Embed Size (px)

Citation preview

___________________________________________________________________________

2017/ISOM/SYM/003 Session 1

Harnessing Inclusive Opportunities: Embracing the Digital Future - Digital Economy and Inclusivity

Submitted by: PECC

Symposium on APEC 2018 PrioritiesPort Moresby, Papua New Guinea

5 December 2017

Harnessing Inclusive

Opportunities: Embracing the

Digital Future

Digital Economy and Inclusivity

ISOM Symposium

Stanley Hotel

Port Moresby

5 December, 2017

Eduardo Pedrosa

Secretary General

Pacific Economic Cooperation Council

The views expressed here are his own and do not necessarily

reflect those of the PECC nor its members.

Trade as a driver of growth?

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

Difference Gross domestic product, constant prices Trade volume of goods and services

Data: The New Driving Force

Source: http://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/the-global-forces-

inspiring-a-new-narrative-of-progress

Are we ready?1

1.1 1

6.2

9.3

7.6

21

.9

7.2

20

.2

28

.6

8.9

7.5

14

.7

4.3

6.2

5.5

20

.3

16

.9

16

18

.7

9.5

0

5

10

15

20

25

30

35

Au

stra

lia

Ca

na

da

Ch

ile

Ch

in

a

Ho

ng K

ong

(C

hin

a)

In

do

nesia

Jap

an

Ko

re

a

Ma

la

ysia

Me

xic

o

Ne

w Z

ealan

d

Pa

pua

N

ew

G

uin

ea

Pe

ru

Ph

ilip

pine

s

Sing

apo

re

Ch

in

ese

T

aipe

i

Th

aila

nd

Un

ited

S

ta

te

s

Vie

tn

am

Average Speed Mbps

Source: Akamai State of the Internet Report 2017 and http://www.dospeedtest.com/speedtest-result/country-statistics/

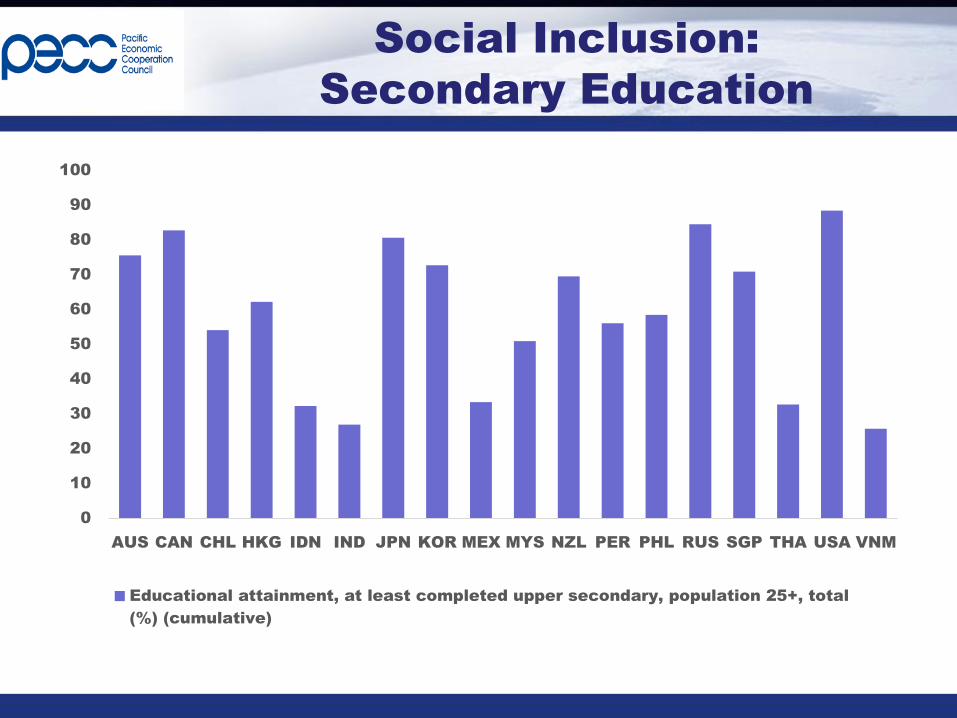

Social Inclusion:

Secondary Education

0

10

20

30

40

50

60

70

80

90

100

AUS CAN CHL HKG IDN IND JPN KOR MEX MYS NZL PER PHL RUS SGP THA USA VNM

Educational attainment, at least completed upper secondary, population 25+, total

(%) (cumulative)

Solution

Tech4Ed: ASL

• Tech4ED example in the Philippines includes Alternative

Learning System

– Uses 1000 public libraries

– TV White Space used to connect base stations to remote areas

– Bandwidth in the 600 MHz frequency range

• travels over hills and buildings and trees

Social Inclusion

Physicians per 10003

.2

7

1.4

4

2.0

7

1.0

3

1.9

4

1.3

2

0.2

0

2.3

0

2.1

4

2.1

0

1.2

0

2.7

4

1.1

3

1.1

5

0.0

6

4.3

1

1.9

5

0.3

9

2.4

5

1.1

9

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

Physicians (per 1,000 people)

Remote Healthcare Solutions

• Challenge:

– Fewer than 50 cardiologists to

service Cameroon’s 23 million

citizens

• Solution:

– Cardio Pad provide solutions

to heart patients based in

remote areas

– Allows nurses in remote areas

to do ECG

– Results sent over-the-air to

cardiologists in city centers

often hundreds of miles away

for doctor’s assessments

Financial Inclusion

% population (15+) with an account at a

financial institution

0

10

20

30

40

50

60

70

80

90

100

AUS CAN CHL CHN HKC IDN JPN KOR MEX MYS NZL PER PHL RUS SGP THA USA VNM

Mobile Accounts and GDP pc

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

6 7 8 9 10 11 12

Mo

bile

A

cc

ou

nt %

+1

5

Ln GDPpc

Early adopters aren’t

necessary high income

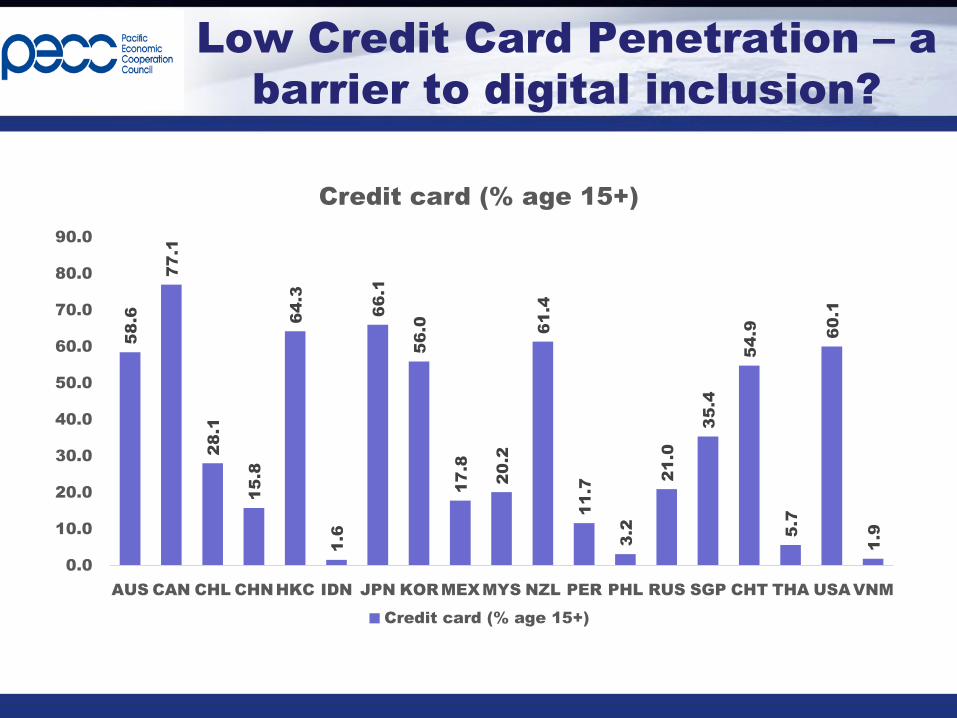

Low Credit Card Penetration – a

barrier to digital inclusion?

58

.6

77

.1

28

.1

15

.8

64

.3

1.6

66

.1

56

.0

17

.8

20

.2

61

.4

11

.7

3.2

21

.0

35

.4

54

.9

5.7

60

.1

1.9

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

AUS CAN CHL CHNHKC IDN JPN KORMEXMYS NZL PER PHL RUS SGP CHT THA USAVNM

Credit card (% age 15+)

Credit card (% age 15+)

Local solutions for Local Problems

Disrupting or Enabling Traditional Retail

Sector?

• Leading Online-to-Offline (O2O)

platform.

• Enables digital entrepreneurs to

become the gateway for unbanked

• Agent network across 500+ cities in

remote towns and rural areas of

Indonesia enables customers to

transact online

• Mixes traditional channels

• Allows online whilst still making

payments through cash.

Vendors not online but you are…

• 95% of home-stays and

guest houses do not have

own website

• Villagehuts.com works with

accommodation and tour

service providers to provide

secure way of booking

accommodation and tours

in PNG

Opportunities for more

inclusive growth

AUSCAN

CHN

HKG

IDN

JPN

MYS

MMR

NZL

PHL

SGP

THA

USA

VNM

0

20

40

60

80

100

120

0 5 10 15 20 25 30 35 40

Ac

co

un

t at a

fin

an

cia

l in

stitu

tio

n (%

a

ge

1

5+)

Commercial bank branches (per 100,000 adults)

Adoption not dependent on

income levels

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16

Nu

mb

er o

f A

ctive

M

ob

ile

M

on

ey

Ac

co

un

ts

East Asia and Pacific Europe and Central Asia

Latin America and the Caribbean Sub-Saharan Africa

Source: GSMA Global Mobile Money dataset Date: April 2017 | Version: 1.0

Y-o-Y Growth Rate of Internet

Users in APEC

19

.2

%

12

.9

%

6.2

%

11

.2

%

9.7

%

3.1

%

8.0

%

1.1

%

-0

.1

%

1.7

%

-0

.2

%

4.5

%

1.4

%

2.5

%

2.6

%

50

.1

%

56

.7

%

32

.5

%

22

.2

%

21

.3

%

21

.6

%

37

.7

%

29

.5

%

22

.3

%

24

.2

%

13

.0

%

13

.6

%

8.0

%

6.2

%

7.9

%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

Advanced Emerging

Source: World Development Indicators

Affordability of Internet Access

0.3

5

0.6

5

0.9

4

1.4

6

1.3

0

0.8

3

1.3

6

1.2

5

0.4

3

1.3

2

1.9

1

0.6

3

21

.0

7

2.6

7

6.7

4

0.5

2

0.3

1

1.2

1

0.3

6

3.5

2

0

5

10

15

20

25

Au

stra

lia

Bru

nei D

aru

ssalam

Ca

na

da

Ch

ile

Ch

in

a

Ho

ng K

ong

(C

hin

a)

In

do

nesia

Jap

an

Ko

re

a

Ma

la

ysia

Me

xic

o

Ne

w Z

ealan

d

Pa

pua

N

ew

G

uin

ea

Pe

ru

Ph

ilip

pine

s

Ru

ssia

Sing

apo

re

Th

aila

nd

Un

ited

S

ta

te

s

Vie

tn

am

Co

st o

f 1

GB

a

s %

G

NI p

er c

ap

ita

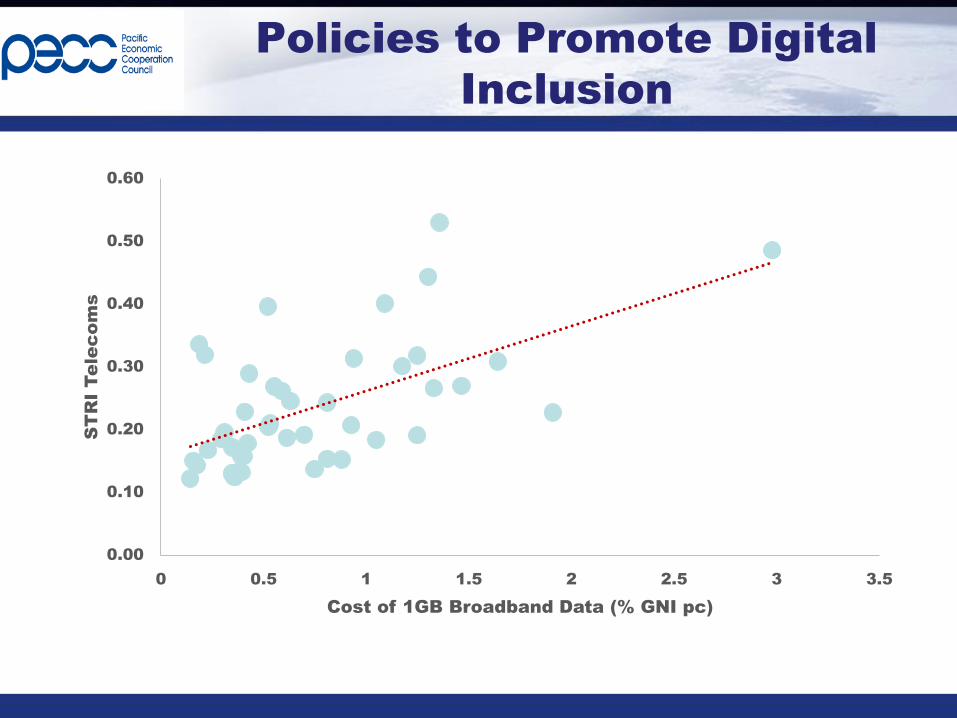

Policies to Promote Digital

Inclusion

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0 0.5 1 1.5 2 2.5 3 3.5

ST

RI Te

le

co

ms

Cost of 1GB Broadband Data (% GNI pc)

What are the most important

benefits of the digital economy?

78.9%

77.3%

71.0%

67.0%

66.6%

58.7%

Growth in productivity

Access to larger markets – especially for micro

and small and medium enterprises

Increased consumer choices

More customized products and services

New job opportunities in my economy

Cheaper products and services

% important

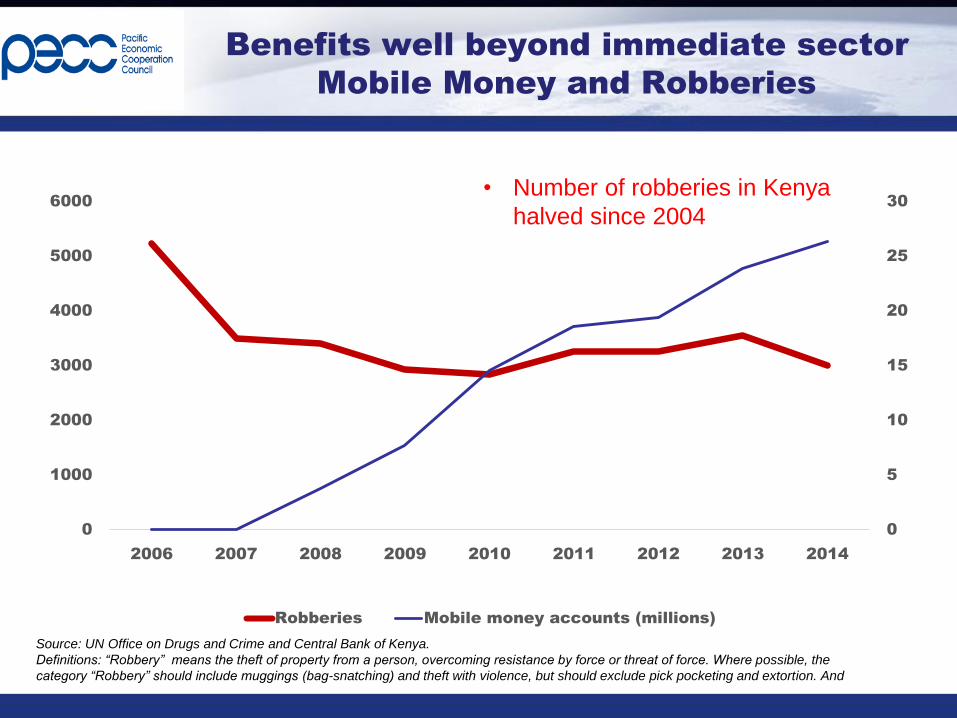

Benefits well beyond immediate sector

Mobile Money and Robberies

0

5

10

15

20

25

30

0

1000

2000

3000

4000

5000

6000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Robberies Mobile money accounts (millions)

• Number of robberies in Kenya

halved since 2004

Source: UN Office on Drugs and Crime and Central Bank of Kenya.

Definitions: “Robbery” means the theft of property from a person, overcoming resistance by force or threat of force. Where possible, the

category “Robbery” should include muggings (bag-snatching) and theft with violence, but should exclude pick pocketing and extortion. And

Priorities issues for the growth

of the digital economy

70.9%

63.2%

60.2%

50.9%

44.4%

40.0%

37.9%

30.5%

29.3%

25.9%

26.4%

23.1%

24.0%

20.6%

11.5%

54.0%

50.3%

44.9%

33.5%

35.2%

32.4%

23.4%

28.3%

19.0%

18.2%

14.2%

14.8%

12.6%

13.9%

10.7%

0% 20% 40% 60% 80%

Data protection

Digital infrastructure

Data privacy

Universal broadband access

Digital literacy

Interoperability of platforms

Holistic (whole-of-government) policy frameworks

Seamless cross-border data flows

Regulatory equivalence to promote mutual recognition

Online dispute resolution mechanisms

Standardized digital economy measurements

Digital IDs

Common application of sales taxes (ie VAT, GST)

Open data programmes

De minimis levels of trade

Emerging Advanced

Question: How important do you think the following areas are for the growth of the digital economy?

Challenge: Speed of Change

Accelerating

75

38

13

4 3.5

0

10

20

30

40

50

60

70

80

Telephone Radio TV Internet Facebook

Years to reach audience of 50 million

Digital Economy and Inclusion

• Accelerating pace of change gives rise to imperatives:

– an imperative for swift action

– flexible approaches

– holistic approaches

• Benefits are beyond any one sectoral interest – social benefits?

• Slowing growth of internet penetration – why?

– Need to look at regulatory environment – openness and competition key to

affordability and speed

• Why is it important?

• Opportunity for more inclusive growth model

– Financial inclusion – mobile money – not correlated with high income

– Local innovators – finding solutions to local context

• Data protection and data privacy

– From being a risk manager, and an enforcer of sectoral regulation, the

regulator needs to become an advocate for, and an enabler of, digital

inclusion and innovation

– Balance need for security and privacy with drive for innovation and

inclusion

• Implementation of APEC Roadmap