Embed Size (px)

Citation preview

Goods & Service Tax Compliance

Ready Reckoner

UltraTech Cement Limited

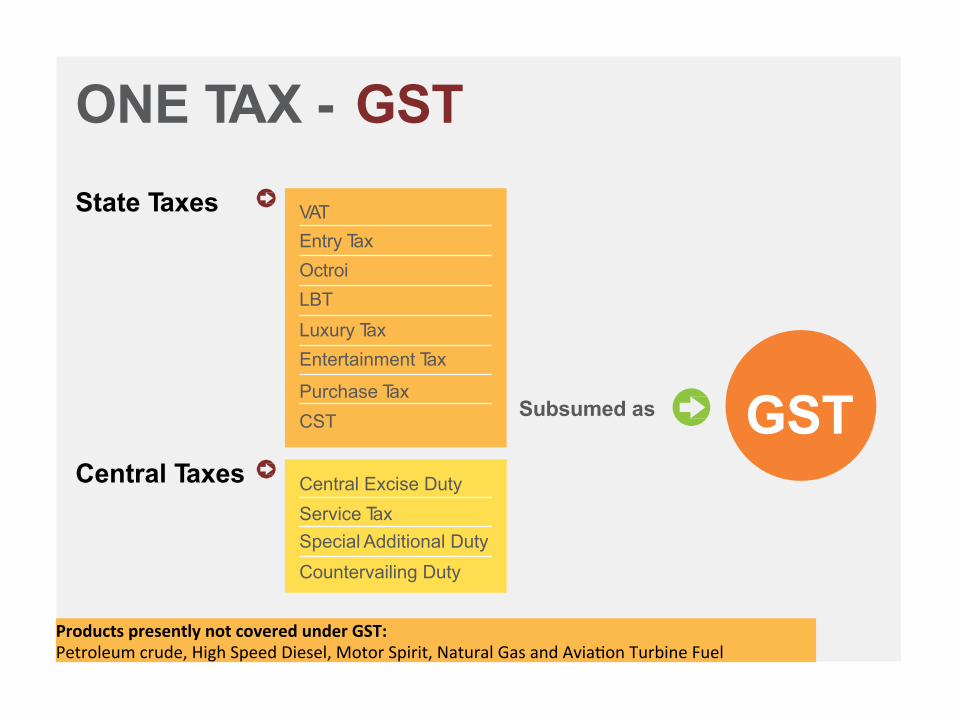

ONE TAX - GST

State Taxes

Subsumed as GST

VAT Entry Tax Octroi LBT Luxury Tax Entertainment Tax

Purchase Tax CST

Central Excise Duty Service Tax Special Additional Duty Countervailing Duty

Central Taxes

ProductspresentlynotcoveredunderGST:Petroleumcrude,HighSpeedDiesel,MotorSpirit,NaturalGasandAvia<onTurbineFuel

DUAL GST SGST/UTGST – State GST/Union Territory GST CGST – Central GST IGST – Integrated GST

Note:

Supplies to include sales, Inter State Stock transfer. No need of C Form for interstate sales. No need of F Forms for interstate stock transfer.

CGST

IGST

SGST/ UTGST

Supplies within the same state - CGST+SGST Supplies within same Union Territory – CGST+UTGST

Supplies between two states/Union Territories/State & UT - IGST

REGISTRATION CRITERIA

Liable for GST if Aggregate Turnover in a Financial Year

Exceeds

RS 20 LACS*

Aggregate Turnover includes All Supplies i.e. exempt supplies, export of goods, Inter state supplies by Taxable Person + Supplies by Registered Job Worker after completion of Job Work but excludes Tax & Cess under GST Law on all India basis. Registration for existing & new application are open from 25th June 2017, ensure to submit your application and get your GST registration number. An Unregistered Dealer will not be able to sell outside state *Rs.10 lacs for Special States: Jammu & Kashmir, Himachal Pradesh, Uttrakhand, Arunachal Pradesh, Assam, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura and Manipur.

COMPOSITE REGISTRATION

Can opt for Composite

Registration if Aggregate Turnover in a Financial Year

is Up to

RS 75 LACS*

Cannot take Input Tax Credit. Cannot collect Tax T o issue “Bill of Supply” with declaration that registered under Composition Scheme GST of 1% on Turnover to be paid (Cannot be collected)

*Rs. 50 lacs in case of Special States

Meant for small Retailer selling to End Consumer – SIMPLER, EASIER

Dealer under composition scheme cannot make sale outside the state.

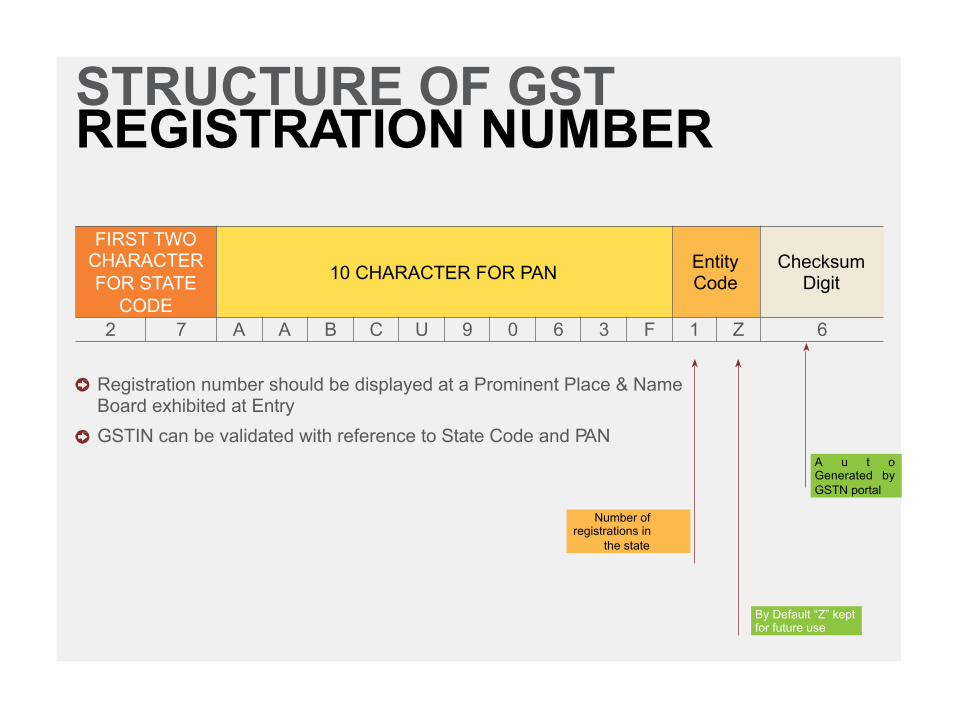

STRUCTURE OF GST REGISTRATION NUMBER

Registration number should be displayed at a Prominent Place & Name Board exhibited at Entry GSTIN can be validated with reference to State Code and PAN

Number of registrations in

the state

By Default “Z” kept for future use

FIRST TWO CHARACTER FOR STATE

CODE

10 CHARACTER FOR PAN Entity Code

Checksum Digit

2 7 A A B C U 9 0 6 3 F 1 Z 6

A u t o Generated by GSTN portal

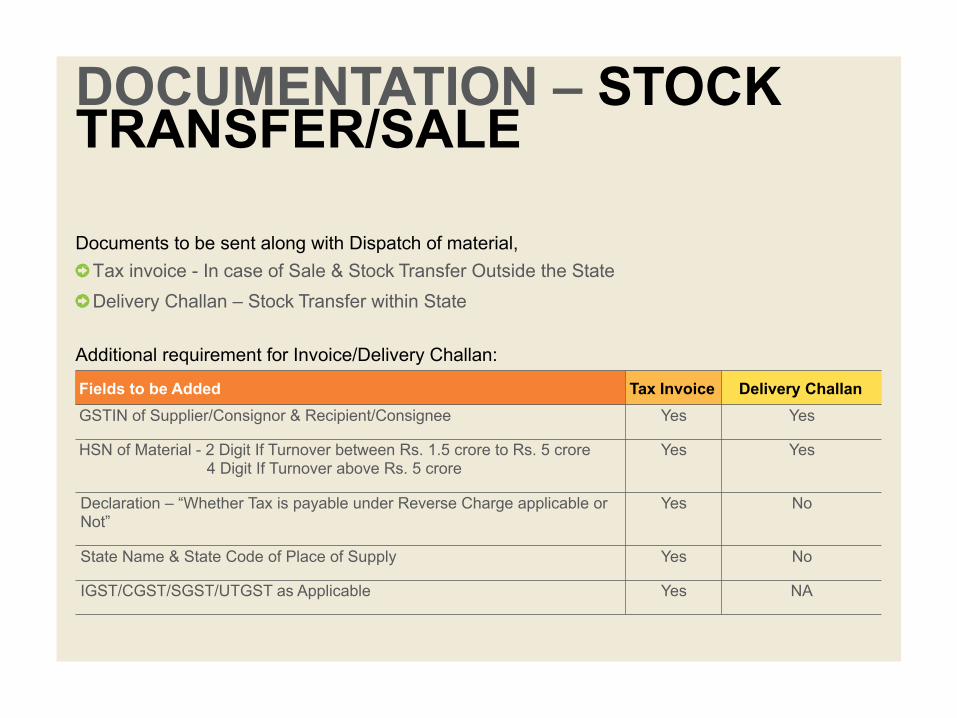

DOCUMENTATION – STOCK TRANSFER/SALE

Documents to be sent along with Dispatch of material, T ax invoice - In case of Sale & Stock Transfer Outside the State Delivery Challan – Stock Transfer within State

Additional requirement for Invoice/Delivery Challan:

Fields to be Added Tax Invoice Delivery Challan

GSTIN of Supplier/Consignor & Recipient/Consignee Yes Yes

HSN of Material - 2 Digit If Turnover between Rs. 1.5 crore to Rs. 5 crore 4 Digit If Turnover above Rs. 5 crore

Yes Yes

Declaration – “Whether Tax is payable under Reverse Charge applicable or Not”

Yes No

State Name & State Code of Place of Supply Yes No

IGST/CGST/SGST/UTGST as Applicable Yes NA

GST RATES

* SGST is 50% and CGST is 50% of Total GST Rate

Product GST Rate*

Grey Cement (All Grades) 28%

Birla White Products and Wall Care Putty 28%

Ready Mix Concrete 18%

Aggregate/Metal 5%

Crush Sand/Manufactured Sand 5%

Paints 28%

PVC Pipes 18%

Transportation ( On Reverse Charge ) 5%

Steel 18%

SAMPLE GST IMPACT ON BILLING

Particulars Current Tax Regime (Rs. Per Bag)

GST Regime (Rs. Per Bag)

Company Billing to Dealer Basic Price 290.00 290.00 Excise 41.25 VAT @ 14.5% 48.03 CGST @ 14% 40.60 SGST @ 14% 40.60 Total Billing to Dealer 379.28 371.20 Dealer Billing to Retailer Total Billing from Company 379.28 371.20 Less: Input Tax Credit 48.03 81.20 Landed Cost to the Dealer 331.25 290.00 Value addition of Dealer 5.00 5.00 Basic Price of Dealer 336.25 295.00 VAT / GST ( CGST + SGST) 48.76 82.60 Total Billing Price to Retailer 385.01 377.60

Retailer Billing to Consumer Total Billing from Dealer 385.01 377.60 Less: Input Tax Credit 48.76 82.60 Landed Cost to Retailer 336.25 295.00 Value addition of Retailer 5.00 5.00 Basic Price of Retailer Billing 341.25 300.00 VAT / GST ( CGST + SGST) 49.48 84.00 Landed Cost to Consumer 390.73 384.00

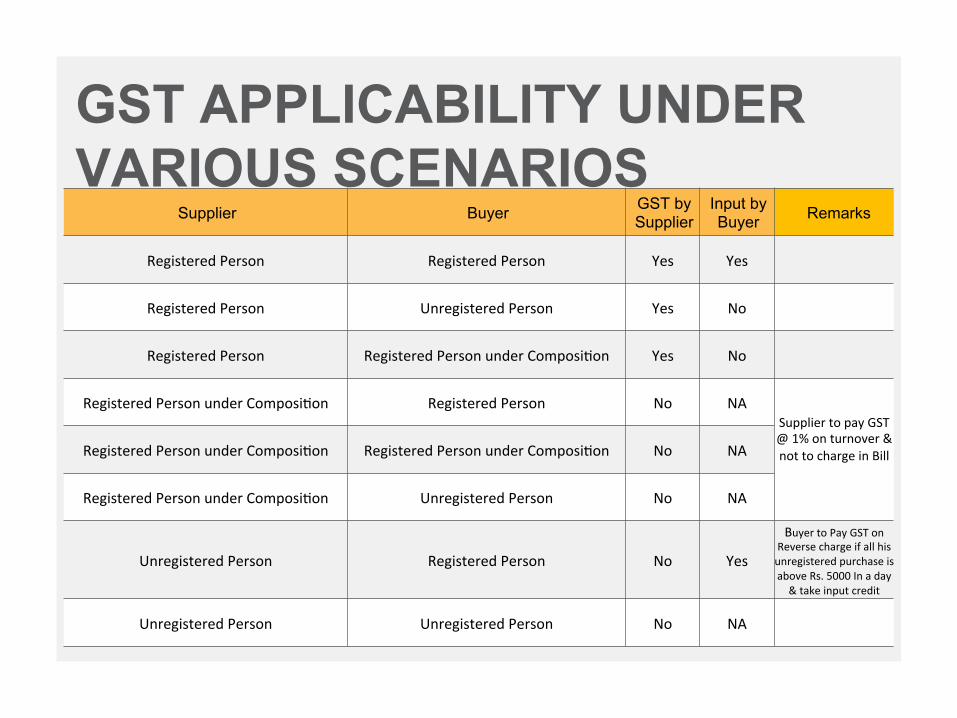

GST APPLICABILITY UNDER VARIOUS SCENARIOS

Supplier Buyer GST by Supplier

Input by Buyer Remarks

RegisteredPerson RegisteredPerson Yes Yes

RegisteredPerson UnregisteredPerson Yes No

RegisteredPerson RegisteredPersonunderComposi<on Yes No

RegisteredPersonunderComposi<on RegisteredPerson No NASuppliertopayGST@1%onturnover¬tochargeinBill

RegisteredPersonunderComposi<on RegisteredPersonunderComposi<on No NA

RegisteredPersonunderComposi<on UnregisteredPerson No NA

UnregisteredPerson RegisteredPerson No Yes

BuyertoPayGSTonReversechargeifallhisunregisteredpurchaseisaboveRs.5000Inaday&takeinputcredit

UnregisteredPerson UnregisteredPerson No NA

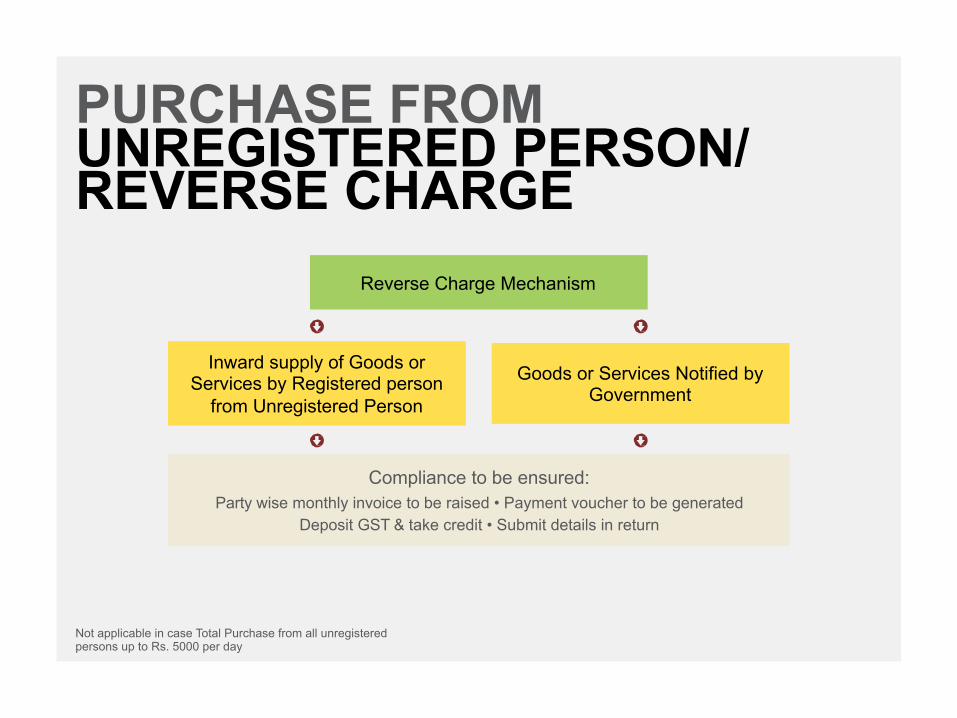

PURCHASE FROM UNREGISTERED PERSON/ REVERSE CHARGE

Not applicable in case Total Purchase from all unregistered persons up to Rs. 5000 per day

Compliance to be ensured: Party wise monthly invoice to be raised • Payment voucher to be generated

Deposit GST & take credit • Submit details in return

Inward supply of Goods or Services by Registered person

from Unregistered Person

Goods or Services Notified by Government

Reverse Charge Mechanism

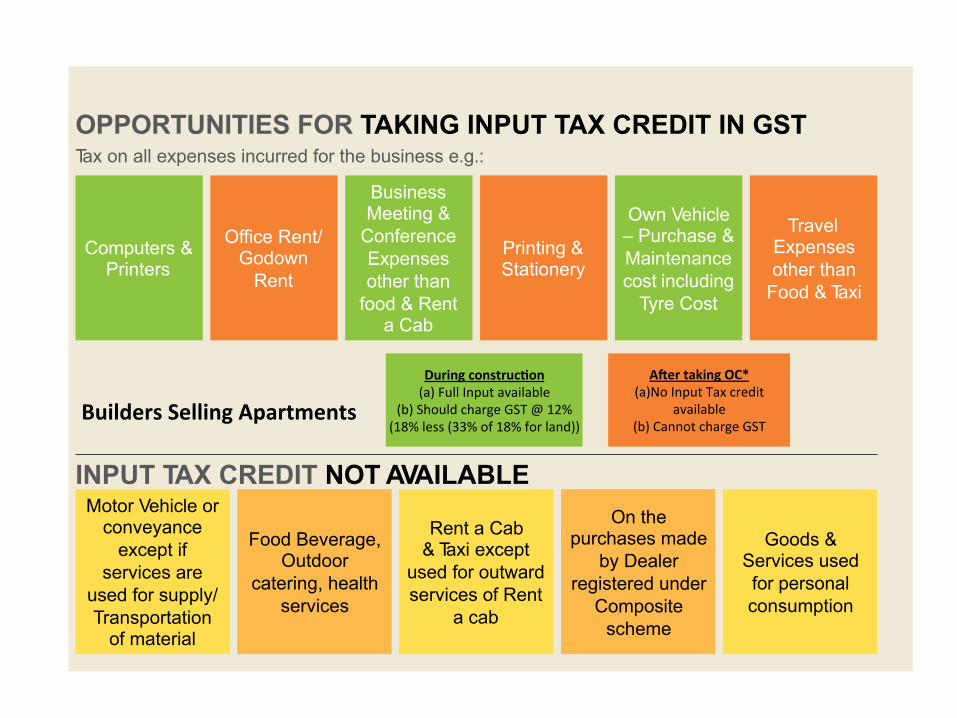

OPPORTUNITIES FOR TAKING INPUT TAX CREDIT IN GST

INPUT TAX CREDIT NOT AVAILABLE

Tax on all expenses incurred for the business e.g.:

Computers & Printers

Motor Vehicle or conveyance

except if services are

used for supply/ Transportation

of material

Food Beverage, Outdoor

catering, health services

Rent a Cab & Taxi except

used for outward services of Rent

a cab

On the purchases made

by Dealer registered under

Composite scheme

Goods & Services used for personal consumption

Office Rent/ Godown

Rent

Business Meeting &

Conference Expenses other than

food & Rent a Cab

Printing & Stationery

Own Vehicle – Purchase & Maintenance cost including

Tyre Cost

Travel Expenses other than

Food & Taxi

Duringconstruc7on(a)FullInputavailable

(b)ShouldchargeGST@12%(18%less(33%of18%forland))

A9ertakingOC*

(a)NoInputTaxcreditavailable

(b)CannotchargeGST

BuildersSellingApartments

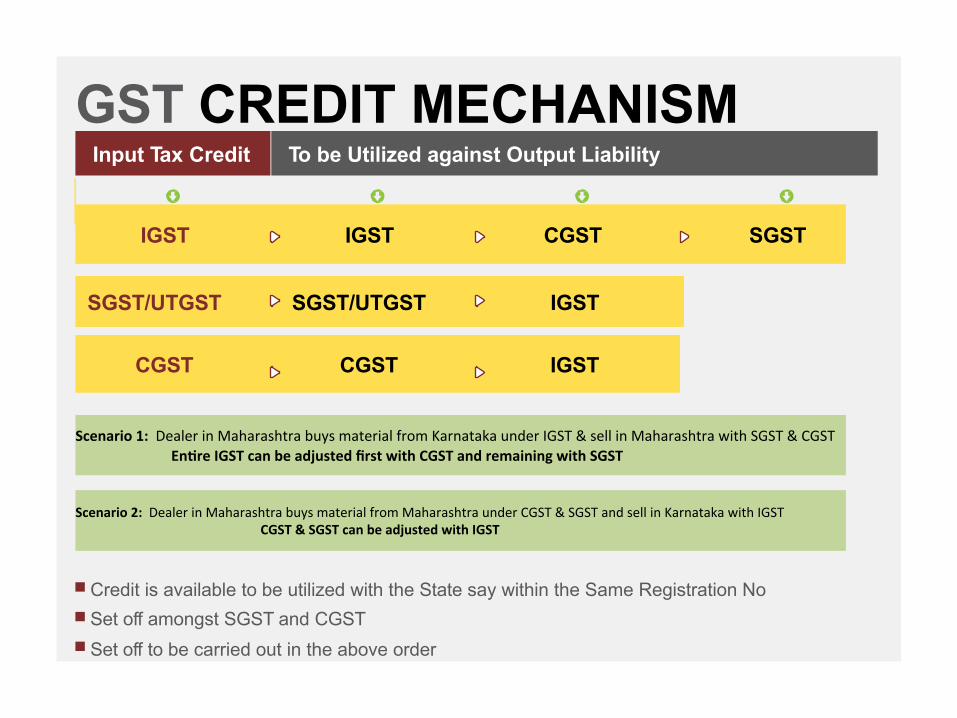

GST CREDIT MECHANISM

Credit is available to be utilized with the State say within the Same Registration No Set off amongst SGST and CGST Set off to be carried out in the above order

IGST IGST CGST SGST

SGST/UTGST SGST/UTGST IGST

CGST CGST IGST

Input Tax Credit To be Utilized against Output Liability

Scenario1:DealerinMaharashtrabuysmaterialfromKarnatakaunderIGST&sellinMaharashtrawithSGST&CGST

En7reIGSTcanbeadjustedfirstwithCGSTandremainingwithSGST

Scenario2:DealerinMaharashtrabuysmaterialfromMaharashtraunderCGST&SGSTandsellinKarnatakawithIGST

CGST&SGSTcanbeadjustedwithIGST

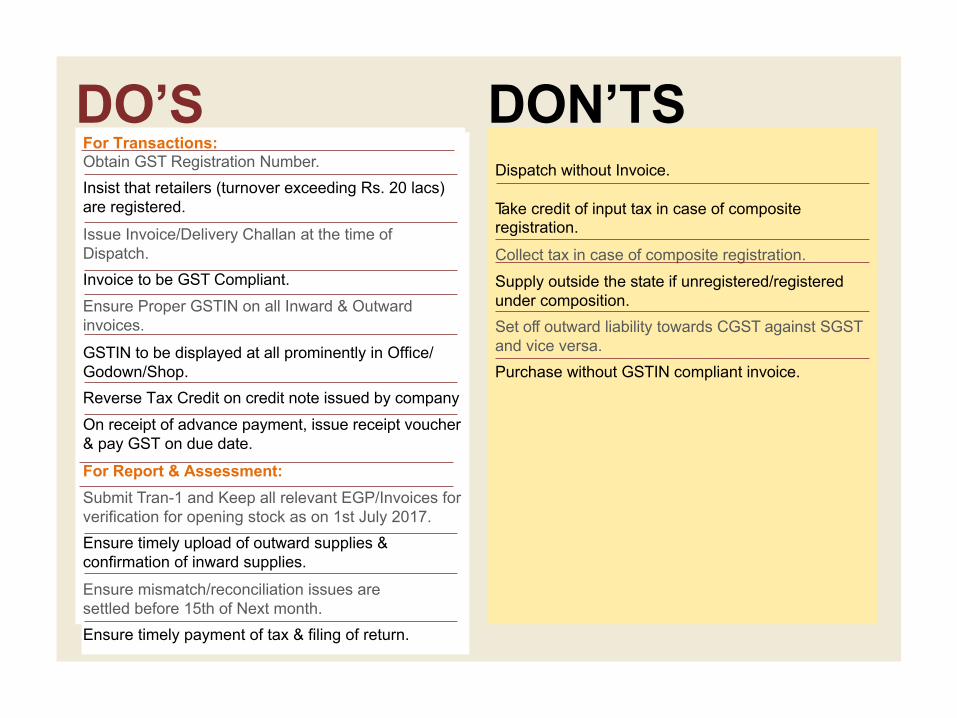

DO’S For Transactions: Obtain GST Registration Number. Insist that retailers (turnover exceeding Rs. 20 lacs) are registered.

Issue Invoice/Delivery Challan at the time of Dispatch. Invoice to be GST Compliant.

Ensure Proper GSTIN on all Inward & Outward invoices.

GSTIN to be displayed at all prominently in Office/Godown/Shop. Reverse Tax Credit on credit note issued by company

On receipt of advance payment, issue receipt voucher & pay GST on due date.

For Report & Assessment: Submit Tran-1 and Keep all relevant EGP/Invoices for verification for opening stock as on 1st July 2017. Ensure timely upload of outward supplies & confirmation of inward supplies.

Ensure mismatch/reconciliation issues are settled before 15th of Next month. Ensure timely payment of tax & filing of return.

DON’TS Dispatch without Invoice. Take credit of input tax in case of composite registration.

Collect tax in case of composite registration.

Supply outside the state if unregistered/registered under composition. Set off outward liability towards CGST against SGST and vice versa. Purchase without GSTIN compliant invoice.

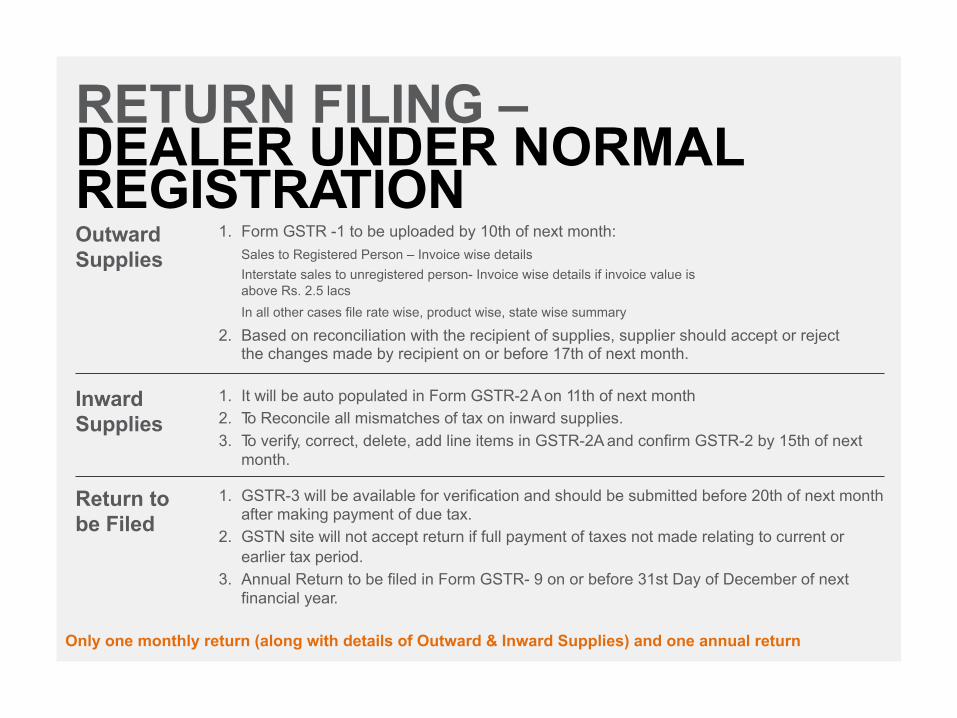

RETURN FILING – DEALER UNDER NORMAL REGISTRATION

Only one monthly return (along with details of Outward & Inward Supplies) and one annual return

Outward Supplies

Inward Supplies

Return to be Filed

1. Form GSTR -1 to be uploaded by 10th of next month: Sales to Registered Person – Invoice wise details Interstate sales to unregistered person- Invoice wise details if invoice value is above Rs. 2.5 lacs In all other cases file rate wise, product wise, state wise summary

2. Based on reconciliation with the recipient of supplies, supplier should accept or reject the changes made by recipient on or before 17th of next month.

1. It will be auto populated in Form GSTR-2 A on 11th of next month 2. To Reconcile all mismatches of tax on inward supplies. 3. To verify, correct, delete, add line items in GSTR-2A and confirm GSTR-2 by 15th of next

month.

1. GSTR-3 will be available for verification and should be submitted before 20th of next month after making payment of due tax.

2. GSTN site will not accept return if full payment of taxes not made relating to current or earlier tax period.

3. Annual Return to be filed in Form GSTR- 9 on or before 31st Day of December of next financial year.

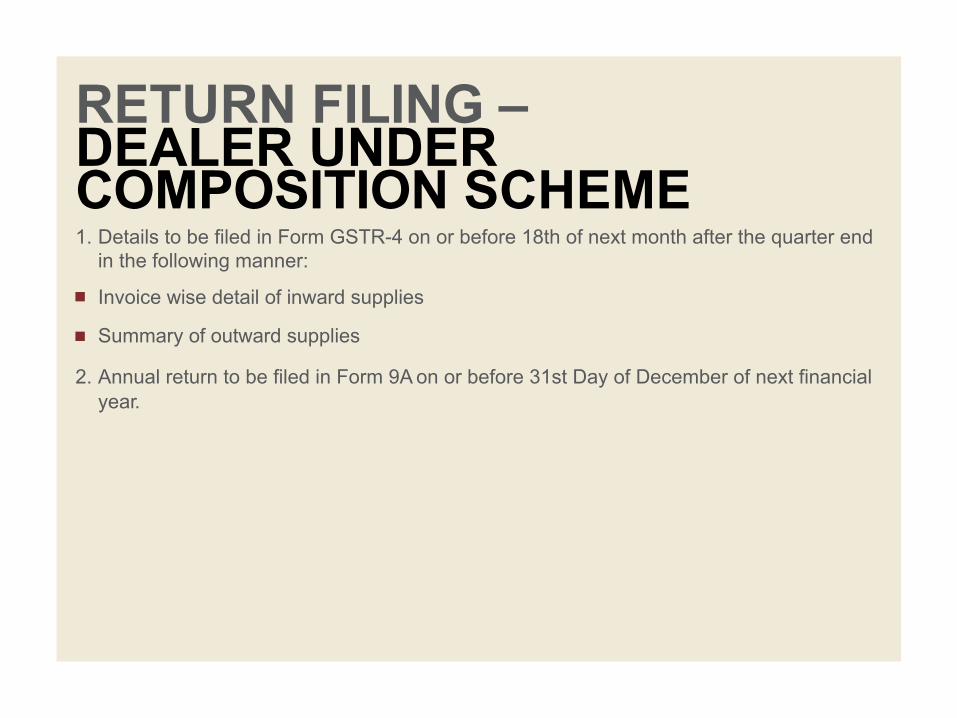

RETURN FILING – DEALER UNDER COMPOSITION SCHEME 1. Details to be filed in Form GSTR-4 on or before 18th of next month after the quarter end

in the following manner:

Invoice wise detail of inward supplies

Summary of outward supplies

2. Annual return to be filed in Form 9A on or before 31st Day of December of next financial year.

RESOURCE FOR GST READINESS

1. UltraTech has tied up with “Tally” for a special price for UltraTech Business Partners/Associates.

2. It will serve the purpose of Accounting software along with ASP/GSP.

3. If you want to take Tally Software you can click on the web link https://goo.gl/forms/xGotSdtyYxQYI2UE3

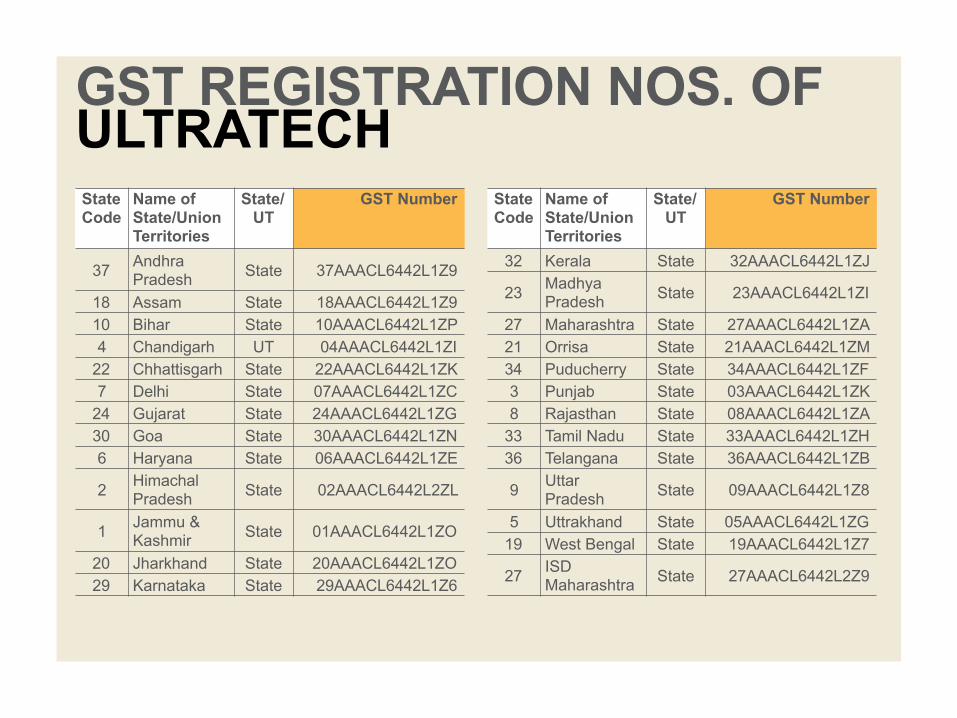

GST REGISTRATION NOS. OF ULTRATECH State Code

Name of State/Union Territories

State/ UT

GST Number

37 Andhra Pradesh State 37AAACL6442L1Z9

18 Assam State 18AAACL6442L1Z9 10 Bihar State 10AAACL6442L1ZP 4 Chandigarh UT 04AAACL6442L1ZI

22 Chhattisgarh State 22AAACL6442L1ZK 7 Delhi State 07AAACL6442L1ZC

24 Gujarat State 24AAACL6442L1ZG 30 Goa State 30AAACL6442L1ZN 6 Haryana State 06AAACL6442L1ZE

2 Himachal Pradesh State 02AAACL6442L2ZL

1 Jammu & Kashmir State 01AAACL6442L1ZO

20 Jharkhand State 20AAACL6442L1ZO 29 Karnataka State 29AAACL6442L1Z6

State Code

Name of State/Union Territories

State/ UT

GST Number

32 Kerala State 32AAACL6442L1ZJ

23 Madhya Pradesh State 23AAACL6442L1ZI

27 Maharashtra State 27AAACL6442L1ZA 21 Orrisa State 21AAACL6442L1ZM 34 Puducherry State 34AAACL6442L1ZF 3 Punjab State 03AAACL6442L1ZK 8 Rajasthan State 08AAACL6442L1ZA

33 Tamil Nadu State 33AAACL6442L1ZH 36 Telangana State 36AAACL6442L1ZB

9 Uttar Pradesh State 09AAACL6442L1Z8

5 Uttrakhand State 05AAACL6442L1ZG 19 West Bengal State 19AAACL6442L1Z7

27 ISD Maharashtra State 27AAACL6442L2Z9

GST AWARENESS SESSIONS 9000+ Business Partners already attended

94 GST Awareness Sessions across country

UltraTech has already changed the price structure and passed on the GST benefit to its

customers

DISCLAIMER The contents shared in this presentation are for awareness & knowledge sharing purposes and based on CGST & IGST Act and Rules, as available in public domain. Same needs to be revisited for amendments, if any, in future. The comments are indicative in nature and based on interpretation of existing CGST & IGST Act and rules, which could be subject to change. UltraTech shall not be liable for any direct or indirect loss from the use of the content shared in this presentation.

THANK YOU

UltraTech Cement Limited