Embed Size (px)

Citation preview

Corporate frauds have exploded in India and have become a phenomenon. From Harshad Mehta to Ketan Parekh, to Madhavapura Co-operatives in 2002 to the CRB scam involving RoopBhansal and further down to the initial public offering scam — popularly known as the Rupalben scam in late 2005 to the latest one Satyam’s fraud, it is a familiar story of a few corporate heads indulging in creative accounting with the sole object of enriching themselves at the cost of the lower middle-class investors.

Frauds are not new for the corporate world. This is because by it very definition, even bribery or supplier kickbacks comprise fraud. Other type of frauds includes accounting frauds (includes financial misconduct by top management), theft of intellectual property, data or information, counterfeiting etc. What is unfortunate is the fact that not many organizations seem to have a complete understanding of frauds that botch their balance sheets and cause financial injury even as they stand helpless in the wake of poor mechanisms to plug loopholes.

According to estimates, India is losing a whopping $40 bn per year because of corporate frauds, which is more than 4% of the country’s gross domestic product.

There is a crisis of confidence arising from the failure of the pillars of the capitalist system such as the stock market, financial analyst and accountants and the investment banks. It is unbelievable that the hundreds and thousands of “whistle-blowers” from board directors to corporate insiders and the accounting firms and the credit-rating agencies were kept in the dark about the goings-on in the Indian financial world.

LIST OF FRAUDS IN INDIA

The Flying Companies: In the last decade of nineteenth century IPO was the buzzword of the stock markets. Investors were lured due to the hefty returns on the listings. It was the IPO boom. There were however no stringent norms for the companies to come out with an IPO. The flying company scam or the IPO bubble in the mid nineties exposed the half baked nature of reforms of Indian Economy.

Plantation boom in 1990’s: Somebody promise that growing plants is the shortest way to create the wealth. Investors are taken for the ride in Plantation Fraud.

Market manipulations: Twice in the history of the stock markets in India single person succeeded in manipulating the share prices on large scale. Ketan Parekh and Harshad Mehta get the dubious distinction of being the Stock Market Fraudsters.

CRB Capital Markets (1996): Chairman Chain RoopBhansali was accused of using CRB’s accounts in SBI to siphon off Rs 1,200 crore bank funds, claiming the firm was encashing interest warrants and refund warrants. He used very innovative products to attract the depositors to his non-banking finance company.

ITC-Chitalia’sFera Violation (1996): It was an $ 80 million fraud into exports transactions between ITC and EST Fibres of the Chitalia group during 1990- 1995 revealed Fera violations.

Western Paques:NandanGadgil who gave his investor the dream of making his company bigger than HDFC suddenly disappeared from the Indian Bourses. All his companies defaulted to a great extent.

Home Trade (2002): A Rs 6,000 crore fraud when eight co-operative banks, including Valsad People’s Co-operative Bank and Navsari Co-operative Bank among others collectively lost over Rs 80 crore.

SSI Technologies Inc: An arm of SSI Technologies Ltd, which figured in the K-10 stocks of broker Ketan Parekh, who led the 2002 market collapse and was arrested later for alleged share price manipulation. Kalpathi Suresh, the chief executive of SSI, eventually sold the software services and software education businesses to PVP group.

DSQ Software (2003): Dinesh Dalmia’s DSQ Software was accused of dubious acquisitions and biased allotments made in 2000 and 2001. It was an Rs 595 crore fraud. In March 2006, Indian authorities arrested Dinesh Dalmia, chief executive of DSQ Software, for fraud and inducing US investors to part with $100 million for investment in substandard equipment for operating a back-office firm out of India.

Along with DSQ Software Ltd, companies like Pentasoft Technologies Ltd and Pentamedia Graphics Ltd also recorded scandals over insider trading and other corporate malpractices and collapsed after their promoters in 1999 diversified from the software and animation services business into new ventures such as resorts and multiplexes.

Rising instances of corporate fraud have set the alarm bells ringing within India Inc. Below is the fact file of Fraud Survey Report 2008, conducted by KPMG: · 70 percent companies believe fraud will increase over the next 2 years.

· 75 percent respondents identified fraud as a matter of highest concern.· 80 percent said fraud poses a big problem.· 60 percent acknowledged fraud occuring in their own companies.· 11 percent lost between Rs. 1 to 100 millions due to fraud.· 5 percent companies lost more than Rs. 100 millions due to fraud.· 53 percent reported loss less than Rs. 1 million.· Unethical behavior of employees and inadequate anti-fraud measure main worrying factors.· 60 percent respondents do not have adequate knowledge of anti-corruption law.· Financial sector hit worst – followed by real estate & infrastructure – pushing IT &ITeS to third place.

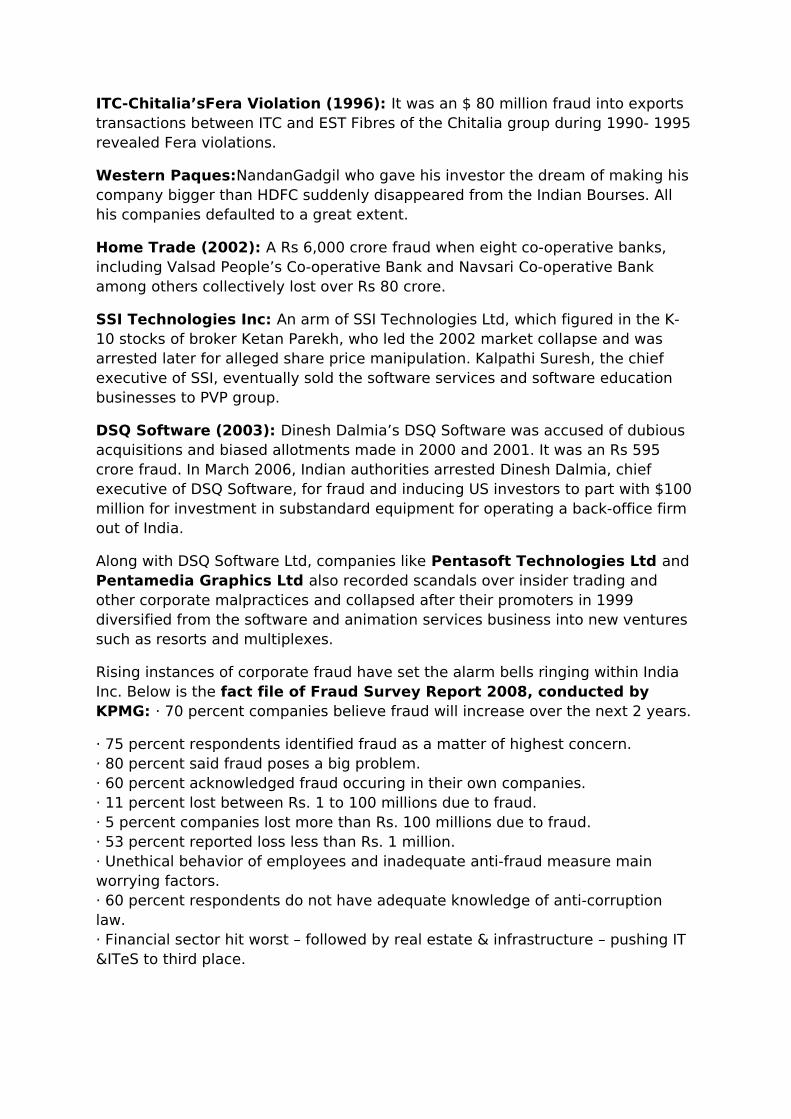

Profile of a fraudsterPeople who have longstanding relationships with the victim company perpetrate a majority of frauds.

How companies treat fraudstersMore than a third of Indian companies do nothing about frauds.

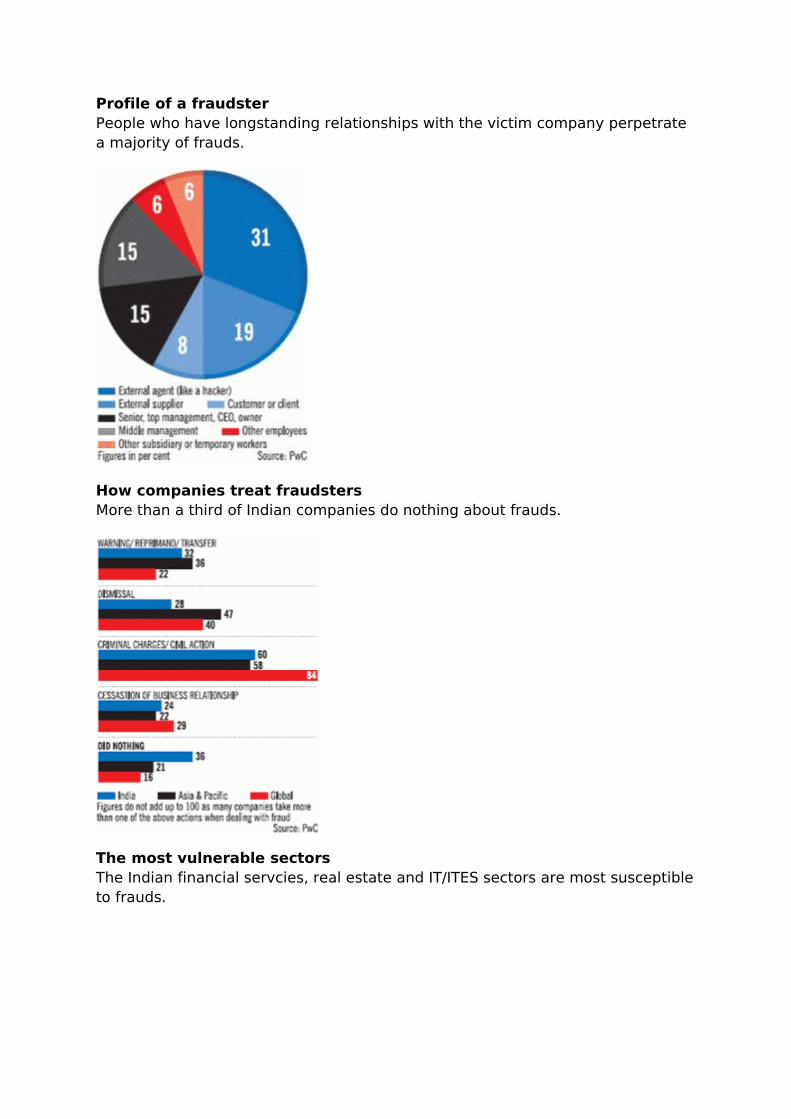

The most vulnerable sectorsThe Indian financial servcies, real estate and IT/ITES sectors are most susceptible to frauds.

SAYTAM’S FARUD

The purpose of the scam

The purpose was aimed to make the company more attractive for investors. Raju pointed out that given the low promoter holding in the company (8.6% as of September 2008), poor performance could result in a take-over. It was important, therefore, to make it seem as if both the top and bottom lines were growing at a healthy rate, even if that was not actually true.

How did the bubble build?

The problem with overstating performance is that if you want to keep growth rate looking good, the absolute extent of the exaggeration has to keep getting bigger. To take this particular example, in 2003-04 Satyam reported net sales of Rs 2,542 crore. In the four years since then, that figure was reported to have grown by 36%, 34%, 40% and 31% respectively to reach Rs 8,473 crore in 2007-08.

Now, if an Rs 2,500-crore company wants to show 35% growth when it has actually grown by only say 25%, the extent of overstatement would be only Rs 250 crore (10% of Rs 2,500 crore).

But if an Rs 8,500-crore company wants to do the same thing, it will have to fudge the figures by Rs 850 crore. It is also important to realise that overstating revenues by 10% can overstate profit by a lot more.

For instance, if actual revenues were Rs 2,000 crore and actual net profits Rs 200 crore, an addition of Rs 500 crore to revenues without changing anything else would also add Rs 500 crore to net profit. While this would mean exaggerating revenues by only 25%, the profit figure would get overstated by 250% (500 cr is two-and-a-half times 200 crore).

Aftermath

The incident has resulted in immeasurable and unjustifiable damage to Brand India and Brand IT in particular. No doubt, India Inc has reacted with shock and dismay to the scam and it is likely to dent the public credibility about the concepts of corporate governance that the Indian industry has been so persistently trying to cultivate for the last decade.

An accounting fraud was the last thing investors in India would have imagined as a trigger for a reversal in investor sentiment. The Satyam accounting fiasco has come at a time when the sentiment is already brittle and is likely to affect the image of Indian companies among foreign portfolio investors.

Impact on Satyam as a company

1. Satyam stock is being removed from its S&P CNX Nifty 50-share index from Jan 12 and the Bombay Stock Exchange is expected to follow suit. Satyam will also be excluded from the CNX 100 index, CNX 500 index and the CNX IT index. Reliance Capital Ltd will replace Satyam in the main index. Satyam has lost more than 10000 Crore rupee in a single day trading (on Thrusday).

2. Satyam’s American Depository Receipts is halted for the time being (suspended) and replaced it by Axis Bank.

3. Satyam’s largest shareholder, Aberdeen AMC, dumped the tainted software entity’s shares on Wednesday, was also a seller in other index stocks like Reliance Communications and JP Associates.

4. Several domestic and foreign brokerage firms, including Credit Suisse, Religare and Angel Broking, suspended their coverage of Satyam shares.

5. The selling after Raju’s 7 pages letter to the board:(a) Swiss Finance Corp Mauritius Ltd: Sold 7786759 shares at Rs.74.61(b) Aberdeen International India Opportunities Mauritius Ltd:Sold 9830811 shares of the company at Rs.43.41(c) Aberdeen Asset Managers Ltd Aberdeen Global Asia Pacific fund: Sold 4179064 shares at Rs.43.41

Impact on Investor

Normally the common man did not really look at balance sheets and only went by media reports, stock market performance and word of mouth to make his investment decisions. Now, he will be careful.

Impact on FII’s

The fraud at Satyam, wherein the books were cooked to show inflated topline and bottomline, will most definitely make foreign institutional investors (FIIs), the biggest believers in the Indian IT story, look at this counter closely.

FIIs had walked the talk and are currently large shareholders of most publicly traded Indian IT companies. In Satyam Computer, the FII holding is about 47%. At Infosys Technologies, it is 41%. At Wipro they hold a third (7%) of the non-

promoter stake. At HCL Technologies, of the 33% held by non-promoters, FII holding is 18%. At TCS, their stake is 11% (promoters own 76%). All figures are for September 30,2008.

FIIs will be cautious about investing in the IT services counter. Naturally there will be higher level of due diligence.

Foreign investor confidence is basically dependent on how the regulators act. In Satyam’s case, uniquely two regulators are involved, SEC in the US and SEBI in India, as Satyam is also listed in the US. A lot depends on how they behave. How our government behaves. Business will take cues from that.

Satyam’s fraud disclosure, the industry believes, has come at a bad time, when recession is likely to hurt the earnings of the IT industry.

Impact on employees

Co. will not pay 2 months salary to the 53,000 employees and strong chances to lay-off of people are there who were sitting on the bench or were close to completing their assigned projects.

For a company, which is indulged in service sector, employees contribute to almost 52% of the co. expense, so lay off is the strong tool to cut the cost.

The other Big IT giants like Infosys has refused to hire any Sataymite.

The India Inc. image

The whole of the Indian industry should not be tarred with the same brush as most of the companies uphold the highest standards of corporate governance and this will help in mitigating the damage done to India’s image.

However, the revival of India’s position as a preferred investment destination would depend on the speed of regulatory action to salvage the situation. The regulators would have to take drastic measures to regain the confidence of foreign investors in Indian companies as frauds like these will have greater implications on emerging markets than developed markets.

Now, All Indian companies listed in the US have to go through a lot of procedures and filings, which talks about risk factors and financial position of the company.

FIIs will be difficult to convince and it will take time before FIIs line up in India and India loss will be the gain of China.

The need of the hour

Tighter rules for accounting and corporate governance, including appointment of independent directors by selection committees, and greater oversight from regulatory and government authorities.

Noble Group also suggests separation of audit and consultancy functions at companies, and quicker publication of annual reports.

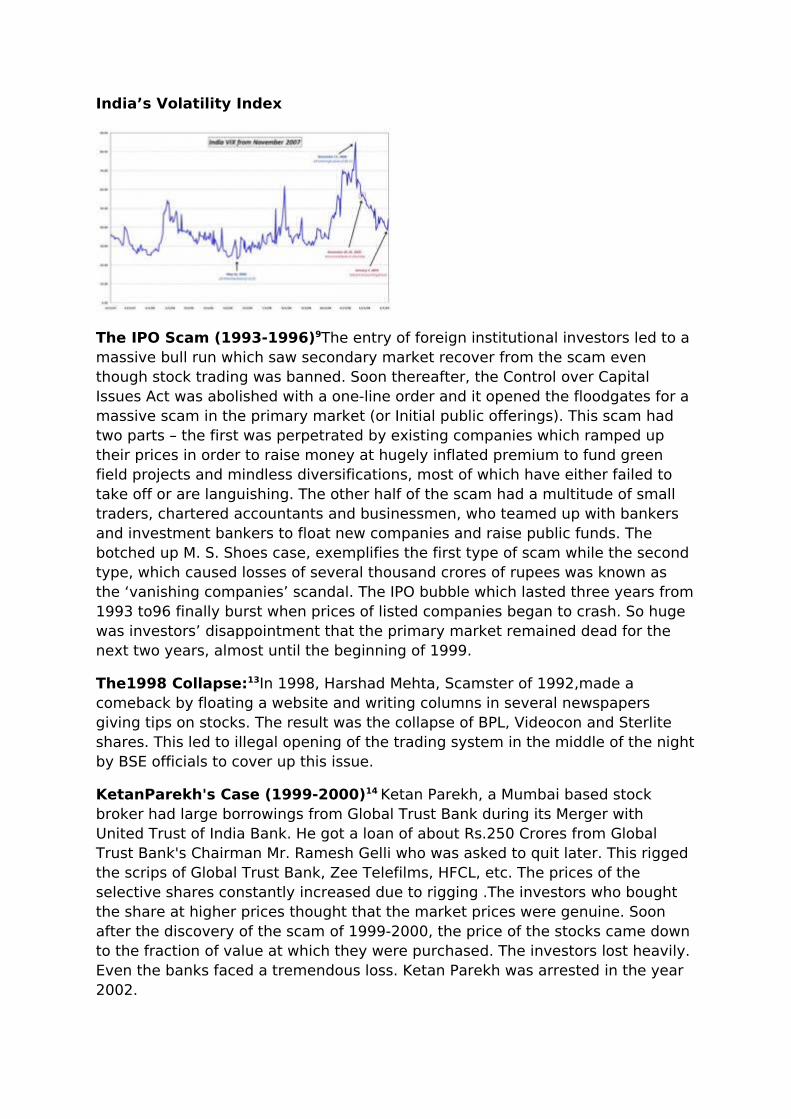

India’s Volatility Index

The IPO Scam (1993-1996)9The entry of foreign institutional investors led to a massive bull run which saw secondary market recover from the scam even though stock trading was banned. Soon thereafter, the Control over Capital Issues Act was abolished with a one-line order and it opened the floodgates for a massive scam in the primary market (or Initial public offerings). This scam had two parts – the first was perpetrated by existing companies which ramped up their prices in order to raise money at hugely inflated premium to fund green field projects and mindless diversifications, most of which have either failed to take off or are languishing. The other half of the scam had a multitude of small traders, chartered accountants and businessmen, who teamed up with bankers and investment bankers to float new companies and raise public funds. The botched up M. S. Shoes case, exemplifies the first type of scam while the second type, which caused losses of several thousand crores of rupees was known as the ‘vanishing companies’ scandal. The IPO bubble which lasted three years from 1993 to96 finally burst when prices of listed companies began to crash. So huge was investors’ disappointment that the primary market remained dead for the next two years, almost until the beginning of 1999.

The1998 Collapse:13In 1998, Harshad Mehta, Scamster of 1992,made a comeback by floating a website and writing columns in several newspapers giving tips on stocks. The result was the collapse of BPL, Videocon and Sterlite shares. This led to illegal opening of the trading system in the middle of the night by BSE officials to cover up this issue.

KetanParekh's Case (1999-2000)14 Ketan Parekh, a Mumbai based stock broker had large borrowings from Global Trust Bank during its Merger with United Trust of India Bank. He got a loan of about Rs.250 Crores from Global Trust Bank's Chairman Mr. Ramesh Gelli who was asked to quit later. This rigged the scrips of Global Trust Bank, Zee Telefilms, HFCL, etc. The prices of the selective shares constantly increased due to rigging .The investors who bought the share at higher prices thought that the market prices were genuine. Soon after the discovery of the scam of 1999-2000, the price of the stocks came down to the fraction of value at which they were purchased. The investors lost heavily. Even the banks faced a tremendous loss. Ketan Parekh was arrested in the year 2002.

8http://www.suchetadalal.com/?id=baebd5a4-0b2c-eda7-492e8a70763c&base=sub_sections_content&f&t=10+years+of+financial+scams

14http://www.indiastudychannel.com/resources/52080-years-major-financial-scams-India.aspx

India a resource rich country has all the means to achieve greatness but it's dense web of corruption has motivated a normal citizen to take the path of dishonesty to get richer. People are exploiting the loopholes in the cracked system at the cost pain and suffering of the poor and the middle class for meeting immediate needs. Indians proudly state that many millionaires are emerging and the country according to certain reports giving most honest people an illusion of hope.

list of multi-crore scams from 2005...2010Prominant Scams Before 2005

1. Harshad Mehta Big Bull Scam - 4000 crore

2. Lalu'sCharaGhotala - 950 crores - July 2008 IAS officer Sajjal gets four-yr RI for 39 crore scam

3. Hawala Scandal - 5000 crores

4. Bofors Scandal - 64 crores (Also Read: 1 2 3)

5. NarendraRastogi serial scammer - more than 43 crores (Read more 1)

6. Dalmia Scandal - 595 crores

7. Civil Aviation Minister Praful Patel fraud case-50 crores

8. UTI Scam - 32 crores

9. Mutual Fund Scam - 1350 crores

10.Bansali Scam - 1200 crores

11.Ketan Parekh's Sebi Scam- 888 crores - June 08 - SC issues arrest warrant against Ketan Parekh

12.Cobbler Scam - 1000 crores

13.Bribe to allot petrol pumps scam

14.Churhat lottery scam - ?

15.Anantnag transport subsidy scam - ?

16.Bangalore - Mysore Infrastructure Corridor - ?

17.Kerala SNC Lavalin power scandal - 374.5 crore loss - Dec 09 - Accused CPM leader Vijayan gets bail in graft case.

January 2005

1. Telgi Scam - 171 crores - Telgi was sentenced 13 yrs RI and 100 cr fine. (Read More 1 2 Timeline 3)

2. Mayawati'sTaj Corridor- 175 crores alleged scam - Case was dropped in 2007 by the pecial designated court due to insufficient evidence (Read more 1 Is Politics such a high paying profession ? 2 May 2008 -Mayawati attempts to stop CBI investigation 3)

3. MotilalGoel Scam - 1000 crore

February 2005

1. West Bengal Telecom Scam - 400 crores

2. India's unchecked textbooks racket - estimated 225 crores

3. Urea Scam - 133 crores

March 2005

1. Meghalaya lottery scam - 25000 crore

April 2005

1. Ration Card Scam - 3 crore

2. Car Financing Scam - ? crore

3. Junior Basic Trained teachers' recruitment scam- ?

May 2005

1. Flood Relief Scam - 13 crores (Read more 1)

2. Let them eat plastic bags - GautamGoswami

June 2005

1. Temple Lands Scam - 30 crores

2. Franking Scam - 30 crores

July 2005

1. Volkswagon Equity Scam - 11 crores - Sep 10 - CBI names 6 accused

2. National Slum Development Programme - 1.52 crores (Same guy of Flood Relief Scam May 05 who said "Victims can eat plastic bags")

3. Kerala State Electricity Board - 89.32 crores (alleged corruption worth Rs. 100 crores was also involved in the drinking water project)

August 2005

1. Indian Oil Corporation Scam - ? crores

September 2005

1. Just talks of investigation of scam shaves off 89000 crores from the market capital

1. CBI nets 70 officials in all-India anti-corruption drive

1. Nagmani Scam - 1.5crore

2. Stamp Scam (Goa) - 30.19 crore

October 2005

1. Evasion of duty on High End Car’s – ? crore

2. Okhla Industrial Development Authority (Noida) land scam – ? crore

3. Employment Guarantee Scheme (EGS) Scam- 9.1 crore

Delivering a talk on Corruption in democratic governance, Pandey said that "At present, the total amount of black money in India has been estimated to be in the range of Rs 50,000 crore and Rs 1,00,000 crore. The most worrisome is the fact that even those quarters that are supposed to fight corruption are not totally corruption-resistant".

November 2005

1. Local Area Development Scheme (MPLADS) Scam - ? crores

2. National Agricultural Cooperative Marketing Federation of India (NAFED) Scam - 250 crores - Sep 2007 - HC pulls up CBI for not registering case

3.

"I am pained to observe that the law in this country punishes very harshly the small offenders involved in offences of stealing of small amounts to the tune of few hundreds or few thousands. "Such accused are often sent to jail by the big fishes who defraud the exchequer of crores of rupees...they are dealt with by investigating agencies in a different manner and the law does not act with the same harshness to these offenders," Justice Dhingra observed in a recent order. "This attitude of the investigating agencies is beyong comprehension," he said while directing the CBI to register a case against PankajAggarwal, the alleged mastermind in the scam. Aggarwal has his business in Dubai.

December 2005

1. Election Fund Scam - ? Crores

2. Operation Blackboard scam - 1000 crores

3. Oil for Food Scam - ?

January 2006

1. Rice Scam - 320 crores

2. Benami Demat Scam - 30 crores (Sanjay Pandey the same guy in cobbler scam pre 2005)

February 2006

1. Benami IPO Scam - 32 crores

2. Liquor Scam - 3600 crores

March 2006

1. Jaitley an MP who allegedly bailed out Ketan Parekh in Madhavpura Mercantile Co-operative Bank scam case (see Pre 2005 list) one of the biggest scammers enjoys a lavish lifestyle.

2. The controversial Scorpene Deal - ? crores

April 2006

1. MTNL GSM Scam - 450 crore

May 2006

1. Chautala Scam - 1400 crores

2. BPL Red Cards Scam - 1400 crores

June 2006

1. The Great Wheat Scam - ?

2. UTI Franchisee forgery - ? crores

3. Punjab State Council of Education Research and Training (SCERT) Scam - more than 3 crores

July 2006

1. BPO Scam - more than 3 crore

2. Bellary bribe - 150 crore

3. Duty Exemption Pass Book (DEPB) scheme Scam - 10 crore

August 2006

1. Unaccounted money on sale of petrol pumps - 18 crores

2. Punjab Chief Minister Captain Amarinder Singh goes on a multi-crore holiday extravaganza - 2.5 crores

3. Tata Finance scandal - ? crores

September 2006

1. Top Punjab cops booked for wireless sets scam - 5 crores

2. Koda Scandal - 2500 crores - Nov 09 - First arrest made Feb 10 - 1 crore ceized , UjjawalChaudhary, senior Income Tax (I-T) officer who was going to reveal connections with politicians and hawals traders abruptly shifted

3. Punjab Chief Minister Captain Amarinder Singh in real estate fraud - more than 2100 crores (See Aug 2006)

4. Earlier, all of them had got anticipatory bail from the Punjab and Haryana High Court. Today, they moved regular bail applications. A senior counsel of the Supreme Court appearing on behalf of Captain Amarinder Singh had stressed before the court that his client be granted regular bail till the conclusion of the trial.

5. “We are discussing legal recourse to be taken in the Apex Court. We may even file public interest litigation before the Supreme Court asking for intervention in the case. It is a mockery of the law we are witnessing in the case. Scores of witnesses are going back on their words. We may even demand the CBI inquiry into the change of stance by the witnesses,” - Report of Jan 2008

October 2006

1. West Bengal State Consumer’s Federation Ltd (CONFED) Paddy Scam - ? crore

2. SEZ Controversies - RBI fears of a revenue loss — some Rs. 170,000 crore over the next five years by way of income tax, excise and customs duties foregone (based on a NIPF study). Read More 1

3. DharmeshDoshi, Madhavpura Cooperative Bank scam - 1030 crores

4. Barak Missile Deal - 400 crore - The CBI case alleges that Rs 2 crore were paid to the president of a political party (Jaya Jaitley), who functioned from the residence of the then Defence Minister (George Fernandes). March 2008 Nandas claim innocence

5. Blood Test Kit Scam - ?

November 2006

1. Bangalore Development Authority and Bangalore MahanagaraPalike on illegal constructions - 180 crore

2. NSDL and CDSL bags illegitimate profits in an IPO manipulation scam - 116 crore

December 2006

1. SMS Con - 40-100 crore (Read more 1)

2. Agrofed job scam - ? crore

3. Haj Quota scam- bribes taken to illegally procure seats from the Government's subsidised Haj quota for 1 lakh muslims.

January 2007

1. Illegal Telephone Exchanges Scam - 1000 crores

2. Non-Banking Financial Companies (NBFC) Scam - swindled 12,000 crores of small investors before leaving the state

Karnataka State Government to award a meagre cash prize (Rs. 2,000) to JayantTinaikar, who reportedly exposed the fake stamp paper scam 12 years ago.February 2007

1. Uranium Corporation of India Limited Scam - 20 crores

2. Oriental Bank Scam - 596.44 crores

3. Mandankumar Scam - 3.5 crores

4. March 2007

5. Pune Hassan Ali Khan Scam - 50 crores - I-T department, ED, and IB estimates that several thousand crore rupees were routed out of India(possibly swiss banks) through havala and banking channels. (Read More 1 2)

6. Congress MP Moni Kumar Subba from Tezpur, lied about his Indian nationality for 16 years manages to scam the country off by 25000 crores

There is little chance of recovery in most of these cases as there are not many assets to recover the arrears, officials claimed.

April 2007

1. Air Ticket Booking Scam - 13 crores

2. The Royapettah Benefit Fund (RBF) in Chennai went bust drowning Rs 450 crore and leaving investors and depositors in the lurch a company allowed to operate by RBI.

3. Fertilizers Subsidies Scam - ? crores

May 2007

1. Arunachal Pradesh's corrupt governance: 1000 crores (Read more Misappropriation under former CM GegongApang and present incumbent DorjeeKhandu) Aug 10 - Apang arrested

There were a number of cases regarding mismanagement in the Public Distribution System. People in the villages were not getting enough food allotted by the Centre. Cooperative rural banking scams affected small depositors like labourers and teachers. The hydel power sector was also in doldrums.

1. SampoornGraminRojgarYogana Scam - 457 crores . Dec 07 - Scam referred to CBI.

A muti-crore scam under which the poor were deprived of foodgrains under the state scheme.A systematic loot was taking place in the state and the government was not willing to give permission for holding a CBI probe into the scam running into crores of rupees.

1. Warehouse Receipts Scandal - 500 crores

July 2007

1. Stock Holding Corporation of India Limited (SHCIL) Scam - ?

2. Hyderabad Metropolitan Water Supply and Sewerage Board (HMWS&SB) Scam - ?

3. Punjab Public Service Commission (PPSC) recruitment scam - 8 crores

Three judges of the High Court were found taking favours from Ravi Sidhu, former PPSC chairman. On April 19, 2004, 25 sitting judges of the High Court had gone on mass leave protesting Chief Justice B K Roy’s move to seek an explanation from two judges, Justice Vinay Mittal and Varinder Singh, who had allegedly applied for membership of a private golf course, Forest Hill Resort Club. The club was involved in litigation and was later demolished on the orders of the High Court. The club was illegally constructed in complete violation of Forest and Environment laws. Honorary memberships were given to IAS officers and the two judges to legitimise the illegalities

August 2007

1. Delhi Development Authority canteen owner Ashok Malhotra owned more than 50 cars and 10 motorcycles were recovered, all bearing special VIP number plates. Raid unearthed 5000 land documents, ? crores

2. Former Supreme Court Chief Justice YK Sabharwal was involved in dubious judicial deal-making that earned his sons huge profits. - ? crores

3. September 2007

4. Kerala State Cooperative Bank Scam - 2000 crores

5. Aircraft Import Scam - 1059 crores

6. Leave Travel Concession (LTC) Scam - loss of Rs 200 crore to Government and PSUs.

7. Indian Space Research Organisation (ISRO) Land Scam - ? crores

'ISRO comes directly under the prime minister and it is they who have to launch an inquiry and not us. If they are ready for it, then the state government will provide all necessary help,' - Kerala Chief Minister V.S. Achuthanandan

October 2007

1. Das filed the petition challenging the actions of the banks in waiving of around Rs 2,300 crore of public money arbitrarily without any valid reason. Describing this as the largest single waiver in the history of Indian banking industry.

2. Fake housing projects in north India - 500 crores - Y S Rana from Delhi. Rana was the owner of PS&G Developers and Engineers Ltd arrested by EOW.

3. Kidney Transplant Racket - ? crores more than a 1000 victims. (Read more 1 2 3 4bar)

4. Many innocent labourers lost their kidney in lure of money and job.The racket is believed to be spread in various states, including Jammu and Kashmir, Rajasthan, Haryana, Delhi and Maharashtra. Source

5. Coal India Ltd illegally diverted at least Rs10 crore from the funds it had collected for over a decade and meant for the Prime Minister’s National Relief Fund (PMNRF).

Part of the funds collected at the time of the Kargil war for the NDF have been transmitted as late as 27 August 2007, after the initiation of this inquiry.” The Kargil war happened in 1999.

December 2007

1. Funds collected for victims of the Kargil war, Orissa cyclone and Gujarat earthquake were misused by top IAS officers in Punjab - the documents prove that officers posted as deputy commissioners in Ludhiana, Patiala and Sangrur misappropriated and misused crores of money while heading the Red Cross societies in their districts.

2. Lucknow Development Authority (LDA) Land Scam - 6 crores

January 2008

1. Punjab VB arrests whistle-blower

Punjab vigilance bureau is penny wise and pound foolish. A sub-divisional officer (SDO) who blew the whistle on a scam worth crores was arrested by the bureau in an alleged graft case (see pre 2005 SNC Lavalin). While the SDO has been suspended, his own report on the utilisation of border area funds — exposing what is probably the tip of the iceberg — is gathering dust.

February 2008

1. Kolkotta Museum Scam - 18 crores

One of the biggest repositories of the country’s cultural and historical heritage, has been siphoning off crores of rupees under the pretext of preserving priceless artifacts, a probe has found.March 2008

1. Senior Punjab IAS officer suspended for going out of his way to help a company by hiring it without inviting tenders and extending advances without proper bank guarantees. The company failed to repay, causing loss of Rs 20 crore to the corporation.

2. KPMG - India is "fraud haven"

April 2008

1. BCCI Dalmiya Scam - ? crores

2. Illegal export of sandalwood - 5 crores

June 2008

1. Madhya Pradesh Health Minister Ajay Vishnoi quits after Income Tax raid on brother's premises - 500 crore

2. Hotel Le Meridien Credit card skimming - 1 crore

July 2008

1. Parliamentary horse trading - ? crores

2. Ghaziabad Provident Fund scam - 23 crores - involved 83 accused included 36 judges, including one sitting Supreme Court judge, 11 High Court judges and 24 judges of subordinate judiciary. Beneficiaries of the ill-gotten money which was siphoned off fraudulently on the basis of fake documents and fictitious government servants and withdrawal of crores of rupees from the provident fund account of third and fourth-grade employees in Ghaziabad region between 2001 and 2008.(Read more 1) Chief Justice of India KG Balakrishnan denied heading the bench hearing (Read more 1) Dec 08 - CBI says it would seek permission to interrogate the judges. Oct - 09 - Key accused dies of heart attack while in custody Jul 10 No evidence against 17 out 41 judges and 24 remaining judges

Ghaziabad police sought permission from the Chief Justice of India and Allahabad Court to initiate a probe against the judges accused in this scam. While the Allahabad High Court dismissed the petition summarily, at the Supreme Court, Chief Justice K. Balakrishnan handled the request with remarkable astuteness and ordered a novel method of investigation that would protect the prestige and the reputation of the judiciary as far as possible.August 2008

1. Fake Currency Scam in Uttar Pradesh Bank - 1.5 crores

September 2008

1. Fake RBI Cheques Scam - 14 crores

October 2008

1. ShirdiGhat Repair - ? crores

November 2008

1. Mid Day Meal Scam - 15.37 crores

2. 2G Spectrum Scam - 1,76,000 crores Dec 08 - Center claims that charges are baseless (Read more 1 2 3 4)

3. Satyam Computer's Emergency Management Research Institute (EMRI) Ambulance Services Scam - 5600 crores

December 2008

1. E-ticketing fraud - 5 crores

January 2009

1. 11 Directors of National Agricultural Marketing Federation of India (Nafed) face criminal action in a Rs3,700 crore fraud.

2. Satyam Fraud - 7 to 14000 crores - Pricewaterhouse Coopers saw no fraud in Satyam - Nov 09 CBI arrested Satyam's internal audit head V S Prabhakar Gupta for allegedly fabricating account books, just days before

it is due to file a second chargesheet in the multi-crore fraud at the IT firm. Jul 10 - Promoters wrongfully gained 2643 crores (Read more 1 2 3 4 5 6 7)

Reports said that investors like DSP Merrill Lynch, DSP Blackrock, ILFS Financial Services and Deutsche Bank offloaded their shares days before Satyam fraud came out in open.

Satyam Scam TimelineMay 2009

1. Computer Purchasing Fraud - 1.53 crores

2. Divine Homeopath Investment Manager - 1600 crore

3. Ordnance Factory Board (OFB) arms deal scam - ? crores - Jul 10 - 6 firms get blacklisted

4. Dr A S Bindra father of ace shooter AbhinavBindra and managing director of Punjab Meats Limited, DeraBassion had charges of cheating, fraud and forgery. He committed fraud with a Delhi-based private financial company, Apple India, to the tune of Rs 4.31 crore and with the IndusInd Bank to the tune of Rs 5 crore. (Read more 1)

June 2009

1. Ashok Jadeja Divine Ayurved and Money Multiplier - 100 to 1600 crores (Read more 1)

2. MCD 45000 Fake Employees Scam - 500-1000 crores annually

July 2009

1. Bitumen Scam - more than 100 crores

2. Chhattisgarh Paddy Scam - 4000 crores

August 2009

1. All India Council of Technical Education bribery scam - ? crores - Chairman R.A. Yadav, who drew a monthly salary of about Rs 80,000, had amassed property worth crores.

2. Metal Scrap Scam - ? crores

3. SBI Kanpur - 52 crores - Assistant General Manager, 2 Chief Managers and some senior managers, who were suspected to be directly involved in pilfering the bank by crediting fake cheques into select accounts.

September 2009

1. Austra Coke - 1000 crores

2. Bollywood star Nasir Khan figures in multi crore rupee chit fund scam - 191 crore

October 2009

1. Gold Quest Scam - 1100 crore

December 2009

1. Dr Suresh Dhotre medicine fraud - 47 crores

January 2010

1. IAS officer Pradeep Sharma Bheed Bazaar Land allotment scam - 70 crores

2. Railways and LIC Scam - 400 crores

February 2010

1. Bhopal Home Loan Scam - 2 crores

2. Wipro Embezzlement Fraud - 180 crores

3. Chak De India Scam - ?

4. PAN Card Scam - 3 crores

March 2010

1. Kandla Port Trust (KPT) Scam - ? crores - 16000 acres of land was leased out to few parties at nominal rates.

2. Fake Income Tax Returns Scam - 6 crores

April 2010

1. President of the Medical Council of India (MCI), Dr Ketan Desai in college scam - 500 crores - Demanded Rs 40 lakh from students seeking admission in a capitation fee racket and money for allotting seat as a management quota student. (Read more 1 2)

2. Financial Fraud hits 87% of Indian companies

Perception of Fraud in IndiaJune 2010

1. Canara Bank defrauded - 9.14 crore

2. Railway Recruitment Board Paper Leak - 15.5 crore (Read more 1 2)

July 2010

1. LalitModi Indian Premier League (IPL) Scam - 1200 crores (Read more 1)

August 2010

1. Commonwealth Games Scam - 8000 crores (Read more 1 2)

September 2010

1. Senior citizen savings scheme (SCSS) Post Office Scam - 2 crores (Read more 1)

October 2010

1. International Film Festival of India (IFFI) Infrastructure creation Scam in Goa - ? crores

November 2010

1. State-owned Mineral Scrap Trading Corporation (MSTC) was defrauded by jewelery traders - 1400 crores

December 2010

1. Citibank swindle - 300 crores

( courtesy:Kaushik's Blog)

The dot-com bubble (also referred to as the dot-com boom, the Internet bubble and the Information Technology Bubble[1]) was a historic speculative bubble covering roughly 1997 – 2000 (with a climax on March 10, 2000, with the NASDAQ peaking at 5132.52 in intraday trading before closing at 5048.62) during which stock markets in industrialized nations saw their equity value rise rapidly from growth in the Internet sector and related fields. While the latter part was a boom and bust cycle, the Internet boom is sometimes meant to refer to the steady commercial growth of the Internet with the advent of the World Wide Web, as exemplified by the first release of the Mosaic web browser in 1993, and continuing through the 1990s.

The period was marked by the founding (and, in many cases, spectacular failure) of a group of new Internet-based companies commonly referred to as dot-coms. Companies were seeing their stock prices shoot up if they simply added an "e-"

prefix to their name and/or a ".com" to the end, which one author called "prefix investing".[2]

A combination of rapidly increasing stock prices, market confidence that the companies would turn future profits, individual speculation in stocks, and widely available venture capital created an environment in which many investors were willing to overlook traditional metrics such as P/E ratio in favor of confidence in technological advancements.

The collapse of the bubble took place during 2000-2001. Some companies, such as Pets.com, failed completely. Others lost a large portion of their market capitalization but remained stable and profitable, e.g., Cisco, whose stock declined by 86%. Some later recovered and surpassed their dot-com-bubble peaks, e.g., Amazon.com, whose stock went from 107 to 7 dollars per share, but a decade later exceeded 200.

Contents

[hide]

• 1 Bubble growth

• 2 Soaring stocks

• 3 Free spending

• 4 The bubble bursts

• 5 Aftermath

• 6 List of companies significant to the bubble

• 7 See also

o 7.1 Terminology

o 7.2 Media

o 7.3 Venture capital

o 7.4 Economic downturn

• 8 References

• 9 Further reading

• 10 External links

[edit] Bubble growth

Venture capitalists saw record-setting growth as dot-com companies experienced meteoric rises in their stock prices and therefore moved faster and with less

caution than usual, choosing to mitigate the risk by starting many contenders and letting the market decide which would succeed. The low interest rates in 1998–99 helped increase the start-up capital amounts. A canonical "dot-com" company's business model relied on harnessing network effects by operating at a sustained net loss to build market share (or mind share). These companies offered their services or end product for free with the expectation that they could build enough brand awareness to charge profitable rates for their services later. The motto "get big fast" reflected this strategy.

[edit] Soaring stocks

In financial markets, a stock market bubble is a self-perpetuating rise or boom in the share prices of stocks of a particular industry. The term may be used with certainty only in retrospect when share prices have since crashed. A bubble occurs when speculators note the fast increase in value and decide to buy in anticipation of further rises, rather than because the shares are undervalued. Typically many companies thus become grossly overvalued. When the bubble "bursts," the share prices fall dramatically, and many companies go out of business.

American news media, including respected business publications such as Forbes and the Wall Street Journal, encouraged the public to invest in risky companies, despite many of the companies' disregard for basic financial and even legal principles.[3]

Andrew Smith [4] has argued that the Financial Industry's handling of Initial Public offerings tended to benefit the banks and initial investors rather than the company itself. This is because company staff were typically barred from reselling their shares for a lock-in period of 12 to 18 months and so did not benefit from the common pattern of a huge short-lived spike in the share price on the day of the launch. By contrast, the financiers and other initial investors were typically entitled to sell at the peak price, and so could immediately profit from short-term price rises. Smith argues that the high profitability of the IPOs to Wall Street was a significant factor the course of events of the bubble. He writes:

"...But did the kids [the often young dotcom entrepreneurs] dupe the establishment by drawing them into fake companies, or did the establishment dupe the kids by introducing them to Mammon and charging a commission on it?"

In spite of this, however, a few company founders made vast fortunes when their companies were bought out at an early stage in the dot-com stock market bubble. These early successes made the bubble even more buoyant. An unprecedented amount of personal investing occurred during the boom, and the press reported the phenomenon of people quitting their jobs to become full-time day traders.[5][6][7]

[edit] Free spending

This section needs additional citations for verification. Please help improve this article by adding citations to reliable sources. Unsourced material may be challenged and removed. (March 2013)

According to dot-com theory, an Internet company's survival depended on expanding its customer base as rapidly as possible, even if it produced large annual losses. For instance, Google and Amazon did not see any profit in their first years. Amazon was spending on expanding customer base and alerting people to its existence and Google was busy spending on creating more powerful machine capacity to serve its expanding search engine.[citation needed] The phrase "Get large or get lost" was the wisdom of the day.[8] At the height of the boom, it was possible for a promising dot-com to make an initial public offering (IPO) of its stock and raise a substantial amount of money even though it had never made a profit — or, in some cases, earned any revenue whatsoever.[citation needed] In such a situation, a company's lifespan was measured by its burn rate: that is, the rate at which a non-profitable company lacking a viable business model ran through its capital served as the metric.

Public awareness campaigns were one of the ways in which dot-coms sought to expand their customer bases. These included television ads, print ads, and targeting of professional sporting events. Many dot-coms named themselves with onomatopoeic nonsense words that they hoped would be memorable and not easily confused with a competitor. Super Bowl XXXIV in January 2000 featured 17 dot-com companies that each paid over $2 million for a 30-second spot. By contrast, in January 2001, just three dot-coms bought advertising spots during Super Bowl XXXV. In a similar vein, CBS-backed iWon.com gave away $10 million to a lucky contestant on an April 15, 2000 half-hour primetime special that was broadcast on CBS.

Not surprisingly, the "growth over profits" mentality and the aura of "new economy" invincibility led some companies to engage in lavish internal spending, such as elaborate business facilities and luxury vacations for employees. Executives and employees who were paid with stock options instead of cash became instant millionaires when the company made its initial public offering; many invested their new wealth into yet more dot-coms.

Cities all over the United States sought to become the "next Silicon Valley" by building network-enabled office space to attract Internet entrepreneurs. Communication providers, convinced that the future economy would require ubiquitous broadband access, went deeply into debt to improve their networks with high-speed equipment and fiber optic cables. Companies that produced network equipment like Nortel Networks were irrevocably damaged by such over-extension; Nortel declared bankruptcy in early 2009. Companies like Cisco, which did not have any production facilities, but bought from other manufacturers, were able to leave quickly and actually do well from the situation as the bubble burst and products were sold cheaply.

In the struggle to become a technology hub, many cities and states used tax money to fund technology conference centers, advanced infrastructure, and created favorable business and tax law to encourage development of the dot com industry in their locale. Virginia's "Technology Corridor" is a prime example of this activity. Large quantities of high speed fiber links were laid, and the State and local governments gave tax exemptions to technology firms. Many of these buildings could be viewed along I-495, after the burst, as vacant office buildings.

Similarly, in Europe the vast amounts of cash the mobile operators spent on 3G licences in Germany, Italy, and the United Kingdom, for example, led them into deep debt. The investments were far out of proportion to both their current and projected cash flow, but this was not publicly acknowledged until as late as 2001 and 2002. Due to the highly networked nature of the IT industry, this quickly led to problems for small companies dependent on contracts from operators. One example is of a then Finnish mobile network company Sonera, which paid huge sums in German broadband auction then dubbed as 3G licenses. 3rd generation networks however took years to catch on and Sonera ended up as a part of TeliaSonera, then simply Telia.

[edit] The bubble bursts

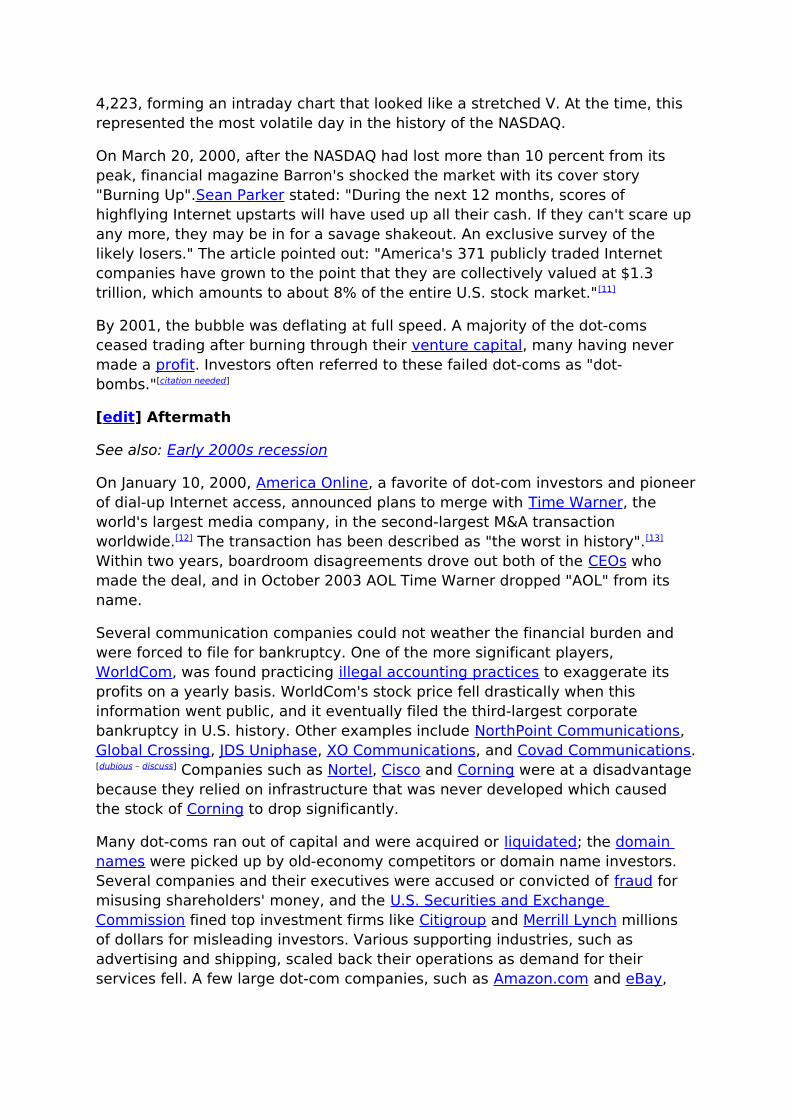

The technology-heavy NASDAQ Composite index peaked at 5,048 in March 2000, reflecting the high point of the dot-com bubble.

Over 1999 and early 2000, the U.S. Federal Reserve increased interest rates six times,[9] and the economy began to lose speed. The dot-com bubble burst, numerically, on Friday, March 10, 2000, when the technology heavy NASDAQ Composite index, peaked at 5,048.62 (intra-day peak 5,132.52), more than double its value just a year before.[10] The NASDAQ fell slightly after that, but this was attributed to correction by most market analysts; the actual reversal and subsequent bear market may have been triggered by the adverse findings of fact in the United States v. Microsoft case which was being heard in federal court.[citation needed] The findings, which declared Microsoft a monopoly, were widely expected in the weeks before their release on April 3.[citation needed] The following day, April 4, the NASDAQ fell from 4,283 points to 3,649 and rebounded back to

4,223, forming an intraday chart that looked like a stretched V. At the time, this represented the most volatile day in the history of the NASDAQ.

On March 20, 2000, after the NASDAQ had lost more than 10 percent from its peak, financial magazine Barron's shocked the market with its cover story "Burning Up".Sean Parker stated: "During the next 12 months, scores of highflying Internet upstarts will have used up all their cash. If they can't scare up any more, they may be in for a savage shakeout. An exclusive survey of the likely losers." The article pointed out: "America's 371 publicly traded Internet companies have grown to the point that they are collectively valued at $1.3 trillion, which amounts to about 8% of the entire U.S. stock market."[11]

By 2001, the bubble was deflating at full speed. A majority of the dot-coms ceased trading after burning through their venture capital, many having never made a profit. Investors often referred to these failed dot-coms as "dot-bombs."[citation needed]

[edit] Aftermath

See also: Early 2000s recession

On January 10, 2000, America Online, a favorite of dot-com investors and pioneer of dial-up Internet access, announced plans to merge with Time Warner, the world's largest media company, in the second-largest M&A transaction worldwide.[12] The transaction has been described as "the worst in history".[13] Within two years, boardroom disagreements drove out both of the CEOs who made the deal, and in October 2003 AOL Time Warner dropped "AOL" from its name.

Several communication companies could not weather the financial burden and were forced to file for bankruptcy. One of the more significant players, WorldCom, was found practicing illegal accounting practices to exaggerate its profits on a yearly basis. WorldCom's stock price fell drastically when this information went public, and it eventually filed the third-largest corporate bankruptcy in U.S. history. Other examples include NorthPoint Communications, Global Crossing, JDS Uniphase, XO Communications, and Covad Communications.[dubious – discuss] Companies such as Nortel, Cisco and Corning were at a disadvantage because they relied on infrastructure that was never developed which caused the stock of Corning to drop significantly.

Many dot-coms ran out of capital and were acquired or liquidated; the domain names were picked up by old-economy competitors or domain name investors. Several companies and their executives were accused or convicted of fraud for misusing shareholders' money, and the U.S. Securities and Exchange Commission fined top investment firms like Citigroup and Merrill Lynch millions of dollars for misleading investors. Various supporting industries, such as advertising and shipping, scaled back their operations as demand for their services fell. A few large dot-com companies, such as Amazon.com and eBay,

survived the turmoil and appear assured of long-term survival, while others such as Google have become industry-dominating mega-firms.

The stock market crash of 2000–2002 caused the loss of $5 trillion in the market value of companies from March 2000 to October 2002.[14] The 9/11 terrorist destruction of the World Trade Center's Twin Towers, killing almost 700 employees of Cantor-Fitzgerald, accelerated the stock market drop; the NYSE suspended trading for four sessions. When trading resumed, some of it was transacted in temporary new locations.

More in-depth analysis shows that 90% of the dot-coms companies survived through 2004.[15] With this, it is safe to assume that the assets lost from the Stock Market do not directly link to the closing of firms. More importantly, however, it can be concluded that even companies who were categorized as the "small players" were adequate enough to endure the destruction of the financial market during 2000-2002.[15] Additionally, retail investors who felt burned by the burst transitioned their investment portfolios to more cautious positions.

Nevertheless, laid-off technology experts, such as computer programmers, found a glutted job market. University degree programs for computer-related careers saw a noticeable drop in new students. Anecdotes of unemployed programmers going back to school to become accountants or lawyers were common.

Turning to the long-term legacy of the bubble, Fred Wilson, who was a venture capitalist during it, said:

"A friend of mine has a great line. He says 'Nothing important has ever been built without irrational exuberance'. Meaning that you need some of this mania to cause investors to open up their pocketbooks and finance the building of the railroads or the automobile or aerospace industry or whatever. And in this case, much of the capital invested was lost, but also much of it was invested in a very high throughput backbone for the Internet, and lots of software that works, and databases and server structure. All that stuff has allowed what we have today, which has changed all our lives. …that's what all this speculative mania built."[4]

[edit] List of companies significant to the bubble

For discussion and a list of dot-com companies outside the scope of the dot-com bubble, see dot-com company.

• Boo.com , spent $188 million in just six months[16] in an attempt to create a global online fashion store. Went bankrupt in May 2000.[17]

• Startups.com was the "ultimate dot-com startup." Went out of business in 2002.

• e.Digital Corporation (EDIG): Long term unprofitable OTCBB traded company founded in 1988 previously named Norris Communications. Changed its name to e.Digital in January 1999 when stock was at $0.06 level. The stock rose rapidly in 1999 and went from closing price of $2.91

on December 31, 1999 to intraday high of $24.50 on January 24, 2000. It quickly retraced and has traded between $0.07 and $0.165 in 2010 .[18]

• Freeinternet.com – Filed for bankruptcy in October 2000, soon after canceling its IPO. At the time Freeinternet.com was the fifth largest ISP in the United States, with 3.2 million users.[19] Famous for its mascot Baby Bob, the company lost $19 million in 1999 on revenues of less than $1 million.[20][21]

• GeoCities , purchased by Yahoo! for $3.57 billion in January 1999.[22] Yahoo! closed GeoCities on October 26, 2009.[23]

• theGlobe.com – Was a social networking service, that went live in April 1995 and made headlines by going public on November 1998 and posting the largest first day gain of any IPO in history up to that date. The CEO became in 1999 a visible symbol of the excesses of dot-com millionaires.

• GovWorks.com – the doomed dot-com featured in the documentary film Startup.com .

• pets.com - a former dot-com enterprise that sold pet supplies to retail customers before entering bankruptcy in 2000.

• open.com - Was a big software security producer, reseller and distributor, declared in bankruptcy in 2001.

• InfoSpace – In March 2000 this stock reached a price $1,305 per share,[24] but by April 2001 its price had crashed down to $22 a share.[24]

• lastminute.com , whose IPO in the UK coincided with the bursting of the bubble.

• The Learning Company , bought by Mattel in 1999 for $3.5 billion, sold for $27.3 million in 2000.[25]

• Think Tools AG , one of the most extreme symptoms of the bubble in Europe: market valuation of CHF 2.5 billion in March 2000, no prospects of having a substantial product (investor deception), followed by a collapse.[26]

• Webvan , an online grocer that operated on a "credit and delivery" system; the original company went bankrupt in 2001. It was later resurrected by Amazon.

• WorldCom , a long-distance telephone and internet-services provider that became notorious for using fraudulent accounting practices to increase their stock price. The company filed for bankruptcy in 2002 and former CEO Bernard Ebbers was convicted of fraud and conspiracy.

• Xcelera.com , a Swedish investor in start-up technology firms.[27] "Greatest one-year rise of any exchange-listed stock in the history of Wall Street." [28]

• Broadcast.com was acquired by Yahoo! for $5.9 billion in stock, making Mark Cuban a multi-billionaire. The site is now defunct and redirects to Yahoo's home page. [1]

• MicroStrategy , whose shares lost more than half their value on March 20, 2000, following their announcement of re-stated financials for the previous two years. A BusinessWeek editorial said at the time, "The company's misfortune is a wake-up call to all dot-com investors. The message: It's time, at last, to pay attention to the numbers." [29]

• inktomi with a valuation of $25 billion in March 2000.

[edit] See also

Internet portal

Economics portal

[edit] Terminology

• Digital Revolution

• E-commerce

• The Long Tail

• South Sea Company

• Tulip mania

• Techno-utopianism

• Technology hype

• Web 2.0

• E-learning

• Dark fiber

[edit] Media

• e-Dreams

• SatireWire

• ebay.com

[edit] Venture capital

• List of venture capital firms

[edit] Economic downturn

• Financial crisis of 2007-2010

• Subprime mortgage crisis

• United States housing bubble

[edit] References

1. ̂ James K. Galbraith and Travis Hale (2004). Income Distribution and the Information Technology Bubble. University of Texas Inequality Project Working Paper

2. ̂ Nanotech Excitement Boosts Wrong Stock , The Market by Mike Maznick, Techdirt.com, Dec 4, 2003

3. ̂ Origins of the Crash: The Great Bubble and Its Undoing, Roger Lowenstein, Penguin Books, 2004, ISBN 1-59420-003-3, ISBN 978-1-59420-003-8 page 114-115.

4. ^ abTotally Wired - on the trail of the great dotcom swindleAndrew Smith (author) Bloomsbury Books 2012 ISBN 978-1-84737-449-3

5. ̂ Kadlec, Daniel (1999-08-09). "Day Trading: It's a Brutal World". Time. http://www.time.com/time/magazine/article/0,9171,991726,00.html. Retrieved 2007-10-09.

6. ̂ Johns, Ray (1999-03-04). "Daytrader Trend". Online Newshour: Forum. PBS. http://www.pbs.org/newshour/forum/february99/daytraders.html. Retrieved 2007-10-09.

7. ̂ Cringely, Robert X. (1999-12-16). "There's a Sucker Born Every 60,000 Milliseconds". I, Cringely. PBS. http://www.pbs.org/cringely/pulpit/1999/pulpit_19991216_000634.html. Retrieved 2007-10-09.

8. ̂ How to Start a Startup , March 2005, Paul Graham

9. ̂ "FRB: Monetary Policy, Open Market Operations" . http://www.federalreserve.gov/fomc/fundsrate.htm. Retrieved 2009-07-01.

10. ̂ "March Nasdaq Historical Prices Charts - Historical Commodity Futures Charts'". Futures.tradingcharts.com. http://futures.tradingcharts.com/historical/ND/1999/3/linewchart.html. Retrieved 2012-11-26.

11. ̂ Burning Up , By JACK WILLOUGHBY, March 20, 2000, Barrons

12. ̂ Worldwide Mergers & Acquisitions , Statistics on Mergers & Acquisitions (M&A)

13. ̂ Goldman, David (February 3, 2010). "Time Warner hikes dividend as outlook brightens". CNN. http://money.cnn.com/2010/02/03/news/companies/time_warner/. Retrieved March 9, 2013.

14. ̂ Gaither, Chris; Chmielewski, Dawn C. (July 16, 2006). "Fears of Dot-Com Crash, Version 2.0". Los Angeles Times. http://articles.latimes.com/2006/jul/16/business/fi-overheat16. Retrieved March 9, 2013.

15.^ ab Goldfarb, Brent; Kirsch, David; Miller, David A. (2007). "Was there too little entry during the Dot Com Era?".Journal of Financial Economics86 (1): 100–44. doi:10.1016/j.jfineco.2006.03.009. Preprint available at SSRN 871210

16. ̂ "INTERNATIONAL BUSINESS; Fashionmall.com Swoops In for the Boo.com Fire Sale". The New York Times. June 2, 2000. http://query.nytimes.com/gst/fullpage.html?res=9F05E4DB103CF931A35755C0A9669C8B63. Retrieved May 1, 2010.

17. ̂ "Top 10 dot-com flops –" . Cnet.com. http://www.cnet.com/4520-11136_1-6278387-1.html. Retrieved 2012-11-26.

18. ̂ "Historical prices of EDIG stock" . Finance.yahoo.com. http://finance.yahoo.com/q/hp?s=EDIG.OB&a=00&b=1&c=2000&d=01&e=15&f=2000&g=d. Retrieved 2012-11-26.

19. ̂ "Another One Bites the Dust – FreeInternet.com Files for Bankruptcy –". Addlebrain.com. 2000-10-09. http://www.addlebrain.com/articles/freei.html. Retrieved 2012-11-26.

20. ̂ "InternetNews Realtime IT News – Freeinternet.com Scores User Surge". Internetnews.com. 2000-08-11. http://www.internetnews.com/xSP/article.php/435691. Retrieved 2012-11-26.

21. ̂ ISP-Planet – News – Freei Files for Bankruptcy [dead link]

22. ̂ "Yahoo! buys GeoCities" . CNN. January 28, 1999. http://money.cnn.com/1999/01/28/technology/yahoo_a/. Retrieved March 9, 2013.

23. ̂ Shaer, Matthew (October 26, 2009). "GeoCities, a relic of an different web era, shuttered by Yahoo". The Christian Science Monitor.

http://www.csmonitor.com/Innovation/Horizons/2009/1026/geocities-a-relic-of-an-different-web-era-shuttered-by-yahoo. Retrieved March 9, 2013.

24.^ a b "The two faces of InfoSpace 1998-2001" . The Seattle Times. http://seattletimes.nwsource.com/art/news/business/infospace/infospaceTimelineDay1_2_intro.swf.

25. ̂ Abigail Goldman (2002-12-06). "Mattel Settles Shareholders Lawsuit For $122 Million". Los Angeles Times. http://securities.stanford.edu/news-archive/2002/20021206_Settlement05_Goldman.htm.

26. ̂ Don't Think Twice: Think Tools is Overvalued, The Wall Street Journal Europe, October 30, 2000

27. ̂ Xcelera's FAQ's

28. ̂ Xcelera.com , GeorgeNichols.com

29. ̂ "Commentary: Earth to Dot-Com Accountants" . http://www.businessweek.com/2000/00_14/b3675112.htm.

The Dot-com bubble or IT bubble was a dramatic boom-bust cycle of the American economy during the years 1995–2002.

The height of the boom was characterized by enormous increases in stock prices, and especially the prices of Internet-related assets. The bust saw the rapid decline of most of the same prices. The Internet companies whose share prices were bid up came to be known as "dot-com" companies, from the common Internet domain name extension, ".com." In addition to the stock market bubble, the period in question saw increasing consumer leverage, a booming housing market, increasing debt-to-equity ratios, and lower down payments on homes. The turn that came in 2000 triggered the liquidation of boom-inspired malinvestments. The Federal Reserve attempted to engineer a "soft landing" with a moderate tightening of credit conditions. By the end of 2000 the NASDAQ slid to 2471 from the March peak of 5048.[1]

Contents

[hide]

• 1 Background

o 1.1 IPO Boom

o 1.2 Monetary policy

o 1.3 1997–1998: A time of crisis

• 2 The Boom

• 3 The burst of the bubble

• 4 The Bust

• 5 Predictions

• 6 References

• 7 Links

[edit] Background

The boom began against a backdrop of generally improving economic conditions in the U.S. in 1993 and 1994. The Plaza Accord of 1985 had improved the profitability of U.S. manufacturing, as the G-5 powers agreed to subsidize U.S. exporters by artificially lowering the exchange rate of the U.S. dollar. (One author identifies the Plaza Accord and the accompanying monetary expansion in Japan as the beginning of that country’s own boom and bust.) The American economy had come out of the recession of 1990–1991 in fair shape, with some of the misallocations of the 1980s boom having been corrected. It seemed investments in information technology were finally paying off, and manufacturing productivity was increasing. The stock market began to climb in 1993, and the recovery looked robust enough that the Federal Reserve began to raise rates.

But, beginning with the Mexican crisis and bailout of late 1994 and early 1995, the Federal Reserve was faced with a series of financial collapses. Over the rest of the nineties, the Federal Reserve oscillated between halfhearted attempts to restrain the equity boom and responding to crises that it believed called for reversing the previous restraint. In the meantime, theories of a "new economy" developed, both inside and outside the Federal Reserve, to justify soaring asset prices.

The "Reverse Plaza Accord" was an important factor in creating the late nineties boom. By that agreement, the big three powers (the U.S., Japan, and Germany) bailed out a Japanese manufacturing economy that was slowing to a halt under the pressure of the record-breaking ascent of the yen. They did so by engineering a striking reversal of the steep decline of the exchange rate of the dollar that had taken place over the previous decade.

Japanese manufacturing firms were faltering in 1995. "By April 1995, the yen had reached an all-time high of 79 to the dollar. . . . With the currency at such a pinnacle, Japanese producers could not even cover their variable costs". Many Japanese banks were facing insolvency. The U.S. had just gone through the Mexican bailout, and authorities were not enthusiastic about having to face a similar bailout scaled up to the size of the Japanese economy. The Reverse Plaza Accord was, in effect, an agreement that the U.S., German, and Japanese

governments would subsidize American consumers’ purchases of Japanese and German manufactured goods. The reversal of the exchange rate trend "was to be accomplished by lowering Japanese interest rates with respect to those in the U.S., but also by substantially enlarging Japanese purchases of dollar-denominated instruments such as Treasury bonds, as well as purchases of dollars by Germany and the U.S. government itself".

Driving the dollar up against foreign currencies would allow the U.S. government to maintain a stance of monetary ease without raising the CPI, since the artificially lowered price of imported goods would tend to counter the price-raising effect of the increased liquidity.

But liquidity has to go somewhere. One place it went was into the U.S. stock market. Another was into the asset markets of the East Asian countries whose currencies were tied to the dollar. The perverse effect of the flows was that, even as the manufacturing profitability of American and East Asian producers was undermined by the rising cost (in the yen and in various European currencies) of both their imported capital goods and their exported output, American and East Asian asset prices were given a further impetus upwards, as Japanese and European investors earned profits from both exchange rate movements and the rise of the American and East Asian stock markets in terms of the native currencies of those markets.

Given that some of the consequences of this policy appear obvious in retrospect, it is reasonable to ask what the thinking of the people who orchestrated the Reverse Plaza Accord was. The chief motivation seems to have been a desire to undo the previous distortions of the Plaza Accord, especially the decline of German and Japanese manufacturing, without too much pain.[1]

[edit] IPO Boom

During 1994 and early 1995, the Internet had begun to enter the broad public consciousness. One of the most prominent companies involved in the transformation of what had been a chiefly academic network into a giant commercial phenomenon was Netscape. Three million copies of Netscape Navigator had been downloaded in three months after its initial release, "making it one of the most popular pieces of software ever launched."

The legendary Netscape initial public offering (IPO) occurred in August of 1995. When planning to take Netscape public, the price at between $12 and $14 a share was found too low, the quantity demanded far outstripped the supply of shares. Morgan Stanley raised the initial price to $28, valuing a fledgling, profitless company at more than a billion dollars. The day the stock began trading on the open market, the demand for shares was so high that the Morgan Stanley traders were unable to find a market-clearing price for two hours after the session began. When Netscape shares finally publicly traded, the stock was priced at $71. It closed the day at 58¼, a first day gain of 108 percent, valuing the company at $2.2 billion. As a commentator said, "Pretty much everybody involved in the IPO had gotten seriously rich."

The Netscape IPO served as a highly visible symbol for the potential of the Internet, and the potential investor profits that might be gained by arriving at the dot-com party early.[1] A few company founders made vast fortunes when their companies were bought out at an early stage in the dot-com stock market bubble. These early successes made the bubble even more buoyant. An unprecedented amount of personal investing occurred during the boom, and the press reported the phenomenon of people quitting their jobs to become full-time day traders.[2][3][4]

[edit] Monetary policy

In March of 1995, following the U.S. bailout of the Mexican economy (and holders of Mexican bonds), the Fed ended its credit tightening campaign begun about a year earlier, and, starting in July 1995, it quickly lowered rates by three-quarters of a percentage point. Meanwhile, the technology-heavy NASDAQ Composite began to rise rapidly, crossing 1,000 for the first time ever. The index rose over 27 percent in a 10-month period.

The Bank of Japan was easing over the same time period, cutting its discount rate from 1.75 percent to 0.5 percent. The policy of maintaining a large interest-rate differential between U.S. and Japanese central bank rates gave rise to the profitable "carry trade," whereby investors would borrow yen at low rates and reinvest at a higher yield in the U.S. The interest rate differential available from the carry trade, combined with the orchestrated rise of the dollar against the yen, meant that as long as the Reverse Plaza Accord held, investors were offered a nearly guaranteed profit by borrowing yen in Japan to invest in U.S. financial assets denominated in dollars. Such an arrangement could not but accelerate the rise in the price of U.S. financial assets. In addition, Asian governments became large buyers of U.S. government securities, helping to send foreign sales of U.S. government securities to several times the level of the early nineties. The already historically high $197.2 billion of sales registered in 1995 rose to $312 billion in 1996.

Even at full employment, the Federal Reserve can stimulate the economy, but the effect of such stimulation is temporary. Long-run considerations—of inflation and economic discoordination—warn against monetary ease in such circumstances. The duration of the seemingly positive but temporary effects of monetary stimulation—the "overheating"—is believed to be roughly 18 months. The most likely episodes of overheating, then, occur in the 18 months prior to a national election. This is the key implication of modern political business cycle theory and is consistent with the Austrian theory of the business cycle. The Fed cut the discount rate in late January of 1996. While a mild increase in the unemployment rate, whatever its actual cause, may have provided some "cover" for the Federal Reserve, there was widespread belief that its monetary tools were being wielded against the Republican party and not against the winter storms. The fact that the expiration of Greenspan’s second four-year term—and

possible reappointment to a third term—fell in March 1996 added an extra element of politics to this particular political business cycle.

When the unemployment rate dropped further and further below the 5 percent level, Greenspan became receptive to the idea that the long-established full-employment range was no longer applicable. The apparent productivity of the labor force had ushered in a "New Economy." The similarity of that phrase to the 1920s slogan, a "New Plateau of Prosperity," seemingly did not attract the notice of the Fed chairman, despite the fact that in his youth he had studied and lectured on the Great Depression, employing the Austrian theory of the business cycle.[1]

[edit] 1997–1998: A time of crisis

A series of economic crises—in East Asia, in Russia, in Brazil, and in the U.S. itself with the Long-Term Capital Management failure and the potential Y2K problem—created a situation in which the Federal Reserve felt obliged to supply repeated influxes of liquidity to the market. As a result, after increasing at a rate of less than 2.5 percent during the first three years of the Clinton administration, MZM (money zero maturity) increased over the next three years (1996–1998) at an annualized rate of over 10 percent, rising during the last half of 1998 at a binge rate of almost 15 percent.

The problems inherent in the Reverse Plaza Accord first appeared in East Asia in early 1997. A significant portion of the enormous increase in liquidity worldwide, originating primarily from the American and Japanese central banks, had flowed into investments in that region. Between 1990 and 1995, 74.5 percent of capital flows to less developed countries went to East Asia. Governments there, operating on the mercantilist Japanese model of development, subsidized a rapid industrial buildup, often channeled into certain "strategic industries" such as high tech manufacturing. Because they partially funded the subsidies by borrowing in dollars, they were reluctant to loosen their pegs, as the cost of paying back dollar loans would increase in terms of the local currency.

However, "[b]etween April 1995 and April 1997, the yen fell by 60 percent . . . with respect to the dollar". If East Asian governments wished to maintain their peg to the dollar, they had to let their currencies rise against the yen as well. But that led to a steady rise in the price of their exports compared to those of their Japanese competitors. The East Asian countries had committed to the U.S. policy of subsidizing German and Japanese manufacturers and their own consumers at the expense of their own manufacturers. However, with smaller economies, manufacturing bases already distorted through extensive subsidies, and without being able to print the world’s reserve currency at will, East Asian governments lacked the ability to sustain such a policy as long as their American counterpart. Corporate profits declined throughout East Asia. In South Korea, for instance, they fell 75 percent in 1996, and went negative in 1997 and 1998.

When, one by one, the East Asian governments finally surrendered their pegs, the value of their countries’ dollar debt rose dramatically in terms of the local

currency. The crisis in East Asia "steadily worsened . . . Throughout much of 1998, stock markets continued to fall and, as money flooded out of the region, currencies swooned, placing great pressure . . . on the rest of the world economy". The crisis spread to Russia in the summer of 1998, when it defaulted on its sovereign debt, much of which was held by U.S. investment banks. "The Brazilian economy started to melt down shortly thereafter". And Japan labored under a "hefty new value-added tax," which, along with other factors, "subtracted . . . the equivalent of 2 per cent of GDP".

The climax came on 20 September, when the huge Long-Term Capital Management hedge fund (LTCM) admitted to the authorities that it was facing massive losses. The Fed then made its three famous successive interest rate cuts, including one dramatic reduction in between its meetings. The Fed also encouraged U.S. Government Sponsored Enterprises— including the FNMA, GNMA, FHLMC, and FHA—to engage in a spate of lending (and borrowing) entirely unprecedented in their history.

The Federal Reserve, during a period of over a decade, had attempted to build a "firewall" protecting the "real" economy from Wall Street shocks. But firewalls work both ways: Protecting the real economy from Wall Street shocks also disconnected Wall Street from the real economy. Hedged on the downside by what could be called "Fed insurance" against falling asset prices, investing on Wall Street began to look better and better compared to investing in the messy "real" economy, where one might lose one’s money.[1]

[edit] The Boom

By 1999, the liquidity party was in full swing. The rate on 30-year Treasuries had dropped from a high of over 7 percent to a low of 5 percent. The stock markets continued to soar. The NASDAQ Composite rose over 80 percent in 1999 alone. People who had stayed in the sidelines during the early part of the festivities began to feel left out. With abundant credit being freely served to Internet startups, hordes of corporate managers, who had seemed married to their stodgy blue-chip companies, suddenly were romancing some young and sexy dot-com.

It is possible to invest more and more if enough consumption is forgone to fully fund the investments being planned. However, during the dot-com boom, both investment and consumption exploded in the U.S. economy. Between 1950 and 1992, the personal savings rate had never gone above 10.9 per cent and never fallen below 7.5 per cent, except in three isolated years. But, between 1992 and 2000, it plummeted from 8.7 per cent to -0.12 per cent. By 2000, households’ outstanding debt as a proportion of personal disposable income reached the all-time high of 97 per cent, up from an average of 80 per cent during the second half of the 1980s. At the same time that consumers were saving less and borrowing more, businesses were increasing their capital spending.

The height of the bubble could, to some extent, be measured by the surge in number and decline in quality of IPOs, especially during 1999. The value of IPO

offerings nearly doubled from 1998 to 1999 alone. Between 1986 and 1990, the San Francisco Bay area saw 90 IPOs, while between 1996 and 2000 there were 390. Before the second half of the 1990s, it was generally considered mandatory for a business to have had at least several profitable quarters before it went public. But by 1999, companies were going public with little more than a sketchy business plan, an Internet address, and a few twenty-somethings who could speak the right lingo. From June 1995 to March 2000, MZM grew 52 percent, well ahead of real GDP growth of 22 percent for the same period.

The stock market, especially the high technology NASDAQ, seemed to levitate as Y2K liquidity hit the market in late 1999 and early 2000. The NASDAQ Composite index moved from 2746 at the end of September 1999 to 5048 on March 10, 2000, an 83 percent rise in under six months!

During the final quarter of the year 1999, the Fed, in anticipation of a possible Y2K liquidity crisis, pumped sufficient liquidity into the banking system to bring down the Federal Funds Rate from 5.5 per cent to below 4 per cent—the widest deviation from its target rate in over nine years —and thereby paved the way for the last frantic, record-shattering upward lunge in the equity markets, which took place in the first quarter of 2000. Bank loans thus raced ahead at a 19.4 per cent annual pace during the fourth quarter of 1999, the highest in at least fifteen years.

By late 1999, production of business equipment was up 74 percent and construction up 35 percent over 1992, while production of consumption goods had risen only 18 percent. Among manufacturing goods, durable good production had risen 76 percent while nondurable good production had risen just 13 percent. Annual borrowing by nonfinancial corporations as a percentage of nonfinancial corporate GDP darted from 3.4 per cent in 1994 to a previously unparalleled 9.9 per cent in the first half of 2000. As a result, by the first half of 2000, nonfinancial corporate borrowing on an annual basis had more than quadrupled with respect to 1994 and nonfinancial corporate debt as a proportion of nonfinancial corporate GDP had reached 85 per cent, the highest level ever.

The personal savings rate declined from an already low 2.1 percent in 1997 to -1.5 percent by 1999. Consumers were increasingly leveraged, especially on their homes. In 1989, about 7 percent of new mortgages had less than a 10 percent down payment, according to Graham Fisher & Co., an investment research firm. By 1999, that was more than 50 percent.[1]

[edit] The burst of the bubble

In the end, there were too few resources available for all of the plans formulated and funded during the boom to succeed. The most crucial—and most general—unavailable factor was a continuing flow of investment funds. There were shortages of programmers, network engineers, technical managers, office space, housing for workers, and other factors of production. Even industry giants like Microsoft, which did not rely on easy credit for their existence or for the bulk of

their growth, were still forced to compete with companies that were relying on easy credit for access to the factors of production.