Embed Size (px)

Citation preview

Has the Eurozone crisis strengthened or weakened the

EU?’

Roger VickermanProfessor of European Economics

Dean, Brussels School of International Studies

Global Skills Lecture 18 February 2013

The Crisis and Economic Coordination• Crisis shows need for international consensus and

coordination• Has the EU failed to achieve this internally and

externally?• Can we only have solidarity in the good times – when is

the EU not a zero-sum game?• Can the new architecture of ESM and EFSF do any

better than the Stability and Growth Pact?• Is completion of EMU with a fiscal as well as a

monetary union a credible development?• How does that affect the non-members of the

Eurozone?• Are we on the road to a multi-speed European Union?

2

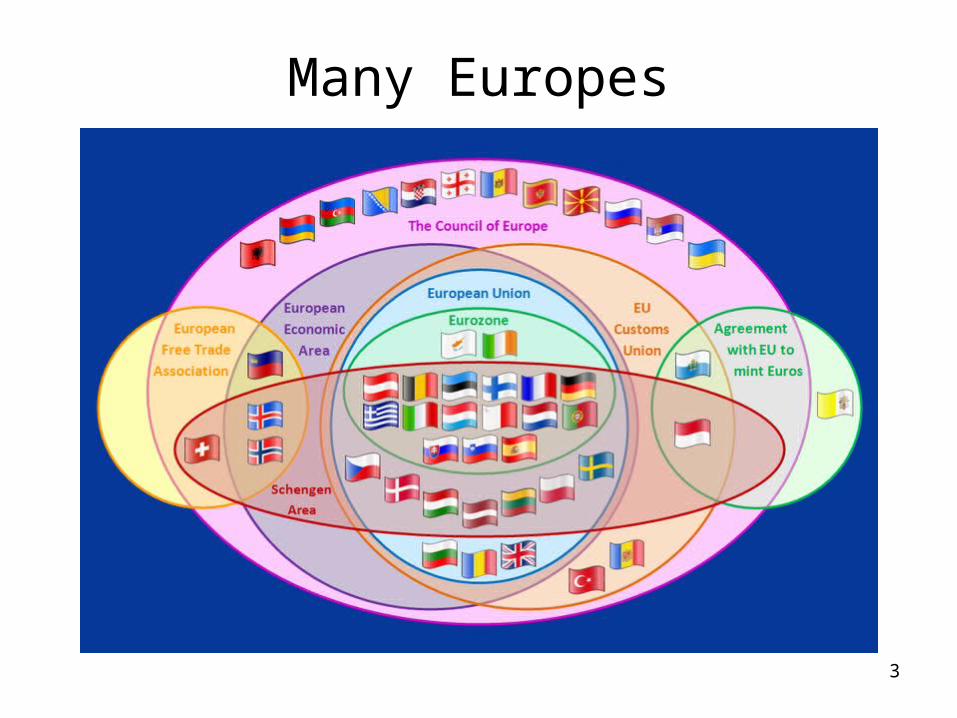

Many Europes

3

Why monetary integration?• Completing the Single Market• Currencies as non-tariff barriers

– Transaction costs of exchange– Cost of hedging future currency expectations– Lack of transparency in prices

• The Single Financial Market– Increased efficiency from a single financial sector– Common banking rules– Common interest rates to avoid market distortions

• Effective macro-stabilisation policy – the one size fits all problem– No exchange rate adjustment– No setting of independent interest rate 4

The Economic Theory• Optimal Currency Areas• Basic question is about exchange rates

– Flexible exchange rates • adjust to cope with asymmetric shocks

– Fixed exchange rates• exchange rates cannot adjust to deal with asymmetric

shocks/productivity differentials/inflation differentials• adjustment has to come through other markets• requires common monetary policy• thus output/employment adjusts• but adjustment less if certain criteria are met• what about fiscal policy?

5

Optimal Currency Area Theory• Six criteria for an OCA

– Labour mobility (Mundell)– Product diversification (Kenen)– Openness (McKinnon)– Fiscal transfers– Homogeneity of preferences– Solidarity

The scoresheet:NOYESYESNOMAYBE???

6

Is the EU an OCA?• Insiders and outsiders

– the converged, the converging and the unconverged – the EU may not be an OCA, but is a subset of the EU an

OCA?– does this imply that some should go it alone (a multi-

speed union), and does this matter?– has the cost of entry been too great for some relative to

the perceived benefits (e.g. Greece, Portugal)?– has entry led to uncontrollable problems (e.g. Ireland,

Spain)?– has the entry of others subverted economic advantage

(e.g. Germany, Netherlands, Austria)?– and what about the effect on the outsiders (UK, Denmark,

Sweden, Poland, Hungary etc)? 7

The EU Practice• The Maastricht Treaty convergence criteria:

– the achievement of price stability – a low rate of inflation close to the best performing states (defined as being within 1½ per cent of the average of the three lowest);

– sustainability of the government financial position – the government should not run a financial deficit greater than 3 per cent of GDP, and gross general government debt should be less than 60 per cent of GDP;

– exchange rate stability – apparent by the observance of the normal fluctuation margins provided by the Exchange Rate Mechanism, for at least two years; and

– durability of convergence – convergence of long-term interest rates (defined as being within 2 per cent of the average long-term interest rate of the three lowest inflation states).

• Note how these ‘monetary’ criteria differ from the ‘real’ criteria of OCA theory 8

Fiscal implications • In Eurozone fiscal decisions left to national governments• But governments can ‘cheat’ on fiscal responsibilities – get

round tight monetary policy by looser fiscal policy• Hence need for a mechanism to control cheating – Stability

and Growth Pact to reinforce Maastricht fiscal criteria• SGP has Excessive Deficit Procedure to ‘fine’ miscreants• But can EDP work effectively if:

– Slow to initiate– Big countries can subvert it– Fines make the position of weaker economies even worse

• Need for better early warning system – the ‘Cologne process’ – implies willingness to share budgetary plans

9

The deficit bias problem• Monetary and fiscal policy must be consistent• Should criteria be relaxed?

– balance over cycle?– political and credibility implications

• Fiscal indiscipline concerns financial markets:– raises borrowing costs– markets can distinguish between countries (credit ratings

affect risk premia)• More serious is the risk of default in one member

country:– capital outflows and a weak Euro– pressure on other governments to help out– pressure on the ECB to help out

• The ‘no-bailout’ clause– was it ever credible? 10

The onset of the Crisis • The origins of the crisis

– Financial markets and ‘sophisticated’ instruments– Toxic assets and asset price bubbles– Who was to blame?

• How to respond– Tax cuts or increased expenditure?– On what?

• Who has been more prudent?– Scale of public expenditure boost– Debt – and who holds it?

• The collapse of world trade and confidence?11

Warning signs

12

0

100

200

300

400

500

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Bps Graph I.1.3:3-month interbank spreads vs T-bills or OIS

EUR USD JPY GBP

Sources: Reuters EcoWin.

Default of Lehman Brothers

BNP Paribas suspends the valuation of two mutual funds

Asset price bubbles

13

0

100

200

300

0

100

200

300

400

500

03

.01

.00

12

.10

.00

27

.07

.01

14

.05

.02

25

.02

.03

05

.12

.03

22

.09

.04

05

.07

.05

12

.04

.06

25

.01

.07

07

.11

.07

22

.08

.08

Graph I.1.7:Stock markets, 2000-09

DJ EURO STOXX (lhs) DJ Emerging Europe STOXX (rhs)

Source: www.stoxx.com

Asset price bubbles

14Source: European Commission

The credit crunch

15Source: European Commission, European Economic Forecast Autumn 2012

Debt composition and trends (% GDP)

US Eurozone

Total debt

Financial capital

House-holds

General govt

Total debt

Financial capital

House-holds

General govt

1999 256 76 67 51 256 66 49 74

2007 334 113 96 51 335 111 62 69

2010 344 101 92 76 381 127 65 87

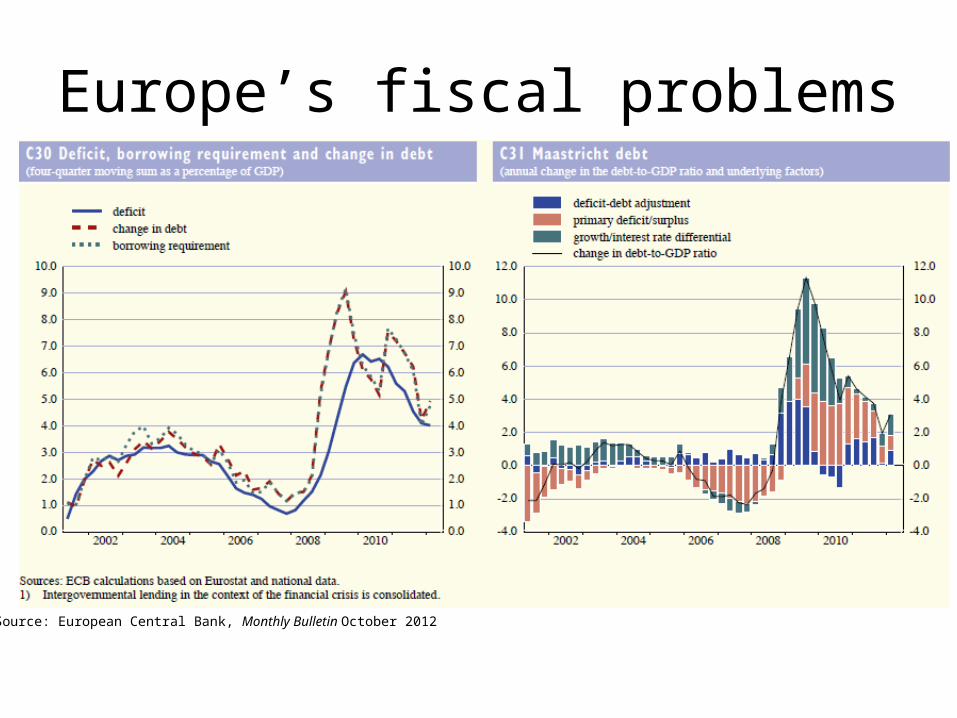

Europe’s fiscal problems

Source: European Central Bank, Monthly Bulletin October 2012

18

Europe’s fiscal problems

The consequences • Unsustainable deficits imply excessive borrowing• Where borrowing is international has two consequences:

– Raises cost of borrowing– Devalues currency

• But within Eurozone no devaluation option so risk premium rises - interest rate spreads on sovereign debt

• Speculators lose power to gain from currency fluctuations, so speculate on debt – risk premium: pick off weakest first and then move along the row of dominos

• Note this is exactly what happened to the old Exchange Rate Mechanism in 1992

• But now net effect is to weaken entire currency• Countries outside Eurozone partially protected as can still

offer currency fluctuation option – but only up to a point

19

Government bond yields

20

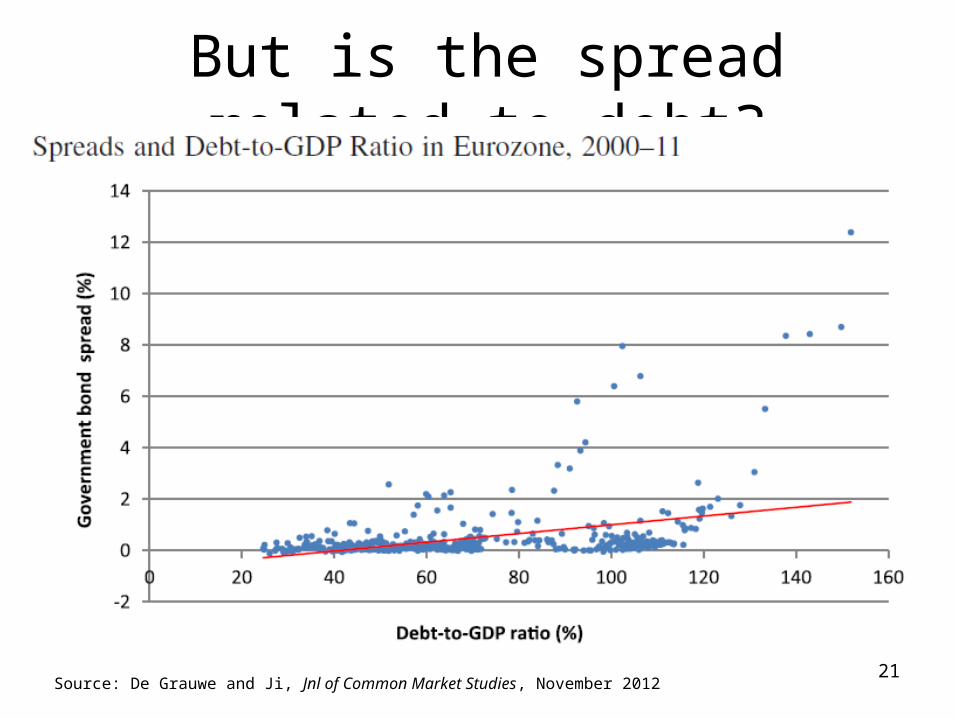

But is the spread related to debt?

21Source: De Grauwe and Ji, Jnl of Common Market Studies, November 2012

A structural break?

22

•De Grauwe and Ji argue that there was a structural break 2008. Before 2008 markets underestimated risk, after 2008 they may have overestimated risk coming from a high debt/ GDP ratio. And that overestimate is cumulative like a bubble effect.

Source: De Grauwe and Ji, Jnl of Common Market Studies, November 2012

Exchange rate consequences

Source: European Central Bank, Monthly Bulletin October 2012

Stock market consequences

Source: European Commission, European Economic Forecast Autumn 2012 Source: European Central Bank, Monthly Bulletin October 2012

Real economy consequences

• But this isn’t just about money and government debts

• The output costs– Less government expenditure– Higher borrowing costs– Reduced values of wealth

• Affects growth and employment– Trade and growth

25

Real economy consequences

Real economy consequences

27

Source: European Commission, European Economic Forecast Autumn 2012

Real economy consequences

28

Employment and unemployment

29

Source: European Commission, European Economic Forecast Autumn 2012

Unemployment rates

0.0

5.0

10.0

15.0

20.0

25.020

07Q

1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

Belgium

Germany

Ireland

Greece

Spain

France

Italy

Portugal

United Kingdom

Unit labour costs and unemployment

31Source: European Commission, European Economic Forecast Autumn 2012

Trends in world trade

32Source: European Commission, European Economic Forecast Autumn 2012

Trade consequences

33

The twin deficits problem

34

Policy responses• Spotting the problem:

– a question of timing– what problems – is it like before– can we resort to old solutions

• Is this the real price of globalisation?• Who is to blame: deficits vs surpluses• Do bail-outs work?• Will a European Stability Mechanism work any

better?• Can the EFSF be funded?• And is there any real appetite for a fiscal union,

on whose terms? 35

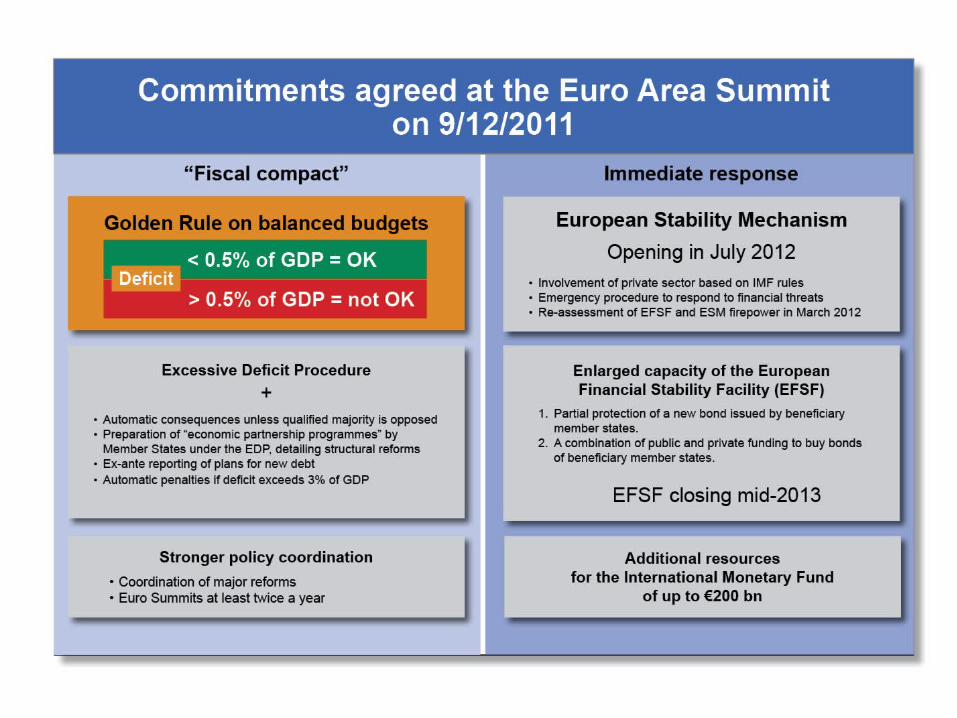

The new architecture – the six pack• Entered into force on 13 December 2011;• Five Regulations and one Directive (that is why it is called

six-pack);• EU secondary law; • Applies to 27 MS with some specific rules for "euro-area

Member States", especially regarding financial sanctions;• The six-pack does not only cover fiscal surveillance, but also

macroeconomic surveillance under the new Macroeconomic Imbalance Procedure.

• In the fiscal field, the six-pack strengthens the Stability and Growth Pact (SGP).. – The six-pack ensures stricter application of the fiscal rules – Moreover, the six-pack operationalizes the debt criterion, – Financial sanctions for "euro-area Member States" are imposed

in a gradual way

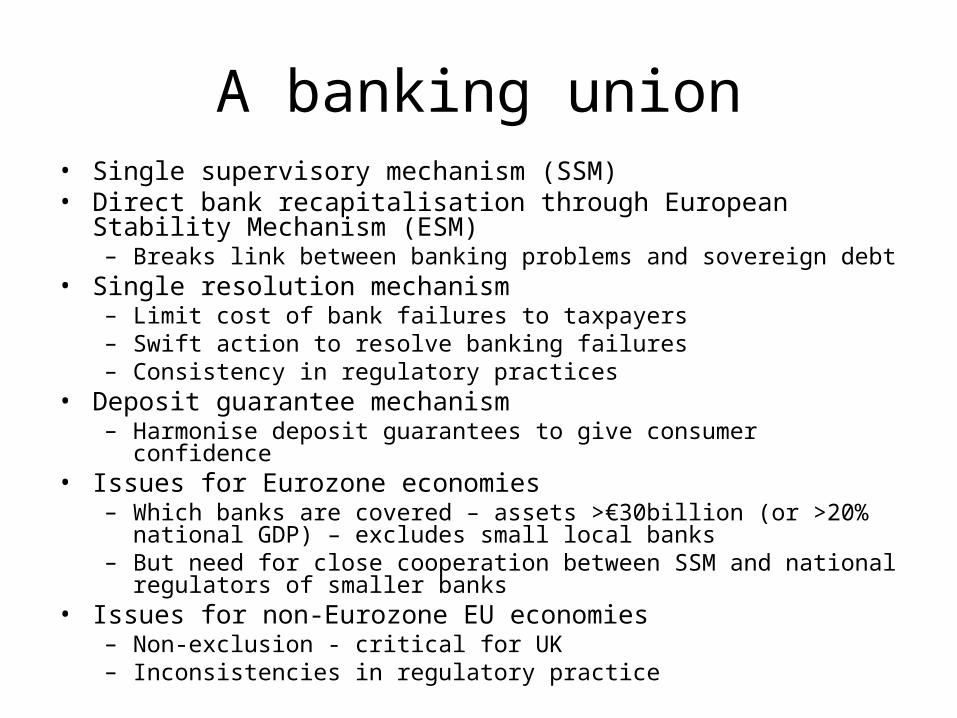

A banking union• Single supervisory mechanism (SSM)• Direct bank recapitalisation through European Stability Mechanism

(ESM)– Breaks link between banking problems and sovereign debt

• Single resolution mechanism– Limit cost of bank failures to taxpayers– Swift action to resolve banking failures – Consistency in regulatory practices

• Deposit guarantee mechanism– Harmonise deposit guarantees to give consumer confidence

• Issues for Eurozone economies– Which banks are covered – assets >€30billion (or >20% national GDP)

– excludes small local banks– But need for close cooperation between SSM and national regulators of

smaller banks • Issues for non-Eurozone EU economies

– Non-exclusion - critical for UK– Inconsistencies in regulatory practice

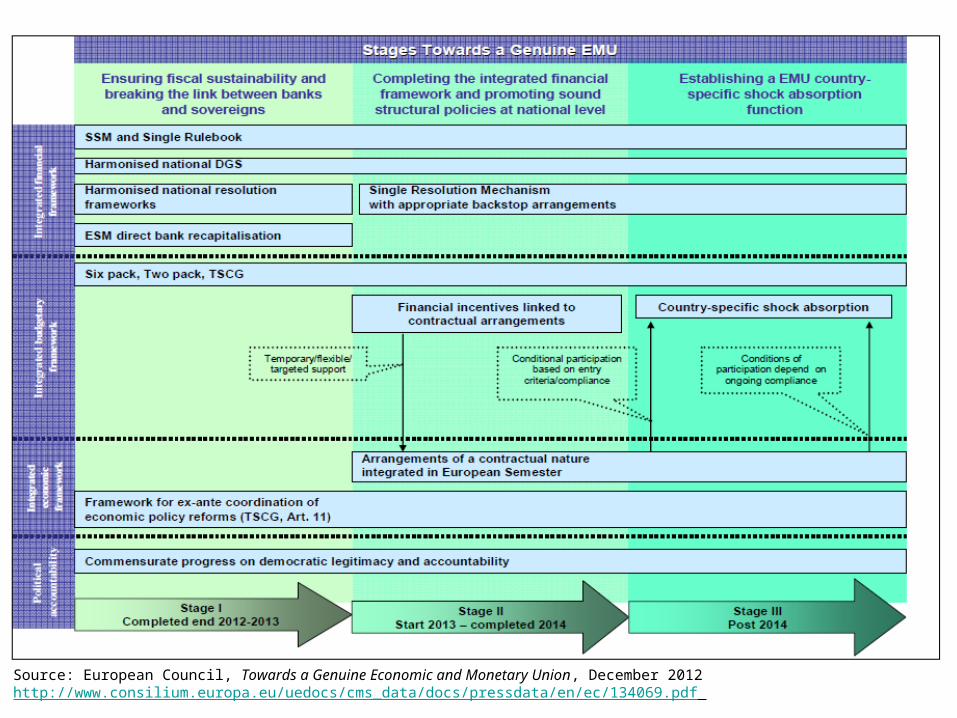

Source: European Council, Towards a Genuine Economic and Monetary Union, December 2012 http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ec/134069.pdf

Critique• Does new fiscal pact act quickly enough?• Should ECB be given more powers – e.g.

Eurobonds, Banking Regulation?• Are there conflicts with the Single Market

– Especially in the context of financial services?– The example of the Financial Transactions Tax

• How will markets react in the medium term?• How will voters react in the medium term?• Can there be fiscal unity without further political

integration?

Co-ordinating action • International financial stability and growth

– The evidence– The incentive to cheat

• International cooperation – The prisoners’ dilemma problem– Reducing informational asymmetry– Voluntarism or legal compulsion– Does the EU need a revised treaty?– International institutions and global federalism

• How big could/should the EU grow?• What next?

Conclusions• Has the EU finally resolved the problems arising from the

financial crisis?• Has this been an economic problem, a policy problem or a

(lack of) solidarity problem• If so who was to blame?• Has the cure been worse than the disease? And for whom?• Is there a better alternative?• Does this mean the end of an integrating Europe and the

beginning of an officially recognised multi-speed Europe of a closely integrated EMU core with a set of loose trading arrangements surrounding it?

• Where does the UK sit in this changing architecture? • What about Europe in the world?

45

Crisis: what crisis?

46

“Europe will be forged in crises, and will be the sum of the solutions adopted for those crises” Jean Monnet