Embed Size (px)

Citation preview

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 1/12

Gold as a sourceof collateral

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 2/12

Contents

Introduction 01

How gold measures up as collateral 05

A case study: ICE Clear Europe 08

About the World Gold Council

The World Gold Council is the market development organisation

for the gold industry. Working within the investment, jewellery

and technology sectors, as well as engaging in government affairs,

our purpose is to provide industry leadership, whilst stimulating

and sustaining demand for gold.

We develop gold-backed solutions, services and markets,

based on true market insight. As a result, we create structural

shifts in demand for gold across key market sectors.

We provide insights into the international gold markets,

helping people to better understand the wealth preservation

qualities of gold and its role in meeting the social and

environmental needs of society.

Based in the UK, with operations in India, the Far East , Turkey,

Europe and the USA, the World Gold Council is an association

whose members include the world’s leading and most forward

thinking gold mining companies.

For more information

Please contact Government Affairs:

Ashish Bhatia

+1 212 317 3850

Natalie Dempster

Director, Government Affairs

[email protected]+44 20 7826 4707

Gold as a source of collateral

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 3/12

Introduction

The 2007-2009 financial crisis highlighted inadequacies

in counterparty risk management in the global over-the-counter (OTC) market. G20 leaders have committed toaddress this by implementing regulatory reforms that willaugment the use of central counterparty (CCP) clearing.This will in turn increase demand for the collateral assetsthat need to be posted with CCPs.

In order to give clearing members as much flexibility as

possible, CCPs have begun searching for appropriate newsources of collateral. This has become a particular focusas the credit quality of many traditional collateral assets,such as European government bonds, has deterioratedsharply as a result of the ongoing sovereign debt crisis.

Gold is emerging as a solution. Its lack of credit risk

and countercyclical behaviour make it an ideal sourceof collateral for CCPs, while their members benefit frombeing able to use their gold holdings more effi ciently.

This report investigates this nascent use for gold andexamines the unique characteristics of gold which makeit an ideal form of collateral.

In addition, Paul Swann, President of ICE Clear Europe,one of Europe’s largest derivatives clearing houses, talksabout ICE’s decision to start accepting gold as collateralin late 2010 and the benefits that gold can bring to a CCP.

01

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 4/12

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 5/12

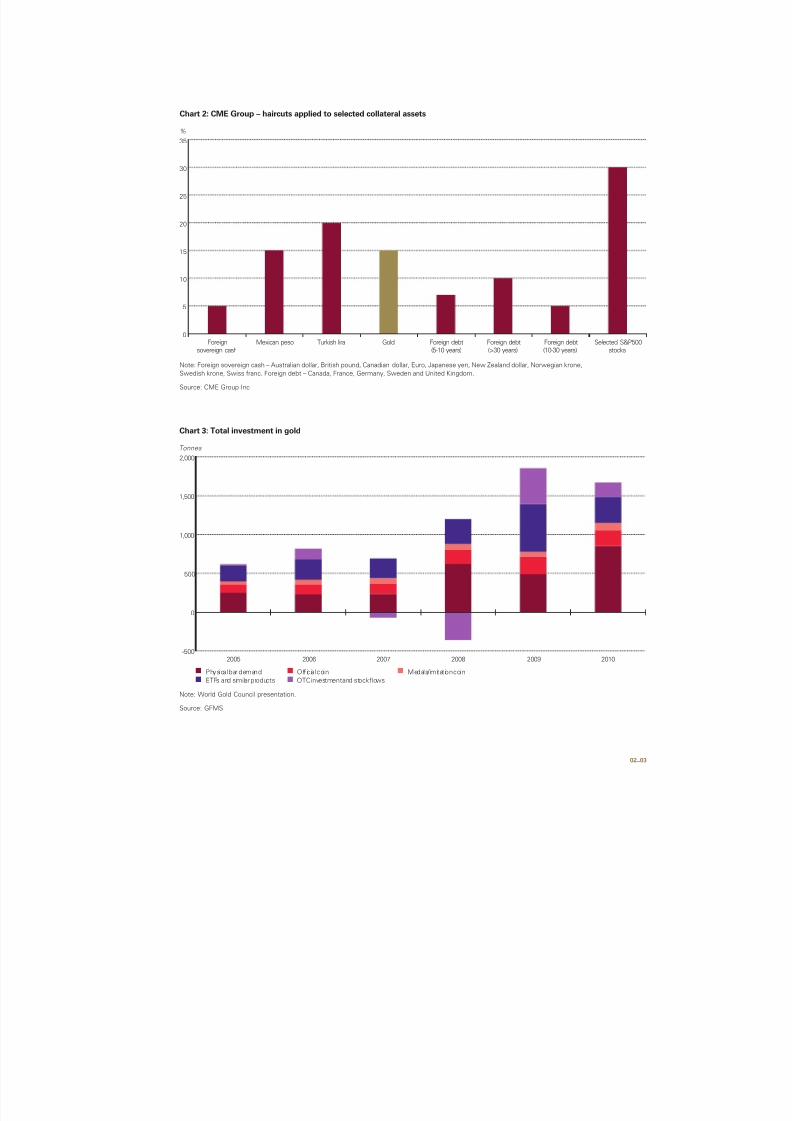

Chart 2: CME Group – haircuts applied to selected collateral assets

Note: Foreign sovereign cash – Australian dollar, British pound, Canadian dollar, Euro, Japanese yen, New Zealand dollar, Norwegian krone,

Swedish krone, Swiss franc. Foreign debt – Canada, France, Germany, Sweden and United Kingdom.

Source: CME Group Inc

0

15

5

10

30

35

25

20

%

Mexican pesoForeign

sovereign cash

Turkish lira Gold Foreign debt

(5-10 years)

Foreign debt

(>30 years)

Foreign debt

(10-30 years)

Selected S&P500

stocks

Chart 3: Total investment in gold

Note: World Gold Council presentation.

Source: GFMS

-500

1,000

0

500

2,000

1,500

Tonnes

20062005 2007 2008 2009 2010

Physical bar demand Official coin Medals/ imitation coin

ETFs and similar products OTC investment and stock flows

02_03

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 6/12

Now, as gold has become acknowledged as a collateral type,

the fund manager can use gold to meet part of his collateral

requirement. In this situation, the fund places the US$100 million

gold position as collateral, which after a 12 percent haircut

funds all but US$12 million of the gold position. The remaining

US$12 million is funded at the same market rate as the

prior example of 100 basis points for a cost of US$120,000.

This represents an actual cash savings of US$880,000 an

implied yield of 0.88 percent on the US$100 million gold position.

The implied yield can be written as:

Implied yield = (1-Gh)*R

Where:

Gh – Gold’s haircut

R – Cash borrowing rate

(Note that for simplicity we assume unchanged vaulting costs

and no limit on gold being applied for initial margin.)

And with most yield curves signalling sharply higher interest

rates in the near future, the savings from using an existing gold

position instead of cash as collateral should increase sharply in

the coming years. Using gold can also help to expand a company’s

balance sheet if gold has a lower haircut than the other assets

currently being used as collateral.

What makes eff ective collateral?

Central Counterparties Clearinghouses (CCPs) are subject

to credit and market risk. Credit risk stems from the CCPsrole as counterparty to both the buyer and seller. The market

risk stems from the CCP’s exposure to the market related

fluctuations in assets that are serving as collateral against

the buyer and seller’s financial exposure.

Collateral assets should have minimal credit and market risk.

They should be easy to value on a continuous basis, allowing

CCPs to calculate realistic haircuts. The assets should be

easy to trade, ideally supported by committed market markers

continuously quoting a two-way price. The market should also

be sufficiently deep and liquid – ideally with a diverse demand

base – that the asset can be readily sold if needed without

resulting in a larger “haircut” than factored into the CCPs

risk calculations.

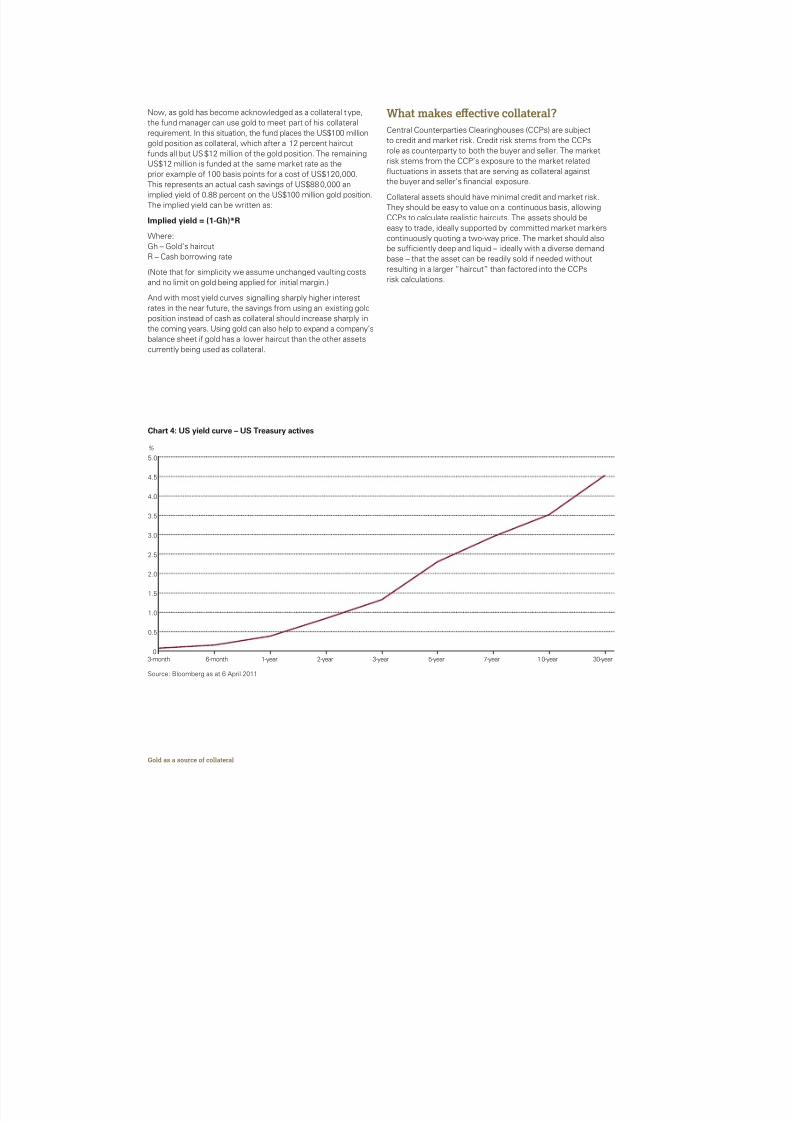

Chart 4: US yield curve – US Treasury actives

Source: Bloomberg as at 6 April 2011

0

2.5

1.5

0.5

1.0

3.0

2.0

4.5

5.0

4.0

3.5

%

3-month 6-month 1-year 2-year 3-year 5-year 7-year 10-year 30-year

Gold as a source of collateral

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 7/12

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 8/12

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 9/12

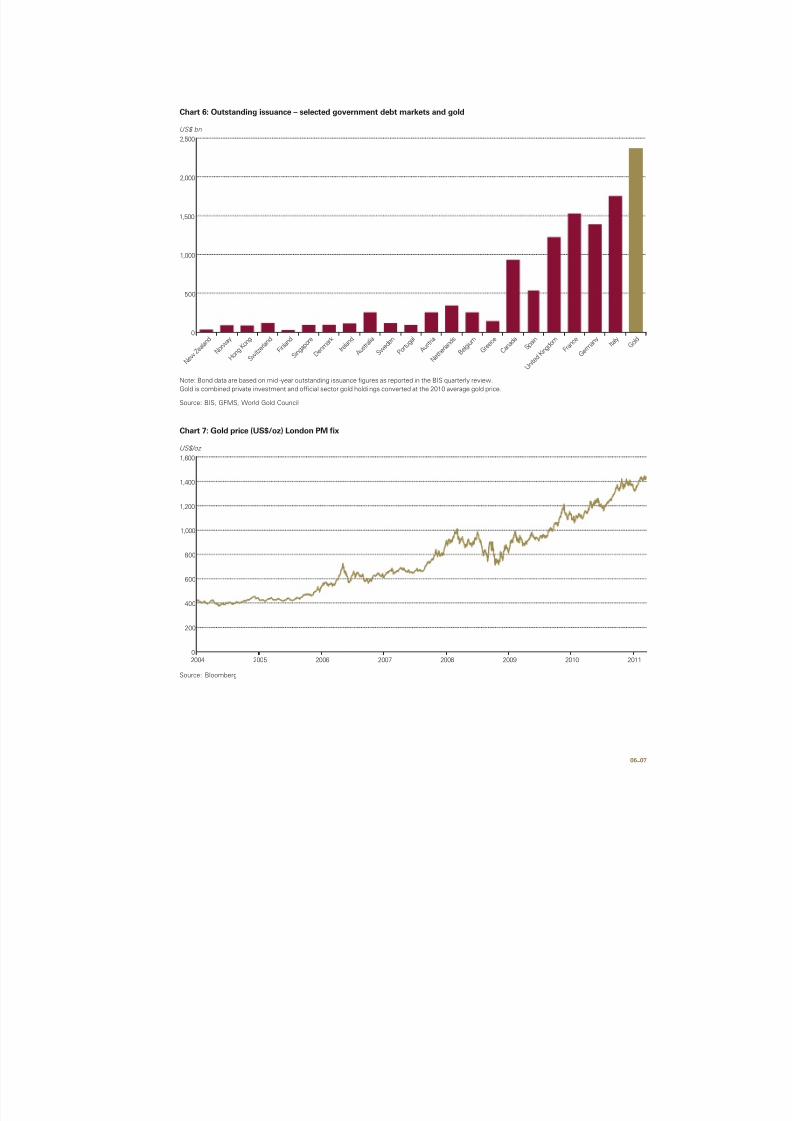

Chart 6: Outstanding issuance – selected government debt markets and gold

Note: Bond data are based on mid -year outstanding issuance figures as reported in the BIS quarterly review.

Gold is combined private investment and official sector gold holdi ngs converted at the 2010 average gold price.

Source: BIS, GFMS, World Gold Council

0

1,000

500

2,500

2,000

1,500

US$ bn

N e w

Z e a l a n

d

H o n g

K o n g

N o r w a y

S w i t z

e r l a n

d

F i n l a n

d

S i n g a p o r e

D e n m

a r k

I r e l a n

d

A u s t r a l i a

S w e d e n

P o r t u

g a l

N e t h e r l a n

d s

A u s t r i a

B e l g i

u m

G r e e c e

S p a i n

U n i t e

d K i n g d o m

C a n a d a

F r a n c e

G e r m

a n y

I t a l y

G o l d

Chart 7: Gold price (US$/oz) London PM fix

Source: Bloomberg

0

1,000

600

800

400

200

1,600

1,400

1,200

US$/oz

2004 2005 2006 2007 2008 2009 2010 2011

06_07

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 10/12

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 11/12

8/9/2019 Gold as Collateral

http://slidepdf.com/reader/full/gold-as-collateral 12/12

Published: April 2011

World Gold Council

10 Old Bailey, London EC4M 7NGUnited Kingdom

T +44 20 7826 4700F +44 20 7826 4799W www.gold.org

Published: May 2011

World Gold Council

10 Old Bailey, London EC4M 7NGUnited Kingdom

T +44 20 7826 4700F +44 20 7826 4799W www.gold.org