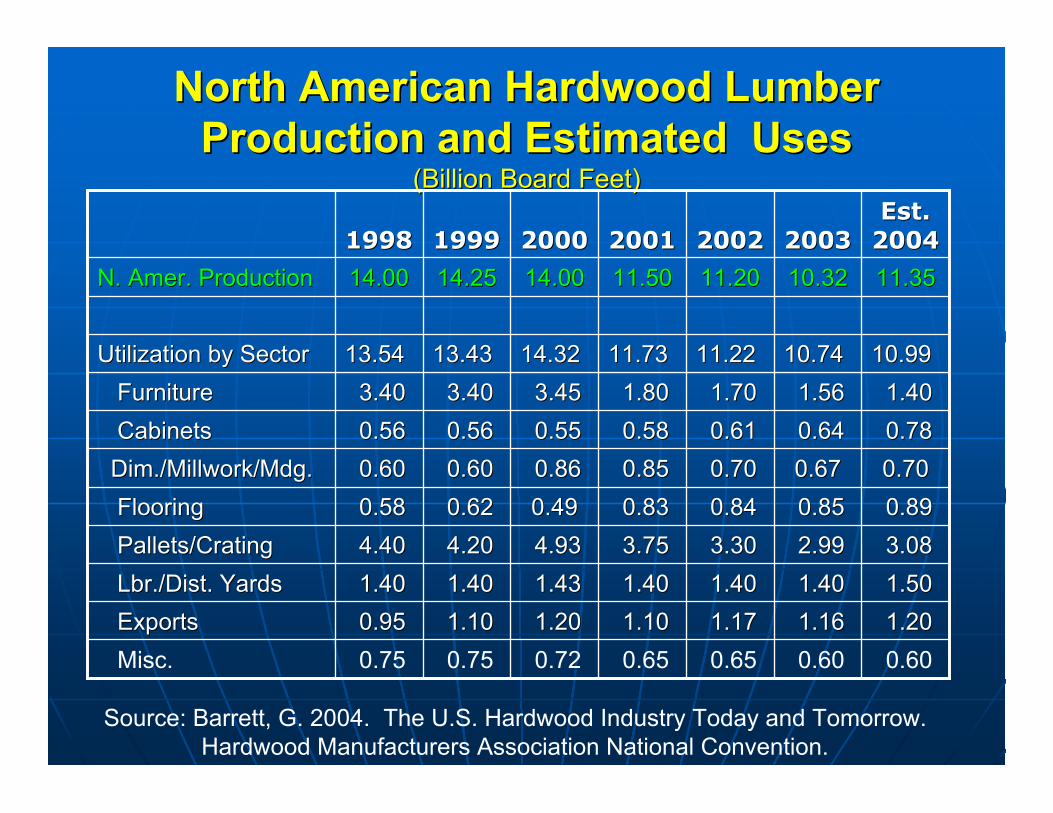

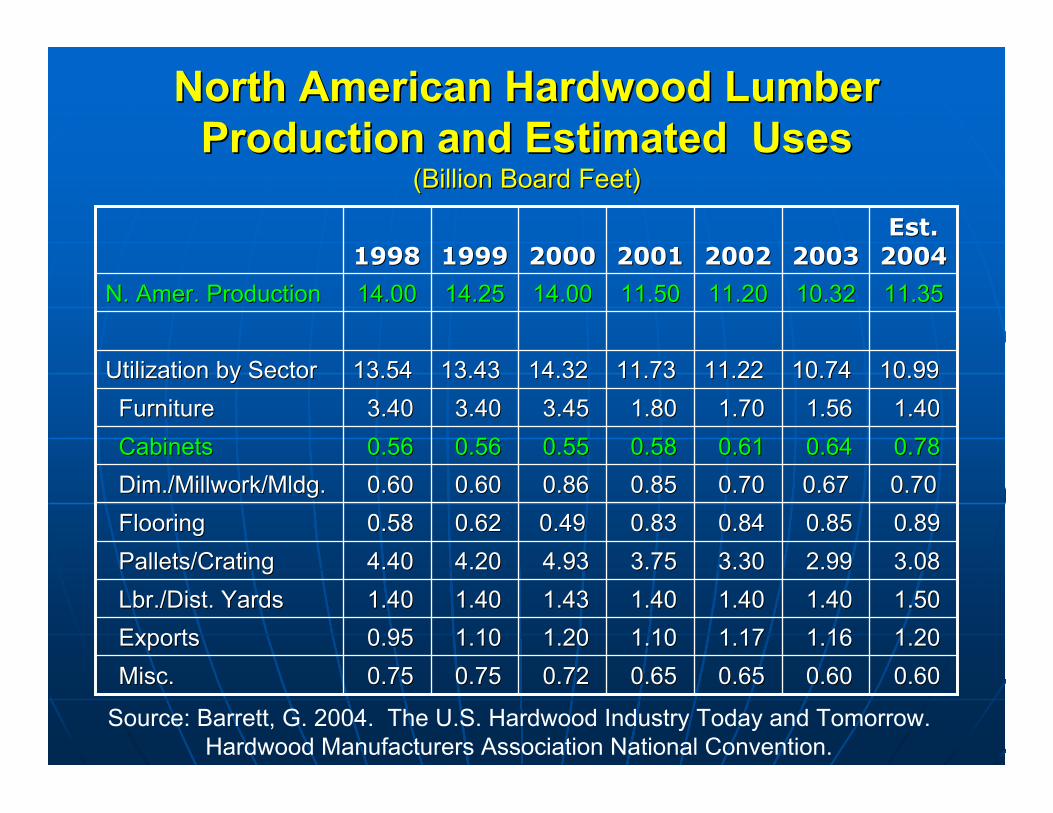

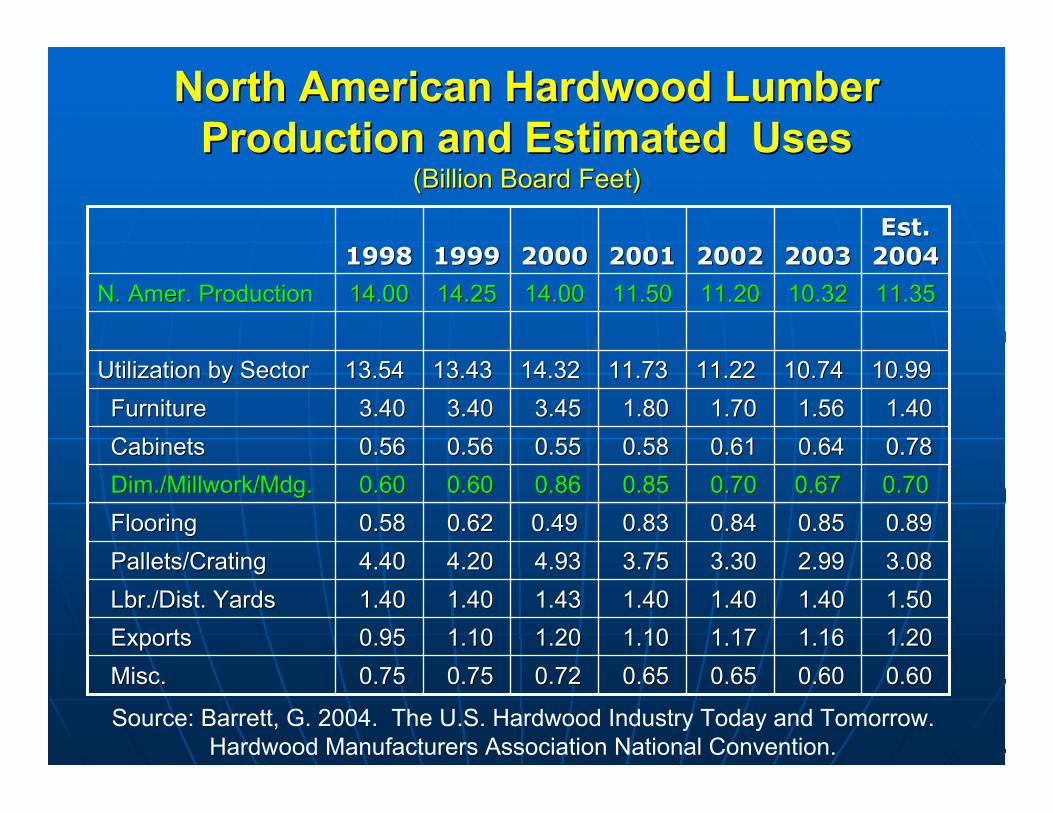

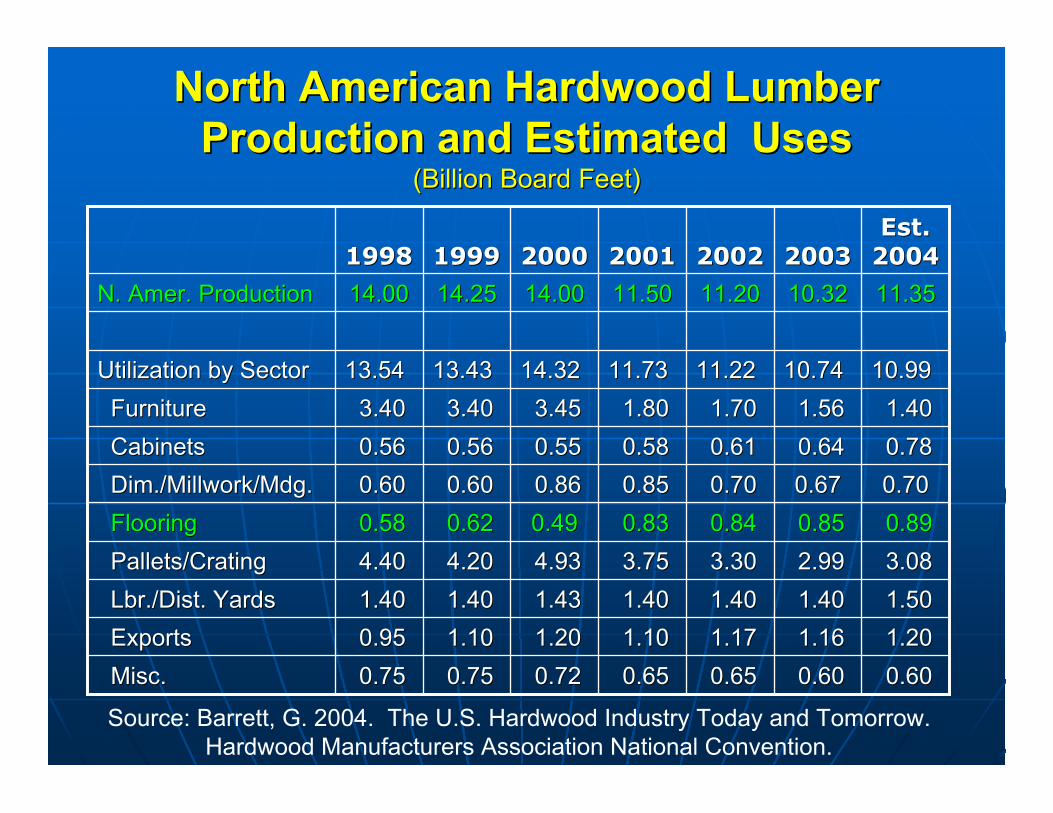

North American Hardwood LumberNorth American Hardwood LumberProduction and Estimated UsesProduction and Estimated Uses

(Billion Board Feet)(Billion Board Feet)

0.60 0.60 0.65 0.65 0.72 0.75 0.75 Misc.

1.20 1.20 1.16 1.16 1.17 1.17 1.10 1.10 1.20 1.20 1.10 1.10 0.95 0.95 Exports Exports

1.50 1.50 1.40 1.40 1.40 1.40 1.40 1.40 1.43 1.43 1.40 1.40 1.40 1.40 LbrLbr./Dist. Yards./Dist. Yards

3.08 3.08 2.99 2.99 3.30 3.30 3.75 3.75 4.93 4.93 4.20 4.20 4.40 4.40 Pallets/Crating Pallets/Crating

0.89 0.89 0.85 0.85 0.84 0.84 0.83 0.830.490.49 0.62 0.62 0.58 0.58 Flooring Flooring

0.700.700.670.67 0.70 0.70 0.85 0.85 0.86 0.86 0.60 0.60 0.60 0.60 Dim./Millwork/ Dim./Millwork/MdgMdg..

0.78 0.78 0.64 0.64 0.61 0.61 0.58 0.58 0.55 0.55 0.56 0.56 0.56 0.56 Cabinets Cabinets

1.40 1.40 1.56 1.56 1.70 1.70 1.80 1.80 3.45 3.45 3.40 3.40 3.40 3.40 Furniture Furniture

10.9910.9910.7410.7411.2211.2211.7311.7314.3214.3213.4313.4313.5413.54Utilization by SectorUtilization by Sector

11.3511.3510.3210.3211.2011.2011.5011.5014.0014.0014.2514.2514.0014.00N. Amer. ProductionN. Amer. Production

Est.Est.20042004200320032002200220012001200020001999199919981998

Source: Barrett, G. 2004. The U.S. Hardwood Industry Today and Tomorrow.Hardwood Manufacturers Association National Convention.

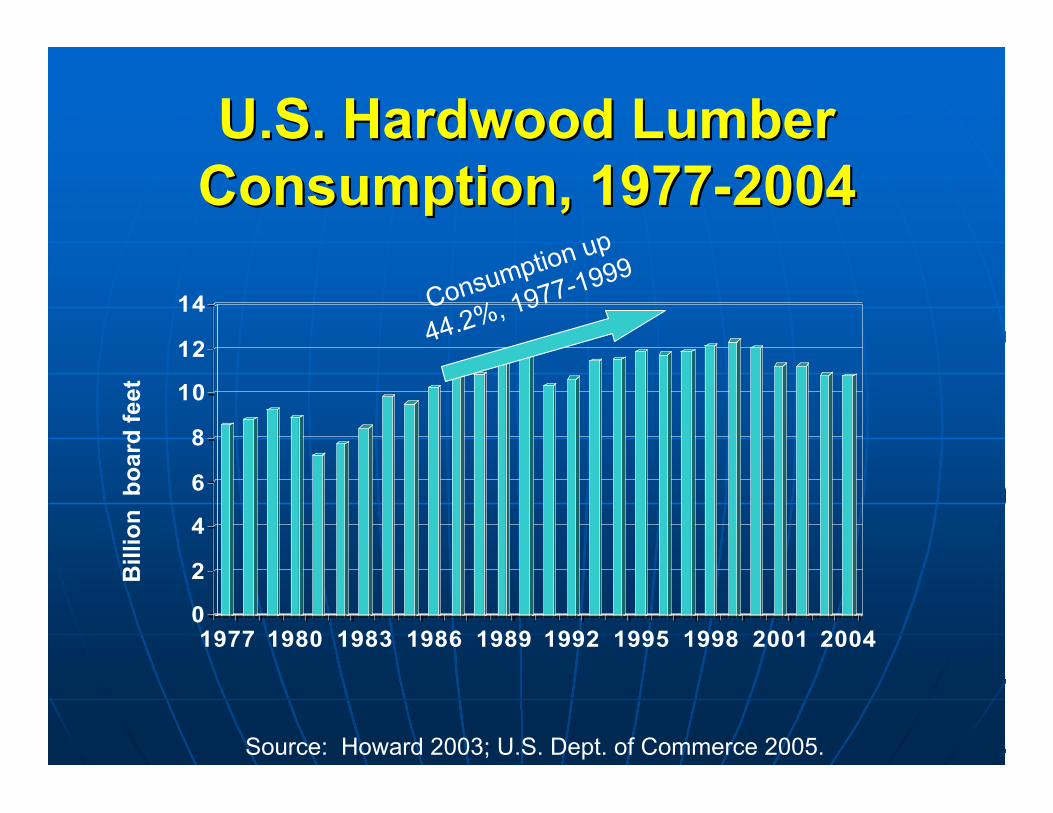

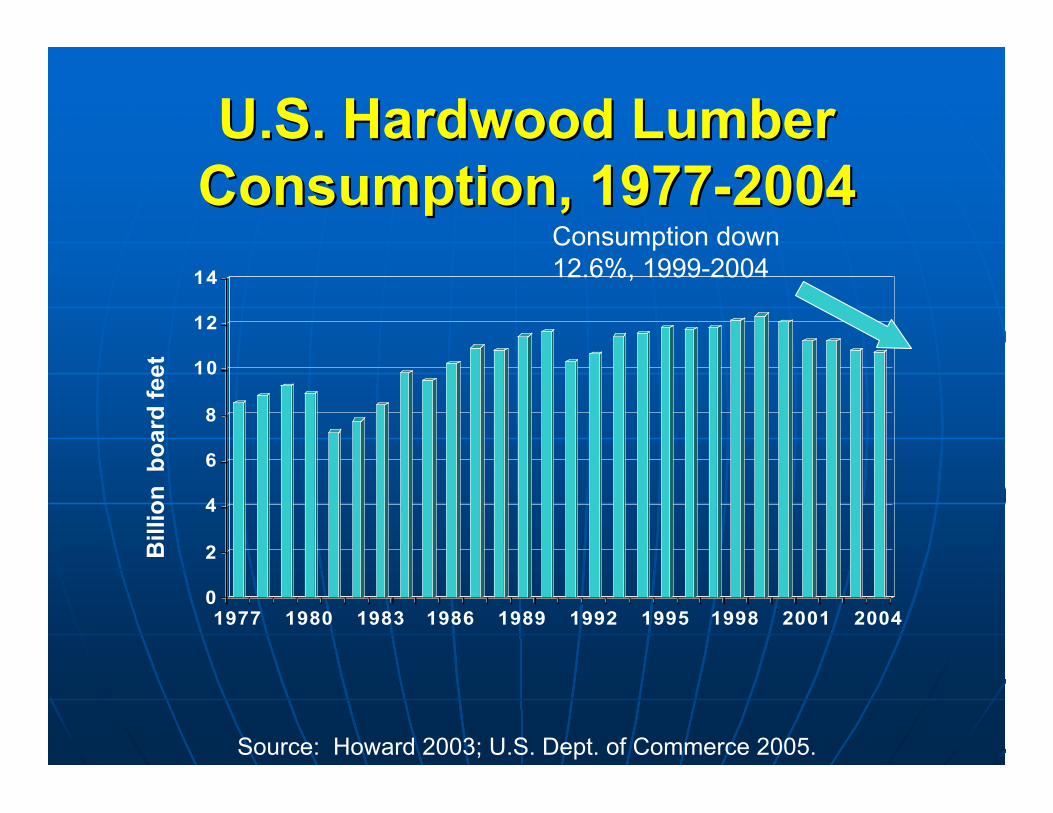

U.S. Hardwood LumberU.S. Hardwood LumberConsumption, 1977-2004Consumption, 1977-2004

0

2

4

6

8

10

12

14

1977 1980 1983 1986 1989 1992 1995 1998 2001 2004

Bill

ion

bo

ard

fee

t

Source: Howard 2003; U.S. Dept. of Commerce 2005.

Consumption up

44.2%, 1977-1999

U.S. Hardwood LumberU.S. Hardwood LumberConsumption, 1977-2004Consumption, 1977-2004

0

2

4

6

8

10

12

14

1977 1980 1983 1986 1989 1992 1995 1998 2001 2004

Bill

ion

bo

ard

fee

t

Source: Howard 2003; U.S. Dept. of Commerce 2005.

Consumption down12.6%, 1999-2004

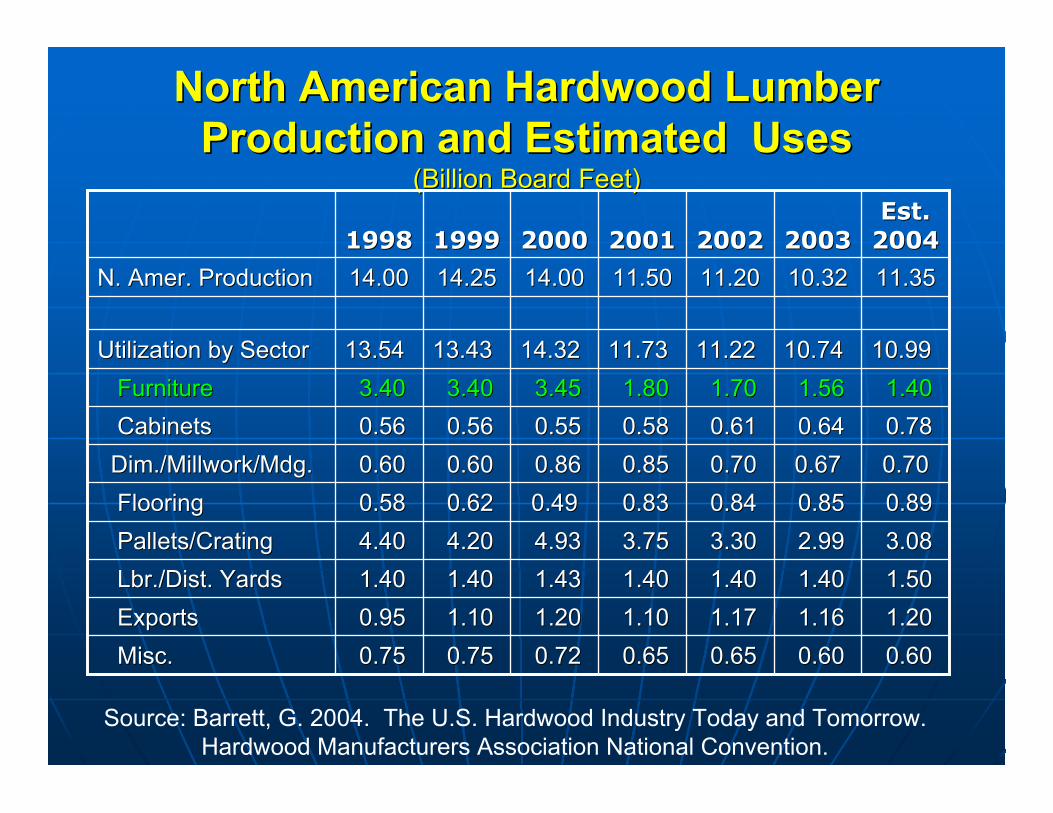

North American Hardwood LumberNorth American Hardwood LumberProduction and Estimated UsesProduction and Estimated Uses

(Billion Board Feet)(Billion Board Feet)

0.60 0.60 0.60 0.60 0.65 0.65 0.65 0.65 0.72 0.72 0.75 0.75 0.75 0.75 Misc. Misc.

1.20 1.20 1.16 1.16 1.17 1.17 1.10 1.10 1.20 1.20 1.10 1.10 0.95 0.95 Exports Exports

1.50 1.50 1.40 1.40 1.40 1.40 1.40 1.40 1.43 1.43 1.40 1.40 1.40 1.40 LbrLbr./Dist. Yards./Dist. Yards

3.08 3.08 2.99 2.99 3.30 3.30 3.75 3.75 4.93 4.93 4.20 4.20 4.40 4.40 Pallets/Crating Pallets/Crating

0.89 0.89 0.85 0.85 0.84 0.84 0.83 0.830.490.49 0.62 0.62 0.58 0.58 Flooring Flooring

0.700.700.670.67 0.70 0.70 0.85 0.85 0.86 0.86 0.60 0.60 0.60 0.60 Dim./Millwork/ Dim./Millwork/MdgMdg..

0.78 0.78 0.64 0.64 0.61 0.61 0.58 0.58 0.55 0.55 0.56 0.56 0.56 0.56 Cabinets Cabinets

1.40 1.40 1.56 1.56 1.70 1.70 1.80 1.80 3.45 3.45 3.40 3.40 3.40 3.40 Furniture Furniture

10.9910.9910.7410.7411.2211.2211.7311.7314.3214.3213.4313.4313.5413.54Utilization by SectorUtilization by Sector

11.3511.3510.3210.3211.2011.2011.5011.5014.0014.0014.2514.2514.0014.00N. Amer. ProductionN. Amer. Production

Est.Est.20042004200320032002200220012001200020001999199919981998

Source: Barrett, G. 2004. The U.S. Hardwood Industry Today and Tomorrow.Hardwood Manufacturers Association National Convention.

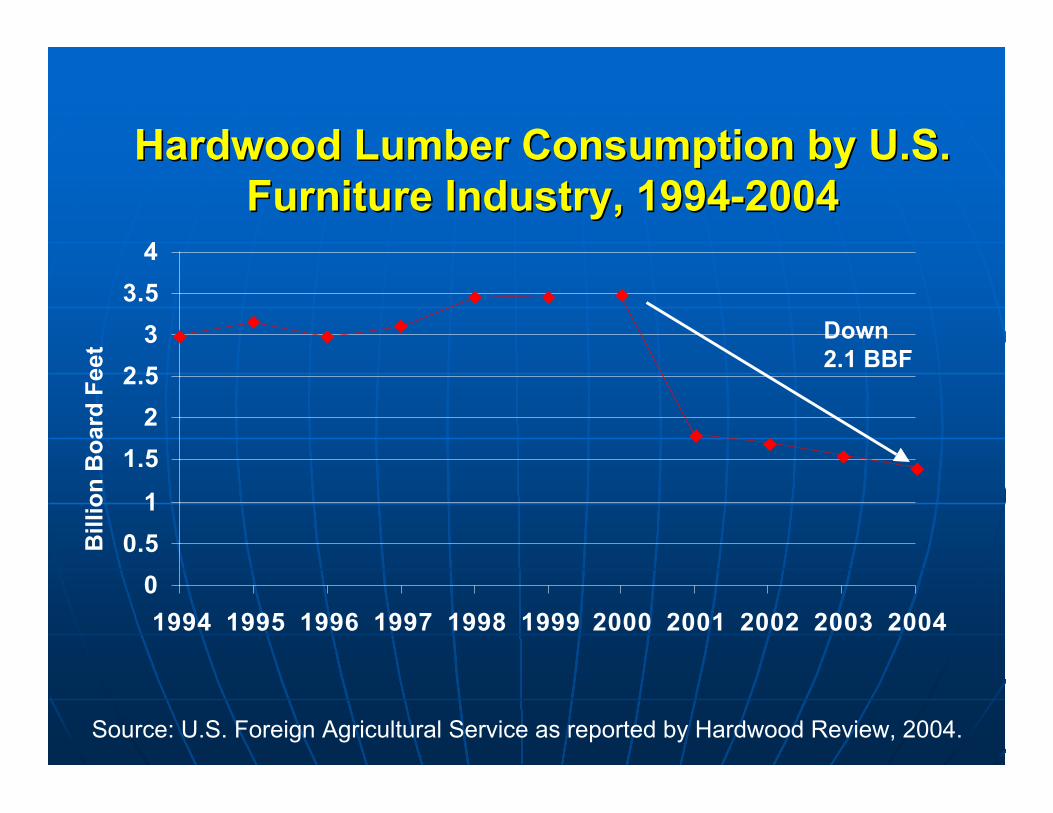

Hardwood Lumber Consumption by U.S.Hardwood Lumber Consumption by U.S.Furniture Industry, 1994-2004Furniture Industry, 1994-2004

0

0.5

1

1.5

2

2.5

3

3.5

4

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Bill

ion

Bo

ard

Fee

t

Source: U.S. Foreign Agricultural Service as reported by Hardwood Review, 2004.

Down2.1 BBF

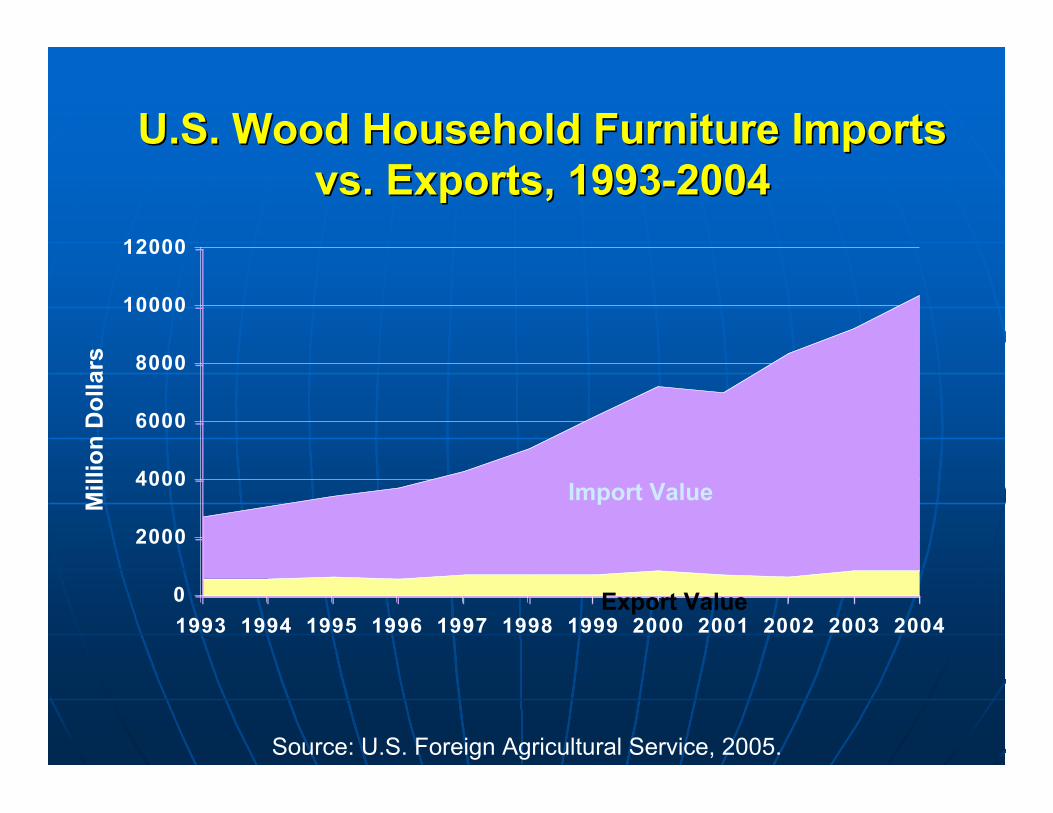

U.S. Wood Household Furniture ImportsU.S. Wood Household Furniture Importsvs. Exports, 1993-2004vs. Exports, 1993-2004

0

2000

4000

6000

8000

10000

12000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Mill

ion

Do

llars

Source: U.S. Foreign Agricultural Service, 2005.

Export Value

Import Value

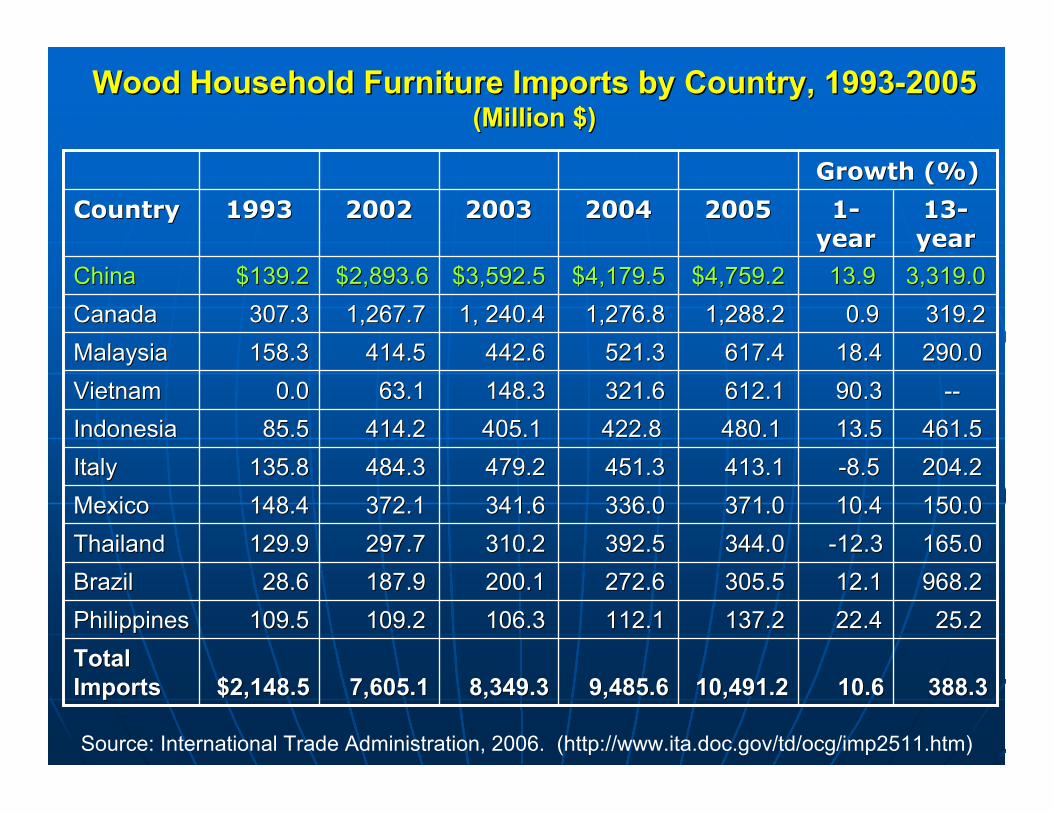

Wood Household Furniture Imports by Country, 1993-2005Wood Household Furniture Imports by Country, 1993-2005(Million $)(Million $)

290.0 290.0 18.4 18.4 617.4 617.4 521.3 521.3 442.6 442.6 414.5 414.5 158.3 158.3MalaysiaMalaysia

9,485.69,485.6

112.1 112.1

272.6 272.6

392.5 392.5

336.0 336.0

451.3 451.3

422.8 422.8

321.6 321.6

1,276.8 1,276.8

$4,179.5$4,179.5

20042004

8,349.38,349.3

106.3 106.3

200.1 200.1

310.2 310.2

341.6 341.6

479.2 479.2

405.1 405.1

148.3 148.3

1, 240.4 1, 240.4

$3,592.5$3,592.5

20032003 13-13-yearyear

1-1-yearyear

200520052002200219931993CountryCountry

10.610.6

22.4 22.4

12.1 12.1

-12.3 -12.3

10.4 10.4

-8.5 -8.5

13.5 13.5

90.3 90.3

0.9 0.9

13.9 13.9

Growth (%)Growth (%)

388.3388.310,491.210,491.27,605.17,605.1$2,148.5$2,148.5TotalTotalImportsImports

25.2 25.2 137.2 137.2 109.2 109.2 109.5 109.5PhilippinesPhilippines

968.2 968.2 305.5 305.5 187.9 187.9 28.6 28.6BrazilBrazil

165.0 165.0 344.0 344.0 297.7 297.7 129.9 129.9ThailandThailand

150.0 150.0 371.0 371.0 372.1 372.1 148.4 148.4MexicoMexico

204.2 204.2 413.1 413.1 484.3 484.3 135.8 135.8ItalyItaly

461.5 461.5 480.1 480.1 414.2 414.2 85.5 85.5IndonesiaIndonesia

-- -- 612.1 612.1 63.1 63.1 0.0 0.0VietnamVietnam

319.2 319.2 1,288.2 1,288.2 1,267.7 1,267.7 307.3 307.3CanadaCanada

3,319.03,319.0$4,759.2$4,759.2 $2,893.6 $2,893.6 $139.2 $139.2ChinaChina

Source: International Trade Administration, 2006. (http://www.ita.doc.gov/td/ocg/imp2511.htm)

North American Hardwood LumberNorth American Hardwood LumberProduction and Estimated UsesProduction and Estimated Uses

(Billion Board Feet)(Billion Board Feet)

0.60 0.60 0.60 0.60 0.65 0.65 0.65 0.65 0.72 0.72 0.75 0.75 0.75 0.75 Misc. Misc.

1.20 1.20 1.16 1.16 1.17 1.17 1.10 1.10 1.20 1.20 1.10 1.10 0.95 0.95 Exports Exports

1.50 1.50 1.40 1.40 1.40 1.40 1.40 1.40 1.43 1.43 1.40 1.40 1.40 1.40 LbrLbr./Dist. Yards./Dist. Yards

3.08 3.08 2.99 2.99 3.30 3.30 3.75 3.75 4.93 4.93 4.20 4.20 4.40 4.40 Pallets/Crating Pallets/Crating

0.89 0.89 0.85 0.85 0.84 0.84 0.83 0.830.490.49 0.62 0.62 0.58 0.58 Flooring Flooring

0.700.700.670.67 0.70 0.70 0.85 0.85 0.86 0.86 0.60 0.60 0.60 0.60 Dim./Millwork/ Dim./Millwork/MldgMldg..

0.78 0.78 0.64 0.64 0.61 0.61 0.58 0.58 0.55 0.55 0.56 0.56 0.56 0.56 Cabinets Cabinets

1.40 1.40 1.56 1.56 1.70 1.70 1.80 1.80 3.45 3.45 3.40 3.40 3.40 3.40 Furniture Furniture

10.9910.9910.7410.7411.2211.2211.7311.7314.3214.3213.4313.4313.5413.54Utilization by SectorUtilization by Sector

11.3511.3510.3210.3211.2011.2011.5011.5014.0014.0014.2514.2514.0014.00N. Amer. ProductionN. Amer. Production

Est.Est.20042004200320032002200220012001200020001999199919981998

Source: Barrett, G. 2004. The U.S. Hardwood Industry Today and Tomorrow.Hardwood Manufacturers Association National Convention.

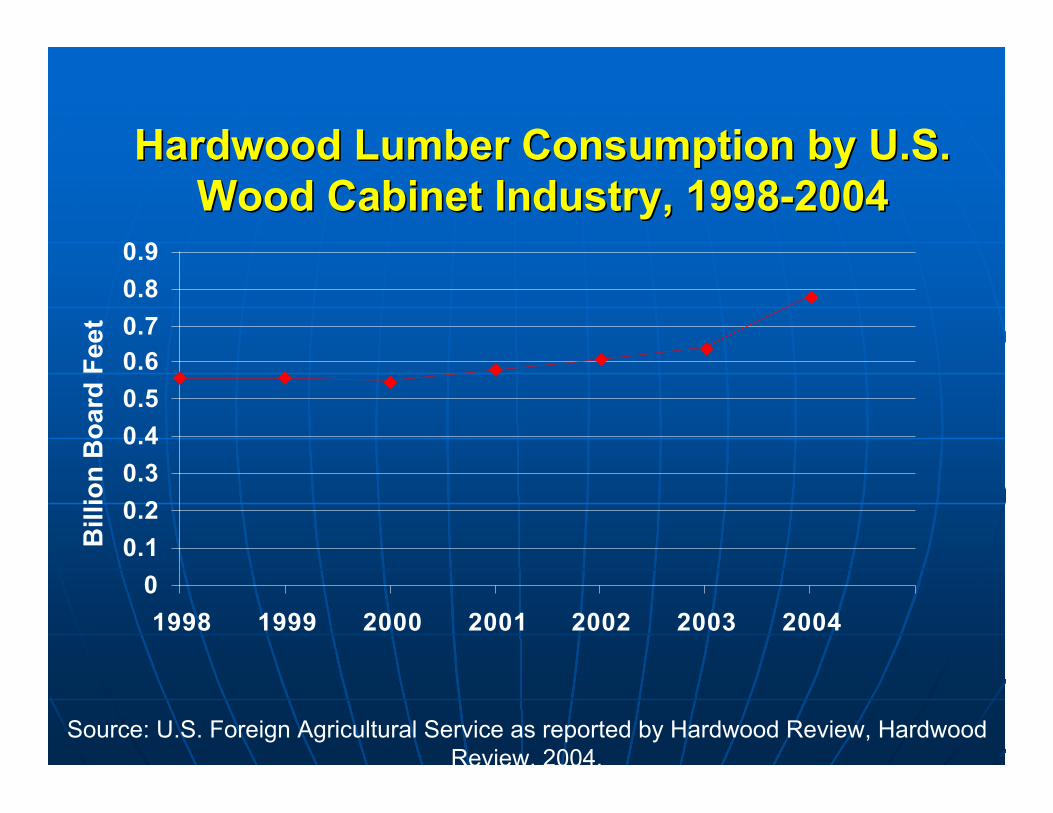

Hardwood Lumber Consumption by U.S.Hardwood Lumber Consumption by U.S.Wood Cabinet Industry, 1998-2004Wood Cabinet Industry, 1998-2004

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1998 1999 2000 2001 2002 2003 2004

Bill

ion

Bo

ard

Fee

t

Source: U.S. Foreign Agricultural Service as reported by Hardwood Review, HardwoodReview, 2004.

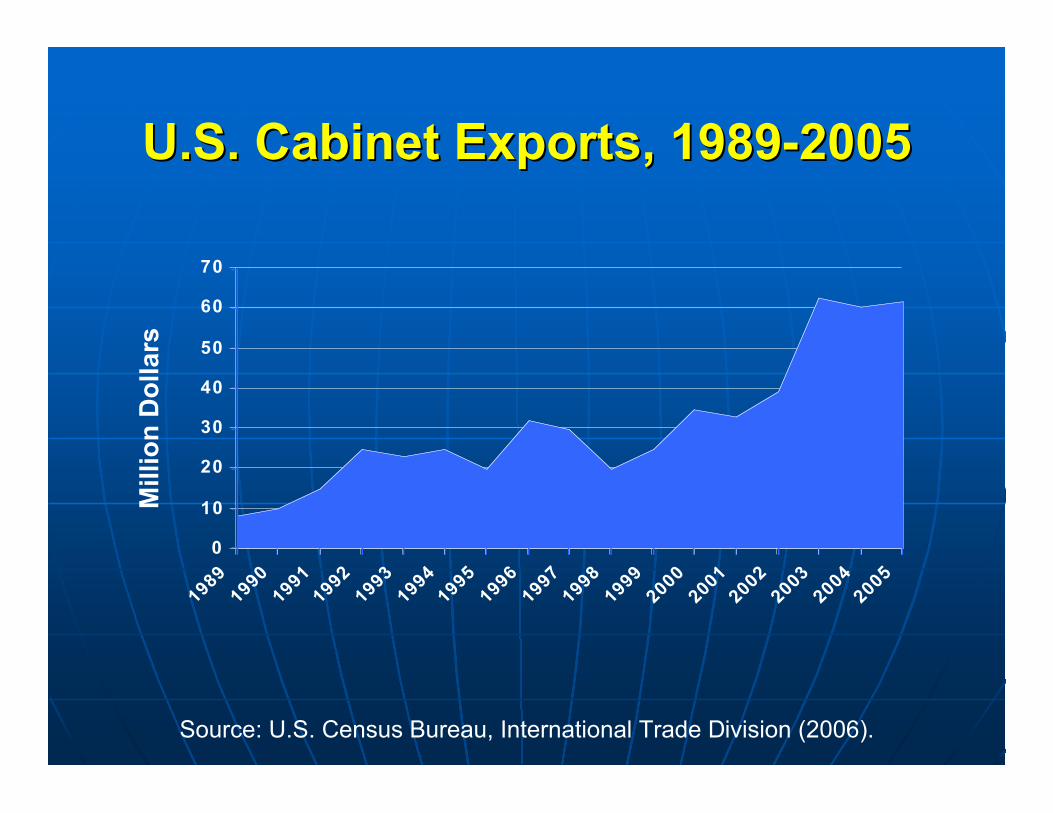

U.S. Cabinet Exports, 1989-2005U.S. Cabinet Exports, 1989-2005

0

10

20

30

40

50

60

70

19891990

19911992

19931994

19951996

19971998

19992000

20012002

20032004

2005

Mill

ion

Do

llars

Source: U.S. Census Bureau, International Trade Division (2006).

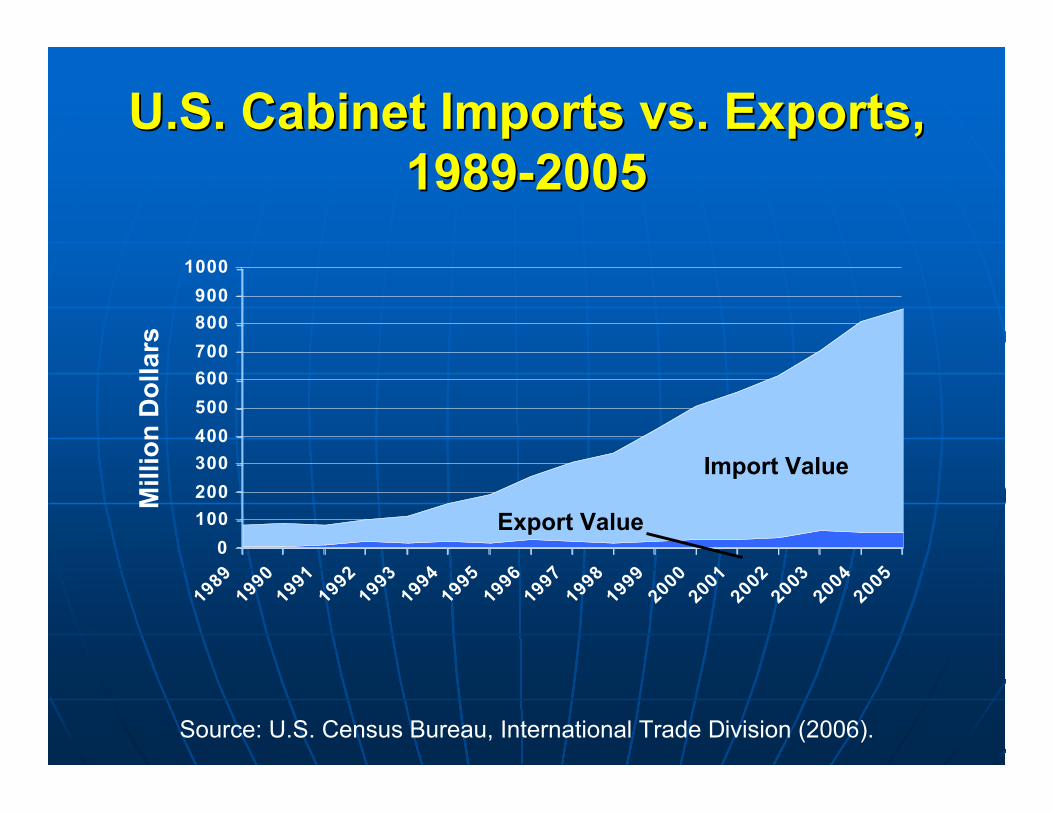

U.S. Cabinet Imports vs. Exports,U.S. Cabinet Imports vs. Exports,1989-20051989-2005

0

100

200

300

400

500

600

700

800

900

1000

19891990

19911992

19931994

19951996

19971998

19992000

20012002

20032004

2005

Mill

ion

Do

llars

Source: U.S. Census Bureau, International Trade Division (2006).

Export Value

Import Value

North American Hardwood LumberNorth American Hardwood LumberProduction and Estimated UsesProduction and Estimated Uses

(Billion Board Feet)(Billion Board Feet)

0.60 0.60 0.60 0.60 0.65 0.65 0.65 0.65 0.72 0.72 0.75 0.75 0.75 0.75 Misc. Misc.

1.20 1.20 1.16 1.16 1.17 1.17 1.10 1.10 1.20 1.20 1.10 1.10 0.95 0.95 Exports Exports

1.50 1.50 1.40 1.40 1.40 1.40 1.40 1.40 1.43 1.43 1.40 1.40 1.40 1.40 LbrLbr./Dist. Yards./Dist. Yards

3.08 3.08 2.99 2.99 3.30 3.30 3.75 3.75 4.93 4.93 4.20 4.20 4.40 4.40 Pallets/Crating Pallets/Crating

0.89 0.89 0.85 0.85 0.84 0.84 0.83 0.830.490.49 0.62 0.62 0.58 0.58 Flooring Flooring

0.700.700.670.67 0.70 0.70 0.85 0.85 0.86 0.86 0.60 0.60 0.60 0.60 Dim./Millwork/ Dim./Millwork/MdgMdg..

0.78 0.78 0.64 0.64 0.61 0.61 0.58 0.58 0.55 0.55 0.56 0.56 0.56 0.56 Cabinets Cabinets

1.40 1.40 1.56 1.56 1.70 1.70 1.80 1.80 3.45 3.45 3.40 3.40 3.40 3.40 Furniture Furniture

10.9910.9910.7410.7411.2211.2211.7311.7314.3214.3213.4313.4313.5413.54Utilization by SectorUtilization by Sector

11.3511.3510.3210.3211.2011.2011.5011.5014.0014.0014.2514.2514.0014.00N. Amer. ProductionN. Amer. Production

Est.Est.20042004200320032002200220012001200020001999199919981998

Source: Barrett, G. 2004. The U.S. Hardwood Industry Today and Tomorrow.Hardwood Manufacturers Association National Convention.

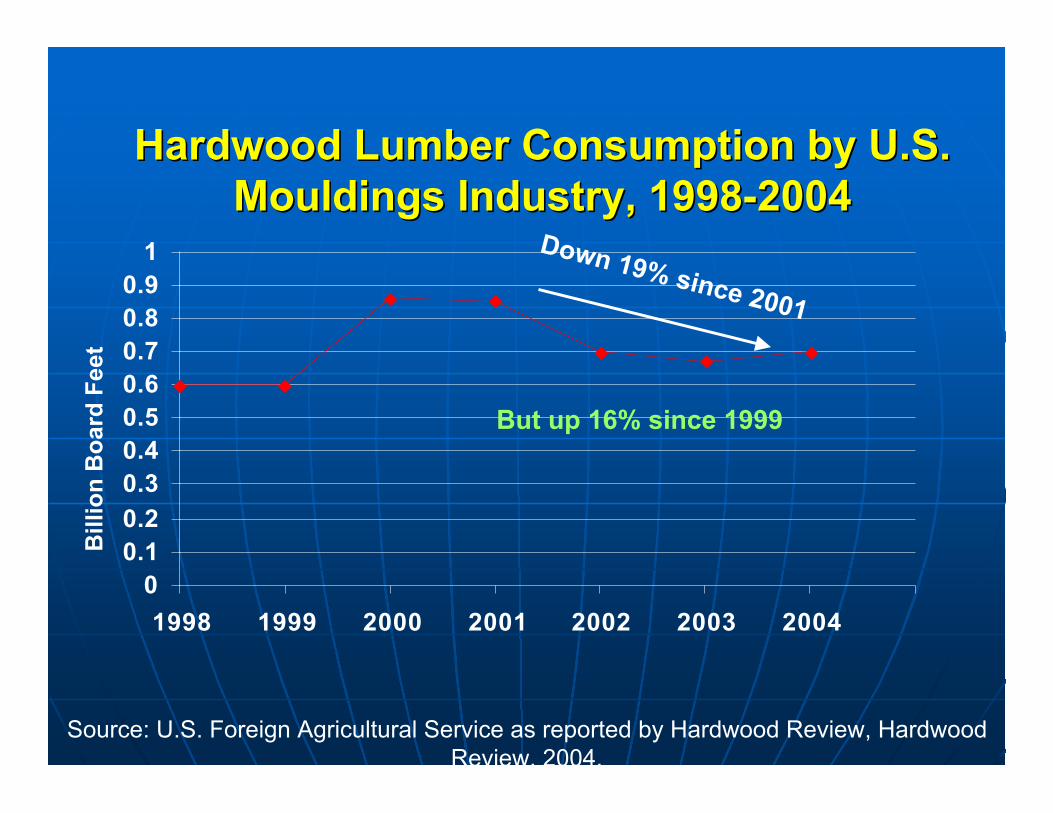

Hardwood Lumber Consumption by U.S.Hardwood Lumber Consumption by U.S.MouldingsMouldings Industry, 1998-2004 Industry, 1998-2004

00.10.2

0.30.40.50.60.70.80.9

1

1998 1999 2000 2001 2002 2003 2004

Bill

ion

Bo

ard

Fee

t

Source: U.S. Foreign Agricultural Service as reported by Hardwood Review, HardwoodReview, 2004.

Down 19% since 2001

But up 16% since 1999

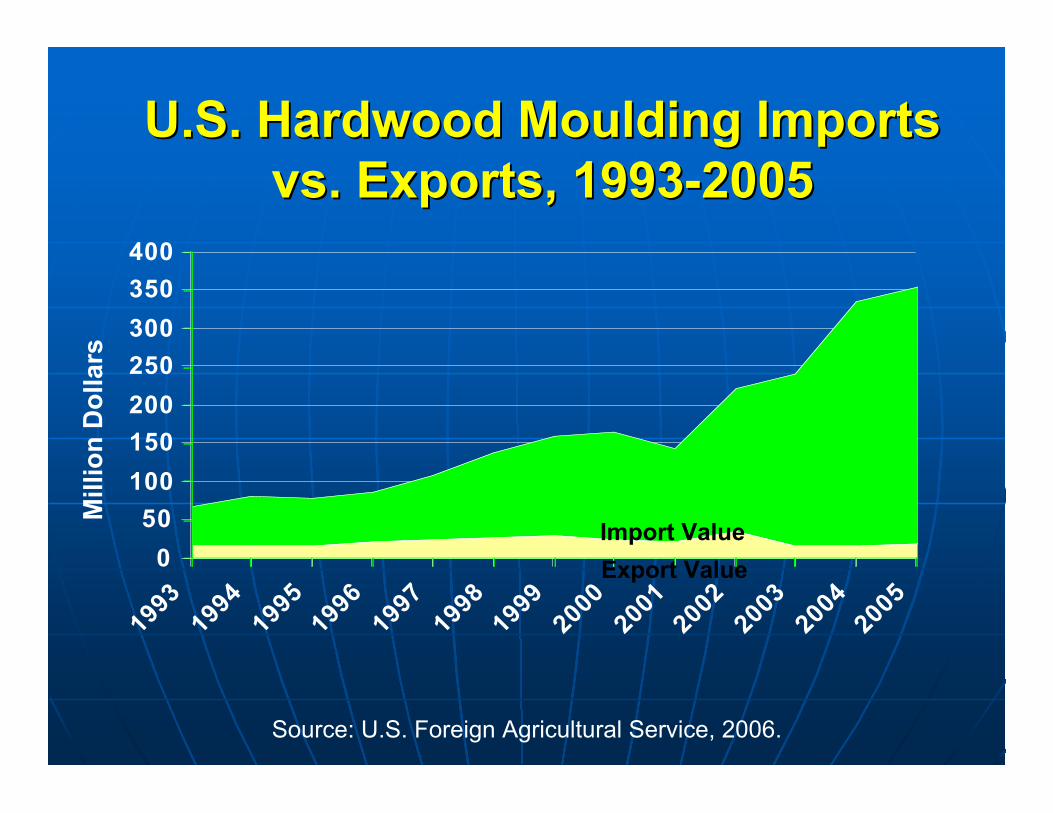

U.S. Hardwood U.S. Hardwood MouldingMoulding Imports Importsvs. Exports, 1993-2005vs. Exports, 1993-2005

0

50

100

150

200

250

300

350

400

19931994

19951996

19971998

19992000

20012002

20032004

2005

Mill

ion

Do

llars

Source: U.S. Foreign Agricultural Service, 2006.

Export Value

Import Value

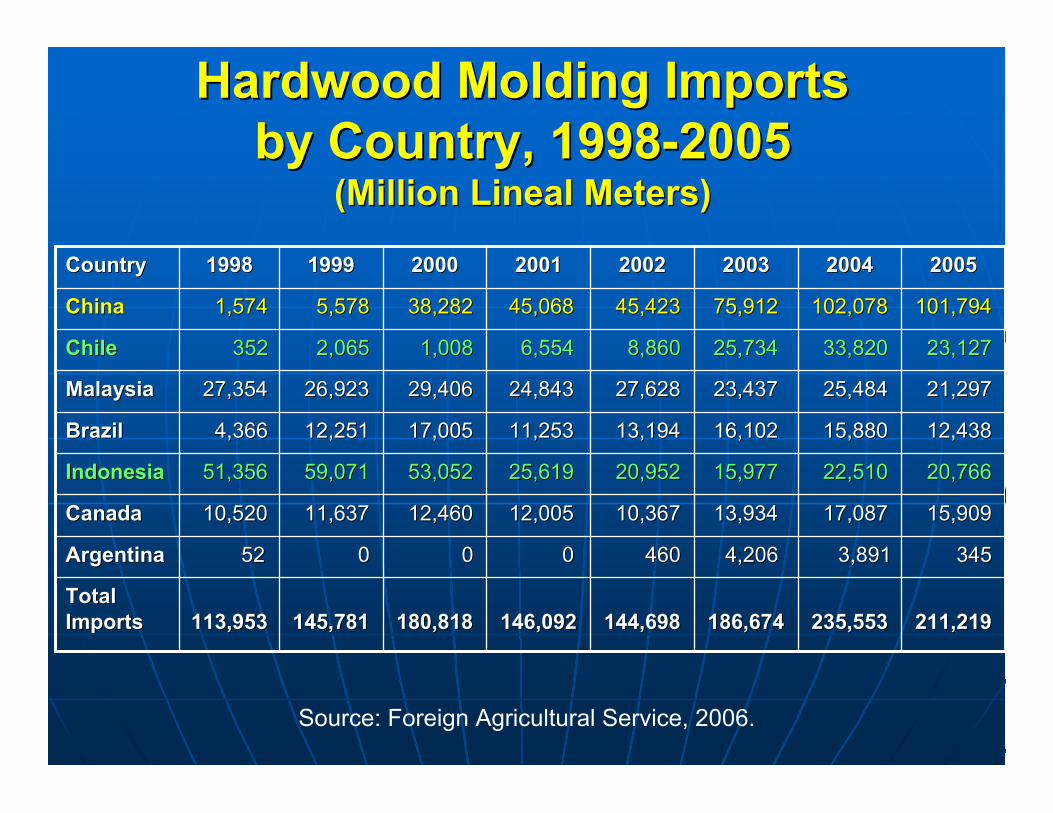

Hardwood Molding ImportsHardwood Molding Importsby Country, 1998-2005by Country, 1998-2005

(Million Lineal Meters)(Million Lineal Meters)

186,674186,674

4,206 4,206

13,93413,934

15,97715,977

16,10216,102

23,43723,437

25,73425,734

75,91275,912

20032003

235,553235,553

3,891 3,891

17,087 17,087

22,510 22,510

15,880 15,880

25,484 25,484

33,820 33,820

102,078102,078

20042004

144,698144,698

460 460

10,367 10,367

20,952 20,952

13,194 13,194

27,628 27,628

8,860 8,860

45,423 45,423

20022002 2005200520012001200020001999199919981998CountryCountry

146,092146,092

0 0

12,005 12,005

25,619 25,619

11,253 11,253

24,843 24,843

6,554 6,554

45,068 45,068

211,219211,219180,818180,818145,781145,781113,953113,953TotalTotalImportsImports

345 345 0 0 0 0 52 52ArgentinaArgentina

15,909 15,909 12,460 12,460 11,637 11,637 10,520 10,520CanadaCanada

20,766 20,766 53,052 53,052 59,071 59,071 51,356 51,356IndonesiaIndonesia

12,438 12,438 17,005 17,005 12,251 12,251 4,366 4,366BrazilBrazil

21,297 21,297 29,406 29,406 26,923 26,923 27,354 27,354MalaysiaMalaysia

23,127 23,127 1,008 1,008 2,065 2,065 352 352ChileChile

101,794101,794 38,282 38,282 5,578 5,578 1,574 1,574ChinaChina

Source: Foreign Agricultural Service, 2006.

North American Hardwood LumberNorth American Hardwood LumberProduction and Estimated UsesProduction and Estimated Uses

(Billion Board Feet)(Billion Board Feet)

0.60 0.60 0.60 0.60 0.65 0.65 0.65 0.65 0.72 0.72 0.75 0.75 0.75 0.75 Misc. Misc.

1.20 1.20 1.16 1.16 1.17 1.17 1.10 1.10 1.20 1.20 1.10 1.10 0.95 0.95 Exports Exports

1.50 1.50 1.40 1.40 1.40 1.40 1.40 1.40 1.43 1.43 1.40 1.40 1.40 1.40 LbrLbr./Dist. Yards./Dist. Yards

3.08 3.08 2.99 2.99 3.30 3.30 3.75 3.75 4.93 4.93 4.20 4.20 4.40 4.40 Pallets/Crating Pallets/Crating

0.89 0.89 0.85 0.85 0.84 0.84 0.83 0.830.490.49 0.62 0.62 0.58 0.58 Flooring Flooring

0.700.700.670.67 0.70 0.70 0.85 0.85 0.86 0.86 0.60 0.60 0.60 0.60 Dim./Millwork/ Dim./Millwork/MdgMdg..

0.78 0.78 0.64 0.64 0.61 0.61 0.58 0.58 0.55 0.55 0.56 0.56 0.56 0.56 Cabinets Cabinets

1.40 1.40 1.56 1.56 1.70 1.70 1.80 1.80 3.45 3.45 3.40 3.40 3.40 3.40 Furniture Furniture

10.9910.9910.7410.7411.2211.2211.7311.7314.3214.3213.4313.4313.5413.54Utilization by SectorUtilization by Sector

11.3511.3510.3210.3211.2011.2011.5011.5014.0014.0014.2514.2514.0014.00N. Amer. ProductionN. Amer. Production

Est.Est.20042004200320032002200220012001200020001999199919981998

Source: Barrett, G. 2004. The U.S. Hardwood Industry Today and Tomorrow.Hardwood Manufacturers Association National Convention.

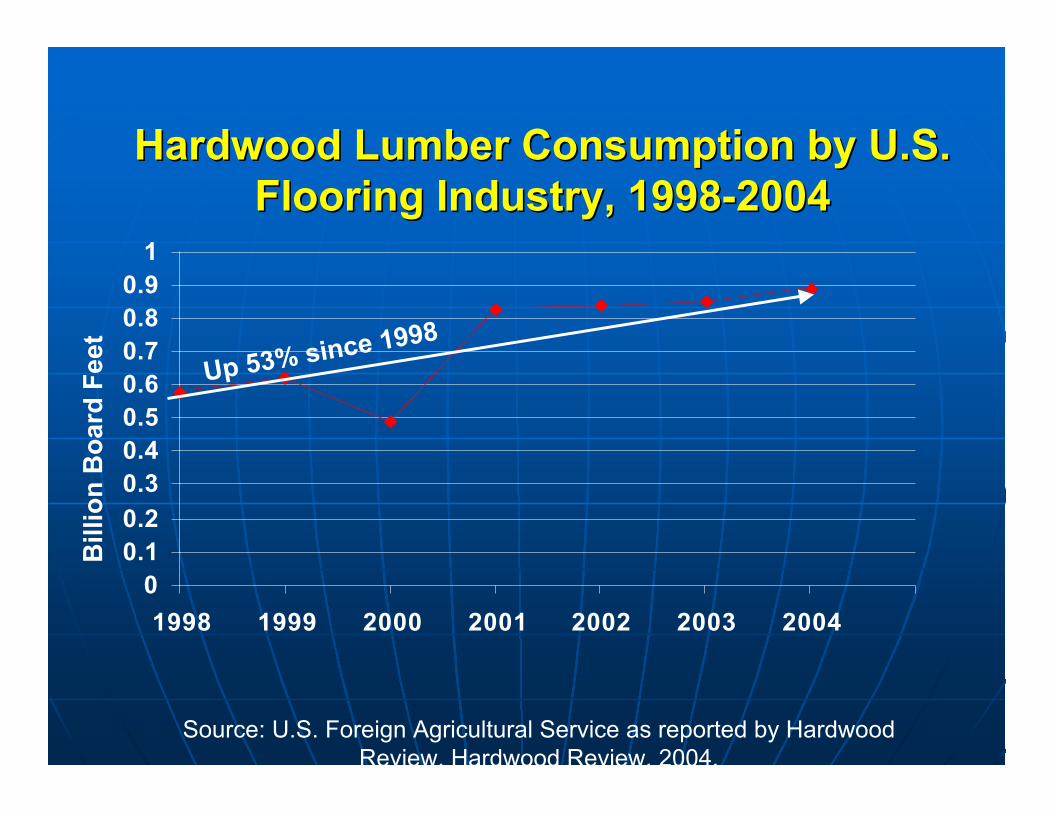

Hardwood Lumber Consumption by U.S.Hardwood Lumber Consumption by U.S.Flooring Industry, 1998-2004Flooring Industry, 1998-2004

00.10.2

0.30.40.50.60.70.80.9

1

1998 1999 2000 2001 2002 2003 2004

Bill

ion

Bo

ard

Fee

t

Source: U.S. Foreign Agricultural Service as reported by HardwoodReview, Hardwood Review, 2004.

Up 53% since 1998

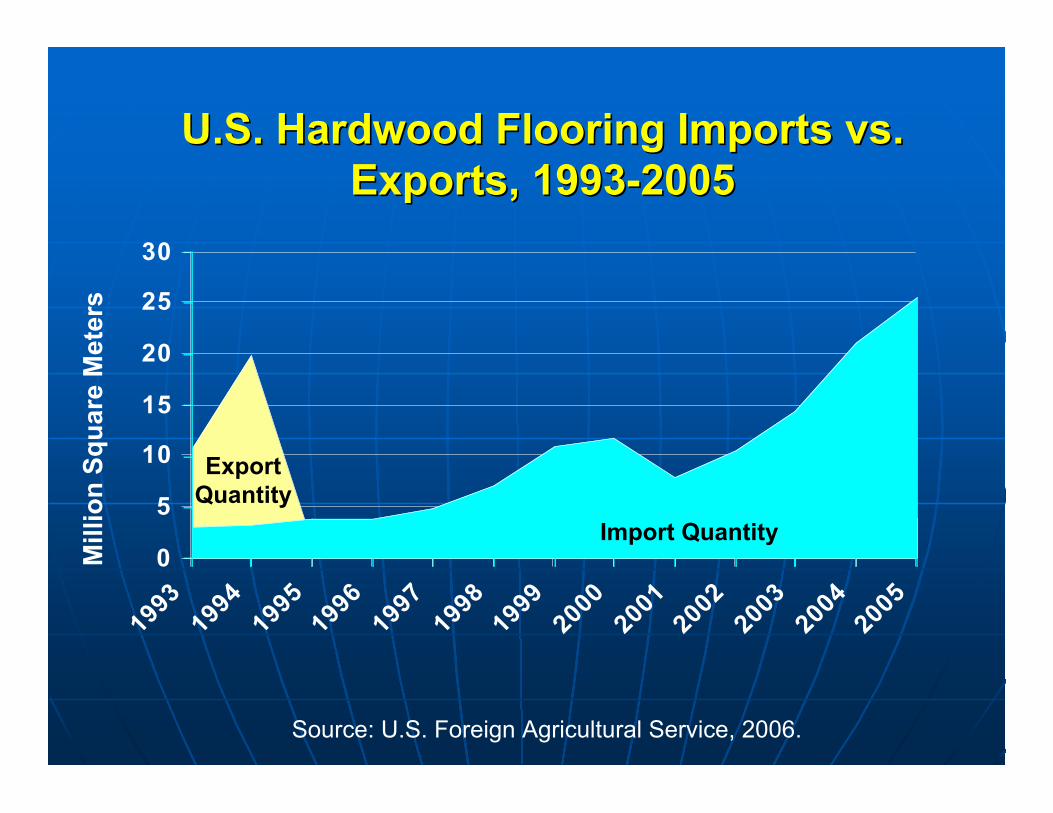

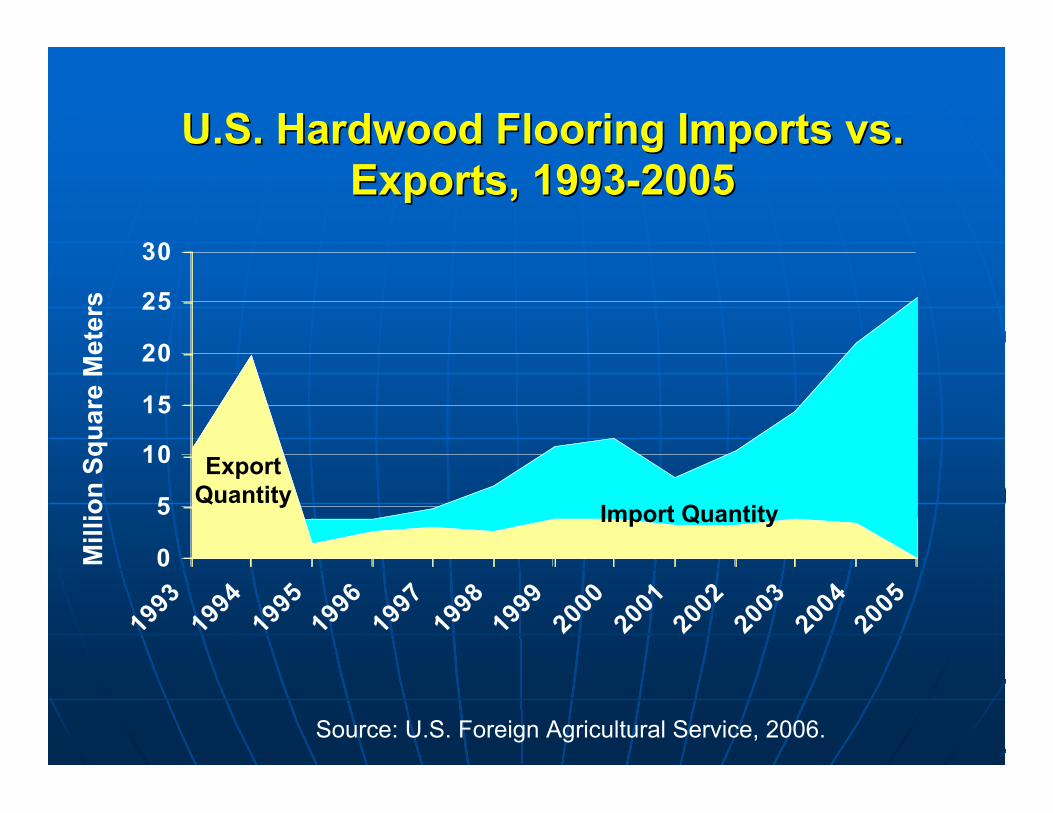

U.S. Hardwood Flooring Imports vs.U.S. Hardwood Flooring Imports vs.Exports, 1993-2005Exports, 1993-2005

0

5

10

15

20

25

30

19931994

19951996

19971998

19992000

20012002

20032004

2005

Mill

ion

Sq

uar

e M

eter

s

Source: U.S. Foreign Agricultural Service, 2006.

ExportQuantity

Import Quantity

U.S. Hardwood Flooring Imports vs.U.S. Hardwood Flooring Imports vs.Exports, 1993-2005Exports, 1993-2005

0

5

10

15

20

25

30

19931994

19951996

19971998

19992000

20012002

20032004

2005

Mill

ion

Sq

uar

e M

eter

s

Source: U.S. Foreign Agricultural Service, 2006.

ExportQuantity

Import Quantity

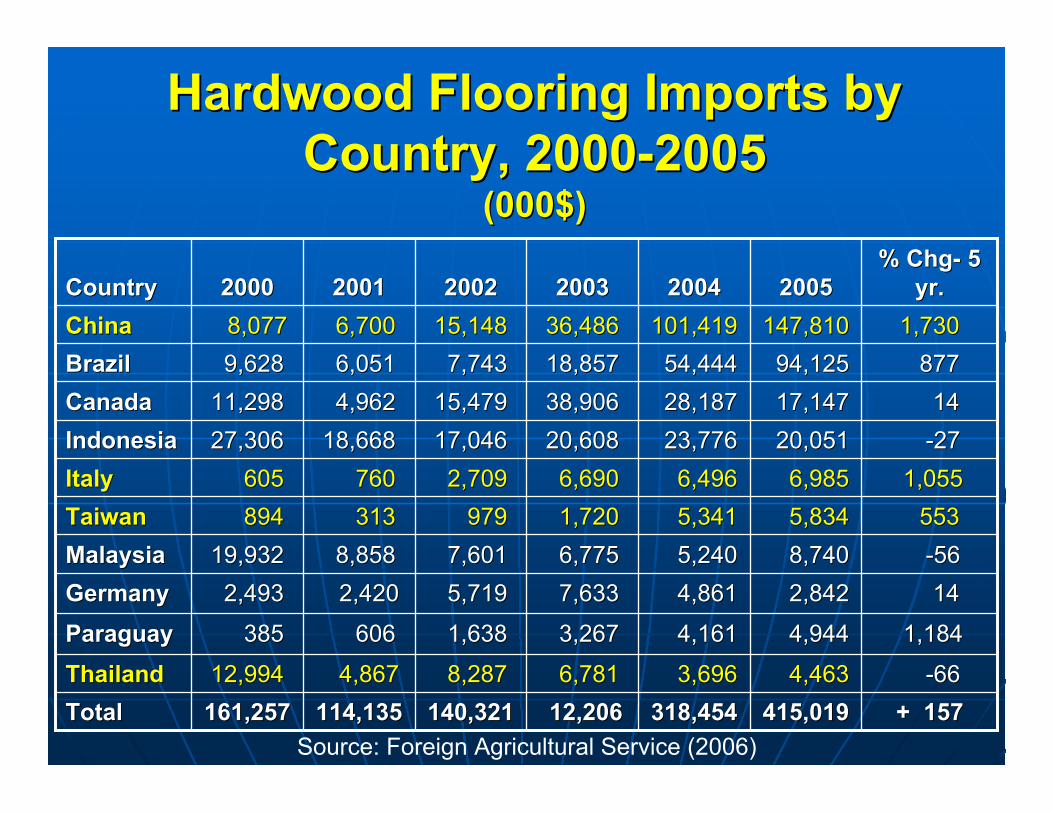

Hardwood Flooring Imports byHardwood Flooring Imports byCountry, 2000-2005Country, 2000-2005

(000$)(000$)

318,454318,454

3,696 3,696

4,161 4,161

4,861 4,861

5,240 5,240

5,341 5,341

6,496 6,496

23,776 23,776

28,187 28,187

54,444 54,444

101,419101,419

20042004

14 14 2,842 2,842 7,633 7,633 5,719 5,719 2,420 2,420 2,493 2,493GermanyGermany

553 553 5,834 5,834 1,720 1,720 979 979 313 313 894 894TaiwanTaiwan

-66 -66 4,463 4,463 6,781 6,781 8,287 8,287 4,867 4,86712,99412,994ThailandThailand

140,321140,321

1,638 1,638

7,601 7,601

2,709 2,709

17,04617,046

15,47915,479

7,743 7,743

15,14815,148

20022002

12,206 12,206

3,267 3,267

6,775 6,775

6,690 6,690

20,60820,608

38,90638,906

18,85718,857

36,48636,486

20032003

415,019415,019

4,944 4,944

8,740 8,740

6,985 6,985

20,051 20,051

17,147 17,147

94,125 94,125

147,810147,810

20052005% Chg- 5% Chg- 5

yr.yr.2001200120002000CountryCountry

+ 157+ 157

1,184 1,184

-56 -56

1,055 1,055

-27 -27

14 14

877 877

1,7301,730

114,135114,135161,257161,257TotalTotal

606 606 385 385ParaguayParaguay

8,858 8,85819,93219,932MalaysiaMalaysia

760 760 605 605ItalyItaly

18,66818,66827,30627,306IndonesiaIndonesia

4,962 4,96211,29811,298CanadaCanada

6,051 6,051 9,628 9,628BrazilBrazil

6,700 6,700 8,077 8,077ChinaChina

Source: Foreign Agricultural Service (2006)

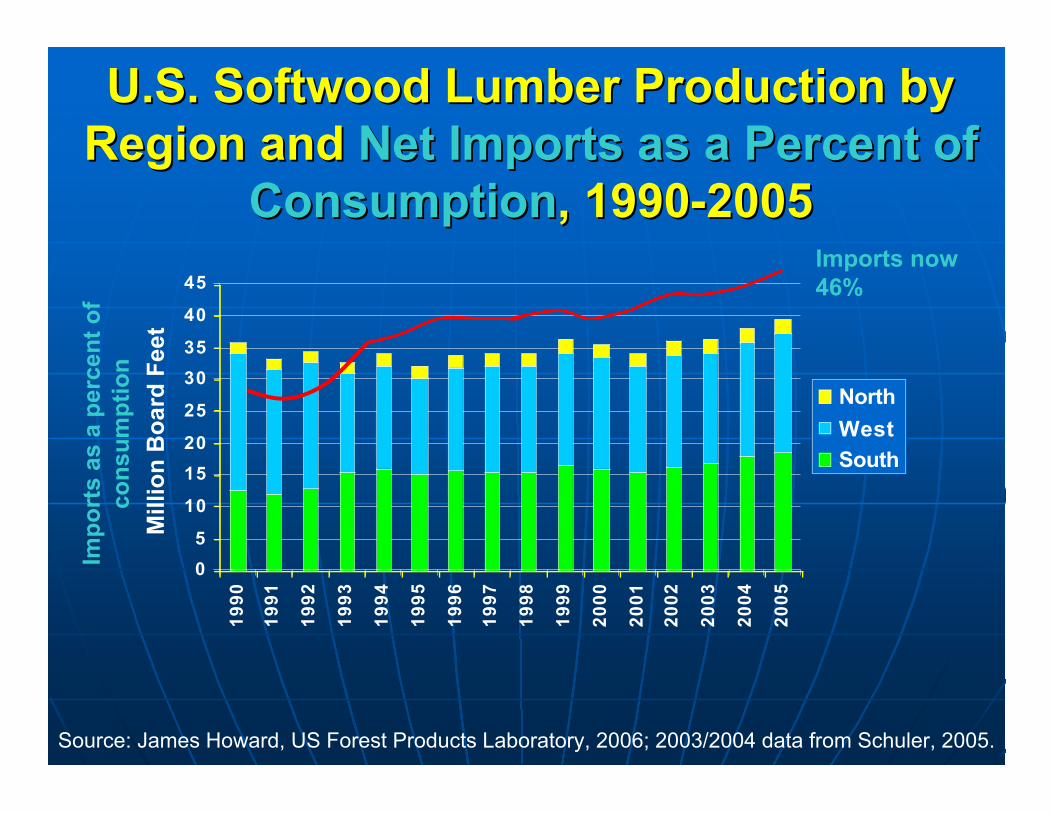

U.S. Softwood Lumber Production byU.S. Softwood Lumber Production byRegion and Region and Net Imports as a Percent ofNet Imports as a Percent of

ConsumptionConsumption, 1990-2005, 1990-2005

0

5

10

15

20

25

30

35

40

45

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

North

West

South

Mill

ion

Bo

ard

Fee

t

Source: James Howard, US Forest Products Laboratory, 2006; 2003/2004 data from Schuler, 2005.

Imports now46%

Imp

ort

s as

a p

erce

nt

of

con

sum

pti

on

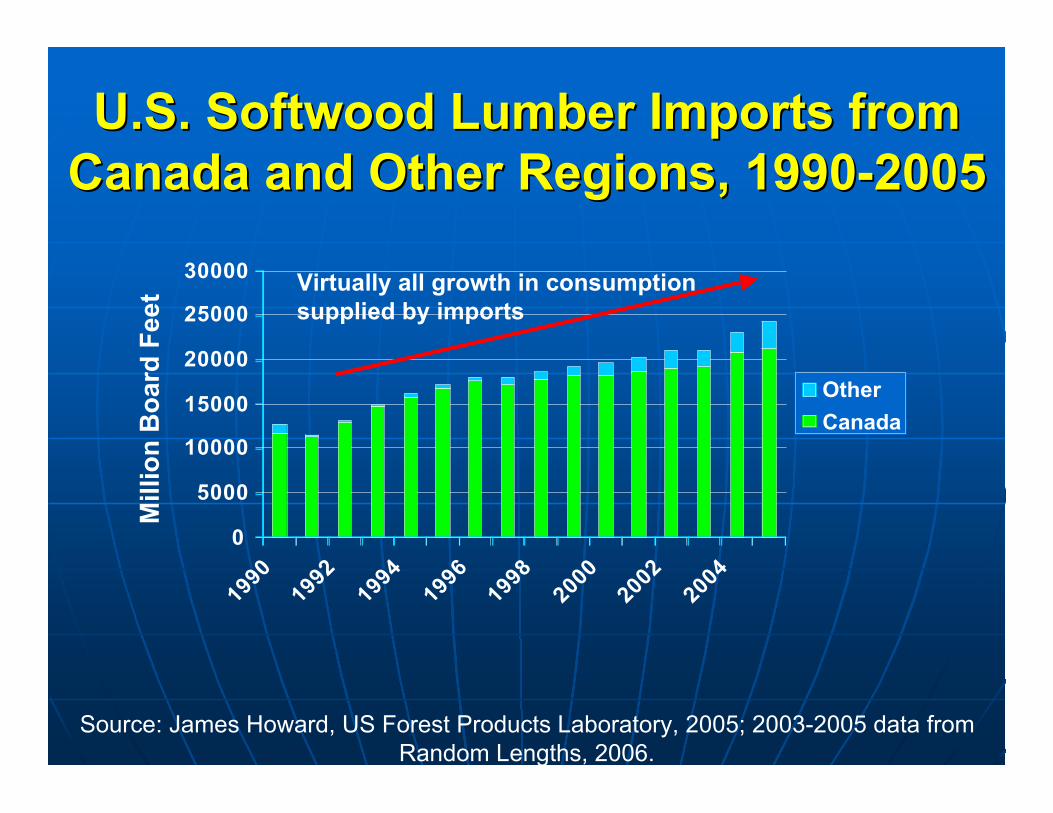

U.S. Softwood Lumber Imports fromU.S. Softwood Lumber Imports fromCanada and Other Regions, 1990-2005Canada and Other Regions, 1990-2005

0

5000

10000

15000

20000

25000

30000

19901992

19941996

19982000

20022004

Other

Canada

Mill

ion

Bo

ard

Fee

t

Source: James Howard, US Forest Products Laboratory, 2005; 2003-2005 data fromRandom Lengths, 2006.

Virtually all growth in consumptionsupplied by imports

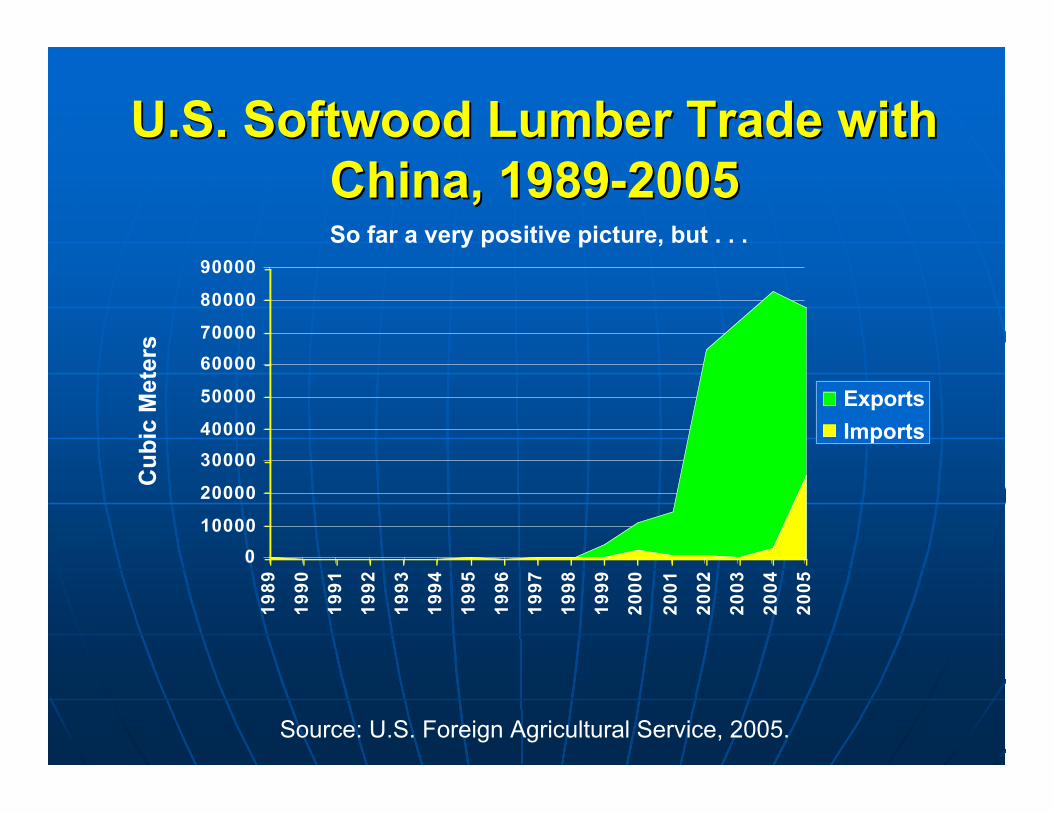

U.S. Softwood Lumber Trade withU.S. Softwood Lumber Trade withChina, 1989-2005China, 1989-2005

0

10000

20000

30000

40000

50000

60000

70000

80000

900001

98

9

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Exports

Imports

Cu

bic

Met

ers

Source: U.S. Foreign Agricultural Service, 2005.

So far a very positive picture, but . . .

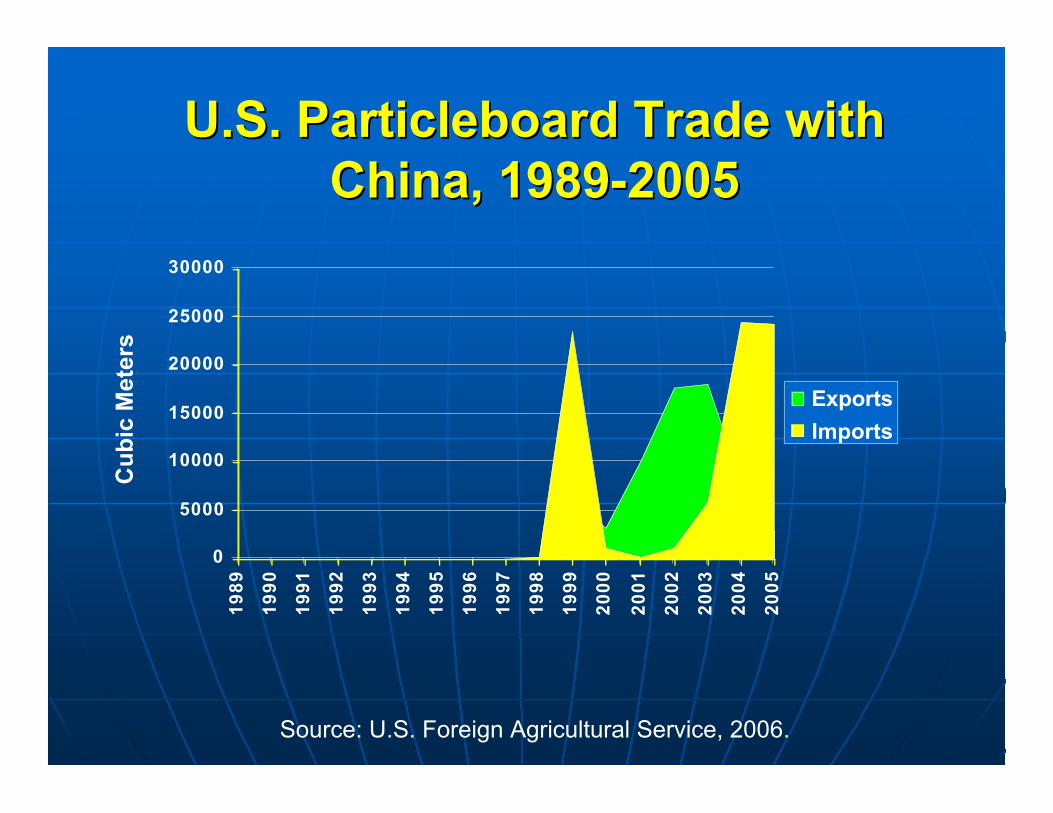

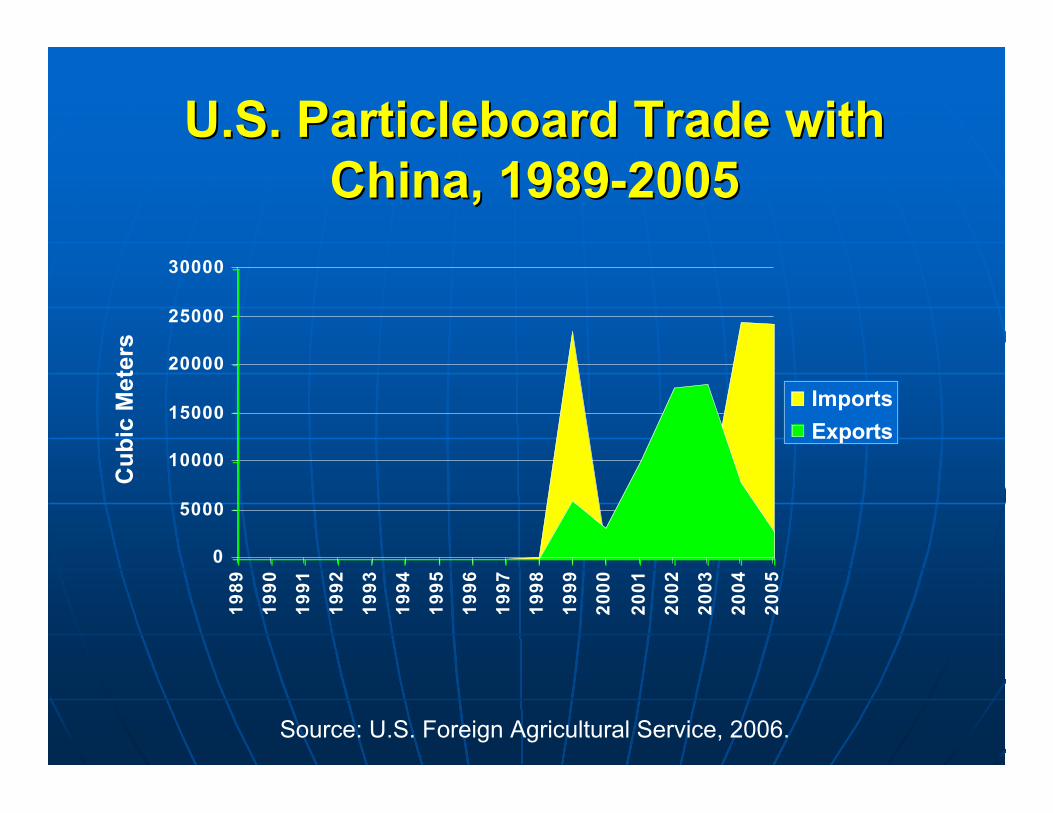

U.S. Particleboard Trade withU.S. Particleboard Trade withChina, 1989-2005China, 1989-2005

0

5000

10000

15000

20000

25000

30000

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Exports

Imports

Cu

bic

Met

ers

Source: U.S. Foreign Agricultural Service, 2006.

U.S. Particleboard Trade withU.S. Particleboard Trade withChina, 1989-2005China, 1989-2005

0

5000

10000

15000

20000

25000

30000

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Imports

Exports

Cu

bic

Met

ers

Source: U.S. Foreign Agricultural Service, 2006.

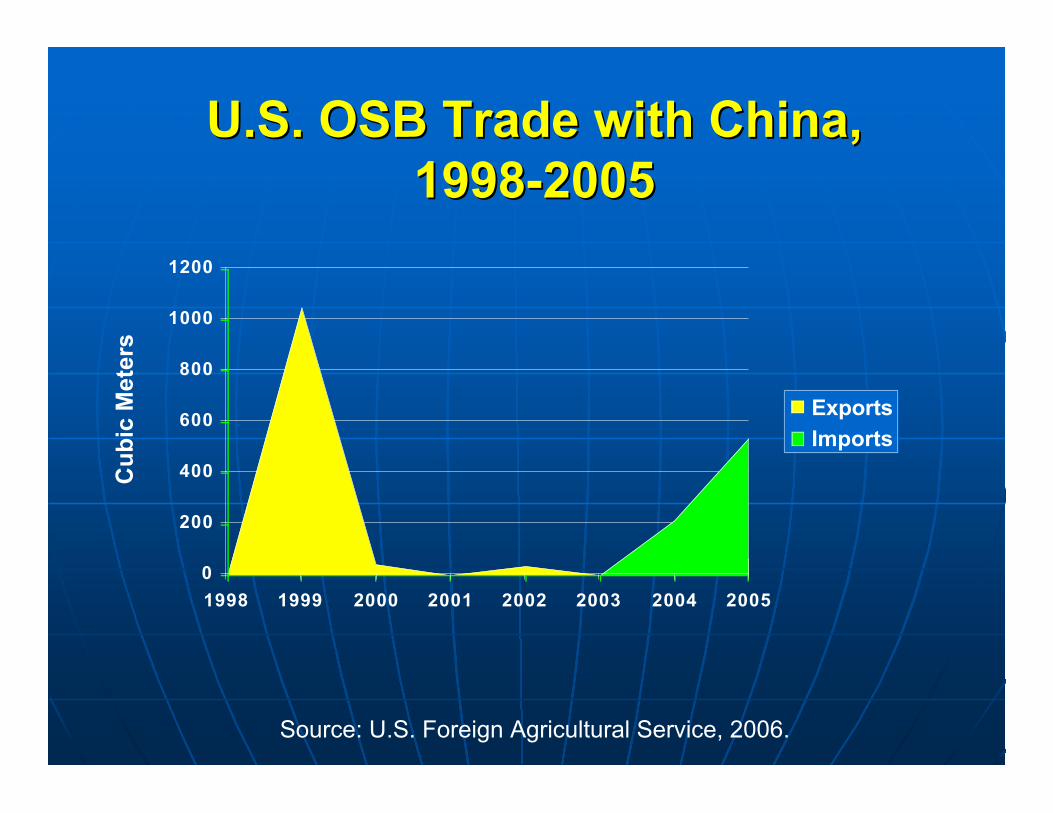

U.S. OSB Trade with China,U.S. OSB Trade with China,1998-20051998-2005

0

200

400

600

800

1000

1200

1998 1999 2000 2001 2002 2003 2004 2005

Exports

Imports

Cu

bic

Met

ers

Source: U.S. Foreign Agricultural Service, 2006.

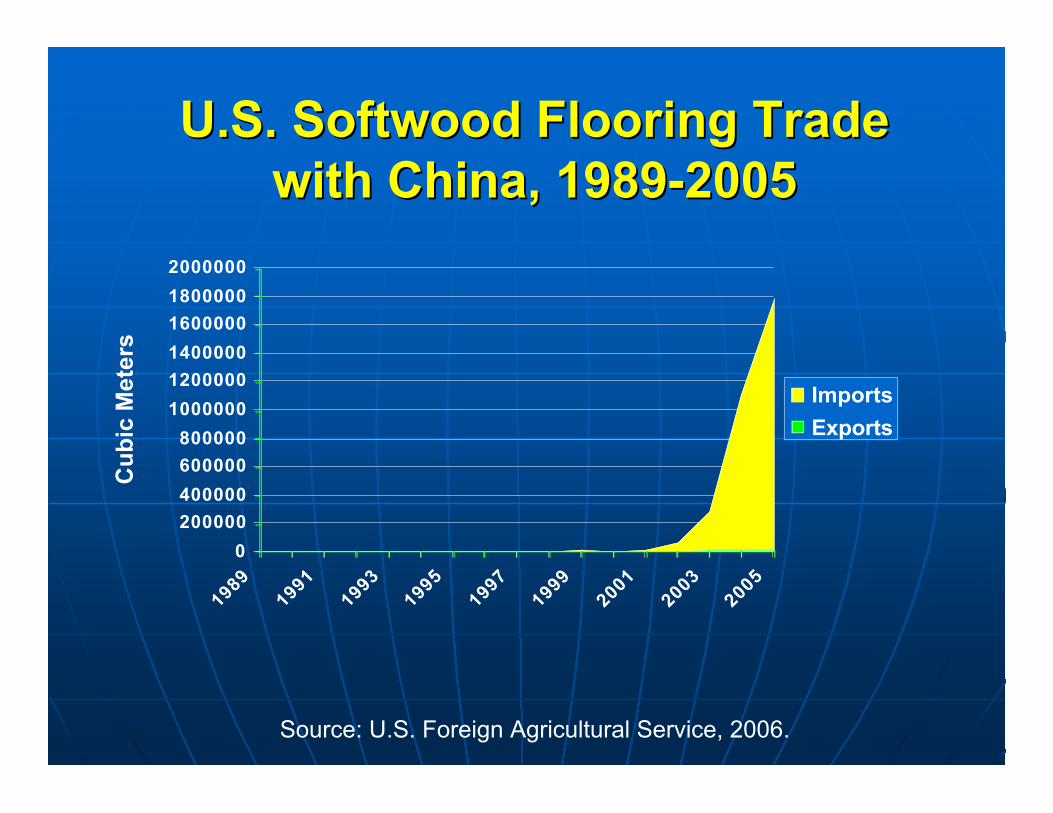

U.S. Softwood Flooring TradeU.S. Softwood Flooring Tradewith China, 1989-2005with China, 1989-2005

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

19891991

19931995

19971999

20012003

2005

Imports

Exports

Cu

bic

Met

ers

Source: U.S. Foreign Agricultural Service, 2006.

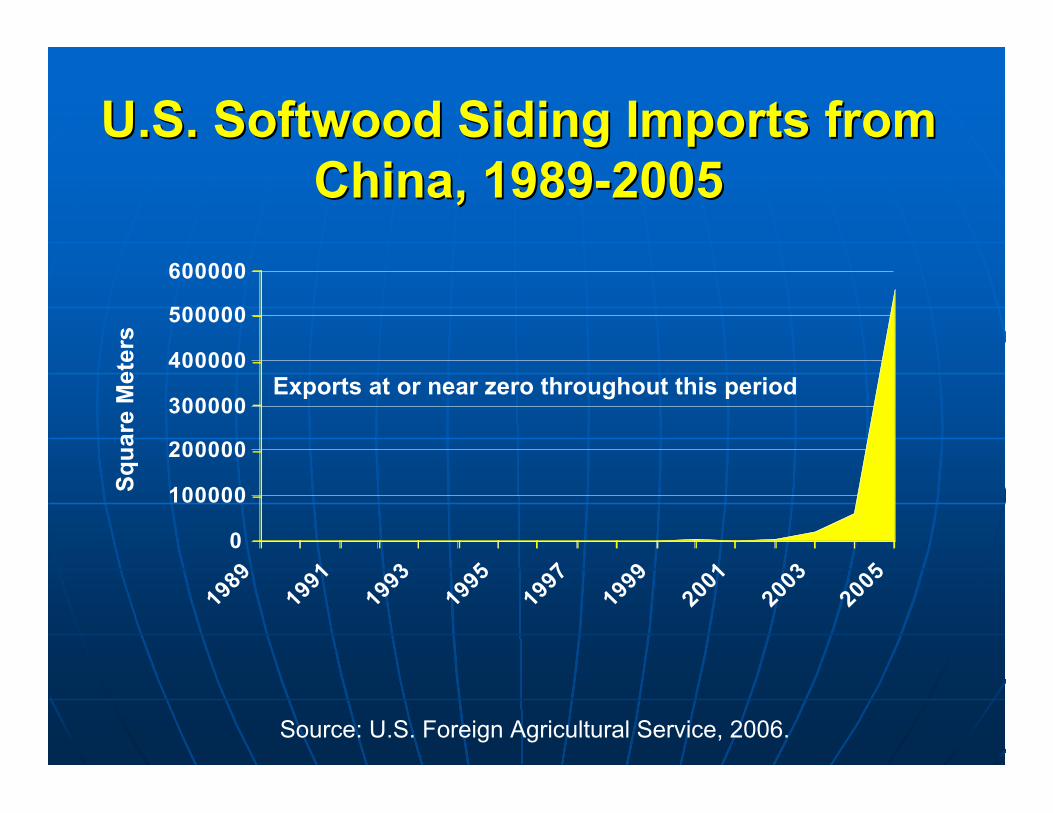

U.S. Softwood SidingU.S. Softwood Siding Imports fromImports fromChina, 1989-2005China, 1989-2005

0

100000

200000

300000

400000

500000

600000

19891991

19931995

19971999

20012003

2005

Sq

uar

e M

eter

s

Source: U.S. Foreign Agricultural Service, 2006.

Exports at or near zero throughout this period

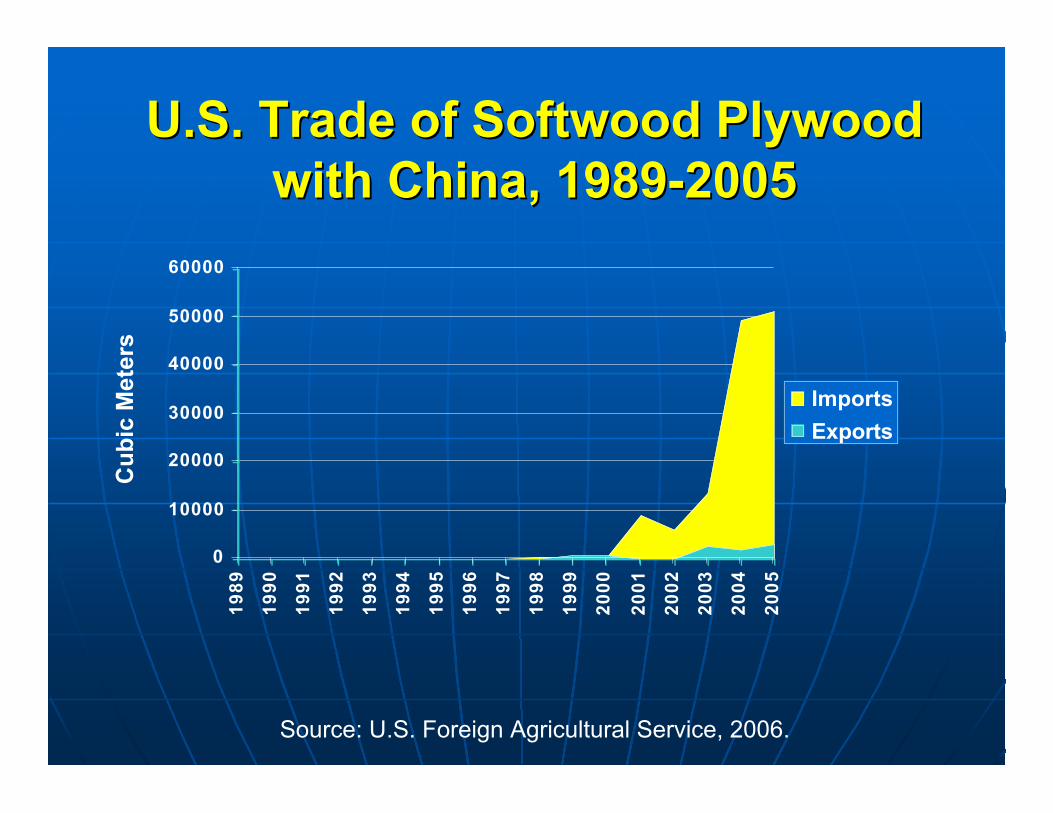

U.S. Trade of Softwood PlywoodU.S. Trade of Softwood Plywoodwith China, 1989-2005with China, 1989-2005

0

10000

20000

30000

40000

50000

60000

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Imports

Exports

Cu

bic

Met

ers

Source: U.S. Foreign Agricultural Service, 2006.

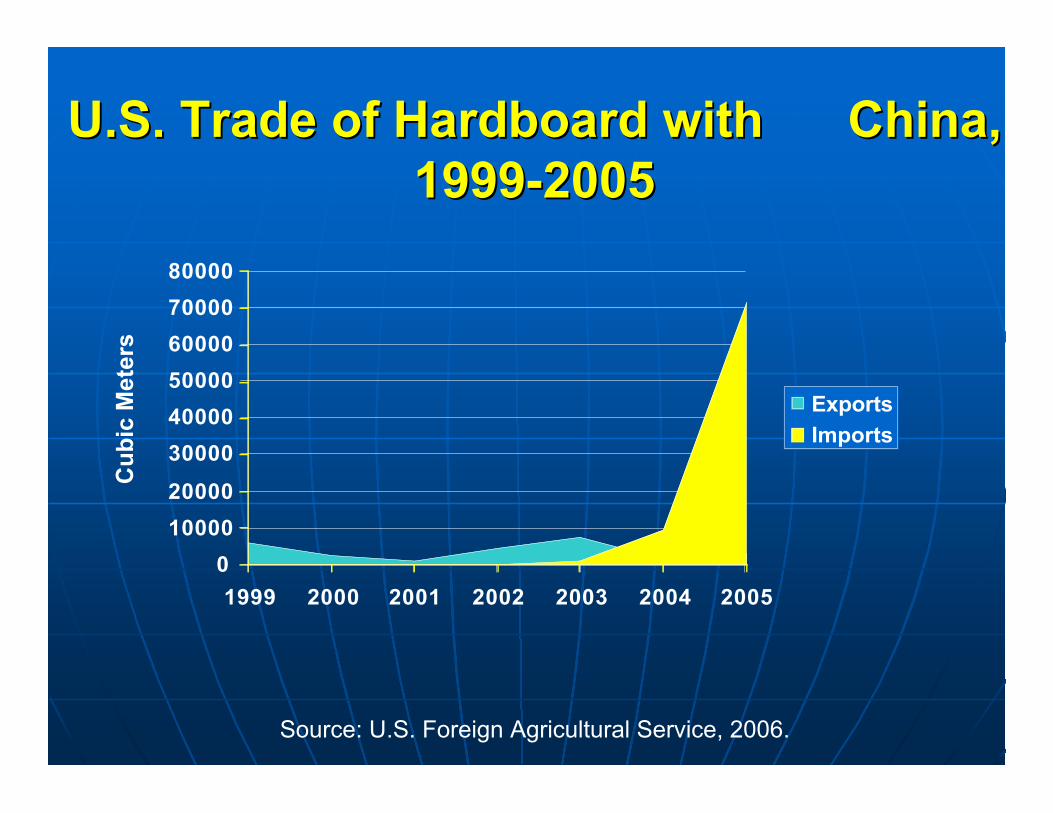

U.S. Trade of Hardboard with China,U.S. Trade of Hardboard with China,1999-20051999-2005

0

10000

20000

30000

40000

50000

60000

70000

80000

1999 2000 2001 2002 2003 2004 2005

Exports

Imports

Cu

bic

Met

ers

Source: U.S. Foreign Agricultural Service, 2006.

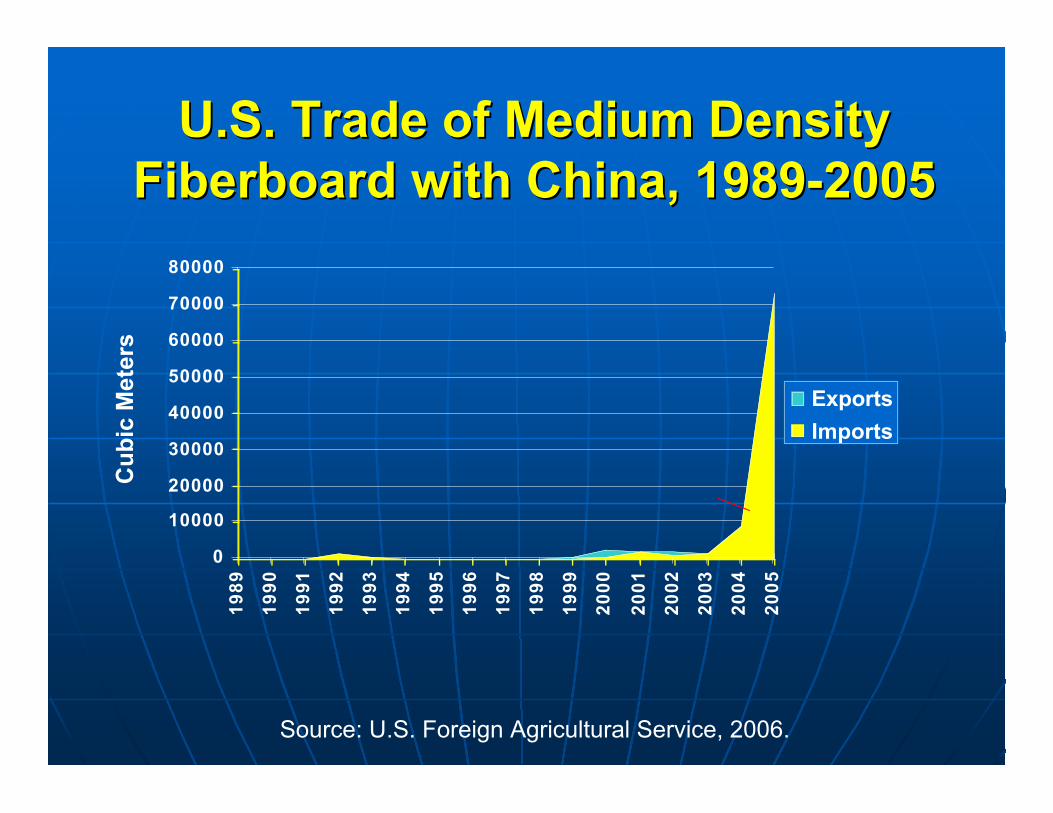

U.S. Trade of Medium DensityU.S. Trade of Medium DensityFiberboard with China, 1989-2005Fiberboard with China, 1989-2005

0

10000

20000

30000

40000

50000

60000

70000

80000

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Exports

Imports

Cu

bic

Met

ers

Source: U.S. Foreign Agricultural Service, 2006.

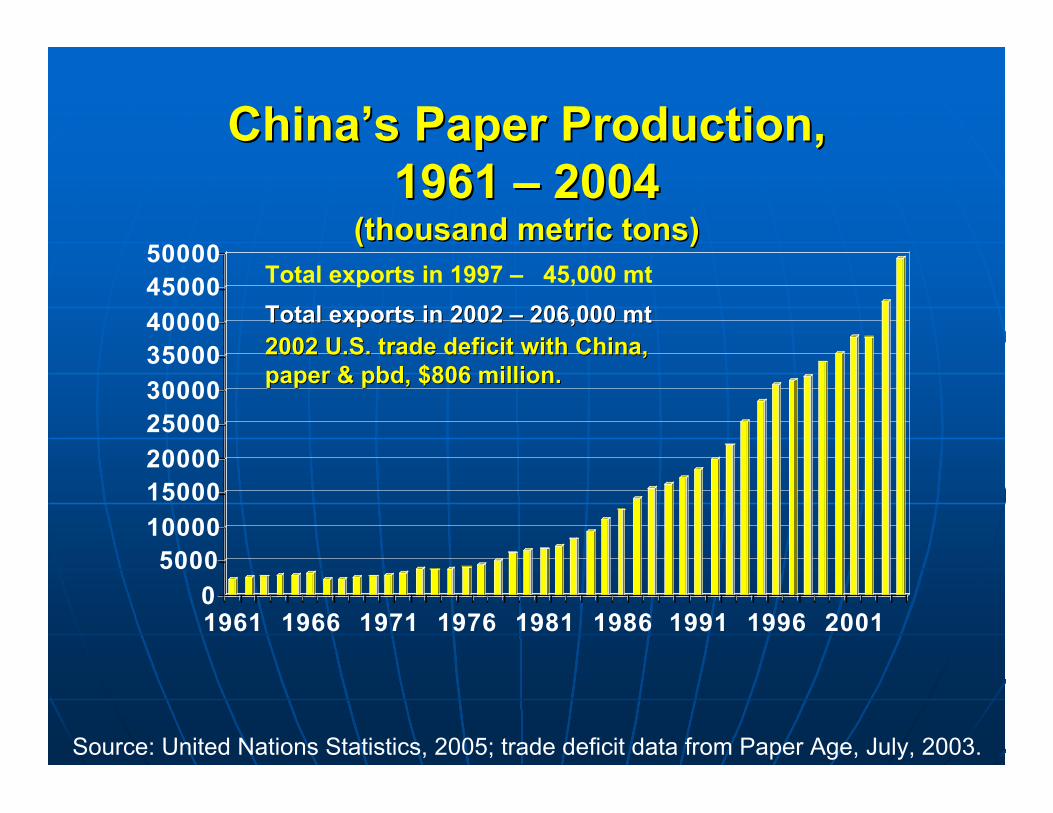

ChinaChina’’s Paper Production,s Paper Production,1961 1961 –– 2004 2004

(thousand metric tons)(thousand metric tons)

0

500010000

1500020000

2500030000

3500040000

4500050000

1961 1966 1971 1976 1981 1986 1991 1996 2001

Source: United Nations Statistics, 2005; trade deficit data from Paper Age, July, 2003.

Total exports in 1997 – 45,000 mt

Total exports in 2002 Total exports in 2002 –– 206,000 206,000 mtmt20022002 U.S. trade deficit with China,U.S. trade deficit with China,paper & paper & pbdpbd, $806 million., $806 million.

Implications of GlobalImplications of GlobalTrends for the ForestTrends for the Forest

Sector of theSector of the United States United States

Implications of Global TrendsImplications of Global Trendsfor the Forest Sector of the U.S.for the Forest Sector of the U.S.nn Expanding global economies areExpanding global economies are

stimulating consumption worldwide,stimulating consumption worldwide,creating market opportunities.creating market opportunities.

nn Global demand for housing is growingGlobal demand for housing is growingmore rapidly than population.more rapidly than population.

nn U.S. population growth will ensureU.S. population growth will ensuregrowing domestic consumption.growing domestic consumption.

nn Expanding middle classes in developingExpanding middle classes in developingeconomies around the world will lead toeconomies around the world will lead toincreasing demand for quality goods.increasing demand for quality goods.

Implications of Global TrendsImplications of Global Trendsfor the Forest Sectorfor the Forest Sector

nn Supplies of low-cost fiber are increasing asSupplies of low-cost fiber are increasing asfast-growing forest plantations expandfast-growing forest plantations expandglobally.globally.

nn In the near term, raw materials will flow toIn the near term, raw materials will flow toinstalled capacity. In the longer term,installed capacity. In the longer term,capital will flow to regions with abundant,capital will flow to regions with abundant,low cost fiber.low cost fiber.

nn The reemergence of Russia as a woodThe reemergence of Russia as a woodproducts producer will add to global timberproducts producer will add to global timberand wood fiber supplies.and wood fiber supplies.

Implications of Global TrendsImplications of Global Trendsfor the Forest Sectorfor the Forest Sector

nn China and other developing nations areChina and other developing nations areaggressively seeking to compete in theaggressively seeking to compete in thewood products arena, severely challengingwood products arena, severely challengingtraditional producing regions.traditional producing regions.

nn Little of the wood flowing through AsianLittle of the wood flowing through Asianwood products industries is certified.wood products industries is certified.Considerable quantities are from illegalConsiderable quantities are from illegalsources.sources.

Implications of Global TrendsImplications of Global Trendsfor the Forest Sectorfor the Forest Sector

nn Rising energy consumption andRising energy consumption andapproaching limits to petroleum productionapproaching limits to petroleum productiontranslate to rising interest in alternatives,translate to rising interest in alternatives,including bio-energy and including bio-energy and biochemicalsbiochemicals and andfeedstocksfeedstocks..

nn Bio-energy development will mean newBio-energy development will mean newmarkets for wood, but also rising prices formarkets for wood, but also rising prices forwood raw materials.wood raw materials.

From a number of perspectives,From a number of perspectives,the changing situation presentsthe changing situation presents

a clear and substantiala clear and substantialopportunity.opportunity.

The Bio-Economy,The Bio-Economy,Bio-EnergyBio-Energy

and the U.S. Forestand the U.S. ForestSector Sector –– Threat or Threat or

Opportunity?Opportunity?

Liquid Fuels Represent anLiquid Fuels Represent anEnormous Opportunity forEnormous Opportunity for

the Forest Sectorthe Forest Sector

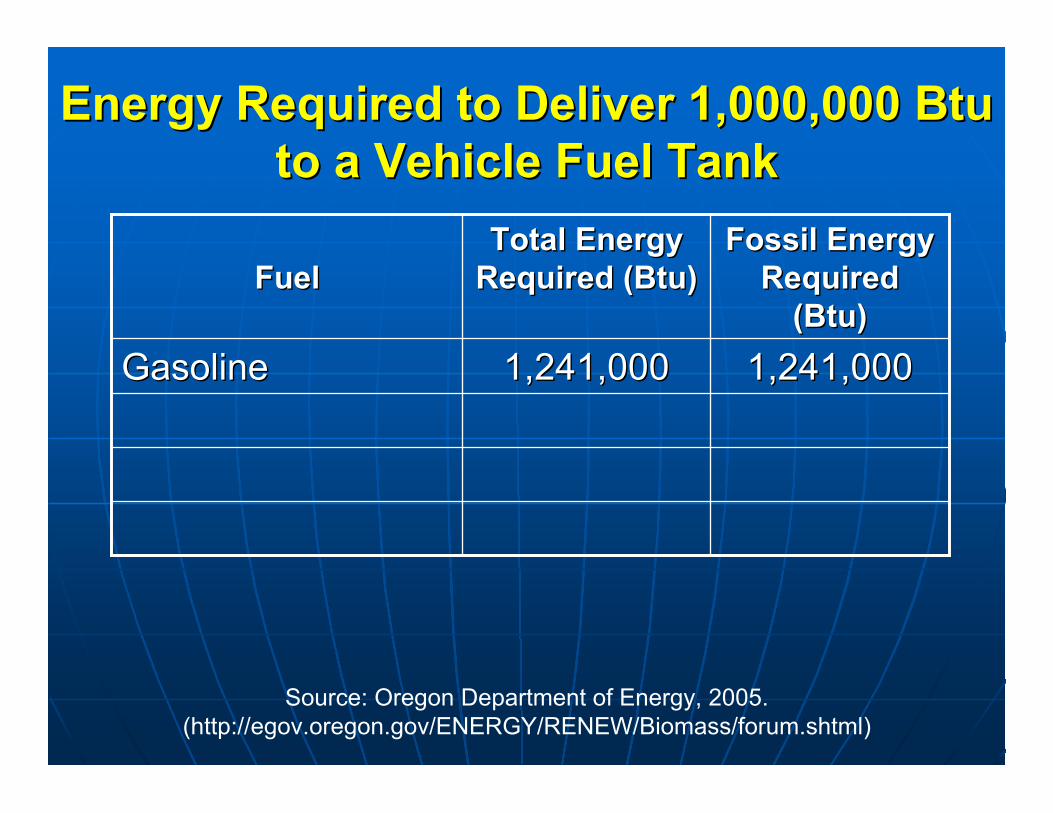

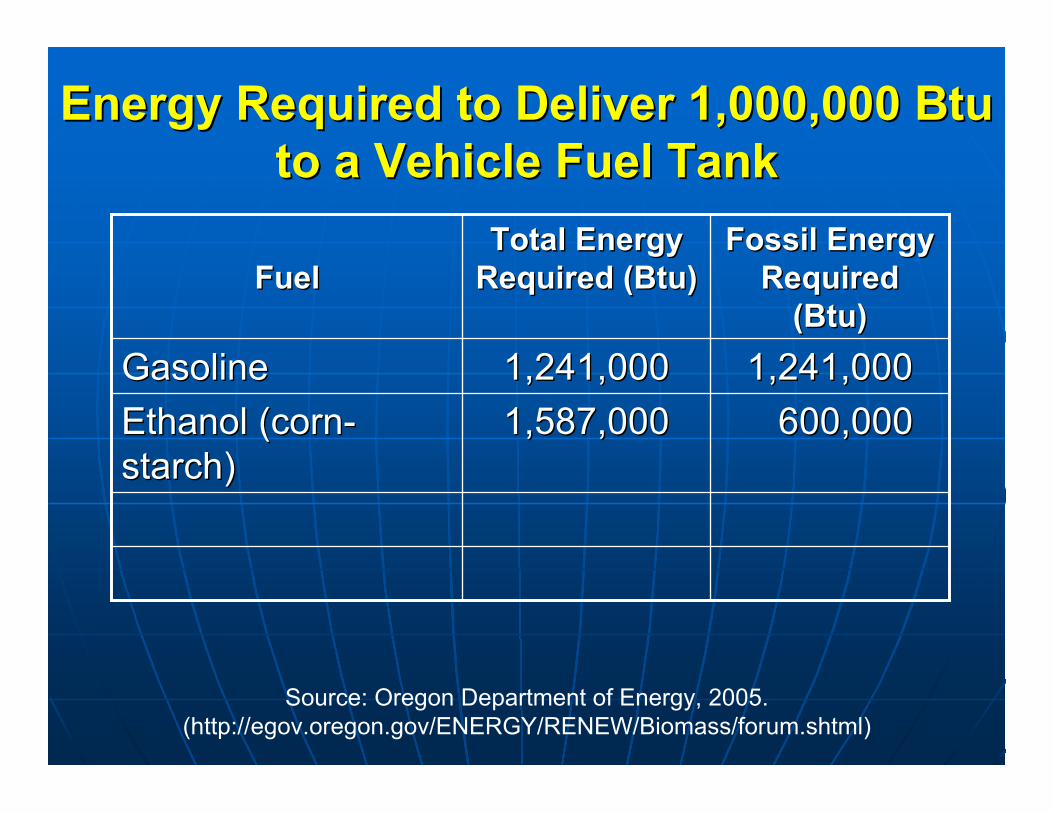

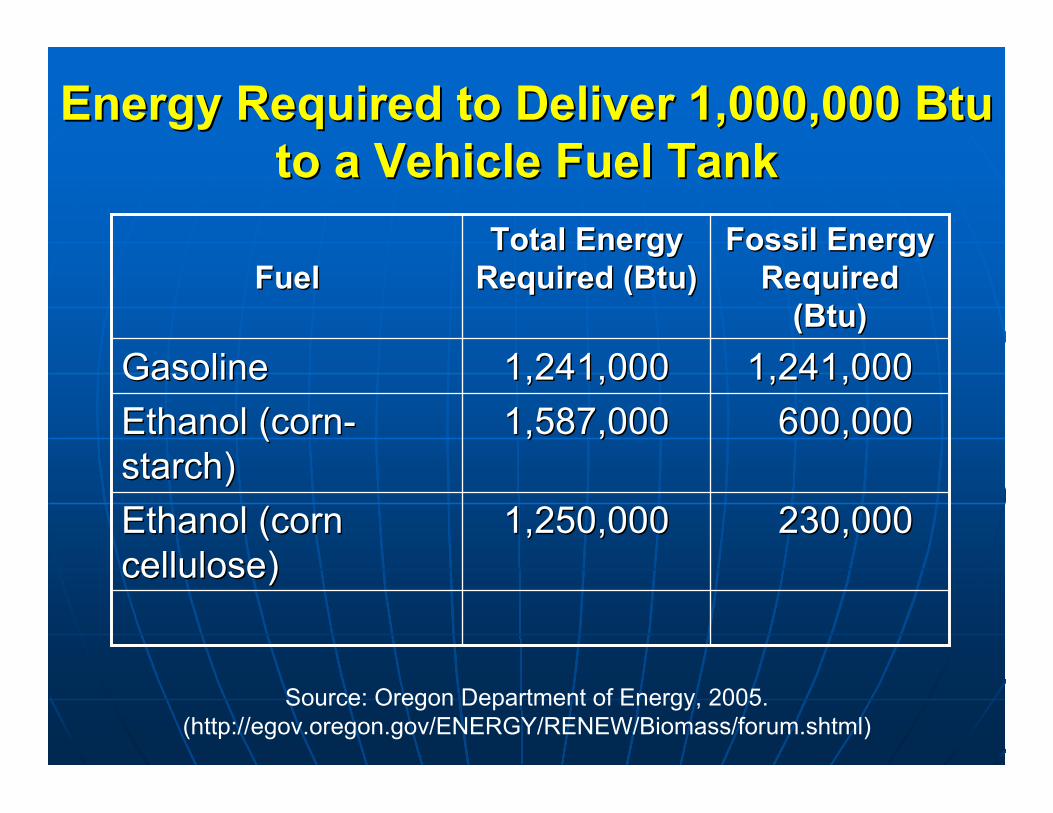

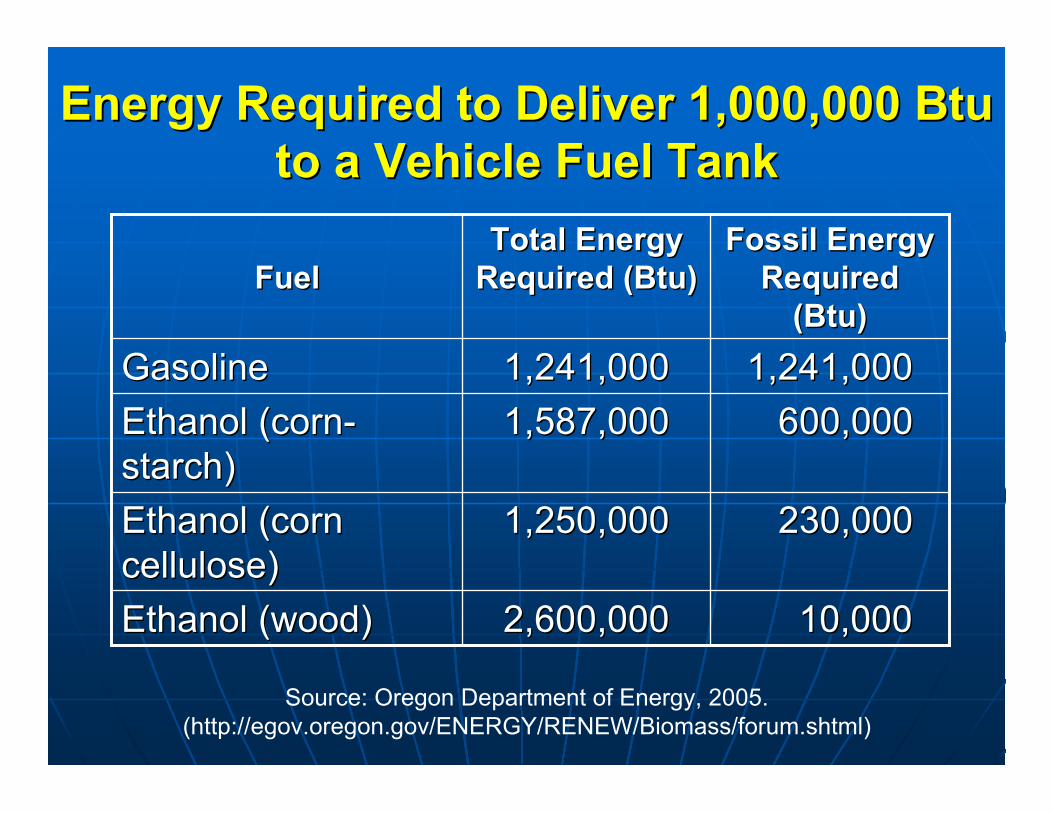

Energy Required to Deliver 1,000,000 BtuEnergy Required to Deliver 1,000,000 Btuto a Vehicle Fuel Tankto a Vehicle Fuel Tank

1,241,0001,241,0001,241,0001,241,000GasolineGasoline

Fossil EnergyFossil EnergyRequiredRequired

(Btu)(Btu)

Total EnergyTotal EnergyRequired (Btu)Required (Btu)FuelFuel

Source: Oregon Department of Energy, 2005.(http://egov.oregon.gov/ENERGY/RENEW/Biomass/forum.shtml)

Energy Required to Deliver 1,000,000 BtuEnergy Required to Deliver 1,000,000 Btuto a Vehicle Fuel Tankto a Vehicle Fuel Tank

600,000 600,0001,587,0001,587,000Ethanol (corn-Ethanol (corn-starch)starch)

1,241,0001,241,0001,241,0001,241,000GasolineGasoline

Fossil EnergyFossil EnergyRequiredRequired

(Btu)(Btu)

Total EnergyTotal EnergyRequired (Btu)Required (Btu)FuelFuel

Source: Oregon Department of Energy, 2005.(http://egov.oregon.gov/ENERGY/RENEW/Biomass/forum.shtml)

Energy Required to Deliver 1,000,000 BtuEnergy Required to Deliver 1,000,000 Btuto a Vehicle Fuel Tankto a Vehicle Fuel Tank

230,000 230,0001,250,0001,250,000Ethanol (cornEthanol (corncellulose)cellulose)

600,000 600,0001,587,0001,587,000Ethanol (corn-Ethanol (corn-starch)starch)

1,241,0001,241,0001,241,0001,241,000GasolineGasoline

Fossil EnergyFossil EnergyRequiredRequired

(Btu)(Btu)

Total EnergyTotal EnergyRequired (Btu)Required (Btu)FuelFuel

Source: Oregon Department of Energy, 2005.(http://egov.oregon.gov/ENERGY/RENEW/Biomass/forum.shtml)

Energy Required to Deliver 1,000,000 BtuEnergy Required to Deliver 1,000,000 Btuto a Vehicle Fuel Tankto a Vehicle Fuel Tank

10,000 10,0002,600,0002,600,000Ethanol (wood)Ethanol (wood)

230,000 230,0001,250,0001,250,000Ethanol (cornEthanol (corncellulose)cellulose)

600,000 600,0001,587,0001,587,000Ethanol (corn-Ethanol (corn-starch)starch)

1,241,0001,241,0001,241,0001,241,000GasolineGasoline

Fossil EnergyFossil EnergyRequiredRequired

(Btu)(Btu)

Total EnergyTotal EnergyRequired (Btu)Required (Btu)FuelFuel

Source: Oregon Department of Energy, 2005.(http://egov.oregon.gov/ENERGY/RENEW/Biomass/forum.shtml)

The potential forThe potential forproduction of production of biochemicalsbiochemicalsand and biofeedstocksbiofeedstocks presents presents

a further opportunity.a further opportunity.

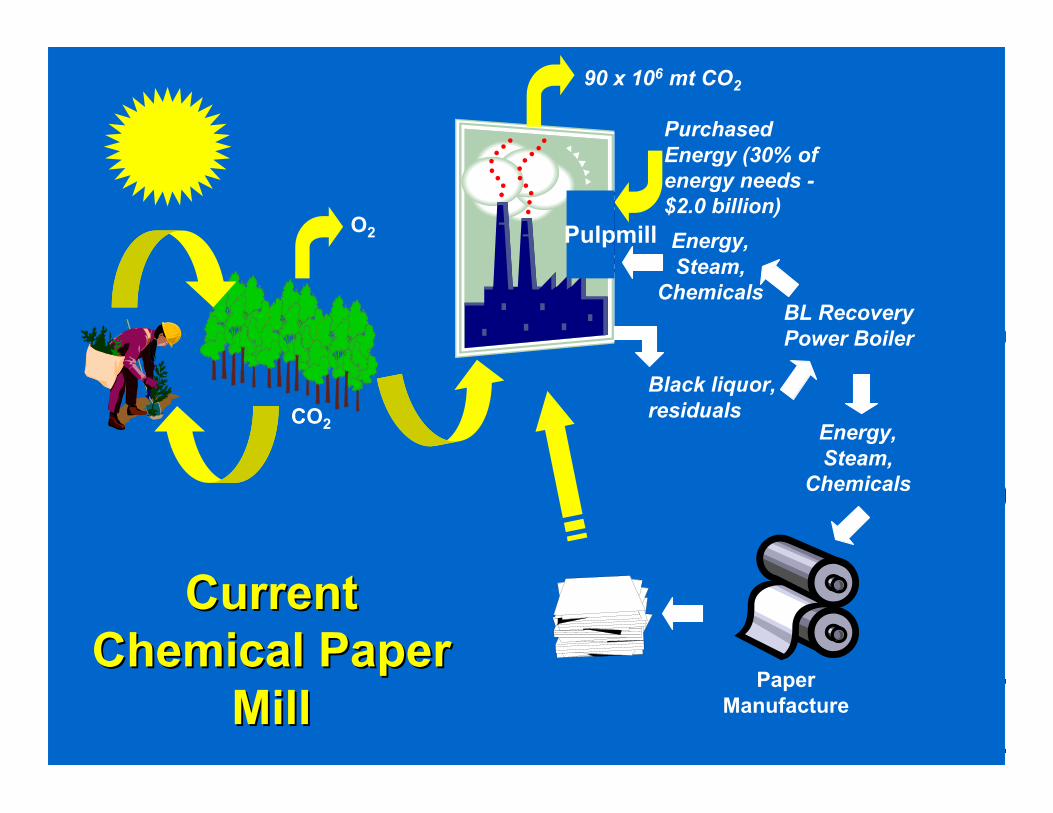

O2

CO2

BL RecoveryPower Boiler

PaperManufacture

Black liquor,residuals

90 x 106 mt CO2

PurchasedEnergy (30% ofenergy needs -$2.0 billion)

Pulpmill Energy,Steam,

Chemicals

Energy,Steam,

Chemicals

CurrentCurrentChemical PaperChemical Paper

MillMill

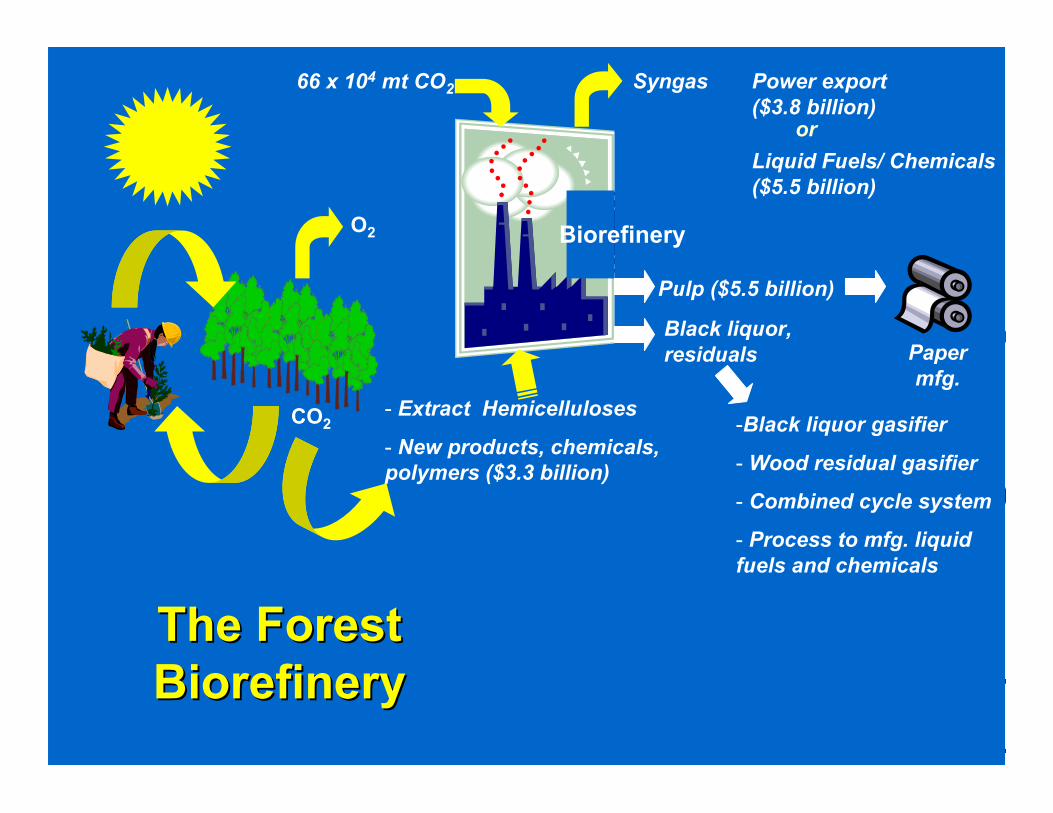

O2

CO2

Black liquor,residuals

66 x 104 mt CO2 Power export($3.8 billion)

Biorefinery

Pulp ($5.5 billion)

The ForestThe ForestBiorefineryBiorefinery

- Extract Hemicelluloses

- New products, chemicals,polymers ($3.3 billion)

-Black liquor gasifier

- Wood residual gasifier

- Combined cycle system

- Process to mfg. liquidfuels and chemicals

or

Liquid Fuels/ Chemicals($5.5 billion)

Syngas

Papermfg.

PositioningPositioning

for thefor theFutureFuture

Positioning for the FuturePositioning for the Future

nn Develop a revitalized program of wood productsDevelop a revitalized program of wood productsresearch and developmentresearch and developmentßß Industry, academia, governmentIndustry, academia, governmentßß Fast, nimble, appliedFast, nimble, appliedßß ProprietaryProprietary

nn Position research establishment for morePosition research establishment for moreeffective monitoring of R&D globally.effective monitoring of R&D globally.

nn Seek to understand foreign competitors on anSeek to understand foreign competitors on anongoing basisongoing basisßß BenchmarkBenchmarkßß MonitorMonitorßß Profile consumer trends, market trendsProfile consumer trends, market trends

Positioning for the Future (Cont.)Positioning for the Future (Cont.)

nn Strategically plan on a region-wide basis.Strategically plan on a region-wide basis.

nn Carefully consider the role of northeasternCarefully consider the role of northeasternforests in bio-fuels initiatives forests in bio-fuels initiatives –– take steps to take steps toproactively anticipate the future.proactively anticipate the future.

nn Ensure that opportunities for production of bio-Ensure that opportunities for production of bio-chemicals/bio-chemicals/bio-feedstocksfeedstocks are part of bio-fuels are part of bio-fuelsdevelopment.development.

nn Seek win-win opportunities between agriculturalSeek win-win opportunities between agriculturaland wood products sectors.and wood products sectors.

The bottom line is that theThe bottom line is that theexistence and vitality of aexistence and vitality of a

future wood products industryfuture wood products industryin the northeastern U.S. will bein the northeastern U.S. will be

largely determined by thelargely determined by theregionregion’’s residents and leaders.s residents and leaders.

For More Information on thisFor More Information on thisTopic:Topic:

nn http://www.cnr.umn.edu/bp/publications/http://www.cnr.umn.edu/bp/publications/index.phpindex.php

nn www.dovetailinc.orgwww.dovetailinc.org

![INDEPENDENT MARKET REPORT FOR SOFTWOOD PLANTATION … · INDEPENDENT MARKET REPORT FOR SOFTWOOD PLANTATION PRODUCTS ... ...]'/!,4./*!!!](https://img.pdfslide.net/doc/110x75/5f2e5de272f6a91abe7a3a7d/independent-market-report-for-softwood-plantation-independent-market-report-for.jpg)