Embed Size (px)

Citation preview

GREEN BANKING PRACTICES AND ITS IMPLICATION ON FINANCIAL PERFORMANCE OF THE COMMERCIAL BANKS

IN BANGLADESH

Ireen Akhter *

Shakila Yasmin **

Nusrat Faria ***

Abstract

Green banking means incorporation of environmental issues in all sorts of banking activities ranging from communication to clients, marketing, service delivery, in house operations to selection of projects to finance. The central bank of Bangladesh insists all commercial banks to implement green banking policy guidelines and make green investments. This study examines the implementation status of the green banking policy guideline and the impact of green banking practices on the financial performance (ROA, ROE, ROI) of the commercial banks in Bangladesh. By analyzing 3 years’ (2016-2018) annual reports of the commercial banks listed in Dhaka Stock Exchange the study found that over 90% of the banks have implemented majority (above 60%) of the green banking policy guidelines provided by the central bank. However, the practices of certain policies such as periodic reporting of green banking practices with standard format and external verification (policy 3.2), client education program (policy 2.5) and creation of climate risk fund (policy 1.9) are not at satisfactory level. Less than 70% of the banks have adopted these policies. Results of correlation and regression analysis indicate that green banking practices positively influence financial performance.

Keywords : Commercial Banks, Financial Performance, Green Banking.

1. INTRODUCTION

Going green is the need of the time. It has been quite some time that global citizens are experiencing the effects of environmental degradation caused by the human race over the years in the name of industrial development, modernization and growth. As a response, protection of the environment and overall eco-system, and reduction of carbon foot print has become principal component of the sustainable development goals (SDGs) of the governments across the world. Policy makers and regulators are mandating all types of industries and businesses to focus on their environment foot-prints. They are also offering incentives for good environmental performance. Bangladesh is not an exception to this trend. The government is encouraging all industry sectors to adopt green operational practices. In the banking sector of Bangladesh, Bangladesh Bank has developed the comprehensive policy guidelines for green banking (GB) to ensure sustainability. Here, ‘Green Banking’ means applying

* Professor, Institute of Business Administration, Jahangirnagar University, Bangladesh** Associate Professor, Institute of Business Administration (IBA), University of Dhaka, Bangladesh*** MBA Graduate, Institute of Business Administration, Jahangirnagar University, Bangladesh

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)2

eco-friendly principles in all kinds of banking activities and prioritizing investment in businesses and projects that are friendly to the environment and/or are reducing environmental impact of other existing operations. The GB guideline formulated by Bangladesh Bank (BB) is to be executed in three phases within given timeline for each phase. BB has provided directive that all Banks in the country should gradually adopt these GB policy guidelines. It has been almost a decade since the GB directive came from BB. So, it is time to evaluate the current status of GB practices and evaluate the reasons of the lacking (if any). Many researchers in the past have scrutinized the GB section of BB annual reports to get an understanding of the GB practices (Ullah, 2020; Masud et al., 2018; Lalon, 2015; Islam & Kamruzzaman, 2015). The studies reveal that majority of the banks though have shown enthusiasm towards adopting the green banking policies, the seriousness to implement the whole policy guideline is not up to the mark in many cases and it varies across the banks. Such a scenario, emphasizes that the capitalist notion of any business is to make profit. In order to motivate the profit seeking institutions to pour money for environmental causes, a business case for doing so must be persuaded. This study therefore intends to reveal an updated view of the GB practices against the policies mandated by BB and to investigate whether there is any relationship between green banking practices and financial performance of the banks.

2. OBjECTIvES OF THE STUDy

Objective of this study is to evaluate the current status of green banking practices and its impact on financial performance of the banks in Bangladesh.

3. LITERATURE REvIEw

Green banking has been defined as incorporation of environmental issues in all sorts of banking activities ranging from communication to clients, marketing, service delivery, in house operations to selection of projects to finance. Green banking practices include mainstreaming on-line banking, reducing energy and paper consumption in every day operations, operating in green buildings that are built and run in eco-friendly manner, incorporating environmental risks while evaluating projects to finance etc. Green investment or green finance or climate finance are crucial part of green banking. Green investments or green finance means making investment in projects and/or enterprises that use eco-friendly technologies such as clean power generation, clean brick production, energy efficient and low-carbon emitting industries etc. (Hohne et al., 2012). Investment in effluent treatment plant, protection of biodiversity, industrial pollution control, water sanitation etc. are also considered as green finance (Hoshen et al., 2017).

In Bangladesh, to inspire green banking and green financing, the central bank has framed and issued a policy guideline to all scheduled banks in February 2011 and for all other new banks in September 2013. This intervention of Bangladesh Bank (BB) has a highly positive impact on the implementation of green banking (Ramnarain & Pillay, 2016; Weber & Oyegunle, 2016). Bangladesh Bank also proposed various

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 3

benefits to the country’s banking sector if they comply with green initiatives. For example, a new refinancing scheme named Green Transformation Fund (GTF) of BDT 17,000 Million was accumulated for the sustainability in export oriented textile and leather sectors , at the beginning of 2016, and BDT 3,413 million has been spent till December 2017 under this revolving “Refinance Scheme” which gave a 5% window on loan interest premium for all commercial banks (Bangladesh Bank, 2017). To comply with Bangladesh Bank, private commercial banks are channeling more funds to the green projects. They also have had the tendency to reinvest in green projects day by day (Hoshen et al., 2017). However, most of the banks and NBFIs practice green banking only in a limited scale and volume (Hoque et al., 2019). The question arises, why not all commercial banks are yet to perform green banking at its full scope. Is it that the banks are taking time and gradually moving towards green banking? Or is there not enough a business case for the profit seeking practitioners to dive deep in green banking and finance? We have explored literature on green banking and green finance in Bangladesh and found that most of the literature have presented a review of the status of green banking practices by the commercial banks at aggregate level (Ullah, 2020; Islam & Kamruzzaman, 2015; Lalon, 2015; Shakil et al., 2014). Other researchers such as Masukuzzaman and Akter (2013) investigated the implementation status of the green banking policies and guidelines. They also have done a comparison with global green banking initiatives. Rahman et al. (2013) examined the prospects of green banking in Bangladesh. They asserted that green banking initiatives will bring changes in six main spheres of banking activities, namely-investment management, deposit management, house-keeping, recruitment and human capital development, CSR practices, and consciousness among clients and general mass. Ullah (2013) conducted a comparative evaluation of green banking practices by different types of banks in Bangladesh namely state owned, private, foreign and specialized using three-year data over 2012-2014 period, However, all these researches have used aggregate data from the annual report of Bangladesh Bank. Only few studies have investigated individual bank’s performances on green banking and green finance. For example, Julia and Kassim (2019) did a comparison between green banking performance of Islamic commercial banks and conventional commercial banks. They examined green banking and financing data over the period 2012-2014 for 10 selected commercial banks. Hossain et al. (2016) investigated disclosure of Green Banking issues by the Banks in Bangladesh. They analyzed annual reports over period 2011-2013 of top 10 (on the basis of total assets as of 2013) commercial banks listed in DSE. Hence, there is a gap in literature in terms of micro-level analysis of green banking practices. Julia and Kassim (2019) thrived to mitigate this gap, but they took only 11 banks in their sample. The study conducted by Hossain et al. (2016) has the same issue, moreover the focus of the study was disclosure of green banking not the adoption status of green banking policies and guideline. Therefore, the researchers of this study intend to mitigate this gap by doing a micro-level (individual bank level) evaluation of the green banking and financings practices against the policy guidelines provided by BB. Policy-wise level of adoption by the banks and bank-wise level of adoption of the policies are investigated to pin-point which policies are not getting adequate attention

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)4

by the banks as well as to outline the overall distribution of the banks in terms of compliance with the GB policies.

Considering the fact, that green initiatives and corporate environmental performances demonstrate positive impact on firm financial performance (Ganda et al., 2015; Iwata & Okada, 2011; King & Lenox, 2001) we explored literature focusing on the impact of green banking and/or finance on financial performance of banks. In this regard, we have got a lot of studies from different countries across the world (Zhou et al., 2021; Laskowska, 2018; Rajput et al., 2013; Nanda & Bihari, 2012). However, in case of Bangladesh, the literature is very meek. Julia and Kassim (2016) explored whether there are any significant differences among the different types of commercial banks (i.e., state owned, conventional, Islamic, foreign) in terms of profitability ratios and green financing utilization. They found that different types of banks have significantly different profitability ratios but they don’t differ significantly in green financing utilization. Another study by Rahman et al. (2018) investigated the impact of green financing on profitability of banks in Bangladesh. Data from purposively selected 11 private commercial banks over the period 2013-2015 were used in their analysis. Green finance to total finance, asset and equity ratios were used as independent variables and ROI, ROE and ROA as the dependent variable. General descriptive, correlation and regression analysis were done. Green financing to total investment ratio showed significant positive association with ROI but not with ROA and ROE. The above-mentioned studies considered the impact of green financing only (which is a part of green banking) and left out the other aspects of green banking. The present study mitigates that gap in literature by using two measures of green banking i.e., green finance ratio and green banking compliance ratio. This research thus intends to provide a more comprehensive insight about the impact of green banking on financial performance of commercial banks operating in Bangladesh.

4. METHODOLOGy

4.1 Sample and Data Sources

Data regarding the green banking policies and guidelines in place are collected from Bangladesh Bank Green Banking Guideline. Sustainability report section of the published annual reports of DSE listed commercial banks are analyzed to evaluate the current state of green banking practices and their disclosure in Bangladesh. Financial performance and green investment data are also collected from published annual reports. Published literature and policy papers are scrutinized for overall understanding to the green banking practices in Bangladesh.

The population of this study comprises of all the commercial banks operating in Bangladesh. Out of 58 scheduled commercial banks 30 are listed in Dhaka Stock Exchange (DSE). For data accessibility, only the listed commercial banks are chosen as sample of this study because they regularly publish annual reports. Last 3 years’ (2016-2018) data are analyzed.

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 5

One of the prime objectives of this study is to empirically find the linkage between green banking and financial performance. Green financing is an important aspect of green banking. So, for this analysis, we need green financing disbursement amount of these listed banks. Upon review of annual reports, we discovered that 9 banks out of the 30 listed commercial banks did not report green financing information over this three-year period. We found 1 bank that started disclosing green financing data since 2017. That leaves us with a sample 60 bank-year when we are concerned about green financing.

4.2 Analysis Technique

For data analysis we have used a mix of quantitative and qualitative approach. Thematic analysis is done to evaluate current state of green financing policies, practices, and disclosure in annual reports. In order to investigate the relationship between financial performance and green financing we have conducted regression and correlation analysis by using Statistical Package for Social Sciences (SPSS) version 25.

4.3 variables

A brief description of both the dependent and independent variables of the study is given below.

4.3.1 Dependent variables

Financial performance is considered to be the dependent variable of this study. There are two approaches to measure financial performance- a) accounting-based approach and b) market-based approach. Market-based approach take market determined data like share price of a company or market share in relation to competitors in the market or growth in market share. These measures may lack objectivity due to anomalies and imperfections in the market (Soana, 2009; Tafti, 2012). Accounting-based measures on the other hand are very much objective (Soana, 2009; Taskın, 2015; Wu & Shen, 2013). Due to this objectivity, we have used accounting-based measures of financial performance. Among the various accounting-based performance measures, we have chosen three widely used profitability ratios namely i) Return on Assets (ROA), ii) Return on Equity (ROE) and iii) Return on Investment (ROI) (Kosmidou, 2008; Sufian & Habibullah, 2009).

Return on Asset (ROA)

ROA is the net profit expressed as a percentage of total assets. It represents profit earned per unit of assets and indicates the efficiency of the asset management. ROA is commonly used as an indicator of competence and operational efficiency of banks since it addresses the profit earned from the assets employed by the bank (Jahan, 2012). Furthermore, ROA is not affected by high equity multipliers (Rivard & Thomas, 1997). The formula used to measure ROA is as follows-

ROA = Net after tax incomeAverage total assets

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)6

Return on Equity (ROE)

Another widely used measure of profitability is ROE. It refers to the ratio of the profits a company generates to the total amount of shareholders’ equity found in the balance sheet (Ongore & Kusa, 2013). Although researchers like Flamini, Mcdonald and Schumacher (2009) and Hassan and Bashir (2005) claim that ROE is not a good proxy of a financial performance because the ratio does not include the borrowed fund; hence is affected by the degree of financial leverage (equity to debt ratio) and ROA. Banks may utilize financial leverage heavily and still generate higher ROE than the competitors but result ROA lower than that of the competitors. However, ROE reflects the efficiency in generating income for an organization’s (in this case bank’s) shareholders whose value maximization is the ultimate goal of any company. So, ROE is another measure of firm performance that we have used in this research. Following formula is used to measure ROE-

ROE = Net after tax incomeAverage shareholders’ equity

Return on Investment (ROI)

ROI is another commonly used measure of profitability. It determines the effectiveness of investment. In other words, it is a way of relating profits to capital invested (Finanace Reference, 2020). Following several previous studies, we decided to use ROI as another measure of financial performance. (Jacobson, 1987; Andru & Botchkarev, 2011). The formula to calculate ROI is given below-

ROI = Earnings before interest and taxAverage total investment

4.3.2 Independent variable

Green Banking (GB) is an approach of delivering banking services in an environment friendly manner and thriving to reduce carbon foot print. It involves reorientation/ reinvention of banking products/services and operational, and strategic activities with an objective to reduce environmental impact of banks. Two variables are used to measure green banking performance- i) GB initiatives score ii) Green finance ratio.

GB Initiatives Score and GB Compliance Rate

The central bank of Bangladesh has prepared and circulated policy guideline for GB practices to the banks operating in Bangladesh. Using those policy guidelines as a framework, GB initiatives score (GBIS) is calculated for each bank. To do this, GB initiatives taken by the banks are tallied against the policy framework. Compliance on each guideline is scored as 1, non-compliance is scored as 0 and partial compliance as 0.5; aggregate GBIS is calculated by adding up all these scores. The numerical score is then converted to ratio by dividing this aggregate score by total score of 18 for 18 policies. This ratio is named as GB compliance rate (GBCR)

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 7

Green Finance Ratio

Green finance is channeling funds to environment friendly projects. In other wording, providing loans and/or refinancing to projects that are likely to contribute towards conserving the environment and/or reducing the harmful effect on environment. For the purpose of this study, green finance ratio (GFR) is calculated by dividing total amount of fund channeled to green projects by total investment made over a particular period. Some previous studies such as Rahman, Huq and Roy (2018); Julia and Kassim (2016) and Zhou, Sun, Luo and Liao (2021) used this ratio.

4.4 Hypothesis of the Study

Green banking policy implementation requires commercial banks to cut energy cost by using cleaner technologies. It also requires banks to reduce consumption of paper, travel cost and other resources by mainstreaming online communication and virtual data storage. Such initiatives reduce operating and general and administrative expenses. Green banking spree also encourage banks to launch innovative online and digital services, which generate new revenue stream and enhance market reach (Song, Deng & Wu, 2019). Moreover, incorporation of environmental risks while assessing credit risk makes the credit evaluation system of the banks more stringent that is likely to enhance asset quality of the banks and reduce non-performing loan (NPL) (Wörsdörfer, 2015). Green projects are by nature less risky compared to traditional projects, hence can effectively curb NPL and increase expected earnings (Sun, Ying & Qinghai, 2017). Green banking and green financing enhance the responsible social image, reputation and competitiveness of commercial banks (Eshet, 2017; Wang, 2016; Cowtown & Thompson, 2000) which in turn increase profitability and/or financial performance. We can therefore hypothesize that green banking has positive influence on financial performance of the commercial banks. The following statements thus formulate the broad null and alternate hypotheses of this study-

Ho : There is no relationship between Green banking practices and financial performance of banks.

Ha : There is positive relationship between Green banking practices and financial performance of banks

Given the proxies of green banking and financial performance presented in subsection 4.3, following specific hypotheses (null and alternate) can be derived from the above stated broad hypothesis.

H1o: GBCR and GFR have no impact on ROA

H1a: GBCR and GFR have positive impact on ROA

H2o: GBCR and GFR have no impact on ROE

H2a: GBCR and GFR have positive impact on ROE

H3o: GBCR and GFR have no impact on ROI

H3a: GBCR and GFR have positive impact on ROI

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)8

Table 1 : Variable, Notation, Measurement, Units and Expected Impact on Different Variables

variable Notation Measurement ExpectedImpact

Return on Asset ROA Net after tax income /Average of Total Assets +

Return on Equity ROE Net after tax income/Average of Total Equity +

Return onInvestment ROI Earnings before interest and tax/

Average of Total Investment +

Green BankingCompliance Rate GBCR GBIS/18 +

Green FinanceRatio GFR Green Investment/AverageTotal

Investment +

Based on the above hypotheses following relational models are expected which will later be tested through regression analysis-

ROA = β0 + β1 (GBCR) + β2 (GFR) + ε

ROE = β0 + β1 (GBCR) + β2 (GFR) + ε

ROI = β0 + β1 (GBCR) + β2 (GFR) + ε

Where, β0 is the constant term; β1 and β2 are the coefficients of GBCR and GFR and ε is the error term

5. FINDINGS OF THE STUDy

This section presents the findings of the study. First, the implementation status of the major green banking policies is presented. Then descriptive statistics of the green banking initiative score (GBIS), green financing (GF) and financial performance of the sample banks are presented. Finally, the influence of green banking on financial performance is revealed.

5.1 Implementation Status of Major Green Banking Policies

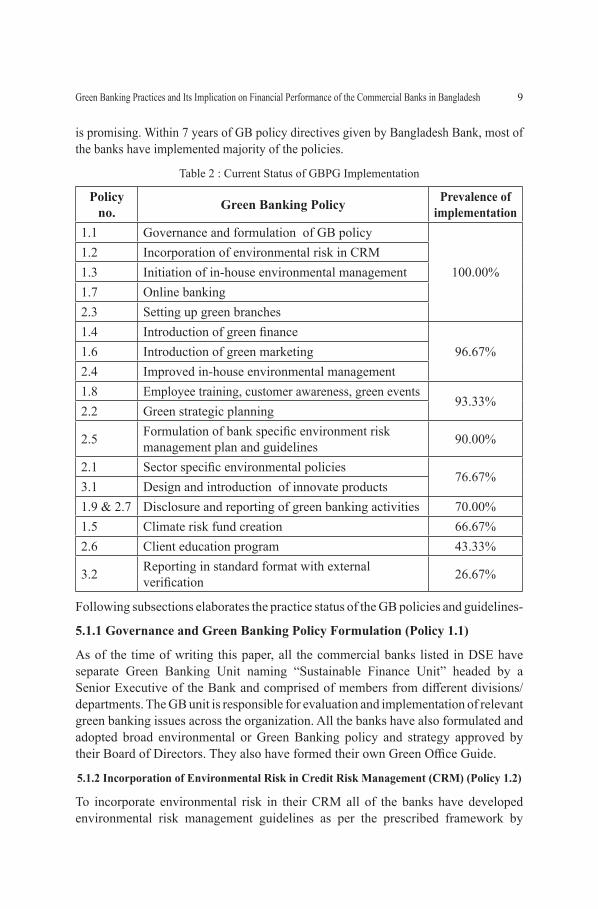

In 2013, through GBCSRD Circular Letter No. 5 titled “Policy Guidelines for Green Banking”, Bangladesh Bank has clearly given directives about green banking that need to be followed by the banks and reported in their quarterly and annual statements. There are 18 policies in the green banking policy guideline (GBPG)– Phase I: policies 1.1 to 1.9, Phase II: policies 2.1 to 2.7 and Phase III: policies 3.1, 3.2. Table 2 presents the current status of implementation of these policies by the DSE listed commercial banks in Bangladesh. All of the banks (100%) have implemented policies 1.1, 1.2, 1.3, 1.7 and 2.3; 96.67% of them are practicing policies 1.4, 1.6 and 2.4 and 93.33% have implemented policies 1.8 and 2.2. Policies 2.1 and 3.1 is implemented by 76.67% of the banks considered for this study. Policies 1.5, 2.5, 2.6, 2.7 & 1.9, and 3.1 are implemented by 66.67%, 90%, 43.33%, 70% and 26.67% of the banks respectively. Overall, implementation status of the GB policies

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 9

is promising. Within 7 years of GB policy directives given by Bangladesh Bank, most of the banks have implemented majority of the policies.

Table 2 : Current Status of GBPG Implementation

Policy no. Green Banking Policy Prevalence of

implementation1.1 Governance and formulation of GB policy

100.00%1.2 Incorporation of environmental risk in CRM1.3 Initiation of in-house environmental management1.7 Online banking2.3 Setting up green branches1.4 Introduction of green finance

96.67%1.6 Introduction of green marketing2.4 Improved in-house environmental management1.8 Employee training, customer awareness, green events

93.33%2.2 Green strategic planning

2.5 Formulation of bank specific environment risk management plan and guidelines 90.00%

2.1 Sector specific environmental policies76.67%

3.1 Design and introduction of innovate products1.9 & 2.7 Disclosure and reporting of green banking activities 70.00%1.5 Climate risk fund creation 66.67%2.6 Client education program 43.33%

3.2 Reporting in standard format with external verification 26.67%

Following subsections elaborates the practice status of the GB policies and guidelines-

5.1.1 Governance and Green Banking Policy Formulation (Policy 1.1)

As of the time of writing this paper, all the commercial banks listed in DSE have separate Green Banking Unit naming “Sustainable Finance Unit” headed by a Senior Executive of the Bank and comprised of members from different divisions/ departments. The GB unit is responsible for evaluation and implementation of relevant green banking issues across the organization. All the banks have also formulated and adopted broad environmental or Green Banking policy and strategy approved by their Board of Directors. They also have formed their own Green Office Guide.

5.1.2 Incorporation of Environmental Risk in Credit Risk Management (CRM) (Policy 1.2)

To incorporate environmental risk in their CRM all of the banks have developed environmental risk management guidelines as per the prescribed framework by

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)10

Bangladesh Bank. While evaluating investment projects, all the banks consider both investment and environmental risk. Environmental risk has been integrated with credit appraisal procedure of the banks.

5.1.3 Initiation of In-house Environmental Management (Policy 1.3)

All the banks have taken in-house environmental management initiatives. Solid wastes are reduced by adopting 3R approach (Reduce, Reuse and Recycle) in day to day activities of the banks. All divisions and branches maintain a stock in-out register to prevent misuse of papers. The banks are building infrastructure and systems to ensure efficient use of gas, fuel, electricity and water with a view to reduce carbon emission. They encourage employees to use Public Transport/Carpool Program and to use eco-friendly energy for private vehicles.

5.1.4 Green Finance (Policy 1.4)

Except ICB Islamic Bank Limited all other banks have already introduced green financing. Banks are focusing on financing in the environment friendly sectors and projects and energy efficient industries. Most of the banks give preferences to environment conserving infrastructure projects including adoption of renewable energy, energy-efficient technology, supply of clean water etc.

5.1.5 Creation of Climate Risk Fund (Policy 1.5)

Among 30 banks, 20 banks have already created climate risk fund. Based on the assessment of environmental risks of financing in climate-vulnerable areas, namely flood, cyclone and draught prone areas in Bangladesh, these banks allocate a Climate Risk Fund for financing in those climate-vulnerable areas. The Fund is created as part of Banks, CSR budget.

5.1.6 Green Marketing (Policy 1.6)

Green Marketing refers to the marketing and promotion of products and services that are presumed to be environmentally friendly or are positioned or marketed in an environment-friendly platform. Among 30 banks all of the banks except Shahjalal Islami Bank Limited do green marketing. This bank announced that they will introduce green marketing very soon.

5.1.7 Online Banking (Policy 1.7)

Online banking refers to the practice of making bank transactions or paying bills via the Internet on a secure website of the respective bank that allows the customers to make deposits, withdrawals and pay bills. All of the banks are providing online banking services through its all branches with giving more emphasis on saving the environment by eliminating paper waste, saving gas and carbon emission, reducing printing costs and postage expenses.

5.1.8 Employee Training, Consumer Awareness and Green Event (Policy 1.8)

Except SIBL, rest 29 banks conduct training program on Green Banking for their employees throughout the year as an integral part of the bank’s human resource

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 11

development process. Banks are also organizing different green events on a continuous basis to develop awareness among the clients and other stakeholder groups on various environmental and social risk related issues through leaf-let, electronic media, print media etc.

5.1.9 Disclosure and Reporting of Green Banking Activities (Policy 1.9 and 2.7)

Among 30 banks listed in the Dhaka stock exchange, all banks provide at least some basic information about Green Banking on their annual report. However, only 15 banks disclose sector wise, product wise and total disbursement details amounts, and highlights of past performance, current activities and initiatives, and future strategies in their annual reports. They regularly report their Green Banking Activities to Bangladesh Bank on quarterly basis. Moreover, they have a separate section in Bank’s official website for disclosing Green Banking activities. About 30% (9 out of 30) of the banks share only subjective information about the green banking policies they have adopted, relevant employee training and customer awareness programs they have launched, their green internal activities, green baking services, green products, and environmental policies. These banks don’t disclose the amount they disburse for Green banking. The rest 6 banks (20%) disclose just the total amount they disburse for Green banking along with few subjective information.

5.1.10 Sector Specific Environmental Policies (Policy 2.1)

About 76.7% (23 out of 30) of the banks have already developed their own Sector Specific Environmental Policies and some of the banks are still on the process of implementing this. In this regard, the banks have adopted Sector Specific Environmental Policies for financing some of the following sectors: Agriculture, Agri-business (Poultry and Dairy), Agro farming, Leather (Tannery), Fisheries, Renewable Energy etc.

5.1.11 Green Strategic Planning (Policy 2.2)

Among 30, 28 banks make green strategic planning by adding value to existing product portfolio by inserting environmental features; using environmental themes, slogans and/or in marketing and promotional activities and highlighting eco-benefits from financing the green products.

5.1.12 Setting up Green Branches (Policy 2.3)

Only Mutual Trust Bank (MTB) has built its two corporate office buildings as fully green buildings. No other banks have fully green branches but they are striking to make its existing branches and new branches “Green” by doing the following-

n Emphasizing on reduction and waste minimization strategy in terms of resources like electricity, water, paper, energy (Petrol /Gas / Octane / Diesel) etc.

n Adopting necessary steps for Reducing, Reusing and Recycling, in terms of both materials and equipment.

n Improving understanding and awareness development among the employees on various environmental and social risk related issues and green banking aspects.

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)12

5.1.13 Improved In-house Environment Management (Policy 2.4)

Except Mercantile Bank Limited, all other banks have improved in-house environmental management.

Banks are switching to more environment-friendly technologies aimed at greater work efficiency; reduction of paper and energy consumption, and subsequent Green House Gas emission. They also reduced some capital expenditure by using cloud-based computing, mobile and other communication technologies. Electronic archival of customer documents, using electronic medium for internal and external communication, SMS-based communication and notification, virtual meetings through video conferencing in lieu of physical travelling etc. are contributing towards energy, paper and stationeries savings and low carbon emission.

5.1.14 Formulation of Bank Specific Environment Risk Management Guidelines (Policy 2.5)

All banks except three of them have formulated specific environment risk management guidelines in light of the directives provided by Bangladesh Bank. While evaluating projects, environmental risk rating (EnvRR) is incorporated with general CAMEL (Capital, Asset, Management, Efficiency and Liquidity) rating. Asset quality is adjusted with underlying environmental risks.

5.1.15 Client Education Programs (Policy 2.6)

Commercial banks in our sample are lagging to take up client education program. Only 43.3% of the banks have made some progress in this aspect of GB policy guideline. Most common initiative to educate clients about GB and its advantages are through slogans such as –‘Save paper, save trees’, ‘Conserve energy, conserve natural resources’, ‘Pay your bills online’, ‘Turn off the tap when not needed’, ‘Always use a cloth bag’, ‘Reduce, reuse and recycle’ etc. Banks promoting this kind of slogans post them in all sorts of communication materials (physical or virtual) they use. Other client education program may involve educative campaign or advertisements, information sharing workshops, webinars, environment conserving social activities etc.

5.1.16 Designing and Introducing Innovative Products (Policy 3.1)

About 76.7% of the banks have introduced various innovative products as part of their GB initiatives. For example, Mercantile bank has introduced “MBL Shakti” to finance for installation of effluent treatment plant, solar energy and bio-gas plant, and “MBL Hybrid Hoffman Kiln (HHK)” for environment friendly brick field finance. United Commercial Bank has introduced “Upay”; whereas, Brac Bank, Dutch Bangla Bank and many others have introduced mobile banking service as environment friendly innovative products/ services.

5.1.17 Reporting in Standard Format with External Verification (Policy 3.2)

This is the least practiced GB policy provided by Bangladesh Bank. Among 30 banks, only 8 have been following standard format for regular reporting of GB practices and initiatives by the banks. Those who use standard format also get external verification of their GB report. For GB reporting purpose, these banks use Global

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 13

Reporting Initiatives (GRI) framework, which is a benchmark to show organizational performance with respect to laws, norms, codes, performance standards and voluntary initiatives and to demonstrate organizational commitment to sustainable development. The framework also captures and helps in comparing sustainable performance of banks. It is mentionable that, National Center for Sustainability Reporting (NCSR), Indonesia has awarded “GOLD“ rank to Prime Bank in Asia Sustainability Report (ASR) rating in 2017. Bank Asia achieved this rank in 2018. Disclosure of Green Banking Issues on Annual Reports

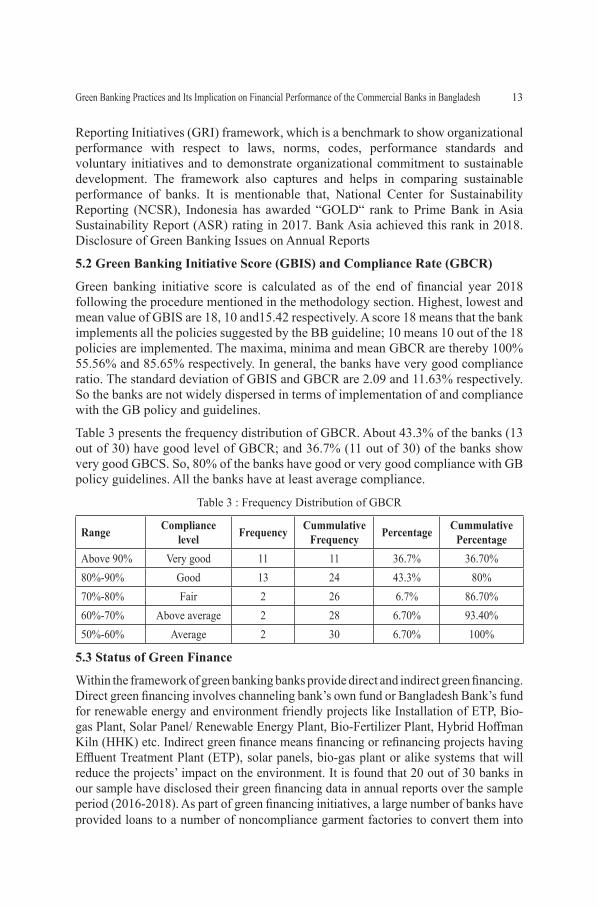

5.2 Green Banking Initiative Score (GBIS) and Compliance Rate (GBCR)

Green banking initiative score is calculated as of the end of financial year 2018 following the procedure mentioned in the methodology section. Highest, lowest and mean value of GBIS are 18, 10 and15.42 respectively. A score 18 means that the bank implements all the policies suggested by the BB guideline; 10 means 10 out of the 18 policies are implemented. The maxima, minima and mean GBCR are thereby 100% 55.56% and 85.65% respectively. In general, the banks have very good compliance ratio. The standard deviation of GBIS and GBCR are 2.09 and 11.63% respectively. So the banks are not widely dispersed in terms of implementation of and compliance with the GB policy and guidelines.

Table 3 presents the frequency distribution of GBCR. About 43.3% of the banks (13 out of 30) have good level of GBCR; and 36.7% (11 out of 30) of the banks show very good GBCS. So, 80% of the banks have good or very good compliance with GB policy guidelines. All the banks have at least average compliance.

Table 3 : Frequency Distribution of GBCR

Range Compliance level Frequency Cummulative

Frequency Percentage Cummulative Percentage

Above 90% Very good 11 11 36.7% 36.70%80%-90% Good 13 24 43.3% 80%70%-80% Fair 2 26 6.7% 86.70%60%-70% Above average 2 28 6.70% 93.40%50%-60% Average 2 30 6.70% 100%

5.3 Status of Green Finance

Within the framework of green banking banks provide direct and indirect green financing. Direct green financing involves channeling bank’s own fund or Bangladesh Bank’s fund for renewable energy and environment friendly projects like Installation of ETP, Bio-gas Plant, Solar Panel/ Renewable Energy Plant, Bio-Fertilizer Plant, Hybrid Hoffman Kiln (HHK) etc. Indirect green finance means financing or refinancing projects having Effluent Treatment Plant (ETP), solar panels, bio-gas plant or alike systems that will reduce the projects’ impact on the environment. It is found that 20 out of 30 banks in our sample have disclosed their green financing data in annual reports over the sample period (2016-2018). As part of green financing initiatives, a large number of banks have provided loans to a number of noncompliance garment factories to convert them into

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)14

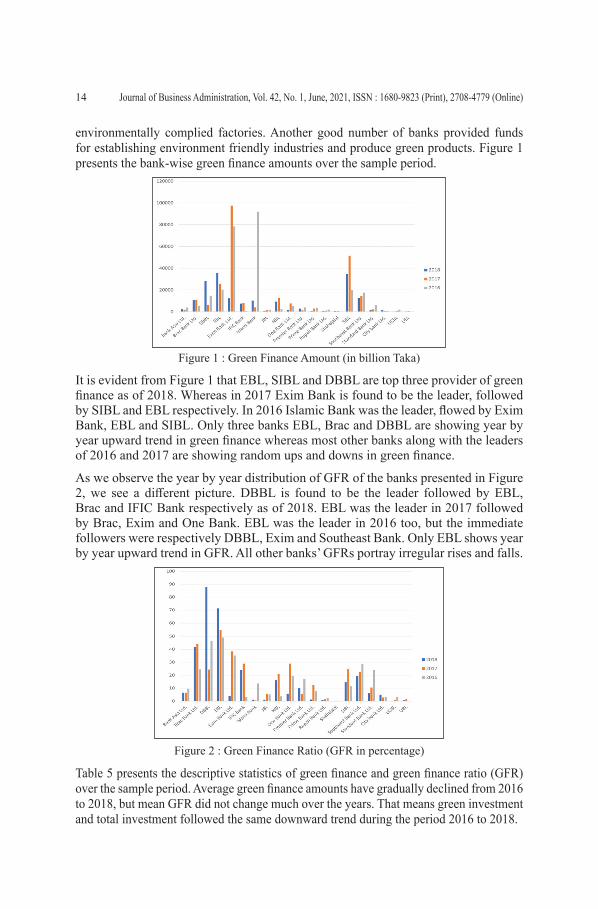

environmentally complied factories. Another good number of banks provided funds for establishing environment friendly industries and produce green products. Figure 1 presents the bank-wise green finance amounts over the sample period.

Figure 1 : Green Finance Amount (in billion Taka)

It is evident from Figure 1 that EBL, SIBL and DBBL are top three provider of green finance as of 2018. Whereas in 2017 Exim Bank is found to be the leader, followed by SIBL and EBL respectively. In 2016 Islamic Bank was the leader, flowed by Exim Bank, EBL and SIBL. Only three banks EBL, Brac and DBBL are showing year by year upward trend in green finance whereas most other banks along with the leaders of 2016 and 2017 are showing random ups and downs in green finance.

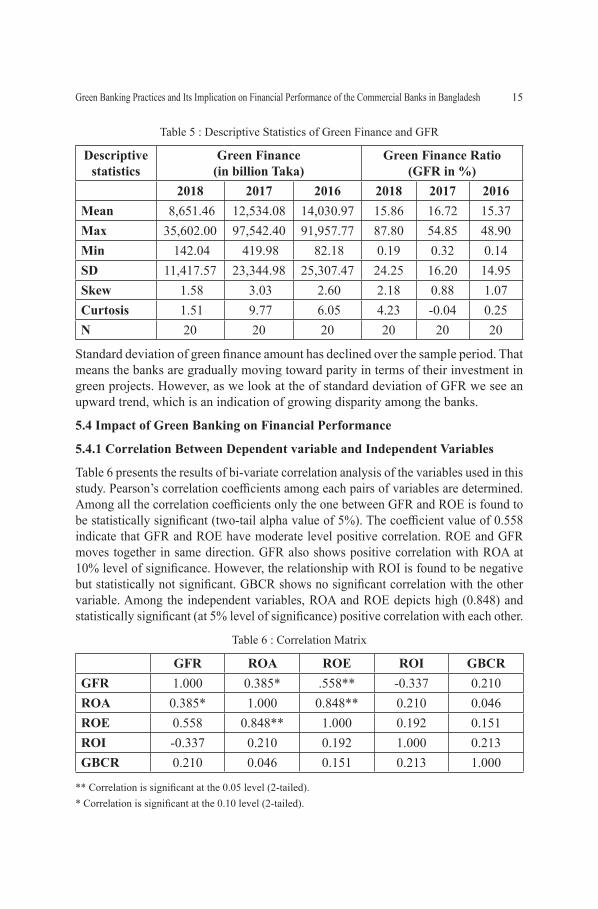

As we observe the year by year distribution of GFR of the banks presented in Figure 2, we see a different picture. DBBL is found to be the leader followed by EBL, Brac and IFIC Bank respectively as of 2018. EBL was the leader in 2017 followed by Brac, Exim and One Bank. EBL was the leader in 2016 too, but the immediate followers were respectively DBBL, Exim and Southeast Bank. Only EBL shows year by year upward trend in GFR. All other banks’ GFRs portray irregular rises and falls.

Figure 2 : Green Finance Ratio (GFR in percentage)

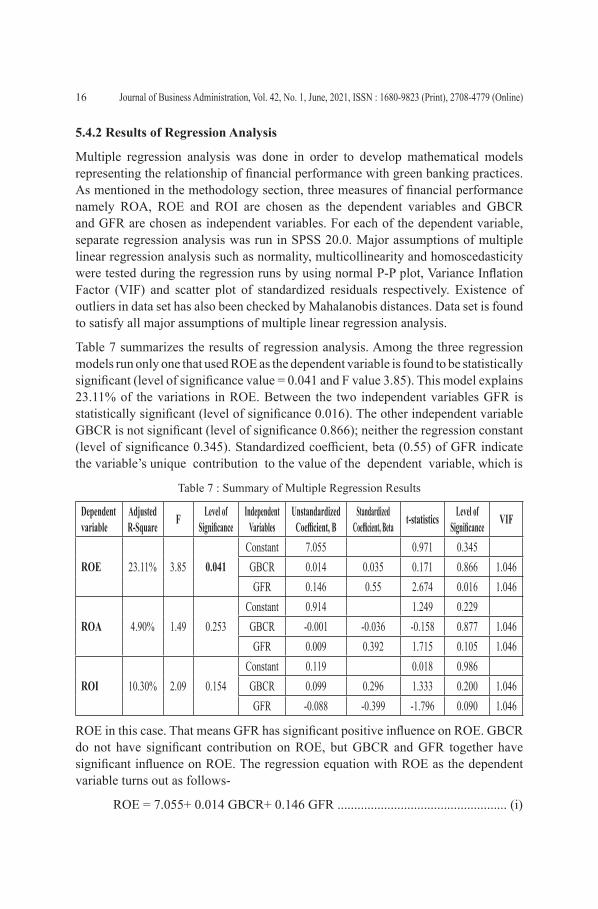

Table 5 presents the descriptive statistics of green finance and green finance ratio (GFR) over the sample period. Average green finance amounts have gradually declined from 2016 to 2018, but mean GFR did not change much over the years. That means green investment and total investment followed the same downward trend during the period 2016 to 2018.

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 15

Table 5 : Descriptive Statistics of Green Finance and GFR

Descriptive statistics

Green Finance(in billion Taka)

Green Finance Ratio(GFR in %)

2018 2017 2016 2018 2017 2016Mean 8,651.46 12,534.08 14,030.97 15.86 16.72 15.37Max 35,602.00 97,542.40 91,957.77 87.80 54.85 48.90Min 142.04 419.98 82.18 0.19 0.32 0.14SD 11,417.57 23,344.98 25,307.47 24.25 16.20 14.95Skew 1.58 3.03 2.60 2.18 0.88 1.07Curtosis 1.51 9.77 6.05 4.23 -0.04 0.25N 20 20 20 20 20 20

Standard deviation of green finance amount has declined over the sample period. That means the banks are gradually moving toward parity in terms of their investment in green projects. However, as we look at the of standard deviation of GFR we see an upward trend, which is an indication of growing disparity among the banks.

5.4 Impact of Green Banking on Financial Performance

5.4.1 Correlation Between Dependent variable and Independent variables

Table 6 presents the results of bi-variate correlation analysis of the variables used in this study. Pearson’s correlation coefficients among each pairs of variables are determined. Among all the correlation coefficients only the one between GFR and ROE is found to be statistically significant (two-tail alpha value of 5%). The coefficient value of 0.558 indicate that GFR and ROE have moderate level positive correlation. ROE and GFR moves together in same direction. GFR also shows positive correlation with ROA at 10% level of significance. However, the relationship with ROI is found to be negative but statistically not significant. GBCR shows no significant correlation with the other variable. Among the independent variables, ROA and ROE depicts high (0.848) and statistically significant (at 5% level of significance) positive correlation with each other.

Table 6 : Correlation Matrix

GFR ROA ROE ROI GBCRGFR 1.000 0.385* .558** -0.337 0.210ROA 0.385* 1.000 0.848** 0.210 0.046ROE 0.558 0.848** 1.000 0.192 0.151ROI -0.337 0.210 0.192 1.000 0.213GBCR 0.210 0.046 0.151 0.213 1.000

** Correlation is significant at the 0.05 level (2-tailed).* Correlation is significant at the 0.10 level (2-tailed).

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)16

5.4.2 Results of Regression Analysis

Multiple regression analysis was done in order to develop mathematical models representing the relationship of financial performance with green banking practices. As mentioned in the methodology section, three measures of financial performance namely ROA, ROE and ROI are chosen as the dependent variables and GBCR and GFR are chosen as independent variables. For each of the dependent variable, separate regression analysis was run in SPSS 20.0. Major assumptions of multiple linear regression analysis such as normality, multicollinearity and homoscedasticity were tested during the regression runs by using normal P-P plot, Variance Inflation Factor (VIF) and scatter plot of standardized residuals respectively. Existence of outliers in data set has also been checked by Mahalanobis distances. Data set is found to satisfy all major assumptions of multiple linear regression analysis.

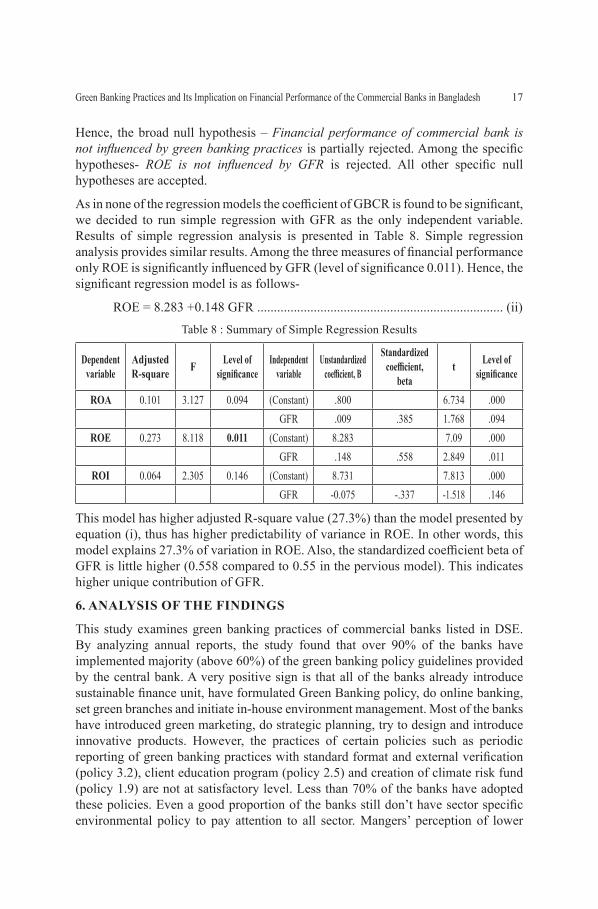

Table 7 summarizes the results of regression analysis. Among the three regression models run only one that used ROE as the dependent variable is found to be statistically significant (level of significance value = 0.041 and F value 3.85). This model explains 23.11% of the variations in ROE. Between the two independent variables GFR is statistically significant (level of significance 0.016). The other independent variable GBCR is not significant (level of significance 0.866); neither the regression constant (level of significance 0.345). Standardized coefficient, beta (0.55) of GFR indicate the variable’s unique contribution to the value of the dependent variable, which is

Table 7 : Summary of Multiple Regression Results

Dependent variable

Adjusted R-Square F Level of

SignificanceIndependent

variablesUnstandardized

Coefficient, BStandardized

Coefficient, Beta t-statistics Level of Significance vIF

ROE 23.11% 3.85 0.041Constant 7.055 0.971 0.345GBCR 0.014 0.035 0.171 0.866 1.046GFR 0.146 0.55 2.674 0.016 1.046

ROA 4.90% 1.49 0.253Constant 0.914 1.249 0.229GBCR -0.001 -0.036 -0.158 0.877 1.046GFR 0.009 0.392 1.715 0.105 1.046

ROI 10.30% 2.09 0.154Constant 0.119 0.018 0.986GBCR 0.099 0.296 1.333 0.200 1.046GFR -0.088 -0.399 -1.796 0.090 1.046

ROE in this case. That means GFR has significant positive influence on ROE. GBCR do not have significant contribution on ROE, but GBCR and GFR together have significant influence on ROE. The regression equation with ROE as the dependent variable turns out as follows-

ROE = 7.055+ 0.014 GBCR+ 0.146 GFR ................................................... (i)

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 17

Hence, the broad null hypothesis – Financial performance of commercial bank is not influenced by green banking practices is partially rejected. Among the specific hypotheses- ROE is not influenced by GFR is rejected. All other specific null hypotheses are accepted.

As in none of the regression models the coefficient of GBCR is found to be significant, we decided to run simple regression with GFR as the only independent variable. Results of simple regression analysis is presented in Table 8. Simple regression analysis provides similar results. Among the three measures of financial performance only ROE is significantly influenced by GFR (level of significance 0.011). Hence, the significant regression model is as follows-

ROE = 8.283 +0.148 GFR .......................................................................... (ii)Table 8 : Summary of Simple Regression Results

Dependent variable

Adjusted R-square F Level of

significanceIndependent

variableUnstandardized

coefficient, B

Standardized coefficient,

betat Level of

significance

ROA 0.101 3.127 0.094 (Constant) .800 6.734 .000GFR .009 .385 1.768 .094

ROE 0.273 8.118 0.011 (Constant) 8.283 7.09 .000GFR .148 .558 2.849 .011

ROI 0.064 2.305 0.146 (Constant) 8.731 7.813 .000GFR -0.075 -.337 -1.518 .146

This model has higher adjusted R-square value (27.3%) than the model presented by equation (i), thus has higher predictability of variance in ROE. In other words, this model explains 27.3% of variation in ROE. Also, the standardized coefficient beta of GFR is little higher (0.558 compared to 0.55 in the pervious model). This indicates higher unique contribution of GFR.

6. ANALySIS OF THE FINDINGS

This study examines green banking practices of commercial banks listed in DSE. By analyzing annual reports, the study found that over 90% of the banks have implemented majority (above 60%) of the green banking policy guidelines provided by the central bank. A very positive sign is that all of the banks already introduce sustainable finance unit, have formulated Green Banking policy, do online banking, set green branches and initiate in-house environment management. Most of the banks have introduced green marketing, do strategic planning, try to design and introduce innovative products. However, the practices of certain policies such as periodic reporting of green banking practices with standard format and external verification (policy 3.2), client education program (policy 2.5) and creation of climate risk fund (policy 1.9) are not at satisfactory level. Less than 70% of the banks have adopted these policies. Even a good proportion of the banks still don’t have sector specific environmental policy to pay attention to all sector. Mangers’ perception of lower

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)18

initial cash flow and margin from green projects (Tu & Dung, 2017), lack of reliable data about environmental benefit of green projects (Zhang, Yang & Bi, 2011), high operating cost (Rahman & Barua, 2016) etc. are identified as the major challenges toward implementation of green banking policies and a flight of green banking practices. Policy makers, regulators and researchers should provide evidence-based communications, trainings and support to eradicate these negative discernments. Benefits of green banking must be highlighted clearly with a focus on longer term strategic implications of the same.

The study also has found that the form and extent of disclosure differed from bank to bank. Half of the banks have provided detailed information with specific quantitative information; the other banks have only presented some general statement that lacked specificity in terms of different aspects of green banking. Such findings are very much in line with previous studies on corporate disclosure of environmental and social responsibility initiatives (Yasmin & Akhter, 2019; Hossain et al., 2016; Azim et al., 2009; Khan & Hossain, 2003; and Bala & Yusuf, 2003). By interviewing managers of non-government organizations (NGOs) Belal and Cooper (2011) identified that scarce resources, profit focus, absence of legal requirements and lack of knowledge and awareness are the major reasons of low level of disclosure in social and environmental reporting. Khan et al. (2013) argued that board independence and presence of audit committee facilitate corporate social and environmental reporting and disclosure. Referring to fast uptake of green banking policy guidelines since Bangladesh Bank provided specific directives to the commercial banks Hossain et al. (2016) argued that the central bank and other regulators are powerful stake holder to the banks. These powerful stakeholders have high influence on the activities of commercial banks. So, they suggested that regulators like the Bangladesh Bank and Security Exchange Commission (SEC) should provide specific guidelines about the structure and format and third-party verification of green baking reporting and disclosure in annual and quarterly reports. In this regard, ICAB (Institute of Chartered Accountants of Bangladesh) too can play a crucial role.

With an ambition to provide evidence-based propositions to promote green banking, the researchers of this study also investigated the influence of green banking on financial performance of the banks. Results of correlation and regression analysis indicate that green banking practices positively influence financial performance. This result is in line with that of other studies like Ganda et al. (2015); Rajput et al. (2013); Iwata and Okada (2011); King and Lenox (2001); Fledman et al. (1997) and Cordeiro and Sarkis (1997). However, between the two measures (GBCR and GFR) of green banking used in this study only GFR shows significant positive impact on financial performance measured by ROE. The influence of green banking (GBCR and GFR) on the other two measures of financial performance (ROA and ROI) is found to be statistically insignificant. The reasons behind such findings perhaps are the following- First, green banking initiatives require investment in new technologies and sometimes temporarily enhance operating expenses (Tu & Dung, 2017; Hart & Ahuja, 1996). Maybe, the cost savings from green initiatives are not enough to cover

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 19

the increased investment and asset value. Second, it takes time to realize the cost savings from lower level of waste, less consumption of papers, lower environmental tax etc. Needless to mention that getting the reputational benefits in the form of increased revenue take much longer time. If tested, we may find that GBCR and GFR have significant impact on long-term forward-looking ROA, ROI and ROE.

7. CONCLUSION

This research has clearly identified where the commercial banks are lagging in terms of green banking practices. This will help policy makers and regulators to design and develop interventions for promoting these weak areas of banking. To the best knowledge of the researchers of this study, this is the first study that investigated the relationship between green banking practices and financial performance of commercial banks in Bangladesh. By discovering positive influence of green banking on financial performance, this research takes the green banking movement a step ahead. Practitioners can refer to this finding of the research to persuade green banking agenda at boards and top management. Policy makers and regulators on the other hand can use this finding to motivate practitioners to take up green banking initiatives as mainstream agenda.

One limitation of this study is that it did not test the impact of green banking on long-term forward-looking firm performance. Researchers in future should do this investigation using time series data. Another limitation of the study is its small sample size and short sample period. Similar research on larger sample size and time frame will deduce more generalizable results. Researchers may also focus on detail analysis of individual green banking policy guideline like on-line banking, innovation in banking service delivery, integration of environmental risks in CRM etc. to get more insightful perspectives and to identify the prospects and challenges of these green banking policy initiatives.

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)20

REFERENCES

Andru, P., & Botchkarev, A. (2011). The Use of Return on Investment (ROI) in the Performance Measurement and Evaluation of Information Systems. Retrieved September 21, 2020, from https://www.researchgate.net/project/Return-on-Investment-ROI

Azim, M. I., Ahmed, S. & Islam, M. S. (2009). Corporate social reporting practice: evidence from listed companies in Bangladesh. Journal of Asia-Pacific Business, 10(2), 130-145.

Bala, S.K. & Yusuf, M.A. (2003). Corporate Environmental Reporting in Bangladesh: A Study of the Listed Public Limited Companies. Dhaka University Journal of Business Studies, XXVI(1), June, 31-45.

Bangladesh Bank. (2017). Bangladesh Bank Annual Report 2017. Retrieved May 30, 2020, from www.bb.org.bd: https://www.bb.org.bd/pub/annual/anreport/ar1617/index1617.php 501-527.

Belal, A. R. & Cooper, S. (2011). The absence of corporate social responsibility reporting in Bangladesh. Critical Perspectives on Accounting, 22, 654-667.

Cordeiro, J., & Sarkis, J. (1997). Environmental proactivism and firm performance: evidence from security analyst earnings forecasts. Business Strategy and Environment, 6, 104–114.

Cowton, Christopher J., & Paul, Thompson (2000). Do codes make a difference? The case of bank lending and the environment. Journal of Business Ethics, 24, 165–78

Eshet, Avital (2017). Sustainable finance? The environmental impact of the equator principles and the credit industry. International Journal of Innovation and Sustainable Development, 11, 106–29.

Finanace Reference. (2020). FINANCE REFERENCE. Retrieved September 20, 2020, from www.FINANCE REFERENCE: https://www.financereference.com/learn/return-on-investment

Flamini, V., Mcdonald, C., & Schumacher, L. (2009). Determinants of profitability in Sub-Shaharan Africa. IMF Working Paper, 9(15), 1-30.

Fledman, S., Sokya, P., & Ameer, P. (1997). Does Improving a Firm‟s Environmental Management System and Environmental Performances Result in Higher Stock Price? The Journal of Investing, 6(4), 87–97.

Ganda, F., Ngwakwe, C., & Ambe, C. (2015). Profitability as a Factor That Spurs Corporate Green Investment Practices in Johannesburg Stock Exchange (JSE) Listed Firms. Managing global transitions, 13, 231-252.

Hart, S., & Ahuja, G. (1996). Does it pay to be Green? An empirical examination of the relationship between emission reduction and firm performance. Business Strategy and Environment, 5, 30–39.

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 21

Hassan, M. K., & Bashir, A. H. (2005). Determinants of islamic banking profitability. Retrieved September 04, 2016 from DOI: 10.3366/edinburgh/9780748621002.003.0008.doi:10.3366/edinburgh/9780748621002.003.0008

Hoque, N., Mowla, M. M., Uddin, M. S., Mamun, A., & Uddin, M. R. (2019). Green Banking Practices. International Journal of Economics and Finance, 11(3), 58-68.

Hohne, N., Khosla, S., Fekete, H., & Gilbert, A. (2012). Mapping of green finance delivered by IDFC members in 2011. Retrieved September 22, 2020, from www.MultiLink: https://www.cbd.int/financial/gcf/definition-greenfinance.pdf

Hoshen, M. S., Hasan, M. N., Hossain, S., Mamun, M. A., Mannan, A., & Mamun, D. M. (2017). Green Financing: An Emerging Form of Sustainable Development in Bangladesh. IOSR Journal of Business and Management (IOSR-JBM), 19(12), 24-30.

Hossain, D. M., Bir, A., Sadiq, A. T., Tarique, K. M., & Momen, A. (2016). Disclosure of green banking issues in the annual reports: A study on Bangladeshi banks. Middle East Journal of Business, 55(3034), 1-12.

Iwata, H., & Okada, K. (2011). How Does Environment Performance Affect Financial Performance? Evidence from Japanese Manufacturing Firms. Ecological Economics, 70(9).

Islam, M. A., & Kamruzzaman, M., (2015) Green Banking Practices in Bangladesh. IOSR Journal of Business and Management (IOSR-JBM), 17 (4), 37-42

Jacobson, R. (1987). The Validity of ROI as a Measure of Business Performance. The American Economic Review, 77(3), 470-478. Retrieved Seotember 20, 2020, from http://www.jstor.org/stable/1804112

Jahan, N. (2012). Determinants of bank’s profitability: Evidence from Bangladesh. Indian Journal of Finance, 6(2), 32-38.

Julia, T., & Kassim, S. (2016). Green Financing and Bank Profitability: Empirical Evidence from the Banking Sector in Bangladesh. Journal of The International Institute of Islamic Thought and Civilization, 21(3), 304-330.

Julia, T., & Kassim, S. (2019). Exploring green banking performance of Islamic banks vs conventional banks in Bangladesh based on Maqasid Shariah framework. Journal of Islamic Marketing.

Khan, A. R. & Hossain, D.M. (2003). Environmental reporting as a corporate responsibility: A study on the annual reports of the manufacturing companies of Bangladesh. The Bangladesh Accountant, January-March.

Khan, A. R., Muttakin, M. B. & Siddiqui, J. (2013).Corporate Governance and Corporate Social Responsibility Disclosures: Evidence from an Emerging Economy. Journal of Business Ethics, 114, 207- 223

King, A. A., & Lenox, M. J. (2001). Does It Really Pay to be Green ? An Empirical Study of Firm Environmental and Financial Performance. Journal of Industrial Ecology, 5(1), 1-27.

Journal of Business Administration, Vol. 42, No. 1, June, 2021, ISSN : 1680-9823 (Print), 2708-4779 (Online)22

Kosmidou, K. (2008). The determinants of banks’ profits in Greece during the period of EU financial integration. Managerial Finance, 34(3), 146 – 159.

Lalon, R. M. (2015). Green banking: Going green. International Journal of Economics, Finance and Management Sciences, 3(1), 34-42.

Laskowska, A. (2018). Green banking as the prospective dimension of banking in Poland. Ecological Questions, 29, 129-135.

Masud, M., Kaium, A., Hossain, M. S., & Kim, J. D. (2018). Is green regulation effective or a failure: comparative analysis between Bangladesh Bank (BB) green guidelines and global reporting initiative guidelines. Sustainability, 10(4), 1267.

Masukujjaman, M., & Aktar, S. (2013). Green banking in Bangladesh: A commitment towards the global initiatives. Journal of Business and Technology (Dhaka), 8(1-2), 17-40.

Nanda, S., & Bihari, S. C. (2012). Profitability in banks of India: an impact study of implementation of green banking. International Journal of Green Economics, 6(3), 217-225.

Ongore, V. O., & Kusa, G. B. (2013). Determinants of financial performance of commercial banks in Kenya. International Journal of Economics and Financial Issues, 3(1), 237-252.

Rahman, M., Ahsan, M., Hossain, M., & Hoq, M. (2013). Green banking prospects in Bangladesh. Ali and Hossain, Md. Motaher and Hoq, Meem, Green Banking Prospects in Bangladesh (June 2, 2013). Asian Business Review, 2(2), 117-121.

Rahman, M., & Barua, S. (2016). The design and adoption of green banking framework for environment protection: Lessons from Bangladesh. Australian Journal of Sustainable Business and Society, 2(1), 1–19.

Rahaman, M. M., Hoque, M. S., & Roy, M. (2018). Green Financing and Its Impact on Profitability of the Banks: An Empirical Study on Banking Sector of Bangladesh. Metropoliton University Journal, 6(1), 42-56.

Rajput, N., Arora, S., & Khanna, A. (2013, September 12). An Empirical Study of Impact of Environmental Performance on Financial Performance in Indian Banking Sector. International Journal of Business and Management Invention, 2(9), 19-24.

Ramnarain, T. D., & Pillay, M. T. ( 2016, June 15 ). Designing Sustainable Banking Services: The Case of Mauritian Banks. Procedia - Social and Behavioral Sciences, 224, 483-490.

Rivard, R., & Thomas, C. (1997). The effect of interstate banking on large bank holding company profitability and risk. Journal of Economics and Business, 49, 61-76.

Shakil, M. H., Azam, M. K. G., & Raju, M. S. H. (2014). An evaluation of green banking practices in Bangladesh. European Journal of Business and Management, 6(31), 8-16.

Soana, M.-G. (2009). The Relationship Between Corporate Social Performance and Corporate Financial Performance in the Banking Sector. Journal of Business Ethics, 104, 133-148.

Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh 23

Song, X., Deng, X., & Wu, R. (2019). Comparing the influence of green credit on commercial bank profitability in china and abroad: Empirical test based on a dynamic panel system using GMM. International Journal of Financial Studies, 7(4), 64-79.

Sufian, F., & Habibullah, M. S. (2009). Determinants of bank profitability in developing economy : Empirical evidence from Bangladesh. Journal of Business Economics and Management, 10(3), 207-217. Retrieved from http://dx.doi.org/10.3846/1611-1619.2009.10207-217

Sun, G., Ying, W. & Qinghai, Li (2017). Impact of green credit on credit risk of commercial banks. Financial BBS, 22, 31–40

Tafti, S. H. (2012). Assessment of the corporate social responsibility according to Islamic values (Case study: Sarmayeh Bank. Procedia – Social and Behavioral Sciences, 58, 1139-1148.

Taskın, i. (2015). The Relationship between CSR and Banks’ Financial Performance: Evidence from Turkey. Journal of Yaşar University, 10(39), 21-30.

Tu, T. T. T., & Dung, N. T. P. (2017). Factors affecting green banking practices: Exploratory factor analysis on Vietnamese banks. Journal of Economic Development, (JED, Vol. 24 (2)), 4-30.

Ullah, M. M. (2013). Green Banking in Bangladesh-A comparative analysis. World Review of Business Research, 3(4), 74-83.

Ullah, M. A. (2020). Green banking in the way of sustainable development: an overview of practice and progress in Bangladesh. Can. J. Bus. Inf. Stud, 2(5), 105-119.

Wang, Xiao-Rao (2016). Investment in environmental governance and asset quality of banks: Analysis from the perspective of green credit. Finance Forum, 11, 12–19.

Weber, O., & Oyegunle, A. (2016). DEVELOPMENT OF SUSTAINABILITY AND GREEN BANKING REGULATIONS EXISTING CODES AND PRACTICES.

Wörsdörfer, Manuel (2015). Equator principles: Bridging the gap between economics and ethics? Business & Society Review, 120, 205–43.

Wu, M.-W., & Shen, C.-H. (2013). Corporate social responsibility in the banking industry: Motives and financial performance. Journal of Banking and Finance, 37(9), 3529-3547.

Yasmin, S., & Akhter, I.(2020). A Review of CSR Initiatives of the Private Commercial Banks in Bangladesh. Journal of business administration, 41 (1), 95-118.

Zhang, B., Yang, Y., & Bi, J. (2011). Tracking the implementation of green credit policy in China: Top-down perspective and bottom-up reform. Journal of Environmental Management, 92(4), 1321–1327. doi: 10.1016/j.jenvman.2010.12.019

Zhou, G., Sun, Y., Luo, S., & Liao, J. (2021). Corporate social responsibility and bank financial performance in China: The moderating role of green credit. Energy Economics, 97, 105190.