Embed Size (px)

DESCRIPTION

Hankore annual reportwater technology firmpeople republic of china

Citation preview

evolveHANKORE ENVIRONMENT TECH GROUP LIMITED

ANNUAL REPORT 2013

CORPORATE VISIONAs an integrated water solutions provider, HanKore shall continuously strive to be at the forefront of China’s water treatment industry and expands into other environment business sectors to include water recycling, sludge treatment and refuse treatment.

Driven by HanKore’s core values of teamwork, innovation, integrity, dedication, passion and responsibility, the Group will keep evolving like the butterfly, to realize its missions gradually. We believe that the Group has the capability to soar new heights in China’s water and environment sector and create higher value to its stakeholders.

2 MESSAGE TO SHAREHOLDERS

6 CORPORATE PROFILE

7 F INANCIAL HIGHLIGHTS

8 BUSINESS REVIEW

12 CORPORATE OUTLOOK

14 BOARD OF DIRECTORS

19 KEY MANAGEMENT

22 CORPORATE INFORMATION

23 CORPORATE GOVERNANCE REPORT

35 REPORT OF THE DIRECTORS

39 STATEMENT BY DIRECTORS

40 INDEPENDENT AUDITORS’ REPORT

41 F INANCIAL REPORTS

118 STATISTICS OF SHAREHOLDINGS

119 NOTICE OF ANNUAL GENERAL MEETING

CONTENTS

Message to Shareholders

HANKORE ANNUAL REPORT 2013 3

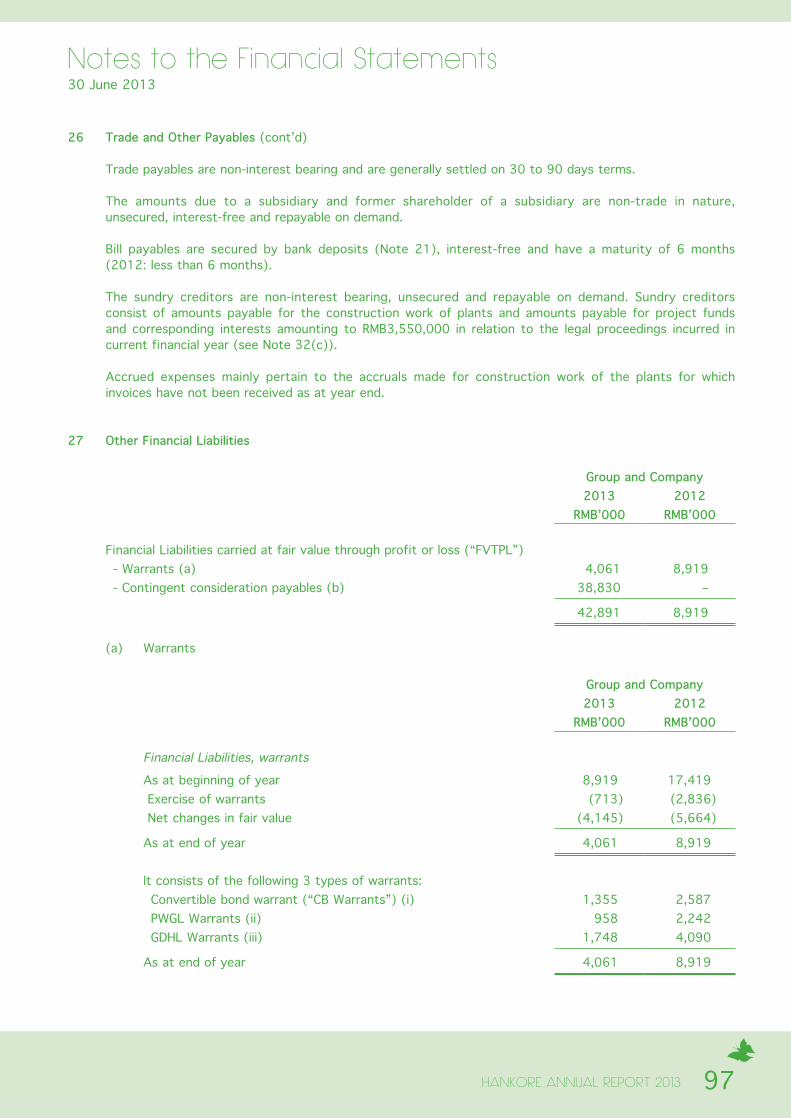

Dear Shareholders: Since our restructuring in 2011, the Group has undergone remarkable improvements in its developments in the water industry over the past two years. Against the headwinds of a slowdown in both the global and Chinese economy, the Group has concerted its efforts to launch the Phase 2 projects. On top of that, we have made improvements to our operational management. I would like to highlight that HanKore has over the past two consecutive years achieved awards in China’s water industry and gained several recognition from the local municipal government. The remarkable changes clearly demonstrate that HanKore has successfully transformed itself towards higher growth and positive development in the water and environment sector.

Key Water Projects Progressing Well

Over the past year, we have launched several projects in Henan, Shaanxi and Jiangsu provinces of China, namely, Henan Sanmenxia Project, Shaanxi Xianyang Phase 2 Expansion, the Second Stage of Phase 1 Expansion and Upgrading of the Group’s Nanjing Liuhe Project, Nanjing Pukou Phase 1 Upgrading, Phase 2 Expansion and Sludge Treatment Project and Yangzhou HanKore Phase 1 Upgrading and Phase 2 Expansion Project.

A New Era of Transformation After Restructuring

Over the past two consecutive years, several of our water plants have achieved various awards and recognitions from the Chinese government and water industry authorities. In February 2013, we have received our most recent award, the “2012 China’s Top Ten Fastest Growing Water Companies” by ChinaWaterNet, one of China’s influential and credible online media in the water industry.

We have returned to the black in FY2012 and FY2013 to achieve a net profit of RMB102.6 million and RMB99.5 million respectively from a reported loss in FY2011. These signify that the Group has successfully entered into a new era of transformation after the completion of our restructuring.

We shall further improve and upgrade our existing operation standards and seek for new areas to develop as an urban environmental solutions provider to achieve better operating margins.

We hope that you will continue to place your trust in our abil ity to drive the Group’s developments to emerge stronger in the international environment and water sector.

Message to Shareholders

HANKORE ANNUAL REPORT 20134

Financial Review

The Group achieved a 50.4% surge in revenue to RMB369.1 million and gained a net profit of RMB99.5 million for FY2013. The higher revenue for FY2013 was achieved on the back of a 130.0% yoy increase in construction revenue to RMB167.5 million and a 16.2% yoy increase in recurring water treatment income to RMB200.5 million which consists of water discharge fees and finance income from service concession arrangements.

We saw higher gross profit margin for both our construction activities and recurring water treatment operation activities which rose from 9.0% for FY2012 to 14.3% for FY2013 and 65.0% for FY2012 to 70.1% for FY2013 respectively.

Set To Benefit from Rising Water Tariffs And More Stringent Discharge Standards

During FY2013, six of the Group’s water plants received the green light to raise our water discharge fees.

According to the 12th Five-Year Plan, China’s wastewater treatment industry will gradually shift its emphasis from the rapid development of wastewater treatment plants to the upgrading and enhancement of the in-depth operations of these plants. Along with the improvement of the facilities of wastewater treatment plants, higher capabilities of sludge treatment and more stringent water discharge standards set by the Chinese government, we foresee higher water tariffs as an inevitable trend that will significantly benefit the Group.

To Become An Integrated Environmental Solutions Provider

As China’s environment industry structure continues to undergo restructuring, the Group is confident that it is well-equipped with solid investment and financing capabilities, advanced technologies, favorable corporate branding and comprehensive wastewater solution services to attain new heights in China’s water sector. As a one-stop wastewater treatment service solution provider, the Group incorporates its planning, designing, construction, operation and supervision in a package to offer higher value to its customers.

HANKORE ANNUAL REPORT 2013 5

In our bid to be an integrated environmental solution provider, we focus on the aspects of investment, facility integration, engineering construction and operation of the environment and water sector.

Looking forward, the Group will proactively seek new acquisition of water projects to increase our domestic market share in China, enhance our corporate governance and transparency and break into new areas of environment business segments to expand our potential earnings.

Appreciation & Acknowledgements

On a final note, I would like to take this opportunity to express my heartfelt appreciation to our board of directors, management, staff and all of our key stakeholders for their long-term support to HanKore.

We hope that you will continue to place your trust in our ability to drive the Group’s developments to emerge stronger in the international environment and water industry.

Executive ChairmanChen Dawei, David

HANKORE ANNUAL REPORT 20136

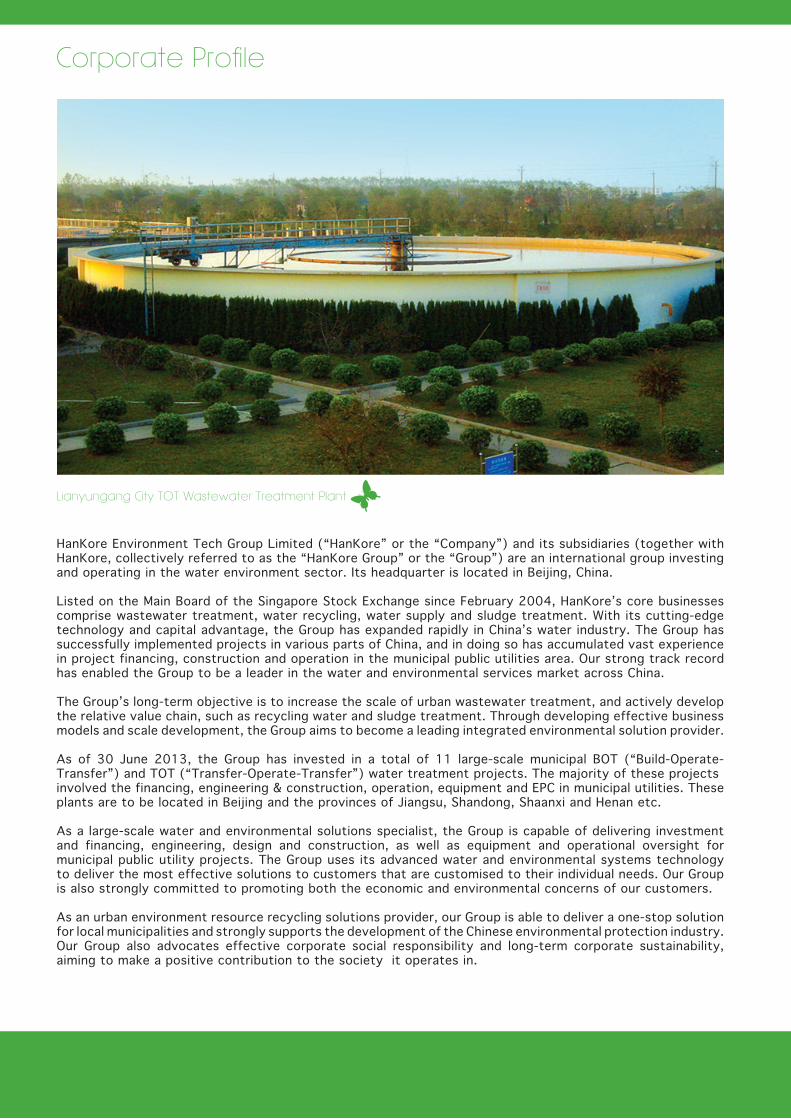

Corporate Profile

HanKore Environment Tech Group Limited (“HanKore” or the “Company”) and its subsidiaries (together with HanKore, collectively referred to as the “HanKore Group” or the “Group”) are an international group investing and operating in the water environment sector. Its headquarter is located in Beijing, China.

Listed on the Main Board of the Singapore Stock Exchange since February 2004, HanKore’s core businesses comprise wastewater treatment, water recycling, water supply and sludge treatment. With its cutting-edge technology and capital advantage, the Group has expanded rapidly in China’s water industry. The Group has successfully implemented projects in various parts of China, and in doing so has accumulated vast experience in project financing, construction and operation in the municipal public utilities area. Our strong track record has enabled the Group to be a leader in the water and environmental services market across China.

The Group’s long-term objective is to increase the scale of urban wastewater treatment, and actively develop the relative value chain, such as recycling water and sludge treatment. Through developing effective business models and scale development, the Group aims to become a leading integrated environmental solution provider.

As of 30 June 2013, the Group has invested in a total of 11 large-scale municipal BOT (“Build-Operate-Transfer”) and TOT (“Transfer-Operate-Transfer”) water treatment projects. The majority of these projectsinvolved the financing, engineering & construction, operation, equipment and EPC in municipal utilities. These plants are to be located in Beijing and the provinces of Jiangsu, Shandong, Shaanxi and Henan etc.

As a large-scale water and environmental solutions specialist, the Group is capable of delivering investment and financing, engineering, design and construction, as well as equipment and operational oversight for municipal public utility projects. The Group uses its advanced water and environmental systems technology to deliver the most effective solutions to customers that are customised to their individual needs. Our Group is also strongly committed to promoting both the economic and environmental concerns of our customers.

As an urban environment resource recycling solutions provider, our Group is able to deliver a one-stop solution for local municipalities and strongly supports the development of the Chinese environmental protection industry. Our Group also advocates effective corporate social responsibility and long-term corporate sustainability, aiming to make a positive contribution to the society it operates in.

Lianyungang City TOT Wastewater Treatment Plant

7HANKORE ANNUAL REPORT 2013

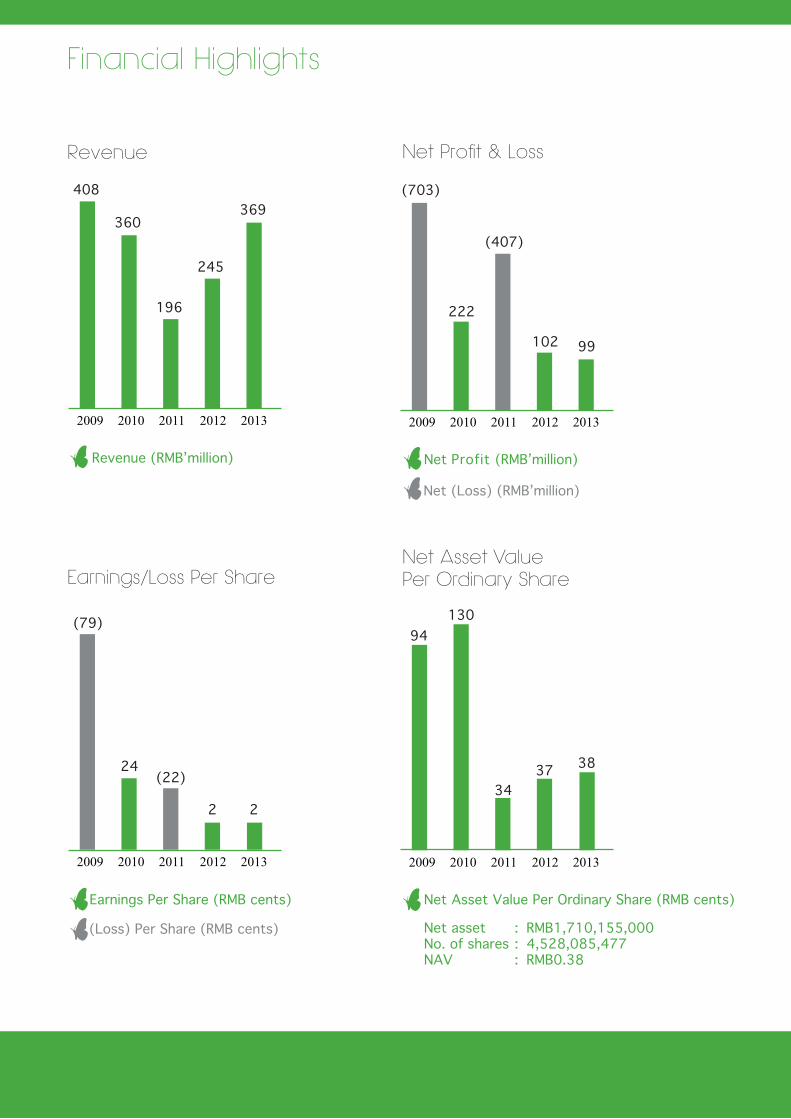

Financial Highlights

Revenue

2009 2010 2011 2012 2013

Revenue (RMB’million)

Earnings/Loss Per Share

Earnings Per Share (RMB cents)

(Loss) Per Share (RMB cents)

2009 2010 2011 2012 2013

Net Asset Value Per Ordinary Share

2009 2010 2011 2012 2013

Net Asset Value Per Ordinary Share (RMB cents)

Net asset : RMB1,710,155,000No. of shares : 4,528,085,477NAV : RMB0.38

Net Profit & Loss

2009 2010 2011 2012 2013

Net Profit (RMB’million)

Net (Loss) (RMB’million)

408

(79)

22

(22)24

(703)

94130

3437 38

222

(407)

102 99

360

196

245

369

Business Review

9HANKORE ANNUAL REPORT 2013

Business Review

FY2013 is an eventful year for HanKore where the Group has swiftly stepped up its efforts in project upgrading and expansion and attained great achievements in the water industry.

Successful Acquisition of Engineering, Procurement and Construction (EPC)Company - Jiangsu Tongyong Environment Engineering Co., Ltd.

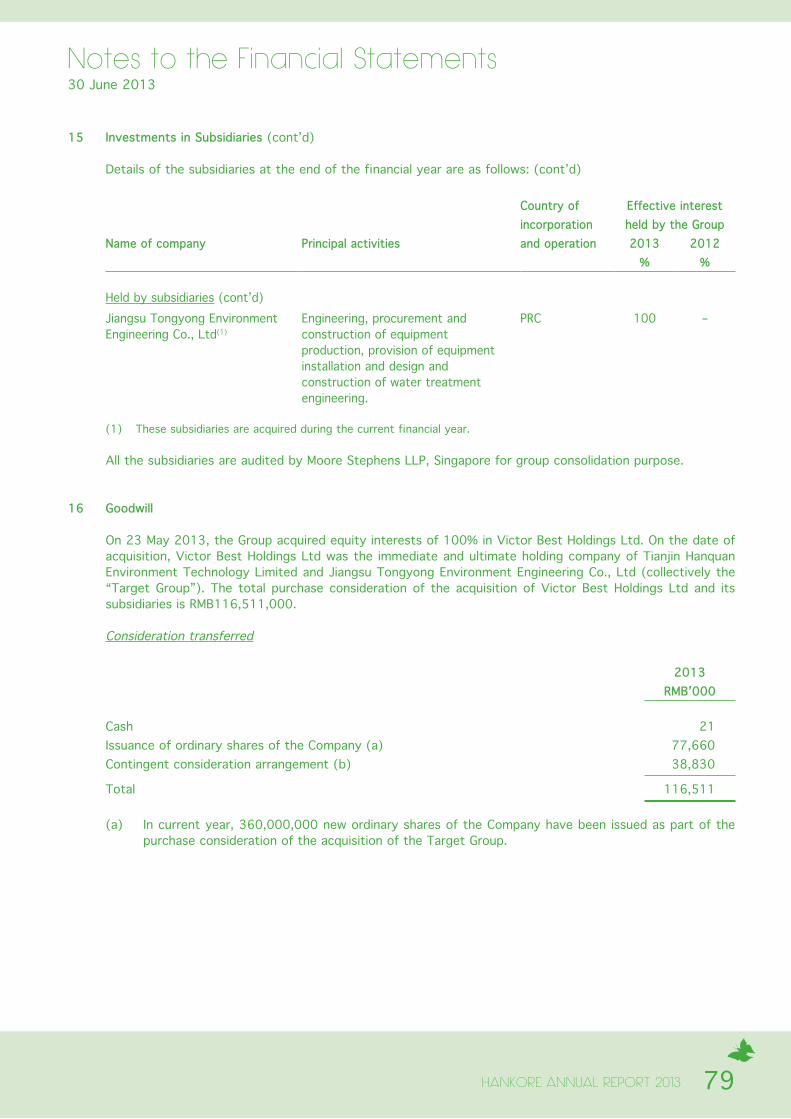

The Group has signed an acquisition agreement with the Jiangsu Tongyong Environment Group Co., Ltd.(“JTEG”) to acquire 100% stake in JTEG’s wholly-owned subsidiary, Jiangsu Tongyong Environment Engineering Co., Ltd. (“JTEE”) in November 2012. In April this year, the Group has convened an Extraordinary General Meeting (“EGM”) on this acquisition agreement and on 14 June announced the completion of the acquisition.

JTEE is primarily engaged in the equipment manufacturing, sales, designing and construction of environmental engineering in the environmental protection sector. As JTEE has established long-term relationships with some of China’s well-known water investment companies and main contractors of water projects, the Jiangsu Tongyong brand is widely recognized in China’s water industry. The Jiangsu Tongyong brand has vast geographical presence especially in Shanghai, Hainan, Guangxi, Inner Mongolia, Zhejiang, Shandong, Jiangsu and Hunan Province. Via this acquisition, the Group will also strengthen its reputation and standing in China’s water industry and diversify its business scope to include environmental protection EPC as JTEE holds the qualifications, licenses and intellectual properties to operate in the EPC sector. The acquisition allows the Group to enhance its product value chain, increase its profitability and reinforce its market competitiveness in this sector.

HANKORE ANNUAL REPORT 201310

In August 2012, the Group’s Kunshan Port East Plant located in Jiangsu Province, recorded significant achievements in business operation and management. This plant had received the government’s approval to increase its water discharge fees by 20.0% from RMB1.00 per ton to RMB1.2016 per ton. The local authorities had agreed to start the fee increase from the day it passed its operational checks in August 2011 to pay HanKore an additional RMB3.296 million.

In November 2012, the Group’s Xianyang Eastern Suburbs Wastewater Treatment Plant located in Xianyang City, Shaanxi Province, signed a Build-Operate-Transfer(“BOT”) supplemental contract with the local government and would see a 44.3% hike in its water discharge fees from RMB0.70 per ton to RMB1.01 per ton on completion of its Phase 2 Expansion. Spanning an area of 102 mu (16.8 acres), with total wastewater treatment capacity 200,000 tons/day, the Group’s Xianyang plant is the largest wastewater treatment plant in the Weihe River Basin and a backbone project of the government’s pollution prevention efforts of the area. This project also plays an instrumental role in the infrastructure and environmental protection development of the Xianyang City in its bid to be a model city in China. Officially launched in 2006, the Phase 1 of Xianyang plant has a wastewater treatment capacity of 100,000 tons per day with “Grade 1B” discharge standard. With the completion of the Phase 2, total wastewater treatment capacity would be raised to 200,000 tons per day with “Grade 1A” water discharge standard and a total investment value of RMB170 million.

In March 2013, Yangzhou HanKore Water Development Co., Ltd. has commenced its Phase 2 Expansion and Phase 1 Upgrading and water discharge fees is expected to increase by 16.9% from RMB1.42 per ton to RMB1.66 per ton. The construction of Phase 2 is expected to cost approximately RMB45 million with a treatment capacity of 12,500 tons per day and upon completion, the water discharge standard will be “Grade 1A”.

Similarly in March 2013, construction work for the second stage of the Phase 1 and upgrading works of the Group’s Nanjing Liuhe wastewater plant commenced. Subsequently in April 2013, the Group has signed with the local authorities a supplementary agreement on the upgrading of the Phase 1 of the plant. Upon completion, the estimated overall water

treatment capacity of the Phase 1 of the Group’s Nanjing Liuhe BOT project would be 40,000 tons per day, with an estimated investment value of RMB45 million. Under the supplementary agreement, the water discharge tariff will increase 57.6% from RMB0.92 per ton to RMB1.45 per ton as water discharge quality upgrades from “Grade 1B” to “Grade 1A”. The building pipelines and other related facilities including water pumping, pretreatment facilities, fan room and mechanical workshop to support the 40,000 tons per day water treatment capacity had been installed under the first stage of Phase 1 of this plant.

In April 2013, the Group’s subsidiary, Beijing Hankelin Environmental Technology Co., Ltd. has entered into a Reuse Water Frame Agreement with Xianyang City Environmental Protection Bureau (“Xianyang EPB”). Xianyang EPB appoints Beijing Hankelin to manage and operate a water reuse plant (“Qingwei Plant”) with a capacity of 30,000 tons per day. The current water reuse tariff is RMB0.56 per ton. Xianyang EPB will assist Beijing Hankelin to increase the water reuse capacity to 200,000 tons per day.

In August 2013, the Group’s subsidiary, Nanjing Golden Idea Water Development Co., Ltd. has entered into a BOT Supplementary Agreement with the Administration of Housing and Urban-Rural Development of Pukou District, Nanjing City, Jiangsu Province to start Phase 1 Upgrading and Phase 2 Expansion for Nanjing Pukou wastewater treatment plant. The total investment value of this project is RMB140 million. Phase 2 of this plant shall increase the treatment capacity by another 40,000 tons per day from the initial 40,000 tons per day of Phase 1, with “Grade 1A” water discharge standard. In view of more stringent water and sludge discharge standards, the water fees is expected to be adjusted upwards by RMB0.59, an increase of 66.3% from RMB0.89 per ton to RMB1.475 per ton.

HanKore has realized its strategic plan in FY2013 to integrate an EPC company in order to reinforce its EPC capabilities. For the coming year, the Group shall actively strengthen its wastewater treatment business segment and cultivate new businesses in the environmental protection industry.

Operational Review of the Group’s Portfolio of Water Plants

HANKORE ANNUAL REPORT 2013 11

Awards

HanKore Environment Tech Group Limited – Binzhou Project Company

October 2012: Awarded the title of “Model Company in Performance Assessment of Wastewater Treatment in 2011 in Shandong Province” by the Shandong Provincial Department of Housing and Urban-Rural Development and Shandong Provincial Department of Supervision.

February 2013: Awarded the “2012 Advanced Company In Energy Saving and Emission Reduction” by the Binzhou Economic Development Zone Committee and Binzhou Economic Development Zone Administration Committee.

HanKore Environment Tech Group Limited – Lianyungang Project Company (Dapu and Xugou wastewater treatment plants)

July 2012: Awarded RMB5,000 under the “Automatic Monitoring Data Acquisition and Transmission Subsidy” by the Lianyungang City Environment Supervision Bureau.

July 2012: Awarded RMB40,000 under the “Installation of Ammonia Nitrogen Auto-monitoring Equipment Subsidy” by the Lianyungang City Environment Supervision Bureau.

October 2012: Awarded RMB190,000 under the “Automatic Monitoring Facilities Socialization Operating Subsidy” by the Lianyungang City Environment Supervision Bureau.

HanKore Environment Tech Group Limited – Xianyang Project Company

June 2012: Awarded RMB3.1 million under the “Removal of Nitrogen and Phosphorus Transformation Bonus” from the local government of Xianyang City.

HanKore Environment Tech Group Limited – Suzhou Project Company

August 2012: Honored and recognized as “Suzhou City Water Saving Education Base” by the local water authority in China.

HanKore Environment Tech Group Limited – Kunshan Project Company

August 2012: Awarded RMB1.32 million under the “Upgrading and Reconstruction Subsidy” from the Jiangsu Housing Development Department.

November 2012: Awarded RMB100,000 under the “2012 Energy Saving and Emission Reduction Subsidy” from the Kunshan Environmental Protection Bureau.

April 2013: Honored the “Green” category (highest level of recognition) under the “2012 Company Environmental Protection Rank” by the Kunshan Environmental Protection Bureau.

HanKore Environment Tech Group Limited – Beijing Project Company

December 2012: Awarded RMB700,000 under the “Special Funds for Environmental Protection” from the Beijing Daxing District Environmental Protection Bureau.

Over the past fiscal year, the Group’s project companies had won a string of awards namely:

In February 2013, the Group was awarded the “2012 China’s Top Ten Fastest Growing Water Companies” which came on the heels of its “2011 China’s New Water Enterprise” award last year. Both awards were given by ChinaWaterNet, one of China’s most influential and credible online media in the water industry. The selection of the “2012 Top Ten Fastest Growing Water Companies” award was based on these criteria, namely fast growing financial results in 2012, achievement of more than 30.0% growth in operating revenue, strong development potential of the company and overall evaluation by water industry experts. The Annual ChinaWaterNet Awards has become a reliable platform with wide influence in China’s water industry.

Corporate Outlook

13HANKORE ANNUAL REPORT 2013

Corporate Outlook

Looking back at 2013, the global economy is still undergoing a period of adjustment over its crisis. In the short run, the international business environment continues to be filled with complexities and uncertainties.

The Chinese economy faced challenges and is trying to find a proper balance amongst staying competitive, sustaining growth, weaker consumer confidence and instability in market expectations. At the same time, developing countries have started to focus on developing the internet and driving new energy markets to hasten the world’s pace towards a third industrial revolution.

Under China’s 12th Five-Year Plan, the planned investment for the national urban wastewater treatment and recycling of RMB430 billion clearly shows China’s higher emphasis placed on this industry. Capital shortage is still a key factor to the development of urban wastewater treatment services in China. With the financial tightening from the local authorities, facility construction of the wastewater industry requires more capital from the market. After the implementation of the 12th Five-Year Plan, we have foreseen that the government will continue to increase its efforts to clean up China’s environment and further develop the environmental protection industry as one of its key emerging strategic industries. During the next three to five years, funding of the water industry will mainly come from the central government and market and rather, less from the provincial authorities. We believe that the future water industry will be propelled by higher investments from the market.

Along with development in the water industry under the 12th Five-Year Plan, HanKore, a new star in China’s water industry, has adjusted its implementation of strategy accordingly. The Group continues to optimize its industry chain, actively incorporate provincial expansion plans, increase its water treatment capacity through upgrading and improving its project management ability. At the same time, the Group shall endeavor to be an integrated service provider to diversify its risks. In light of an ever-changing global economy, the Group will gradually broaden its focus to expand its array of solutions and services across the environment and water sector to bring in higher recurring income for the Group. Leveraging on its own assets as well as external resources, the Group will strive to equip itself with cutting edge technologies and advanced internal operating systems in order to stay relevant and competitive in the environment and water sector.

To obtain long term and stable capital support, the Group has in July 2013 established its S$300 million multicurrency Medium Term Note (“MTN”) program, and on 1 August 2013 successfully carried out its inaugural MTN issuance of a total value of $50 million. This marks a significant milestone deal for the Group and the SGD bond market as it is the first high yield transaction from a PRC company tapping the SGD market in 2013. Not only does the MTN program open a new funding channel for the Group, but also elevate HanKore’s popularity in the bond market in Singapore. The income from the bond issue will be used to expand its portfolio of investments and operations. Besides this, the Group has gained recognition from several potential investors and received substantial investment from Mr Wang Yu Huei of Asdew Acquisitions Pte. Ltd. Mr Wang Yu Huei has subscribed 293,617,000 new ordinary shares with the Group in August 2013 and this shows his strong vote of confidence in the Group’s potential development in the water and environment sector.

2014 will be a year of opportunities and challenges for HanKore, and we strongly believe that with the continued trust and faith from our stakeholders, we will be able to soar higher in our achievements in the water industry.

Board of Directors

HANKORE ANNUAL REPORT 2013 15

Board of Directors

Chen Dawei, DavidExecutive Chairman

Mr Chen joined the Group as Executive Chairman and CEO from 21 May 2011 to 20 December 2011. He relinquished his position as the Chief Executive Officer (“CEO”) and was re-designated as Executive Chairman on 21 December 2011. He is also a member of our Nominating Committee. He is responsible for the Group’s strategic planning and oversees the management and business development for the Group.

Mr Chen is the sole shareholder and Director of Giant Delight Holdings Limited (“GDHL”), which holds 16.47% of the shareholding in the capital of the Company.

Prior to joining the Group in September 2010, Mr Chen was the CEO of China Media Development Group and was responsible for its operations in China, and sat on the Board of Beijing Jun Tai Investment Management Co., Ltd. He is also the Founder and CEO of Beijing Revolution Science and Technology Co., Ltd. Mr Chen has over 17 years of experience in business operations, mergers & acquisitions in China, of which 10 years were spent in the wastewater treatment industry.

Mr Chen holds an MBA from Southwestern University and an EMBA degree (majoring in China-America Finance) from Peking University, China. Mr Chen is currently an Executive Master of Business Administration Candidate at the National University of Singapore.

Nie Jian ShengExecutive Director and Chief Executive Officer

Mr Nie was appointed as our Executive Director and Chief Executive Officer on 21 December 2011. He is responsible for the daily operational activities and operational development of the Group. He is also responsible for establishing and consolidating corporate culture and team building for the Group.

Mr Nie has more than 21 years of experience in government administration, capital operation, business operations and investment. Prior to joining our Group, Mr Nie worked at the Tianjin Commission of Commerce office. His other past positions were the Deputy General Manager of the Tsinlien Group Co., Ltd., Department Chief and the Deputy Head of the Foreign Affairs Office of the Tianjin Municipal People’s Government liaison office in Hong Kong, and Executive Director and Deputy General Manager at Tianjin Development Holdings Limited, a company listed on the Main Board of the Stock Exchange of Hong Kong Limited (“HKSE”) .

Mr Nie also served as Vice-Chairman of several companies under Tianjin Port Development Holdings Limited, including Tiangong Wine Co., Ltd. in Tianjin, Tianjin Port Container Terminal Co., Ltd. and Tianjin Harbour Second Port Company Limited. Between August 2004 and January 2008, Mr Nie was the Executive Director and Senior Vice-President of Dynasty Fine Wines Group Limited, a company listed on the Main Board of the HKSE, as well as Vice-Chairman and Executive Director of Tianjin Port Development Holdings Limited, a company listed on the Main Board of the HKSE.

Mr Nie graduated from Tianjin University in 1980 majoring in economics and philosophy, and completed postgraduate courses at the Tianjin Institute of Finance, International Trade in 1998.

HANKORE ANNUAL REPORT 201316

Board of Directors

Yau Wing-YiuExecutive Director and Chief Financial Officer

Mr Yau joined the Group as Independent Director on 1 November 2011. He relinquished his position of Independent Director and was re-designated as our Executive Director and Chief Financial Officer on 6 February 2013.

Mr Yau has more than 20 years of working experience. He is currently an Independent Director of Carry Wealth Holdings Limited, a company listed on the HKSE. Prior to joining the Group, he was Executive Director of China Strategic Holdings Limited, a company listed on the Main Board of the HKSE, the Finance Director of Microsoft China Company Limited and Senior Vice-President, Mergers and Acquisition of PCCW. He has extensive experiences in financial management, corporate finance and investment. Prior to PCCW, he also worked for BNP Paribas Peregrine, Socie´ te´ Ge´ne´ rale and Arthur Andersen.

Mr Yau holds an MBA from the Hong Kong University of Science and Technology and a Bachelor of Arts from the City University of Hong Kong. He is also a member of the American Institute of Certified Public Accountants and the Hong Kong Institute of Certified Public Accountants.

Lin Zhe YingExecutive Director

Mr Lin joined our Group as Executive Director on 21 May 2011.

He is currently the Chairman of Jade Capital Management Limited. Mr Lin is also a specialist to the State Development Bank, a member of the SME Committee of the Shenzhen Stock Exchange and the China - Italy Mandarin Fund Advisory Committee.

Previously, Mr Lin was the Deputy Director of Department of Foreign Trade of Ministry of Commerce of the PRC. Mr Lin also had a leading role in the founding of the RMB fund-New Development Fund, which is invested by the China Development Bank and major State-Level development zones.

Mr Lin holds a Doctor degree of Business Administration from ESC Rennes School of Business and an MBA from the Peking University School of Guanghua Management.

HANKORE ANNUAL REPORT 2013 17

Chen Da Zhi Non-Executive Director

Mr Chen was appointed as Non-Executive Director on 21 May 2011. He is also a member of Remuneration Committee.

Mr Chen is currently the Board President of Protown Technology Development Ltd. Prior to this, Mr Chen was the CEO of China InfoWorld. His other past positions are CEO of Beijing CCID Capital, Non-Executive Director of CCID Consulting Co. Ltd. (a company listed on the HKSE), and Director of Red Flag’s Software Co., Ltd.

Mr Chen holds a Master of Arts in Journalism from the Renmin University of China and a Bachelor of Computer Science (Software Engineering) from the Nanjing University of Science.

Lim Yu Neng, PaulLead Independent Director

Mr Lim joined the Group on 31 July 2007 and was re-designated as Lead Independent Director on 6 February 2013. Mr Lim is also the Chairman of Audit Committee and a member of Nominating Committee.

Mr Lim has over 25 years of banking experience. He is the Managing Director of Leafgreen Capital Partners Pte Ltd. and the Non-Executive Chairman of PT BNI Securities Indonesia. Prior to his appointment as Interim Acting CEO for our Group in June 2010, Mr Lim held various positions in Morgan Stanley, Deutsche Bank, Salomon Smith Barney, Schroder International Merchant Bankers Limited and Bankers Trust.

Presently, Mr Lim is an Independent Director of United Fiber System Ltd. and Nippecraft Limited. Both companies are listed on the Singapore Exchange Limited.

Mr Lim obtained his MBA in Finance and Bachelor of Science in Computer Science from the University of Wisconsin, Madison, USA. He is also a Chartered Financial Analyst (CFA).

HANKORE ANNUAL REPORT 201318

Board of Directors

Lee Kheng JooIndependent Director

Mr Lee was appointed as our Independent Director on 21 May 2011. He is the Chairman of Nominating Committee and a member of Remuneration Committee and Audit Committee.

Mr Lee is currently the CEO of Longmen Group, a leading unconventional gas development company in China. He is also the Vice-President of Xi’an Chamber of Commerce and the Vice Chairman of the Shaanxi Province International Chamber of Commerce. Mr Lee used to work as a commercial manager at Philips Lighting in Asia Pacific Management Center based in Taiwan. He became the product manager of Singapore Telecommunications Limited and was subsequently based in China as Sales and Marketing Director of Hutchinson Telecoms. Mr Lee was the Chief Operating Officer of Pacific Internet’s Hong Kong operations before joining Asia Online as the Group General Manager.

Mr Lee graduated with a Bachelor degree of Business Administration from the National University of Singapore.

Cheng Fong Yee, FondaIndependent Director

Ms Cheng was appointed as our Independent Director on 31 July 2007. She is the Chairman of Remuneration Committee and a member of Audit Committee.

Ms Cheng currently heads the Insurance Division of the Bok Seng Group, AsiaOne Insurance Agency Pte Ltd. in Singapore and is also the principal representative in the Cambodia Branch of AsiaOne Insurance Agency in Singapore. Her role involves risk management and the development of insurance business in emerging markets for the Company. She has more than 20 years of experience in the insurance industry. Ms Cheng is an Associate of the Australian Insurance Institute. She has been involved in major overseas insurance projects, particularly in the Asia Pacific, and is actively involved in utilizing insurance as a financial tool for project development in this region.

Ms Cheng completed her insurance study at Australian Insurance Institute.

Key Management

HANKORE ANNUAL REPORT 201320

Ge Lun CanVice- President in Finance

Ms Ge was appointed Vice-President in Finance on 26 March 2012.

Ms Ge has more than 30 years of experience in financial operations and listed companies, and is familiar with the laws and regulations relevant to these areas. Prior to joining our Group, Ms Ge was the General Manager of the Investment Development Department both at Tsinlien Group Company Limited and Tianjin Development Holdings Limited, as well as the Deputy General Manager at Tianjin Development Holdings Limited, a company listed on the Main board of the HKSE in 1997, and Chief Representative of Tianjin Representative Office for Tianjin Development Holdings Limited. Ms Ge’s other past positions include the Vice- President of Finance Department for Hong Kong Tsinlien Group Company Ltd.(an outfit of Tianjin Municipal Government based in Hong Kong) delegated by the former Tianjin Foreign Economic and Trade Commission and Chief Representative of Tianjin Representative Office and Department Director.

Ms Ge majored in English and graduated from the University of Tianjin Xinhua University in 1980.

Cui JunVice- President

Mr Cui was appointed Vice-President in Engineering Technology on 8 December 2010. With over 21 years of environmental engineering experience, Mr Cui brings to the Group strong technical expertise. His career achievements include being in-charge of the project design and engineering of the North District Wastewater Treatment Plant in Shanghai, a project which won the Third-Grade Award of Shanghai Science and Research. He also designed many other waste and wastewater treatment projects including commercial, residential, industrial, and municipal projects such as the mobile toilets for Ministry of Railways of the PRC.

Mr Cui also serves as an Assistant Professor in Tongji University, Shanghai, specializing in waste and wastewater treatment. As many of his students are from the environmental protection industry, Mr Cui brings to the Group an extensive network of client contracts from both the private and public sectors.

Prior to working for the Group, Mr Cui worked as a Senior Engineer in the Shanghai Railway City Transportation Design Department for 20 years.

Key Management

HANKORE ANNUAL REPORT 2013 21

Li Shi HuaVice -President

Mr Li was appointed Vice-President in investment and financing and operations on 18 January 2013.

Mr Li has more than 13 years of experience in corporate finance in water industry. Mr Li is very familiar with domestic and worldwide financing policies. He has accessed to many corporate financing channels and fully understood the new corporate accounting standard, be good at formulating a plan of corporate budget system and financial analysis. Prior to joining the Group, Mr Li was the manager of corporate finance of Beijing Sound Global Group Limited, Financial Controller of Beijing Haisidun Environmental Protection Engineering Co., Ltd. and Vice-President and Director of Finance of Beijing Xiao Qing Environmental Protection Group.

Mr Li holds a Master Degree in World Economics from the Renmin University of China. He is a Certified Public Accountant (CPA).

Wang Wei DongVice -President

Mr Wang was appointed Vice-President on 8 Dec 2010.

Mr Wang has more than 17 years of experience in operations and marketing in the environmental protection industry. Mr Wang was previously the Chief Designer of the Beijing Metallurgical Department’s Fusion Explosion Division, and was the Deputy Plant Manager at Beijing Metallurgical Equipment Manufacturing plant. Mr Wang had also previously held the positions of Deputy General Manager at Hong Kong Jin Tai International Technology & Trade Limited, and General Manager at Shanghai Chang Qiang Electrical and Mechanical Equipment Co., Ltd.

Mr Wang holds a Machine Building diploma at Shenyang University and majoring Economic Management at China Central Party School (“CCPS”).

HANKORE ANNUAL REPORT 201322

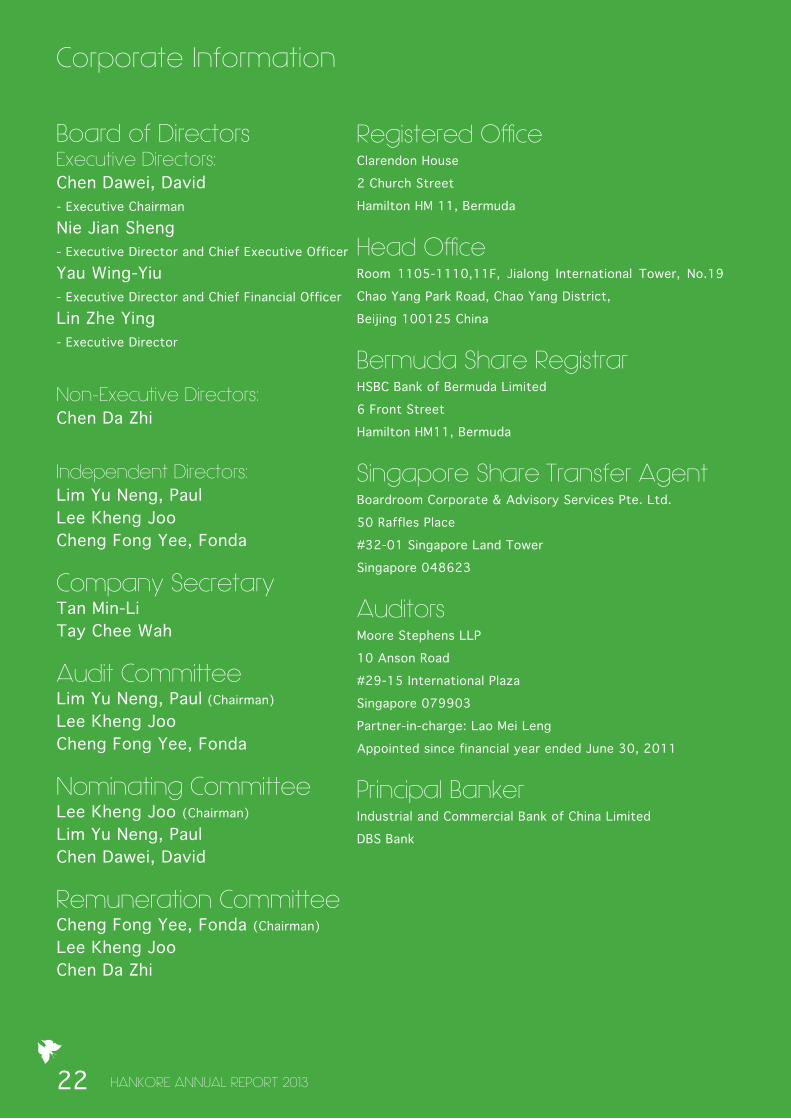

Corporate Information

Board of DirectorsExecutive Directors:Chen Dawei, David- Executive ChairmanNie Jian Sheng - Executive Director and Chief Executive OfficerYau Wing-Yiu - Executive Director and Chief Financial OfficerLin Zhe Ying - Executive Director

Non-Executive Directors:Chen Da Zhi

Independent Directors:Lim Yu Neng, PaulLee Kheng JooCheng Fong Yee, Fonda

Company SecretaryTan Min-LiTay Chee Wah

Audit CommitteeLim Yu Neng, Paul (Chairman)Lee Kheng JooCheng Fong Yee, Fonda

Nominating CommitteeLee Kheng Joo (Chairman)Lim Yu Neng, PaulChen Dawei, David

Remuneration CommitteeCheng Fong Yee, Fonda (Chairman)Lee Kheng JooChen Da Zhi

Registered OfficeClarendon House2 Church StreetHamilton HM 11, Bermuda

Head OfficeRoom 1105-1110,11F, Jialong International Tower, No.19 Chao Yang Park Road, Chao Yang District, Beijing 100125 China

Bermuda Share RegistrarHSBC Bank of Bermuda Limited6 Front StreetHamilton HM11, Bermuda

Singapore Share Transfer AgentBoardroom Corporate & Advisory Services Pte. Ltd.50 Raffles Place #32-01 Singapore Land Tower Singapore 048623

AuditorsMoore Stephens LLP10 Anson Road#29-15 International PlazaSingapore 079903Partner-in-charge: Lao Mei LengAppointed since financial year ended June 30, 2011

Principal BankerIndustrial and Commercial Bank of China LimitedDBS Bank

Corporate Governance Report

23HANKORE ANNUAL REPORT 2013

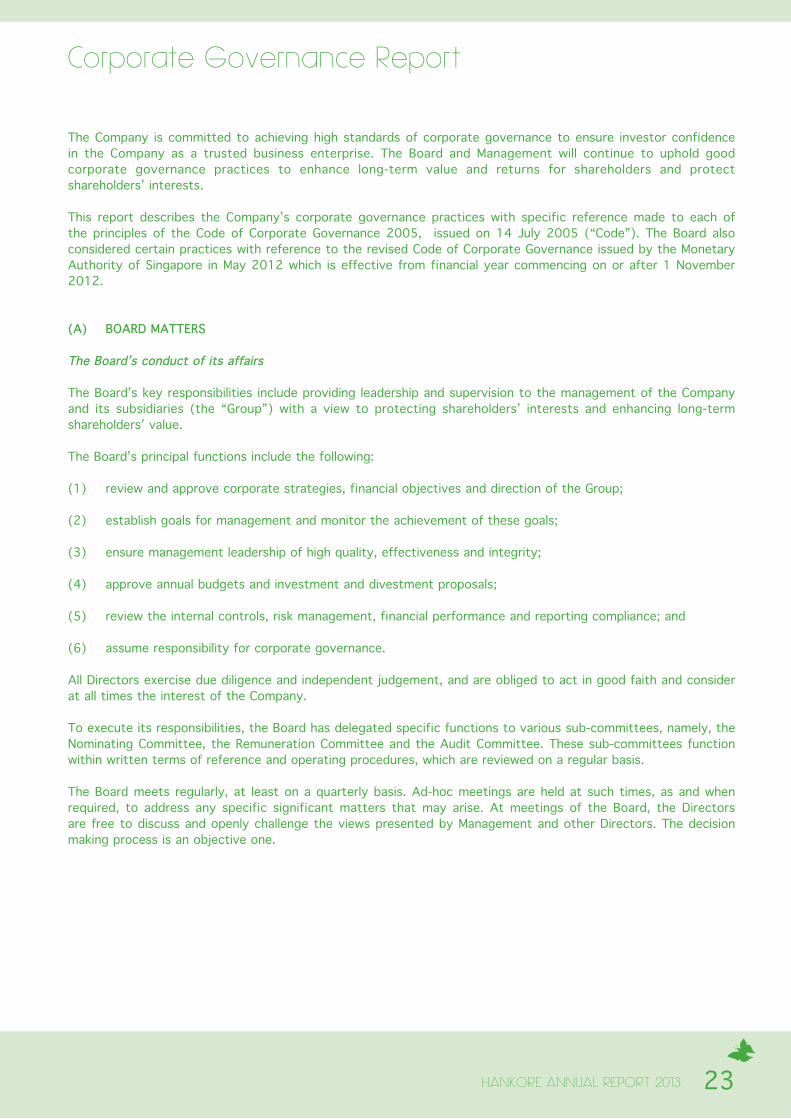

The Company is committed to achieving high standards of corporate governance to ensure investor confidence in the Company as a trusted business enterprise. The Board and Management will continue to uphold good corporate governance practices to enhance long-term value and returns for shareholders and protect shareholders’ interests.

This report describes the Company’s corporate governance practices with specific reference made to each of the principles of the Code of Corporate Governance 2005, issued on 14 July 2005 (“Code”). The Board also considered certain practices with reference to the revised Code of Corporate Governance issued by the Monetary Authority of Singapore in May 2012 which is effective from financial year commencing on or after 1 November 2012.

(A) BOARD MATTERS

The Board’s conduct of its affairs

The Board’s key responsibilities include providing leadership and supervision to the management of the Company and its subsidiaries (the “Group”) with a view to protecting shareholders’ interests and enhancing long-term shareholders’ value.

The Board’s principal functions include the following:

(1) review and approve corporate strategies, financial objectives and direction of the Group;

(2) establish goals for management and monitor the achievement of these goals;

(3) ensure management leadership of high quality, effectiveness and integrity;

(4) approve annual budgets and investment and divestment proposals;

(5) review the internal controls, risk management, financial performance and reporting compliance; and

(6) assume responsibility for corporate governance.

All Directors exercise due diligence and independent judgement, and are obliged to act in good faith and consider at all times the interest of the Company.

To execute its responsibilities, the Board has delegated specific functions to various sub-committees, namely, the Nominating Committee, the Remuneration Committee and the Audit Committee. These sub-committees function within written terms of reference and operating procedures, which are reviewed on a regular basis.

The Board meets regularly, at least on a quarterly basis. Ad-hoc meetings are held at such times, as and when required, to address any specific significant matters that may arise. At meetings of the Board, the Directors are free to discuss and openly challenge the views presented by Management and other Directors. The decision making process is an objective one.

Corporate Governance Report

HANKORE ANNUAL REPORT 201324

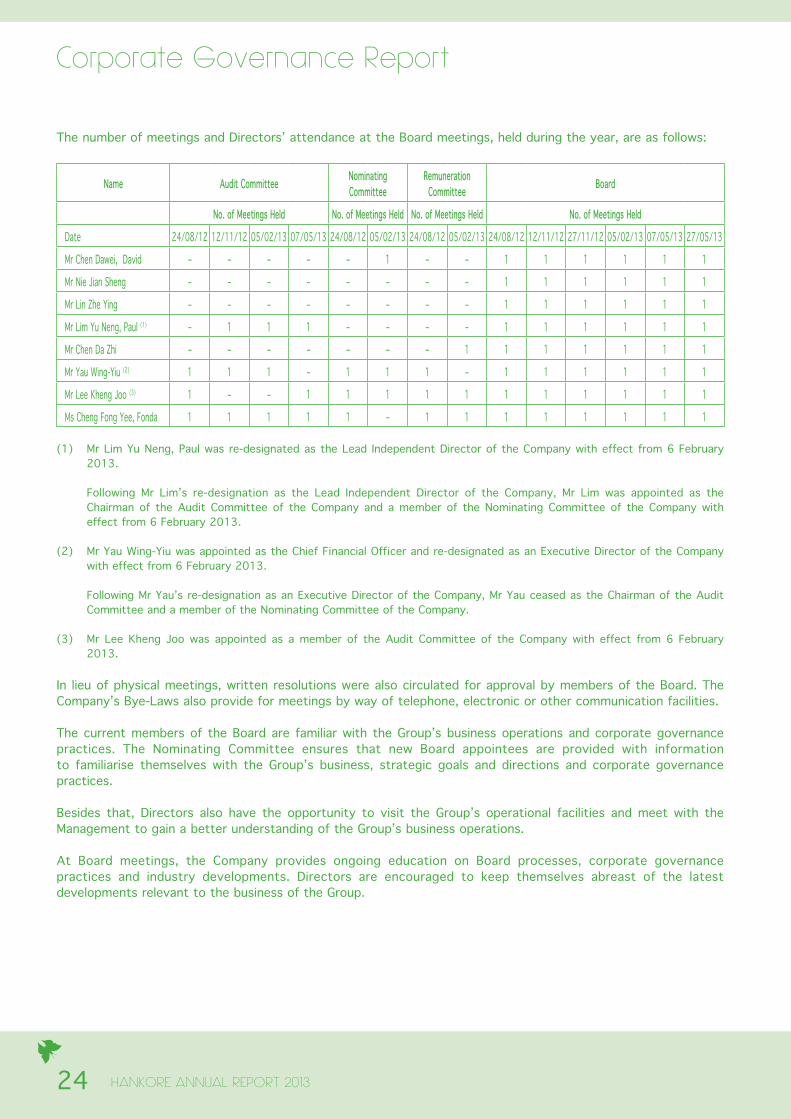

The number of meetings and Directors’ attendance at the Board meetings, held during the year, are as follows:

Name Audit Committee Nominating Committee

Remuneration Committee Board

No. of Meetings Held No. of Meetings Held No. of Meetings Held No. of Meetings Held

Date 24/08/12 12/11/12 05/02/13 07/05/13 24/08/12 05/02/13 24/08/12 05/02/13 24/08/12 12/11/12 27/11/12 05/02/13 07/05/13 27/05/13

Mr Chen Dawei, David – – – – – 1 – – 1 1 1 1 1 1

Mr Nie Jian Sheng – – – – – – – – 1 1 1 1 1 1

Mr Lin Zhe Ying – – – – – – – – 1 1 1 1 1 1

Mr Lim Yu Neng, Paul (1) – 1 1 1 – – – – 1 1 1 1 1 1

Mr Chen Da Zhi – – – – – – – 1 1 1 1 1 1 1

Mr Yau Wing-Yiu (2) 1 1 1 – 1 1 1 – 1 1 1 1 1 1

Mr Lee Kheng Joo (3) 1 – – 1 1 1 1 1 1 1 1 1 1 1

Ms Cheng Fong Yee, Fonda 1 1 1 1 1 – 1 1 1 1 1 1 1 1

(1) Mr Lim Yu Neng, Paul was re-designated as the Lead Independent Director of the Company with effect from 6 February 2013.

Following Mr Lim’s re-designation as the Lead Independent Director of the Company, Mr Lim was appointed as the

Chairman of the Audit Committee of the Company and a member of the Nominating Committee of the Company with effect from 6 February 2013.

(2) Mr Yau Wing-Yiu was appointed as the Chief Financial Officer and re-designated as an Executive Director of the Company with effect from 6 February 2013.

Following Mr Yau’s re-designation as an Executive Director of the Company, Mr Yau ceased as the Chairman of the Audit Committee and a member of the Nominating Committee of the Company.

(3) Mr Lee Kheng Joo was appointed as a member of the Audit Committee of the Company with effect from 6 February 2013.

In lieu of physical meetings, written resolutions were also circulated for approval by members of the Board. The Company’s Bye-Laws also provide for meetings by way of telephone, electronic or other communication facilities.

The current members of the Board are familiar with the Group’s business operations and corporate governance practices. The Nominating Committee ensures that new Board appointees are provided with information to familiarise themselves with the Group’s business, strategic goals and directions and corporate governance practices.

Besides that, Directors also have the opportunity to visit the Group’s operational facilities and meet with the Management to gain a better understanding of the Group’s business operations.

At Board meetings, the Company provides ongoing education on Board processes, corporate governance practices and industry developments. Directors are encouraged to keep themselves abreast of the latest developments relevant to the business of the Group.

Corporate Governance Report

25HANKORE ANNUAL REPORT 2013

Board Composition and Balance

The Board currently comprises of eight Directors, three of whom are Independent Directors. The Directors of the Company as at the date of this report are:-

(i) Chen Dawei, David (Executive Chairman)(ii) Nie Jian Sheng [Executive Director & Chief Executive Officer (“CEO”)](iii) Yau Wing-Yiu [Executive Director and Chief Financial Officer (“CFO”)](iv) Lin Zhe Ying (Executive Director)(v) Chen Da Zhi (Non-Executive Director)(vi) Lim Yu Neng, Paul (Lead Independent Director)(vii) Lee Kheng Joo (Independent Director)(viii) Cheng Fong Yee, Fonda (Independent Director)

The independence of each Director is assessed and reviewed annually by the NC. Each Independent Director is required to complete a Director’s Independence Checklist annually to confirm his/her independence based on the guidelines as set out in the Code. For FY2013, the NC has determined that all the three Non-Executive Directors are independent.

The Board has determined that it is of an appropriate size to facilitate effective decision making, and to meet the objective of having a balance of skills and experience, taking into account the size and scope of Company’s operations.

The current Board comprises of business leaders and professionals with industry, accounting, financial, business and management backgrounds. This composition enables the management to benefit from a diverse and objective external perspective, on issues raised before the Board. Each Director has been appointed based on the strength of his caliber, experience and his potential to contribute to the Group and its businesses. Profiles of the Directors are set out on pages 14 and 18 of this Annual Report.

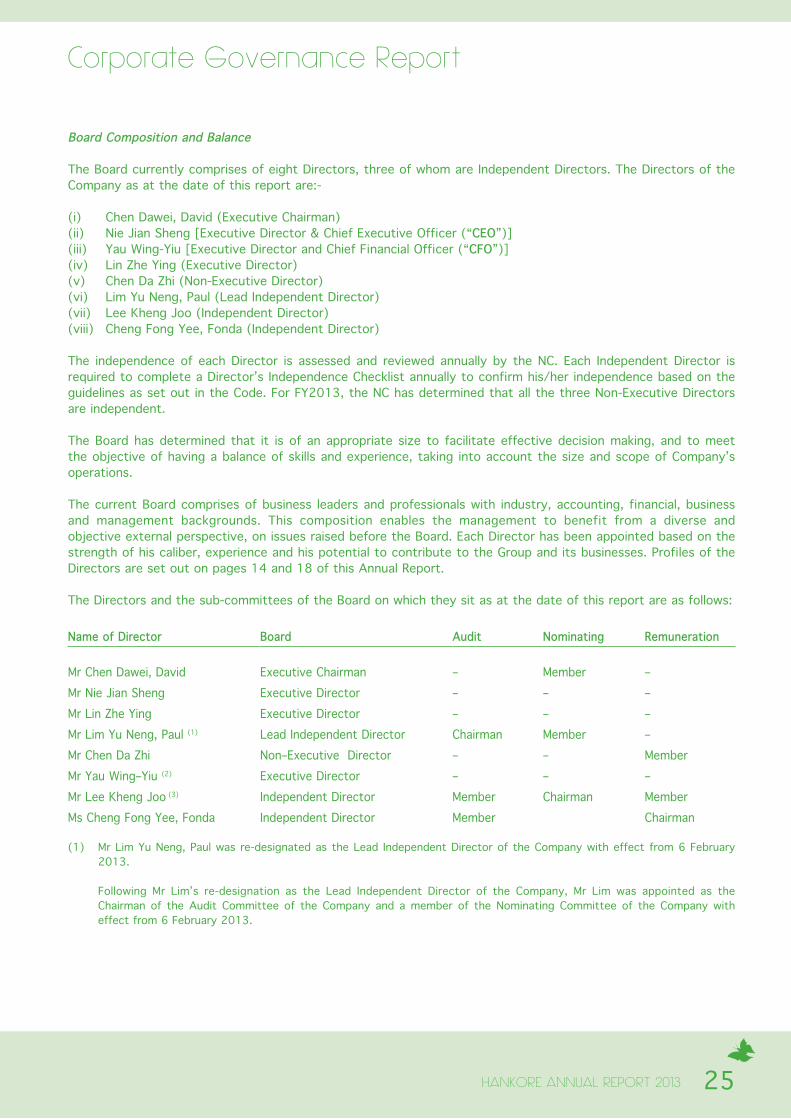

The Directors and the sub-committees of the Board on which they sit as at the date of this report are as follows:

Name of Director Board Audit Nominating Remuneration

Mr Chen Dawei, David Executive Chairman – Member –Mr Nie Jian Sheng Executive Director – – –Mr Lin Zhe Ying Executive Director – – –Mr Lim Yu Neng, Paul (1) Lead Independent Director Chairman Member –Mr Chen Da Zhi Non–Executive Director – – MemberMr Yau Wing–Yiu (2) Executive Director – – –Mr Lee Kheng Joo (3) Independent Director Member Chairman MemberMs Cheng Fong Yee, Fonda Independent Director Member Chairman

(1) Mr Lim Yu Neng, Paul was re-designated as the Lead Independent Director of the Company with effect from 6 February 2013.

Following Mr Lim’s re-designation as the Lead Independent Director of the Company, Mr Lim was appointed as the Chairman of the Audit Committee of the Company and a member of the Nominating Committee of the Company with effect from 6 February 2013.

Corporate Governance Report

HANKORE ANNUAL REPORT 201326

(2) Mr Yau Wing-Yiu was appointed as the Chief Financial Officer and re-designated as an Executive Director of the Company with effect from 6 February 2013.

Following Mr Yau’s re-designation as an Executive Director of the Company, Mr Yau ceased to be the Chairman of the Audit Committee and a member of the Nominating Committee of the Company.

(3) Mr Lee Kheng Joo was appointed as a member of the Audit Committee of the Company with effect from 6 February 2013.

The Board is able to exercise objective judgment on corporate affairs independently from the Management. No individual or group of individuals is allowed to dominate the Board’s decision making. The Board is of the view that, given its current structure, there is sufficiently strong independent element on the Board to enable independent exercise of objective judgment on corporate affairs of the Group by members of the Board, taking into account factors such as the number of Independent Directors on the Board, as well as the size and scope of the affairs and operations of the Group.

Chairman and Chief Executive Officer

The Board recognises the Code’s recommendation that the Chairman and the Chief Executive Officer should be separate persons to ensure that there is an appropriate balance of power and authority within the Company.

The Executive Chairman and CEO are responsible for exercising control over the quality and timeliness of the flow of information between management and the Board and ensuring compliance with the Group’s guidelines on corporate governance. They ensure that Board meetings are held regularly in accordance with as agreed schedule of meetings. They are also responsible for the day to day management of the Company and work with the Board for strategic planning, business development and charting the growth of the Group.

The Board is of the view that there are sufficient safeguards and checks to ensure that the process of decision making by the Board is independent and based on collective decisions without any individual exercising any considerable concentration of power or influence. Further, the Audit Committee, Remuneration Committee and Nominating Committee are chaired by Independent Director.

The Board had appointed Mr Lim Yu Neng, Paul as the Lead Independent Director to co-ordinate and becomes the principal liaison on Board issues between the Independent Directors and the Chairman. He is available to shareholders where they have concerns which contact through the normal channels of the Chairman, CEO or CFO has failed to resolve or for which such contact is inappropriate.

Board Membership

The Nominating Committee comprises Mr Lee Kheng Joo as its Chairman, Mr Lim Yu Neng, Paul and Mr Chen Dawei, David as its member with majority of whom, including the Chairman are Independent Directors. The Chairman of the Nominating Committee is not directly associated with a substantial shareholder of the Company within the meaning of the Code.

The principal functions of the Nominating Committee are as follows:

(1) establish procedures and make recommendations to the Board on all board appointments and re-nominations with regards to each Director’s contribution and performance, his or her attendance at meetings of the Board or Board committees (where applicable), participation, candour and any special contributions;

(2) review and determine annually whether a Director is independent, bearing in mind the considerations set out in the Code;

Corporate Governance Report

27HANKORE ANNUAL REPORT 2013

(3) decide whether or not each Director is able to and has adequately carried out his duties as a Director of the company, in particular where the Director concerned has multiple board representations;

(4) identify any gaps in the mix of skills, experience and other qualities required in an effective Board and nominate or recommend suitable candidate(s) to fill these gaps; and

(5) ensure that all Board appointees undergo an appropriate orientation programme.

In considering the re-appointment of a Director, the Nominating Committee evaluates such Director’s contribution and performance, such as his or her attendance at meetings of the Board or Board committees, where applicable, participation, candour and any special contributions.

All Directors are subject to the provisions of the Company’s Bye-Laws whereby each Director shall retire at least once every three (3) years and shall be eligible for re-election. Mr Lim Yu Neng, Paul and Ms Cheng Fong Yee, Fonda are subject to retirement pursuant to the Company’s Bye-Laws at the forthcoming AGM. The NC recommended that Mr Lim Yu Neng, Paul and Ms Cheng Fong Yee, Fonda be nominated for re-election at the forthcoming AGM.

The NC conducts an annual review of Directors’ independence and is of the view that Mr Lim Yu Neng, Paul, Mr Lee Kheng Joo and Ms Cheng Fong Yee, Fonda are independent and that, no individual or small group of individual dominates the Board’s decision-making process.

Board Performance

The NC has adopted a formal process for the evaluation of the performance of the Board. The performance criteria includes, amongst others, an evaluation of the size and composition of the Board, the Board’s access to information, accountability, Board processes and Board performance in relation to discharging its principal responsibilities in terms of the financial indicators as set out in the Code.

During the financial year, all Directors are requested to complete a Board Evaluation Questionnaire designed to seek their view on the various aspects of the Board performance so as to assess the overall effectiveness of the Board. The assessment process involves and includes input from the Board members before submitting to the Board for discussing and determining areas for improvement and enhancement of the Board’s effectiveness as well as its implementation.

Following the review, the NC assessed the Board’s performance as a whole in FY2013 and is of the view that the Board’s performance as a whole is satisfactorily.

Access to Information

To enable the Board to function effectively and to fulfill its responsibilities, Management strives to provide Board members with adequate information for Board meetings and on an ongoing basis.

The Board is furnished with Board papers prior to any Board meeting. These papers are issued in sufficient time to enable Directors to obtain additional information or explanations from Management, if necessary.

The Board also is informed of any significant developments or events relating to the Company timely.

Directors are given separate and independent access to the Management team to address any enquiries and also have separate and independent access to the Company Secretary. The Company Secretary attends all Board meetings and ensures that they are conducted in accordance with the Bye-Laws of the Company and the applicable rules and regulations are complied with. When necessary, Directors can seek independent professional advice at the Company’s expense.

Corporate Governance Report

HANKORE ANNUAL REPORT 201328

(B) REMUNERATION MATTERS

Procedures for Developing Remuneration Policies

The Remuneration Committee comprises Ms Cheng Fong Yee, Fonda as Chairman, Mr Lee Kheng Joo and Mr Chen Da Zhi as its member with majority of whom, including the Chairman are Independent Directors.

The RC is responsible for ensuring that a formal and transparent procedure is in place for developing an appropriate executive remuneration policy and a competitive framework for determining the remuneration packages of individual Directors and senior Management. The RC recommends for the Board’s endorsement, a framework of remuneration, including but not limited to Director’s fees, salaries, allowances, bonuses, options and benefits in kind for each Director and senior Management. No Director shall be involved in any decision-making in respect of any compensation to be offered or granted to him.

Level and Mix of Remuneration

Under the framework developed by the Remuneration Committee, the Remuneration Committee uses the following factors to determine Directors’ remuneration:

(1) qualifications and experience of Directors required by the Company;

(2) for Independent Directors, the general level of fees earned by each Director in his professional capacity or billed by professionals in their industry;

(3) time spent in preparing for meetings and actual attendance;

(4) indirect costs and expenses incurred by the Directors;

(5) such remuneration as may be considered fair and reasonable having regard to the nature and size of the business of the Company;

(6) level of remuneration to vary in direct proportion to the extent of involvement and participation in and contribution to the business of the Company;

(7) the level of commitment and the ability to devote sufficient time and attention to the business of the Company; and

(8) where special circumstances justify, the payment of additional remuneration.

Annual reviews are carried out by the Remuneration Committee to ensure that key executives are appropriately rewarded, giving due regard to the financial health and business needs of the Group without being excessive and thereby maximize shareholder value.

The Executive Directors have service agreements with the Company. Their compensation consists of salary, bonus, fixed fee and incentive bonus that is dependent on the Group’s performance.

The Group’s remuneration policy is to provide compensation packages appropriate to attract, retain and motivate key executives and Directors.

Corporate Governance Report

29HANKORE ANNUAL REPORT 2013

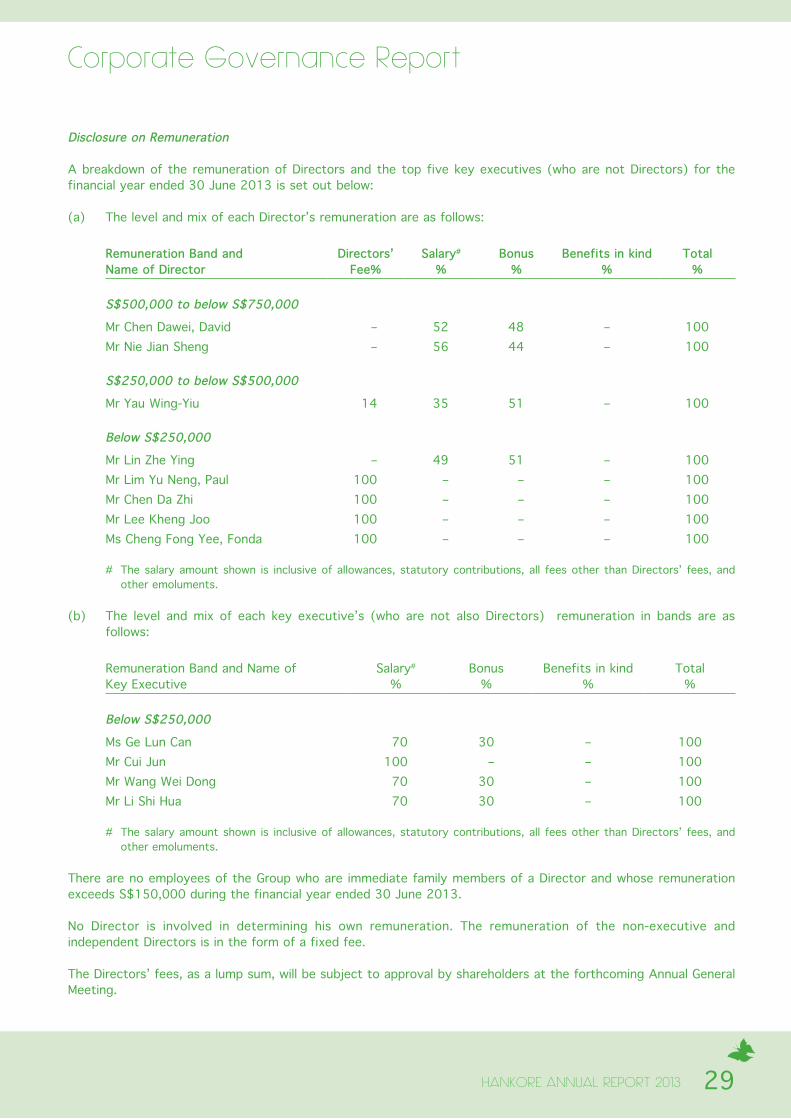

Disclosure on Remuneration

A breakdown of the remuneration of Directors and the top five key executives (who are not Directors) for the financial year ended 30 June 2013 is set out below:

(a) The level and mix of each Director’s remuneration are as follows:

Remuneration Band and Name of Director

Directors’ Fee%

Salary#

%Bonus

%Benefits in kind

%Total

%

S$500,000 to below S$750,000Mr Chen Dawei, DavidMr Nie Jian Sheng

––

5256

4844

––

100100

S$250,000 to below S$500,000Mr Yau Wing-Yiu 14 35 51 – 100

Below S$250,000Mr Lin Zhe YingMr Lim Yu Neng, PaulMr Chen Da ZhiMr Lee Kheng JooMs Cheng Fong Yee, Fonda

–100100100100

49––––

51––––

–––––

100100100100100

# The salary amount shown is inclusive of allowances, statutory contributions, all fees other than Directors’ fees, and other emoluments.

(b) The level and mix of each key executive’s (who are not also Directors) remuneration in bands are as follows:

Remuneration Band and Name of Key Executive

Salary#

%Bonus

%Benefits in kind

%Total

%

Below S$250,000Ms Ge Lun CanMr Cui JunMr Wang Wei DongMr Li Shi Hua

70100

7070

30–

3030

––––

100100100100

# The salary amount shown is inclusive of allowances, statutory contributions, all fees other than Directors’ fees, and other emoluments.

There are no employees of the Group who are immediate family members of a Director and whose remuneration exceeds S$150,000 during the financial year ended 30 June 2013.

No Director is involved in determining his own remuneration. The remuneration of the non-executive and independent Directors is in the form of a fixed fee.

The Directors’ fees, as a lump sum, will be subject to approval by shareholders at the forthcoming Annual General Meeting.

Corporate Governance Report

HANKORE ANNUAL REPORT 201330

The Company had in June 2005 cancelled all outstanding options granted to Directors and employees under the Bio-Treat Technology Employee Share Option Scheme (the “Scheme”). As at the date of this Report, there are no outstanding options under the Scheme.

(C) ACCOUNTABILITY AND AUDIT

Accountability

The Board’s primary role is to protect and enhance long-term value and returns for shareholders. In the discharge of its duties to shareholders, the Board, when reporting the Group’s financial performance via SGXNET announcements and the Annual Report, has a responsibility to present a fair assessment of the Group’s financial performance, position and prospects. Management currently provides the Board with detailed management accounts of the Group’s performance, position and prospects on a quarterly basis. Directors have access to the Management at all times.

Audit Committee

The Audit Committee (“AC”) comprises three Independent Directors and is chaired by Mr Lim Yu Neng, Paul. The other two members are Mr Lee Kheng Joo and Ms Cheng Fong Yee, Fonda.

The AC meets regularly with the Group’s external auditors and Management to review accounting, auditing and financial reporting matters, so as to ensure that an effective control environment is maintained in the Group.

The Audit Committee also monitors proposed changes in accounting policies, reviews the internal audit functions and discusses the accounting implications of major transactions. In addition, the AC also advises the Board regarding the adequacy of the Group’s internal controls and the contents and presentation of its reports.

The functions of the AC include:

(a) reviews with the external independent auditors their audit plan, their evaluation of the system of internal accounting controls in the course of their external audit, their letter to management and management response;

(b) reviews the quarterly and annual financial statements with management and the external independent auditors (where applicable) before submission to the board of Directors;

(c) reviews the adequacy of the Group’s internal controls, including financial, operational and compliance controls and risk management policies and systems;

(d) reviews and approves the internal audit plans of the internal auditors;

(e) evaluates the effectiveness of both the internal and external audit efforts through regular meetings;

(f) determines that no unwarranted management restrictions are being placed upon either the internal or external independent auditors;

(g) recommend to the board of Directors the appointment or re-appointment of the external independent auditors for the coming year;

Corporate Governance Report

31HANKORE ANNUAL REPORT 2013

(h) reviews the nature and extent of non-audit services provided by external independent auditors;

(i) meet with the external independent auditors, without the presence of the Company’s management, at least annually; and

(j) reviews interested person transactions (if any), in accordance with the requirements of the SGX-ST Listing Manual.

The Audit Committee is authorised to investigate any matter within its terms of reference, and has full access to the Management and also full discretion to invite any Director or executive officer to attend its meetings, as well as reasonable resources to enable it to discharge its functions properly.

The AC meets with the internal auditor and external auditors separately, at least once a year, without the presence of the Management to review any matter that might be raised.

The AC is satisfied with the independence and objectivity of the external auditors, Moore Stephens LLP and noted that there were no non-audit services provided by the external auditor during the financial year ended 30 June 2013. The Audit Committee is satisfied with the independence and objectivity of the external auditors and has recommended to the Board the re-appointment of Moore Stephens LLP as the external auditors of the Company at the forthcoming Annual General Meeting. The Company has complied with Rules 712 and 715 of the SGX-ST Listing Manual in relation to the engagement of its auditors, which is registered with the Accounting and Corporate Regulatory Authority.

Internal Controls

The Group’s internal controls and systems are designed to provide reasonable, but not absolute assurance to the integrity and reliability of the financial information and to safeguard and maintain the accountability of the assets. While no cost effective internal control system can provide absolute assurance against loss or misstatement, the Audit Committee, with the participation of the Board, has reviewed the adequacy of the Group’s internal controls and systems to ensure that they are designed to provide reasonable assurance that assets are safeguarded, operational controls are in place, business risks are suitably managed, proper accounting records are maintained and the integrity of financial information used for business and publication are preserved.

The internal auditors conduct annual review of the effectiveness of the Group’s key internal controls including financial, operational and compliance controls and risks management. The external auditors during the conduct of their normal audit procedures may also report on matters relating to internal control. Any material non-compliance and recommendation for improvements are reported to the Audit Committee. The Audit Committee also reviews and continues to monitor the effectiveness of the actions taken by the management on the recommendations made by the internal and external auditors in this respect.

Based on the work performed by the internal and external auditors (to the extent as required by the external auditor to form an opinion of the financial statements), reviews of the findings from the internal auditors on the Group’s internal controls and the management’s responses to the auditors’ recommendations for improvement to the Group’s internal controls and discussions with the auditors and management, the Board, with the concurrence of the Audit Committee, is satisfied with the adequacy of the Group’s internal controls, addressing financial, operational and compliance risks as at 30 June 2013 and that management has taken efforts to minimise the risk of recurrence of such lapses.

Internal Audit

The objective of the internal audit function is to provide an independent review of the effectiveness of the Group’s internal controls and provide reasonable assurance to the Audit Committee and the management that the Group’s risk management, controls and governance processes are adequate and effective.

Corporate Governance Report

HANKORE ANNUAL REPORT 201332

The Internal Audit function of the Group has been outsourced to RSM Nelson Wheeler Consulting Limited (“RSM”) to strengthen the internal audit function and promote sound risk management, including financial, operational and compliance controls and good corporate governance. RSM report directly to the Audit Committee on audit matters and to the Chairman on administrative matters.

RSM is a Certified Internal Auditor and the audit work is carried out in accordance with the International Standards for the Professional Practice of Internal Auditing pronounced by The Institute of Internal Auditors.

RSM’s main scope of work covers the review and evaluation of processes and areas of concerns identified. RSM assists management in enhancing existing risk management initiatives and carry out regular independent monitoring of key controls and procedures. The findings and recommendations in relation to the adequacy and effectiveness of internal controls and process improvements will be presented to the Audit Committee and the management.

Material non-compliance and internal control weaknesses noted during reviews are reported together with recommended corrective actions to the Audit Committee on a regular basis. The results of the internal audit findings are also shared with the External Auditors to assist them in their audit planning and also for them to perform further checks on the weak areas identified.

(D) COMMUNICATION WITH SHAREHOLDERS

In line with continuous disclosure obligations of the Company, and pursuant to the Singapore Exchange Securities Trading Limited (“SGX-ST”) Listing Rules and Bermuda Companies’ legislation, the Board ensures that shareholders are fully informed of all major developments that impact the Group.

Information is disseminated to the shareholders on a timely basis through:

(i) SGXNET announcements and press releases;

(ii) Annual Reports prepared and issued to all shareholders; and

(iii) Company’s website at www.hankore.com at which shareholders can access information on the Group.

Quarterly results are released within 45 days of the quarter of the financial year. The Company ensures that it does not practise selective disclosure of material information. Material information is publicly released before the Company meets with investors or analysts.

Shareholders are encouraged to attend the Company’s Annual General Meeting to be kept informed of the Group’s strategy and goals. The notice of the Annual General Meeting is despatched to shareholders, together with explanatory notes or a circular on items of special business, at least 14 working days before the meeting.

The Annual General Meeting is the principal forum for dialogue with shareholders.

The respective Board members will be available at the forthcoming Annual General Meeting to answer questions relating to the work of those sub-committees.

Our Management acknowledges that effective communication with investors is of paramount importance to the Group. In order to reinforce mutual understanding between shareholders and the Company, we have established and maintained a number of ways to strengthen our communication with investors.

Corporate Governance Report

33HANKORE ANNUAL REPORT 2013

Measures that the Company has taken are as follows:

(a) organise analyst briefings to explain our latest published financial information as well as to provide our business update when necessary;

(b) attend meetings/ telephone conferences requested by investors/ shareholders/ analysts on an ongoing basis throughout the year to assist them in understanding the latest updates relating to the Company;

(c) organise road shows for our investors/ potential investors. This may be done solely by ourselves or coordinated with investment bankers;

(d) organise plant visits by investors/ potential investors to our facilities; and

(e) ensure important information of the Group will be announced in a timely manner without delay.

(E) GREATER SHAREHOLDER PARTICIPATION

Shareholders are informed of shareholders’ meetings through notices contained in annual reports or circulars sent to all shareholders. Theses notices are also published in the Business Times and posted onto the SGXNet.

If shareholders are unable to attend the meetings, the Bye-Laws allow a shareholder of the Company to appoint not more than two proxies to attend and vote instead of him.

Resolutions at general meetings are on each substantially separate issue. All the resolutions at the general meetings are single item resolutions.

The Chairman of the Executive, Audit, Remuneration and Nominating Committees are in attendance at the Company’s AGM to address shareholders’ questions relating to the work of these Committees.

The Company’s external auditors, Moore Stephens LLP, are also invited to attend the AGM and are available to assist the Directors in addressing any relevant queries by the shareholders relating to the conduct of the audit and the preparation and content of the auditors’ report.

(F) DEALINGS IN SECURITIES

In line with Listing Rule 1207(19) of the Listing Manual, the Group prohibits its Directors and employees from trading in the Company’s securities on short-term considerations. In addition, the Group prohibits its Directors and employees from dealing in the Company’s securities during the period beginning one month before the release of any financial results of the Group or if they are in possession of any unpublished material price-sensitive information relating to the Group.

(G) MATERIAL CONTRACTS

There are no material contracts of the Group involving the interests of any Directors or controlling shareholders subsisting at the end of the financial year ended 30 June 2013, or entered into since the end of the previous financial year.

Corporate Governance Report

HANKORE ANNUAL REPORT 201334

(H) INTERESTED PERSON TRANSACTIONS

The Company has established procedures to ensure that all transactions with interested persons are reported in a timely manner to the Audit Committee and that transactions are conducted on arm’s length basis and not prejudicial to the interests of the shareholders.

The Company does not have a general shareholders’ mandate for recurrent interested person transaction. The Company confirms that there were no interested person transactions during the financial year under review.

(I) RISK MANAGEMENT

The risk management is subject to the Audit Committee and no other dedicated committee will be set up. The Group has appointed the financial controller of the Group to manage the risk of the Group. He is responsible for summarizing the risk management results of each department and assessing the potential material risks confronting the group according to the risk management program of the Group, formulating and implementing the risk management plan for the next year.

Report of the Directors30 June 2013

35HANKORE ANNUAL REPORT 2013

The directors are pleased to present their report to the members together with the consolidated financial statements of Hankore Environment Tech Group Limited (the “Company”) and its subsidiaries (the “Group”) for the financial year ended 30 June 2013 and the audited statement of financial position of the Company as at 30 June 2013.

1 Directors

The directors of the Company in office at the date of this report are as follows: Chen Dawei, David Nie Jian Sheng Lin Zhe Ying Lim Yu Neng, Paul Cheng Fong Yee Chen Da Zhi Yau Wing-Yiu Lee Kheng Joo

2 Arrangements to Enable Directors to Acquire Shares or Debentures

Neither at the end of nor at any time during the financial year was the Company a party to any arrangement whose object is to enable the directors of the Company to acquire benefits by means of the acquisition of shares in or debentures of the Company or any other body corporate.

3 Directors’ Interests in Shares or Debentures

According to the register of directors’ shareholdings, none of the directors holding office at the end of the financial year had any interest in the shares or debentures of the Company or its related corporations, except as follows:

Name of directorsShareholdings registeredin the name of directors

Shareholdings in which directors are deemed to have an interest

As at 1/7/2012

As at 30/6/2013

As at 21/7/2013

As at1/7/2012

As at 30/6/2013

As at 21/7/2013

The CompanyNumber of ordinary shares

Chen Dawei, David – – – 794,203,561 794,203,561 794,203,561Lim Yu Neng, Paul – – – 1,000,000 1,000,000 1,000,000

Report of the Directors30 June 2013

HANKORE ANNUAL REPORT 201336

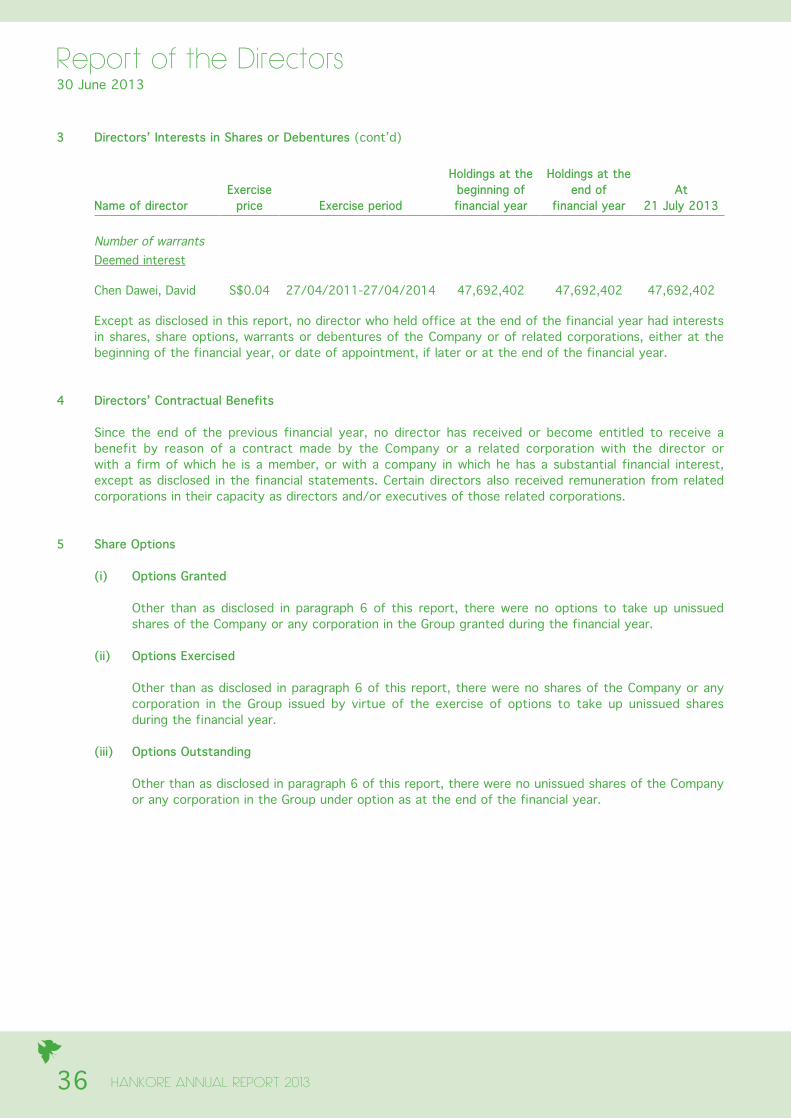

3 Directors’ Interests in Shares or Debentures (cont’d)

Name of director Exercise

price Exercise period

Holdings at the beginning of financial year

Holdings at the end of

financial yearAt

21 July 2013

Number of warrantsDeemed interest

Chen Dawei, David S$0.04 27/04/2011-27/04/2014 47,692,402 47,692,402 47,692,402

Except as disclosed in this report, no director who held office at the end of the financial year had interests in shares, share options, warrants or debentures of the Company or of related corporations, either at the beginning of the financial year, or date of appointment, if later or at the end of the financial year.

4 Directors’ Contractual Benefits

Since the end of the previous financial year, no director has received or become entitled to receive a benefit by reason of a contract made by the Company or a related corporation with the director or with a firm of which he is a member, or with a company in which he has a substantial financial interest, except as disclosed in the financial statements. Certain directors also received remuneration from related corporations in their capacity as directors and/or executives of those related corporations.

5 Share Options

(i) Options Granted

Other than as disclosed in paragraph 6 of this report, there were no options to take up unissued shares of the Company or any corporation in the Group granted during the financial year.

(ii) Options Exercised

Other than as disclosed in paragraph 6 of this report, there were no shares of the Company or any corporation in the Group issued by virtue of the exercise of options to take up unissued shares during the financial year.

(iii) Options Outstanding

Other than as disclosed in paragraph 6 of this report, there were no unissued shares of the Company or any corporation in the Group under option as at the end of the financial year.

Report of the Directors30 June 2013

37HANKORE ANNUAL REPORT 2013

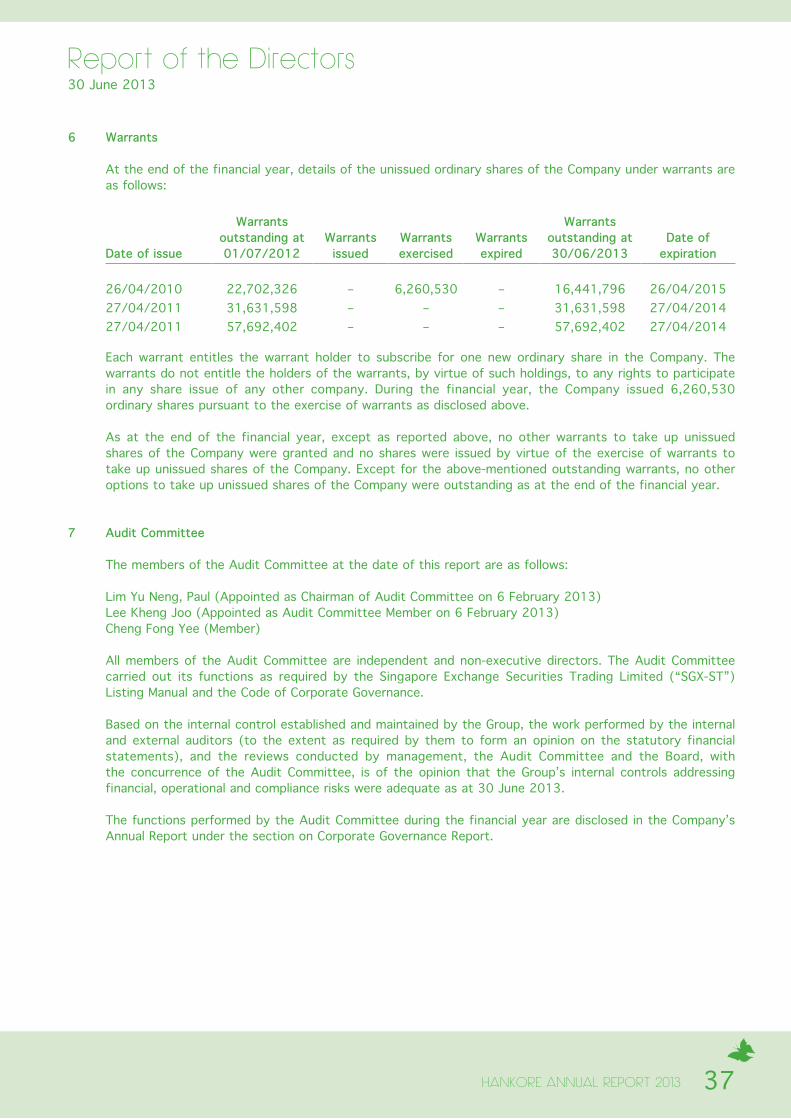

6 Warrants

At the end of the financial year, details of the unissued ordinary shares of the Company under warrants are as follows:

Date of issue

Warrants outstanding at 01/07/2012

Warrants issued

Warrants exercised

Warrants expired

Warrants outstanding at 30/06/2013

Date of expiration

26/04/2010 22,702,326 – 6,260,530 – 16,441,796 26/04/201527/04/2011 31,631,598 – – – 31,631,598 27/04/201427/04/2011 57,692,402 – – – 57,692,402 27/04/2014

Each warrant entitles the warrant holder to subscribe for one new ordinary share in the Company. The warrants do not entitle the holders of the warrants, by virtue of such holdings, to any rights to participate in any share issue of any other company. During the financial year, the Company issued 6,260,530 ordinary shares pursuant to the exercise of warrants as disclosed above.

As at the end of the financial year, except as reported above, no other warrants to take up unissued shares of the Company were granted and no shares were issued by virtue of the exercise of warrants to take up unissued shares of the Company. Except for the above-mentioned outstanding warrants, no other options to take up unissued shares of the Company were outstanding as at the end of the financial year.

7 Audit Committee

The members of the Audit Committee at the date of this report are as follows:

Lim Yu Neng, Paul (Appointed as Chairman of Audit Committee on 6 February 2013) Lee Kheng Joo (Appointed as Audit Committee Member on 6 February 2013) Cheng Fong Yee (Member)

All members of the Audit Committee are independent and non-executive directors. The Audit Committee carried out its functions as required by the Singapore Exchange Securities Trading Limited (“SGX-ST”) Listing Manual and the Code of Corporate Governance.

Based on the internal control established and maintained by the Group, the work performed by the internal and external auditors (to the extent as required by them to form an opinion on the statutory financial statements), and the reviews conducted by management, the Audit Committee and the Board, with the concurrence of the Audit Committee, is of the opinion that the Group’s internal controls addressing financial, operational and compliance risks were adequate as at 30 June 2013.

The functions performed by the Audit Committee during the financial year are disclosed in the Company’s Annual Report under the section on Corporate Governance Report.

Report of the Directors30 June 2013

HANKORE ANNUAL REPORT 201338

8 Independent Auditors

The independent auditors, Moore Stephens LLP, Public Accountants and Chartered Accountants, have expressed their willingness to accept reappointment.

On behalf of the Board of Directors,

CHEN DAWEI, DAVIDExecutive Chairman

NIE JIAN SHENGExecutive Director and Chief Executive Officer

25 September 2013

Statement by Directors30 June 2013

39HANKORE ANNUAL REPORT 2013

(a) The directors are of the opinion that the consolidated financial statements of the Group and the statement of financial position of the Company set out on pages 41 to 117 are drawn up so as to give a true and fair view of the state of affairs of the Group and of the Company as at 30 June 2013 and of the results, changes in equity and cash flows of the Group for the year then ended; and