Embed Size (px)

Citation preview

Government of India Ministry of Finance

Department of Financial Services

Report of the Key Advisory Group on the Non-Banking Finance Companies

(NBFCs)

31st January, 2012

2

F.No.17/7/2011-BO.II Government of India Ministry of Finance

Department of Financial Services

REPORT OF THE KEY ADVISORY GROUP (KAG) ON THE NON-BANKING FINANCE COMPANIES (NBFCs)

Government constituted a Key Advisory Group (KAG) on the Non-Banking Finance

Companies (NBFCs) vide Order dated 30.09.2011. The constitution and terms of reference of

the Group is in ANNEX. The Group had representation from all the stakeholders from the sector

including the Indian Banks' Association, FICCI, CII and ASSOCHAM representing major NBFCs

in the Country; Ernst & Young, prominent Law firms viz. Amarchand Mangaldas, Juris Corp;

FIDC (a representative body of NBFCs) and also from some prominent NBFCs. The terms of

reference of the Group was as under –

i. Review of existing legal / regulatory / institutional framework for NBFCs and its efficacy;

ii. Action plan including policy initiatives for orderly growth of the Sector;

iii. To recommend the legal / institutional / regulatory initiatives related measures required for orderly growth of the Sector.

2. Though RBI was included as a member of the KAG, they have expressed their inability

to be a part of the Group stating that the KAG is to essentially discuss and deliberate on the

Report of RBI Working Group, and therefore, their association with the Group may not be

desirable. The Group held its meetings on 8.10.2011 and 8.11.2011 and had extensive

deliberations and consultation on a wide range of issues having a bearing on orderly growth of

the sector. The draft Report was also discussed with the stakeholders, and has been modified

taking into consideration the views expressed by the stakeholders. Accordingly, the Report of

the Group has been finalised on 31.01.2012.

3. The Group expresses its sincere gratitude to the team of Shri D.D. Maheshwari, Under

Secretary, Department of Financial Services for putting in unstinting efforts in organising the

meetings of the Group, facilitating deliberations, organising relevant information and finalizing its

Report.

(Alok Nigam) Chairman

31st January, 2012

3

Contents 1. Overview of the NBFC sector ...............................................................................................4

1.1 Introduction 1.2 NBFCs - growth and evolution 1.3 Bank Exposure to NBFCs 1.4 Summing up

2. Role and Vision for the NBFC sector ..................................................................................10 2.1 Issues 2.2 Is there an economic role that the NBFCs fulfill? 2.2.1 Infrastructure financing 2.2.2 Serving unbanked customer segments 2.2.3 Strong understanding of customer segments and ability to deliver customized products 2.3 What kind of regulatory structure that can be envisaged for the sector? 2.4 What is the systemic risk posed by the sector and the progression curve for NBFCs? 2.5 Is there any additional category of NBFCs required? 2.6 Future growth and development of NBFCs

3. Recommendations of the Thorat Committee ....................................................................14 3.1 The RBI Working Group Report 3.2 Broader objective of RBI Working Group Report 3.3 Recommendations 3.3.1 General 3.3.2 Categorization of NBFCs

4. Recommendations - II .......................................................................................................19 4.1 Prior approval of RBI for mergers of NBFCs 4.2 Definition of Public Funds 4.3 Participative Financing 4.4 Fixed Deposits as Financial Assets 4.5 Banking credit for priority sector lending 4.6 ECB financing 4.7 Prudential norms for certain categories of NBFCs to be more relaxed 4.8 Lending to stock brokers and merchant banks

5. Recommendations - III ......................................................................................................23 5.1 Direct Tax Issues 5.1.1 Tax Deduction at Source on Interest (Section 194A of the Income Tax Act) 5.1.2 Tax benefits for Income deferral under Section 43D of the Income Tax Act 5.1.3 Allowing of provisions made for Non-performing Assets (NPAs) under Section 36(1)(viia) of the

Income Tax Act 5.1.4 Declaration in Form 15G / 15H read with Section 206AA 5.1.5 Introduction of the threshold limit for TDS on the interest income on unlisted debentures 5.1.6 Depreciation in respect of Construction Equipments registered under the Motor Vehicles Act

5.2 Indirect Tax Issues 5.2.1 Extension of Cenvat credit rule to other services 5.2.2 Service Tax on Hire Purchase / Lease Transactions

6. Gist of recommendations…………………………………………………………………………………………….27

7. Conclusion…………………………………………………………………………………………………………………...30

8. ANNEX - Order of Constitution of the Key Advisory Group on NBFCs…………………………..….31

4

1. Overview of the NBFC sector 1.1 Introduction

The Indian economy has been witnessing high rates of growth in the last few years. Financing

requirements have also risen commensurately and will continue to increase in order to support

and sustain the tremendous economic growth.

NBFCs have been playing a complementary role to the other financial institutions including

banks in meeting the funding needs of the economy. They help fill the gaps in the availability of

financial services that otherwise occur in bank-dominated financial systems. The gaps are in

regards the product as well customer and geographical segments.

NBFCs over the years have played a very vital role in the economy. They have been at the

forefront of catering to the financial needs and creating livelihood sources of the so-called un-

bankable masses in the rural and semi-urban areas. Through strong linkage at the grassroots

level, they have created a medium of reach and communication and are very effectively serving

this segment. Thus, NBFCs have all the key characteristics to enable the government and

regulator to achieve the mission of financial inclusion in the given time.

1.2 NBFCs – growth and evolution

The number of NBFCs has decreased from 13,014 in FY06 to 12,409 in FY11 however the

sector has grown by 2.6 times between FY06 and FY11 at a CAGR of 21%. It accounted for

10.8% in terms of outstanding advances and 13% in terms of assets of the banking system in

FY06. This share has risen to 13.2% and 13.78% respectively in FY11. In terms of deposits the

share of public deposits held by NBFCs as compared to deposit base of banks has decreased

from 1.05% in FY06 to 0.22% in FY11.

Public deposits held by NBFCs have shown a falling trend, decreasing by approximately 48% in

the last 5 years, while owned funds (reserves & surplus and capital deployed) have gone up by

195%. The outstanding advances have grown approximately 3 times in the last 5 years to reach

Rs.536,074 crores in FY11. Banks exposure to NBFCs has increased from Rs.62,308 crore in

FY06 to Rs.183,839 crore in FY11, an increase of approximately 3 times growing at a CAGR of

24% during the period FY06-FY11 and a 37% increase over FY10.

5

SCBs include Regional Rural Banks and Co-operative Banks

NBFCs include NBFCs-D, NBFCs-ND-SI and RNBCs

All amounts in Rs.Crores

Table 1 – Consolidated Balance Sheet of NBFCs*

FY06 (Rs.Cr) FY10 (Rs.Cr) FY11 (Rs.Cr) % FY11

Share Capital 22,154 43,275 47,222 6%

Reserves & Surplus 47,741 1,39,312 1,58,683 19%

Public Deposits 22,842 17,352 11,964 1%

Borrowings 2,07,597 4,49,857 5,70,754 67%

Of which Borrowings from Banks/FIs 62,308 1,31,720 1,83,839 22%

Current liabilities and Provisions 30,267 51,139 58,629 7%

Total Liabilities 3,30,601 7,00,935 8,47,252 100%

Loans and Advances 1,69,449 4,19,636 5,36,074 63%

Bill Business 45 45 89 0%

Hire Purchase Assets 44,715 41,685 50,019 6%

Investments 81,630 1,52,183 1,64,130 19%

Cash & Bank Balances NA 25,857 29,877 4%

Other Current Assets NA 40,565 42,444 5%

Other Assets 34,762 20,965 24,619 3%

Total Assets 3,30,601 7,00,936 8,47,252 100%

*NBFCs include NBFC-D, NBFC-ND-SI and RNBCs (Residuary Non-Banking Companies)

6

Table 2 – Comparison with Banking Sector

FY06 (Rs.Cr) FY10 (Rs.Cr) FY11 (Rs.Cr)

No. of NBFCs 13,014 12,630 12,409

Bank credit of all Scheduled Banks* 1,572,780 3,337,659 4,060,843

NBFC advances as a % of Bank credit 10.77% 12.57% 13.20%

Assets of all Scheduled Banks* 2,531,462 5,258,495 6,146,590

NBFC assets as a % of Bank assets 13.06% 13.33% 13.78%

Deposits of all Scheduled Banks* 2,185,809 4,635,224 5,355,160

NBFC Public Deposits as a % of Bank Deposits 1.05% 0.37% 0.22%

*Scheduled Banks include Scheduled commercial banks and Co-operative Banks

For FY06 - 218 and 71, Total – 289, For FY11 - 163 and 69, Total – 232

2 Dependence on Public Funds

Table 3 – Sources of Funds of NBFCs

FY06 (Rs.Cr) FY10 (Rs.Cr) FY11 (Rs.Cr) FY06 FY10 FY11

Share Capital 20,971 40,444 44,234 7% 6% 6%

Reserves and Surplus 48,924 142,233 161,671 16% 22% 21%

Public Deposits 22,842 17,352 11,964 8% 3% 2%

Borrowings 207,597 449,857 570,754 69% 69% 72%

Bank/FI borrowings 62,308 131,720 183,839 21% 20% 23%

Debentures 68,138 156,107 205,320 23% 24% 26%

Inter-corporate

Borrowings 19,459 22,153 24,883 6% 3% 3%

Commercial Paper 13,123 31,049 32,321 4% 5% 4%

Others 44,569 108,828 124,391 15% 17% 16%

Total 300,334 649,886 788,623 100% 100% 100%

Table 4 – Public Funds as a percentage of Total Sources of Funds

FY06 FY10 FY11

NBFCs-D 59.3% 59.8% 59.0%

NBFCs-ND-SI 59.4% 53.6% 57.8%

RNBCs 94.5% 83.3% 72.6%

Overall NBFC Sector 61.9% 55.1% 58.1%

Public Funds (as defined by RBI) – funds raised either directly or indirectly through public deposits, commercial papers, debentures, inter-corporate deposits, guarantees and bank finance or any other debt instrument, but exclude funds raised by issue of share capital and/ or instruments compulsorily convertible into equity shares

7

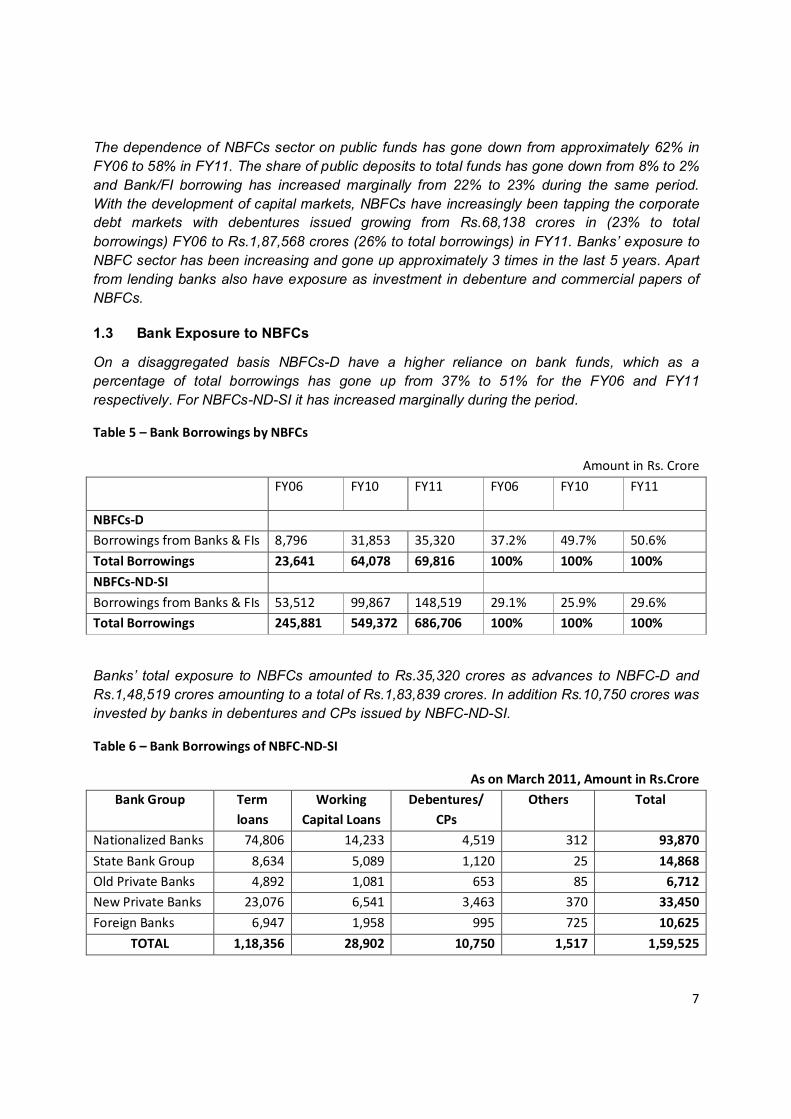

The dependence of NBFCs sector on public funds has gone down from approximately 62% in

FY06 to 58% in FY11. The share of public deposits to total funds has gone down from 8% to 2%

and Bank/FI borrowing has increased marginally from 22% to 23% during the same period.

With the development of capital markets, NBFCs have increasingly been tapping the corporate

debt markets with debentures issued growing from Rs.68,138 crores in (23% to total

borrowings) FY06 to Rs.1,87,568 crores (26% to total borrowings) in FY11. Banks’ exposure to

NBFC sector has been increasing and gone up approximately 3 times in the last 5 years. Apart

from lending banks also have exposure as investment in debenture and commercial papers of

NBFCs.

1.3 Bank Exposure to NBFCs

On a disaggregated basis NBFCs-D have a higher reliance on bank funds, which as a

percentage of total borrowings has gone up from 37% to 51% for the FY06 and FY11

respectively. For NBFCs-ND-SI it has increased marginally during the period.

Table 5 – Bank Borrowings by NBFCs

Amount in Rs. Crore

FY06 FY10 FY11 FY06 FY10 FY11

NBFCs-D

Borrowings from Banks & FIs 8,796 31,853 35,320 37.2% 49.7% 50.6%

Total Borrowings 23,641 64,078 69,816 100% 100% 100%

NBFCs-ND-SI

Borrowings from Banks & FIs 53,512 99,867 148,519 29.1% 25.9% 29.6%

Total Borrowings 245,881 549,372 686,706 100% 100% 100%

Banks’ total exposure to NBFCs amounted to Rs.35,320 crores as advances to NBFC-D and

Rs.1,48,519 crores amounting to a total of Rs.1,83,839 crores. In addition Rs.10,750 crores was

invested by banks in debentures and CPs issued by NBFC-ND-SI.

Table 6 – Bank Borrowings of NBFC-ND-SI

As on March 2011, Amount in Rs.Crore

Bank Group Term

loans

Working

Capital Loans

Debentures/

CPs

Others Total

Nationalized Banks 74,806 14,233 4,519 312 93,870

State Bank Group 8,634 5,089 1,120 25 14,868

Old Private Banks 4,892 1,081 653 85 6,712

New Private Banks 23,076 6,541 3,463 370 33,450

Foreign Banks 6,947 1,958 995 725 10,625

TOTAL 1,18,356 28,902 10,750 1,517 1,59,525

8

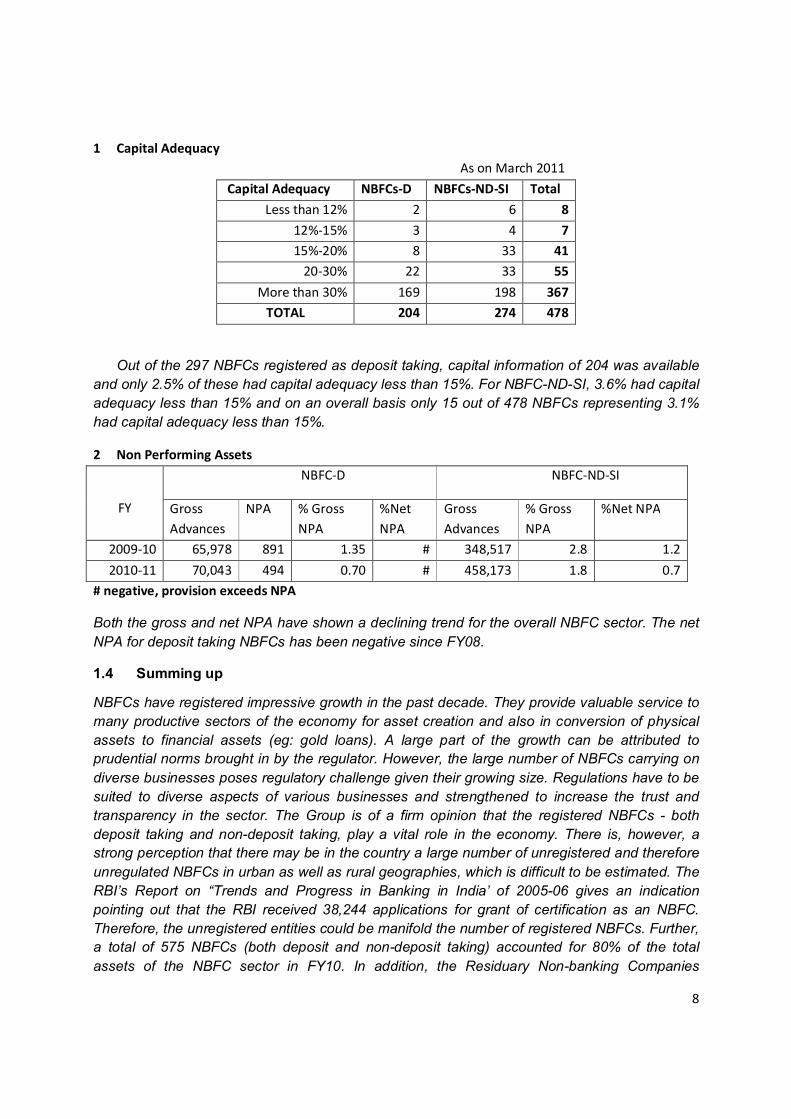

1 Capital Adequacy

As on March 2011

Capital Adequacy NBFCs-D NBFCs-ND-SI Total

Less than 12% 2 6 8

12%-15% 3 4 7

15%-20% 8 33 41

20-30% 22 33 55

More than 30% 169 198 367

TOTAL 204 274 478

Out of the 297 NBFCs registered as deposit taking, capital information of 204 was available

and only 2.5% of these had capital adequacy less than 15%. For NBFC-ND-SI, 3.6% had capital

adequacy less than 15% and on an overall basis only 15 out of 478 NBFCs representing 3.1%

had capital adequacy less than 15%.

2 Non Performing Assets

FY

NBFC-D NBFC-ND-SI

Gross

Advances

NPA % Gross

NPA

%Net

NPA

Gross

Advances

% Gross

NPA

%Net NPA

2009-10 65,978 891 1.35 # 348,517 2.8 1.2

2010-11 70,043 494 0.70 # 458,173 1.8 0.7

# negative, provision exceeds NPA

Both the gross and net NPA have shown a declining trend for the overall NBFC sector. The net

NPA for deposit taking NBFCs has been negative since FY08.

1.4 Summing up

NBFCs have registered impressive growth in the past decade. They provide valuable service to

many productive sectors of the economy for asset creation and also in conversion of physical

assets to financial assets (eg: gold loans). A large part of the growth can be attributed to

prudential norms brought in by the regulator. However, the large number of NBFCs carrying on

diverse businesses poses regulatory challenge given their growing size. Regulations have to be

suited to diverse aspects of various businesses and strengthened to increase the trust and

transparency in the sector. The Group is of a firm opinion that the registered NBFCs - both

deposit taking and non-deposit taking, play a vital role in the economy. There is, however, a

strong perception that there may be in the country a large number of unregistered and therefore

unregulated NBFCs in urban as well as rural geographies, which is difficult to be estimated. The

RBI’s Report on “Trends and Progress in Banking in India’ of 2005-06 gives an indication

pointing out that the RBI received 38,244 applications for grant of certification as an NBFC.

Therefore, the unregistered entities could be manifold the number of registered NBFCs. Further,

a total of 575 NBFCs (both deposit and non-deposit taking) accounted for 80% of the total

assets of the NBFC sector in FY10. In addition, the Residuary Non-banking Companies

9

(RNBCs) account for 66% of public deposits held by the NBFC sector. Therefore, the Group

underlines that the regulatory and supervision mechanism for the NBFC sector need to be

widened and strengthened.

***

10

2. Role and Vision for the NBFC sector

2.1 Issues

The Group underlines the fact that the NBFCs have grown substantially and are rendering

valuable services to the unbanked and under-banked population of the country. Even the RBI

appointed Thorat Committee has lauded the role of NBFCs in the economic growth of the

country. NBFCs have been innovators in financial services, designing products and services

customized to the needs of the target customers. In addition they have created a suitable

operational structure to make the business models viable. They have helped expand the

financial services markets to the interiors of the country and newer products and services.

The role and vision for NBFC sector has, therefore, been looked at and analyzed from the

following viewpoints:

1. Is there an economic role that the NBFCs fulfill?

2. What is the kind of regulatory structure that can be envisaged for the sector?

3. What is the systemic risk posed by the sector and the progression curve for NBFCs?

4. Apart from the existing categories, is there any need for providing of additional

categories of NBFCs considering the economic role played by them?

Answering the above questions will crystallize the shape and direction of policy action for the

sector.

2.2 Is there an economic role that the NBFCs fulfill?

NBFCs have been operating various businesses under sound economics. Many businesses

started by the sector have later been taken up by banks and become regular banking services.

For instance, car financing, which was started by NBFCs has now become one of the larger

revenue streams for banks. The NBFCs themselves have now moved on to financing second

hand cars. Other businesses, namely, infrastructure finance, asset finance, hire purchase and,

in the recent past, microfinance have been the major areas of operations for NBFCs.

Additionally, NBFCs play a supportive role in the economy and also in financial inclusion and

therefore need to be encouraged. Some of the economic roles played by NBFCs are:

2.2.1 Infrastructure financing

While the RBI doesn’t have any specific sector exposure limits, it has asked the banks to

formulate internal policies for exposure to the infrastructure sector. The banking sector’s

exposure to infrastructure was Rs. 5,50,178 crore as on May 2011, which was 15% of

total non-food bank credit of the banks. In comparison, the Infrastructure Finance

11

NBFCs had an outstanding infrastructure loan book size of Rs.1,96,158 crore. Banks’

further exposure to infrastructure is constrained by prudential internal limits (which

typically are 12-15%) and asset liability mismatch due to long tenure of assets and short

tenure of liabilities.

Given the projected capital requirement for infrastructure sector in the 12th five-year plan,

NBFCs will play a part in supplying capital to the sector. However, proper credit rating,

accounting and financial norms have to be ushered in for greater transparency and

soundness of the sector as also operating in the NBFC sector.

2.2.2 Serving unbanked customer segments

NBFCs have traditionally focused on customer segments which were not served by

banks like micro, small and medium enterprises (MSMEs), funding of commercial

vehicles including old vehicles, farm equipments viz. tracking, harvesters, etc. loan

against shares, funding of plant and machinery; etc.

NBFCs typically are specialized vehicles –both in terms of products and the geographies

in which they operate. This specialization provides them a unique framework to assess

the risk in the undertaken business. A much closer market awareness provides them the

ability to rate borrowers, monitor them, price the relative credit suitably and effect

recoveries from them.

NBFCs also provide credit for certain sectors which are not served by banks and

Financial Institutions because Banks/FIs do not have adequate market relationships and

infrastructure for the same. Some of these sectors are:

(a) Used Trucks

(b) Used passenger vehicles

(c) Consumer durable loans

(d) Personal Loans

(e) Funding to the Small & Medium Enterprises (SME Sector) which do not have access to

institutionalized funding, etc.

Traditionally, these sectors were financed entirely by the unorganized financiers at

exorbitant high interest rates. In the last 10 years, with their retail strength, NBFCs have

rendered significant service by extending credit to these sectors. Now banks and

financial institutions are availing of the reach and expertise of NBFCs for employing

funds in these sectors through NBFCs. This has brought in lot of funds into these

sectors, thereby reducing interest rates.

2.2.3 Strong understanding of customer segments and ability to deliver customized

products

The ability of NBFCs to produce innovative products in consonance with needs of their

clients is well recognized. This, in addition to the proximity to the clients, makes the

12

NBFCs distinct from its banking sector counterparts. In a short period of time, NBFCs

have become market leaders in most of the retail finance segments like commercial

vehicles, car financing and personal loans. In the last decade or so, the Indian retail

finance markets have seen several new products being developed and introduced by

NBFCs. The following are some cases in point - Used vehicle financing, Small ticket

personal loans (ST-PL), Three-wheeler financing, Loan against shares, Promoter

funding, Public issue financing (IPO financing) and Finance for tyres and fuel.

NBFCs have a significant economic role, especially servicing the under-banked and unbanked

populace and geographies. Bringing the diverse set of NBFCs under regulation rather than

curtailing their operations, would help orderly growth of the sector.

2.3 What kind of regulatory structure that can be envisaged for the sector?

With the substantial size of the NBFC sector it is prudent that the regulation and supervision

structure is strengthened. However, given the large numbers, the regulation and supervision is a

huge challenge. Prudential norms for stricter monitoring and reporting norms should be put in

place and, at an initial stage; it could be through data mining and analytics which could evolve

into on-site and other inspections in due course of time. Further, increased regulatory focus and

prudential framework are required for systemically important NBFCs. For smaller entities,

elaborates reporting norms is likely to a better option –as it will same on time, energy, cost and

resources both to the Regulator as well as to the regulated entities. To achieve this objective,

the Regulator may also consider size-wise uniform accounting requirements and financials

reporting requirements for different sets of NBFCs.

2.4 What is the systemic risk posed by the sector and the progression curve for NBFCs?

The systemic risk posed by the sector is the inter-connect and dependence on public funds

which amounts to approximately 58% of all funding to the sector. The size of the NBFC sector is

approximately 13% of the banking sector. Once the regulatory structure and prudential norms

are put in place and the regulator is in a position to assess and manage the risks posed by the

sector, there could be an even increased interplay with the banking sector. Additionally,

development of the corporate bond market will help the NBFC sector source funds from the

capital market and be less dependent on deposits or bank borrowings and limit the risk posed to

the banking sector.

2.5 Apart from the existing categories, is there any additional category of NBFCs

required in view of the economic role played by them?

Currently, the RBI classifies NBFCs into 7 categories as following:

1. Asset finance company (AFC)

2. Investment company (IC)

3. Loan company (LC)

13

4. Infrastructure finance companies (IFC)

5. Core investment companies (CIC)

6. Infrastructure debt fund – Non-banking finance company (IDF-NBFC)

7. Non-banking finance company – Micro finance institution (NBFC-MFI) - (introduced on

December 2, 2011).

The Group has observed that the NBFCs are engaged in financing physical assets and resultant

creation of a large number of jobs - which supports and strengthens economic activities across

sectors, and play a critical role as an effective instruments of credit delivery particularly in the

small and retail sectors of the economy. Therefore, the Group is of the opinion that the policies

may be geared towards the development and growth of the sector. The regulator has also been

proactive in recognizing the diverse and critical role played NBFCs and has accorded added

regulatory focus on the sector by introducing and strengthening prudential frameworks for

NBFCs. Considering the role played by NBFCs in creation of assets, financial inclusion,

generation of employment opportunities for marginalized sections of the society and their

outreach, an additional category of NBFC loan company – priority sector (NBFC-LC-PS) may

be looked at for NBFCs engaged in servicing priority sector customers as defined by RBI.

2.6 Future growth and development of NBFCs

Given the important role played by NBFCs as innovators, serving unbanked and under-banked

geographies and customer segments and services not provided by banks, it is imperative that

the growth and development of the sector be accorded some degree of priority. With adequate

regulatory oversight of systemically important NBFCs, implementation of prudential norms,

regular reporting and monitoring, etc., NBFCs may be looked at playing a larger part in the

financial services sector.

***

14

3. Recommendations of the Thorat Committee

3.1 The RBI Working Group Report

The Report of the Working Group on the "Issues and Concerns in the NBFC Sector", chaired by

Smt. Usha Thorat, was released by The Reserve Bank of India (RBI) on August 29, 2011. The

report made recommendations on strengthening the governance and supervision of NBFCs,

which are greatly appreciated especially in the following matters:

Extension of the benefits of the SARFAESI Act, 2002 to NBFCs

Extension of the benefit of tax deduction for provisions made by NBFCs

Strengthening of the Corporate governance and supervisory framework for the NBFCs

3.2 Broader objectives of RBI Working Group Report

The KAG appreciates the concerns indicated in the Thorat Committee Report arising out of

regulatory arbitrage and constraints in regulating a large number of smaller NBFCs. The KAG is

also conscious of the risks associated with a large number of un-registered / un-regulated

smaller entities, particularly because of their activities among and inter-action with the low-

income target populations. The KAG also notes that RBI views a large part of the activities of

the NBFCs as productive in nature and also views positively the role played by most of the

NBFCs including the smaller ones in meeting the funding requirements of the financially

excluded sections of the society. Therefore, KAG is of the view that addressing the regulatory

and supervisory concerns should not be abrupt, may not result in policy uncertainties, and also

not create a vacuum in the financial space for the financially excluded sections of the society.

The KAG also underlines and appreciates the aspect that, in view of diverse circumstances and

requirements of different sets of entities, RBI has been prescribing different regulatory norms for

various category of entities, such as, banks, NBFCs, target sectors, etc. For example, exposure-

norms, provisioning requirements, NPA classification norms, priority sector prescriptions, etc.

are different for various categories of entities (banks / NBFCs) or sectors, etc.

3.3 Recommendations

Keeping in view all these factors and to harmonise the broader objectives of financial inclusion

viz-a-viz to gradually minimise the regulatory arbitrage, we make a few observations on some of

the recommendations of the Working Group Report, as under:

(i) RBI recognises a large part of the activities of NBFCs as productive in nature.

However, because of increase in cost of funding, the ability of NBFCs to carry on

business may be impacted adversely. RBI may create framework and prudential

15

norms to contain the risks posed with a view to support and develop those

NBFCs which meet the needs and requirements of the productive sectors of the

economy. RBI also need to support NBFC-IFC, NBFC-MFI and NBFC-LC-PS by

facilitating bank lending to this sector by easing in securitization of assets of

these sectors, lower capital requirements, lower provisioning requirements and

by taking other appropriate regulatory measures.

(ii) The use of public funds by NBFCs has gone down from 62% in FY06 to 58% in

FY11. During the same period, owned funds as a percent of total source of funds

increased from 23.3% to 26.1%. However, in the absence of authentic data, it

may not be possible to assess the actual usage of public funds by NBFCs for

productive and non-productive segments of the economy. The data available with

RBI may suggest / identity the NBFCs which have borrowed from Banks for

onward lending to the Priority Sector segments. Such entities should be

encouraged in larger public interest and such NBFCs should be distinguished

from other NBFCs which access bank funds for other end uses – such as real

estate / capital market transactions. RBI may also consider putting in place

appropriate framework to ensure any potential mal-practices noticed in this

regard, instead of blocking flow of funds altogether, which may be detrimental to

the access of genuine priority sector borrowers to the funding through NBFCs.

Further, this also underlines the requirement of creating a comprehensive data-

bank of NBFCs to ascertain the funding pattern vis-à-vis the growth in assets for

different class of NBFCs, which may provide valuable pointers and enable

meaningful decision making for regulatory framework and prescriptions required

for various types of NBFCs.

(iii) At the time the Companies Act was last amended, it provided that an issuance to

more than 49 persons would make such issuance a “public issue”. However,

considering their business requirements and subject to their complying with other

requirements of a “private placement” as set out in Section 67 of the Companies

Act, the Government of India decided to exempt Banks, Financial Institutions and

NBFCs from this limit. This exemption to the NBFCs may be allowed to continue.

Liquidity:

(iv) Asset Liability Management (ALM) guidelines have been made mandatory for

NBFC-ND-SIs with assets of Rs. 100 crore and above and for deposit taking

NBFCs with deposits more than Rs. 20 crore. Such NBFCs are required to

maintain a gap not exceeding 15% of their net cash outflows in the 1-30/31 day

bucket. The KAG is of the view that prescribing a separate liquidity requirement

for near-term bucket (upto 1 month) will avoidably increase the cost for NBFCs,

and consequent cost of funds for their customers. KAG therefore recommends

that for NBFCs, the tolerance limit of 15% for the negative mis-matches over one

year time buckets may be restored, which would be in line with the existing

16

prudential guidelines for both banks and NBFCs. Alternatively, the changes are

phased-out to provide adequate time to the affected entities to align with the

revised regulations.

(v) NBFCs normally invest in money market instruments indirectly through liquid

money market Mutual Funds. Therefore, for the purpose of computing total

financial assets, investments in liquid funds of mutual fund should also be

included in the eligible liquid instruments apart from G-Sec, T-Bills etc.

(vi) The non-deposit taking systematically important NBFCs were permitted to

augment their capital by issuing perpetual bonds, after their CRAR requirement

was increased from 12% to 15%. RBI has now prescribed similar CRAR

requirements for Deposit accepting NBFCs as well. Therefore, the same flexibility

of raising perpetual bonds may be permitted to both deposit-taking systematically

important and non-deposit taking systematically important NBFCs.

Capital Adequacy:

(vii) The RBI Working Group has suggested that the Tier-I CRAR be raised to 12%

from the current 10%. It is evident from the report that the main consideration for

raising the Tier-I CRAR is on the basis that banks have CRR/SLR requirements

as well as priority sector obligations. But, while the banks have the burden of

CRR/SLR as well as priority sector obligations, they also have the benefit of risk-

weighted CRAR requirements based on the credit rating of their borrowers. For

example, for AAA rated borrower, the applicable risk weightage is 20%. After

adjusting the potential Tier-II capital, the Tier-I capital to be provided against the

AAA asset will be 1.2% of the value of the loan. The NBFCs do not have the

benefit of such calibrated risk weightage. An increase in the Tier-I CRAR would

severely impact the competitiveness of NBFCs. Therefore, KAG is of the view

that the Tier-I CRAR requirement for the NBFCs may be retained at 10%.

(viii) From 01.04.2011, RBI had increased the CRAR requirements for NBFCs from

12% to 15%, out of which 10% should be Tier-I capital. The RBI Working Group

has recommended that Tier-1 CRAR requirement for NBFCs be raised to 12%.

This would mean another increase in Tier-I capital of NBFCs by 20%, which

would severely affect the cost side of NBFCs. RBI has prescribed a calibrated

risk-weighted regime for the banks depending upon the associated risk in lending

- both for the sectors as well as the borrowal entities. KAG is of the view that the

importance of 'risk-assessment' or 'risk-perception' as guiding principles for

determining capital requirement of NBFCs need no additional emphasis, and

would bring enhanced discipline and efficiency in their functioning. The KAG also

recommends that –

17

i. the risk weightage for asset financing / financial inclusion / SME

businesses be reduced to 50%; and

ii. on Loan against property where shares are only taken as secondary

collateral (property being the main security), it doesn’t tantamount to

capital market exposure, and as such risk-weight may be prescribed as

100%.

Minimum Net Owned Funds:

(ix) RBI permits NBFCs an overall leverage by borrowing based on the prescribed

CAR. NBFCs essentially borrow only as working capital loans as they are

deployed for their business and the repayment is also funded out of the business

collections. Currently, rated AFCs are permitted to accept deposits upto 4 times

of their net-owned-funds (NOF). RBI Working Group has recommended that the

limit for acceptance of deposits for rated Asset Finance Companies (AFCs)

should be reduced from 4 times NOF to 2.5 times NOF. AFCs presently

exceeding this limit may not renew or accept fresh deposits till such time as they

reach the revised limit. The committee has recommended compulsory rating of

AFCs for raising deposits. Most of AFCs raise fund by way of NCD issuance

which are rated and if same are not secured by immovable property equivalent to

one times the issue size are considered as deposit. The aforesaid restriction will

further limit the avenue of raising money by NBFCs and thereby hamper their

contribution to economic growth by way of financing of productive assets.

Non Performing Assets (NPAs):

(x) The period for classifying loans as NPAs in case of NBFCs is higher at 180/360

days compared to 90 days for banks. A 90 day reference for recognizing NPAs in

NBFCs in line with banks would impose provisioning burden on the NBFCs and

could result in NBFCs deciding to opt for early foreclosures, depriving their

borrowers of an income generating asset. Given the higher capital requirements,

accelerated provisioning would further burden the NBFCs. Any change in the

provisioning requirements for NBFCs to match that of Banks may be to the

detriment of NBFCs which serve specific unbanked sections of the society,

particularly the small truck operators and the SME businessmen. Their

repayment to the NBFC is linked to their collection. Invariably, their collection

gets delayed due to various reasons beyond their control. Further, the small

borrowers of NBFCs have, over the years, tuned their business model to match

the collection requirements of the NBFCs. The NBFCs have also been able to

exhibit good collection record and the default rate is extremely low. Therefore,

KAG is of the view that the current NPA classification norms for NBFCs may

continue. Instead, RBI may put in place an effective and elaborate reporting

18

mechanism to assess the delinquency pattern, behavior and incidents in various

categories of NBFCs; to design an appropriate regulatory regime.

3.3.1 GENERAL

In respect of the capital requirements; risk-weights for various classes of assets, sectors and

entities, the classification and provisioning requirements for stressed assets, borrowing-limits; or

the balance-sheet size of the NBFCs for registration / de-registration requirements, KAG is of

the view that the regulatory prescriptions should be gradual and duly phased-out so as not to

create policy uncertainties; and also afford adequate time to the affected NBFCs to be able to

align themselves with the revised regulatory framework without substantial dislocation of their

normal business activities. This will also inculcate a sense of stability among the stakeholders to

visualise and undertake long term plans.

3.3.2 Categorization of NBFCs

The RBI Working Group has recommended that since there is no difference in the regulatory

framework for loan companies (LCs) and investment companies (ICs), and since most of the

NBFCs-ND-SI are a mixture of loan and investment companies, a single category of LCs and

ICs should be made. The KAG is of the view that may not appropriately factor-in the risk profile

of LCs viz-a-viz ICs. While the assets of ICs typically carry the risk of equity / capital markets,

the asset side of LCs largely consist of loan receivables. Consequently, LCs present a far lesser

risk than ICs and therefore need to be differentially regulated from ICs. Also, the borrowings by

LCs are typically supported by credit rating by independent credit rating agencies.

***

19

4. Recommendations - II

4.1 Prior approval of RBI for mergers of NBFCs

The RBI Working Group has recommended that all registered NBFCs should take prior approval

of the RBI whenever there is a change in control or transfer of shareholding of the said NBFC,

directly or indirectly, exceeding 25% of its paid-up share capital. Prior approval of the RBI

should also be taken for mergers of NBFCs under the Companies Act or any acquisition by / of

an NBFC governed by the SEBI Takeover Regulations.

Recommendation: The requirement of taking prior approval of the RBI whenever there is a

change in control or transfer of shareholding of an NBFC, directly or indirectly, exceeding 25%

of its paid-up share capital, should only apply in cases where the acquirer acquiring the NBFC

or the NBFC being acquired has raised public deposits. In other cases, the requirement of only

providing information to the RBI should be mandated.

Similarly, considering that the public offers under the SEBI Takeover Regulations are presently

being supervised by SEBI and mergers under the Companies Act, 1956 require prior approval

of the High Court, the need for approval from another regulatory authority viz. RBI may be

dispensed with. Further acquisitions / mergers may also require approval of the Competition

Commission of India under the Competition Act. Approvals from multiple regulatory authorities

will only delay the process. Therefore, in such cases also, the requirement of providing

information to the RBI should be mandated.

In case the proposal for prior approval from RBI for such restructuring of NBFCs is accepted, for

increased transparency, accountability and objectivity in the decision making process of the

regulatory functions of RBI, KAG also recommends that the concept of ‘deemed approval’

should also be provided in cases where the RBI does not communicate its approval / rejection

to the said restructuring within a certain prescribed reasonable period.

4.2 Definition of Public Funds

The RBI Working Group has defined ‘public funds’ as funds raised either directly or indirectly

through public deposits, commercial papers, debentures, inter-corporate deposits, guarantees

and bank finance or any other debt instrument, but exclude funds raised by issue of share

capital and/ or instruments compulsorily convertible into equity shares within a period not

exceeding 10 years from the date of issue or registration with RBI.

Recommendation: KAG recommends that the term ‘public funds’ should not include loans /

deposits from the Holding / Group Company, if funded through internal accruals of the Holding /

Group Company. The RBI may insist on a certificate from the statutory auditors of the Holding

Company to that effect.

20

4.3 Participative Financing:

In the backdrop of the recent concerns pertaining to levy of usurious rate of interests by Micro

Financial Institutions and earlier RBI guidelines on Fair Practice Code in 2009 (to ensure

transparency in charging high rates of interests by NBFCs), charging of high interests on loans

disbursed to retail borrowers, has always raised issues in India.

This can be mitigated if NBFCs are expressly allowed to undertake participative financing which

consist of financings in a manner that returns are linked to the actual cash flows of the venture

for which financing was availed but such that the returns are capped. Mezzanine financing is

one such form.

While per se the Reserve Bank of India Act, 1934 does not prohibit participative financing, the

circular on 2nd January 2009 on Fair Practice Code required NBFCs to, inter-alia, adopt an

interest rate model taking into account relevant factors such as, cost of funds, margin and risk

premium, etc. and determine the rate of interest to be charged for loans and advances. In our

view, while the said 2009 circular was intended to clarify RBI’s earlier circular on Fair Practice

Code and ensure transparency, given the language used therein, it has been interpreted to

mean that NBFCs must follow an explicit interest based model.

We therefore urge the RBI to issue a clarificatory circular stating therein that the 2nd January

2009 circular on Fair Practice Code applies to those NBFCs that are disbursing interest based

loans and does not prohibit NBFCs from undertaking other forms of financing such as

participative financing / non-interest based financing.

As regards NBFCs that are undertaking participative financing and / or any other non-interest

based financing, the following directions should be complied with:

(i) The Fair Practice Code should set out the model on which facilities will be granted to

borrowers. The NBFCs should also set out the commercial considerations for its

facilities, (after factoring in aspects such as cost of funds, expected return and other

parameters to determine credit viability). The Fair Practice Code should be displayed on

the website of the NBFCs and updated periodically;

(ii) The borrowers should be made aware of these commercial considerations in the

agreement and the loan sanction letter. Expected returns, servicing charges should be

communicated separately. If the expected rates of return and service charges are

different for different category of borrowers, then the same should be communicated to

the borrowers.

4.4 Fixed Deposits as Financial Assets:

Presently RBI excludes “fixed deposits” from the definition of “financial assets”. Secondly, the

Report recommends that bank deposits maturing within 30 days should be taken into

21

consideration for computing “financial assets”. We urge the RBI to consider including fixed

deposits under financial assets for the purpose of computing principal business of an NBFC.

For this purpose, the following amendment (in bold) is proposed to the definition of “principal

business” stated in the circular dated 19th October 2006 on “Amendment to NBFC regulations -

Certificate of Registration (CoR) issued under Section 45-IA of the RBI Act, 1934 – Continuation

of business of NBFI -Submission of Statutory Auditors Certificate- Clarification”

“The company will be treated as a non-banking financial company (NBFC) if its financial assets

(including fixed deposits) are more than 50 per cent of its total assets (netted off by intangible

assets) and income from financial assets is more than 50 per cent of the gross income. Both

these tests are required to be satisfied as the determinant factor for principal business of a

company.”

4.5 Bank credit for priority sector lending:

Banks lending to NBFCs who further supported the priority sector was previously allowed to be

classified by banks as priority sector. NBFCs therefore received such funding at a discounted

cost of funds. However such on lending by banks has been disallowed for NBFCs in a circular

issued by RBI on May 3, 2011.

Given the importance of the role that NBFCs play in propagating financial inclusion, i.e serving

low income families and small businesses, on lending by banks should be classified as priority

sector. This will not only enhance the growth for NBFCs but also give banks a profitable channel

to deploy funds earmarked for priority sector instead of investing the funds at a nominal return.

The NBFCs could be asked to provide evidence to the effect that the end use of the borrowed

funds was by the priority sector participants; Further banks could be assigned the responsibility

of monitoring the end use of funds.

4.6 ECB financing:

Sources of funding for NBFCs are currently limited - this hampers the growth of credit by NBFCs

and ultimately the government's objective of financial inclusion. Much like infrastructure finance

companies, NBFCs should be allowed to raise funds in the form of ECB financing In a rising

interest rate environment, this will give NBFCs the much needed fillip in terms of funding cost.

Further, the differential cost would be the difference between rupee finance and ECB financing

(post hedging). In our view this could range between 1% to 2%, and would significantly ease the

interest cost burden that NBFCs are facing. End use of the ECB should be allowed to on-lend to

the end customers.

22

4.7 Prudential norms for certain categories of NBFCs to be more relaxed

Currently, all NBFCs are treated equally with regard to prudential norms. However given their

contribution to the development of the economy, infrastructure finance companies have been

carved out as a separate category with relaxation in terms of sources of borrowings (ECB

allowed) given the long term funding needs. Certain large NBFCs that are systematically

important and have healthy asset quality, good corporate governance practices, sufficient

capital, strong parentage need to be given a separate status to enhance their growth and reach.

Secondly, these NBFCs must be differentiated from a few smaller NBFCs that have indulged in

unsecured lending leading to higher levels of non-performing assets. Therefore our

recommendation is to create a separate category of NBFCs either in terms of (i) size or in terms

of (ii) lending against a security / income generating asset ("asset financing") or (iii) a

combination of both these parameters.

The capital adequacy, provisioning, risk weight norms for these NBFCs can be more relaxed i.e

retained at the current levels.

4.8 Lending to stock brokers and merchant banks

The working group has recommended that regulations for lending to stockbrokers and merchant

bankers by NBFCs (Loan companies focused on capital market financing) should be similar to

banks. We believe that the NBFCs / Loan companies focused on capital market financing are

essentially capital market players while banks are lenders; consequently these NBFCs face

capital market risk while banks deal with lending risk. Hence we suggest that the current NBFC

regulations on the subject be retained and RBI must address the regulatory need through

reporting by NBFCs of stockbroker and merchant bank exposures.

***

23

5. Recommendations – III 5.1 DIRECT TAX ISSUES

5.1.1 Tax Deduction at Source on Interest (Section 194A of the Income Tax Act)

As per Sec 194A of the Act, the Tax Deduction at Source (TDS) @10% is required to be

deducted on the interest portion of the installment paid to the NBFC under loan / finance

agreements. However, the banking companies, LIC, UTI, public financial institution, etc.

engaged in banking business are exempted from the purview of this Section.

NBFCs carry-on the financing business mostly to retail customers, most of whom are in

unorganized sectors including a large number of individuals and SME sector borrowers. A single

point collection of tax by way of advance tax payments from NBFCs would mean greater

convenience to the Income Tax Department than collecting of tax through large number of such

customers from all over the country by way of TDS. Further, the distinction in the provision puts

NBFCs in a disadvantageous position viz-a-viz other financing entities.

Recommendation – This Group, therefore, recommends that the NBFCs may also be

exempted from the provisions of section 194A of the Income Tax Act, at par with other financial

sector entities.

5.1.2 Tax benefits for Income deferral under Section 43D of the Income Tax Act

Section 43D of the Income Tax Act recognises the principle of taxing income on sticky advances

only in the year they are received. The provisions of Section 43D have been extended to the

Banks, Financial Institutions and State Financial Corporations. Further, this benefit was also

extended to the Housing Finance Companies by the Finance Act, 1999.

In accordance with the directions issued by the RBI, NBFCs follow prudential norms in line with

other financial sector entities to defer income in respect of their non-performing accounts.

However, the Income Tax authorities do not recognise these directions and tax such deferred

income on accrual basis, resulting in levying of tax on income which may not be realized at all.

Recommendation – This Group, therefore, recommends that the provisions / benefits of

Section 43D of the Income Tax Act be extended to include NBFCs registered with RBI, as in the

case of other institutions.

5.1.3 Allowing of provisions made for Non-performing Assets (NPAs) under Section

36(1)(viia) of the Income Tax Act

24

NBFCs are RBI regulated entities and are required to make provisions for NPAs in

accordance with the applicable RBI guidelines concerning income recognition and provisioning

norms. The provisions of Section 36(1)(viia) of the Income tax Act allow the banks a deduction

to the extent of 7.5% from the gross total income and 10% of aggregate average rural advances

towards provisions for bad and doubtful debts made by them. Alternatively, such banks have

been given an option to claim a deduction in respect of any provision made for assets classified

by the RBI as doubtful assets or loss assets to the extent of 10% of such assets.

Recommendation – Since the NBFCs are also RBI regulated entities and are required to make

provisions for NPAs as per applicable RBI guidelines, the benefits of Section 36(1)(viia) of the

Income tax Act may also be extended to the NBFCs, as available to the banks.

5.1.4 Declaration in Form 15G / 15H read with Section 206AA

Effective 1st April, 2010, a new Section 206AA has been introduced in the Income Tax Act

which require furnishing of the Permanent Account Number (PAN) issued by the Income Tax

Department mandatorily for all categories of payments. The mandatory quoting of PAN has

been extended to cover payment of interest without tax deduction even for those persons who

provide the declaration in Form 15G / 15H. The declaration in Form 15G / 15H are given by

those persons who have income below the taxable threshold limits, and therefore, may not have

a PAN number. Further, the details of depositors giving such declarations in Form 15G / 15H

are being furnished in the TDS Returns filed electronically every quarter and such declaration

forms are also submitted to the relevant authority as prescribed under the Income Tax Act. This

provision causes undue hardship to the small depositors, pensioners and senior citizens, etc.

whose income is below the taxable threshold, as they are also required to apply and obtain PAN

from the Income Tax Department.

Recommendation – This Group, therefore, suggests that sub-section 2 of Section 206AA may

be removed to enable the small depositors to furnish declaration forms 15G / 15H without

mandatorily furnishing PAN.

5.1.5 Introduction of the threshold limit for TDS on the interest income on unlisted debentures

“NBFC-AFCs issue secured non-convertible debentures to retail investors (individuals) in order

to raise funds. In the case of unlisted debentures, TDS is to be deducted from the interest paid,

without any minimum threshold limit. This provision proves harsh for the individuals investing

their small savings in these secured debentures.

Recommendation – This Group, therefore, suggests that clause (v) of proviso to Section 193

may be suitably amended, and the words “…, being debentures listed on a recognised stock

exchange in India in accordance with the Securities Contracts (Regulation) Act, 1956 (42 of

1956), and any rules made there-under,” may be considered for deletion.

25

5.1.6 Depreciation in respect of Construction Equipments registered under the Motor

Vehicles Act

The Income Tax Act allows depreciation at the rate of 100% in case of certain equipment used

for pollution control, solid waste control, mineral oil concerns, mines and quarries, energy saving

devices and renewable energy devices. The Act also allows high rate of depreciation to

motorcars, buses, motor lorries and taxies used in a business of running them on hire.

Construction equipments, which contribute immensely to infrastructure development, are not

given this benefit of higher depreciation rate.

In our view, Construction equipment which are used in the infrastructure development should be extended this benefit of higher depreciation rate.

5.2 INDIRECT TAX ISSUES

5.2.1 Extension of Cenvat credit rule to other services

In terms of Service Tax credit rules, currently 16 Services fall under Rule 6(5) of the Cenvat

Credit Rules wherein credit may be availed to the extent of 100% in connection with both

taxable and non-taxable services. The other services are covered by Rule 6(3) of the Cenvat

Credit Rules where one is able to claim credit either on a ratio of Taxable vs Non-Taxable

Services generated or by paying a pre-fixed percentage (8%) of the value of total turnover. This

sometimes results in a vague situation because the service is not a commodity where one is

able to identify unit-wise as to what exactly results in generation of Taxable and Non-Taxable

products, separately. This provision also leaves scope for subjective interpretation or mis-

interpretation of the provisions of law.

Recommendation – The Group, therefore, recommends that application of Rule 6(5) of Cenvat

Credit may be extended to any service that results in generation of both Taxable and Non-

Taxable services. Further, for availing the Credit, one-to-one correlation need not be insisted

upon, as in certain cases expenses have very close nexus with the generation of Taxable

Services yet as the same are falling under Rule 6(3), and thereby the claimant has no other

option but to avail Cenvat Credit on proportionate basis. Therefore, the distinction between Rule

6(3) and Rule 6(5) may be avoided, and the input credit need to be seamless.

5.2.2 Service Tax on Hire Purchase / Lease Transactions

26

Service Tax is imposed on Hire Purchase and Finance Leasing transactions. Both these

transactions have been defined as "sale" transactions. Legally also, any transaction can either

be a "Sale" or a "Service", but can not be both. Service tax is imposed on the interest

component of Hire-Purchase / Finance-Lease transactions. In addition, VAT is also levied on

the installment amounts in most of the states. Such dual taxation on transaction of lease and

hire-purchase is impacting the profitability and sustainability of financing industry. In March

2006, abatement to the extent of 90% of the interest component was allowed. In terms of small

retail customers, who depend on lease and hire-purchase for their finance needs, taxing these

products causes undue financial hardship to them.

Recommendation – The Group, therefore, recommends that the Lease and Hire-Purchase

transactions may be considered as ‘Deemed Sale’ and accordingly be subjected only to VAT,

and not Service Tax.

***

27

6. Gist of recommendation

Reference Recommendation Authority

concerned

Priority

3.3 (i) Framework and prudential norms to contain

the risks and to support and develop NBFC

sector

Reserve Bank

of India

High

3.3 (ii) Creating a comprehensive data-bank of

NBFCs to ascertain the funding pattern of

NBFCs

Reserve Bank

of India

High

3.3 (iii) Exemption to the NBFCs under Section 67

of the Companies Act may be continued for

'private placement'.

Ministry of

Corporate

Affairs

High

3.3 (iv) Tolerance limit of 15% for the negative mis-

matches over one year time buckets may

be restored

Reserve Bank

of India

Medium

3.3 (v) For the purpose of computing total financial

assets, investments in liquid funds of

mutual fund should also be included in the

eligible liquid instruments apart from G-Sec,

T-Bills, etc.

Reserve Bank

of India

Medium

3.3 (vi) Raising perpetual bonds may be permitted

to both deposit-taking systematically

important and non-deposit taking

systematically important NBFCs

Reserve Bank

of India

Medium

3.3 (vii) Tier-I CRAR requirement for the NBFCs

may be retained at 10%

Reserve Bank

of India

High

3.3 (viii) Prescribing a calibrated risk-weighted

regime for the NBFC sector

Reserve Bank

of India

High

3.3 (viii) The risk-weight for asset financing /

financial inclusion / SME businesses be

reduced to 50%

Reserve Bank

of India

Medium

3.3 (viii) Loan against property where shares are

only taken as secondary collateral (property

being the main security), risk-weight may be

prescribed as 100%

Reserve Bank

of India

Medium

3.3 (ix) Sub-limit for borrowing by NBFCs may be

removed

Reserve Bank

of India

High

28

3.3 (x) Current NPA classification norms for

NBFCs may continue

Reserve Bank

of India

Medium

3.3.1 The regulatory prescriptions should be

gradual and duly phased-out so as not to

create policy uncertainties

Reserve Bank

of India

High

3.3.2 LCs need to be differentially regulated from

ICs

Reserve Bank

of India

Medium

4.1 Change in control or transfer of

shareholding of an NBFC - requirement of

information to the RBI should be mandated

Reserve Bank

of India

Medium

4.1 Concept of ‘deemed approval’ should also

be provided in cases where the RBI does

not communicate its approval / rejection

within a certain prescribed reasonable

period

Reserve Bank

of India

High

4.2 Public funds’ should not include loans /

deposits from the Holding Company if

funded through internal accruals

Reserve Bank

of India

Medium

4.3 NBFCs may be allowed to undertake

participative financing

Reserve Bank

of India

Medium

4.4 RBI to consider including fixed deposits

under financial assets for the purpose of

computing principal business of an NBFC

Reserve Bank

of India

Medium

4.5 Bank credit for NBFCs for priority sector

lending

Reserve Bank

of India

High

4.6 ECB financing for NBFCs Reserve Bank

of India

Medium

4.7 Prudential norms for certain categories of

NBFCs to be more relaxed

Reserve Bank

of India

Medium

4.8 Lending to stock brokers and merchant

banks

Reserve Bank

of India

Medium

5.1.1 Tax Deduction at Source on Interest

(Section 194A of the Income Tax Act)

Department of

Revenue

High

5.1.2 Tax benefits for Income deferral under

Section 43D of the Income Tax Act

Department of

Revenue

High

5.1.3 Allowing of provisions made for Non-

performing Assets (NPAs) under Section

Department of High

29

36(1)(viia) of the Income Tax Act Revenue

5.1.4 Declaration in Form 15G / 15H read with

Section 206AA

Department of

Revenue

Medium

5.1.5 Introduction of the threshold limit for TDS

on the interest income on unlisted

debentures

Department of

Revenue

Medium

5.1.6 Depreciation in respect of Construction

Equipments registered under the Motor

Vehicles Act

Department of

Revenue

High

5.2.1 Extension of Cenvat credit rule to other

services

Department of

Revenue

Low

5.2.2 Service Tax on Hire Purchase / Lease

Transactions

Department of

Revenue

Medium

***

30

7. Conclusion

The recommendations made in Chapter 3 and 4 of the Report are aimed at removing

the bottleneck and introducing measures and creating a prudential environment for

effective functioning of the NBFCs in the country. The Group is of the opinion that the

recommendations are critical for the growth of NBFCs; and also for achieving the

broader objectives of financial inclusion and extension of effective prudential framework

for the entire financial sector including NBFCs.

The Group appreciates the initiative of the Government and conveys its gratitude for the

opportunity given to study the NBFC sector and make recommendations for the orderly

and systematic development of the NBFC sector enabling these important entities to

contribute to the development of Indian economy. Finally, it is recommended that the

Key Advisory Group on NBFCs should function as a standing committee and meet at

regular intervals to review the progress and developments on an ongoing basis.

Sd/- (K. Unnikrishnan)

Indian Banks’ Association

Sd/- (M.R. Umarji)

Indian Banks’ Association

Sd/- (Ved Jain)

ASSOCHAM

Sd/- (N. Sivaraman)

L&T Finance Holdings

Sd/- (Sunil Sanghai)

MD, HSBC

Sd/- (Suhan Mukerji)

Amarchand Mangaldas

Sd/- (H. Jayesh Shah)

Juris Corp

Sd/- (Ashwin Parekh)

Ernst & Young

Sd/- (R Sridhar)

MD, Sriram Transport

Sd/- (T.T. Srinivasaraghvan)

Chairman, FIDC

Sd/- (Raman Agarwal) Co-Chairman, FIDC

Sd/- (Arun Duggal)

Shriram Capital Ltd.

Sd/- (Sanjeev Gupta) Nexgen Financial Solutions Pvt. Ltd.

Sd/- (Dr. Rajiv Kumar)

Secretary General FICCI

Sd/-

(Dr. Shashank Saksena) Director (DFS) and Member Secretary

Sd/- (Alok Nigam)

Joint Secretary (BO), DFS and Chairman

31

ANNEX

IMMEDIATE F.No.17/7/2011-BO.II Government of India Ministry of Finance

Department of Financial Services

IIIrd Floor, Jeevandeep Building,Parliament Street, New Delhi, 30th September, 2011

ORDER

Subject: Constitution of a Key Advisory Group on Non Banking Finance Companies (NBFCs).

A Key Advisory Group has been constituted under the Chairmanship of Shri

Alok Nigam, Joint Secretary (Banking Operations) in this Department to examine the

issues in NBFCs. The composition of the Group is as under –

i. Shri Alok Nigam, Joint Secretary (BO) – Chairman

Members

ii. S. K. Pable, DGM, DNBS, RBI. iii. Shri K. Unnikrishnan, Dy. Chief Executive, IBA iv. A representative each of IIM, FICCI, CII, PHDCCI and Assocham v. Shri TT Srinivasaraghvan, Chairman, FIDC & MD, Sundram. Finance Ltd.

(Alternate representation - Shri Raman Agarwal, Co-Chairman, FIDC). vi. Shri H Jayesh Shah, Juris Corp. vii. Shri Ashvin Parekh, Ernst & Young. viii. Shri Suhaan Mukerji, Amarchand Mangaldas. ix. Shri R Sridhar, MD, Shriram Transport Finance Co. Ltd. x. Director (BO.II&PR), DFS, New Delhi – Member Secretary.

2. The ‘Terms of Reference’ of the Group is in Appendix.

3. The Group will meet at such places and intervals, as decided by the Chairman.

(D.D. Maheshwari) Under Secretary to the Government of India

Tel: 23748750

32

To

i. Shri Alok Nigam, Joint Secretary (BO), DFS, New Delhi ii. Director (BO.II&PR), DFS, New Delhi iii. S. K. Pable, DGM, DNBS, RBI. iv. Shri K. Unnikrishnan, Dy. Chief Executive, IBA, Mumbai v. Shri TT Srinivasaraghvan, Chairman, FIDC, New Delhi. vi. Shri Raman Agarwal, Co-Chairman, FIDC, New Delhi. vii. Shri H Jayesh Shah, Juris Corp., Mumbai. viii. Shri Ashvin Parekh, Ernst & Young, Mumbai. ix. Shri Suhaan Mukerji, Amarchand Mangaldas, New Delhi. x. Shri R Sridhar, MD, Shriram Transport Finance Co. Ltd., Mumbai. xi. Director, Indian Institute of Management, Ahmedabad, Gujrat. xii. Dr. Rajiv Kumar, Secretary General, FICCI, New Delhi. xiii. Shri Chandraji Banerjee, Director General, CII, New Delhi. xiv. Shri Girish Menon, Executive Officer, PHDCCI, New Delhi. xv. Shri D.S. Rawat, Secretary General, Assocham, New Delhi

Copy for information to –

1. PS to FM 2. PS to MoS (E&FS) 3. PPS to Secretary (FS) 4. PS to AS(FS) 5. PSs to JS(BA) / JS (BO) / JS(IF) / JS(VPB) / JS(P&I) / JS(AB) / EA 6. All Directors / Deputy Secretaries / Under Secretaries 7. All Sections in DFS

33

8.

APPENDIX F.No.17/7/2011-BO.II Government of India Ministry of Finance

Department of Financial Services

The Terms of Reference of the Key Advisory Group on NBFCs

i. Review of existing legal / regulatory / institutional framework for

NBFCs and its efficacy;

ii. Action plan including policy initiatives for orderly growth of the Sector;

iii. To recommend the legal / institutional / regulatory initiatives related

measures required for orderly growth of the Sector.

***