Embed Size (px)

Citation preview

www.hemas.com

Contents

• Country Overview : Key Statistics

• Hemas Group: A Snap Shot

• Our Businesses

• FMCG

• Healthcare

• Transportation

• Leisure

• Power

• CSR – Hemas Outreach Foundation

2

Sri Lanka: Key Statistics

Nominal GDP USD 51Bn (2010)

GDP per Capita USD 2,399 (2010)

Real GDP Growth 8.0% (2010)

Inflation 9.8% (April 11, CCPI Y-Y change)

Interest Rate 7.3 % (12-month T-bill)

Exchange Rate LKR 110/USD

3Source: CBSL, Country Report - Sri Lanka, Economist Intelligence Unit, Global Finance, Asian Tribune

Post War: A new era of opportunity

4

• Political stability post elections

• Economy expected to expand ~ 6.6% a year over the next 5 years

• Improved investor confidence: stock market performance in 2010 ~104% (2009 ~ 125% )

• Tourism potential: 46% growth in arrivals for 2010

Source: CBSL, Country Report - Sri Lanka, Economist Intelligence Unit, Global Finance, Asian Tribune

HEMAS GROUP

5

Hemas : Key Statistics

Share Price Rs 47.50

Market Capitalization Rs 24.3Bn

% of Total Market 0.94%

PER 20.1 times

PBV 2.7 times

No of Shares 512Mn

Public Shareholding 28.05%

6

Rs Mn. 10/11 09/10 Change

Group Turnover 18,067 14,997 20.5%

Group Earnings 1,210 902 34.2%

Shareholders’ Funds 8,874 7,692 15.4%

Capital Employed 14,666 12,367 18.5%

The Hemas Group

Hemas Holdings PLC

FMCG Healthcare

Pharma

Hospitals (70%)

Leisure

SerendibHotels PLC

(51%)

Diethelm Travels

(80%)

Transportation

GSAs

Travels

Maritime

Freight & Logistics

(49%)

Hemas Power PLC (75%)

Heladhanavi (47%)

Hydro Power

Other

IT Network Solutions

Property

BPO

7

Our Portfolio - FY10/11

8

18%

27%

10%

30%

5%

9%

Capital Employed

FMCG HEALTHCARE LEISURE POWER TRANSPORTATION OTHER

32%

36%

6%

19%

4% 3%

Turnover

38%

19%

4%

23%

16%0%

Earnings

Group Revenue: 5-Year CAGR ~ 13.1%

9

20% 20%

7%

-1%

20%

-5%

0%

5%

10%

15%

20%

25%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2007 2008 2009 2010 2011

Rs. Mn.

Top line Growth

Growth in EPS Expected to Rebound

10

Comparative figures adjusted for sub division of ordinary shares in the proportion of 5:1

4%

12%

-32%

17%

34%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-

0.50

1.00

1.50

2.00

2.50

2007 2008 2009 2010 2011

Rs.

EPS Growth

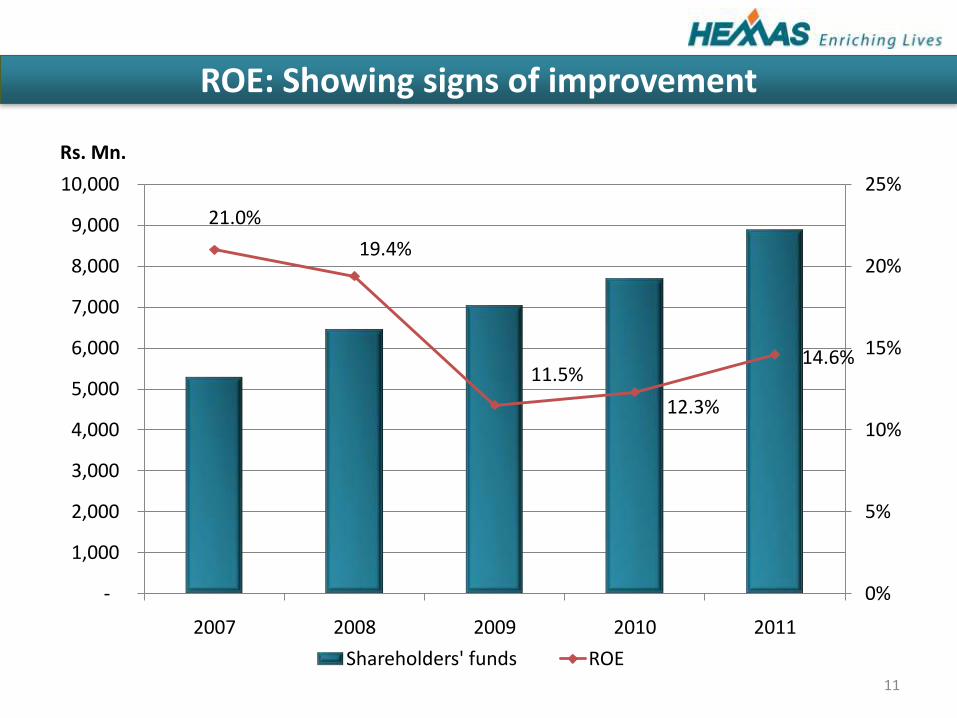

ROE: Showing signs of improvement

11

21.0%

19.4%

11.5%

12.3%

14.6%

0%

5%

10%

15%

20%

25%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2007 2008 2009 2010 2011

Rs. Mn.

Shareholders' funds ROE

Cash flows Vs Earnings

12

-

500

1,000

1,500

2,000

2,500

2007 2008 2009 2010 2011

Rs. Mn.

Operating Cashflow Earnings

Governance

• Board of Directors:

– Four independent non- executive directors (including Chairman), one non-executive director, three executive directors

• Board sub committees:

– Audit committee – Two independent non- executive directors

– Remuneration committee - Two independent non- executive directors

• Focus on Risk Management

13

FMCG: Overview

• Hemas, No.2 in Personal Care category

• Portfolio includes 18 popular brands

• Market Leader in baby care, hair oil and men’s grooming categories

• Modern state-of-the-art production factory with R&D facilities

• Island wide distribution reach ~ 80,000 outlets

14

74%

15%

11%

FMCG Market ~ 141Bn

Food & Beverages

Personal Care

Homecare

59%22%

19%

Hemas

Personal Care

Food & Home Care

Personal Wash

FMCG: Key Brands

15

Baby Cheramy

• Market leader in the baby care category

Clogard

• Clear USP - Clove oil

Kumarika

• Market leader in the hair oil market

• 4th largest revenue generator in the sector

Diva

• A leading washing powder in the market

Velvet

• Toilet soap, re-launched in December 09

FMCG: 10-11 update

16

Key Statistics 2010/11 2009/10 Growth

Turnover (Rs. Mn) 5799 5247 11%

Profit After Tax (Rs. Mn) 519 636 (18%)

• Baby care, Fragrances, Homecare and Personal wash contributed positively to growth in turnover

• New taxes levied on imports and increasing raw material prices impacted profitability, year-on-year

• Diva commenced local manufacturing at Dankotuwa

• Re-launch of Fems, our sanitary napkin brand and the launch of new variants of Kumarika, our hair oil brand

32%

Turnover

Sector Group

FMCG: Accolades for our manufacturing facility

• Gold award for the Extra Large Category at the CNCI ‘Achievers of Industrial Excellence’ Awards 2010

17

• GOLD Award at the ‘National Productivity Award 2009/10’ presented by the National Productivity Secretariat

FMCG: Strategic Focus

• Consolidation of Personal care brands

• Strengthen Household and Feminine Hygiene categories

• Expand with selected categories in Bangladesh market

• Explore opportunities to expand the Foods portfolio

18

Healthcare: Overview of the Pharmaceutical business

• Core business: distribution of pharmaceutical products

• Market leader with a share of 16.4% (source: IMS)

• Represents 25 multinational pharmaceutical companies

• Widest and strongest distribution network

• Overall pharmaceutical market grew by ~ 20% , in 2010, driven by growth in volume (Source: IMS )

19

60%

10%

30%

Total Market

Private/Retail segment - pharmacies

Institutional segment - Private hospitals & Osu Sala

Tender segment - govt. hospitals & SPC

60%

10%

30%

Total Market

Healthcare: Overview of Hospitals

20

• 100-bed hospital in Wattala and a 50-bed hospital in Galle

• Operations of Wattala commenced in December 2008 and Galle in March 2009

• Dedicated to provide patient centric medical care at affordable prices

• Certification pending for ACHSI accreditation

• ISO 15189 awarded for laboratory services

• Tie-ups with institutions providing tertiary education in nursing

• 3rd hospital at Battaramulla, to commence construction

13%

87%

Inpatient split between Govt. and Private

Hospitals

Private Public

60%

40%

Out Patient split between Govt. and Private Hospitals

Private Public

22%

24%

12%

12%

1%

23%

6%

Western Province Private Sector Revenue Split

Durdans Nawaloka Asiri Medical

Asiri Surgical Asiri Central Lanka Hospitals

Hemas

21

Healthcare: Our Hospitals at Wattala & Galle

Wattala

• 100-bed state-of-the-art hospital with 10-bed ICU & NICU

• Approximately 130 consultants practice on a visiting basis

• Modern facilities including 20 consultation chambers and 5 operating theaters

• Fixed priced health packages to ensure affordability & predictability

Galle

• 50-bed hospital with ICU

• Focus on providing health services to the fast growing suburban community

Healthcare: 10-11 update

• Hospital sector showed a Turnover growth of 45% for the year

• Wattala Hospital achieved cash break-even position in May 2010, 18 months after commencement

• Growing consumer confidence in our Hospitals reflected by a 38% increase in surgeries

• Pharmaceutical business continued to maintain its position as market leader, recording a turnover growth of 24%

22

Key Statistics 2010/11 2009/10 Growth

Turnover (Rs. Mn) 6514 5049 29%

Profit After Tax (Rs. Mn) 232 68 239%

36%

Turnover

Sector Group

Healthcare: Hospital laboratory expands to open in Ragama

• The new lab is equipped with automated biochemistry and hematology analyzers, providing speedy and accurate laboratory test reports round the clock

• Lab records 110 blood tests per day

23

• The lab also provides ECG service, Channeling & information services and CT & MRI referral services for Hemas Hospital Wattala

Healthcare: Hospital Expansion Plan

• Two 50 bed hospitals in Battaramullaand Ratmalana

• Approximate date for commencement of construction - May 2011 (1st

Hospital in Battaramulla)

• Period of construction estimated at 12 months

• Commercial operations expected to start within 3 months following completion

• Estimated project cost per new hospital – Rs 950 Mn

24

Battaramulla

Colombo South

Healthcare: Strategic Focus

• Expansion plans for OTC business

• Looking to attract new agencies and consolidate market position in the Pharmaceutical market

• Stabilize operations in existing hospitals and expand into identified key locations & sites

25

Transportation: Overview

• Sector operates in the Aviation, Maritime and integrated logistics space

• Market leader in aviation, representing two of the largest airlines, Emirates (EK) and Malaysia Airlines (MAS)

• Maritime arm represents a Singaporean feeder agency, Far Shipping

• Entered the asset ownership business space by acquiring a 17% stake in MSL

• Sector entered into an agreement with NCGB India and Lanka IOC to provide Maritime Support Services

• Retains interest in Courier and the Freight Forwarding industry

26

Transportation: 10-11 Update

• Growth in passenger sales drives sector performance during the year

• GSA passenger and cargo sales have shown a growth of 38% and 21% respectively, year-on-year

• Hemas was appointed as the GSA in Sri Lanka for Ukraine International Airlines during the year

• Positive sentiment surrounding maritime industry contributes growth in Far Shipping sales

• Far shipping operations expands to Chittagong , Bangladesh 27

Key Statistics 2010/11 2009/10 Growth

Turnover (Rs. Mn) 734 664 11%

Profit After Tax (Rs. Mn) 224 181 24%

4%

Turnover

Sector Group

Transportation: Strategic Focus

• Consolidate the market leadership position in the Aviation business

• Look out for opportunities in the local aviation industry

• Opportunities to expand the Maritime and Ports related business

28

Hotel Dolphin,Waikkal

Serendib Hotel,Bentota

Hotel Sigiriya,Sigiriya

Kuchchaveli*

Mowbray,Kandy

Peace Haven,Tangalle

Leisure: Overview

• Hemas owns 51% stake in Serendib Hotels, a public listed hotels group

• Serendib Group consists 3 hotels located in Bentota, Negombo, Sigiriya, and manages and owns 19.9% of a fourth hotel in Kalutara with a room strength of 105

• Hemas owns 2 undeveloped properties in Kandy and Tangalle

• Strategic alliance with Minor International, Thailand

• Diethelm Travels, a strategic partnership with Diethelm Group, recently started operations in Maldives

29Source: SLTDA *To be acquired

Leisure: Market Statistics of Serendib Hotels

30

Voting Non Voting

Share Price Rs 30.80 Rs 18.70

Market Capitalization Rs 1.9Bn Rs 0.5Bn

% of Total Market 0.07% 0.02%

PER 16.0times 4.6times

PBV 1.5times 0.5times

No of Shares 60.4Mn 28.8Mn

Public Shareholding 29.66% 26.64%

Leisure: 10-11 Update

• Our hotels continued to benefit from the positive outlook of the country

• Hotels recorded an average occupancy in excess 80%, for the year under review

• Dolphin Hotel was refurbished at a cost of Rs. 530Mn and reopened in October 2010

• Kani Lanka Resort and Spa was acquired by Hemas through Serendib Hotels PLC

31

Key Statistics 2010/11 2009/10 Growth

Turnover (Rs. Mn) 1035 752 38%

Profit After Tax (Rs. Mn) 122 33 263%

6%

Turnover

Sector Group

Leisure: Dolphin Hotel upgraded to 4 star

32

• Reopened in October 2010

• Refurbishment cost - Rs. 530Mn

Leisure : Twin Experience of PLAY & PAUSE at Dolphin . . .

33

Leisure: Acquisition of Kani Lanka

• Hemas acquired a 19.9% stake in KaniLanka Resort and Spa, through its subsidiary Serendib Hotels PLC

• Minor International PLC, our strategic partner, acquired the remaining 80.1%

• The hotel is being managed by SerendibLeisure Management Limited

34

• A 150 key luxury hotel is being developed adjacent to the current hotel and will be the first – ever ‘Anantara‘ branded resort in Sri Lanka

Leisure: Strategic Focus

• Refurbishment and repositioning of Hotel Serendib - construction to begin in May 2011

• Development of existing land banks, Peace Haven and Mowbray

• Strategic investments with Minor to develop the Anantara brand

35

Power: Overview

• 100MW thermal power plant: a joint venture with a 10 year PPA expiring in 2014

• Hydro power plants with operational capacities of 2.0MW and 2.6MW

• 2.4MW hydro power plant under construction

• Hemas Power was listed in Sep 09, and raised Rs. 626Mn for new investments

• Electricity demand to grow at a CAGR of 8.6% over the long-term in Sri Lanka

• Long-Term Generation Plan of CEB estimates electricity demand to increase by 5,430MW by 2022

36

Energy Demand Vs Generation Requirement in Sri Lanka

Power: Key Statistics

Share Price Rs 35.80

Market Capitalization Rs 4.5Bn

% of Total Market 0.17 %

PER 10.9 times

PBV 1.3 times

No of Shares 125Mn

Public Shareholding 24.93%

37

10/11 09/10 Growth

Group Turnover Rs 3.4Bn Rs 2.9Bn 19%

Group Earnings Rs 426Mn Rs 244Mn 75%

Shareholders’ Funds Rs 2.9Bn Rs 2.5Bn 17%

Capital Employed Rs 4.4Bn Rs 3.7Bn 17%

Power: 10-11 Update

• Heladhanavi continues to be the largest contributor to group profits

• Hydro power contribution to sector profits grow to 45% in comparison to 25% in 09/10

• Sector finance costs show significant reduction due to refinancing of working capital at Heladhanavi

• Hemas contributed ~ 7% to the national grid this year

• Magal Ganga set to complete in September 2011

38

Key Statistics 2010/11 2009/10 Growth

Turnover (Rs. Mn) 3,412 2,867 19%

Profit After Tax (Rs. Mn) 426 244 75%

19%

Turnover

Sector Group

Power: Strategic Focus

• Development of on-going mini-hydro projects

• Looking to enter non-conventional renewable energy space – Bio mass & wind energy

• Explore overseas investments opportunities

39

CSR: Hemas Outreach Foundation

40

CSR: Our Objectives

1. Focus on Early Childhood Care and Development (ECCD) of young children through pre- schools

2. Training of pre-school teachers

3. Empower community led social development through island wide parental awareness programs

4. Improve children’s recreational facilities in disadvantaged communities

5. Improve child protection legislation and provide publicity for children’s issues

6. Sustaining the Menik Farm temporary preschools and play areas

41

CSR: Our activities this year . . .

• 33 Piyawara model pre-schools are being monitored and sustained by Hemas Outreach Foundation

• Opened first ever model pre-school in the Northern Region in Jaffna in January 2011

• Set up pre-schools and play areas in post war relief villages in Vavuniya

• Set up a special school for children with Down’s Syndrome in Hambantotaarea - 42 children are being rehabilitated

• Conducted residential training programs for pre-school teachers

• Weekly TV programme on Nugasevana to educate young mothers on early childhood development

42

In conclusion . . .

• All sectors in the Group are well placed to benefit from expected economic growth

• Growth of the middle class segment to drive growth in FMCG and Healthcare industries

• Major investments in the medium term to be in Hospitals, Hotels and Power

• Exploring opportunities to enter new categories in the FMCG market

43

Investor Relations Contact:

Malinga Arsakularatne Chief Financial Officer

+94 11 4731728 / +94 77 [email protected]

CONFIDENTIALITY AGREEMENT:

Any confidentiality information disclosed in this presentation shall be used by the receiving party exclusively for the purposes of fulfilling the receiving party’s obligation and for no other purpose except with the consent of the disclosing party.

44