Embed Size (px)

Citation preview

0

HAND BOOK ON CIVIL AVIATION STATISTICS

a glimpse of aviation statistics…..

2015-16

B. S. BHULLAR, rAS

DIRECTOR GENERAL OF CIVIL AVIATIONTECHNICAL CENTRE

OPPOS ITE SAFDARJUNG AI RPORTNew Delhi - 110003

ff.gtt. Tffi, rn.c.t.

FOREWORD

DGCA has been publishing on its website the monthly operating statisticsof scheduled airlines and air transport statistics every year. The annualpublication includes besides traffic statistics, fleet, and personnel statisticsas well as time series data.

In the year 20 13, it was decided to bring out regular annual publication viz.Handbook on civil aviation statistics, which illustrates civil aviation dataand brief analysis on passenger & freight traffic, aircraft, air safety, humanresources, operating economics and other aviation related statistics. I havegreat pleasure in releasing the fourth edition of Handbook on Civil AviationStatiStics pertaining to the year,2015-16.

In2O15-16, air traffic registered a robust growth compared to the previousyear. While the domestic passenger traffic registered a growth of 2I.6%o,international passenger traffic witnessed a growth of 8.9o/o during theperiod.

I am sure that the information containJd in this Handbook would be usefulto civil aviation stakeholders and researchers. I wish to complement thestaff of Statistics Division for their efforts to put all the data together andbring out this Handbook.

It will be our endeavour to include more topics in subsequent editions.Users are welcome to send in their suggestions to the Statistics Division ate-mail id:

--e(B.S. Bhullar)

Dated: 24th January, 2OI7

Tef.: +91 11 24620784, +91 11 24627830 . Fax: +91 11 24652760 . email : [email protected]

1

DGCA OVERVIEW

The Directorate General of Civil Aviation (DGCA) is a regulatory body in the field of Civil

Aviation primarily dealing with Air Safety issues. It is responsible for regulation of air

transport services to/from/within India and for enforcement of civil air regulations, air

safety and air worthiness standards. It also interfaces with all the regulatory functions of

International Civil Aviation Organization.

DGCA’s Vision Statement:

“Endeavour to promote safe and efficient Air Transportation through regulation and

proactive safety oversight system.”

DGCA has several directorates and divisions under its purview to carry out its functions and

services. Apart from this, there are 5 regional offices and 10 sub-regional offices as shown

below.

2

Sl. No. CONTENTS PAGE No.

1. PASSENGER TRAFFIC STATISTICS 1-5

2. FREIGHT TRAFFIC STATISTICS 6-7

3. AIRCRAFT STATISTICS 8-10

4. NSOP STATISTICS 11-12

5. OPERATING ECONOMICS STATISTICS 13-15

6. HUMAN RESOURCE STATISTICS 16-19

7. AIR SAFETY STATISTICS 20

8. OTHER AVIATION RELATED STATISTICS 21-22

1

PASSENGER TRAFFIC

Air Passenger Traffic in India, both domestic and international witnessed a positive growth in the year 2015-16 compared to the previous year.

TABLE 1: PASSENGER TRAFFIC AT A GLANCE

PASSENGER TRAFFIC UNIT 2015-16 2014-15

Domestic Passengers Departing Passengers

85.20 million

(21.58)

70.08 million (15.51)

Domestic Airline Demand Revenue Passenger Kilometers (RPK)

80.96 billion (20.80)

67.02 billion (13.32)

Domestic Airline Capacity Available Seat Kilometers (ASK)

97.71 billion (15.21)

84.81 billion (5.07)

International Passengers Departing and Arriving Passengers

49.78 million

(8.85)

45.74 million (5.85)

Total Passengers (Domestic & International) 134.98 (16.54)

115.82 (11.63)

Figures in parenthesis refer to percentage change over previous year.

ASK is calculated as the sum of products obtained by multiplying the total number of seats that are available in each flight by the

flight stage distance.

RPK is calculated as the sum of the product obtained by multiplying the number of revenue passengers carried on each flight stage

by the stage distance.

The domestic passenger traffic registered a compound annual growth rate (CAGR) of 10.10% during the period 2006-07 to 2015-16 while the international passenger traffic grew at 8.75% (CAGR) during the same period.

During the years from 2006-07 to 2015-16, the capacity (ASK) in the domestic market grew at a rate of 8.04% (CAGR) while the demand (RPK) grew at 10.29% (CAGR) during the same period.

35.844.4 39.5 45.3

53.860.8 57.6 60.6

70.1

85.2

23.4 27.2 28.9 32.1 35.1 38.1 40.3 43.1 45.7 49.8

59.271.6 68.4

77.488.9

98.9 97.9 103.7115.8

135.0

0

20

40

60

80

100

120

140

160

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

----

-Pas

sen

gers

(In

Mill

ion

)---

--

CHART 1. PASSENGER TRAFFIC CARRIED BY SCHEDULED CARRIERS OVER THE PAST DECADE

DOMESTIC PASSENGERS INTERNATIONAL PASSENGERS TOTAL PASSENGERS

2

TABLE 2: YEAR ON YEAR GROWTH IN PASSENGERS AND PASSENGER LOAD FACTOR (PLF)

NAME OF THE AIRLINE

PASSENGERS (2014-15)

(In Number)

PASSENGERS (2015-16)

(In Number)

YoY GROWTH IN PASSENGERS

(%)

PLF (2014-15)

(%)

PLF (2015-16)

(%)

YoY GROWTH IN

PLF (%)

AIR INDIA 11727171 12742163 8.7 77.2 79.2 2.6

AIR INDIA EXPRESS

191095 149217 -21.9 73.5 80.1 9.0

ALLIANCE AIR 310492 400340 28.9 68.3 66.5 -2.6

SPICEJET 10716089 10670866 -0.4 81.8 92.0 12.5

JET ARWAYS 12473808 15961308 28.0 78.4 80.6 2.8

INDIGO 23727080 31453451 32.6 79.4 84.1 5.9

GO AIR 6529936 7160189 9.7 79.1 83.7 5.7

JETLITE 3030638 2439721 -19.5 80.1 79.3 -0.9

AIR ASIA 553106 1705808 208.4 76.1 80.2 5.4

AIR COSTA 723627 711836 -1.6 74.1 80.7 9.0

VISTARA 100919 1422611 1309.7 53.7 69.4 29.1

TRUJET 0 204588 - - 80.1 -

AIR PEGASUS 0 175577 - - 78.5 -

Note: VISTARA OPERATED FOR ONLY THREE MONTHS i.e. JANUARY-MARCH DURING THE YEAR 2014-15.

AIR PEGASUS STARTED ITS OPERATIONS IN JULY 2015 AND TRUJET IN MAY 2015.

If we look at Airline-wise Growth in the number of Domestic Passengers, it is found that the high growth of 21.58 % in the total domestic passengers during 2015-16 is mainly due to the high growth in passengers carried by Alliance Air, Jet Airways, IndiGo and Air Asia. Another factor which led to the high growth is the introduction of the new Airlines such as Vistara, Trujet and Air Pegasus.

In the year 2015-16, both ASK and RPK in the domestic market registered a positive growth compared to the previous year. The Passenger Load Factor in the domestic market, which fell from 74.6% in 2012-13 to 73.3% in 2013-14, went up to 82.9% in 2015-16 after rising to 79.0 % in 2014-15.

33

51

9

41

71

8

37

70

4

43

95

9

52

70

7

59

08

4

56

55

3

59

13

9

67

02

3

80

95

8

48

70

2

60

59

0

59

16

0

61

09

1

68

21

6

78

63

9

75

84

3

80

71

6

84

80

5

97

71

3

68.8 68.963.7

72.077.3 75.1 74.6 73.3

79.082.9

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

----

-Pax

Lo

ad F

acto

r (%

)---

--

----

-RP

K &

ASK

(In

Mill

ion

)---

--

CHART 2: CAPACITY V/S DEMAND IN DOMESTIC MARKET OVER THE PAST DECADE

RPK (DEMAND) ASK (CAPACITY) PAX LOAD FACTOR

3

In the year 2015-16, domestic market experienced expansion in capacity as well as demand which is evident from the Chart 3 as both RPK & ASK witnessed positive growth in all the months as compared to the corresponding months in the previous year. Also, in most of the months YoY growth in RPK exceeded the YoY growth in ASK implying an improvement in the passenger load factor and hence efficiency except for the months of September, December and February.

In the year 2015-16 both in terms of passenger carried and RPK, IndiGo had the maximum market share

followed by Jet Airways, Air India and SpiceJet.

21.6

18.0

15.6

28.1

18.0

12.5

17.5

24.9

19.6

22.8 24.3

27.0

7.8 8.1 8.7

10.912.3

12.6

13.2

20.1

20.221.8

26.8

20.8

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

APR MAY JUN JUL AUG SEP OCT NOV DEC JAN FEB MAR

----

Yo

Y G

row

th in

Pax

Lo

ad F

acto

r (%

)---

-

---Y

oY

Gro

wth

in R

PK

& A

SK (

%)-

--

CHART 3: MONTH-WISE GROWTH IN CAPACITY V/S DEMAND IN DOMESTIC MARKET, 2015-16

YoY Growth in RPK YoY Growth in ASK YoY Growth in PLF

39.9

17.0

15.1

11.5

8.42.6

2.31.8

0.7

0.3

0.10.10.1

1.3

CHART 4: MARKET SHARE(%) IN TERMS OF DOMESTIC MARKET DEMAND (RPK) -

2015-16

INDIGO JET AIRWAYS AIR INDIA

SPICEJET GO AIR JETLITE

AIR ASIA VISTARA AIR COSTA

ALLIANCE AIR TRUEJET AIR PEGASUS

AIR INDIA EXPRESS

36.9

18.7

15.0

12.5

8.42.9

2.01.7

0.8

0.5

0.2

0.2

0.2

0.6

CHART 5: DOMESTIC MARKET SHARE(%) IN TERMS OF PASSENGERS CARRIED -

2015-16

INDIGO JET AIRWAYS AIR INDIA

SPICEJET GO AIR JETLITE

AIR ASIA VISTARA AIR COSTA

ALLIANCE AIR TRUEJET AIR PEGASUS

AIR INDIA EXPRESS

4

In terms of Passenger Load Factor (PLF), a measure of capacity utilisation of airlines, for scheduled domestic operations, SpiceJet registered the highest PLF of 92.0 % followed by IndiGo (84.1%), Go Air (83.7%). SpiceJet also topped the position in terms of scheduled international operations with a PLF of 85.4% followed by Jet Airways (83.7%) and IndiGo (82.8%).

INTERNATIONAL PASSENGER MARKET SHARE

TABLE 3: MARKET SHARE (%) OF INTERNATIONAL PASSENGERS CARRIED BY SCHEDULED INDIAN CARRIERS

AND FOREIGN CARRIERS.

YEAR FOREIGN CARRIERS INDIAN CARRIERS

2004-05 71.1 28.9

2009-10 65.5 34.5

2010-11 63.8 36.2

2011-12 64.1 35.9

2012-13 66.2 33.8

2013-14 61.7 38.3

2014-15 63.0 37.0

2015-16 63.4 36.6

92.084.1

80.6 80.1 79.2 83.7 80.7 80.2 80.1 79.3 78.5

69.4 66.5

85.482.8

83.7 82.4

73.9

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

----

-Pax

Lo

ad f

cato

r (%

)---

--CHART 6: PASSENGER LOAD FACTOR (PLF) OF SCHEDULED INDIAN CARRIERS, 2015-16

DOMESTIC INTERNATIONAL

5

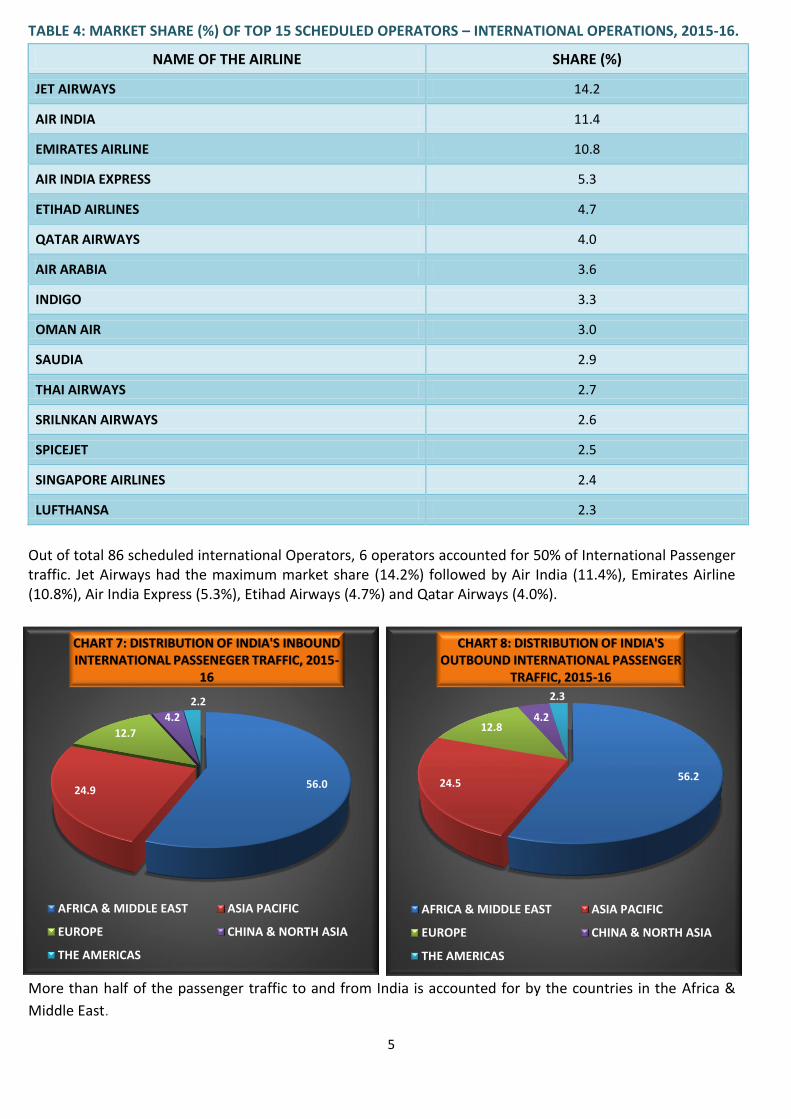

TABLE 4: MARKET SHARE (%) OF TOP 15 SCHEDULED OPERATORS – INTERNATIONAL OPERATIONS, 2015-16.

NAME OF THE AIRLINE SHARE (%)

JET AIRWAYS 14.2

AIR INDIA 11.4

EMIRATES AIRLINE 10.8

AIR INDIA EXPRESS 5.3

ETIHAD AIRLINES 4.7

QATAR AIRWAYS 4.0

AIR ARABIA 3.6

INDIGO 3.3

OMAN AIR 3.0

SAUDIA 2.9

THAI AIRWAYS 2.7

SRILNKAN AIRWAYS 2.6

SPICEJET 2.5

SINGAPORE AIRLINES 2.4

LUFTHANSA 2.3

Out of total 86 scheduled international Operators, 6 operators accounted for 50% of International Passenger traffic. Jet Airways had the maximum market share (14.2%) followed by Air India (11.4%), Emirates Airline (10.8%), Air India Express (5.3%), Etihad Airways (4.7%) and Qatar Airways (4.0%).

More than half of the passenger traffic to and from India is accounted for by the countries in the Africa &

Middle East.

56.024.9

12.7

4.2

2.2

CHART 7: DISTRIBUTION OF INDIA'S INBOUND INTERNATIONAL PASSENEGER TRAFFIC, 2015-

16

AFRICA & MIDDLE EAST ASIA PACIFIC

EUROPE CHINA & NORTH ASIA

THE AMERICAS

56.224.5

12.84.2

2.3

CHART 8: DISTRIBUTION OF INDIA'S OUTBOUND INTERNATIONAL PASSENGER

TRAFFIC, 2015-16

AFRICA & MIDDLE EAST ASIA PACIFIC

EUROPE CHINA & NORTH ASIA

THE AMERICAS

6

FREIGHT TRAFFIC

Air cargo carried by scheduled airline operators, both domestic and international witnessed a positive growth

in 2015-16.

TABLE 5: FREIGHT TRAFFIC AT A GLANCE

The domestic cargo traffic registered a growth of 7.6% (CAGR) over the period from 2006-07 to 2015-16 while International cargo traffic grew at 4.7% (CAGR) during the same period.

Dedicated cargo refers to the cargo carried by aircrafts solely meant for freight carriage.

The proportion of the total domestic cargo carried as belly cargo has generally been declining over the years

since 2005-06 with the exception of 2014-15.

9271025 1072

1139

12921219 1238 1262

1368 1404

322 368 342 394465 453 452 508

591 624

0

200

400

600

800

1000

1200

1400

1600

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

--Fr

eig

ht

(Th

ou

san

d M

etr

ic T

on

ne

)--

CHART 9: FREIGHT TRAFFIC CARRIED BY SCHEDULED CARRIERS OVER THE PAST DECADE

INTERNATIONAL DOMESTIC

86.0 83.3 82.1 79.7 78.8 76.9 80.0 79.9

14.0 16.7 17.9 20.3 21.2 23.1 20.0 20.1

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2005-06 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

CHART 10: PROPORTION OF DOMESTIC CARGO CARRIED AS BELLY CARGO AND IN DEDICATED FREIGHTERS

BELLY CARGO DEDICATED CARGO

FREIGHT TRAFFIC 2015-16 2014-15

DOMESTIC 6.24 Lakh MT

(5.41) 5.91 Lakh MT

(16.54)

INTERNATIONAL 14.04 Lakh MT

(2.63) 13.68 Lakh MT

(8.57)

Figures in parenthesis refer to percentage change over previous year; MT: Metric Tonne.

7

TABLE 6: PROPORTION OF INTERNATIONAL CARGO CARRIED BY INDIAN AND FOREIGN CARRIERS

Freight traffic is coming to India in almost equal proportion from around the World except the freight traffic

from the Americas while from India, more than half of the freight traffic is carried to the countries in the

Africa & Middle East.

27.0

26.3

22.6

22.6 1.5

CHART 11: DISTRIBUION OF INDIA'S INBOUND INTERNATIONAL FREIGHT

TRAFFIC, 2015-16

EUROPE AFRICA & MIDDLE EAST

ASIA PACIFIC CHINA & NORTH ASIA

THE AMERICAS

52.0

23.5

15.58.0

1.0

CHART 12: DISTRIBUTION OF INDIA'S OUTBOUND INTERNATIONAL FREIGHT

TRAFFIC, 2015-16

AFRICA & MIDDLE EAST EUROPE

ASIA PACIFIC CHINA & NORTH ASIA

THE AMERICAS

YEAR INDIAN CARRIERS (%) FOREIGN CARRIERS (%)

2004-05 13.6 86.4

2009-10 16.1 83.9

2010-11 20.3 79.7

2011-12 21.1 78.9

2012-13 17.7 82.3

2013-14 18.3 81.7

2014-15 17.8 82.2

2015-16 16.9 83.1

8

AIRCRAFT

TABLE 7: AIRCRAFT STATISTICS AT A GLANCE

SCHEDULED AIRCRAFT MOVEMENTS( IN LAKHS)

2015-16 2014-15

DOMESTIC 7.00 (13.45) 6.17

INTERNATIONAL 3.22 (10.65) 2.91

Figures in parenthesis refer to percentage change over previous year.

As in the case of passenger and freight traffic, aircraft movements (both domestic and international) also have

registered a positive growth in the year 2015-16 over 2014-15.

*Average Seat Capacity= Total ASK flown/ Total Aircraft Km. Flown.

149

185180

158

133

176 180

157148

105

70 66

47

212

186

180 179

160

0

50

100

150

200

250

----

Ave

rage

Se

at C

apac

ity

(In

No

.)--

--

Chart 13: AVERAGE SEAT CAPACITY* OF SCHEDULED OPERATING INDIAN FLEET (2015-16)

DOMESTIC INTERNATIONAL

9

TABLE 8: FLEET STATISTICS OF SCHEDULED INDIAN OPERATORS AS ON 31st MARCH, 2015.

NAME OF THE OPERATOR TYPE OF AIRCRAFT NUMBER OF AIRCRAFTS

SEAT CAPACITY

AIR INDIA

Boeing747-400 5 423

777-200LR 3 238

777-300ER 12 342

B-787 19 256

A-319 22 122/144

A-320 20 150/168/180

A-321 20 182

Total (All Types) 101

AIR INDIA EXPRESS Boeing 737-800 17 186

ALLIANCE AIR

ATR 42-320 4 48

CRJ-700 4 70

ATR-72-212A 2 70

Total (All Types) 10

INDIGO A320-200 94 180

SPICEJET

Boeing 737-800 18 186

Boeing 737-900ER 1 212

Q-400 15 78

Total (All Types) 34

GO AIR A320 Leased 19 180

JETLITE

Boeing 737-700 3 134

Boeing 737-800 5 168

Boeing 737-900ER 1 202

Total (All Types) 9

BLUE DART Boeing 757-200 5 Freighter

JET AIRWAYS

B-737-700 3 134

B-737-800 59 168

B-737-900 5 184

ATR72-500/600 18 68

A330-200/300 12 293

B-777-300ER 10 346

Total (All Types) 107

AIR COSTA

Embraer and ERJ 170 -100 LR (VT-LSR)

1 67

Embraer and ERJ 170 -100 LR (VT-LNR)

1 67

Embraer and ERJ 190 -100 STD (VT-LBR)

1 112

Embraer and ERJ 190 -100 STD (VT-LVR)

1 112

Total (All Types) 4

VISTARA Airbus A320 6 148

AIR ASIA Airbus A320 3 180

Total All Airlines (All Types) 409

10

STAGE LENGTH

TABLE 9: AVERAGE STAGE LENGTH* FLOWN (IN KILOMETRES) BY SCHEDULED INDIAN FLEET, 2015-16.

NAME OF THE AIRLINE DOMESTIC OPERATION INTERNATIONAL OPERATION

AIR INDIA 1117.4 6200.2

INDIGO 947.5 2219.8

AIR INDIA EXPRESS 919.4 2374.6

JET AIRWAYS 748.7 2946.9

SPICEJET 739.6 1714.0

AIR ASIA 1093.2

No Operation

VISTARA 1022.6

GO AIR 949.9

JETLITE 790.1

AIR COSTA 751.6

ALLIANCE AIR 677.8

TRUJET 437.6

AIR PEGASUS 416.2

*Average Stage Length is calculated by dividing the total aircraft km flown by the total number of aircraft departure.

TABLE 10: SUMMARY OF AIR OBJECTS REGISTERED WITH DGCA AS ON 8th April, 2016.

OPERATOR TYPE

AIR

CR

AFT

HEL

ICO

PTE

R

BA

LLO

ON

HA

NG

GLI

DER

GLI

DER

MO

TOR

GLI

DER

ULT

RA

-LIG

HT

EXP

ERIM

ENTA

L

TOTA

L SCHEDULED 468 0 0 0 0 0 0 0 468

NON-SCHEDULED 186 213 7 0 0 0 0 0 406

GOVERNMENT 125 37 0 5 41 0 0 1 209

PRIVATE 164 52 14 15 6 0 6 0 257

TRAINING 285 1 0 1 16 1 6 1 311

MISCELLANEOUS 6 0 0 3 0 0 28 4 41

GRAND TOTAL 1234 303 21 24 63 1 40 6 1692

Source: Directorate of Air Worthiness, DGCA.

11

NON-SCHEDULED OPERATORS (NSOP)

Source: Directorate of Air Transport- I and Directorate of Air Worthiness.

Out of the total 72 NSOP domestic (aircraft) operators, top 15 operators accounted for more than half of the

total number of domestic flights operated in the year 2015-16.

156183

229

272

327

370

409 412

366 361

393406

44 56 66

99122 127 134

147125 120 126 123

0

50

100

150

200

250

300

350

400

450

----

---N

um

be

r---

----

CHART 14: NON-SCHEDULED OPERATORS

Number of aircrafts (including helicopters) Number of OperatorsAs on 31st March

12.6

5.7

5.4

3.8

3.7

3.1

2.9

2.8

2.6

2.5

2.5

2.2

2.2

2.2

2.2

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0

Relience Commercial

A R Airways

BG Shirke

Pinnacle

Saraya

Air Charter Services

Himayaputra

Orbit

VRL

Span

Joy Jets

Airmid

GMR

Trans Bharat

Karnawati

CHART 15: TOP 15* NSOP-DOMESTIC (AIRCRAFT) OPERATIONS (% SHARE)- 2015-16

* In terms of number of flights operated.

12

Out of the total 32 non-scheduled international (aircraft) operators, top 15 operators accounted for more

than 80% of the total number of international flights operated in the year 2015-16.

Out of the total 54 non-scheduled Helicopter operators, top 3 operators accounted for 87% of the total

number of flights operated in the year 2015-16.

14.8

9.6

9.0

6.5

6.1

5.6

4.6

4.3

4.3

4.0

2.9

2.8

2.8

2.5

2.3

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0

Reliance Commercial (P) Ltd.

VRL Logistics Ltd.

A R Airways (P) Ltd.

Poonawalla Aviation (P) Ltd.

Zest Aviaition (P) Ltd.

Karnavati Aviaition (P) Ltd.

Airmid Aviaition Services

Raymond Ltd.

Universal Airways (P) Ltd.

Relience Transport & Travels Ltd.

Taj Air Ltd.

L&T Aviaiton Service (P) Ltd.

Coromandal Travels Ltd.

Ligare Aviation Ltd.

Ashley Aviation Ltd.

CHART 16: TOP 15* NSOP-INTERNATIONAL (AIRCRAFT) OPERATIONS (% SHARE)- 2015-16

* In terms of number of flights operated

36.7

31.1

19.2

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0

Global Vectra

Pawan Hans

Himalyan helicharters

CHART 17: TOP 3* NON-SCHEDULED HELICOPTER OPERATORS (% SHARE)- 2015-16

* In terms of number of flights operated.

13

OPERATING ECONOMICS

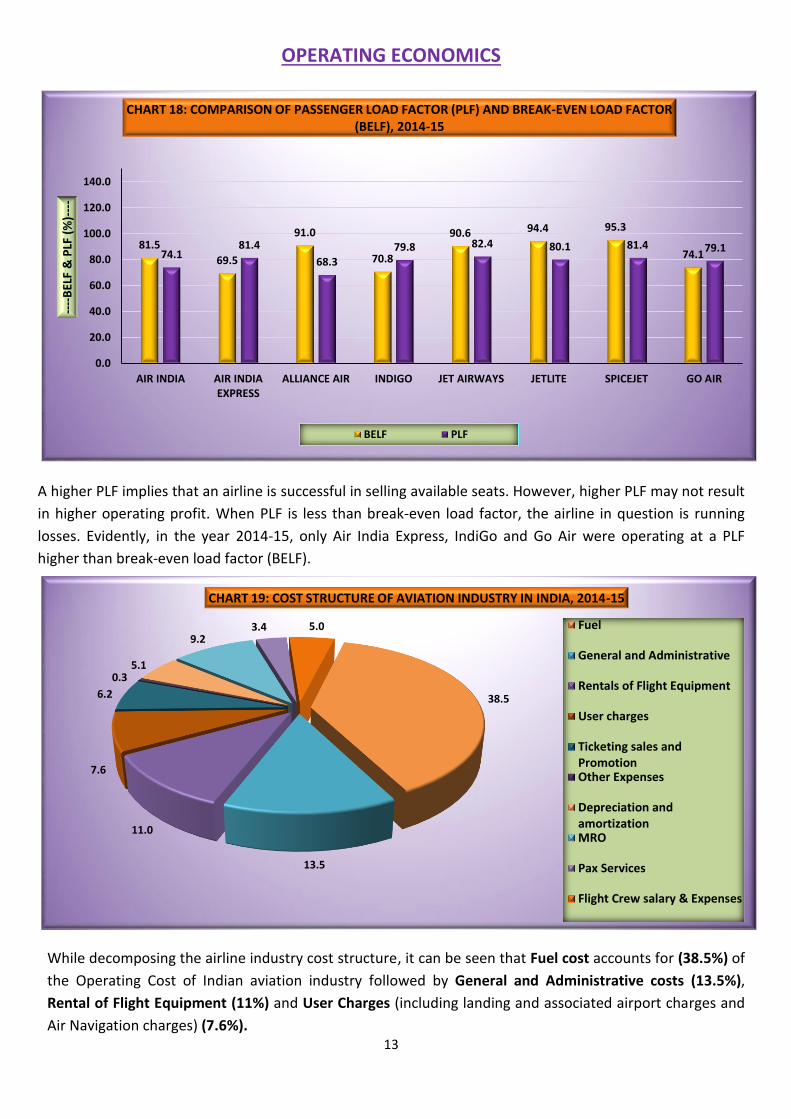

A higher PLF implies that an airline is successful in selling available seats. However, higher PLF may not result

in higher operating profit. When PLF is less than break-even load factor, the airline in question is running

losses. Evidently, in the year 2014-15, only Air India Express, IndiGo and Go Air were operating at a PLF

higher than break-even load factor (BELF).

While decomposing the airline industry cost structure, it can be seen that Fuel cost accounts for (38.5%) of

the Operating Cost of Indian aviation industry followed by General and Administrative costs (13.5%),

Rental of Flight Equipment (11%) and User Charges (including landing and associated airport charges and

Air Navigation charges) (7.6%).

81.5

69.5

91.0

70.8

90.6 94.4 95.3

74.174.181.4

68.379.8 82.4 80.1 81.4 79.1

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

AIR INDIA AIR INDIAEXPRESS

ALLIANCE AIR INDIGO JET AIRWAYS JETLITE SPICEJET GO AIR

----

BEL

F &

PLF

(%

)---

-

CHART 18: COMPARISON OF PASSENGER LOAD FACTOR (PLF) AND BREAK-EVEN LOAD FACTOR (BELF), 2014-15

BELF PLF

38.5

13.5

11.0

7.6

6.2

0.35.1

9.23.4 5.0

CHART 19: COST STRUCTURE OF AVIATION INDUSTRY IN INDIA, 2014-15

Fuel

General and Administrative

Rentals of Flight Equipment

User charges

Ticketing sales andPromotionOther Expenses

Depreciation andamortizationMRO

Pax Services

Flight Crew salary & Expenses

14

The cost comparison was undertaken before and after adjusting Operating Cost to Average Stage Length.

Because of high fixed cost of airlines unit cost decrease as distance increases. Hence a stage length

adjustment is necessary for fairer comparison. In the year 2014-15, in terms of cost efficiency of airlines, Air

India Express had the least operating cost (adjusted for stage length) per ASK, followed by IndiGo and Go Air.

Passenger yield is a measure of average fare paid per passenger km flown, calculated by dividing Passenger

Revenue by Revenue Passenger Kilometers. In the year 2014-15, Air India Express had the lowest passenger

yield followed by Air Asia and SpiceJet.

10.5

6.15.5 5.3 5.1

4.74.2

3.7 3.5

2.4

7.8

4.8 4.5 4.3

5.66.1

3.7 3.4 3.4 3.4

0.0

500.0

1000.0

1500.0

2000.0

2500.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

---A

vera

ge S

tage

Le

ngt

h (

In K

ilom

ete

rs)-

---

----

Op

era

tin

g C

ost

Pe

r A

SK (

In R

up

ee

s)--

--

Chart-20: OPERATING COST PER ASK, 2014-15

UNADJUSTED OPERATING COST PER ASK ADJUSTED OPERATING COST PER ASK AVERAGE STAGE LENGTH

11.5

5.6 5.85.2 4.9 4.8 4.5 4.2

3.7 3.4

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

----

-Ru

pe

es

Pe

r R

PK

(In

Nu

mb

er)

----

-

CHART-21: COMPARISON OF PASSENGER YIELD OF SCHEDULED INDIAN CARRIERS, 2014-15

15

TABLE 11: FINANCIAL SUMMARY OF ALL SCHEDULED INDIAN CARRIERS- 2014-15

(RS. IN MILLION)

OPERATING REVENUE OPERATING EXPENSES OPERATING RESULT

SCHEDULED NATIONAL CARRIERS

AIR INDIA 2,06,131.60 2,26,854.40 -20,722.80

AI EXPRESS 22,948.20 19,597.60 3,350.60

ALLIANCE AIR 2,279.50 3,034.00 -754.50

SUB TOTAL (A) 2,31,359.30 2,49,486.00 -18,126.70

SCHEDULED DOMESTIC PRIVATE CARRIERS

JET AIRWAYS 1,95,606.05 2,15,030.10 -19,424.04

JET LITE (P) LTD. 14,229.36 16,775.22 -2,545.86

GO AIR 30,664.24 28,715.82 1,948.43

SPICE JET 52,015.25 60,884.99 -8,869.74

INDIGO 1,39,253.36 1,23,578.64 15,674.72

AIR COSTA 3,268.62 4,571.57 -1,302.96

AIR ASIA 1,551.87 2,885.01 -1,333.14

VISTARA 691.28 2,681.94 -1,990.66

SUB TOTAL (B) 4,37,280.03 4,55,123.29 -17,843.26

GRAND TOTAL (A+B) 6,68,639.33 7,04,609.29 -35,969.96

16

HUMAN RESOURCE

TABLE 12: PERSONNEL STATISTICS OF SCHEDULED INDIAN OPERATORS FOR THE YEAR 2014-15. NAME OF

THE AIRLINE Pilots & Co-

Pilots Other

Flight Crew Cabin Crew Maintenance

& Overhaul Personal Overhaul

Ticketing & Sales

Personnel

All Other Personnel

Total

AIR INDIA 1457 - 2321 5931 4221 7383 21313

AIR INDIA EXPRESS

236 - 729 133 145 1243

ALLIANCE AIR 59 37 402 40 167 705

JET AIRWAYS 1488 318 2974 2116 967 5615 13478

JETLITE 164 1 243 322 79 809

INDIGO 1320 140 2520 739 69 5748 10536

SPICEJET 403 60 718 569 116 2326 4192

GO AIR 216 71 418 339 397 739 2180

AIR COSTA 47 27 76 105 159 332 746

AIR ASIA 63 138 138 169 178 686

VISTARA 62 5 205 17 35 348 672

TOTAL 5515 797 10744 10480 5964 23060 56560

Out of the total airline staff of 56560, 37.7% is employed by Air India Ltd followed by Jet Airways (23.8%), IndiGo

(18.6%) and SpiceJet (7.4%).

Source: Directorate of Training & Licensing, DGCA. CPL- Commercial Pilot License; ATPL-Air Transport Pilot License.

720

108

828

474

64

538

395

66

461

384

47

431

0

100

200

300

400

500

600

700

800

900

MALE FEMALE TOTAL MALE FEMALE TOTAL

2014-15 2015-16

----

-Nu

mb

er o

f Li

cen

ses

issu

ed--

---

CHART-22: PILOT LICENCES ISSUED BY DGCA

CPL ATPL

17

ASK PER EMPLOYEE

Available Seat Kilometer (ASK) per Employee is an indicator of efficiency both in terms of capacity planning

and utilization of work force and is calculated by dividing Average Seat Kilometers by Number of Employees.

In terms of the ASK per employee, Jetlite is the most efficient followed by Go Air and SpiceJet.

REVENUE PER EMPLOYEE

Revenue per employee is an indicator of productivity of human resource of an airline and is calculated by dividing Operating Revenue by Number of Employees. Employee productivity was highest for JetLite followed by Jet Airways and Go Air.

3.73.6

3.53.4

3.1

2.4

1.0 1.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

----

-ASK

Pe

r Em

plo

yee

(In

Mill

ion

)---

--

CHART-23: ASK PER EMPLOYEE, (2014-15)

* National Airlines Includes Air India, Air India Express & Alliance Air.

17.6

14.5 14.113.2

12.4

10.2

4.4

2.8

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

----

-Re

ven

ue

Pe

r Em

plo

yee

(R

s. I

n M

illio

n)-

---

CHART 24: REVENUE PER EMPLOYEE- 2014-15

* National Airlines Includes Air India, Air India Express & Alliance Air.

18

TABLE 13: DGCA APPROVED AME TRAINING INSTITUTES (AS ON 08th APRIL, 2016)

REGION STATE NUMBER OF AME INSTITUTES

NORTH

Delhi 3

Haryana 2

Uttar Pradesh 4

Rajasthan 1

Himachal Pradesh 1

Uttarakhand 1

EAST

West Bengal 1

Assam 1

Bihar 1

Odisha 1

WEST

Maharashtra 9

Gujarat 1

Madhya Pradesh 2

Chhattisgarh 1

SOUTH

Tamil Nadu 6

Kerala 5

Karnataka 3

Telangana 3

TOTAL 46

Source: Directorate of Air Worthiness, DGCA.

19

TABLE 14: DGCA APPROVED FLYING TRAINING ORGANISATIONS (AS ON 10th AUGUST, 2016).

STATE OWNERSHIP NUMBER OF FLYING ORGANIZATION

TELANGANA

Private/Public Ltd. 3

State Govt. 1

GUJARAT Private/Public Ltd. 2

HARYANA State Govt. 1

KARNATAKA

State Govt. 1

Private 1

MADHYA PRADESH Private/ Trust/ Public Ltd. 4

MAHARASHTRA

Society 1

Private 3

BIHAR State Govt. 1

ODISHA State Govt. 1

PUNJAB State Govt. 1

RAJASTHAN Private 1

TAMIL NADU Private 1

UTTAR PRADESH

Private/Trust 5

Central Govt. 1

UTTRAKHAND Private 1

TOTAL 29

Source: Directorate of Flying Training, DGCA.

20

AIR SAFETY

TABLE 15: YEAR-WISE NUMBER OF ACCIDENTS.

TABLE 16: YEAR-WISE NUMBER OF SERIOUS INCIDENTS.

YEAR

TYPE OF OPERATOR

SCHEDULED OPERATORS

NON-SCHEDULED OPERATORS

FLYING TRAINING INSTITUTE

GOVT. OPERATORS

PRIVATE OPERATORS

FOREIGN OPERATORS

TOTAL ACCIDENTS

2011 0 6 2 2 0 1 11

2012 0 3 2 2 2 0 9

2013 0 5 2 1 0 0 8

2014 1 2 2 1 0 0 6

2015 4 5 1 0 0 0 10

2016* 2 1 0 1 0 0 4

*As in May 2016 Source: Directorate of Air Safety, DGCA.

Year

TYPE OF INCIDENT

ENGINEERING OPERATIONAL RUNWAY

EXCURSION WEATHER MISCELLANEOUS

TOTAL INCIDENTS

2011 1 1 1 1 1 5

2012 3 4 0 0 0 7

2013 2 3 1 0 0 6

2014 6 1 1 1 2 11

2015 1 3 0 0 1 5

2016* 0 2 0 0 0 2

*As in May 2016 Source: Directorate of Air Safety, DGCA.

21

OTHER AVIATION RELATED STATISTICS

Source: Ministry of Tourism.

An important aspect of international traffic to and from India pertains to trend in foreign tourist arrivals in India. In 2015, Foreign Tourist Arrivals accounted for 33.6% of inbound international traffic in India.

Source: Ministry of Petroleum & Natural Gas.

3.9 4.5 5.1 5.3 5.2 5.8 6.3 6.6 7.0 7.7 8.0

9.711.3

13.1 14.1 15.717.4

18.9 19.821.2

22.423.8

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

----

No

. o

f P

asse

nge

rs (

In M

illio

n)-

---

CHART-25: FOREIGN TOURIST ARRIVAL & INTERNATIONAL INBOUND PAX TRAFFIC

FOREIGN TOURISTS ARRIVAL INBOUND INTERNATIONAL PAX

3983

4543 44234627

50785536

52715505

5723

6220

0

1000

2000

3000

4000

5000

6000

7000

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16----

ATF

Co

nsu

mp

tio

n (

Tho

usa

nd

me

tric

to

nn

e)-

---

CHART 26: ATF CONSUMPTION OVER THE DECADE

22

The Air Turbine Fuel (ATF) consumption growth in India has been moving in tandem with the growth of air

traffic. In the year 2015-16, ATF consumption went up by 8.7% which is consistent with increase in aircraft and

air traffic movement.

Source: Ministry of Petroleum & Natural Gas.

TABLE 17: AIRPORTS IN INDIA (AS ON 31st March, 2016).

TOTAL INTERNATIONAL AIRPORTS 24

AAI Airports 18

Civil Enclave 3

Private Airports (JVs)

3

TOTAL CUSTOMS AIRPORTS 8

AAI Airports 4

Civil Enclave 4

TOTAL DOMESTIC AIRPORTS 101

AAI Operational Airports 47

AAI Operational Civil Enclave 18

AAI Non-Operational 31

STATE/ PRIVATE GOVERNMENT 5

TOTAL AIRPORTS (ALL TYPES) 133 Source: Airport Authority of India.

GLIDER TRAINING CENTRES IN INDIA*

1. Gliding Centre, Pune, Maharashtra: - It is attached with DGCA and its gliders belong to Government of India.

2. Deolali Gliding Club, Nasik, Maharashtra:- It is registered under Society Act, 1816 by Charitable Commissioner F68

and the gliders of this club belong to Government of India.

*Source: Directorate of Air Worthiness, DGCA

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

0

100

200

300

400

500

600

----

Yo

Y G

row

th in

ATF

Co

nsu

mp

tio

n (

%)-

---

----

ATF

Co

nsu

mp

tio

n (

00

0 m

etr

ic t

on

ne

)---

-

Chart 27: YoY GROWTH OF ATF CONSUMPTION, 2015-16

2014-15 2015-16 YoY GROWTH OF ATF CONSUMPTION

23

OFFICERS AND STAFF OF DIRECTORATE OF AIR TRANSPORT-II, DGCA ASSOCIATED WITH THE PUBLICATION

Notes:

1. Sources of data: Directorate of Air Transport- II, unless otherwise specified.

2. Data published in the handbook is provisional.

DEPUTY DIRECTOR GENERAL (SAG)

Sh. P C Cyriac

DIRECTOR

Smt. Ruchika Gupta

DEPUTY DIRECTOR

Sh. P K Srivastava

Sh. Narendra Singh

ASSISTANT DIRECTOR

Sh. Devendra Kumar

Sh. B P Majhi

STATISTICAL OFFICER

Sh. Mani Bhushan

Smt. Shweta Sharma

Sh. Ravi Kant Soni

Sh. Sandeep Verma