Embed Size (px)

Citation preview

WORKING DRAFT – DECEMBER 2020 | 1

Global Vaccine Market Report

Overview of MI4AWHO launched MI4A (Market Information for Access to Vaccines) in January 2018 in response to calls by the World Health Assembly, Member States and WHO’s Strategic Advisory Group (SAGE) on Immunization to:

• Improve access to market information for health commodities;

• Enhance the understanding of global vaccine demand, supply and pricing dynamics and identify affordability and shortage risks;

• Convene all relevant global health partners to contribute to the development of policies, strategies and guidance to address identified risks;

• Strengthen national and regional capacity for improved access to vaccines supply.

MI4A focuses on addressing the needs of self-procuring countries that benefit from limited international support.

This initiative helps inform dialogue on access in context of WHO’s work on Fair Pricing of Medicines.

MI4A information and reports are available at: who.int/immunization/MI4A

You can contact the MI4A project team at [email protected].

Executive SummarySARS-CoV-2 has impacted health and immunization systems around the world since early 2020 and is likely to alter vaccine markets for several years. This report, based on country-reported purchase data from 2019, cannot yet show the impact of the SARS-CoV-2 pandemic on vaccine markets. The 2020 Global Vaccine Market Report summarizes the state of the global vaccine market in 2019 to serve as a baseline against which impacts, captured in future editions of the report, can be compared.

This report covers: 1. Collection of Global Vaccine Market Information, 2. Global Market Volumes, 3. Vaccine Supply Dynamics, 4. Vaccine Prices, 5. Vaccine Regulation, 6. Vaccine Stockouts & Shortages, 7. Global Market Value.Key observations this year include:

• 2020 country reporting of data was down 9% this year most likely due to the SARS-CoV-2 pandemic, with 166 countries (85%) reporting any data and 140 countries (72%) reporting complete data this year compared to 183 and 159 last year. Most of this decrease comes from high-income countries, primarily in the European and American regions. Over all years, fifteen countries still do not report data.

• Global market volume estimates for 2019 totalled 5.5 billion doses, excluding travel and military markets. Bivalent oral polio vaccine, diphtheria- and tetanus-containing and measles-containing vaccines were the largest vaccines by volume. Self-procuring MICs drive over half of global volume or one fifth of global volume, excluding India and China.

• Constraints in access to supply persist, though newer manufacturers in Asia are expanding the supplier base for pneumococcal conjugate vaccine, rotavirus vaccine, human papillomavirus vaccine and regional vaccines – leading to a more competitive market while larger established vaccine producers continue to represent the largest share of the market.

• Fifty-six countries reported national stockouts of one or more vaccines in 2019 representing 42% of 132 reporting countries. This represents a drop from last year’s 69 countries, though still falls short of the Global Vaccine Action Plan 2020 target of 25 countries. Thirty-four countries reported national stockouts of two or more vaccines, with oral polio, Bacillus Calmette–Guérin and yellow fever vaccines topping the list. Procurement delays1 were the most common cause of national stockouts.

• There is evidence of price tiering by procurement mechanism, despite variation in prices across vaccines and income groups. Pooled procurement mechanisms lead to lower prices for 21 of 28 vaccines, compared to self-procurement. On average, pooled procurement prices were 60% lower for MICs procuring from UNICEF or PAHO RF.

• MI4A estimates global 2019 market value for vaccines to be approximately $33 billion, representing about 2% of the overall pharmaceutical market. High-income countries account for 68% of global value. Pneumococcal conjugate, diphtheria- and tetanus-containing and human papillomavirus vaccines remain top-value vaccines, and the pneumococcal conjugate and human papillomavirus vaccines markets are likely to grow substantially by 2030.

1 Procurement delays can refer to delays in the procurement process by the procuring agency or delays by countries to initiate their procurement

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 2

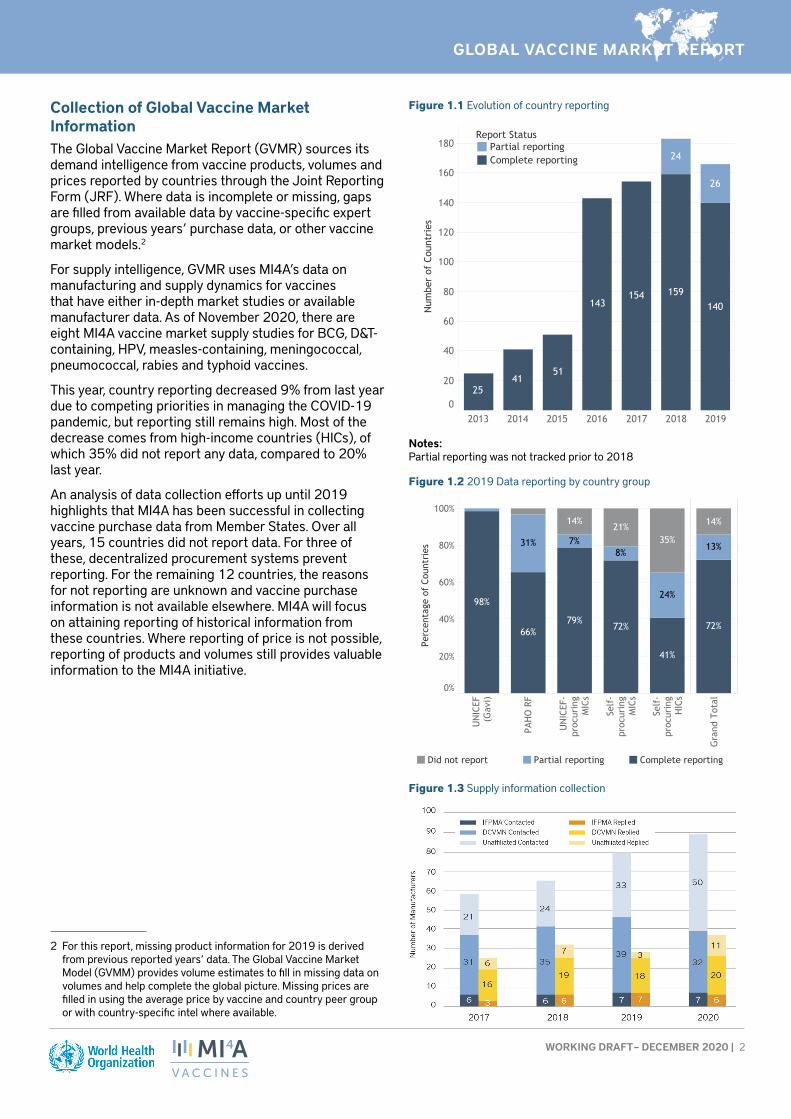

Collection of Global Vaccine Market InformationThe Global Vaccine Market Report (GVMR) sources its demand intelligence from vaccine products, volumes and prices reported by countries through the Joint Reporting Form (JRF). Where data is incomplete or missing, gaps are filled from available data by vaccine-specific expert groups, previous years’ purchase data, or other vaccine market models.2

For supply intelligence, GVMR uses MI4A’s data on manufacturing and supply dynamics for vaccines that have either in-depth market studies or available manufacturer data. As of November 2020, there are eight MI4A vaccine market supply studies for BCG, D&T-containing, HPV, measles-containing, meningococcal, pneumococcal, rabies and typhoid vaccines.

This year, country reporting decreased 9% from last year due to competing priorities in managing the COVID-19 pandemic, but reporting still remains high. Most of the decrease comes from high-income countries (HICs), of which 35% did not report any data, compared to 20% last year.

An analysis of data collection efforts up until 2019 highlights that MI4A has been successful in collecting vaccine purchase data from Member States. Over all years, 15 countries did not report data. For three of these, decentralized procurement systems prevent reporting. For the remaining 12 countries, the reasons for not reporting are unknown and vaccine purchase information is not available elsewhere. MI4A will focus on attaining reporting of historical information from these countries. Where reporting of price is not possible, reporting of products and volumes still provides valuable information to the MI4A initiative.

2 For this report, missing product information for 2019 is derived from previous reported years’ data. The Global Vaccine Market Model (GVMM) provides volume estimates to fill in missing data on volumes and help complete the global picture. Missing prices are filled in using the average price by vaccine and country peer group or with country-specific intel where available.

2013 2014 2015 2016 2017 2018 20190

20

40

60

80

100

120

140

160

180

Num

ber

of C

ount

ries

154143

5141

25

159140

24

26

-Partial reporting was not tracked prior to 2018

Report StatusPartial reportingComplete reporting

Figure 1.1 Evolution of country reporting

UN

ICEF

(Gav

i)

PAH

O R

F

UN

ICEF

-pr

ocur

ing

MIC

s

Self

-pr

ocur

ing

MIC

s

Self

-pr

ocur

ing

HIC

s

Gra

nd T

otal

0%

20%

40%

60%

80%

100%

Perc

enta

ge o

f Co

untr

ies

14%21%

35%

14%

31%

24%

13%

98%

66%79%

72%

41%

72%

7%8%

Did not report Partial reporting Complete reporting

Figure 1.2 2019 Data reporting by country group

Figure 1.3 Supply information collection

Notes:Partial reporting was not tracked prior to 2018

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 3

Global Market VolumesGlobal market estimates for 2019 totalled 5.5 billion doses with the exclusion of travel and military markets. This is a more comprehensive estimate than last year due to improved methodologies and inclusion of estimates for seasonal influenza and OPV vaccine demand. Global volume estimates, aside from these new inclusions, remained steady.

SEAR and AFR are still the largest regional purchasers of vaccines. India accounted for 80% of SEAR’s volume in 2019. AFR volumes will likely continue to grow as countries introduce more recommended vaccines.

Self-procuring middle-income countries (MICs) remained the highest-volume country group, with over half of this volume for India and China. Excluding India and China, self-procuring MICs still purchase 20% of global volumes.

Vaccines with broad use globally and use in supplementary immunization activities (SIAs) top the charts in purchased volumes. Bivalent OPV is the vaccine with the highest global demand in volume. D&T-containing and MCVs follow as the second- and third-highest vaccine groups.

Looking ahead, vaccine-specific market studies3 forecasted growth for almost all vaccines. PCV is anticipated to show the highest growth due to expected universal country adoption to meet WHO recommendations and to the three-dose series. HPV growth is also expected to be high due to broad country adoption driven by elimination goals and anticipated resolution of supply constraints that have limited uptake to date. Use of measles monovalent, however, is expected to decline as rubella-containing vaccines MR and MMR replace it in routine immunization schedules per WHO recommendations.

3 These market studies were completed before the impact of the SARS-CoV-2 pandemic was fully ascertained. Demand projections are based on the assumption that any delay or disruption will be absorbed and resolved in the short term. Uncertainty on the progression of the pandemic raises the risk that disruptions will extend beyond 2021, which would require an updated analysis of the forecasted growth of these markets.

Figure 2.1 Global volumes by region, country groups and vaccine

Self-procuring MICs

UNICEF (Gavi)

Self-procuring HICs

PAHO RF

UNICEF-procuring MICs

2.7B

1.8B

0.6B

0.2B

0.1B

SEARO

AFRO

AMRO

EMRO

WPRO

EURO

1.6B

1.2B

0.9B

0.7B

0.6B

0.4B

0B 1B 2B 3B

Volume (doses)

bOPV

D&T-containing

MCVs

Seasonal Influenza

BCG

DTwP-HepB-Hib

PCV

Rota

HepB

Meningococcal

IPV

YF

JE

Varicella

HPV

1.5B

0.7B

0.7B

0.5B

0.3B

0.3B

0.3B

0.2B

0.2B

0.2B

0.1B

0.1B

0.1B

0.0B

0.0B

-Only the top 15 vaccines by market volume are shown in the vaccinegroup section-Analysis excludes travel and military markets

Country (group)ChinaIndiaRest of world

Notes:Only the top 15 vaccines by market volume are shown in the vaccine group section

Analysis excludes travel and military markets

Figure 2.2 Potential vaccine market volume growth 2020-2030

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 4

SII28%

Sanofi9%

Other37%

Haffkine7%

GSK11%

BBIL9%

Sanofi15%

Pfizer17%

Other9%

Merck17%

GSK40%

SII 3%

Vaccine Supply DynamicsVaccine manufacturing remains concentrated, with four large manufacturers (GSK, Pfizer, Merck, and Sanofi) controlling 90% of global vaccine value and five producing 60% of global volume (SII, GSK, Sanofi, BBIL and Haffkine4). Increasingly, mid-size manufacturers (mostly in Asia) are expanding their portfolios to compete in regional and new vaccine markets, such as HPV and PCV, offering additional and often more affordable choices (see Figure 3.2).

While concentrated in aggregate, few specific vaccine markets are true monopolies with only one supplier. Nineteen vaccines have three or fewer suppliers. Thirty-six have two or fewer prequalified (PQ'd) suppliers. Half of the vaccines with few or no PQ'd suppliers are aP-containing vaccines or vaccines only used in one or two countries.

The true availability of quality, affordable vaccine options may be more limited when considering whether the manufacturers export vaccines, registration of products, and product differentiation within each vaccine market. Additionally, countries, particularly in AMR and EMR regions, show preference for procurement from domestic or regional manufacturers, potentially limiting available options due to regulatory, legislative and political constraints (see Figure 3.3). Understanding the true level of access to quality, affordable vaccines requires in-depth analysis of specific vaccine markets that considers all of these factors. For more information on findings from the in-depth vaccine studies conducted thus far, please see the callout box on the next page.

4 Haffkine's large volumes are due to OPV supply to India.

Figure 3.1 Manufacturer share by global value (left) and volume (right)

0% 50% 100%

Proportion of total volume

Original EPI vaccines BCGbOPVDTDTP-containing (aP)DTP-containing (wP)HepAHepBHibIPVMeaslesMMRMMRVMRTdTT

Regional and targetedvaccines

JEOCVYF

New vaccines HPVMenAMeningococcal (conj.)Meningococcal (Ps)PCVPPSVRotaSeasonal InfluenzaShinglesVaricella

Manufacturer GroupTop 5 Mid-size Small or local

Figure 3.2 Procurement by manufacturer type and vaccine

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 5

Tota

l Num

ber

ofCo

mpa

nies

PQ'd

Pro

duct

Vacc

ine

1

0

DTaP-HepBDTaP-HepB-HibDTaP-HepB-IPVDTwP-HepB-Hib-IPVMenBCMenC PsTyphoid (Other)

1 MenA2

0

DTaP-Hib-IPVMenA PsMenAC-HibMenACW PsMenBMMRVTdap-IPV

1 DTaP-HepB-Hib-IPV3 0 DTaP-Hib

2 HPV3 MenACWY

40

MenACMenCPPSV

1DTwP-HibEbola

5 0 TBE2 Tdap3 PCV4 YF

6 1 TCV3 OCV4 Rota

70

DTaP-IPVPandemic Flu H5N1

2 Measles8 0 MenAC Ps9 0 DTaP

1 DTwP-HepB2 MR3 MMR5 IPV

10 0 MenACWY Ps3 JE5 Pandemic Flu H1N1

11 2 HepA7 DTwP-HepB-Hib

12 2 Varicella14 8 bOPV17

3DTDTwPHib

8 Seasonal Influenza18 5 Td20 4 Rabies21 6 TT23 4 BCG29 4 HepB

Table 3 Number of companies and PQ’d products for each vaccine

Figure 3.3 Regional procurement by manufacturer type

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Percent of Doses per Region

AFRO

AMRO

EMRO

EURO

SEARO

WPRO

European

European

European

European

European Chinese

Indian

Indian

Indian

Indian

Indian

Manufacturer regionEastern MediterraneanEuropeanCentral and South AmericanChineseIndian

North AmericanSE AsianSouth KoreanOther

Vaccine conclusions from in-depth market studies

Shortages have been identified for HPV and some meningococcal vaccines and supply risks exist for aP-containing vaccines, PCV and MMR/MMRV.*

HPV supply lags global demand due to insufficient manufacturing capacity, with additional supply and new products becoming available in the mid-2020s. To make most impactful use of available supply in the meantime, SAGE recommends that all countries should temporarily pause implementation of gender-neutral, older age group (>15 years) and multi-age cohort HPV vaccination strategies and look to other alternative strategies.

MICs and HICs primarily have reported issues in accessing meningococcal vaccines for both polysaccharide (Ps) and conjugate C- and W-containing vaccines. MenACWY Ps, specifically, has been reduced to one product for the global market. Meanwhile, rising incidence of C and W serogroups in all regions and the requirement for quadrivalent vaccination of Hajj pilgrims has led to higher demand in countries that cannot afford the much higher-prices conjugate vaccine.

PCV, aP-containing vaccines, and MCVs currently have sufficient supply relative to demand but require careful monitoring of upcoming demand from new introductions, switches, or SIAs because of volatile demand, demand segmentation between products or limited buffer between available supply and demand.

BCG supply is more than sufficient to meet global demand. However, the continued risk of production failure and/or countries’ registration of one or fewer products or reliance on few suppliers can create a risk of shortages or stockouts.

*A shortage occurs when “the supply of medicines, health products, and vaccines identified as essential by the health system is considered to be insufficient to meet public health and patient needs or when demand exceeds supply at any point in the supply chain.” (Source: WHO [2017], Technical Definitions of Shortages and Stockouts of Medicines and Vaccines)

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 6

10K 20K 30K 40K 50K 60K 70K

Purchaser's GNI

$0

$0

$1

$10

$100

Pric

e (L

ogar

ithm

ic)

MIC HIC

Vaccine Price ~ Purchase VolumeSE

ARO

AFRO

EMRO

WPR

O

EURO

AMRO

$0

$50

$100

$150

Pric

e

Vaccine Price ~ WHO Region

0 2 4 6 8 10 12 14

% of GDP

$0

$0

$1

$10

$100

Pric

e (L

ogar

ithm

ic)

Vaccine Price ~ Health Expenditure

1 100 10,000 1,000,000

Volume (Logarithmic)

$0

$0

$1

$10

$100

Pric

e (L

ogar

ithm

ic)

Vaccine Price ~ Purchase VolumeU

NIC

EF S

D

PAH

O R

F

Self

-pro

cure

men

t$0

$50

$100

$150

Pric

e

Vaccine Price ~ Procurement Mechanism

Sing

leDe

liver

y

1 ye

ar

2 ye

ars

3 ye

ars

4 ye

ars

5 ye

ars

5+ y

ears

$0

$50

$100

$150

Pric

e

Vaccine Price ~ Contract Length

Figure 4.1 Correlation of factors impacting vaccine price

Vaccine PricesPrice is clearly tiered by procurement mechanism, with procurement from pooled procurement mechanisms associated with lower prices.5 Pooled procurement mechanisms lead to lower prices for 21 of 28 vaccines compared to self-procurement. Self-procuring MICs pay 2x more than non-Gavi MICs procuring through UNICEF and 1.5x more than PAHO RF-procuring countries.

Pooled procurement mechanisms work with an array of tools and partners to actively shape markets towards a healthier state in order to improve availability and affordability of quality assured vaccines for participating countries. These tools include generating larger order volumes and longer-term contracts that minimize risk for manufacturers.

5 The mean vaccine price by procurement mechanism was compared via the ANOVA test and pairwise comparison t-test using a Bonferroni correction. Since the mean vaccine price by procurement mechanism could have been inflated by the HIC purchases, the median prices were also compared through the Kruskal-Wallis test and multiple pairwise comparison using the Wilcoxon rank-sum test with the Benjamini-Hochberg p-value adjustment method. Both approaches yielded similar, statistically significant results.

6 The visuals show bilateral relationships between price and key variables (order volumes, purchasing country GNI per capita, contract length, region, purchaser domestic health expenditure as a percent of GDP). The MLR results show the impact of that variable alone, with other impacting variables held constant. The MLR includes all variables of interest and also attempts to control for vaccine production costs by including vaccine production complexity, income level of the manufacturing country, and number of years the vaccine has been on the market.

Multiple linear regression (MLR) analysis6 showed that these same variables (order volume and contract length) had a less clear impact on prices for self-procured vaccine purchases. Only very large volume purchases result in a reduced price. A 1 million dose increase in the purchased vaccine volume is associated with a 1.8% decrease in the vaccine price. Longer contracts are associated with lower prices, but this relationship is not statistically significant (likely due to small sample size). The effect of contract length on the purchase price is statistically significant only for specific vaccines that had enough data to run independently: PCV, HPV, HepB, BCG and MMR. MI4A will continue to assess these relationships as countries report enough data to make these analyses possible.

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 7

UN

ICEF

pur

chas

es (

Gav

i elig

.)

UN

ICEF

-pro

curi

ng M

ICpu

rcha

ses

PAH

O R

F pu

rcha

ses

Self

-pro

cure

d M

IC p

urch

ases

Self

-pro

cure

d H

IC p

urch

ases

BCGbOPV

DTDTaP

DTaP-HepB-Hib-IPVDTaP-Hib-IPV

DTaP-IPVDTwP

DTwP-HepB-HibHepA

HepBHib

HPVIPV

JEMeasles

MenACYW-135MMRMR

OCVPCV

PPSVRabies

Rota (per course)Seasonal Influenza

TBETd

TdapTT

Typhoid PsVaricella

YF 20.0026.50

8.024.05

24.5210.88

12.0422.03

21.1423.98

45.44

9.78

53.013.90

9.8613.30

54.319.65

10.8620.08

4.922.95

24.61

27.3922.43

18.130.81

1.011.00

20.0222.61

0.29

28.970.25

4.474.08

13.82

6.499.66

18.29

0.923.92

21.910.77

1.045.07

11.674.40

1.0512.30

1.140.18

15.55

15.8323.52

14.270.22

0.200.22

1.4316.58

13.230.10

2.4413.00

13.008.19

14.50

0.772.75

20.30

3.10

9.582.97

0.3212.72

1.090.19

15.2421.12

15.560.16

0.160.22

0.97

0.08

0.10

8.00

9.39

0.661.45

0.32

3.23

26.12

0.42

1.200.17

0.17

0.180.12

0.97

0.11

0.11

7.03

7.50

3.081.29

0.662.85

0.32

0.452.95

4.50

0.296.99

0.750.17

0.16

0.140.12

- UNICEF and PAHO RF prices are average prices as reported bythese organizations; self-procured prices are median prices- Groups are based on the method of procurement for eachpurchase, not country groups- Only included in analysis if there were purchases from >=2countries for each group

Figure 4.2 Median price per dose by income and procurement group

Notes:UNICEF and PAHO RF prices are average prices as reported by these organizations; self-procured prices are median prices

Groups are based on the method of procurement for each purchase, not country groups

Only included in analysis if there were purchases from >=2 countries for each group

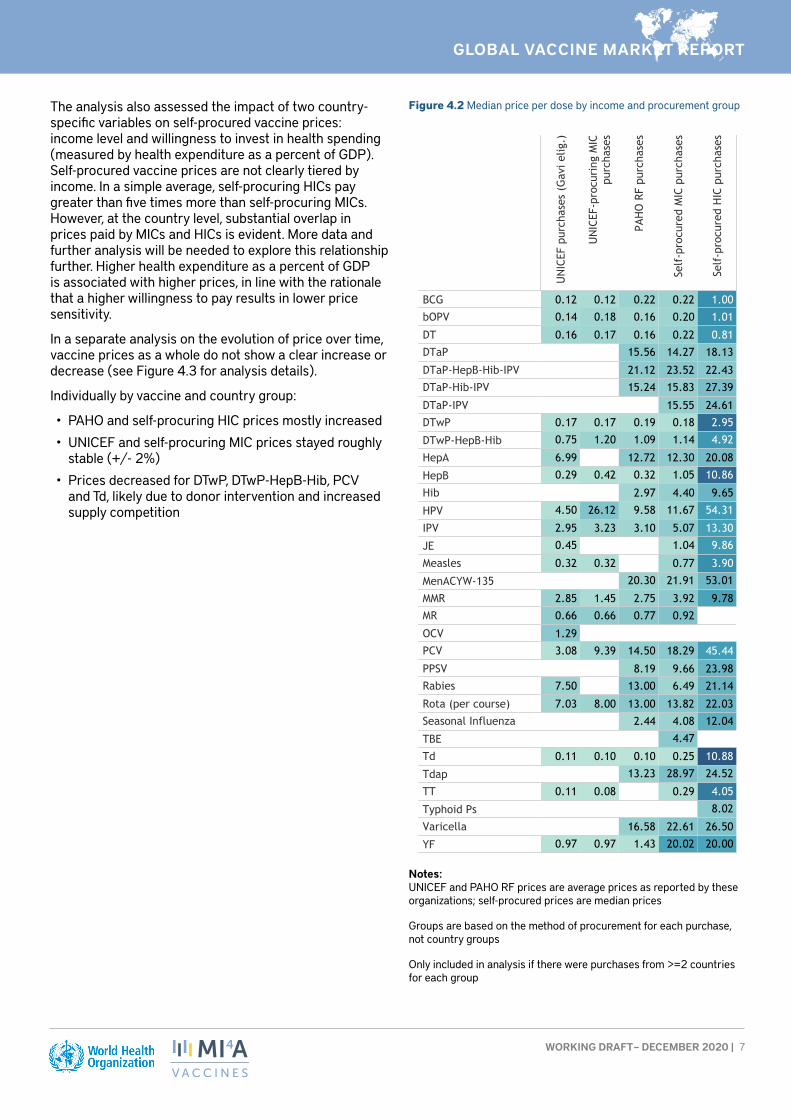

The analysis also assessed the impact of two country-specific variables on self-procured vaccine prices: income level and willingness to invest in health spending (measured by health expenditure as a percent of GDP). Self-procured vaccine prices are not clearly tiered by income. In a simple average, self-procuring HICs pay greater than five times more than self-procuring MICs. However, at the country level, substantial overlap in prices paid by MICs and HICs is evident. More data and further analysis will be needed to explore this relationship further. Higher health expenditure as a percent of GDP is associated with higher prices, in line with the rationale that a higher willingness to pay results in lower price sensitivity.

In a separate analysis on the evolution of price over time, vaccine prices as a whole do not show a clear increase or decrease (see Figure 4.3 for analysis details).

Individually by vaccine and country group:

• PAHO and self-procuring HIC prices mostly increased• UNICEF and self-procuring MIC prices stayed roughly

stable (+/- 2%)• Prices decreased for DTwP, DTwP-HepB-Hib, PCV

and Td, likely due to donor intervention and increased supply competition

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 8

-100% 0% 100%

BCG Self-procuring HIC purchases

PAHO RF

UNICEF SD

DT PAHO RF

UNICEF SD

DTaP PAHO RF

DTaP-HepB-Hib-IPV Self-procuring HIC purchases

PAHO RF

DTaP-Hib-IPV Self-procuring HIC purchases

PAHO RF

DTaP-IPV Self-procuring HIC purchases

PAHO RF

DTwP PAHO RF

UNICEF SD

DTwP-HepB-Hib PAHO RF

UNICEF SD

DTwP-Hib PAHO RF

HepA PAHO RF

HepB Self-procuring HIC purchases

Self-procuring MIC purchases

PAHO RF

UNICEF SD

Hib Self-procuring HIC purchases

PAHO RF

HPV* Self-procuring HIC purchases

PAHO RF

UNICEF SD

IPV Self-procuring HIC purchases

Self-procuring MIC purchases

PAHO RF

UNICEF SD

JE UNICEF SD

28%

59%

-48%

31%

35%

66%

3%

-36%

18%

8%

29%

-23%

-22%

-31%

-67%

-65%

-11%

4%

42%

-34%

-21%

55%

10%

13%

-11%

-4%

-37%

43%

43%

-6%

-1%

55%

-100% 0% 100%

Measles UNICEF SD

MenA UNICEF SD

MenACW-135 Ps UNICEF SD

MenACYW-135 PAHO RF

MMR Self-procuring HIC purchases

Self-procuring MIC purchases

PAHO RF

UNICEF SD

MR PAHO RF

UNICEF SD

OCV PAHO RF

PCV* Self-procuring HIC purchases

Self-procuring MIC purchases

PAHO RF

UNICEF SD

PPSV Self-procuring HIC purchases

PAHO RF

Rabies Self-procuring HIC purchases

PAHO RF

UNICEF SD

Rota* Self-procuring MIC purchases

PAHO RF

UNICEF SD

Seasonal Influenza Self-procuring HIC purchases

Self-procuring MIC purchases

PAHO RF

Td Self-procuring HIC purchases

PAHO RF

UNICEF SD

TT Self-procuring HIC purchases

UNICEF SD

Typhoid Ps PAHO RF

Varicella PAHO RF

YF PAHO RF

UNICEF SD

-8%

-6%

2%

-33%

24%

18%

14%

-14%

23%

22%

-19%

-20%

-19%

1%

-28%

9%

73%

-17%

-9%

2%

-58%

-11%

14%

-17%18%

105%

-14%

-14%

-7%

8%

-9%

11%

18%

10%

16%

*UNICEF prices for HPV, PCV and Rota are the prices offered to Gavi-supported countries only

- Groups are based on the method of procurement for each purchase and the income level of the country purchasing.- Vaccines are included where there are at least three data points for both 2014/15 and 2019 data for the same reporting countries- The same countries must have reported purchases in both 2014/15 and 2019 to have the reported price included.- Average price is adjusted for cumulative inflation in the same time period.

Figure 4.3 Average percent change in price from 2014/2015 to 2019

Notes:

*UNICEF prices for HPV, PCV and Rota are the prices offered to Gavi-supported countries only

Groups are based on the method of procurement for each purchase and the income level of the country purchasing

Vaccines are included if there are at least three data points for both 2014/15 and 2019 data for the same reporting countries

The same countries must have reported purchases in both 2014/15 and 2019 to have the reported price included

Average price is adjusted for cumulative inflation in the same time period

Vaccine RegulationWHO and its partners strive to ensure all countries have access to sufficient doses of vaccine that are of assured quality.7 Stable, well-functioning and integrated regulatory systems (maturity level 3 or above) with streamlined processes and predictable timelines are key to facilitate this access.

In 2019, more than 98.5% of the globally available vaccine doses used in NIPs were of assured quality, up 2.5% from 2017. Additional vaccine-producing countries with functional national regulatory authorities (NRAs) are expected to reduce the remaining 1.5% gap in the coming years. In 2019, the NRA of one more vaccine-producing

7 Vaccines of assured quality include vaccines produced in a country with a stable, well-functioning and integrated national regulatory authority (NRA), including vaccines prequalified by WHO. For more information, please refer to GVAP Secretariat Report 2013; page 80 (www.who.int/immunization/global_vaccine_action_plan/GVAP_secretariat_report_2013.pdf#page=92) and WHO Vaccine Supply and Quality Unit GPV policy statement on vaccine quality (https://apps.who.int/iris/handle/10665/63578).

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 9

Figure 6.1 Reported stockouts over timecountry achieved the status of maturity level 3. Key remaining challenges that could stall progress are lack of necessary commitment and plans to further strengthen regulatory authorities of concern, insufficient resources at the country level, and inconsistent vaccine production by local manufacturers. WHO continues to work with Member States to strengthen their regulatory capacity and achieve stable, well-functioning and integrated regulatory systems.

Countries’ access to sufficient doses of preferred products could be improved by standardizing and streamlining regulatory pathways for registering and approving vaccines. Flexible legislation and enhanced regulatory actions to mitigate anticipated risks – such as registering more than one product or establishing more streamlined registration processes utilizing reliance mechanisms – can help countries to avoid stockouts in the case of market exit or supply shortage from the preferred manufacturer or in case of emergencies and need for new vaccines. However, countries and suppliers are challenged in achieving this flexibility by lengthy and widely varying regulatory requirements that prolong timelines and drive up costs. These requirements are more burdensome for lower-cost manufacturers, potentially limiting access to more affordable products. The extensive ongoing discussions related to facilitating access to future COVID-19 vaccines may provide opportunities to identify suitable avenues to effectively address those constraints.

Vaccine Stockouts & ShortagesFifty-six countries (42% of 132 reporting countries) reported national stockouts8 of one or more vaccines

8 From the 2014 Global Vaccine Action Plan: “A stock-out event is defined when a stock-out of a vaccine occurred for a duration of

Figure 6.2 2019 Stockouts by vaccine

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

0

20

40

60

Num

ber

of C

ount

ries 7365

50

6667 6954

57

70

25GVAP 2020 Target:

BCG

DTP

Hep

B

Hib

HPV IPV

Mea

sles

Men

ingo

cocc

al

OPV PCV

Rota

TT/D

T/Td YF

0%

20%

40%

60%

80%

100%

Prop

orti

on o

f Co

untr

ies

12%19%

27%

54%

27%19% 18%

51%

14%25% 20%

14%

19%

75%73%

66%

46%

63%74% 74%

42%

70%

66%68%

76%72%

13% 10%16% 11% 11%

9%

7%7% 9%8% 8% 8%

National Stockout?No data No Yes

Self-procuring HICs(n=7)

Self-procuring MICs(n=13)

PAHO RF(n=12)

UNICEF (Gavi)(n=21)

0%

20%

40%

60%

80%

100%

Prop

orti

on o

f Co

untr

ies

13%22%

32%

11%

12%13%

11%

13%

11%

50%29%

22%

11%

13%

29%22%

50%

6%6%

Stockout causeCold chain issuesDistribution issuesFunding delaysInaccurate forecastsNRA lot releaseOther/Not identified/Not knownQuality issue on the vaccineStock management issuesGlobal vaccine shortageProcurement delays

Figure 6.3 2019 Reported stockout causes

Notes:Excludes groups with fewer than five countries

Distinct count of countries reporting is provided. However, countries may have reported more than one cause

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 10

Self-procuring HICs

Self-procuring MICs

UNICEF (Gavi)

PAHO RF

UNICEF-procuring MICs

22.5B

8.2B

1.4B

0.9B

0.2B

AMRO

EURO

WPRO

EMRO

AFRO

SEARO

17.2B

6.2B

6.0B

1.6B

1.2B

1.2B

$0B $5B $10B $15B $20B

Value (USD)

PCVD&T-containing

HPVSeasonal Influenza

ShinglesRota

MeningococcalMCVs

VaricellaHepBHepA

IPVPPSV

DTwP-HepB-HibbOPV

7.0B4.3B4.1B4.0B

2.4B2.3B2.3B

1.9B1.7B

0.7B0.5B0.5B0.4B0.2B0.2B

-Only the top 15 vaccines by market value are shown in the vaccinegroup section-Analysis excludes travel and military markets

Country (group)ChinaIndiaRest of world

Figure 7.1 Global market value by region, county group and vaccine

Notes:Only the top 15 vaccines by market value are shown in the vaccine group section

Analysis excludes travel and military markets

in 2019. This is down from 69 countries reporting stockouts last year, but still falls far short of the GVAP 2020 target of 25 countries. Thirty-four of the 56 countries (65%) reported national stockouts for two or more vaccines.

YF, OPV, and BCG had the highest rates of reported stockouts.

Procurement delays9 and global shortages accounted for 33% and 21% of reported stockouts across country groups, respectively. Global shortages alone were responsible for 50% of self-procuring HIC stockouts. For pooled-procuring countries, funding delays were large contributors to stockouts (20-40%).

Global Market ValueMI4A estimates global market value for vaccines to be approximately $33 billion in 2019, representing about 2% of the overall pharmaceutical market.10 This estimate includes for the first time seasonal influenza, OPV and revised value estimates for the US allowing for a more comprehensive estimate that is also supported by an improved methodology.

HICs – in particular in the AMR and EUR regions – represent the largest share (68%) of the global market value. PCV, D&T-containing, HPV, seasonal influenza and shingles are the franchises with the highest global value in 2019. Higher market value derives from large volumes, high prices or a combination of the two. PCVs command high prices and a three-dose schedule, while D&T-containing vaccines are six-dose series and have more expensive combination/aP products, boosting value. HPV and shingles have comparatively low volumes but high prices, while seasonal influenza has high volume, particularly in HICs.

Based on in-depth market studies, HPV and PCV are likely to see high value growth, with HPV expecting a nearly 60% increase in value due to expected introductions by 2030.11

at least one month… If a stock-out (of at least one month) in one country were reported for two vaccines, these would be considered as two stock-out events for that country.” Available at: www.who.int/immunization/global_vaccine_action_plan/gvap_secretariat_report_2014.pdf

9 Procurement delays can refer to delays by the procuring agency or delays by countries to initiate their procurement

10 Institute of Medicine (US) Committee on the Evaluation of Vaccine Purchase Financing in the United States. Financing Vaccines in the 21st Century: Assuring Access and Availability. Washington (DC): National Academies Press (US); 2003. 5, Vaccine Supply. Available from: www.ncbi.nlm.nih.gov/books/NBK221811/

11 Market value projections leverage the same high-growth volume assumptions presented in the global volume section. For price, market value projections assume the continuation of a country’s 2019 reported price for each vaccine. For countries that have not

Figure 7.2 Potential vaccine market value growth 2020–2030

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 11

Annex 1: Additional ResourcesUNICEF Immunization Supplies and Logistics publications and data (including vaccine price data used in this report): www.unicef.org/supply/influencing-markets

PAHO RFVaccine price data (used in this report):

www.paho.org/hq/index.php?option=com_content&view=article&id=1864:paho-revolving-fund&Itemid=4135&lang=en

GaviVaccine Roadmap public summaries and other supply and procurement related documents:

www.gavi.org/library/gavi-documents/supply-procurement/

Other WHO MI4A resourcesVaccine purchase data (in Excel format for download) and vaccine-specific global market studies:

www.who.int/immunization/mi4a

reported to the JRF, price was estimated based on a country’s procurement mechanisms and income groups.

Annex 2: Data Sources The primary data source for the analyses in this report is purchase and schedule data reported by countries through the WHO-UNICEF Joint Reporting Form (JRF). This is supplemented with additional publicly available information from PAHO RF, UNICEF and past WHO MI4A individual vaccine market studies.

Remaining information gaps are filled using the Global Vaccine Market Model (GVMM), which estimates demand and price by country and vaccine across all WHO Member States, leveraging publicly available information.

World Bank provides data for GNI (gross national income) per capita and global cumulative inflation rate:

https://data.worldbank.org/indicator/NY.GNP.ATLS.CD

https://data.worldbank.org/indicator/FP.CPI.TOTL.ZG

DisclaimerInformation contained in the MI4A database is provided by participating countries that have agreed to share vaccine price and procurement data. Participating countries are solely responsible for the accuracy of the data provided.The information contained in the MI4A database does not in any way imply an endorsement, certification, warranty of fitness or recommendation by WHO of any company or product for any purpose, and does not imply preference over products of a similar nature that are not mentioned. WHO furthermore does not warrant that: (1) the information is complete and/or error free; and/or that (2) the products listed are of acceptable quality, have obtained regulatory approval in any country, or that their use is otherwise in accordance with the national laws and regulations of any country, including but not limited to patent laws. Inclusion of products in the database does not furthermore imply any approval by WHO of the products in question (which is the sole prerogative of national authorities).WHO will not accept any liability or responsibility whatsoever for any injury, death, loss, damage, or other prejudice of any kind that may arise as a result of, or in connection with the procurement, distribution and use of any product listed in the MI4A database.

GLOBAL VACCINE MARKET REPORT

WORKING DRAFT – DECEMBER 2020 | 12

Annex 3: Acronym List

AFR/AFRO WHO African Region MMR Measles, mumps and rubella

AMR/AMRO WHO Region of the Americas MMRV Measles, mumps, rubella and varicella

aP-containing acellular pertussis–containing MR Measles and rubella

BCG Bacillus Calmette–Guérin (for tuberculosis) NIP(s) National immunization program(s)

bOPV Polio vaccine – oral (OPV) bivalent types 1 and 3

NRA(s) National regulatory authority/ies

D&T-containing Diphtheria- and tetanus-containing OCV Oral cholera vaccine

DCVM(s) Developing country vaccine manufacturer(s)

OPV Oral polio vaccine

DTaP Diphtheria-tetanus-pertussis (acellular) PAHO RF Pan American Health Organization Revolving Fund

DTwP Diphtheria-tetanus-pertussis (whole cell) PCV Pneumococcal conjugate vaccine

EMR/EMRO WHO Eastern Mediterranean Region PPSV Pneumococcal polysaccharide vaccine

EUR/EURO WHO European Region PQ’d Prequalified

GDP Gross domestic product Ps Polysaccharide

GNI Gross national income Rota Rotavirus

GVAP Global Vaccine Action Plan SE South-East

GVMM Global Vaccine Market Model SEAR/SEARO WHO South-East Asia Region

HepA, HepB Hepatitis A, hepatitis B SIA Supplementary immunization activities

Hib Haemophilus influenzae type b TBE Tick-borne encephalitis

HIC(s) High-income country/ies TCV Typhoid conjugate vaccine

HPV Human papillomavirus Td Tetanus-diphtheria (reduced antigen content)

IPV Inactivated Polio Vaccine Tdap Tetanus-diphtheria-acellular pertussis (reduced antigen content)

IVIR-AC Immunization and Vaccine-related Implementation Research (IVIR) Advisory Committee

TT Tetanus toxoid

JE Japanese encephalitis UNICEF United Nations Children’s Fund

JRF Joint Reporting Form WHO World Health Organization

MCV(s) Measles-containing vaccine(s) wP whole-cell pertussis

MCV2 Measles-containing-vaccine second-dose WPR/WPRO WHO Western Pacific Region

MenA, Men B, MenC Meningococcal A, B, C YF Yellow fever

MenACW-135 (Ps) Meningococcal ACW-135 polysaccharide

MenACWY Meningococcal ACWY

MIC(s) Middle-income country/ies