Embed Size (px)

Citation preview

HALF-YEAR RESULTS 2014 AND STRATEGY 2018

SIKA PRESENTATION JULY 2014

1. HIGHLIGHTS AND RESULTS HALF-YEAR 2014

HIGHLIGHTS HALF-YEAR 2014 Strategy 2018 well on track

18.1% sales growth (10.6% in CHF) to CHF 2,656.9 million

High growth dynamic in all regions

Sales up 18.1% in emerging markets

25.7% increase in net profit to CHF 177.6 million

3 new factories in Brazil, Indonesia, and India

3 acquisitions with CHF 53 million in sales

3

4

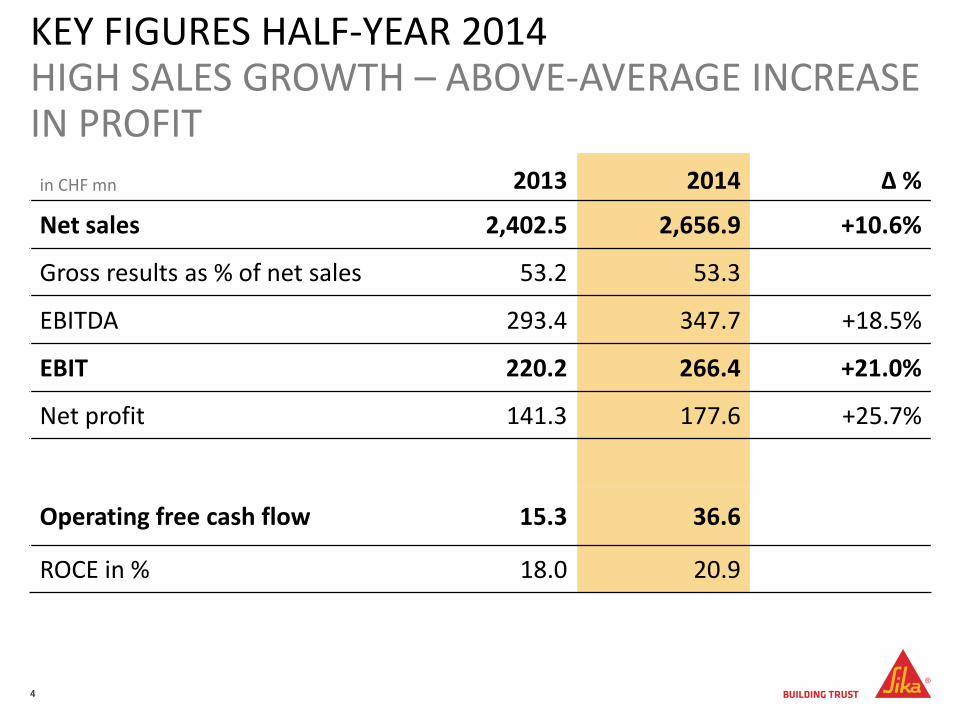

KEY FIGURES HALF-YEAR 2014 HIGH SALES GROWTH – ABOVE-AVERAGE INCREASE IN PROFIT

in CHF mn 2013 2014 Δ %

Net sales 2,402.5 2,656.9 +10.6%

Gross results as % of net sales 53.2 53.3

EBITDA 293.4 347.7 +18.5%

EBIT 220.2 266.4 +21.0%

Net profit 141.3 177.6 +25.7%

Operating free cash flow 15.3 36.6

ROCE in % 18.0 20.9

+ 16.8%

+ 21.7%

+18.1% + 6.5%

GROWTH MOMENTUM CONTINUES HALF-YEAR 2014 18.1% SALES GROWTH (10.6% IN CHF)

Growth of 18.1% in Emerging Markets

5

,

335

296

1,336

485

North America

Latin America

EMEA

Asia/Pacific

HY 1 / 2013 HY 1 / 2014 (in CHF mn, growth at constant exchange rates)

Opening of Sika plant:

7th plant in Brazil (Aparecida de Goiânia, January 2014)

2nd plant in Indonesia (Surabaya, May 2014)

6th plant in India (Jhagadia, June 2014)

ACCELERATED BUILD-UP OF EMERGING MARKETS INVESTMENTS IN HALF-YEAR 2014

6

India Brazil

LEADING ROLE IN MARKET CONSOLIDATION ACQUISITIONS HALF-YEAR 2014

Company Country Target Market

Klebag Chemie AG Switzerland Sealing & Bonding, Flooring

Company for flooring and coating products

South Korea Flooring

Lwart Química Ltda. Brazil Waterproofing, Roofing

7

Total sales: CHF 53 million

2. PERFORMANCE HALF-YEAR 2014

9

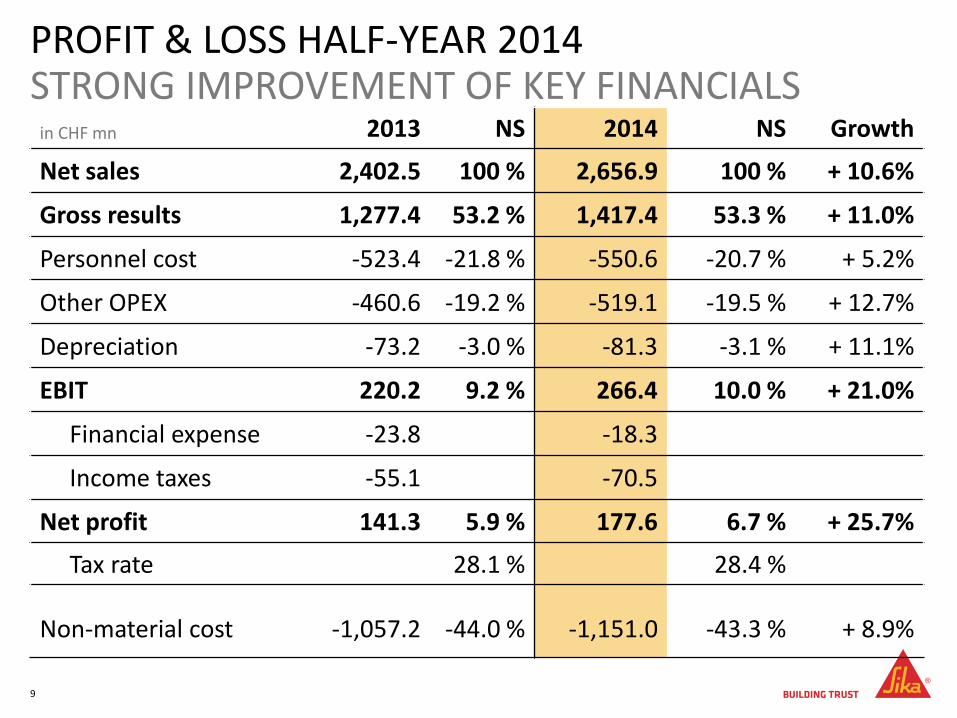

PROFIT & LOSS HALF-YEAR 2014 STRONG IMPROVEMENT OF KEY FINANCIALS

in CHF mn 2013 NS 2014 NS Growth

Net sales 2,402.5 100 % 2,656.9 100 % + 10.6%

Gross results 1,277.4 53.2 % 1,417.4 53.3 % + 11.0%

Personnel cost -523.4 -21.8 % -550.6 -20.7 % + 5.2%

Other OPEX -460.6 -19.2 % -519.1 -19.5 % + 12.7%

Depreciation -73.2 -3.0 % -81.3 -3.1 % + 11.1%

EBIT 220.2 9.2 % 266.4 10.0 % + 21.0%

Financial expense -23.8 -18.3

Income taxes -55.1 -70.5

Net profit 141.3 5.9 % 177.6 6.7 % + 25.7%

Tax rate 28.1 % 28.4 %

Non-material cost -1,057.2 -44.0 % -1,151.0 -43.3 % + 8.9%

10

SALES HALF-YEAR 2014 NEGATIVE CURRENCY IMPACT OF 7.5%

in CHF mn 2013 2014 Δ %

Net sales 2,402.5 2,656.9 + 254.4 +10.6

Organic growth + 237.5 +9.9

Acquisition effect + 197.0 +8.2

Currency effect - 180.1 -7.5

11

SALES GROWTH BY QUARTER CONTINUED GROWTH MOMENTUM

-1.3%

7.0% 7.3% 8.2%

14.1%

6.6%

+1.1%

1.2% 3.3%

9.6%

9.2%

7.4%

acquisition organic

Net sales 12 month rolling

at constant FX

-0.2%

8.2%

10.6%

17.8%

in CHF mn Q1 PY Q2 PY Q3 PY Q4 PY Q1 CY Q2 CY

Quarterly sales

1,043.1 1,359.4 1,405.2 1,334.5 1,206.2 1,450.7

23.3%

14.0%

12

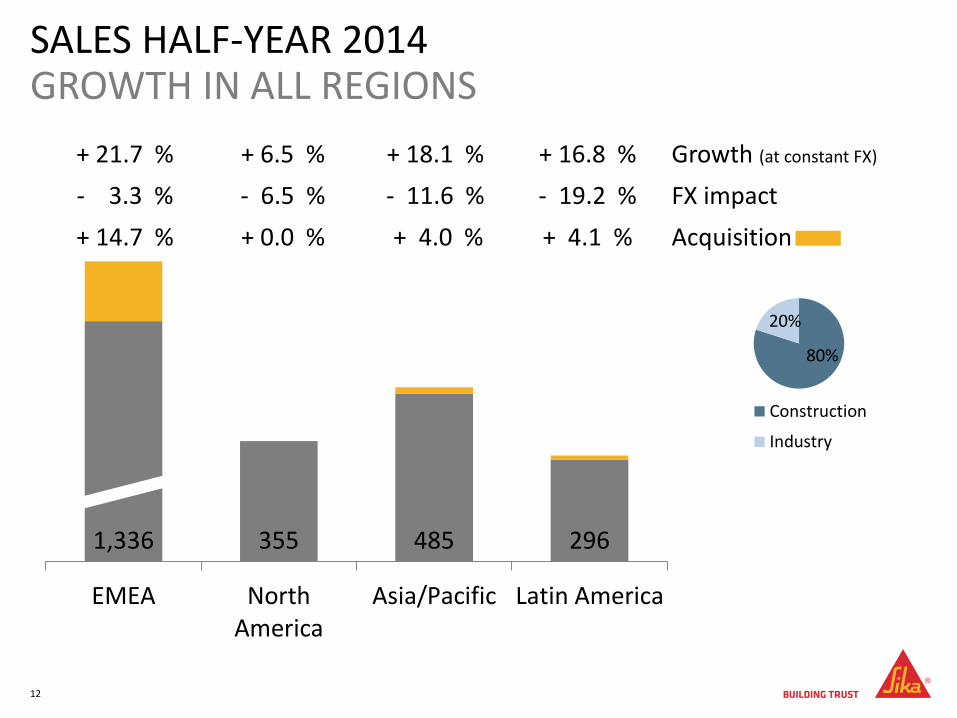

SALES HALF-YEAR 2014 GROWTH IN ALL REGIONS

1,336 355 485 296

EMEA NorthAmerica

Asia/Pacific Latin America

80%

20%

Construction

Industry

+ 21.7 % + 6.5 % + 18.1 % + 16.8 % Growth (at constant FX)

- 3.3 % - 6.5 % - 11.6 % - 19.2 % FX impact

+ 14.7 % + 0.0 % + 4.0 % + 4.1 % Acquisition

13

GROSS RESULT DEVELOPMENT STABLE GROSS RESULT

Gross result (trailing 12 months)

2009 2010 2011 2012 2013 2014 Jun (YTD)

55.1 % 53.9 % 50.5 % 52.2 % 52.4 % 53.3 %

14

CONSOLIDATED BALANCE SHEET JUNE 2014

in CHF mn 31.12.2013 30.06.2014 Δ

Cash and cash equivalents 1,028.3 526.8 - 501.5

Other current assets 1,559.6 1,862.3 + 302.7

Current assets 2,587.9 2,389.1 - 198.8

Non-current assets 2,144.1 2,194.3 + 50.2

Total assets 4,732.0 4,583.4 - 148.6

Current liabilities 1,189.1 997.6 - 191.5

Non-current liabilities 1,406.7 1,438.7 + 32.0

Equity incl. minorities 2,136.2 2,147.1 + 10.9

Total liabilities and equity 4,732.0 4,583.4 - 148.6

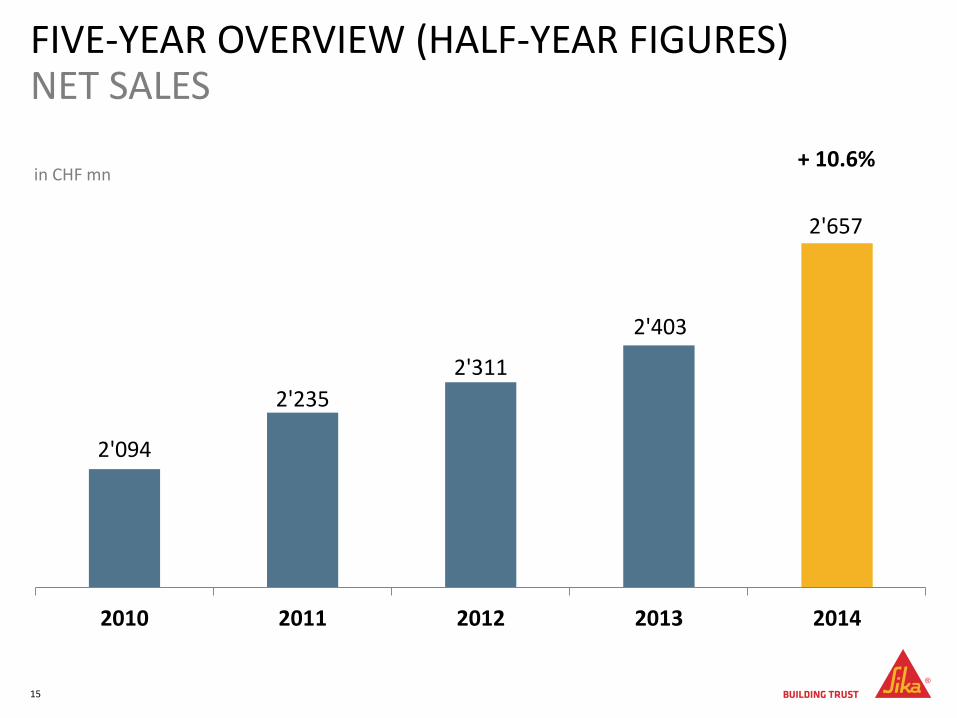

FIVE-YEAR OVERVIEW (HALF-YEAR FIGURES) NET SALES

in CHF mn

2'094

2'235

2'311

2'403

2'657

2010 2011 2012 2013 2014

15

+ 10.6%

FIVE-YEAR OVERVIEW (HALF-YEAR FIGURES) EBIT in CHF mn

217

178

198

220

266

2010 2011 2012 2013 2014

16

+ 21.0%

17

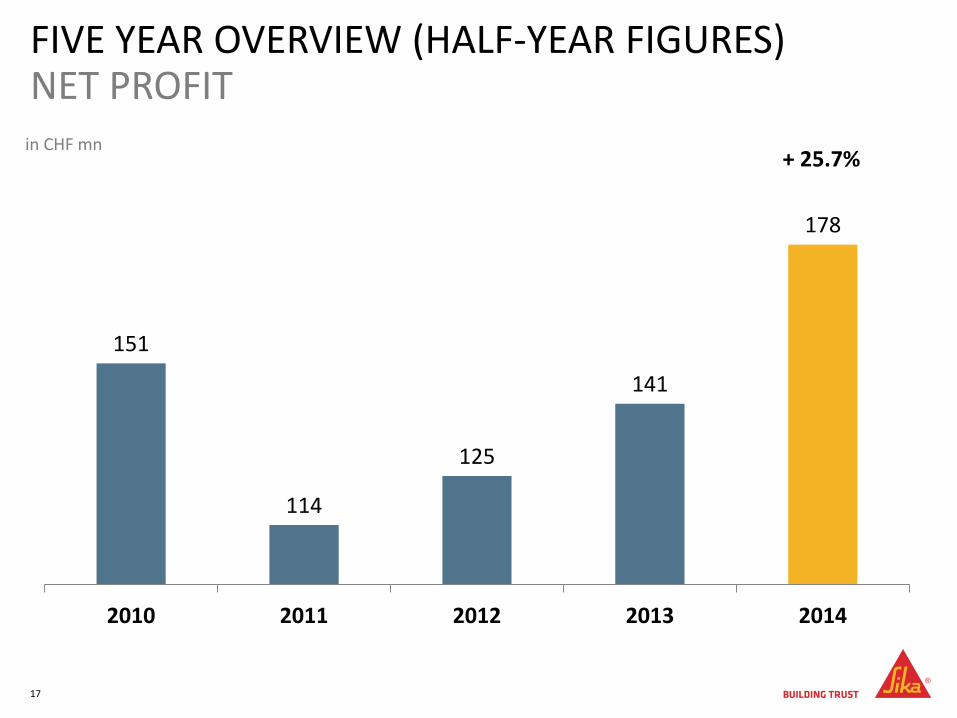

FIVE YEAR OVERVIEW (HALF-YEAR FIGURES) NET PROFIT

in CHF mn

151

114

125

141

178

2010 2011 2012 2013 2014

+ 25.7%

3. STRATEGY 2018

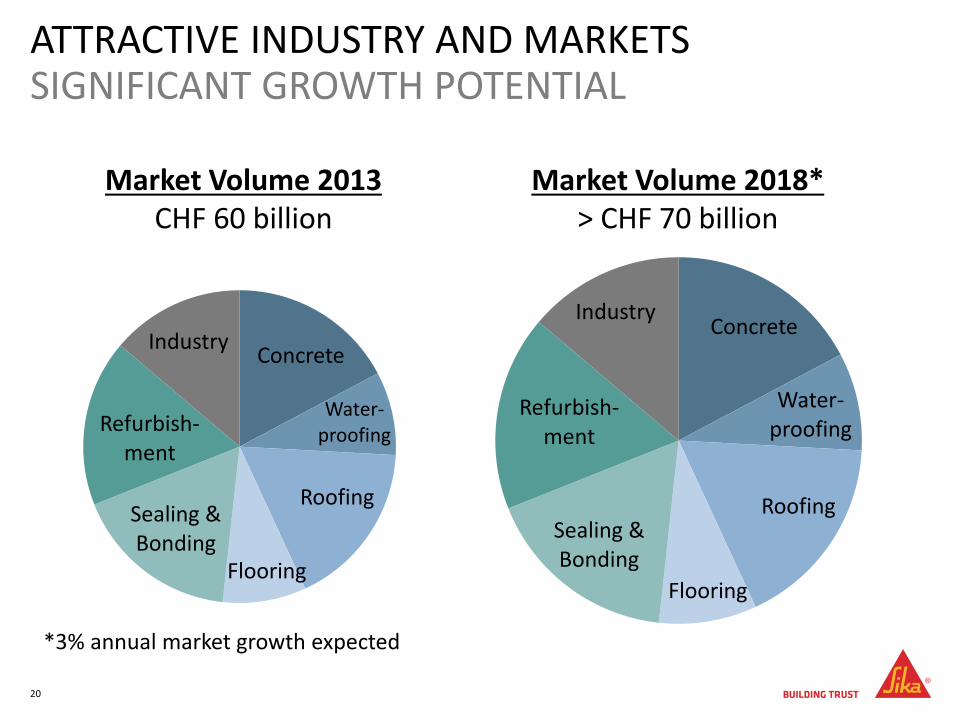

ATTRACTIVE INDUSTRY AND MARKETS

19

ATTRACTIVE INDUSTRY AND MARKETS SIGNIFICANT GROWTH POTENTIAL

Market Volume 2018* > CHF 70 billion

Concrete

Water- proofing

Roofing

Flooring

Sealing & Bonding

Refurbish-ment

Industry Concrete

Water- proofing

Roofing

Flooring

Sealing & Bonding

Refurbish-ment

Industry

Market Volume 2013 CHF 60 billion

*3% annual market growth expected

20

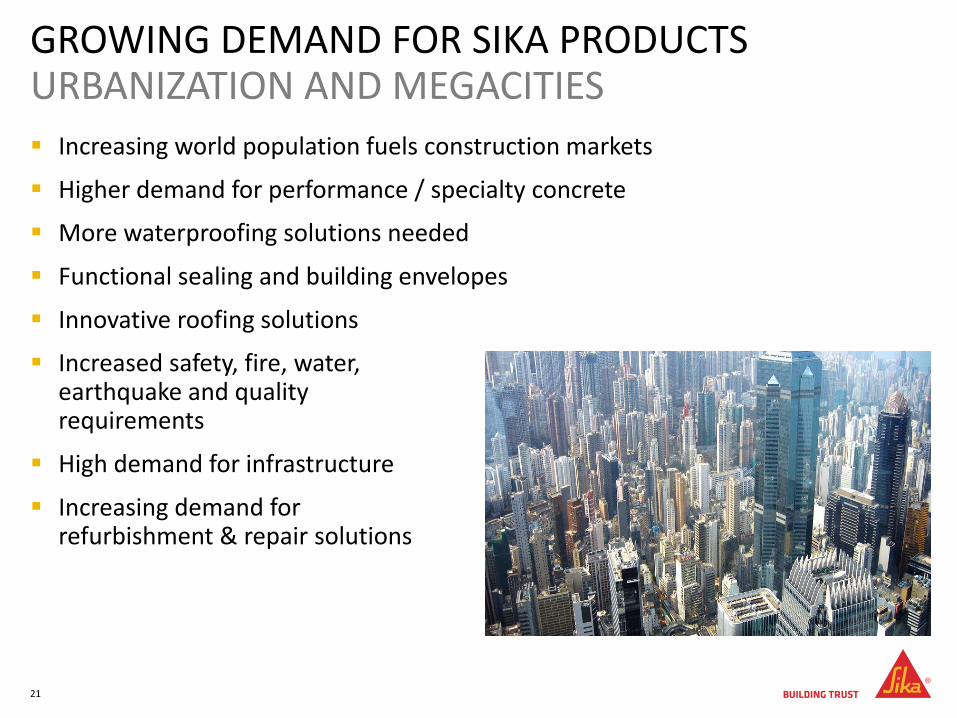

GROWING DEMAND FOR SIKA PRODUCTS URBANIZATION AND MEGACITIES

Increasing world population fuels construction markets

Higher demand for performance / specialty concrete

More waterproofing solutions needed

Functional sealing and building envelopes

Innovative roofing solutions

Increased safety, fire, water, earthquake and quality requirements

High demand for infrastructure

Increasing demand for refurbishment & repair solutions

21

GROWING DEMAND FOR SIKA PRODUCTS TREND FOR LIGHTER, SAFER VEHICLES

New materials like carbon fiber require bonding solutions

Composite body structures need bonding instead of welding

Adhesives enable stiffer, lighter, safer metal structures

Modular production concepts are based on fast, high strength bonding systems

22

GROWING DEMAND FOR SIKA PRODUCTS TREND FOR SUSTAINABILITY

More efficient use of limited natural resources and energy («green cities»)

Demand for longer life cycles of infrastructure and buildings

Demand for low-energy housing

Drive towards higher recyclability of materials

Demand for safe-to-use products, lower-emission products

New technologies for vehicles and transportation

Increasing environmental regulations

23

FRAGMENTED GLOBAL INDUSTRY OFFERS SIGNIFICANT GROWTH POTENTIAL

Construction Chemical Market 2013 > CHF 50 billion

Sika

Others

Competitor 2

Competitor 1

Competitor 3

Competitor 4

Top 5 companies with 26% market share

24

SIKA’S POSITION & COMPETITIVE ADVANTAGES

25

FOCUS ON 7 TARGET MARKETS

26

With our core competencies bonding, sealing, damping, reinforcing and protecting

Sealing & Bonding Refurbishment Industry

Concrete Waterproofing Roofing Flooring

STRONG GLOBAL POSITION: COMPETITIVE ADVANTAGES FOR PROFITABLE GROWTH

World market leader in construction chemicals

Leading adhesive producer for industrial markets

Successful focus on innovation (73 patents in 2013)

First mover in emerging markets (38% of sales)

Global footprint with over 160 factories worldwide

Leading global brand

Entrepreneurial company culture

Solid financial position (A- rating)

27

GROWTH MODEL AND TARGETS 2018

28

1. Market penetration - from roof to floor (cross selling, 7 target markets, KPM) - from new-build to refurbishment (life-cycle management) - push and pull market channels (specification, branding)

2. Global technology leadership with continuous innovations and economies of scale in core technologies

3. Accelerated build-up of emerging markets

4. Acquisitions to strengthen market access, technology, economies of scale

5. Strong company values with entrepreneurial spirit and high employee loyalty

STRATEGY 2018 SIKA’S GROWTH MODEL WILL DELIVER

29

Annual sales growth of 6% to 8% (at constant exchange rates, including acquisitions)

Emerging markets with 42% to 45% of group sales by 2018

Operating profit (EBIT) above 10% of net sales

Operating free cash flow above 6% of net sales

ROCE above 20%

Maintain A- rating

STRATEGY 2018 TARGETS

30

4. OUTLOOK

OUTLOOK 2014

32

Sales growth expectations lifted from 6 – 8% to 9 – 11% (at constant exchange rates)

Continued build-up of growth markets with 8 new factories

Asia/Pacific: double-digit growth expected in China and Southeast Asia, stable volumes in Japan, Korea and Pacific

Latin America: double-digit growth expected overall but uncertainties in various markets

North America: after positive development of residential market in 2013, commercial and infrastructure markets are expected to improve, expect mid single-digit growth

EMEA: Continuation of slow recovery, double-digit growth in Middle East and Africa, high acquisition impact

Margins on 2013 level expected

This presentation contains certain forward-looking statements. These forward-looking statements may be identified by words such as ‘expects’, ‘believes’, ‘estimates’, ‘anticipates’, ‘projects’, ‘intends’, ‘should’, ‘seeks’, ‘future’ or similar expressions or by discussion of, among other things, strategy, goals, plans or intentions. Various factors may cause actual results to differ materially in the future from those reflected in forward-looking statements contained in this presentation, among others:

Fluctuations in currency exchange rates and general financial market conditions

Interruptions in production

Legislative and regulatory developments and economic conditions

Delay or inability in obtaining regulatory approvals or bringing products to market

Pricing and product initiatives of competitors

Uncertainties in the discovery, development or marketing of new products or new uses of existing products, including without limitation negative results of research projects, unexpected side-effects of pipeline or marketed products

Increased government pricing pressures

Loss of inability to obtain adequate protection for intellectual property rights

Litigation

Loss of key executives or other employees

Adverse publicity and news coverage.

Any statements regarding earnings per share growth is not a profit forecast and should not be interpreted to mean that Sika’s earnings or earnings per share for this year or any subsequent period will necessarily match or exceed the historical published earnings or earnings per share of Sika.

For marketed products discussed in this presentation, please see information on our website: www.sika.com

All mentioned trademarks are legally protected.

FORWARD-LOOKING STATEMENTS

33

THANK YOU FOR YOUR ATTENTION