Embed Size (px)

Citation preview

HEALTH INSURANCE

EXCHANGES 101

Copyright © PeopleKeep, Inc., 2018. PeopleKeep® is a registered trademark of PeopleKeep, Inc.

Hello. We’re glad you’re checking out our content. We just wanted to let you know that this content is a little bit behind the times. It’s still useful—but it’s not our freshest material.

For more timely resources, visit www.peoplekeep.com/resources.

Wondering why PeopleKeep is showing up in your Zane Benefits content?

PeopleKeep was created to personalize benefits for small business. Zane Benefits and PeopleKeep worked in parallel for a short time, but as PeopleKeep grew, we decided they should function as one company. Zane Benefits is now part of PeopleKeep.

Copyright © PeopleKeep, Inc., 2017. PeopleKeep® is a registered trademark of PeopleKeep, Inc.

Self-administer 20171017 V2.R1

ii

Copyright © PeopleKeep, Inc. 2017. PeopleKeep® is a registered trademark of PeopleKeep, Inc.Personalized Benefits 20171017 V1.R3

Our storyOffering traditional group benefits sucks. Why? They’re too expensive, too complex, and too one-size-fits-all. PeopleKeep is a new way to offer benefits called personalized benefits. Most people believe benefits are the services a company offers, such as a health insurance plan or 401k. With personalized benefits, it’s the opposite. Companies give people tax-free money to spend on the consumer services they find most valuable. It’s as simple as wages. For small businesses that think offering traditional group benefits sucks, PeopleKeep is personalized benefits automation software that makes offering benefits simple, painless, and personal for everyone.

Today more than 3,000 companies use PeopleKeep to hire and keep their people across the United States. PeopleKeep is based in Salt Lake City, Utah.

To learn more about PeopleKeep, visit www.peoplekeep.com.

Ready to see how PeopleKeep can work for your company? Visit www.peoplekeep.com/demo to preview our software or click below to have a Personalized Benefits Advisor contact you.

contact sales

Copyright © PeopleKeep, Inc., 2018. PeopleKeep® is a registered trademark of PeopleKeep, Inc.

HEALTH INSURANCE EXCHANGES 101

2

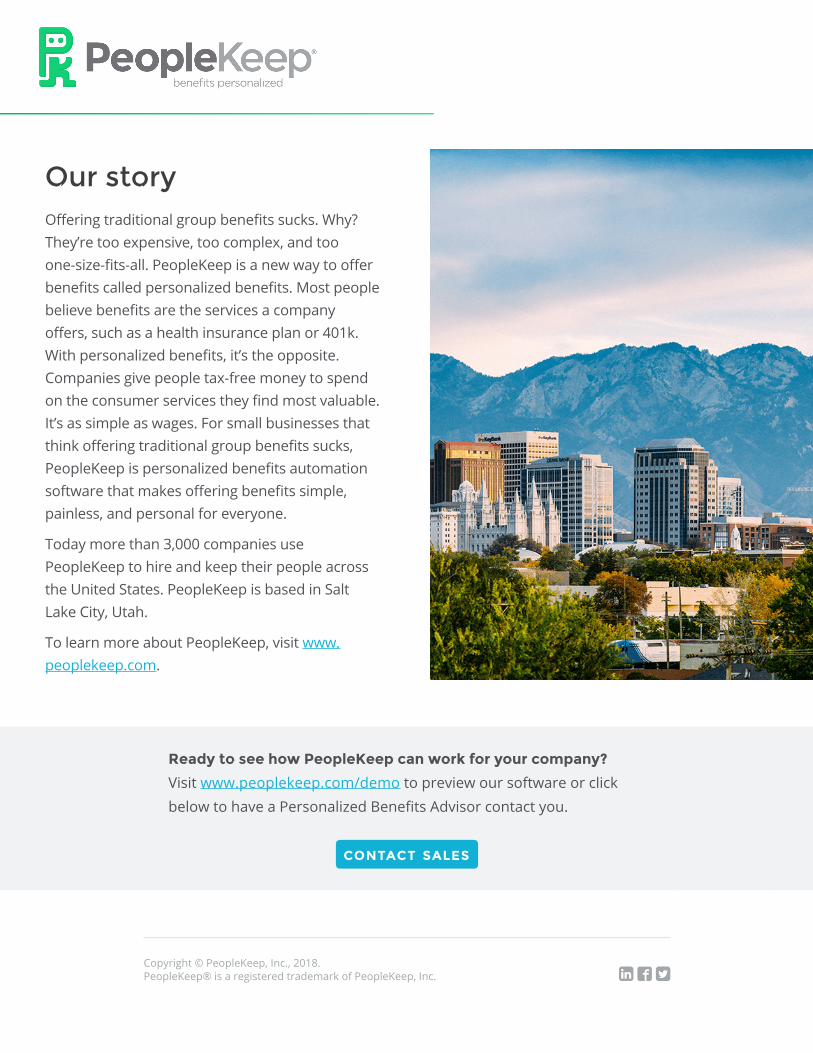

PREFACE

The biggest buzzword of this decade in the employee health benefits market is "Health Insurance

Exchange". Starting January 1st, 2014, the Affordable Care Act (ACA) requires every state to create

health insurance exchanges for businesses, employees and individual. And, if a state fails to set up

the exchanges in time, the federal government will step in.

What is a Health Insurance Exchange?

Webster defines an exchange as a place where things or services are exchanged, such as a store or

shop specializing in merchandise usually of a particular type.

So, at a basic level, a health insurance exchange is a store or shop specializing in health insurance

merchandise. More specifically, a health insurance exchange is an insurer’s broker’s or government’s

insurance offering to individuals and/or employees.

Today's health insurance exchanges typically include the following components:

A choice of two or more health insurance options

Advice and recommendation on what health insurance options best fit your needs

Automated billing for the chosen health insurance plan premium(s)

On-going support for the chosen health insurance plan(s)

HEALTH INSURANCE EXCHANGES 101

3

How Does a Health Insurance Exchange Work?

Health insurance exchanges come in many different shapes and sizes. They almost always include

choice of two or more health insurance options, advice on the best fit for each client, automated

billing, and ongoing support.

To understand how a particular health insurance exchange (such as the exchanges required by ACA

in 2014) works, you must answer the following questions about the particular exchange:

1. Is the health insurance exchange Public or Private?

2. Is the health insurance exchange Individual Market Based or Group

Market Based?

3. Who is eligible to participate in the health insurance exchange?

4. What products are available in the health insurance exchange?

5. What is unique about the health insurance exchange?

Let's walk through (and answer) the above questions from the perspective the of the imminent health

care reform exchanges. This will give you the tools to analyze and understand any health insurance

exchange you come across.

1. IS THE HEALTH INSURANCE EXCHANGE PUBLIC OR PRIVATE?

This is pretty straightforward:

A private health insurance exchange is a health insurance

exchange run by a private company.

A public health insurance exchange is a health insurance

exchange run by a government (or government-contracted)

entity.

Since the ACA requires states to create the exchanges in 2014,

those exchanges will be considered public health insurance exchanges. If a state fails to set up a

health exchange, the federal government will set up and run one for them.

Numerous entities ranging from start-ups to new divisions of leading insurance companies have

been created to offer new Private Health Exchanges.

To understand health insurance exchanges, you

must answer these questions.

HEALTH INSURANCE EXCHANGES 101

4

2. IS THE HEALTH INSURANCE EXCHANGE INDIVIDUAL OR GROUP MARKET BASED?

In general, there are two core health insurance exchange models:

Group Market Health Insurance Exchange – An exchange that sells “group”

health insurance to employees of employers. This is traditionally referred to as a

"Cafeteria Plan".

Individual Market Health Insurance Exchange – An exchange that sells

“individual” health insurance to individuals and families (that may be employees) in

the individual health insurance market. This is traditionally referred to as "Individual

Health Insurance Quoting".

The ACA requires states to create both a Group Market Health Insurance Exchange (called the

"SHOP") and an Individual Market Health Insurance Exchange (called the "American Health

Benefit Exchange") in 2014.

3. WHO IS ELIGIBLE TO PARTICIPATE?

A health insurance exchange may have specific eligibility rules outlining who can participate in the

exchange. For example, an exchange might limit eligibility to only specific individuals or business

based on:

An individual's household income

An individual's employer

A business's size (i.e. number of employees)

A business's ability to meet minimum employer

contribution requirements

A business's ability to meet minimum

employee participation requirements, etc.

Initially, the SHOP exchange limits eligibility to only businesses with up to 100 employees.

Similarly, the American Health Benefit Exchange limits eligibility to only individuals who are U.S.

citizens and legal immigrants who are not incarcerated.

HEALTH INSURANCE EXCHANGES 101

5

4. WHAT PRODUCTS ARE AVAILABLE IN THE EXCHANGE?

A health insurance exchange may offer a

variety of insurance products from a variety of

providers. There is no minimum or maximum

requirement. For example, a health insurance

exchange might offer:

Different Medical Plans from Multiple

Carriers, and/or

Different Medical Plan Designs from a

Single Carrier.

Both the SHOP Exchange and the American Health Benefit Exchange will provide multiple major

medical carriers with multiple plan design options (so, both #1 and #2).

5. WHAT IS UNIQUE ABOUT THE EXCHANGE?

A health insurance exchange may offer unique or "special" services to the businesses, employees

or individuals participating in the exchange. These unique offerings might include:

Exclusive product

Special rates

Tax advantages, etc.

CONCLUSION

Starting in 2014, small businesses can only access the small business healthcare tax credits through

the public SHOP exchange. Similarly, starting in 2014, massive tax subsidies will be available for

Individuals earning less than 400 percent of the federal poverty level. Individuals can only access the

premium subsidies through their state’s Individual Health Insurance Exchange.

For up-to-date information about health insurance exchanges, visit our health care reform and

www.zanebenefits.com/health-care-reform-and-state-insurance-insurance exchange blog at

exchange-blog.

HEALTH INSURANCE EXCHANGES 101

6

ADDITIONAL HEALTH BENEFITS RESOURCES

View our full library of free health benefits tools, on-demand webinars, and eBooks at: www.zanebenefits.com/health-benefits-resources

HEALTH INSURANCE EXCHANGES 101

7

The #1 Online Health Benefits Solution Successfully transition to a health benefits solution that creates happier employees, reduces costs,

. Request a Demo. and frees up time for meaningful work

Zane Benefits' Partner Program is an opportunity for insurance professionals to provide clients with

Request a Partner Evaluation. custom Zane Benefits solutions.

Like Us on Facebook

Follow us on Twitter

Join our Defined Contribution Group

Watch our videos on YouTube

DISCLAIMER The information provided herein by Zane Benefits is general in nature and should not be relied on for commercial decisions without conducting independent review and analysis and discussing alternatives with legal, accounting, and insurance advisors. Furthermore, health insurance regulations differ in each state; information provided does not apply to any specific U.S. state except where noted. See a licensed agent for detailed information on your state. www.ZaneBenefits.com.

Happier Employees

With Zane’s solution, employees choose the health plan that best fits

their families' needs. Learn more.

Controllable Costs

Employers fix their costs by utilizing a

defined contribution approach.

Learn more.

More Time for Meaningful Work

Once implemented, Zane’s solution

takes less than 5 minutes per month

to administer online. Learn more.

Easy Transition

Zane Benefits’ implementation

team will ensure a smooth and fast transition for you

and your employees. Learn more.