Embed Size (px)

Citation preview

1

6th Annual Global Forum

TAXATION ASPECTS OF ELECTRONIC COMMERCE

Addressing the Challenges and Opportunities

‘The state of play’

September 2001

26th Global Forum26-Sep-01

The role of the OECD: e-commerce taxation

Facilitating an international dialogue

which… brings together governments and business

to… build an international consensus

where... e-commerce flourishes and tax sovereignty and

neutrality of treatment is maintained

36th Global Forum26-Sep-01

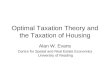

We have some basic principles for guidance

Solutions must meet the twin challenges– Fostering economic growth;

while– Safeguarding revenues

Guiding principle - neutrality– Neither more nor less favourable treatment

International consensus desirable

46th Global Forum26-Sep-01

But first some context before delving in

While estimates vary considerably...

56th Global Forum26-Sep-01

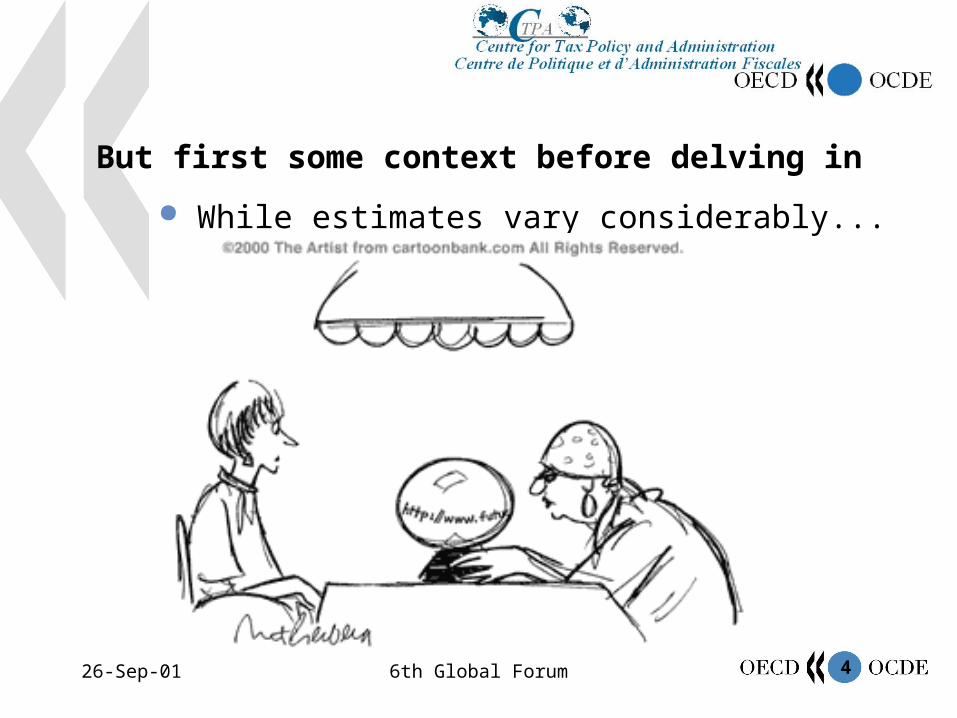

e-commerce context 1

e-commerce is becoming mainstream business It is a global phenomena

66th Global Forum26-Sep-01

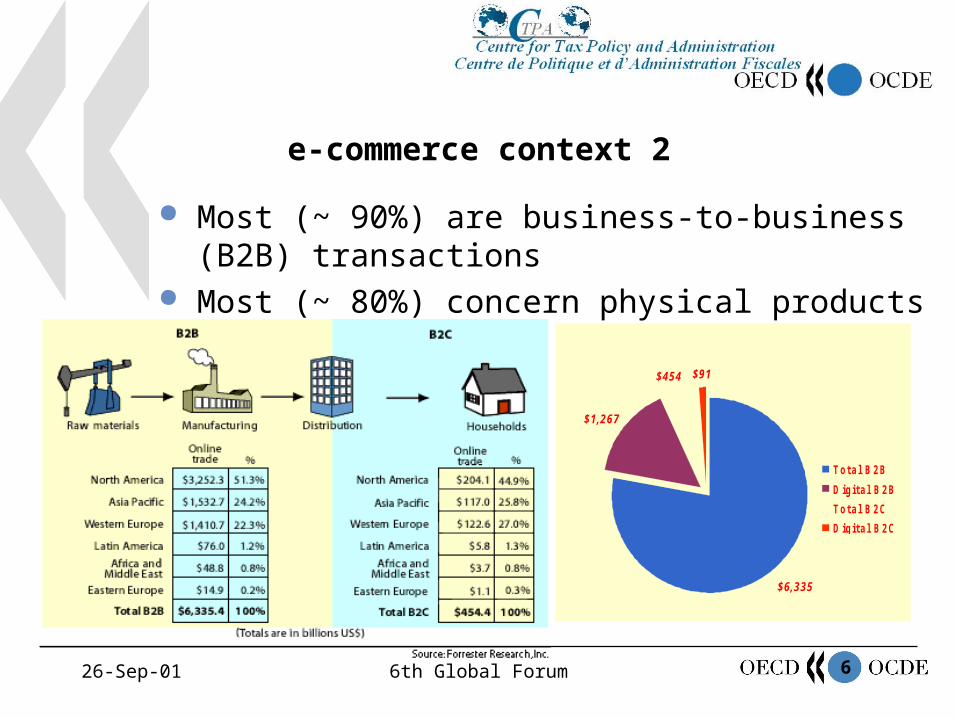

e-commerce context 2

Most (~ 90%) are business-to-business (B2B) transactions

Most (~ 80%) concern physical products

$6 ,3 35

$1 ,2 67

$454 $91

To t a l B 2 B

D ig it a l B 2 B

To t a l B 2 C

D ig it a l B 2 C

2004 forecast

76th Global Forum26-Sep-01

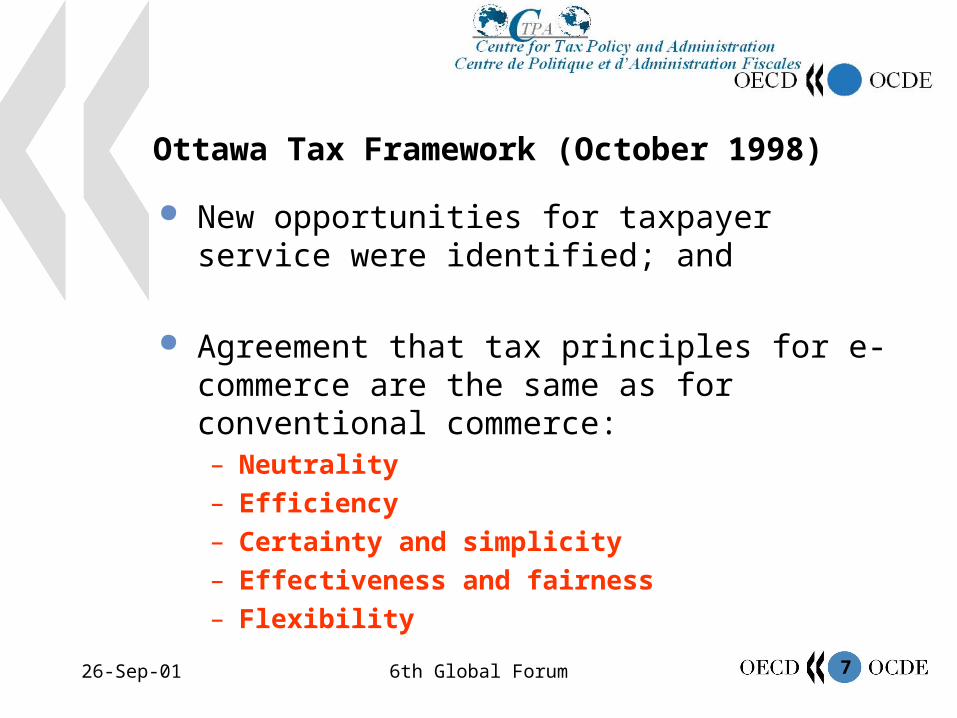

Ottawa Tax Framework (October 1998)

New opportunities for taxpayer service were identified; and

Agreement that tax principles for e-commerce are the same as for conventional commerce: – Neutrality– Efficiency– Certainty and simplicity– Effectiveness and fairness– Flexibility

86th Global Forum26-Sep-01

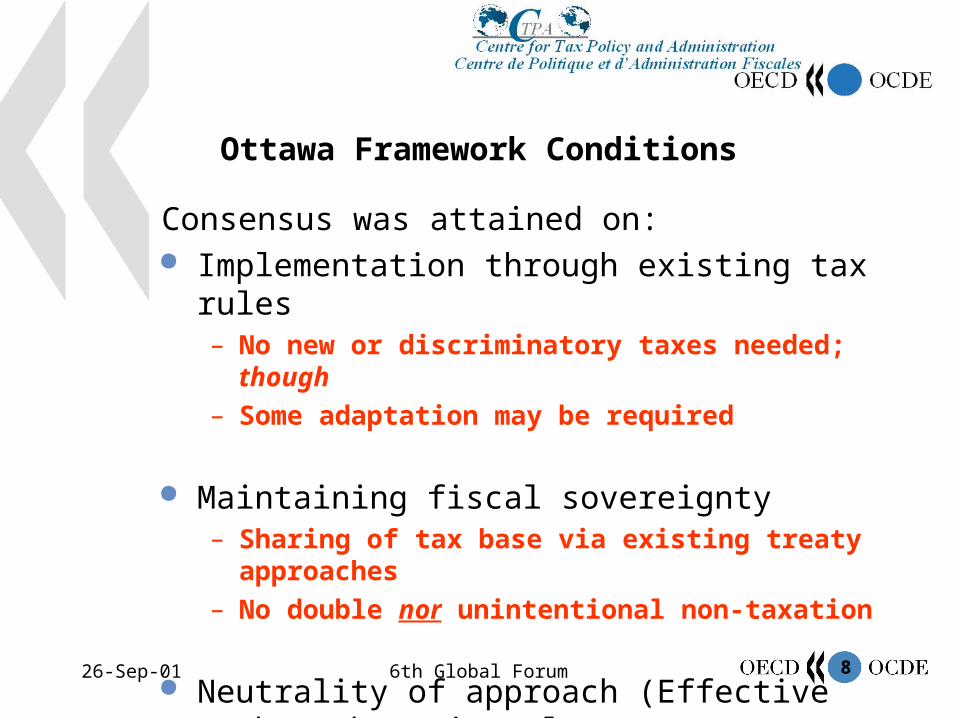

Ottawa Framework Conditions

Consensus was attained on: Implementation through existing tax rules

– No new or discriminatory taxes needed; though– Some adaptation may be required

Maintaining fiscal sovereignty– Sharing of tax base via existing treaty approaches– No double nor unintentional non-taxation

Neutrality of approach (Effective rather than Literal)

96th Global Forum26-Sep-01

A global dialogue has been initiated

Global issues require global solutions New working partnership established with

– Member countries– Non-member economies– Business

New methods– Technical Advisory Groups (TAGs)

Bringing all parties to the table as equals

106th Global Forum26-Sep-01

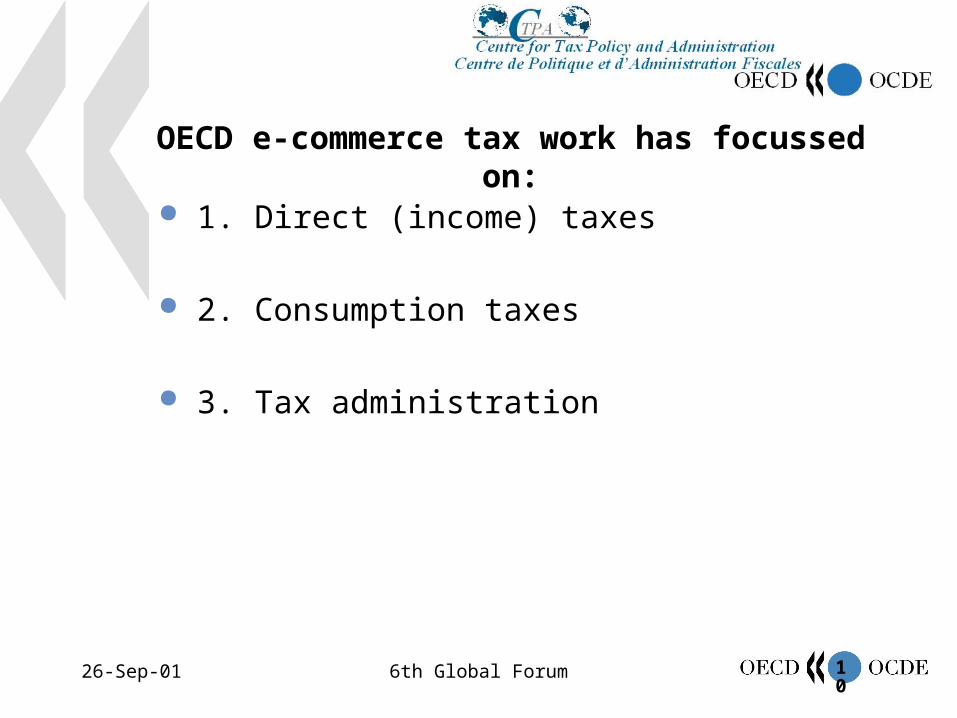

OECD e-commerce tax work has focussed on:

1. Direct (income) taxes

2. Consumption taxes

3. Tax administration

116th Global Forum26-Sep-01

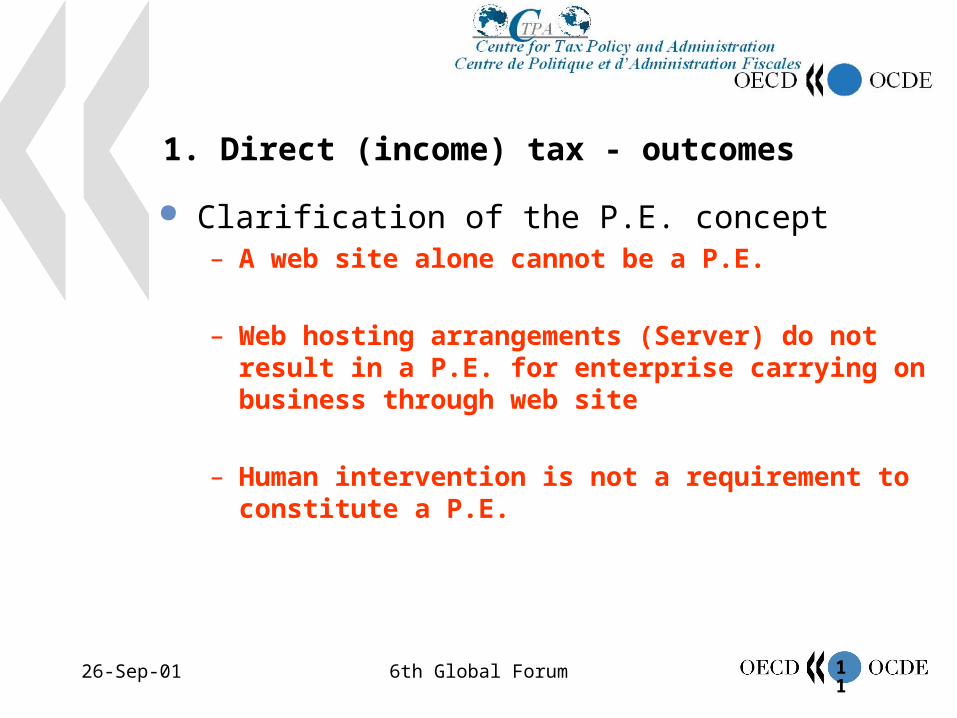

1. Direct (income) tax - outcomes

Clarification of the P.E. concept– A web site alone cannot be a P.E.

– Web hosting arrangements (Server) do not result in a P.E. for enterprise carrying on business through web site

– Human intervention is not a requirement to constitute a P.E.

126th Global Forum26-Sep-01

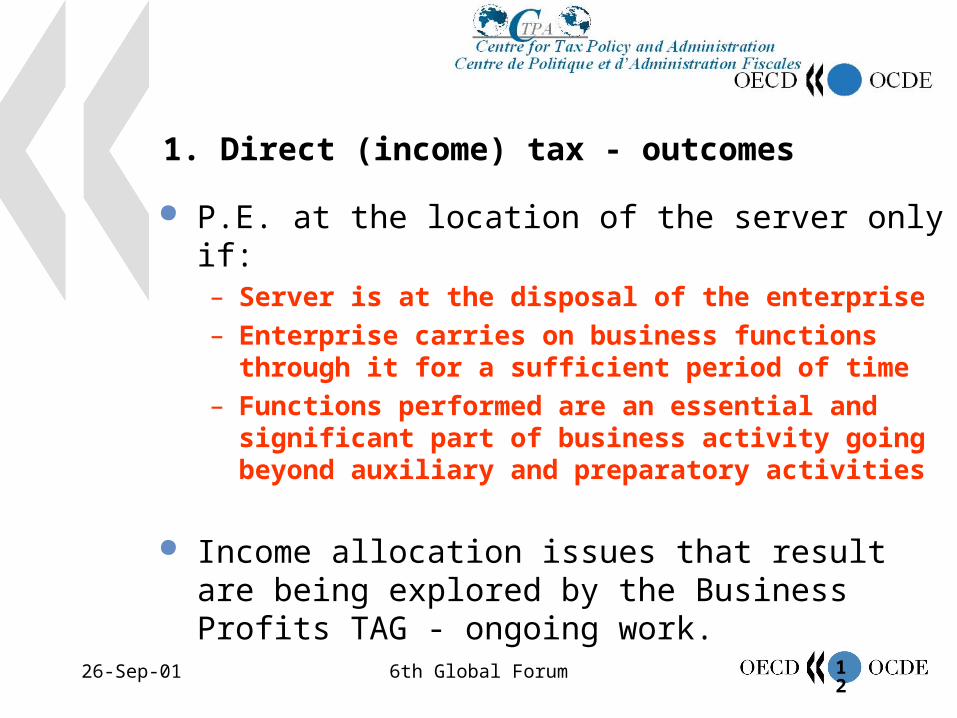

1. Direct (income) tax - outcomes

P.E. at the location of the server only if:– Server is at the disposal of the enterprise– Enterprise carries on business functions through it for

a sufficient period of time– Functions performed are an essential and significant

part of business activity going beyond auxiliary and preparatory activities

Income allocation issues that result are being explored by the Business Profits TAG - ongoing work.

136th Global Forum26-Sep-01

1. Direct (income) tax - outcomes

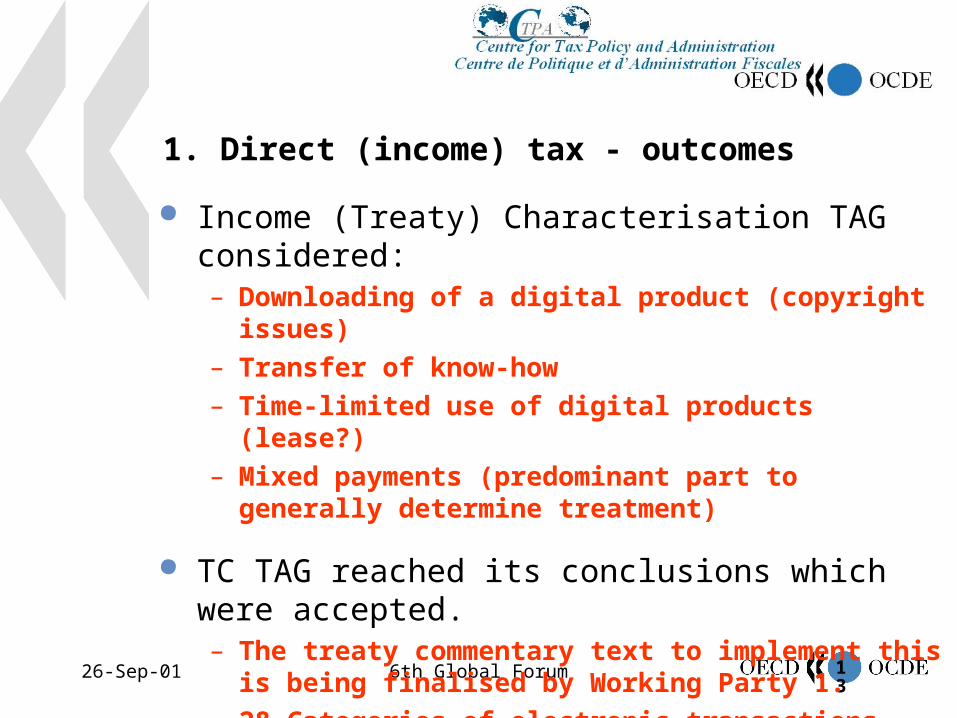

Income (Treaty) Characterisation TAG considered:– Downloading of a digital product (copyright issues)– Transfer of know-how– Time-limited use of digital products (lease?)– Mixed payments (predominant part to generally

determine treatment)

TC TAG reached its conclusions which were accepted. – The treaty commentary text to implement this is being

finalised by Working Party 1. – 28 Categories of electronic transactions considered

146th Global Forum26-Sep-01

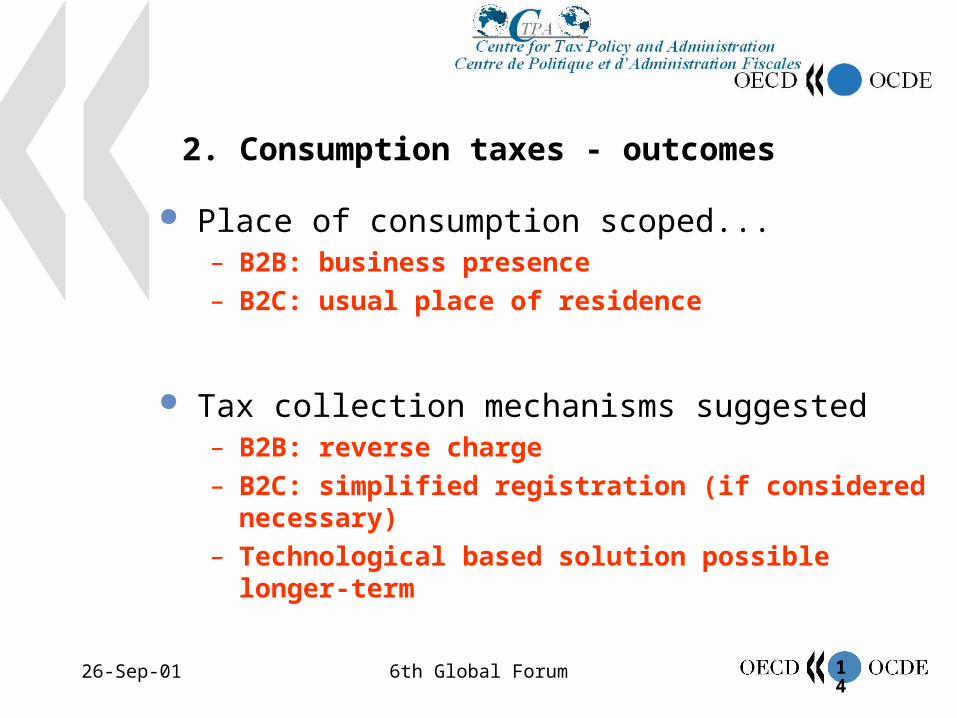

2. Consumption taxes - outcomes

Place of consumption scoped...– B2B: business presence– B2C: usual place of residence

Tax collection mechanisms suggested– B2B: reverse charge– B2C: simplified registration (if considered necessary)– Technological based solution possible longer-term

156th Global Forum26-Sep-01

2. Consumption taxes - on-going

Explore technology-based collection mechanisms

Practical means of verification for the place/status of the customer

Simplification of tax compliance requirements

Promoting administrative international co-operation

166th Global Forum26-Sep-01

3. Tax administration

Administrative issues consist of:– Compliance challenges; and– Taxpayer service opportunities

Both discussed at Montreal in June (www.ae-tax.ca)

Compliance challenges such as:– Identity issues - who, where– Access to information - when, what (transparency)– Tax collection mechanisms– International co-operation

176th Global Forum26-Sep-01

3. Tax administration

Opportunities abound...– Providing greater access to information– Registration and filing simplification– Electronic assessment and collection– Secure ways of paying taxes

Sharing best practice in administration

(www.fsmke.org)

186th Global Forum26-Sep-01

Outcomes

Comprehensive reports published (February 2001) detailing full range of emerging conclusions and recommendations:– P.E. - revised Commentary language– Income Characterisation - TAG conclusion agreed– Allocation to PE - discussion drafts from TAG– Consumption Tax - full report for comment– Administration - report for comment– Plus reports/papers from all TAGs

196th Global Forum26-Sep-01

Next steps

Continued efforts toward international consensus in various fields - particular focus on CT issues

Continued commitment to dialogue with business and non-member economies – TAGs: Business Profits, Consumption Tax &

Compliance Information and Documentation

Aim to progress the tax framework implementation requirements through 2001-2003

20

Stuart Hamilton [email protected]

http://www.oecd.org/subject/e_commerce/

TAXATION ASPECTS OF ELECTRONIC COMMERCE

Addressing the Challenges and Opportunities