Embed Size (px)

Citation preview

Rue d’Arlon 80

1040 Brussels,Belgium

T. +32 2 213 18 97

www.gwec.net

Globalization of Offshore WindBen Backwell, GWEC

Tokyo, 8 March 2019

Ben Backwell - CEO of GWEC

Author of Wind Power, the Struggle for Control of a New Global

Industry (Taylor and Francis , 2017) Haynes Guide to Offshore

Wind Energy (Haynes/Renewable UK)

Former industry consultant at FTI Consulting, advised leading

players in UK offshore wind market on political stake holder

management, lobbying and media engagement

Former energy journalist and analyst, covering energy policy

and markets for 15 years

å

CO Members

Associations

C1, C2, and C3 Members

GWEC Offshore Task Force Workplan 2018/19

Activity Nov

Nov

Dec

Dec

Dec

Dec

Dec

Jan

Jan

Jan

Jan

Feb

Feb

Feb

Feb

Mar

Mar

Mar

Mar

Apr

Apr

Apr

Apr

Apr

May

May

May

May

Jun

Jun

Jun

Jun

Jul

Jul

Jul

Jul

Jul

Aug

Aug

Aug

Aug

Sep

Sep

Sep

Sep

Sep

Oct

Oct

Oct

Oct

Nov

Nov

Nov

Nov

Dec

Dec

Dec

Dec

A Stakeholder engagement

Stakeholder mapping

Comms planning, 1st engagement

1st engagement - tier 1

1st engagement - tier 2

1st engagement - tier 3

Collate feedback

Comms planning, subsequent engagements → → →

Press articles Recharge 600 words

B Policy toolkit

Calibration workshop in UK 27

Adjust toolkit

Identify US calibration State

Identify Asia calibration country

Set up US workshop

Deploy US workshop IPF

Set up Asia workshop

Deploy Asia workshop

Identify countries/states for deployment

Finalise toolkit v1

Plan roll-out for 2019

Roll-out workshops → → →

C Best practice guidance

List topics

Agree topics

Topic 1 drafting

Topic 1 expert review

Topic 1 task force review

Publish topic 1 guidance

Further topics → → →

D Joint industry workstreams

Propose themes

Agree themes

Plan themes ⇣

Budget themes ⇣

Agree funding sources ⇣

Propose funding ⇣ ⇣

Agree funding ⇣ ⇣ → → →

⇣ ⇣ ⇣

E Events ⇣ ⇣ ⇣

Task Force meetings 21

Global Offshore Summit & Taiwan Wind Power 25

International Partnering Forum, US 8

Global Offshore Wind, UK 25

F Policy research

Market opportunities updates

Country profiles

Topic specific research

G Programme activities

Risk register

Theme reviews

After action reviews UK w/s India w/s 1st comms Agree themes US w/s 1st guidance GOW Themes funding

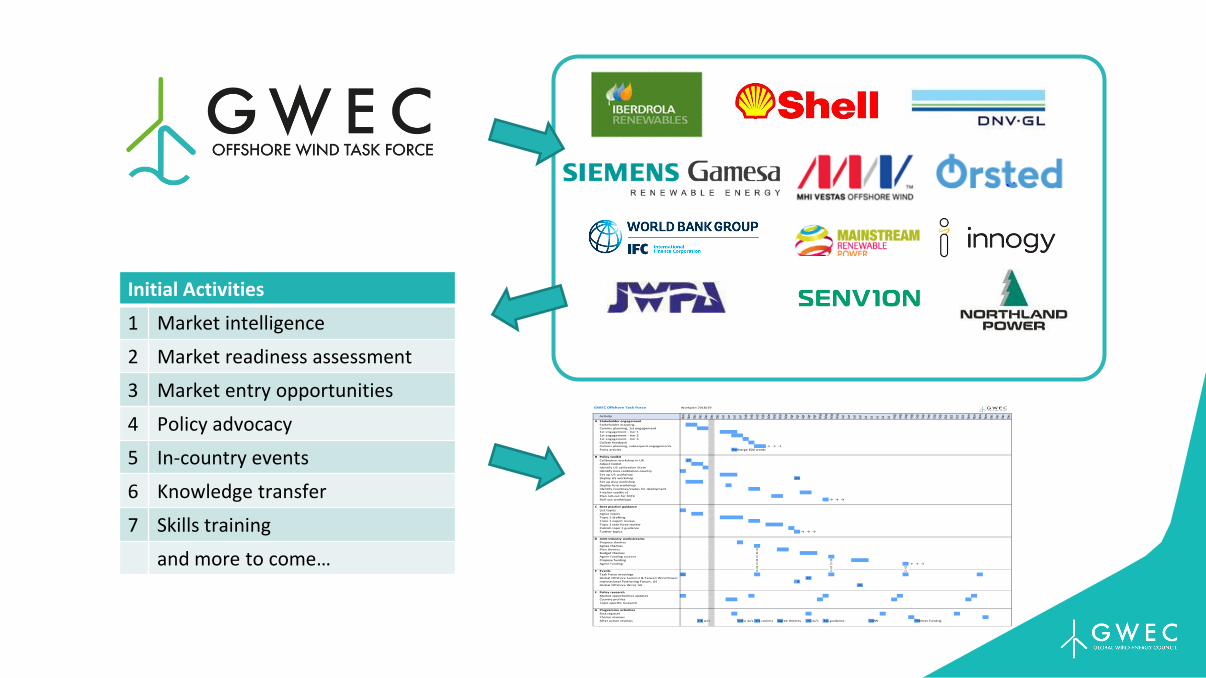

Initial Activities

1 Market intelligence

2 Market readiness assessment

3 Market entry opportunities

4 Policy advocacy

5 In-country events

6 Knowledge transfer

7 Skills training

and more to come…

Main text to go in this space

• Bullet

• Bullet

• Bullet

Heading in this

space

Global Wind Ambassador – Henrik Stiesdal

• Designed seminal wind turbine models that

shaped modern wind industry

• Built world’s first full scale Offshore Wind farm

• Designed most successful offshore wind

turbines in market as CTO of Siemens

Windpower

• Has designed revolutionary floating wind

concept with pilot set to be deployed and

investment from Shell and Innogy

Main text to go in this space

• Bullet

• Bullet

• Bullet

Heading in this

space

Task Force Chairman - Alastair Dutton

• Former BP - developed solar, onshore wind

and offshore wind projects.

• Former Programme Manager for all the UK’s

offshore wind projects for the Crown Estate

which owns the UK seabed. Managed

successful Round 3 and N Ireland tenders

and chaired the selection panel for the site

awards.

• Former Expert Advisor for Offshore Wind at

the UK Department for Business, Energy and

Industrial Strategy (BEIS)

Main text to go in this space

• Bullet

• Bullet

• Bullet

Heading in this

space

”.

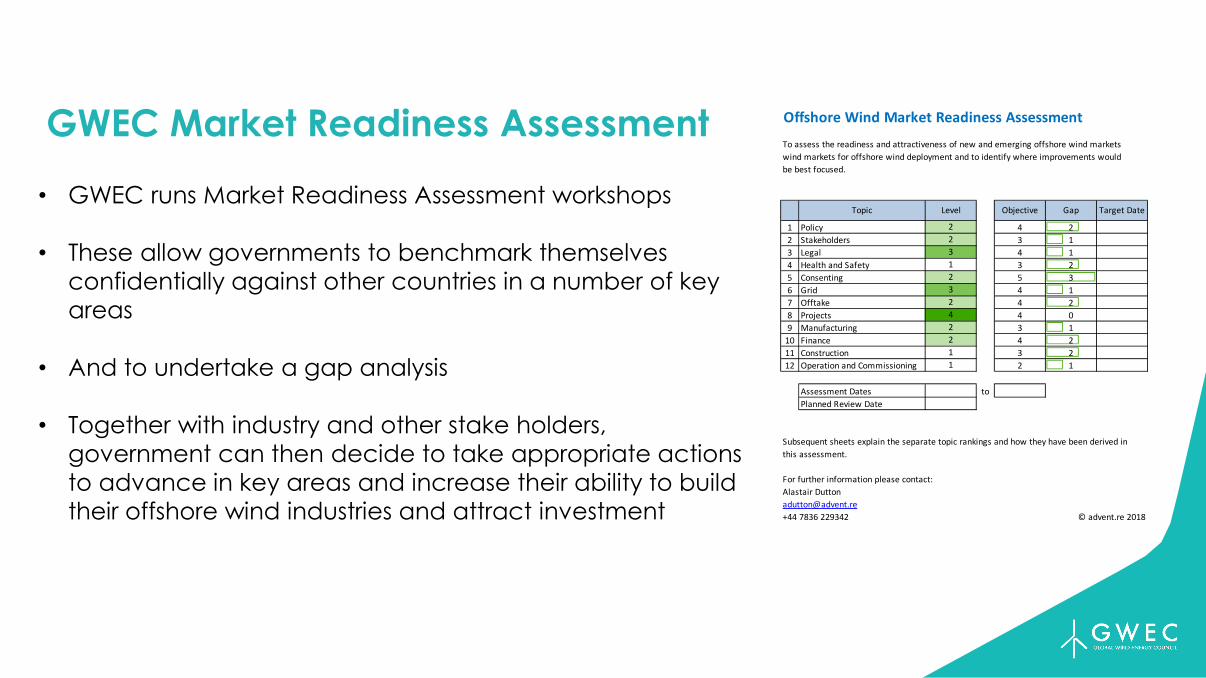

GWEC Market Readiness Assessment

• GWEC runs Market Readiness Assessment workshops

• These allow governments to benchmark themselves

confidentially against other countries in a number of key

areas

• And to undertake a gap analysis

• Together with industry and other stake holders,

government can then decide to take appropriate actions

to advance in key areas and increase their ability to build

their offshore wind industries and attract investment

Copyright Advent.re 2018

Offshore Wind Market Readiness Assessment

To assess the readiness and attractiveness of new and emerging offshore wind markets

wind markets for offshore wind deployment and to identify where improvements would

be best focused.

Topic Level Objective Gap Target Date

1 Policy 2 4 2

2 Stakeholders 2 3 1

3 Legal 3 4 1

4 Health and Safety 1 3 2

5 Consenting 2 5 3

6 Grid 3 4 1

7 Offtake 2 4 2

8 Projects 4 4 0

9 Manufacturing 2 3 1

10 Finance 2 4 2

11 Construction 1 3 2

12 Operation and Commissioning 1 2 1

Assessment Dates to

Planned Review Date

Subsequent sheets explain the separate topic rankings and how they have been derived in

this assessment.

For further information please contact:

Alastair Dutton

+44 7836 229342 © advent.re 2018

Main text to go in this space

• Bullet

• Bullet

• Bullet

Heading in this

space

”.

GWEC – World Bank/IFC Cooperation to take Offshore

Global

* Preliminary

Source: GWEC Market Intelligence

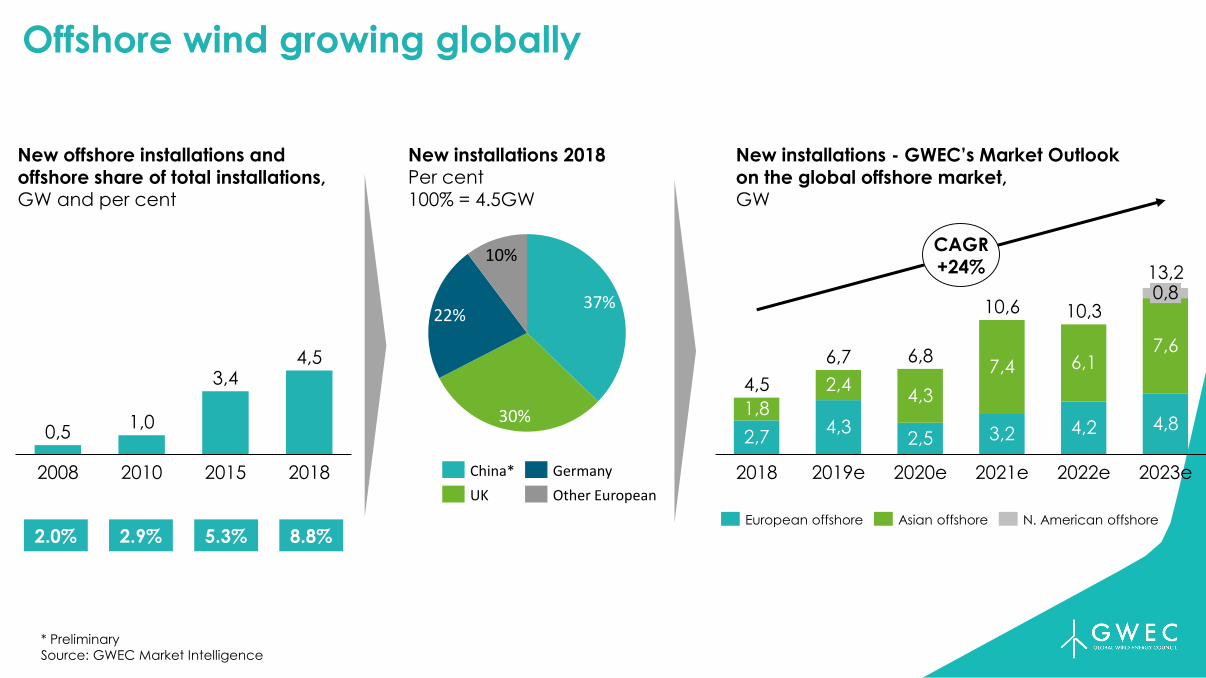

Offshore wind growing globally

0,5

3,4

20182008 2010 2015

1,0

4,5

New offshore installations and offshore share of total installations,GW and per cent

5.3% 8.8%2.0% 2.9%

New installations - GWEC’s Market Outlook on the global offshore market,GW

13,2

4,3 3,2

2,47,4

2019e

2,5

4,34,5

10,6

2020e 2021e

4,2

6,1

2022e

10,3

4,8

6,87,6

2,7

2023e

6,7

0,8

2018

1,8

CAGR+24%

Asian offshoreEuropean offshore N. American offshore

New installations 2018Per cent100% = 4.5GW

37%

30%

22%

10%

China* Germany

UK Other European

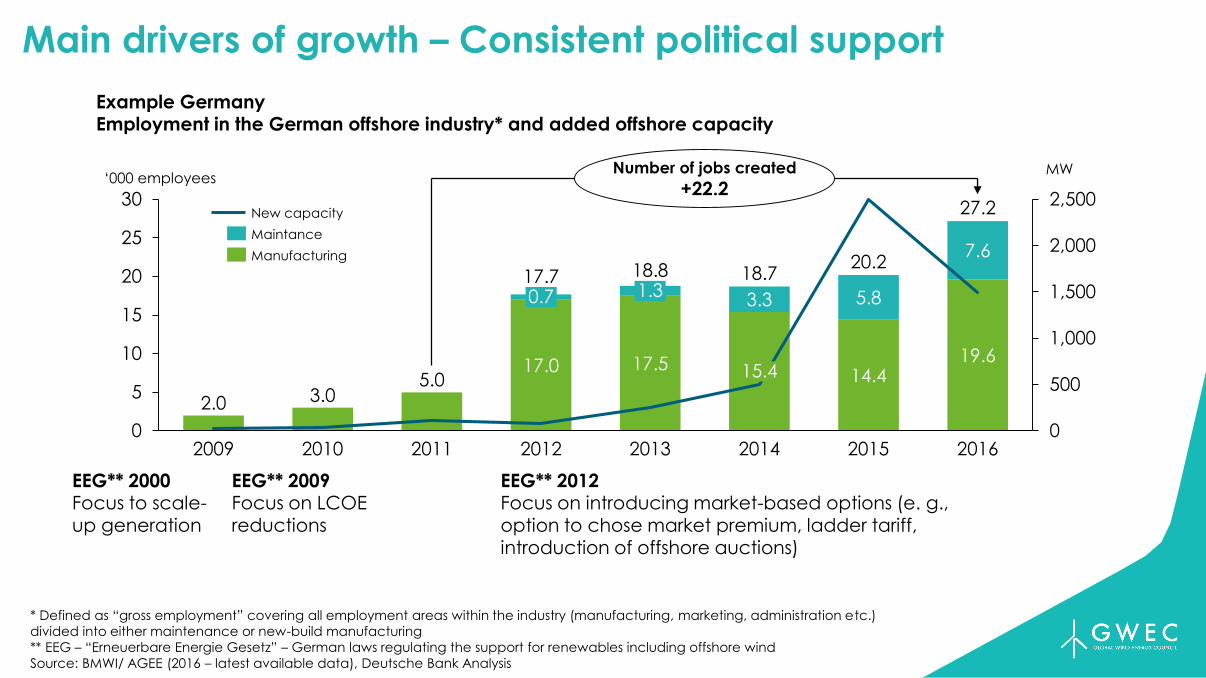

Main drivers of growth – Consistent political support

Example GermanyEmployment in the German offshore industry* and added offshore capacity

2.0 3.05.0

17.0 17.514.4

19.6

3.3 5.8

7.6

0

500

1,000

1,500

2,000

2,500

0

5

10

15

20

25

30

201320122009

15.4

2010 2011

0.7 1.3

20152014 2016

17.7 18.8 18.720.2

27.2

Number of jobs created

+22.2

New capacity

Maintance

Manufacturing

‘000 employeesMW

EEG** 2000Focus to scale-

up generation

EEG** 2009Focus on LCOE

reductions

EEG** 2012Focus on introducing market-based options (e. g.,

option to chose market premium, ladder tariff, introduction of offshore auctions)

* Defined as “gross employment” covering all employment areas within the industry (manufacturing, marketing, administration etc.)

divided into either maintenance or new-build manufacturing

** EEG – “Erneuerbare Energie Gesetz” – German laws regulating the support for renewables including offshore wind

Source: BMWI/ AGEE (2016 – latest available data), Deutsche Bank Analysis

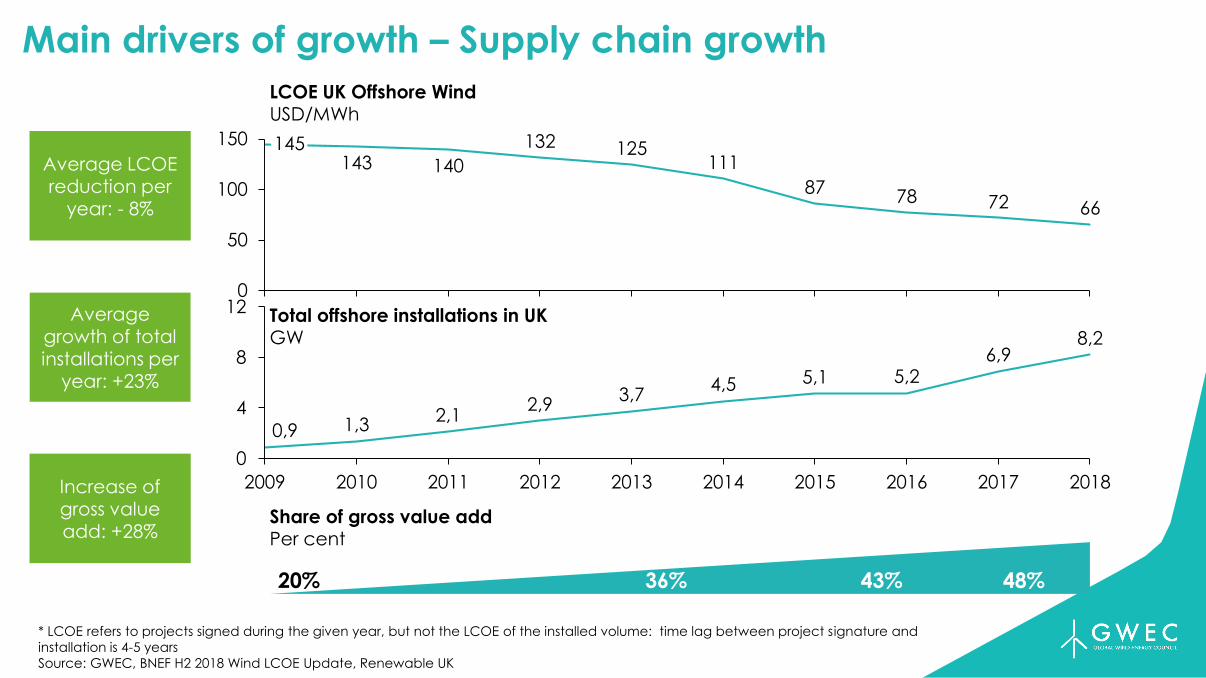

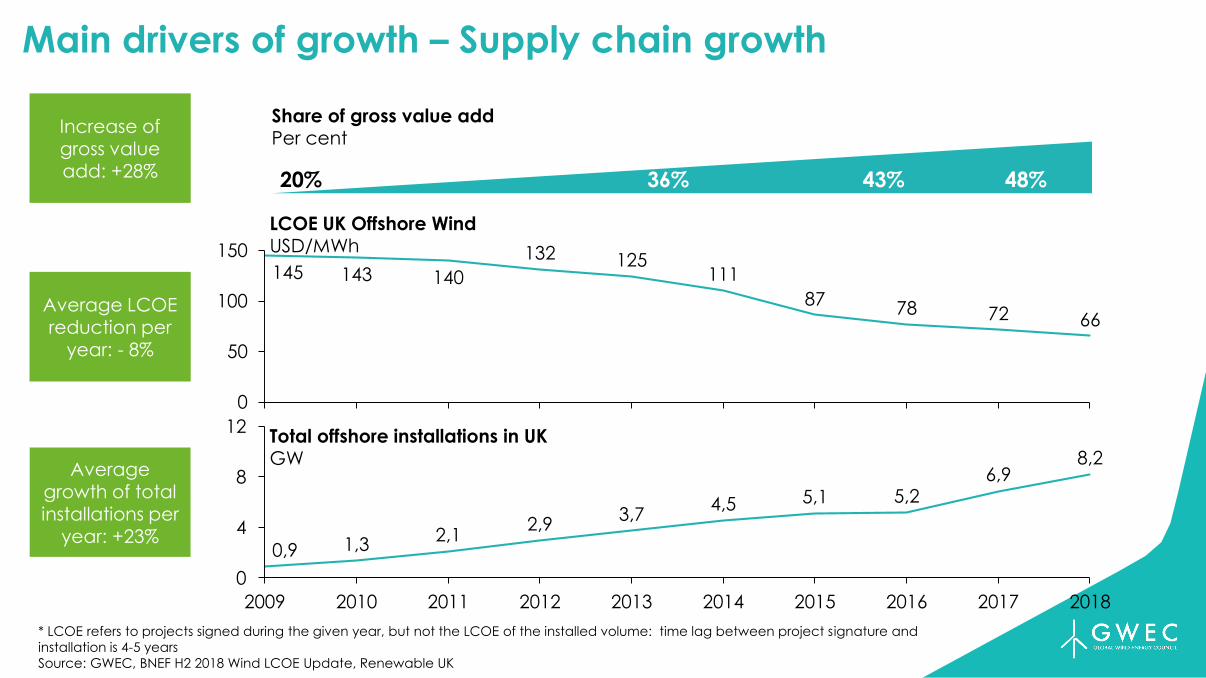

Main drivers of growth – Supply chain growth

* LCOE refers to projects signed during the given year, but not the LCOE of the installed volume: time lag between project signature and

installation is 4-5 years

Source: GWEC, BNEF H2 2018 Wind LCOE Update, Renewable UK

143 140

132 125111

8778 72 66

0

50

100

150 145

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

12

4

0

8

2,92,1

6,9

4,5

1,3

3,75,1 5,2

8,2

0,9

48%43%36%20%

LCOE UK Offshore WindUSD/MWh

Total offshore installations in UKGW

Share of gross value addPer cent

Average LCOE reduction per

year: - 8%

Average growth of total installations per

year: +23%

Increase of gross value add: +28%

Main drivers of growth – Supply chain growth

* LCOE refers to projects signed during the given year, but not the LCOE of the installed volume: time lag between project signature and

installation is 4-5 years

Source: GWEC, BNEF H2 2018 Wind LCOE Update, Renewable UK

145 143 140

132 125111

8778 72 66

0

50

100

150

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

0

4

8

12

2,92,1

1,30,9

3,74,5 5,1 5,2

6,98,2

LCOE UK Offshore WindUSD/MWh

Total offshore installations in UKGW

48%43%36%20%

Share of gross value addPer cent

Average LCOE reduction per

year: - 8%

Average growth of total installations per

year: +23%

Increase of gross value add: +28%

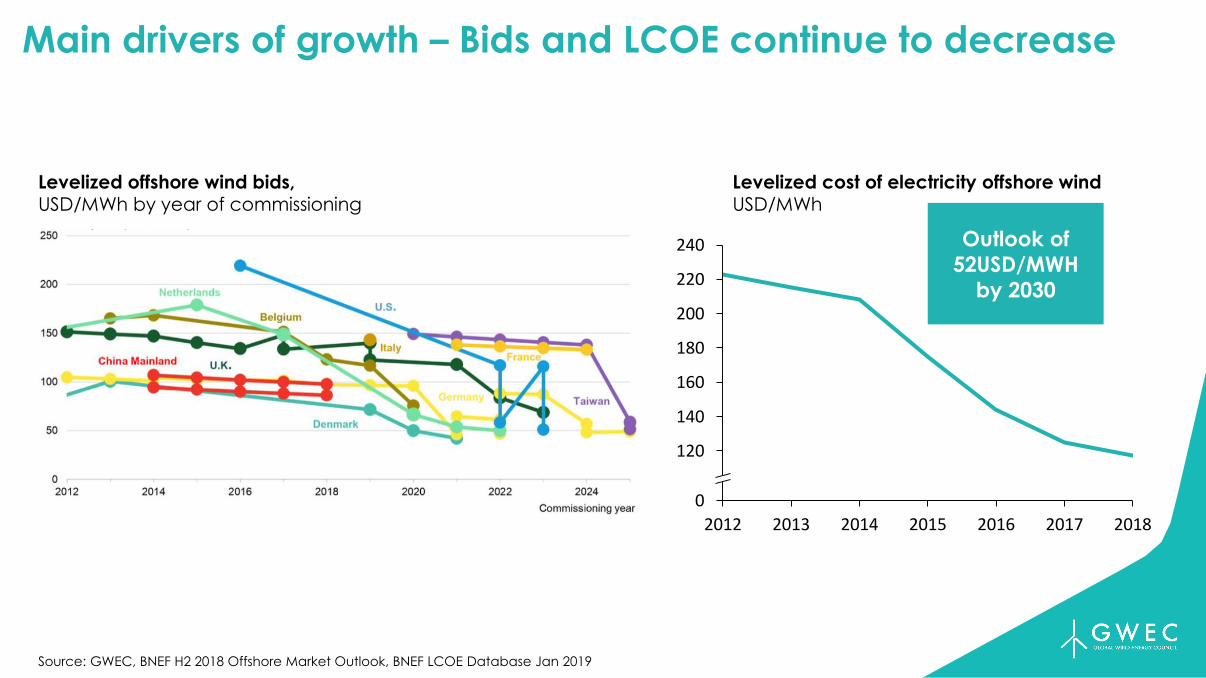

Main drivers of growth – Bids and LCOE continue to decrease

Source: GWEC, BNEF H2 2018 Offshore Market Outlook, BNEF LCOE Database Jan 2019

Levelized offshore wind bids,USD/MWh by year of commissioning

Levelized cost of electricity offshore windUSD/MWh

2012 2013 2014 2015 2016 2017 2018

140

0

120

200

160

180

220

240 Outlook of

52USD/MWH

by 2030

Main text to go in this space

• Bullet • Bullet• Bullet

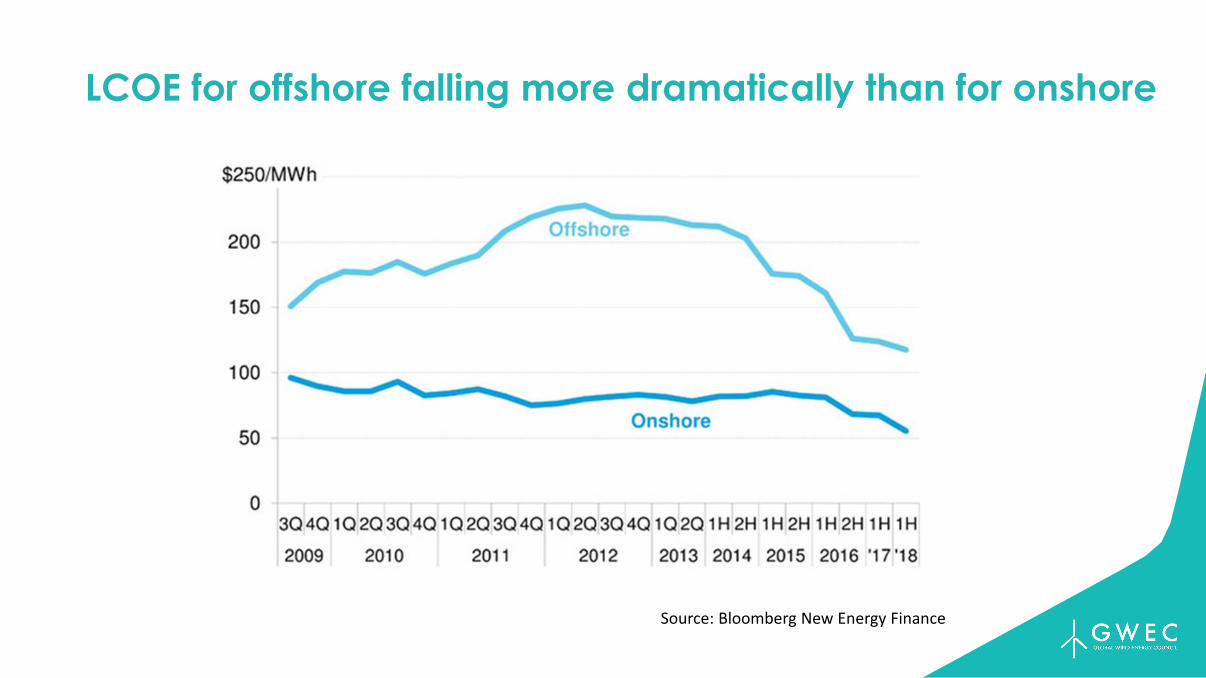

Heading in this spaceLCOE for offshore falling more dramatically than for onshore

Source: Bloomberg New Energy Finance

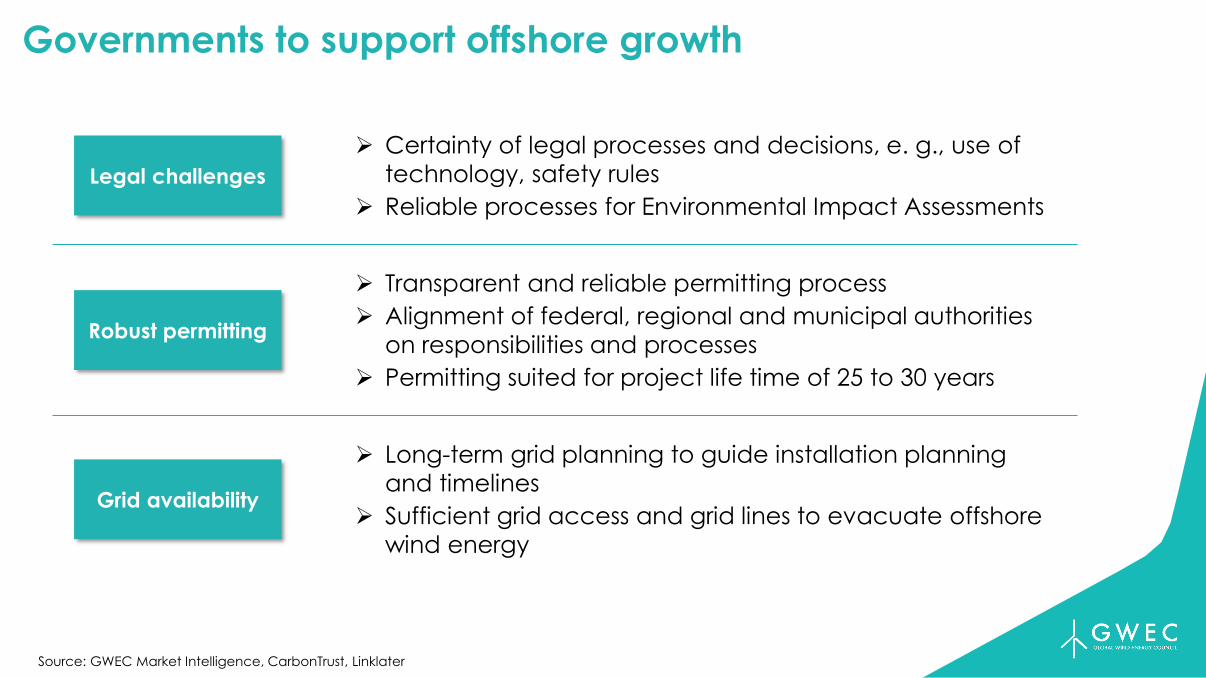

Governments to support offshore growth

Source: GWEC Market Intelligence, CarbonTrust, Linklater

Robust permitting

➢ Transparent and reliable permitting process

➢ Alignment of federal, regional and municipal authorities

on responsibilities and processes

➢ Permitting suited for project life time of 25 to 30 years

Legal challenges

➢ Certainty of legal processes and decisions, e. g., use of

technology, safety rules

➢ Reliable processes for Environmental Impact Assessments

Grid availability

➢ Long-term grid planning to guide installation planning

and timelines

➢ Sufficient grid access and grid lines to evacuate offshore

wind energy

Source: GWEC Market Intelligence, Press

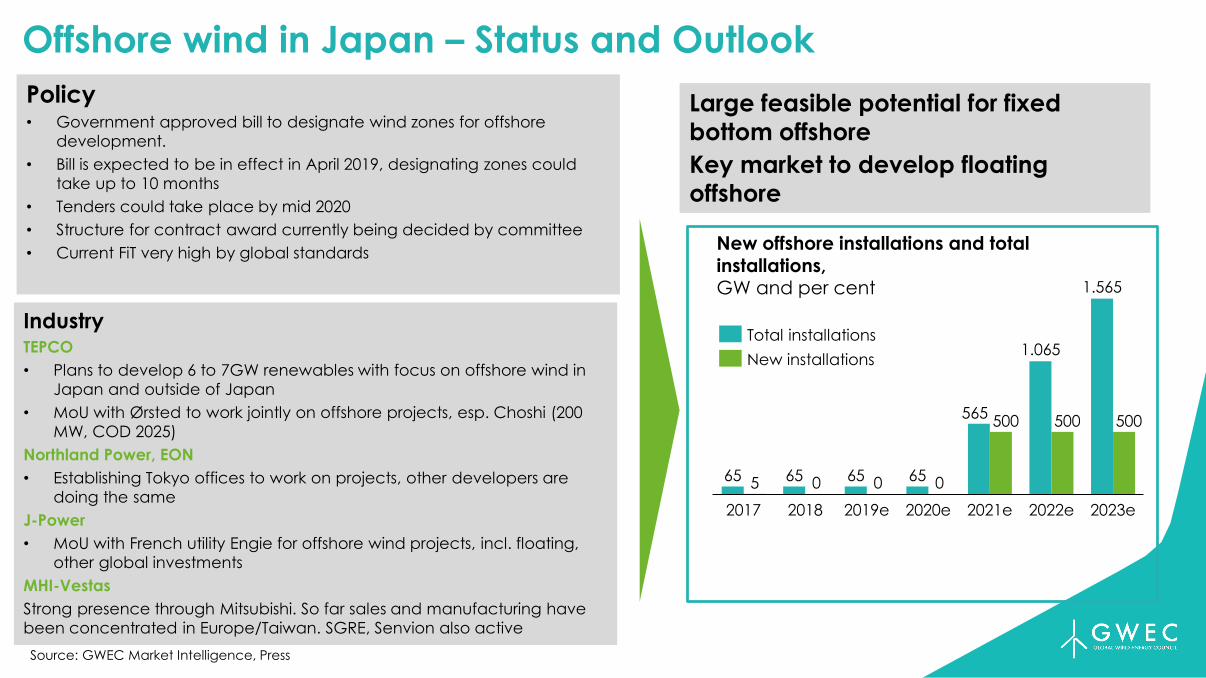

Offshore wind in Japan – Status and Outlook

65 65 65 65

565

5

500 500 500

2017

0

2018 2020e2019e 2021e

0

2022e 2023e

1.065

1.565

0

Total installations

New installations

New offshore installations and total installations,GW and per cent

Policy• Government approved bill to designate wind zones for offshore

development.

• Bill is expected to be in effect in April 2019, designating zones could

take up to 10 months

• Tenders could take place by mid 2020

• Structure for contract award currently being decided by committee

• Current FiT very high by global standards

IndustryTEPCO

• Plans to develop 6 to 7GW renewables with focus on offshore wind in

Japan and outside of Japan

• MoU with Ørsted to work jointly on offshore projects, esp. Choshi (200

MW, COD 2025)

Northland Power, EON

• Establishing Tokyo offices to work on projects, other developers are

doing the same

J-Power

• MoU with French utility Engie for offshore wind projects, incl. floating,

other global investments

MHI-Vestas

Strong presence through Mitsubishi. So far sales and manufacturing have

been concentrated in Europe/Taiwan. SGRE, Senvion also active

Large feasible potential for fixed

bottom offshore

Key market to develop floating

offshore

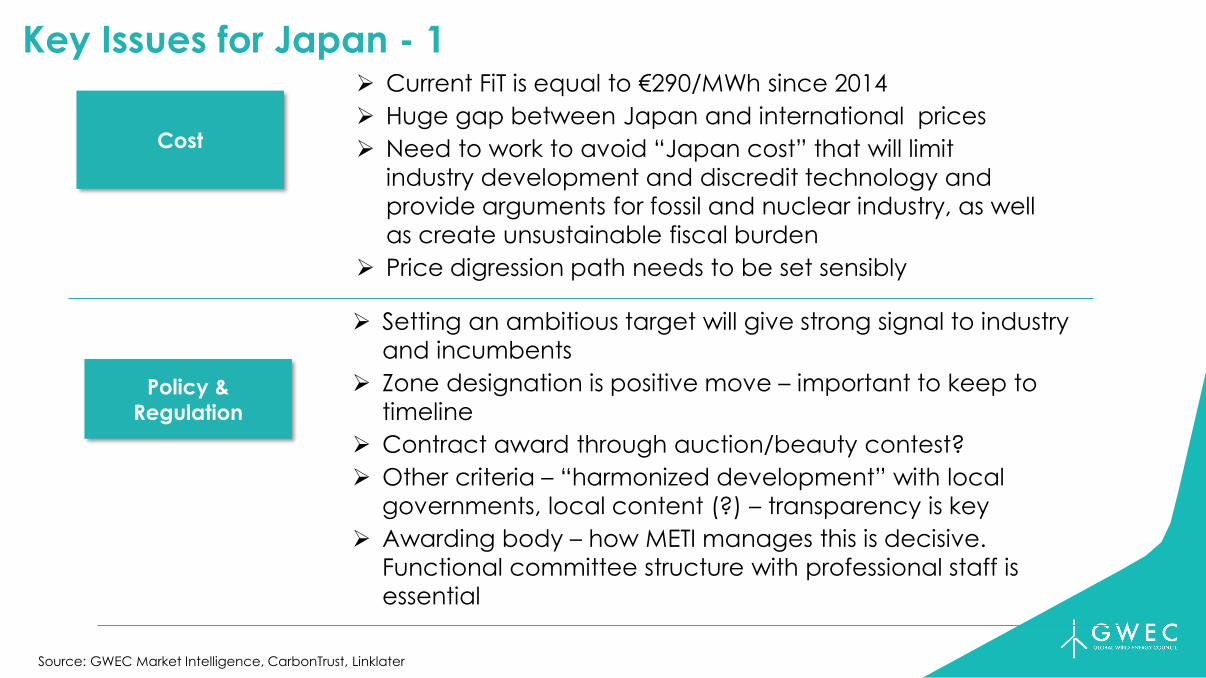

Key Issues for Japan - 1

Source: GWEC Market Intelligence, CarbonTrust, Linklater

Policy &

Regulation

Cost

➢ Current FiT is equal to €290/MWh since 2014

➢ Huge gap between Japan and international prices

➢ Need to work to avoid “Japan cost” that will limit

industry development and discredit technology and

provide arguments for fossil and nuclear industry, as well

as create unsustainable fiscal burden

➢ Price digression path needs to be set sensibly

➢ Setting an ambitious target will give strong signal to industry

and incumbents

➢ Zone designation is positive move – important to keep to

timeline

➢ Contract award through auction/beauty contest?

➢ Other criteria – “harmonized development” with local

governments, local content (?) – transparency is key

➢ Awarding body – how METI manages this is decisive.

Functional committee structure with professional staff is

essential

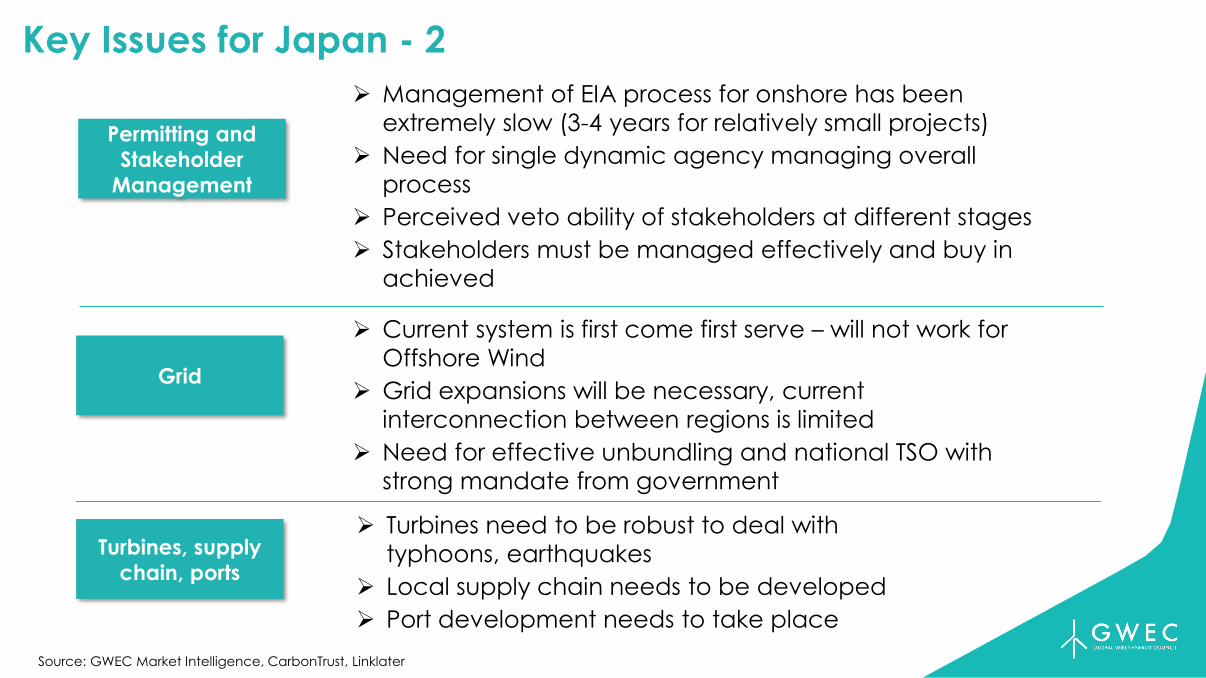

Key Issues for Japan - 2

Source: GWEC Market Intelligence, CarbonTrust, Linklater

Permitting and

Stakeholder

Management

➢ Management of EIA process for onshore has been

extremely slow (3-4 years for relatively small projects)

➢ Need for single dynamic agency managing overall

process

➢ Perceived veto ability of stakeholders at different stages

➢ Stakeholders must be managed effectively and buy in

achieved

Grid

➢ Current system is first come first serve – will not work for

Offshore Wind

➢ Grid expansions will be necessary, current

interconnection between regions is limited

➢ Need for effective unbundling and national TSO with

strong mandate from government

Turbines, supply

chain, ports

➢ Turbines need to be robust to deal with

typhoons, earthquakes

➢ Local supply chain needs to be developed

➢ Port development needs to take place

Main text to go in this space

• Bullet

• Bullet

• Bullet

Heading in this

space

”.

Offshore wind – two scenarios…

• Offshore wind is a golden chance for Japan to create economical zero carbon energy and

increase its energy independence

• But to achieve this, it needs to let the wind industry build and grow

• The danger is that to much complexity is created, which will keep volumes small, prices high

and allow incumbent energy interests to prevail

• But if the government has the courage to seize the opportunity and get the right frameworks

in place, offshore wind can be built quickly, economically and at large scale, helping to

create economic growth, employment and new skills.

This is too good an opportunity for Japan to miss!

Rue d’Arlon 80

1040 Brussels,Belgium

T. +32 2 213 18 97

www.gwec.net

Thank you!For more information please contact:

Ben Backwell I [email protected]

![Globalization Globalization - The External Pressures.[2001.ISBN0471499382]](https://img.pdfslide.net/doc/110x75/54e9c2e54a795910478b4905/globalization-globalization-the-external-pressures2001isbn0471499382.jpg)