Embed Size (px)

Citation preview

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

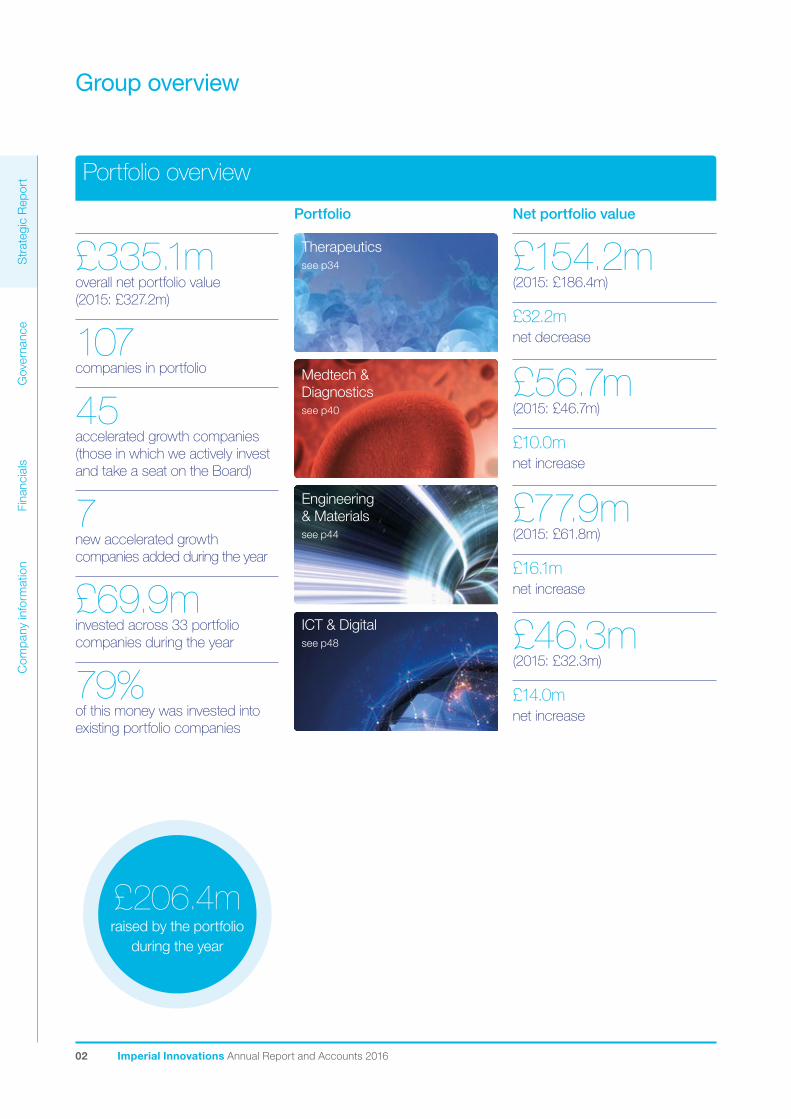

02 Imperial Innovations Annual Report and Accounts 2016

£335.1moverall net portfolio value (2015: £327.2m)

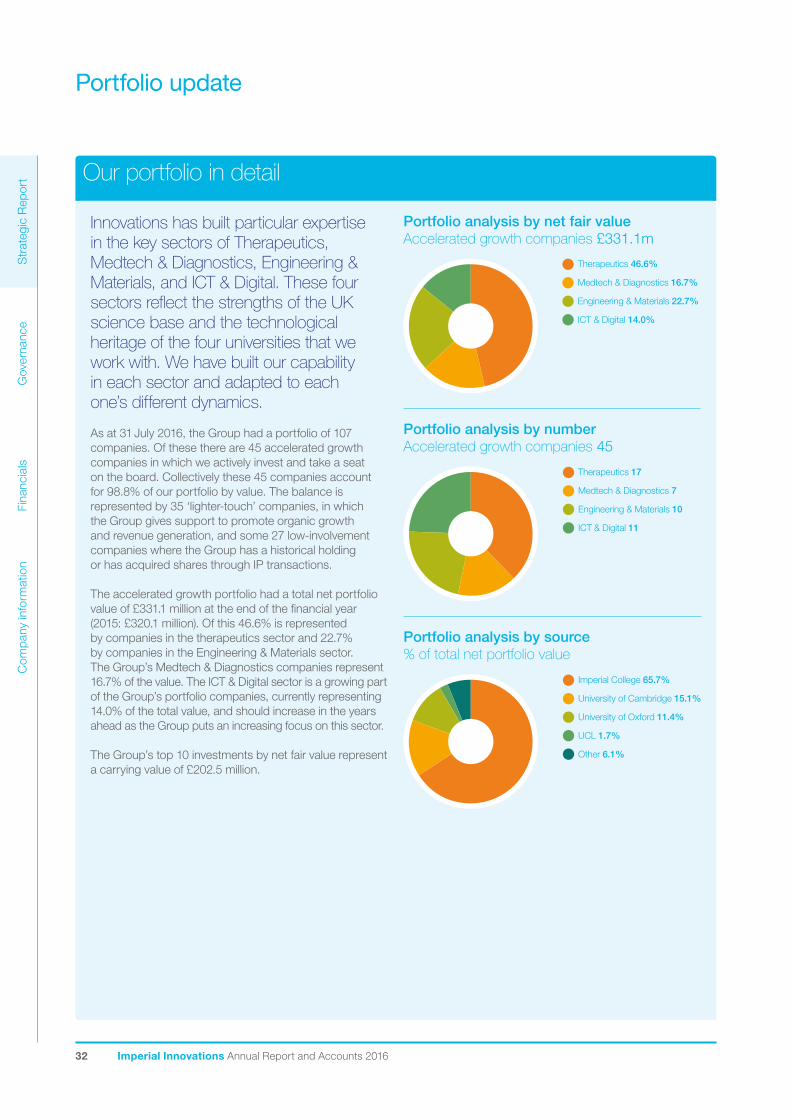

107companies in portfolio

45accelerated growth companies (those in which we actively invest and take a seat on the Board)

7new accelerated growth companies added during the year

£69.9minvested across 33 portfolio companies during the year

79%of this money was invested into existing portfolio companies

Portfolio

Therapeuticssee p34

Medtech & Diagnosticssee p40

Engineering & Materialssee p44

ICT & Digitalsee p48

Net portfolio value

£154.2m(2015: £186.4m)

£32.2mnet decrease

£56.7m(2015: £46.7m)

£10.0mnet increase

£77.9m(2015: £61.8m)

£16.1mnet increase

£46.3m(2015: £32.3m)

£14.0mnet increase

Group overview

Portfolio overview

£206.4mraised by the portfolio

during the year

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 03

Nurturing innovation

Imperial Innovations Group plc (known as Innovations) creates, builds and invests in pioneering technology companies and licensing opportunities developed from outstanding scientific research focusing on the ‘Golden Triangle’, the geographical region broadly bounded by London, Cambridge and Oxford.

This area has an unrivalled cluster of outstanding academic research and technology businesses, and is home to four of the world’s top 10 universities (source: QS World University Rankings ® 2016/17) as well as leading research institutions, the cream of the UK’s science and technology businesses and many of its leading investors.

The Group supports scientists and entrepreneurs in the commercialisation of their ideas, through protecting and licensing out intellectual property, by leading the formation of new companies, by recruiting high-calibre management teams and by providing investment and encouraging co-investment.

Innovations provides continuity of funding from start-up to scale-up, with initial investments from seed stage onwards. Innovations remains an active investor over the life of its portfolio companies, with the majority of Innovations’ investment going into businesses in which it is already a shareholder. This strategy substantially de-risks investment scale-up in our portfolio companies. As Innovations invests from its own balance sheet it is not constrained by the five-to-seven year investment horizons of closed-end funds, nor is it under pressure to sell early in order to demonstrate a return to Limited Partners (LPs).

Innovations has a technology pipeline agreement with Imperial College London that extends until 2020, under the terms of which it has exclusive commercialisation rights and as acts as the College’s Technology Transfer Office (TTO). The Group also acts as the TTO for a number of NHS Trusts linked to Imperial College London, including Imperial College Healthcare NHS Trust and London North West Healthcare NHS Trust. Further information on the Group’s role as TTO for Imperial College can be found on page 11.

Following a fundraising in January 2011, Innovations broadened its addressable market beyond Imperial College London by making investments in opportunities arising from intellectual property developed at, or associated with, the University of Cambridge, the University of Oxford and University College London (UCL). Since then around one-third of all of the Group’s new companies have come from Imperial College London, one-third from the Cambridge cluster, with the final third derived from University of Oxford, UCL and management teams and research organisations around London.

In June 2014, Innovations completed a £150.0 million fundraising. Following this transaction, the Group expanded its operation to include sourcing of opportunities not only from its existing University partners, but also from the extensive network of entrepreneurs, management teams and co-investors that the Group has established within the ‘Golden Triangle’ over the last 10 years.

During the year, the Group raised £100.0 million through a placing in February which provided the Group with the capacity to maintain its interests in the larger later stage funding rounds of its maturing portfolio, whilst also seeking to capitalise on two new strategic partnerships signed during the year that were designed to increase Innovations’ access to deal flow. These were the UCL Technology Fund, which provides Innovations’ with formal access to IP created by UCL researchers, and the creation of Apollo Therapeutics. The latter is a pioneering collaboration between AstraZeneca, GlaxoSmithKline, Johnson & Johnson and TTOs of Imperial College London, University College London and the University of Cambridge, which aims to accelerate the development of new medicines and provides Innovations with visibility of therapeutics IP across all three universities.

Since becoming a public company in 2006, Innovations has raised more than £440.0 million of equity from investors, which has enabled it to invest in some of the most exciting spin-outs to come out of UK research. In addition, the Group has a £50.0 million undrawn loan facility from the European Investment Bank (EIB).

Between Innovations’ admission to AIM (August 2006) and 31 July 2016, Innovations has invested a total of £306.7 million and the total raised by the Group’s portfolio companies is more than £1.5 billion, with £206.4 million being raised this year.

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

04 Imperial Innovations Annual Report and Accounts 2016

Chairman’s statement

David NewlandsChairman

Innovations is an outstanding business based on access to the best in UK science, a deep understanding of the academic mindset and a highly professional investment capability.

It gives me great pleasure to present this Annual Report to shareholders, my first as Chairman. After nearly three months in the role, I have had an opportunity to meet with many of Innovations’ key stakeholders and I have been struck by the consistently high regard in which the business is held as a leader in the rapidly emerging technology commercialisation sector.

I would like to start by thanking my predecessor Dr Martin Knight, the Group’s founder and Chairman from its Admission to AIM in 2006 until 31 July 2016, for his vision in developing such an exciting company. The team has built an outstanding business based on access to the finest science-driven intellectual property (IP) in the UK, a deep understanding of the academic mindset and a highly professional investment capability.

We have the opportunity to build on this platform to create important, powerful and valuable businesses, to the benefit of our shareholders and our wider stakeholder community.

Make no mistake, what we do is important. Commercialising outstanding UK research and creating the next generation of world-leading technology companies is crucial for the UK economy, not only in economic terms but also in reinforcing the UK’s position as a world-leader in scientific research. We have both the expertise and the financial strength needed to play an important role in this endeavour.

A platform on which to create important, powerful and valuable businesses

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 05

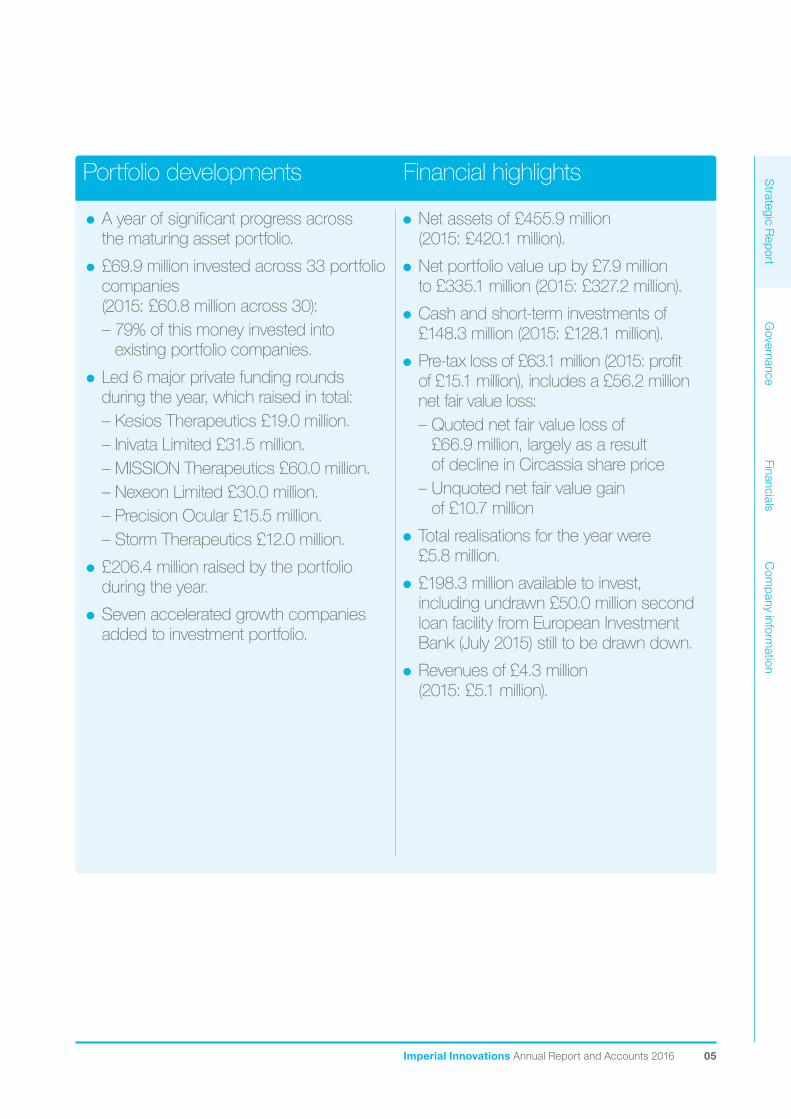

A year of significant progress across the maturing asset portfolio.

£69.9 million invested across 33 portfolio companies (2015: £60.8 million across 30):

– 79% of this money invested into existing portfolio companies.

Led 6 major private funding rounds during the year, which raised in total:

– Kesios Therapeutics £19.0 million. – Inivata Limited £31.5 million. – MISSION Therapeutics £60.0 million. – Nexeon Limited £30.0 million. – Precision Ocular £15.5 million. – Storm Therapeutics £12.0 million.

£206.4 million raised by the portfolio during the year.

Seven accelerated growth companies added to investment portfolio.

Net assets of £455.9 million (2015: £420.1 million).

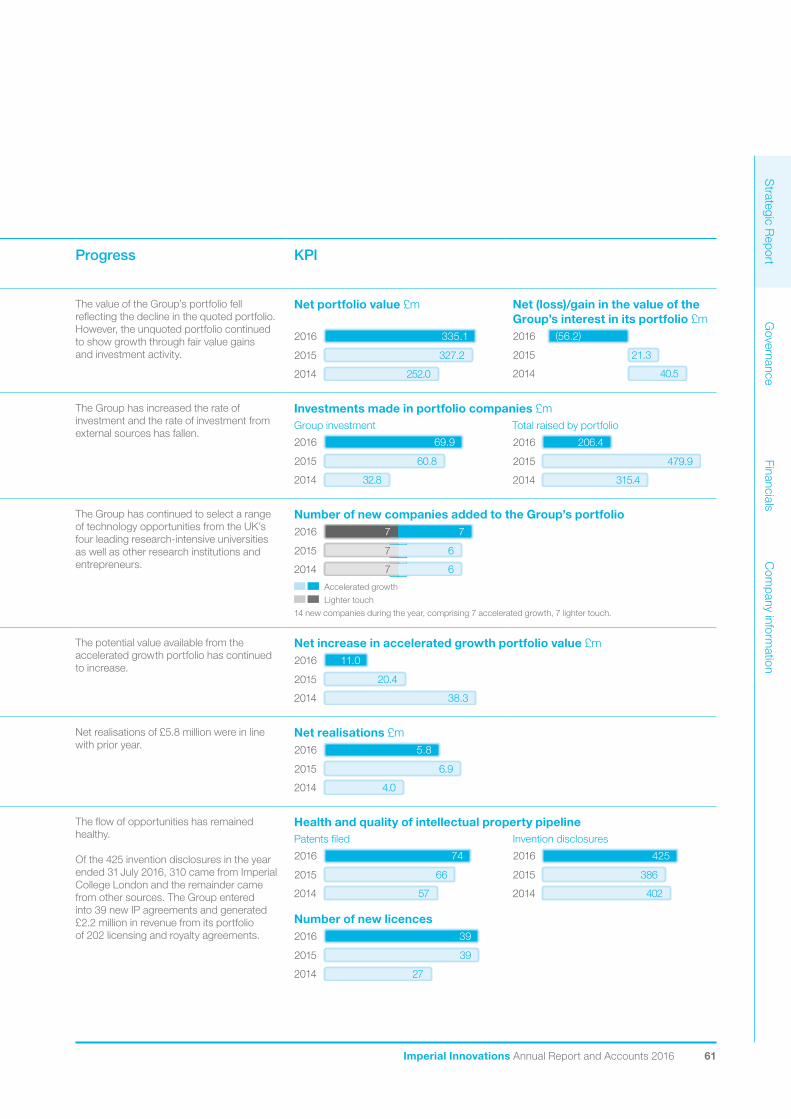

Net portfolio value up by £7.9 million to £335.1 million (2015: £327.2 million).

Cash and short-term investments of £148.3 million (2015: £128.1 million).

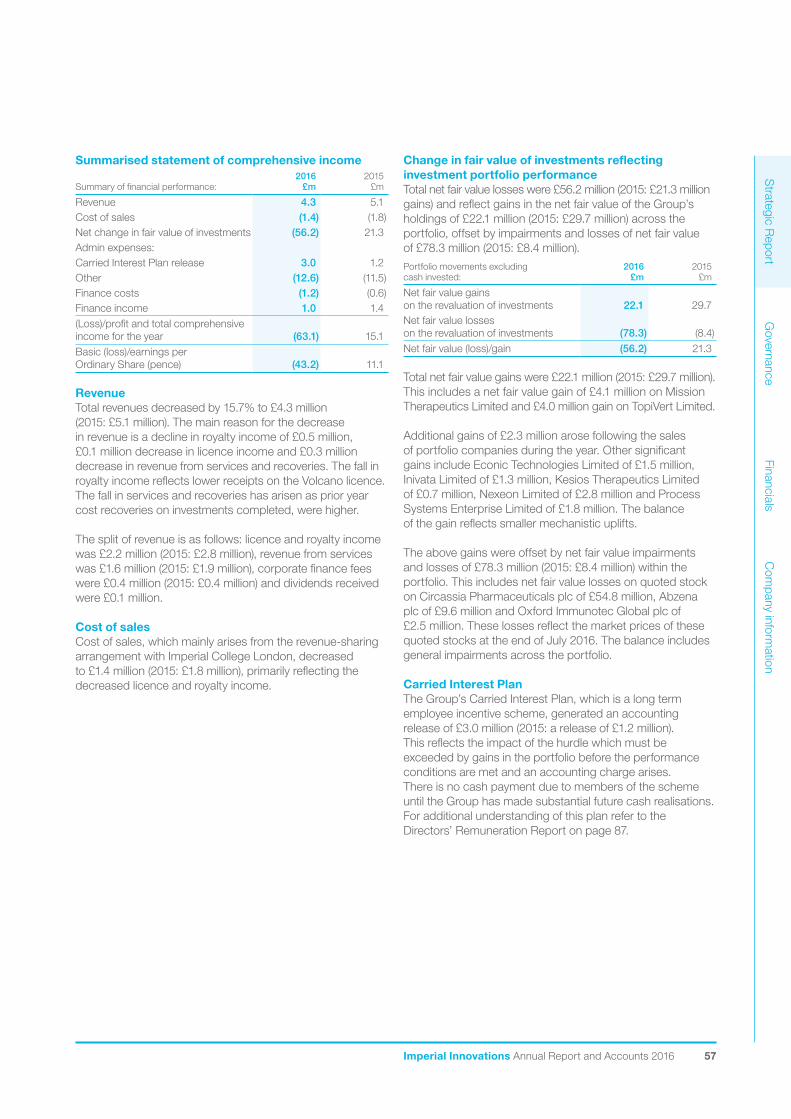

Pre-tax loss of £63.1 million (2015: profit of £15.1 million), includes a £56.2 million net fair value loss:

– Quoted net fair value loss of £66.9 million, largely as a result of decline in Circassia share price

– Unquoted net fair value gain of £10.7 million

Total realisations for the year were £5.8 million.

£198.3 million available to invest, including undrawn £50.0 million second loan facility from European Investment Bank (July 2015) still to be drawn down.

Revenues of £4.3 million (2015: £5.1 million).

Portfolio developments Financial highlights

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

06 Imperial Innovations Annual Report and Accounts 2016

Our timeline IPO on AIM market raising £25.0 million. Focused on IP derived from Imperial College London.

Innovations raises £30.0 million in a placing.

£140.0 million rights issue. Operations broadened to encompass sourcing opportunities from University of Cambridge, University of Oxford and UCL, in addition to Imperial College London.

201120072006

Financial performanceOur focus is on building a portfolio of substantial high-quality, well-funded and well-managed businesses. The Group’s Net Asset Value (NAV), increased by £35.8 million to £455.9 million (2015: £420.1 million). The Group’s Net Portfolio Value (NPV) was £335.1 million (2015: £327.2 million).

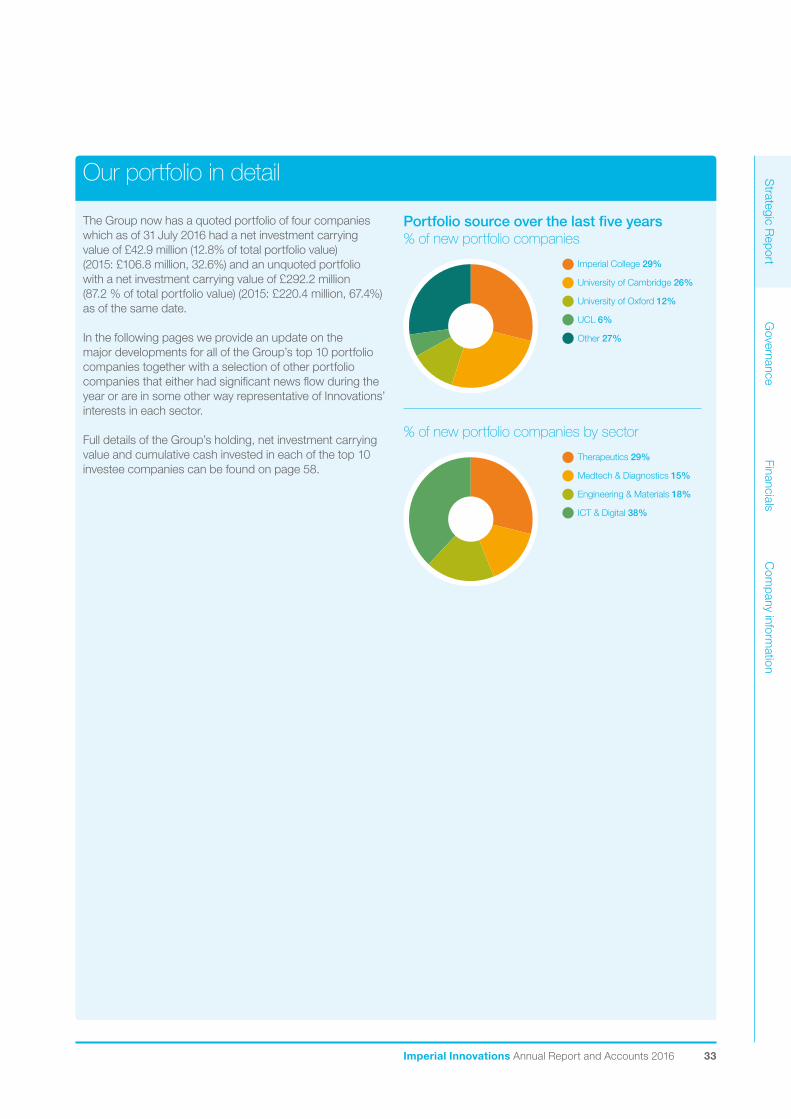

The carrying value of the Group’s listed investments (Abzena plc, Circassia Pharmaceuticals plc, IXICO plc and Oxford Immunotec Global plc) are all marked-to-market at period end. At the end of the financial year they had a total net valuation of £42.9 million (2015: £106.8 million); a net fall of £63.9 million comprising investments of £3.0 million, less net fair value movements of £66.9 million. The largest component of this decline resulted from the fall in the share price of Circassia Pharmaceuticals following the failure of its cat allergy Phase III study.

This was a major disappointment but the results of a single clinical trial will not cause us to change our long-term strategy. We make investments that involve carefully calculated risks, including investing in drug development companies and clinical trials are an inherent feature of this sector.

What matters over the medium to long-term is the ultimate value of the companies we are creating. We are confident that we are building a number of UK science-based companies that have the potential to make a significant impact, not only on Innovations but on the UK as a whole.

We are very encouraged by the performance of our unquoted portfolio which gives us confidence for the future. Many of our companies made significant technical, clinical and commercial progress during the year. Notable examples include Cell Medica’s partnership with Baylor College of Medicine, PsiOxus’ collaboration with Bristol-Myers Squibb and the completion of recent funding rounds for Inivata, Nexeon and Econic.

Operational progressDuring the year Innovations completed three major transactions which strengthened the balance sheet and increased our pipeline of opportunities.

In February 2016, we raised £100.0 million which provided the Group with the resources to maintain its holdings in the larger later-stage funding rounds of its maturing portfolio.

The Group has also started to capitalise on the new strategic partnerships signed during the year with the UCL Technology Fund and Apollo Therapeutics. These agreements have significantly increased our visibility of technology coming from UCL and the University of Cambridge, as well as broadening and deepening our existing relationships with three of the world’s leading pharma companies (AstraZeneca, GlaxoSmithKline and Johnson & Johnson).

At the same time, we have continued to deploy our capital, investing £69.9 million across 33 companies, including £14.6 million invested in seven new additions to the portfolio which will provide the foundations for value generation in future. Collectively the portfolio raised £206.4 million of total investment during the year.

Chairman’s statementcontinued

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 07

Innovations obtains £30.0 million loan facility from European Investment Bank (EIB).

June Innovations raises £150.0 million in a placing.

July Innovations obtains £50.0 million second loan facility from European Investment Bank (EIB).

January Innovations launches Apollo Therapeutics.

Innovations commits £24.8 million to UCL Technology Fund.

FebruaryInnovations raises £100.0 million in a placing.

2016201520142013

Such events illustrate the potential of these private companies to drive long-term returns for shareholders, but this potential does not necessarily translate into significant changes in valuation straight away. The growing partnership interest we are seeing from pharma companies and other industry partners in our companies is also very encouraging.

BrexitRight at the end of the financial year, the UK voted to leave the EU. In the months after this vote, the UK has entered a period of uncertainty. Whilst the full picture is yet to play out, we are confident UK science will maintain its pre-eminent position on the world stage.

However there are risks to research funding, to attracting and retaining talent and to university finances. We believe the UK government recognises these challenges and will address them as part of its new UK industrial strategy. Significantly, our ongoing partnership with the European Investment Bank (EIB) and European Investment Fund (EIF) remains strong with both organisations reaffirming their commitment to our loan facility and the UCL Technology Fund respectively. The impact on our own staff resourcing will be minimal.

Board changesAt the end of the financial year, after 13 years of outstanding service, my predecessor Dr Martin Knight stepped down from the Board. Martin became the Chairman of the Imperial Innovations group of companies in 2003 and was Chairman when the Group was quoted on AIM in 2006. He is one of the pioneers of the emerging IP commercialisation industry and provided outstanding leadership to Innovations over the last 13 years. On behalf of the Board and everyone at the Group, I would like to thank him for his huge contribution to the business.

I joined the Board as non-executive Chairman on 1 August 2016.

The opportunity Our executive team has built a powerful and strong platform for nurturing innovation and turning raw IP into a portfolio of early-stage businesses. Our ambition is to create a portfolio of companies that deliver real value to shareholders, as well as adding value to the wider economy.

We are well placed to do this. All the key ingredients are in place. We have a strong balance sheet, an experienced Board and our portfolio companies are led by world-class management teams. We are supported by a strong group of like-minded shareholders and co-investors.

Our confidence for the future extends beyond our existing portfolio. The quality of the IP we are seeing from the academic, research and entrepreneurial community within the ‘Golden Triangle’ augurs well for the future and we expect it to lead to exciting investment opportunities and prospects for further value creation.

David NewlandsChairman

12 October 2016

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

08 Imperial Innovations Annual Report and Accounts 2016

Our markets

Operating in a growing market

Innovations is focused on the commercial exploitation of outstanding research originating in the ‘Golden Triangle’.

The Group’s focus on this geography, combined with the pull of its capital and growing track record, puts Innovations at the heart of this world-class science cluster from which it derives the vast majority of its spin-outs and investment opportunities.

Innovations’ integrated business model (see page 18), which extends from original research through seed funding, scale-up, and long-term support, equips the Group with a detailed understanding of the process of translating early-stage research into commercial business opportunities. In addition, deep sector-specialist knowledge provides expertise in evaluating the likely success of new scientific ideas, which makes Innovations an attractive partner for research teams seeking to commercialise their technology.

Academic insight and visionThe majority of the Group’s investments are derived from academic research. This provides the Group with early sight of discoveries in fundamental science that may have commercial application, as well as insight into the future and the development of next-generation technologies.

The Technology Pipeline Agreement (TPA) with Imperial College London provides Innovations with exclusive access to all the unencumbered IP developed at the College and the flexibility to commercialise that IP in any way it considers appropriate. Typically, this is achieved either through the formation of a spin-out company, or through licensing IP to an existing company in the same field.

The Group also works closely with academic communities associated with the University of Cambridge, the University of Oxford and University College London on a non-exclusive basis. This includes working with those universities’ own technology transfer offices (Cambridge Enterprise Limited, Oxford University Innovation (formerly ISIS Innovation) and UCL Business, respectively) as well as collaborating directly with the universities’ own dedicated funds in backing new spin-out businesses.

The most recent example of this is the UCL Technology Fund, which was launched in January 2016. This is the first investment fund that University College London has created to commercialise its multidisciplinary research.

Over the next five years this fund is expected to invest £50.0 million to support ideas from academics in life sciences and physical sciences, and will be used for early-stage proof of concept funding, licensing opportunities and the formation of new spin-out companies. Innovations is a Limited Partner (LP) in the fund and has committed £24.8 million to the fund, matched by a commitment of the same amount from the European Investment Fund (EIF).

During the year, the Group also committed £3.3 million to Apollo Therapeutics, a new £40.0 million joint venture between AstraZeneca, GlaxoSmithKline, Johnson & Johnson and the technology transfer offices of Imperial College London, University College London and the University of Cambridge.

The aim of this new venture is to support the translation of outstanding academic therapeutic science into innovative new medicines, and is yet another example of Innovations operating at the nexus of outstanding academic research and industrial strength expertise.

Funding UK innovationThe UK has long been criticised for its apparent inability, or the reluctance of its ecosystem, to fund and develop the scientific research breakthroughs that are generated at its many world-class universities. In 2014, figures from the British Venture Capital Association (BVCA) suggest that, out of total private equity and venture investments of £4.7 billion in the UK, just £108.0 million was deployed into seed, start-up and early-stage investments (http://www.bvca.co.uk/Portals/0/library/documents/IAR%20Autumn15.pdf).

This may be due to the fact that early-stage investors in cutting-edge science experience not only high technical and market risk, but may also have to wait a long time before they see a return on their investment. Nevertheless, whatever the underlying cause, the last decade has seen an emergence of funding vehicles that look to fund early-stage high-risk technology companies with a long-term investment horizon – so-called ‘Patient Capital’.

Flexible, open-ended funding models of this type are appropriate for funding spin-outs from universities because of the typically long gestation period from lab bench to commercialisation. Inventions generated at our leading academic institutions typically require substantial development before they are commercially viable. Companies based around high-technology university inventions may take more than 10 years (and sometimes even longer) from first patent filing to exit or IPO, and frequently require considerable funding to develop their technology.

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 09

Geographic focus and established network within

the ‘Golden Triangle’ The Group has an established network

of academics, industry partners and co-investors which makes the Group the partner of choice for leading academics

and management teams within this world-class science cluster.

3

Track record of forming management teams to maximise

opportunity from IPThe Group has a significant network

of experienced entrepreneurs and managers with proven expertise in forming and growing early-stage companies. The Group’s ability to create and develop top-quality management

teams for its portfolio companies is a significant attraction for scientists

partnering with the Group.

2

Proprietary technology pipeline with Imperial College London and

commercialisation rightsThe Group has early and exclusive access

to research outputs from one of the world’s leading research universities,

and through Imperial College London, to one of the largest medical

schools in the UK.

Well-developed and mature portfolio of companies

Approximately 80% of the Group’s investment goes into businesses in which Innovations is already a shareholder, holds a board seat and knows from the inside.

This significantly reduces the risk of scaling up investment.

6

Deep sector-specialist knowledge

The Group has expertise in evaluating the likely success, both technical and

commercial, of new scientific ideas. The ability to understand and talk deep science makes the Group an attractive partner for research teams seeking to commercialise

their technology, and differentiates us from many ‘digital’ investors.

7

Investing from its own balance sheet

This gives the Group the ability to be involved with all stages of the

commercialisation process and the flexibility to take a long term approach to investments. This gives Innovations an opportunity to form companies and establish an influential role in the business before a venture capital investor

would get involved, and the ability to scale-up its investment as portfolio

companies develop.

5

Track record and integrated business model, which extends from original

research through to scale-up

The Group’s skills in IP management, technology and market assessment, product development, licensing and

investment make it an attractive partner for academics,

management teams and co-investors.

4

Competitive strengthsInnovations has a number of distinct strengths that differentiate it, not only

from its listed peers but also from venture capital firms, institutional investors and other organisations that may compete with the Group by providing funding to companies in the commercialisation process.

1

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

10 Imperial Innovations Annual Report and Accounts 2016

Traditional venture capital (VC) funding, which has relied on the limited partnership model in which the likes of pension funds put their money into a closed fund managed by a venture capital firm, has proved unsuitable for supporting early-stage high-technology companies in the UK. This is chiefly a result of the fixed life of these funds and pressure to deliver a return to Limited Partners, which means that funding typically operates over a five-to-seven year horizon. In general, this means VCs often prefer to wait until a technology is substantially de-risked before making their initial investment – typically at the Series A stage (the first substantial funding round following seed and other development funding).

In contrast, seed investors invest earlier than VCs but usually lack the cash to ‘follow’ their money, and therefore often shy away from investing in certain sectors such as biotechnology and automotive/aerospace engineering, which are capital-intensive with long development cycles.

Because neither of these models is particularly supportive of university spin-outs, academic-associated technology start-ups historically found themselves falling into the gap (often described as the ‘Valley of Death’); on the one hand finding it difficult to attract seed funding, and on the other, discovering that venture finance was similarly limited.

Patient Capital arose as a potential solution. The longer-term outlook and investment profile of these funds is ideally suited to technologies arising from academia. Patient Capital providers can afford to ‘get in early’ (at seed stage or earlier) and continue to invest (sometimes alongside VCs, corporate VCs or other Patient Capital providers) throughout the lifecycle of a high-technology business, protecting their equity position through follow-on investment. Furthermore, because they invest from their own balance sheet, they are not under pressure to return capital to their shareholders or unit holders within a short period, thus retaining the flexibility of growing into more substantial businesses over time.

Competitive environmentAs recently as two years ago, there were just three long-established companies: Imperial Innovations, IP Group and Fusion IP (subsequently acquired by IP Group) that were dedicated, university-associated listed Patient Capital businesses. However, over the last two years the IPO’s of Allied Minds, PureTech Healthcare and Mercia Technologies, have added greater weight to an IP commercialisation sector that has now raised more than £1.0 billion of capital.

Much of this technology commercialisation sector has been cornerstoned and underpinned by long-term supportive investment from wealth management funds such as Invesco Perpetual, Woodford Investment Management, Lansdowne Partners and others, who have all championed the benefits of investing in early-stage companies borne out of university research.

A common theme is the belief that UK intellectual property and early-stage spin-outs are significantly undervalued in comparison to their US counterparts and that there is a large potential upside to investing in UK innovation.

In addition, we have seen the emergence of specialist funds such as Woodford Patient Capital Trust (which last year raised more than £800.0 million of capital from investors to invest in early-stage technology companies) and other funds dedicated to commercialising the output of specific universities. The latter include the £50.0 million UCL Technology Fund (in which the Group is a Limited Partner), the £320.0 million Oxford Sciences Innovation (OSI) (launched in 2015) and Cambridge Innovation Capital (CIC) which has raised £125.0 million dedicated to investing in IP-rich companies from the University of Cambridge and the wider research and business community around the Cambridge area.

More recently, Draper Esprit became the first British venture capital investor of its type to float, raising £103.0 million by listing on AIM in June 2016. At the time of its IPO the company cited Innovations and IP Group as IP commercialisation companies whose success it was seeking to replicate, by gaining access to a more flexible source of capital and holding stakes in favoured businesses for longer without being forced to sell too early.

Sector growth brings greater choiceThe UK technology commercialisation sector is therefore clearly flourishing. These are welcome developments as they are not only beneficial for promoting UK innovation in general, but more specifically because they are likely to increase the number of potential opportunities in which the Group may invest, particularly as much of this new money is being deployed within the ‘Golden Triangle’.

Clearly, as a result of greater investor choice, there is increased competition in terms of attracting investment capital in the public markets, but this does not necessarily translate into direct competition when it comes to deploying that capital into university spin-outs and early-stage businesses. Each commercialisation company has its own geographic and sector specialisations, and as a result, they rarely compete in funding new opportunities. Greater choice is thus beneficial not only for investors but also for those seeking investment. Furthermore, despite the substantial sums raised recently, there is still a shortage of capital relative to the abundant supply of IP available to commercialise.

In addition, specialist skills and industry-specific expertise are needed to deploy capital effectively. On the rare occasions two or more investors do congregate around an opportunity, the tendency is to collaborate on creating stronger, more productive investor syndicates rather than to compete on terms.

Our markets continued

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 11

However, Innovations is well equipped to deal with competitive situations because of a number of key strengths which help the Group to source outstanding opportunities (see diagram on page 9).

So these macro-economic changes and new competition do not deflect the Group from its strategy. Rather, by virtue of its geographic focus, capital strength and track record, Innovations is well placed to be the lead investor or partner of choice for academics, management teams and co-investors within the ‘Golden Triangle’.

Furthermore, the Group’s active syndication of investments means it will continue to work collaboratively with dedicated university funds as well as leading financial investors, specialist venture capital firms and strategic investors. Further details of the key components of the Group’s investment case are articulated in pages 14-25.

Benefits of operating a Technology Transfer OfficeOperating a Technology Transfer Office (TTO) at Imperial College London gives Innovations a direct pipeline to the research being carried out at one of the world’s leading technical universities.

Staff in the TTO work every day in close proximity and collaboration with the academic staff developing ground-breaking technologies, which may in the future lead to substantial business opportunities.

As a result, the Group is intimately familiar with the technology that goes into Imperial College London spin-outs as the team has tracked its progression for a long time, even before a company is formed. The team seeks to leverage grant funding to help de-risk and develop these technologies at a very early stage, and use its sector-specific expertise to

step in to provide guidance and influence over the direction of technology development. This is beneficial, as it means that the technology and the future company develop in alignment so that the new spin-out company can hit the ground running. In addition, this familiarity allows the Group to determine early the optimum route forward for each technology for example, in deciding whether it should be licensed or form the basis of a new spin-out.

Aside from the benefits of working closely with technologies that may go on to form the basis of new businesses, the TTO also provides a reliable revenue stream that supports the operation of the Group.

Every year, many licence deals are signed with industry partners, whereby technology developed at Imperial College London is licensed for development to these companies. As the Group has undertaken IP protection on these technologies, it can generate revenue through up front licensing fees and future royalties in exchange for allowing industry partners access, sharing that 50/50 with Imperial College London.

In addition to generating revenue, this activity has additional related benefits. Firstly, industry partners who work with Innovations often see the benefit of technology developed at universities, and often provide specific research funding, which allows academics to undertake research in industry-relevant fields; secondly, the experience offered to academics through working with industry in licensing deals stands them in good stead for future industry interactions – such as entering into collaborations or forming businesses; and thirdly, this activity generates a network of scientific knowledge and contributors that ultimately benefits the pipeline of future technologies.

Alkion Biopharma is an example of one of Innovations’ many successful spin-outs from Imperial College London that are able to grow without receiving venture funding from the Group. It was formerly part of the Group’s organic growth portfolio of around 30 companies, for which the Innovations team provides ongoing support to raise funding, recruit management and promote organic growth.

Alkion is an Imperial College London spin-out co-founded by Innovations in 2011 and based on the work of Professor Peter Nixon and Dr Franck Michoux (Biochemistry). The company has developed a unique set of technologies that allow it to sustainably produce and purify valuable materials from

plant biomass and has positioned itself with a unique offering to several life sciences-based industries. These activities are backed by a strong portfolio of patented technology.

In May 2016, Innovations completed the sale of its shares in Alkion to Evonik Industries, a leading specialist chemical company operating in several fields such as nutrition, resource efficiency and performance materials. Commercial terms have not been disclosed. Innovations’ equity in Alkion derives from the early commercial support provided to the founders by Innovations’ Technology Transfer Office, as well as from licensing the founding IP.

Focus on Alkion Biopharma

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

12 Imperial Innovations Annual Report and Accounts 2016

Our strategy

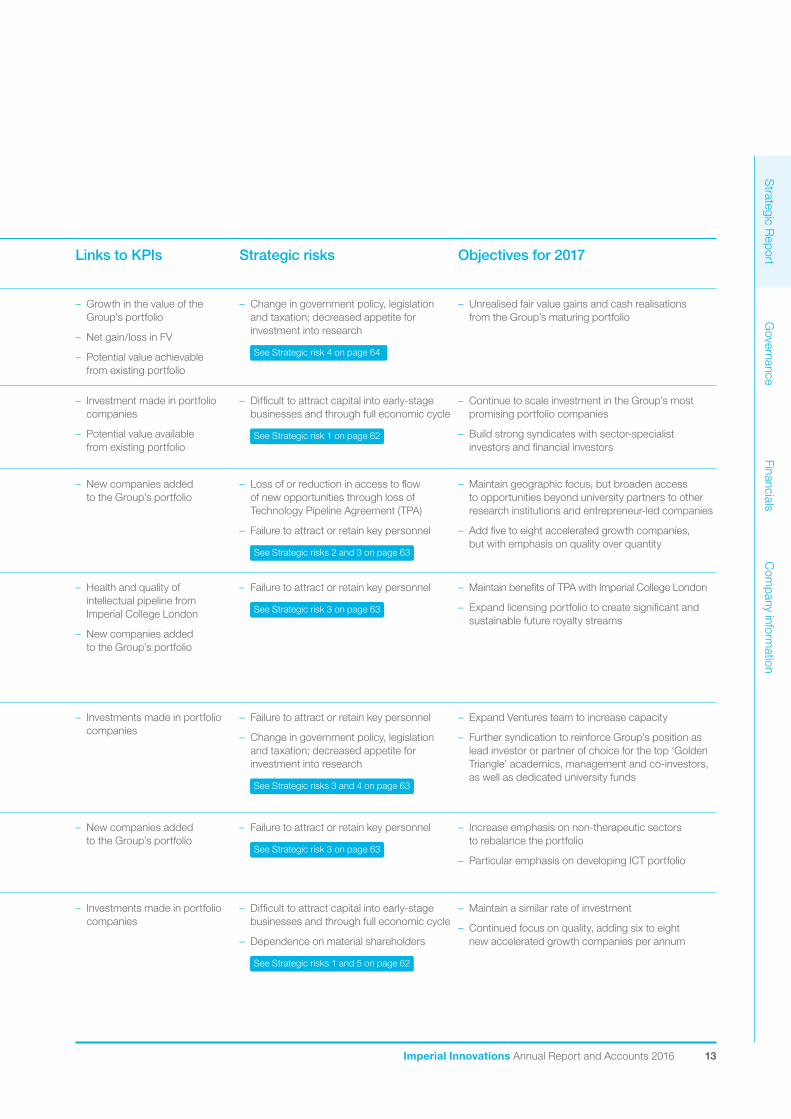

Our goals What we did in 2016 Links to KPIs Strategic risks Objectives for 2017

Generate exceptional returns for shareholdersGenerate exceptional returns to our shareholders through both unrealised fair value gains and cash realisations executed at the optimal time.

– Net portfolio value up by £7.9 million to £335.1 million

– Pre-tax loss of £63.1 million (includes net FV loss of £56.2 million)

– Disposals generated net proceeds of £5.8 million

– Growth in the value of the Group’s portfolio

– Net gain/loss in FV

– Potential value achievable from existing portfolio

– Change in government policy, legislation and taxation; decreased appetite for investment into research

See Strategic risk 4 on page 64

– Unrealised fair value gains and cash realisations from the Group’s maturing portfolio

Build $1.0 billion companiesSelectively back a few of our portfolio companies with patient capital to build $1.0 billion companies.

– Led major funding rounds for MISSION Therapeutics (£60.0 million), Inivata (£31.5 million), Nexeon (£30.0 million), Kesios Therapeutics (£19.0 million), Precision Ocular (£15.5 million) and Storm Therapeutics (£12.0 million)

– Investment made in portfolio companies

– Potential value available from existing portfolio

– Difficult to attract capital into early-stage businesses and through full economic cycle

See Strategic risk 1 on page 62

– Continue to scale investment in the Group’s most promising portfolio companies

– Build strong syndicates with sector-specialist investors and financial investors

Leverage the UK’s outstanding scienceLeverage the strengths of the outstanding science emanating from the ‘Golden Triangle’ by engaging with the most promising technology opportunities and progressing them from inception to maturity.

– Seven new accelerated growth companies added to the portfolio, plus seven organic growth companies

– New companies added to the Group’s portfolio

– Loss of or reduction in access to flow of new opportunities through loss of Technology Pipeline Agreement (TPA)

– Failure to attract or retain key personnel

See Strategic risks 2 and 3 on page 63

– Maintain geographic focus, but broaden access to opportunities beyond university partners to other research institutions and entrepreneur-led companies

– Add five to eight accelerated growth companies, but with emphasis on quality over quantity

Successfully commercialise IPUse our deep sector knowledge and judgement to take calculated risks to deliver successful commercialisation of intellectual property through licensing or by forming portfolio companies.

– Licence and royalty revenues of £2.2 million (2015: £2.8 million)

– 39 commercial licence agreements signed (2015: 39) and 74 patents filed (2015: 66)

– A total of 14 new companies added to the portfolio

– Sale of Stanmore Implants, Alkion Biopharma and Hark Health Solutions

– Health and quality of intellectual pipeline from Imperial College London

– New companies added to the Group’s portfolio

– Failure to attract or retain key personnel

See Strategic risk 3 on page 63

– Maintain benefits of TPA with Imperial College London

– Expand licensing portfolio to create significant and sustainable future royalty streams

Build teams and syndicatesAttract high-calibre management teams to our portfolio companies.

Build strong syndicates with sector-specialist investors and financial investors.

– High-quality management appointments across portfolio

– Innovations’ venture partners appointed to Board positions in portfolio companies

– £206.4 million raised by the portfolio during the year (2015: £479.9 million)

– Investments made in portfolio companies

– Failure to attract or retain key personnel

– Change in government policy, legislation and taxation; decreased appetite for investment into research

See Strategic risks 3 and 4 on page 63

– Expand Ventures team to increase capacity

– Further syndication to reinforce Group’s position as lead investor or partner of choice for the top ‘Golden Triangle’ academics, management and co-investors, as well as dedicated university funds

Focus on sectors where we have expertiseUse our deep sector knowledge and judgement to identify new licensing and investment opportunities by evaluating the likely success of new scientific ideas (both technical and commercial).

– Seven accelerated growth companies added to the portfolio, comprising one therapeutics company, one engineering & materials company and five ICT & digital companies

– New companies added to the Group’s portfolio

– Failure to attract or retain key personnel

See Strategic risk 3 on page 63

– Increase emphasis on non-therapeutic sectors to rebalance the portfolio

– Particular emphasis on developing ICT portfolio

Provide continuity of funding from start-up to scale-upRetain flexibility to take a long term approach to realisation. Start small and then selectively scale investment in the most promising portfolio companies as they develop.

Continue to create new ventures to develop longevity in our portfolio.

– Increased investment rate in line with stated strategy

– £69.9 million invested in 33 portfolio companies (2015: £60.8 million in 30 companies)

– £100.0 million raised by means of a Placing in February 2016

– Investments made in portfolio companies

– Difficult to attract capital into early-stage businesses and through full economic cycle

– Dependence on material shareholders

See Strategic risks 1 and 5 on page 62

– Maintain a similar rate of investment

– Continued focus on quality, adding six to eight new accelerated growth companies per annum

Innovations’ strategy is to build substantial, high-quality, well-funded and well-managed businesses.

–

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 13

Our goals What we did in 2016 Links to KPIs Strategic risks Objectives for 2017

Generate exceptional returns for shareholdersGenerate exceptional returns to our shareholders through both unrealised fair value gains and cash realisations executed at the optimal time.

– Net portfolio value up by £7.9 million to £335.1 million

– Pre-tax loss of £63.1 million (includes net FV loss of £56.2 million)

– Disposals generated net proceeds of £5.8 million

– Growth in the value of the Group’s portfolio

– Net gain/loss in FV

– Potential value achievable from existing portfolio

– Change in government policy, legislation and taxation; decreased appetite for investment into research

See Strategic risk 4 on page 64

– Unrealised fair value gains and cash realisations from the Group’s maturing portfolio

Build $1.0 billion companiesSelectively back a few of our portfolio companies with patient capital to build $1.0 billion companies.

– Led major funding rounds for MISSION Therapeutics (£60.0 million), Inivata (£31.5 million), Nexeon (£30.0 million), Kesios Therapeutics (£19.0 million), Precision Ocular (£15.5 million) and Storm Therapeutics (£12.0 million)

– Investment made in portfolio companies

– Potential value available from existing portfolio

– Difficult to attract capital into early-stage businesses and through full economic cycle

See Strategic risk 1 on page 62

– Continue to scale investment in the Group’s most promising portfolio companies

– Build strong syndicates with sector-specialist investors and financial investors

Leverage the UK’s outstanding scienceLeverage the strengths of the outstanding science emanating from the ‘Golden Triangle’ by engaging with the most promising technology opportunities and progressing them from inception to maturity.

– Seven new accelerated growth companies added to the portfolio, plus seven organic growth companies

– New companies added to the Group’s portfolio

– Loss of or reduction in access to flow of new opportunities through loss of Technology Pipeline Agreement (TPA)

– Failure to attract or retain key personnel

See Strategic risks 2 and 3 on page 63

– Maintain geographic focus, but broaden access to opportunities beyond university partners to other research institutions and entrepreneur-led companies

– Add five to eight accelerated growth companies, but with emphasis on quality over quantity

Successfully commercialise IPUse our deep sector knowledge and judgement to take calculated risks to deliver successful commercialisation of intellectual property through licensing or by forming portfolio companies.

– Licence and royalty revenues of £2.2 million (2015: £2.8 million)

– 39 commercial licence agreements signed (2015: 39) and 74 patents filed (2015: 66)

– A total of 14 new companies added to the portfolio

– Sale of Stanmore Implants, Alkion Biopharma and Hark Health Solutions

– Health and quality of intellectual pipeline from Imperial College London

– New companies added to the Group’s portfolio

– Failure to attract or retain key personnel

See Strategic risk 3 on page 63

– Maintain benefits of TPA with Imperial College London

– Expand licensing portfolio to create significant and sustainable future royalty streams

Build teams and syndicatesAttract high-calibre management teams to our portfolio companies.

Build strong syndicates with sector-specialist investors and financial investors.

– High-quality management appointments across portfolio

– Innovations’ venture partners appointed to Board positions in portfolio companies

– £206.4 million raised by the portfolio during the year (2015: £479.9 million)

– Investments made in portfolio companies

– Failure to attract or retain key personnel

– Change in government policy, legislation and taxation; decreased appetite for investment into research

See Strategic risks 3 and 4 on page 63

– Expand Ventures team to increase capacity

– Further syndication to reinforce Group’s position as lead investor or partner of choice for the top ‘Golden Triangle’ academics, management and co-investors, as well as dedicated university funds

Focus on sectors where we have expertiseUse our deep sector knowledge and judgement to identify new licensing and investment opportunities by evaluating the likely success of new scientific ideas (both technical and commercial).

– Seven accelerated growth companies added to the portfolio, comprising one therapeutics company, one engineering & materials company and five ICT & digital companies

– New companies added to the Group’s portfolio

– Failure to attract or retain key personnel

See Strategic risk 3 on page 63

– Increase emphasis on non-therapeutic sectors to rebalance the portfolio

– Particular emphasis on developing ICT portfolio

Provide continuity of funding from start-up to scale-upRetain flexibility to take a long term approach to realisation. Start small and then selectively scale investment in the most promising portfolio companies as they develop.

Continue to create new ventures to develop longevity in our portfolio.

– Increased investment rate in line with stated strategy

– £69.9 million invested in 33 portfolio companies (2015: £60.8 million in 30 companies)

– £100.0 million raised by means of a Placing in February 2016

– Investments made in portfolio companies

– Difficult to attract capital into early-stage businesses and through full economic cycle

– Dependence on material shareholders

See Strategic risks 1 and 5 on page 62

– Maintain a similar rate of investment

– Continued focus on quality, adding six to eight new accelerated growth companies per annum

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

14 Imperial Innovations Annual Report and Accounts 2016

Business review

Russ CummingsChief Executive Officer

A unique and compelling investment case

The UK’s technology commercialisation sector is thriving, drawing in additional capital and shining a spotlight on us all.

The UK’s public technology commercialisation sector is thriving with a market capitalisation of £3.5 billion having raised over £1.0 billion in capital over the last two years (source: Eye on IP, Ken Rumpf, Stifel 4 July 2016).

Investors keen to gain an exposure to the sector now have a choice of six UK listed companies in which to invest, as well as a number of overseas companies. Common to all is that they provide exposure to very early-stage, potentially disruptive IP-based companies. However, there are significant differences in sector focus, business model, accounting policies and approach to valuation that make direct comparisons challenging.

For example, Innovations, IP Group and Mercia Technologies all focus predominantly on commercialising the output of academic research in the UK, whilst Allied Minds and PureTech Health target the US market and are basically US companies that have chosen to list in the UK because of the greater understanding of IP commercialisation in the London market. Even within the UK, Innovations is focused on the output of the ‘Golden Triangle’, whereas IP Group adopts a UK-wide approach and Mercia is focused predominantly on the Midlands and the North of England.

As a guide to investors we have set out, on the following pages, what we believe to be the five key components of Innovations’ investment case.

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 15

Key components of our investment case

Unrivalled access to the UK’s best researchInnovations provides investors with an opportunity to gain exposure to the output of the best and most exciting research emanating from the ‘Golden Triangle’ of Oxford, London and Cambridge, including sourcing opportunities across all four of the UK’s leading research-intensive universities.

See pages 16-17 for more detail

Proven strong business model Our integrated business model, which includes patent and licensing activities, provides us with a unique insight into leveraging early-stage research and turning it into substantial, high-quality, well-managed and well-funded businesses. This end-to-end capability is not replicated by our listed peers.

See pages 18-19 for more detail

Established portfolio – with exciting pipelineOver the last decade, Innovations has built an outstanding portfolio of early-stage companies, many of which are close to value creation events. These are businesses in which we have already invested £306.7 million and which have collectively raised investment of more than £1.5 billion.

See pages 20-21 for more detail

Matching world-class management to world-class scienceIt takes high-quality, proven, highly-motivated management teams to build a successful business. It is not easy recruiting top talent into young companies, but companies in the ‘Golden Triangle’ have an advantage over those in other regions, because of the rich talent pool in the region and proximity to London, which makes it easier to attract international talent to the South East.

See pages 22-23 for more detail

Syndication Syndication remains an important part of how we create strong businesses and we are very proud of the quality of co-investors that we are attracting to our portfolio. We work closely with leading financial investors, specialist venture capital firms and strategic investors such as the venture investment arms of major pharmaceutical companies.

See pages 24-25 for more detail

1

2

3

4

5

Key components of our investment case

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

16 Imperial Innovations Annual Report and Accounts 2016

A compelling investment case

1. Unrivalled access to the UK’s best research

The ‘Golden Triangle’ is an unrivalled cluster of outstanding academic research and technology businesses. We are deeply embedded within this geography, which puts us at the heart of UK science, making connections between the research community and the commercial world. While the whole of the UK is rightly described as a research powerhouse, we believe the wealth of high-quality opportunities coming from this science cluster means that we do not need to expand our focus at the present time.

‘Golden Triangle’

University of Oxford

University of Cambridge

University College London

Imperial College London

Imperial College London, the University of Cambridge, the University of Oxford and University College London are the UK’s four leading research-intensive universities and are ranked as four of the top 10 universities in the world (source: QS World University Rankings 2016/17).

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 17

Focus on

SAM Labs

SAM Labs is a great example of Innovations championing innovation, in this case by backing an Imperial College London alumni company that has developed wireless construction kits that are encouraging school children to take an interest in technology and engineering, thereby helping to inspire the next generation of STEM students.

SAM Labs’ wireless electronic kits allow users to build their own smart inventions using hardware, software and apps through the Internet of Things (IoT). The kits are aimed specifically at school-age children so they readily fit in with the UK’s national Computing at School curriculum that requires schools to introduce the concepts of coding to students from the age of six.

Importantly, the kits have been designed to make the basic elements of coding quick and easy to learn, which means that children learn even the most advanced coding concepts swiftly through the power of play.

The company was founded in April 2014 by a group of graduates from Imperial College London led by CEO Joachim Horn. SAM Labs raised more than £125,000 in October 2014 via the crowdfunding site Kickstarter and in May 2016, completed a £3.2 million funding round led by Innovations, which contributed £2.0 million to the round.

This new funding will allow SAM Labs to further develop its products and expand the commercial reach of its SAM kits which are already sold via its web site and through retailers such as the Science Museum and the Conran Shop.

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

18 Imperial Innovations Annual Report and Accounts 2016

A compelling investment case continued

2. Proven strong business model

By virtue of the fact that we invest from our own balance sheet, we have flexibility with respect to the amount invested and the timescale for realisation.

We are not constrained by the five-to-seven year investment horizons of closed-end venture capital funds, nor under pressure to sell early in order to demonstrate a return to Limited Partners. Quite the contrary; if we have a portfolio company with significant growth potential we can increase our investment and hold for the long term.

By leveraging grant and proof-of-concept funding for early-stage investments, less than 6% of our own funds go into the highest risk start-up phase investments. The vast majority of our capital is deployed in the scale-up of portfolio companies, which we know intimately from the inside. This gives us the opportunity to invest with the benefit of more influence and make better-informed decisions than would be the case for late-stage investors.

From start-up to scale-up

One of the factors that makes us different is our ability to invest over long periods, forming companies before a venture capital company (VC) would get involved and scaling our investment in our maturing companies when they approach value.

Typically, we start with an initial seed investment in the order of £25,000 to £1.0 million to get the business off the ground. Assuming we are satisfied with the venture’s development, we then progressively deploy more

capital over time, typically in the order of £1.0 million to £5.0 million in Series A funding rounds to help the business build organisational strength and develop necessary partnerships.

We then selectively build our stake in our most promising assets by deploying more capital and attracting co-investors to the business. Our largest investments to date have been Nexeon (£27.4 million) and Circassia Pharmaceuticals plc (£25.5 million).

Continuity of funding with deep knowledge of assets

Start-up phase Scale-up phaseSeed investment £25k–£1m<6% of capital invested

Understand the opportunity & market

Seat on Board Build organisational strength

Exit at most opportune time

‘Live with’ the technology Accelerate investment in best opportunities

Series A round £1m–£5mIncreasing momentum and accelerating pace of development

Stake building £5m–£25m+

Po

tent

ial

op

po

rtun

ity

Com

mer

cial

isat

ion

exit

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 19

Focus on

Kesios Therapeutics

During the year the Group continued to deploy its substantial capital resources into its investment portfolio. In total the Group invested £69.9 million across 33 portfolio companies during the period. Kesios Therapeutics was one of the companies that benefited, with the Group committing £6.0 million to a £19.0 million Series A funding round, investing alongside SV Life Sciences and Abingworth.

Kesios is developing novel therapeutics for the treatment of multiple myeloma and other cancers. The company was created in 2011 to commercialise research led by Professor Guido Franzoso from the Department of Medicine at Imperial College London and has made rapid progress since Innovations first seed-funded the business.

Concurrent with its financing, Kesios has made swift progress in building a world-class management team to advance its innovative science and drug development. This includes the appointment of Paolo Paoletti MD, formerly President of GSK Oncology, as Chief Executive Officer, who leads an experienced team drawn from across the biotech/pharma industry.

Kesios’ lead drug candidate is about to enter clinical studies and, with this substantial Series A financing behind it, the team is in a strong position to deliver a new treatment option for patients with multiple myeloma.

1 MISSION Therapeutics 2 Econic3 TopiVert4 Abingdon

5 PsiOxus Therapeutics6 Nexeon7 Circassia

8 Cell Medica9 Veryan Holdings10 Abzena

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

20 Imperial Innovations Annual Report and Accounts 2016

A compelling investment case continued

3. Established portfolio – with exciting pipeline

At 31 July 2016, our net portfolio value was £335.1 million. It comprises businesses that we have co-founded and know intimately.

Strong, well-funded pipeline

The average age of our eight largest unlisted portfolio companies (Nexeon, Cell Medica, Veryan Medical, PsiOxus Therapeutics, Mission Therapeutics, TopiVert, Abingdon Health and Econic Technologies respectively) is 8.6 years and these companies have raised commitments on average of £38.9 million each. These are substantial, well-managed and well-funded businesses, and are good examples of companies in the portfolio that we expect to trigger significant value-creation events over the medium term.

Beyond this leading cohort, we have a very strong and well-funded follow-on pipeline of exciting businesses, some of which will generate value in years to come.

An investment in Innovations is therefore a way for shareholders to support and participate in the growth in value of a diverse portfolio of early-stage technology companies, whilst leveraging Innovations’ expertise to select and build those businesses on their behalf.

Net

inve

stm

ent

carr

ying

val

ue

31 J

uly

2016

£m

Years since founded

0

5

10

15

20

25

30

35

40

0 2 4 6 8 10 12 14 16

8

9

10

7

5

6

431

2

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 21

Focus on

Inivata

Inivata shows how Innovations’ capital strength has allowed the Group to rapidly accelerate the development of an extremely promising early-stage company, from a £4.0 million funding round in September 2014, to a £31.5 million Series A fundraising in January 2016.

Inivata is a clinical cancer genomics company harnessing the emerging potential of circulating tumour DNA (ctDNA) analysis to improve testing and treatment for oncologists and their patients. Unlike conventional invasive biopsies, Inivata detects and analyses genomic material from a cancer patient’s cell-free DNA (ctDNA) which can be collected through a simple blood sample.

This minimally-invasive approach – a liquid biopsy – offers a revolution in how cancer is detected, monitored and treated. The test allows precise analysis of cancer-related mutations present in ctDNA, and is designed to provide oncologists with clinically actionable genomic information to guide therapy selection, monitor treatment progress and detect new mutations as they emerge.

Inivata was spun out from Cancer Research UK in 2014 and launched with £4.0 million in funding from Innovations, Cambridge Innovation Capital and Johnson & Johnson Development Corporation.

The company made such rapid progress that in January 2016 it attracted a further £31.5 million in Series A fundraising. Innovations committed £10.0 million to the round alongside existing investors Cambridge Innovation Capital (CIC) and Johnson & Johnson Innovation (JJDC) and new investor Woodford Patient Capital Trust.

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

22 Imperial Innovations Annual Report and Accounts 2016

A compelling investment case continued

4. Matching world-class management to world-class science

A common theme amongst the management that we attract to our portfolio companies is that many have blue-chip CVs, having worked for large corporations before going on to success in high-growth entrepreneurial start-ups. We like people who have proven abilities to operate in both environments, because we need both the entrepreneurial drive and an ability to understand what the ultimate acquirer expects to see before writing a large cheque, or what the public markets expect post IPO.

Putting the right team in place

Crucially for long term value creation, Innovations makes sure that its portfolio companies are set up correctly from the start. This means ensuring that the venture is funded sufficiently to attract experienced management with a track record and an insightful understanding of the market in which the technology will be deployed. It also means managing the evolution of the management team so that it is ‘stage-relevant’ to the lifecycle of the company.

The continuity of funding we provide from start-up to scale-up, and our close working relationship with the management of our portfolio companies, are important components of our model – it is far harder to influence a company’s development if you are a late-stage investor inheriting a team and investor base.

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 23

Focus on

Inflowmatix

Water network data analytics business Inflowmatix demonstrates the advantages of bringing in management with directly relevant industry experience to work alongside academic founders to lead the development of spin-out companies. This pairing ensures the correct blend of research, application expertise, technical skills and business innovation.

Inflowmatix provides water flow and pipe health analytics to water utilities worldwide, enabling them to diagnose hydraulic instabilities and failures, reduce bursts, prioritise network maintenance and reduce operating costs. The company was formed in July 2015 with £1.0 million in seed funding from Innovations. In May 2016, the company completed a £3.0 million series A round led by Innovations alongside new investor Parkwalk Advisors Limited.

Inflowmatix’s technology is based on research carried out in Dr Ivan Stoianov’s InfraSense Labs, in the Department of Civil & Environmental Engineering at Imperial College London.

In just over a year since formation, Innovations and Dr Stoianov have together brought in an experienced

management team including Chairman Dr David Parker, who has extensive experience in building companies from early-stage, and new CEO Steve George, who joined the company in October 2015.

Steve has worked in the water industry since 1999 and joined Inflowmatix from the Suez Group, where he worked in business and market development. He holds a wealth of experience in providing services and software solutions to water network management and was formerly IT Director for a leading UK consultancy company providing leakage management software and services. This industry expertise has helped Inflowmatix engage closely with water companies in order to ensure that the data and solutions the company is developing are valuable to customers.

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

24 Imperial Innovations Annual Report and Accounts 2016

A compelling investment case continued

5. Syndication

Smart, sector-focused co-investors bring significant added value. They carry out extensive due diligence (in addition to our own) and thus help us to validate our portfolio and avoid ‘originator’s bias’, thereby ensuring that there is real quality in our portfolio. Meanwhile, we use our position of influence and our pre-emption rights as a founder shareholder to deploy the appropriate share of our capital.

Quality shareholders and co-investors

Syndication of investment is an important part of our approach to building strong companies. Our co-investors bring capital, but they also bring insight and people with operational experience, which can be invaluable.

Strategic investors also bring directly relevant expertise that can help with our companies’ development, for example with clinical development plans. And of course, they may be a potential acquirer, so they increase the range of trade sale options.

Shareholders• Invesco Asset Management• Lansdowne Partners• Woodford Patient Capital Trust• Imperial College London

Specialist investors• Sofinnova Partners• SV Life Sciences• Fidelity BioSciences• Abingworth• Octopus Investments• Jetstream Ventures

Strategic investors• Astellas• SR One• Pfizer Ventures Investments• Roche Venture Fund• Johnson & Johnson Innovation• Merck Ventures BV• Robert Bosch Venture Capital• Lundbeckfond Ventures

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 25

Focus on

Storm Therapeutics

Storm Therapeutics (formerly Iceni Therapeutics) is a classic example of our model – helping world-leading scientists to turn their outstanding research into exciting early-stage companies by providing long-term funding and building great syndicates of like-minded co-investors.

Storm Therapeutics is a drug discovery and development company focused on the identification and development of small molecules that target RNA-modifying enzymes. The company is a spin-out from the University of Cambridge’s Gurdon Institute and was created to commercialise the ground-breaking work of its founders, Professor Tony Kouzarides and Professor Eric Miska, in the field of RNA epigenetics.

RNA (ribonucleic acid) is the template of all protein synthesis and has key regulatory functions in cells. There is growing understanding of the importance of RNA modification in the development of cancer, opening up novel therapeutic targets in cancer treatment.

Innovations led the seed funding round for Storm Therapeutics in May 2015. On 28 June 2016, Innovations committed a further £3.0 million to the company’s £12.0 million Series A funding round, alongside existing investor Cambridge Innovation Capital and new investors Merck Ventures BV and Pfizer Venture Investments.

Storm Therapeutics intends to develop therapeutics, using IP licensed from Cambridge Enterprise (the commercialisation arm of the University of Cambridge). The proceeds of the funding will be used to identify small molecule modulators of these novel targets in RNA modification pathways and develop them into new classes of anti-cancer treatments.

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

26 Imperial Innovations Annual Report and Accounts 2016

Chief Executive Officer’s review

The long-term prospects for the Group remain very good

The fundamentals of our business are very strong, with many of our portfolio companies making significant progress during the year.

I am pleased to report on another year of progress as we continue to develop our portfolio and lay the foundations for future value creation. However, I look back on the year with somewhat mixed emotions, because whilst I am excited about the very real progress we are making in the business and across our portfolio, I am disappointed by one specific non-cash event which impacted our headline numbers, namely the failure of Circassia’s Phase III trial.

This event should not overshadow a very good year for the Group. We have come a long way with a number of key developments which may ultimately prove to be of greater significance to shareholders.

Notable achievements included signing new strategic partnerships to increase our visibility of new investment opportunities; strengthening our balance sheet by means of a £100 million Placing; and once again increasing the level of investment in our portfolio to a record level. The Group’s net portfolio value is now £335.1 million and, although we are reporting a loss of £63.1 million for the period, net assets increased by £35.8 million to £455.9 million.

Russ CummingsChief Executive Officer

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 27

The fundamentals of the business are very strong. Many of our portfolio companies made significant technical, clinical and commercial progress during the year and we led six major private funding rounds.

Significantly, there is growing evidence of strong partnership interest in our portfolio, both from corporate venture investors (e.g. Johnson & Johnson Innovations, SR One, Roche Venture Fund and Robert Bosch) and industry (e.g. BMS, Consort Medical, TSYS Inc and Sumitomo Chemical Co Limited) with the recently announced collaboration and licence agreement between Crescendo Biologics and Takeda Pharmaceuticals being a prime example. We remain confident about the prospects for long-term value creation.

Visibility of new investment opportunities remains very high. The quality and experience of our team means our ability to identify potential stars is continually improving. We have accelerated the development of some of our more recently formed companies. Good examples of this include the £31.5 million Series A funding round for Inivata and the £19 million Series A round in Kesios.

We added seven new companies to the accelerated growth portfolio during the year. As always, we have adopted a measured approach to growing the number of companies in our portfolio with a resolute focus on quality over quantity. Already the pipeline for the next financial year is looking strong.

Circassia’s Phase III trialThe result of Circassia’s Phase III trial was a disappointment. The large body of Phase II clinical data was indicative of a successful outcome. However, we understand that clinical trials do not always go to plan, so we hold a diversified portfolio of strong, well-funded and well-managed portfolio companies, which reduces the Group-level risk of failure of individual assets.

We are encouraged that Circassia has taken a similar approach in its own business. In addition to its allergy immunotherapy products, Circassia has built a fast-growing asthma diagnostics and management platform, and a broad pipeline of respiratory products, each of which have considerable value in their own right. The business is well funded and we are confident its experienced management team will implement whatever changes they deem necessary to adjust for this setback and create value in future.

The failure of this trial has led to a non-cash reduction in carrying value of Circassia, down by £54.8 million.

Strong balance sheetIn February 2016, the Group raised £100.0 million (before expenses) by means of a Placing. As of 31 July 2016, the Group had total cash and short-term liquidity investments of £148.3 million (2015: £128.1 million). In addition, the Group had a £50.0 million EIB loan facility that was undrawn at year-end.

This balance sheet strength combined with our policy of building strong investor syndicates, means we are in a strong position both in absolute terms and relative to our peers, particularly over companies with earlier-stage portfolios or non-syndicated investments.

“ The quality of new opportunities that the Group is seeing from the academic, research and entrepreneurial community within the ‘Golden Triangle’ remains very high, with a healthy stream of new investment opportunities.”

Str

ateg

ic R

epor

tG

over

nanc

eFi

nanc

ials

Com

pany

info

rmat

ion

28 Imperial Innovations Annual Report and Accounts 2016

Major funding rounds completed during the yearPortfolio company Funding round Co-investors

Kesios Therapeutics Limited £19.0 million series A SV Life Sciences, AbingworthInivata Limited £31.5 million Series A Cambridge Innovation Capital, Johnson & Johnson Innovation,

Woodford Patient Capital TrustMISSION Therapeutics £60.0 million funding round Woodford Patient Capital Trust plc, Sofinnova Partners, SR One,

Roche Venture Fund and Pfizer Venture InvestmentsNexeon Limited £30.0 million equity funding round Invesco Asset Management, Woodford Investment Management LLPPrecision Ocular Ltd £15.5 million investment Consort Medical plc, NeoMed, Hovione Scientia LimitedStorm Therapeutics £12.0 million Series A Cambridge Innovation Capital and new investors Merck Ventures BV

and Pfizer Venture Investments

Chief Executive Officer’s review continued

Putting our capital to workDuring the year the Group continued to deploy its substantial capital resources into its investment portfolio, and once again increased its investment levels, investing £69.9 million across 33 portfolio companies during the year (2015: £60.8 million across 30 portfolio companies). This is more than double the level of just two years ago and reflects the ambition and increasing maturity of our portfolio companies.

Of this 79% (£55.0 million) was invested into existing portfolio companies, with the balance being invested in new companies added to the portfolio. The Group’s portfolio companies raised a total of £206.4 million during the year (2015: £479.9 million).

Six portfolio companies completed major funding rounds during the period. Collectively these companies: MISSION Therapeutics, Nexeon, Inivata, Kesios Therapeutics, Precision Ocular and Storm Therapeutics raised £168.0 million. The fact that these private companies were able to raise such substantial funding is a result of our proactive policy of building strong investor syndicates and shows that the Group is not dependent upon the public markets to ensure that its portfolio companies grow with pace and ambition. The calibre and breadth of co-investors is notable and includes strategic investors, specialist funds and financial investors (see Table).

In addition to these major rounds, the Group completed investments into 20 other portfolio companies, including leading funding rounds in Featurespace (£6.2 million), Econic (£5.0 million), Abingdon Health (£3.0 million), Aqdot (£5.0 million) and Inflowmatix (£3.0 million).

The overall net portfolio value increased by £7.9 million to £335.1 million (2015: £327.2 million) through a combination of investments of £69.9 million, disposals of £5.8 million and net portfolio losses of £56.2 million. A major component this year was the £66.9 million net fair value loss attributable to movements in the value of the Group’s quoted portfolio which is marked-to-market at period end. Circassia Pharmaceuticals accounted for £54.8 million (or 81.9%) of the drop in value in the quoted portfolio.

Net assets were £455.9 million (2015: £420.1 million).

Total disposals for the year were £5.8 million. We completed the sale of three portfolio companies. In April 2016, the Group crystallised a net fair value gain of circa £1.4 million from the sale of its 16.4% interest in Stanmore Implants Worldwide to Stryker Corporation. This was followed by the sale of two organic portfolio companies, Alkion Biopharma and Hark Health Solutions, which were sold to Evonik Industries and Google DeepMind respectively. Both of these companies were spin-outs from Imperial College London in which Innovations held equity as a result of the Group’s Technology Transfer Office providing early commercial support to the founders, as well as from licensing the founding IP.

Strategic R

eportG

overnanceFinancials

Com

pany information

Imperial Innovations Annual Report and Accounts 2016 29

Technology Transfer OfficeThe Group’s Technology Transfer Office (‘TTO’) was broadly in line with budget on all key metrics. Licensing and royalty income was £2.2 million (2015: £2.8 million). The TTO managed the sale of two portfolio companies: Hark Health Solutions and Alkion Biopharma.