Embed Size (px)

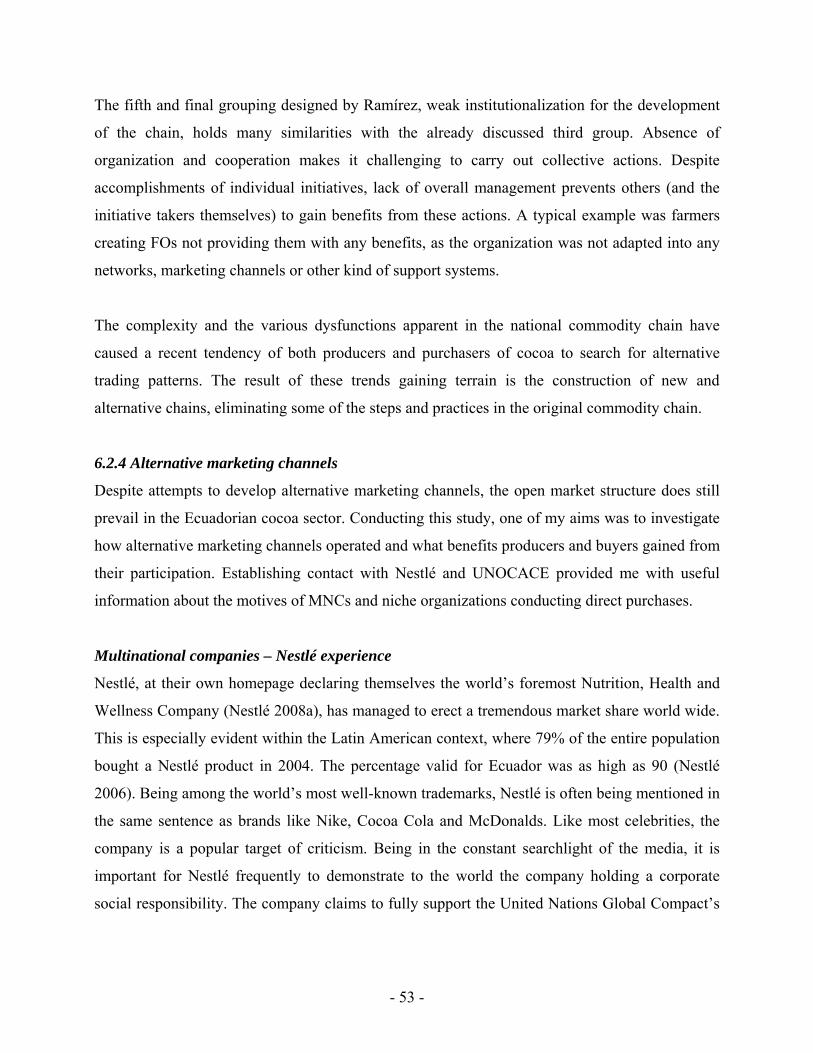

Citation preview

The Department of International Environment and Development Studies, Noragric, is the international gateway for the Norwegian University of Life Sciences (UMB). Eight departments, associated research institutions and the Norwegian College of Veterinary Medicine in Oslo. Established in 1986, Noragric’s contribution to international development lies in the interface between research, education (Bachelor, Master and PhD programmes) and assignments. The Noragric Master theses are the final theses submitted by students in order to fulfil the requirements under the Noragric Master programme “Management of Natural Resources and Sustainable Agriculture” (MNRSA), “Development Studies” and other Master programmes. The findings in this thesis do not necessarily reflect the views of Noragric. Extracts from this publication may only be reproduced after prior consultation with the author and on condition that the source is indicated. For rights of reproduction or translation contact Noragric. ©Marte Haugerud Moe, June 2008 [email protected] Noragric Department of International Environment and Development Studies P.O. Box 5003 N-1432 Ås Norway Tel.: +47 64 96 52 00 Fax: +47 64 96 52 01 Internet: http://www.umb.no/noragric

I

Declaration

I, Marte Haugerud Moe, declare that this thesis is a result of my research investigations and

findings. Sources of information other than my own have been acknowledged and a reference list

has been applied. This work has not previously been submitted to any other university for award

of any type of academic degree.

Place and date: Signature:

_________________________________ ______________________________

II

Acknowledgement

To my supervisor Arild Vatn - this thesis could never been accomplished without you,

To my co-supervisor Simon Pahle for inspiration and actuation,

To José Garcia and the rest of the ACDI/VOCA staff in Quevedo,

To Iven Ose and the rest of the ADCI/VOCA staff in Guayaquil,

To Frank Blacio and the rest of the Nestlé staff in Guayaquil,

To all my respondents for sharing their experiences,

To the Nobel Institute for providing a work space and brilliant assistance,

To my family and friends for continuous support and encouragement,

To Jostein for always believing in me,

Thank you / Muchas gracias

III

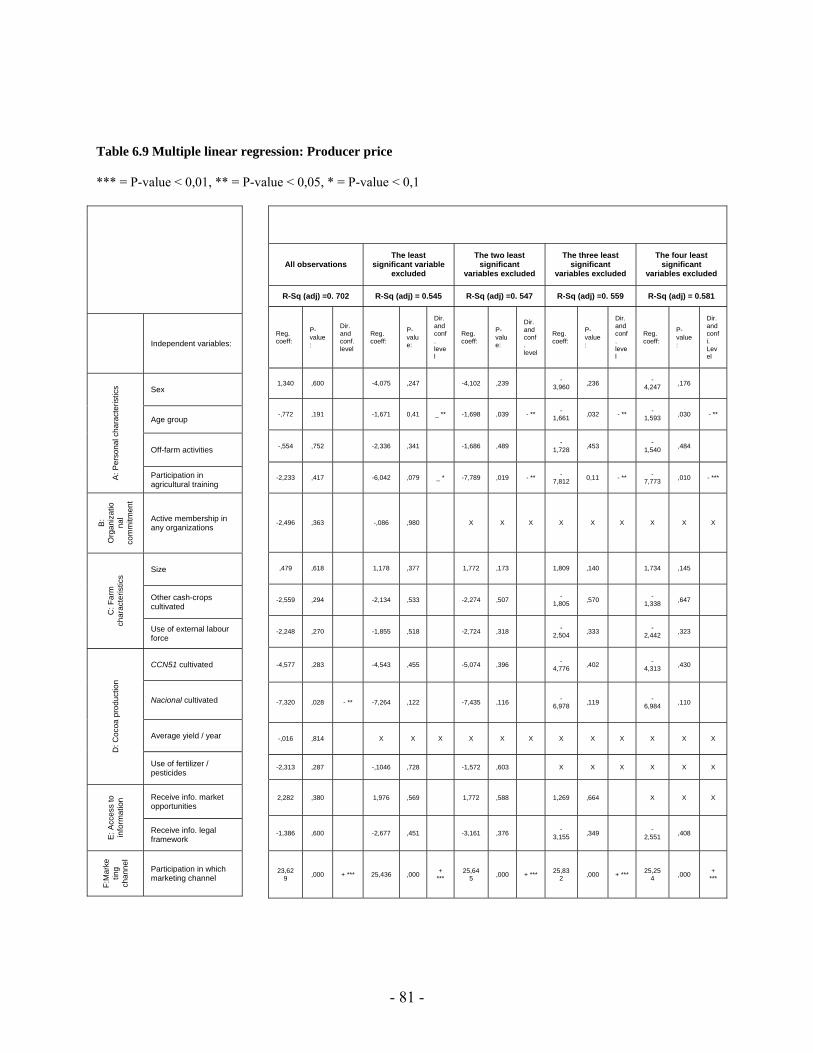

Abstract Despite Ecuador is considered one of the world’s leading providers of fine and aromatic cocoa,

the economic reward appears to be absent at producer level. The extended poverty found among

Ecuadorian small scale cocoa producers, most studies conclude to be caused by scarce

agricultural output. Writing this thesis, my aim was to see whether there were any additional

explanatory facts, with the attention directed towards the price received by the producers.

I came to recognize the open market structure, prevailing in Ecuador, to be highly labour

intensive and complex. Lack of governmental intervention, neither regulating competition nor

ensuring proper quality controls to be carried out, made intermediaries inhabit a dominant

position. The existing challenges within the conventional market structure have caused a recent

increase of initiatives seeking to break with the traditional structures. In order to answer the main

objective: To calculate the producer price received by Ecuadorian small scale cocoa farmers,

and furthermore seek explanations for the variations I expect to reveal point of departure was

taken in the typology of value chain governance published by Gereffi et al. (2005). By carrying

out a comparative case study, a producer price comparison among the participants in the three

different marketing chains; 1) open markets 2) contractors with MNCs1 and 3) direct purchases.

A price analysis revealed producers carrying out direct sales to receive a price more than 25%

higher than the producers within the open market structure. The positive impacts choice of

marketing channel has on producer price were confirmed running a regression analysis.

Qualitative research found evidence for organizational commitment and assistance from external

contributors (NGOs) to be highly influential to the choice of marketing channel. Additionally, a

quantitative analysis identified Geographical location (+/-), Age group (+), Use of

Fertilizer/pesticides (-) and Access to information of the legal framework (+) to be of influence.

Based on the findings of my research, I developed four recommendations of how to increase the

producer price level among Ecuadorian small scale producers of cocoa: 1) Governmental

attention should increase 2) Producers to carry out direct sales (in order to easier succeed, form

FOs and seek assistance from NGOs) 3) Obtain certifications, and finally 4) Transfer quality

incentives to producer level. 1 Due to unforeseen occurrences, this group had to be eliminated. The study was carried out with the remaining two.

IV

Table of contents 1. Introduction…………………………………………………………………………………… 1

1.1 Global production systems……………………………………………………...………. 1

1.2 Purpose of the study including its objectives……………………………………........... 2

1.3 Limitations of the thesis…………………………………………………………………. 3

1.4 Chapter outline………………………………………………………………………...… 3

2. Background……………………………………………………………………………………. 4

2.1 Ecuadorian cocoa production…………………………………………………………… 4

2.2 Causes of change………………………………………………………………………..... 6

2.3 Profoundness of the problem……………………………………………………………. 9

3. Theory……………………………………………………………………………………...… 10

3.1 Commodity Chains……………………………………………………………………... 10

3.1.1 Commodity Chain Analysis (CCA)…………………………………………….…. 10 3.1.2 Global Value Chains (GVCs)……………………………………………………... 11 3.1.3 Global Commodity Chains (GCCs)……………………………………………….. 14

3.2 Organization and participation……………………………………………………...… 16 3.2.1 Organization and its obstacles………………….…………………………………. 16 3.2.2 Participation……………………………………………………………………..… 18

3.3 The role of NGOs……………………………………………………………………….. 19

3.4 Theoretical framework……………………………………………………………….… 21

4. Previous studies…………………………………………………………………………...… 25

4.1 Commodity chain studies in Ecuador…………………………………………………. 25

4.2 Studies of international cocoa trade……………………………………………..…….. 27

5.0 Method………………………………………………………………………………………. 29

5.1 Case studies……………………………………………………………………………... 29

5.2 Choice of research strategies……………………………………...…………………… 29

5.2.1 Abduction…………………………………………………………………….…… 30 5.2.2 Combining qualitative and quantitative research…………………………….…… 31

5.3 Choice of methods for data collection……………………………………………….… 31 5.3.1 Quantitative methods…………………………………………………..………….. 32

V

5.3.2 Qualitative methods……………………………………………………………..… 32

5.4 Choice of methods for analysis………………………………………………………… 33

5.4.1 Analysis of quantitative data……………………………………………………… 33 5.4.2 Analysis of qualitative data………………………………………………….……. 36

6. Analysis and discussions……………………………………………………………..……… 37

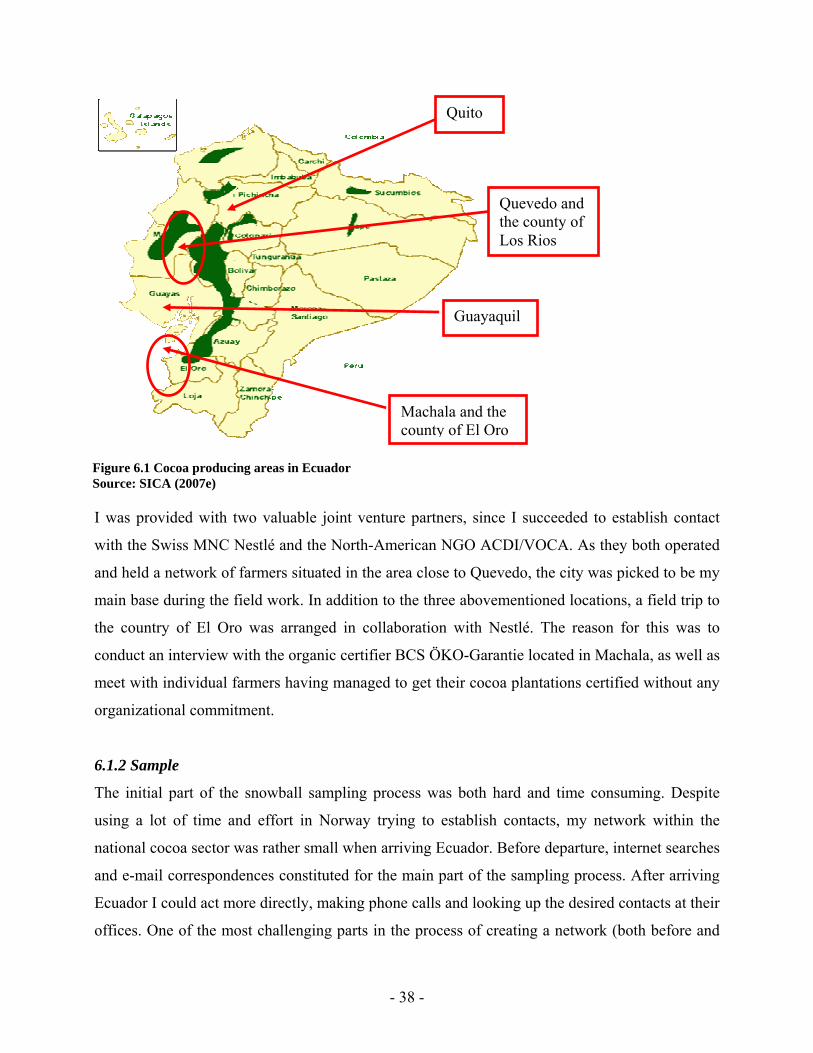

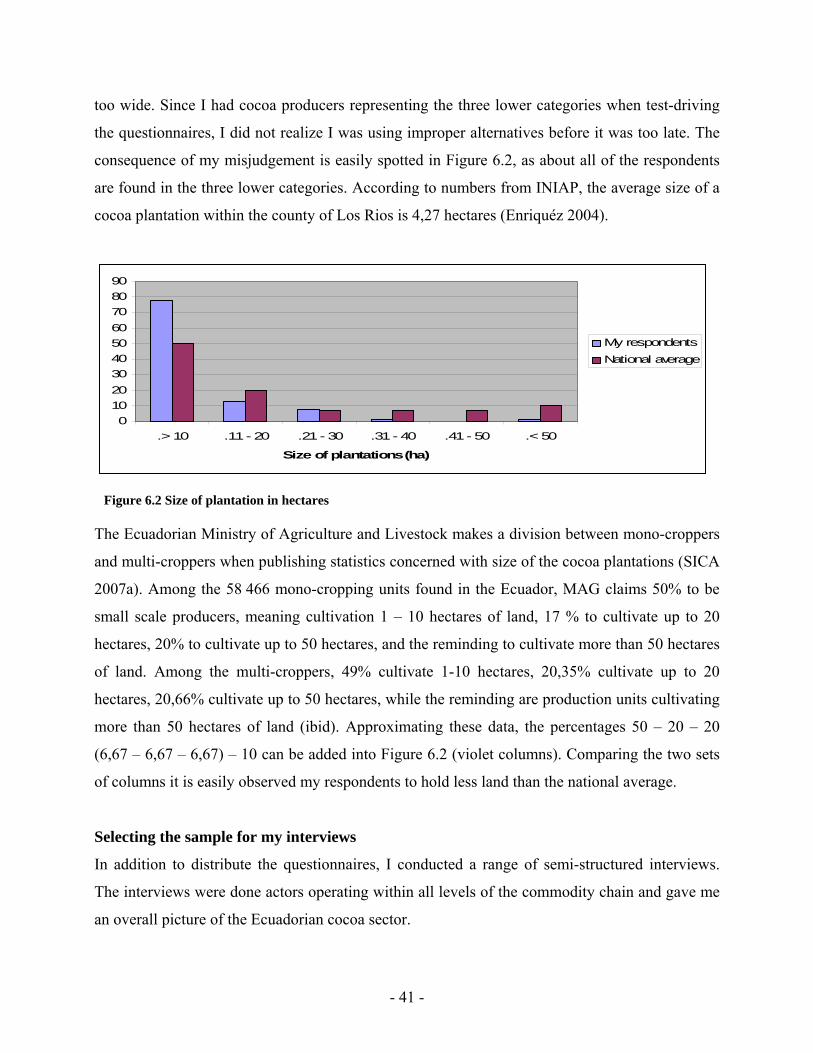

6.1 Research area and sample …………………………………………….………………. 37

6.1.1 Research area…………………………………………………………………...…. 37 6.1.2 Sample…………………………………………………………………………….. 38

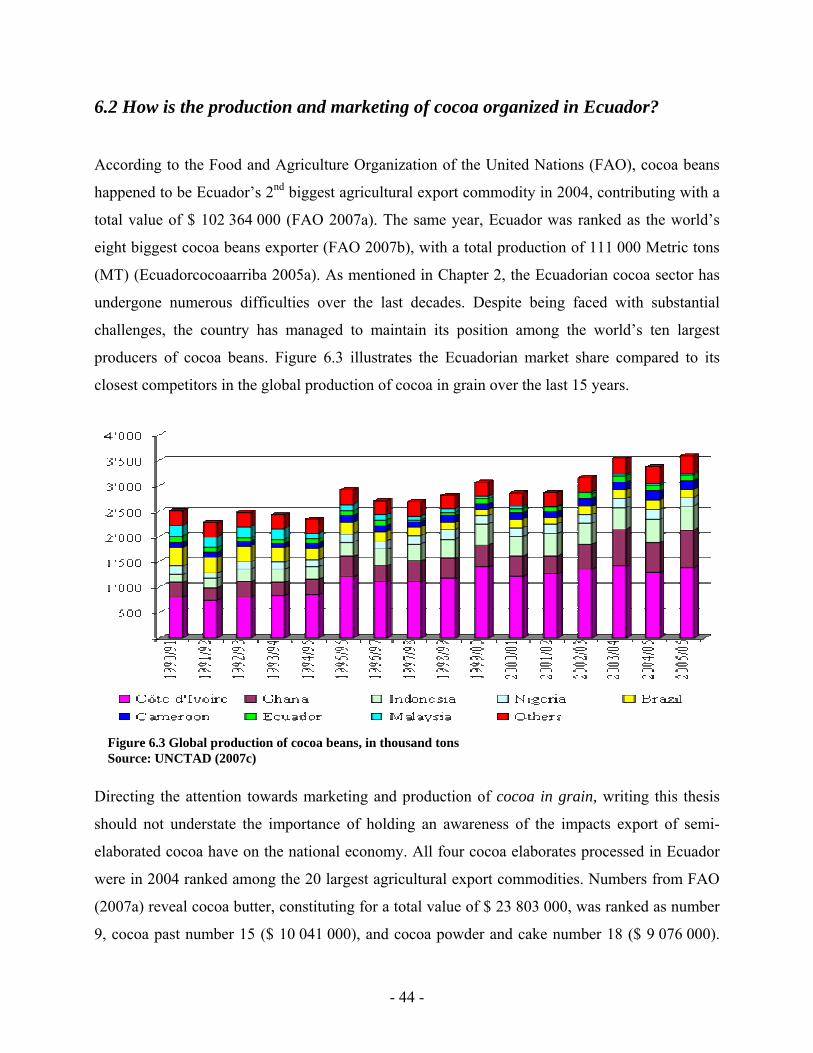

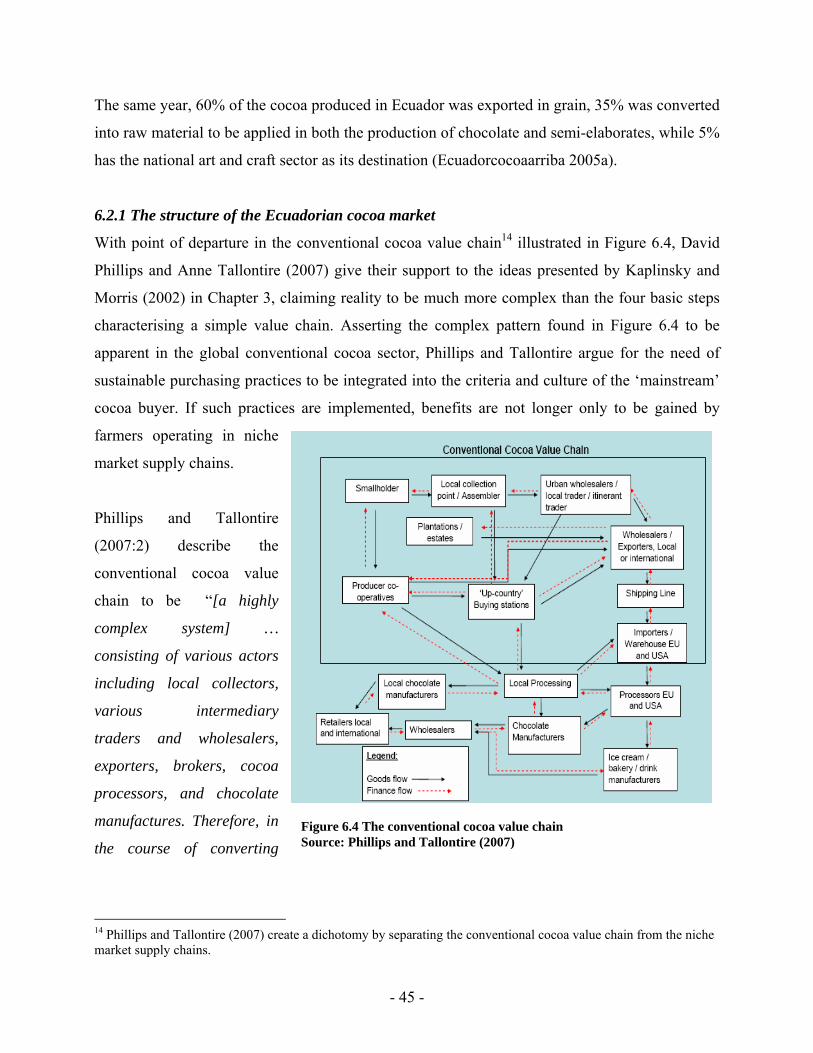

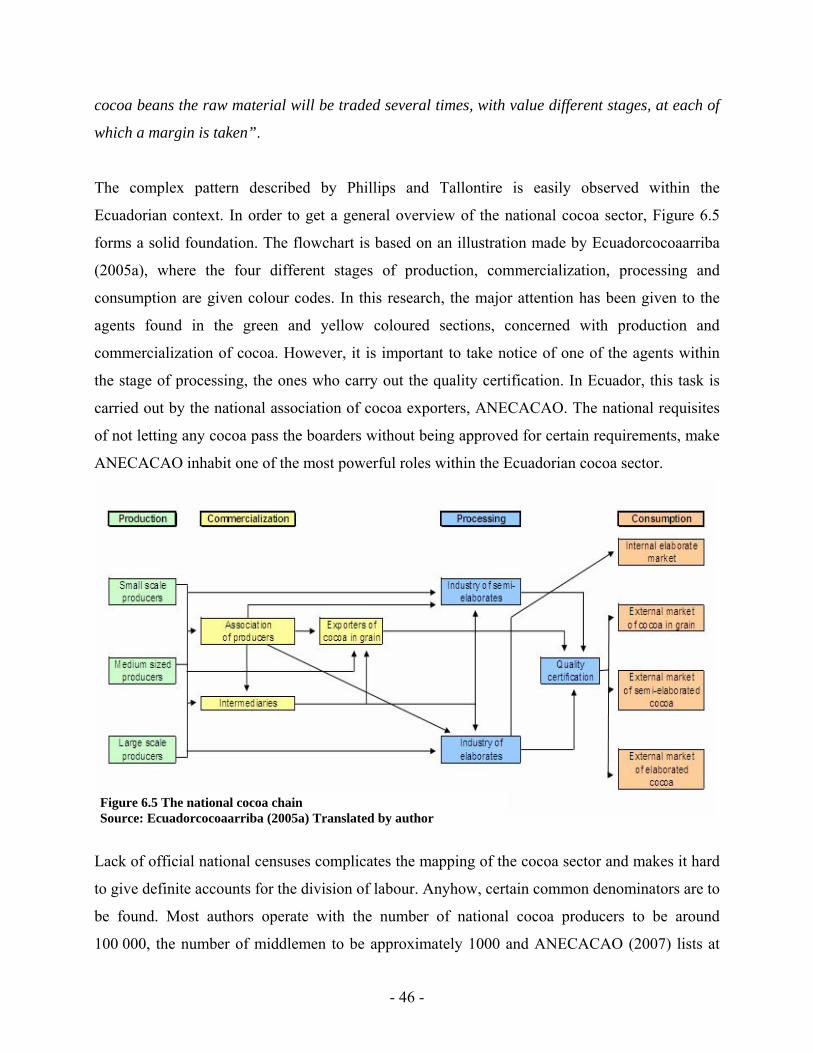

6.2 How is the production and marketing of cocoa organized in Ecuador?..................... 44

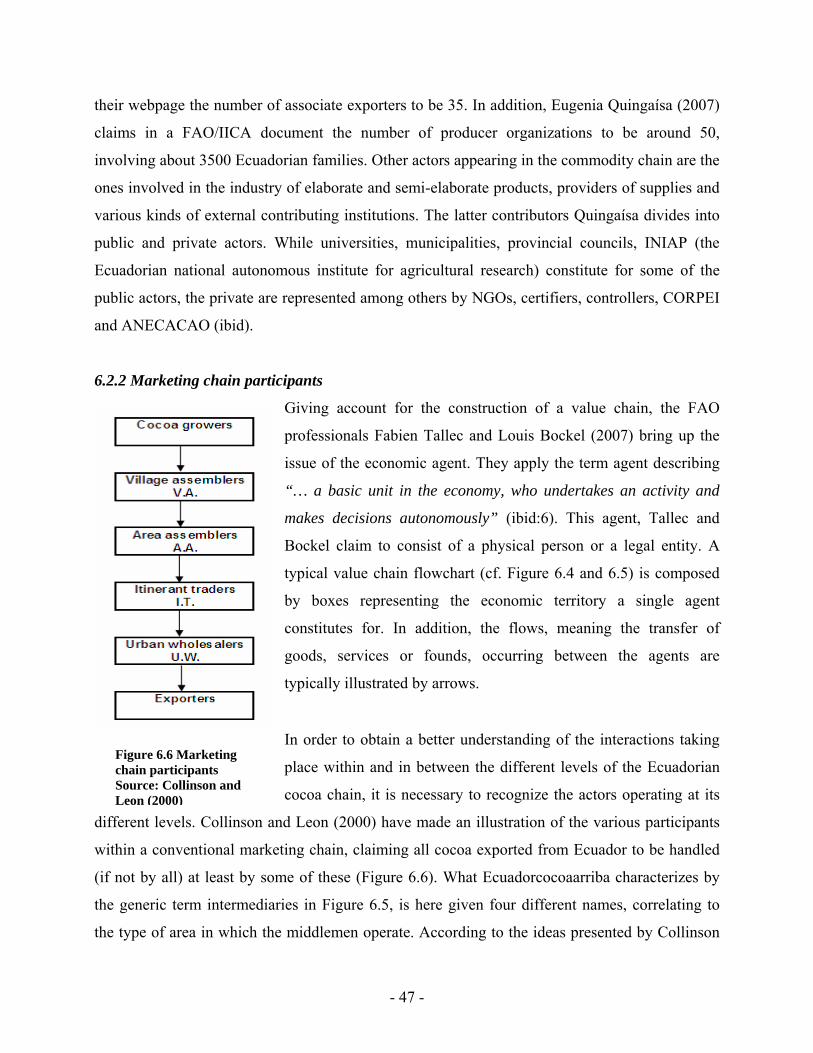

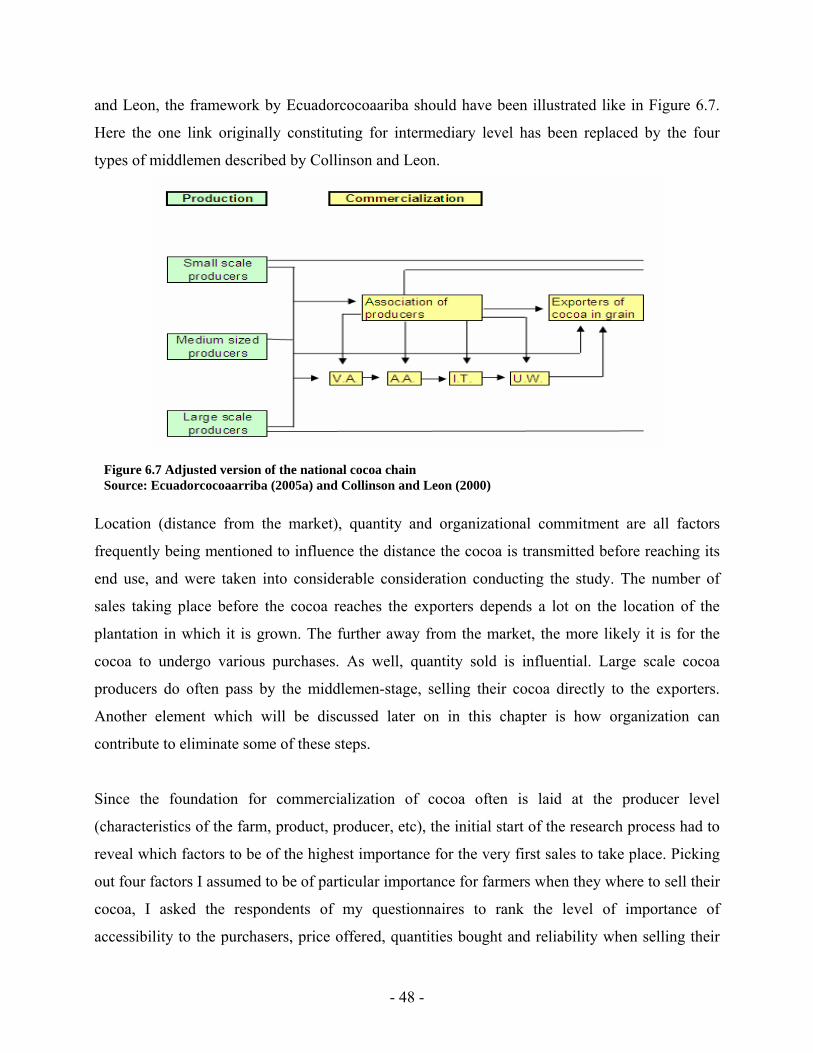

6.2.1 The structure of the Ecuadorian cocoa market……………………………………. 45 6.2.2 Marketing chain participants……………………………………………...………. 47 6.2.3 Challenges within the commodity chain……………………..…………………… 50 6.2.4 Alternative marketing channels………………………………………………….... 53

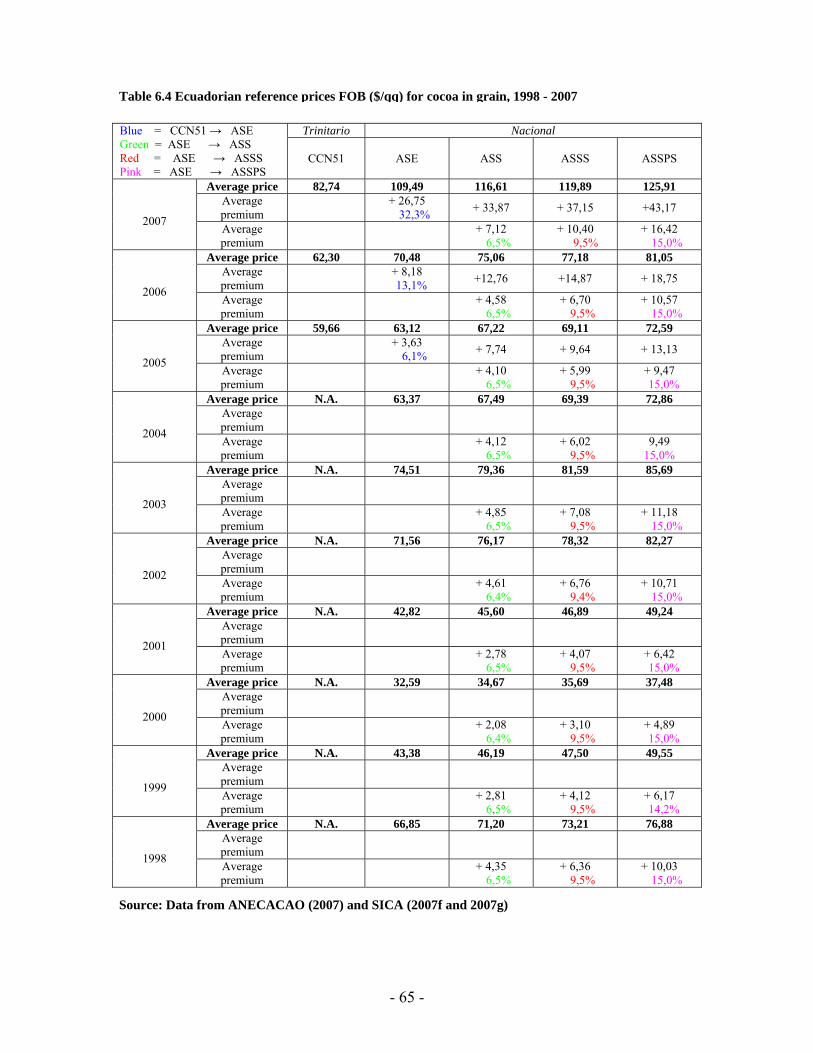

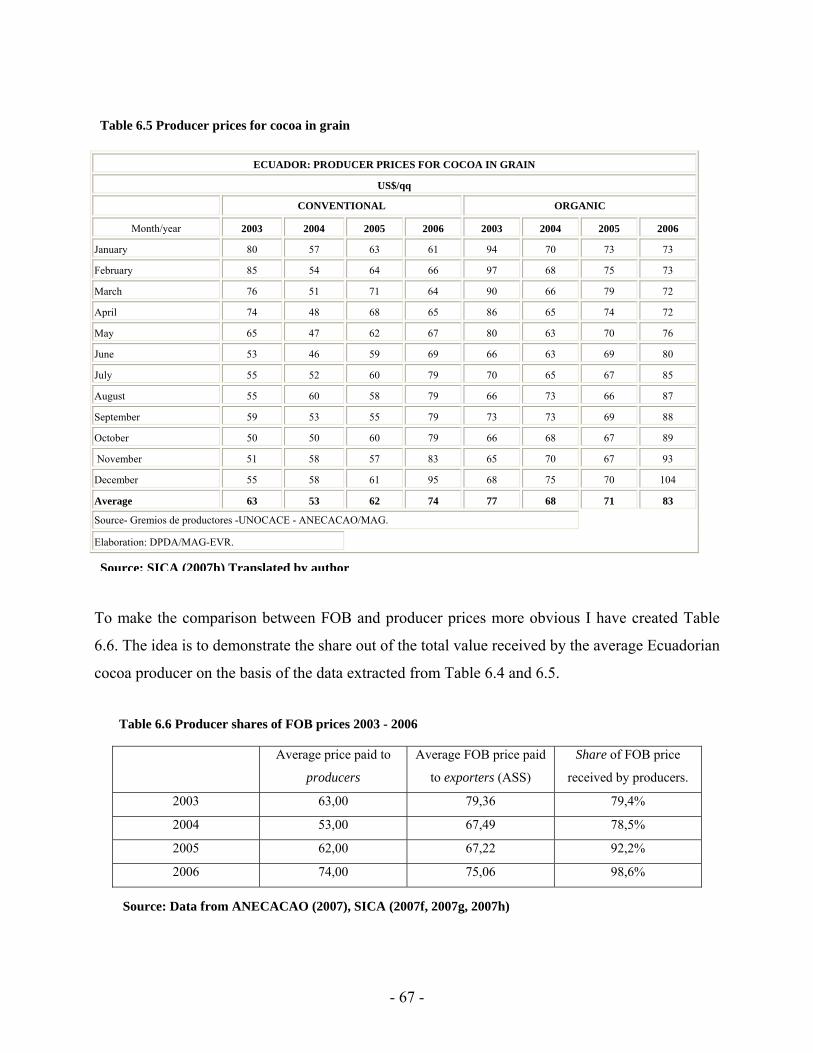

6.3 What is the average price ($/qq) farmers participating in the different marketing channels receive for their cocoa?........................................................................ 59

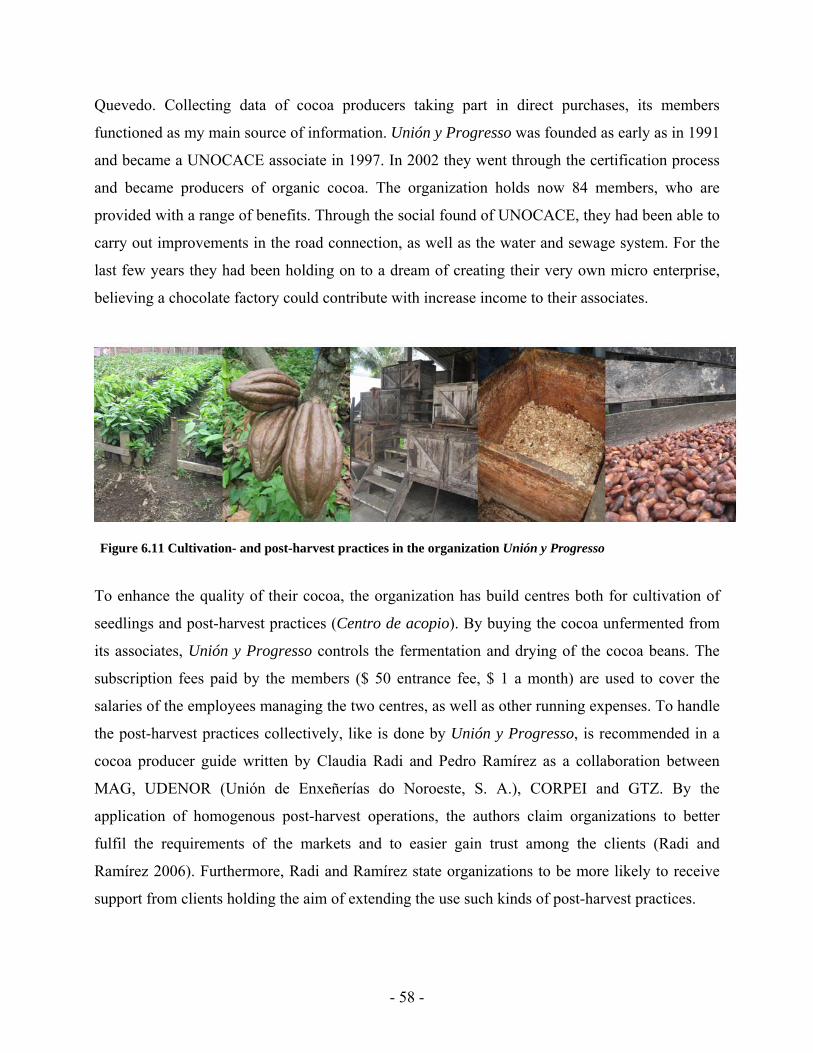

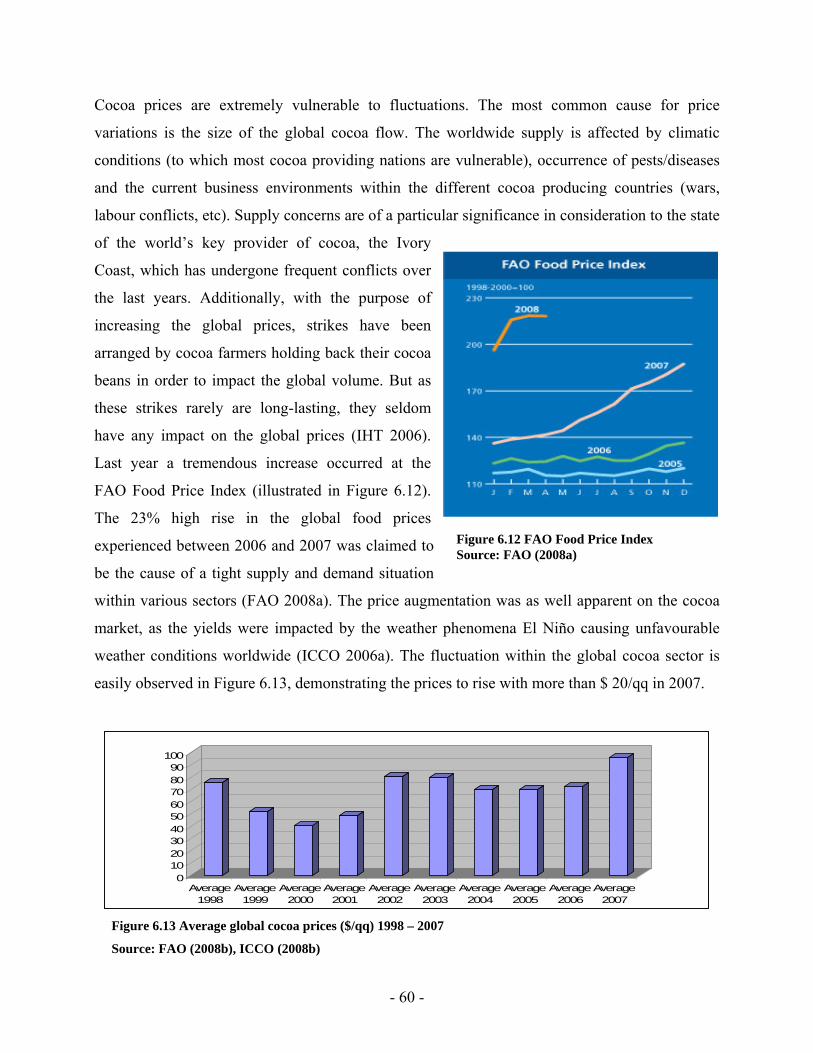

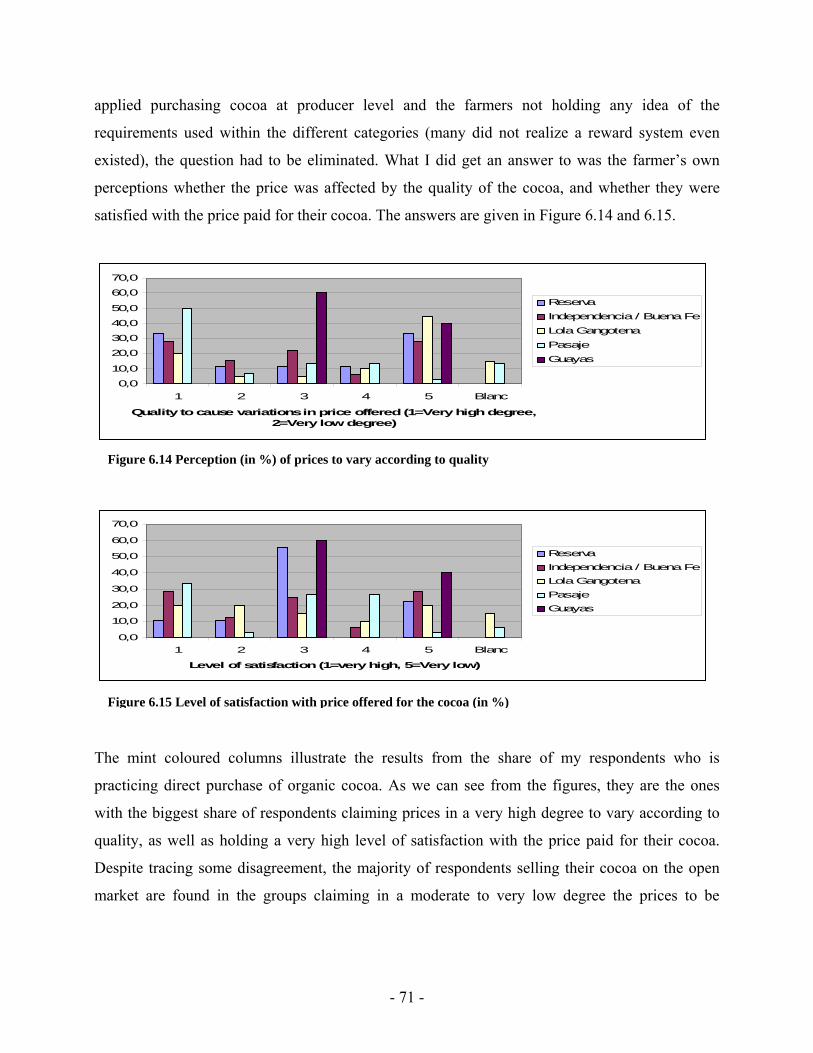

6.3.1 Price setting mechanisms in the global cocoa market………………………..…… 59 6.3.2 Price setting mechanisms in the Ecuadorian domestic cocoa market……..……… 61 6.3.3 FOB prices of cocoa in grain……………………………………………………… 64 6.3.4 Average price received among Ecuadorian cocoa farmers………………………... 66 6.3.5 Price variations in correspondence to quality……………………………………... 70

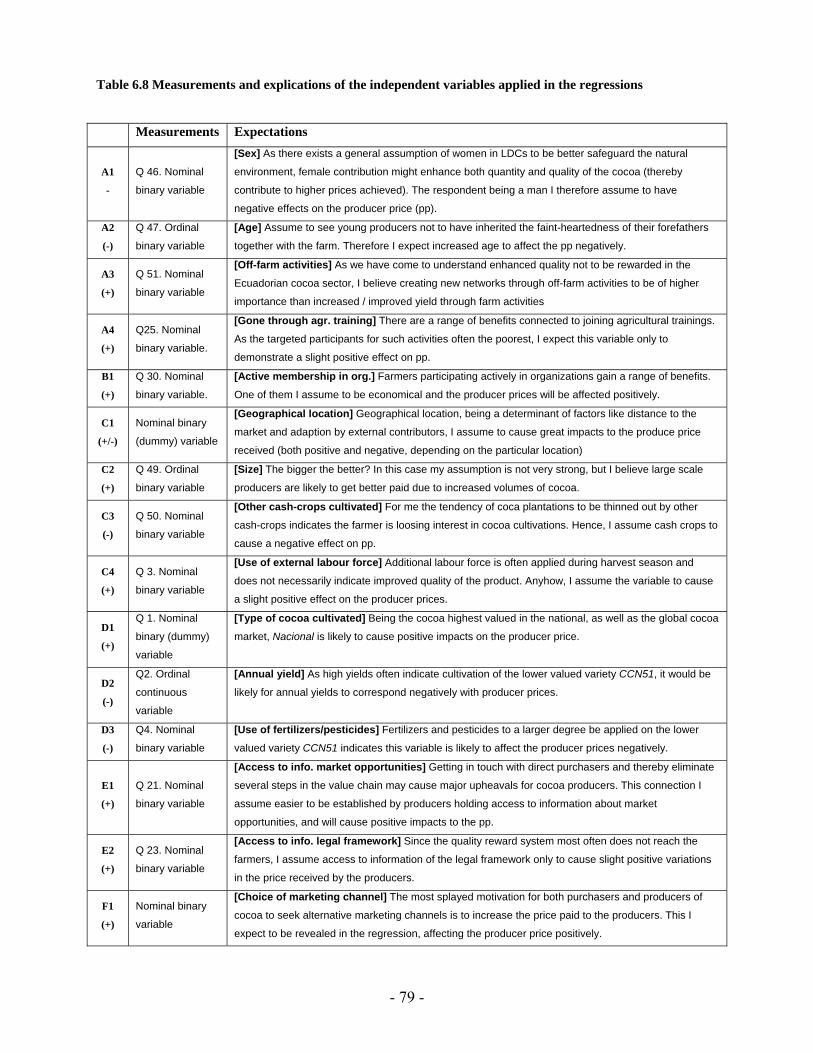

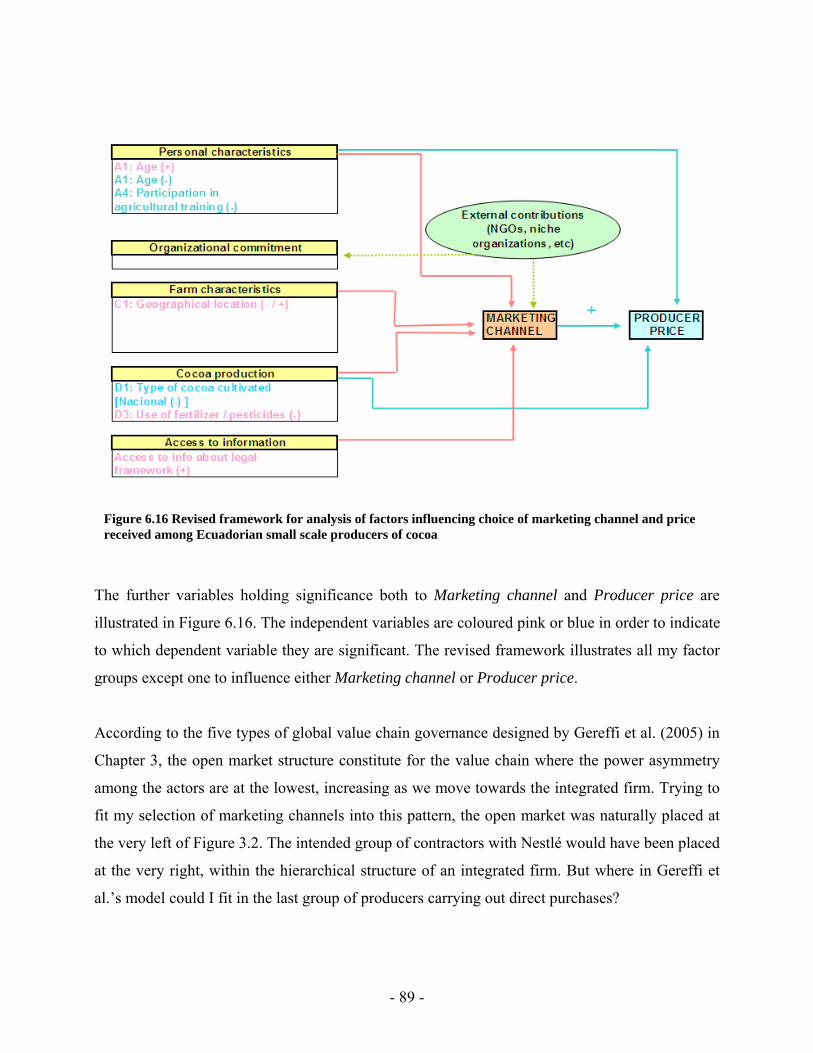

6.4 How can the variation in producer prices be explained?.............................................. 73 6.4.1 Presentation of the independent variables included in the regression analyses…... 73 6.4.2 Which factors are influential to the price paid to the producers………………....... 78 6.4.3 Which factors are influential to the choice of marketing channel?.......................... 84 6.4.4 What are my major findings and how do they relate to the framework sketched out in Chapter 3?................................................................................................. 88

7.0 Conclusion and recommendations……………………………………………….………… 94

7.1 How is the production and marketing of cocoa organized in Ecuador?..................... 94

7.2 What is the average price ($/qq) offered to the producers within the

various marketing channels and how does this price correlate with the quality

of the cocoa purchased?......................................................................................................... 95

7.3 How can the variation in the producer prices be explained?....................................... 96

7.4 Recommendation of improvements to be carried out in order to enhance to

producer prices…………………………………………………………………………..…. 97

References………………………………………………………………………………...…… 100

VI

List of figures Figure 2.1 FOB prices cocoa in grain 2006…………………………………………….……. 5 Figure 2.2 The vicious circle within the Ecuadorian cocoa sector…………………...……… 6 Figure 2.3 National vs. international prices for cocoa in grain 2005 and 2006……………… 9 Figure 3.1 Four links in a simple value chain…………………………………….………… 11 Figure 3.2 Five global value chain governance types…………………………………….… 13 Figure 3.3 The Organization of Producer-driven Commodity Chains……………………… 15 Figure 3.4 The Organization of Buyer-driven Commodity Chains ………………….…….. 15 Figure 3.5 NGOs: diversity in the crowd…………………………………………………… 20 Figure 3.6 Framework for analysis of factors influencing choice of marketing channel and

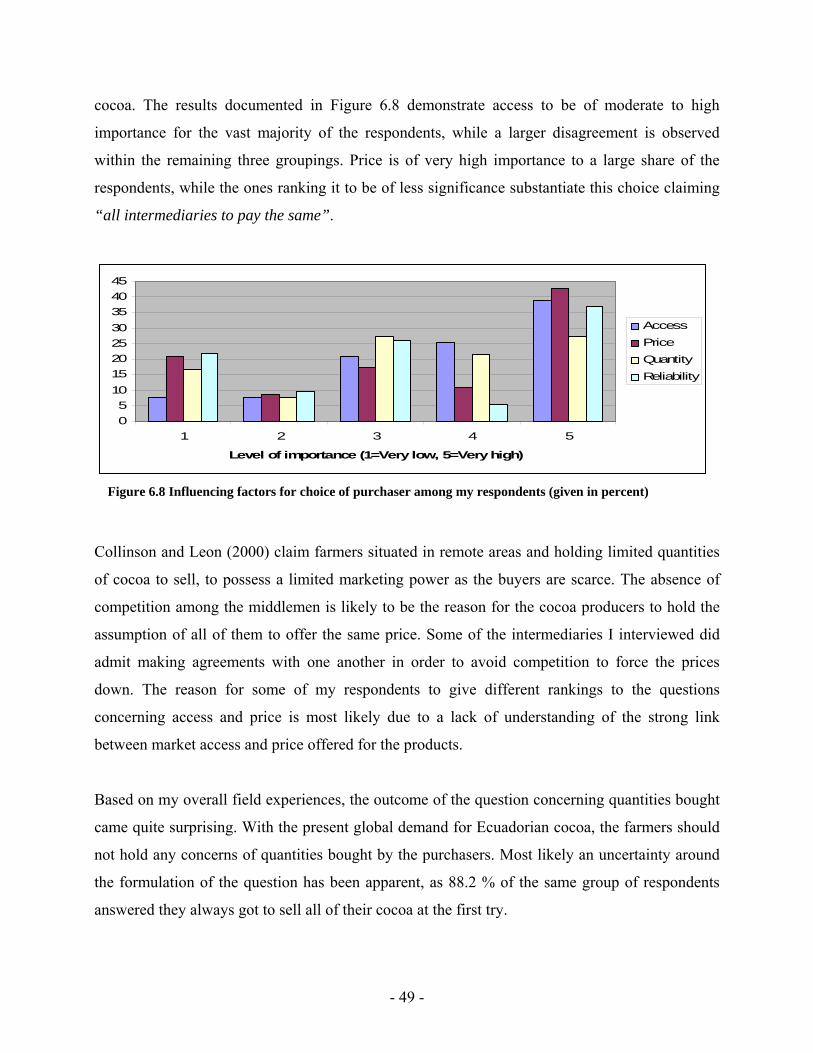

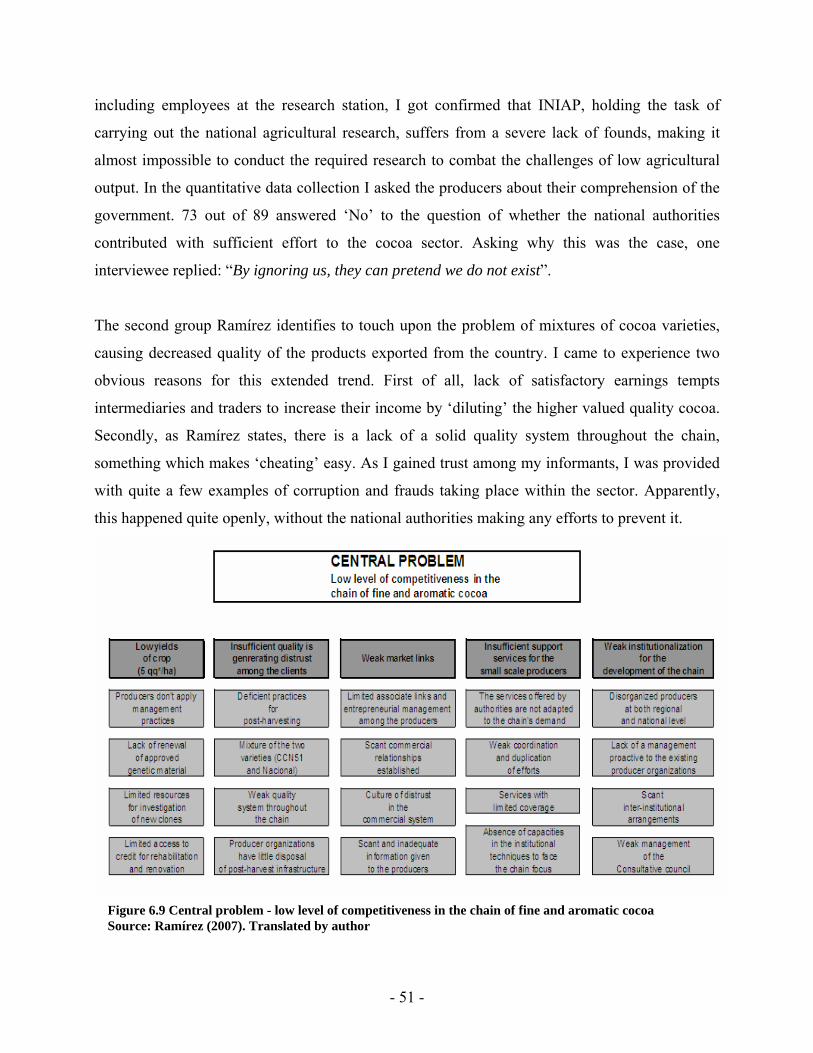

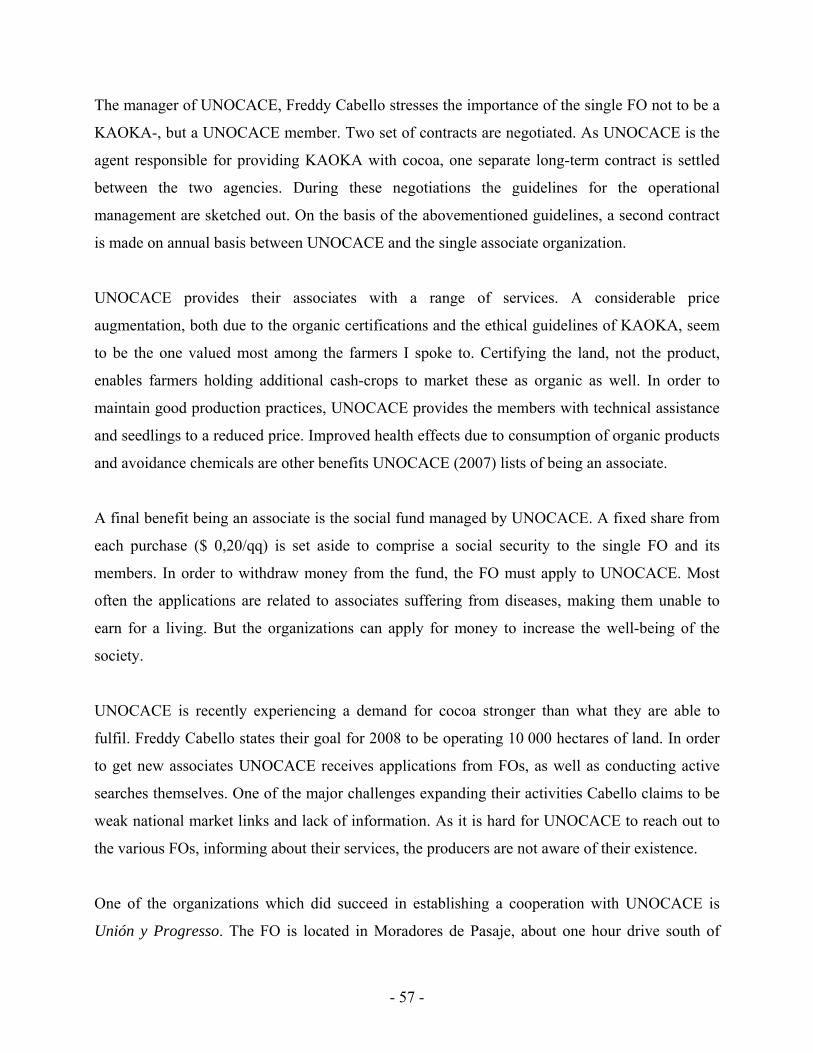

price received among Ecuadorian small scale producers of cocoa……………… 22 Figure 5.1 The epistemological model of diagnostic reasoning………………………….… 30 Figure 6.1 Cocoa producing areas in Ecuador………………………………………...……. 38 Figure 6.2 Size of plantation in hectares………………………………………….………… 41 Figure 6.3 Global production of cocoa beans, in thousand tons……………………….…… 44 Figure 6.4 The conventional cocoa value chain………………………………………..…… 45 Figure 6.5 The national cocoa chain…………………………………………………...…… 46 Figure 6.6 Marketing chain participants………………………………………………….… 47 Figure 6.7 Adjusted version of the national cocoa chain…………………………………… 48 Figure 6.8 Influencing factors for choice of purchaser among my respondents……….…… 49 Figure 6.9 Central problem - low level of competitiveness in the chain of fine and

aromatic cocoa…………………………………………….…………………..… 51 Figure 6.10 The process of measurement and quality certification at Nestlé, Guayaquil…… 55 Figure 6.11 Cultivation- and post-harvest practices in the organization Unión y Progresso... 58 Figure 6.12 FAO Food Price Index…………………………………………………….......… 60 Figure 6.13 Average global cocoa prices ($/qq) 1998 – 2007…………………………..…… 60 Figure 6.14 Perception (in %) of prices to vary according to quality……………………...… 71 Figure 6.15 Level of satisfaction with price offered for the cocoa (in %)…………………… 71 Figure 6.16 Revised for analysis of factors influencing choice of marketing channel

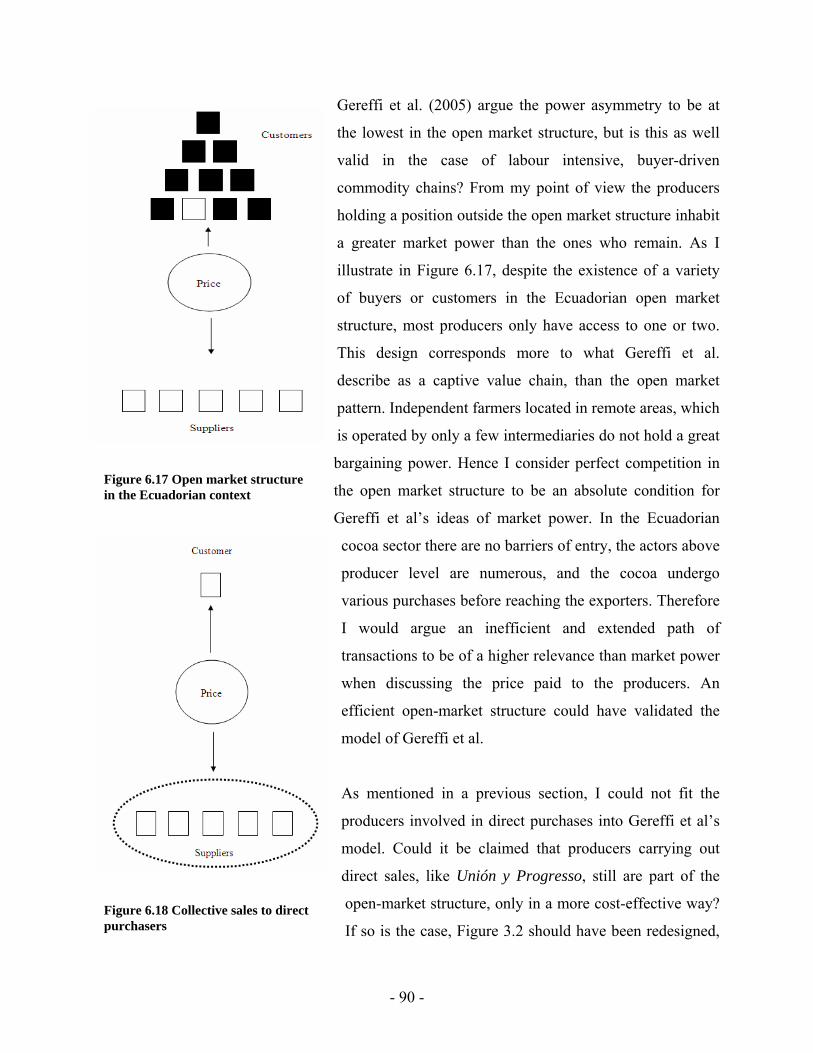

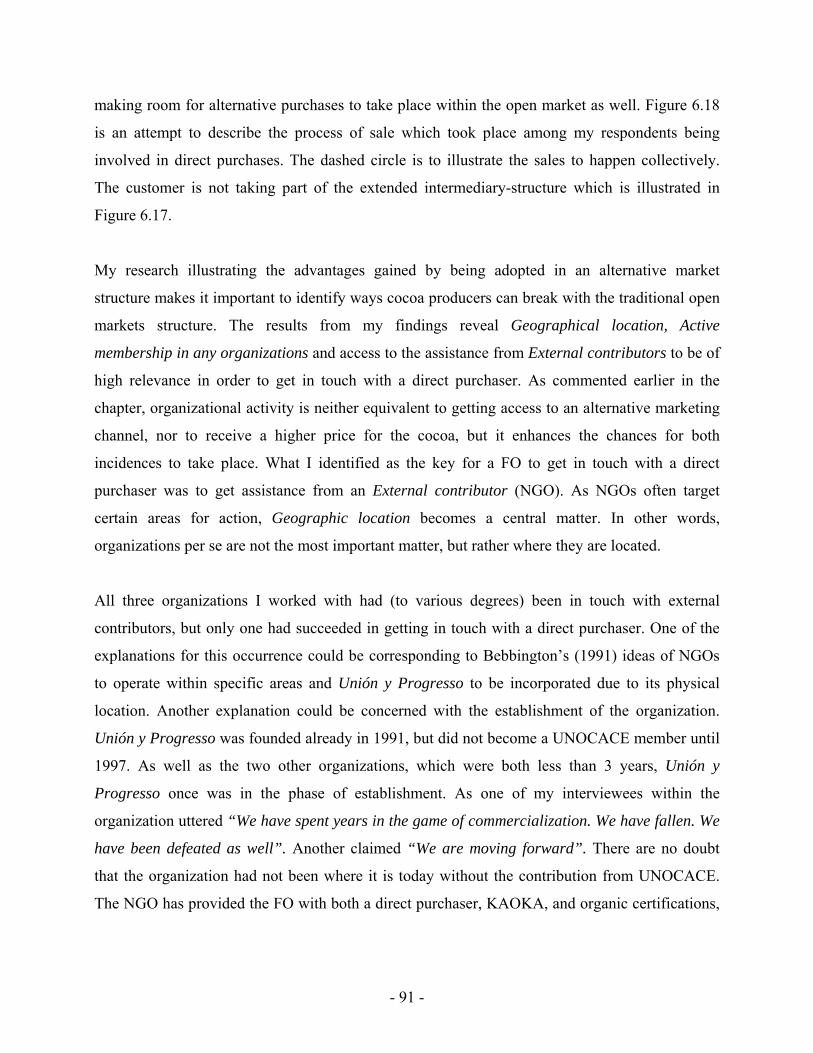

and price received among Ecuadorian small scale producers of cocoa……….… 89 Figure 6.17 Open market structure in the Ecuadorian context…………………………….… 90 Figure 6.18 Collective sales to direct purchasers…………………………………………..… 90

VII

List of tables Table 6.1 Age, sex and geographical division of the respondents answering the survey...... 40 Table 6.2 List of interviewees……………………………………………………...……… 42 Table 6.3 UNOCACE associates and their levels of production………………………...… 56 Table 6.4 Ecuadorian reference prices FOB ($/qq) for cocoa in grain, 1998 – 2007……… 65 Table 6.5 Producer prices for cocoa in grain…………………………………………….… 67 Table 6.6 Producer shares of FOB prices 2003 – 2006………………………………….… 67 Table 6.7 Cocoa Prices 2007 – Average prices received among Ecuadorian cocoa

producers compared to the global stock exchange prices…..…………………… 69 Table 6.8 Measurements and explications of the independent variables applied in the

regressions…………….………………………………………………………… 79 Table 6.9 Multiple linear regression: Producer price……………………..……………..… 81 Table 6.10 Binary Logistic regression: Marketing channel…………………………….…… 85 List of appendices Appendix 1 ICCO forecast on global cocoa production and consumption……………………...i Appendix 2 The 3 botanic varieties of cocoa trees worldwide…………………………………ii Appendix 3 The 3 different stages of the harvest season………………………………………iv Appendix 4 Quality classification system of Ecuadorian cocoa……………………………….vi Appendix 5 Original questionnaire in Spanish………………………………………………..vii Appendix 6 English version of questionnaire………………………………………………...xvi Appendix 7 Total exportations of cocoa in grain 2003 – 2007…………………………...….xxv Appendix 8 Collinearity diagnostics – producer price………………………………………xxvi Appendix 9 Multiple linear regression – producer price (1st & 5th run)…………………...xxviii Appendix 10 Collinearity diagnostics – Marketing channel…………………………………..xxx Appendix 11 Binary logistic regression – Marketing channel (1st & 4th run)………………..xxxii

VIII

List of abbreviations ANECACAO Asociacíon Nacional de Exportadores de Cacao

(The Ecuadorian national association of cocoa exporters) CC Commodity Chain CCA Commodity Chain Analysis CORPEI Corporación de Promoción de Exportaciones y Inversiones Ecuadorian organ for the promotion of export and innovations) FFS Farmer Field School FO Farmer Organisation FOB Free On Board BCS BCS Öko-Garantie GmbH

(A Germany based international organic certifier and controlling agency)

FAO Food and Agriculture Organization of the United Nations GCC Global Commodity Chains GDP Gross Domestic Product GTZ Deutche Gesellschaft für Technische Zusammenarbeit (A Germany based international cooperation enterprise for sustainable development with worldwide operations) GVC Global Value Chain ha Hectares ICCO International Cocoa Organization ICE Intercontinental Exchange IICA Instituto Interamericano de Cooperación para la Agrícultura (Inter-American institute for agricultural cooperation) IMF International Monetary Fund

IX

INIAP Instituto Nacional Autónomo de Investigaciones Agropecuarias (The Ecuadorian national autonomous institute for agricultural research)

LA Latin America LCA Latent Content Analysis LDC Low Developed Country LIFFE London International Financial Futures Exchange MAG Ministerio de Agricultura, Ganadería, Acuacultura y Pesca (the Ecuadorian Ministry of Agriculture and Livestock) MCA Manifest Content Analysis MIC Ministerio de Industrias y Competitividad (the Ecuadorian Ministry of Industrialisation and Competitiveness) MNC Multi National Company MT Metric tons. Unit of measurement equivalent to 1000 kilograms NBR National Bureau of Economic Research NGO Non-Governmental Organisation NRI Natural Research Institute NYBOT New York Board of Trade PP Producer price qq Quintales. 1 quintal = 100 Spanish libras. Unit of measurement

equivalent to 45,36 kilograms TNC Trans National Company UDENOR Unión de Enxeñerías do Noroeste, S. A. Union of Engineers in the south-western part of South America) UNOCACE La Unión de Organizaciones Campesinas Cacaoteras del Ecuador

(Union of Ecuadorian cocoa producer organizations)

X

‘[Value] is adjusted… Not by any accurate measure, but

by the haggling and bargaining of the market, according

to that sort of rough equality which, though not exact, is

sufficient for carrying on the business of common life’

Adam Smith2

2 In The Wealth of Nations, book 1, chapter V.

XI

1. Introduction

1.1 Global production systems Increased globalization has made a variety of services offered in all corners of the world available

to the ‘global client’. The international trading pattern is frequently expanded through factors like

extended division of labour and global dispersion of production. A recent trend is outsourcing of

labour, which has been proved to be a very efficient way to conduct business. To comply with the

demands of a fastidious group of clients, improvements must be carried out continuously. The

high levels of expertise required in various fields have resulted in extended specialization. This

development of ‘knowledge clusters’ corresponds to Adam Smith’s ideas of an advanced

economy best to be achieved through specialization and detailed division of labour (Todaro and

Smith 2003). As a consequence, it is not longer sufficient for an industry to maintain an efficient

production in order to enter the global market and allow for sustained income growth. As well,

an overall understanding of the existing dynamics of the entire value chain is required to take

advantage of the new global production system (Kaplinsky and Morris 2002).

Unfortunately, it is still apparent that the appointment of winners cannot happen without losers.

Prebish and Singer presented in 1950 evidence for a tendency of relative prices of raw materials

(including agricultural products), when compared with the price of manufactured goods, to

experience a steady decline in the long term (Todaro and Smith 2003). As most production of

primary goods is located in Low Developed Countries (LDCs), their inhabitants tend to account

for the losers within the global trade pattern.

Tracing a global value chain of agricultural commodities reveals the ‘losers’ often to be found at

the very bottom; the farm level. This tendency being apparent in the world’s cocoa trade is

demonstrated by farmers struggling with low return of investments, despite the global cocoa

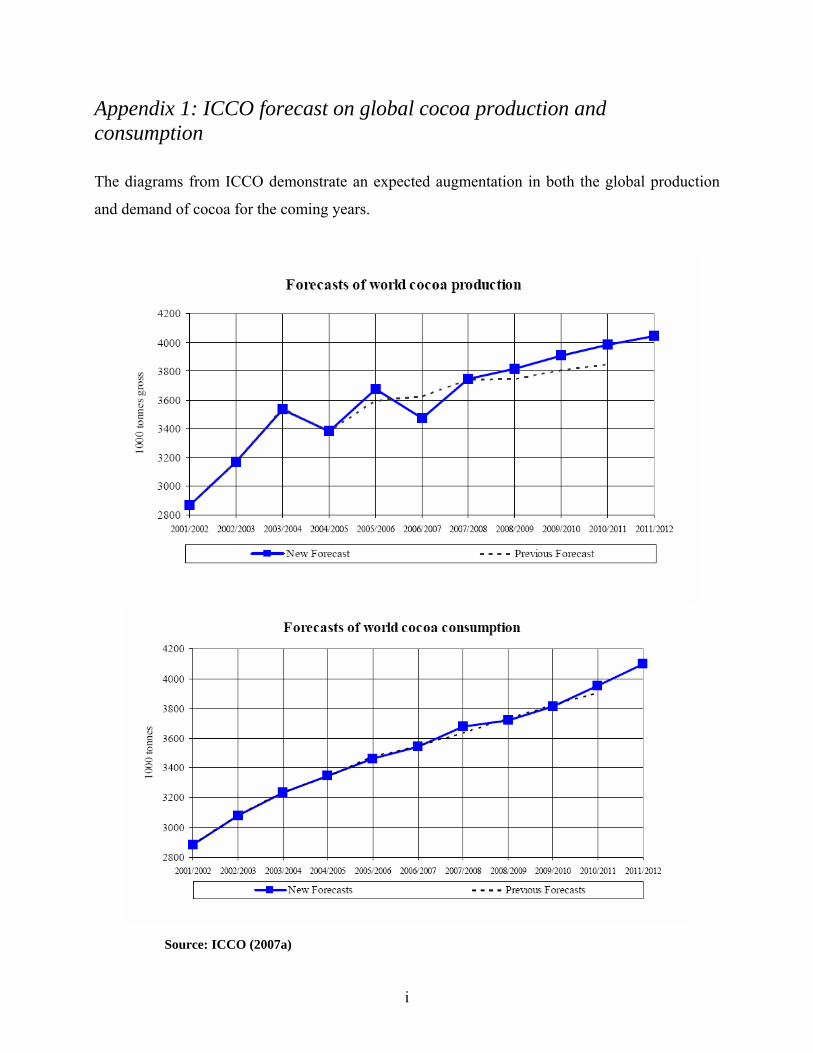

consumption3 is reaching new peaks annually (ICCO 2007a). Cocoa, being a buyer-driven

commodity whose value is set by the global produce exchange, is extremely vulnerable to price

fluctuation. When prices are low, it is easily observed within all levels of the value chain. But is

3 For further details, see ICCO forecast for global cocoa production and consumption in Appendix 1.

- 1 -

this the case as well when the prices are increasing? Or is some of the surplus likely to disappear

within the chain before reaching producer level? How can it else be explained that most

Ecuadorian farmers are living in poverty when the global market seems never to get enough of

the fine and aromatic cocoa of which Ecuador is the world’s leading producer?

1.2 Purpose of the study including its objectives Low agricultural output has been uttered by numerous (Ramírez 2006, 2007, Collinson and Leon

2000) to be the main explanation to the extended problem of poverty among actors operating at

the lower levels within the Ecuadorian cocoa sector. This is a well-documented and

acknowledged fact. The purpose of this study is to reveal whether there are any other

explanations to the existing poverty among Ecuadorian cocoa producers, with special attention

drawn to the price disbursed at farm level. With the goal set, I defined my main objective to be:

To calculate the producer price received by Ecuadorian small scale cocoa farmers, and

furthermore seek explanations for the variations I expect to reveal.

As I assume participation in alternative marketing channels to be of considerable importance to

the price received by the individual farmer, generating a general overview of the organization of

the national cocoa industry early in the research process will be crucial. Holding the motivation

of acquiring a profound understanding of both the design and structure of the commodity chain

constituted for the design of the first of my three sub-objectives:

Q1: How is the production and marketing of cocoa organized in Ecuador?

After having recognized its main components, my aim is to move all the way down to the very

bottom of the chain. Here I am to investigate the average price paid to producers participating in

the various marketing channels. In addition, I seek to reveal whether the price paid to the

producers is influenced by the quality of the product they offer.

Q2: What is the average price ($/qq) offered to the producers within the various marketing

channels and how does this price correlate with the quality of the cocoa purchased?

- 2 -

Expecting to find variations in the price offered to the producers within the different marketing

channels, I now seek to know why it is so. What characteristics do the farmers participating in the

commodity chain offering the highest/lowest prices inhabit, and how can they be differentiated

from the other cocoa producers?

Q3: How can the variation in the producer prices be explained?

In order to give an answer to the third sub-objective, the structural advantages as well as

disadvantages of each particular marketing chain must be given account for. Asking how come

farmers are better off participating in one commodity chain, may help reveal weaknesses or

limitations within the other chains, seen from the farmers’ perspective.

1.3 Limitations of the thesis As indicated in the previous section, the focus of this thesis is to trace the commodity chain of

Ecuadorian cocoa. Due to time constrains and vast amount of information in need to be gathered,

the limitation is set by the marketing of cocoa in grain. My sample will be gathered within the

region of Los Rios with the respondents selected randomly. Cocoa producers giving their answers

to my survey will constitute for the main sample, but additional information will be extracted

through semi-structured and observations of actors found at all level of the commodity chain.

1.4 Chapter outline The outline of the thesis will be as follows: With the purpose of providing the reader with basic

information of the functions, mechanisms and challenges within the Ecuadorian cocoa market, I

will in the following chapter (2) give a presentation of the national production system. Chapter 3

is used to present the theory, resulting in a framework to be applied in the analysis. For the reader

to obtain a better insight of the existing studies within the field, Chapter 4 will give account for

some of the previous research conducted. In Chapter 5 the methods applied in this study are

presented. Chapter 6 contain findings, analyses and discussions. With basis in the prior analyses,

I conclusions are drawn in Chapter 7.

- 3 -

2. Background

2.1 Ecuadorian cocoa production Ecuador is said to be the birthplace of cocoa (The Success Alliance 2007), and the country’s

history of cocoa cultivation can be traced back to the 17th century. Ecuador experienced a rapid

economic growth at the very start of the 20th century, with cocoa as the dominant export

commodity. When the Panama Canal opened in 1914, Ecuador was brought to the position as the

world’s main cocoa exporter, accounting for 20% of the global market (UN 1994). A historical

peak was reached in the years 1914 and 1916, when exports amounted for approximately $ 77

millions. In the latter period of the cocoa cycle (1926 – 1930), the structure of Ecuadorian exports

diversified, now accounting for coffee and rice as well. This transformation brought the shares of

cocoa exports to account for less than 50% of the total national exports (ibid). Despite the fact

that cocoa maintained the position as one of Ecuador’s most important export commodities

throughout big parts of the 20th century, the country’s share of the world’s total cocoa production

fell from 18% at the very start of the century, to 2% in 1945 (UNCTAD 1991).

Ecuador, producing the two types of cocoa; Nacional and CCN51, is world famous for its high

quality products. The variety Nacional, being a unique Ecuadorian product, has experienced a

widespread global demand for decades. Nacional, being the traditional variety cultivated for

centuries, does still dominate the national cocoa production, covering 95% of all the land areas

applied for cocoa production (SICA 2007a). Despite having its origin from the Forastero4 family

Nacional is considered being a fine and aromatic cocoa. Due to its characteristics, it has been

described as Pepa del Oro (‘Golden bean’) for decades. Its large sized seeds are developed by

light brown cotillions. The aroma of chocolate which is delicately accompanied by a floral

flavour characterizes its taste, is known as Arriba (ANECACAO 2007). The extraordinary

flavour is developed due to the quick fermentation5 of the cocoa seeds. In contrast to most other

types of cocoa which seeds in about six days, the Ecuadorian only needs three or four (Shared

interests 2007).

4 See Appendix 2 for further information about the different cocoa varieties. 5 See Appendix 3 for further information about the different stages of the harvest season.

- 4 -

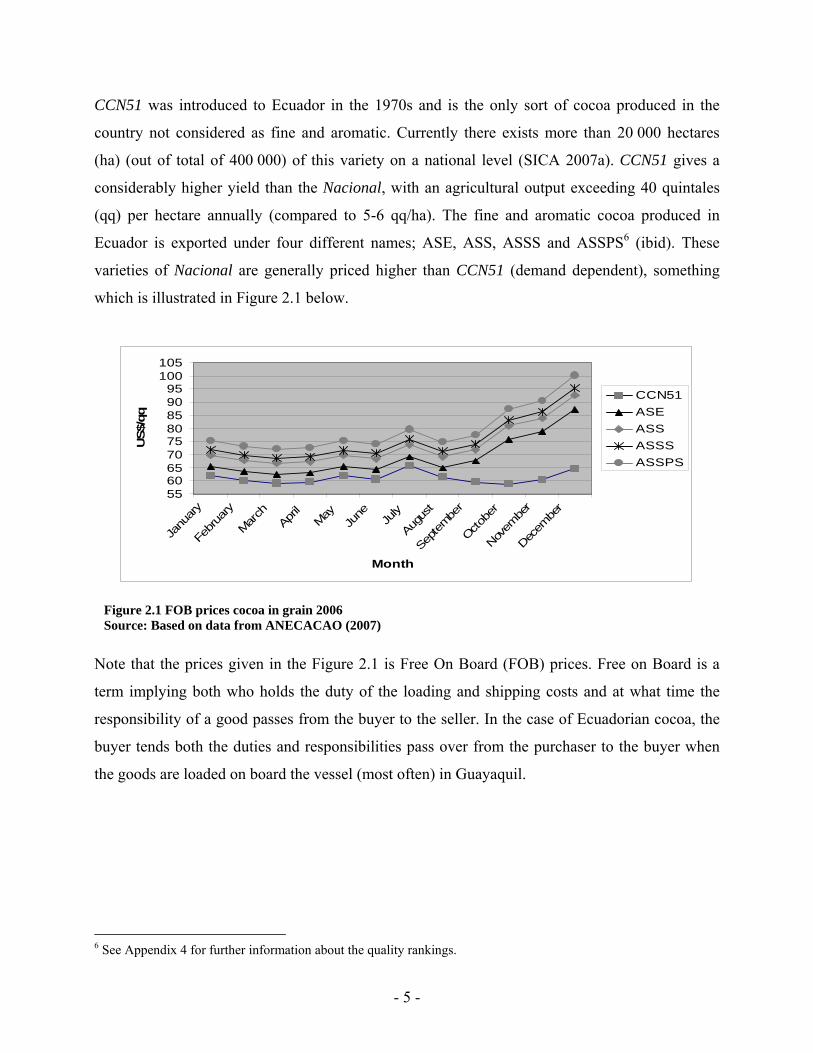

CCN51 was introduced to Ecuador in the 1970s and is the only sort of cocoa produced in the

country not considered as fine and aromatic. Currently there exists more than 20 000 hectares

(ha) (out of total of 400 000) of this variety on a national level (SICA 2007a). CCN51 gives a

considerably higher yield than the Nacional, with an agricultural output exceeding 40 quintales

(qq) per hectare annually (compared to 5-6 qq/ha). The fine and aromatic cocoa produced in

Ecuador is exported under four different names; ASE, ASS, ASSS and ASSPS6 (ibid). These

varieties of Nacional are generally priced higher than CCN51 (demand dependent), something

which is illustrated in Figure 2.1 below.

556065707580859095

100105

Janu

ary

Februa

ry

March

April

MayJu

ne July

Augus

t

Septembe

r

Octobe

r

Novem

ber

Decem

ber

Month

US$

CCN51ASEASSASSSASSPS

N

t

r

b

t

6

Figure 2.1 FOB prices cocoa in grain 2006 Source: Based on data from ANECACAO (2007)

ote that the prices given in the Figure 2.1 is Free On Board (FOB) prices. Free on Board is a

erm implying both who holds the duty of the loading and shipping costs and at what time the

esponsibility of a good passes from the buyer to the seller. In the case of Ecuadorian cocoa, the

uyer tends both the duties and responsibilities pass over from the purchaser to the buyer when

he goods are loaded on board the vessel (most often) in Guayaquil.

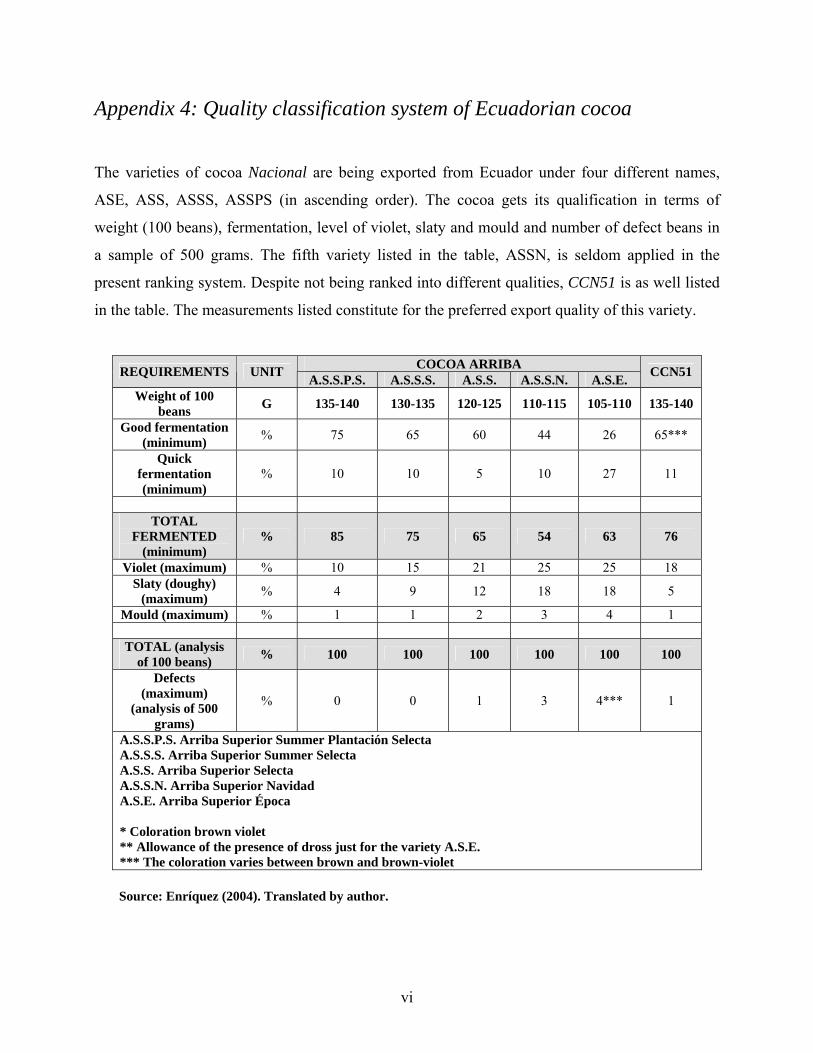

See Appendix 4 for further information about the quality rankings.

- 5 -

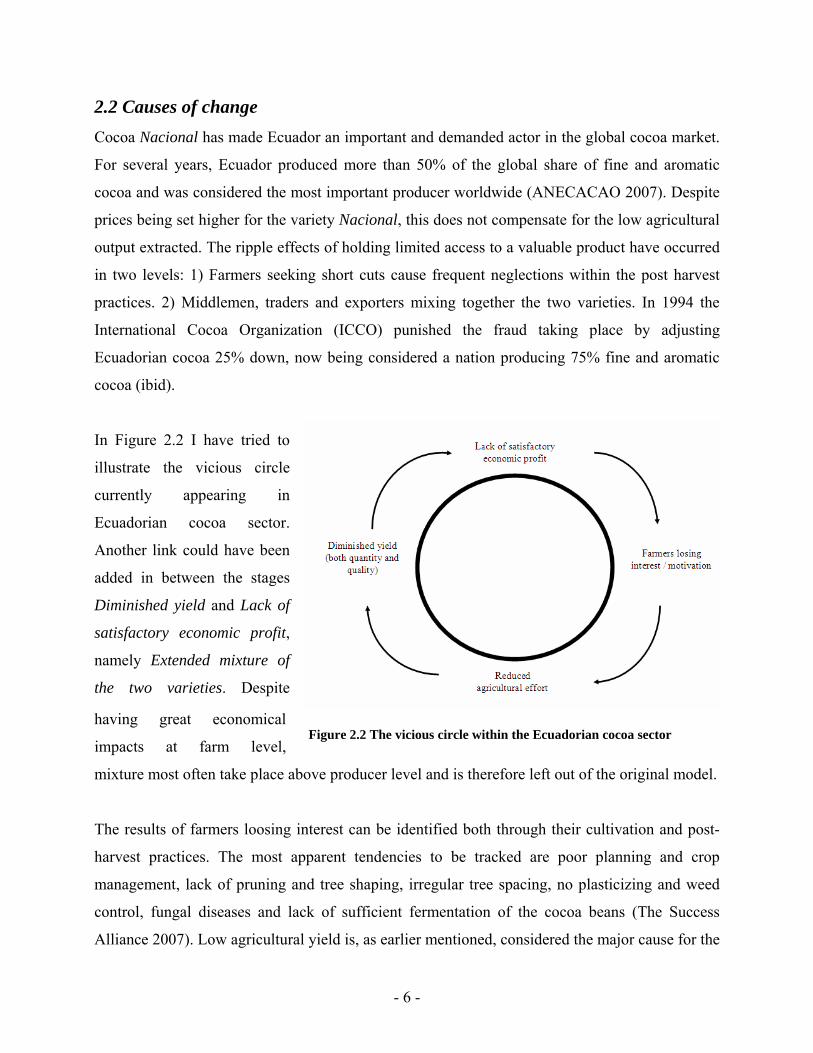

2.2 Causes of change Cocoa Nacional has made Ecuador an important and demanded actor in the global cocoa market.

For several years, Ecuador produced more than 50% of the global share of fine and aromatic

cocoa and was considered the most important producer worldwide (ANECACAO 2007). Despite

prices being set higher for the variety Nacional, this does not compensate for the low agricultural

output extracted. The ripple effects of holding limited access to a valuable product have occurred

in two levels: 1) Farmers seeking short cuts cause frequent neglections within the post harvest

practices. 2) Middlemen, traders and exporters mixing together the two varieties. In 1994 the

International Cocoa Organization (ICCO) punished the fraud taking place by adjusting

Ecuadorian cocoa 25% down, now being considered a nation producing 75% fine and aromatic

cocoa (ibid).

Figure 2.2 The vicious circle within the Ecuadorian cocoa sector

In Figure 2.2 I have tried to

illustrate the vicious circle

currently appearing in

Ecuadorian cocoa sector.

Another link could have been

added in between the stages

Diminished yield and Lack of

satisfactory economic profit,

namely Extended mixture of

the two varieties. Despite

having great economical

impacts at farm level,

mixture most often take place above producer level and is therefore left out of the original model.

The results of farmers loosing interest can be identified both through their cultivation and post-

harvest practices. The most apparent tendencies to be tracked are poor planning and crop

management, lack of pruning and tree shaping, irregular tree spacing, no plasticizing and weed

control, fungal diseases and lack of sufficient fermentation of the cocoa beans (The Success

Alliance 2007). Low agricultural yield is, as earlier mentioned, considered the major cause for the

- 6 -

extended poverty among Ecuadorian cocoa producers and a range of studies and projects have

been carried out holding the aim of increase the agricultural output extracted. However, there are

factors above actor level which should be brought up, discussing influences for Ecuador

gradually to loose its position in the global cocoa market.

Rough and unpredictable weather conditions make farming in Ecuador a continuous struggle. The

country has been a victim of natural hazards as drought and floods over the years, most severe in

the years 1975, 1983, 1995 and 1998, as well as earthquakes (1987) and volcano eruptions (1999)

(ICG 2007). Secondly, unstable relations to their neighbouring countries have made Ecuador

suffer from lack of foreign investment initiatives. The Colombian guerrilla movements in the

north and brief wars with Peru in the south (1981, 1995) have contributed to undermine the

nation’s economic environment (ibid). Furthermore, the nation’s economy has suffered from

governmental mismanagement (rent-seeking and corruption) throughout the last decades. U.S.

Department of State utters Ecuador's political parties to “... have historically been small, loose

organizations that depend more on populist, often charismatic, leaders to retain support than on

programs or ideology” (U.S. Department of State 2007). Years of governmental mismanagement

has made the population loose faith in the political system, as there has been a tendency of

Ecuadorian politicians to prioritize western interest (as well as self interests) rather than the

national. As a consequence of natural disasters (among others El Niño) and a sharp decline in the

world’s petroleum prices, Ecuador experienced a major banking crisis and recession in 1999

(CIA 2007). As the real GDP contracted with more then 6% and the banking system collapsed,

Ecuador had no choice but to adopt U.S. dollars as a legal tender in 2000 (ibid).

During the decades of 1950s, ‘60s and ‘70s, import substitution policies were pursued in most

Latin American (LA) countries (Stiglitz & Charlton 2005). Despite experiencing a rapid growth

in their economies during the period, a turning point was met in the early 1980s when none of the

LA countries experienced much economic growth. A regional average of 6% growth during the

1970s felt to almost zero in the 80s. Professionals have argued against one another for the causes

of this stagnation. While the neo-liberal view, favoured by IMF and the World Bank, put the

blame on import substitution combined with an excessively degree of state intervention, an

alternative view has put more emphasis on Latin America’s open capital markets. This view

- 7 -

claims Latin America’s reliance on foreign direct investments and external flows of capital to be

the factor most influential for the area being so vulnerable of global economic shocks. The heavy

loans the LA nations undertook during the ‘70s enabled them, for some while, to avoid the global

recession which followed the oil price shock. Finally, the Latin American debt crisis became a

crude fact in the early 1980s, when the US Federal Reserve augmented the interest rates of these

loans to level unmanageable for most of the nations to handle (ibid).

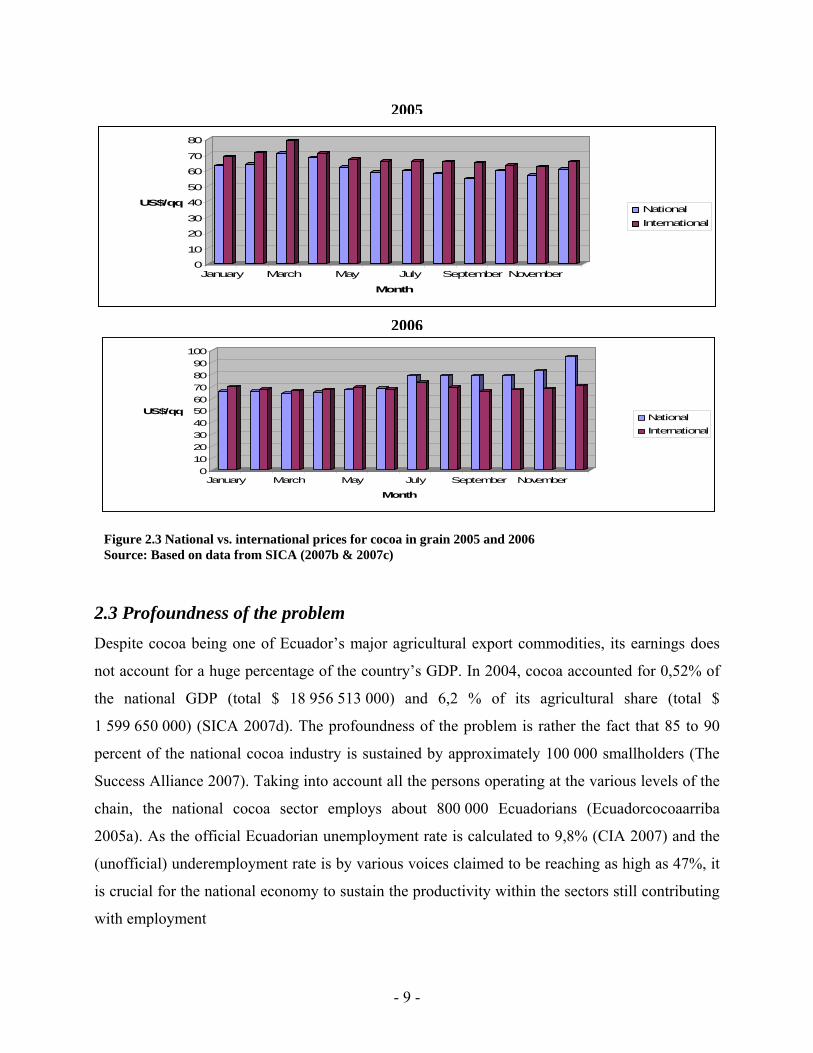

According to a report from The Natural Resource Institute (NRI) Ecuadorian cocoa is marketed

without governmental interference, meaning local prices are calculated taking point of departure

in international prices and local supply and demand (Collinson and Leon 2000). This leads local

prices occasionally to move out-of-sympathy with the New York7 and London prices (where the

world’s cocoa exchange are situated) as they are determined by the demand from the nations own

cocoa processing industry and neighbouring countries (ibid). The report identifies other

hallmarks in the Ecuadorian cocoa sector to be lack of competition laws, absence of monopolies

and cartels, minimal governmental interference, low levels of vertical and horizontal integration

and finally no existence of barriers to entry (ibid). Figure 2.3, on the following page, illustrates

the divergence between national and international cocoa prices in 2005 and 2006.

Cocoa being a product highly vulnerable to price volatility has motivated many cocoa producing

countries to establish ways of protecting the farmers economically. Primarily, this is done by

setting fixed producer prices. Setting fixed producer prices does not only imply economic

security for the producers, but as well for the government. In addition to work as an incentive for

the expansion or contraction of production, a set price pattern makes the collection of general

revenue and taxation of the producers easier for the government (UNCTAD 1991). As pointed

out by Collinson and Leon (2000), not all cocoa producing countries experience governmental

interference. This is specially being the case within the countries in Latin America and in Asia

where the marketing of cocoa is left to the private producers, as the governmental agencies are

overseeing a variety of aspects (UNCTAD 1991).

7 Corresponding to the overall Ecuadorian practices, point of departure will primarily be taken in the NYBOT (New York Board of Trade) prices in this paper.

- 8 -

2005

0

10

20

30

40

50

60

70

80

US$/qq

January March May July September November

Month

NationalInternational

2006

0102030405060708090

100

US$/qq

January March May July September November

Month

NationalInternational

Figure 2.3 National vs. international prices for cocoa in grain 2005 and 2006 Source: Based on data from SICA (2007b & 2007c)

2.3 Profoundness of the problem Despite cocoa being one of Ecuador’s major agricultural export commodities, its earnings does

not account for a huge percentage of the country’s GDP. In 2004, cocoa accounted for 0,52% of

the national GDP (total $ 18 956 513 000) and 6,2 % of its agricultural share (total $

1 599 650 000) (SICA 2007d). The profoundness of the problem is rather the fact that 85 to 90

percent of the national cocoa industry is sustained by approximately 100 000 smallholders (The

Success Alliance 2007). Taking into account all the persons operating at the various levels of the

chain, the national cocoa sector employs about 800 000 Ecuadorians (Ecuadorcocoaarriba

2005a). As the official Ecuadorian unemployment rate is calculated to 9,8% (CIA 2007) and the

(unofficial) underemployment rate is by various voices claimed to be reaching as high as 47%, it

is crucial for the national economy to sustain the productivity within the sectors still contributing

with employment

- 9 -

3. Theory

Holding the motive of producing a theoretical framework to guide the further analysis, various

theories are introduced throughout this chapter. By gradually filling in pieces to the puzzle, the

final goal is to develop an overall theoretical basis contributing to ease the analysis of my third

research objective, factors influencing the prices received by Ecuadorian cocoa producers.

3.1 Commodity Chains In order to present the action taking place between actors operating at the various levels in the

Ecuadorian cocoa sector, and furthermore identify which impacts these interactions have on the

producer price received by the farmers located at the very bottom of the chain, theories concerned

with the functions of commodity chains (CCs) can contribute with beneficial information.

Different methodologies and theories have been developed in order to analyse commodity chains.

In this thesis the focus will be directed towards the most significant approaches found in

literature, Commodity Chain Analysis/French Filière (CCA), Global Value Chains (GVC) and

Global Commodity Chains (GCC). Assuming participation in alternative marketing channels to

be of great impact to the price received by the Ecuadorian cocoa producers, their structure and

agents (‘requirements of admission’) are important to reveal. Directing their focus towards the

different practices taking place within the single chain, each of the above listed commodity chain

approaches can make useful contributions to my research.

3.1.1 Commodity Chain Analysis (CCA)

The Commodity Chain Analysis (CCA) was developed by the French Research Institution

(French Filière) dealing with local production systems and consumptions in the 1960’s in order to

achieve “… a neutral, value-free technique applied to analyze existing marketing chains for

agricultural commodities assessing how public policies, investments and institutions affect local

production systems”, and is composed of “… a quantitative analysis of inputs and outputs, prices

and value added along a commodity chain through agents accounts” (Tallec and Bockel 2005:3).

The term is used referring to a general group of economic agents, and their activities, making a

direct contribution to the determination of a final product. The chain of production includes all

- 10 -

processes taking place from the transformation until delivery to the final market of one particular

agricultural product (ibid). The empirical research tradition has been dominant since the rise of

the filière analysis. Throughout its development the main objective has always been to map out

the abovementioned commodity flows and to identify the agents (typically done through the

design of flow-charts of commodities and transformations) (Raikes et al. 2000). Launched almost

half a century ago, the CCA has provided the basis for the development of the GVC and GCC

approaches. Due to their common origin, similarities are easily traced and differentiation can

sometimes be hard.

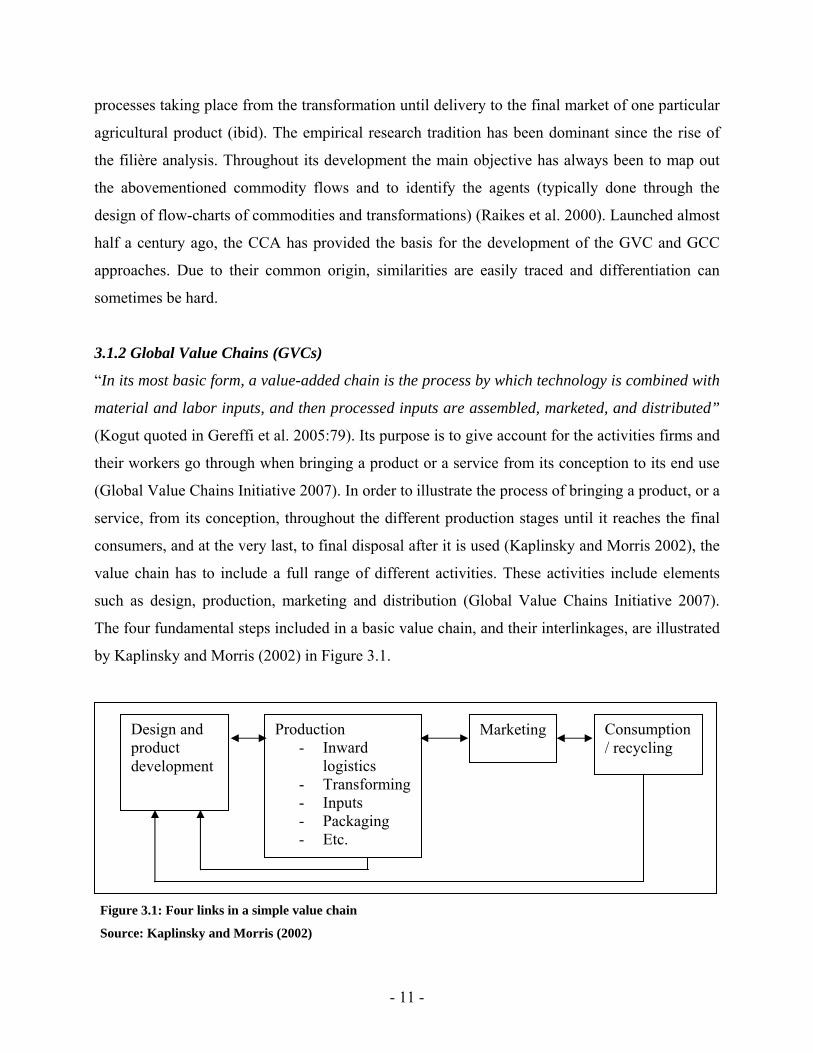

3.1.2 Global Value Chains (GVCs)

“In its most basic form, a value-added chain is the process by which technology is combined with

material and labor inputs, and then processed inputs are assembled, marketed, and distributed”

(Kogut quoted in Gereffi et al. 2005:79). Its purpose is to give account for the activities firms and

their workers go through when bringing a product or a service from its conception to its end use

(Global Value Chains Initiative 2007). In order to illustrate the process of bringing a product, or a

service, from its conception, throughout the different production stages until it reaches the final

consumers, and at the very last, to final disposal after it is used (Kaplinsky and Morris 2002), the

value chain has to include a full range of different activities. These activities include elements

such as design, production, marketing and distribution (Global Value Chains Initiative 2007).

The four fundamental steps included in a basic value chain, and their interlinkages, are illustrated

by Kaplinsky and Morris (2002) in Figure 3.1.

Design and product development

Production - Inward

logistics - Transforming - Inputs - Packaging - Etc.

Marketing Consumption / recycling

Figure 3.1: Four links in a simple value chain

Source: Kaplinsky and Morris (2002)

- 11 -

Moving away from theory and into the real world, you are not likely to come across such a

simple structure within the value chain of any product or service (Kaplinsky and Morris 2002).

The reality is normally much more complex. One of the most apparent differences is the number

of linkages in the chain; there tend to be many more. Taking the complexity of the real world into

account makes it a comprehensive task to conduct research on global value chains. Examples of

areas you are dependent of obtaining sufficient knowledge about are job details, technologies,

standards, regulations, products, processes and markets valid for the specific product and the

region under investigation (Global Value Chains Initiative 2007).

To explain the binary view of how global production is to be organized - either through markets

or within transnational firms, Gereffi et al. (2005) address the issue of transaction costs. They

furthermore claim the global value chains to be found in different forms, as they display a range

of different characteristics and have a multiplicity of impacts on diverse communities. The issue

of governance is central in the global value chain approach, as “… a chain without governance

would just be a string of market relations” according to Humphrey and Schmitz (2001:2). With

information gathered from global case studies, Gereffi et al. (2005) are proposing a complete

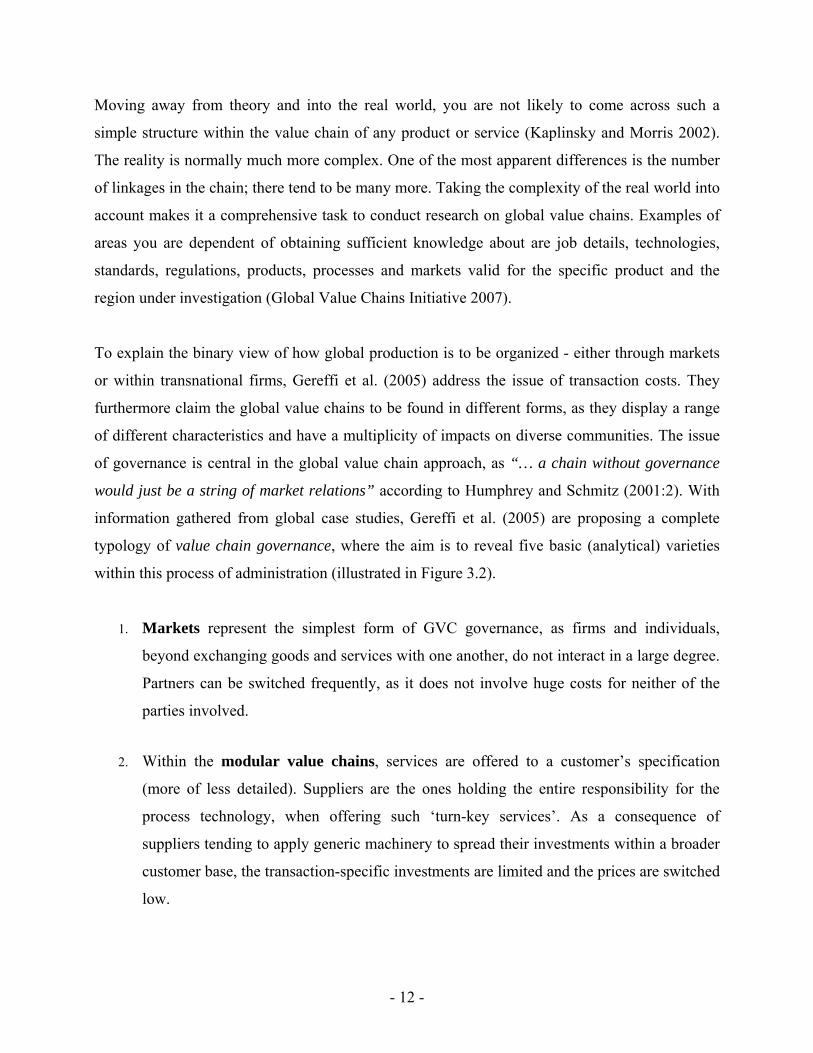

typology of value chain governance, where the aim is to reveal five basic (analytical) varieties

within this process of administration (illustrated in Figure 3.2).

1. Markets represent the simplest form of GVC governance, as firms and individuals,

beyond exchanging goods and services with one another, do not interact in a large degree.

Partners can be switched frequently, as it does not involve huge costs for neither of the

parties involved.

2. Within the modular value chains, services are offered to a customer’s specification

(more of less detailed). Suppliers are the ones holding the entire responsibility for the

process technology, when offering such ‘turn-key services’. As a consequence of

suppliers tending to apply generic machinery to spread their investments within a broader

customer base, the transaction-specific investments are limited and the prices are switched

low.

- 12 -

3. Relational value chains are built upon complex relationships between buyers and sellers,

frequently resulting in mutual dependence and a high level of assets specificity. The

relationship can either be based upon family or ethnic ties, reputation, social or spatial

proximity.

4. In the captive value chains small scale suppliers tend to be dependent on larger,

dominant buyers. These networks are often characterized by asymmetric power relations

with high degree of monitoring and control by the lead firm, as the suppliers are relying

on their cooperation.

5. Vertical integration is the characteristic of hierarchy, where the dominant form of

governance is managerial (top-down) control (Gereffi et al. 2005).

Figure 3.2 Five global value chain governance types

Source: Gereffi et al. (2005)

- 13 -

3.1.3 Global Commodity Chains (GCCs)

While the Global Value Chains has its focus directed towards the value added to a product while

it moves upwards the chain, the GCC approach is more interested in revealing the processes

taking place between the different stages.

Despite being defined by Hopkins and Wallerstein already in 1986 as “… a network of labour

and production processes whose end result is a finished commodity” (Gereffi and Korzeniewicz

1994:2), the concept of Global Commodity Chains became first well-known after being

introduced to the literature by Gary Gereffi in the mid-1990’s, referring to GCCs as the whole

range of activities involved in the design, production and marketing of a product (ibid). The

global Commodity Chain has as its primary focus “… to analyse the international trading system

and the increasing economic integration of international production and marketing chains”

(Tallec and Bockel 2005:3). Hopkins and Wallerstein indicate its greatest virtue to be its

emphasis on the process (Gereffi and Korzeniewicz 1994). Originally the concept of GCC was

created to analyse the impact of globalization on industrial commodity chains. Moreover, GCCs

were to emphasize the embedded power relations in value chain analyses, by unveiling the

dominant party (parties) determining the overall characteristic of the chain. Gereffi and

Korzeniewicz apply the term network referring to the overall configuration of relations in the

network or its parts. By using these properties in their analyses of commodity chains, they claim

to include the ‘length’ of the chain and the ‘density’ of interactions in a particular segment, as

well as the ‘depth’ or number of levels occurring at different stages of a GCC (ibid).

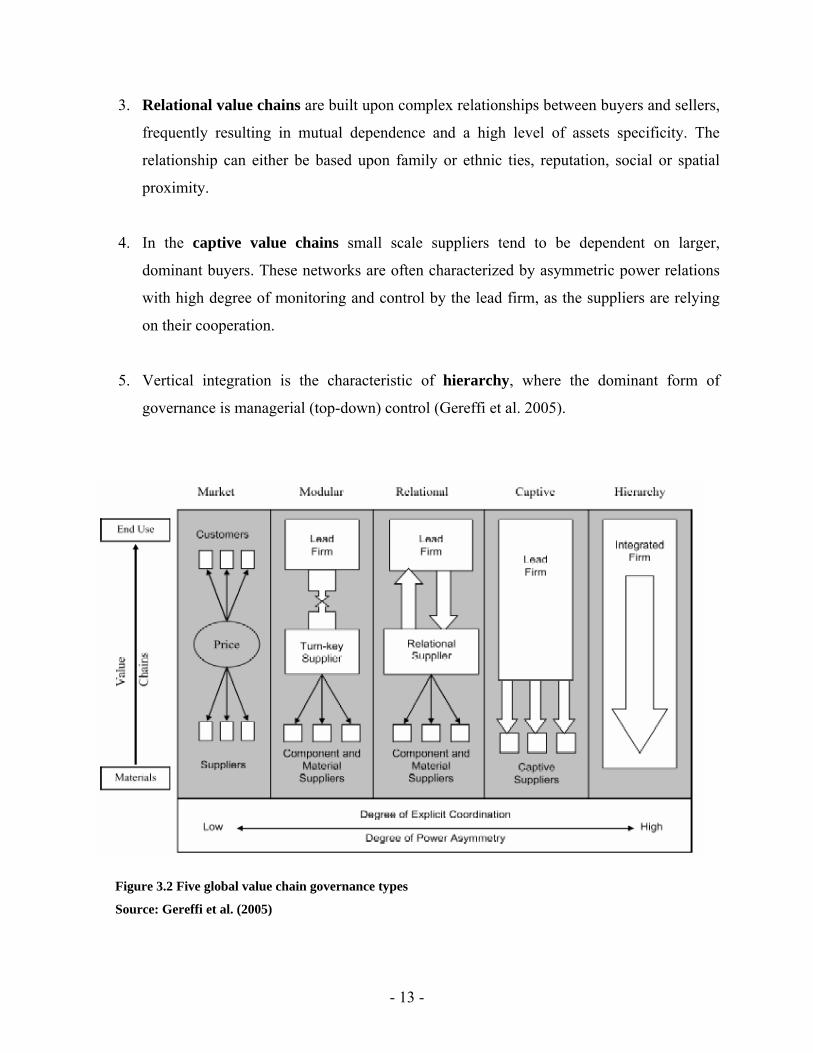

The form for governance conducted in a GCC, Gereffi (1999) argues either to be producer- or

buyer driven. The producer-driven commodity chain he characterizes to contain huge firms

playing central roles in the coordination of the production networks. The archetypal actors are

technology- and capital intensive manufacturers, including the industry of cars, aircrafts and

other heavy machineries (ibid). One of the major differences between the producer- and buyer

driven commodity chains is the control being exercised by the administrative headquarters of

Transnational Companies (TNCs) in producer-driven production systems (Gereffi and

Korzeniewicz 1994). Figure 3.3 illustrates the structure of a simple producer-driven commodity

chain.

- 14 -

Figure 3.3 The Organization of Producer-driven Commodity Chains

Source: Gereffi and Korzeniewicz (1994)

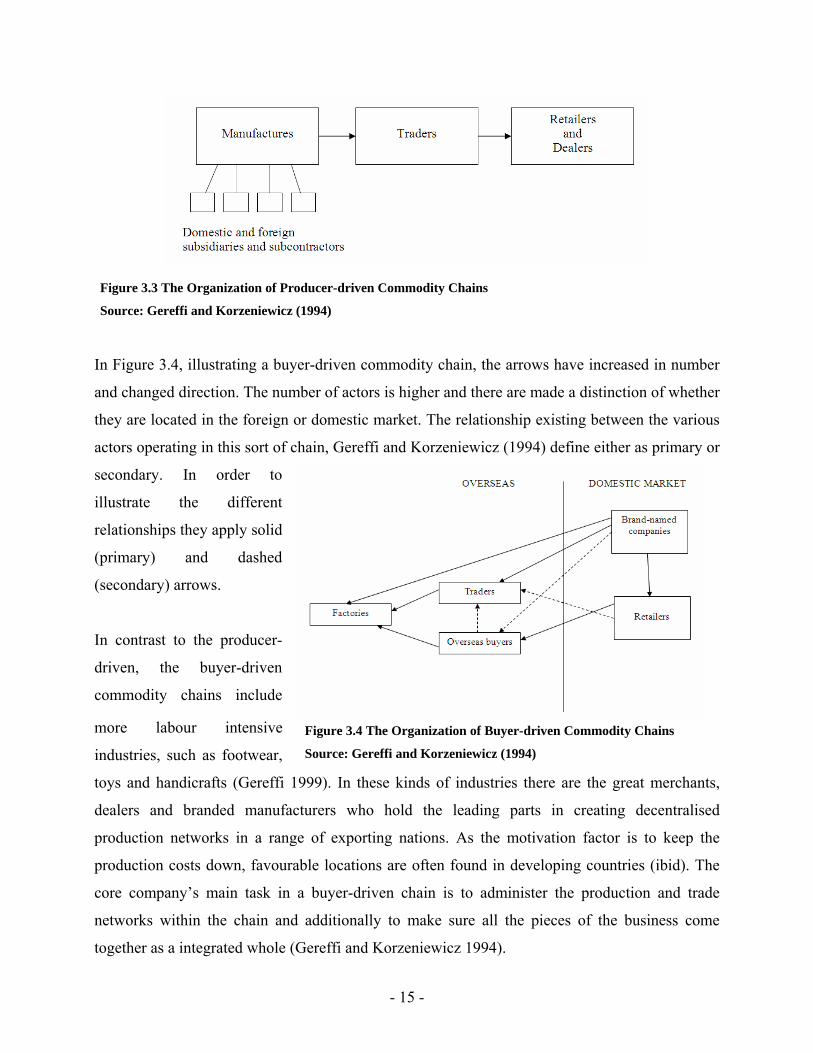

In Figure 3.4, illustrating a buyer-driven commodity chain, the arrows have increased in number

and changed direction. The number of actors is higher and there are made a distinction of whether

they are located in the foreign or domestic market. The relationship existing between the various

actors operating in this sort of chain, Gereffi and Korzeniewicz (1994) define either as primary or

secondary. In order to

illustrate the different

relationships they apply solid

(primary) and dashed

(secondary) arrows.

Figure 3.4 The Organization of Buyer-driven Commodity Chains

Source: Gereffi and Korzeniewicz (1994)

In contrast to the producer-

driven, the buyer-driven

commodity chains include

more labour intensive

industries, such as footwear,

toys and handicrafts (Gereffi 1999). In these kinds of industries there are the great merchants,

dealers and branded manufacturers who hold the leading parts in creating decentralised

production networks in a range of exporting nations. As the motivation factor is to keep the

production costs down, favourable locations are often found in developing countries (ibid). The

core company’s main task in a buyer-driven chain is to administer the production and trade

networks within the chain and additionally to make sure all the pieces of the business come

together as a integrated whole (Gereffi and Korzeniewicz 1994).

- 15 -

3.2 Organization and participation As already mentioned, the national cocoa sector employs a rather large share (6%) of the

Ecuadorian population, accounting for about 13.9 millions inhabitants (CIA 2007). The 100 000

producers alone represent about 0,7% of the total population. Taking into account the national

underemployment rate (47%) and the age structure (62,7% being between 15 – 64 years), cocoa

farmers constitute for 2,2% of the working (fulltime) share of the population.

Despite being part of such a large occupational group, the Ecuadorian cocoa producers hold an

extreme limited market power. One of the explanations could be found in the structure of the

commodity chain in which the farmers participate; the individual producer being just one out of

numerous actors in the labour intensive buyer-driven commodity chain. Stimulating to collective

action and enhanced level of participation through the creation of Farmer Organizations (FOs)

could be one alternative way of breaking down the existing (hierarchical) power pattern within

the cocoa chain.

3.2.1 Organization and its obstacles

The occurrence of Farmer Organisations in developing countries (both at local and higher levels),

became for real triggered in the 1980’s and 1990’s. FOs ought to fulfill numerous roles and

functions. Denis Pesche (2002) has identified the major ones to be; 1) provide services to their

members (technical or economic), 2) represent the interests of both their members and the other

farmers situated in the area, and 3) be involved in local development by providing different sorts

of social investments. Furthermore, Pesche makes a division between the internal and the external

work done by the FOs. While the internal work takes basis in the strengthening of their functions

and fulfilling the needs of their members, the external work is primarily focused on extending

their networks (external partners) and to achieve overall recognition of their work (ibid).

With basis in his wide experiences working with farmer organizations in Ecuador and several

other countries in Latin America, Anthony Bebbington (1991) utters FOs being able to help

strengthen the market power among agriculturalists holding scarce resources. Collective sales are

often mentioned as one of the major benefits of being part of a larger union. Not only are prices

often set higher when larger quantities are purchased, also competition is likely to be reduced

- 16 -

when the farmers collaborate rather than compete. Finally, Bebbington utters farmers being easier

detected by the other participants within the chain to be of crucial importance when combating

the existing power structures in the general commodity chain.

According to Bebbington (1991), FOs can furthermore, by actively adapt and disseminate

agricultural technologies in programs they themselves control and administer, contribute to build

sustainable livelihood for the rural poor. In addition, farmer organizations can act as a ‘user

constituency’ for the rural poor, pressuring public sector and non-governmental agricultural

agencies to orient their work to the needs of the rural poor. Lastly, farmer organizations is

claimed by Bebbington to act as an ‘interface’ between the research and extension worlds of

development agencies and the livelihood conditions of the resource poor farmer population (ibid).

With the current recognition of the benefits attached to the creation of farmer organization, how

come the phenomena are not better splayed on a global scale? The Norwegian sociologist, author

and politician Gudmund Hernes (1975) lists five circumstances, under which the possibilities for

people organizing are reduced. The first obstacle in order to organize, Hernes claims to be the

possible deprivation of freedom of speech and organization among the citizens within a nation.

The second obstacle he identifies to involve costs. Namely, that the ones with the highest

advantages of joining such an organization are in some cases unable of handling the costs of

establishment, something often resulting in insufficient representation of interests. In his third

point, Hernes emphasizes the problem of solidarity. He claims the possibilities for organization to

be reduced when the actors with common interest within one field, are affected in different

degrees of resolutions made within other fields. His fourth point is touching upon more concrete

barriers. Even though actors have democratic freedom and permanent interests which are shared

with others, they can meet problems in terms of organization due to physical barriers (i.e. large

distances, poor infrastructure, etc.). In his final point, Hernes underlines despite overcoming all

the abovementioned factors, actors can still meet difficulties in the case of organization due to

their personal terms of action. The problem of free riders is to be found within the field of

organization as well as most other places in the society. When the services offered by an

organization are not limited only to its members, but to all members of the society, it is difficult

- 17 -

to encourage organizational commitment (ibid). Despite being presented more than 30 years ago,

the problematic brought up by Hernes do still prevail, especially within the context of LDCs.

3.2.2 Participation

Holding the common goal of increased development for the global poor, the importance of

participation is commonly agreed. Organizing farmers is one way to encourage involvement, and

the history provides us with numerous evidences of the close connection existing between NGOs,

FOs and the level of participation.

The era of aid and development was up to the late 1970’s dominated by top-down approaches,

concerned by implementing western ideas and knowledge rather than to encourage participation.

Throughout history agricultural projects have tended to be (at least to some degree) participatory,

as farmers often have been included in discussions about their challenges and needs. Anyhow, it

is not until recently that the necessity of more formal participation has been recognized within

most disciplines, including the agricultural (Oakley et al. 1991). A common understanding does

now exist among most professionals, namely that in order to better ensure the success of a project

farmers’ participation has to be developed more formally (ibid).

In addition to recognize how to best ensure an agricultural project’s efficiency and effectiveness,

Oakley et al. (1991:26) address a range of benefits that can be gained from formal participation of

farmers. In areas containing low level of farmers with access and active contact with agricultural

services, formal participation can make the farmers (or clients) more visible and thereby

contribute to increase the coverage and extension of such services (individual farmers easier

ignored or ‘failed to see’). Furthermore, formal participation of farmers can help breaking down

the inherent resistance to change often apparent in farming communities, and as well assist dispel

any mistrust of external ideas by ensuring the farmers that their ideas will be taken into

consideration and built into the objectives of any given projects. By formal participation it is

easier to guarantee the needs of the farmers to be covered rather than only depend of the ideas of

the outside professionals. Finally, formal participation can make contributions to ensure projects

to benefit the groups of smaller and more marginal farmers, not only the ones better off (ibid).

- 18 -

3.3 The role of NGOs NGOs, or non-governmental organizations, have experienced a steady increase of their activities

throughout the twentieth century, with a particular acceleration within the last couple of decades.

A recent estimate has claimed it to be between fifteen and twenty five thousand NGOs operating

on a global scale (Eade 2000). The primary geopolitical focus is concentrated on the ‘Third

World’ of former European colonies and the ‘Second World” of former (and some still

remaining) communist states (DeMars 2005). Their activities cover a spectre of issues, “…from

feeding famine victims and protecting endangered species, to eliminating nuclear weapons and

AIDS, to democratizing Russia and the Arab world” (ibid:1). Farrington, Bebbington et al.

(1993) claim NGOs to constitute for a promising, but not yet firmly established ‘third sector’.

Hence, it is a sector which is contrasting itself from the practices of both the public (state) and

private (for-profit), due to its frequent interaction with both.

But what is to be included in the expression NGO? All organizations without any governmental

interference, as the name implies? Bebbington, Thiele et al. (1993) claim the term NGOs to

traditionally been applied describing both national and international organizations, based either in

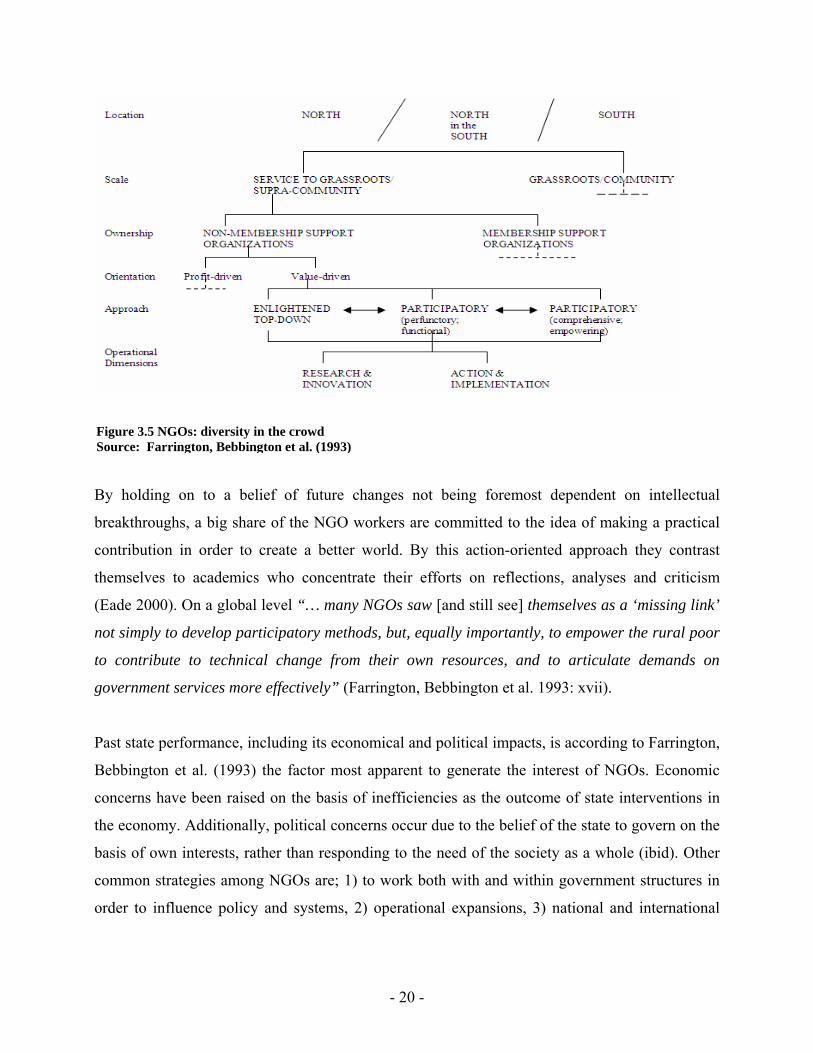

North or South. Clark is being criticized by Farrington, Bebbington et al. (1993) to be all

inclusive when applying the term. Despite distinguishing between the six categories relief and

welfare agencies, technical innovation organizations, public service contractors, popular

development organizations, grassroots development organizations and advocacy groups and

networks, Clark consider them all as NGOs. These classifications made by Clark do not make

any sense according to Farrington, Bebbington et al, claiming they are not being able to

distinguish the work by Oxfam with the work of a local neighbourhood organization when

applying his system. Instead they are presenting their own figure (3.5), where classifications in

accordance to location, scale ownership, orientation, approach and operational dimensions are

made (ibid).

Having the complexity of the term presented, I will throughout the remaining parts of the thesis

refer to NGOs as organizations giving support to grassroots organizations, rather than themselves

being one.

- 19 -

Figure 3.5 NGOs: diversity in the crowd Source: Farrington, Bebbington et al. (1993)

By holding on to a belief of future changes not being foremost dependent on intellectual

breakthroughs, a big share of the NGO workers are committed to the idea of making a practical

contribution in order to create a better world. By this action-oriented approach they contrast

themselves to academics who concentrate their efforts on reflections, analyses and criticism

(Eade 2000). On a global level “… many NGOs saw [and still see] themselves as a ‘missing link’

not simply to develop participatory methods, but, equally importantly, to empower the rural poor

to contribute to technical change from their own resources, and to articulate demands on

government services more effectively” (Farrington, Bebbington et al. 1993: xvii).

Past state performance, including its economical and political impacts, is according to Farrington,

Bebbington et al. (1993) the factor most apparent to generate the interest of NGOs. Economic

concerns have been raised on the basis of inefficiencies as the outcome of state interventions in

the economy. Additionally, political concerns occur due to the belief of the state to govern on the

basis of own interests, rather than responding to the need of the society as a whole (ibid). Other

common strategies among NGOs are; 1) to work both with and within government structures in

order to influence policy and systems, 2) operational expansions, 3) national and international

- 20 -

lobbying and advocacy, and finally 4) to strength the organization of the poor (including

networking and federations) (Eade 2000).

The last point by Eade is of particular interest conducting research at farm level. As mentioned

earlier in this chapter, farmers who organize enhance their chances of breaking out of the

traditional power structure within a commodity chain. Their odds are further strengthened if their

FO receives support from a NGO, as these organizations often constitute a part of an extended

network of partners not only holding agricultural knowledge and technology/equipment, but as

well political influence and economic resources. Being intercepted by a NGO can be vital for the

prosperity among individual farmers or an independent FO. By strengthening the producers in

certain areas or within specific organizations, Bebbington (1991) claims the appearance of NGOs

is likely cause power asymmetries at the producer level.

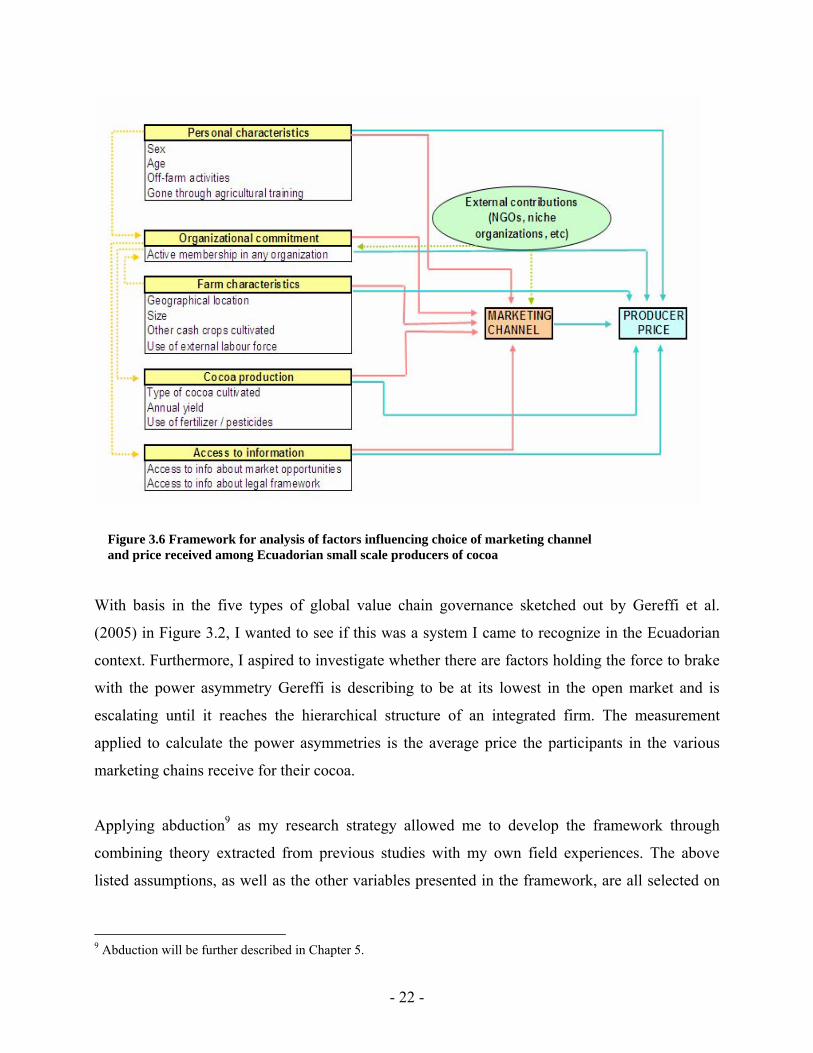

3.4 Theoretical framework One of the aims of this study (Q3) is to reveal the structure of three different types of marketing

channels within the Ecuadorian cocoa sector; the open market, direct purchases and contractors

with Multinational Companies (MNCs), and furthermore give account for the impacts

participation in each and every has on the price paid to the producers. Before initiate the process

of analysis, it is essential to give account for the factors expected to most influential for the

individual producer’s access to/choice of marketing channel. To be better equipped to analyze

this process, a framework for analysis of factors influencing choice of marketing channel and

price received among Ecuadorian small scale producers of cocoa was developed (Figure 3.6).

The framework, which aim is to give an answer to the third sub-objective, is principally build up

on three assumptions. The first is, as already indicated, choice of marketing channel to affect the

producer prices. The second assumption is, farmers with organizational commitment being more

likely to gain access to alternative8 marketing channels. And finally, external contributors to

accelerate contact between the different actors in the commodity chain; in this case enhance the

chances of a FO to be included in an alternative marketing channel.

8 By alternative marketing channel I indicate alternatives to the open market structure.

- 21 -

Figure 3.6 Framework for analysis of factors influencing choice of marketing channel and price received among Ecuadorian small scale producers of cocoa

With basis in the five types of global value chain governance sketched out by Gereffi et al.

(2005) in Figure 3.2, I wanted to see if this was a system I came to recognize in the Ecuadorian

context. Furthermore, I aspired to investigate whether there are factors holding the force to brake

with the power asymmetry Gereffi is describing to be at its lowest in the open market and is

escalating until it reaches the hierarchical structure of an integrated firm. The measurement

applied to calculate the power asymmetries is the average price the participants in the various

marketing chains receive for their cocoa.

Applying abduction9 as my research strategy allowed me to develop the framework through

combining theory extracted from previous studies with my own field experiences. The above

listed assumptions, as well as the other variables presented in the framework, are all selected on

9 Abduction will be further described in Chapter 5.

- 22 -

basis of first and secondary information and experiences of which determinants to be influential

to the price setting mechanisms within the Ecuadorian cocoa sector.

The uncertainties were many in the initial part of the research process as I neither held much

knowledge about the global, nor the Ecuadorian cocoa sector before start writing this thesis. Not

knowing exactly ‘where to start searching’ resulted in a rather comprehensive questionnaire10.

The survey was divided into five subsections, each one constituting for what I considered to be of

overall importance in revealing the differences in producer prices.

The first sequence of my questionnaire, cocoa production, was included with the intention to

reveal whether cultivation practices had any impacts on the price received by the farmer. As

already mentioned, there have been conducted a range of studies demonstrating insufficient effort

at producer level to cause low agricultural output (Ramírez 2006, 2007, Collinson and Leon

2000, etc). My motivation was to test whether the agricultural efforts had any impacts on the

price offered the farmers as well (through enhanced quality of the product). The second

subsection is marketing. Taking basis in the commodity chain theory presented earlier in this

chapter, I sought to identify the economical impacts of the individual producer’s sales practices.

Motivated to unveil the advantages obtained by producers participating in different kinds of

marketing channels, special attention was given to the five types of value chain governance

Gereffi et al. (2005) describe in Figure 3.2. Questions concerning national structures/policy

constitute the third part. This group of question was included into the questionnaire to

demonstrate the effects of Collinson and Leon (2000) claiming Ecuadorian cocoa to be marketed

without governmental interference. The matter of organization is the concern of the fourth

subsection, organization and participation theories providing the basis. Here I aspired to figure

out whether the motivation factors and outcome of joining an organization among my selection of

respondents being organized could be compared to the ones listed by Pesche (2000) and

Bebbington et al. (1991). Simultaneously I sought to disclose if it was possible to draw parallels

betweens the ideas presented Hernes (1975) and the motivations for not joining organizations

among the unorganized share of my respondents. In the last subsection, the respondents of my

questionnaire were asked to give account for their background information. These questions

10 See Appendix 5 and 6 for outline of the questionnaires (Spanish and English version)

- 23 -

worked as control variables, controlling whether any personal characteristics could cause impacts

on the producer price.

In the selection of which questions from my survey to transform into independent variables in the

framework, two considerations were done. First, I drew advantage of the experiences gained

through conducting interviews and observations. Additionally, I got the questionnaires reviewed

by professionals within the Ecuadorian cocoa sector, expressing their opinions of the covered

issues. The hypotheses developed in this process (presented in Chapter 6), became later on the

independent variables presented in Figure 3.6.

The yellow dashed arrows at the very left side of the framework are included in order to illustrate

the assumed relationship between the independent variables. Unveiling the relationships between

these variables will be a task too comprehensive to include in this study, and they will therefore

not be given any further attention.

- 24 -

4. Previous studies There exist a range of studies with their attention drawn towards agricultural commodity trade.

While some narrow down their focus to concentrate on one particular link within the commodity

chain, others hold motive of mapping the entire chain, including its function and its stakeholders.

These latter kinds of studies can either trace the chain upwards, with point of departure in farm

level, or downwards, with a finish product as their starting point. The amount of studies covering

the same aspects of cocoa trade, within the similar conditions as in my research area in Ecuador,

is however smaller. The absence of identical studies causes a wider range of studies to be referred

to in this chapter. Some of the research looks at trade and marketing of cocoa in West African

countries, while other is conducted in Ecuador, concentrating on various aspects within the

national cocoa sector. Unfortunately, I am a little bit too early in getting my hands on a study

currently carried out by the ICCO11 in Ecuador (among several countries), analysing the value

chain in cocoa producing countries

4.1 Commodity chain studies in Ecuador Pilar A. Jano (2007), conducting a study of the marketing chain of Ecuadorian cocoa for her

Master degree at Virginia Polytechnic Institute and State University in 2007, brings up the very

important issue of incentives to produce quality, in form of price premiums, not to be transmitted

efficiently along the marketing chain all the way down to farm level. Among the range of themes

she covers in her thesis, a specific attention directed towards the role of the middlemen is to be

found. Jano concludes with intermediaries to be weak on transaction transparency, creating

transaction costs impediments and reducing the transmission of price incentives to the farmers,

with particular respect to incentives to produce high quality cocoa. Additionally, the author

advertises for the national standards to approve the cocoa exports (INEN norms) to be modified,

resulting in exporters being more demanding with respect to quality from the wholesalers who

will transmit these requirements to the local middlemen and finally to the producers.

Conducting a study of the economic viability of ethical cocoa trading in Ecuador, Chris Collinson

and Marcelo Leon (2000) take point of departure in Agroexportadora Maquita, an alternative 11 For further project description, see http://www.icco.org/projects/projects1.aspx?id=z2p2766

- 25 -

trade organization operating in Ecuador. The aim of their study is to find out how current ethical

trade practitioners operate in the forest products context and whether the trade brings incremental

benefits to forest dependent people. They conclude with Maquita’s business performance to be

impressive, as Ecuador provides a difficult environment in which to conduct business with a

national marketing system not restricting competition. Due to its remarkable commercial

performance, the organization has managed to deliver substantial economic benefits to its target

smallholder cocoa producers. Thereby the authors stress the importance of organization and

collective sales to be carried out in order to enhance the income level of Ecuadorian cocoa

farmers. Certifications (Fair Trade, Rain Forest friendly, Organic, etc) contributing to increase

the value of their product are difficultly achieved for individual farmers. Easier access to

certifications is one of a whole range of factors contributing to an enhanced likelihood of

increased income for smallholders joining organizational activities.

Anthony Bebbington (1991) is covering the issue of farmer organizations in Ecuador. In addition

to bring up three main functions of farmer organizations (already referred to in the theory

chapter), Bebbington claims Ecuadorian FOs to be formally organized at several levels. Moving

away from the basic stage constituting for a household or kin group, FO’s are found at

community-, parish- and county level. While the lower level groups primarily perform an

interfacing function, the active research and extension function, in addition to the constituency

role, are more likely to be performed among the higher level groups. Another point made by

Bebbington is the interference of NGOs. Despite bringing a range of advantages to the FOs

‘gaining their support’, external contributions by NGOs are likely stimulate competitiveness

between communities and thereby weaken the inter-community collaboration.

Being presented as a study of the structure and dynamics of the Ecuadorian cocoa chain, the

technical document set out by Pedro Ramírez (2006) for Ecuadorcocoaarriba12 gives a thorough

account for the different mechanics and actors in the global cocoa market. Loaded with frequent

statistics and illustrations, the paper is designed as a general ‘cocoa guide’. The document

provides the reader with useful and well arranged information, especially in its last chapter,

12 A collaboration between the German international cooperation enterprise GTZ and the Ecuadorian innovation and exportation organ CORPEI

- 26 -

presenting the visions and goal for how the chains should develop towards 2010. The formulation

of these goals can be interpreted as solution to current problems or challenges within the sector.

Some of them Ramírez identifies to be: 1) Renovate and create new plantations in order to obtain

larger volumes 2) Ensure better quality of the cocoa exported by strengthen the national quality

control system, forbid exportation of products with poor quality and create agreement within all

levels of the chain in order award (economically) high quality cocoa 3) Create new and

strengthen existing farmer organizations to encourage collective commercialization.

CORPEI (2006) is the author of Ecuador Exporta, a magazine presenting various issues

concerned with innovations and market dynamics. In December 2006 the entire edition was

dedicated to the topic of how to establish a competitive strategy of the chain of fine and aromatic

cocoa in Ecuador, with various key figures in the Latin American cocoa industry making their

contribution. The conclusion of where to direct the attention after having the different viewpoint

presented, was narrowed down to include four core areas: 1) Enter new markets 2) Increased

quality of the cocoa 3) Provide technical assistance 4) Extended commercialization. Based upon

the background of the contributors in this debate, these four areas are where the LA ‘cocoa elite’

identifies the recent, most severe challenges in Ecuadorian cocoa sector to be located, and where

future improvements must be carried out.

4.2 Studies of international cocoa trade With an aim to investigate the effects of domestic policies on exportable primary commodities,

W. Asenso Okyere (1989) applies the case of cocoa in Ghana. In the paper he argues it is not only

international market problems, but additionally the misguided and conflicting economic policies

of LDCs which are responsible for the economic challenges faced by these nations. In order to

illustrate his point, Okyere illuminate the strong connection between LDCs domestic economic

policies and the well-being of their export sector. In the conclusion, the author explains the

improvements in the Ghanaian cocoa sector and the nation’s economy to be caused by the

country’s careful examination and adjustment of its domestic economic prices, rather than

improvements in international terms of trade or dramatic changes in the consumer demand for

cocoa.

- 27 -

In a working paper for National Bureau of Economic Research (NBR), Christopher L. Gilbert

and Panos Varangis (2003) take point of departure in West African cocoa producers in

illustrating the effects of liberalization of the tropical agricultural markets. As a consequence of

the liberalization, which major objective was farmers to obtain a higher share of the FOB price,

cocoa producers do now face global, rather than domestic prices. The motivation for the study

conducted by Gilbert and Varangis was to identify what impacts this new trade pattern, caused by

an increased globalization, has caused on producer level. The authors argue producers currently

to get a higher share of a lower price, as lower world prices are the outcome of a downward shift

of the aggregated supply curve, in conjunction with inelastic demand. In other words, the farmers

belonging to the liberalized African markets can in general not be claimed for being better or

worse off.

Ghana provides as well the basis for Niels Fold’s (2002) studies stressing the importance of

spatial sub-systems of the global cocoa chain. According to Fold, the structural patterns and

relationships in two given sub-systems, the regional trading-sorting-grinding complex in the

Zaanstreek, Amsterdam and the national cocoa bean supply system in Ghana, suggest that the

dynamic of ‘bi-polar’ buyer-driven chains is best comprehended in terms of various types of

containment strategies of the lead firm. In the type of bi-polar chain Fold claims the cocoa chain

to be, the major markets are slow-growing and far-reaching mergers and acquisitions are

extremely costly. These characteristics make containment the key for understanding the dynamics

of the chain. In the understanding of the word containment, Fold includes “…company strategies

constantly defend and try to improve positions in the global market by creating competition

among suppliers upstream and expanding the portfolio of customers and sales outlets

downstream” (ibid: 246). Like Gilbert and Varangis, Fold brings up the theme of liberalization

and privatization of domestic trade, by stating the former focus on market prices now to have

been accompanied by a concern for global supply stability. The reason for this concern is the

impacts declined income among smallholders may have on the global supply of cocoa. The

producers are likely to put less effort in the cultivation practices if they feel they are not awarded

properly for their labour input.

- 28 -

5. Method

“Sometimes we find a case, and sometimes a case finds us. In both instances, selection combines

purpose and serendipity” (Hay 2000:41).

5.1 Case studies The phrase by Iain Hay introducing this chapter does in a large degree reflect the circumstances