Embed Size (px)

DESCRIPTION

Harris Smith - GT White Paper

Citation preview

Top trends in middle-market private equity

Contents

1 Executive summary

3 The impact of the credit crunch

7 The explosion of cross-border M&A activity

11 The proliferation of operational partners

13 The emergence of sovereign wealth funds

16 The middle-market compensation squeeze

18 Three hot sectors for investment

21 The natural evolution of the private equity firm

23 Conclusion

About the author

Harris Smith Managing Partner, Private Equity and Strategic Relationships

Harris Smith is a Certified Public Accountant and the managingpartner of Private Equity and Strategic Relationships for Grant Thornton LLP. In 1976 Smith started his career in theBaltimore office of Grant Thornton. In 1986, he was promoted topartner and in 1989 he relocated to the Southern California officeto head up the Assurance practice. In 1998, Smith was promotedto office managing partner of the Greater Bay Area offices, and in2003 he became the West Region managing partner. In 2008 hebecame the managing partner of Private Equity and StrategicRelationships.

In his current role, Smith is responsible for the development andenhancement of strategic relationships for the firm and at thesame time, overseeing the services provided to private equityclients. This dual role provides Smith the opportunity to furtherelevate the firm’s reputation and to create relationships with keyinfluencers to deal with challenges in the marketplace and toenhance our brand. With over 30 years of experience, Smith is amember of the firm’s National Leadership Team and the sponsor ofGrant Thornton’s Women’s Initiative.

Smith is a director, executive committee member and chairman ofthe Association of Corporate Growth. He served as president(2003) and director of the San Francisco Chapter of theAssociation of Corporate Growth beginning in 2000. Smith residesin Los Angeles with Jill, his wife of 26 years, and is the father oftwins, Stephanie and Jordan, who are seniors at the University ofSouthern California and UC Berkeley, respectively.

AcknowledgementsThe author would like to thank Danielle Fugazy, Lora DeSanto, Pat Fanelli and Bill Haynes for their contributions to this project.

Top trends in middle-market private equity 1

Executive summary

This white paper explores seven trendsthat have recently altered the way theprivate equity community conductsbusiness. Some of the issues explored inthe white paper are important because ofthe cyclicality of the private equitybusiness, while others are emergingtrends that may become mainstream inthe coming years. As these private equitytrends have gained visibility and affectedinvestment opportunity in the middle-market private equity sector, Grant Thornton decided to seek a broadperspective on their current and emergingimpact, how they developed, what isdriving them, how widespread they havebecome, how they affect marketparticipants and what challenges theycreate for the middle market.

To explore these questions, a Grant Thornton team considered manydata points, including reviewingAssociation for Corporate Growth(ACG) and Thomson Reuters surveys,interviewing private equity professionalsabout the state of the market, and drawingupon the expertise and experiences of ourprivate equity service professionals.Through many different sources andoriginal reporting, Grant Thorntoncompiled the white paper to give readers abetter understanding of where the middlemarket is today, how it got there andwhere it is heading.

The key areas explored are: • the impact of the credit crunch, • the explosion of cross-border M&A

activity, • the proliferation of operational

partners,• the emergence of sovereign wealth

funds, • the middle-market compensation

squeeze, • three hot sectors for investment, and • the natural evolution of the private

equity firm.

The current environmentThe private equity market will finish out ayear that will be remembered as the onewhen the record dealmaking streak ended.A new era of quiet uncertainty has comeover the industry. Gone are the days offrenzied dealmaking. 2007 produced thethird and last year of consecutive record-breaking deal volume. According toThomson Reuters, U.S. buyout firmscompleted only about $55 billion worthof deals during the first half of 2008,making it extremely doubtful that 2008will reach the $475 billion in dealscompleted in 2007.

The first trend is that a cyclical market brings change and change breeds uncertainty. The subprimemortgage/housing debacle and its impacton credit is the primary trend that hastriggered the 2008 down cycle. Privateequity firms are returning to the dayswhere they spend substantially more timelooking for quality companies to invest in,and they are performing more thoroughdue diligence rather than jumping in to aninvestment headfirst.

However, contrary to the headlinesthat grace industry trade publications, allis not doom and gloom. The middlemarket has been able to hold its own quitewell compared to the big-deal market.That being said, there’s no denying thatthere has been a flight to quality, acontraction in leverage multiples and atightening of financing terms. The goodnews is that deals are still getting done.

The second trend is that private equityfirms have adapted to the changingmarket by opting to do cross-borderdeals. Middle-market investment bankingfirms, like Harris Williams & Co. forexample, say that they expect to spendmore time on globalization and emergingmarkets, and they see their clients alsodoing so in the next year.

The middle market has been able to hold its own quite wellcompared to the big-deal market.

2 Top trends in middle-market private equity

A third trend is the hiring ofoperational partners, representinganother way private equity firms havebeen able to transform themselves. Hiringoperational partners is a recentphenomenon. While larger firms alwaysput big-name advisors on their letterhead,middle-market firms have increasinglybeen hiring partners who don’tnecessarily have private equityknowledge, but who do possess expertknowledge in a particular sector. Toutingoperational partners is a good way forfirms to woo management teams intoday’s market, where competition forquality deals is more fierce than ever.Bringing extra capabilities to thebargaining table can only help firmsbecome more competitive.

The fourth trend affecting the privateequity community is the emergence ofsovereign wealth funds (SWFs). MorganStanley researchers say SWFs, mainly inAsia and the Middle East, poured around$45 billion into a range of companies andassets in 2007 alone. Some analysts believeSWF assets could reach $15 trillion by2015. SWFs are here to stay; they willhave an increasing long-term impact onthe marketplace.

The squeeze on middle-marketcompensation is the fifth significant trend.As the megafunds have grown even larger,they have hired more talent to broadentheir scope, luring private equity talentaway from middle-market firms. Thiswhite paper discusses practices thatmiddle-market firms are using to retaintop talent.

The sixth trend is that certain industrysectors have remained particularly strong,despite the global credit crisis. Thetechnology, health care and energy sectorscontinue to present strong investmentopportunities and are expected to do sofor years to come.

Lastly, with the lines blurringbetween private equity firms, hedgefunds, lenders and bankers, private equityfirms are emerging as asset managers.This trend has already begun to takeplace in the larger market, and is nowemerging in the middle market. Manybelieve it is the natural evolution of theindustry. This white paper explores whatfirms are doing to drive this trend, andwhat some middle-market private equitymanagers think of it.

With the lines blurring between private equity firms, hedge funds, lenders and bankers, private equity firms are emerging as asset managers.

Top trends in middle-market private equity 3

The impact of the credit crunch

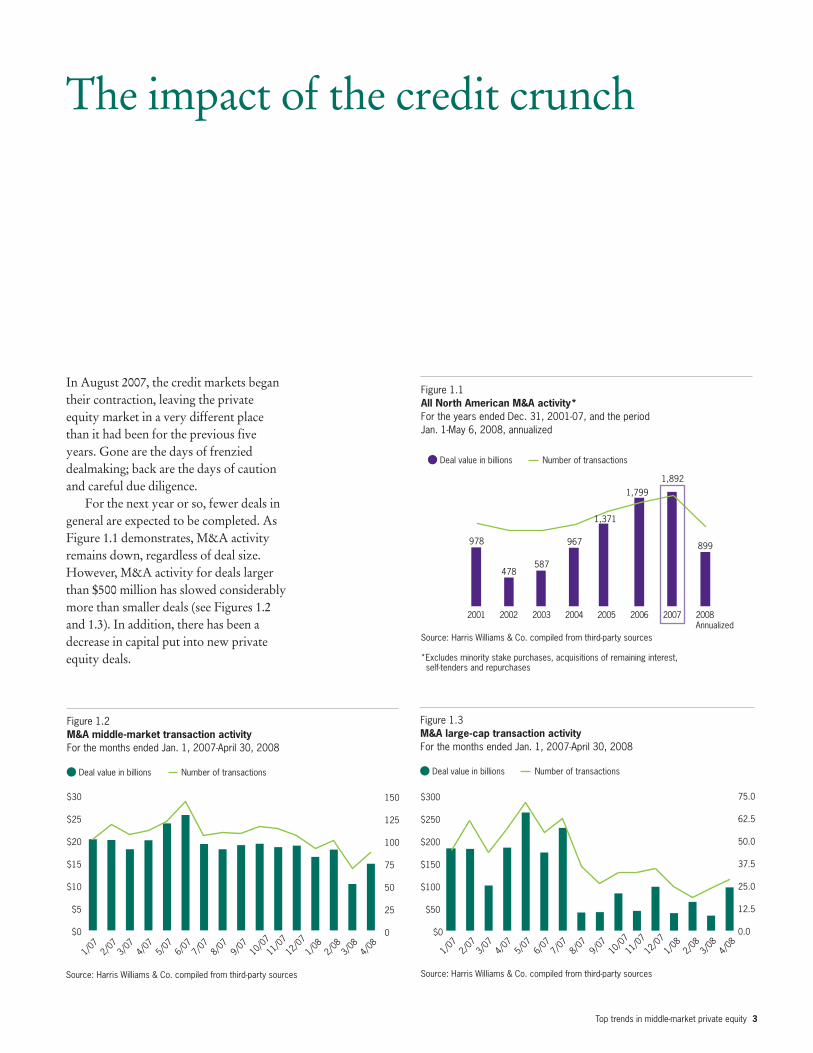

In August 2007, the credit markets begantheir contraction, leaving the privateequity market in a very different placethan it had been for the previous fiveyears. Gone are the days of frenzieddealmaking; back are the days of cautionand careful due diligence.

For the next year or so, fewer deals ingeneral are expected to be completed. AsFigure 1.1 demonstrates, M&A activityremains down, regardless of deal size.However, M&A activity for deals largerthan $500 million has slowed considerablymore than smaller deals (see Figures 1.2and 1.3). In addition, there has been adecrease in capital put into new privateequity deals.

Figure 1.1All North American M&A activity* For the years ended Dec. 31, 2001-07, and the periodJan. 1-May 6, 2008, annualized

Source: Harris Williams & Co. compiled from third-party sources

*Excludes minority stake purchases, acquisitions of remaining interest, self-tenders and repurchases

2001 2002 2003 2004 2005 2006 2007 2008Annualized

Deal value in billions Number of transactions

978

478 587

967

1,371

1,799

1,892

899

Figure 1.2M&A middle-market transaction activity For the months ended Jan. 1, 2007-April 30, 2008

Source: Harris Williams & Co. compiled from third-party sources

$0

$5

$10

$15

$20

$25

$30

Deal value in billions Number of transactions

0

25

50

75

100

125

150

1/07

2/07

3/07

4/07

5/07

6/07

7/07

8/07

9/07

10/0

711

/07

12/0

71/

082/

083/

084/

08

Figure 1.3M&A large-cap transaction activity For the months ended Jan. 1, 2007-April 30, 2008

Source: Harris Williams & Co. compiled from third-party sources

$0

$50

$100

$150

$200

$250

$300

Deal value in billions Number of transactions

0.0

12.5

25.0

37.5

50.0

62.5

75.0

1/07

2/07

3/07

4/07

5/07

6/07

7/07

8/07

9/07

10/0

711

/07

12/0

71/

082/

083/

084/

08

4 Top trends in middle-market private equity

While private equity deals smallerthan $750 million experienced a less sharpdecline in the number of deals than thelarger-size deals market, total deal volumeis down from a year ago (see Figures 1.4and 1.5). Overall in 2007, private equityfirms put $474.8 billion of capital intoU.S. deals, marking the third straight yearof record volume. For the first half of2008, a paltry $63.2 billion of U.S. dealvolume was recorded (see Figure 1.6).

“It’s still a good time for cleancompanies to sell in the middle market,”says Mark Jones, a partner with RiverAssociates Investments LLC. “If thecompanies are of real quality, the debtsources are there. In fact, it’s a good timefor traditional debt players, as well. It’sless competitive for them without all theCLOs [collateralized loan obligations]and BDCs [business developmentcompanies] that private equity firms wereusing. Mezz guys [mezzanine investors]are a lot busier and getting involved inlarger transactions these days, but at verysafe multiples. There are opportunities inthe middle and lower ends of the market.”

Even though middle-market firms arebest at weathering the storm, dealprofessionals are certainly feeling lessoptimistic. According to the December2007 ACG/Thomson Financial survey,dealmaking professionals were lessoptimistic about the strength of the M&Amarket at the end of 2007 than they wereearlier at midyear 2007. Thirty-eightpercent of survey respondents rightlyexpected transaction levels to drop in2008. That was more than double thenumber of respondents who in August2007 thought levels would drop at thesame time last year. To be fair, last year’ssurvey was taken when dealmakers werestill in a hot M&A market and the drop-off had not yet hit, whereas the May 2008ACG/Thomson Reuters survey was takenas we continue to be, arguably, in theworst of it.

Most of the decrease in activity hascome from the large market. As a result oflarge-market firms’ inability to access debtto complete megadeals, many of themhave moved downstream. However, notall mega-firms are taking the sameapproach. For example, The CarlyleGroup partnered with J.H. Whitney &Co., a middle-market buyout firm, to buyDallas-based Authentix, which developsand delivers authentication and brandprotection devices. Financial terms were

not disclosed, but the Dealmakerestimates the price tag to be a bit over$100 million, which pales in comparisonto Carlyle’s $6.3 billion Manor Care deallast year. The Authentix deal wascompleted using capital from its CarlyleU.S. Growth Capital fund, while theManor Care deal was completed using thefirm’s main buyout fund. This wouldseem to indicate that Carlyle has beenfocusing more on its growth buyoutpractice rather than its large buyout fundfor which it is more widely known.

Other large private equity firms havedecided to raise dedicated middle-marketfunds for the first time. At the beginningof the year, TPG Capital raised $1.2billion to invest in middle-marketbuyouts. And in April, Silver Lake held afinal closing of Silver Lake Sumeru, itsinaugural middle-market investment fund,with $1.1 billion of equity capitalcommitments.

“Getting out of your comfort zone isa formula for disaster,” says Jay Jester, amanaging director with Audax Group. “A couple of the megafunds will put somedollars to work on smaller deals, butwhen the market comes back, they willleave. I prefer to focus on the 300 to 400formidable middle-market firms thatreally present competition.”

With larger competitors moving intotheir turf, a flight to quality and harder-to-come-by debt (see Figure 1.7), middle-market dealmakers are feeling pinched.

Figure 1.4Private equity volumefor deals less than$750M

2000 179 $20.12001 84 5.32002 75 6.82003 82 7.92004 110 15.92005 137 24.82006 153 24.62007 140 25.42008 50 6.9

Source: Thomson Reuters

Figure 1.5Private equity volumefor deals larger than$750M

2000 13 $ 19.82001 5 6.22002 11 21.92003 8 13.52004 31 56.72005 29 87.52006 66 349.12007 53 289.32008 9 13.9

Source: Thomson Reuters

Figure 1.6Private equity deals completed and fundsraised through June 13, 2008

2007 2008

Dealscompleted

Buyout fundsraised

Source: Thomson Reuters

$474.863.2

$292.2133.6

Billions

Figure 1.7Average leverage as a multiple of EBITDA for middle-market LBO dealsFor the years ended Dec. 31, 2001-07 and Q1 2008

Source: S&P Leveraged Loan Review

2001 2002 2003 2004 2005 2006 2007 2008

7-year average: 4.3x

3.4x

3.8x 3.8x4.7x

4.3x 4.7x 4.5x

5.6x

Total debt

No. of Valuedeals (millions)

No. of Valuedeals (millions)

Top trends in middle-market private equity 5

Some private equity firms have settheir sights on smaller deals, as well. InApril, Norwest Equity Partners boughtShock Doctor, a sports protectionequipment company. The property wasacquired exclusively with equity providedby Norwest and the management team.The price tag was below what Norwestusually pays for a deal, making it possibleto get the deal done debt free.

The type of debt available for deals hasalso changed radically over the past year.There’s been an enormous contraction inthe pool of debt buyers for new issuances,particularly among collateralized debt andloan obligations. According to Standard& Poor’s, in the first half of 2008,collateralized debt obligations (CDOs)fell for the first time since 2004. What’smore, Lehman Brothers estimated therewould be only $30 billion to $35 billion innew CLOs issued in 2008 — a 60 percentdrop from 2007 levels.

As of April 2008, the number of U.S.CDO managers on the league tables,which include CLO issuance, was small,with only five banks issuing deals,according to Thomson Reuters(see Figure 1.8).

BDCs appear to be out of favor.Depressed valuations of publicly tradedBDCs, which were once a strong sourceof debt financing for middle-leveragedbuyouts (LBOs), are also gone (see Figure 1.9).

By the end of May 2008, almost everysingle BDC was trading below its bookvalue as investors anticipated write-downs(see Figure 1.10), according to an index ofBDCs compiled by analysts at investmentbank Stifel Nicolaus. A depressed stockprice makes it difficult for BDCs tooriginate new loans, drying up moreliquidity in the middle-market debt arena.

At the same time that BDCs startedon a downward spiral, the FinancialAccounting Standards Board (FASB)implemented the fair value accountingrule FASB 157, which requires the BDCsto set the value of their private portfoliocompanies to fair value based on publicmarket data or other market comparables.Many private firms are anticipating write-downs as a result of the poor performanceof BDCs due in part to the impact ofFASB 157.

Figure 1.8Collateralized debt obligations for Q2 2008

Citigroup Global 38% 5 $2.3Morgan Stanley 21% 3 1.3JPMorgan Securities 21% 3 1.2Barclays Capital 10% 1 .608Lehman Brothers 10% 2 .605

Source: Bank Loan Report/Thomson Reuters

Name Market No. of Totalshare deals issuance

(billions)

Figure 1.9SF BDC price index two-year performanceAs of May 30, 2008

7/28

/06

Source: Factset

110

120

130

140

150

160

170

180

190

200

10/0

6/06

2/23

/07

12/1

5/06

5/04

/07

7/13

/07

10/0

5/07

12/1

4/07

5/16

/08

2/22

/08

Millions

Figure 1.10Performance of top four BDCs from January to May 2008

BDCs ~500+ million market capALD Allied Capital -21% -17% -44% -21% 6% -10% -20%ACAS American Capital -5% -15% -29% 10% 73% -12% -6%AINV Apollo Investment Management 2% 17% -18% 32% - 9% 4%ARCC Ares Capital Corp. 1% -8% -26% -10% - -5% -15%

Source: Stifel Nicolous

Total return 1 2 1 3 5 QTD YTD(millions) month month year year year

6 Top trends in middle-market private equity

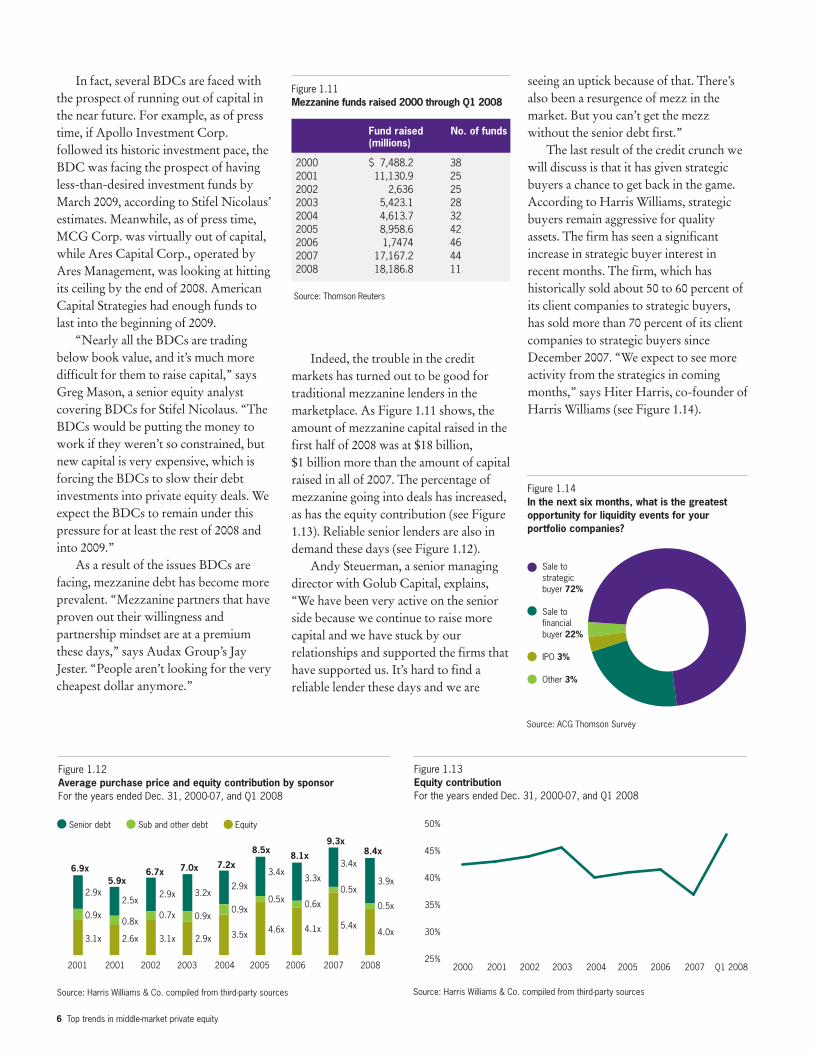

In fact, several BDCs are faced withthe prospect of running out of capital inthe near future. For example, as of presstime, if Apollo Investment Corp.followed its historic investment pace, theBDC was facing the prospect of havingless-than-desired investment funds byMarch 2009, according to Stifel Nicolaus’estimates. Meanwhile, as of press time,MCG Corp. was virtually out of capital,while Ares Capital Corp., operated byAres Management, was looking at hittingits ceiling by the end of 2008. AmericanCapital Strategies had enough funds tolast into the beginning of 2009.

“Nearly all the BDCs are tradingbelow book value, and it’s much moredifficult for them to raise capital,” saysGreg Mason, a senior equity analystcovering BDCs for Stifel Nicolaus. “TheBDCs would be putting the money towork if they weren’t so constrained, butnew capital is very expensive, which isforcing the BDCs to slow their debtinvestments into private equity deals. Weexpect the BDCs to remain under thispressure for at least the rest of 2008 andinto 2009.”

As a result of the issues BDCs arefacing, mezzanine debt has become moreprevalent. “Mezzanine partners that haveproven out their willingness andpartnership mindset are at a premiumthese days,” says Audax Group’s JayJester. “People aren’t looking for the verycheapest dollar anymore.”

Indeed, the trouble in the creditmarkets has turned out to be good fortraditional mezzanine lenders in themarketplace. As Figure 1.11 shows, theamount of mezzanine capital raised in thefirst half of 2008 was at $18 billion, $1 billion more than the amount of capitalraised in all of 2007. The percentage ofmezzanine going into deals has increased,as has the equity contribution (see Figure1.13). Reliable senior lenders are also indemand these days (see Figure 1.12).

Andy Steuerman, a senior managingdirector with Golub Capital, explains,“We have been very active on the seniorside because we continue to raise morecapital and we have stuck by ourrelationships and supported the firms thathave supported us. It’s hard to find areliable lender these days and we are

seeing an uptick because of that. There’salso been a resurgence of mezz in themarket. But you can’t get the mezzwithout the senior debt first.”

The last result of the credit crunch wewill discuss is that it has given strategicbuyers a chance to get back in the game.According to Harris Williams, strategicbuyers remain aggressive for qualityassets. The firm has seen a significantincrease in strategic buyer interest inrecent months. The firm, which hashistorically sold about 50 to 60 percent ofits client companies to strategic buyers,has sold more than 70 percent of its clientcompanies to strategic buyers sinceDecember 2007. “We expect to see moreactivity from the strategics in comingmonths,” says Hiter Harris, co-founder ofHarris Williams (see Figure 1.14).

Figure 1.11Mezzanine funds raised 2000 through Q1 2008

2000 $ 7,488.2 38 2001 11,130.9 25 2002 2,636 25 2003 5,423.1 28 2004 4,613.7 32 2005 8,958.6 42 2006 1,7474 46 2007 17,167.2 44 2008 18,186.8 11

Source: Thomson Reuters

Fund raised No. of funds(millions)

Figure 1.14In the next six months, what is the greatestopportunity for liquidity events for yourportfolio companies?

Source: ACG Thomson Survey

Sale tostrategicbuyer 72%

Sale tofinancialbuyer 22%

IPO 3%

Other 3%

Figure 1.13Equity contributionFor the years ended Dec. 31, 2000-07, and Q1 2008

Source: Harris Williams & Co. compiled from third-party sources

25%

30%

35%

40%

45%

50%

2000 2001 2002 2003 2004 2005 2006 2007 Q1 2008

Figure 1.12Average purchase price and equity contribution by sponsorFor the years ended Dec. 31, 2000-07, and Q1 2008

2001 2002 2003 2004 2005 2006 2007 2008

6.9x5.9x

6.7x7.2x7.0x

8.5x9.3x

8.1x

Senior debt Sub and other debt Equity

2001

8.4x

2.9x

0.9x

3.1x

2.5x

0.8x

2.6x

3.2x

0.9x

2.9x

2.9x

0.7x

3.1x

2.9x

0.9x

3.5x

3.4x

0.5x

4.6x

3.3x

0.6x

4.1x

3.4x

0.5x

5.4x

3.9x

0.5x

4.0x

Source: Harris Williams & Co. compiled from third-party sources

Top trends in middle-market private equity 7

The explosion of cross-border activity

Cross-border M&A has become anincreasingly vital part of strategic plans formiddle-market companies and privateequity firms. Large U.S.-based privateequity firms have already proven thatdoing business in different parts of theworld often equates to success in today’srapidly growing global economy. Reasonsto go global include the need forgeographic diversification, the availabilityof good acquisition candidates in placesoutside the United States, the need tooutsource divisions of portfoliocompanies to places where there arecheaper labor costs, and the continuedconsumer growth in emerging markets.

Going global is not new. Large-marketU.S.-based private equity firms startedopening up offices overseas to pursueopportunities in the late 1990s. Today, thefive largest private equity firms cover theworld with offices (see Figures 2.1). U.S.middle-market firms have taken this cueand have also started expanding globally(see Figure 2.2).

Figure 2.1Office locations of the five largest private equity firms

Figure 2.2Office locations of the five largest middle-market private equity firms

Firms representedThe Carlyle GroupWarburg PincusThe Blackstone GroupKKRBain Capital

Firms representedTA AssociatesSun Capital PartnersAmerican Capital StrategiesAdvent InternationalRiverside & Co.

●

●

● ● ●●

●●

● ●

●

●

●

● ●● ●

●

●

●

● ●

● ●

●

● ●

●●● ●

●●●

●

● ●

●●●●

●●●

●●

●

●

●●

●

●

●●

Cross-border M&A has become an increasingly vital partof strategic plans for middle-market companies and privateequity firms.

8 Top trends in middle-market private equity

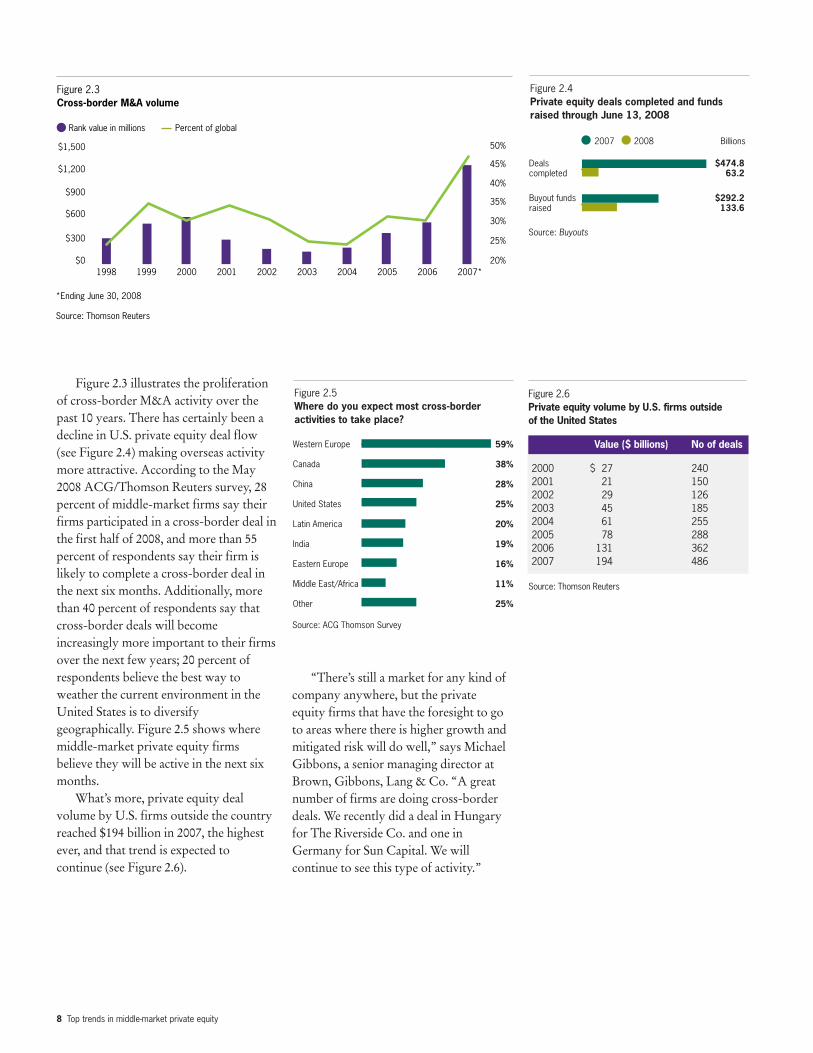

Figure 2.3 illustrates the proliferationof cross-border M&A activity over thepast 10 years. There has certainly been adecline in U.S. private equity deal flow(see Figure 2.4) making overseas activitymore attractive. According to the May2008 ACG/Thomson Reuters survey, 28percent of middle-market firms say theirfirms participated in a cross-border deal inthe first half of 2008, and more than 55percent of respondents say their firm islikely to complete a cross-border deal inthe next six months. Additionally, morethan 40 percent of respondents say thatcross-border deals will becomeincreasingly more important to their firmsover the next few years; 20 percent ofrespondents believe the best way toweather the current environment in theUnited States is to diversifygeographically. Figure 2.5 shows wheremiddle-market private equity firmsbelieve they will be active in the next sixmonths.

What’s more, private equity dealvolume by U.S. firms outside the countryreached $194 billion in 2007, the highestever, and that trend is expected tocontinue (see Figure 2.6).

“There’s still a market for any kind ofcompany anywhere, but the privateequity firms that have the foresight to goto areas where there is higher growth andmitigated risk will do well,” says MichaelGibbons, a senior managing director atBrown, Gibbons, Lang & Co. “A greatnumber of firms are doing cross-borderdeals. We recently did a deal in Hungaryfor The Riverside Co. and one inGermany for Sun Capital. We willcontinue to see this type of activity.”

Figure 2.3Cross-border M&A volume

*Ending June 30, 2008

Source: Thomson Reuters

Rank value in millions Percent of global

2001 2002 2003 2004 2005 2006 2007*1998 1999 2000

$1,500

$1,200

$900

$600

$300

$0 20%

25%

30%

35%

40%

45%

50%

Figure 2.4Private equity deals completed and fundsraised through June 13, 2008

2007 2008

Dealscompleted

Buyout fundsraised

Source: Buyouts

$474.863.2

$292.2133.6

Billions

Figure 2.5Where do you expect most cross-border activities to take place?

Source: ACG Thomson Survey

59%

38%

28%

25%

20%

19%

16%

11%

25%

Western Europe

Canada

China

United States

Latin America

India

Eastern Europe

Middle East/Africa

Other

Figure 2.6Private equity volume by U.S. firms outside of the United States

Value ($ billions) No of deals

2000 $ 27 2402001 21 1502002 29 1262003 45 1852004 61 2552005 78 2882006 131 3622007 194 486

Source: Thomson Reuters

Top trends in middle-market private equity 9

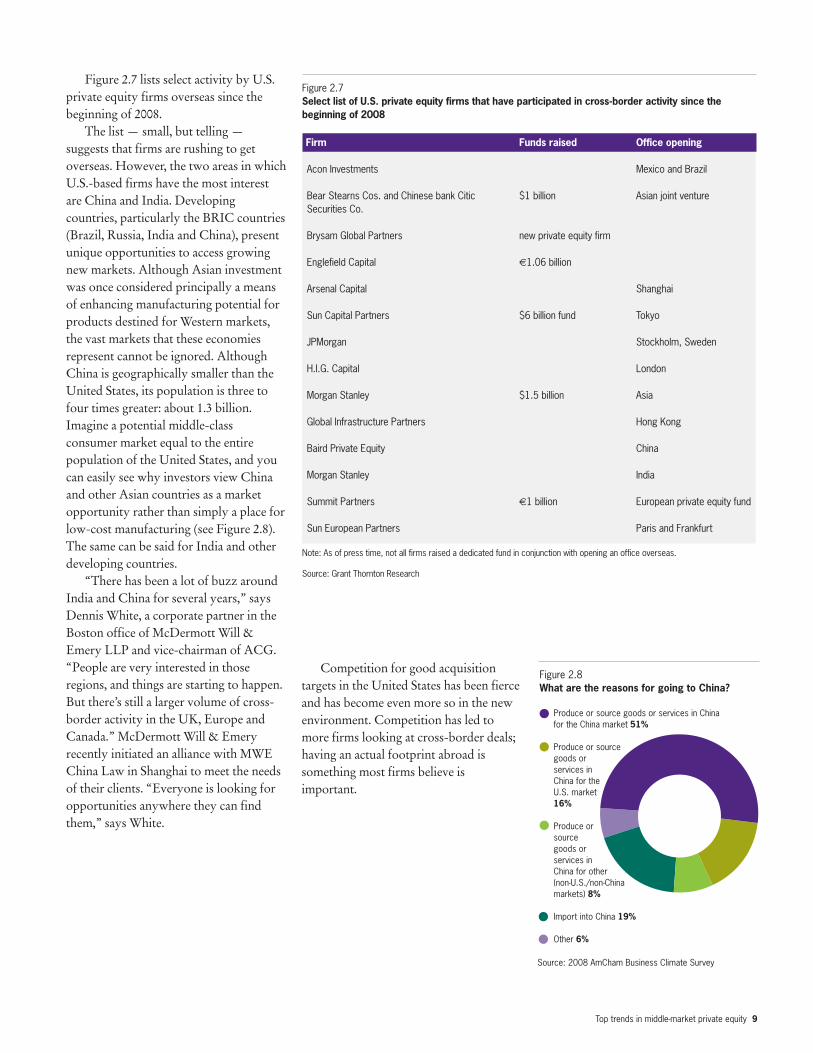

Figure 2.7 lists select activity by U.S.private equity firms overseas since thebeginning of 2008.

The list — small, but telling —suggests that firms are rushing to getoverseas. However, the two areas in whichU.S.-based firms have the most interestare China and India. Developingcountries, particularly the BRIC countries(Brazil, Russia, India and China), presentunique opportunities to access growingnew markets. Although Asian investmentwas once considered principally a meansof enhancing manufacturing potential forproducts destined for Western markets,the vast markets that these economiesrepresent cannot be ignored. AlthoughChina is geographically smaller than theUnited States, its population is three tofour times greater: about 1.3 billion.Imagine a potential middle-classconsumer market equal to the entirepopulation of the United States, and youcan easily see why investors view Chinaand other Asian countries as a marketopportunity rather than simply a place forlow-cost manufacturing (see Figure 2.8).The same can be said for India and otherdeveloping countries.

“There has been a lot of buzz aroundIndia and China for several years,” saysDennis White, a corporate partner in theBoston office of McDermott Will &Emery LLP and vice-chairman of ACG.“People are very interested in thoseregions, and things are starting to happen.But there’s still a larger volume of cross-border activity in the UK, Europe andCanada.” McDermott Will & Emeryrecently initiated an alliance with MWEChina Law in Shanghai to meet the needsof their clients. “Everyone is looking foropportunities anywhere they can findthem,” says White.

Competition for good acquisitiontargets in the United States has been fierceand has become even more so in the newenvironment. Competition has led tomore firms looking at cross-border deals;having an actual footprint abroad issomething most firms believe isimportant.

Figure 2.8What are the reasons for going to China?

Source: 2008 AmCham Business Climate Survey

Produce or source goods or services in Chinafor the China market 51%

Produce or sourcegoods orservices inChina for theU.S. market16%

Produce orsourcegoods orservices inChina for other(non-U.S./non-Chinamarkets) 8%

Import into China 19%

Other 6%

Figure 2.7Select list of U.S. private equity firms that have participated in cross-border activity since thebeginning of 2008

Firm Funds raised Office opening

Acon Investments Mexico and Brazil

Bear Stearns Cos. and Chinese bank Citic $1 billion Asian joint ventureSecurities Co.

Brysam Global Partners new private equity firm

Englefield Capital €1.06 billion

Arsenal Capital Shanghai

Sun Capital Partners $6 billion fund Tokyo

JPMorgan Stockholm, Sweden

H.I.G. Capital London

Morgan Stanley $1.5 billion Asia

Global Infrastructure Partners Hong Kong

Baird Private Equity China

Morgan Stanley India

Summit Partners €1 billion European private equity fund

Sun European Partners Paris and Frankfurt

Note: As of press time, not all firms raised a dedicated fund in conjunction with opening an office overseas.

Source: Grant Thornton Research

10 Top trends in middle-market private equity

Best practices“There’s an invaluable benefit of having alocal presence,” says Steve Collins, amanaging director with AdventInternational. “It’s hard enough to get adeal done in a country where you knowthe local customs and laws — forget abouta foreign country. Not all markets need alocal presence, but most do.”

White agrees. “It’s easier to do deals inthe UK than in China,” he says. “Thereare varying degrees of a presence needed.Having a presence on the ground andrelationships with local banks and firmscan make all the difference. The customsand cultural issues can make a bigdifference in getting a deal done.”

The opportunity available indeveloping regions is not just for U.S.private equity firms. In the past year,many European-based firms have alsomoved into the growing territories.

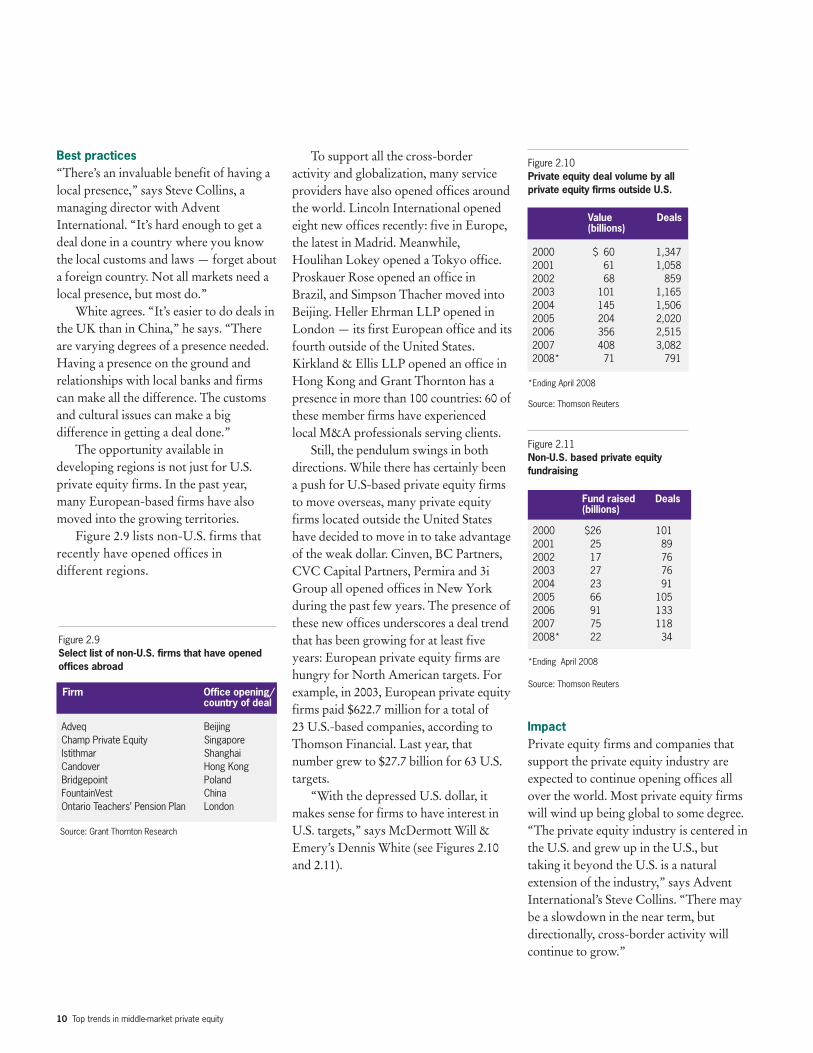

Figure 2.9 lists non-U.S. firms thatrecently have opened offices indifferent regions.

To support all the cross-borderactivity and globalization, many serviceproviders have also opened offices aroundthe world. Lincoln International openedeight new offices recently: five in Europe,the latest in Madrid. Meanwhile,Houlihan Lokey opened a Tokyo office.Proskauer Rose opened an office inBrazil, and Simpson Thacher moved intoBeijing. Heller Ehrman LLP opened inLondon — its first European office and itsfourth outside of the United States.Kirkland & Ellis LLP opened an office inHong Kong and Grant Thornton has apresence in more than 100 countries: 60 ofthese member firms have experiencedlocal M&A professionals serving clients.

Still, the pendulum swings in bothdirections. While there has certainly beena push for U.S-based private equity firmsto move overseas, many private equityfirms located outside the United Stateshave decided to move in to take advantageof the weak dollar. Cinven, BC Partners,CVC Capital Partners, Permira and 3iGroup all opened offices in New Yorkduring the past few years. The presence ofthese new offices underscores a deal trendthat has been growing for at least fiveyears: European private equity firms arehungry for North American targets. Forexample, in 2003, European private equityfirms paid $622.7 million for a total of 23 U.S.-based companies, according toThomson Financial. Last year, thatnumber grew to $27.7 billion for 63 U.S.targets.

“With the depressed U.S. dollar, itmakes sense for firms to have interest inU.S. targets,” says McDermott Will &Emery’s Dennis White (see Figures 2.10and 2.11).

ImpactPrivate equity firms and companies thatsupport the private equity industry areexpected to continue opening offices allover the world. Most private equity firmswill wind up being global to some degree. “The private equity industry is centered inthe U.S. and grew up in the U.S., buttaking it beyond the U.S. is a naturalextension of the industry,” says AdventInternational’s Steve Collins. “There maybe a slowdown in the near term, butdirectionally, cross-border activity willcontinue to grow.”

Figure 2.9Select list of non-U.S. firms that have openedoffices abroad

Firm Office opening/country of deal

Adveq BeijingChamp Private Equity SingaporeIstithmar ShanghaiCandover Hong KongBridgepoint PolandFountainVest ChinaOntario Teachers’ Pension Plan London

Source: Grant Thornton Research

Figure 2.10Private equity deal volume by allprivate equity firms outside U.S.

Value Deals(billions)

2000 $ 60 1,3472001 61 1,0582002 68 8592003 101 1,1652004 145 1,5062005 204 2,0202006 356 2,5152007 408 3,0822008* 71 791

*Ending April 2008

Source: Thomson Reuters

Figure 2.11Non-U.S. based private equityfundraising

Fund raised Deals(billions)

2000 $26 1012001 25 892002 17 762003 27 762004 23 912005 66 1052006 91 1332007 75 1182008* 22 34

*Ending April 2008

Source: Thomson Reuters

Top trends in middle-market private equity 11

The proliferation of operationalpartners

Twenty-two percent of respondents to theMay 2008 ACG/Thomson Reuters surveycite strategic investors as one of thegreatest impediments to dealmakingtoday. Increased competition fromstrategics, coupled with the proliferationof private equity firms, have made wooingmanagement teams into a sale morechallenging than ever, especially for teamsthat plan on participating after thebuyout. Over the past couple of years, ithas become more common for privateequity firms to hire operational partnersin hopes of gaining a competitive edge.According to the ACG/Thomson Reuterssurvey, about 80 percent of respondentsbelieve there has been an increase in thenumber of private equity firms hiringoperational partners. While these partnersare not hired for their expertise withprivate equity, firms expect them to haveexpansive knowledge of the sector theyworked in and be able to deliver addedvalue to their portfolio companies.

When Lincolnshire Managementdecided to hire James Binch as a senioroperating partner and managing director,the New York-based firm was looking forsomeone who was a capable fixer ofcompanies. After being a seller in themarketplace until mid-2008, Lincolnshiredecided it was time to become a buyeragain; and having someone to helpimprove the performance of portfoliocompanies made perfect sense. Prior tojoining Lincolnshire, Binch was presidentand CEO of medical componentmanufacturer Memry Corporation(AMEX: MRY). “What better person tohire than someone who has on-the-ground experience,” says Bill Buttrick,communications director at Lincolnshire.“It’s not primarily the sector experiencewe’re interested in. Rather, we look for amanager who is capable of getting on theground and figuring out what’s going onat a portfolio company quickly.”

Lincolnshire is just one such firm thathas hired an operating partner lately. SeeFigure 3.0 for recent examples of otherfirms that have hired operating partners.

From the largest private equity shopslike Bain Capital to the mid-market oneslike Industrial Growth Partners, firms areincreasingly finding operations peopleinvaluable to their teams.

“A lot of firms are adapting anoperating partner model,” says BrianKorb, partner with Glocap, a privateequity recruitment firm. “And notsurprising, we have definitely seen anincrease in the hiring of these types ofindividuals. These partners come withadditional credibility and a network thatcan add value in a number of ways. Theycan help with deal flow, apply bestpractices across portfolio operations and,when necessary, they can even parachutein and run them.”

Another reason for the proliferationof operational partners is the need forprivate equity firms to really showcasetheir capabilities to sellers, especially inthis environment. Many dealmakersbelieve that an operating partner givesthem the edge (see Figures 3.1 and 3.2).

“No matter how good an idea aprivate equity professional has, themanagement team looks at a 40-yearveteran’s ideas differently because theyhave sat in the same chair,” says TimDeVries, managing general partner atNorwest Equity Partners.

Many dealmakers believethat an operating partnergives them the edge.

12 Top trends in middle-market private equity

Lincolnshire’s Bill Buttrick explains,“It makes sense to have an operationalpartner. A private equity company mayown 15 portfolio companies and half mayrun into the occasional trouble. You wantthe ability to air-drop someone in whocan work with current management or ina worst case scenario, replace them if

necessary. And it helps to have anoperational partner when you are tryingto buy a company. When there’s someonefrom your group who can prove theyhave experience, management teamsappreciate that, and it adds to the chancesof working with them.”

Additionally, operational partners cancut to the chase, getting a job donequicker and with less trouble. “Firmsrealize that to stay competitive in thiscurrent environment, they need to extractmaximum value from their investments.They can hire outside consultants, but itpays off to have tactical in-house advisorsyou can also turn to,” says Glocap’s BrianKorb. “You can justify paying someone$1 million a year if they are saving you$10 million.”

Impact Private equity firms will continue to hireMBA students and investment bankers,but they will increasingly seek outveteran operational partners. They willcontinue to hire any professionals whomay make them more competitive, even ifit’s outside of what was once consideredthe normal realm.

“If an operational partner can make a5 percent to 10 percent impact on one ofour businesses, that puts us at a hugeadvantage,” says Norwest’s Tim DeVries.“Private equity has maturedtremendously, and we all have to do abetter job. Every increment helps. Someoperational partners help us with contactsor give CEOs advice or set a great team inplace. All of those things help us performsuperiorly.”

Advent International Pam Patsley First Data Corp. Financial services operating partnersArcapita William Miller Boston Consulting Group Strategic performanceArsenal Capital Partners Larry Resnick M&A Executive, Triumph Group Aerospace and defenseArsenal Capital Partners Anthony Giorgio Corporate Development, SYMYX Technology Specialty chemical and materialsBlue Point Capital Thomas Cresante CEO Special DevicesBlue Wolf Capital Van Walbridge CEO of Mobile Tool InternationalBlue Wolf Capital Walter Stasik CEO of Genesis Worldwide IICalera Capital Paul Walsh EFund Corp. Business and financial servicesCalera Capital Clyde Thomas eFunds Corp. Business and financial servicesCalera Capital (Fremont Partners) Michael Murray Head of I-bank with Bank of AmericaCCMP Capital John Bowlin Kraft Foods Consumer investmentsCCMP Capital Denny Shelton CEO of Triad Hospitals Health care investmentsDLJ Merchant Banking Neal Pomroy MD with Mercer Management Head of portfolio strategyDoughty Hanson & Co. Adam Black Associate Director KMPG Oversee sustainability mattersFidelity Equity Partners Gray Hall CEO of CeriCenter Inc.Genstar Capital Paul Clark CEO of ICOS Corp. Biotech investmentsMorgan Stanley James Howland President of Dun & BradstreetNatural Gas Partners Jack Holmes Syntroleum Corp. Deal generationNavigation Capital Partners O.G. Greene CEO of Burroughs Corp., National Data Corp.Norwest Equity Partners Jeffrey Greiner Founder of Wessels, Arnold & Henderson Technology add-onsPegasus Capital Advisors Steven Marton President of office products at Newell RubbermaidProvidence Equity Partners Barry Allen VP of operations at Qwest CommunicationsWater Street Healthcare Partners Curt Selquist Johnson & JohnsonWelsh Carson Anderson & Stowe Stephen Larned Chief Marketing Officer DigitalGlobeWelsh Carson Anderson & Stowe Daniel Lieber CEO of Union Site ManagementWL Ross & Co. John Kanas CEO of North Fork Bank Distressed financial services opportunities

Source: Grant Thornton Research

Figure 3.1Select list of U.S. operating partners hired from January to June 2008

Private equity firm New hire Previous position Private equity focus

Figure 3.2Does having operational partners giveprivate equity firms an edge when looking forinvestments?

Source: ACG Thomson Survey

Yes, itdemonstratesknowledgeandexperiencein certainmarkets79%

No, itdoesn’t reallymake adifference 21%

Top trends in middle-market private equity 13

The emergence of sovereignwealth funds

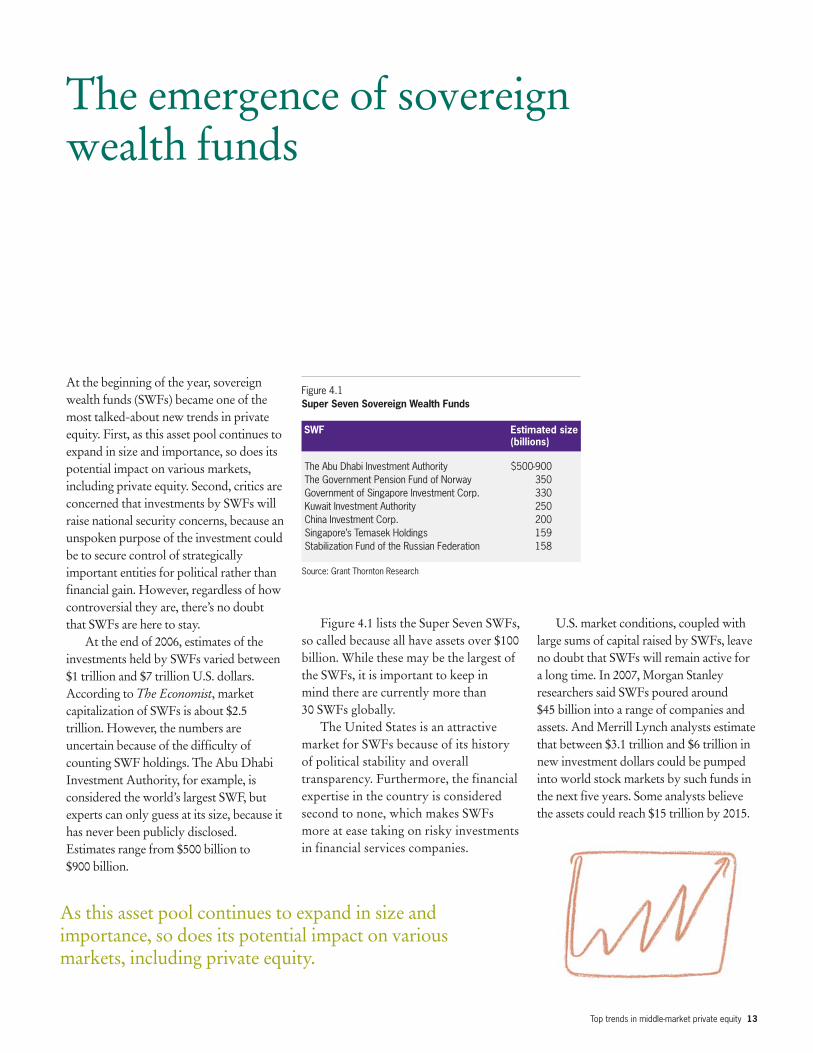

At the beginning of the year, sovereignwealth funds (SWFs) became one of themost talked-about new trends in privateequity. First, as this asset pool continues toexpand in size and importance, so does itspotential impact on various markets,including private equity. Second, critics areconcerned that investments by SWFs willraise national security concerns, because anunspoken purpose of the investment couldbe to secure control of strategicallyimportant entities for political rather thanfinancial gain. However, regardless of howcontroversial they are, there’s no doubtthat SWFs are here to stay.

At the end of 2006, estimates of theinvestments held by SWFs varied between$1 trillion and $7 trillion U.S. dollars.According to The Economist, marketcapitalization of SWFs is about $2.5trillion. However, the numbers areuncertain because of the difficulty ofcounting SWF holdings. The Abu DhabiInvestment Authority, for example, isconsidered the world’s largest SWF, butexperts can only guess at its size, because ithas never been publicly disclosed.Estimates range from $500 billion to $900 billion.

Figure 4.1 lists the Super Seven SWFs,so called because all have assets over $100billion. While these may be the largest ofthe SWFs, it is important to keep inmind there are currently more than 30 SWFs globally.

The United States is an attractivemarket for SWFs because of its historyof political stability and overalltransparency. Furthermore, the financialexpertise in the country is consideredsecond to none, which makes SWFsmore at ease taking on risky investmentsin financial services companies.

U.S. market conditions, coupled withlarge sums of capital raised by SWFs, leaveno doubt that SWFs will remain active fora long time. In 2007, Morgan Stanleyresearchers said SWFs poured around $45 billion into a range of companies andassets. And Merrill Lynch analysts estimatethat between $3.1 trillion and $6 trillion innew investment dollars could be pumpedinto world stock markets by such funds inthe next five years. Some analysts believethe assets could reach $15 trillion by 2015.

As this asset pool continues to expand in size andimportance, so does its potential impact on various markets, including private equity.

SWF Estimated size(billions)

The Abu Dhabi Investment Authority $500-900The Government Pension Fund of Norway 350Government of Singapore Investment Corp. 330Kuwait Investment Authority 250China Investment Corp. 200Singapore’s Temasek Holdings 159Stabilization Fund of the Russian Federation 158

Source: Grant Thornton Research

Figure 4.1Super Seven Sovereign Wealth Funds

14 Top trends in middle-market private equity

Figure 4.2 shows recent examples ofSWFs making their way into the U.S.economy in general and into private equityin particular.

SWFs raise concernsIt is important to note that most of theSWFs do not have board seats at privateequity firms, yet there is still uneasinessabout their participating in the U.S. privateequity market. Americans accept foreigninvestment to a certain degree, especially ifit adds up to more jobs for Americans. Forexample, no one really complains aboutToyota producing cars in the United Statesor cell phone companies opening officesand sites in the country. Additionally, it’sawkward to complain when SWFs haveprovided cash infusions to credit-troubledU.S. banking institutions during the pastyear. But the public in general has concernsregarding foreign investors. The mostfamous example of this was the 2006uproar over the proposed purchase ofseveral U.S. ports by Dubai Ports World,which wound up pulling out of the deal inthe face of public controversy.

Despite public perception, the privateequity community largely sees SWFinvestments as beneficial. Speaking at aconference hosted by The Deal, GaryParr, vice chairman of Lazard, urged theaudience to think about what state U.S.banks would be in “if sovereign wealthfunds hadn’t been there to step in lastNovember. It would’ve been Bear Stearnsbut all over [Wall Street]. It would’ve been chaos.”

He continued, “We shouldn’t beprohibiting this money from coming in.When you look at the deals they havemade, there are so many constraints onthe sovereign wealth funds that there aremany ways to do this without a newbody of law.”

While monitoring SWFs is deemednecessary by most in the private equitybusiness, SWFs are believed to be fairlyharmless. “The risk isn’t as great as peopleare making it out to be,” says Dan Reid,national managing principal, TransactionAdvisory Services at Grant Thornton. “In fact, the risks are really no differentthan they are from any foreign investors.People really need to look at theseinvestments on a case-by-case basis.Believe it or not, there’s already a lot of

scrutiny being placed on these funds tomake sure everything is legitimate. If anSWF is one of many LPs [limited partners]in a $10 billion fund, how much control dothey really have? Perhaps not much.”

Nonetheless, the fear exists that theSWFs are working toward political gain.When a U.S. private equity firm buys alarge U.S. company, everyone knows it’sfor the money. The worry is that SWFsmight not be in it just for the money. Willthe Abu Dhabi Investment Authorityreally act like a limited partner if a privateequity firm is trying to buy a company thatsells an alternative to oil?

Another worry is experience or lackthereof. Just as many argued that hedgefunds didn’t have the sophistication andsticking power of private equity firms,some now wonder whether SWFs do.However, that concern doesn’t realisticallyseem to be the case. “These are notunsophisticated investors,” says Reid.“They didn’t just come into cash, anddecide to start investing it. SWFs havehired many experienced M&Aprofessionals, and many of the staff havebeen educated and trained in the UnitedStates. They are making smart financialdecisions.”

SWF Amount committed To whom

Mubadala Development Corp. $1.35B/7.5% stake The Carlyle GroupBeijing’s State Foreign Exchange Investment Co. $3B The Blackstone GroupThe Abu Dhabi Investment Authority $7.5B CitigroupSingapore’s Temasek Holdings $9.72B UBSAdu Dhabi Investment Authority 10% Apollo ManagementAdu Dhabi Investment Authority 5% Sony (SNE)Singapore’s Temasek Holdings $4.4 with an option to buy Merrill LynchChina Investment Corp. $5B/10% Morgan StanleyChina’s State Administration of Foreign Exchange $2.5B TPG

Source: Grant Thornton Research

Figure 4.2Recent activity of SWFs in the United States

Top trends in middle-market private equity 15

The early resultsWhile the end result of what will happen toSWFs investing in private equity is not yetknown, measures have already been taken:

• In early 2007, legislation wasintroduced in California to bar statepension funds from investing inprivate equity firms that are partlyowned by SWFs from countries withabusive human rights records.Although the bill never receivedsupport from Gov. ArnoldSchwarzenegger and was withdrawn,the fact that such legislation wasproposed represents a red flag forSWF investment in the United States.

• In October 2007, the ForeignInvestment and National SecurityAct of 2007 (FINSA) went intoeffect, broadening the president’s andthe executive branch’s ability tocontrol foreign investment in theUnited States.

• The European Union and the Bushadministration are backing an effortby the International Monetary Fundto develop a voluntary code of “bestpractices” for the funds.

• Peter Mandelson, the EuropeanUnion’s (EU) trade commissioner, hasspoken out against certain foreigninvestment opportunities, such asinvesting in defense contractors, bysovereign nations.

• In June 2008, Treasury SecretaryHenry Paulson worked to alleviateconcerns about SWFs. He told theaudience at the U.S.-U.A.E. BusinessCouncil in Abu Dhabi that the UnitedStates is open to investments fromSWFs. “As we seek to open newmarkets abroad, America will keep ourmarkets open at home to investmentfrom private firms and from sovereignwealth funds,” he says. “We rejectmeasures that would isolate us from theworld economy.”

However, lawmakers are stillconcerned about political motivations andwill fight against opening up the UnitedStates to the funds. As of publication ofthis white paper, lawmakers were alreadystarting to discuss the possibility oflimiting SWFs in the country.

“This will likely be a topic inWashington for quite some time,” saysGrant Thornton’s Dan Reid.

ImpactWhile it remains unclear what exactimpact SWFs will have on the privateequity community, there’s no doubt thatthey are here to stay and will be a drivingforce. To date, SWFs have investedprimarily in very large companies ormega-private equity firms. While theimpact on the middle market has beennegligible, that could change in thefuture. Just as many large state pensionfunds started investing in large privateequity firms before they decided to givethe middle market a try, the same couldhappen with SWFs and middle market.

“The opportunity is significant,” saysReid. “There’s a whole new spigot of cashflowing into private equity. Over timesovereign wealth funds will make more andmore direct investments but right nowthey are acting as LPs. The amount ofcapital they have is staggering.”

While it remains unclear what exact impact SWFs will have on the private equity community, there’s nodoubt that they are here to stay and will be a driving force.

16 Top trends in middle-market private equity

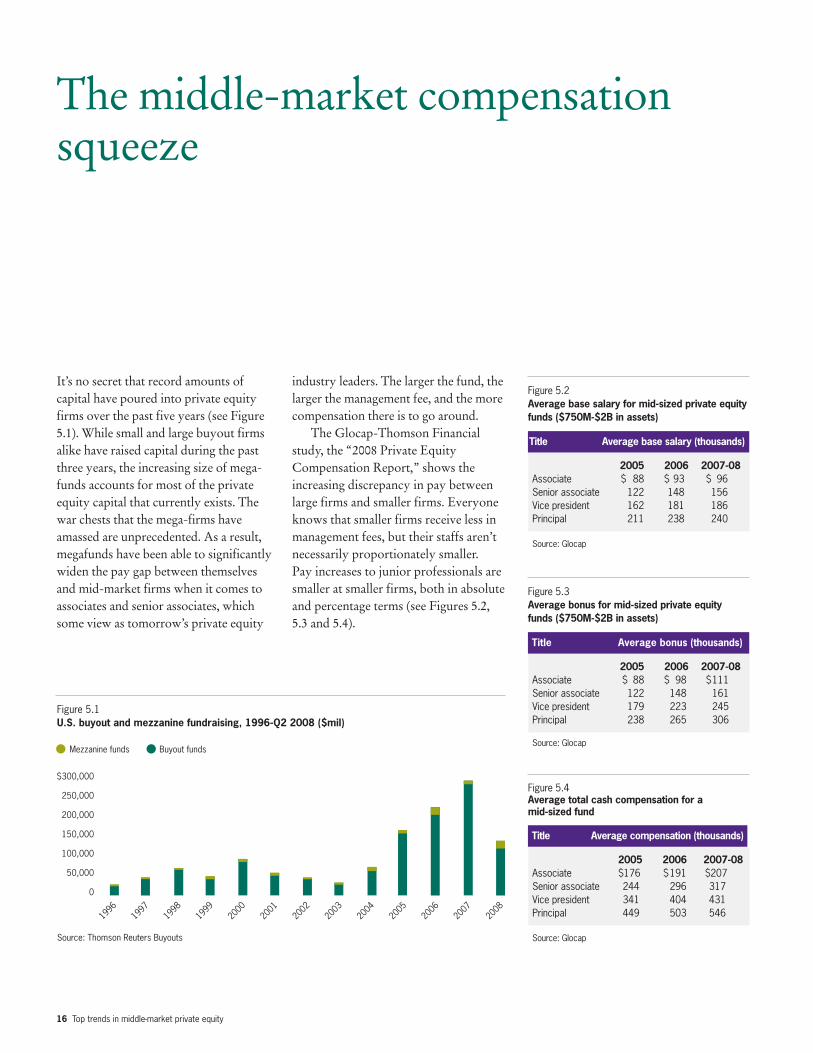

The middle-market compensationsqueeze

It’s no secret that record amounts ofcapital have poured into private equityfirms over the past five years (see Figure5.1). While small and large buyout firmsalike have raised capital during the pastthree years, the increasing size of mega-funds accounts for most of the privateequity capital that currently exists. Thewar chests that the mega-firms haveamassed are unprecedented. As a result,megafunds have been able to significantlywiden the pay gap between themselvesand mid-market firms when it comes toassociates and senior associates, whichsome view as tomorrow’s private equity

industry leaders. The larger the fund, thelarger the management fee, and the morecompensation there is to go around.

The Glocap-Thomson Financialstudy, the “2008 Private EquityCompensation Report,” shows theincreasing discrepancy in pay betweenlarge firms and smaller firms. Everyoneknows that smaller firms receive less inmanagement fees, but their staffs aren’tnecessarily proportionately smaller. Pay increases to junior professionals aresmaller at smaller firms, both in absoluteand percentage terms (see Figures 5.2,5.3 and 5.4).

Title Average base salary (thousands)

2005 2006 2007-08Associate $ 88 $ 93 $ 96Senior associate 122 148 156Vice president 162 181 186Principal 211 238 240

Source: Glocap

Figure 5.2Average base salary for mid-sized private equityfunds ($750M-$2B in assets)

Title Average bonus (thousands)

2005 2006 2007-08Associate $ 88 $ 98 $111Senior associate 122 148 161Vice president 179 223 245Principal 238 265 306

Source: Glocap

Figure 5.3Average bonus for mid-sized private equityfunds ($750M-$2B in assets)

Figure 5.1U.S. buyout and mezzanine fundraising, 1996-Q2 2008 ($mil)

Source: Thomson Reuters Buyouts

0

50,000

100,000

150,000

200,000

250,000

$300,000

Mezzanine funds Buyout funds

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Title Average compensation (thousands)

2005 2006 2007-08Associate $176 $191 $207Senior associate 244 296 317Vice president 341 404 431Principal 449 503 546

Source: Glocap

Figure 5.4Average total cash compensation for a mid-sized fund

Top trends in middle-market private equity 17

According to the study, an associate isdefined as a pre-MBA who generally hasfewer than five years of total workexperience, including two or three years atan investment bank. A senior associate isdefined as having an MBA and betweenfour and seven years of work experience.

“The larger funds with yearlymanagement fees of $100 million plushave the cushion to pay up to retain andattract top talent,” says Glocap’s BrianKorb. “The mid-market firms feel thesqueeze of this comp inflation driven bythe megafunds.”

According to Glocap, in 2006, anassociate at a mega-firm earned anaverage of $238,000 in compensation,including base salary and bonus. Thatsame position paid $290,000 in 2007-08, a22 percent year-over-year increase. In thelarge firm category, an associate makes$238,000 in 2008, equivalent to last year’ssalary and bonus at a mega-firm and a 16 percent increase from the previousyear. However, in the mid-size range, theaverage associate makes $207,000 in cashcompensation, up only eight percentfrom 2006. In the two smallest segments,a newly minted associate can expect toearn $172,000 and $157,000, respectively,in base salary and bonus. Both represent four percent increases from 2006 levels.

For senior associates, the good newsis that the numbers, percentage-wise, tella somewhat better story. Salary andbonus at the mega-firm level are up nine percent to $419,000 over 2006. Forthe large firms, compensation is also up nine percent to $356,000. For mid-sizefirms, a senior associate makes $317,000,a seven percent increase from 2006. Atsmall-to-mid-size firms, pay is up sixpercent to $277,000. At the smallestfunds, senior associates should expect tomake $223,000, a five percent increasefrom a year ago. However, that’s almosthalf of what a senior associate wouldmake at a mega-firm.

Advent International hired four newassociates in the past year. Steve Collins, amanaging director with the firm, admits itis harder to recruit new talent. “Thesupply of associates is the same, but thedemand is three- or fourfold from what itwas. There are big funds out there nowwhere increasing salaries doesn’t changetheir bottom line that much. But it isn’t aseasy for smaller funds,” says Collins.

A mid-market private equityprofessional who wished to remain off therecord agreed that the competition istough. “I can’t believe what kids comingout of banking are demanding. It’s notonly the pay, but the options. It wasn’talways like this, but now they arechoosing between staying in the bankingindustry, and going to a private equityfirm or a hedge fund. They have moreoptions. If there used to be 100 jobsavailable to these people 10 years ago, I would say there are 500 now.”

ImpactMiddle-market private equity firms aregoing to have to work harder to recruitand retain strong talent.

According to Glocap’s Brian Korb,one recruiting tool that mid-market andsmall private equity firms can use to helpretain quality staff is the promise of afaster path to becoming a partner. Someassociates and senior associates might bewilling to take less money with thepromise of earning much more when theyjoin the partnership, which can happenmuch more quickly at a smaller firm.Small firms also arguably give junior levelstaff a better opportunity to learn theropes of the business.

Some private equity firms have triedother tactics to retain their staff. Ahandful, mostly unsuccessfully, have triedto raise management fees to produce theextra cash for compensation. “It’schallenging to a certain degree to stay inthe middle market,” says Korb. “If yoursuccess allows you to raise a much largerfund and move out of the middle market,then you run the risk of growing out ofyour sweet spot. However, if you turndown the extra capital, you risk cuttingoff the additional resources to hire andretain top investment professionals tomaintain your previous success. It’s tricky.”

Figure 5.5Percentage ofcompensation changefrom 2006 to 2007for an associate

Change

Megafund 22%Large fund 16%Mid-market 8%Small market 4%Microfund 4%

Source: Glocap

Figure 5.6Percentage ofcompensation changefrom 2006 to 2007for a senior associate

Change

Megafund 9%Large fund 9%Mid-market 7%Small market 6%Micrcofund 5%

Source: Glocap

Middle-market private equity firms are going to have to work harder to recruit and retain strong talent.

18 Top trends in middle-market private equity

Three hot sectors for investment

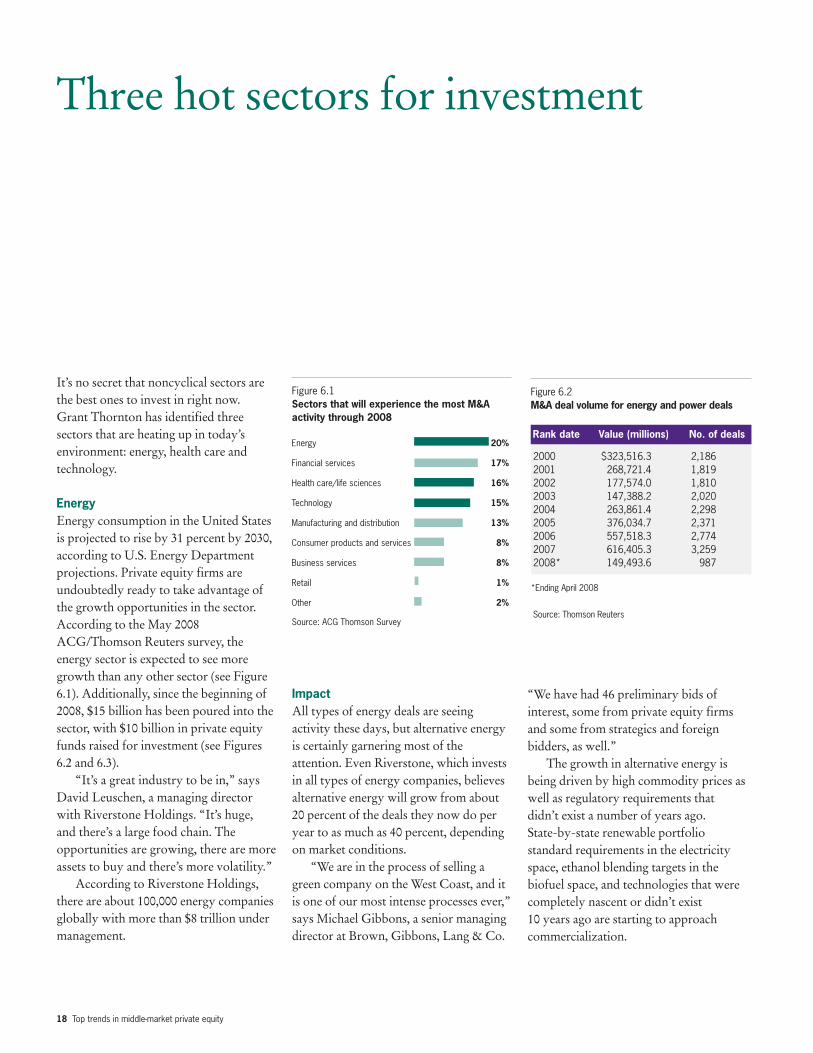

It’s no secret that noncyclical sectors arethe best ones to invest in right now. Grant Thornton has identified threesectors that are heating up in today’senvironment: energy, health care andtechnology.

EnergyEnergy consumption in the United Statesis projected to rise by 31 percent by 2030,according to U.S. Energy Departmentprojections. Private equity firms areundoubtedly ready to take advantage ofthe growth opportunities in the sector.According to the May 2008ACG/Thomson Reuters survey, theenergy sector is expected to see moregrowth than any other sector (see Figure6.1). Additionally, since the beginning of2008, $15 billion has been poured into thesector, with $10 billion in private equityfunds raised for investment (see Figures6.2 and 6.3).

“It’s a great industry to be in,” says David Leuschen, a managing directorwith Riverstone Holdings. “It’s huge, and there’s a large food chain. Theopportunities are growing, there are moreassets to buy and there’s more volatility.”

According to Riverstone Holdings,there are about 100,000 energy companiesglobally with more than $8 trillion undermanagement.

ImpactAll types of energy deals are seeingactivity these days, but alternative energyis certainly garnering most of theattention. Even Riverstone, which investsin all types of energy companies, believesalternative energy will grow from about20 percent of the deals they now do peryear to as much as 40 percent, dependingon market conditions.

“We are in the process of selling agreen company on the West Coast, and itis one of our most intense processes ever,”says Michael Gibbons, a senior managingdirector at Brown, Gibbons, Lang & Co.

“We have had 46 preliminary bids ofinterest, some from private equity firmsand some from strategics and foreignbidders, as well.”

The growth in alternative energy isbeing driven by high commodity prices aswell as regulatory requirements thatdidn’t exist a number of years ago. State-by-state renewable portfoliostandard requirements in the electricityspace, ethanol blending targets in thebiofuel space, and technologies that werecompletely nascent or didn’t exist 10 years ago are starting to approachcommercialization.

Figure 6.2M&A deal volume for energy and power deals

2000 $323,516.3 2,1862001 268,721.4 1,8192002 177,574.0 1,8102003 147,388.2 2,0202004 263,861.4 2,2982005 376,034.7 2,3712006 557,518.3 2,7742007 616,405.3 3,2592008* 149,493.6 987

*Ending April 2008

Source: Thomson Reuters

Rank date Value (millions) No. of deals

Figure 6.1Sectors that will experience the most M&Aactivity through 2008

Source: ACG Thomson Survey

Energy 20%

Financial services 17%

Health care/life sciences 16%

Technology 15%

Manufacturing and distribution 13%

Consumer products and services 8%

Business services 8%

Retail 1%

Other 2%

Top trends in middle-market private equity 19

However, while transactions inalternative energy can vary widely, sectorfragmentation is the single attribute thatremains constant. “You have a lot ofhighly fragmented services in the energysector,” says Grant Thornton’s Dan Reid.“Especially in oilfield services. Thisindustry was depressed for 15 years priorto the last couple of years, and manyentrepreneurs are considering exiting orretiring. In addition, we have seen asignificant trend that children don’t wantto take over family businesses anymore,so these businesses will likely be sold.This creates an incredible opportunity toroll these companies up.”

Another factor driving energy deals isthe price of oil. As the price of a barrel ofoil continues to remain high, spending themoney to find an alternative makeseconomic sense. “At $110 a barrel,alternative energy becomes feasible andmany traditional energy companies lookattractive. There’s no question why moneyis starting to focus there,” says Reid.

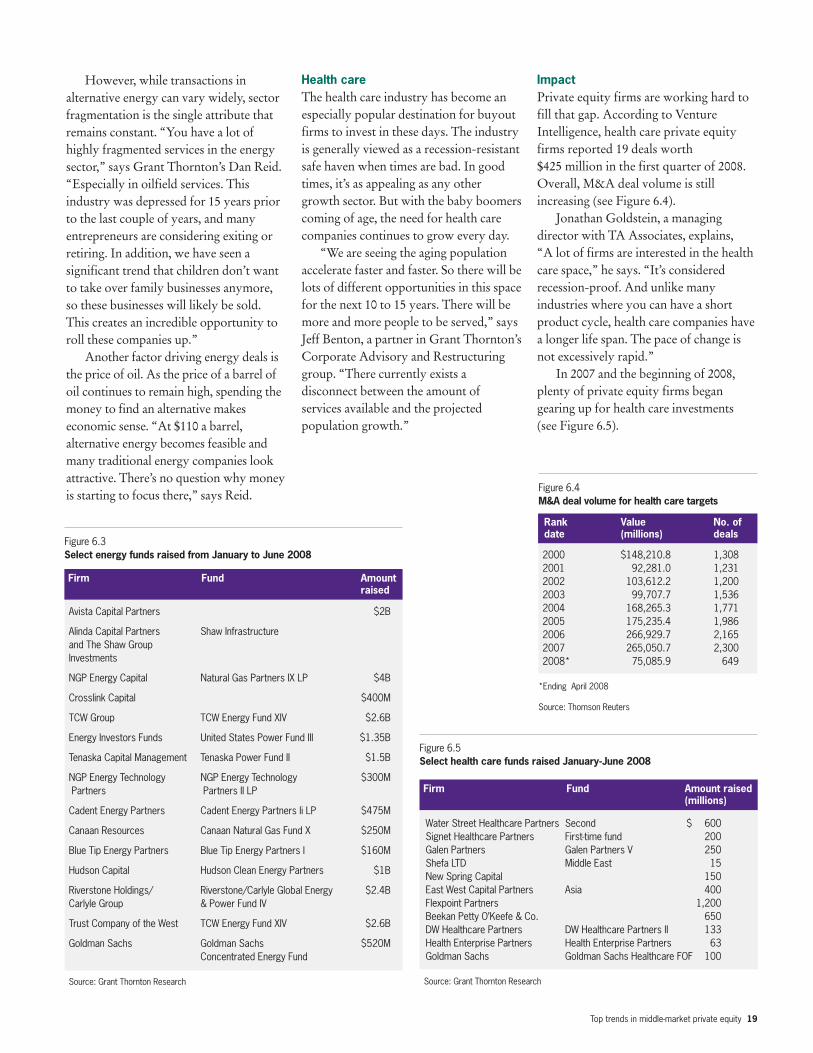

Health careThe health care industry has become anespecially popular destination for buyoutfirms to invest in these days. The industryis generally viewed as a recession-resistantsafe haven when times are bad. In goodtimes, it’s as appealing as any othergrowth sector. But with the baby boomerscoming of age, the need for health carecompanies continues to grow every day.

“We are seeing the aging populationaccelerate faster and faster. So there will belots of different opportunities in this spacefor the next 10 to 15 years. There will bemore and more people to be served,” saysJeff Benton, a partner in Grant Thornton’sCorporate Advisory and Restructuringgroup. “There currently exists adisconnect between the amount ofservices available and the projectedpopulation growth.”

ImpactPrivate equity firms are working hard tofill that gap. According to VentureIntelligence, health care private equityfirms reported 19 deals worth $425 million in the first quarter of 2008.Overall, M&A deal volume is stillincreasing (see Figure 6.4).

Jonathan Goldstein, a managingdirector with TA Associates, explains, “A lot of firms are interested in the healthcare space,” he says. “It’s consideredrecession-proof. And unlike manyindustries where you can have a shortproduct cycle, health care companies havea longer life span. The pace of change isnot excessively rapid.”

In 2007 and the beginning of 2008,plenty of private equity firms begangearing up for health care investments (see Figure 6.5).

Water Street Healthcare Partners Second $ 600Signet Healthcare Partners First-time fund 200Galen Partners Galen Partners V 250Shefa LTD Middle East 15New Spring Capital 150East West Capital Partners Asia 400Flexpoint Partners 1,200Beekan Petty O’Keefe & Co. 650DW Healthcare Partners DW Healthcare Partners II 133Health Enterprise Partners Health Enterprise Partners 63Goldman Sachs Goldman Sachs Healthcare FOF 100

Source: Grant Thornton Research

Figure 6.5Select health care funds raised January-June 2008

Firm Fund Amount raised(millions)

Firm Fund Amount raised

Avista Capital Partners $2B

Alinda Capital Partners Shaw Infrastructureand The Shaw GroupInvestments

NGP Energy Capital Natural Gas Partners IX LP $4B

Crosslink Capital $400M

TCW Group TCW Energy Fund XIV $2.6B

Energy Investors Funds United States Power Fund III $1.35B

Tenaska Capital Management Tenaska Power Fund II $1.5B

NGP Energy Technology NGP Energy Technology $300MPartners Partners II LP

Cadent Energy Partners Cadent Energy Partners Ii LP $475M

Canaan Resources Canaan Natural Gas Fund X $250M

Blue Tip Energy Partners Blue Tip Energy Partners I $160M

Hudson Capital Hudson Clean Energy Partners $1B

Riverstone Holdings/ Riverstone/Carlyle Global Energy $2.4BCarlyle Group & Power Fund IV

Trust Company of the West TCW Energy Fund XIV $2.6B

Goldman Sachs Goldman Sachs $520MConcentrated Energy Fund

Source: Grant Thornton Research

Figure 6.3Select energy funds raised from January to June 2008

Figure 6.4M&A deal volume for health care targets

2000 $148,210.8 1,3082001 92,281.0 1,2312002 103,612.2 1,2002003 99,707.7 1,5362004 168,265.3 1,7712005 175,235.4 1,9862006 266,929.7 2,1652007 265,050.7 2,3002008* 75,085.9 649

*Ending April 2008

Source: Thomson Reuters

Rank Value No. ofdate (millions) deals

20 Top trends in middle-market private equity

Grant Thornton’s Jeff Benton hasobserved this development. “People arealways going to need health care andservices,” he says. “Private equity is in agreat position to take advantage of thegrowing demands.”

However, there are risks. The majorone is an increase in the reimbursementrate, which will most likely be seen afterthe 2008 U.S. presidential election. Achange in reimbursement rates will adjustany company’s earnings, in most cases notfor the better. Another risk includeschanges to government regulation. “It’s asolid place to invest, but there are trapsinvestors need to be aware of,” warnsGoldstein.

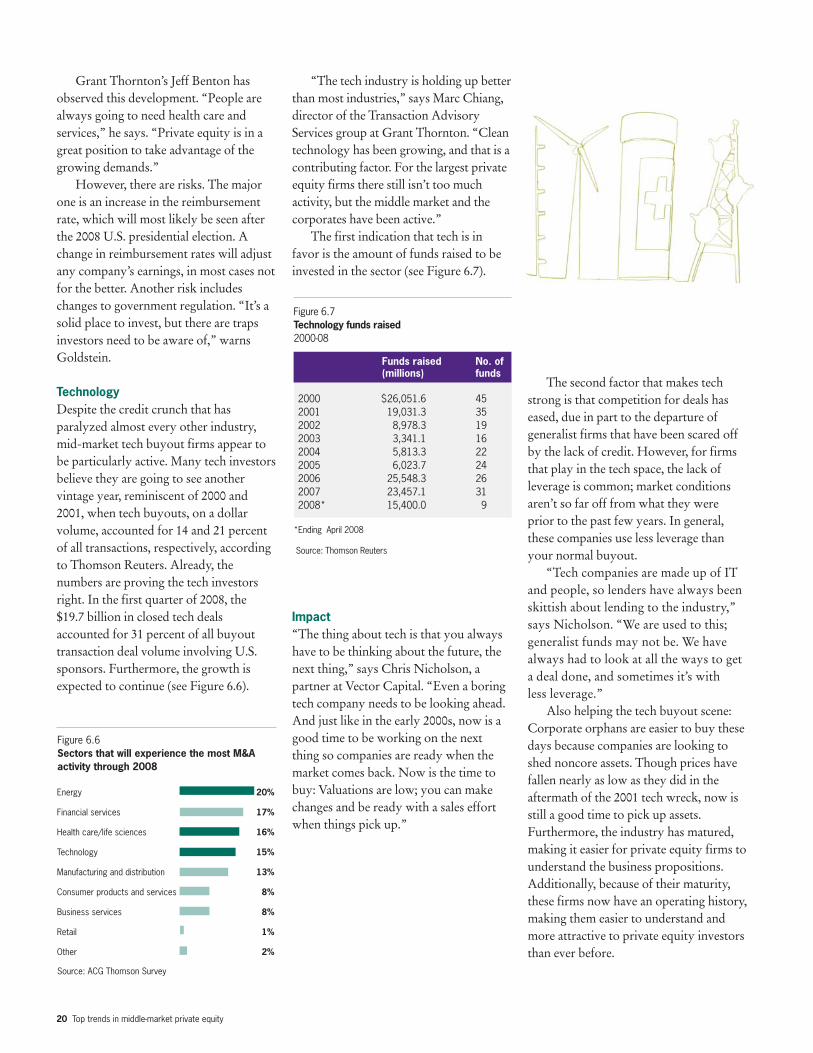

TechnologyDespite the credit crunch that hasparalyzed almost every other industry,mid-market tech buyout firms appear tobe particularly active. Many tech investorsbelieve they are going to see anothervintage year, reminiscent of 2000 and2001, when tech buyouts, on a dollarvolume, accounted for 14 and 21 percentof all transactions, respectively, accordingto Thomson Reuters. Already, thenumbers are proving the tech investorsright. In the first quarter of 2008, the$19.7 billion in closed tech dealsaccounted for 31 percent of all buyouttransaction deal volume involving U.S.sponsors. Furthermore, the growth isexpected to continue (see Figure 6.6).

“The tech industry is holding up betterthan most industries,” says Marc Chiang,director of the Transaction AdvisoryServices group at Grant Thornton. “Cleantechnology has been growing, and that is acontributing factor. For the largest privateequity firms there still isn’t too muchactivity, but the middle market and thecorporates have been active.”

The first indication that tech is infavor is the amount of funds raised to beinvested in the sector (see Figure 6.7).

Impact“The thing about tech is that you alwayshave to be thinking about the future, thenext thing,” says Chris Nicholson, apartner at Vector Capital. “Even a boringtech company needs to be looking ahead.And just like in the early 2000s, now is agood time to be working on the nextthing so companies are ready when themarket comes back. Now is the time tobuy: Valuations are low; you can makechanges and be ready with a sales effortwhen things pick up.”

Figure 6.7Technology funds raised 2000-08

2000 $26,051.6 45 2001 19,031.3 35 2002 8,978.3 19 2003 3,341.1 16 2004 5,813.3 22 2005 6,023.7 24 2006 25,548.3 26 2007 23,457.1 31 2008* 15,400.0 9

*Ending April 2008

Source: Thomson Reuters

Funds raised No. of(millions) funds

Figure 6.6Sectors that will experience the most M&Aactivity through 2008

Source: ACG Thomson Survey

Energy 20%

Financial services 17%

Health care/life sciences 16%

Technology 15%

Manufacturing and distribution 13%

Consumer products and services 8%

Business services 8%

Retail 1%

Other 2%

The second factor that makes techstrong is that competition for deals haseased, due in part to the departure ofgeneralist firms that have been scared offby the lack of credit. However, for firmsthat play in the tech space, the lack ofleverage is common; market conditionsaren’t so far off from what they wereprior to the past few years. In general,these companies use less leverage thanyour normal buyout.

“Tech companies are made up of ITand people, so lenders have always beenskittish about lending to the industry,”says Nicholson. “We are used to this;generalist funds may not be. We havealways had to look at all the ways to geta deal done, and sometimes it’s with less leverage.”

Also helping the tech buyout scene:Corporate orphans are easier to buy thesedays because companies are looking toshed noncore assets. Though prices havefallen nearly as low as they did in theaftermath of the 2001 tech wreck, now isstill a good time to pick up assets.Furthermore, the industry has matured,making it easier for private equity firms tounderstand the business propositions.Additionally, because of their maturity,these firms now have an operating history,making them easier to understand andmore attractive to private equity investorsthan ever before.

Top trends in middle-market private equity 21

The natural evolution of theprivate equity firm

While private equity’s place in the marketused to be clear, recently the lines betweenprivate equity and other asset classes havestarted to blur. Many of the large playershave diversified their offerings: buyinghedge funds, raising middle-market fundsand launching new vehicles to capitalizeon the dislocation in the credit markets.There are a number of middle-marketfirms that have also expanded beyondtheir normal realm. The practice allowsLPs to look at private equity firms as aone-stop shop, while giving private equityfirms the opportunity to stay activeregardless of market conditions. However,the question remains: Can private equityfunds be all things to all investors?

According to some, just as there hasbeen a consolidation in the number ofcompanies that make cars, the same willhappen in the private equity world.Thirty-five years ago, when private equitywas really making a name as an asset class,companies were bought cheaply and thenew owner could make a few changeswhile generating a profit and a high returnfor the investor. That simply isn’t the caseanymore. Because of the increasednumber of private equity firms, hedgefunds and strategic buyers, there is muchmore competition, prices are up andreturns are on the decline.

“It’s natural that over time the privateequity industry will consolidate,” saysStewart Kohl, co-CEO of The RiversideCo. “Every other industry has, and why

should we be different? Based oncompetitive advantage, there’s going to bean evolution where most of the talent andmoney ends up in firms having 200 ormore employees and $5 billion or more inassets under management. However, asprivate equity firms grow, there willcontinue to be increasing specialization byindustry, stage, geography and otherfactors. For example, even with ourmultiple funds in various geographies,Riverside will continue to dedicate itselfto the smaller end of the middle market.”

According to results from the May2008 ACG/Thomson Reuters survey,while middle-market firms are split onwhether diversification makes sense, mostthink asset expansion is inevitable (seeFigure 7.1).

“It’s easy when you can diversify yourassets within one firm that you trust,”says one LP. “You just have to be sure thatthe firm has the proper infrastructure tosupport so many different businesses.”

Jack Katz, Grant Thornton’s New York Cluster managing partner andFinancial Services group nationalmanaging partner says, “If a privateequity firm has the track record, it canset up other funds to remain nimble,especially at times like we areexperiencing. For example, moredistressed funds are being set up now,but those private equity firms maychoose to start a different fund in thefuture. There are advantages todiversifying within the same fund. You can choose between differentalternatives in different industries.”

Figure 7.1Is raising a diversified set of investment funds the wave of the future for middle-marketprivate equity firms?

Source: ACG Thomson Survey

Yes, it only makes sense for private equity firms to be able to showLPs a diverse offering 12%

Yes, the large market is already doing it, it’s just a matter of time until themiddle market follows suit 30%

No, that’s not what private equity investing is about 40%

I am not crazy about the idea, but my firm may eventually have todo it to stay competitive 18%

Indeed, and the bottom line is thatLPs want solid investment choices. “It’sall about generating good returns for yourinvestors,” says one private equity player.“Managers don’t get in trouble forsuggesting to invest in well-establishedfunds with a good track record, but themanager will get fired if the recommendedinvestment results in lost capital for theLPs. Once you have the track record,raising multiple funds is a good growthstrategy for PE [private equity] funds,assuming that they can executesuccessfully on the expanded philosophyand don’t compromise what made themsuccessful in the first place.”

The trend really started recently withthe megafunds, which have built out theirbusinesses in many different directions.For example, in the past year, TPG hasraised $3 billion for distressed investing,$1.2 billion for middle-market buyoutinvestments, $7 billion for financialservices investments, and $4.2 billion forinvestment in Asia. This is on top of an$18 billion fund the firm raised to handleits regular private equity investments.

TPG is not alone. While othermegafunds might not have raised as manydifferent types of private equity funds,some are raising different vehiclesaltogether to keep business robust, even if regular LBO business is not. TheBlackstone Group raised several newfunds during the past year. Blackstoneraised $1.3 billion for distressed investing,a $400 million CLO vehicle called St.James’s Park CDO B.V., seven U.S.CDOs with $4.7 billion, four EuropeanCLOs with $2.9 billion, and two privatemezzanine funds with $2.1 billion. Alltold, the firm’s new CLO group manages$14 billion across 26 funds in the UnitedStates and Europe. Additionally, in Marchthe firm acquired GSO Capital Partners, ahedge fund, for $365 million. This is all inaddition to the firm’s $21.7 billion buyoutfund, not to mention its real estate andmutual funds.

It’s clear that the listing of large-market firms raising multiple funds can goon and on. However, right now there arejust a handful of middle-market firmsfollowing suit. Riverside has successfullyraised a buyout fund, a microcap fund andan Asian fund, all on top of a Europeanfund. Monomoy Capital Partners closedan inaugural turnaround fund with $280 million in capital commitments.TriLyn LLC and Investcorp have held$100 million for a first close on TriLyn-Investcorp Mezzanine Partners I, a fundthat will make structured mezzanine andother high-yielding debt and preferredequity deals in U.S. commercial andresidential real estate. The Audax Groupalso has a private equity fund, mezzanineand senior debt funds. Sun CapitalPartners has diversified its fund offerings.

ImpactWhile turning into true asset managersmay be the wave of the future, it’s notexpected to happen overnight. “Theprivate equity industry will continue toevolve, and it will take 10 to 20 years forthis consolidation to play out,importantly because fund lives are long,”says Riverside’s Stewart Kohl. “And therewill always be some private equity shopsthat choose to stay small and operate asboutiques. But most of the large pensionfunds and other leading private equityinvestors would really like to find homes

where they can invest larger amountswithout doing multiple searches andmonitoring multiple firms.”

According to the May 2008ACG/Thomson Reuters survey, despitethe interest of LPs, raising multiple fundswon’t be an easy task (see Figure 7.2) formiddle-market private equity firms.

“It’s smart from a private equitystandpoint,” says River Associates’ MarkJones. “It broadens their depth andexposure. And you have been seeingmiddle-market funds carve out newfunds. At ACG Capital Connections, yousee a couple of different names at onetable, then you come to learn they are all apart of the firm. But it’s a much larger taskfor middle-market firms. It’s going to takea while for middle-market firms to be ableto offer investors what Blackstone can.The megafunds have the resources. Themiddle market is approaching this muchmore slowly.”

According to Grant Thornton’s JackKatz, the evolution has already started,and it will just keep on going. “Privateequity has been around for a long time,”he says. “It goes through differentvariations and reinvents itself from timeto time. Firms adjust their focus, debtratios and fund sizes, so this is notnecessarily so surprising.”

Figure 7.2Can middle-market private equity firms handle raising and putting multiple funds to work?

Source: ACG Thomson Survey

Yes, we might have more overhead, but it’s possible 28%

Yes, but it will take a significant ramp-up period 35%

No, it just wouldn’t add up. Returns would be diminished with allthe extra overhead 26%

No, fundraising is too exhausting -- there would be no time to putthe money to work 11%

22 Top trends in middle-market private equity

Top trends in middle-market private equity 23

Conclusion

It is clear that private equity has entered adifferent era of dealmaking. With theproliferation of cross-border activity,operational partners and sovereign wealthfunds, and private equity firms becomingall-around asset managers, the industry ispoised for more growth than ever before,despite the credit crunch. All of these newtrends solidify two key points: Privateequity is an ever-changing and maturingasset class, and savvy private equityinvestors have proved there are ways toreinvent the business and create new andexciting opportunities.