Embed Size (px)

Citation preview

Going Beyond Beta in Bonds: The Need for Active Management

Presenter:

MIHIR WORAH CIO Asset Allocation & Managing Director PIMCO

Your Global Investment Authority

Mihir Worah

November 5, 2015

Pacific Investment Management

Company LLC, 650 Newport Center

Drive, Newport Beach, CA 92660,

949.720.6000

For investment professional use only

pg 3 Your Global Investment Authority

176% 88% 63% 33% 31% 53% 136% 26% 314% -20%

Cumulative returns: Mar '09–Sep '15

Since the financial crisis, most asset classes have

experienced exceptionally strong returns

As of 30 September 2015

SOURCE: Bloomberg, PIMCO

* Global developed bonds, ex-U.S. hedged

U.S. equities: S&P 500 Index; Developed int’l equities: MSCI EAFE Net Dividend Index (USD Unhedged); EM Equities: MSCI Emerging Markets Index; U.S. core fixed income:

Barclays U.S. Aggregate Index; Global bonds (H): JPMorgan GBI Global ex-US USD Hedged; Global IG: Barclays Global Agg Credit (USD Hedged); Global HY: MLX

DevelMarkHighYieldConstr(USD Hedged); EM local bonds: JPMorgan Government Bond Index- Emerging Markets Global Diversified Index (Unhedged); REITS: Dow Jones

U.S. Select REIT Total Return Index; Diversified commodities: Bloomberg Commodity Index Total Return

Refer to Appendix for additional investment strategy and risk information.

18%

11%8%

5% 4%7%

15%

4%

26%

-3%-5%

0%

5%

10%

15%

20%

25%

30%

U.S.

equities

Developed

int'l

equities

EM

equities

U.S. core

fixed

income

Global

bonds

(H)*

Global

IG

Global

HY

EM local

bonds

REITs Diversified

commodities

Annualized asset class returns: Mar '09–Sep '15

pg 4 Your Global Investment Authority

Lower discount rates fueled asset returns and

supported higher valuations

Real

policy

rate

Inflation

premium

Term

premium

Credit

risk

premium

Equity

risk

premium

Sovereign

Credit

Equity

For Illustrative Purposes Only

SOURCE: PIMCO

Refer to Appendix for additional investment strategy and risk information.

Fair

Value

Discoun

t Rate

pg 5 Your Global Investment Authority

PIMCO’s capital market assumptions

(10-year, nominal)

Capital_Securities_outlook_01 As of 30 September 2015

SOURCE: PIMCO

Hypothetical example for illustrative purposes only.

* Return estimates are derived from an internal process based on a combination of methods: pulling together historical data, valuation metrics and qualitative

inputs based on PIMCO’s secular views

U.S. cash – Citi 3-Month Treasury Bill Index; U.S. core bonds – Barclays U.S. Aggregate Index; global bonds (USD-hedged) – Barclays Global Aggregate ex USD Index; U.S. high yield –

Barclays U.S. High Yield Index; U.S. equities – S&P 500 Index; European equities (USD-hedged) – MSCI Europe Index; Japanese equities (USD-hedged) – MSCI Japan Index; EM cash

(unhedged) – J.P. Morgan ELMI + Unhedged Index; EM sovereign bonds (unhedged) – J.P. Morgan GBI-EM Global Index; EM corporates (unhedged) – J.P. Morgan CEMBI Diversified Index;

EM equities (unhedged) – MSCI Emerging Markets Index; TIPS (U.S. Treasury Inflation-Protected Securities) – Barclays U.S. TIPS Index; commodities – Bloomberg Commodity TR Index;

REITs (real estate investment trusts) – Dow Jones U.S. REIT Index; hedge funds – Dow Jones Credit Suisse Hedge Fund Index; Private equity – Cambridge Associates U.S. Private Equity

Index; infrastructure – Macquarie Global Infrastructure Index.

Refer to Appendix for additional forecast, hypothetical example, outlook , and return assumption information.

Fixed Income sectors

1.62.5

1.8

4.5

5.6

4.55.3

7.5

5.3

2.4

5.0

7.3

0123456789

10

Cash U.S. Core

Bonds

Global Bonds

(USD

Hedged)

U.S. High

Yield

EM

Sovereign

Bonds

(Unhedged)

U.S. Equities European

Equities

(USD

Hedged)

EM Equities

(unhedged)

REITs Commodities Hedge

Funds

Private EquityEst

imate

d r

etu

rns

(%)

PIMCO's capital market assumptions* (10 year)

pg 6 Your Global Investment Authority

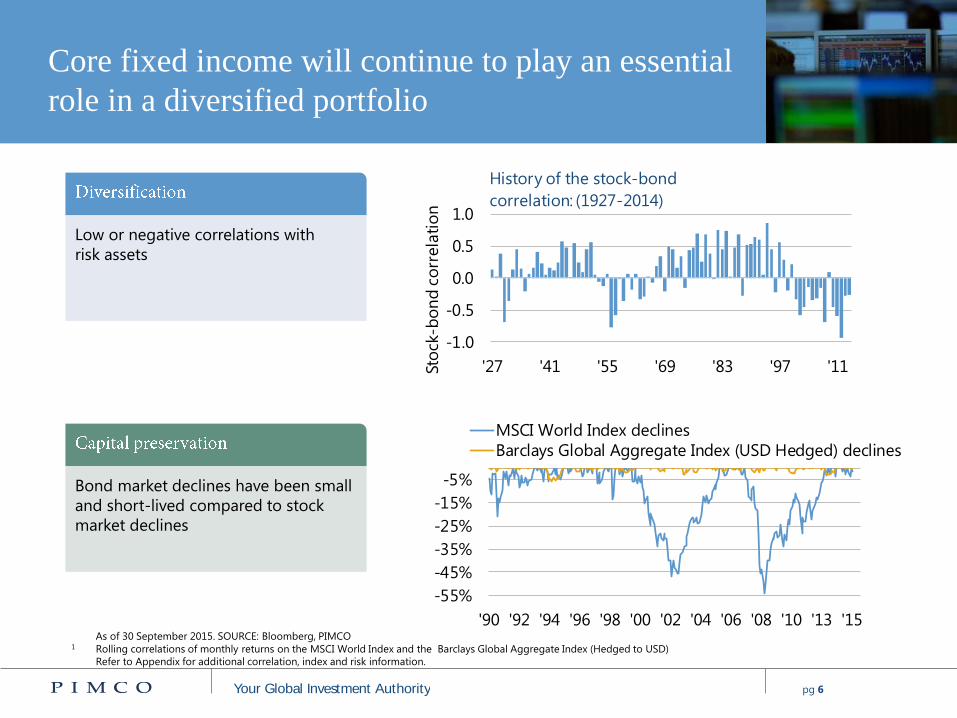

Core fixed income will continue to play an essential

role in a diversified portfolio

As of 30 September 2015. SOURCE: Bloomberg, PIMCO 1 Rolling correlations of monthly returns on the MSCI World Index and the Barclays Global Aggregate Index (Hedged to USD)

Refer to Appendix for additional correlation, index and risk information.

Low or negative correlations with

risk assets

Bond market declines have been small

and short-lived compared to stock

market declines

-1.0

-0.5

0.0

0.5

1.0

'27 '41 '55 '69 '83 '97 '11Sto

ck-b

on

d c

orr

ela

tio

n

History of the stock-bond

correlation: (1927-2014)

-55%

-45%

-35%

-25%

-15%

-5%

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '13 '15

MSCI World Index declines

Barclays Global Aggregate Index (USD Hedged) declines

pg 7 Your Global Investment Authority

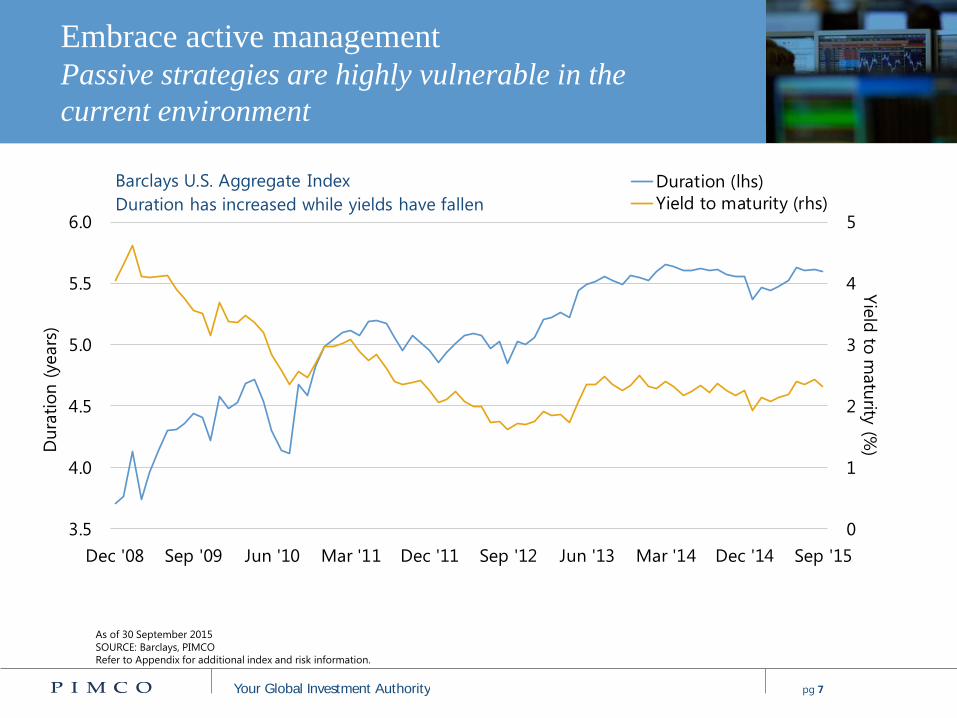

Embrace active management Passive strategies are highly vulnerable in the

current environment

As of 30 September 2015

SOURCE: Barclays, PIMCO

Refer to Appendix for additional index and risk information.

0

1

2

3

4

5

3.5

4.0

4.5

5.0

5.5

6.0

Dec '08 Sep '09 Jun '10 Mar '11 Dec '11 Sep '12 Jun '13 Mar '14 Dec '14 Sep '15

Yie

ld to

matu

rity (%

)Du

rati

on

(years

)

Barclays U.S. Aggregate Index

Duration has increased while yields have fallen

Duration (lhs)

Yield to maturity (rhs)

pg 8 Your Global Investment Authority

The high interest rates of the 70s and 80s, not today’s low yields, were the aberration

Long-term history of sovereign bond yields

0

2

4

6

8

10

12

14

16

1713 1763 1813 1863 1913 1963 2013

Yie

ld (

%)

Three centuries of long-term yields in the U.K.

2014

As of 30 September 2014

SOURCE: Bank of England

pg 9 Your Global Investment Authority

The New Neutral® We expect rates to be lower for longer

2cs_asset_allocation_outlook_01

As of 30 September 2015

Refer to Appendix for additional outlook information.

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Perc

en

t (%

)

U.S. real yield, 5y5y forward U.S. 5Y5Y real yield

"Old Neutral"

"New Neutral"Long-term average real policy rate

New Neutral expected real policy rate

Fair value

range for

5y5y real

yield

pg 10 Your Global Investment Authority

PIMCO’s cyclical outlook

PIMCO forecast as of 22 September 2015

BRIM is Brazil, Russia, India and Mexico

Real GDP and inflation projections reflect the midpoints of PIMCO’s forecasts for the four quarters ending Q3 2016

Refer to Appendix for additional forecast and outlook information.

U.S.

2.50%

2.00%

GDP

Inflation

BRIM

5.50%

2.50% GDP

Inflation

EUROZONE

1.25%

1.75% GDP

Inflation

U.K.

2.50%

1.50%

GDP

Inflation

CHINA

6.00%

2.00%

GDP

Inflation

JAPAN

1.50%

1.25%

GDP

Inflation

3cs_intl_outlook_01c

pg 11 Your Global Investment Authority

Oil prices likely to stabilize in 2016

U.S. production growth is at inflection point; if not for increases in OPEC supply, global

balances would have been much tighter today

OECD demand growth is the strongest in a decade, led by the U.S. and Europe

– China demand growth has also been robust

Swing in OECD demand growth has

boosted the world demand growth

OECD

demand Non-OECD

demand OECD

5y mo. avg.

Non-OECD

5y mo. avg.

3,000

2,500

2,000

1,500

1,000

500

0

-500

-1,000

-1,500

-2,000

-2,500

As of 30 September 2015

SOURCE: EIA, Bloomberg

Barr

els

per

day (

tho

usa

nd

s)

3

4

5

6

7

8

9

10

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Millio

n b

arr

els

per

day

U.S. crude oil production flattening

Total

6-period moving average

pg 12 Your Global Investment Authority

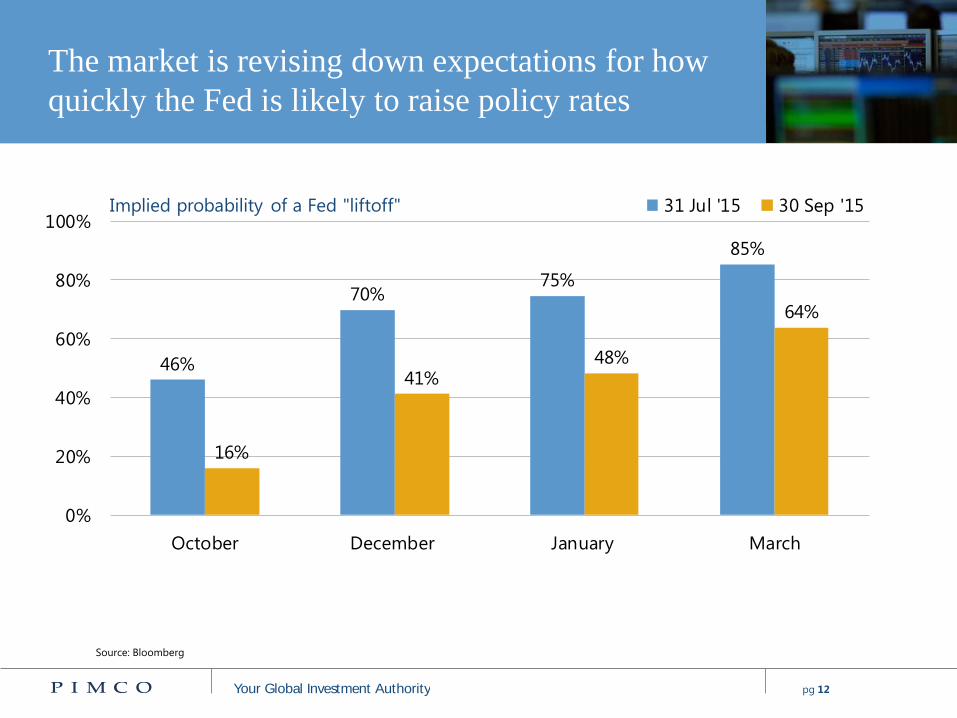

The market is revising down expectations for how

quickly the Fed is likely to raise policy rates

Source: Bloomberg

46%

70%75%

85%

16%

41%48%

64%

0%

20%

40%

60%

80%

100%

October December January March

Implied probability of a Fed "liftoff" 31 Jul '15 30 Sep '15

pg 13 Your Global Investment Authority

U.S. TIPS offer value as high quality alternative

in portfolio

As of 30 September 2015

SOURCE: Bloomberg

BEI: Defined as the difference between the nominal yield on a fixed-rate investment and the real yield (fixed spread) on an inflation-linked investment of similar maturity

and credit quality

3cs_income_review_26

0

2

4

6

8

10

12

'45 '50 '55 '60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '10 '15

Rate

(%

)

Monthly rolling five year inflation

vs. current five year breakeven inflation Five year rolling inflation Five year BEI

(Current 5-year U.S. breakeven inflation 1.1%)

pg 14 Your Global Investment Authority

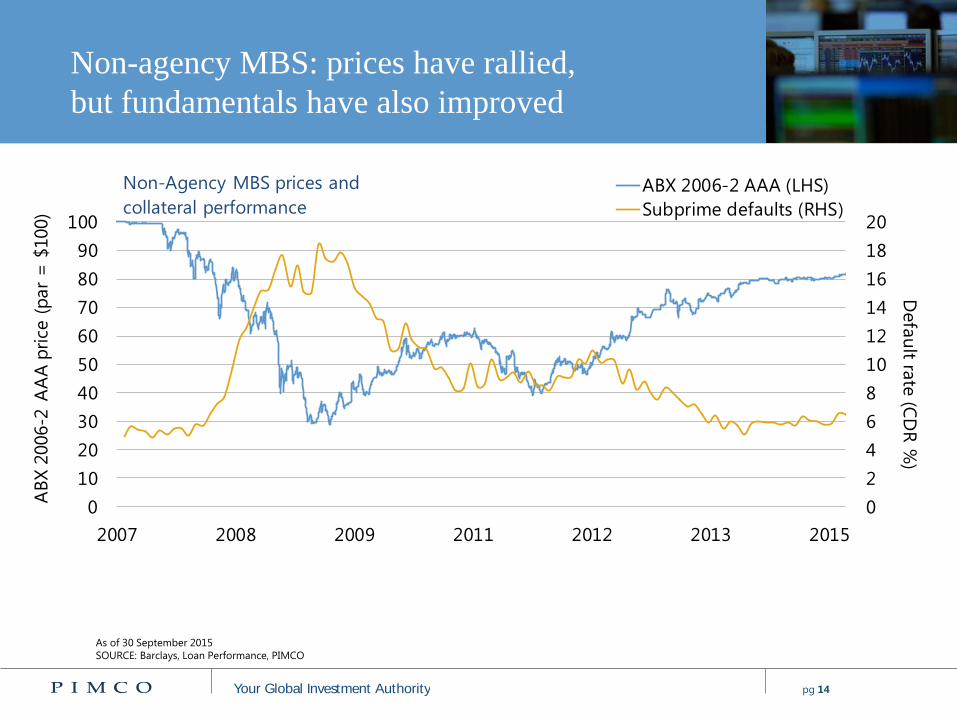

Non-agency MBS: prices have rallied,

but fundamentals have also improved

Copy of income_review_37

As of 30 September 2015

SOURCE: Barclays, Loan Performance, PIMCO

3cs_income_review_23

0

2

4

6

8

10

12

14

16

18

20

0

10

20

30

40

50

60

70

80

90

100

2007 2008 2009 2011 2012 2013 2015

Defa

ult ra

te (C

DR

%)

AB

X 2

006-2

AA

A p

rice (

par

= $

100)

Non-Agency MBS prices and

collateral performance

ABX 2006-2 AAA (LHS)

Subprime defaults (RHS)

pg 15 Your Global Investment Authority

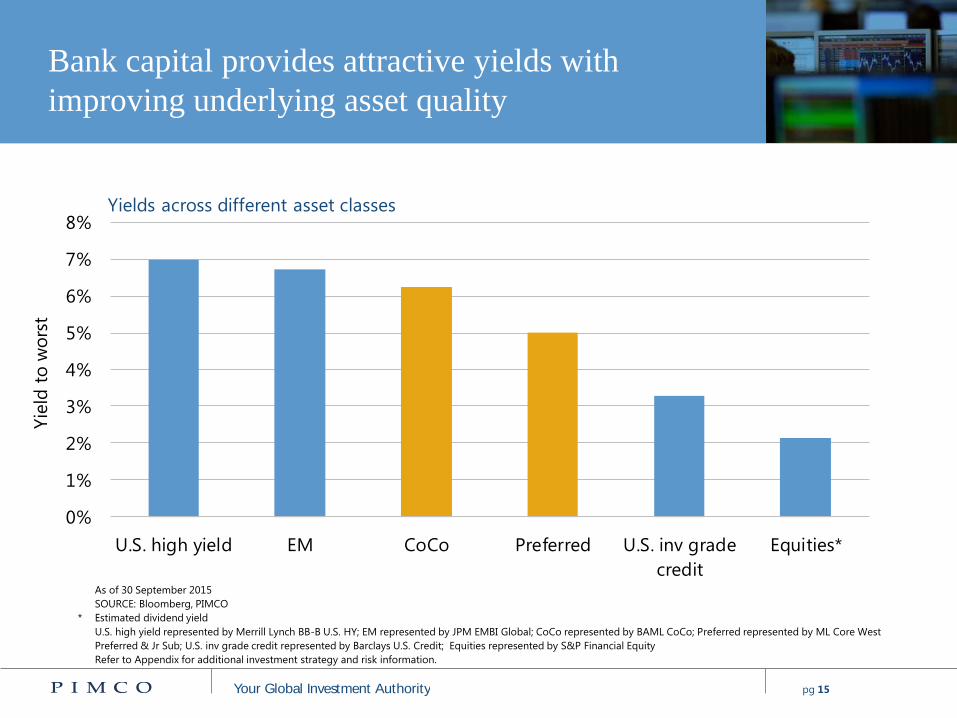

Bank capital provides attractive yields with

improving underlying asset quality

Capital_Securities_Review_11_US

As of 30 September 2015

SOURCE: Bloomberg, PIMCO

* Estimated dividend yield

U.S. high yield represented by Merrill Lynch BB-B U.S. HY; EM represented by JPM EMBI Global; CoCo represented by BAML CoCo; Preferred represented by ML Core West

Preferred & Jr Sub; U.S. inv grade credit represented by Barclays U.S. Credit; Equities represented by S&P Financial Equity

Refer to Appendix for additional investment strategy and risk information.

0%

1%

2%

3%

4%

5%

6%

7%

8%

U.S. high yield EM CoCo Preferred U.S. inv grade

credit

Equities*

Yie

ld t

o w

ors

t

Yields across different asset classes

pg 16 Your Global Investment Authority

Summary

1cs_TR_attrib_01_700

We face a “New Neutral” world defined by lower rates and higher

valuations, which leads to lower prospective returns

Despite low yields, and potentially rising rates, core fixed income retains

an essential role within the context of a multi-asset portfolio

Recent developments across bond markets increases the need for active

management

Investors can still generate attractive risk-adjusted return in the bond

markets by broadening the opportunity set

pg 17 Your Global Investment Authority

Appendix

Past performance is not a guarantee or a reliable indicator of future results.

CORRELATION

The correlation of various indexes or securities against one another or against inflation is based upon data over a certain time period. These correlations may vary substantially

in the future or over different time periods that can result in greater volatility.

CREDIT QUALITY

The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio.

FORECAST

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of

any particular security, strategy or investment product. There is no guarantee that results will be achieved.

HYPOTHETICAL EXAMPLE

No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Hypothetical or simulated

performance results have several inherent limitations. Unlike an actual performance record, simulated results do not represent actual performance and are generally prepared

with the benefit of hindsight. There are frequently sharp differences between simulated performance results and the actual results subsequently achieved by any particular

account, product, or strategy. In addition, since trades have not actually been executed, simulated results cannot account for the impact of certain market risks such as lack of

liquidity. There are numerous other factors related to the markets in general or the implementation of any specific investment strategy, which cannot be fully accounted for in

the preparation of simulated results and all of which can adversely affect actual results.

INVESTMENT STRATEGY

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to

invest long-term, especially during periods of downturn in the market. No representation is being made that any account, product, or strategy will or is likely to achieve profits,

losses, or results similar to those shown.

OUTLOOK

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment

strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during

periods of downturn in the market. Outlook and strategies are subject to change without notice.

RETURN ASSUMPTION

Return assumptions are for illustrative purposes only and are not a prediction or a projection of return. Return assumption is an estimate of what investments may earn on

average over the long term. Actual returns may be higher or lower than those shown and may vary substantially over shorter time periods.

asset_allocation_appendix

pg 18 Your Global Investment Authority

Appendix

RISK

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are

impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices

generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased

market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and

perceived general market, economic and industry conditions. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk,

and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Investing in foreign-

denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging

markets. Inflation-linked bonds (ILBs) issued by the various governments around the world are fixed-income securities whose principal value is periodically adjusted according to

the rate of inflation. Repayment upon maturity of the original principal as adjusted for inflation is guaranteed by the government that issues them. Neither the current market value

of inflation-indexed bonds nor the value a portfolio that invests in ILBs is guaranteed, and either or both may fluctuate. ILBs decline in value when real interest rates rise. In certain

interest rate environments, such as when real interest rates are rising faster than nominal interest rates, ILBs may experience greater losses than other fixed income securities with

similar durations. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Currency rates may

fluctuate significantly over short periods of time and may reduce the returns of a portfolio. All investments contain risk and may lose value.

This material contains the current opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only

and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained

from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written

permission. Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660, 800.387.4626. ©2015, PIMCO.

It is not possible to invest directly in an unmanaged index.

Going Beyond Beta in Bonds: The Need for Active

Management Q&A

Thank You