Embed Size (px)

Citation preview

AQR C A P I T A L

M A N A G E M E N T

Clifford Asness

Managing and Founding Principal

AQR Capital Management, LLC

Hedge Funds, Hedge Fund Beta,

and the Future for Both

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 1

An Alternative Future

Seven years ago, I wrote a paper about hedge

funds in general (and ten years ago about

whether they actually hedge)

I was smart enough to present the pros and

cons of hedge fund investing

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 2

An Alternative Future

Seven years ago, I wrote a paper about hedge

funds in general (and ten years ago about

whether they actually hedge)

I was smart enough to present the pros and

cons of hedge fund investing, i.e., I hedged

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 3

An Alternative Future

Seven years ago, I wrote a paper about hedge

funds in general (and ten years ago about

whether they actually hedge)

I was smart enough to present the pros and

cons of hedge fund investing, i.e., I hedged

The basic conclusion was that something like

index funds and hedge funds represent the

future, but not yet…

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 4

Sources of Portfolio Returns

Dynamic

Returns

Market Returns

Skill

• Active strategies (“alpha”)

• Unique to certain managers

• Cynics and believers disagree on

its existence

• Pure value

• Pure momentum

• Arbitrage strategies

• Many agree on return premium

• Global equities

• Global bonds

• Commodities

• Most agree on

return premium

WHAT

HEDGE

FUNDS

SAY

WHAT

HEDGE

FUNDS

DO

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 5

Two Definitions of Hedge Funds

A strategy that:

Trades relatively liquid assets

Seeks to make positive

average returns over time

Provides diversification versus

traditional stock and bonds

markets

Investment pools that are:

Unconstrained

Unregulated

High fees

Illiquid

Non-transparent

Supposed to make money all

the time

Run for rich people in Geneva

by rich people in Greenwich

A Compensation Structure

Source: “An Alternative Future”. Diversification does not eliminate the risk of experiencing investment losses.

A Portfolio Tool

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 6

Hedge Fund Styles

Event Driven

Convertible Arbitrage

Global Macro

Fixed Income

Arbitrage

Equity Market Neutral

Long/Short Equity

Dedicated Short Bias

Emerging Markets

Managed Futures

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

5%

6%

7%

8%

9%

10%

2% 4% 6% 8% 10% 12% 14% 16%

Retu

rn

Volatility

Stocks & Bonds

Stocks, Bonds & Hedge Funds

7

Hedge Funds: The Good News

1. Hedge funds offer a diversifying, positive expected return

2. This can improve almost any portfolio’s risk-adjusted return

100% Bonds

100% Hedge Funds

100% Stocks

Note: We believe index results are exaggerated by illiquidity and survivorship bias,

but are in the right direction

Realized Efficient Frontier

Jan 1994 – June 2011

Source: Hedge Funds: DJ CS Total Hedge Fund Index, Stocks: S&P 500, Bonds: Barclays Capital Aggregate. For illustration only. Past performance is not an indication of future results.

Diversification does not eliminate the risk of experiencing investment losses.

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 8

Growth of Hedge Fund Assets

Source: Hedge Fund Research Inc.

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

Hedge Fund Industry AUM (Jan 1990 – Jun 2011, billions)

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 9

1. Lags in Mark to Market [Illiquidity]

2. Correlation

3. Momentum Strategies

4. Survivorship Bias

5. Option Writing

6. Performance Fee Option Maximization

7. Taxes

8. Spotty Historical Track Record

9. Hot Money

10. High-Water Mark Abuse

11. Structured / Levered / Guaranteed Products

12. Crowded Strategies

The “Dark Sides” of Hedge Funds (2004)

Source: “An Alternative Future”

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 10

Hedge funds have high and increasing levels of passive

market exposure

High & Rising Correlations

Source: Dow Jones Credit Suisse Hedge Fund Index (data from January 1994 – June 2011) and HFRI Hedge Fund Index (data from January 1990 – June 2011). Past performance is not an

indication of future results.

Popular Hedge Fund Indices’ Correlations with MSCI World

(Rolling quarterly hedge fund index returns through August 2011)

Since

Inception

10Yrs

7Yrs

5Yrs

3Yrs

Dow Jones Credit Suisse

Hedge Fund Index 0.66 0.86 0.90 0.90 0.92

HFRI Hedge Fund Index 0.82 0.94 0.94 0.95 0.96

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 11

Illiquidity Still a Big Problem

Source: HFRI Hedge Fund Index. For illustrative purposes only.

5-Year Rolling Regression of HFRI on S&P 500 and Lagged Quarter Graph Below is T-stat on Lagged Quarter

0.0

1.0

2.0

3.0

4.0

5.0

1995 1997 1999 2001 2003 2005 2007 2009 2011

T-Stat

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 12

What Happened in 2008?

1. Spectacular Asset Growth

2. Scaling Up Non-Scalable Strategies

Load up on beta (no longer “alternative”)

Load up on leverage (no longer “investment”)

Reduce liquidity (no longer “marketable”)

3. A Series of Unfortunate Events

Market Crisis (prices fall = bad for beta)

Financing Crisis (capital evaporates = bad for leverage)

Liquidity Crisis (everyone sells = bad for liquidity)

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 13

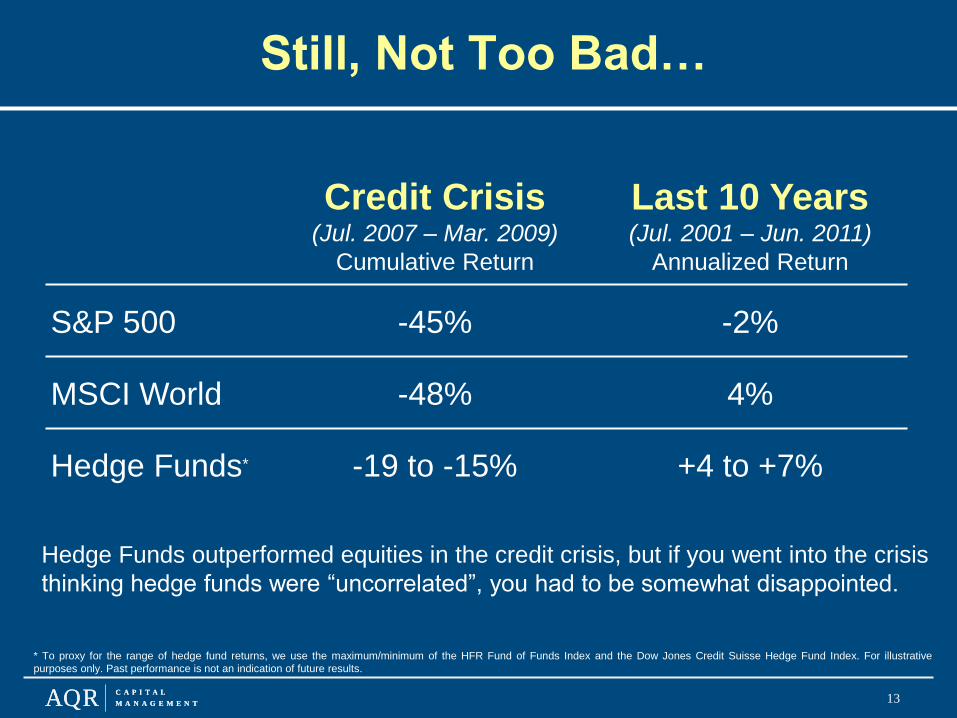

Still, Not Too Bad…

Credit Crisis (Jul. 2007 – Mar. 2009)

Cumulative Return

Last 10 Years (Jul. 2001 – Jun. 2011)

Annualized Return

S&P 500 -45% -2%

MSCI World -48% 4%

Hedge Funds* -19 to -15% +4 to +7%

Hedge Funds outperformed equities in the credit crisis, but if you went into the crisis

thinking hedge funds were “uncorrelated”, you had to be somewhat disappointed.

* To proxy for the range of hedge fund returns, we use the maximum/minimum of the HFR Fund of Funds Index and the Dow Jones Credit Suisse Hedge Fund Index. For illustrative

purposes only. Past performance is not an indication of future results.

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 14

Is There Still an Alternative Future?

Hedge Funds have a role in asset allocation if they:

1. Offer positive expected returns

2. Are uncorrelated (or at least low correlation) to

markets, especially equities

3. Are relatively liquid (if not please call them

something else)

Can this be done?

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 15

Time

ALPHA

ALPHA

HEDGE FUND

BETA

NON-

TRADITIONAL

BETA

TRADITIONAL

BETA

ALPHA

TRADITIONAL

BETA

ALPHA

NON-

TRADITIONAL

BETA

TRADITIONAL

BETA

Prior to Equity

Indices

‒ Returns viewed as

alpha

Traditional

Beta introduced

Examples:

– S&P 500 Index

– Barclays Aggregate

Non-Traditional

Beta introduced

Examples:

– Commodity Indices

– Real Estate

Hedge Fund

Beta introduced

Examples:

– Merger Arbitrage

– Convertible Arbitrage

How Alpha Becomes Beta

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 16

Why Might Alternative Returns Exist?

Liquidity Needs

• Companies need financing on good terms (convertible arbitrage)

• Supply and demand for capital not always balanced (carry trades)

Risk Aversion

• Investors don’t want to wait for mergers to close (merger arbitrage)

• General aversion to short stocks (short bias)

Suboptimal Investor Behavior

• Slow reaction to news, tendency to sell winners (managed futures)

• Avoid investments with bad news / poor results (value)

Manager Expertise

• Some people may be able to predict the future better than others

• Manager “craftsmanship”

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 17

Hedge Fund Beta

We think investors can access many hedge fund

strategies through hedge fund betas

Hedge Fund Beta is the set of risks shared by hedge fund

managers pursuing similar strategies

It can be invested in directly at low cost vs. hedge funds

Potential Advantages of investing in Hedge Fund Beta

• Diversified

• Economically Intuitive

• Lower Cost / Liquid

• Transparent

• Alternative

• Can be run hedged

Diversification does not eliminate the risk of experiencing investment losses.

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 18

Hedge Fund Beta Everywhere

Event Driven

Convertible Arbitrage

Global Macro

Fixed Income

Arbitrage

Equity Market Neutral

Long/Short Equity

Dedicated Short Bias

Emerging Markets

Managed Futures

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 19

HF Beta ≠ Replication

Hedge Fund

Beta

Hedge Fund

Replication

Primary

Objective:

Maximize diversifying

returns

High R2 to hedge fund

indices

Strategy

Construction: Bottom-up Top-down

Investment

Approach:

Dynamic strategies using

current information

Regression using prior

returns

Building

Blocks: Individual securities Broad indices

Traditional

Beta

Exposure:

Tactical and kept at

modest levels Potentially large

Diversification does not eliminate the risk of experiencing investment losses.

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 20

Drawing the Right Lessons

Some lessons from the crisis for hedge fund investors:

• Know where returns come from (alpha, hedge fund

beta, market beta)

• Be conscious of fees for each return source

• Build a portfolio based on this separation

Hopefully these steps pave the way to a brighter alternative

future for all of us

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T 21

Disclosures

The information set forth herein has been obtained or derived from sources believed by AQR Capital Management, LLC (“AQR”) to be reliable.

However, AQR does not make any representation or warranty, express or implied, as to the information’s accuracy or completeness, nor does

AQR recommend that the attached information serve as the basis of any investment decision. This document has been provided to you solely for

information purposes and does not constitute an offer or solicitation of an offer, or any advice or recommendation, to purchase any securities or

other financial instruments, and may not be construed as such. This document is intended exclusively for the use of the person to whom it has

been delivered by AQR, and it is not to be reproduced or redistributed to any other person. This document is subject to further review and revision.

There are many risks associated with convertible securities including but not limited to liquidity risk, equity risk, interest rate risk, and credit risk of

the underlying bond. Convertible bond securities may be considered illiquid securities, which cannot be sold or disposed of in the ordinary course

of business at approximately the prices at which they are valued. Difficulty in selling securities may also result in a loss or may be costly to the

portfolio. There is a risk of substantial loss associated with trading commodities, futures, options, derivatives and other financial instruments.

Before trading, investors should carefully consider their financial position and risk tolerance to determine if the proposed trading style is

appropriate. Investors should realize that when trading futures, commodities, options, derivatives and other financial instruments one could lose

the full balance of their account. It is also possible to lose more than the initial deposit when trading derivatives or using leverage. All funds

committed to such a trading strategy should be purely risk capital.